Embed Size (px)

Citation preview

CR Common Practices Inventories under IFRS

1 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

Introduction

Under International Financial Reporting Standards, the accounting of Inventories is governed by IAS 2 “Inventories”. Focusing on a sample of 28 large listed European companies that report under IFRS, supplemented by Company Reporting data and comment, this report analyses the disclosure of inventory accounting practice. Included is an examination of company disclosures relating to cost allocation formulae and a survey of the methods identified. Under IAS 2 companies have a choice to adopt either a weighted average or a first in first out stock valuation model (para 25). The model adopted should be identified as part of a company’s accounting policy (para 36 (a)).

Considered also are inventory impairment disclosures such as the amount of any inventory write-down recognised as an expense (para 36 (e)), the amount of any reversals (para 36 (f)) and the explanation for any reversals (para 36 (g)). Examined also will be other inventory disclosures including the total carrying amount of inventories in appropriate classifications (para 36 (b)) the amount of inventories recognised as an expense during the year (para 36 (d)) and the amount of inventories pledged as security (para 36 (h))

Key observations include the following. A cost allocation formula is disclosed by 89% of sample companies. The weighted average cost method of stock valuation is more popular than first in first out with 76% of the companies that identify a method disclosing the use of the former and 32% the latter. Quantification of inventory write-downs is disclosed by 71% of companies with 36% disclosing information relating to reversals. Of those companies with reversals only 11% give an explanation of the circumstances or events that led to it. Multiple classes of inventory are identified by 82% of companies with 18% disclosing a single class. The cost of inventories expensed during the year is identified by 71% of companies.

Companies under examination

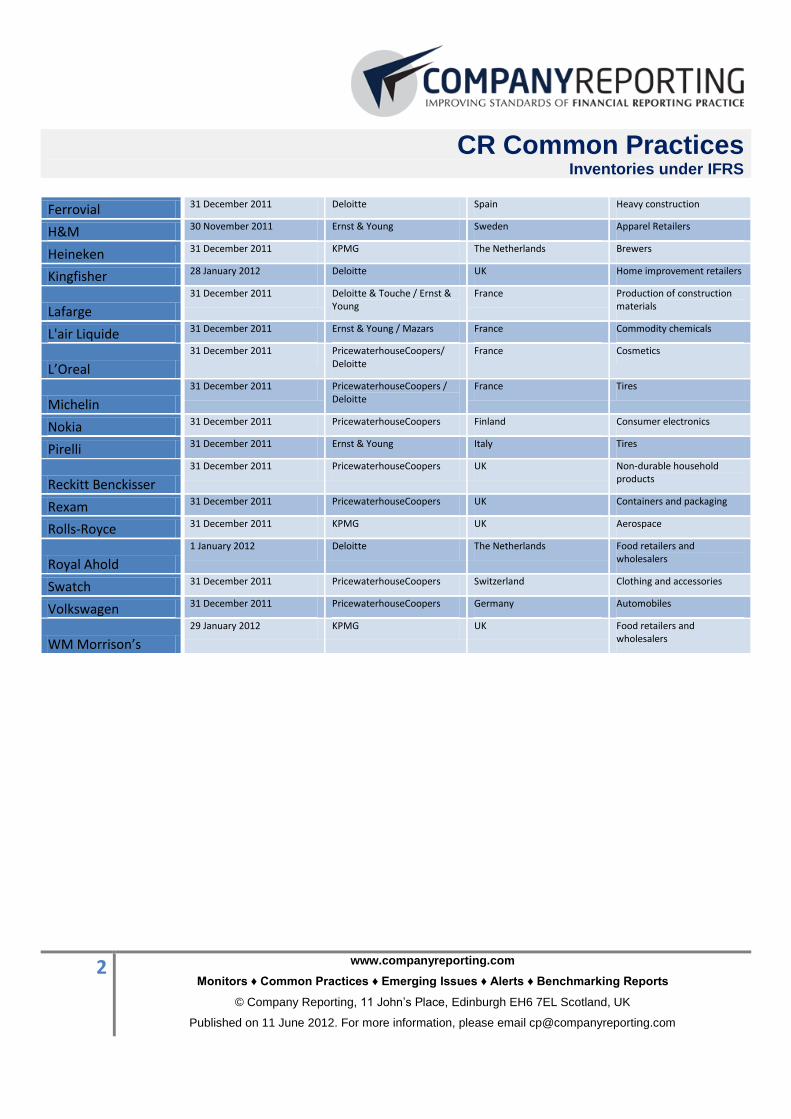

Our sample consists of 28 listed European companies, which feature in the Standard & Poor’s Europe 350 dataset with period ends of between 30 November 2011 and 29 January 2012 that have published recently their annual reports. The sample contains a spread of companies from different countries and industry classes. The companies of which the accounts have been analysed are as follows:

Company Period End Auditors Country Industry Classification

Adidas 31 December 2011 KPMG Germany Clothing and footwear

Arm 31 December 2011 PricewaterhouseCoopers UK Semiconductors

AstraZeneca 31 December 2011 KPMG UK Pharmaceuticals

BAE Systems 31 December 2011 KPMG UK Defence

BASF 31 December 2011 KPMG Germany Commodity chemicals

British American Tobacco

31 December 2011 PricewaterhouseCoopers UK Tobacco

Carlsberg 31 December 2011 KPMG Denmark Brewers

Cobham 31 December 2011 PricewaterhouseCoopers UK Aerospace

Daimler 31 December 2011 KPMG Germany Automobiles

Delhaize

31 December 2011 Deloitte & Touche Belgium Food retailers and wholesalers

Electrolux 31 December 2011 PricewaterhouseCoopers Sweden Durable household products

