Embed Size (px)

Citation preview

www.pwc.com/us/

Intel’s EconomicImpacts on the USEconomy, 2008 - 2012

Prepared for Intel Corporation

Intel’s EconomicImpacts on the USEconomy, 2008 - 2012

December 17, 2013

Intel’s Economic Impacts on the US Economy, 2008 – 2012

Contents

Executive Summary 1

I. Introduction 5

II. Industry Classfication 7

III. Intel’s Economic Impact through its Operations, Capital Investments, andDistribution Channels 9

IV. Intel’s Economic Impact by Sector 16

V. Intel’s Products and Services Impacts 18

VI: Case Studies 28

Appendix A: Data Sources and Methodology 58

Appendix B: Intel’s Indirect and Induced Impacts on the US Economy by Sector 61

Appendix C: Literature Review 66

Intel’s Economic Impacts on the US Economy, 2008 – 2012

1

Intel’s Economic Impacts on the US Economy,2008 - 2012

Executive Summary

Intel Corporation and its wholly-owned subsidiaries (“Intel”) design and manufactureadvanced integrated digital technology platforms. A platform consists of amicroprocessor and chipset, and may be enhanced by additional hardware, software,and services. The platforms are used in a wide range of applications, such as PCs,laptops, servers, tablets, smartphones, automobiles, automated factory systems, andmedical devices. Intel also develops and sells software and services primarily focused onsecurity and technology integration.

Intel Corporation engaged PwC to assess its economic impacts on the US economy. Thisreport provides PwC’s economic impact estimates for Intel in terms of employment,labor income, and gross domestic product (or GDP) for 2008 - 2012.1 These impacts arefurther highlighted through a series of case studies on important contributions Intelmakes to the US national and local economies.

Key Findings

Intel, the world’s largest semiconductor manufacturer,2 has a widespread economicimpact throughout all sectors of the US economy through its operations andinvestments. Intel not only provides a large number of jobs to US workers,3 but alsoinvests heavily in the United States: since 2009, the company has announced plans tobuild two new factories in Oregon and Arizona and upgrade its existing manufacturingfacilities in those two states and in New Mexico with next-generation technology. Intelis currently ranked first in R&D among US public companies and it is the fifth largestcapital investor in the United States.4 In addition, Intel’s products and services directlyboost economy-wide productivity.

1 A company’s GDP is also known as its value added, i.e., the additional value created at a particular stageof production. It is equal to the company’s sales less its purchases from other businesses. It can also bemeasured as the sum of employee compensation, proprietors' income, income to capital owners fromproperty, and indirect business taxes (including excise taxes, property taxes, fees, licenses, and sales taxespaid by businesses).2 See IBISWorld Industry Report 33441a, “Semiconductor and Circuit Manufacturing in the US,” August2013, pg. 29.3 According to Intel’s 2012 Annual Report, approximately 51 percent of its 105,000 worldwide employeesare located in the United States, with the majority of the company’s microprocessor manufacturing beingdone at facilities in Arizona, Oregon and New Mexico.4 Scott Thurm, “Behind the Big Profits: A Research Tax Break,” The Wall Street Journal, June 14, 2013;Diana G. Carew and Michael Mandel, “U.S. Investment Heroes of 2013: The Companies Betting onAmerica’s Future,” Progressive Policy Institute, September 2013.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

2

A. Quantitative Analysis

In 2012:

Intel employed 53,200 full- and part-time workers in the United States. Eachjob at Intel is estimated to support more than 13 other jobs elsewhere in the USeconomy.

Intel paid out a total of $9.3 billion in wages and salaries and benefits anddirectly contributed $26.0 billion in GDP in 2012.

Counting economic impacts through operations, investments, and distributionchannels, Intel’s total employment impact on the US economy was 774,600 jobs.

Counting economic impacts through operations, investments, and distributionchannels, Intel’s total impact on labor income (including wages, salaries,benefits, and proprietors’ income) was $52.2 billion.

Counting economic impacts through operations, investments, and distributionchannels, Intel’s total impact on US GDP was $95.8 billion.

Cumulative Economic Impact, 2008-2012:

Intel’s direct employment in the United States increased from 44,800 in 2008to 53,200 in 2012.

Intel paid out a total of $39.4 billion in wages and salaries and benefits (incurrent dollars) over this period and directly contributed a total of $120.7 billion(in current dollars) to GDP.

Intel’s total employment impact on the US economy through operations,investments, and distribution channels rose from 581,600 jobs in 2008 to774,600 jobs in 2012, or an increase of 33 percent.

Intel’s total impact on labor income through operations, investments, anddistribution channels for the period was $214.6 billion (in current dollars).

Intel’s total impact on US GDP through operations, investments, anddistribution channels for the period was $408.5 billion (in current dollars).

Between 2007 and 2011, the most recent 5-year period for which relevant dataare available, Intel’s products and services are estimated to have contributed$54.8 billion in GDP (in current dollars) to the US economy through its impacton total factor productivity and capital deepening.

Intel’s direct, upstream, and downstream impacts on the US economy for the 2008 –2012 period are summarized in Table E-1.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

3

Table E-1.− Intel’s Impacts on the US Economy, 2008 – 2012

Item 2008 2009 2010 2011 2012

Em ploy ment* 581,600 584,500 600,900 7 08,900 7 7 4,600

Direct impact 44,800 44,500 44,100 50,100 53,200

Indirect and induced impacts

Upstream (operations and capital investment) 441,800 444,400 460,100 554,300 606,300

Downstream (distribution channel) 95,000 95,600 96,7 00 104,500 115,100

Labor Incom e ($ m illions)** $37 ,328 $37 ,541 $40,032 $47 ,503 $52,226

Direct impact $6,7 00 $6,854 $7 ,7 43 $8,859 $9,283

Indirect and induced impacts

Upstream (operations and capital investment) $25,090 $25,004 $26,452 $32,328 $35,87 8

Downstream (distribution channel) $5,538 $5,683 $5,837 $6,316 $7 ,065

GDP ($ m illions) $7 4,97 4 $7 3,434 $7 6,196 $88,07 5 $95,802

Direct impact $23,951 $22,801 $22,939 $25,001 $26,044

Indirect and induced impacts

Upstream (operations and capital investment) $41,541 $40,940 $43,293 $52,307 $57 ,7 20

Downstream (distribution channel) $9,483 $9,694 $9,964 $10,7 67 $12,038

Source: Intel data on direct employment and labor income and PwC calculations using the IMPLAN modeling sy stem.

Note: Details may not add to totals due to rounding.

* Direct employment is defined as the num ber of full- and part-tim e jobs. Indirect and induced em ploy m ent includes pay roll em ploy ment and self-employ m ent.

** Direct labor income is defined as wages and salaries and benefits. Indirect and induced labor income includes wages and salaries, benefits, and proprietors' incom e.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

4

B. Qualitative Case Studies

In addition to the significant economic impact generated from Intel’s operations andcapital investments at locations with large Intel manufacturing facilities in Oregon,Arizona and New Mexico, there are other impacts related to job creation and talentgrowth, innovation, industry leadership, supplier benefits and clustering impacts. Toqualitatively assess Intel’s impacts in these areas, PwC and Intel jointly identified threethemes that would be the focus of three field-level case studies of Intel’s operations andinvestments in the United States.5 PwC developed these case studies through interviewsof external stakeholders and industry experts. Quotes from some of these respondentsare included in the highlights below.

1. Research and Development (“R&D”) – In 2012 Intel’s global R&D spendingwas $10.1 billion, with a five-year R&D spend of over $36.5 billion. US-basedR&D spending accounted for the majority of the total global spend in 2012. In a2013 survey conducted by Booz & Co, Intel was the number one R&D spenderamong publicly traded US companies in all sectors. Interview respondents calledIntel’s R&D efforts in the United States “rich with innovation” and “industry-leading,” pointing to years of being on the “leading-edge of development” and“bringing forward technology that matters.”

2. Supply Chain Ecosystem – Intel maintains and interacts with a vast supplychain as both a consumer and a supplier. With $11B in global capitalexpenditures (about 80% in the US) and $53.3 billion in global sales, thecompany operates in the middle of a supply chain that is continuously improvingthe usability and interactivity of technology. Interview respondents describedIntel’s impact on its Oregon supply chain as “the most important economic factorin Oregon” and that Intel “makes a difference and is stable in our economy.”Furthermore, industry veterans viewed Intel as a company that “kept themanufacturing and expertise in this country [US]” and noted that “without Intel,the semiconductor industry would be considerably less US-centric and furtherbehind.”

3. Venture Capital – Since its inception in 1991, Intel Capital has invested morethan $10.8 billion in over 1,276 companies in 54 countries. Intel Capital’sinvestment in the US Technology industry has been evident with $6.7 billion, or62% of its total capital investment going to US-based companies. Furthermore,Intel Capital’s focus on company building has resulted in over 500 acquisitions,mergers, and IPOs. Intel Capital’s contribution to the US economy and businessenvironment goes beyond capital investment. As industry experts and executivesof former portfolio companies stated, Intel Capital is “among the best in knowingthe industry” and their “stamp of approval is hard to match.” Intel Capital’sadvantages are described as “longevity, experience, size, consistency, andfinancial returns were among the best, if not the best of any unit.” Portfolio

5 For the purposes of the Case Studies, Intel refers to Intel Corporation, excluding McAfee and Wind Riversubsidiaries.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

5

companies benefit from investments and interactions that “helped us to span outgeographically and grow the sales team.”

