Embed Size (px)

Citation preview

| P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

INTRINSIC VALUATION

OF EQUITY SHARE OF A

COMPANY

This report was made during summer internship

at Stoic Advisors LLP Company. Stoic started

recently to provide investor education in India.

Stoic is run by an eminent value investor who

walks on the principles led by Benjamin Graham.

Submitted by: Nitin Kolapkar (15IB341)

JUNE 2016

Industry Mentor: Faculty Mentor:

Mr. Puneet Khurana Prof. Arindam Banerjee

CFA USA Faculty - Finance and Accounting

Managing Partner BIMTECH

Stoic Advisors LLP

i | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

Table of Contents

List of Tables .......................................................................................................................................... iii

List of charts and graphs .................................................................................................................. iv

Summer Project Certificate .............................................................................................................. v

Letter of Authorization ...................................................................................................................... vi

Letter of Transmittal ......................................................................................................................... vii

Executive Summary ......................................................................................................................... viii

About Stoic Advisors Llp ................................................................................................................... x

Concept of Value Investing ............................................................................................................... 1

Overview of Indian Economy .......................................................................................................... 3

Overview of Indian Paint Industry ................................................................................................ 5

Asian Paint .............................................................................................................................................. 8

About Asian Paint .............................................................................................................................. 10

Performance Highlights .................................................................................................................. 12

Financial Ratio Analysis .................................................................................................................. 13

Porters Five Forces Analysis ......................................................................................................... 17

Intrinsic Valuation (DCF Model) ................................................................................................. 19

Intrinsic Valuation (EPV Model) …………………………………………………………………… 23

Overview of Indian 2w Automibile Industry..………………………………….……………… 27

Hero Motocorp Ltd ............................................................................................................................ 28

Performance Highlights .................................................................................................................. 29

Financial Ratio Analysis .................................................................................................................. 34

Intrinsic Valuation (DCF Model) ................................................................................................. 36

Glossary .................................................................................................................................................. 38

References ............................................................................................................................................. 40

ii | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

Acknowledgement

It is difficult to acknowledge precious a debt as that of learning as it is the only debt that is

difficult to repay except through gratitude.

It is my profound privilege to express sincere gratitude to MR. PUNEET KHURANA and MR.

MANISH DHAWAN for giving me the opportunity to do my summer training at STOIC ADVISORS

LLP. and for their expert guidance and support. They continuously motivated me to work on this

project and make it a success. Their willingness to inspire me contributed tremendously in its

completion. They had been very kind and patient while suggesting the outlines of this project

and correcting my doubts.

I would also like to express my gratitude to entire STOIC TEAM for their co-operation and

willingness to answer all my queries and provide valuable assistance and thereby helped me in

my project.

My heartfelt gratitude also goes to PROF. ARINDAM BANERJEE, my faculty mentor at BIMTECH,

who provided valuable suggestions, shared his rich experience and helped me script the

meticulous requisites

iii | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

List of Tables & Figures

Sr. No. Name of Table & Figures Page No. 1 Factors Affecting Operating Profit 17

2 % of Net Sales Contribution 21

3 Shareholding Pattern 21

4 WACC Calculation 27 5 FCF Calculation 28

6 Expenditure Breakup 33

7 Shareholding Pattern 34

8 FCF Calculation 37

iv | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

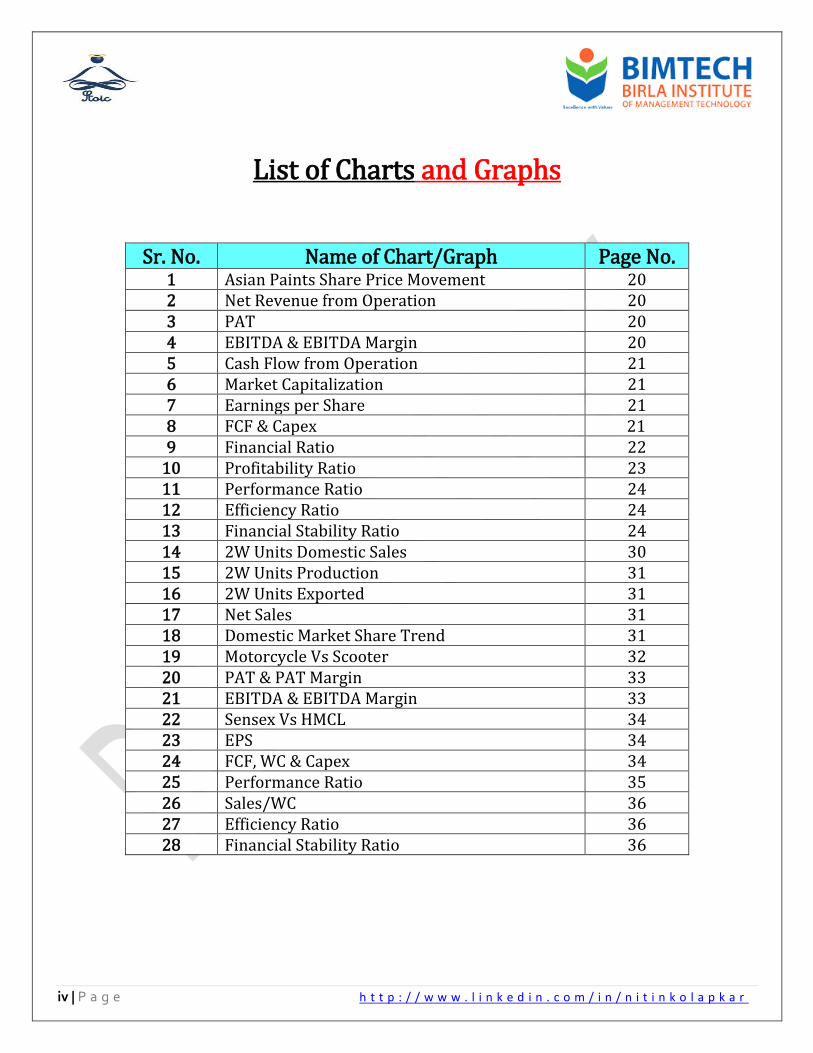

List of Charts and Graphs

Sr. No. Name of Chart/Graph Page No. 1 Asian Paints Share Price Movement 20 2 Net Revenue from Operation 20 3 PAT 20 4 EBITDA & EBITDA Margin 20 5 Cash Flow from Operation 21 6 Market Capitalization 21 7 Earnings per Share 21 8 FCF & Capex 21 9 Financial Ratio 22

10 Profitability Ratio 23 11 Performance Ratio 24 12 Efficiency Ratio 24 13 Financial Stability Ratio 24 14 2W Units Domestic Sales 30 15 2W Units Production 31 16 2W Units Exported 31 17 Net Sales 31 18 Domestic Market Share Trend 31 19 Motorcycle Vs Scooter 32 20 PAT & PAT Margin 33 21 EBITDA & EBITDA Margin 33 22 Sensex Vs HMCL 34 23 EPS 34 24 FCF, WC & Capex 34 25 Performance Ratio 35 26 Sales/WC 36 27 Efficiency Ratio 36 28 Financial Stability Ratio 36

v | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

Summer Project Certificate

This is to certify that Mr. Nitin Kolapkar, Roll No. 15IB341 student of PGDM- International

Business (Finance), Birla Institute of Management Technology, has worked on a summer project

titled “INTRINSIC VALUATION OF EQUITY SHARE OF A COMPANY” at Stoic Advisors LLP after

Trimester-III in partial fulfillment of the requirement for the Post Graduate Diploma in

Management program. This is his original work to the best of my knowledge.

Date: July 4, 2016 Signature _________________

(Prof. Arindam Banerjee)

vi | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

Letter of Authorization

I, Nitin Kolapkar, a student of Birla Institute of Management Technology (BIMTECH), hereby

declare that I have worked on a project titled “INTRINSIC VALUATION OF EQUITY SHARE OF A

COMPANY” during a summer internship at Stoic Advisors LLP, in partial fulfillment of the

requirement for the Post Graduate Diploma in Management program.

I guarantee/underwrite my research work to be authentic and original to the best of my

knowledge in all respects of the process carried out during the project tenure.

My learning experience at Stoic Advisors LLP under the guidance of Mr. Puneet Khurana and Mr.

Manish Dhawan and my college mentor Prof. Arindam Banerjee has been truly enriching.

Date: July 4, 2016 (Nitin Kolapkar)

vii | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

Letter of Transmittal

Birla Institute of Management Technology,

Plot no. 5, Knowledge Park-II, Institutional Area,

Greater Noida (NCR), U.P. – 201306, INDIA

Date: July 4, 2016

Mr. Puneet Khurana

CEO- Stoic Advisors LLP

Dear Sir,

SUBJECT: Summer Project Report

Attached herewith is a copy of my summer project report entitled “Intrinsic Valuation of

Equity Share of a Company” which I am submitting in order to mark the completion of 2.5

months (7 April’16 – 17 June’16) summer project at your organization. This report was

prepared by me using the best of practices and summarizes the work performed on the

project and is being submitted in partial fulfilments of the requirements for the award of a

diploma.

I would like to mention that the overall experience with the organization was very

good, which helped me to know how the work is carried out in real practice with the

help of your esteemed organization.

I hope I did justice to the project and added some value to your organization.

Suggestions/comments are most welcome/would be appreciated.

Yours truly,

Nitin Kolapkar

viii | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

EXECUTIVE SUMMARY

“Price is what you pay and value is what you get”- Warren Buffet “Intrinsic value” is the worth of an enterprise to one who owns it “for keeps.” Logically, it must be based on the cash flow that would go to a continuing owner over the long run, as distinct from a speculative assessment of its resale value i.e. book value. DCF model and earning power value model can be used for calculating the intrinsic value of an asset or business. In Discounted Cash Flow model, we use FCF because FCF is what we finally get out of that business. The discounting factor that we use in DCF is weighted average cost of capital (WACC). Value investing is a concept coined by Benjamin Graham in his fabulous book “Security Analysis” written in 1934. He led basic principles that value investor uses in the intrinsic valuation of an asset. This principle is still found to be relevant in today's’ age. Many value investors walk on the way defined by Ben Graham. Framework for intrinsic valuation: Analyzing fundamentals of the company which includes studying Income statement (earning power of the company), Balance Sheet (Insights about assets of the company), Cash Flow Statement (Which differentiate accrual accounting vis a vis cash based accounting), Management leadership (How the management is utilizing assets in order to create value for their investors). Using this fundamental, we actually calculate what the company or an asset is worth today. In this research report, we have used two-stage DCF model for intrinsic valuation of Asian Paints and Hero MotoCorp Ltd. Since both the companies are market leaders in their respective industries we were keen to know about their fundamentals. Both the company have consistently created value for their investors. After intrinsic valuation of those two company, it was found that Asian Paint’s share price is undervalued whereas Hero MotoCorp Ltd.’s share price is overvalued. We have also used the concept of margin of safety of 30% for both the stocks in order to come out with the final buy price. MOS is used as a safeguard mechanism because no one can predict the future precisely. A value investor should think ahead of the management in order forecast the future of the company. But no research can ever be wrong or right. All researches are justifiable. Because no valuation comes without an assumption whether it is earnings, capex or FCF. It is the time which can only tell us about the mistakes what we have committed during the valuation. Forecasting is a vital part of the intrinsic valuation because, at the end of the day, results of forecasting give you a signal to take a decision on the stock. Key learning points of forecasting:

1. What all things we need to forecast 2. What is the sensible way of forecasting 3. What errors we generally commit in forecasting 4. How to avoid those errors 5. What is conservative way of doing forecasting 6. What is base rate forecasting

ix | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

7. What is the best case scenario forecasting This internship report will give a complete view of value investing and how it differs from what we have learned in academics. There are many differences in opinions of academicians and value investors about principles of investing.

x | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

ABOUT STOIC ADVISORS

Stoic advisors LLP is an emerging startup started by Mr. Puneet Khurana who is a CFA charter

holder. Mr. Puneet handled research work for some of the prominent hedge funds in Singapore,

Mauritius, and India for around eight years. He believes that Indian investors have many capabilities

but they should be groomed in a good manner. He is a professional investor and visiting faculty in

IIT Delhi, also he is a strong book lover.

Unlike the USA, Indian retail investors are risk averse and also poor in investing in the stock markets

because the lack of financial literacy is prevalent. But he believes that with proper investment

education, Indian investment community can change the face of investing.

In the wake of this, he has started Stoic Advisors a limited liability partnership firm which is providing

advice and insights to value investors. Stoic has achieved many milestones in their journey since

2014. Stoic has started a podcast series on their website stoicinvesting.com. Stoic invites successful

value investor, momentum investors, and decision-makers from India and abroad to share their

journey of investing and nuggets of wisdom. The one on one communication with those investors is

recorded and launched on the websites. Stoic Advisors got a huge response by investor community

since Stoic Advisor’s podcast offers incredible insights from successful investors.

Stoic Advisors also provides advisory services to HNI’s and fund houses. Stoic Advisors is about to

launch a full fledged website which will offer fundamental analysis of stocks listed on NSE and BSE.

Being a follower of Ben Graham and Warren Buffet Puneet is working towards building better

investment society in India.

0 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

CONCEPT OF VALUE INVESTING

The concept of value investing is coined by Benjamin Graham in his book “Security valuation” written

in 1934.

Value Investing Fundamental No. 1: Companies Have Intrinsic Value

The basic concept behind value investing is so simple that you might already do it on a regular basis.

Every asset has some worth. But the worth should be calculated on the basis of its value creation. If

it is cheaper then you will buy it otherwise not.

Most folks would agree that whether you buy a new mobile phone when it's on sale or when it's at

full price, you're getting the same mobile phone with the same features and the same service

warranty. The obvious assumption that we have to make is that the value of the mobile phone will

not depreciate with time as new technology becomes available. Stocks are the same way: the

company's stock price can change even when the company's intrinsic value is the same. Stocks, like

mobile phones, go through periods of higher and lower demand. These fluctuations change prices,

but they don't change what you're getting.

Many savvy shoppers would argue that it makes no sense to pay full price for a mobile phone since

mobile phones go on sale several times a year. Stocks work the same way. The only difference is

that, unlike mobile phones, stocks will not have offered on discount openly, you have worked hard

to find that stock which you are getting on discount. If they were, stocks on sale would be less of a

bargain because more people would know about the sale and drive the price up. If you're willing to

do the detective work to find these secret sales, you can get stocks at a bargain price.