CR Common Practices Inventories under IFRS

2 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

Ferrovial 31 December 2011 Deloitte Spain Heavy construction

H&M 30 November 2011 Ernst & Young Sweden Apparel Retailers

Heineken 31 December 2011 KPMG The Netherlands Brewers

Kingfisher 28 January 2012 Deloitte UK Home improvement retailers

Lafarge

31 December 2011 Deloitte & Touche / Ernst & Young

France Production of construction materials

L'air Liquide 31 December 2011 Ernst & Young / Mazars France Commodity chemicals

L’Oreal

31 December 2011 PricewaterhouseCoopers/ Deloitte

France Cosmetics

Michelin

31 December 2011 PricewaterhouseCoopers / Deloitte

France Tires

Nokia 31 December 2011 PricewaterhouseCoopers Finland Consumer electronics

Pirelli 31 December 2011 Ernst & Young Italy Tires

Reckitt Benckisser

31 December 2011 PricewaterhouseCoopers UK Non-durable household products

Rexam 31 December 2011 PricewaterhouseCoopers UK Containers and packaging

Rolls-Royce 31 December 2011 KPMG UK Aerospace

Royal Ahold

1 January 2012 Deloitte The Netherlands Food retailers and wholesalers

Swatch 31 December 2011 PricewaterhouseCoopers Switzerland Clothing and accessories

Volkswagen 31 December 2011 PricewaterhouseCoopers Germany Automobiles

WM Morrison’s

29 January 2012 KPMG UK Food retailers and wholesalers

CR Common Practices Inventories under IFRS

3 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

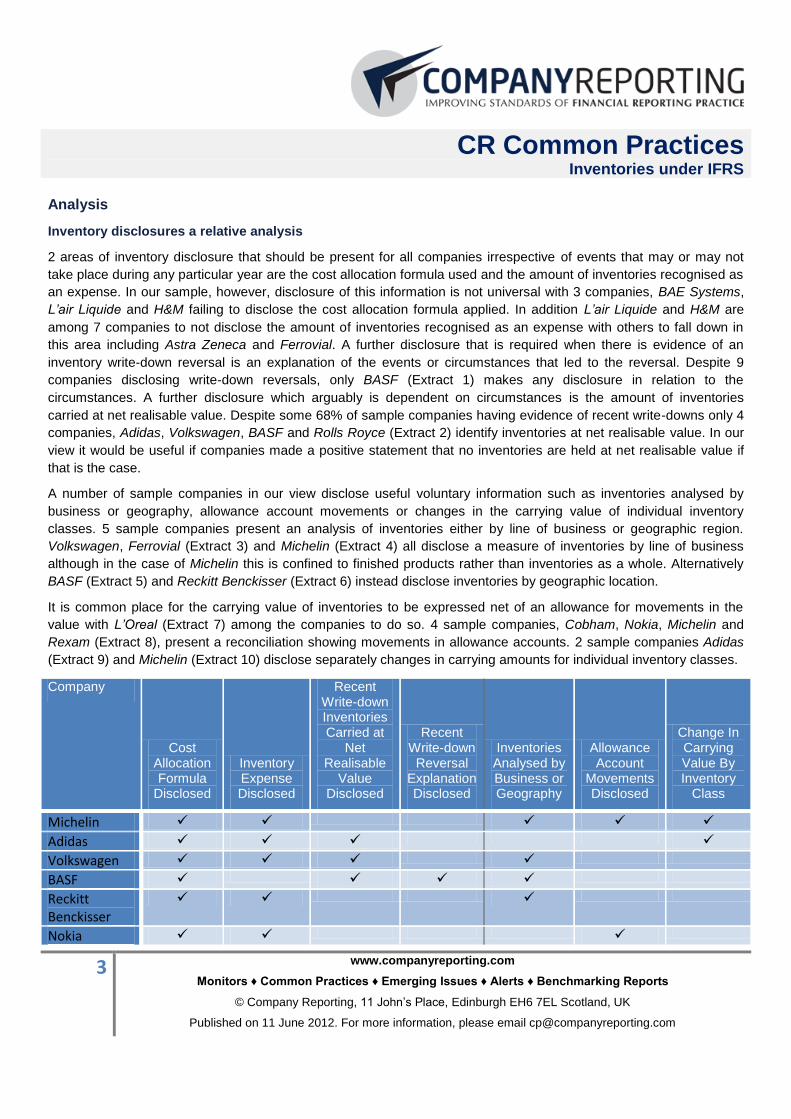

Analysis

Inventory disclosures a relative analysis

2 areas of inventory disclosure that should be present for all companies irrespective of events that may or may not

take place during any particular year are the cost allocation formula used and the amount of inventories recognised as

an expense. In our sample, however, disclosure of this information is not universal with 3 companies, BAE Systems,

L’air Liquide and H&M failing to disclose the cost allocation formula applied. In addition L’air Liquide and H&M are

among 7 companies to not disclose the amount of inventories recognised as an expense with others to fall down in