Intel’s Economic Impacts on the US Economy, 2008 – 2012

6

Intel’s Economic Impacts on the US Economy,2008 - 2012

I. Introduction

This report estimates the US economic impact of Intel Corporation and its wholly-owned subsidiaries McAfee, Inc. and Wind River Systems, Inc. (“Intel”) in terms ofemployment, labor income, and gross domestic product (or value added) for 2008 -2012. These impacts are highlighted through a series of case studies on importantcontributions Intel makes to the US national and local economies.

The IMPLAN model, an input-output model based on federal government data, wasused to quantify the economic impact of Intel on the US economy for each year from2008 through 2012.6 As described below, three types of economic impacts attributableto Intel – direct, indirect, and induced – were quantified:

Direct impact measures Intel’s jobs, labor income, and gross domestic product(or GDP).

Indirect impact measures the jobs, labor income, and GDP occurringthroughout Intel’s supply chain, including both its upstream purchases fromsuppliers and the downstream impacts associated with the distribution of Intel’sproducts through its wholesalers, distributors, and retailers.

Induced impact measures the jobs, labor income, and GDP resulting fromhousehold spending of labor and proprietor’s income earned either directly orindirectly from Intel’s spending.

For the indirect and induced impacts, the report considers both operational impacts(due to purchases of intermediate inputs and payments of labor compensation) andcapital investment impacts (due to investment in new structures and equipment).

This report also separately estimates the impact of Intel’s products and services onother sectors of the US economy, such as through productivity enhancement.

It should be noted that this report reflects Intel’s gross contribution to US employment,labor income, and gross domestic product (GDP), and does not account for potentialredeployment of labor and capital in the absence of Intel’s US operations.

The rest of this report is organized as follows. Section II defines the primary industriesin which Intel Corporation and its wholly-owned subsidiaries operate. Section IIIestimates Intel’s upstream (operations and capital investment) and downstream(distribution channel) impacts on the US economy for 2008 through 2012. Section IVestimates Intel’s economic impact by US industrial sector. Section V discusses theeconomic impacts of Intel’s products and services. Section VI presents three casestudies that build upon the quantitative analyses to further highlight Intel’s economic

6 The IMPLAN input-output economic modeling system is developed by the IMPLAN Group LLC. TheIMPLAN model is based on input-output tables that map the flow of value along the supply chain fordifferent industries in the economy.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

7

impacts from a qualitative perspective. A description of the data and methodology usedin this report is in Appendix A. Appendix B provides additional detail on Intel’sindirect and induced impacts on the US economy by sector. Appendix C summarizesthe economic literature on the Information and Communications Technology (ICT)sector’s impact on productivity and economic growth.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

8

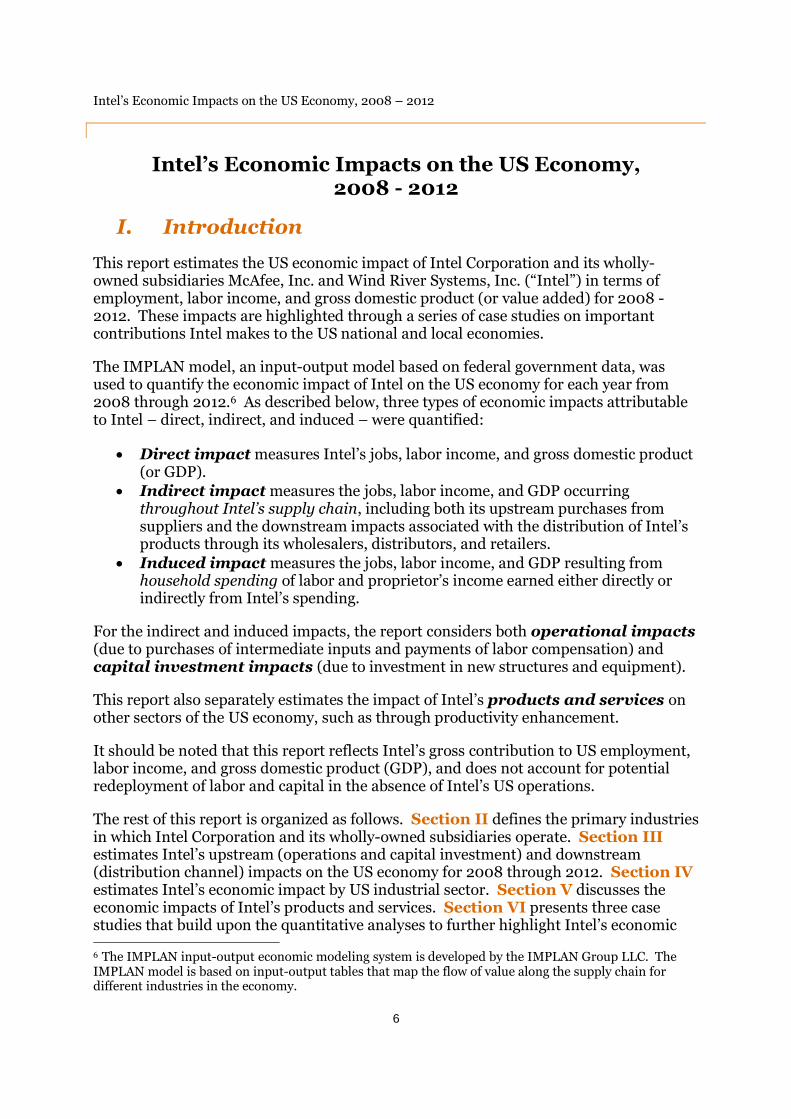

II. Industry Classification

Intel Corporation and its wholly-owned subsidiaries McAfee, Inc. and Wind RiverSystems, Inc. encompass a number of activities that span separate industryclassifications in government economic data. For this report, Intel Corporation’s maineconomic activities are classified under “semiconductor and other electronic componentmanufacturing.” McAfee, Inc.’s and Wind River Systems, Inc.’s activities are classifiedunder “software publishers” and “custom computer programming services,”respectively.

Intel Corporation designs and manufactures advanced integrated digital technologyplatforms. A platform consists of a microprocessor and chipset, and may be enhancedby additional hardware, software, and services. Intel Corporation sells these platformsprimarily to original equipment manufacturers, original design manufacturers, andindustrial and communications equipment manufacturers in the computing andcommunications industries. The platforms are used in a wide range of applications,such as PCs, laptops, servers, tablets, smartphones, automobiles, automated factorysystems, and medical devices.

McAfee, Inc. develops and sells software and services primarily focused on technologysecurity including integration of anti-malware, anti-spyware, and antivirus software forpersonal computers, computer networks and other systems around the world. WindRiver Systems, Inc. develops embedded and mobile software enabling companies todevelop, run, and reliably manage device software.

Intel’s three main business segments fall within the following industrial categories in theNorth American Industry Classification System (“NAICS”) (see Table 1):

1. NAICS 334413. Semiconductor and related device manufacturing.This subsector comprises establishments primarily engaged in manufacturingsemiconductors and related solid state devices. Examples of products made bythese establishments are integrated circuits, memory chips, microprocessors,diodes, transistors, solar cells and other optoelectronic devices.

2. NAICS 51121. Software publishers. This subsector comprisesestablishments primarily engaged in computer software publishing or publishingand reproduction. Establishments in this industry carry out operations necessaryfor producing and distributing computer software, such as designing, providingdocumentation, assisting in installation, and providing support services tosoftware purchasers.

3. NAICS 213112. Custom computer programming services. Thissubsector comprises establishments primarily engaged in writing, modifying,testing, and supporting software to meet the needs of particular customers.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

9

Table 1.− Intel by Business Segment

BusinessSegment

NAICSIMPLAN

SectorDescription

IntelCorporation

334413 243Semiconductor and related devicemanufacturing

McAfee, Inc. 51121 345 Software publishers

Wind RiverSystems, Inc.

541511 371Custom computer programmingservices

Intel’s Economic Impacts on the US Economy, 2008 – 2012

10

III. Intel’s Economic Impact through itsOperations, Capital Investments, and DistributionChannels

This section presents Intel’s economic impact on the US economy through itsoperations, capital investment, and distribution channel. The results reflect the impactof Intel Corporation, and its wholly-owned subsidiaries, McAfee, Inc. and Wind RiverSystems, Inc. The total economic impact includes:

1. Direct impact (the jobs, labor income, and GDP within Intel),2. Indirect impact (the jobs, labor income, and GDP occurring throughout the

upstream and downstream supply chain of Intel), and3. Induced impact (the jobs, labor income, and GDP resulting from household

spending of income earned either directly or indirectly from Intel’s spending).

Upstream impacts arise from Intel’s operations (due to both purchases ofintermediate inputs and payments of labor compensation) and capital investment (dueto its investment in new structures and equipment). Downstream impacts arise fromIntel’s distribution channel and include the operational impacts of Intel’sdistributors. Intel’s distribution channel includes wholesalers, distributers, andretailers. Each business in Intel’s distribution channel provides jobs and labor incomeand generates GDP.

