Embed Size (px)

Citation preview

Institute of International Finance

Mumbai, 15 December 2005

Corporate governance:

investor perspectives

December 2005 2

Agenda

Opinions

Performance

Action

December 2005 3

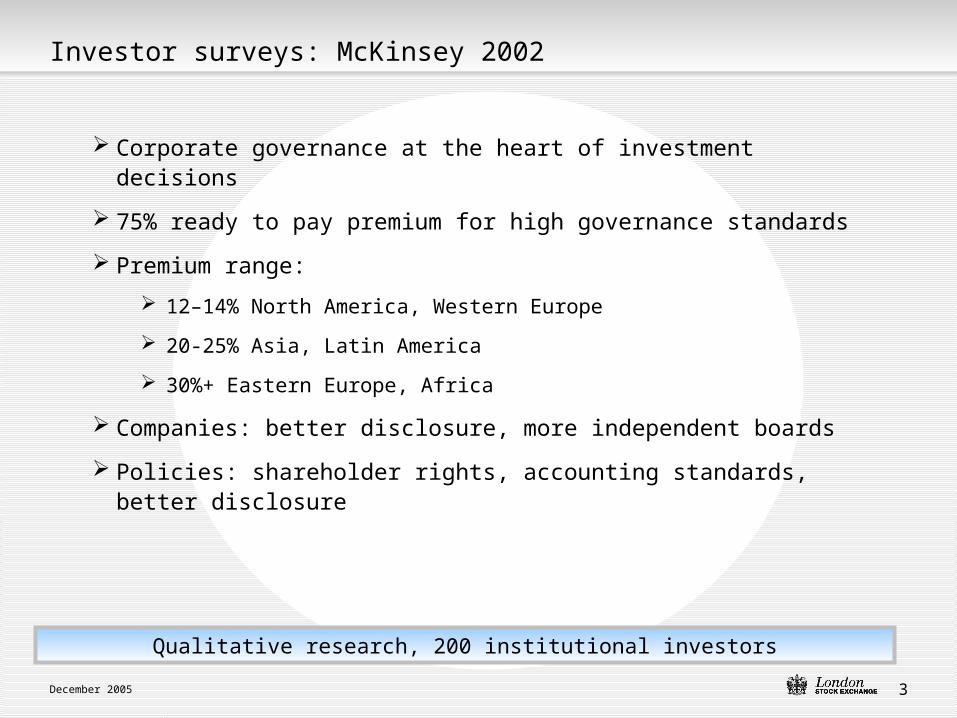

Corporate governance at the heart of investment decisions

75% ready to pay premium for high governance standards

Premium range:

12–14% North America, Western Europe

20-25% Asia, Latin America

30%+ Eastern Europe, Africa

Companies: better disclosure, more independent boards

Policies: shareholder rights, accounting standards, better disclosure

Investor surveys: McKinsey 2002

Qualitative research, 200 institutional investors

December 2005 4

Investor surveys: Investor Relations Society (UK) 2005

Qualitative research, 100 institutional investors

To what extent do you incorporate corporate governance issues in your stock selection procedures?

4% 2% 18%

35%41%

A great deal

A fair amount

J ust a little

None at all

No opnion

December 2005 5

Does good corporate governance have a significant impact on improving a company’s valuation?

Investor surveys: London Stock Exchange, 2005

Opinion survey: 100 institutional investors

1%

4%

51%

44%

0% 10% 20% 30% 40% 50% 60%

Strongly disagree

Disagree somewhat

Agree somewhat

Strongly agree

% respondents

December 2005 6

How important is good corporate governance in influencing investment decisions?

Investor surveys: London Stock Exchange, 2005

Opinion survey: 100 institutional investors

12%

35%

46%

7%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Not very / not at allimportant

Fairly important

Very important

Extremely important

% respondents

December 2005 7

Board independence: no positive correlation to performance

Professor Sanjai Bhagat: worst performers in 1990s had most outside directors

Outsiders in practice may not resist bad decisions

Independence vs. knowledge and incentives

Read across to SEBI/Irani debate?

Limits of analysis based on discrete CG variables?