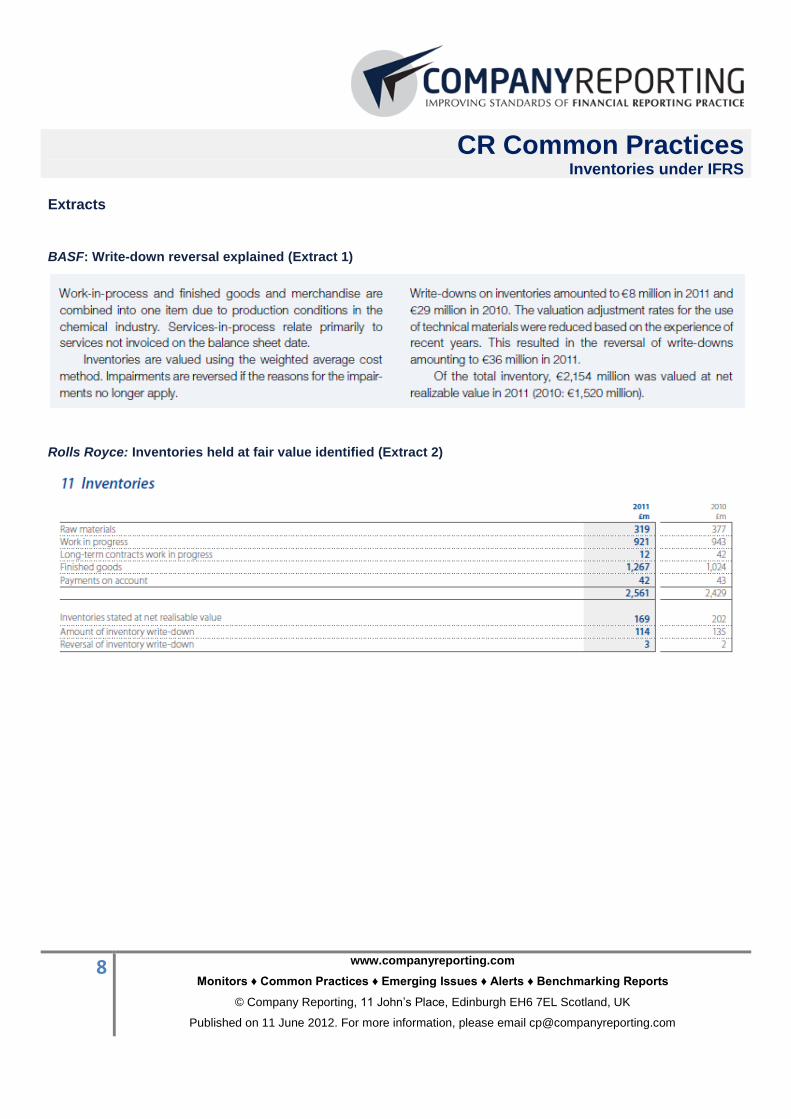

this area including Astra Zeneca and Ferrovial. A further disclosure that is required when there is evidence of an

inventory write-down reversal is an explanation of the events or circumstances that led to the reversal. Despite 9

companies disclosing write-down reversals, only BASF (Extract 1) makes any disclosure in relation to the

circumstances. A further disclosure which arguably is dependent on circumstances is the amount of inventories

carried at net realisable value. Despite some 68% of sample companies having evidence of recent write-downs only 4

companies, Adidas, Volkswagen, BASF and Rolls Royce (Extract 2) identify inventories at net realisable value. In our

view it would be useful if companies made a positive statement that no inventories are held at net realisable value if

that is the case.

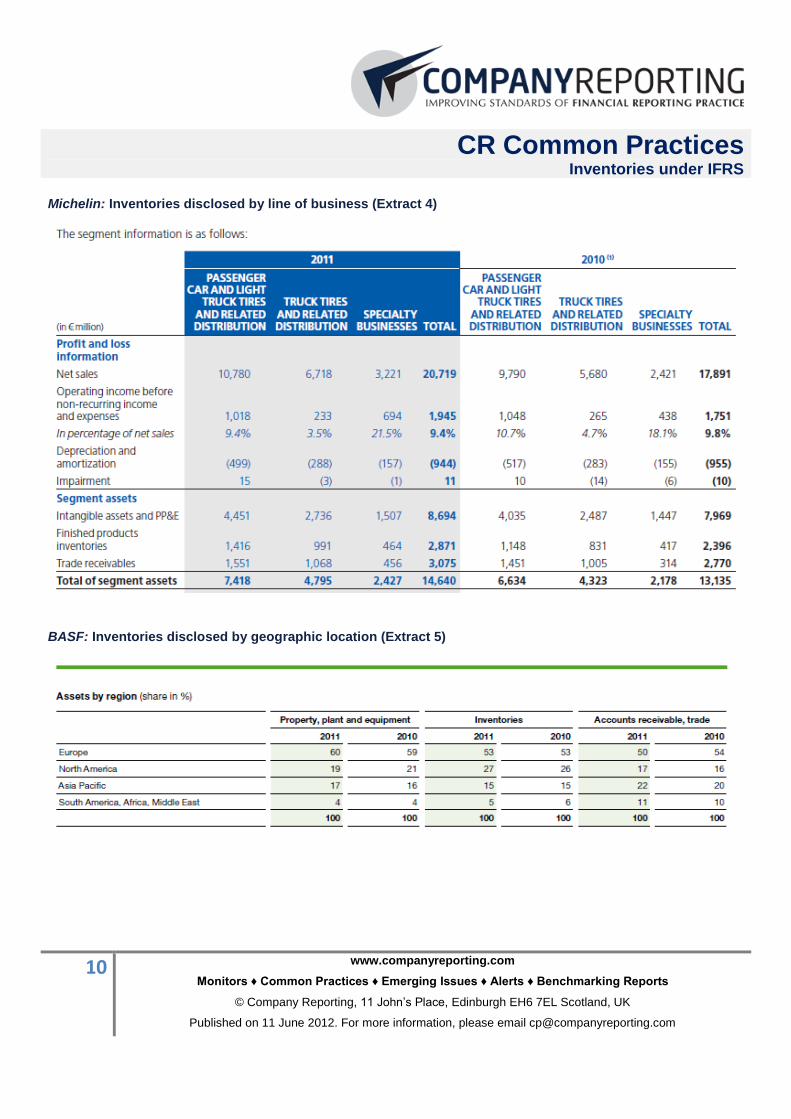

A number of sample companies in our view disclose useful voluntary information such as inventories analysed by

business or geography, allowance account movements or changes in the carrying value of individual inventory

classes. 5 sample companies present an analysis of inventories either by line of business or geographic region.