Value Investing Fundamental No. 2: Always Have a Margin of Safety

Buying stocks at bargain prices gives you a better chance at earning a profit later when you sell

them. It also makes you less likely to lose money if the stock doesn't perform as you hope. This

principle called the margin of safety, is one of the keys to successful value investing. Unlike

speculative stocks whose price can plummet, it is less probable that value stocks will continue to

experience price declines.

You might already apply this principle when you shop something. When you buy a new shirt, maybe

you don't like to pay full price because sometimes you feel that this shirt doesn’t deserve. It might

look good and feel comfortable in the store, but then when you wear it in real life, it feels too tight or

too loose or it fades or shrinks in the washing machine. If you buy a shirt on sale for 500 rupees

instead of buying it at full price for 1500 rupees, you will only lose 500 bucks on a bad shirt purchase.

If you pay 1500 rupees, your loss will be significantly greater. By purchasing the shirt on sale for 500

rupees, you limit your potential loss. On the other hand, you might end up wearing the shirt a hundred

times, making it a great bargain at only 500 bucks. Either way, you're better off buying the shirt for

500 than for 1500.But yes, your shirt Shirts’ value will not appreciate, unlike stock.

1 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

Value investors implement the same sort of reasoning. If a stock is worth 100 rupees and you buy it for 75 rupees, you'll make a profit of 25 rupees simply by waiting for the stock's price to rise to the 100 rupees. On above of that, the company might outperform your estimate offering you a chance to earn even more money. If you had purchased it at its full price of 100 rupees, you would only make a 10 rupees’ profit. Benjamin Graham, the father of value investing, only bought stocks when they were priced at two-thirds or less of their intrinsic value. This is the margin of safety that he believed to give the maximum return.

Value Investing Fundamental No. 3: The Efficient-Market Hypothesis Is Wrong

Value investors don't believe in the efficient-market hypothesis, EMH tells us that all the information in incorporated in price. In today's’ age information is no more an edge of investing. Everyone is full of information. If we say that EMH is true, then no stock can ever be treated as undervalued or overvalued. But value investors believe that the stocks are always either undervalued or overvalued or correctly valued. As I said information is no more remained an edge in investing but processing and coming at one judgment is an edge of investing in today's’ world of investing.

Value Investing Fundamental No. 4: Successful Investors Don't Follow the Herd

Value investors possess many characteristics of contrarians – they don't follow the herd. Not only do they reject the efficient-market hypothesis, but when everyone else is buying, they're often selling or standing back. When everyone else is selling, they're buying or holding. Value investors don't buy the most popular stocks of the day (because they're typically overpriced), but they are willing to invest in companies that aren't household names if the financials are good. They also take a second look at stocks that are household names when those stocks' prices have plummeted. Value investors are actually on the journey like an alchemist to find the gems in the mines of coal. What matters to the value investor is the intrinsic value of stock. There are two types of value investors, first who buy growth stocks and the second who buy junk stock. Junk stock buyer will actually liquidate the whole company assets and earn money out of it. Growth stock buyer sticks with the company for 10-15 years.

Value Investing Fundamental No. 5: Beta cannot be considered as a risk

Beta is nothing but the relative volatility of the stock with the market. According to academicians, there are two types of risk Viz. Systematic and unsystematic. Beta captures systematic risk. But value investors such as Warren Buffet openly criticized the concept of beta and Capital Asset Pricing Model (CAPM is used to calculate the cost of equity) as according to them cannot be a risk. The volatility of the stock cannot be a risk. According to warren buffet risk to business can be categorized into two types. First losing the invested capital and second is a business risk (uncertainty of revenue). Therefore, value investors generally prefer to assume the cost of equity rather than calculate it by the proposed wring method.

2 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

OVERVIEW OF INDIAN ECONOMY

With the strong political mandate, India is believed to be a bright spot in the global economic

slowdown. Where world economy is growing at the prospective rate of 2.4% (World Bank), India is

able to achieve a GDP growth of 7.6% in 2015-16 against 7.2% in 2014-15. Which particularly tells

us the potential of this consumption based emerging market. Expectations are running high because

of passionate and strong government. India is proved to be the fastest growing economy in the world.

During the year India has managed to achieve or restore economic stability by using various tools

such as current account deficit, fiscal deficit, and inflation level. Weak commodity prices are proved

to be the major force behind economic stability. The Indian government has achieved a fiscal deficit

target of 3.9% of GDP. Fiscal consolidation by the Indian government has helped India’s sovereign

ratings. Inflation which is measured by CPI remained around 5.5% for most of the part in 2015-16,

whereas WPI remained negative since November 2014. Lower inflation level is mainly due to weak

commodity prices.

Government’s agenda to improve Ease of Doing Business has actually improved FII’s in India which

is an indicator of trust of foreign investors on Indian economy. Also, government’s programs such as

“Jan Dhan Program” for financial inclusion and direct benefit transfer has helped Indian rural

economy. The Indian government has launched “Smart City” program under which hundred smart

cities will be built. Which will create immense employment opportunities in construction sector

consequently will boost demand.

Despite all this Indian agriculture sector has underperformed because of weak monsoon in last two

years. But a recent optimistic report by Institute of Meteorological Dept. has kindled hope in the

corporate world. Since a major chunk of the population depends on agriculture for their livelihood,

monsoon has become the biggest determinant of economic success. Also, the government has

taken various initiatives to invest in rural infrastructure by increasing budgetary support in the recent

union budget.

This year has ended on a strong note of NPAs by Indian banks. Major corporates and banks

remained under stress on account of bad debt problems; this, in turn, has an adverse impact on

private investments. The whole corporate world is hoping for GST bill but, the picture is still gloomy.

On the international front, weak commodity prices such as crude oil have adversely impacted major

crude producing countries in the middle east which in turn affected demand. Devaluation of Chinese

Yuan has made economist worry. The Indian rupee has depreciated significantly during 2015-16

from 62 to nearly 69 Rupees to the US dollar, but Indian economy could not capitalize this opportunity

because of a global slowdown. In fact, India is not the only state of the depreciating currency, it’s

because of strong US dollar.

Meanwhile, Warren Buffet’s MCAP/GDP valuation triggered fear on Dalal Street as India’s

MCAP/GDP ratio is 153 which is more than the threshold. That means market capitalization of Indian

companies is far more overvalued as compared to its GDP if we compare this ratio to other

3 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

economies. Indian economy is consumption-led economy witnessed by 1.25 billion populations.

Which gives a strong mandate to a foreign investor to invest in India. India is proved to be a fastest

growing state in the world.

Recent news of cabinet approval to the Seventh Pay Commission also kindled hope in the corporate

world as it promises to hike salary of central government employees (Nearly 1 crore employee) by

average 23.55%. Which can boost demand in urban India? But one more side of the coin in that it is

gone increase government burden by 1.07 lac crores which will increase fiscal deficit.

This year India has developed a new statistical method to calculate GDP number, but unfortunately

many renowned economists have raised concern about methodology. Recent BREXIT issue has

also shaken world’s stock markets as it triggers fear about the unity of European Union. Stocks like

TCS, TATA MOTORS stumbled on the day of the referendum as their 30-35% topline is contributed

by Britain. Many investors are suffering from uncertainty about new policy framework of exited Britain.

4 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

INDIAN PAINT INDUSTRY OVERVIEW

Indian paint industry has dramatically changed over the years as it moved forward from decorative

paints market to the more diversified seasonal market. There are many factors that helped for the

rapid growth of the Indian paint industry such as adoption of new technology, availability of an

innovative range of products, increased disposable income, rapid urbanization, immense

infrastructure investment. Indian paint industry has grown 12.5% and it is estimated that it will grow

at the rate of 14% CAGR till 2019-20.

Indian paint industry has now begun to look like FMCG industry where brand, distribution, and

innovative use of technology become important determinants of growth. Current market size of

Indian paint industry is estimated at 350 Billion Rupees and which can easily grow at the rate of 12-

13%. In India, the per capita consumption of paint is 4 kgs is very low as compared to the developed

nations. Therefore, it seems that Indian paint industry has an optimistic outlook as the Indian

economy is emerging. As the economy modernizes or develops the per capita consumption of paint

will increase.

Indian paint market is not fully organized as 35% of the paint market is controlled by unorganized

players. There are around 2000 units of small and medium capacity which control this unorganized

paint market. Asian Paints, Kansai Nerolac, Berger Paints, and ICI are top players in Indian paint

industry.

There are two broad categories which drive demand:

Decorative:

This category includes the major segments such as interior wall paints, exterior wall paints, wood

finishes, coatings, enamel and supporting products such as putty, primers, etc. Decorative paint

segment accounts for around 70% of Indian paint market. Asian Paints is the market leader in this

category. Mainly Household painting drives demand for decorative paints. Demand for decorative

paints is seasonal and it is highest in September to November. This category is price sensitive and

it provides higher margin to players as compared to industry paint.

Industrial:

There are three main segments in this category named automotive coatings, powder coatings, and

protective coatings. Kansai Nerolac is the market leader in this category. Industrial paint category

requires more technological innovations as compared to decorative paint category. Therefore, many

domestic players have tied up with foreign players capitalizing their technology.

On an average Indian paint, industry spends 55% of total expenditure for purchase of raw materials

(50% Petro-based derivatives). That is why paint industry is highly dependent on crude oil prices.

Decorative paints are expected to promise higher growth in near term given the favorable economic

conditions and sufficient monsoon. Although demand for industry paint is warm in past year as it is

5 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

highly dependent on automobile sector. Weak monsoon in last two years has affected automobile

industry and consequently industry paint category.

Decorative paint segment is also dependent on the housing market. If we take current year inflation

of around 5.5% and interest rates into consideration, Indian paint industry looks promising. Last three

years were bad for the housing market because of high inflation and high-interest rates but now the

housing market is getting revived given the best monetary policies ever.

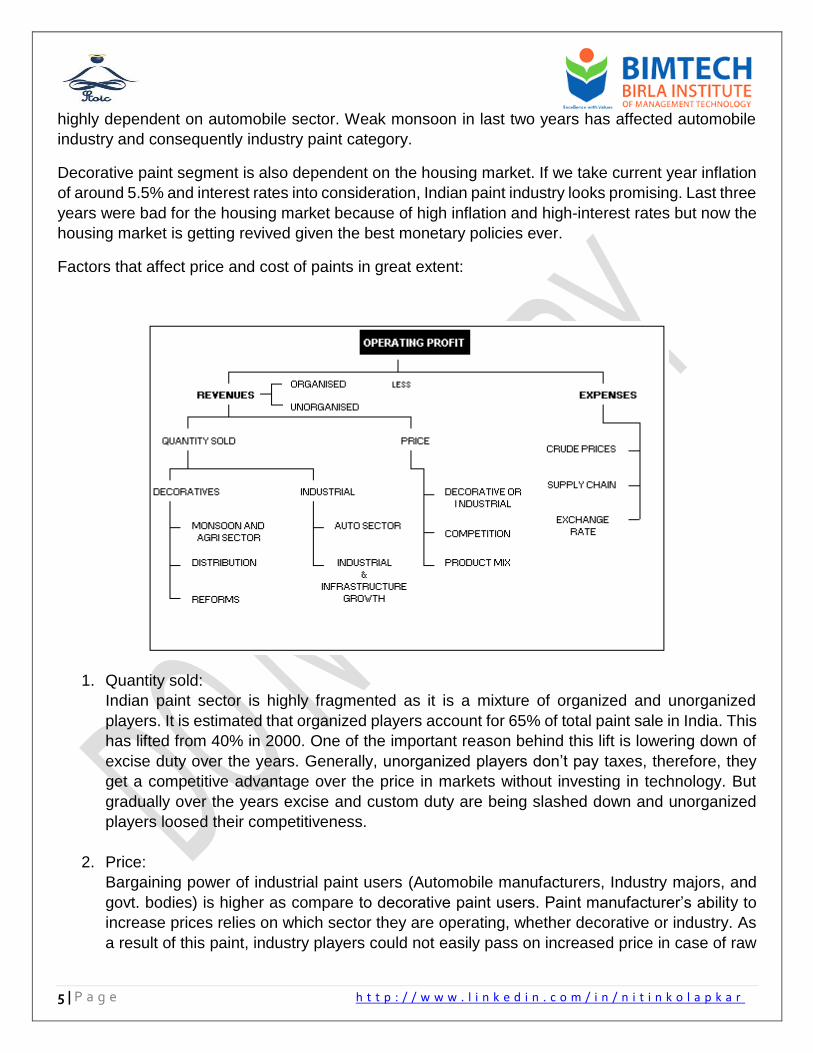

Factors that affect price and cost of paints in great extent:

1. Quantity sold:

Indian paint sector is highly fragmented as it is a mixture of organized and unorganized

players. It is estimated that organized players account for 65% of total paint sale in India. This

has lifted from 40% in 2000. One of the important reason behind this lift is lowering down of

excise duty over the years. Generally, unorganized players don’t pay taxes, therefore, they

get a competitive advantage over the price in markets without investing in technology. But

gradually over the years excise and custom duty are being slashed down and unorganized

players loosed their competitiveness.

2. Price:

Bargaining power of industrial paint users (Automobile manufacturers, Industry majors, and

govt. bodies) is higher as compare to decorative paint users. Paint manufacturer’s ability to

increase prices relies on which sector they are operating, whether decorative or industry. As

a result of this paint, industry players could not easily pass on increased price in case of raw

6 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

material price escalation. Economies of scale have enormous importance in industry paint

manufacturing as compare to decorative paint segment.

However decorative paint industry players can easily raise prices given its brand, product mix.

The decorative paint industry is highly competitive and seasonal. Since the demand is

seasonal, many players lower down prices of decorative paints in festive seasons. The dealer

tinting machine has played a vital role in decorative paint industry in recent years as it has

helped to increase customer engagement in the selection of colors. Therefore, this sector is

highly investing in brand building.

3. Cost:

Crude prices and dollar rate:

Raw material cost accounts for around 50% of total gross expenditure. There are more than

three hundred raw material used in the manufacturing of paints with Titanium Dioxide account

for more than 30% of sales. While some are crude derivatives. In the manufacturing of paint,

crude is used as a source of energy. Therefore, whenever crude prices increase in

international market paint manufactures feel the pressure.

Since Titanium Dioxide in India is of inferior quality, paint manufacturers import it. Therefore,

rupee-dollar movement plays an important role in cost structure. Another important factor is

the strength of supply chain of a company. Since this industry is highly working capital

intensive (300 raw materials) efficient distribution network can easily help the player to

achieve control on cost.

Indian paint sector is now moving towards FMCG status from commodity image.