The IMPLAN input-output model was used to estimate Intel’s economic impacts on theUS economy over the 2008-2012 period.7

7 When comparing this report to other input-output analyses, note that not all input-output analysesnecessarily incorporate capital investment and/or distribution channel impacts.

Key Findings:

Intel’s total employment impact on the US economy rose from 581,600 jobs in 2008 to774,600 jobs in 2012, or an increase of 33.2 percent.

In 2012, Intel employed 53,200 full- and part-time workers in the United States. Each job atIntel supported more than 13 other jobs elsewhere in the US economy.

Intel’s total impact on labor income was $52 billion in 2012 and nearly $215 billion over the2008-2012 period.

Intel’s total impact on US GDP was $96 billion in 2012 and more than $408 billion over the2008-2012 period.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

11

Employment

Intel employed 53,200 US workers in 2012. In addition, Intel indirectly supported721,400 other full-time and part-time jobs in the US economy: 496,300 from Intel’soperations; 110,000 from Intel’s capital investment; and 115,000 from its distributionchannel. Combining the direct, indirect and induced impacts, Intel’s total employmentimpact on the US economy is estimated to be 774,600 full-time and part-time jobs in2012, roughly ½ of 1 percent of total US employment.

Intel’s total employment impact on the US economy rose from 581,600 jobs in 2008 to774,600 jobs in 2012 (see Table 2). The largest component of Intel’s total employmentimpact is attributable to its operational supply chain.

Table 2.− Intel’s Impact on US Employment, 2008-2012 [Direct impact and indirect/induced impacts due to operations, capital investment, and distribution]

Source: Intel data on direct employment and PwC calculations using the IMPLAN modeling system.

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

2008 2009 2010 2011 2012

Direct Operational Capital Investment Distribution Channel

Intel’s Economic Impacts on the US Economy, 2008 – 2012

12

Labor Income

According to Intel, it paid $9.3 billion in wages, salaries and fringe benefits to its USemployees in 2012. Including the jobs indirectly supported by Intel through itsoperational spending, capital investment, and distribution channel, the associated totalimpact on US labor income (including wages and salaries and benefits as well asproprietors’ income) is estimated to be $52.2 billion in 2012.

Intel’s total impact on US labor income grew each year from $37.3 billion in 2008 to$52.2 billion in 2012 (see Table 3).

Table 3.− Intel’s Impact on US Labor Income, 2008 – 2012(In billions of dollars)

[Direct impact and indirect/induced impacts due to operations, capital investment, and distribution]

Source: Intel data on direct labor income and PwC calculations using the IMPLAN modeling system.

$0

$10

$20

$30

$40

$50

$60

2008 2009 2010 2011 2012

Direct Operational Capital Investment Distribution Channel

Intel’s Economic Impacts on the US Economy, 2008 – 2012

13

GDP

PwC estimates that Intel’s operations directly generated $26.0 billion of GDP to the USeconomy in 2012. Intel’s operations indirectly generated an additional $48.4 billion tothe US economy in 2012, while its capital investment and distribution channel impactadded another $9.8 billion and $12.0 billion of GDP, respectively. Combining theoperational, capital investment, and distribution channel impacts, Intel’s total GDPimpact on the US economy was $95.8 billion, accounting for 6/10 of 1 percent of USGDP in 2012.

Intel’s GDP contribution to the US economy grew from $75.0 billion in 2008 to $95.8billion in 2012 despite a slight reduction in 2009 to $73.4 billion during a period of USeconomic contraction (see Table 4).

Table 4.− Intel’s US GDP Impact, 2008 – 2012 (In billions of dollars)

[Direct impact and indirect/induced impacts due to operations, capital investment, and distribution]

Source: PwC calculations using the IMPLAN modeling system.

$0

$20

$40

$60

$80

$100

$120

2008 2009 2010 2011 2012

Direct Operational Capital Investment Distribution Channel

Intel’s Economic Impacts on the US Economy, 2008 – 2012

14

Case Study: Intel’s Fabrication Site in Hillsboro,Oregon

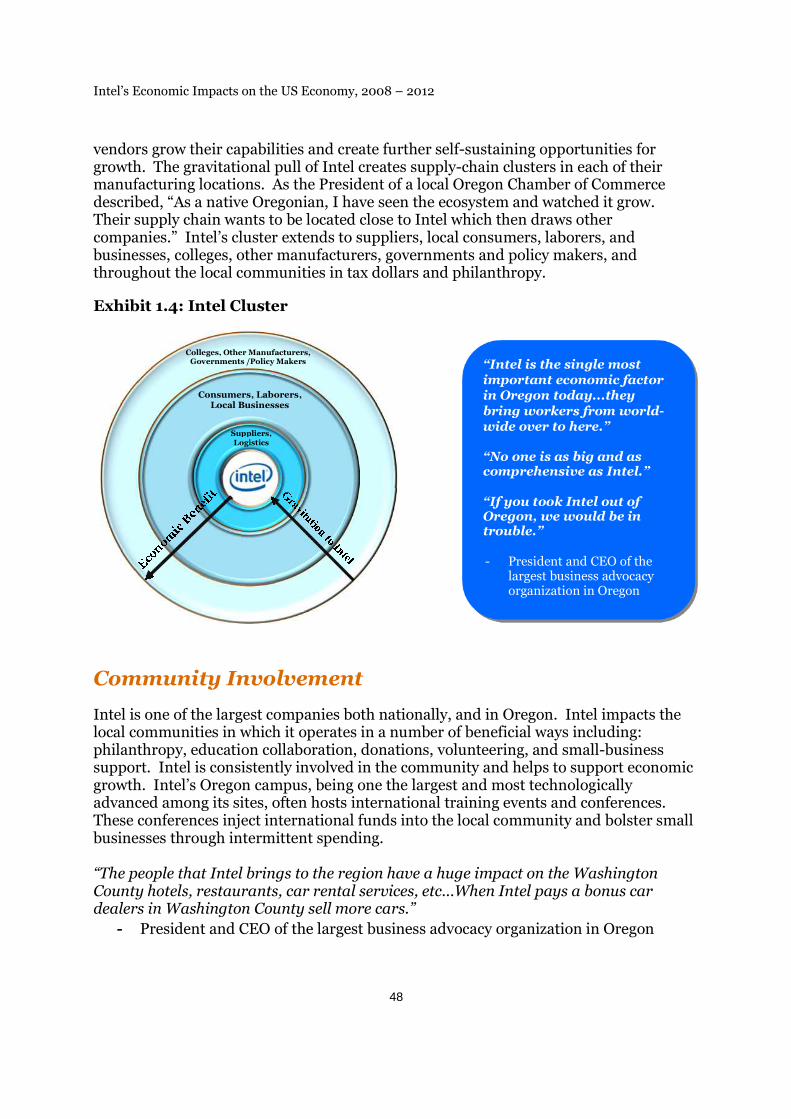

Intel provides the Oregon region with approximately 16,400 direct jobs, making it the state’s largest private employer.For perspective, Intel represents approximately 20% of tech employment in Oregon which has more than 5,300 techcompanies employing a total of 81,632 tech industry professionals.

Intel also compares favorably with respect to employee salaries and Oregon’s standard of living. The average annualsalary of tech sector employees in Oregon was $94,200 in 2012, or 123 percent higher than other private sectoremployment within Oregon.

“Intel’s average wage is approximately $125,000 here in the Portland metro area, while average per capita income is$41,000.”

- President and CEO of the largest business advocacy organization in Oregon

Intel is the largest taxpayer in Washington County, contributing $20.8 million in taxes to the County in 2012. Oregondoes not have a sales tax; therefore, its excise tax (i.e., the tax for the privilege of doing business in the state) is theprimary revenue source for the state along with property and employment taxes. Tax revenues serve to fund, for example,public safety employees, public school employees, government officials and staff, and state economic developmentinitiatives. As a result, tax contributions provide an employment impact beyond Intel’s direct workers.

“[As] the largest [employer] in the state...Intel has a huge impact from a state-wide perspective.”

- President of a local Oregon Chamber of Commerce

Intel’s total capital investment in the state has exceeded $25 billion since the company acquired its first piece of propertyin Oregon in 1974. A senior member of the Oregon Building Trades and Portland Development Commission recentlyremarked that the construction jobs that Intel provides have a ripple effect on the economy in numerous areas including,for example, construction workers paying mortgages, going out to dinner, and making other purchases.

“All of the construction jobs related to Intel’s new fabrication sites put the construction industry back to work in thestate [Oregon].”

- President and CEO of the largest business advocacy organization in Oregon

“Through some of our darkest times during the technology bust in 1999-2000, Intel had cranes in the air doingconstruction. Intel makes a difference and is stable in our economy.”

- President of a local Oregon Chamber of Commerce

“Intel is the single mostimportant economic factor inOregon today...they bringworkers from world-wideover to here.”

“No one is as big and ascomprehensive as Intel.”

“If you took Intel out ofOregon, we would be introuble.”

- President and CEO of thelargest business advocacyorganization in Oregon

Intel’s Economic Impacts on the US Economy, 2008 – 2012

15

The results for each year are summarized in Table 5. The total economic impact ofIntel in terms of jobs and labor income (including wages and salaries and benefits aswell as proprietors’ income) grew steadily throughout the period. The total economicimpact in terms of GDP in nominal terms grew at an average rate of 6 percent per yearfrom 2008 through 2012 despite a contraction in 2009.