Volkswagen, Ferrovial (Extract 3) and Michelin (Extract 4) all disclose a measure of inventories by line of business

although in the case of Michelin this is confined to finished products rather than inventories as a whole. Alternatively

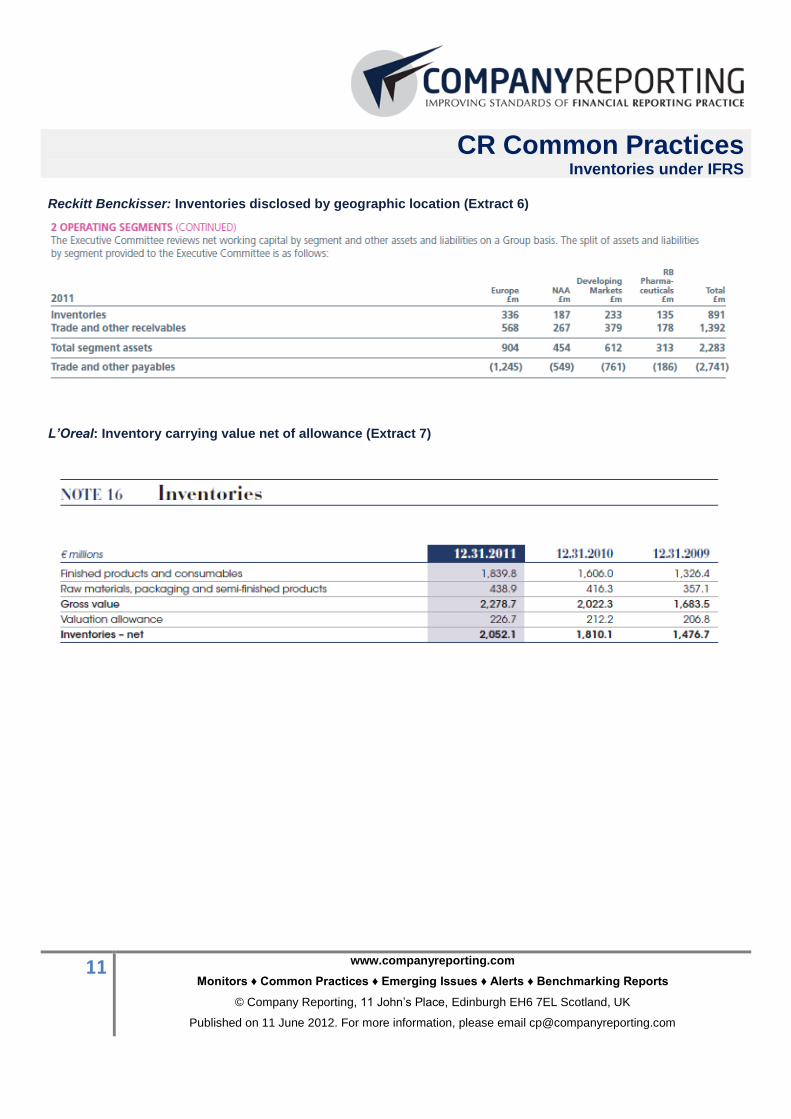

BASF (Extract 5) and Reckitt Benckisser (Extract 6) instead disclose inventories by geographic location.

It is common place for the carrying value of inventories to be expressed net of an allowance for movements in the

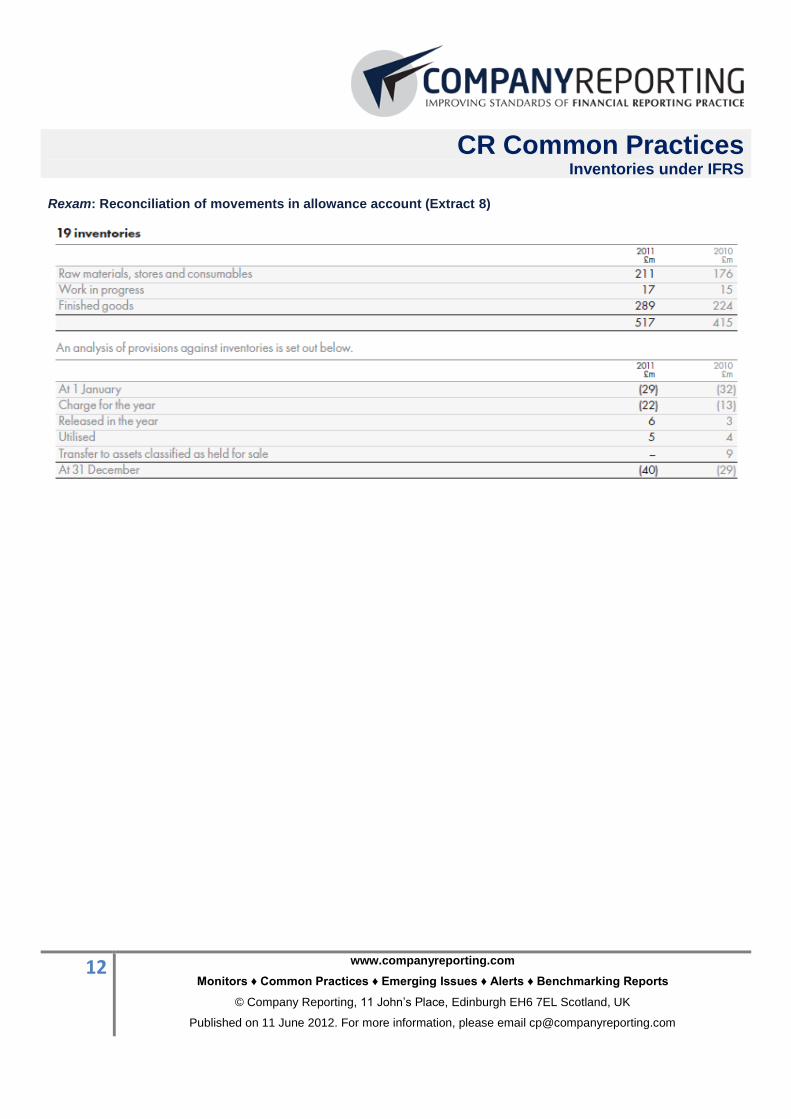

value with L’Oreal (Extract 7) among the companies to do so. 4 sample companies, Cobham, Nokia, Michelin and

Rexam (Extract 8), present a reconciliation showing movements in allowance accounts. 2 sample companies Adidas

