Embed Size (px)

Citation preview

KIRBY McINE 3ZNEY & SQUIRE, ir PRoger W. Kirby, Esq.Alice McInerney, Esq. 11VAndrea Bierstein, Esq.830 Third Avenue 3 \994New York, NY 10022 ,ck-1A 1(212) 317-2300

AT 8:30 ........ ...........4111.1.0n1,10K ,

Lead Counsel for the PRIDES class

UNITED STATES DISTRICT COURTFOR THE DISTRICT OF NEW JERSEY

IN RE CENDANT CORPORATION Master File No.SECURITIES LITIGATION CV-98-2819 (WHW)

This Document Relates To: PRIDES JURY TRIALclaims DEMANDED

SECOND AMENDED AND CONSOLIDATED COMPLAINTRESPECTING THE PRIDES CLAIMS

April 5, 1999

•

TABLE OF CONTENTS

I. JURISDICTION AND VENUE 1

ALLEGATIONS RELATING TO THE SECURITIES ACT CLAIMS 2

II. INTRODUCTION 2

III. THE PARTIES 5

PLAINTIFFS 5

DEFENDANTS 6

A. CENDANT DEFENDANTS 6

B. THE INDIVIDUAL DEFENDANTS 7

1. Inside Directors of Cendant 7

a. Former CUC Inside Directors 7

b. Former HFS Inside Directors 9

2. Outside Directors of Cendant 1 1

a. Former Members of CUC Audit Committee 1 1

b. Certain Other Outside Directors 1 2

3. Other Individual Cendant Defendants 1 3

C. ACCOUNTANT DEFENDANT 1 3

D. UNDERWRITER DEFENDANTS 1 5

E. CERTAIN NON-PARTIES: OTHER CENDANT OFFICERS ANDEMPL OYEES 1 8

IV. BACKGROUND 2 1

A. CUC MERGES WITH HFS AND CHANGES NAME TO CENDANT 21

B. THE PRIDES OFFERING AND SURROUNDING CIRCUMSTANCES .. . 22

V. CLAIMS UNDER SECTIONS 11 AND 12(a)(2) OF THE SECURITIES ACT 25

A. THE MATERIALLY FALSE AND MISLEADING REGISTRATIONSTATEMENT 25

B. CENDANT'S ADMISSIONS AS TO THE FALSITY OF THE FINANCIALINFORMATION CONTAINED IN THE REGISTRATION STATEMENT ANDPROSPECTUS 30

C. THE NATURE OF THE ACCOUNTING IRREGULARITIES IN CENDANT'SFINANCIAL STATEMENTS 38

1. Topside Adjustments to Quarterly Results 38

2. Irregularities Involving Utilization of Merger Reserves 39

3. Irregularities in Connection with Revenue Recognition 40

4. Irregularities Concerning the Membership Cancellation Reserve 41

D. VIOLATIONS OF GAAP 41

1. Internal Control Deficiencies Cited in Audit Committee Report 46

2. The Financial Reporting Process 47

3. The Budget and Planning Process 48

4. The Internal Audit Function 49

5. Information for Management 49

E. THE INDIVIDUAL DEFENDANTS FAILED TO EXERCISE REASONABLECARE IN THE PREPARATION AND DISSEMINATION OF THEREGISTRATION STATEMENT AND PROSPECTUS 50

1. Cendant Directors Who Were Former CUC Insiders 52

2. Cendant Directors Who Were Members of the CUC AuditCommittee 55

3. Cendant Directors Who Were Former HFS Directors and Officers . .. . 56

F. THE NATURE OF THE UNDERWRITER DEFENDANTS'0 WRONGDOING 61

G. THE NATURE OF ERNST & YOUNG'S WRONGDOING 63

VI. CLAIMS UNDER THE SECURITIES ACT OF 1933 78

FIRST CLAIM FOR RELIEF(Against the Cendant Defendants forViolations of Section 11 of the Securities Act) 78

SECOND CLAIM FOR RELIEF(Against the Individual Defendantsfor Violations of Section 11 of the Securities Act) 80

THIRD CLAIM FOR RELIEF(Against Ernst & Young For Violations ofSection 11 of the Securities Act) 81

FOURTH CLAIM FOR RELIEF(Against the Underwriter Defendants

0 For Violations of Section 11 of the Securities Act) 83

FIFTH CLAIM FOR RELIEF(Against the Cendant Defendants and the UnderwriterDefendants For Violations of Section 12(a)(2) of the Securities Act) 84

SIXTH CLAIM FOR RELIEF(Against the Individual Defendantsfor Violation of Section 15 of the Securities Act) 86

ALLEGATIONS RELATING TO THE EXCHANGE ACT CLAIMS 86

VII. INTRODUCTION TO THE EXCHANGE ACT CLAIMS 86

A. THE CONTINUING FRAUD: REPRESENTATIONS MADE ON AND AFTERAPRIL 15, 1998 90

B. THE TRUTHFUL REVELATION OF THE FRAUD 102

VIII. ERNST & YOUNG'S KNOWLEDGE OF THE FRAUD 105

A. ERNST & YOUNG'S SCIENTER 105

)

B. FAILURE TO NOTE IMPROPER RECOGNITION) OF MEMBERSHIP REVENUE 107

C. SPECIFIC KNOWLEDGE OF THE CNA CONTRACT FRAUD 108

D. KNOWLEDGE OF THE $170 MILLION COMP-U-CARD) DISCREPANCY 109

E. WILLFUL IGNORANCE OF THE COMP-U-CARDQUARTERLY REPORTING PACKAGES 109

) F. KNOWLEDGE OF INFLATION OF INCOME 110

G. KNOWLEDGE OF MISMATCHING OF REVENUE AND EXPENSES . . 110

H. ERNST & YOUNG'S KNOWLEDGE OF IMPROPER MERGERRESERVES 111

L FAILURE TO REPORT INTERNAL CONTROL DEFICIENCIES 112

J. FAILURE TO MAINTAIN PROFESSIONAL SKEPTICISM 113

)K. FAILURE TO MAINTAIN INDEPENDENCE 115

L. ERNST & YOUNG'S COMPLICITY IN THE MISLEADINGAPRIL 15, 1998 PRESS RELEASE 115

) IX. SCIENTER OF CENDANT AND THE INDIVIDUAL DEFENDANTS 119

A. CENDANT DIRECTORS WHO WERE FORMER CUCINSIDERS AND CFO CORIGLIANO 123

B. DISCOVERY BY SILVERMAN AND SCIENTER AS TOTHE APRIL 15, 1998 AND APRIL 27, 1998 STATEMENTS 127

X. INAPPLICABILITY OF SAFE HARBOR PROVISION 131

XI. APPLICABILITY OF PRESUMPTION OF RELIANCE AND FRAUD ON THEMARKET DOCTRINE 132

XII. CLAIMS UNDER THE EXCHANGE ACT 133

iv

SEVENTH CLAIM FOR RELIEFUNDER SECTION 10(b) OF THE EXCHANGE ACTAND RULE 10b-5(Against Cendant and Certain Individual Defendants) 133

EIGHTH CLAIM FOR RELIEFUNDER SECTION 10(b) OF THE EXCHANGE ACT

0 AND RULE 10b-5 (Against Ernst & Young) 138

NINTH CLAIM FOR RELIEFUNDER EXCHANGE ACT SECTION 20(a)(Against Certain Individual Defendants) 142

XIII. CLASS ACTION ALLEGATIONS FOR ALL CLAIMS 143

JURY DEMAND 145

PRAYER 145

Its

Plaintiffs, individually and on behalf of all others similarly situated, through

their undersigned counsel, allege the following upon personal knowledge as to their own acts,

and on information and belief as to all other matters. Plaintiffs' information and belief is based

upon, inter alia, an investigation by their counsel of publicly filed documents by Cendant0

Corporation ("Cendant" or the "Company") with the Securities and Exchange Commission

("SEC"), press releases and news reports issued by or otherwise concerning Cendant, information

concerning open market purchases and sales of Cendant securities, individual filings of Forms 3,

4, and 5 with the SEC that reflect insider holdings, purchases and sales of Cendant securities, and

other publicly available information.