7 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

ASIAN PAINTS (NSE CODE: ASIANPAINT, BSE CODE: 500820,

CMP:980, FV: ₹ 1)

Asian Paints Limited (the ‘Company’) is a public limited Company incorporated under the Indian Companies Act 1913. The Company is engaged in the business of manufacturing, selling, and distribution of paints, coatings, products related to home décor, bath fittings and providing of related services. Asian Paints was established in 1942 as a partnership firm. Over the course of 25 years, Asian Paints has achieved many milestones. Today Asian Paints is India’s largest player and Asia’s second largest player in paint industry with a turnover of 155 billion rupees. It has operations in 19 countries and has 26 manufacturing facilities, servicing consumers in over 65 countries. Asian Paints is the market leader in paints since 1967. Especially in decorative paints, Asian Paints has more than 50% market share in Indian paint market. Asian paint has a range of products in decorative as well as industry segment.

Besides Asian Paints the company operates in the whole world through its subsidiaries. To name a

few Berger International Limited, Apco Coatings, SCIB Paints, Taubmans and Kadisco. Asian Paints

has consistently made money for shareholders and have a professional reputation in the corporate

world.

The company is mainly present in the decorative segment, which contributes over 75% of its sales. The company features among the top 10 decorative paint players globally. It has a large distribution network of over 25,000 dealers and 27,000 'Colour World' outlets across India. The company's international revenue comes from countries in the Caribbean, Middle East, South Pacific and Asian regions.

In decorative paints, Asian Paints has a presence in interior wall finishes, exterior wall finishes,

enamels and wood finishes. Asian Paints has contributed a lot to the industry by its technologically

prudent innovations such as Colour Worlds (Dealer Tinting System), Home Solution (Painting

Solution Service) and Royal Play Special Effect Paints, etc. Asian Paints has always remained ahead

of the competitors in identifying consumer sentiments. They set a trend of consumer involvement in

the selection of paints in the paint industry. They came up with Signature Stores in Mumbai, Delhi,

and Kolkata, where consumers are educated about colors and how colors can change their dream

homes. They also set up AP Homes a multi-category store which provides a complete solution for

home décor (Kitchen, bath fittings, sanitary wares, paints, furnishings) in Coimbatore (Chennai).

Asian Paint had tied up with Henkel Adhesives, Germany for manufacturing and distributing Loctite

brand of adhesives. Asian Paints got success in vertical integration for manufacturing Phthalic

Anhydride and Pentaerythritol, which is used in paint manufacturing process. Asian Paints also

operates through PPG Asian Paints PVT LTD (50:50 JV between Asian Paints and PPG Inc, USA,

one of the largest automotive coatings manufacturer in the world) in order to service exponentially

growing Indian automotive coating market.

Asian Paints is highly motivated to enter and capture the home décor market. In order to do so, it

has acquired 51% stake in Sleek Group, a leading kitchen solution provider and Ess Ess Bathroom

Products Ltd., a prominent player in bath segment.

8 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

Recently, the company has launched ‘Smart Kitchen’ range for easy installation and design under

the Sleek brand. In the Bath space, it has introduced ‘Royale’ – premium range of bath fittings as

well as ‘Bathsense’ – sanitary ware range of products for the evolving consumer.

The company has a dedicated Group R&D Centre in India for paints and has been one of the

pioneering companies in India for effectively harnessing Information Technology solutions to

maximize efficiency in operations.

AP is successful in identifying consumer sentiment, in lieu of this AP has launched unique color

visualizer app that allows the customer to experience colors and décor. This app also provides color

consultancy to the buyers which offer a unique value proposition in the market. The company is now

preparing to rollout full-fledged ERP software which will give real-time information about inventory

holding at the dealer’s stores and efficiently managing inventory as production. Also, ERP can be

effectively used for the sales forecasting, data mining, and analysis purpose. ERP rollout will

definitely solve the logistics problems that AP is currently facing.

Crisil has rated Asian Paints for long-term debentures, cash credit and working capital loan as an

AAA company.

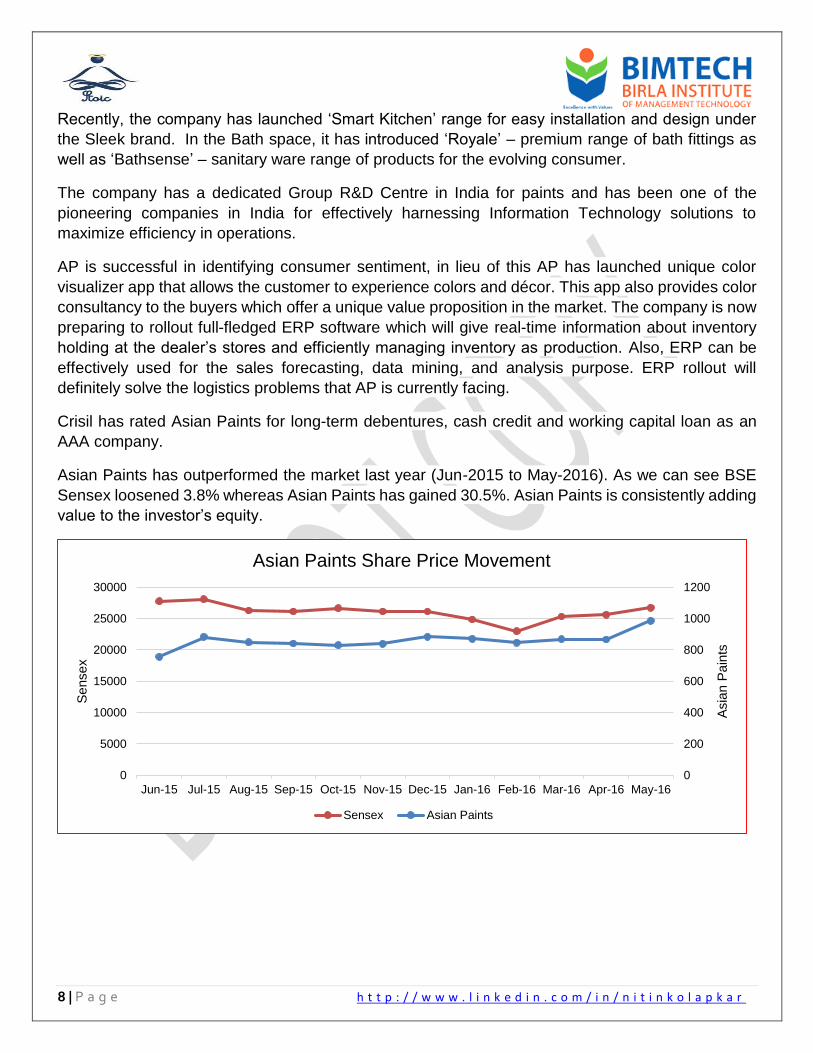

Asian Paints has outperformed the market last year (Jun-2015 to May-2016). As we can see BSE

Sensex loosened 3.8% whereas Asian Paints has gained 30.5%. Asian Paints is consistently adding

value to the investor’s equity.

0

200

400

600

800

1000

1200

0

5000

10000

15000

20000

25000

30000

Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16

Asia

n P

ain

ts

Sensex

Asian Paints Share Price Movement

Sensex Asian Paints

9 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

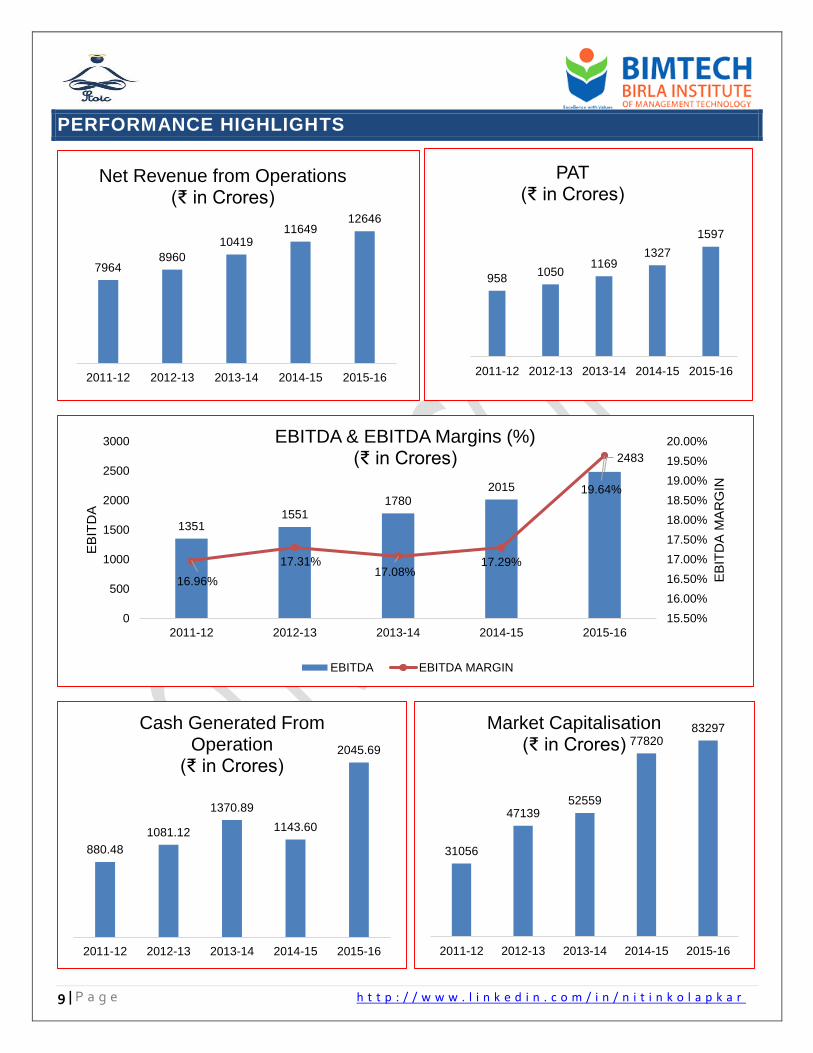

PERFORMANCE HIGHLIGHTS

79648960

1041911649

12646

2011-12 2012-13 2013-14 2014-15 2015-16

Net Revenue from Operations(₹ in Crores)

9581050

11691327

1597

2011-12 2012-13 2013-14 2014-15 2015-16

PAT(₹ in Crores)

13511551

17802015

2483

16.96%

17.31%17.08%

17.29%

19.64%

15.50%

16.00%

16.50%

17.00%

17.50%

18.00%

18.50%

19.00%

19.50%

20.00%

0

500

1000

1500

2000

2500

3000

2011-12 2012-13 2013-14 2014-15 2015-16

EB

ITD

A M

AR

GIN

EB

ITD

A

EBITDA & EBITDA Margins (%)(₹ in Crores)

EBITDA EBITDA MARGIN

880.48

1081.12

1370.89

1143.60

2045.69

2011-12 2012-13 2013-14 2014-15 2015-16

Cash Generated From Operation

(₹ in Crores)

31056

4713952559

7782083297

2011-12 2012-13 2013-14 2014-15 2015-16

Market Capitalisation(₹ in Crores)

10 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

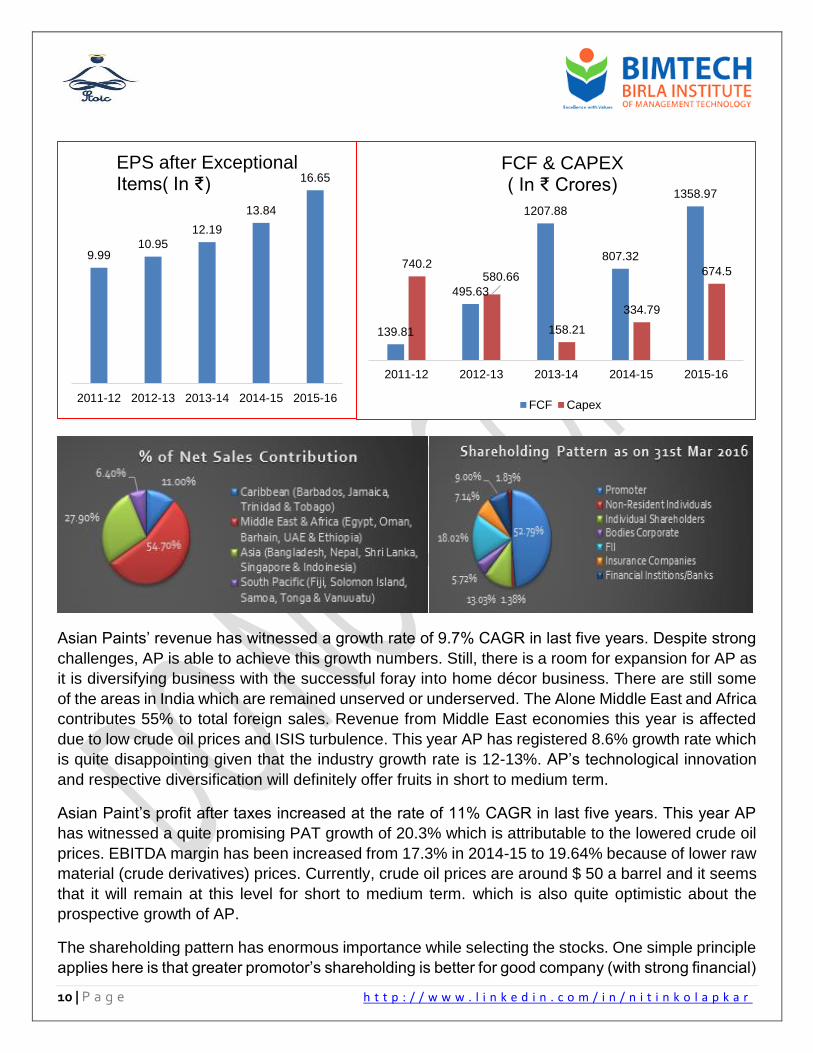

Asian Paints’ revenue has witnessed a growth rate of 9.7% CAGR in last five years. Despite strong

challenges, AP is able to achieve this growth numbers. Still, there is a room for expansion for AP as

it is diversifying business with the successful foray into home décor business. There are still some

of the areas in India which are remained unserved or underserved. The Alone Middle East and Africa

contributes 55% to total foreign sales. Revenue from Middle East economies this year is affected

due to low crude oil prices and ISIS turbulence. This year AP has registered 8.6% growth rate which

is quite disappointing given that the industry growth rate is 12-13%. AP’s technological innovation

and respective diversification will definitely offer fruits in short to medium term.

