Embed Size (px)

Citation preview

CMA Inter

Income Tax OTHER THAN HEADS OF INCOME

Part 2

Dr CMA T K Sridhar

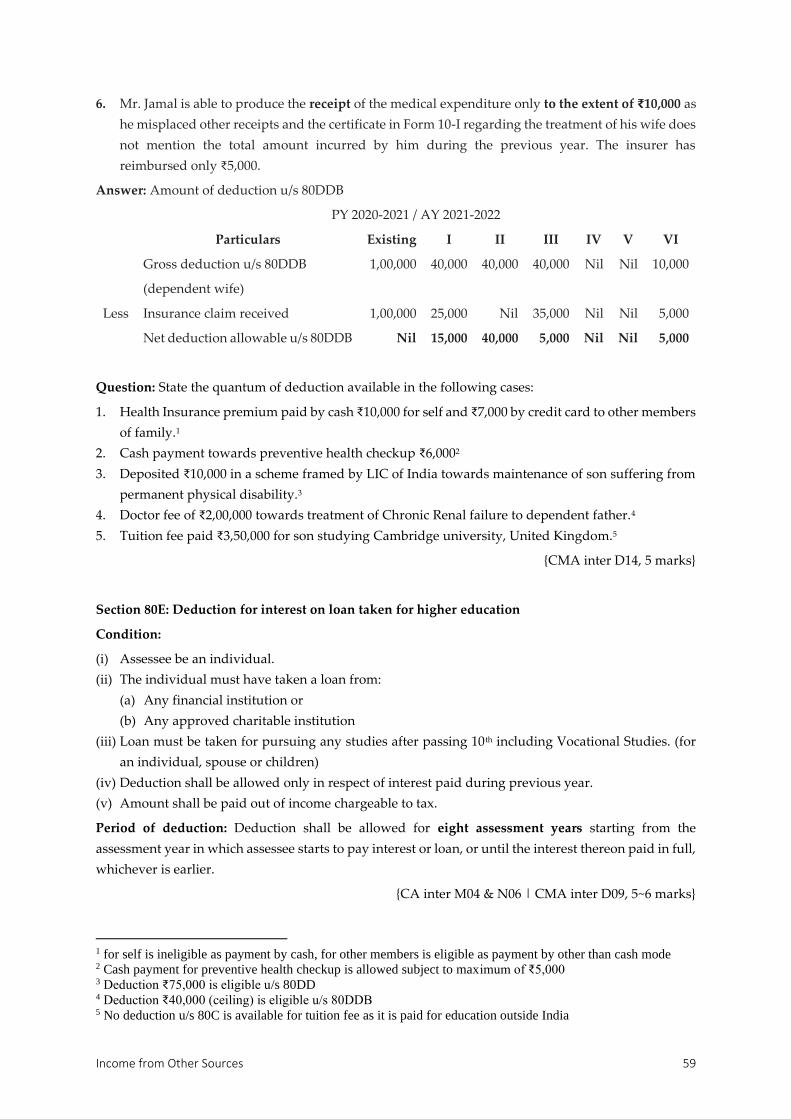

Price: ₹300 [for volumes I and II]

For users who are benefited, pay to…

Account holder name: Singar Educational and Charitable Trust

Account number: 1262115000009481

IFSC code: KVBL0001262

Bank name: karur Vysya Bank

CALL OR VISIT FOR COPIES

Published by

SINGAR BOOKS AND PUBLICATIONS

Head Office: 32-B, Vivekananda Nagar, Ramalinga Nagar, Woriur, Trichy 620 003, TN

Branch Office: 76/1, New Street, Valluvar Kottam High Road,

Nungambakkam, Chennai – 600 034

Ph: Trichy: 93451 22645 | Chennai: 93453 96855

www.singaracademy.in | [email protected]