1. This action seeks remedies against Cendant and Cendant Capital I, certain of

Cendant's current and former directors and officers, Ernst &Young, LLP, and certain underwriter

defendants, pursuant to Sections 11, 12(a)(2), and against all individual defendants under Section

15 of the Securities Act of 1933 (the "Securities Act") for all persons who purchased or acquired

PRIDES from the underwriter defendants between February 24, 1998 and April 15, 1998,

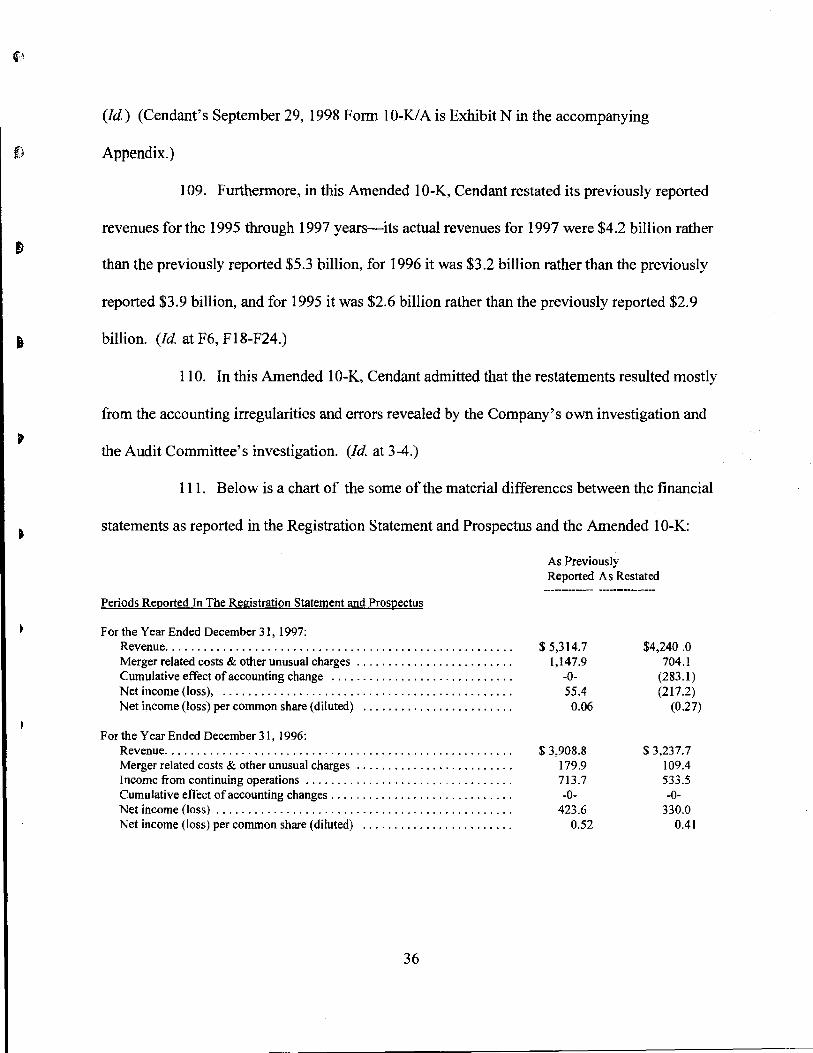

inclusive (the "1933 Act Class").

2. Plaintiffs also bring this action to recover damages for violations of Section

10(b) of the Securities and Exchange Act (the "Exchange Act"), and Rule 10-b-5 promulgated

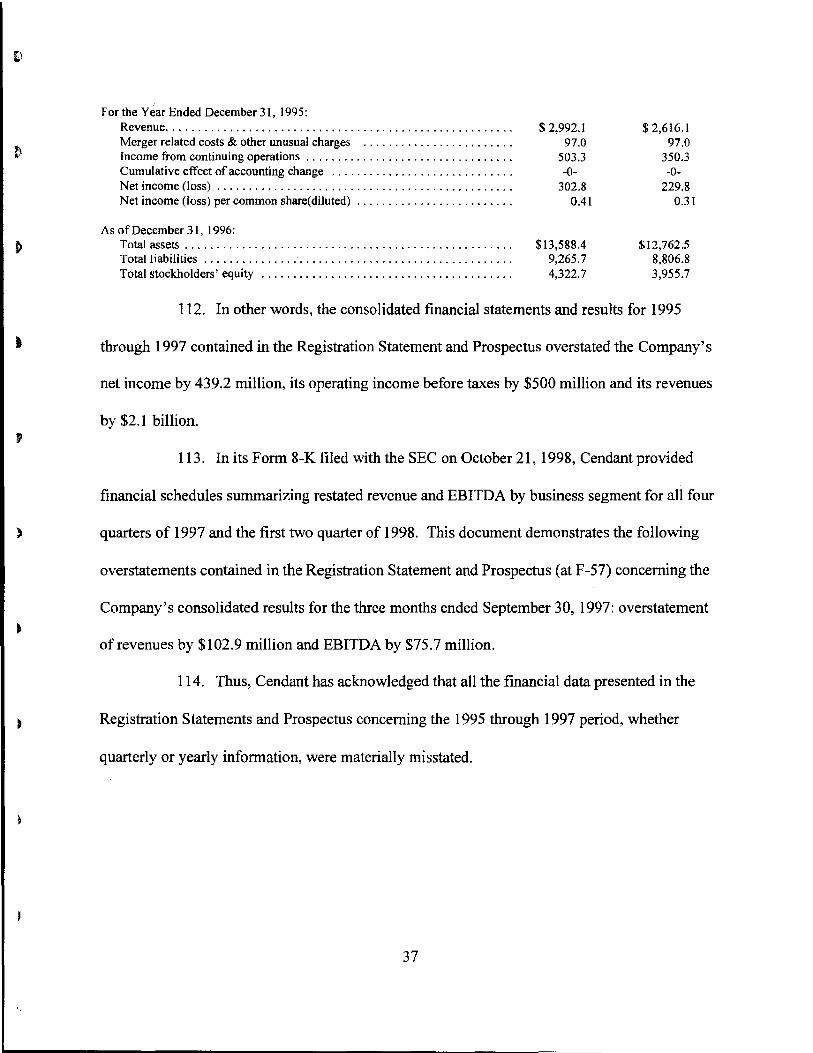

thereunder, against Cendant, certain of its former officers and directors, and Ernst & Young.

LLP, on behalf of purchasers of PRIDES on the open market during the period from April 16,

1998 through July 13, 1998, inclusive (the "Exchange Act Class").

I. JURISDICTION AND VENUE

3. The claims set forth herein arise under Sections 11, 12(a)(2) and 15 of the

Securities Act of 1933, 15 U.S.C. §§ 77k, 771(2), and 77(o), Sections 10(b) and 20(a) of the

Securities Exchange Act of 1934, 15 U.S.C. §§ 78j(b), 78t(a), and Rule 10b-5, 17 C.F.R. §

240.10b-5.

4. The jurisdiction of this court is founded upon Section 22(a) of the Securities

Act, 15 U.S.C. § 77v(a), Section 27 of the Exchange Act, 15 U.S.C. § 78aa, and 28 U.S.C.

§§ 1331, 1337.

5. Venue is proper in this judicial district pursuant to Section 22 of the Securities

Act, 15 U.S.C. § 78v, and Section 27 of the Exchange Act, 15 U.S.C. § 78aa . Many of the acts

and transactions giving rise to the violations of law complained of herein occurred in this district,

including the preparation and dissemination of various false and misleading statements

complained of herein occurred in this district.

6. In connection with the acts, conduct, and other wrongs complained of herein,

the defendants, directly and indirectly, used the means and instrumentalities of interstate

commerce, including the mails, interstate telephone communications, and the facilities of the

national securities exchanges.

0ALLEGATIONS RELATING TO THE SECURITIES ACT CLAIMS

II. INTRODUCTION

7. Plaintiffs bring this class action to recover damages for violations of the federal

securities laws on behalf of purchasers of a derivative-type convertible security known as

Cendant FELINE PRIDES ("PRIDES"). Cendant Corporation ("Cendant" or the "Company")

and its wholly owned subsidiary, Cendant Capital I, issued the PRIDES in an initial public

offering (the "PRIDES Offering" or "Offering") pursuant to materially false and misleading

registration statements on SEC Form 8-Al2B filed on February 23, 1998, Amendment No. 3 to

2

the Registration Statement on Form S-3 filed with the SEC on February 20, 1998 (the

"Registration Statement") and the forms of prospectus and prospectus supplement for the

PRIDES included therein, and the definitive copies of the prospectus and prospectus supplement

on Form 424B5 with the SEC on February 26, 1998 (the "Prospectus"). The Offering closed on

March 2, 1998. Cendant is the successor entity of CUC international Inc. ("CUC"), which

merged with HFS International Incorporated ("HFS") on December 17, 1997. (The Registration

Statement and Prospectus are Exhibits B and C in the accompanying Appendix.)

8. The Offering involved the sale of approximately $1.5 billion PRIDES.

Defendants Merrill Lynch & Co. and Merrill Lynch, Pierce, Fenner & Smith Incorporated and

Chase Securities Inc., were the underwriters. Collectively they received approximately $40

million of underwriting commissions.

9. Among other financial information, the Registration Statement and Prospectus

contained Cendant's audited consolidated statements of income for the three years ended

December 31, 1996 and the Company's unaudited financial results for 1997. Cendant has now

admitted that these financial results overstated income and revenues and understated expenses by

astronomical amounts.

10. More specifically, on April 15, 1998, Cendant disclosed "accounting

irregularities" that would require it to restate its 1997 net income by $1004115 million, and also

restate earlier periods. These accounting irregularities occurred within former CUC units that

had been audited by Ernst & Young, LLP ("E&Y"). This announcement caused the value of

PRIDES to lose approximately one-third of their value or approximately $400 million of market

capitalization in one day.

3

11. E&Y, CUC's accountant, had audited the 1995 and 1996 financial statements

of CUC which were incorporated into the consolidated financial statements of Cendant contained

in the Registration Statement and Prospectus. E&Y explicitly consented to the incorporation by

reference into the Prospectus and Registration Statement within the section entitled "Experts" of

its unqualified audit opinions on the CUC financials.

12. On July 14, 1998, based upon information developed from an independent

investigation commissioned by the audit committee of the Cendant board of directors, Cendant

disclosed that the accounting irregularities were far more pervasive than had been previously

disclosed and resulted in an overstatement of net income for 1997 that was more than double the

amount announced on April 15, 1998, i.e. over $200 million. It further acknowledged that net

income for 1995 and 1996 had been inflated by approximately $250 million (pre-tax) and that it

would be restating its financial reports for the prior three years, from 1995 through 1997. This

disclosure caused additional substantial decline in the value of the PRIDES.