Asian Paint’s profit after taxes increased at the rate of 11% CAGR in last five years. This year AP

has witnessed a quite promising PAT growth of 20.3% which is attributable to the lowered crude oil

prices. EBITDA margin has been increased from 17.3% in 2014-15 to 19.64% because of lower raw

material (crude derivatives) prices. Currently, crude oil prices are around $ 50 a barrel and it seems

that it will remain at this level for short to medium term. which is also quite optimistic about the

prospective growth of AP.

The shareholding pattern has enormous importance while selecting the stocks. One simple principle

applies here is that greater promotor’s shareholding is better for good company (with strong financial)

9.9910.95

12.19

13.84

16.65

2011-12 2012-13 2013-14 2014-15 2015-16

EPS after ExceptionalItems( In ₹)

139.81

495.63

1207.88

807.32

1358.97

740.2580.66

158.21

334.79

674.5

2011-12 2012-13 2013-14 2014-15 2015-16

FCF & CAPEX( In ₹ Crores)

FCF Capex

11 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

and less promotor shareholding is considered as the worst for bad companies (with weak financials).

AP’s promoters’ shareholding is 53% which is quite promising. Also, a best-practiced value investor

who generally in pursuit of finding hidden gems ignore the stocks which have a mutual fund, FI’s

shareholding in them because they consider that this stock is already identified by many investors.

FII’s holding stands at 18% which clearly shows their trust on AP and likely on Indian paint industry.

But risk-averse investor generally likes the stocks which are held by FI’s, mutual funds, etc. since

they consider it as a safe stock to invest.

12 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

FINANCIAL RATIO ANALYSIS

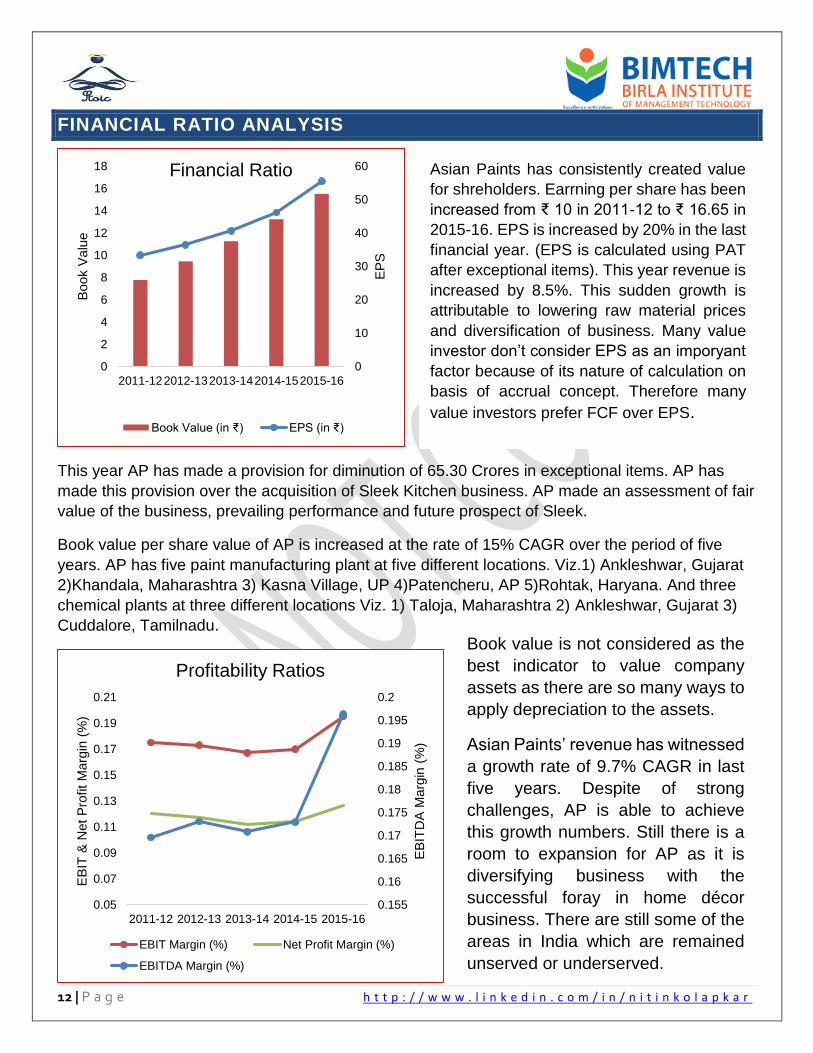

This year AP has made a provision for diminution of 65.30 Crores in exceptional items. AP has

made this provision over the acquisition of Sleek Kitchen business. AP made an assessment of fair

value of the business, prevailing performance and future prospect of Sleek.

Book value per share value of AP is increased at the rate of 15% CAGR over the period of five

years. AP has five paint manufacturing plant at five different locations. Viz.1) Ankleshwar, Gujarat

2)Khandala, Maharashtra 3) Kasna Village, UP 4)Patencheru, AP 5)Rohtak, Haryana. And three

chemical plants at three different locations Viz. 1) Taloja, Maharashtra 2) Ankleshwar, Gujarat 3)

Cuddalore, Tamilnadu.

0

10

20

30

40

50

60

0

2

4

6

8

10

12

14

16

18

2011-122012-132013-142014-152015-16E

PS

Book V

alu

e

Financial Ratio

Book Value (in ₹) EPS (in ₹)

0.155

0.16

0.165

0.17

0.175

0.18

0.185

0.19

0.195

0.2

0.05

0.07

0.09

0.11

0.13

0.15

0.17

0.19

0.21

2011-12 2012-13 2013-14 2014-15 2015-16

EB

ITD

A M

arg

in (

%)

EB

IT &

Net

Pro

fit

Marg

in (

%)

Profitability Ratios

EBIT Margin (%) Net Profit Margin (%)

EBITDA Margin (%)

Asian Paints has consistently created value

for shreholders. Earrning per share has been

increased from ₹ 10 in 2011-12 to ₹ 16.65 in

2015-16. EPS is increased by 20% in the last

financial year. (EPS is calculated using PAT

after exceptional items). This year revenue is

increased by 8.5%. This sudden growth is

attributable to lowering raw material prices

and diversification of business. Many value

investor don’t consider EPS as an imporyant

factor because of its nature of calculation on

basis of accrual concept. Therefore many

value investors prefer FCF over EPS.

Book value is not considered as the

best indicator to value company

assets as there are so many ways to

apply depreciation to the assets.

Asian Paints’ revenue has witnessed

a growth rate of 9.7% CAGR in last

five years. Despite of strong

challenges, AP is able to achieve

this growth numbers. Still there is a

room to expansion for AP as it is

diversifying business with the

successful foray in home décor

business. There are still some of the

areas in India which are remained

unserved or underserved.

13 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

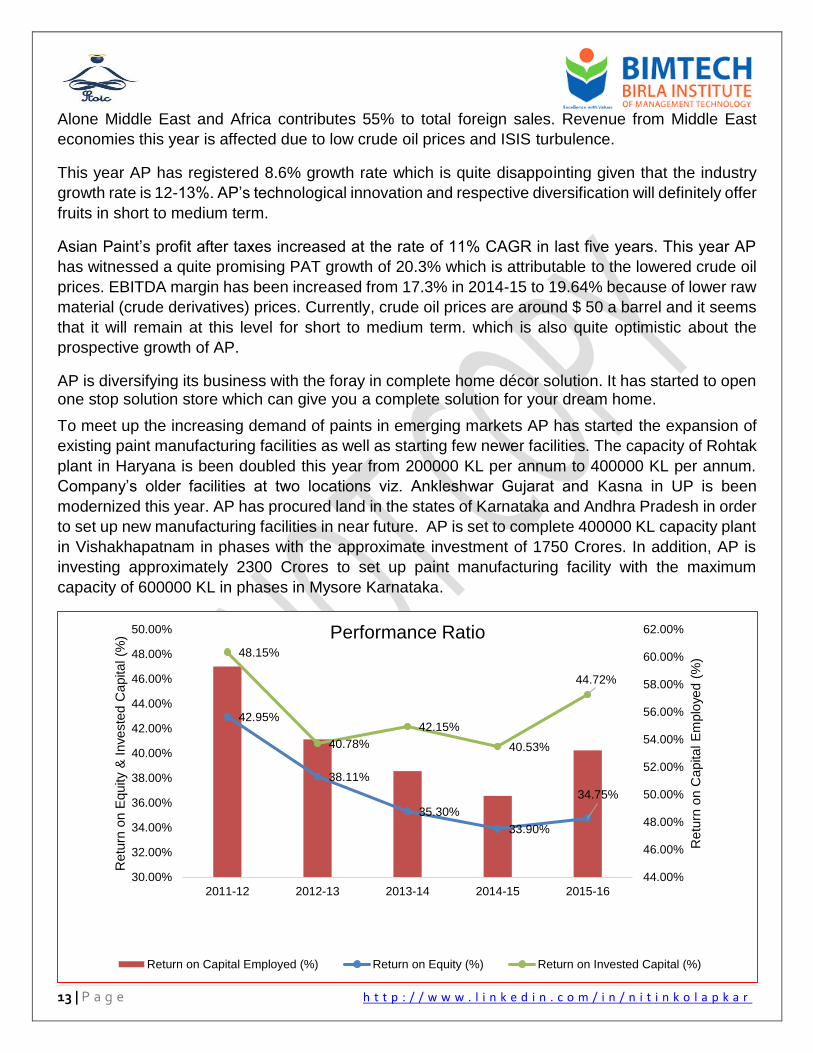

Alone Middle East and Africa contributes 55% to total foreign sales. Revenue from Middle East

economies this year is affected due to low crude oil prices and ISIS turbulence.

This year AP has registered 8.6% growth rate which is quite disappointing given that the industry

growth rate is 12-13%. AP’s technological innovation and respective diversification will definitely offer

fruits in short to medium term.

Asian Paint’s profit after taxes increased at the rate of 11% CAGR in last five years. This year AP

has witnessed a quite promising PAT growth of 20.3% which is attributable to the lowered crude oil

prices. EBITDA margin has been increased from 17.3% in 2014-15 to 19.64% because of lower raw

material (crude derivatives) prices. Currently, crude oil prices are around $ 50 a barrel and it seems

that it will remain at this level for short to medium term. which is also quite optimistic about the

prospective growth of AP.

AP is diversifying its business with the foray in complete home décor solution. It has started to open one stop solution store which can give you a complete solution for your dream home.

To meet up the increasing demand of paints in emerging markets AP has started the expansion of

existing paint manufacturing facilities as well as starting few newer facilities. The capacity of Rohtak

plant in Haryana is been doubled this year from 200000 KL per annum to 400000 KL per annum.

Company’s older facilities at two locations viz. Ankleshwar Gujarat and Kasna in UP is been

modernized this year. AP has procured land in the states of Karnataka and Andhra Pradesh in order

to set up new manufacturing facilities in near future. AP is set to complete 400000 KL capacity plant

in Vishakhapatnam in phases with the approximate investment of 1750 Crores. In addition, AP is

investing approximately 2300 Crores to set up paint manufacturing facility with the maximum

capacity of 600000 KL in phases in Mysore Karnataka.

42.95%

38.11%

35.30%

33.90%

34.75%

48.15%

40.78%

42.15%

40.53%

44.72%

44.00%

46.00%

48.00%

50.00%

52.00%

54.00%

56.00%

58.00%

60.00%

62.00%

30.00%

32.00%

34.00%

36.00%

38.00%

40.00%

42.00%

44.00%

46.00%

48.00%

50.00%

2011-12 2012-13 2013-14 2014-15 2015-16

Retu

rn o

n C

apital E

mplo

yed (

%)

Retu

rn o

n E

quity

& I

nveste

d C

apital (%

) Performance Ratio

Return on Capital Employed (%) Return on Equity (%) Return on Invested Capital (%)

14 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

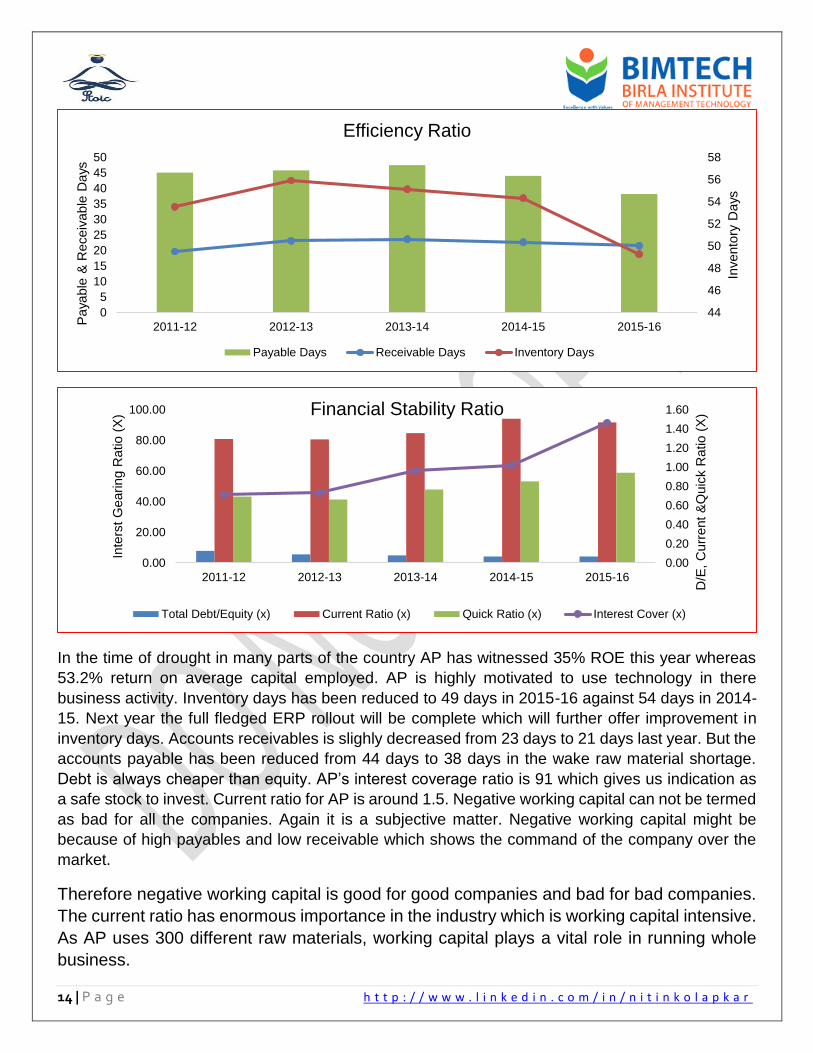

In the time of drought in many parts of the country AP has witnessed 35% ROE this year whereas

53.2% return on average capital employed. AP is highly motivated to use technology in there

business activity. Inventory days has been reduced to 49 days in 2015-16 against 54 days in 2014-

15. Next year the full fledged ERP rollout will be complete which will further offer improvement in

inventory days. Accounts receivables is slighly decreased from 23 days to 21 days last year. But the

accounts payable has been reduced from 44 days to 38 days in the wake raw material shortage.