INCOME TAX

CONTENT

Part 2: Other than Heads of Income Page

1 Income Tax Law: An Introduction 1

2 Basis of Charge and Rates of Tax 8

3 Residential Status & Scope of Total Income 15

4 Agricultural Income 22

5 Income Which Do Not Form Part of Total Income 24

6 Income of Other Persons Include in Assessee’s Total Income 32

7 Set-off and Carry Forward of Losses 40

8 Deductions from Gross Total Income 49

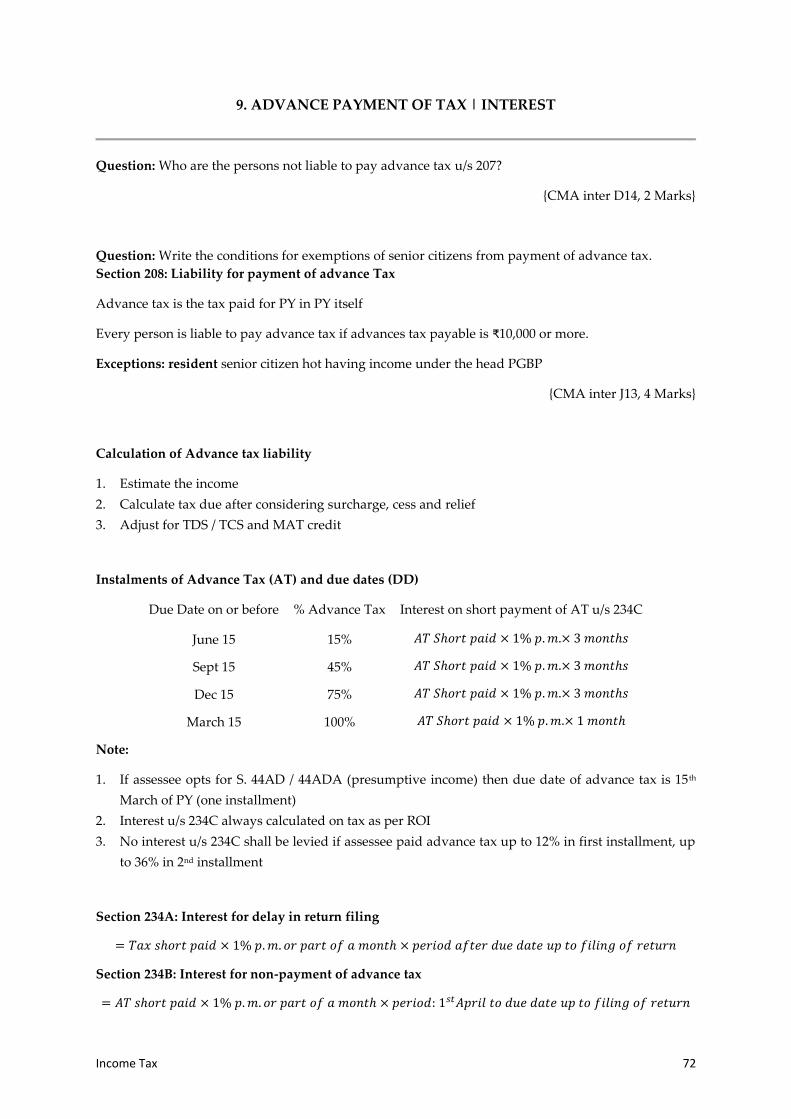

9 Advance Payment of Tax | Interest 72

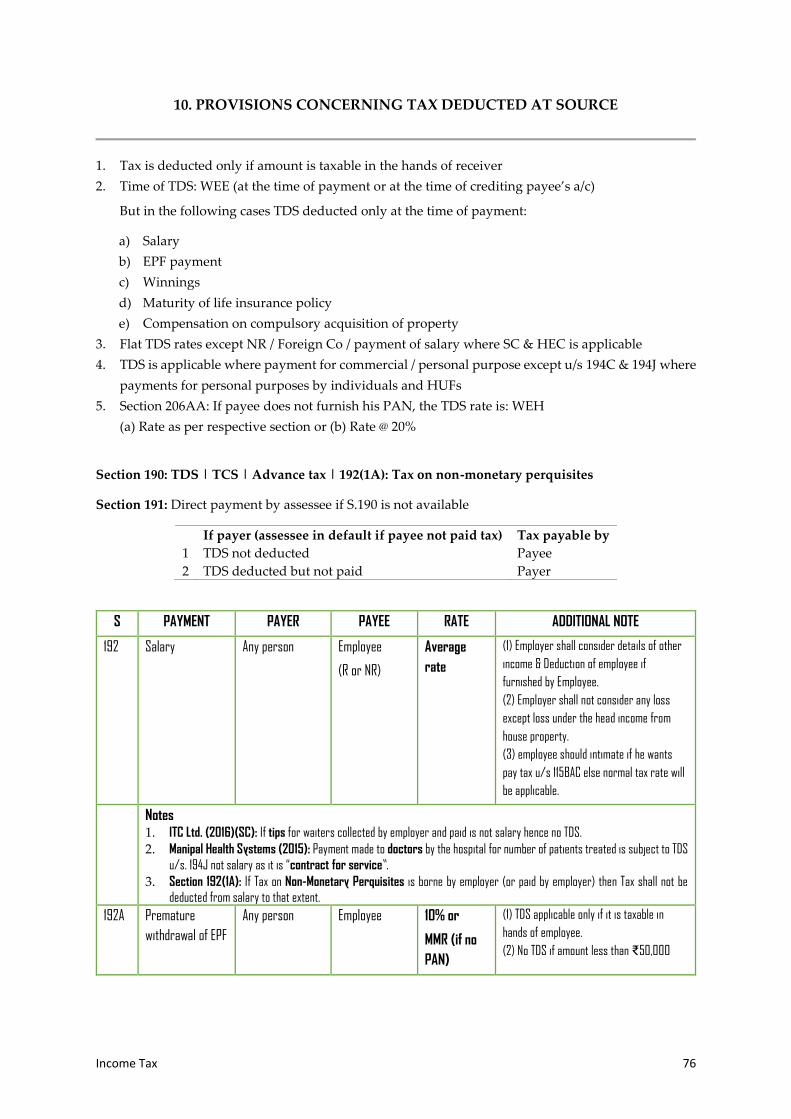

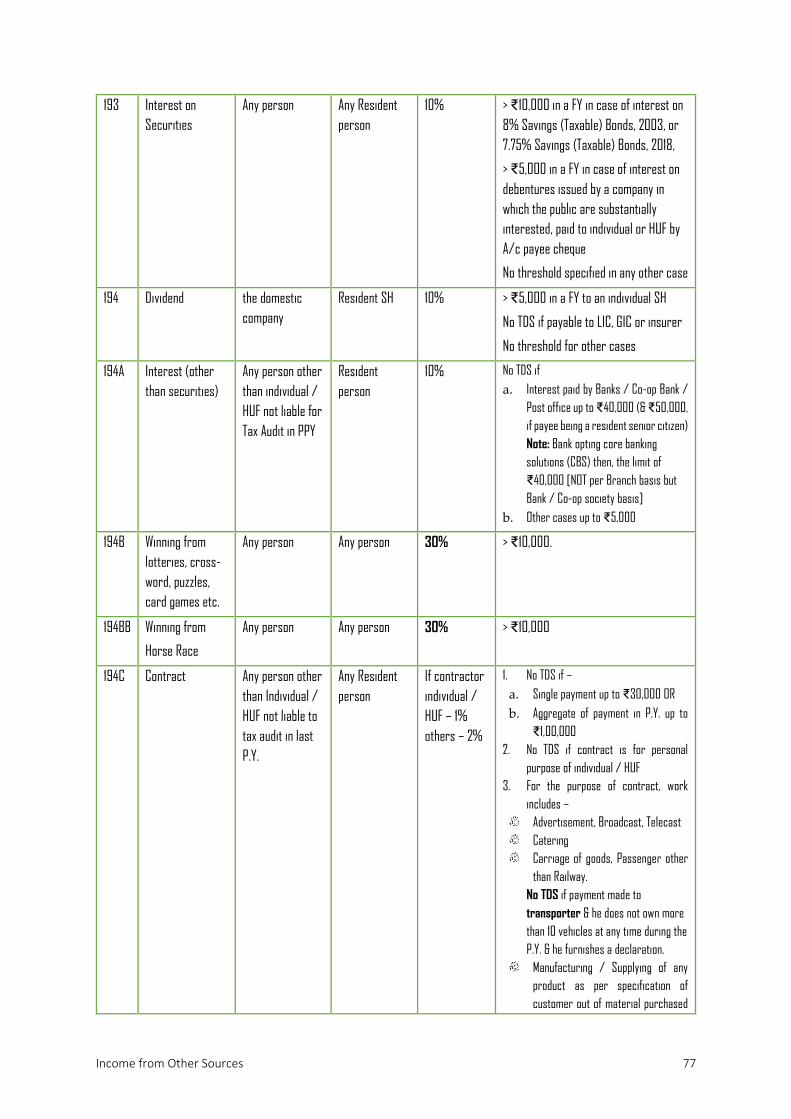

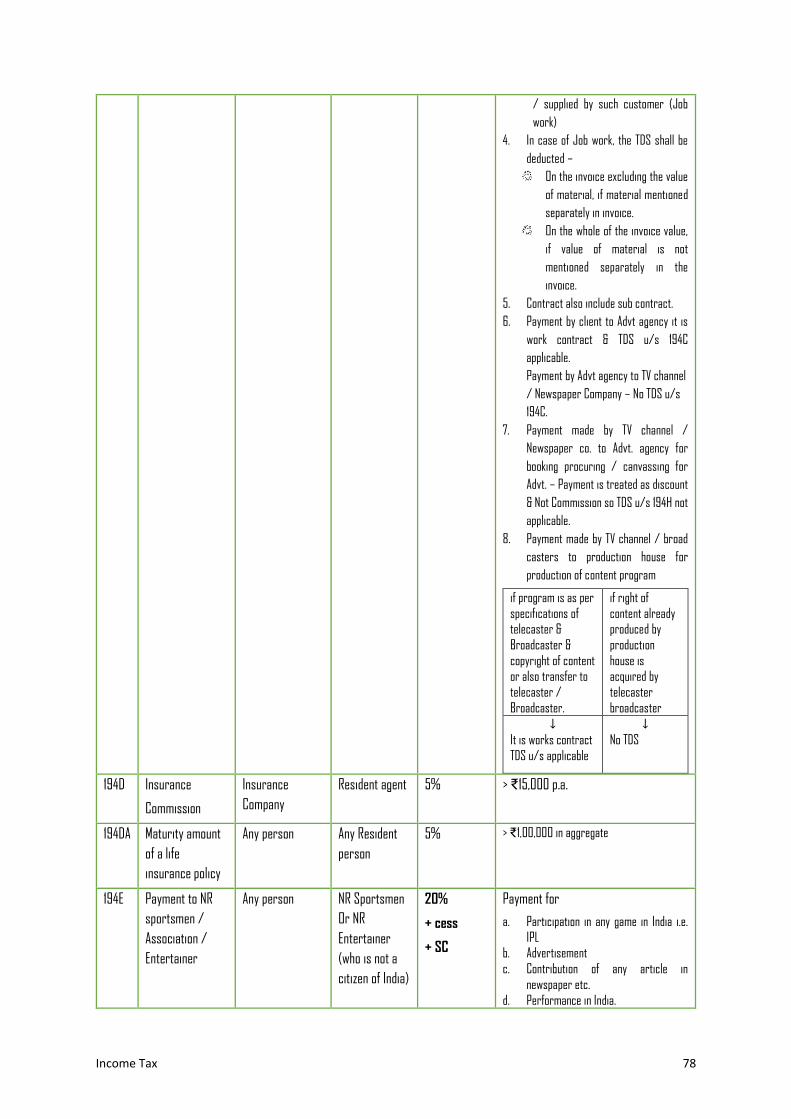

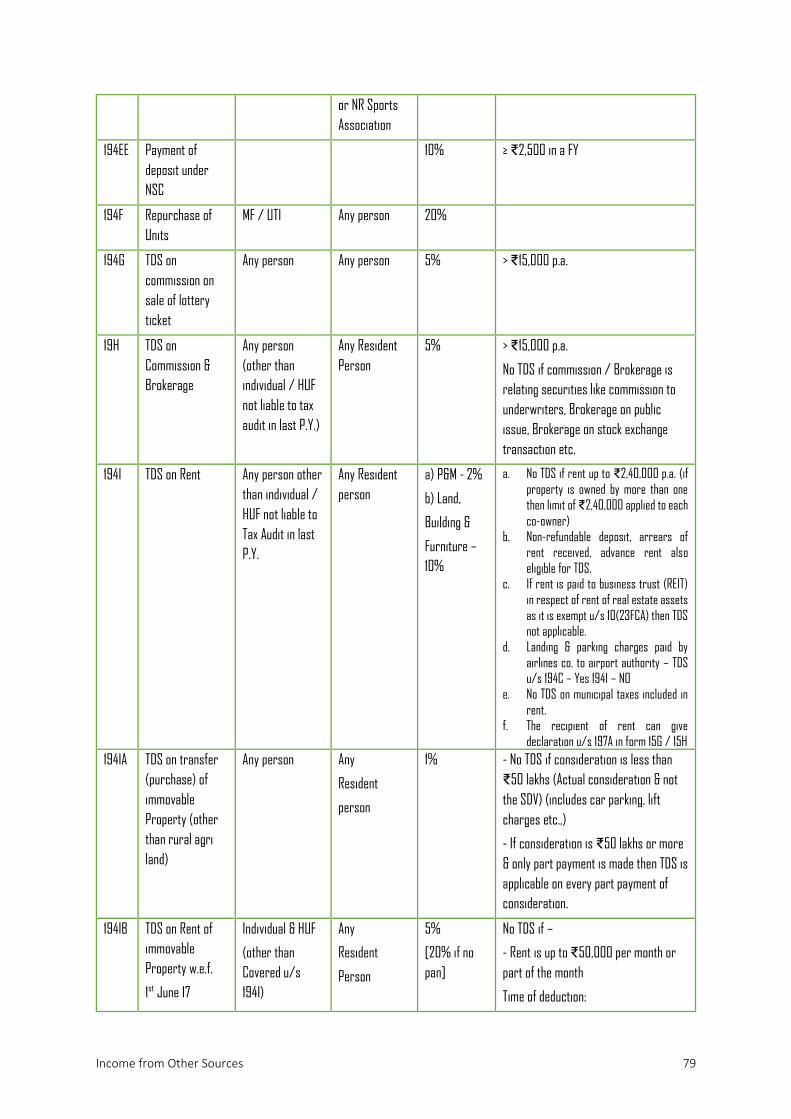

10 Provisions Concerning Tax Deducted at Source 76

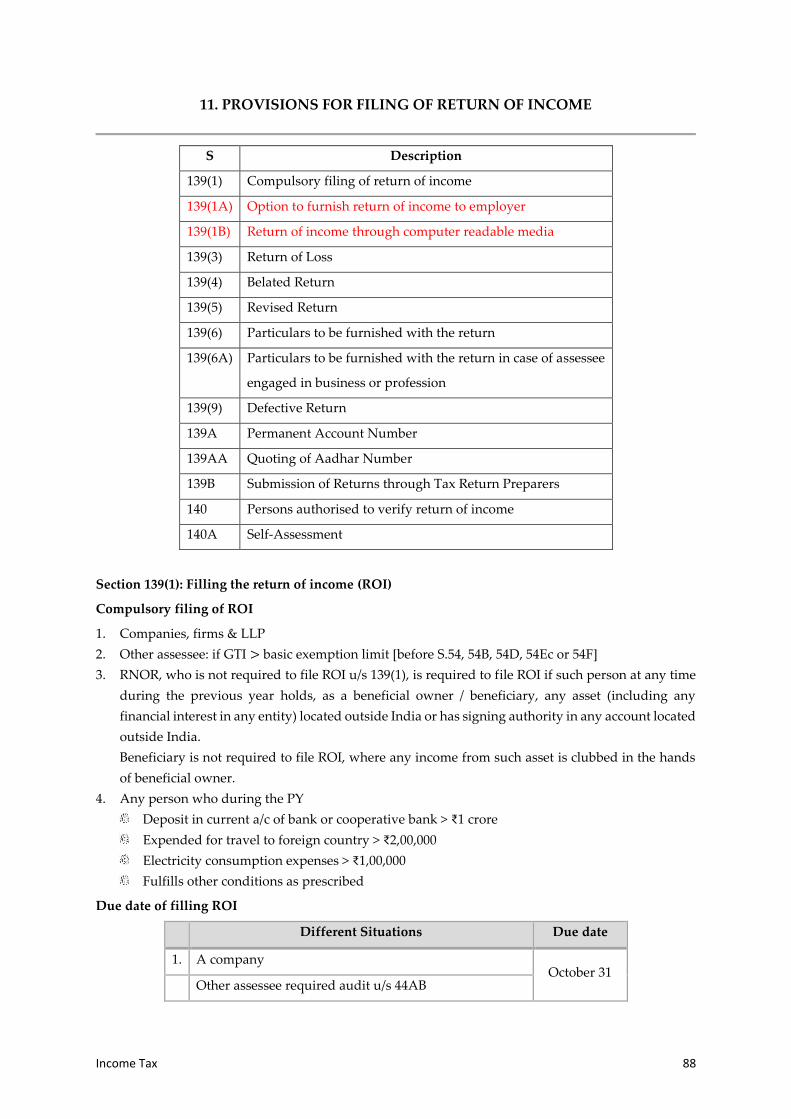

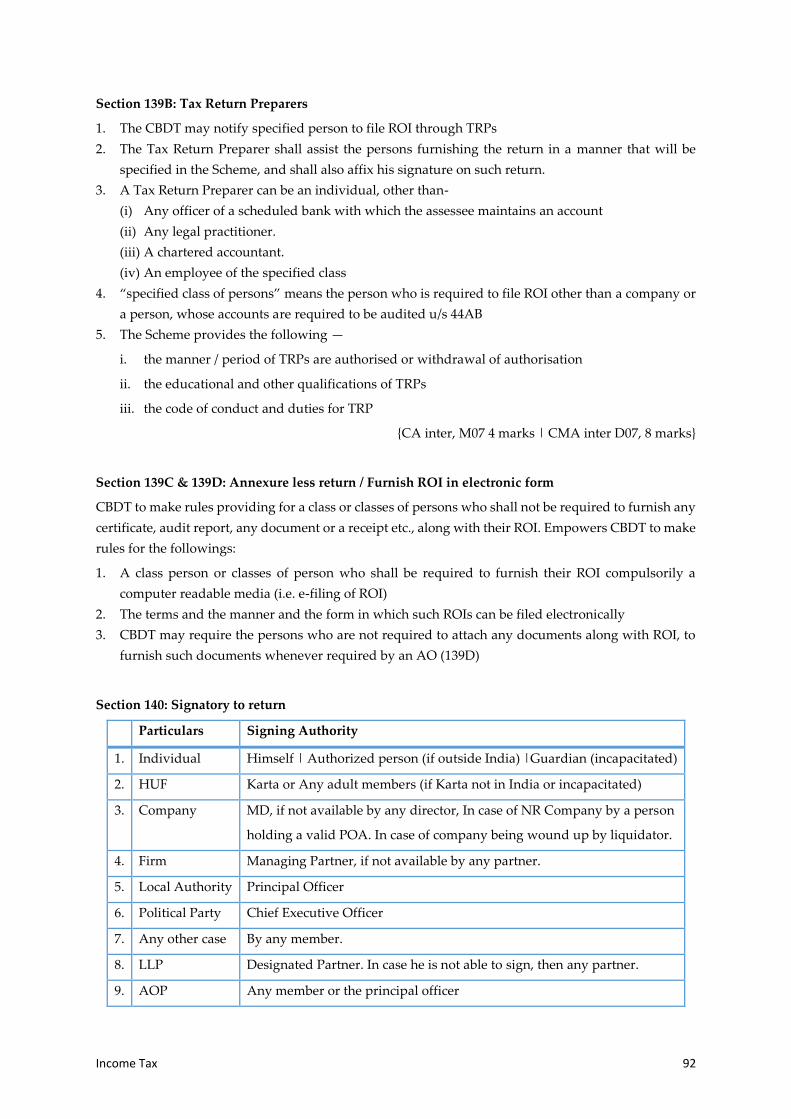

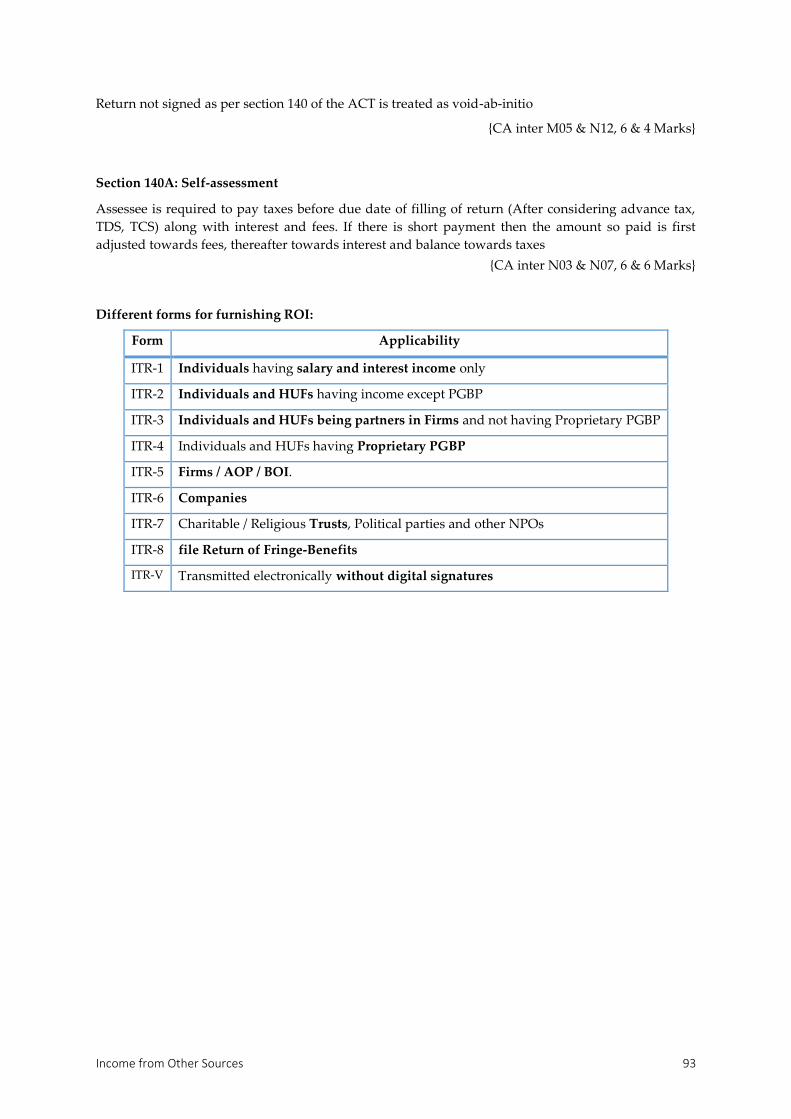

11 Provisions for Filing of Return of Income 89

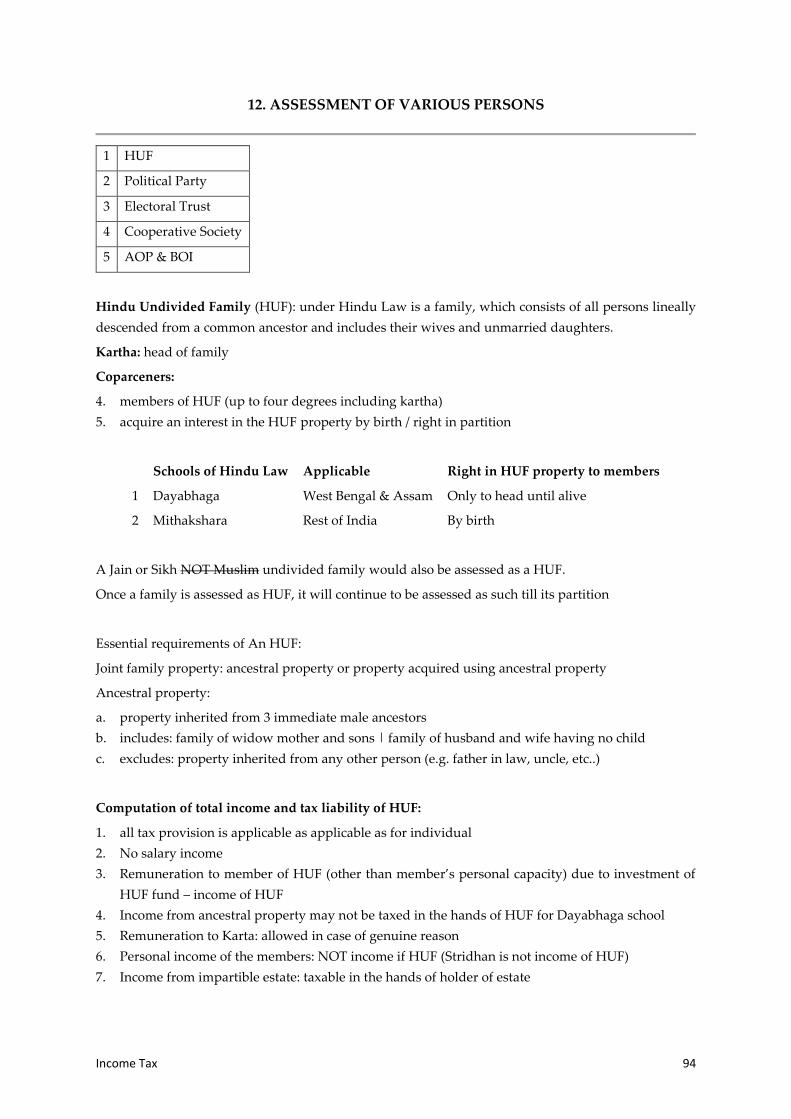

12 Assessment of Various Persons 95

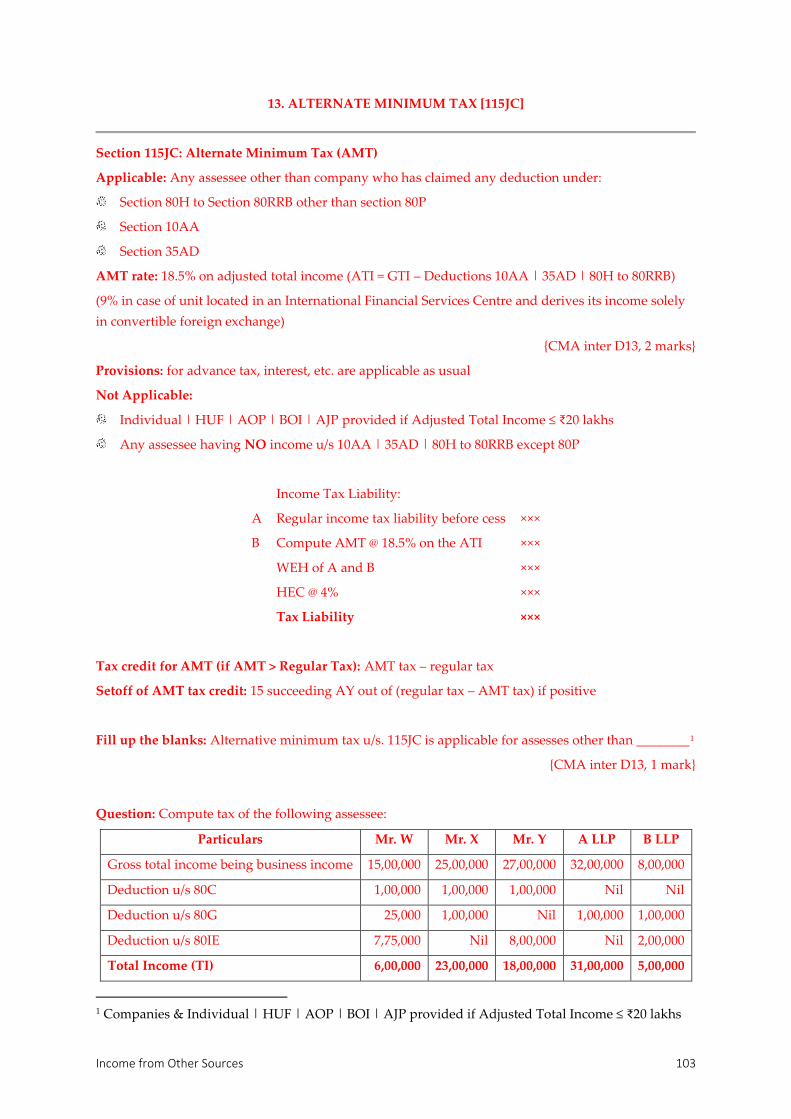

13 Alternate Minimum Tax

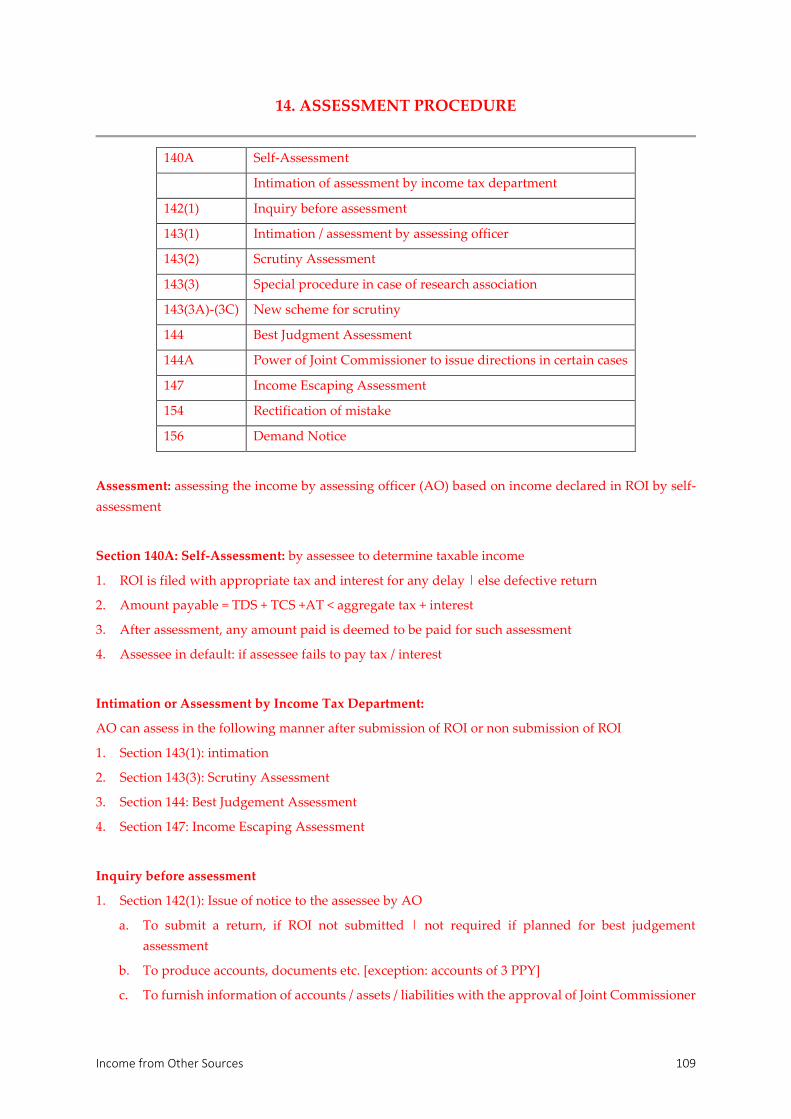

14 Assessment Procedure

15 Income Computation and Disclosure Standards

Income from Salaries 1

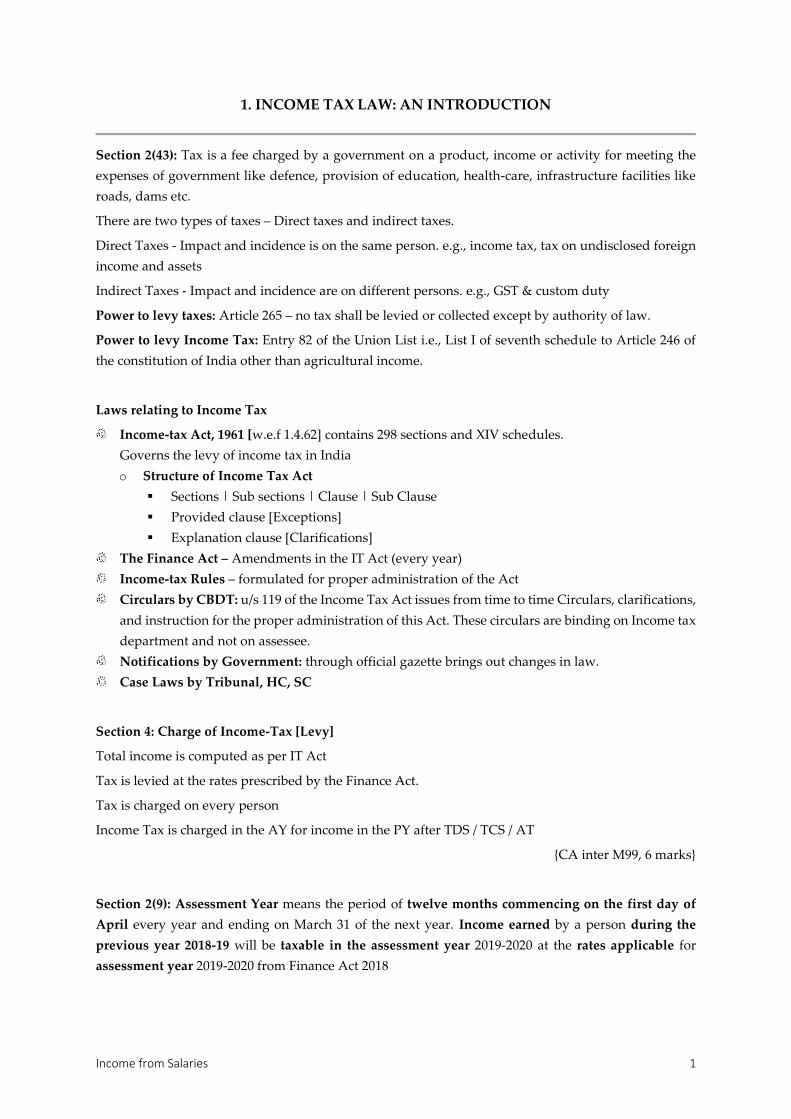

1. INCOME TAX LAW: AN INTRODUCTION

Section 2(43): Tax is a fee charged by a government on a product, income or activity for meeting the

expenses of government like defence, provision of education, health-care, infrastructure facilities like

roads, dams etc.

There are two types of taxes – Direct taxes and indirect taxes.

Direct Taxes - Impact and incidence is on the same person. e.g., income tax, tax on undisclosed foreign

income and assets

Indirect Taxes - Impact and incidence are on different persons. e.g., GST & custom duty

Power to levy taxes: Article 265 – no tax shall be levied or collected except by authority of law.

Power to levy Income Tax: Entry 82 of the Union List i.e., List I of seventh schedule to Article 246 of

the constitution of India other than agricultural income.

Laws relating to Income Tax

Income-tax Act, 1961 [w.e.f 1.4.62] contains 298 sections and XIV schedules.

Governs the levy of income tax in India

o Structure of Income Tax Act

▪ Sections | Sub sections | Clause | Sub Clause

▪ Provided clause [Exceptions]

▪ Explanation clause [Clarifications]

The Finance Act – Amendments in the IT Act (every year)

Income-tax Rules – formulated for proper administration of the Act

Circulars by CBDT: u/s 119 of the Income Tax Act issues from time to time Circulars, clarifications,

and instruction for the proper administration of this Act. These circulars are binding on Income tax

department and not on assessee.

Notifications by Government: through official gazette brings out changes in law.

Case Laws by Tribunal, HC, SC

Section 4: Charge of Income-Tax [Levy]

Total income is computed as per IT Act

Tax is levied at the rates prescribed by the Finance Act.

Tax is charged on every person

Income Tax is charged in the AY for income in the PY after TDS / TCS / AT

{CA inter M99, 6 marks}

Section 2(9): Assessment Year means the period of twelve months commencing on the first day of

April every year and ending on March 31 of the next year. Income earned by a person during the

previous year 2018-19 will be taxable in the assessment year 2019-2020 at the rates applicable for

assessment year 2019-2020 from Finance Act 2018

Income Tax 2

Section 3: Previous Year means the financial year immediately preceeding the assessment year. The

year in which income is earned is known as previous year.

Previous year in the case of newly set up business / profession

First previous year for a business / profession newly set up during the financial year or for a new

source of income comes in to existence during the financial year, the period beginning form the date

of setting up of the business or from the date the new source come into existence, and ending on the

last date of the previous year i.e. March 31 shall be the first previous year for that business or source of

income.

Section 2(31): The term "Person" includes:

1. An individual

2. A Hindu Undivided Family (HUF)

3. A Company

4. A firm

5. An association of person (AOP) or a Body of Individuals (BOI)

6. A local authority: and

7. Every Artificial Judicial Person, not falling with in any preceding categories.

Individual: means only a natural person. It also includes a minor or a person of unsound mind but the

assessment in such a case may be made on guardian or manager who is entitled to receive his income.

In the case of deceased person, assessment would be made on the legal representative.

Hindu Undivided Family (HUF): under Hindu Law is a family, which consists of all persons lineally

descended from a common ancestor and includes their wives and unmarried daughters.

Kartha: head of family

Coparceners:

1. members of HUF (up to four degrees including kartha)

2. acquire an interest in the HUF property by birth / right in partition

3. HUF should have at least two male members or two coparceners

Schools of Hindu Law Applicable Right in HUF property to members

1 Dayabhaga West Bengal & Assam Only to head until alive

2 Mithakshara Rest of India By birth

A Jain or Sikh undivided family would also be assessed as a HUF.

Once a family is assessed as HUF, it will continue to be assessed as such till its partition

Section 2(17): Company means

(i) any Indian company; or

(ii) body corporate incorporated outside India under the laws of a foreign country; or

Income from Salaries 3

(iii) any institution, association or a body which is assessed or was assessable / assessed as a company

for any AY commencing on or before 1.4.1970; or

(iv) any institution, association or body whether incorporated or not and whether Indian or non-

Indian which is declared by general or special order of the CBDT to be a company.

Section 2(22A): A ‘Domestic Company’ means —

(i) an Indian company; or

(ii) in case of foreign company, who has made the prescribed arrangements for the declaration and

payment of dividends within India

Section 2(26): Indian Company

A company formed and registered under the Companies Act or

Registered under any law of state or UT.

Corporation under Government

Any institution, association or body which is declared by the Board to be a company

Section 2(23A): ‘Foreign Company’ – a company which is not Indian Company

Section 2(23): The terms ‘firm’, ‘partner’ and ‘partnership’ are as per Indian Partnership Act and

applicable in LLP. However, for income-tax purposes a minor admitted to the benefits of an existing

partnership would also be treated as partner.

Association of Persons (AOP) and Body of Individuals (BOI) [Group of persons]

Group Consist Purpose Common Purpose Become

AOP Any persons Income earning Must be Not BOI

BOI Only Individuals Income earning / Co-heirs May be AOP

{CA inter N98, 5 marks}

Local Authority: means a municipal committee, district board, body of port commissioners or other

authority legally entitled to or entrusted by the Government with the control or management of a

municipal or local fund.

Taxable: income from business from supply of commodity or service to jurisdiction other than its own

Exempt: Income arising from the supply of water and electricity anywhere

Artificial Juridical Person – Separate entity in the eyes of law

Sued in court through person managing them

Example: An idol, deity, university, bar council etc.

Income Tax 4

Section 2(7): Assessee means a person by whom any tax or any other sum of money is payable under

the act, and includes

(a) every person in respect of whom any proceeding under this Act has been taken for the assessment

of his income or assessment of fringe benefits or of the income of any other person in respect of

which he is assessable, or of the loss sustained by him or by such other person, or of the amount of

refund due to him or to such other person;

(b) every person who is deemed to be an assessee under any provision of this Act;

(c) every person who is deemed to be an assessee in default under any provision of this Act;

Deemed to be an assessee: the following persons are deemed to be assesse

1. Legal hire

2. Representatives: representatives of foreigner, a lunatic, a minor or an incompetent person is liable

to pay tax on their income.

Deemed to be an assessee in default:

A person who does not fulfill the legal obligations as per IT Act

Due to which a loss of revenue is caused to the income-tax department,

The person is entitled to compensate the department for such loss.

For this purpose he is deemed to be assessee in default.