13. On September 29, 1998, the Company filed with the SEC a Form 10-K/A

restating "its previously reported financial results for 1997, 1996 and 1995." The restatement

showed that the revenues and net income for this period that were reported in the Registration

Statement and Prospectus had been inflated by over $2.1 billion and over $430 million,6

respectively. Further illustrating the magnitude of the difference between the financial picture

presented in the offering materials and the actual facts, in 1997 Cendant had a loss of $217.2

million rather than the reported net income of $55.4 million.

14. In October 1998, the Company also restated its results for the first two quarters

of 1998 and the four quarters of 1997.

4

)

15. As discussed in detail in the Forms 8-K filed with the SEC on August 28, 1998

) containing the Report to the audit committee of the board of directors of Cendant Corporation,

prepared by Wilkie Farr & Gallagher ("Wilkie Farr") and Arthur Andersen LLP ("Andersen")

(the "Report"), the restatements were necessitated by numerous accounting irregularities and)

improper accounting practices in 17 of CUC's 22 units, which inflated CUC's operating income

by approximately $500 million during 1995 through 1997, including unsupported topside

1 adjustments to quarterly results, inappropriate utilization of merger reserves, improper irregular

recognition practices and irregularities concerning the membership cancellation reserve. (An

Appendix to the Report was filed in a Form 8-K/A on September 17, 1998.) (Cendant's Form 8-)

K filed on August 28, 1998 containing the Report is Exhibit M in the accompanying Appendix.)

III. THE PARTIES

) PLAINTIFFS

16. The history of the plaintiffs' PRIDES investments is set forth in the attached

schedule, incorporated herein by reference. Asterisks denote plaintiffs who purchased PRIDES

)directly from an Underwriter Defendant during the period February 24, 1998 to April 15, 1998,

inclusive. Each plaintiff has been damaged directly by the wrongdoing complained of. Each

plaintiff has filed a certificate that has been made part of the record of these proceedings, except

for Mr. Fugitt, whose certificate is attached hereto.

5

DEFENDANTS

A. CENDANT DEFENDANTS

17. Defendant Cendant is a Delaware corporation with executive offices in

Parsippany, New Jersey. Cendant is identified in the Registration Statement and Prospectus as

one of the two issuers of the PRIDES Offering. (Registration Statement at S-7; Prospectus at S-

7.)

18. Cendant, which had operated under the corporate name of CUC prior to its

December 17, 1997 merger with HFS, provides all of the services formerly offered by both CUC

and HF S.

19. CUC had been a membership-based consumer services company providing

members with access to a variety of goods and services. It also offered consumer software

through certain businesses acquired during 1996. The membership business offered a variety of

goods and services. CUC categorized the membership services offered as individual, wholesale

and discount programs.

20. CUC's membership activities were conducted through its Comp-U-Card

division and, as of December, 1997, through approximately 20 wholly-owned subsidiaries

located throughout the United States and Europe. The Comp-U-Card division was CUC's largest

business unit and its general ledger functioned as the general ledger for CUC Corporate.

21. CUC used a fiscal January 31 year-end and quarters ending January 31, April

30, July 31 and October 31. Therefore, CUC's "fiscal 1997" refers to the year ended January 31,

1998; "fiscal 1996" refers to the year ended January 31, 1997, and so forth. Following the

merger of CUC and HFS, Cendant reported on a calendar year basis.

6

22. The other issuer of the PRIDES Offering identified in the Registration

Statement and Prospectus is Cendant Capital I. (Registration Statement at S-7; Prospectus at S-

7).

23. Defendant Cendant Capital I is a wholly owned subsidiary of Cendant.

(Prospectus at 24. Cendant's quarterly report on SEC Form 10-Q/A for the quarterly period

ended March 31, 1998, filed on October 13, 1998 p. 19 at 10.) It is a statutory business trust

formed by Cendant under the Delaware Business Trust Act. The February 5, 1998 declaration

creating Cendant Capital I was qualified as an indenture under the Trust Indenture Act of 1939,

as amended. Cendant has declared in its Prospectus that this trust was created for the exclusive

purpose of enabling the creation and issuance of PRIDES by providing the indenture trust

structure necessary for the issuance of trust securities and investing the gross proceeds from the

sale of such trust securities so as to create the form of PRIDES securities described in the

Prospectus and sold in the Offering. (Prospectus at 1, 5).

24. Cendant and Cendant Capital I are together referred to as the "Cendant Defen-

)dants."

B. THE INDIVIDUAL DEFENDANTS

I. Inside Directors of Cendant

a. Former CUC Inside Directors

25. Defendant Walter A. Forbes ("Walter Forbes") was chairman of the board of

directors ("Cendant Board") and a director of Cendant throughout the class periods as defined

below. Forbes signed the Registration Statement through his attorney-in-fact and agent. In 1973,

Forbes founded what subsequently became CUC. Before the Merger, Forbes had served as

7

CUC's chief executive officer, director, chairman of the board of directors ("CUC Board"), and

as a member of the executive committee of the CUC Board. Between the time of the Merger

and the first disclosure of accounting irregularities by Cendant on April 15, 1998, Forbes sold

478,922 shares of Cendant common stock at prices in excess of $38 per share. Forbes realized

gross income of over $17,588,525 from these sales. As shown by SEC filings, Walter Forbes

also sold about $30 million of stock in CUC during the years that accounting irregularities had

inflated profits. The filings show that Walter Forbes regularly sold stock in CUC between 1993

and March 1998, after the Merger but before the drop in stock price. These sales were both on

the open market and through exercising and selling options. Forbes resigned his positions with

Cendant on July 28, 1998.

26. Defendant E. Kirk Shelton ("Shelton") was Cendant's vice chairman, member

of the executive committee of the Cendant Board and director throughout much of the 1933 Act

Class Period as defined below. Shelton signed the Registration Statement through his attorney-

in-fact and agent. Before the Merger, Shelton had served as CUC's president, chief operating

0officer, member of the executive committee of the CUC Board and a director. As CUC's

president and chief operating officer, Shelton reported directly to Walter Forbes. Between the

time of the Merger and the first disclosure of accounting irregularities by Cendant on April 15,

1998, Shelton sold 62,620 shares of Cendant common stock at prices in excess of $31 per share.

From these sales, Shelton realized gross income of over $1,941,220. Shelton purportedly

resigned his position with Cendant effective July 28, 1998 but was terminated for cause on

August 27, 1998.

8

27. Defendant Christopher K. McLeod ("McLeod") was Cendant's vice chairman,

member of the executive committee of the Cendant Board and a director throughout the class

periods. In addition, McLeod was chief executive officer of Cendant Software, a subsidiary of

Cendant. McLeod signed the Registration Statement through his attorney-in-fact and agent.0

Before the Merger, McLeod had served as director of CUC and held a position as an executive

officer in the office of the president reporting directly to Walter Forbes. McLeod resigned his

positions with Cendant on October 12, 1998.

28. Defendant Robert T. Tucker ("Tucker") was Cendant's vice chairman,

secretary, member of the compensation committee of the Cendant Board and a director

throughout the class periods. Tucker signed the Registration Statement and Prospectus through

his attorney-in-fact and agent. Before the Merger, Tucker had served as secretary and a director

of CUC. Tucker resigned his positions with Cendant on October 12, 1998.

b. Former HFS Inside Directors

29. Defendant Henry R. Silverman ("Silverman") was Cendant's president, chief

executive officer, and director throughout the class periods. Silverman signed the Registration

Statement through his attorney-in-fact and agent. Prior to the Merger, Silverman had served as

president, chief executive officer, director, and chairman of the board of directors of HFS.

Following the resignation of Walter Forbes on July 28, 1998, Silverman became chairman of

Cendant's Board and has continued as Cendant's president and chief executive officer.

Silverman was trained as a tax lawyer. On September 24, 1998, following the decimation of the

price of Cendant's common stock, the Company repriced the stock options it had previously

awarded to certain of the Individual Defendants in order to lower the price at which these options

9

could be exercised. Cendant Press Release (Sept. 24, 1998). In this press release, the Company

'6) also announced defendant Silverman's intent to exercise a portion of his in-the-money stock

options and purchase shares of Cendant common stock which would result in his beneficial

ownership of approximately 1.5 million shares. Between the time of the Merger and the first

disclosure of accounting irregularities by Cendant on April 15, 1998, Silverman sold 2,164,210

shares of Cendant common stock at prices in excess of $36 per share. From these sales,

Silverman realized gross income of over $61,420,239.

30. Defendant Michael P. Monaco ("Monaco") was Cendant's vice chairman, chief

financial officer and a director throughout the class periods. Monaco signed the Registration

Statement through his attomey-in-fact and agent. Before the Merger, Monaco had served as vice

chairman, chief financial officer and director of HFS.

31. Defendant Stephen P. Holmes ("Holmes") was Cendant's vice chairman,

member of the executive committee of the Cendant Board and a director throughout the class

periods. Holmes signed the Registration Statement and Prospectus through his attorney-in-fact

and agent. Before the Merger. Holmes had served as vice chairman and a director of HFS.

32. Defendant Robert D. Kunisch ("Kunisch") was Cendant's vice chairman and

director throughout the class periods. In addition, Kunisch was chief executive officer and

president of PHH Corp., a subsidiary of Cendant. Kunisch signed the Registration Statement

through his attorney-in-fact and agent. Prior to the Merger, Kunisch had served as vice chairman

and director of HFS.