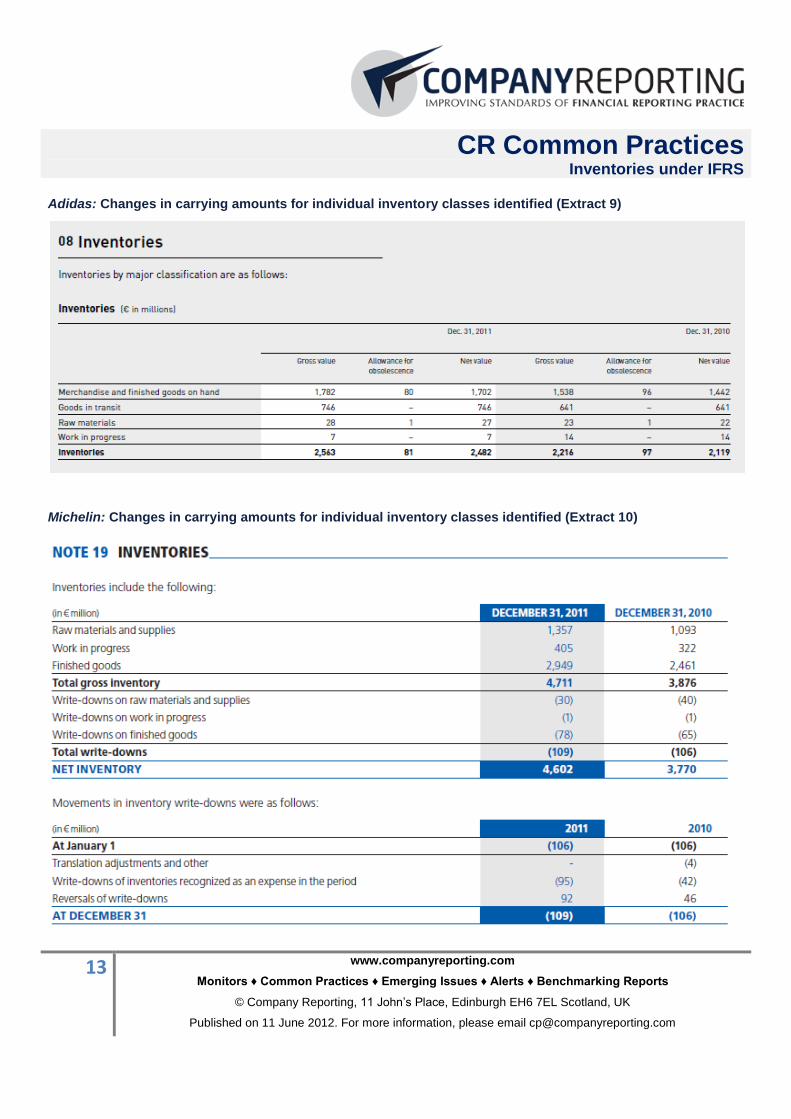

(Extract 9) and Michelin (Extract 10) disclose separately changes in carrying amounts for individual inventory classes.

Company

Cost Allocation Formula

Disclosed

Inventory Expense Disclosed

Recent Write-down Inventories Carried at

Net Realisable

Value Disclosed

Recent Write-down

Reversal Explanation Disclosed

Inventories Analysed by Business or Geography

Allowance Account

Movements Disclosed

Change In Carrying Value By Inventory

Class

Michelin

Adidas

Volkswagen

BASF

Reckitt Benckisser

Nokia

CR Common Practices Inventories under IFRS

4 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

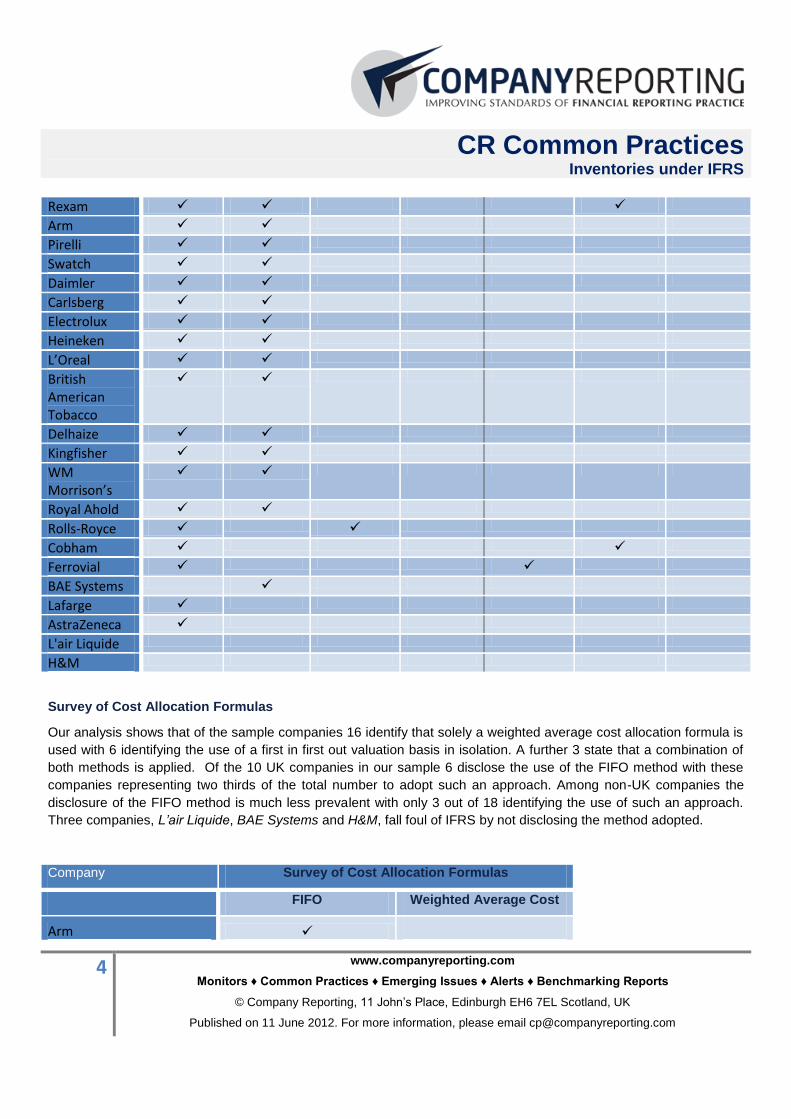

Rexam

Arm

Pirelli

Swatch

Daimler

Carlsberg

Electrolux

Heineken

L’Oreal

British American Tobacco

Delhaize

Kingfisher

WM Morrison’s

Royal Ahold

Rolls-Royce

Cobham

Ferrovial

BAE Systems

Lafarge

AstraZeneca

L'air Liquide

H&M

Survey of Cost Allocation Formulas

Our analysis shows that of the sample companies 16 identify that solely a weighted average cost allocation formula is