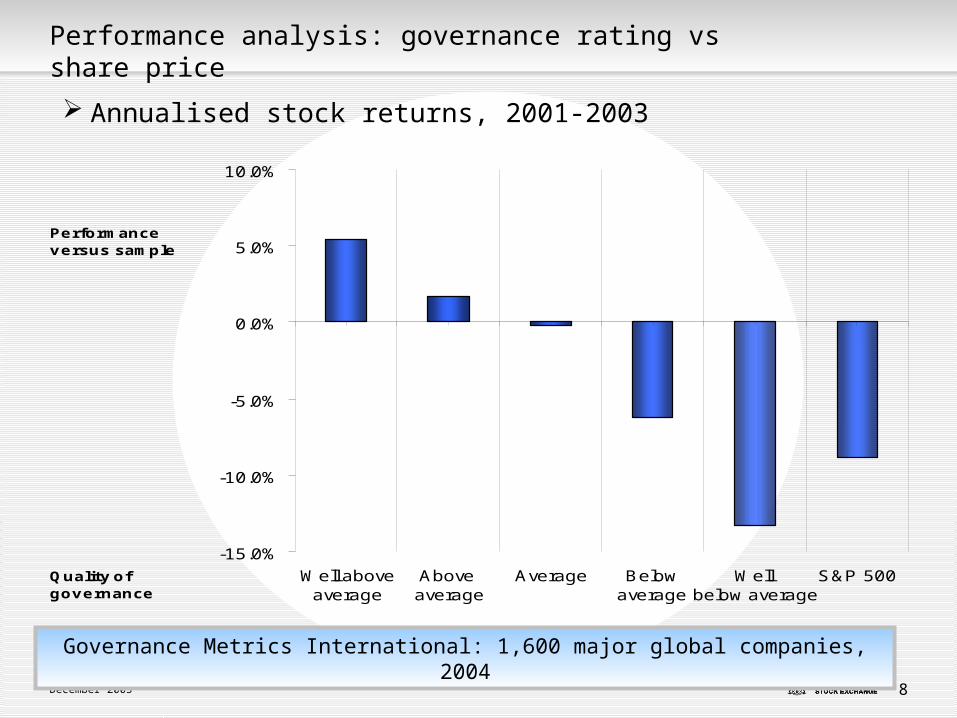

Performance analysis: independent directors (1999)

Quantitative survey: 1,000 US companies

December 2005 8

Annualised stock returns, 2001-2003

Performance analysis: governance rating vs share price

Governance Metrics International: 1,600 major global companies, 2004

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

Well aboveaverage

Above average

Average Below average

Well below average

S&P 500

Performance versus sample

Quality of governance

December 2005 9

It pays to be good: FTSE 350, top vs bottom 10% scores on corporate governance

Performance analysis: Deutsche Bank 2004

Source: Bloomberg, Deutsche Bank Securities Inc. estimates and company information

December 2005 10

Deutsche Bank: building corporate governance into research metrics

Corporate governance impacts, analysed retrospectively:

Profitability, RoE

Bottom 20%: 2002 RoE 1.5%

Top 20%: 2002 RoE 15.9%

Share price performance

Volatility

Impact on current valuations harder to define

“Investors currently do not possess the tools necessary to incorporate corporate governance assessments into valuation on a timely basis.”

Corporate governance: component of equity risk

Corporate governance scoring mechanism, correlated with financial indicators

December 2005 11

Will corporate governance play a greater role in investment decisions over the next year?

Investor surveys: London Stock Exchange, 2005

26%

74%

0%

10%

20%

30%

40%

50%

60%

70%

80%

greater same

% r

esp

on

den

ts

Increasing investor focus on corporate governance: a permanent trend

December 2005 12

Size matters: bigger companies have better governance

Growth strategy co-ordinated to governance strategy

Check governance strategy against best known metrics: try rating yourself

Explore, work with analysts’ approaches to corporate governance analysis / measurement

Communicate corporate governance strategy

None of this should get in the way of common sense

Action: linking governance to valuation

Break rules rather than do anything against common sense