Table 5.− Intel’s Direct, Operational, Capital Investment, and DistributionChannel Impacts on the US Economy, 2008-2012

(Dollar amounts in millions of current dollars)

ItemDirect

Impacts

Indirect and Induced Impacts

TotalImpacts

Upstream ImpactsDownstream

ImpactOperational

ImpactsCapital

InvestmentImpacts

DistributionChannelImpacts

2008Employment1 44,800 408,900 32,900 95,000 581,600Labor Income2 $6,700 $23,142 $1,948 $5,538 $37,328GDP $23,951 $38,660 $2,881 $9,483 $74,974

2009Employment 44,500 405,900 38,500 95,600 585,500Labor Income $6,854 $22,727 $2,277 $5,683 $37,541GDP $22,801 $37,592 $3,347 $9,694 $73,434

2010Employment 44,100 415,500 44,600 96,700 600,900Labor Income $7,743 $23,762 $2,690 $5,837 $40,032GDP $22,939 $39,333 $3,960 $9,964 $76,196

2011Employment 50,100 463,600 90,700 104,500 708,900Labor Income $8,859 $26,925 $5,403 $6,316 $47,503GDP $25,001 $44,462 $7,846 $10,767 $88,075

2012Employment 53,200 496,300 110,000 115,100 774,600Labor Income $9,283 $29,399 $6,478 $7,065 $52,226GDP $26,044 $48,442 $9,278 $12,038 $95,802

Source: Intel data on direct labor income and PwC calculations using the IMPLAN modeling system.Note: Details may not add to totals due to rounding.1 Direct employment is defined as the number of full- and part-time jobs. Indirect and induced employment includespayroll employment and self-employment.2 Direct labor income is defined as wages and salaries and benefits. Indirect and induced labor income includes wagesand salaries, benefits, and proprietors’ income.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

16

IV. Intel’s Economic Impact by Sector

Intel purchases intermediate inputs from a variety of other US industries, supportingjobs in these industries and spurring additional rounds of input purchases by theseindustries. Other economic impacts are generated by the personal spending of Intelemployees and out of the additional income earned by employees in the supply chain toIntel. The jobs, labor income (including wages and salaries and benefits as well asproprietors’ income), and GDP supported by this cycle of spending, or multiplierprocess, are referred to as the indirect and induced economic impacts.

Intel also purchases capital goods from a variety of US suppliers, which has a similarmultiplier effect on the rest of the US economy.

Table 6 shows Intel’s indirect and induced economic impacts by receiving sectors. PwCestimates that at the national level, each direct job at Intel supported more than 13 jobselsewhere in the US economy in 2012. That is, in addition to the 53,200 jobs directlyprovided by Intel, 721,400 additional jobs were supported in the US economy throughthe indirect and induced impacts of Intel. Intel’s purchase of intermediate inputs fromother US suppliers supported 496,300 indirect and induced jobs in other industriesacross the country in 2012. Intel’s capital investment supported 110,000 additionalindirect and induced jobs across the US economy and Intel’s distribution channelsupported another 115,100 jobs. Combined, Intel directly or indirectly supported774,600 jobs in the US economy in 2012. The service sector, being the largest sector inthe US economy, accounted for the largest number of indirect and induced jobsattributable to Intel’s spending (324,400) in 2012, followed by Wholesale and RetailTrade (135,700), Finance, Insurance, Real Estate, Rental and Leasing (65,000),Manufacturing (61,000), and Construction (45,300).

PwC estimates that in 2012 the $9.3 billion in employee compensation directly paid outby Intel led to an additional $42.9 billion in labor income in the US economy – amultiplier effect of 4.6. In addition, Intel’s direct GDP contribution of $26.0 billion in2012 resulted in an additional $69.8 billion of GDP to the US economy – a multipliereffect of 2.7. Detailed impact results by sector for the 2008-2012 period are presentedin Appendix B.

Key Findings:

Intel Corporation and its wholly-owned subsidiaries have a widespread economic impactthroughout all sectors of the economy.

In 2012, the service sector accounted for the largest number of indirect and induced jobsattributable to Intel’s spending, followed by wholesale and retail trade, and finance,insurance, real estate, rental and leasing.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

17

Table 6.− Intel’s Indirect and Induced Impacts on the US Economy, by Receiving Industry, 2012

Source: PwC calculations using the IMPLAN modeling system.

* Employment is defined as the number of full- and part-time jobs, including self-employment.

** Labor income is defined as wages and salaries and benefits and proprietors' income.

Indirect Induced Indirect Induced Indirect Induced

Agriculture 1 ,200 6,900 $37 $214 $55 $327

Mining 3,100 1,7 00 $232 $130 $682 $386

Utilities 1 ,900 1,300 $248 $169 $899 $613

Construction 41 ,500 3,800 $2,319 $216 $2,480 $248

Manufacturing 45,600 15,400 $3,820 $1,065 $7 ,454 $2,17 1

Wholesale and retail trade 7 1 ,300 64,400 $5,327 $2,544 $9,212 $4,158

Transportation and warehousing 20,600 9,600 $1,109 $531 $1,494 $7 22

Information 8,900 6,000 $999 $557 $1,668 $1,161

Finance, insurance, real estate, rental and leasing 19,200 45,800 $1,151 $2,187 $3,325 $8,27 0

Services 160,300 164,100 $10,258 $7 ,543 $12,661 $9,17 6

Other 17 ,7 00 11,100 $1,408 $880 $1,600 $995

Total Indirect and Induced Im pacts 391,300 330,100 $26,906 $16,037 $41,531 $28,227

Sector DescriptionEm ploym ent* Labor Incom e ($ m illion)** GDP ($ m illion)

Intel’s Economic Impacts on the US Economy, 2008 – 2012

18

V. Intel’s Products and Services Impacts

This section first reviews the economic literature on the impact of the Information andCommunications Technology (“ICT”) sector on US economic growth and then estimatesIntel’s share of the overall contribution of the ICT sector.

Contribution of the ICT Sector to US Economic Growth – Literature Review

The ICT sector’s economic impacts include improved labor productivity, lower prices,and faster economic growth. Moore’s Law, named after Intel co-founder Gordon Moore,states that the number of transistors on integrated circuits doubles approximately everytwo years. The capabilities of computers and other semiconductor-dependent devicesare strongly linked to Moore’s Law. Computing power, processing speeds, and memorycapacity have all increased exponentially. From the early 1970s to 2000, the power ofmicroprocessors increased by a factor of 7,000 while the cost of storing one megabit ofdata fell from more than $5,000 to just 17 cents.8 A large body of economics researchfinds that the ICT sector has fueled technological change and productivity growth acrossall sectors of the economy.

In general, companies increase productivity through three channels:

1. Capital deepening: Increased investment in capital equipment (includingcomputers and other information technology) allows workers to be more efficientand more productive.

2. Improved labor quality: Investments in “human capital” through trainingand investments in education increase worker productivity.

3. Total factor productivity: Increases in productivity achieved throughtechnological progress and innovations in business systems or organizationalstructure.

8 Rauch, Jonathan, “The New Old Economy: Oil, Computers, and the Reinvention of the Earth,” TheAtlantic Monthly, January 2001.

Key Findings:

Users of Intel's products and services benefit from productivity enhancements and costreductions.

Intel’s products and services contribute to the growth of productivity and GDP throughtwo channels: total factor productivity and capital deepening.

Through these two channels, Intel’s products and services contributed $54.8 billion inGDP to the US economy over the 2007-2011 period.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

19

Case Study: Selected Intel R&D Facilities

Intel’s Arizona operations are spread across two large sites in the City of Chandler. Roughly half of Intel’s 11,000 employee basein the state works at the 700-acre Ocotillo campus which is dedicated to manufacturing the company’s latest silicon technology.The remaining employees are located at Intel’s 150-acre Chandler campus where a substantial portion of employees are dedicatedto research and development. In fact, Intel has invested more than $300 million to build a new research and development facilityat this site. The facility, which is nearing completion, will be used to expand Intel’s packaging operations. The innovation thatwill occur in this facility is aimed at influencing technology trends for years to come. This investment is creating several hundredIntel R&D-related jobs and nearly a thousand construction jobs. Intel’s Arizona employees, on average, earn over $130,000 peryear (including total compensation, benefits and bonuses).

Intel’s Massachusetts Design Center in Hudson, Massachusetts is home to more than 825 engineers engaged inmicroprocessor design, testing and validation for the development of next generation multi-core Itanium® and Xeon®microprocessors for high-end servers. Lab facilities, technical staff, and engineers work directly with product design teams onfirst silicon readiness to support the introduction of new high performance products before they are released for high volumemanufacturing. Labs are staffed by a cross-functional team of content developers, debug engineers, software engineers,technicians and inventory control specialists, working closely with design and validation engineering working on first silicon tovolume validation to deliver production ready quality products.

In Intel’s New Hampshire R&D and production facility, a group of 60 Intel research and development employees researchesmethods to make it easier to perform parallel programming on Intel processing cores while maximizing application performance.Parallel programming by definition is aimed at compartmentalizing complex problems into smaller, more manageable problemsand computing solutions simultaneously. The site manager of the New Hampshire Intel facility described the importance of thework being performed as, “enabling the technology created by Intel, meaning, without them, the development community wouldnot be able to “unlock” the potential and performance of the newer multi-core processors developed at Intel.” The programminglanguage, prototypes and tools developed here allow end-users of Intel’s silicon to better understand and utilize the capabilities ofthe products. Intel’s R&D at this facility is aimed at faster computing, higher efficiency, and ease of technology use for moreapplications.