Debt is always cheaper than equity. AP’s interest coverage ratio is 91 which gives us indication as

a safe stock to invest. Current ratio for AP is around 1.5. Negative working capital can not be termed

as bad for all the companies. Again it is a subjective matter. Negative working capital might be

because of high payables and low receivable which shows the command of the company over the

market.

Therefore negative working capital is good for good companies and bad for bad companies.

The current ratio has enormous importance in the industry which is working capital intensive.

As AP uses 300 different raw materials, working capital plays a vital role in running whole

business.

44

46

48

50

52

54

56

58

0

5

10

15

20

25

30

35

40

45

50

2011-12 2012-13 2013-14 2014-15 2015-16

Invento

ry D

ays

Paya

ble

& R

eceiv

able

Days

Efficiency Ratio

Payable Days Receivable Days Inventory Days

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

0.00

20.00

40.00

60.00

80.00

100.00

2011-12 2012-13 2013-14 2014-15 2015-16

D/E

, C

urr

ent

&Q

uic

k R

atio (

X)

Inte

rst

Gearing R

atio (

X) Financial Stability Ratio

Total Debt/Equity (x) Current Ratio (x) Quick Ratio (x) Interest Cover (x)

15 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

PORTER’S FIVE FORCES ANALYSIS

BARGAINING POWER OF SUPPLIERS

The paint industry is basically working capital intensive as it uses more than 300 raw materials in the

manufacturing. Among them, Titanium Dioxide is major content. After 2008-09 crisis, all the Titanium

Dioxide plant present is the USA and Europe forced to close then. Till now the global supply of TiO2

is not able to meet up with the growing demand. China is one biggest producer of TiO2. But Chinese

TiO2 is of inferior quality to USA’s TiO2. DUPONT is a major player available in the USA which

manufactures high-quality TiO2. Other raw material components are crude derivatives; the price of

crude derivatives depends on international crude prices. AP is the only player in paint industry who

manufactures Phthalic Anhydride which is an important raw material required in paint manufacturing.

In fact, AP is thriving to achieve full fledge vertical integration. Therefore, overall bargaining power

of suppliers in mediocre.

BARGAINING POWER OF THE BUYERS

The end user of this paints are industry are corporates and households. Decorative paint buyers

have much more options available in the market. Over the years Asian Paints increased consumer

involvement in the selection of decorative paints. Dealer tinting machine is one of the disruptions

that helped Asian paints achieve this position. Decorative paint buyers are price sensitive which

pressures paint manufactures. They have many more options available in the market. Understanding

this condition Asian Paint in past made huge investment to create a brand. Asian Paint has a

reputation to run a successful marketing campaigns.

Industrial paint segment is high revenue low margin business. The buyer of industrial paints is

generally automotive industries. Very prudently they compare prices and select their vendor. But

fortunately industrial paint business would have to run on economies of scale principle. And very few

players achieved this. Industry paints contribute 30% to the topline of Asian Paints. Therefore,

bargaining power of Asian Paints buyers is medium.

THREAT OF NEW ENTRANT

The paint industry is working capital intensive industry as it requires 300 different raw materials to

manufacture paint. Technological innovation in paint industry is critical factor to witness success.

Indian paint market is dominated by 5-6 major players as they have made huge investments in brand

building, distribution network, research, and development. Scarce availability of raw material is also

a critical factor while establishing new paint industry. In fact, technology, intensive working capital,

brand equity, supply chain are the critical factors which create barriers to the new entrant. Therefore,

the threat of new entrant is very low in the paint industry.

THREAT OF SUBSTITUTE

16 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

In rural areas lime wash is used as a substitute. Another alternative to the wall paint is wallpaper.

But the price of the wallpaper is too high as compared to the paints. And now there are many varieties

available in the market which can easily emulate the wallpapers. By considering this factors Asian

Paints forayed into home décor space where they are developing a complete solution to the house

décor. Therefore, the threat of substitute is very low.

COMPETITIVE RIVALRY

Asian Paints is the dominant player in the market with the market share more than 50%. About 80%

of the organized paint market is contributed by only three players. AP is dominant in decorative paint

segment. Where AP has actually capitalized the innovative technologies and not the product. AP’s

R & D Centre are renowned and world class. This year AP got success in registering five patents.

AP is the only paint company which manufactures phthalic Anhydride which is an important raw

material. In fact, AP is thriving to achieve full fledge vertical integration. The unorganized industry

players are small and don’t use much technology. In industry paint segment Kansai Nerolac is

dominant. The industrial paint industry is technology intensive which demands continuous

technology up gradation. The competitive rivalry for AP is medium.

17 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

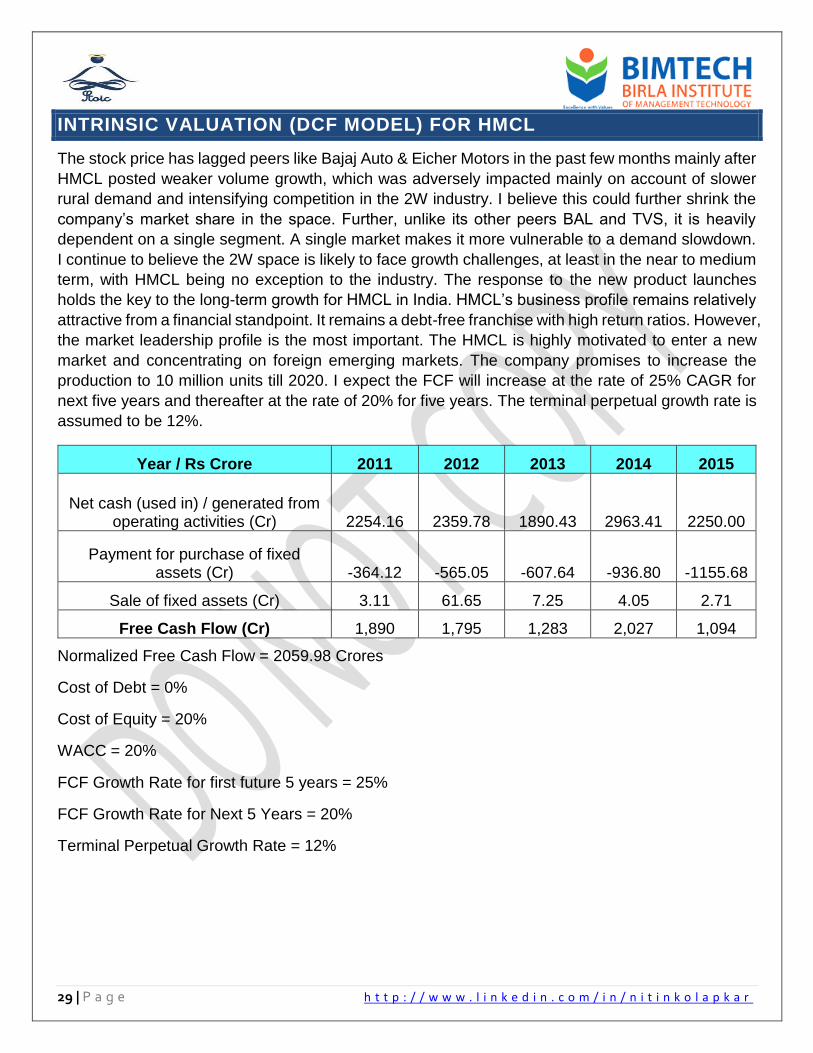

INTRINSIC VALUATION (DCF MODEL)

“Intrinsic value” is the worth of an enterprise to one who owns it “for keeps.” Logically, it must be based on the cash flow that would go to a continuing owner over the long run, as distinct from a speculative assessment of its resale value i.e. book value. DCF model can be used for calculating the intrinsic value of an asset or business. In Discounted Cash Flow model, we use FCF because FCF is what we finally get out of that business. The discounting factor that we use in DCF is weighted average cost of capital (WACC).

WEIGHTED AVERAGE COST OF CAPITAL (WACC)

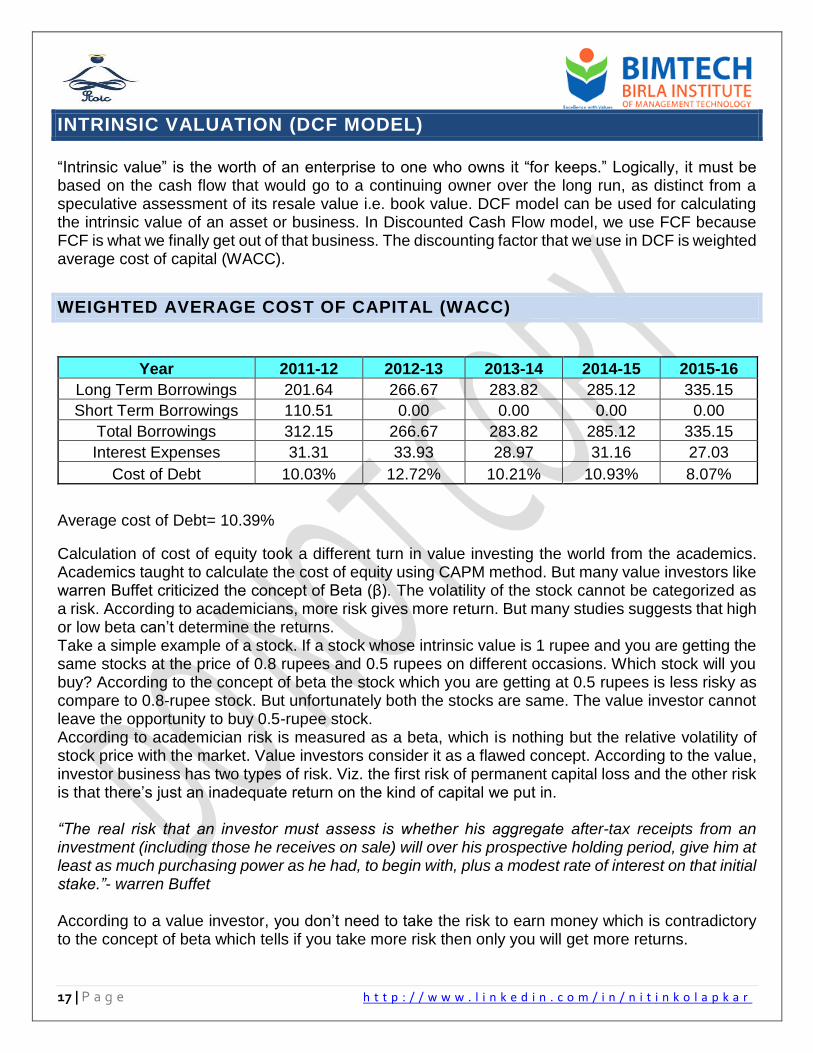

Year 2011-12 2012-13 2013-14 2014-15 2015-16

Long Term Borrowings 201.64 266.67 283.82 285.12 335.15

Short Term Borrowings 110.51 0.00 0.00 0.00 0.00

Total Borrowings 312.15 266.67 283.82 285.12 335.15

Interest Expenses 31.31 33.93 28.97 31.16 27.03

Cost of Debt 10.03% 12.72% 10.21% 10.93% 8.07%

Average cost of Debt= 10.39%

Calculation of cost of equity took a different turn in value investing the world from the academics. Academics taught to calculate the cost of equity using CAPM method. But many value investors like warren Buffet criticized the concept of Beta (β). The volatility of the stock cannot be categorized as a risk. According to academicians, more risk gives more return. But many studies suggests that high or low beta can’t determine the returns. Take a simple example of a stock. If a stock whose intrinsic value is 1 rupee and you are getting the same stocks at the price of 0.8 rupees and 0.5 rupees on different occasions. Which stock will you buy? According to the concept of beta the stock which you are getting at 0.5 rupees is less risky as compare to 0.8-rupee stock. But unfortunately both the stocks are same. The value investor cannot leave the opportunity to buy 0.5-rupee stock. According to academician risk is measured as a beta, which is nothing but the relative volatility of stock price with the market. Value investors consider it as a flawed concept. According to the value, investor business has two types of risk. Viz. the first risk of permanent capital loss and the other risk is that there’s just an inadequate return on the kind of capital we put in. “The real risk that an investor must assess is whether his aggregate after-tax receipts from an investment (including those he receives on sale) will over his prospective holding period, give him at least as much purchasing power as he had, to begin with, plus a modest rate of interest on that initial stake.”- warren Buffet According to a value investor, you don’t need to take the risk to earn money which is contradictory to the concept of beta which tells if you take more risk then only you will get more returns.