used with 6 identifying the use of a first in first out valuation basis in isolation. A further 3 state that a combination of

both methods is applied. Of the 10 UK companies in our sample 6 disclose the use of the FIFO method with these

companies representing two thirds of the total number to adopt such an approach. Among non-UK companies the

disclosure of the FIFO method is much less prevalent with only 3 out of 18 identifying the use of such an approach.

Three companies, L’air Liquide, BAE Systems and H&M, fall foul of IFRS by not disclosing the method adopted.

Company Survey of Cost Allocation Formulas

FIFO Weighted Average Cost

Arm

CR Common Practices Inventories under IFRS

5 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

Cobham

Reckitt Benckisser

Nokia

Pirelli

Rolls-Royce

Swatch

Michelin

Daimler

Adidas

BASF

Carlsberg

Electrolux

Heineken

Lafarge

L’Oreal

British American Tobacco

Volkswagen

Ferrovial

Delhaize

Kingfisher

WM Morrison’s

AstraZeneca

Rexam

Royal Ahold

L'air Liquide (a)

BAE Systems (a)

H&M (a)

(a) No disclosure of cost allocation formula

CR Common Practices Inventories under IFRS

6 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

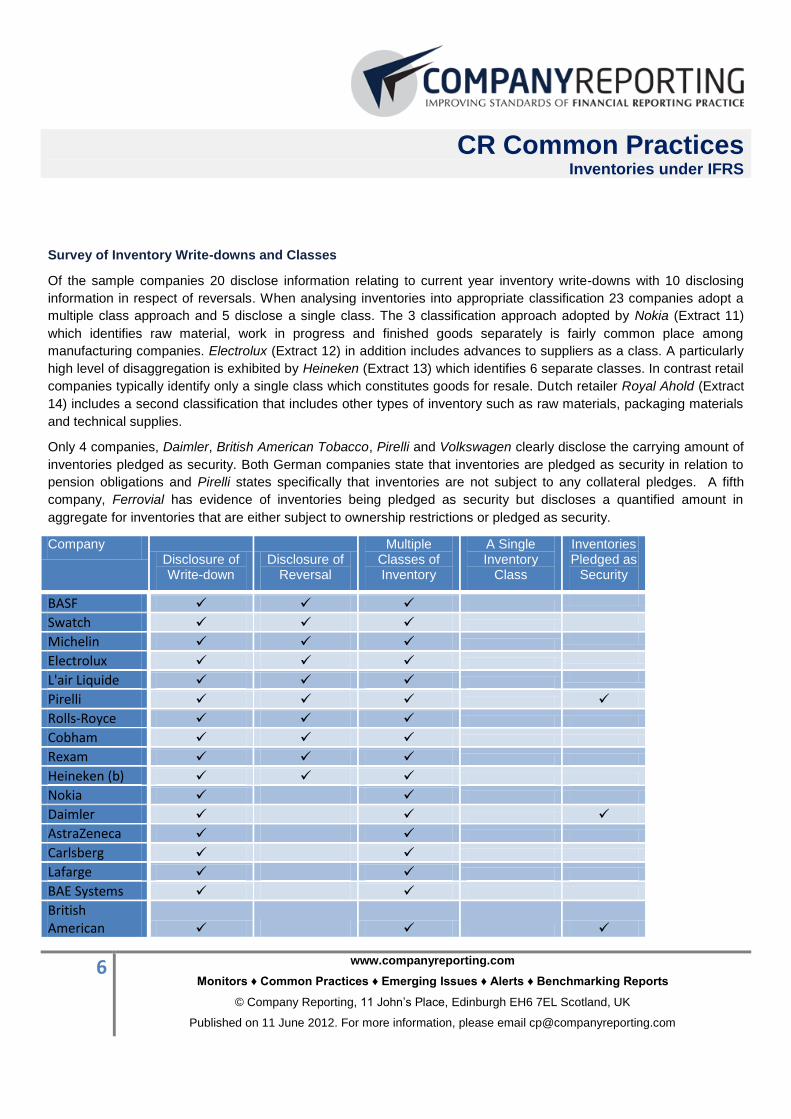

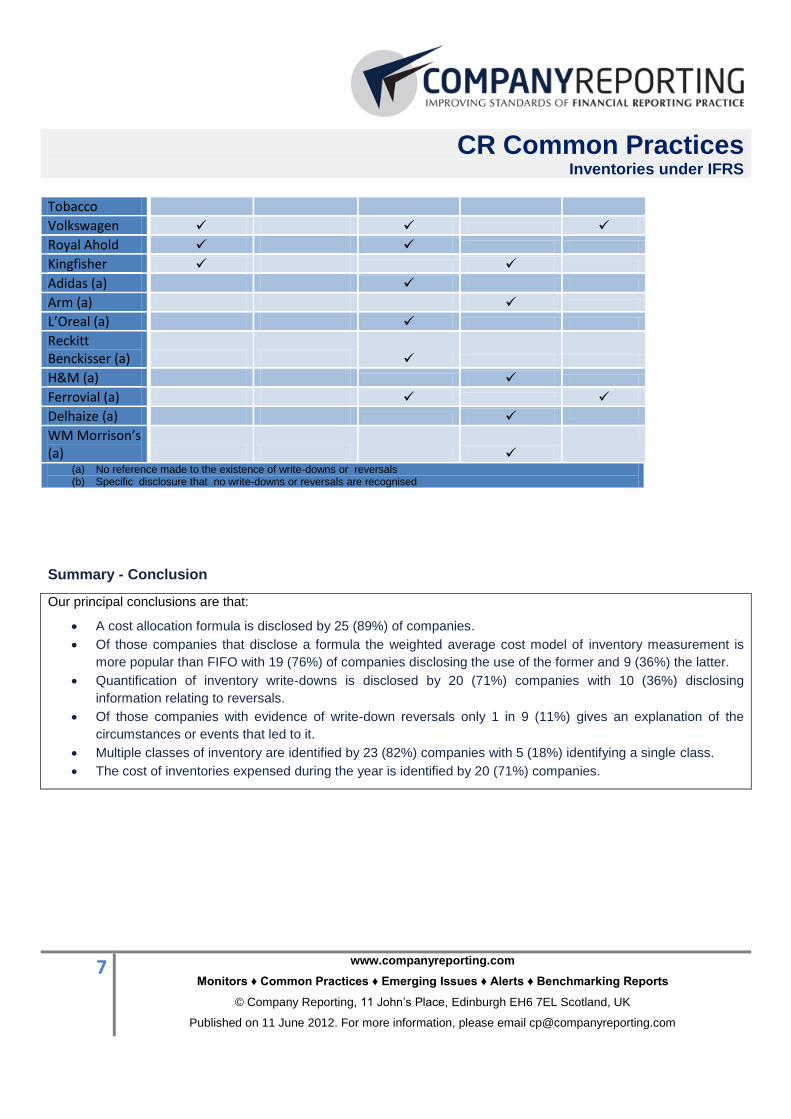

Survey of Inventory Write-downs and Classes

Of the sample companies 20 disclose information relating to current year inventory write-downs with 10 disclosing

information in respect of reversals. When analysing inventories into appropriate classification 23 companies adopt a

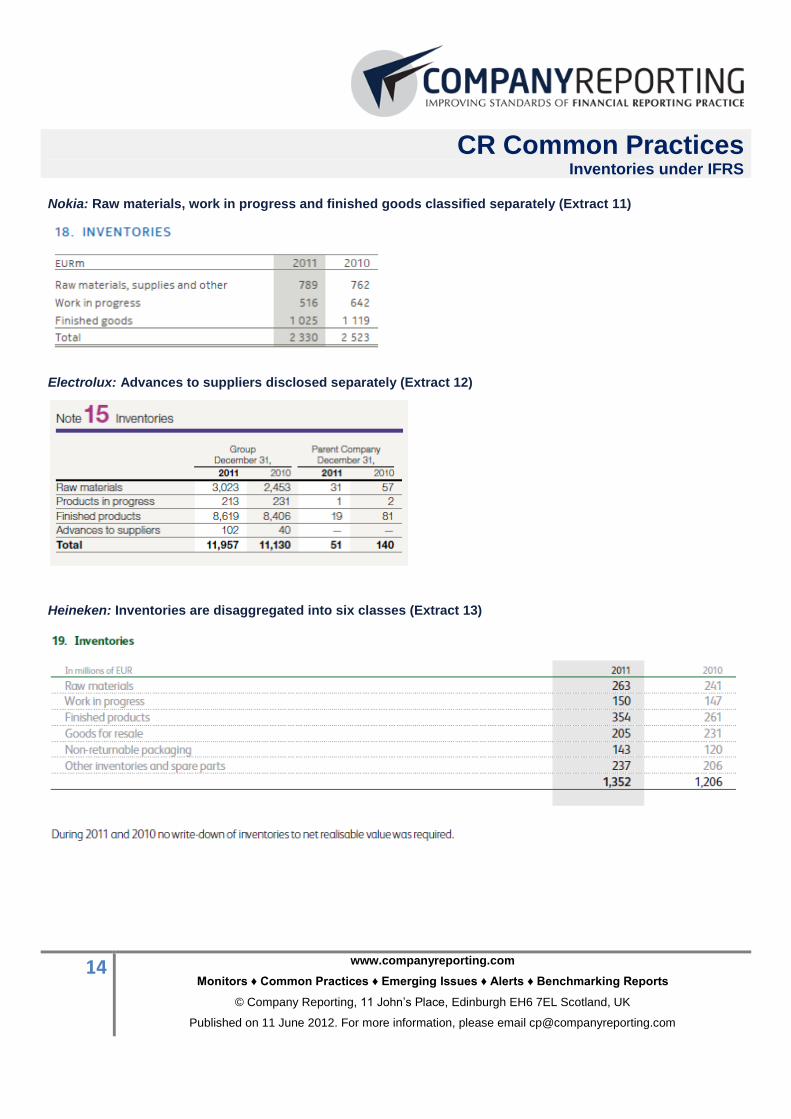

multiple class approach and 5 disclose a single class. The 3 classification approach adopted by Nokia (Extract 11)

which identifies raw material, work in progress and finished goods separately is fairly common place among

manufacturing companies. Electrolux (Extract 12) in addition includes advances to suppliers as a class. A particularly

high level of disaggregation is exhibited by Heineken (Extract 13) which identifies 6 separate classes. In contrast retail