33. Defendant James E. Buckman ("Buckman") was Cendant's senior executive

vice president, general counsel and a director throughout the class periods. As described herein,

10

)

Buckman signed the Registration Statement on behalf of himself and as attorney-in-fact and

agent for each of the individual defendants who signed the Statement, and for Cendant. Before

the Merger, Buckman had served as senior executive vice president, general counsel, assistant

secretary and director of HFS. Between the time of the Merger and the first disclosure of)

accounting irregularities by Cendant on April 15, 1998, Buckman sold 300,000 shares of

Cendant common stock at prices in excess of $36 per share. From these sales, Buckman realized

) gross income of over $10, 857,000,

2. Outside Directors of Cendant

a. Former Members of CUC Audit Committee)

34. T. Barnes Donnelly ("Donnelly") was a Cendant director and member of

Cendant's Audit Committee of its Board ("Cendant's Audit Committee") throughout the class

) periods. Before the Merger, Donnelly had been a CUC director and member of CUC's Audit

Committee of its Board ("CUC's Audit Committee") for more than ten years. Donnelly signed

the Registration Statement through his attorney-in-fact and agent. On July 28, 1998 Donnelly

)resigned his positions with Cendant.

35. Stephen A. Greyser ("Greyser") was a Cendant director and member of

Cendant's Audit Committee throughout the class periods. Prior to the Merger, Greyser had been

a CUC director and member of CUC's Audit Committee for more than ten years. Greyser

signed the Registration Statement through his attorney-in-fact and agent. On July 28, 1998

) Greyser resigned his positions with Cendant.

36. Burton C. Perfit ("Perfit") was a Cendant director and member of Cendant's

Audit Committee throughout the class periods. Prior to the Merger. Perfit had been a CUC

11

director and the chairman of CUC's Audit Committee for more than ten years. Perfit signed the

Registration Statement through his attorney-in-fact and agent. Between the time of the Merger

and the first disclosure of accounting irregularities by Cendant on April 15, 1998, Perfit sold

3,938 shares of Cendant common stock at prices in excess of $35 per share. From these sales,

Perfit realized gross income of over $140, 783. On July 28, 1998, Perfit resigned his positions

with Cendant.

b. Certain Other Outside Directors

37. Bartlett Bumap ("Burnap"), Martin L. Edelman ("Edelman") Stanley M.

Rumbough, Jr. ("Rumbough"), and John D. Snodgrass ("Snodgrass") were directors of Cendant

throughout the class periods. Each signed the Registration Statement through his or her attorney-

in-fact and agent.

38. Between the time of the Merger and the first disclosure of accounting

irregularities by Cendant on April 15, 1998, Burnap, Edelman, Rumbough, and Snodgrass sold

shares of Cendant common stock. Bumap sold 575,000 shares of Cendant common stock at

prices in excess of $38 per share. From these sales, Bumap realized gross income of over

$19,997,000. Edelman sold 60,000 shares of Cendant common stock at prices in excess of $40

per share. From these sales, Edelman realized gross income of over $2,447,400. Rumbough sold

75,938 shares of Cendant common stock at prices in excess of $37 per share. From these sales.

Rumbough realized gross income of over $2,756,190. Snodgrass sold 1,604,449 shares of

Cendant common stock at prices in excess of $40 per share. From these sales, Rumbough

realized gross income of over $60, 876, 832. Bumap and Rumbough resigned their positions

with Cendant on July 28, 1998.

12

3. Other Individual Cendant Defendants

0 39. Defendant Scott E. Forbes ("Scott Forbes") was senior vice president-Finance

and Chief Accounting Officer of Cendant throughout the class periods. Scott Forbes signed the

Registration Statement through his attorney-in-fact and agent to sign the Registration Statement

on his behalf. Scott Forbes is not related to Walter Forbes.

40. The individuals named as defendants are referred to as the "Individual Defen-

dants."

41. Each of the Individual Defendants, by reason of their positions, were

controlling persons of Cendant within the meaning of Section 15 of the Securities Act. Because

of their executive, managerial, and/or directorial positions with Cendant, the Individual

Defendants had access to the adverse, non-public information about the financial condition,

operations, and future business prospects of Cendant as particularized herein and improperly

omitted to disclose the same. Any acts attributed herein to Cendant were caused and/or

influenced by the Individual Defendants by virtue of their domination and control thereof.

C. ACCOUNTANT DEFENDANT

42. From 1983 through early 1998, E&Y had been the independent auditor for

CUC. E&Y issued unqualified opinions on CUC's consolidated financial statements for the

fiscal years ended January 31, 1997, 1996 and 1995. E&Y's opinions inaccurately represented

that its audit of CUC's fiscal 1997, 1996, and 1995 annual financial statements were conducted

in accordance with generally accepted auditing standards ("GAAS"), and that CUC's financial

statements fairly presented CUC's financial condition and results of operations in conformity

with GAAP. The Registration Statement and Prospectus within the section entitled "Experts,"

13

incorporated therein by reference, with E&Y's consent, E&Y's unqualified audit report on

CUC's financials for "each of the three years in the period ended January 31, 1997".

43. E&Y also reviewed and reported on CUC's quarterly financial statements,

provided opinions on Cendant' financial statements in connection with acquisitions by CUC,

analyzed CUC's internal controls, and involved itself in the management of CUC in its role as

management consultant.

0

44. E&Y performed numerous management consulting and accounting services for

CUC prior to and during the class period. Among other things:

A. E&Y acted as a business consultant to CUC. In that role, E&Yconducted an extensive review of the status of and prospects for CUC'smerger integrations;

B. E&Y reviewed CUC's quarterly financial statements and providedreports to CUC's Audit Committee concerning the conformity of thesefinancial statements with GAAP;

C. E&Y analyzed CUC's internal controls and reported to CUC's AuditCommittee concerning its analysis; and

45. E&Y's extensive involvement with CUC also included the following:

A. E&Y had unlimited access to all of CUC's books, records anddocuments;

B. several of CUC's employees responsible for accounting and financialmatters had previously worked at E&Y, including defendant Corigliano,Pember, Controller of CUC, CUC's Spark's divisional controller, KevinT. Kearney, and Mary Sattler, current manager of financial reporting ofCendant and former assistant to Pember; and

5 C. E&Y personnel regularly attended meetings of the CUC Board and AuditCommittee.

14

46. Furthermore, E&Y also audited the financial statements of a Cendant

subsidiary, Cendant Membership Services ("CMS"), including for the year ended December 31,

1997, and issued an unqualified report thereon.

47. In connection with the services E&Y provided to CUC, E&Y personnel were

frequently present at CUC's corporate headquarters throughout the year, and had continual access

to and knowledge of CUC's confidential corporate financial, operating and business information.

E&Y personnel responsible for auditing CUC's financial statements included those who attended

meetings of the Audit Committee of CUC's board of directors.

48. CUC was one of the largest clients of E&Y's Stamford Connecticut office.

E&Y was paid at least $750,000 in fees for services rendered in 1997. The compensation of

E&Y partners reflected the financial performance of the office in which they are located. Thus,

fees from CUC engagements had a direct economic impact on the earnings of E&Y partners in

the Stamford office. E&Y also received fees from CUC for services in connection with its

acquisitions, and CUC's ability to make further acquisitions depended on the company's reported

financial performance. E&Y had reason for concern about retaining and/or expanding its

business relationship with CUC, having lost CUC's audit business to Deloitte and Touche

("Deloitte") in connection with the Merger. E&Y placed undue reliance on CUC's

management's representations and was lax in undertaking verifications because it wanted to

retain CUC as a client and maintain its competitive position.

D. UNDERWRITER DEFENDANTS

49. During the class periods, defendant Merrill Lynch & Co. ("Merrill Lynch &

Co."), a Delaware corporation, had its principal place of business at 250 Vesey Street, World

15

Financial Center, N Tower, New York, New York. Merrill Lynch & Co. is a holding company

that through its subsidiaries and affiliates, provides investment, financing, advisory, insurance,

and related services on a global basis. More specifically, these services include investment

banking, underwriting, strategic services, and other corporate finance advisory services to a wide

array of clients, including large corporations such as Cendant. Merrill Lynch & Co. had a history

providing investment banking services to Cendant predecessors, and a financial interest in

continuing the relationship. Throughout the class periods, Merrill Lynch & Co. had a securities

analyst, Mark Miller, follow and report on Cendant with a view to generating brokerage coverage

business for the firm.

50. During the class periods, defendant Merrill Lynch, Pierce, Fenner & Smith

Incorporated ("Merrill Lynch, Pierce") was a Delaware Corporation, doing business throughout

the United States. Merrill Lynch, Pierce is one of the largest securities firms in the world

providing brokerage, investment banking services and insurance products to over nine million

retail and institutional investor accounts. Merrill Lynch, Pierce regularly makes a market in

1equity securities of approximately 550 U.S. corporations. In addition, it engages in market-

making for approximately 4,800 securities of non-U.S. issuers traded in the over-the-counter

1 markets.

51. During the class periods, defendant Chase Securities Inc. ("Chase"), a

Delaware corporation, had its principal place of business at 270 Park Avenue, New York, New

York. Chase offers various investment banking and financial advisory services in connection

with mergers and acquisitions, financial structuring and loan syndications.