18 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

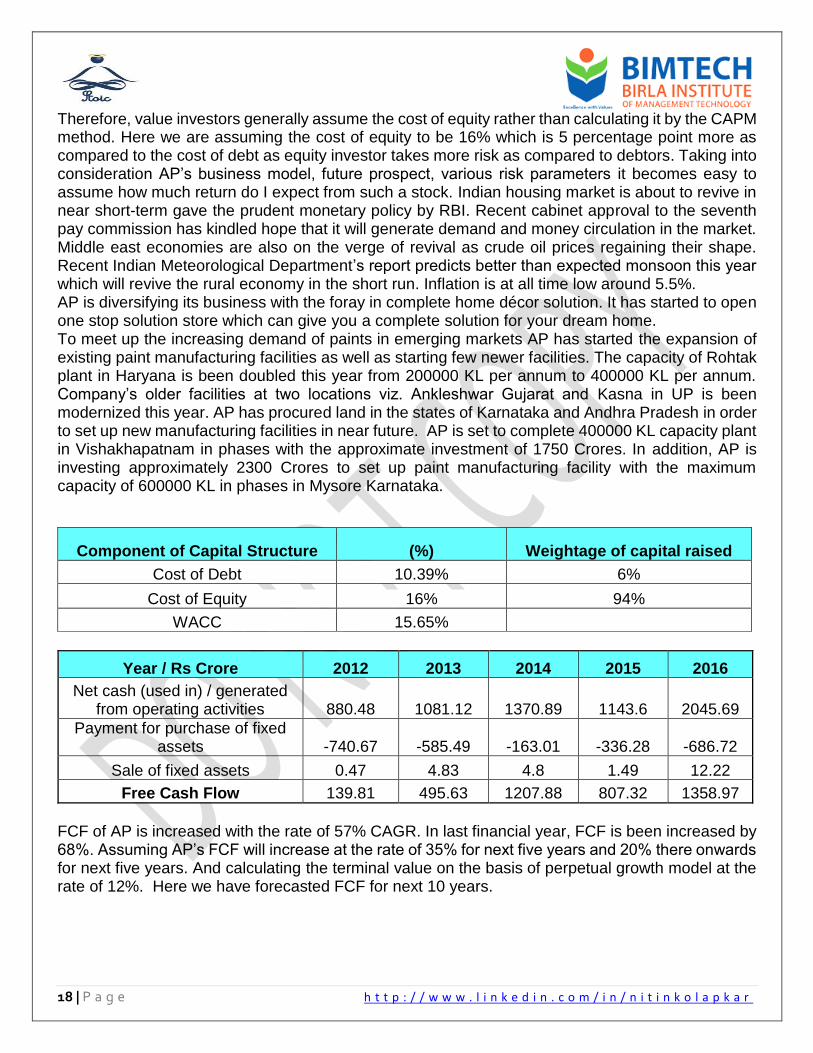

Therefore, value investors generally assume the cost of equity rather than calculating it by the CAPM method. Here we are assuming the cost of equity to be 16% which is 5 percentage point more as compared to the cost of debt as equity investor takes more risk as compared to debtors. Taking into consideration AP’s business model, future prospect, various risk parameters it becomes easy to assume how much return do I expect from such a stock. Indian housing market is about to revive in near short-term gave the prudent monetary policy by RBI. Recent cabinet approval to the seventh pay commission has kindled hope that it will generate demand and money circulation in the market. Middle east economies are also on the verge of revival as crude oil prices regaining their shape. Recent Indian Meteorological Department’s report predicts better than expected monsoon this year which will revive the rural economy in the short run. Inflation is at all time low around 5.5%. AP is diversifying its business with the foray in complete home décor solution. It has started to open one stop solution store which can give you a complete solution for your dream home. To meet up the increasing demand of paints in emerging markets AP has started the expansion of existing paint manufacturing facilities as well as starting few newer facilities. The capacity of Rohtak plant in Haryana is been doubled this year from 200000 KL per annum to 400000 KL per annum. Company’s older facilities at two locations viz. Ankleshwar Gujarat and Kasna in UP is been modernized this year. AP has procured land in the states of Karnataka and Andhra Pradesh in order to set up new manufacturing facilities in near future. AP is set to complete 400000 KL capacity plant in Vishakhapatnam in phases with the approximate investment of 1750 Crores. In addition, AP is investing approximately 2300 Crores to set up paint manufacturing facility with the maximum capacity of 600000 KL in phases in Mysore Karnataka.

Component of Capital Structure (%) Weightage of capital raised

Cost of Debt 10.39% 6%

Cost of Equity 16% 94%

WACC 15.65%

Year / Rs Crore 2012 2013 2014 2015 2016

Net cash (used in) / generated from operating activities 880.48 1081.12 1370.89 1143.6 2045.69

Payment for purchase of fixed assets -740.67 -585.49 -163.01 -336.28 -686.72

Sale of fixed assets 0.47 4.83 4.8 1.49 12.22

Free Cash Flow 139.81 495.63 1207.88 807.32 1358.97

FCF of AP is increased with the rate of 57% CAGR. In last financial year, FCF is been increased by 68%. Assuming AP’s FCF will increase at the rate of 35% for next five years and 20% there onwards for next five years. And calculating the terminal value on the basis of perpetual growth model at the rate of 12%. Here we have forecasted FCF for next 10 years.

19 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

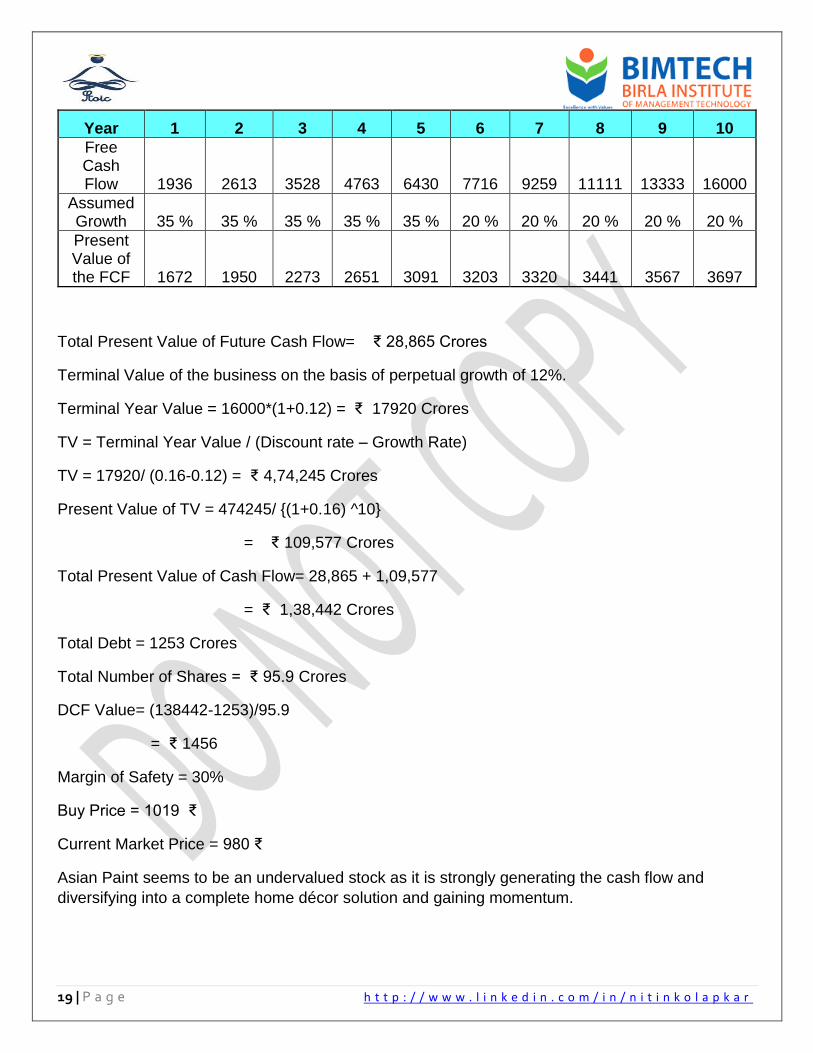

Year 1 2 3 4 5 6 7 8 9 10

Free Cash Flow 1936 2613 3528 4763 6430 7716 9259 11111 13333 16000

Assumed Growth 35 % 35 % 35 % 35 % 35 % 20 % 20 % 20 % 20 % 20 %

Present Value of the FCF 1672 1950 2273 2651 3091 3203 3320 3441 3567 3697

Total Present Value of Future Cash Flow= ₹ 28,865 Crores

Terminal Value of the business on the basis of perpetual growth of 12%.

Terminal Year Value = 16000*(1+0.12) = ₹ 17920 Crores

TV = Terminal Year Value / (Discount rate – Growth Rate)

TV = 17920/ (0.16-0.12) = ₹ 4,74,245 Crores

Present Value of TV = 474245/ {(1+0.16) ^10}

= ₹ 109,577 Crores

Total Present Value of Cash Flow= 28,865 + 1,09,577

= ₹ 1,38,442 Crores

Total Debt = 1253 Crores

Total Number of Shares = ₹ 95.9 Crores

DCF Value= (138442-1253)/95.9

= ₹ 1456

Margin of Safety = 30%

Buy Price = 1019 ₹

Current Market Price = 980 ₹

Asian Paint seems to be an undervalued stock as it is strongly generating the cash flow and

diversifying into a complete home décor solution and gaining momentum.

20 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

HERO MOTOCORP (NSE CODE: HEROMOTOCO, BSE CODE: 500182,

CMP:3186, FV: ₹ 2)

Hero MotoCorp Ltd. is the world's largest manufacturer of two – wheelers. In 2001, the company

achieved this coveted position of being the largest two-wheeler manufacturing company in India and

also, the World No.1 two-wheeler company in terms of unit volume sales in a calendar year. Hero

MotoCorp Ltd. continues to maintain this position till the date. Hero MotoCorp (HMCL) is a leading

2W manufacturer globally and the market leader in the domestic motorcycle segment with

approximately 52% market share. HMCL has four manufacturing facilities in India, located at four

different locations Viz.Gurgaon, Dharuhera, Haridwar and Neemrana. HMCL’s total capacity is

7.7mn units/year as of FY2014. Over 2008 to 2014, HMCL recorded a strong volume growth of 11%

CAGR, with its two strong brands (Passion and Splendor) and a well-entrenched dealership and

distribution network around rural India. Rural areas contribute for 49% of total volumes of the

company. Hero MotoCorp Sales from operation grew at an impressive 25.88 % CAGR. The company

is sitting on the reserves in excess of Rupees 5,582.70 Cr and is enjoying debt-free position for the

past 13 years. The company has an impressive dividend history and has maintained an average

dividend yield of 3.93 % over the last 5 financial years.

INDIAN TWO WHEELER AUTOMOBILE INDUSTRY OVERVIEW

Indian 2W market is continued to dominate in the automobile industry. 2W production accounts for

79% of total vehicle production in India against 75% five years ago. Two Wheelers sales registered

growth of 8.09 percent in April-March 2015 over April-March 2014. Within the Two Wheelers

segment, Scooters, Motorcycles, and Mopeds grew by 25.06 percent, 2.50 percent, and 4.51 percent

respectively in April-March 2015 over April-March 2014.

1.17

1.34 1.37

1.48

1.591.64

2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

Two Wheelers Domestic Sales Units(Crores)

The overall outlook for the 2W industry remains to be promising because in a country like India four out of five homes don’t possess 2W. There is tremendous room to grow in emerging markets such as India. Besides, over the last decade, 2W ownership in rural homes significantly increased. Automobile Export has been increased at the rate of 14.9% in Apr-Mar 2015 over the same period last year. 2015-16 has proved to be lukewarm for 2W industry as it has witnessed only 1% growth in export in number of units.

21 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

Domestic sale of 2W is increased by ~3.2% which is quite disappointing, main reason behind this slower growth is consecutive drought for last two years. The 2W industry comprises three distinct categories Viz. entry, Deluxe and Premium. In 2014-15 entry and premium category accounts for 18.8% of the sales each whereas deluxe category accounts for 62.4% of sales. Deluxe, Entry and Premium have witnessed -2.1%, 8.4%, 21,5% growth during 2014-15.

[

1.33

1.54 1.571.68

1.84 1.88

2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

Two Wheelers Units Production (Crores)

15.31

19.75 19.5620.84

24.57 24.81

2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

Two Wheelers Exported Units (Lacs)

22 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

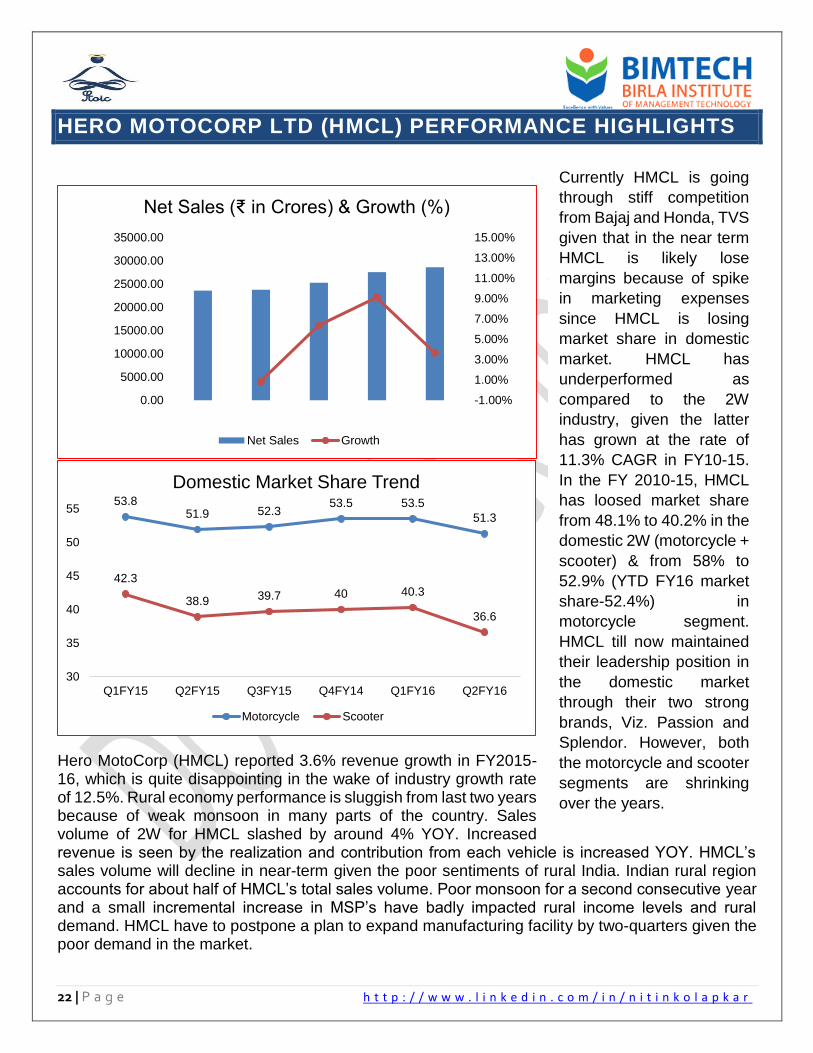

HERO MOTOCORP LTD (HMCL) PERFORMANCE HIGHLIGHTS

Hero MotoCorp (HMCL) reported 3.6% revenue growth in FY2015-16, which is quite disappointing in the wake of industry growth rate of 12.5%. Rural economy performance is sluggish from last two years because of weak monsoon in many parts of the country. Sales volume of 2W for HMCL slashed by around 4% YOY. Increased revenue is seen by the realization and contribution from each vehicle is increased YOY. HMCL’s sales volume will decline in near-term given the poor sentiments of rural India. Indian rural region accounts for about half of HMCL’s total sales volume. Poor monsoon for a second consecutive year and a small incremental increase in MSP’s have badly impacted rural income levels and rural demand. HMCL have to postpone a plan to expand manufacturing facility by two-quarters given the poor demand in the market.