1. Any assessee if fails to pay off whole or part of the demand raised by the Income Tax Authorities

u/s 156 within 30 days of its receipt, is usually termed as assessee in default

2. Fails to comply with the provision of TDS

3. Fails to pay advance tax

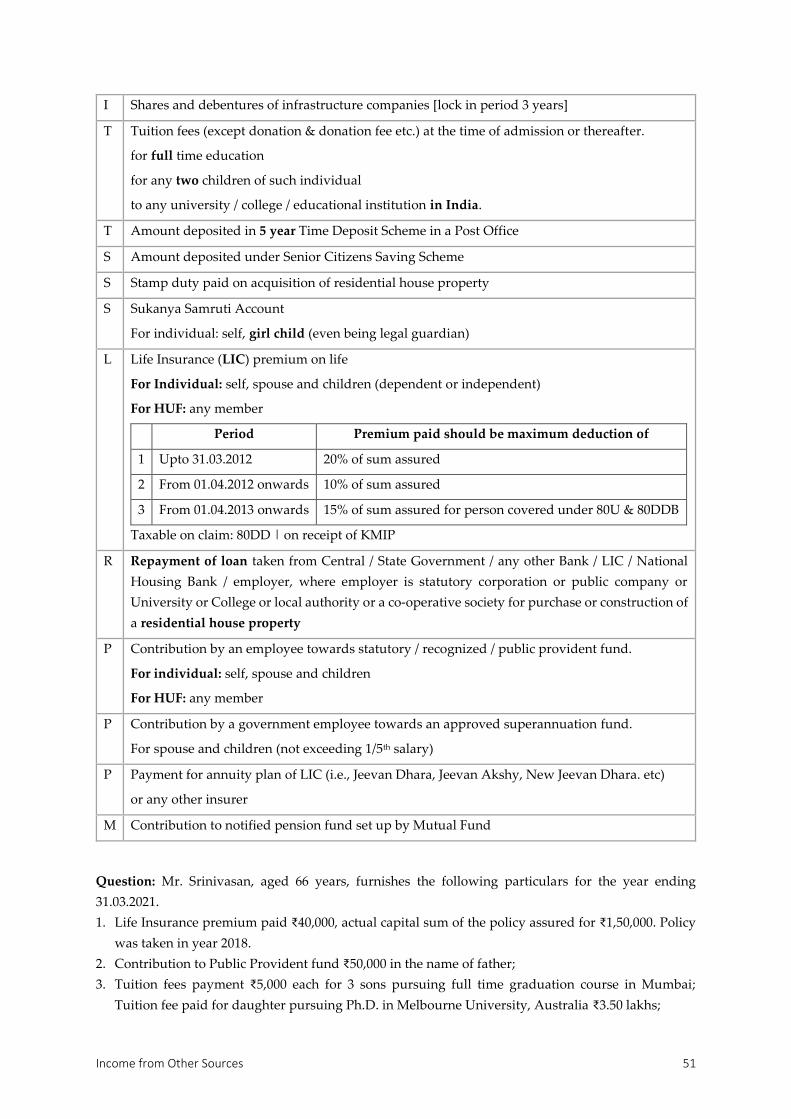

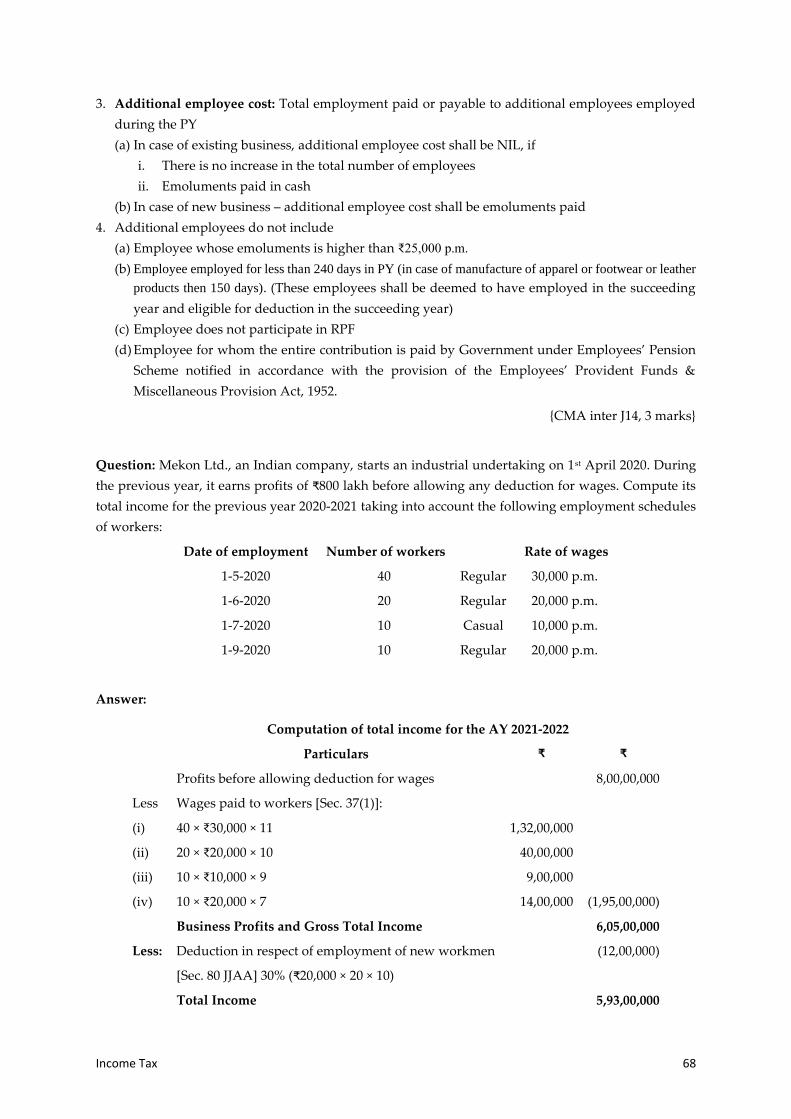

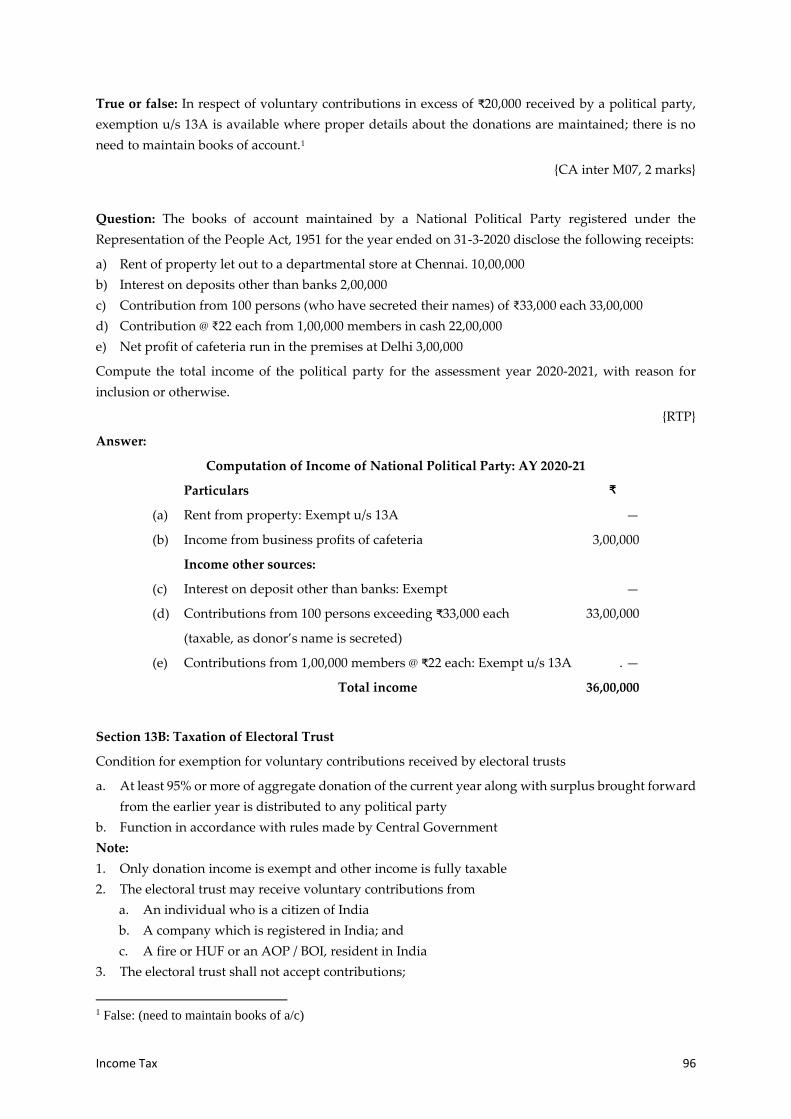

Question: A single letter of enquiry was issued by the Income Tax department to Mr. Shoumik of Pune.

In this letter there was no specific mention of any provision of the Income Tax Act. Can Mr. Shoumik

be treated as an assessee under the Income Tax Act?1

{CA inter N98 & N13, 6 & 4 marks}

Section 2(24): "income" includes—

Regular receipts and casual receipts (such as winning from lotteries etc.) are also taxable

Income may be cash or kind

Income normally refers to revenue receipts. [Except Capital gains]

Income means net receipts (including loss) [revenue – expenses] and not gross receipts

Income is taxable either on due basis or receipt basis [except PGBP and IFOS (regularly followed)]

Income earned in a previous year is chargeable to tax in the assessment year.

Legal and illegal income is taxable

Money embezzled – income

Not taxable: reimbursement | pin money | contingent income | income from mutual activity

1 Yes

Income from Salaries 5

A person cannot make profit out of transaction with himself

Criteria for determining whether a receipt or revenue in nature

Fixed capital (capital receipt) or circulating capital (revenue receipt)

Income from transfer of capital asset (capital receipt) or trading asset (revenue receipt)

Capital receipts vis-à-vis revenue receipts: test to be applied

1. Transaction entered into the regular course of business – (revenue receipt)

2. Profit arising from sale of shares and securities (revenue receipt if trading motive)

3. A single transaction may also be revenue receipt in certain circumstances

4. Liquidated damages linked with delayed supply of capital asset is capital receipt

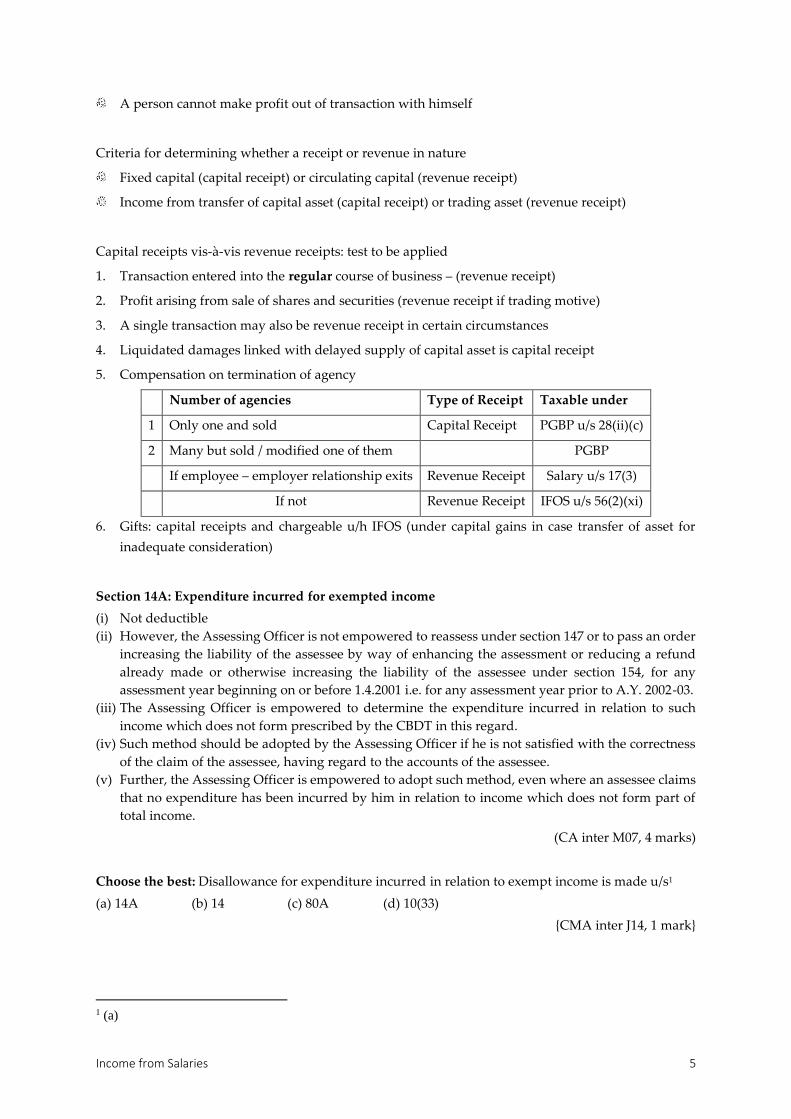

5. Compensation on termination of agency

Number of agencies Type of Receipt Taxable under

1 Only one and sold Capital Receipt PGBP u/s 28(ii)(c)

2 Many but sold / modified one of them PGBP

If employee – employer relationship exits Revenue Receipt Salary u/s 17(3)

If not Revenue Receipt IFOS u/s 56(2)(xi)

6. Gifts: capital receipts and chargeable u/h IFOS (under capital gains in case transfer of asset for

inadequate consideration)

Section 14A: Expenditure incurred for exempted income

(i) Not deductible

(ii) However, the Assessing Officer is not empowered to reassess under section 147 or to pass an order

increasing the liability of the assessee by way of enhancing the assessment or reducing a refund

already made or otherwise increasing the liability of the assessee under section 154, for any

assessment year beginning on or before 1.4.2001 i.e. for any assessment year prior to A.Y. 2002-03.

(iii) The Assessing Officer is empowered to determine the expenditure incurred in relation to such

income which does not form prescribed by the CBDT in this regard.

(iv) Such method should be adopted by the Assessing Officer if he is not satisfied with the correctness

of the claim of the assessee, having regard to the accounts of the assessee.

(v) Further, the Assessing Officer is empowered to adopt such method, even where an assessee claims

that no expenditure has been incurred by him in relation to income which does not form part of

total income.

(CA inter M07, 4 marks)

Choose the best: Disallowance for expenditure incurred in relation to exempt income is made u/s1

(a) 14A (b) 14 (c) 80A (d) 10(33)

{CMA inter J14, 1 mark}

1 (a)

Income Tax 6

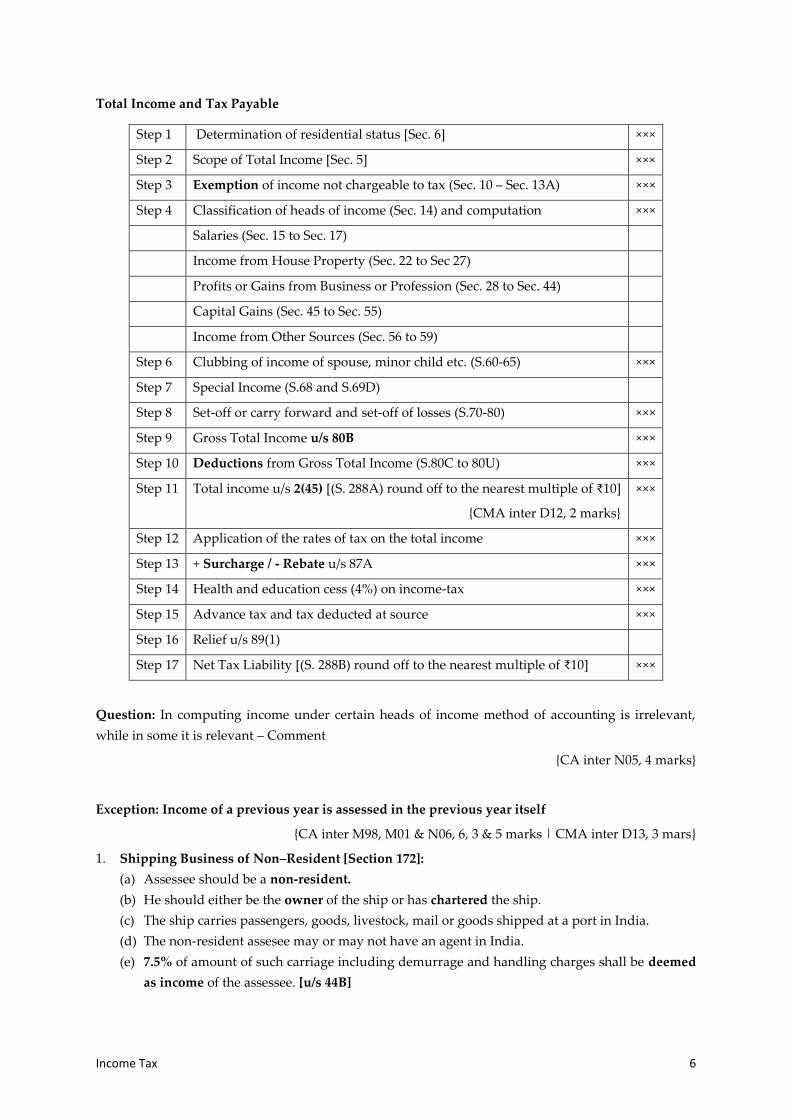

Total Income and Tax Payable

Step 1 Determination of residential status [Sec. 6] ×××

Step 2 Scope of Total Income [Sec. 5] ×××

Step 3 Exemption of income not chargeable to tax (Sec. 10 – Sec. 13A) ×××

Step 4 Classification of heads of income (Sec. 14) and computation ×××

Salaries (Sec. 15 to Sec. 17)

Income from House Property (Sec. 22 to Sec 27)

Profits or Gains from Business or Profession (Sec. 28 to Sec. 44)

Capital Gains (Sec. 45 to Sec. 55)

Income from Other Sources (Sec. 56 to 59)

Step 6 Clubbing of income of spouse, minor child etc. (S.60-65) ×××

Step 7 Special Income (S.68 and S.69D)

Step 8 Set-off or carry forward and set-off of losses (S.70-80) ×××

Step 9 Gross Total Income u/s 80B ×××

Step 10 Deductions from Gross Total Income (S.80C to 80U) ×××

Step 11 Total income u/s 2(45) [(S. 288A) round off to the nearest multiple of ₹10]

{CMA inter D12, 2 marks}

×××

Step 12 Application of the rates of tax on the total income ×××

Step 13 + Surcharge / - Rebate u/s 87A ×××

Step 14 Health and education cess (4%) on income-tax ×××

Step 15 Advance tax and tax deducted at source ×××

Step 16 Relief u/s 89(1)

Step 17 Net Tax Liability [(S. 288B) round off to the nearest multiple of ₹10] ×××

Question: In computing income under certain heads of income method of accounting is irrelevant,

while in some it is relevant – Comment

{CA inter N05, 4 marks}

Exception: Income of a previous year is assessed in the previous year itself

{CA inter M98, M01 & N06, 6, 3 & 5 marks | CMA inter D13, 3 mars}

1. Shipping Business of Non–Resident [Section 172]:

(a) Assessee should be a non-resident.

(b) He should either be the owner of the ship or has chartered the ship.

(c) The ship carries passengers, goods, livestock, mail or goods shipped at a port in India.

(d) The non-resident assesee may or may not have an agent in India.

(e) 7.5% of amount of such carriage including demurrage and handling charges shall be deemed

as income of the assessee. [u/s 44B]

Income from Salaries 7

(f) The Master of the Ship should file the return and pay tax on such income before departure or

must make necessary arrangements for payment of such tax within 30 days of departure of the

ship.

(g) If the above conditions are fulfilled, the Collector or Customs shall grant the port clearance.

(h) This assessment is mandatory. The Assessing Officer may call for such accounts as to determine

the tax liability.

2. Persons leaving India [Section 174]:

(a) The assessee leaves India either during the current previous year or immediately thereafter.

(b) He does not have any intention to return to India immediately.

(c) His total income from the date of commencement of previous year up to the date of departure

shall be assessed as income of the same previous year.

(d) This assessment is mandatory.

3. AOP or BOI or Artificial Juridical Person formed for a particular event or purpose [Sec. 174A]:

(a) AOP or BOl established or incorporated for a particular event or purpose.

(b) It is likely to be dissolved in the assessment year in which it was established or incorporated or

immediately after such assessment year.

(c) The total income of the period from the expiry of the previous year for that assessment year up

to the date of dissolution shall be chargeable to tax in that assessment year.

4. Persons likely to transfer property to avoid tax [Section 175] :

(a) The assessee is likely to charge, sell or transfer or dispose of his asset.

(b) The asset may be movable or immovable property.

(c) The intention of transfer is to avoid payment of any tax liability under Income Tax Act.

(d) The total income from the commencement of previous year up to the date of proceedings u/s

175 is taxable in that year itself.

(e) This assessment is mandatory.

5. Discontinued business [Section 176]:

(a) Business or profession carried on by the assessee is discontinued during the previous year.

(b) The income from the first day of the previous year up to the date of discontinuation may be

assessed in the previous year itself.

(c) The assessee discontinuing the business/profession shall give within 15 days of such

discontinuance a notice about the discontinuance to the Assessing Officer.

(d) This assessment is discretionary.

Fill up the blank: There are two schools of Hindu Law, one is Mitakshara and the other is ___1

{CMA inter J14, 1 mark}

Question: A single letter of enquiry was issued by the Income Tax Department to X of Mumbai. In this

letter there was no specific mention of any provision of the Income Tax Act, Can X be treated as an

‘Assessee’?

{CMA inter D09, 2 marks}

1 Dayabhaga

Income Tax 8

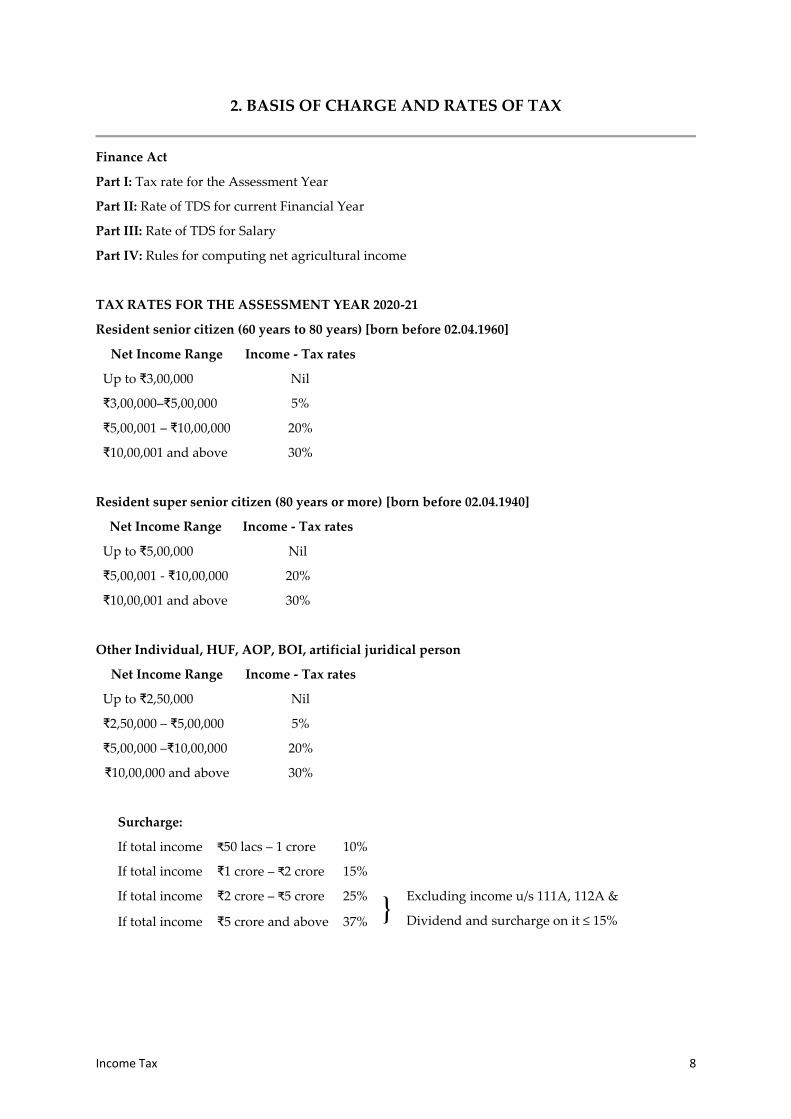

2. BASIS OF CHARGE AND RATES OF TAX

Finance Act

Part I: Tax rate for the Assessment Year

Part II: Rate of TDS for current Financial Year

Part III: Rate of TDS for Salary

Part IV: Rules for computing net agricultural income

TAX RATES FOR THE ASSESSMENT YEAR 2020-21

Resident senior citizen (60 years to 80 years) [born before 02.04.1960]

Net Income Range Income - Tax rates

Up to ₹3,00,000 Nil

₹3,00,000–₹5,00,000 5%

₹5,00,001 – ₹10,00,000 20%

₹10,00,001 and above 30%

Resident super senior citizen (80 years or more) [born before 02.04.1940]

Other Individual, HUF, AOP, BOI, artificial juridical person

Net Income Range Income - Tax rates

Up to ₹2,50,000 Nil

₹2,50,000 – ₹5,00,000 5%

₹5,00,000 –₹10,00,000 20%

₹10,00,000 and above 30%

Surcharge:

If total income ₹50 lacs – 1 crore 10%

If total income ₹1 crore – ₹2 crore 15%

If total income ₹2 crore – ₹5 crore 25%

} Excluding income u/s 111A, 112A &

Dividend and surcharge on it ≤ 15% If total income ₹5 crore and above 37%

Net Income Range Income - Tax rates

Up to ₹5,00,000 Nil

₹5,00,001 - ₹10,00,000 20%

₹10,00,001 and above 30%

Income from House Property 9

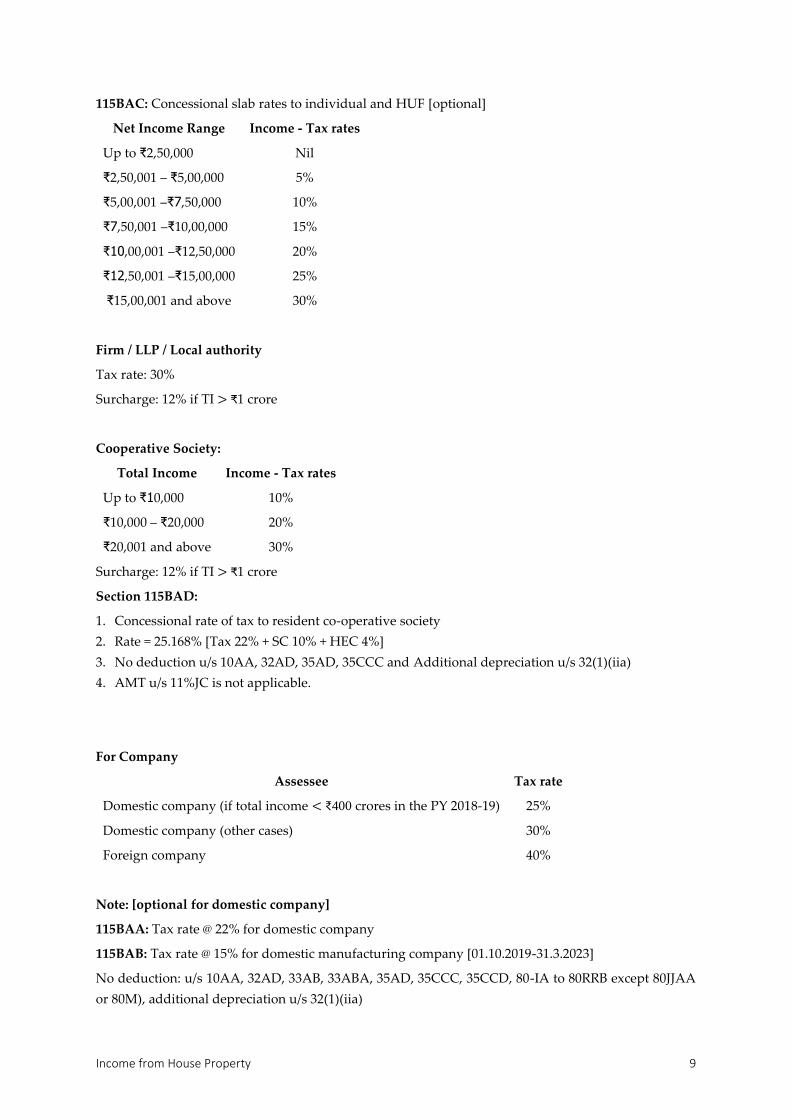

115BAC: Concessional slab rates to individual and HUF [optional]