In the Columbia, South Carolina facility, approximately 310 Intel engineers test Intel’s products to verify the already-designed product’s features work as advertised and meet stated specifications. It is considered the “last step” before thecompleted piece of research and development becomes commercialized. The site manager of the South Carolina design centerstated, “All of our validation activities have successfully yielded commercialized products in the XeonTM and CoreTM product lines;for example, XeonTM E5 is a recent product predominantly supporting Cloud and Data Center programs validated at the SouthCarolina facility and the highly successful 4th Generation CoreTM graphics system was also validated here.” When asked about theeffects of the research and development site on the local economy, the site manager responded, “Salaries for this site are notablyhigher than the comparative geography and our employees enjoy a generally higher standard of living…The South CarolinaCommerce Secretary’s office tells us our gross salary of $26 million has a compounded effect of nearly three times [$76 million]on the local economy.”

In Intel’s Eau Claire, Wisconsin lab, a group of 60 Intel employees are defining, designing, validating, and testing componentsinto which fabric connects. Fabric is high-speed interface that connects elements of a computing system and a key technology forsupercomputing. Fiber cables act like the network connection on a computer, allowing the user to send and receive data. Datatransfers through fiber 25 billion times per second, allowing for faster sending and receiving of information than ever before.Fiber cables play a key role in high performance computing, which improves our economy, safety, and fundamental knowledge.This technology helps oil companies reduce wasted effort by accurately identifying and locating oil reserves, improves theaccuracy of weather predictions allowing for accelerated warning systems, and allows for intricate simulations of real-worldcatastrophes to predict impact and provide planning tools for disaster relief efforts. The Wisconsin team has grown by 20 percentin the past year and is expected to continue to grow.

In Fort Collins, Colorado, approximately 425 Intel employees design data center applications and solutions including theXeonTM and ItaniumTM architectures. The Fort Collins R&D center is responsible for the architecture, design, and development ofhigh-performance server microprocessors for server and workstation applications. The site collaborates with universities byparticipating in programs to grow awareness of and support professorships in Science, Technology, Engineering andMathematics (“STEM”) careers. In addition, the site participates on external boards and conference committees to supportwomen and minorities in STEM. The design center also impacts its community through environmental initiatives such asrecycling (68,000 lbs in 2011), reducing onsite energy and gas consumption (by an amount that is equivalent to the annual energyand gas onsumption by 250 average American households), and improving eco-friendly options for worker transportation byimplementing and incentivizing a “bike to work” program. This group also is noteworthy because it is the largest per employeedonor to the United Way in the country with an average gift size per donor at $3,500.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

20

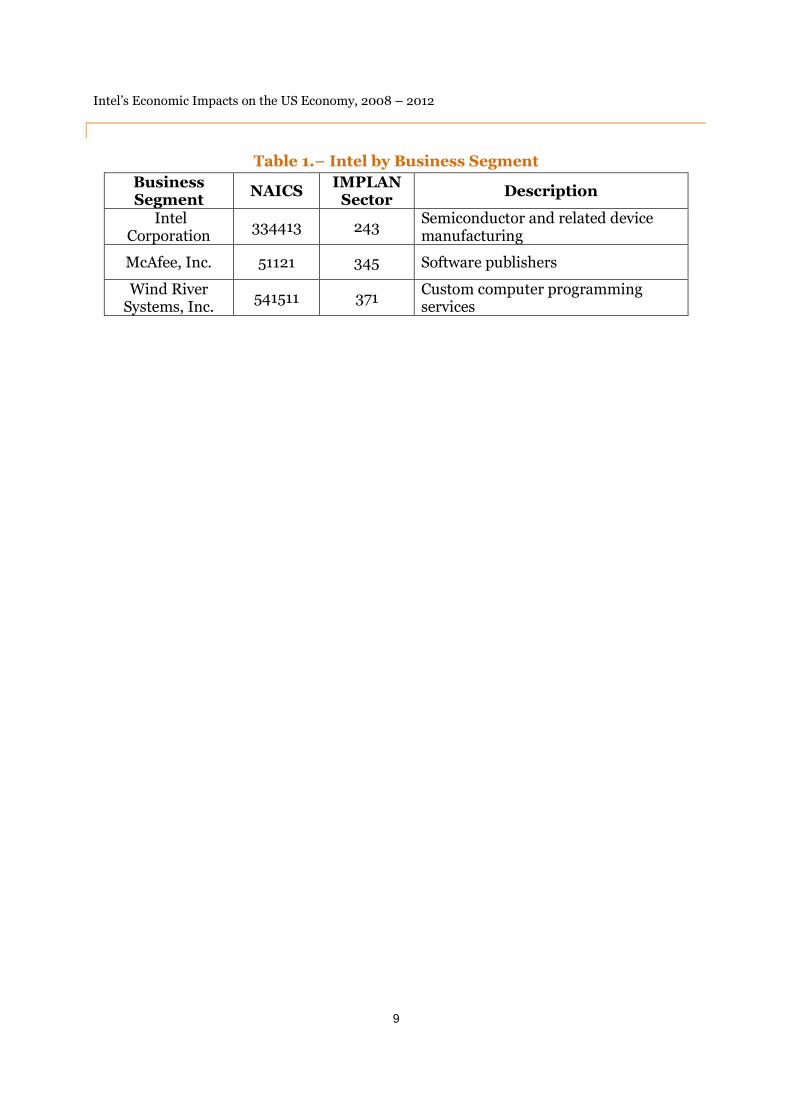

Capital deepening. According to the US Bureau of Economic Analysis, nominalbusiness investment in information processing equipment and software grew at anaverage annual rate of 8.8 percent between 1970 and 2012, 1.7 percentage points fasterthan the overall rate of growth of investment in all nonresidential capital equipment andsoftware. Due to technological advancements and declining real costs of informationprocessing equipment and software relative to other types of equipment, realinvestment in information processing equipment and software grew more than twice asfast as investment in other nonresidential capital equipment. By 2012, informationprocessing equipment and software accounted for 55.4 percent of investment innonresidential equipment and software and 31.0 percent of the total net stock ofnonresidential equipment and software in the United States (Table 7).

Note: Annual investment measured in nominal dollars.Source: US Bureau of Economic Analysis, Fixed Asset Accounts, Table 2.7.

Total factor productivity (“TFP”). TFP (also known as multifactor productivity)accounts for changes in productivity not directly attributable to capital or labor. TFPgenerally results from technological improvements as well as changes in businessorganizational structures or processes that allow companies to better utilize new orexisting technologies. Intel and the larger ICT industry have been a significant source ofTFP in the United States. The contribution of computers and electronics manufacturingto overall US total factor productivity increased significantly in the 1990s before levelingoff in recent years (see Table 8). According to data from the US Bureau of Labor

25.3%

38.8%

45.4%

50.4% 50.3%

0%

10%

20%

30%

40%

50%

60%

1970-79 1980-89 1990-99 2000-09 2010-12

Table 7. -- Average Share of Information ProcessingEquipment and Software in Total Nonresidential

Investment in Equipment and Software

Intel’s Economic Impacts on the US Economy, 2008 – 2012

21

Statistics, computers and electronics manufacturing accounted for 0.46 percentagepoints of the 0.92 percentage point increase in annual private nonfarm business TFPover the 1987 to 2011 period. In other words, computers and electronics manufacturingaccounted for approximately half of the TFP growth in the private nonfarm businesssector over this 25-year period.

Source: US Bureau of Labor Statistics, Contributions of Manufacturing Industries to PrivateNonfarm Business Multifactor Productivity, June 19, 2013.

The benefits of productivity growth take many forms. The most immediate benefit isthat labor can produce more output for a given hour of work. Firms that utilize newforms of technology are able to produce the same number of goods or services ofequivalent quality at lower costs given the same number of inputs. Productivity gainsare shared by consumers, workers, and shareholders in the form of lower prices, higherwages, and higher returns on investment. Longer-term effects include higher levels ofICT investment and the development of a labor force with the skills required to utilizeICT in the workplace.

Although the impact of technological progress on productivity gains is difficult to assess,the general consensus among economists has centered around the followingobservations and trends (see Appendix C):

0.30

0.51

0.85

0.36

0.22

0.460.48 0.48

1.341.40

0.44

0.92

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1987-90 1990-95 1995-00 2000-07 2007-11 1987-11

Table 8. -- Contribution of Computers and ElectronicsManufacturing to Private Nonfarm Business Total

Factor Productivity Growth, 1987-2011[Percentage points]

Computers and Electronics

Private Nonfarm Business TFP

Intel’s Economic Impacts on the US Economy, 2008 – 2012

22

1. The decline in prices of ICT hardware,2. Growth of employment in ICT-intensive businesses compared to growth in

employment in non-ICT intensity businesses,3. The ICT industry’s positive contribution to economic growth since the early

1990s, and4. Positive "spillover" effects in relation to firms' proximity and access to ICT

investment.