-1.00%

1.00%

3.00%

5.00%

7.00%

9.00%

11.00%

13.00%

15.00%

0.00

5000.00

10000.00

15000.00

20000.00

25000.00

30000.00

35000.00

Net Sales (₹ in Crores) & Growth (%)

Net Sales Growth

53.851.9 52.3

53.5 53.5

51.3

42.3

38.9 39.7 40 40.3

36.6

30

35

40

45

50

55

Q1FY15 Q2FY15 Q3FY15 Q4FY14 Q1FY16 Q2FY16

Domestic Market Share Trend

Motorcycle Scooter

Currently HMCL is going

through stiff competition

from Bajaj and Honda, TVS

given that in the near term

HMCL is likely lose

margins because of spike

in marketing expenses

since HMCL is losing

market share in domestic

market. HMCL has

underperformed as

compared to the 2W

industry, given the latter

has grown at the rate of

11.3% CAGR in FY10-15.

In the FY 2010-15, HMCL

has loosed market share

from 48.1% to 40.2% in the

domestic 2W (motorcycle +

scooter) & from 58% to

52.9% (YTD FY16 market

share-52.4%) in

motorcycle segment.

HMCL till now maintained

their leadership position in

the domestic market

through their two strong

brands, Viz. Passion and

Splendor. However, both

the motorcycle and scooter

segments are shrinking

over the years.

23 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

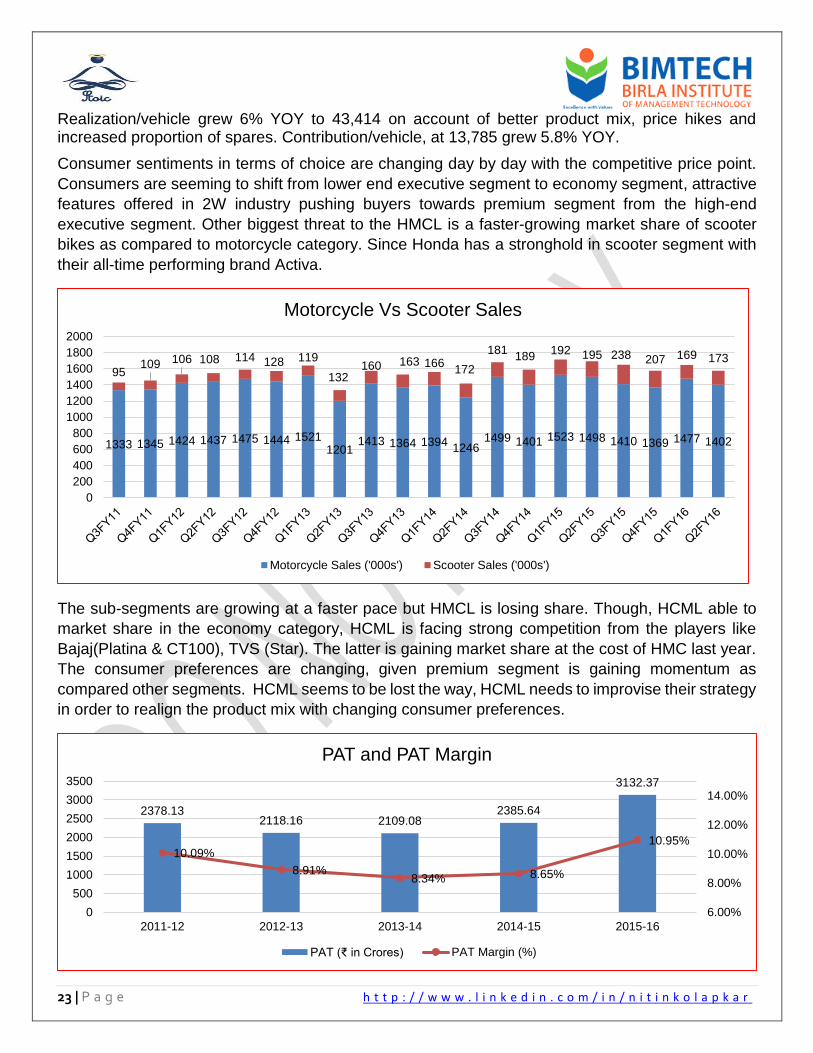

Realization/vehicle grew 6% YOY to 43,414 on account of better product mix, price hikes and increased proportion of spares. Contribution/vehicle, at 13,785 grew 5.8% YOY.

Consumer sentiments in terms of choice are changing day by day with the competitive price point.

Consumers are seeming to shift from lower end executive segment to economy segment, attractive

features offered in 2W industry pushing buyers towards premium segment from the high-end

executive segment. Other biggest threat to the HMCL is a faster-growing market share of scooter

bikes as compared to motorcycle category. Since Honda has a stronghold in scooter segment with

their all-time performing brand Activa.

The sub-segments are growing at a faster pace but HMCL is losing share. Though, HCML able to

market share in the economy category, HCML is facing strong competition from the players like

Bajaj(Platina & CT100), TVS (Star). The latter is gaining market share at the cost of HMC last year.

The consumer preferences are changing, given premium segment is gaining momentum as

compared other segments. HCML seems to be lost the way, HCML needs to improvise their strategy

in order to realign the product mix with changing consumer preferences.

1333 1345 1424 1437 1475 1444 15211201

1413 1364 13941246

1499 1401 1523 1498 1410 1369 1477 1402

95109 106 108 114 128 119

132160 163 166

172

181189

192 195 238 207 169 173

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Motorcycle Vs Scooter Sales

Motorcycle Sales ('000s') Scooter Sales ('000s')

2378.132118.16 2109.08

2385.64

3132.37

10.09%

8.91%8.34% 8.65%

10.95%

6.00%

8.00%

10.00%

12.00%

14.00%

0

500

1000

1500

2000

2500

3000

3500

2011-12 2012-13 2013-14 2014-15 2015-16

PAT and PAT Margin

PAT (₹ in Crores) PAT Margin (%)

24 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

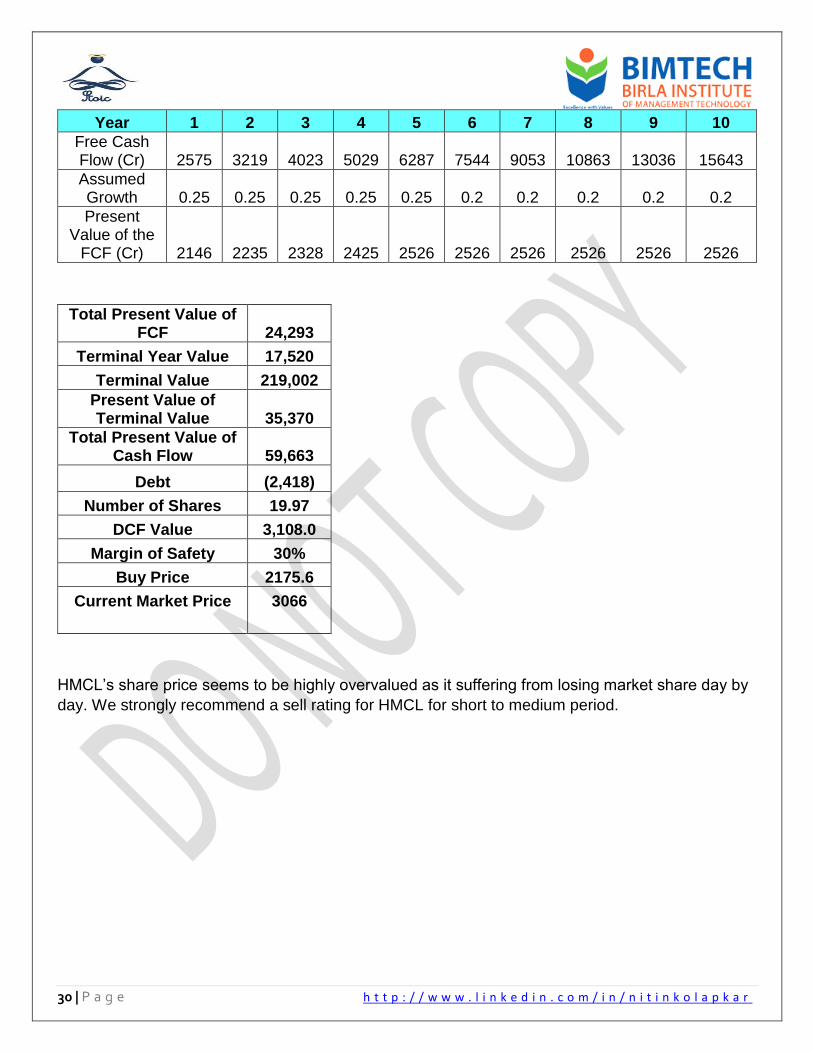

The company reported a PAT of 3132 in 2015-16 crores against 2385 crores last year 2014-15.

HMCL witnessed quite promising 10.95% PAT margin which is highest in last 5 years. Raw material

prices play a vital role in witnessing margins. Major metals used in manufacturing 2W are Nickel,

Steel, and Aluminum. The prices of those commodities remained as expected for last year.

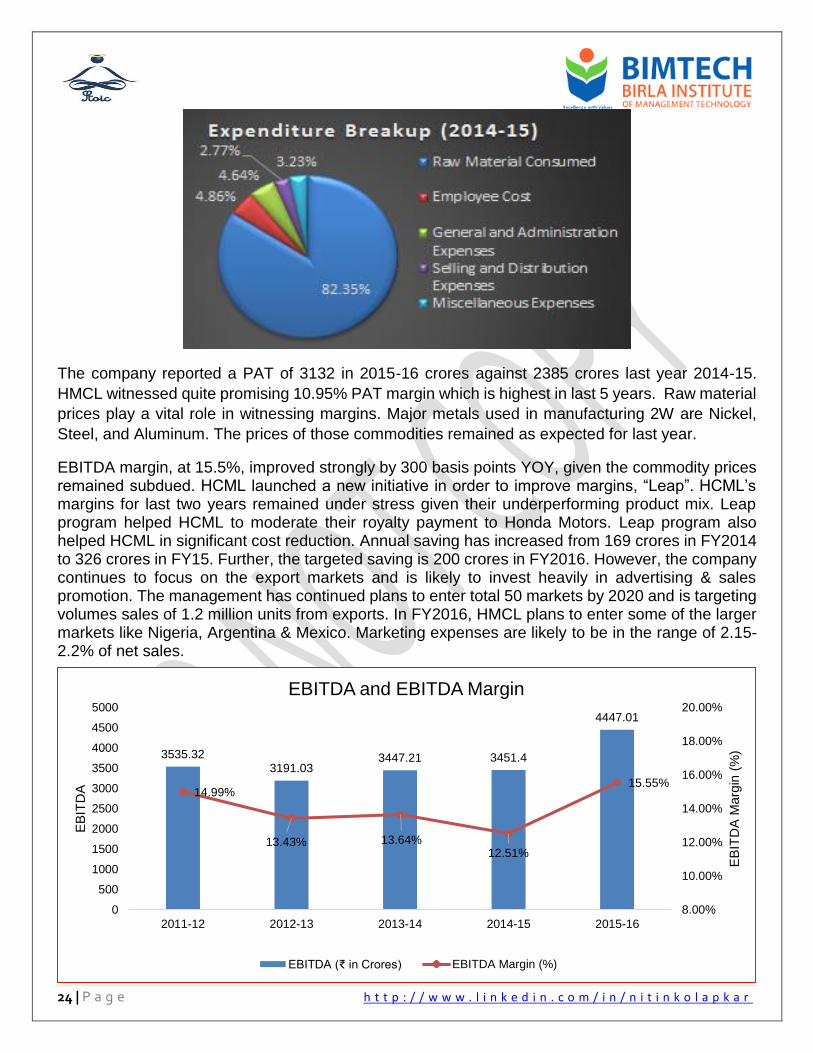

EBITDA margin, at 15.5%, improved strongly by 300 basis points YOY, given the commodity prices remained subdued. HCML launched a new initiative in order to improve margins, “Leap”. HCML’s margins for last two years remained under stress given their underperforming product mix. Leap program helped HCML to moderate their royalty payment to Honda Motors. Leap program also helped HCML in significant cost reduction. Annual saving has increased from 169 crores in FY2014 to 326 crores in FY15. Further, the targeted saving is 200 crores in FY2016. However, the company continues to focus on the export markets and is likely to invest heavily in advertising & sales promotion. The management has continued plans to enter total 50 markets by 2020 and is targeting volumes sales of 1.2 million units from exports. In FY2016, HMCL plans to enter some of the larger markets like Nigeria, Argentina & Mexico. Marketing expenses are likely to be in the range of 2.15-2.2% of net sales.