Net Income Range Income - Tax rates

Up to ₹2,50,000 Nil

₹2,50,001 – ₹5,00,000 5%

₹5,00,001 –₹7,50,000 10%

₹7,50,001 –₹10,00,000 15%

₹10,00,001 –₹12,50,000 20%

₹12,50,001 –₹15,00,000 25%

₹15,00,001 and above 30%

Firm / LLP / Local authority

Tax rate: 30%

Surcharge: 12% if TI > ₹1 crore

Cooperative Society:

Total Income Income - Tax rates

Up to ₹10,000 10%

₹10,000 – ₹20,000 20%

₹20,001 and above 30%

Surcharge: 12% if TI > ₹1 crore

Section 115BAD:

1. Concessional rate of tax to resident co-operative society

2. Rate = 25.168% [Tax 22% + SC 10% + HEC 4%]

3. No deduction u/s 10AA, 32AD, 35AD, 35CCC and Additional depreciation u/s 32(1)(iia)

4. AMT u/s 11%JC is not applicable.

For Company

Assessee Tax rate

Domestic company (if total income < ₹400 crores in the PY 2018-19) 25%

Domestic company (other cases) 30%

Foreign company 40%

Note: [optional for domestic company]

115BAA: Tax rate @ 22% for domestic company

115BAB: Tax rate @ 15% for domestic manufacturing company [01.10.2019-31.3.2023]

No deduction: u/s 10AA, 32AD, 33AB, 33ABA, 35AD, 35CCC, 35CCD, 80-IA to 80RRB except 80JJAA

or 80M), additional depreciation u/s 32(1)(iia)

Income Tax 10

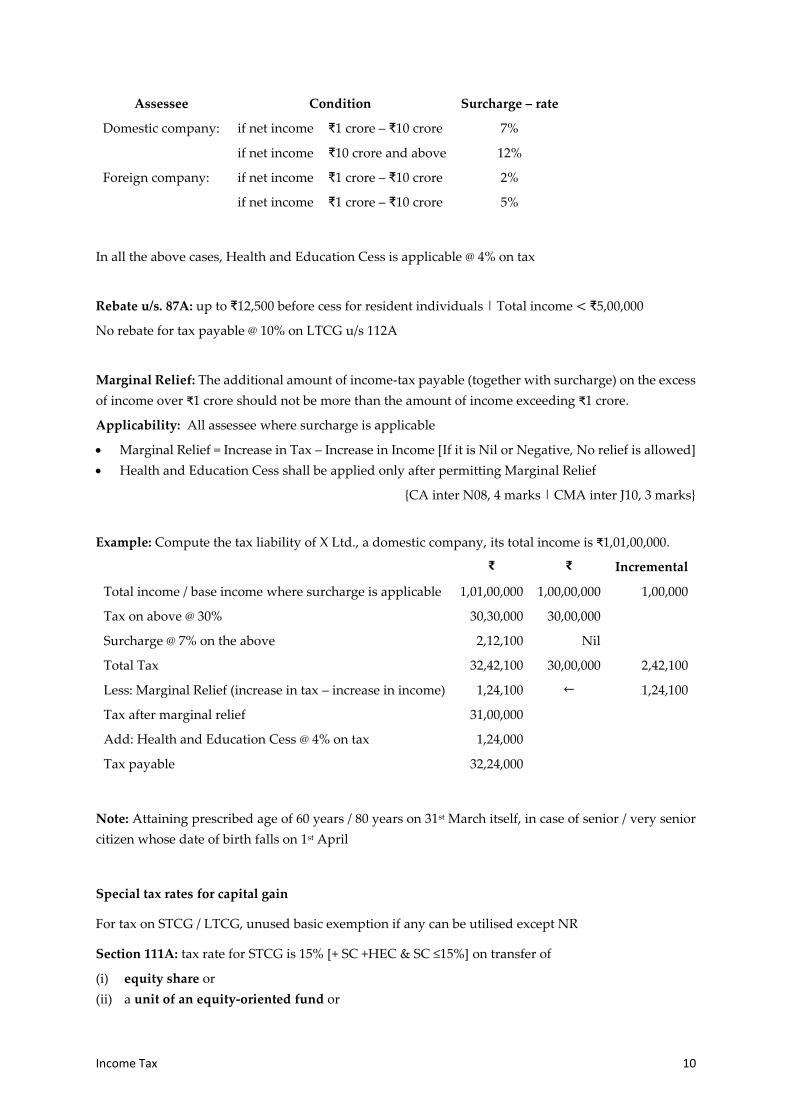

Assessee Condition Surcharge – rate

Domestic company: if net income ₹1 crore – ₹10 crore 7%

if net income ₹10 crore and above 12%

Foreign company: if net income ₹1 crore – ₹10 crore 2%

if net income ₹1 crore – ₹10 crore 5%

In all the above cases, Health and Education Cess is applicable @ 4% on tax

Rebate u/s. 87A: up to ₹12,500 before cess for resident individuals | Total income < ₹5,00,000

No rebate for tax payable @ 10% on LTCG u/s 112A

Marginal Relief: The additional amount of income-tax payable (together with surcharge) on the excess

of income over ₹1 crore should not be more than the amount of income exceeding ₹1 crore.

Applicability: All assessee where surcharge is applicable

• Marginal Relief = Increase in Tax – Increase in Income [If it is Nil or Negative, No relief is allowed]

• Health and Education Cess shall be applied only after permitting Marginal Relief

{CA inter N08, 4 marks | CMA inter J10, 3 marks}

Example: Compute the tax liability of X Ltd., a domestic company, its total income is ₹1,01,00,000.

₹ ₹ Incremental

Total income / base income where surcharge is applicable 1,01,00,000 1,00,00,000 1,00,000

Tax on above @ 30% 30,30,000 30,00,000

Surcharge @ 7% on the above 2,12,100 Nil

Total Tax 32,42,100 30,00,000 2,42,100

Less: Marginal Relief (increase in tax – increase in income) 1,24,100 ← 1,24,100

Tax after marginal relief 31,00,000

Add: Health and Education Cess @ 4% on tax 1,24,000

Tax payable 32,24,000

Note: Attaining prescribed age of 60 years / 80 years on 31st March itself, in case of senior / very senior

citizen whose date of birth falls on 1st April

Special tax rates for capital gain

For tax on STCG / LTCG, unused basic exemption if any can be utilised except NR

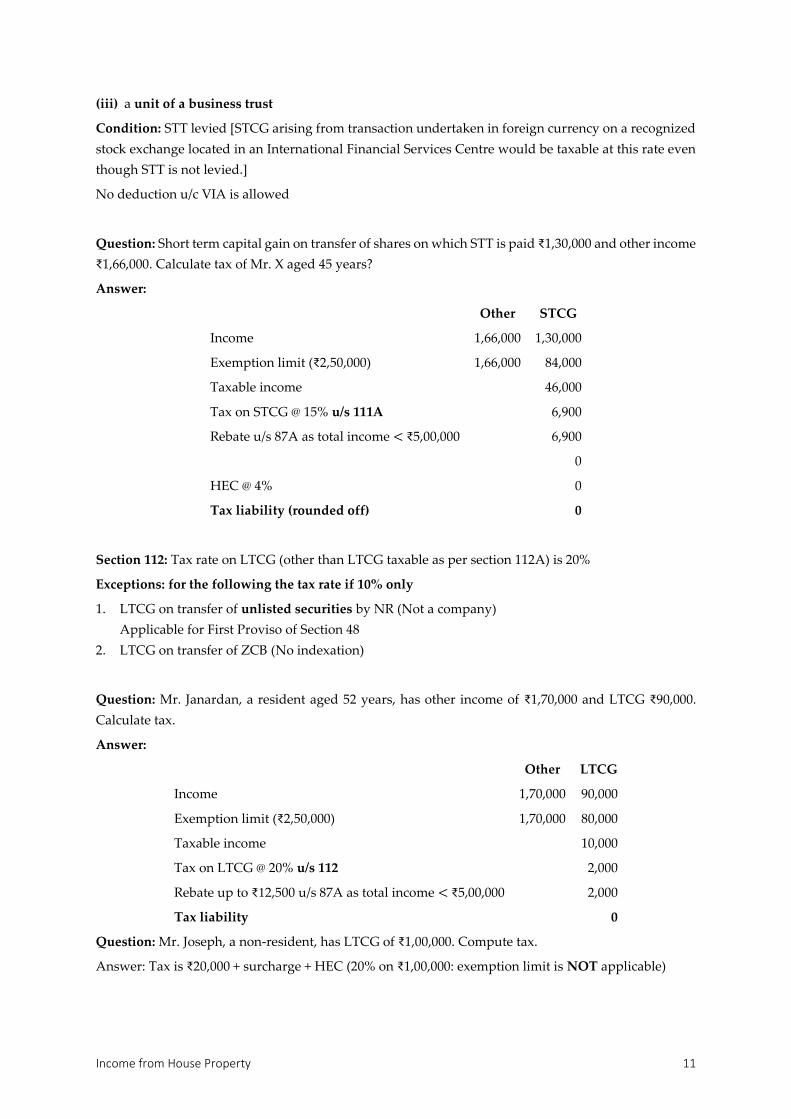

Section 111A: tax rate for STCG is 15% [+ SC +HEC & SC ≤15%] on transfer of

(i) equity share or

(ii) a unit of an equity-oriented fund or

Income from House Property 11

(iii) a unit of a business trust

Condition: STT levied [STCG arising from transaction undertaken in foreign currency on a recognized

stock exchange located in an International Financial Services Centre would be taxable at this rate even

though STT is not levied.]

No deduction u/c VIA is allowed

Question: Short term capital gain on transfer of shares on which STT is paid ₹1,30,000 and other income

₹1,66,000. Calculate tax of Mr. X aged 45 years?

Answer:

Other STCG

Income 1,66,000 1,30,000

Exemption limit (₹2,50,000) 1,66,000 84,000

Taxable income 46,000

Tax on STCG @ 15% u/s 111A 6,900

Rebate u/s 87A as total income < ₹5,00,000 6,900

0

HEC @ 4% 0

Tax liability (rounded off) 0

Section 112: Tax rate on LTCG (other than LTCG taxable as per section 112A) is 20%

Exceptions: for the following the tax rate if 10% only

1. LTCG on transfer of unlisted securities by NR (Not a company)

Applicable for First Proviso of Section 48

2. LTCG on transfer of ZCB (No indexation)

Question: Mr. Janardan, a resident aged 52 years, has other income of ₹1,70,000 and LTCG ₹90,000.

Calculate tax.

Answer:

Other LTCG

Income 1,70,000 90,000

Exemption limit (₹2,50,000) 1,70,000 80,000

Taxable income 10,000

Tax on LTCG @ 20% u/s 112 2,000

Rebate up to ₹12,500 u/s 87A as total income < ₹5,00,000 2,000

Tax liability 0

Question: Mr. Joseph, a non-resident, has LTCG of ₹1,00,000. Compute tax.

Answer: Tax is ₹20,000 + surcharge + HEC (20% on ₹1,00,000: exemption limit is NOT applicable)

Income Tax 12

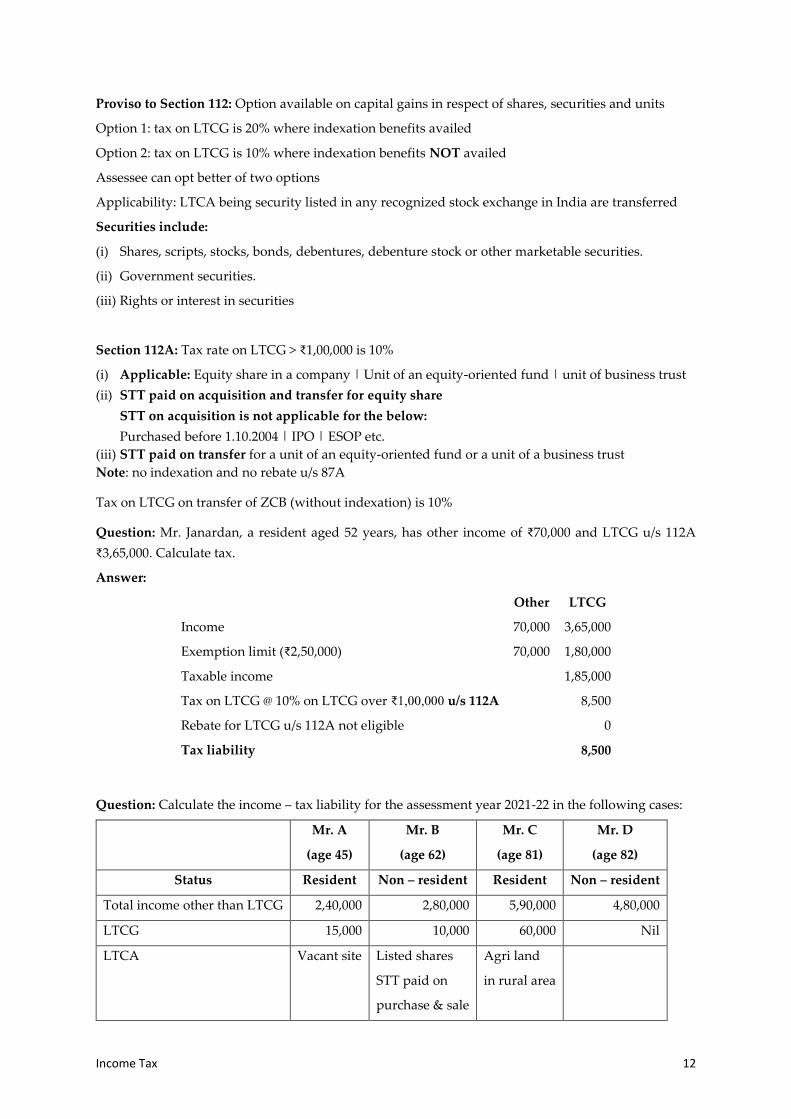

Proviso to Section 112: Option available on capital gains in respect of shares, securities and units

Option 1: tax on LTCG is 20% where indexation benefits availed

Option 2: tax on LTCG is 10% where indexation benefits NOT availed

Assessee can opt better of two options

Applicability: LTCA being security listed in any recognized stock exchange in India are transferred

Securities include:

(i) Shares, scripts, stocks, bonds, debentures, debenture stock or other marketable securities.

(ii) Government securities.

(iii) Rights or interest in securities

Section 112A: Tax rate on LTCG > ₹1,00,000 is 10%

(i) Applicable: Equity share in a company | Unit of an equity-oriented fund | unit of business trust

(ii) STT paid on acquisition and transfer for equity share

STT on acquisition is not applicable for the below:

Purchased before 1.10.2004 | IPO | ESOP etc.

(iii) STT paid on transfer for a unit of an equity-oriented fund or a unit of a business trust

Note: no indexation and no rebate u/s 87A

Tax on LTCG on transfer of ZCB (without indexation) is 10%

Question: Mr. Janardan, a resident aged 52 years, has other income of ₹70,000 and LTCG u/s 112A

₹3,65,000. Calculate tax.

Answer:

Other LTCG

Income 70,000 3,65,000

Exemption limit (₹2,50,000) 70,000 1,80,000

Taxable income 1,85,000

Tax on LTCG @ 10% on LTCG over ₹1,00,000 u/s 112A 8,500

Rebate for LTCG u/s 112A not eligible 0

Tax liability 8,500

Question: Calculate the income – tax liability for the assessment year 2021-22 in the following cases:

Mr. A

(age 45)

Mr. B

(age 62)

Mr. C

(age 81)

Mr. D

(age 82)

Status Resident Non – resident Resident Non – resident

Total income other than LTCG 2,40,000 2,80,000 5,90,000 4,80,000

LTCG 15,000 10,000 60,000 Nil

LTCA Vacant site Listed shares

STT paid on

purchase & sale

Agri land

in rural area

Income from House Property 13

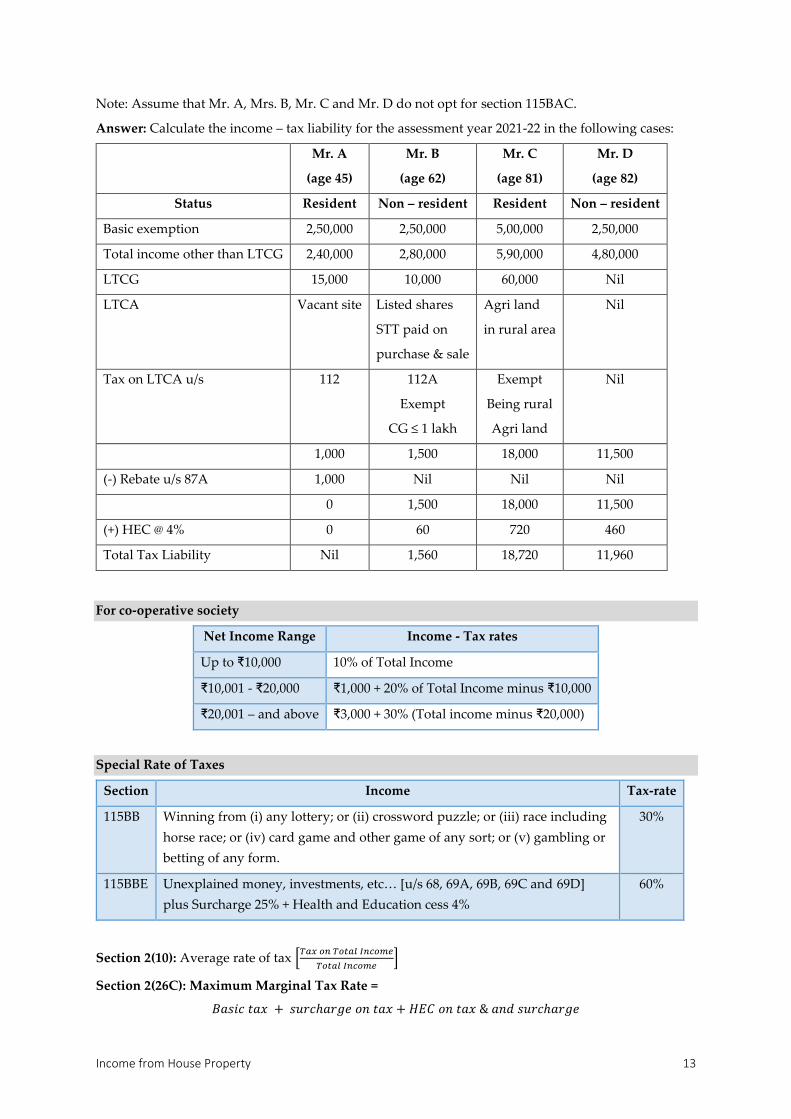

Note: Assume that Mr. A, Mrs. B, Mr. C and Mr. D do not opt for section 115BAC.

Answer: Calculate the income – tax liability for the assessment year 2021-22 in the following cases:

Mr. A

(age 45)

Mr. B

(age 62)

Mr. C

(age 81)

Mr. D

(age 82)

Status Resident Non – resident Resident Non – resident

Basic exemption 2,50,000 2,50,000 5,00,000 2,50,000

Total income other than LTCG 2,40,000 2,80,000 5,90,000 4,80,000

LTCG 15,000 10,000 60,000 Nil

LTCA Vacant site Listed shares

STT paid on

purchase & sale

Agri land

in rural area

Nil

Tax on LTCA u/s 112 112A

Exempt

CG ≤ 1 lakh

Exempt

Being rural

Agri land

Nil

1,000 1,500 18,000 11,500

(-) Rebate u/s 87A 1,000 Nil Nil Nil

0 1,500 18,000 11,500

(+) HEC @ 4% 0 60 720 460

Total Tax Liability Nil 1,560 18,720 11,960

For co-operative society

Net Income Range Income - Tax rates

Up to ₹10,000 10% of Total Income

₹10,001 - ₹20,000 ₹1,000 + 20% of Total Income minus ₹10,000

₹20,001 – and above ₹3,000 + 30% (Total income minus ₹20,000)

Special Rate of Taxes

Section Income Tax-rate

115BB Winning from (i) any lottery; or (ii) crossword puzzle; or (iii) race including

horse race; or (iv) card game and other game of any sort; or (v) gambling or

betting of any form.

30%

115BBE Unexplained money, investments, etc… [u/s 68, 69A, 69B, 69C and 69D]

plus Surcharge 25% + Health and Education cess 4%

60%

Section 2(10): Average rate of tax [𝑇𝑎𝑥 𝑜𝑛 𝑇𝑜𝑡𝑎𝑙 𝐼𝑛𝑐𝑜𝑚𝑒

𝑇𝑜𝑡𝑎𝑙 𝐼𝑛𝑐𝑜𝑚𝑒]

Section 2(26C): Maximum Marginal Tax Rate =

𝐵𝑎𝑠𝑖𝑐 𝑡𝑎𝑥 + 𝑠𝑢𝑟𝑐ℎ𝑎𝑟𝑔𝑒 𝑜𝑛 𝑡𝑎𝑥 + 𝐻𝐸𝐶 𝑜𝑛 𝑡𝑎𝑥 & 𝑎𝑛𝑑 𝑠𝑢𝑟𝑐ℎ𝑎𝑟𝑔𝑒

Income Tax 14

𝐈𝐧𝐝𝐢𝐯𝐢𝐝𝐮𝐚𝐥, 𝐀𝐎𝐏 & 𝐁𝐎𝐈 = 30% × 115% × 104% = 35.88%)

𝐒𝐞𝐜𝐭𝐢𝐨𝐧 𝟏𝟏𝟓𝐁𝐁𝐄 = 60% × 125% × 104% = 78%)

Profits and Gains from Business or Profession 15

3. RESIDENTIAL STATUS & SCOPE OF TOTAL INCOME

Section 6(1): Basic Conditions for Resident [individual]

1. Stay in India in the PY ≥ 182 days or

2. Stay in India in the PY ≥ 60 days and Stay in India 4 PPY ≥ 365 days

Exceptions: the second condition is not applicable for

1 Indian citizen → Foreign Member of the crew of an Indian ship# /

Employment outside India

2 Indian citizen or Person of Indian Origin1 → India Engaged outside India in employment

/ business / profession / vocation

Section 6(1A): Deemed resident: if Total Income other than foreign income > ₹15 lakhs

And if he is not liable to pay tax in any other country

Period of stay: 120 days or more but less than 182 days in India in the PY

[not applicable for an individual who is resident India in the PY as per S.6(1).]

# Determination of period of stay in India for and Indian citizen, being a crew member:

Period to be excluded:

Period commencing from the date entered into the Continuous Discharge Certificate in respect of

joining the ship by the said individual for the eligible voyage and

Period ending on the date entered in to the Continuous Discharge Certificate in respect of signing off

by that individual from the ship in respect of such voyage.

Note:

a. Continuous Discharge Certificate: as per the Merchant Shipping (Continuous Discharge

Certificate-cum Seafarer’s Identity Document) Rules, 2001 made under the Merchant Shipping Act,

1958)

b. Eligible voyage: a voyage undertaken by a ship engaged in the carriage of passengers or freight in

international traffic where-

i. For the voyage having originated from any port in India, has as its destination any port outside

India; and

ii. For the voyage having originated from any port outside India, has as its destination any port

in India

Question: Mr. Anand is an Indian citizen and a member of the crew of a Singapore bound Indian ship

engaged in carriage of passengers in international traffic departing from Chennai port on 6th June, 2020.

From the following details for the PY 2020-21, determine the residential status of Mr. Anand for AY

2021-22, assuming that his stay in India in the last 4 PPY is 400 days.

1 Explanation to section 115C(e): to a person is said to be of Indian origin if he or either of his parents or either

of his grandparents were born in undivided India.