16

52. Merrill Lynch & Co. and Merrill Lynch & Pierce (together referred to as

"Merrill") and Chase ("The Underwriter Defendants") were underwriters regarding the PRIDES

that were sold pursuant to the Registration Statement and Prospectus. As such, and by their

material role in respect of road shows, inter alia, they successfully solicited and were substantial

factors in the purchase of the PRIDES, motivated in part to generate greater fees for themselves

and to obtain other economic benefits in connection with the offering and those of the issuer.

Both Merrill and Chase regularly conduct business in this district.

53. Prior to the PRIDES Offering, the Underwriter Defendants were required to

conduct an investigation into the business, operations, business strategy, prospects, financial

condition and accounting and management control systems of Cendant, known as a "due

diligence investigation." In the course of such investigation, the Underwriter Defendants would

have obtained knowledge of the facts alleged herein if they had acted with reasonable care,

including but not limited to making reasonable attempts to verify the data submitted to them.

The Underwriter Defendants had ready access to the subsidiary documents that revealed the

actual results of CUC and were negligent either for not obtaining, or reviewing such materials, or

for blindly relying on the auditors in the presence of red flags, discussed below.

54. Defendant Underwriters, in the absence of negligence on their parts, should

have known the adverse non-public information about Cendant's accounting and financial results

and reporting practices that were materially untrue or misleading in the Registration Statement

and Prospectus. The Underwriter Defendants substantially participated in the commission of the

wrongs alleged under the Securities Act herein through their involvement in the PRIDES

Offering. The Underwriter Defendants were at all times engaged in the business of investment

17

)

banking underwriting and selling securities to the investing public. The Underwriter Defendants

were the lead underwriters of the Offering, for which they received substantial fees in the least of

approximately $43 million in underwriting commissions. After purchasing the shares in the

Offering from the Company, the Underwriter Defendants sold the shares to the investing public.)

E. CERTAIN NON-PARTIES: OTHER CENDANTOFFICERS AND EMPLOYEES

55. Stuart L. Bell ("Bell") was CUC's Chief Financial Officer from 1981 until his)

departure in January, 1995. Bell was a member of the office of the president along with Shelton

and McLeod. Corigliano replaced Bell as CUC's Chief Financial Officer. Bell reported to

) Walter Forbes.

56. Defendant Cosmo Corigliano ("Corigliano") was executive vice president of

Cendant from the commencement of the 1933 Act Class Period through April 9, 1998. Before)

joining CUC in 1983 as assistant controller, Corigliano had been employed by E&Y. Prior to the

Merger, Corigliano had been senior vice president and chief financial officer of CUC and

) reported directly to Shelton. On April 17, 1998, Cendant disclosed that it had terminated

Corigliano for cause from his positions with the Company.

57. Amy N. Lipton ("Lipton") came to CUC in 1987 as its first lawyer. She was

)vice president and CUC's general counsel until the Merger. After the Merger, Lipton became

general counsel of Card Member Services ("CMS"), a subsidiary of Cendant, as well as deputy

general counsel and executive vice president of Cendant. Lipton reported to Bell until his

departure in 1995, and then to Shelton. After the Merger, she reported to Buckman.

18

58. Anthony L. Menchaca ("Menchaca") came to CUC in July 1985 and held a

variety of positions thereafter. In 1995, he became president of the Comp-U-Card division, and

reported to McLeod. When McLeod became CEO of the Software division in early 1997,

Menchaca began reporting to Shelton and continued to do so until April 1998. After the Merger.

Menchaca continued to run Comp-U-Card and in April, 1998 he was named Co-Chairman of

what is now known as Cendant's Alliance Marketing Group, comprising Comp-U-Card and the

other former membership businesses of CUC.

59. John H. Fullmer ("Fullmer") came to CUC in April 1980 and held a variety of

positions over the years in the areas of marketing, sales and product development. He became

executive vice president of the Comp-U-Card division in March, 1991, and chief marketing

officer of CUC in April, 1996, titles he held until the Merger. In April, 1998, he became co-

) chairman of the Alliance Marketing Group, along with Menchaca. He is also the Chief

Marketing Officer of Cendant.

60. Tobia Ippolito ("Ippolito") was Cendant's Vice President and Corporate

Controller throughout the class periods.

61. Anne M. Pember ("Pember") replaced Corigliano as the corporate controller of

the Comp-U-Card division in April, 1995. Pember previously had been employed by E & Y

from 1981 through 1983, and had joined CUC in March, 1989. During her tenure as controller of

Comp-U-Card, Pember reported to Corigliano. In June, 1997 she was promoted to senior vice

president and controller for CUC and continued to report to Corigliano. After the Merger,

Pember did not assume a new title and continued in her role as senior vice president while

management reorganized her CUC responsibilities into a new position.

19

62. Casper Sabatino ("Sabatino") joined CUC as the Manager of Financial

0 Reporting in 1985. He was promoted to director of Financial Reporting in approximately 1988

and then to vice president of Accounting and Financial Reporting in June, 1991. Sabatino

currently is the vice president of Business Development for Cendant. Prior to 1998, Sabatino0

reported principally to Corigliano and Pember. Since March, 1998, Sabatino has reported to Scott

Forbes.

63. Kevin T. Kearney ("Kearney") joined CUC in 1993 as Manager of Financial

Reporting in the corporate office in Stamford, reporting to Sabatino. Prior to coming to CUC,

Kearney worked for E&Y for approximately four years. Kearney was promoted to director of

Financial Reporting around July, 1995, and continued to report to Sabatino. Ile became the

controller of Spark in March, 1997 and remains in this position.

64. Kathleen M. Mills ("Mills") came to CUC as a junior accountant in the Comp-

U-Card division's revenue accounting area in 1991 and remained in that position until July,

1993. Mills was the supervisor of the Financial Reporting Department of CUC from July, 1993

to October, 1995. Mills was promoted to manager of Financial Services or CUC in October,

1995 and remained there until June, 1997.

B

65. Mary Sattler ("Saltier") came to CUC as supervisor of Financial Reporting in

December, 1995 and remained in that position until the Merger. Prior to coming to CUC, Sattler

was employed as a staff accountant at E&Y. Sattler is currently the manager of Financial

Reporting of Cendant. Sattler reported to Kearney who reported to Sabatino prior to Kearney's

move to Spark in 1997. After June, 1997, Sattler reported to Pember.

20

66. Steven P. Speaks ("Speaks") joined SafeCard Services, Inc., a subsidiary of

Ideon based in Cheyenne, Wyoming, as controller for Client Services in July, 1993 and thereafter

held various positions.

67. Bruce B. Tolle ("Tolle") joined CUC as a supervisor of the General Ledger of

the Comp-U-Card division in 1997. Tolle was promoted to the position of manager of the

General Ledger of CMS in March, 1998. Tolle reported to Paul J. Hiznay ("Hizany"),

Accounting Manager, before Hiznay left CUC in October, 1997. After Hiznay left, Tolle

reported to Speaks.

68. The E&Y partner in charge of the audits of CUC's financial for the years ended)

December 31, 1997 and January 31, 1997 was Marc Rabinowitz ("Rabinowitz") and the review

partner was Louis Scherra ("Scherra").

IV. BACKGROUND

A. CUC MERGES WITH HFS AND CHANGESNAME TO CENDANT

)

69. On May 27, 1997, CUC and HFS entered into a merger agreement. The

Merger was approved by the shareholders of both companies on October 1, 1997, and was com-

pleted on December 17, 1997. CUC was the surviving entity and was renamed Cendant Corpora-

)tion.

70. Pursuant to the Plan for Corporate Governance (the "Governance Plan")

executed in connection with the Merger, the Cendant Board was expanded to twenty-eight)

members, fourteen of whom were to be appointed by CUC and fourteen by HFS. The

Governance Plan provided that the compensation and audit committees would each be comprised

)

21

of two directors appointed by CUC and two by HFS. It also established the managerial positions

that the CUC and HFS officers would occupy in the new entity and provided for the succession

of leadership in the year 2000. As part of this Governance Plan, Silverman was to serve as CEO

irnmediately after the Merger—and for his team to run the combined companies—while Walter

Forbes was to serve as chairman of the Cendant Board. The two men would then shift positions

on January I, 2000.

71. Also pursuant to the Governance Plan, most of the former executives of both

HFS and CUC remained with Cendant. Furthermore, CUC's financial and accounting personnel

continued to obtain and consolidate the financial information from the different CUC units.

including Comp-U-Card, its largest subsidiary. (Report at 51.)

72. As a result of the Merger, senior management of both companies received

additional benefits including in most cases increased base salaries, increased bonus

compensation, improved severance benefits, additional stock options, immediate vesting of

certain options, and in the case of CUC management, lapsing of restrictions on restricted stock

and acceleration of lump sum payments under the senior executive retirement plan. (Report at

46.).

B. THE PRIDES OFFERING AND SURROUNDINGCIRCUMSTANCES

73. On January 27. 1998, Cendant made a proposal to acquire American Bankers

Insurance Group Inc. ("American Bankers") for an aggregate purchase price approximating $2.7t$

billion on a fully diluted basis. In connection with the proposal to acquire American Bankers,

Cendant entered into a commitment letter dated January 23, 1998, with The Chase Manhattan

22

)

Bank, and Chase Securities Inc., one of the defendant underwriters here, to provide a $1.5 billion

364-Day revolving credit facility, the same approximate amount that the PRIDES would realize

upon their sale.