3535.323191.03

3447.21 3451.4

4447.01

14.99%

13.43% 13.64%12.51%

15.55%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2011-12 2012-13 2013-14 2014-15 2015-16

EB

ITD

A M

arg

in (

%)

EB

ITD

A

EBITDA and EBITDA Margin

EBITDA (₹ in Crores) EBITDA Margin (%)

25 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

17404

18836

22386

27957

23779

2054.85

1541.9

2272.85

2642.6

2940

0

500

1000

1500

2000

2500

3000

3500

5000

10000

15000

20000

25000

30000

2011-12 2012-13 2013-14 2014-15 2015-16H

MC

Sensex

Sensex Vs HMC

Sensex 31st Mar HMC Stock Price (in ₹)

119

106 106

119

157

2011-12 2012-13 2013-14 2014-15 2015-16

EPS ( in ₹)

Category Shares

Held (%)

Promoter (Indian) 34.64%

Mutual Funds / UTI 3.41%

Financial Institutions / Banks 1.14%

Insurance Companies 6.34%

Foreign Institutional Investors 40.77%

Bodies Corporate 1.76%

Indian Public 6.76%

Trusts 0.64%

Clearing Members 0.11%

Non-Resident Indians 0.16%

Foreign Bodies 4.27%

26 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

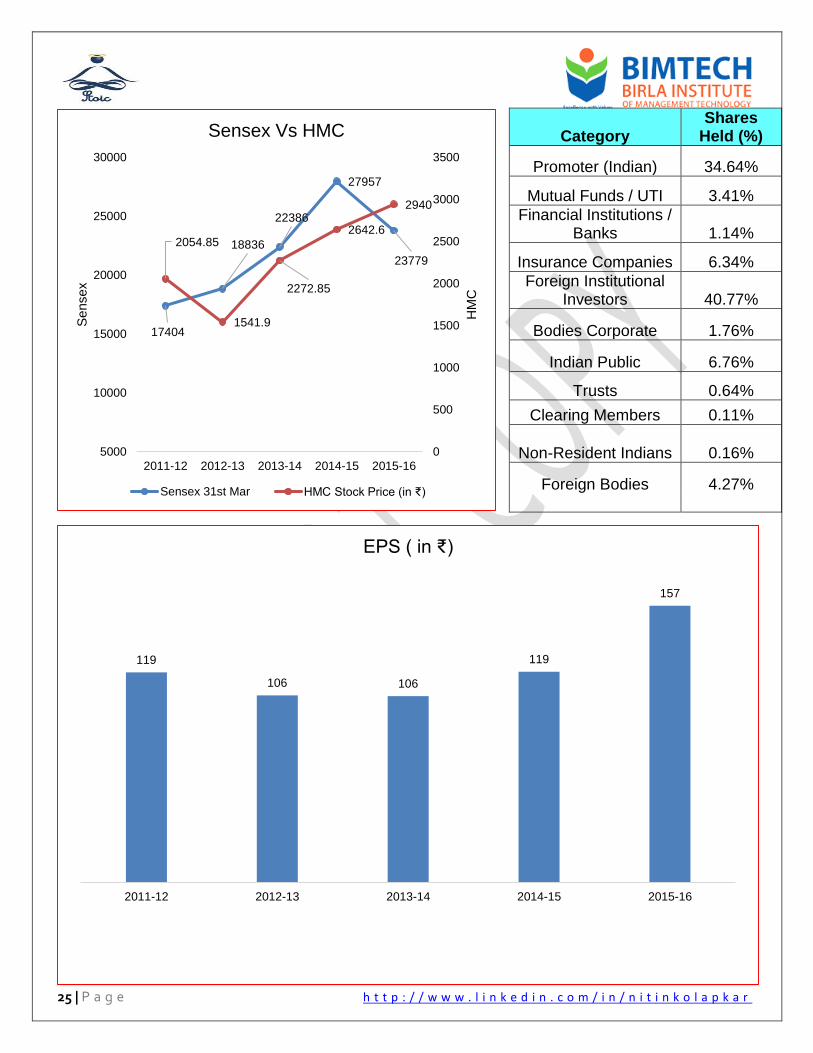

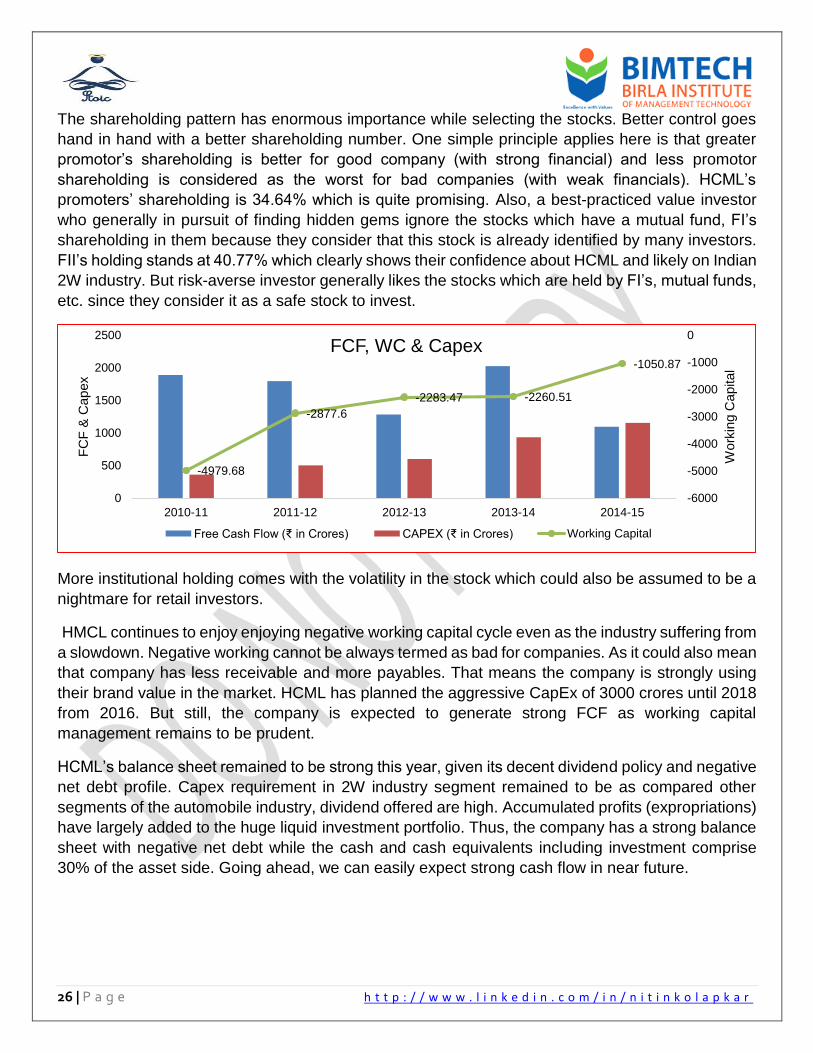

The shareholding pattern has enormous importance while selecting the stocks. Better control goes

hand in hand with a better shareholding number. One simple principle applies here is that greater

promotor’s shareholding is better for good company (with strong financial) and less promotor

shareholding is considered as the worst for bad companies (with weak financials). HCML’s

promoters’ shareholding is 34.64% which is quite promising. Also, a best-practiced value investor

who generally in pursuit of finding hidden gems ignore the stocks which have a mutual fund, FI’s

shareholding in them because they consider that this stock is already identified by many investors.

FII’s holding stands at 40.77% which clearly shows their confidence about HCML and likely on Indian

2W industry. But risk-averse investor generally likes the stocks which are held by FI’s, mutual funds,

etc. since they consider it as a safe stock to invest.

More institutional holding comes with the volatility in the stock which could also be assumed to be a

nightmare for retail investors.

HMCL continues to enjoy enjoying negative working capital cycle even as the industry suffering from

a slowdown. Negative working cannot be always termed as bad for companies. As it could also mean

that company has less receivable and more payables. That means the company is strongly using

their brand value in the market. HCML has planned the aggressive CapEx of 3000 crores until 2018

from 2016. But still, the company is expected to generate strong FCF as working capital

management remains to be prudent.

HCML’s balance sheet remained to be strong this year, given its decent dividend policy and negative

net debt profile. Capex requirement in 2W industry segment remained to be as compared other

segments of the automobile industry, dividend offered are high. Accumulated profits (expropriations)

have largely added to the huge liquid investment portfolio. Thus, the company has a strong balance

sheet with negative net debt while the cash and cash equivalents including investment comprise

30% of the asset side. Going ahead, we can easily expect strong cash flow in near future.

-4979.68

-2877.6

-2283.47 -2260.51

-1050.87

-6000

-5000

-4000

-3000

-2000

-1000

0

0

500

1000

1500

2000

2500

2010-11 2011-12 2012-13 2013-14 2014-15

Work

ing C

apital

FC

F &

Capex

FCF, WC & Capex

Free Cash Flow (₹ in Crores) CAPEX (₹ in Crores) Working Capital

27 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

FINANCIAL RATIO ANALYSIS

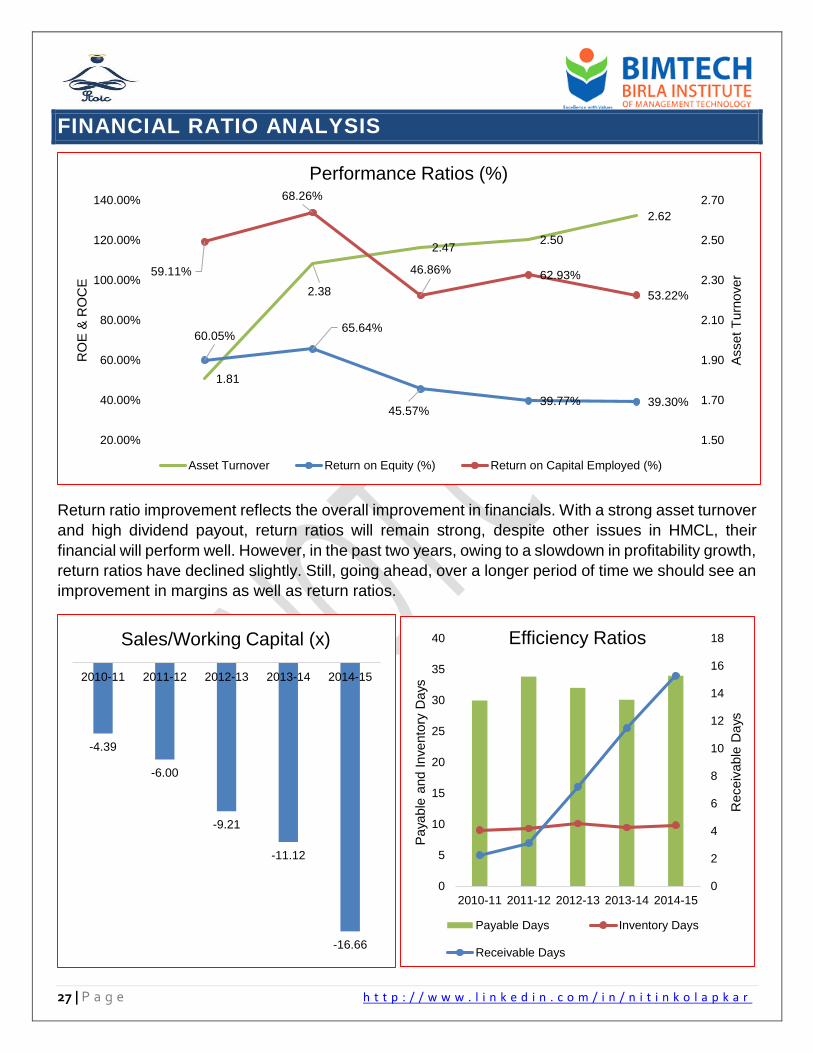

Return ratio improvement reflects the overall improvement in financials. With a strong asset turnover

and high dividend payout, return ratios will remain strong, despite other issues in HMCL, their

financial will perform well. However, in the past two years, owing to a slowdown in profitability growth,

return ratios have declined slightly. Still, going ahead, over a longer period of time we should see an

improvement in margins as well as return ratios.

1.81

2.38

2.472.50

2.62

60.05%65.64%

45.57%39.77% 39.30%

59.11%

68.26%

46.86% 62.93%

53.22%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

140.00%

1.50

1.70

1.90

2.10

2.30

2.50

2.70

RO

E &

RO

CE

Asset

Turn

over

Performance Ratios (%)

Asset Turnover Return on Equity (%) Return on Capital Employed (%)

-4.39

-6.00

-9.21

-11.12

-16.66

2010-11 2011-12 2012-13 2013-14 2014-15

Sales/Working Capital (x)

0

2

4

6

8

10

12

14

16

18

0

5

10

15

20

25

30

35

40

2010-11 2011-12 2012-13 2013-14 2014-15

Receiv

able

Days

Paya

ble

and I

nvento

ry D

ays

Efficiency Ratios

Payable Days Inventory Days

Receivable Days

28 | P a g e h t t p : / / w w w . l i n k e d i n . c o m / i n / n i t i n k o l a p k a r

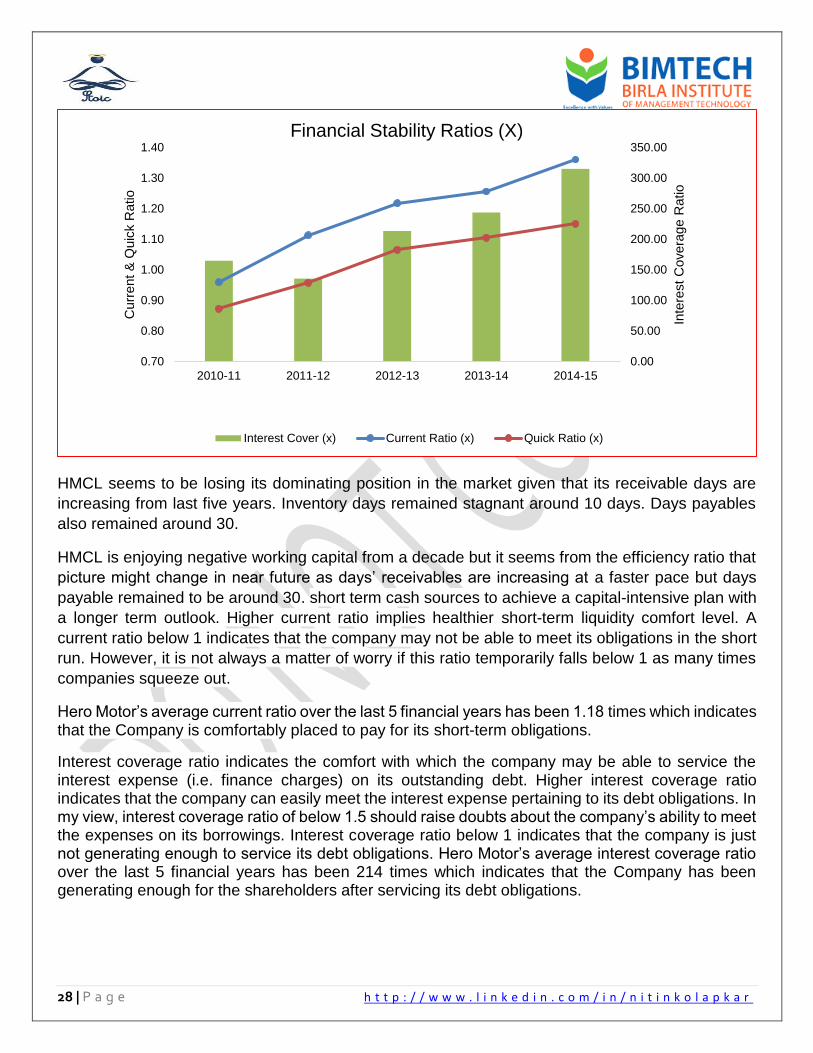

HMCL seems to be losing its dominating position in the market given that its receivable days are

increasing from last five years. Inventory days remained stagnant around 10 days. Days payables

also remained around 30.

HMCL is enjoying negative working capital from a decade but it seems from the efficiency ratio that

picture might change in near future as days’ receivables are increasing at a faster pace but days

payable remained to be around 30. short term cash sources to achieve a capital-intensive plan with

a longer term outlook. Higher current ratio implies healthier short-term liquidity comfort level. A

current ratio below 1 indicates that the company may not be able to meet its obligations in the short

run. However, it is not always a matter of worry if this ratio temporarily falls below 1 as many times

companies squeeze out.

Hero Motor’s average current ratio over the last 5 financial years has been 1.18 times which indicates that the Company is comfortably placed to pay for its short-term obligations.