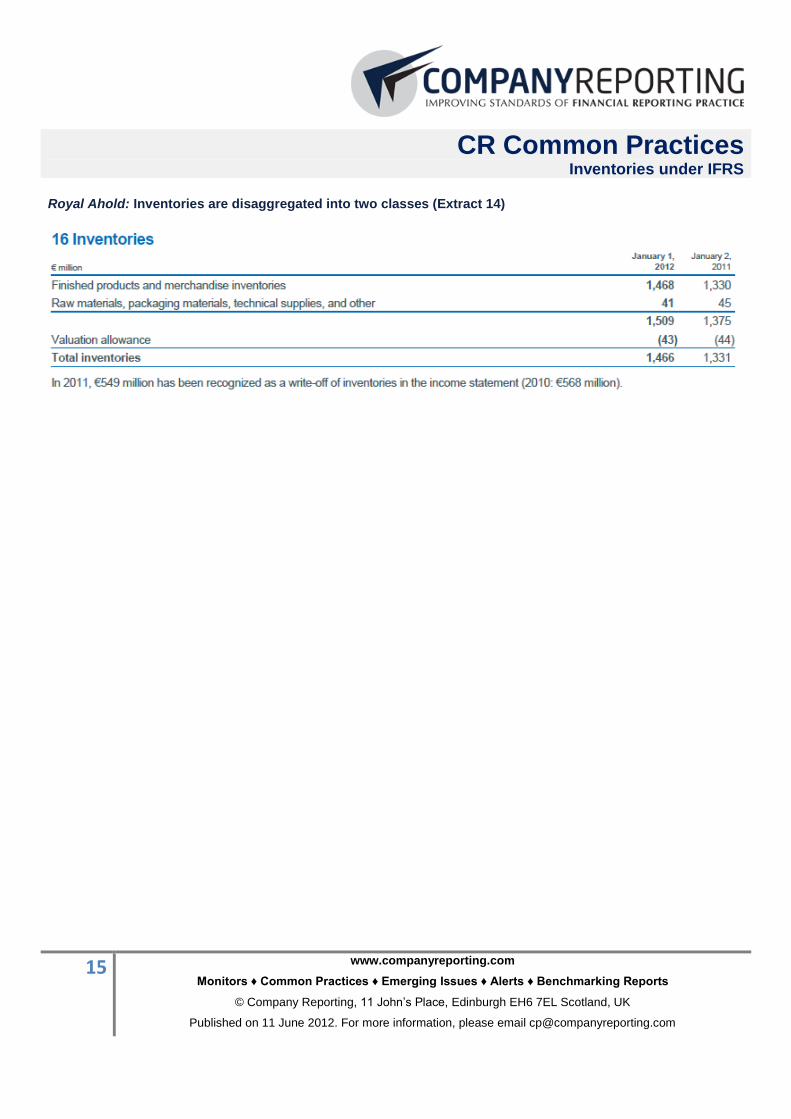

companies typically identify only a single class which constitutes goods for resale. Dutch retailer Royal Ahold (Extract

14) includes a second classification that includes other types of inventory such as raw materials, packaging materials

and technical supplies.

Only 4 companies, Daimler, British American Tobacco, Pirelli and Volkswagen clearly disclose the carrying amount of

inventories pledged as security. Both German companies state that inventories are pledged as security in relation to

pension obligations and Pirelli states specifically that inventories are not subject to any collateral pledges. A fifth

company, Ferrovial has evidence of inventories being pledged as security but discloses a quantified amount in

aggregate for inventories that are either subject to ownership restrictions or pledged as security.

Company Disclosure of Write-down

Disclosure of Reversal

Multiple Classes of Inventory

A Single Inventory

Class

Inventories Pledged as

Security

BASF

Swatch

Michelin

Electrolux

L'air Liquide

Pirelli

Rolls-Royce

Cobham

Rexam

Heineken (b)

Nokia

Daimler

AstraZeneca

Carlsberg

Lafarge

BAE Systems

British American

CR Common Practices Inventories under IFRS

7 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

Tobacco

Volkswagen

Royal Ahold

Kingfisher

Adidas (a)

Arm (a)

L’Oreal (a)

Reckitt Benckisser (a)

H&M (a)

Ferrovial (a)

Delhaize (a)

WM Morrison’s (a)

(a) No reference made to the existence of write-downs or reversals (b) Specific disclosure that no write-downs or reversals are recognised

Summary - Conclusion

Our principal conclusions are that:

A cost allocation formula is disclosed by 25 (89%) of companies.

Of those companies that disclose a formula the weighted average cost model of inventory measurement is

more popular than FIFO with 19 (76%) of companies disclosing the use of the former and 9 (36%) the latter.

Quantification of inventory write-downs is disclosed by 20 (71%) companies with 10 (36%) disclosing

information relating to reversals.

Of those companies with evidence of write-down reversals only 1 in 9 (11%) gives an explanation of the

circumstances or events that led to it.

Multiple classes of inventory are identified by 23 (82%) companies with 5 (18%) identifying a single class.

The cost of inventories expensed during the year is identified by 20 (71%) companies.

CR Common Practices Inventories under IFRS

8 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

Extracts

BASF: Write-down reversal explained (Extract 1)

Rolls Royce: Inventories held at fair value identified (Extract 2)

CR Common Practices Inventories under IFRS

9 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

Ferrovial: Inventories disclosed by line of business (Extract 3)

CR Common Practices Inventories under IFRS

10 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

Michelin: Inventories disclosed by line of business (Extract 4)

BASF: Inventories disclosed by geographic location (Extract 5)

CR Common Practices Inventories under IFRS

11 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

Reckitt Benckisser: Inventories disclosed by geographic location (Extract 6)

L’Oreal: Inventory carrying value net of allowance (Extract 7)

CR Common Practices Inventories under IFRS

12 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

Rexam: Reconciliation of movements in allowance account (Extract 8)

CR Common Practices Inventories under IFRS

13 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

Adidas: Changes in carrying amounts for individual inventory classes identified (Extract 9)

Michelin: Changes in carrying amounts for individual inventory classes identified (Extract 10)

CR Common Practices Inventories under IFRS

14 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

Nokia: Raw materials, work in progress and finished goods classified separately (Extract 11)

Electrolux: Advances to suppliers disclosed separately (Extract 12)

Heineken: Inventories are disaggregated into six classes (Extract 13)

CR Common Practices Inventories under IFRS

15 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

Royal Ahold: Inventories are disaggregated into two classes (Extract 14)

CR Common Practices Inventories under IFRS

16 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

CR Common Practices Inventories under IFRS

17 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

CR Common Practices Inventories under IFRS

18 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

CR Common Practices Inventories under IFRS

19 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

CR Common Practices Inventories under IFRS

20 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]

CR Common Practices Inventories under IFRS

21 www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 11 June 2012. For more information, please email [email protected]