Income Tax 16

Particulars Date

Date entered into the Continuous Discharge Certificate

in respect of joining the ship by Mr. Anand

6th June, 2020

Date entered into the Continuous Discharge Certificate

in respect of signing off the ship by Mr. Anand1

9th December, 2020

Section 6(6): Not Ordinarily Resident one who satisfies any one of the conditions mentioned below.

Applicable: Individual

1. Non-Resident in India: 9 out of 10 PPYs. and

2. Stay in India in the 7 PPY ≤ 729

3. If such individual is an Indian citizen or person of Indian origin

his stay 120 days or more but less than 182 days in India in the PY and

Total income other than foreign income < ₹15 lakhs

4. Deemed resident u/s 6(1A) [Deemed resident will always be resident but not ordinarily resident]

Question: Brett Lee, an Australian cricket player visits for 100 days in every financial year. This has

been his practice for the past 10 FYs.

a. Find out his residential status for the AY 2021-222

b. Would your answer change if the above facts relate to Srinath, an Indian citizen who resides in

Australia and represents the Australian cricket team?3

c. What would be your answer if Srinath had visited India for 120 days instead of 100 days every year,

including PY 2020-21?4

Question: Mr. B, a Canadian citizen, comes to India for the first time during the PY 2016-17. During the

financial years 2016-17, 2017-18, 2018-19, 2019-20 and 2020-21, he was in India for 55 days, 60 days, 90

days, 150 days and 70 days respectively. Determine his residential status for the AY 2021-22.5

Section 6(2): Basic Conditions for Resident [HUF / Firm / AOP]

Section 6(4): Basic Conditions for Resident [every other person (BOI, LA, AJP)]

Place of control Status

1 wholly or partly situated in India Resident

2 wholly situated in outside India Non-resident

Additional Conditions u/s. 6(6) for ROR / RNOR – is applicable only for HUF (Karta’s stay)

1 NR: 178 days stayed in India in the PY < 182 days | 365 – [06.06.2020 to 09.12.2020] 2 RNOR: as stay in the PY > 60 days + stay in 4 PPYs > 365 days & stays ≤ 729 days in 7 PPYs [non citizen] 3 NR: as he is being Indian citizen 4 RNOR: if his income other than foreign income > ₹15 lakhs 5 NR: Stay in the PY > 60 days but stay in 4 PPYs < 365 days

Profits and Gains from Business or Profession 17

Section 6(6): Additional Conditions for Resident and Ordinarily Resident / Not [ROR / RNOR]

Applicable: HUF

1. Resident in India: at least 2 times out of 10 PPYs. and

2. Stay in India in the 7 PPY ≥ 730

ROR: Satisfies ONE of the basic conditions and BOTH the additional condition.

RNOR: Satisfies ONE of the basic conditions but does NOT satisfy BOTH the additional conditions.

Non-Resident: does not satisfy any of the basic conditions

{CA inter J09, 6 marks}

Question: The business of a HUF is transacted from Australia and all the policy decisions are taken

there. Mr. E, the Karta of the HUF, who was born in Kolkata, visits India during the PY 2020-21 after 15

years. He comes to India on 1.4.2020 and leaves for Australia on 1.12.2020. Determine the residential

status of Mr. E and the HUF for AY 2021-22.1

Section 6(3): Condition for residential status of company

Situation Status

1 Indian Company Resident

2 Foreign Company

Place of control wholly situated in India

[Place of Effective Management (POEM)]

Resident

Place of control wholly or partly situated outside India Non-resident

Note: Control and Management means de-facto control and management and not merely the right to

control or manage. Control and Management are usually situated at a place where the head and brain

of the directing power are situated.

In the case of a company, the control and management are presumed to be situated

Where head and brain of the company is situated.

Where the meeting of the board of directors are held.

True or false with reasons: A non-Indian company is treated as resident, only if the control and

management of its affairs is situated wholly in India during the previous year.2

{CA inter N06, 2 marks}

Section 6(5): Residential status determined for PY is common for all source of income in that PY

Section 5: Residence and Scope of Total Income S.5 [T – Taxable & NT – Not Taxable]

ROR RNOR NR

1 Mr.E is RNOR as his stay in the PY > 180 days | HUF is NR as the control is from Australia 2 True

Income Tax 18

Indian Income T T T

Foreign Income

1. If it is business income and the business is controlled

wholly or partly from India /

If it is income from profession which is set up in India

T T NT

2. Others T NT NT

Income received / deemed to be received / accrued / deemed to accrue [ALL / ANY] in India

then Indian Income else Foreign income

Question: Write a note on “Income accruing” and “Income due”. Can an income which has been taxed

on accrual basis be assessed again on receipt basis?1

{CA inter M05, 6 marks}

Section 7: The following incomes shall be deemed to be received in the previous year:

1. Employer’s RPF contribution > 12% of salary / interest credited in RPF a/c > 9.5% p.a.

2. Unrecognized PF to recognized provident fund (employer’s contribution and interest thereon)

3. Central Government or other employer’s contribution to employee’s pension scheme u/s 80CCD

4. tax deducted at source

Section 9(1): Income deemed to accrue or arise in India

(i) Income from connection in India through or from

1. any business connection in India, or

2. any property in India, or

3. any asset or source of income in India, or

4. the transfer of a capital asset situated in India.

{CA inter N01, N04 & M08, 4, 6 & 6 marks}

(ii) Salary earned in India (services rendered in India)

(iii) Salary by Government to an Indian Citizen for services rendered outside India

(iv) Dividend paid by an Indian company to outside India

(v) Interest / royalty / fee for technical services payable by

1. Government

2. Resident person provided borrowing is not used outside India for

business or profession

earning any income from any source

3. Non resident person provided borrowing is used in India for

business or profession

earning any income from any source

(vi) Deemed Receipts of Gift: When

1. A non-resident or foreign company receives any gift referred u/h IFOS

2. From a resident person

1 Income accruing – right to receive | income due – right to enforce | taxable once

Profits and Gains from Business or Profession 19

3. Outside India

Section 9(2): Pensions payable outside India to certain categories of Government employees and judges

who permanently reside outside India, shall not be deemed to arise or accrue in India.

Explanation 2 to section 9(1): Examples for business connections

1. Maintaining a branch office in India

2. Appointing an agent in India

3. Erecting a factory in India where the raw material purchased locally is worked into form suitable

for export abroad;

4. Forming a local subsidiary company

5. Having financial association between a resident and non-resident company, etc.

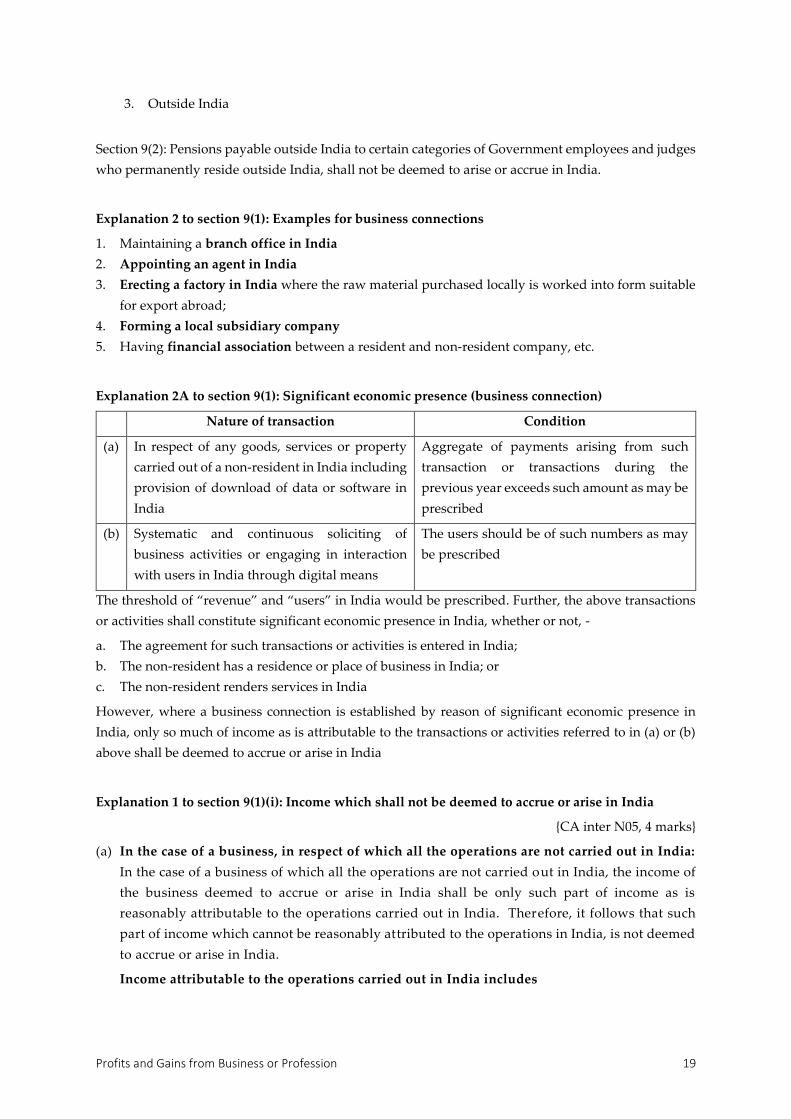

Explanation 2A to section 9(1): Significant economic presence (business connection)

Nature of transaction Condition

(a) In respect of any goods, services or property

carried out of a non-resident in India including

provision of download of data or software in

India

Aggregate of payments arising from such

transaction or transactions during the

previous year exceeds such amount as may be

prescribed

(b) Systematic and continuous soliciting of

business activities or engaging in interaction

with users in India through digital means

The users should be of such numbers as may

be prescribed

The threshold of “revenue” and “users” in India would be prescribed. Further, the above transactions

or activities shall constitute significant economic presence in India, whether or not, -

a. The agreement for such transactions or activities is entered in India;

b. The non-resident has a residence or place of business in India; or

c. The non-resident renders services in India

However, where a business connection is established by reason of significant economic presence in

India, only so much of income as is attributable to the transactions or activities referred to in (a) or (b)

above shall be deemed to accrue or arise in India

Explanation 1 to section 9(1)(i): Income which shall not be deemed to accrue or arise in India

{CA inter N05, 4 marks}

(a) In the case of a business, in respect of which all the operations are not carried out in India:

In the case of a business of which all the operations are not carried out in India, the income of

the business deemed to accrue or arise in India shall be only such part of income as is

reasonably attributable to the operations carried out in India. Therefore, it follows that such

part of income which cannot be reasonably attributed to the operations in India, is not deemed

to accrue or arise in India.

Income attributable to the operations carried out in India includes

Income Tax 20

i. Income from advertisement, targeting customers residing in India or accessing advt. thro

[Internet Protocol Address] IPA located in India

ii. Income from sale of data collected from persons residing in India or using IPS located in

India

iii. Income from sale of goods and services using data collected from persons residing in India

or using IPA located in India

(b) Purchase of goods by NR in India for export

(c) Collection of news and views in India by NR for transmission out of India

(d) Shooting of cinematograph films in India: In the case of a non-resident, no income shall be

deemed to accrue or arise in India through or from operations which are confined to the

shooting of any cinematograph film in India, if such non-resident is –

a) an individual, who is not a citizen of India or

b) a firm which does not have any partner who is a citizen of India or who is resident in India;

or

c) a company which does not have any shareholder who is a citizen of India or who is resident

in India.

(e) Activities confined to display of rough diamonds in Special Notified Zone (SNZ): in the case

of a foreign company engaged in the business of mining of diamonds, no income shall be

deemed to accrue or arise in India to it through or from the activities which are confined to

display of uncut and un-assorted diamonds in any SNZ.

[Sec. 9A] Fund management activity: In the case of an “eligible investment fund”, the fund

management activity carried out through an “eligible fund manager” acting on behalf of such fund

shall not constitute business connection in India of the said fund.

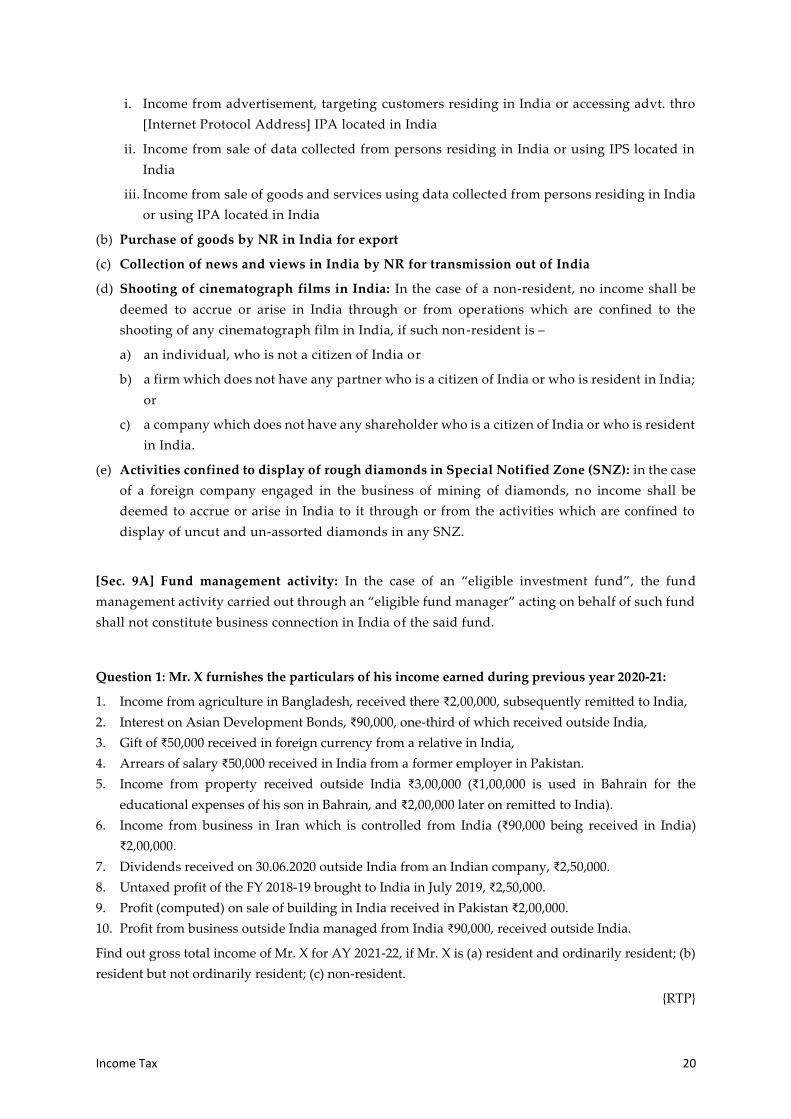

Question 1: Mr. X furnishes the particulars of his income earned during previous year 2020-21:

1. Income from agriculture in Bangladesh, received there ₹2,00,000, subsequently remitted to India,

2. Interest on Asian Development Bonds, ₹90,000, one-third of which received outside India,

3. Gift of ₹50,000 received in foreign currency from a relative in India,

4. Arrears of salary ₹50,000 received in India from a former employer in Pakistan.

5. Income from property received outside India ₹3,00,000 (₹1,00,000 is used in Bahrain for the

educational expenses of his son in Bahrain, and ₹2,00,000 later on remitted to India).

6. Income from business in Iran which is controlled from India (₹90,000 being received in India)

₹2,00,000.

7. Dividends received on 30.06.2020 outside India from an Indian company, ₹2,50,000.

8. Untaxed profit of the FY 2018-19 brought to India in July 2019, ₹2,50,000.

9. Profit (computed) on sale of building in India received in Pakistan ₹2,00,000.

10. Profit from business outside India managed from India ₹90,000, received outside India.

Find out gross total income of Mr. X for AY 2021-22, if Mr. X is (a) resident and ordinarily resident; (b)

resident but not ordinarily resident; (c) non-resident.

{RTP}

Profits and Gains from Business or Profession 21

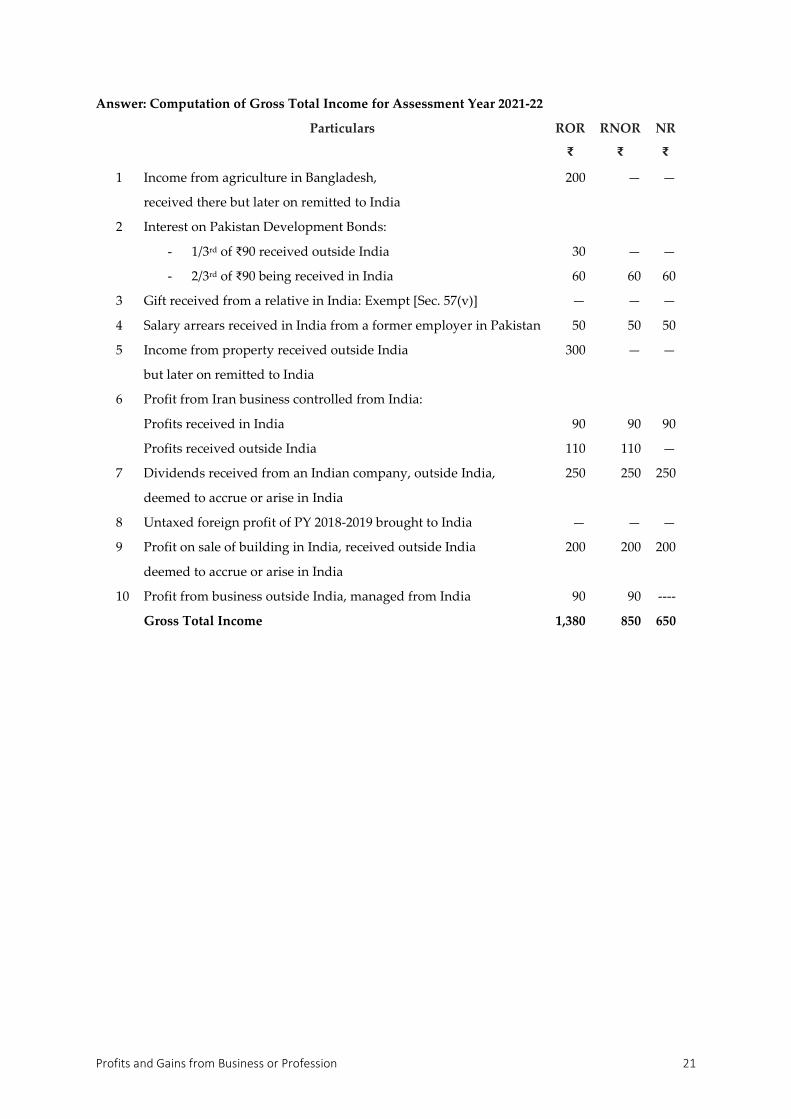

Answer: Computation of Gross Total Income for Assessment Year 2021-22

Particulars ROR RNOR NR

₹ ₹ ₹

1 Income from agriculture in Bangladesh,

received there but later on remitted to India

200 — —

2 Interest on Pakistan Development Bonds:

- 1/3rd of ₹90 received outside India 30 — —

- 2/3rd of ₹90 being received in India 60 60 60

3 Gift received from a relative in India: Exempt [Sec. 57(v)] — — —

4 Salary arrears received in India from a former employer in Pakistan 50 50 50

5 Income from property received outside India

but later on remitted to India

300 — —

6 Profit from Iran business controlled from India:

Profits received in India 90 90 90

Profits received outside India 110 110 —

7 Dividends received from an Indian company, outside India,

deemed to accrue or arise in India

250 250 250

8 Untaxed foreign profit of PY 2018-2019 brought to India — — —

9 Profit on sale of building in India, received outside India

deemed to accrue or arise in India

200 200 200

10 Profit from business outside India, managed from India 90 90 ----

Gross Total Income 1,380 850 650

Income Tax 22

4. AGRICULTURAL INCOME

EXEMPTION [S. 10(1)]: AGRICULTURAL INCOME

1. Agricultural Income and non-agricultural income

2. Complete exemption of agricultural income

3. Apportionment of income between business income and agricultural income

4. Partial integration of agricultural income with non-agricultural income and tax calculation

Section 2(1A): Agricultural Income

1. any rent or revenue derived from land / building

which is situated in India and

is used for agricultural purposes;

in case of building: should be immediate vicinity of the land | dwelling house | store building |

out building (in connection with land)

2. Agricultural purpose means

a. Performance by a cultivator

b. Receiver of rent in kind

i. Any process ordinarily employed by a cultivator

ii. To render the produce fit to be taken to market

c. Sale of agricultural produce in the market

d. Income derived from saplings or seedlings grown in a nursery {deemed agricultural income}

3. NOT agricultural income: Letting of land for residential purpose | business or profession

Non-agricultural income: Income from

1. self-grown grass, trees or bamboos

2. fisheries

3. brick making

4. company engaged in agriculture as dividend

5. dairy farm, poultry farming etc.

6. interest on arrears of rent of agricultural land.

7. land used for storing agricultural produce.

8. agricultural farm for manager remuneration

9. harvest crop on purchased land

10. mining royalties

11. markets

12. stone quarries.

Scheme of partial integration of agricultural income

Nature of Business Agricultural

Income

Non-Agricultural

Income

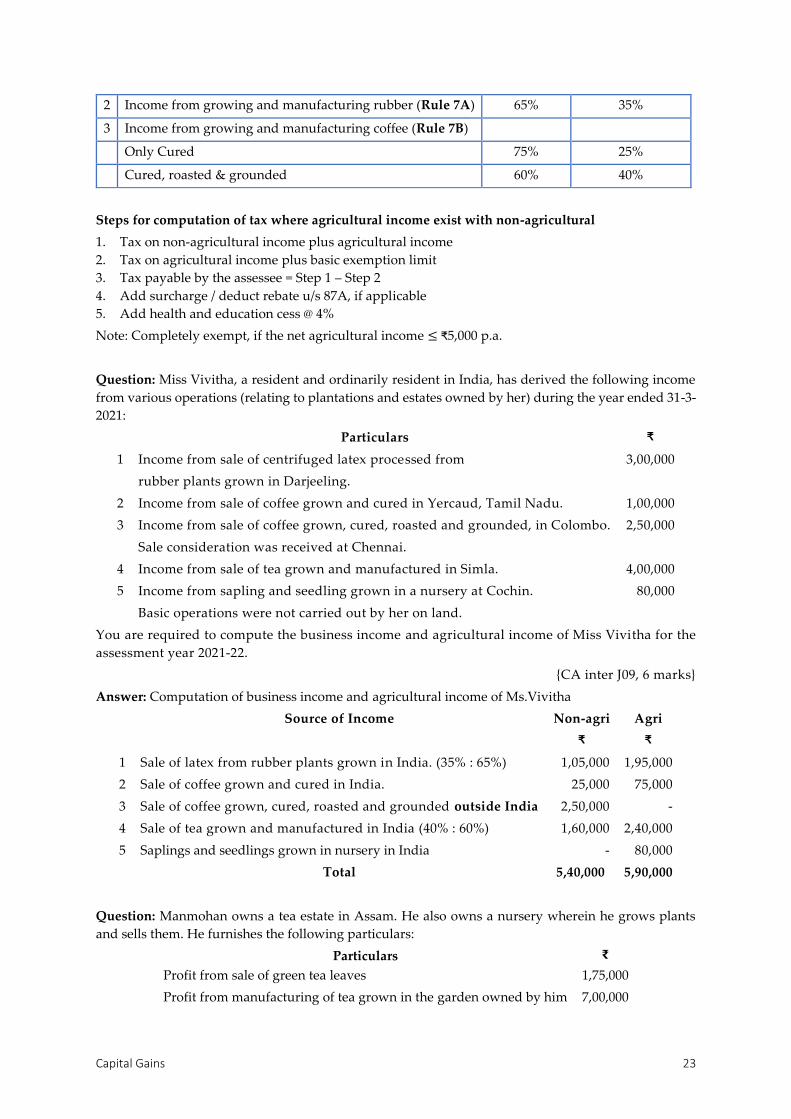

1 Income from growing and manufacturing tea (Rule 8) 60% 40%

Capital Gains 23

2 Income from growing and manufacturing rubber (Rule 7A) 65% 35%

3 Income from growing and manufacturing coffee (Rule 7B)

Only Cured 75% 25%

Cured, roasted & grounded 60% 40%

Steps for computation of tax where agricultural income exist with non-agricultural

1. Tax on non-agricultural income plus agricultural income

2. Tax on agricultural income plus basic exemption limit

3. Tax payable by the assessee = Step 1 – Step 2

4. Add surcharge / deduct rebate u/s 87A, if applicable

5. Add health and education cess @ 4%

Note: Completely exempt, if the net agricultural income ≤ ₹5,000 p.a.