74. On January 29, 1998, a few days after Cendant's announced proposal to)

acquire American Bankers, Cendant filed with the SEC a registration statement which eventuated

into the issuance of 26,000,000 PRIDES expected to raise for Cendant at least $1,265,000,000

) and possibly $1.5 billion (considering the underwriters' additional allotments). This registration

statement was amended on three occasions—February 6, 1998, February 17, 1997 and February

20, 1998—before it became effective. The final Prospectus for the PRIDES offering is dated

February 24, 1998 and was filed with the SEC on February 26, 1998. The PRIDES Offering

commenced on February 24, 1998.

)

75. The Registration Statement and Prospectus offered two types of FELINE

PRIDES for sale: Income PRIDES and Growth PRIDES. In general, the Income PRIDES pay a

specified amount to the holders thereof for three years and then, at maturity, are automatically

)converted into Cendant common shares. The Income PRIDES and similar types of securities

have been extremely popular because they offer a high rate of return and a greater potential

equity upside than normal convertible securities. There was such a demand for the Income

PRIDES that the Offering was increased by $300 million above the amount initially planned.

76. Specifically, each of the Income PRIDES consists of a unit comprised of a

Purchase Contract under which the holder will purchase from Cendant on February 16, 2001 for

$50 (the "Stated Amount") in cash, a specified number of newly issued shares of Cendant

common stock, and Cendant will pay to holders "Contract Adjustment Payments" at the rate of

23

5% of the Stated Amount per annum, and an interest in Trust Preferred Securities ("Trust

Preferred Securities") paying 6,45% of the Stated Amount per annum, and paying the holders

$50 at maturity. Holders own the Trust Preferred Securities, but pledge them to the Company to

secure their obligations under the Purchase Contract. Pursuant to the terms of the Registration

Statement, Cendant Capital I acts as the Indenture Trustee for the Trust Preferred Securities

pledged by the purchasers of Income PRIDES.

77. Each of the Growth PRIDES consists of a unit comprised of a Purchase

Contract under which the holder will purchase from the Company on February 16, 2001 for the

Stated Amount in cash, a specified number of newly issued shares of Cendant common stock,

and Cendant will pay to holders "Contract Adjustment Payments" at the rate of 5 €1/0 of the Stated

Amount per annum, and a 1/20th undivided beneficial interest in a treasury security having a

principal amount of $1000 and maturing in 2001.

78. The trading price of the Income and Growth PRIDES in the secondary market

was and is greatly dependent on the financial performance of Cendant. As acknowledged in the

Registration Statement and Prospectus:

The trading prices of Income PRIDES and GrowthPRIDES in the secondary market will be directly affected bythe trading prices of the Common Stock in the secondarymarket, the general level of interest rates and the credit qualityof the Company. It is impossible to predict whether the price ofthe Common Stock or interest rates will rise or fall. Tradingprices of the Common Stock will be influenced by theCompany's operating results and prospects and by economic,financial and other factors and market conditions that can affectthe capital markets generally, including the level of, andfluctuations in, the trading prices of stocks generally and salesof substantial amounts of Common Stock in the marketsubsequent to the offering of the Securities or the perception

24

that such sales could occur. Fluctuations in interest rates maygive rise to opportunities of arbitrage based upon changes in therelative value of the Common Stock underlying the PurchaseContracts and of the other components of the FELINEPRIDES. Any such arbitrage could, in turn, affect the tradingprices of the Income PRIDES, Growth PRIDES, TrustPreferred Securities and Common Stock.

)

(Id at S-29 - S-30.)

79. The Offering was underwritten by Merrill and Chase.

) 80. The Offering closed on March 2, 1998, with Cendant announcing that Merrill

and Chase had exercised their option to purchase an additional allotment of $195 million of

PRIDES. Thus, the Offering succeeded in raising approximately $1.5 billion for Cendant, less)

expenses, or an amount roughly equivalent to the increased debt Cendant intended to assume in

order to complete the American Bankers transaction.

)

81. Of this amount the Underwriter Defendants realized approximately $43 million

in underwriting commissions.

82. On March 5, 1998, Cendant filed with the SEC a Form 8-K concerning the

)March 2, 1998 consummation of the Offering.

V. CLAIMS UNDER SECTIONS 11 AND 12(a)(2) OF THE SECURITIES ACT

A. THE MATERIALLY FALSE AND MISLEADINGREGISTRATION STATEMENT

83. Among other financial statements, report and information, the Registration

Statement and Prospectus contained the following:

A. Cendant's Consolidated Balance Sheets for the years ended December31, 1996 and 1995 (audited) (Registration Statement and Prospectus atF3);

25

B. Cendant's Consolidated Statements of Income for the years endedDecember 31, 1996, and 1995 (audited) (Registration Statement andProspectus at F-5). More specifically, concerning its 1996 results,Cendant reported net income of $423.6 million or diluted earnings pershare of $0.52, and revenues of $3.9 billion; and as to its 1995 results,reported revenues of $3.0 billion or a diluted earnings per share of $0.42,and net income of $302.8 million.

C. Cendant's Consolidated Balance Sheets for September 30, 1997(unaudited) (Registration Statement and Prospectus at p. F-55 - F-56);

D. Cendant's Consolidated Statements of Income for the three monthsended September 30, 1997 (unaudited) (Registration Statement andProspectus at F-57): Cendant reported net income of $248.3 million ordiluted earnings per share of $0.28, and revenues of $1.4 billion; and forthe three months ended September 30, 1996 (id): reported net income of$68.5 million or diluted earnings per share of $0.08, and revenues of $1.0billion; and

E. Cendant's Consolidated Statements of Income for the first nine monthsended September 30, 1997 (unaudited) (Registration Statement andProspectus at F-57): Cendant reported net income of $400.7 million ordiluted earnings per share of $0.47 per share, and revenues of $3.9billion; and for the first nine months ended September 30, 1996 (id.):reported net income of $265.5 million or diluted earnings per share of$0.33, and revenues of $2.8 billion.

84. Furthermore, the Registration Statement and Prospectus also described

Cendant's consolidated financial results for the 1997 year ended December 31, 1997, which

results it had first announced on February 4, 1998 (Registration Statement and Prospectus at S-

P37). More specifically, in the section of this document entitled "Recent Developments," Cendant

stated:

On February 4, 1998, the Company announced its financialresults for the year ended December 31, 1997. The Companyreported diluted earnings per share of $1.00 for 1997, a 49%increase compared to $.67 earnings per share reported for 1996,excluding one-time charges recognized in both 1997 and 1996.The Company had revenues of $5.3 billion for 1997, compared

26

with $3.9 billion for 1996, an increase of 36%, and net incomeof $872.2 million for 1997, excluding one-time charges,compared with $542.3 million of 1996, excluding one-timecharges, an increase of 61%. On a pro forma basis, whichassumes that the financial results include all of the Company's1996 acquisitions, accounted for under the purchase method, asif they had occurred as of January 1, 1996, earnings per sharefor the year ended December 31, 1997, excluding one timecharges, was $1.00 representing a 43% increase over pro forma$.70 per share for the year ended December 31, 1996.

When giving effect to one-time charges, the Companyreported $.06 diluted earnings per share for the year endedDecember 31, 1997 and net income of $55A million for 1997compared to $423.6 million for 1996. In 1997, one-timecharges totaled $1.1 billion ($816.8 million after tax, or $.94per share) for merger related costs and unusual charges . . . . In1996, one-time charges totaled $179.9 million ($118.7 million

6 after-tax, or $.15 per share) related to three CUC mergers.

85. Cendant's consolidated audited results for the year ended December 31, 1997

were filed with the SEC on March 31, 1998 on a Form 10-K, which included E&Y's unqualified

audit opinions on CUC's financial statements for fiscal 1997 and 1996.

86. The financial data and results reported in the Registration Statement and

Prospectus for 1997, 1996 and 1995 (both year-end and quarterly information) detailed above

were materially false and misleading, as Cendant has subsequently admitted on numerous

occasions.

87. Because Deloitte, Cendant's current auditor at the time of the Offering, was not

involved in the fiscal 1995, 1996 or 1997 audits of CUC or HFS, it issued the following

statement in the Registration Statement and Prospectus:

In our opinion, based on our audits and the reports of .. . otherauditors, the consolidated financial statements referred to [para-graphs above] present fairly, in all material respects, thefinancial position of Cendant Corporation and subsidiaries at

27

December 31, 1996 and 1995, and the results of theiroperations and their cash flows for each of the three years in theperiod ended December 31, 1996 in conformity with generallyaccepted accounting principles.

Id at F-2. Deloitte further represented, as per the audits of the "other auditors," that CUC had "total

assets of approximately $2.5 billion and $2.1 billion as of January 31, 1997 and 1996, respectively,

and net income of approximately $164.1 million, $145.0 million and $164.1 million for the years

ended January 31, 1997, 1996 and 1995, respectively."