Prices

Data provided by the Bureau of Labor Statistics indicates that prices for informationtechnology hardware and software fell by more than 67 percent during the 1990s.9

Between 1994 and 2001, the price of semiconductors dropped by 47.1 percent comparedto a decline of 18.6 percent between 1988 and 1994 (Aizcorbe, Oliner and Sichel,2006).10 In 1998 alone, the end-use price for computers fell by 40.3 percent with thedecline in semiconductors prices accounting for 40 to 60 percent of the decline(Aizcorbe, Flamm and Khurshid, 2001).11

Technological change in the semiconductor manufacturing industry was the main driverof the observed decline in ICT prices (Mann, 2003). The manufacture of dynamicrandom access memory (DRAMs) and personal computers (PC) both experiencedsignificant price declines during the 1990s. Cheaper semiconductors explained abouthalf of the decline in PC prices (Mann, 2003). Microprocessor unit (MPU) chips alsofollowed an overall trend in price decline, accelerating in the mid-90s and slowing after2001. During this period Intel was the dominant producer of MPU chips (Aizcorbe,Oliner and Sichel, 2006).

While technological progress in the ICT-producing industry was the main driver of thedecline in ICT prices during the 1990s, globalized production contributed to additionprice declines, which allowed for the diffusion of ICT hardware throughout theeconomy. Globalized production and international trade accounted for 10 to 30 percenttradeoff of the decline in ICT hardware prices over this period (Mann, 2003). Forexample, regression analysis has found that an increase in net imports of PCs isassociated with a reduction in PC prices. As the global capacity to produce dynamicrandom access memory (DRAMs) hardware increased relative to actual production, thedecline in prices accelerated (Mann, 2003). As a result of the lower prices, ICThardware was more easily diffused throughout the economy. This diffusion was theresult of two related effects. First, technological advances in semiconductors resulted incontinuing price declines for a given level of performance. These price reductionsincreased demand for intermediate inputs in industries that use semiconductors, suchas computer and communications equipment manufacturing. Second, the price ofoutput in semiconductor-using industries was lower, increasing the quantity demanded

9 PwC calculation using the consumer price index for all urban consumers for information technologyhardware and services.10 The decline in semiconductor prices slowed between 2001 and 2004, declining by 28.2 percent.11 The largest end users of semiconductor chips in 1999 were computer manufacturers, making up half ofthe value of worldwide shipments; the next largest end users were communications equipment (21percent) and consumer electronics (14 percent) manufacturers (Aizcorbe, Flamm and Khurshid, 2001).

Intel’s Economic Impacts on the US Economy, 2008 – 2012

23

by other industries for products like computers and telecommunications equipment(Jorgenson, Ho and Stiroh, 2002).

Firms that purchased and incorporated ICT inputs into their production processesprovided indirect contributions to economic growth. Declines in the price of ICT inputshelped slow price inflation across the economy and allowed policymakers to maintainlower interest rates over a longer timeframe (Mann 2003). From the standpoint of thefinal consumer, technological improvements that reduced the cost of microprocessorsand PCs result in direct gains in the form of increased consumer surplus. For otherbusinesses, these technological improvements mean cheaper inputs and changes inproduction processes that provide further indirect benefits to the economy in the formof lower output prices form non-ICT products to the final consumer. This indirectcontribution is known as “social surplus.” From 2000 to 2007, the social surplusassociated with the declining prices of ICT hardware and software was about 4 percentof real GDP or about $500 billion. This increase in GDP was the result of decliningprices of ICT, which resulted in new business startups and the diffusion of new businessprocesses and practices (Mann 2012).12

Employment

During the 1990s, wholesale trade, securities and commodity brokers, depositoryinstitutions, and telecommunications all had relatively higher levels of informationtechnology. These sectors also experienced higher contributions to GDP growth relativeto other sectors in the economy (Mann, 2003). While the intensity of ICT technologyincreased by an average of 150 percent during the 2000s, the diffusion of ICTtechnology was not equally distributed across all industries. In fact, there was awidening dispersion in ICT-intensity among sectors within the US economy (Mann,2012).

The difference in relative ICT-intensity among industries had varying impacts onemployment. ICT producers, which made up about 3 percent of total employment,continued to add jobs over the 2001-2009 period. Employment in ICT-intensive serviceestablishments grew by 5 percent during this period, adding about 1 million jobs to theUS economy. In contrast, non-ICT intensive services, which accounted for about twothirds of total employment, only grew by 1.5 percent over the same period (Mann, 2012).ICT-intensive manufacturing establishments expanded and contracted with the businesscycle relatively more closely than non-ICT intensive manufacturing. Over the 2001-2009 period, employment in ICT-intensive manufacturing establishments declined by34 percent compared to a decline of 17 percent in non-ICT intensive manufacturingestablishments (Mann, 2012). Although small ICT-intensive services made up just 5 to6 percent of overall employment in the United States, these establishments accountedfor a much higher share of overall net job creation, ranging from 13 percent in 2003 to68 percent in 2008 (Mann, 2012).

12 ICT hardware price declines contributed the most to social surplus. Although software prices did notdecline as quickly, their rate-of-return was greater than hardware. Expenditures on software and ICTservices are also much greater than expenditures on hardware (Mann, 2012).

Intel’s Economic Impacts on the US Economy, 2008 – 2012

24

Case Study: Intel’s Education Collaboration

Intel supports technology education of Texas students in a number of ways so that they can be better prepared for the ICTworkforce of tomorrow. Since 2000, 28,500 Texas teachers have completed the Intel Teach Program, which is designed as aworldwide professional development program, aimed at giving teachers the tools to integrate technology into their teachingcurriculum. In addition, Intel has sponsored 100 paid interns from the University of Texas. These interns are integrated intothe Texas research and development site and can further study and generate interest in research and development in thecommunity and at universities.

Intel interacts with the education community through various outreach programs, direct donations, and volunteer hours. ADirector from the University of Texas explained, “…the tech sector is a busy place right now with a lot going on. From astudent perspective it helps to attract interest.” Intel has invested in a variety of University programs to foster the kind ofexperience they can leverage to continue with their education and in employment with sophisticated technology firms such asIntel. The company has also been a long-time funder of diversity programs and has “changed the conversation at a local andnational level.”

“Intel’s commitment has made it possible to grow programs and grow staff. We have gone from 4 to 42 programs, 60 to1000 girls, and our 8-week program has expanded from 250 girls to more than 500 girls.”

- Executive Director of an Austin non-profit organization

Intel provides direct capital dollars, access to resources, and numerous volunteers. The Executive Director of a local non-profitsaid, “Intel shows up when they say they will show up. It’s not just lip service.” Intel received high marks from a SeniorDirector at a local education organization, “I would give Intel high marks in volunteering…they are doing a good job recentlyon community involvement…and they are very consistent, not doing things as one-offs, but having conversations about thewhole year and looking for opportunities to invest and grow.”

“I can easily say that Intel has had the most strategic view and execution of their core university partnerships of anycompany with which I’ve worked.”

- Senior Director of Research Relations at a large university in Texas

Structure of Labor Force

ICT-intensive firms require a workforce adept at implementing and operating newtechnologies. Growth in ICT investment at the end of the 20th century was coupled witha more educated workforce. The structure of the US labor force has increasingly seen ashift toward college-educated workers, who are often identified as “knowledge workers”that “make use of information technology equipment and software.” Between 1977 and2007, the college-educated labor force grew at an average annual rate of 3.8 percentcompared to 1.3 percent for the non-college educated labor input (Jorgenson, Ho andStiroh, 2002). The college-educated workforce had a higher contribution to the GDPgrowth than non-college educated labor. Overall, labor inputs accounted for 1.19percentage points of the 3.08 percent average annual GDP growth between 1977 and2000. The contribution of college-educated workers during the same period was 0.72percentage points compared to 0.48 percentage points for non-college educated workers(Jorgenson, Ho and Stiroh, 2002).

Economic Growth

The ICT sector's most significant economic impact is a result of the rapid expansion inthe production of microprocessors, computers, and other electronic devices that beganin the 1990s. The contribution of ICT production to output almost doubled during theearly 1990s and accounted for 28.9 percent of growth in output between 1990 and 1995.By the latter half of the decade, ICT capital services made up half of the capital input

Intel’s Economic Impacts on the US Economy, 2008 – 2012

25

contribution (Jorgenson, 2001). ICT equipment and software played an important rolein the acceleration of productivity growth over the 1995 to 2003 period (Corrado,Hulton, and Sichel, 2009). Output per hour in the private nonfarm business sector grewat an average annual rate of 2.95 percent between 1995 and 2003 compared to 1.47percent between 1973 and 1995, an increase of 1.48 percentage points. Corrado, Hultonand Sichel found that 0.53 percentage points (or 36 percent) of this increase was due tocapital deepening in the form of ICT equipment and software. Another 0.85 percentagepoints was accounted for by growth in total factor productivity, with the remainderaccounted for by changes in the composition of labor.13 As discussed below, thecomputer and electronics manufacturing sector plays an important role in the TFPgrowth. In fact, between 1995 and 2000, this industry accounted for more than 60% ofthe TFP growth in the private nonfarm business sector.14

Beginning in the 1990s, ICT hardware laid the groundwork for increased economicproductivity and economic growth. According to the Bureau of Labor Statistics,between 1987 and 2011 the computer and electronics manufacturing industrycontributed 50 percent of private nonfarm business TFP growth (0.46 percentage pointsout of the 0.92 percentage point average annual TFP growth). Over the same period,output per hour for all private non-farm businesses grew at an average annual rate of2.2 percent. In other words, computer and electronics manufacturing accounted forapproximately 21 percent of the increase in output per worker over this period.15

Productivity gains related to a rapid price decline of ICT hardware resulted inapproximately $230 billion of additional GDP growth between 1995 and 2002 (Mann,2003). The direct and indirect gains in economic growth related to lower ICT prices andincreased ICT-intensity amounted to an economic gain between $810 billion and $935billion from the 2002-2007 period. After including ICT-services (such as computerdesign), the overall gain is closer to $1 trillion given the broad use of ICT hardware,software, and services across all industries in the US economy (Mann, 2012). Lower ICTprices supported additional investment in ICT capital which translated into productivitygrowth and higher growth in GDP (Mann, 2003).