Question: Miss Vivitha, a resident and ordinarily resident in India, has derived the following income

from various operations (relating to plantations and estates owned by her) during the year ended 31-3-

2021:

Particulars ₹

1 Income from sale of centrifuged latex processed from

rubber plants grown in Darjeeling.

3,00,000

2 Income from sale of coffee grown and cured in Yercaud, Tamil Nadu. 1,00,000

3 Income from sale of coffee grown, cured, roasted and grounded, in Colombo.

Sale consideration was received at Chennai.

2,50,000

4 Income from sale of tea grown and manufactured in Simla. 4,00,000

5 Income from sapling and seedling grown in a nursery at Cochin.

Basic operations were not carried out by her on land.

80,000

You are required to compute the business income and agricultural income of Miss Vivitha for the

assessment year 2021-22.

{CA inter J09, 6 marks}

Answer: Computation of business income and agricultural income of Ms.Vivitha

Source of Income Non-agri Agri

₹ ₹

1 Sale of latex from rubber plants grown in India. (35% : 65%) 1,05,000 1,95,000

2 Sale of coffee grown and cured in India. 25,000 75,000

3 Sale of coffee grown, cured, roasted and grounded outside India 2,50,000 -

4 Sale of tea grown and manufactured in India (40% : 60%) 1,60,000 2,40,000

5 Saplings and seedlings grown in nursery in India - 80,000

Total 5,40,000 5,90,000

Question: Manmohan owns a tea estate in Assam. He also owns a nursery wherein he grows plants

and sells them. He furnishes the following particulars:

Particulars ₹

Profit from sale of green tea leaves 1,75,000

Profit from manufacturing of tea grown in the garden owned by him 7,00,000

Income Tax 24

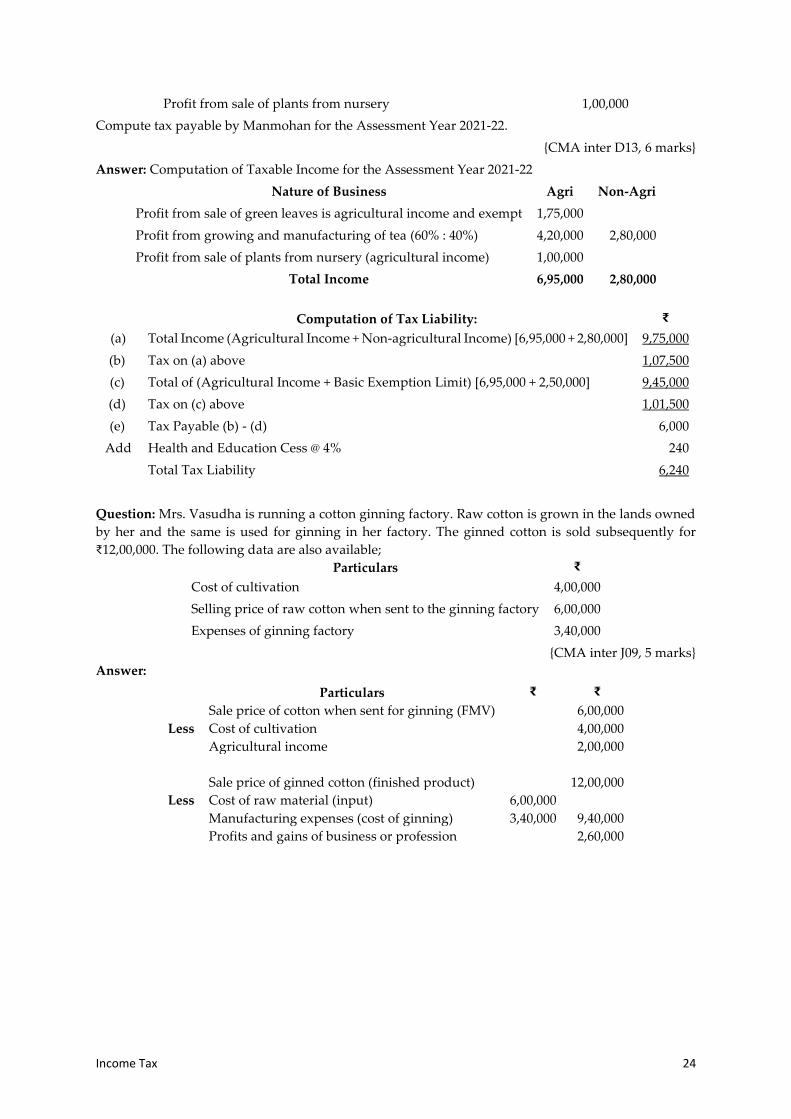

Profit from sale of plants from nursery 1,00,000

Compute tax payable by Manmohan for the Assessment Year 2021-22.

{CMA inter D13, 6 marks}

Answer: Computation of Taxable Income for the Assessment Year 2021-22

Nature of Business Agri Non-Agri

Profit from sale of green leaves is agricultural income and exempt 1,75,000

Profit from growing and manufacturing of tea (60% : 40%) 4,20,000 2,80,000

Profit from sale of plants from nursery (agricultural income) 1,00,000

Total Income 6,95,000 2,80,000

Computation of Tax Liability: ₹

(a) Total Income (Agricultural Income + Non-agricultural Income) [6,95,000 + 2,80,000] 9,75,000

(b) Tax on (a) above 1,07,500

(c) Total of (Agricultural Income + Basic Exemption Limit) [6,95,000 + 2,50,000] 9,45,000

(d) Tax on (c) above 1,01,500

(e) Tax Payable (b) - (d) 6,000

Add Health and Education Cess @ 4% 240

Total Tax Liability 6,240

Question: Mrs. Vasudha is running a cotton ginning factory. Raw cotton is grown in the lands owned

by her and the same is used for ginning in her factory. The ginned cotton is sold subsequently for

₹12,00,000. The following data are also available;

Particulars ₹

Cost of cultivation 4,00,000

Selling price of raw cotton when sent to the ginning factory 6,00,000

Expenses of ginning factory 3,40,000

{CMA inter J09, 5 marks}

Answer:

Particulars ₹ ₹

Sale price of cotton when sent for ginning (FMV) 6,00,000

Less Cost of cultivation 4,00,000

Agricultural income 2,00,000

Sale price of ginned cotton (finished product) 12,00,000

Less Cost of raw material (input) 6,00,000

Manufacturing expenses (cost of ginning) 3,40,000 9,40,000

Profits and gains of business or profession 2,60,000

Income from Other Sources 25

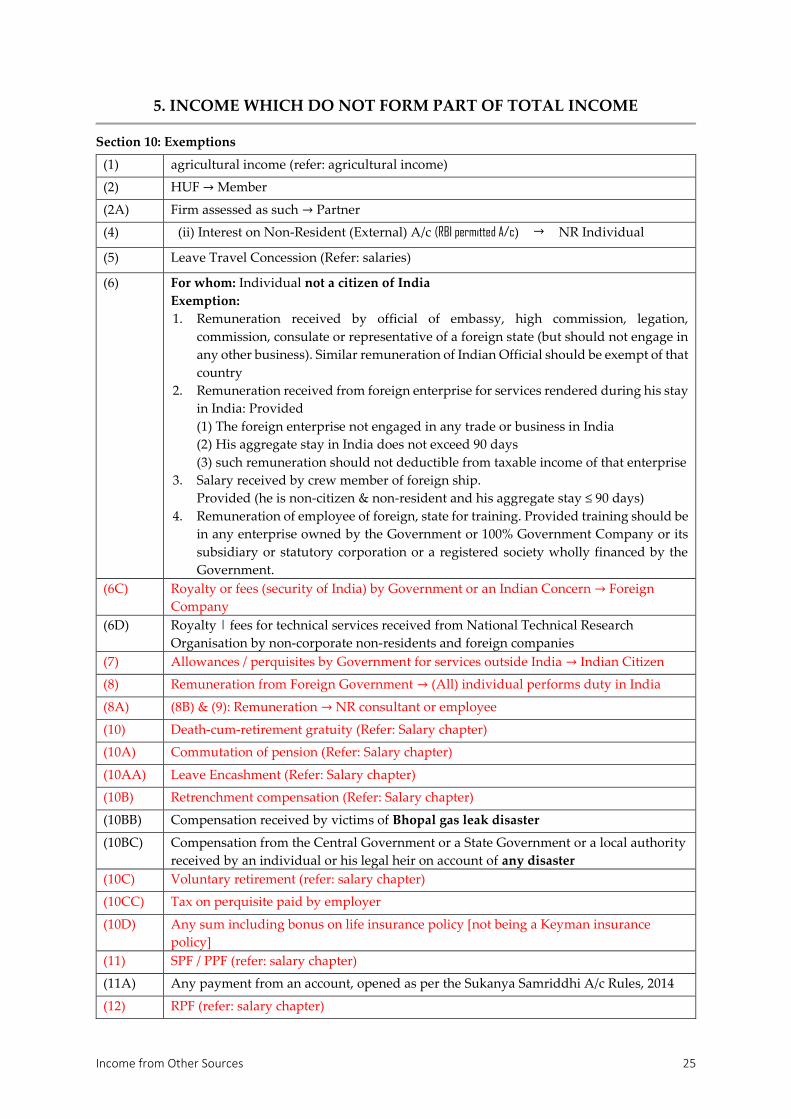

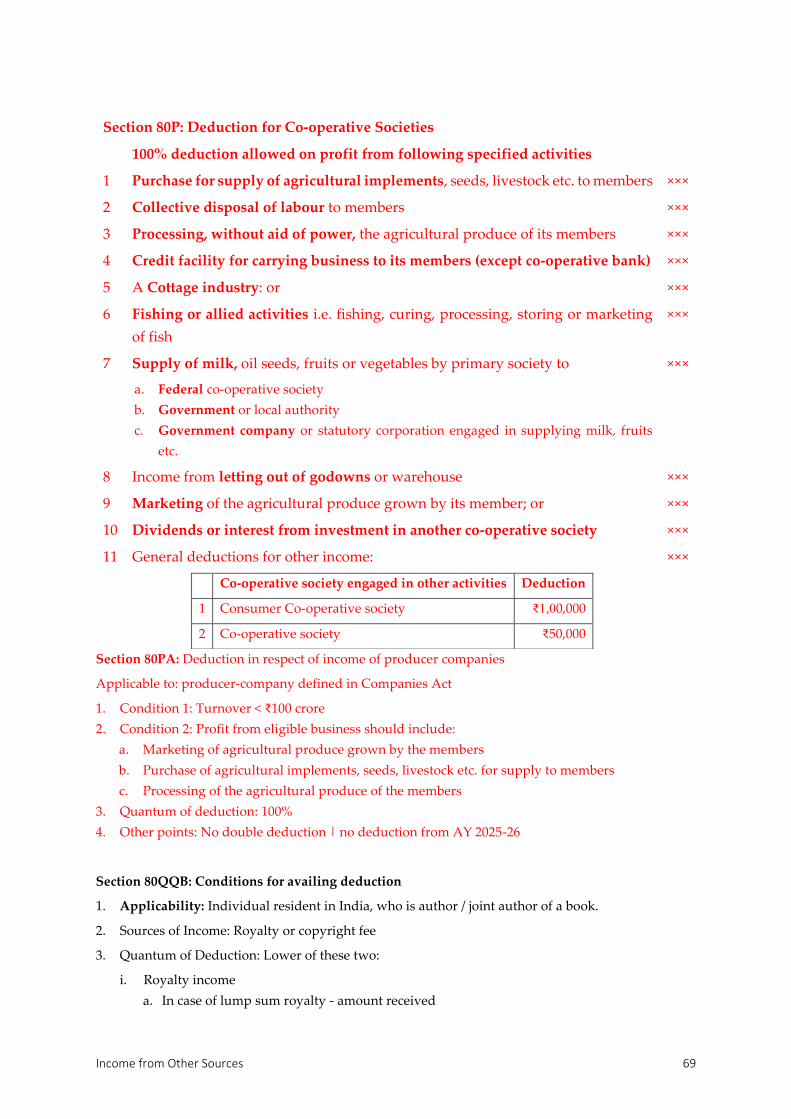

5. INCOME WHICH DO NOT FORM PART OF TOTAL INCOME

Section 10: Exemptions

(1) agricultural income (refer: agricultural income)

(2) HUF → Member

(2A) Firm assessed as such → Partner

(4) (ii) Interest on Non-Resident (External) A/c (RBI permitted A/c) → NR Individual

(5) Leave Travel Concession (Refer: salaries)

(6) For whom: Individual not a citizen of India

Exemption:

1. Remuneration received by official of embassy, high commission, legation,

commission, consulate or representative of a foreign state (but should not engage in

any other business). Similar remuneration of Indian Official should be exempt of that

country

2. Remuneration received from foreign enterprise for services rendered during his stay

in India: Provided

(1) The foreign enterprise not engaged in any trade or business in India

(2) His aggregate stay in India does not exceed 90 days

(3) such remuneration should not deductible from taxable income of that enterprise

3. Salary received by crew member of foreign ship.

Provided (he is non-citizen & non-resident and his aggregate stay ≤ 90 days)

4. Remuneration of employee of foreign, state for training. Provided training should be

in any enterprise owned by the Government or 100% Government Company or its

subsidiary or statutory corporation or a registered society wholly financed by the

Government.

(6C) Royalty or fees (security of India) by Government or an Indian Concern → Foreign

Company

(6D) Royalty | fees for technical services received from National Technical Research

Organisation by non-corporate non-residents and foreign companies

(7) Allowances / perquisites by Government for services outside India → Indian Citizen

(8) Remuneration from Foreign Government → (All) individual performs duty in India

(8A) (8B) & (9): Remuneration → NR consultant or employee

(10) Death-cum-retirement gratuity (Refer: Salary chapter)

(10A) Commutation of pension (Refer: Salary chapter)

(10AA) Leave Encashment (Refer: Salary chapter)

(10B) Retrenchment compensation (Refer: Salary chapter)

(10BB) Compensation received by victims of Bhopal gas leak disaster

(10BC) Compensation from the Central Government or a State Government or a local authority

received by an individual or his legal heir on account of any disaster

(10C) Voluntary retirement (refer: salary chapter)

(10CC) Tax on perquisite paid by employer

(10D) Any sum including bonus on life insurance policy [not being a Keyman insurance

policy]

(11) SPF / PPF (refer: salary chapter)

(11A) Any payment from an account, opened as per the Sukanya Samriddhi A/c Rules, 2014

(12) RPF (refer: salary chapter)

Income Tax 26

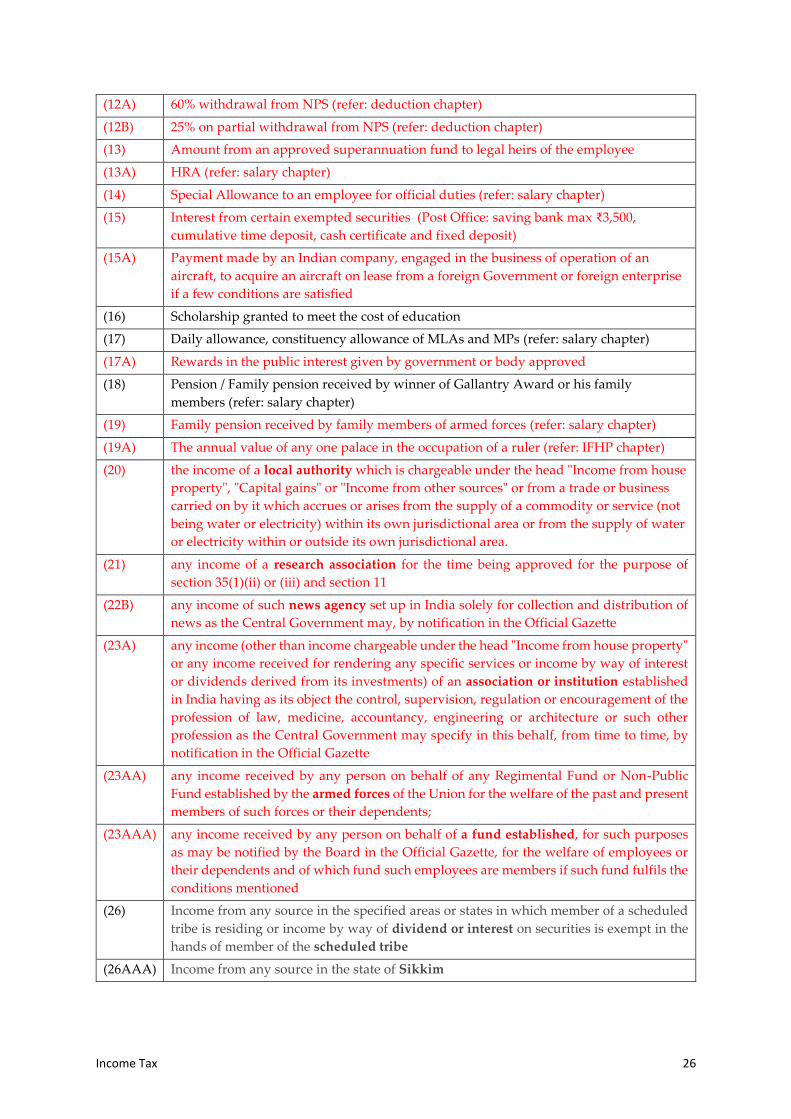

(12A) 60% withdrawal from NPS (refer: deduction chapter)

(12B) 25% on partial withdrawal from NPS (refer: deduction chapter)

(13) Amount from an approved superannuation fund to legal heirs of the employee

(13A) HRA (refer: salary chapter)

(14) Special Allowance to an employee for official duties (refer: salary chapter)

(15) Interest from certain exempted securities (Post Office: saving bank max ₹3,500,

cumulative time deposit, cash certificate and fixed deposit)

(15A) Payment made by an Indian company, engaged in the business of operation of an

aircraft, to acquire an aircraft on lease from a foreign Government or foreign enterprise

if a few conditions are satisfied

(16) Scholarship granted to meet the cost of education

(17) Daily allowance, constituency allowance of MLAs and MPs (refer: salary chapter)

(17A) Rewards in the public interest given by government or body approved

(18) Pension / Family pension received by winner of Gallantry Award or his family

members (refer: salary chapter)

(19) Family pension received by family members of armed forces (refer: salary chapter)

(19A) The annual value of any one palace in the occupation of a ruler (refer: IFHP chapter)

(20) the income of a local authority which is chargeable under the head "Income from house

property", "Capital gains" or "Income from other sources" or from a trade or business

carried on by it which accrues or arises from the supply of a commodity or service (not

being water or electricity) within its own jurisdictional area or from the supply of water

or electricity within or outside its own jurisdictional area.

(21) any income of a research association for the time being approved for the purpose of

section 35(1)(ii) or (iii) and section 11

(22B) any income of such news agency set up in India solely for collection and distribution of

news as the Central Government may, by notification in the Official Gazette

(23A) any income (other than income chargeable under the head "Income from house property"

or any income received for rendering any specific services or income by way of interest

or dividends derived from its investments) of an association or institution established

in India having as its object the control, supervision, regulation or encouragement of the

profession of law, medicine, accountancy, engineering or architecture or such other

profession as the Central Government may specify in this behalf, from time to time, by

notification in the Official Gazette

(23AA) any income received by any person on behalf of any Regimental Fund or Non-Public

Fund established by the armed forces of the Union for the welfare of the past and present

members of such forces or their dependents;

(23AAA) any income received by any person on behalf of a fund established, for such purposes

as may be notified by the Board in the Official Gazette, for the welfare of employees or

their dependents and of which fund such employees are members if such fund fulfils the

conditions mentioned

(26) Income from any source in the specified areas or states in which member of a scheduled

tribe is residing or income by way of dividend or interest on securities is exempt in the

hands of member of the scheduled tribe

(26AAA) Income from any source in the state of Sikkim

Income from Other Sources 27

(30) The amount of any subsidy received by any assessee engaged in the business of growing

and manufacturing tea in India through or from the Tea Board will be wholly exempt

from tax

(31) Coffee board, Rubber board, Spices board

(35) Any income received in respect of units from the administrator of the specified

undertaking / specified company / mutual fund shall be exempt. However, income

arising from transfer of such units would not be exempt.

(45) Chairman / Member of UPSC (refer: salary chapter)

Difference between exemption and deduction

Exemption u/s 10 Deduction u/c VIA

1 Total income Not form part Forms part

2 Expenditure Not deductible Deductible

3 Basis Conditions Payment or conditions

{CMA inter J14, 3 marks}

State taxability: Sum received by individual as member of HUF out of the income of the family.

However it is not an amount received out of partition.1

{CMA inter D13, 6 marks}

State taxability: Salary received by ambassador of Russia who is posted in New Delhi.2

{CMA inter D13, 6 marks}

Choose the Best: Subject to fulfillment of other conditions, remuneration received by a foreign national

as an employee of a foreign enterprise for services rendered by him during his stay in India is exempted

from Income tax, if his stay in India does not exceed a period of 3

(a) 30 days (b) 60 days (c) 90 days (d) 120 days

{CMA inter J15, 1 mark}

Choose the Best: Commuted pension received by a State Government employee is exempt up to ₹____4

(a) 3 lakhs (b) 5 lakhs (c) 10 lakhs (d) Fully exempt

{CMA inter J14, 1 mark}

Question: Amount received from superannuation fund on resignation before specified age is exempt

from income tax. Comment5

{CMA inter D09, 2 marks}

1 Exempt U/s 10(2) 2 Exempt U/s 10(6) since he would not be a citizen of India 3 (c) 90 days 4 (d) Fully exempt 5 Exempt refer section 10(13)

Income Tax 28

True or false: Compensation on account of disaster received from local authority by an individual or

his / her legal heir is taxable.1

{CA inter N08, 2 marks}

Decide the taxability: Educational scholarship of ₹10,000 received from a charitable trust by a college

student.2

{CMA inter J13, 1 mark}

Section 10(21): conditions for exemption of income of Scientific Association

Approval: The Association / Institution should be approved u/s 35(1)(ii). (Form 3CF)

Application of Income: For its objects only. In case of accumulation, Notice is given

Investments: It should deposit its funds in the modes specified u/s 11(5)

Business Income: Exemption is not available for income under "Profits and Gains of

a. Such business is incidental to the attainment of Association's object and

b. Separate books of accounts are kept for such business.

Withdrawal of Approval - The approval u/s 35(1)(ii) can be withdrawn by an order, after giving a

reasonable opportunity of being heard, if the approving authority is satisfied that-

The association has not applied its income wholly and exclusively for its objects, or

The association has not invested or deposited its funds as per Section 11(5), or

The activities of the association are not genuine, or

The activities of the association are not being carried out in accordance with all or any of the

condition subject to which such association was approved.

Section 10(23BB): Exempted income of khadi and Village Industries Board exempt from tax

{CMA inter J12, 2 marks}

Income is exempt if

Any income by Khadi Village Industries Board

Established under a State or Provincial Act

For the development of khadi or village industries

Choose the Best: Income of securitization trust form the activity of securitization is3

(a) Exempt (b) Taxable of 20% (c) Taxable of 5% (d) Taxable at the regular rate

{CMA inter D14, 1 mark}

State taxability: Rental income earned by a registered trade union.4

{CMA inter J13, 1 mark}

Section 10(26AAA): Exempted incomes of Sikkimese individual are

1. any income source in the State of Sikkim or

1 False. Refer S. 10(10BC)

2 Exempt: S. 10(16) 3 (a) Exempt [S.10 (23DA)] 4 Rental income of registered trade union is exempt from tax. [Section 10(24)].

Income from Other Sources 29

2. by way of dividend or interest on securities

Note: Exemption is not available if Sikkimess woman who, on or after 01.04.2009, marries a non

Sikkimese individual.