88. The Registration Statement and Prospectus expressly referred to E&Y's audit

opinions on CUC's financials and incorporated them by reference. In this regard both the

1r Registration Statement and Prospectus, through this attached document, stated under a section

captioned "Experts":

The consolidated financial statements of the Company and itsconsolidated subsidiaries, except PHH Corporation ("PHH"),as of December 31, 1996 and January 31, 1996 and for theyears ended December 31, 1996, January 31, 1996 and 1995and CUC International Inc. ("CUC") as of January 31, 1997and 1996 and for each of the three years in the period endedJanuary 31, 1997 incorporated in this Prospectus by referencefrom the Company Form 8-K dated January 29, 1998, havebeen audited by Deloitte & Touche LLP, as stated in theirreport which is incorporated herein by reference. The financialstatements of PHH (consolidated with those of the Company)have been audited by KPMG Peat Marwick LLP, independentauditors of P1111 Corporation, as stated in their reportincorporated herein by reference. . . . The consolidatedfinancial statements of CUC (consolidated with those of theCompany) have been audited by Ernst & Young LLP, as setforth in their report included in the Current Report on Form8-K, dated January 29, 1998 incorporated herein by reference. . . Such supplemental consolidated financial statements of theCompany and its consolidated subsidiaries are incorporated byreference herein in reliance upon the respective reports of such

28

firms given upon their authority as experts in accounting andauditing. All of the foregoing firms are independent auditors.

Registration Statement, Prospectus at 28 (emphasis added).

89. Furthermore, the Form 8-K filed by Cendant dated January 29, 1998 incorporated

in the Registration Statement and Prospectus (id.; see also Registration Statement at S-38, S-42, and

Prospectus at S-39, S-43), included E&Y's March 10, 1997 audit report ("March 10, 1997 Audit

Report") on CUC's financial condition for "each of the three years in the period ended January 31,

1997." In this letter E&Y further represented:

We conducted our audits in accordance with generally acceptedauditing standards. Those standards require that we plan andperform the audit to obtain reasonable assurance about whetherthe financial statements are free of material misstatement. Anaudit includes examining, on a test basis, evidence supportingthe amounts and disclosures in the financial statements. Anaudit also includes assessing the accounting principles used and

fs significant estimates made by management, as well asevaluating the overall financial statement presentation. Webelieve that our audits and the reports of other auditors providea reasonable basis for our opinion.

In our opinion, based upon our audits and the reports of otherauditors, the consolidated financial statements referred to abovepresent fairly, in all material respects, the consolidated financialposition of CUC at January 31, 1997 and 1996, and theconsolidated results of its operations and its cash flows for eachof the three years in the period ended January 31, 1997, inconformity with generally accepted accounting principles.

(January 29, 1998 SEC Form 8-K, Exhibit 99.1 at 2.) (Cendant's January 29, 1998 Form 8-K is

Exhibit A in the accompanying Appendix.)

90. Thus, the March 10, 1997 Audit Report was incorporated by reference into the

Registration Statement and Prospectus. Simultaneously, also incorporated by reference was the

29

unaudited computation of Cendant's per share earnings for the three and six-month period ended

June 30, 1997 and for the three and nine-month period ended September 30, 1997.

91. E&Y consented to the incorporation by reference into the Registration State-

ment and Prospectus of its March 10, 1997 Audit Report. Attached to Cendant's Amendment

No. 2 to Form S-3 Registration Statement, filed by the Company on February 17, 1998 in prepa-

ration for the PRIDES Offering, is E&Y's express consent to be referenced as an "expert," which

states:

We consent to the reference to our firm under the caption"Experts" and to the use of our report dated March 10, 1997,included in the Current Report on Form 8-K, dated January 29,1998, with respect to the consolidated financial statements ofCUC International, Inc. incorporated by reference in Amend-ment No. 1 to Form S-3 Registration Statement (No. 333-45227) and related Prospectus of Cendant Corporation(formerly "CUC International Inc.") for the registration of upto $4,000,000,000 of its debt securities, preferred stock and/orcommon stock.

(Registration Statement at Exhibit 23.2.)

92. The March 10, 1997 Audit Report incorporated into the Registration Statement

and Prospectus, as well as the other incorporated unaudited Cendant's per share earnings for the

three and six-month period ended June 30, 1997 and for the three and nine-month period ended

September 30, 1997, were materially false and misleading.

B. CENDANT'S ADMISSIONS AS TO THE FALSITY OF THEFINANCIAL INFORMATION CONTAINED IN THEREGISTRATION STATEMENT AND PROSPECTUS

93. On April 15, 1998, less than six weeks after the consummation of the PRIDES

Offering, Cendant first admitted that the financial results which were reported in the Registration

30

Statement were materially overstated. At that time it announced that it had discovered

accounting irregularities that caused it to overstate net income for 1997 by approximately $100-

$115 million, and earnings per share by approximately $0.1140.13, before restructuring and

unusual charges. As already detailed, in the Registration Statement and Prospectus. Cendant

reported net income of $872.2 million and earnings per share of $1.00, before restructuring and

unusual charges. The pertinent parts of Cendant's April 15, 1998 press release stated:

[Cendantj today reported that, in the course of trans-ferring responsibility for the Company's accounting functionsfrom former [CUC] personnel to former [HFS] accounting per-sonnel and preparing for the reporting of first quarter 1998results, it has discovered potential accounting irregularities incertain former CUC business units which are part of Cendant'sAlliance Marketing Division (formerly the Membership seg-ment). Accordingly, Cendant said it expects to restate annualand quarterly net income and earnings per share for 1997 andmay restate certain other previous periods related to formerCUC businesses.

Based on presently available information, the effect on1997 results is expected to be a reduction to net income priorto restructuring and unusual charges of approximately $100 to$115 million and earnings per share by about 11 to 13 cents,respectively. . .

Cendant said the potential accounting irregularities arelimited to certain former CUC businesses, which accounted forless than one third of Cendant's net income in 1997.

94. In its April 15, 1998 announcement, Cendant also reported that its Audit

Committee had engaged Willkie Farr as special legal counsel, which had retained Anderson, to

perform an independent investigation of the accounting irregularities.

95. On April 14, 1998, Steven Speaks and Casper Sabatino signed affidavits that

swore to facts that pertained to the Cendant April 15, 1998 press release respecting accounting

irregularities.

31

96. The market responded to the April 15, 1998 announcements by reducing

Cendant's market capitalization by approximately $14 billion. Cendant's stock price plunged

from the April 15 closing price of $35 518 per share to close at $19 1/16 per share, reflecting

more than a 46% drop on April 16, 1998. At the same time, the price of the Income PRIDES fell0

from $49-3/16 to $33-3/4, a more than 31% drop, while the Growth PRIDES dropped from $42-

1/8 to $25-3/4, a more than 38% drop.

97. Prior to this April 15, 1998 announcement, there had been no public disclosure

of any impropriety in Cendant's reported results. When on April 9, 1998, Cendant had

announced the resignation of its vice chairman, defendant Shelton, and two other top officials,ty

Amy Lipton and defendant Corigliano—all former CUC officers—it had stated only that they

were leaving "to pursue other interests." It was only on April 17, 1998 that Cendant

acknowledged that defendant Corigliano had been terminated.

98. In press releases issued on July 14, 1998, Cendant disclosed that its overstate-

ment of net income for 1977 was more than double what it had reported on April 15, 1998 and

that in addition to 1997, it would also have to restate its financial statements for 1996 and 1995

for an aggregate $250 million, pretax, for accounting irregularities alone. It further disclosed that

in connection with the restatements, Deloitte had replaced E&Y as CUC's auditor.

99. More specifically, Cendant announced:

"In addition, Cendant's investigation now confirms thataccounting irregularities existed in CUC's financialstatements in years prior to 1997 and that in addition to 1997,1996 and 1995 results will be restated to correctirregularities.

. . . .

32

7

Cendant now believes its restatement will lower 1997 netincome before merger-related and one-time charges by 22 to28 cents per share. . . . . Between 16 and 19 cents of the 22to 28 cent 1997 impact of restatement will result from thecorrection of accounting irregularities.

100. Cendant then went on to explain "some of the most significant irregularities

now confirmed".

101. Cendant additionally stated in this release that it "expects to provide detailed

information regarding all material CUC irregular accounting practices when it releases its

restated and re-audited financial statements for the 1995-1997 period."

102. In another release issued later on July 14, 1998, "Cendant said that 1996 and

1995 will be impacted by many of the same items that affected 1997. . . In addition,.. . CUC

also overstated its quarterly results by recording fictitious revenues." The company then

acknowledged that "Nile amounts that are expected to be restated from accounting irregularities

are, on a pre-tax basis, approximately $150 million for 1996 and $100 million for 1995."

103. These July 14, 1998 announcements led to further declines in the prices of both

PCendant common stock and PRIDES. Cendant's stock price dropped from the previous day's

close of $18-7/8 per share to close at $15-11/16 per share on July 14 reflecting an approximate

drop of 17%; the Income PRIDES' price dropped from the previous day close of $34-3/32 per

unit to close at $30-1/4 per unit on July 14, reflecting an approximate drop of 11%; and the

Growth PRIDES' price dropped from the previous day's close of $29-3/8 per unit to close at

$25 per unit on July 14, reflecting an approximate drop of 15 %.

104. On July 28, 1998, Walter Forbes and eight additional members of Cendant's

Board, with prior CUC affiliations, resigned, effective iminediately. The Company also

33

disclosed that the one remaining Cendant director with past CUC affiliation would resign before

the end of 1998.

105. On August 13, 1998, Cendant announced that "its investigation of accounting

irregularities and errors in the CUC businesses was complete." Defendant Monaco was quoted in

this release as stating: "[W]e have unflinchingly accepted and reported Ethel results [of this

investigation]."