Spillover Effects

Geographical proximity to pools of ICT investment results in positive "spillover" effects.Recent research looked at 4-digit SIC level industries within the Northern Californiaregion (a highly ICT-intensive region) compared to other regions. Firms with easyaccess to ICT capital had more flexibility in production. The increased specialization oftechnology firms within close proximity of each other allows non-ICT establishments totake advantage of their resources to ramp up or slow down production with more ease.For example, the output elasticity of ICT investment (i.e., the change in production withrespect to a change in ICT investment) for non-durable goods manufactured in

13 See Table 6 in Corrado, Hulton and Sichel, 2009.14 US Bureau of Labor Statistics, “Contributions of Manufacturing Industries to Private Nonfarm BusinessMultifactor Productivity,” June 19, 2013.15 PwC calculations based on data from US Bureau of Labor Statistics, “Contributions of ManufacturingIndustries to Private Nonfarm Business Multifactor Productivity,” June 19, 2013 and “MultifactorProductivity Trends – 2011,” April 9, 2013.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

26

Northern California was 5 percent higher than firms in the same industry outside theregion (Tambe and Hitt, 2010). Firms with relatively more access to outside sources ofICT investment were better equipped to utilize new production methods and practices.The relatively higher elasticity in supply also suggests that firms with access to otherhighly ICT-intensive firms are more flexible in response to market changes.

Conclusion

The ICT sector boosts productivity through various channels. The rapid decline in ICThardware prices between 1995 and 2002 contributed to $230 billion in GDP growth.The combination of ICT hardware and services contributed to an additional $1 trillion inGDP growth between 2002 and 2007. The total contribution of the ICT industry tooverall economic growth over the 1995-2007 period was approximately $1.3 trillion(Mann, 2003 and Mann, 2012). Investment in ICT capital was coupled with a highly-educated workforce. As a result of the change in the structure of labor force, the realgrowth rate in labor productivity during the 2000s was 10 to 20 percent higher relativeto its baseline from 1995 to 2003 (Corrado, Hulten and Sichel, 2009). Spillover effectsrelated to the proximity of other ICT-intensive firms are associated with higher outputper given amount of capital input.

Intel’s Contribution to US Economic Growth

Intel operates in the larger ICT sector by designing and manufacturing microprocessors,motherboard chipsets, integrated circuits, and other similar products. Microprocessorsrepresent the largest segment of Intel’s business, accounting for an estimated 76 percentof the company’s revenue in 2012. Intel is the world’s largest supplier ofsemiconductors in terms of sales, with a global market share of approximately 15.7percent.16 The microprocessors that Intel produces are components of computers andmany other commonly used electronic devices. As electronic devices become moreefficient (e.g., increased computing power, higher-resolution graphics, etc.), so does theproductivity of the households and firms that use them.

As with the ICT sector as a whole, Intel’s products and services contribute to economicgrowth both through their impact on total factor productivity and through theircontribution to capital deepening.

Total factor productivity. According to the US Bureau of Labor Statistics, thegrowth in total factor productivity (also called “multifactor productivity”) accountedfor 0.4 percentage points of the 1.9 percent annual average increase in the privatenonfarm business sector’s real output over the most recent five-year period for whichdata are available (2007 to 2011). The remaining 1.5 percentage points are due to thecombined contribution of capital and labor.17 BLS data show that the Computer and

16 IHS iSuppli Research, December 2012.17 BLS, Multifactor Productivity Trends - 2011, Table B (http://www.bls.gov/mfp/mprdload.htm).Weighting is necessary in order for the individual factor growth rates to sum to the overall growth ofprivate nonfarm business sector output.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

27

Electronics Manufacturing sector (NAICS 334) accounted for half of the TFP growthin the private nonfarm business sector between 2007 and 2011.18 Given that Intel’soutput accounted for approximately 8.5 percent of output in the Computer andElectronics Manufacturing sector during this period, we estimate that Intel’scontribution to nonfarm private business TFP growth averaged 4.2 percent (8.5percent of 50 percent). Thus, through the TFP impact, Intel’s products and servicescontributed 0.02 percentage points to the private nonfarm business sector’s realGDP growth over the 2007 to 2011 period (4.2 percent of 0.4 percent). Thisamounts to $9.0 billion of real GDP between 2007 and 2011 (measured in 2005dollars), or $10.2 billion nominal GDP (measured in current dollars). In otherwords, Intel’s products and services contributed an average of $2.o billion ofnominal GDP per year in this 5-year period due to its impact on total factorproductivity.

Capital deepening. Intel also contributes to GDP growth through increasedinvestment in information processing capital by other sectors of the economy (i.e.,capital deepening). Capital services contributed 1.1 percentage points out of the 1.9percentage increase in the private nonfarm business sector’s real GDP between 2007and 2011. Using data from the US Bureau of Labor Statistics, we estimate thatcomputers and related equipment accounted for approximately one-half of onepercentage point of the increase in the private nonfarm business sector’s real GDPbetween 2007 and 2011 (or $51.4 billion).19 Intel's global market share ofmicroprocessors was 80 percent in 2011.20 Assuming that roughly 80 percent ofcomputers in the United States use an Intel microprocessor, we estimate that Intel'scontribution to real GDP growth through capital deepening was $41.1 billion overthe 2007 and 2011 period (measured in 2005 dollars), or $44.6 billion in nominalGDP (measured in current dollars).21 In other words, Intel’s products and servicescontributed to an average of $8.9 billion of nominal GDP per year through capitaldeepening in this 5-year period.

18 Bureau of Labor Statistics, Multifactor Productivity Trends in Manufacturing, 2011. The contributionof the computers and electronics manufacturing sector to TFP was 0.22 during the period of 2007-2011.The contribution of private nonfarm business to TFP was 0.44 for the same period. The computers andelectronics manufacturing sector therefore contributed half of private nonfarm business TFP growth.19 BLS, Multifactor Productivity Trends- 2011, Table 5. Various asset shares can be found in the MFPcomprehensive tables, "Capital and Information Capital Measure by Asset Type,"http://bls.gov/mfp/mprdload.htm20 Statista, Microprocessor Market Share Worldwide 2009-2011.21 This analysis implicitly assigns all of the value of a personal computer with an Intel chip to Intel andexcludes the value of Intel’s chips used in other types of communications and electronic equipment.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

28

As shown in Table 9,22 the contribution to GDP of Intel's products and services throughtotal factor productivity growth and capital deepening over the 2007-2011 period wasestimated to be $54.8 billion in nominal terms, or approximately $11.0 billion per year.

Table 9 – Contribution of Intel's Products and Services to US EconomicGrowth, 2007-2011

22 BLS, Multifactor Productivity Trends – 2011, Statista, and PwC Calculations. GDP price deflatorsconverting real to nominal growth are from Appendix B of the 2013 Economic Report of the President.

$10.2 billion

$44.6 billion

Contribution to TFP

Contribution due to CapitalDeepening

Total Contribution = $54.8 billion

Source: PwC calculations based on data from IMPLAN and the Bureau of Labor Statistics.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

29

VI: Case Studies

In addition to the significant economic impact generated from operations and capitalinvestments at locations with large Intel manufacturing facilities in Oregon, Arizona andNew Mexico, there are other impacts related to job creation and talent growth,innovation, industry leadership, supplier benefits and clustering impacts. Toqualitatively assess Intel’s impacts on the US national and local economies, PwC andIntel jointly identified three themes that would be the focus of three field-level casestudies of Intel’s operations and investments in the United States.23

In creating the case studies PwC utilized the following approach:

First, PwC created a strategy and plan to assess Intel’s impact. We incorporatedexisting known information supplemented with research and a structuredstakeholder analysis that leveraged input and guidance from internal Intelsources, suppliers, consumers, laborers, colleges, community programs, andgovernmental policy makers.

Next, PwC focused its efforts on conducting face-to-face interviews with keystakeholders as they were identified within both the direct value chain andindirect channels using structured interviews. While the interviewing teamfollowed scripted questions, in order to obtain rich qualitative insights from therespondents, the team pursued additional lines of questioning and themes wheninteresting issues arose as part of the conversation.

Finally, upon completion of research, interviews, and analysis, the PwC teamdeveloped a comprehensive economic overview which is outlined herein.

Quotes from some of these respondents are included in the highlights below.