{CA inter N10, 4 marks}

Question: Ms. Monisha, a Sikkimess woman, married Mr. Atul of Surat in June, 2008. She has income

from let out property at Sikkim being ₹10,000 per month. She is employed in a bank at Surat and her

salary income for the year ended 31.03.2020 was computed at ₹3,12,000. Determine her total income.

What would be your answer if she got married on 30th June, 2014?1

{CMA inter J12, 4 marks}

State the taxability: Co-operatives formed for promoting the interest of scheduled tribes.2

{CMA inter J13, 1 mark}

Section 10(48): The exemption in respect of income received by certain foreign companies from sale of

crude oil.

{CA inter N13, 4 marks}

Any Income received in India, in Indian Currency by a Foreign Company on account of sale of Crude

Oil, or any other goods or rendering of services, as notified by Central Government in this behalf, to

any person is exempt, based on following conditions:

1. Income is received as per approval of Central Government.

2. Having regard to the national interest, the Foreign Company and the agreement or arrangement

are notified by the Central Government in this behalf.

3. The Foreign Company is not engaged in any activity in India, other than the receipt of such income.

State the taxability: Giant Oil Inc, sold crude oil to HPCL a company in India. The sale was made within

India. Is the income arising from such sale liable to tax?3

{CMA inter D13, 1 mark}

Section 10AA: Exemption of income of Special Economic Zone (SEZ)

1. PGBP is exempted for newly established in SEZ

2. New establishment does not include the unit formed by splitting from existing unit

3. It can be formed by transfer of old plant and machinery to the extent of 20%.

4. Quantum of exemption: [15 years]

For first 5 AYs 100% of export profit

For next 5 AYs 50% of export profit

For next 5 AYs 50% of export profit (provided invested in SEZ Re-investment Reserve A/c)

Export profits = Profits of Business × Export Turnover

Total Turnover

5. Need to audit and file ROI with audit report

6. If a unit was located in any free trade zone or export processing zone which was converted to

special economic zone, the period of 10 years shall be considered from the assessment year relevant

to the previous year in which the unit began to manufacture, or produce or process such articles or

things in that free trade zone or export processing unit.

1 Married in June, 2008: salary income only is taxable. If married in June 2014: salary and IFHP are taxable. 2 is exempt [S.10(27)]. 3 Exempt (S. 10(48))

Income Tax 30

7. If a unit has already completed the period of 10 consecutive assessment years, no deduction is

allowed under this section.

8. In case of amalgamation or demerger, the deduction is availed by amalgamated company or

resulting company.

9. No deduction shall be allowed under section 80-I, 80-IA or 80-IB.

Section 10AA: What is the impact of availing deduction u/s 10AA of the income-tax Act, 1961?

{CMA inter D13, 5 marks}

Impact of availing deduction u/s 10AA:

1. Unabsorbed depreciation allowance or unabsorbed capital expenditure on Scientific research or

unabsorbed family planning expenditure or unabsorbed Loss under the head capital gains are not

allowed to be carried forward and set off against the income of Assessment years following the

period of deduction. However, this restriction is not applicable to losses in respect of other business.

2. Depreciation will be deemed to have been allowed and the WDV of the assets after exemption

period will be computed accordingly.

3. Deduction u/s 80IA and 80IB shall not be allowed.

4. Provisions of sec. 80IA(8) relating to inter unit transfer and provisions of sec. 80IA(10) relating to

showing excess profit from such unit apply to this undertaking.

Question: Nathan Aviation Ltd. is running two industrial undertakings, one in a SEZ (Unit S) and

another in a normal area (Unit N). The brief summarized details for the year ended 31.3.2021 are as

under:

₹ in lacs ₹ in lacs

S N

Domestic turnover 10 100

Export turnover 120 Nil

Gross profit 20 10

Less: Expenses and depreciation 7 6

Profits derived from the unit 13 4

The brought forward business loss pertaining to Unit N is ₹2 lacs. Briefly compute the business income

of the assessee.

{CA inter M11 & N13, 5 marks | CMA inter D11, 7 marks (modified)}

Answer: Computation of Business Income of Nathan Aviation Ltd.

Particulars ₹ in lakhs ₹ in lakhs

S N

Total profit derived from Units S & N 13 4

Less: Exemption under section 10AA1 12

1 4

Less: Brought Forward Business Loss 2

1 2

1 𝑃𝑟𝑜𝑓𝑖𝑡 𝑜𝑓 𝑈𝑛𝑖𝑡 𝑆 ×

𝐸𝑥𝑝𝑜𝑟𝑡 𝑡𝑢𝑟𝑛𝑜𝑣𝑒𝑟 𝑜𝑓 𝑢𝑛𝑖𝑡 𝑆

𝑇𝑜𝑡𝑎𝑙 𝑡𝑢𝑟𝑛𝑜𝑣𝑒𝑟 𝑜𝑓 𝑢𝑛𝑖𝑡 𝑆= 13 ×

120

130

Income from Other Sources 31

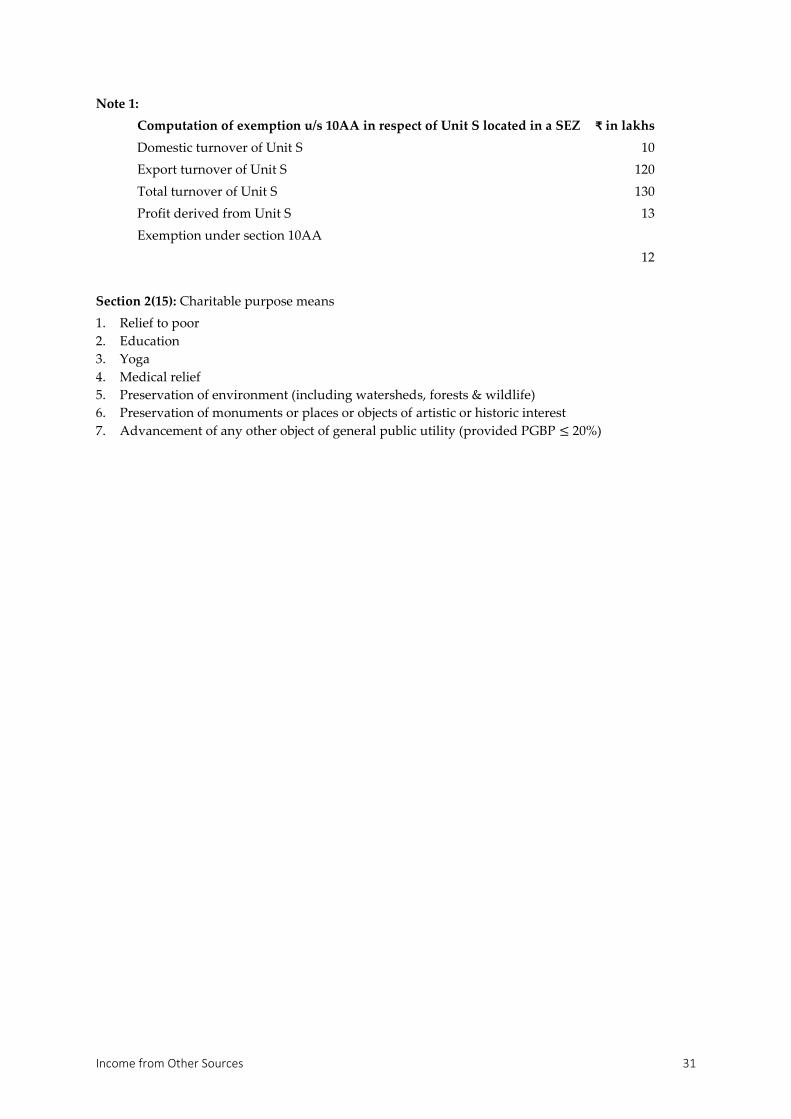

Note 1:

Computation of exemption u/s 10AA in respect of Unit S located in a SEZ ₹ in lakhs

Domestic turnover of Unit S 10

Export turnover of Unit S 120

Total turnover of Unit S 130

Profit derived from Unit S 13

Exemption under section 10AA

12

Section 2(15): Charitable purpose means

1. Relief to poor

2. Education

3. Yoga

4. Medical relief

5. Preservation of environment (including watersheds, forests & wildlife)

6. Preservation of monuments or places or objects of artistic or historic interest

7. Advancement of any other object of general public utility (provided PGBP ≤ 20%)

Income Tax 32

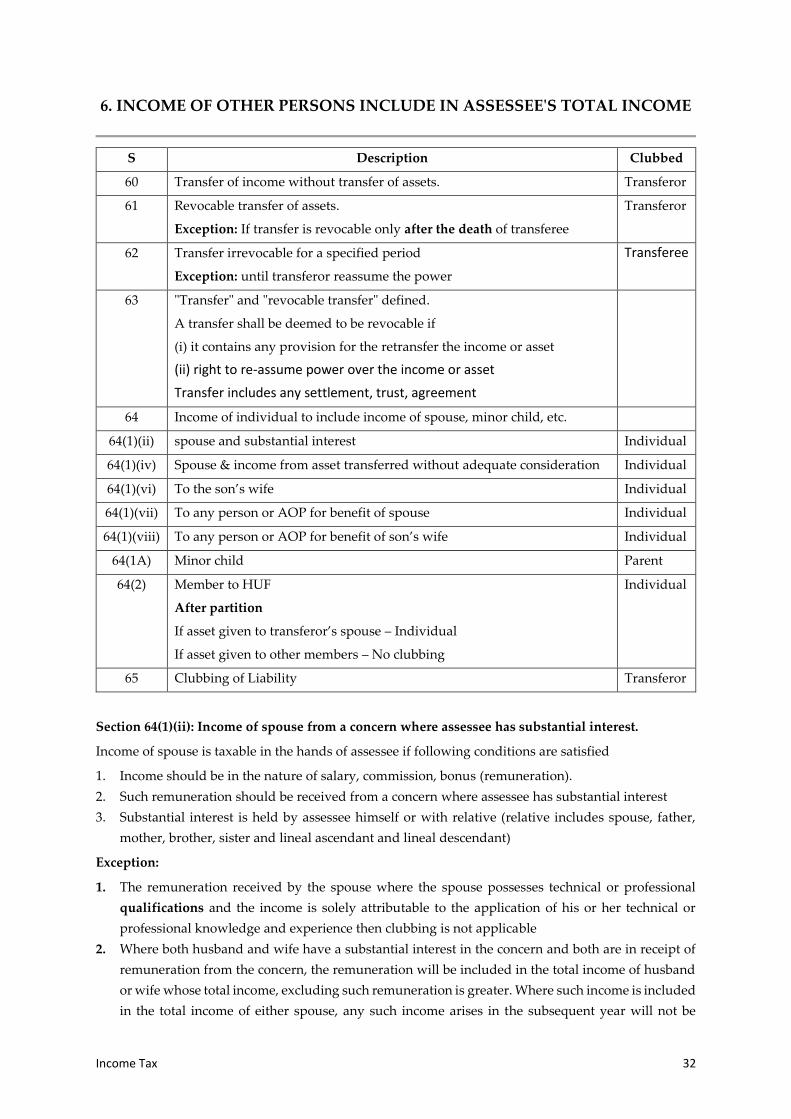

6. INCOME OF OTHER PERSONS INCLUDE IN ASSESSEE'S TOTAL INCOME

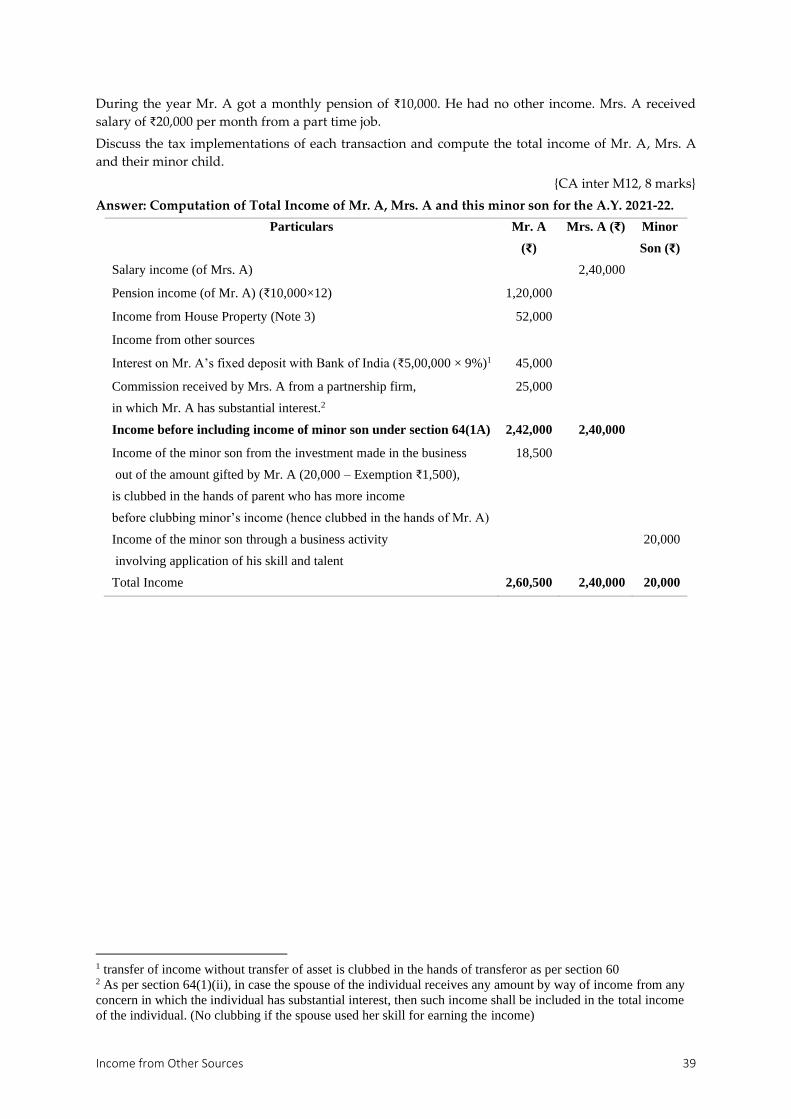

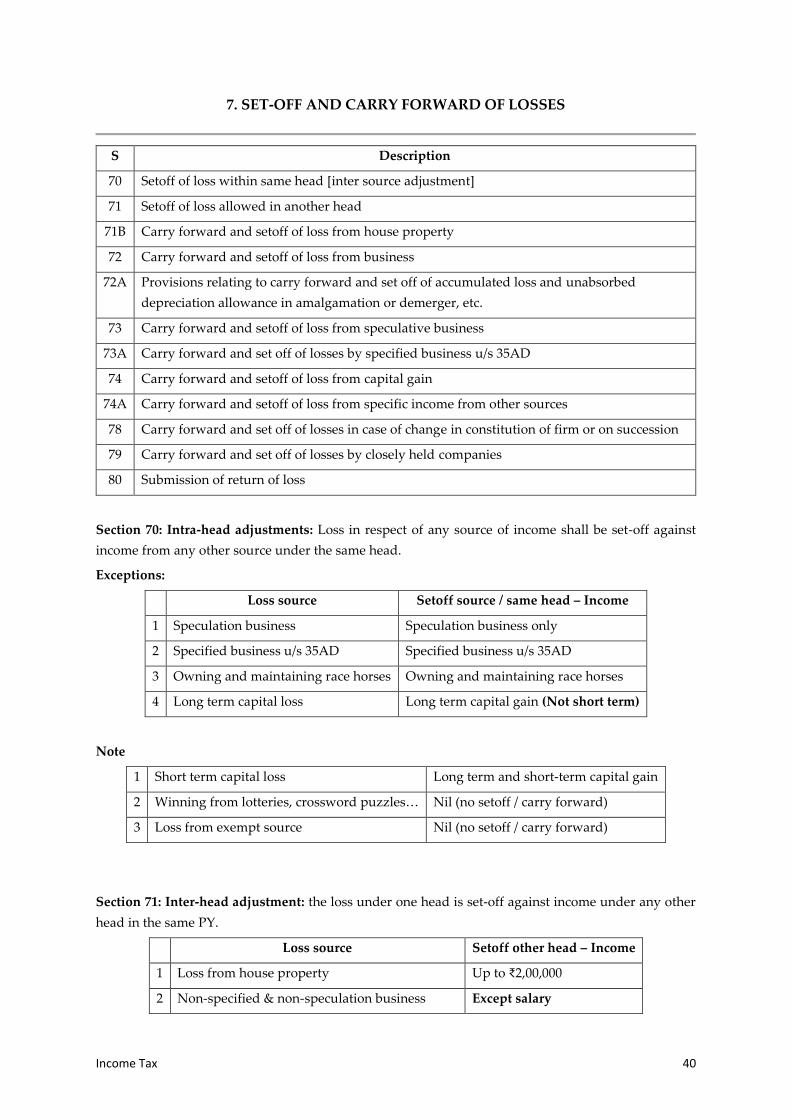

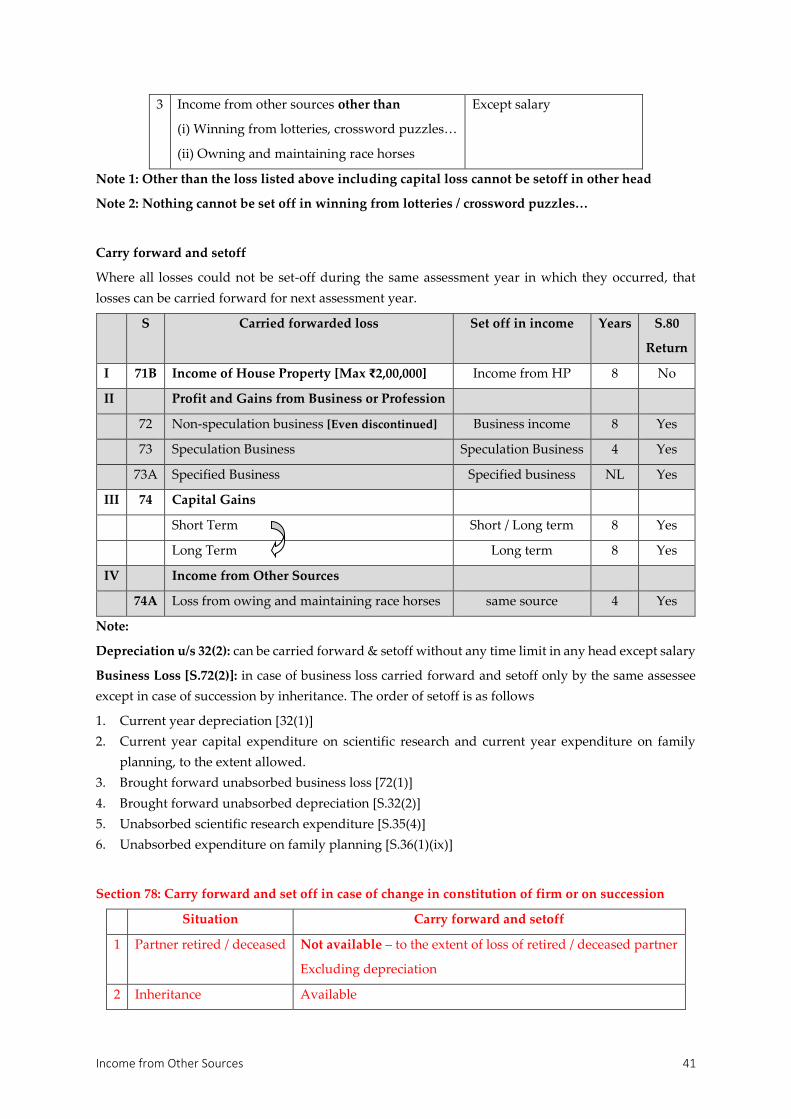

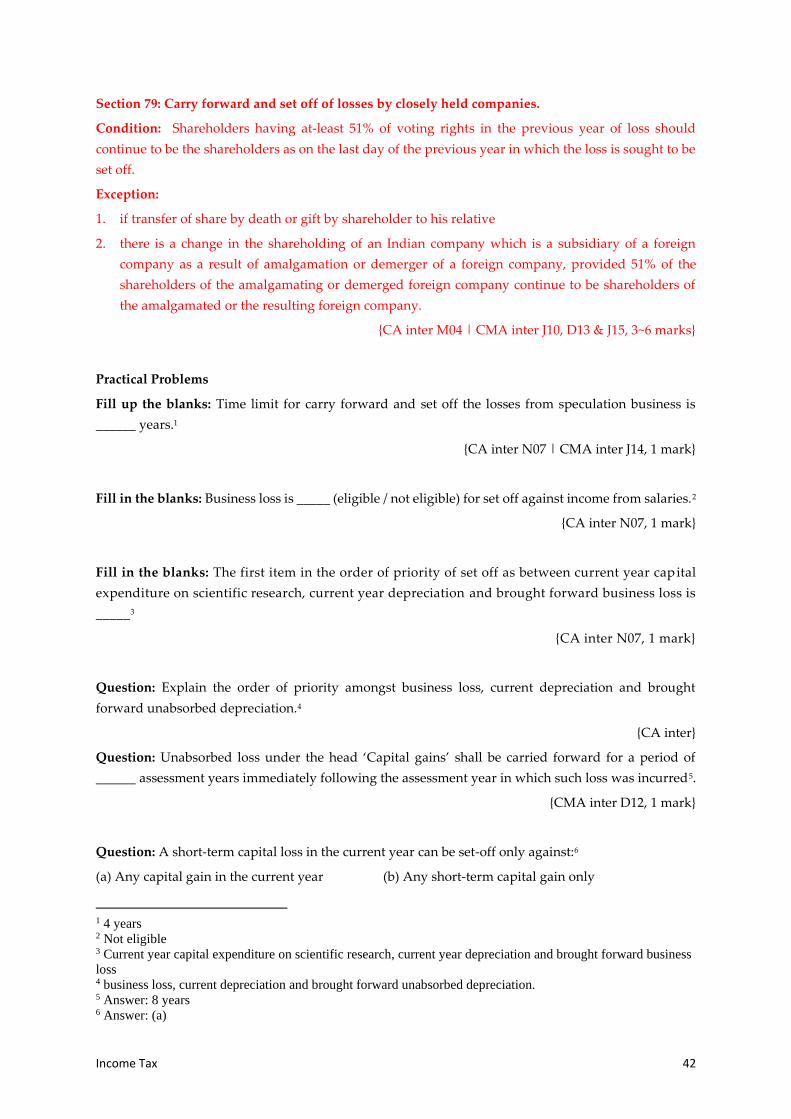

S Description Clubbed

60 Transfer of income without transfer of assets. Transferor

61 Revocable transfer of assets.

Exception: If transfer is revocable only after the death of transferee

Transferor

62 Transfer irrevocable for a specified period

Exception: until transferor reassume the power

Transferee

63 "Transfer" and "revocable transfer" defined.

A transfer shall be deemed to be revocable if

(i) it contains any provision for the retransfer the income or asset

(ii) right to re-assume power over the income or asset

Transfer includes any settlement, trust, agreement

64 Income of individual to include income of spouse, minor child, etc.

64(1)(ii) spouse and substantial interest Individual

64(1)(iv) Spouse & income from asset transferred without adequate consideration Individual

64(1)(vi) To the son’s wife Individual

64(1)(vii) To any person or AOP for benefit of spouse Individual

64(1)(viii) To any person or AOP for benefit of son’s wife Individual

64(1A) Minor child Parent

64(2) Member to HUF

After partition

If asset given to transferor’s spouse – Individual

If asset given to other members – No clubbing

Individual

65 Clubbing of Liability Transferor

Section 64(1)(ii): Income of spouse from a concern where assessee has substantial interest.

Income of spouse is taxable in the hands of assessee if following conditions are satisfied

1. Income should be in the nature of salary, commission, bonus (remuneration).

2. Such remuneration should be received from a concern where assessee has substantial interest

3. Substantial interest is held by assessee himself or with relative (relative includes spouse, father,

mother, brother, sister and lineal ascendant and lineal descendant)

Exception:

1. The remuneration received by the spouse where the spouse possesses technical or professional

qualifications and the income is solely attributable to the application of his or her technical or

professional knowledge and experience then clubbing is not applicable

2. Where both husband and wife have a substantial interest in the concern and both are in receipt of

remuneration from the concern, the remuneration will be included in the total income of husband

or wife whose total income, excluding such remuneration is greater. Where such income is included

in the total income of either spouse, any such income arises in the subsequent year will not be

Income from Other Sources 33

included in the total income of the other spouse unless the Assessing Officer is satisfied, after giving

that spouse an opportunity of being heard, that is necessary to do so.

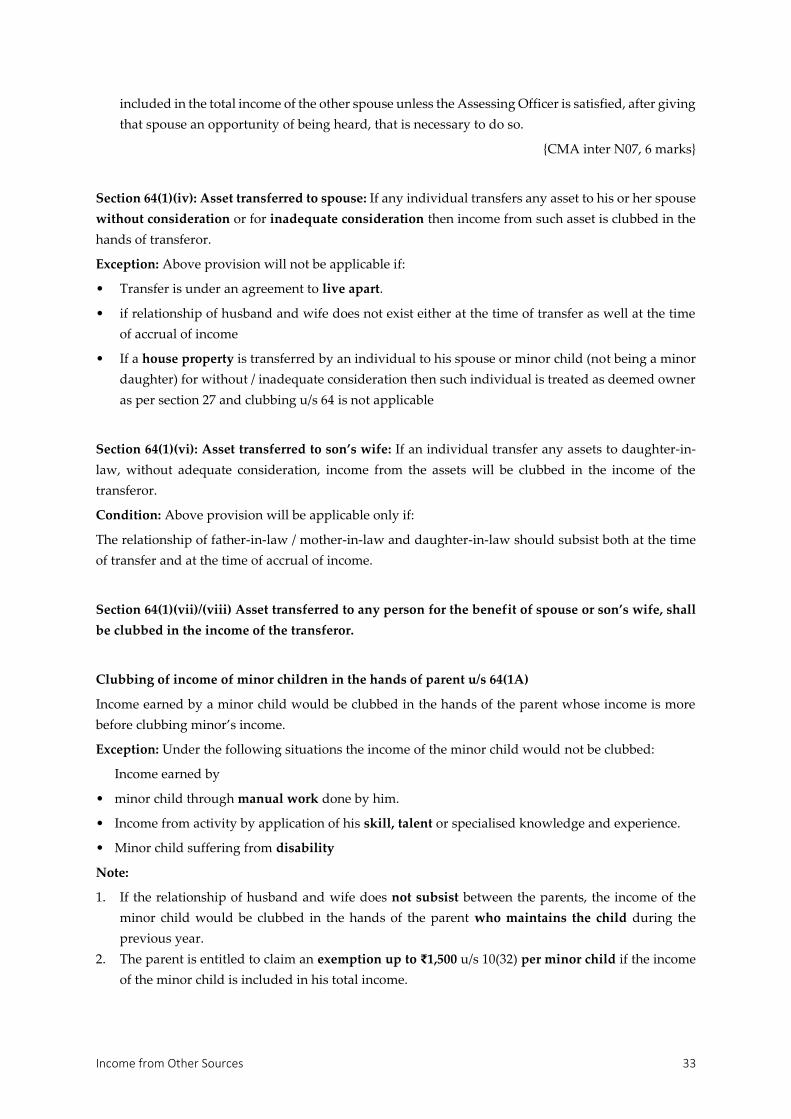

{CMA inter N07, 6 marks}

Section 64(1)(iv): Asset transferred to spouse: If any individual transfers any asset to his or her spouse

without consideration or for inadequate consideration then income from such asset is clubbed in the

hands of transferor.

Exception: Above provision will not be applicable if:

• Transfer is under an agreement to live apart.

• if relationship of husband and wife does not exist either at the time of transfer as well at the time

of accrual of income

• If a house property is transferred by an individual to his spouse or minor child (not being a minor

daughter) for without / inadequate consideration then such individual is treated as deemed owner

as per section 27 and clubbing u/s 64 is not applicable

Section 64(1)(vi): Asset transferred to son’s wife: If an individual transfer any assets to daughter-in-

law, without adequate consideration, income from the assets will be clubbed in the income of the

transferor.

Condition: Above provision will be applicable only if:

The relationship of father-in-law / mother-in-law and daughter-in-law should subsist both at the time

of transfer and at the time of accrual of income.

Section 64(1)(vii)/(viii) Asset transferred to any person for the benefit of spouse or son’s wife, shall

be clubbed in the income of the transferor.

Clubbing of income of minor children in the hands of parent u/s 64(1A)

Income earned by a minor child would be clubbed in the hands of the parent whose income is more

before clubbing minor’s income.

Exception: Under the following situations the income of the minor child would not be clubbed:

Income earned by

• minor child through manual work done by him.

• Income from activity by application of his skill, talent or specialised knowledge and experience.

• Minor child suffering from disability

Note:

1. If the relationship of husband and wife does not subsist between the parents, the income of the

minor child would be clubbed in the hands of the parent who maintains the child during the

previous year.

2. The parent is entitled to claim an exemption up to ₹1,500 u/s 10(32) per minor child if the income

of the minor child is included in his total income.

Income Tax 34

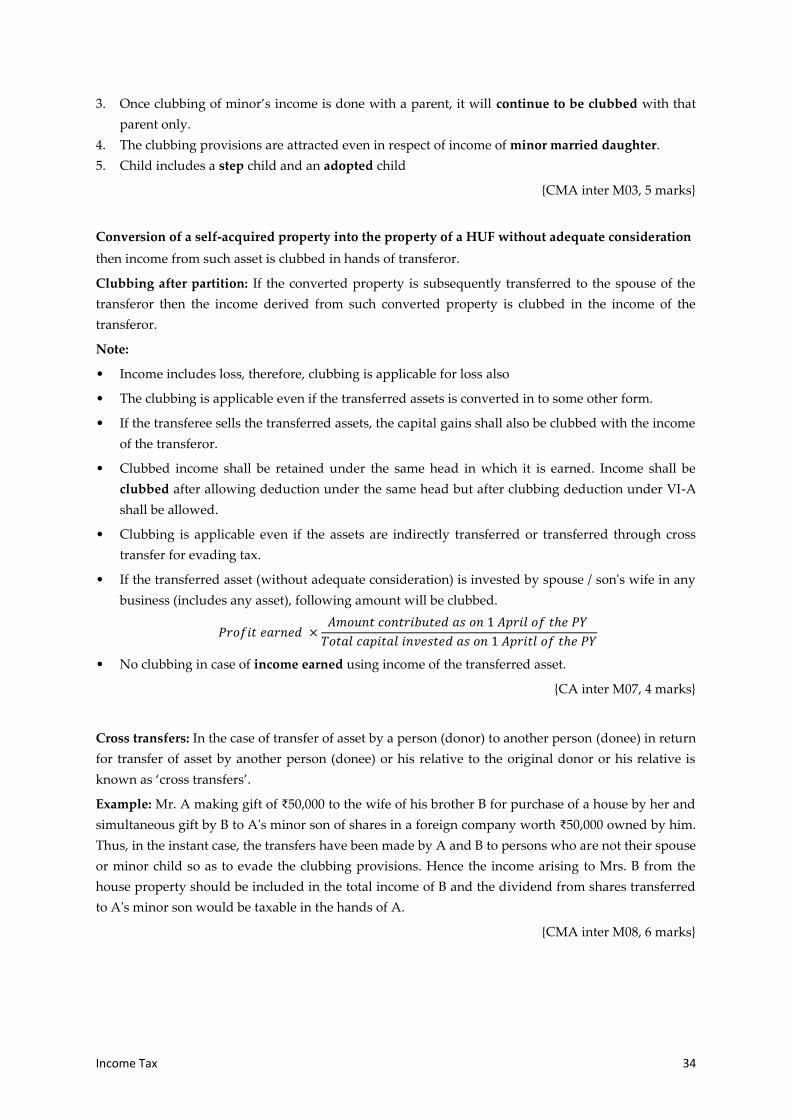

3. Once clubbing of minor’s income is done with a parent, it will continue to be clubbed with that

parent only.

4. The clubbing provisions are attracted even in respect of income of minor married daughter.

5. Child includes a step child and an adopted child

{CMA inter M03, 5 marks}

Conversion of a self-acquired property into the property of a HUF without adequate consideration

then income from such asset is clubbed in hands of transferor.

Clubbing after partition: If the converted property is subsequently transferred to the spouse of the

transferor then the income derived from such converted property is clubbed in the income of the

transferor.

Note:

• Income includes loss, therefore, clubbing is applicable for loss also

• The clubbing is applicable even if the transferred assets is converted in to some other form.

• If the transferee sells the transferred assets, the capital gains shall also be clubbed with the income

of the transferor.

• Clubbed income shall be retained under the same head in which it is earned. Income shall be

clubbed after allowing deduction under the same head but after clubbing deduction under VI-A

shall be allowed.

• Clubbing is applicable even if the assets are indirectly transferred or transferred through cross

transfer for evading tax.

• If the transferred asset (without adequate consideration) is invested by spouse / son's wife in any

business (includes any asset), following amount will be clubbed.

𝑃𝑟𝑜𝑓𝑖𝑡 𝑒𝑎𝑟𝑛𝑒𝑑 ×𝐴𝑚𝑜𝑢𝑛𝑡 𝑐𝑜𝑛𝑡𝑟𝑖𝑏𝑢𝑡𝑒𝑑 𝑎𝑠 𝑜𝑛 1 𝐴𝑝𝑟𝑖𝑙 𝑜𝑓 𝑡ℎ𝑒 𝑃𝑌

𝑇𝑜𝑡𝑎𝑙 𝑐𝑎𝑝𝑖𝑡𝑎𝑙 𝑖𝑛𝑣𝑒𝑠𝑡𝑒𝑑 𝑎𝑠 𝑜𝑛 1 𝐴𝑝𝑟𝑖𝑡𝑙 𝑜𝑓 𝑡ℎ𝑒 𝑃𝑌

• No clubbing in case of income earned using income of the transferred asset.

{CA inter M07, 4 marks}

Cross transfers: In the case of transfer of asset by a person (donor) to another person (donee) in return

for transfer of asset by another person (donee) or his relative to the original donor or his relative is

known as ‘cross transfers’.

Example: Mr. A making gift of ₹50,000 to the wife of his brother B for purchase of a house by her and

simultaneous gift by B to A's minor son of shares in a foreign company worth ₹50,000 owned by him.

Thus, in the instant case, the transfers have been made by A and B to persons who are not their spouse

or minor child so as to evade the clubbing provisions. Hence the income arising to Mrs. B from the

house property should be included in the total income of B and the dividend from shares transferred

to A's minor son would be taxable in the hands of A.

{CMA inter M08, 6 marks}

Income from Other Sources 35

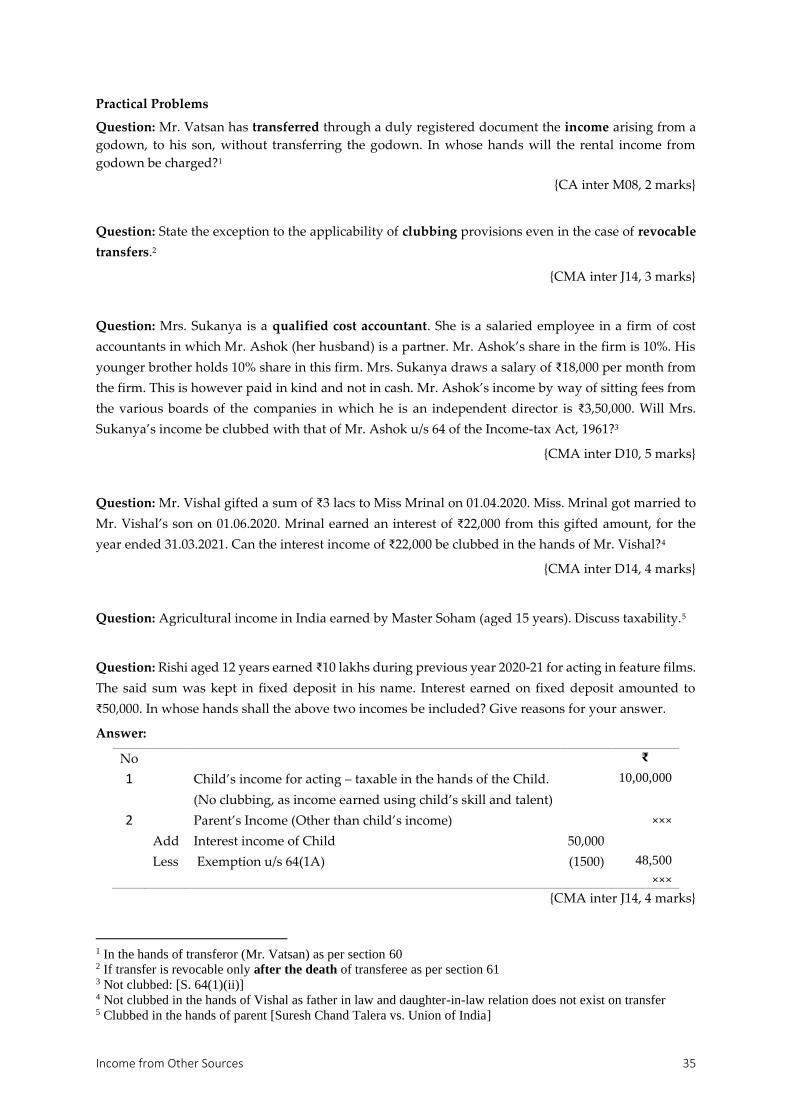

Practical Problems

Question: Mr. Vatsan has transferred through a duly registered document the income arising from a

godown, to his son, without transferring the godown. In whose hands will the rental income from

godown be charged?1

{CA inter M08, 2 marks}

Question: State the exception to the applicability of clubbing provisions even in the case of revocable

transfers.2

{CMA inter J14, 3 marks}

Question: Mrs. Sukanya is a qualified cost accountant. She is a salaried employee in a firm of cost

accountants in which Mr. Ashok (her husband) is a partner. Mr. Ashok’s share in the firm is 10%. His

younger brother holds 10% share in this firm. Mrs. Sukanya draws a salary of ₹18,000 per month from

the firm. This is however paid in kind and not in cash. Mr. Ashok’s income by way of sitting fees from

the various boards of the companies in which he is an independent director is ₹3,50,000. Will Mrs.

Sukanya’s income be clubbed with that of Mr. Ashok u/s 64 of the Income-tax Act, 1961?3

{CMA inter D10, 5 marks}

Question: Mr. Vishal gifted a sum of ₹3 lacs to Miss Mrinal on 01.04.2020. Miss. Mrinal got married to

Mr. Vishal’s son on 01.06.2020. Mrinal earned an interest of ₹22,000 from this gifted amount, for the

year ended 31.03.2021. Can the interest income of ₹22,000 be clubbed in the hands of Mr. Vishal?4

{CMA inter D14, 4 marks}

Question: Agricultural income in India earned by Master Soham (aged 15 years). Discuss taxability.5

Question: Rishi aged 12 years earned ₹10 lakhs during previous year 2020-21 for acting in feature films.

The said sum was kept in fixed deposit in his name. Interest earned on fixed deposit amounted to

₹50,000. In whose hands shall the above two incomes be included? Give reasons for your answer.

Answer:

No ₹

1 Child’s income for acting – taxable in the hands of the Child.

(No clubbing, as income earned using child’s skill and talent)

10,00,000

2 Parent’s Income (Other than child’s income) ×××

Add Interest income of Child 50,000

Less Exemption u/s 64(1A) (1500) 48,500

×××

{CMA inter J14, 4 marks}

1 In the hands of transferor (Mr. Vatsan) as per section 60 2 If transfer is revocable only after the death of transferee as per section 61 3 Not clubbed: [S. 64(1)(ii)] 4 Not clubbed in the hands of Vishal as father in law and daughter-in-law relation does not exist on transfer 5 Clubbed in the hands of parent [Suresh Chand Talera vs. Union of India]

Income Tax 36

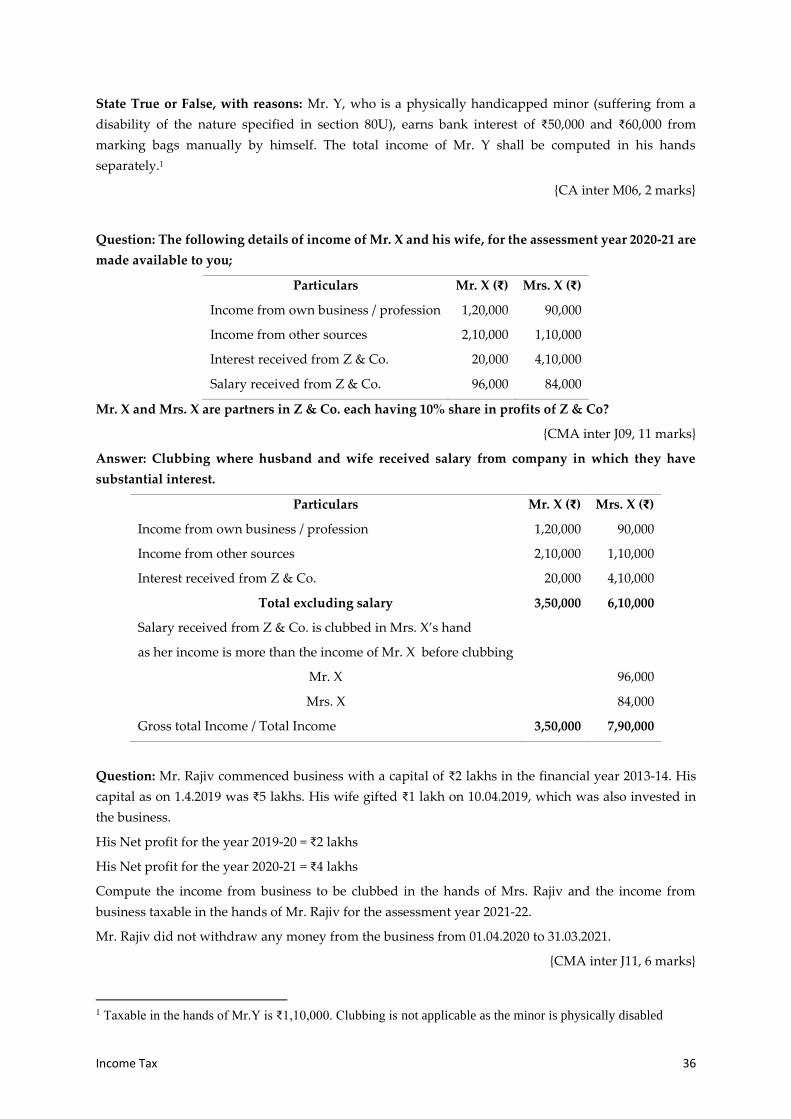

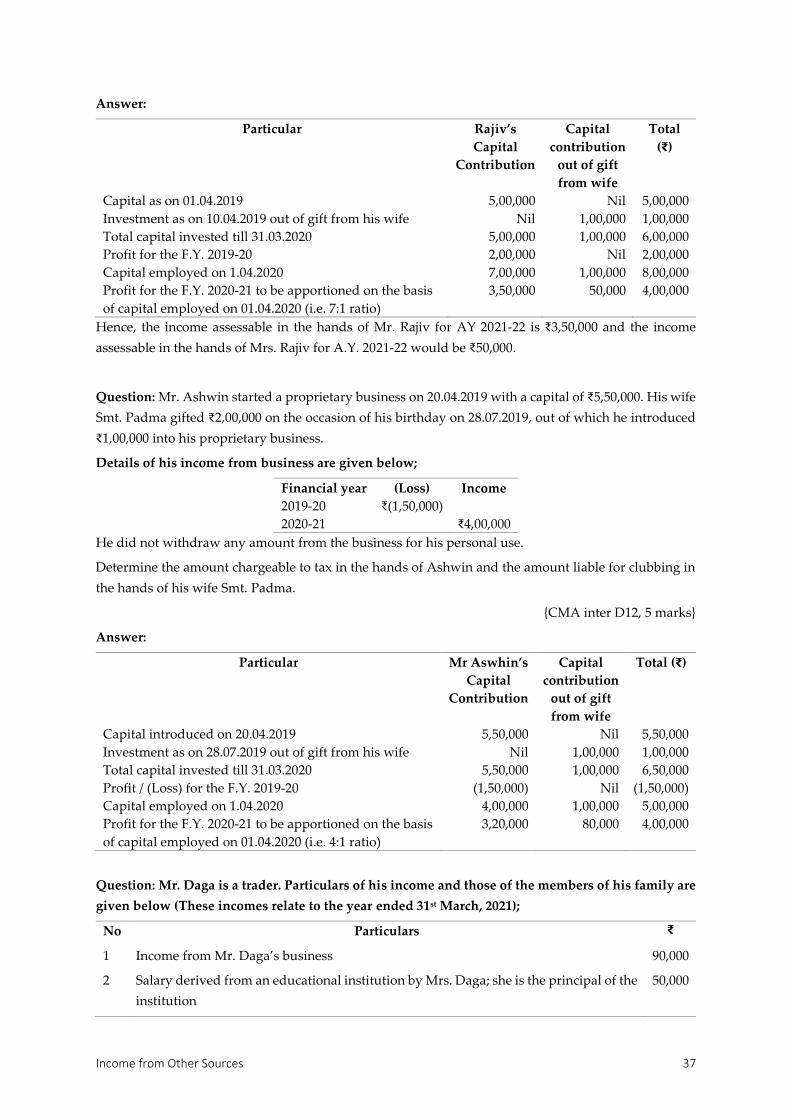

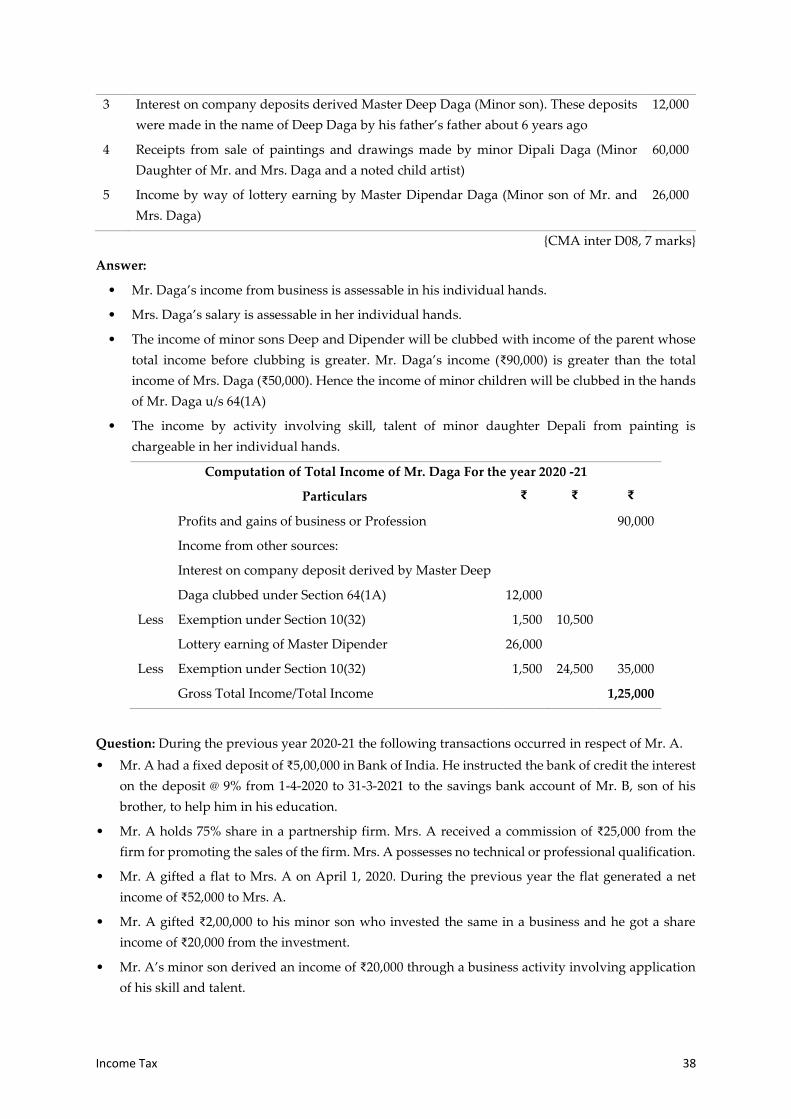

State True or False, with reasons: Mr. Y, who is a physically handicapped minor (suffering from a