106. In this August 13, 1998 release, the Company further disclosed:

[Cendant's} final calculation of the impact of accountingirregularities and errors on its 1997, 1996 and 1995 full yearresults. Cendant will lower 1997 results by $0.28 per share or$392 million pretax. The net impact of this restatement plus$0.02 of discontinued operations will lower net income fromcontinuing operations before one-time merger and otherunusual charges to $0.70 per share versus the $1.00 per sharepreviously [included in the Registration Statement andProspectus} reported. A substantial amount of the adjustmenthad the impact of reducing revenues.

. . .

Cendant will lower 1996 results by $0.18 per share. Cendanthas also determined that certain one-time merger charges takenby CUC in 1996 should be reversed and will eliminate $0.02per share of these charges. 1995 results will be lowered by$0.14 per share.

107. On August 28, 1998, Cendant filed with the SEC a Form 8-K containing

certain "Additional Conclusions of the Audit Committee . . . With Respect to Investigation Into

Accounting Irregularities," the Report, an Addendum to the Report, and a related press release

dated August 27, 1998 concerning the presentation of the Report by the Audit Committee to the

Cendant Board, and a brief description of the Report.

f

34

108. On September 29, 1998, the Company issued a Form 10-K/A ("Amended

10-K") amending the Form 10-K for the year ended December 31, 1997 that it had previously

filed with the SEC on March 31 1997. In this document, Cendant restated "its previously

reported financial results for 1997, 1996 and 1995." (Amended 10-K at 4.) More specifically:

The restated net income (loss) totalled $(217.2) million,$330.0 million and $229.8 million in 1997, 1996 and 1995,respectively ($(0.27), $0.41 and $0.31 per diluted share,respectively). The Company originally reported corresponding

4 net income of $55.4 million, $423.6 million and $302.8 millionin 1997, 1996 and 1995, respectively ($0.06, $0.52 and $0.42per diluted share, respectively).

The Company originally reported $872.2 million of 1997net income excluding merger-related costs and other unusualcharges ("Unusual Charges") or $1.00 per diluted share whichincluded $816.2 million or $.94 per diluted share from continu-ing operations. The restated income from continuing

• operations excluding Unusual Charges, extraordinary gain andthe cumulative effect of a change in accounting totaled $571.0million or $.66 per diluted share. The $245.2 million or $.28per diluted share decrease in income from continuingoperations represents additional after tax expense of $15.3million ($.02 per diluted share) due to ... change in accountingand $229.9 million ($.26 per diluted share) of accounting errorsand irregularities.

The Company originally reported $542.3 million and$364.9 million of 1996 and 1995 net income excludingUnusual Charges, respectively ($0.67 and $0.50 per dilutedshare, respectively). The restated income from continuingoperations excluding Unusual Charges totaled $383.3 millionand $269.2 million in 1996 and 1995, respectively ($0.47 and$0.36 per diluted share, respectively). The $159.0 million and$95.7 million decreases in 1996 and 1995, respectively,primarily represent accounting errors and irregularities in bothperiods.

35

(Id.) (Cendant's September 29, 1998 Form 10-K/A is Exhibit N in the accompanying

Appendix.)

109. Furthermore, in this Amended 10-K, Cendant restated its previously reported

revenues for the 1995 through 1997 years—its actual revenues for 1997 were $4.2 billion rather

than the previously reported $5.3 billion, for 1996 it was $3.2 billion rather than the previously

reported $3.9 billion, and for 1995 it was $2.6 billion rather than the previously reported $2.9

billion. (Id. at F6, F18-F24.)

110. In this Amended 10-K, Cendant admitted that the restatements resulted mostly

from the accounting irregularities and errors revealed by the Company's own investigation and

the Audit Committee's investigation. (Id. at 3-4.)

111. Below is a chart of the some of the material differences between the financial

statements as reported in the Registration Statement and Prospectus and the Amended 10-K:

As PreviouslyReported As Restated

Periods Reported In The Registration Statement and Prospectus

For the Year Ended December 31, 1997:Revenue $ 5,314.7 $4,240 .0Merger related costs & other unusual charges 1,147.9 704.1Cumulative effect of accounting change -0- (283.1)Net income (loss), 55.4 (217.2)Net income (loss) per common share (diluted) 0.06 (0.27)

For the Year Ended December 31, 1996:Revenue $ 3,908.8 $ 3,237.7Merger related costs & other unusual charges 179.9 109.4Income from continuing operations 713.7 533.5Cumulative effect of accounting changes -0- -0-Net income (loss) 423.6 330.0Net income (loss) per common share (diluted) 0.52 0.41

36

For the Year Ended December 31, 1995:Revenue $ 2,992.1 $ 2,616.1Merger related costs & other unusual charges 97.0 97.0Income from continuing operations 503.3 350.3Cumulative effect of accounting change -0- -0-Net income (loss) 302.8 229.8Net income (loss) per common share(diluted) 0.41 0.31

As of December 31, 1996:Total assets $13,588.4 $12,762.5Total liabilities 9,265.7 8,806.8Total stockholders' equity 4,322.7 3,955.7

112. In other words, the consolidated financial statements and results for 1995

through 1997 contained in the Registration Statement and Prospectus overstated the Company's

net income by 439.2 million, its operating income before taxes by $500 million and its revenues

by $2.1 billion.

113. In its Form 8-K filed with the SEC on October 21, 1998, Cendant provided

financial schedules summarizing restated revenue and EBITDA by business segment for all four

quarters of 1997 and the first two quarter of 1998. This document demonstrates the following

overstatements contained in the Registration Statement and Prospectus (at F-57) concerning the

Company's consolidated results for the three months ended September 30, 1997: overstatement

of revenues by $102.9 million and EBITDA by $75.7 million.

114. Thus, Cendant has acknowledged that all the financial data presented in the

Registration Statements and Prospectus concerning the 1995 through 1997 period, whether

quarterly or yearly information, were materially misstated.

37

C. THE NATURE OF THE ACCOUNTING IRREGULARITIES INCENDANT'S FINANCIAL STATEMENTS

115. The Audit Committee Report details the numerous accounting manipulations

that were used to overstate Cendant's consolidated financial results for the 1995 through 1997

years ("Restatement Period"), and also its quarterly results for this period.

116. The Report by Willi& and Andersen was submitted to the Audit Committee,

which preliminarily approved the Report on August 24, 1998 and thereafter finally approved it

before its filing with the SEC on August 28, 1998. (Addendum to Report of the Audit

Committee of the Board of Directors of Cendant Corporation, Exhibit 99.3 to Cendant's report on

SEC Form 8-K filed on August 28, 1998.). The Report was presented to Cendant's full board of

directors on Aug. 27, 1998. (Press Release Aug. 27, 1998)

117. The Report details numerous accounting irregularities and improper accounting

practices that occurred at CUC, which resulted in the already detailed overstatement of Cendant's

consolidated results and CUC's own reported results for the 1995 through 1997 period. The

irregularities can be categorized into five broad categories. (Report at 9.)

1. Topside Adjustments to Quarterly Results

118. At each of the first three fiscal quarters since 1995, CUC inflated its operating

income by increasing revenues and/or decreasing expenses of its largest business unit, the

Comp-U-Card division in Trumbull, Connecticut, without any valid basis. So-called "topside"

entries were made by accounting personnel at corporate headquarters to increase accounts

receivable and revenues, or to decrease accounts payable and expenses, although (as these

personnel acknowledged) there was no actual receivable supporting the entry giving rise to the

revenues, and no actual reduction of a payable obligation to justify the reduced expense. The

38

>

topside entries were not recorded on any general ledger, thereby creating a discrepancy between

the adjusted figures and those reflected on CUC's actual books and records. The amount of these

quarterly adjustments increased during the Restatement Period, from $31 million pretax income

in 1995 to $87 million in 1996 to $176 million in 1997. (Report at 9-10, 68-70, 71-99.)

119. The amount of the income adjustments at each quarter closely mirrored the

amount needed to bring CUC's results into line with Wall Street earnings expectations, e.g., if

actual income in a particular quarter was 10(cents) per share and consensus analysts'

expectations were 18(cents) per share, then adjustments of approximately 8(cents) were made,

without support, to increase earnings. (Report at 10-11, 69, 75-76, 82-87.)

120. The inflated earnings results were then publicly reported and presented to the

CUC Board at each quarter. Because these results were often above the combined budgets of

CUC's individual business units for the quarters, the consolidated quarterly budget figures

presented to the CUC's Board that accompanied the financial results were frequently increased at

corporate headquarters to eliminate any substantial variance. (Id.)

121. In addition to adjusting CUC's income at each quarter to meet Wall Street

expectations, CUC also made quarterly unsupported topside adjustments to its balance sheet,

particularly to show a greater cash balance than CUC actually had on its books. These adjust-)

ments were generally made in conjunction with the earnings adjustments described above.

(Report at 71-99.)

2. Irregularities Involving Utilization of Merger Reserves

122. As a result of the quarterly topside adjustments to earnings, there was a

substantial gap between what was reported to the public and what was recorded on CUC's books.

39

'71

To help close this gap, CUC made various year-end adjustments to its books to increase revenues

or decrease expenses. In 1997, these largely took the form of reversals of previously established

merger and restructuring reserves into income, by decreasing the reserves and correspondingly

increasing income (again either by increasing revenues or decreasing expenses) through

numerous unsupported journal entries. Unsupported journal entries to reduce reserves and

increase income were made after year-end and backdated to prior months; merger reserves were