1. Research and Development (“R&D”) – In 2012 Intel’s global R&D spendingwas $10.1 billion, with a five-year R&D spend of over $36.5 billion. US-basedR&D spending accounted for the majority of the total global spend in 2012. In a2013 survey conducted by Booz & Co, Intel was the number one R&D spenderamong publicly traded US companies in all sectors. Interview respondents calledIntel’s R&D efforts in the United States “rich with innovation” and “industry-leading,” pointing to years of being on the “leading-edge of development” and“bringing forward technology that matters.”

2. Supply Chain Ecosystem – Intel maintains and interacts with a vast supplychain as both a consumer and a supplier. With $11B in global capitalexpenditures (about 80% in the US) and $53.3 billion in global sales, thecompany operates in the middle of a supply chain that is continuously improvingthe usability and interactivity of technology. Interview respondents described

23 For the purposes of the Case Studies, Intel refers to Intel Corporation, excluding McAfee and WindRiver subsidiaries.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

30

Intel’s effects on its Oregon supply chain as “the most important economic factorin Oregon” and that Intel “makes a difference and is stable in our economy.”Furthermore industry veterans touted Intel as a company that “kept themanufacturing and expertise in this country [US]” and noted that “without Intel,the semiconductor industry would be considerably less US-centric and furtherbehind.”

3. Venture Capital – Since its inception in 1991, Intel Capital has invested morethan $10.8 billion in over 1,276 companies in 54 countries. Intel Capital’sinvestment in the US Technology industry has been evident with $6.7 billion, or62% of its total capital investment going to US-based companies. Furthermore,Intel Capital’s focus on company building has resulted in over 500 acquisitions,mergers, and IPOs. Intel Capital’s contribution to the US economy and businessenvironment goes beyond capital investment. As industry experts and executivesof former portfolio companies stated, Intel Capital is “among the best in knowingthe industry” and their “stamp of approval is hard to match.” Intel Capital’sadvantages are described as “longevity, experience, size, consistency, andfinancial returns were among the best, if not the best of any unit.” Portfoliocompanies benefit from investments and interactions that “helped us to span outgeographically and grow the sales team.”

The following pages describe the results of the individual Case Studies.

Intel’s Economic Impacts on the US Economy, 2008 – 2012

31

Case Study 1: Research and DevelopmentInnovations and Technology Advancements with Local,State, National and Global Implications

Globally, Intel spent $10.1 billion on research and development (“R&D”) in 2012, themajority of which is staffed and occurs within the United States. Intel’s R&D initiativesare constantly expanding the technology market and creating opportunity forimprovements in efficiency, data analysis, and user-experience. Major research anddevelopment hubs for Intel are spread across the United States including: Oregon,Texas, Pennsylvania, Wisconsin, South Carolina, New Hampshire, Washington,California, and Colorado. Each of these sites is designed to stay closely connected to itstechnology ecosystem and each site contributes to the research and developmentcapabilities of Intel nationally.

Exhibit 1.1: Intel’s Worldwide Research and Development Spend (2008-2012)

Intel’s R&D initiatives have delivered a number of major technology advancementsincluding, to name a few: low-power architectures; virtualization technologies; and,teraflops research processors. Intel is consistently an early adopter of innovativetechnology, which can be seen through Intel’s equipment purchasing. An internal Intelmanufacturing equipment buyer stated, “We see a 1 to 3 year gap between the first smallwave of equipment buyers, mainly Intel, and the second large wave of equipmentbuyers…the gap is mainly a function of Intel’s technology growing faster than thecompetition.”

0

1

2

3

4

5

6

7

8

9

10

11

2008 2009 2010 2011 2012

5.7 5.7

6.6

8.4

10.1

US

Din

Billi

on

s

R&D Spend by Year

Intel’s Economic Impacts on the US Economy, 2008 – 2012

32

Below are two examples of Intel’s R&D contributions, impact and leadership.

Intel recently built a development fabrication facility in Oregon that opened in 2013 andis building a leading-edge technology, large-scale fabrication facility in Arizona. R&Dspending increased in 2012 by 22 percent over 2011, driven by increasing investments insmartphones, tablets, Ultrabook systems, and data centers. Furthermore, R&Dspending increased with annual wage increases, higher process development costs forIntel’s next-generation 14 nano-meter process technology, and higher costs related todeveloping the 450 millimeter wafer technology.

Examples of Intel Impacts by Particular R&D CenterGeographic Locations

Intel’s Arizona operations are spread across two large sites in the City of Chandler.Roughly half of Intel’s 11,000 employee base in the state works at the 700-acre Ocotillocampus which is dedicated to manufacturing the company’s latest silicon technology.The remaining employees are located at Intel’s 150-acre Chandler campus where asubstantial portion of employees are dedicated to research and development. In fact,Intel has invested more than $300 million to build a new research and developmentfacility at this site. The facility, which is nearing completion, will be used to expandIntel’s packaging operations. The innovation that will occur in this facility is aimed atinfluencing technology trends for years to come. This investment is creating severalhundred Intel R&D-related jobs and nearly a thousand construction jobs. Intel’sArizona employees, on average, earn over $130,000 per year (including totalcompensation, benefits and bonuses).

Intel’s Massachusetts Design Center in Hudson, Massachusetts is home to morethan 825 engineers engaged in microprocessor design, testing and validation for thedevelopment of next generation multi-core Itanium® and Xeon® microprocessors forhigh-end servers. Lab facilities, technical staff, and engineers work directly withproduct design teams on first silicon readiness to support the introduction of new highperformance products before they are released for high volume manufacturing. Labsare staffed by a cross-functional team of content developers, debug engineers, softwareengineers, technicians and inventory control specialists, working closely with design andvalidation engineering working on first silicon to volume validation to deliverproduction ready quality products.

In Intel’s New Hampshire R&D and production facility, a group of 60 Intel researchand development employees researches methods to make it easier to perform parallelprogramming on Intel processing cores while maximizing application performance.Parallel programming by definition is aimed at compartmentalizing complex problemsinto smaller, more manageable problems and computing solutions simultaneously. Thesite manager of the New Hampshire Intel facility described the importance of the workbeing performed as, “enabling the technology created by Intel, meaning, without them,the development community would not be able to “unlock” the potential andperformance of the newer multi-core processors developed at Intel.” The programming

Intel’s Economic Impacts on the US Economy, 2008 – 2012

33

language, prototypes and tools developed here allow end-users of Intel’s silicon to betterunderstand and utilize the capabilities of the products. Intel’s R&D in New Hampshirefocuses on faster computing, higher efficiency, and ease of technology use for moreapplications.

In Intel’s Columbia, South Carolina facility, approximately 310 Intel engineers testIntel’s products to verify the already-designed product’s features work as advertised andmeet stated specifications. It is considered the “last step” before the completed piece ofresearch and development becomes commercialized. The site manager of the SouthCarolina design center stated, “All of our validation activities have successfully yieldedcommercialized products in the XeonTM and CoreTM product lines; for example, XeonTM

E5 is a recent product predominantly supporting Cloud and Data Center programsvalidated at the South Carolina facility and the highly successful 4th Generation CoreTM

graphics system was also validated here.” When asked about the effects of the researchand development site on the local economy, the site manager responded, “Salaries forthis site are notably higher than the comparative geography and our employees enjoy agenerally higher standard of living…The South Carolina Commerce Secretary’s officetells us our gross salary of $26 million has a compounded effect of nearly three times[$76 million] on the local economy.”

In Intel’s Eau Claire, Wisconsin lab, a group of 60 Intel employees are defining,designing, validating, and testing components into which fabric connects. Fabric ishigh-speed interface that connects elements of a computing system and a keytechnology for supercomputing. Fiber cables act like the network connection on acomputer, allowing the user to send and receive data. Data transfers through fiber 25billion times per second, allowing for faster sending and receiving of information thanever before. Fiber cables play a key role in high performance computing, whichimproves our economy, safety, and fundamental knowledge. This technology helps oilcompanies reduce wasted effort by accurately identifying and locating oil reserves,improves the accuracy of weather predictions allowing for accelerated warning systems,and allows for intricate simulations of real-world catastrophes to predict impact andprovide planning tools for disaster relief efforts. The Wisconsin team has grown by 20percent in the past year and is expected to continue on its growth trajectory.

In Fort Collins, Colorado, approximately 425 Intel employees design data centerapplications and solutions including the XeonTM and ItaniumTM architectures. The FortCollins R&D center is responsible for the architecture, design, and development of high-performance server microprocessor for server and workstation applications. The sitecollaborates with universities by participating in programs to grow awareness of andsupport professorships in Science, Technology, Engineering and Mathematics (“STEM”)careers. In addition, the site participates on external boards and conference committeesto support women and minorities in STEM. The design center also impacts itscommunity through environmental initiatives such as recycling (68,000 lbs. in 2011),reducing onsite energy and gas consumption (by an amount that is equivalent to theannual energy and gas consumption by 250 average American households), andimproving the eco-friendly options for worker transportation by implementing andincentivizing a “bike to work” program. This group also is noteworthy because it

Intel’s Economic Impacts on the US Economy, 2008 – 2012

34

benefits its community through direct community giving. Intel Fort Collins is Intel’snumber one United Way contributor in the nation by average gift size per donor at$3,500.

Intel R&D: Case Study Interview Results

Intel’s research and development efforts contribute to the US economy in significantways: