Embed Size (px)

Citation preview

How does earnings management influence investor’sperceptions of firm value? Survey evidencefrom financial analysts

Abe de Jong • Gerard Mertens •

Marieke van der Poel • Ronald van Dijk

Published online: 8 October 2013

� Springer Science+Business Media New York 2013

Abstract Survey evidence shows CFOs to believe that earnings management can

enhance investor valuation of their firms. This evidence raises the question of

correspondence between the beliefs of CFOs and investors. Surveying financial

analysts to gain insight into how earnings management influences investor per-

ception of firm value, we find analysts’ and CFOs’ beliefs to be generally consistent.

We find that analysts perceive meeting earnings benchmarks and smoothing earn-

ings to enhance investor perception of firm value and all earnings management

actions to reach a benchmark, save share repurchases, to be value destroying. CFOs,

however, are reluctant to repurchase shares, preferring to use techniques viewed by

analysts as value destroying (e.g., reductions in discretionary spending). Analysts’

inability to unravel such techniques perhaps explains CFOs’ preferences.

Opinions expressed in this article strictly represent the authors’ personal views and opinions and cannot

in any way be construed as statements or views of APG.

A. de Jong � M. van der Poel

Rotterdam School of Management, Erasmus University, PO Box 1738, 3000 DR Rotterdam,

The Netherlands

e-mail: [email protected]

M. van der Poel

e-mail: [email protected]

A. de Jong

University of Groningen, PO Box 800, 9700 AV Groningen, The Netherlands

G. Mertens (&)

Faculty of Management, Science and Technology, Open Universiteit Nederland, PO Box 2960,

6410 DL Heerlen, The Netherlands

e-mail: [email protected]

R. van Dijk

APG Asset Management, PO Box 75283, 1070 AG Amsterdam, The Netherlands

e-mail: [email protected]

123

Rev Account Stud (2014) 19:606–627

DOI 10.1007/s11142-013-9250-y

Keywords Financial reporting � Earnings management � Earnings

benchmark � Earnings smoothing � Financial analysts � Financial executives

JEL Classification M41

1 Introduction

According to survey evidence, CFOs believe that earnings management can enhance

investor valuation of their firms (Graham et al. 2005; Graham et al. henceforth). The

evidence suggests that they are even willing to sacrifice economic value to fulfill

investors’ earnings expectations. The importance CFOs attach to investors raises the

question of correspondence between the beliefs of CFOs and investors. Taking as

our research question how earnings management influences investor perception of

firm value, we conduct a large-scale survey and interviews with sell-side analysts.

Empirical studies show analysts, who are experienced, well-trained observers of

financial reporting and sources of investment advice, to be important for investor

attention, price setting, and liquidity (e.g., Brown and Rozeff 1978; Womack 1996;

Graham et al.; Anantharaman and Zhang 2011; Mola et al. 2012).

We present survey and interview evidence of analysts’ views on policies for such

corporate financial reporting mechanisms as earnings benchmarks, within-GAAP

earnings management, and earnings smoothing. Asking analysts questions similar to

those to which CFOs responded in Graham et al. enables us to describe analysts’

views in conjunction with those of the CFOs. Our survey (which achieved a 48 %

response rate) of 306 analysts employed by 11 of the world’s largest investment

banks was complemented by interviews with 21 analysts.

The study addresses three specific questions. The first concerns analysts’ beliefs

regarding the importance of meeting earnings benchmarks. We find analysts to share

CFOs’ beliefs about the importance of stock-price-related motivations for meeting

benchmarks. Analysts’ views suggest that analysts perceive long-term consequences

to accrue to meeting or missing short-term earnings benchmarks. This perception of

long-term consequences is perhaps explained by analysts’ awareness that firms

manage their earnings to benchmarks. Our interviews corroborate this explanation.

Some analysts, for instance, posit that a firm that fails to meet its earnings

benchmark lacks the flexibility to bridge the gap between earnings and benchmark

by managing its earnings to the benchmark.

The second question explores analysts’ views of the value implications of using

different types of within-GAAP earnings management techniques to achieve earnings

benchmarks. Whereas analysts view all earnings management actions to reach a

benchmark, save share repurchases, as value destroying, CFOs are reluctant to

repurchase shares but willing to take earnings management actions analysts perceive to

be value destroying (e.g., decreasing discretionary spending). Analysts’ inability to

unravel certain earnings management actions might perhaps explain CFOs’ preferences.

The third question we address concerns analysts’ beliefs about how much value a

firm should sacrifice to avoid a bumpy earnings path and the consequences of

earnings smoothing. Our results suggest that analysts recognize the positive

Survey evidence from financial analysts 607

123

consequences of smoothing firms’ earnings paths, believing, for instance, that

smoothing earnings reduces perceived riskiness and that achieving the resulting

benefits is worth a small sacrifice in value. That analysts are nevertheless less

positive than CFOs about smoothing could explain CFOs’ willingness to sacrifice

much more value than analysts recommend. Our findings further indicate that,

although they prefer to follow firms with smooth earnings paths, analysts dislike

firms that intentionally smooth their earnings paths because their performance is

consequently akin to a black box. We infer from their answers that analysts cannot

always unravel earnings management practices.

Overall, our evidence suggests that analysts’ and CFOs’ beliefs are generally

consistent, both believing that meeting earnings benchmarks and smoothing

earnings can enhance investor perception of firm value. Where they differ with

respect to earnings management actions to meet benchmarks is in CFOs’

preferences for decreasing discretionary spending and delaying the start of new

projects and analysts’ view that only share repurchases are value enhancing.

Analysts are also less positive than CFOs about sacrificing value to smooth

earnings.

Our paper contributes to the literature on the market perspective on earnings

management. Empirical evidence in this strand of literature is mixed, with some

studies suggesting that analysts do not anticipate earnings management to achieve a

benchmark (e.g., Abarbanell and Lehavy 2003; Burgstahler and Eames 2003) and

others that analysts rationally anticipate earnings management (e.g., Coles et al.

2006; Kim and Schroeder 1990). Market responses to announcements that earnings

benchmarks have been met, moreover, depend on whether earnings management

was needed to reach the benchmark (e.g., Bartov et al. 2002; Gleason and Mills

2008). A review by Dechow et al. (2010) suggests that difficulty unraveling

earnings management to meet benchmarks potentially explains differing market

responses. Evidence from our survey and interviews suggests that analysts are aware

of earnings management, but their answers to questions on actions and smoothing

indicate that they are not always able to unravel earnings management.

Our paper is also related to the literature on the endogenous interplay between

analysts’ forecasting, and managers’ reporting behavior. Beyer’s (2008) model

posits that managers manipulate earnings in response to analyst forecasts that, in

fact, take earnings management into account. Other papers that model the

interaction between analysts and managers include Dutta and Trueman (2002),

Fischer and Stocken (2004), and Mittendorf and Zhang (2005). Our findings on

analysts’ vis-a-vis CFOs’ beliefs afford a deeper understanding of this interplay. For

example, analysts are aware that firms employ earnings management to reach

benchmarks, but CFOs believe they should manage earnings to benchmarks because

analysts might perceive missing a benchmark to signal negative future prospects.

The survey methodology we use to examine earnings management’s influence on

investor perception of firm value is subject to the following limitations. First, we use

sell-side analysts’ answers as a proxy for investor beliefs. Although analysts, being

sophisticated users of financial information who can influence investor perceptions

of firm value, constitute a good proxy, they are nevertheless intermediaries between

firms and investors and not actual investors. Investors, for example, may not share

608 A. de Jong et al.

123

analysts’ view that all earnings management actions save share repurchases are

value destroying. Analysts’ stated beliefs, moreover, may not match their behavior,

inasmuch as analysts may recommend that firms not smooth their earnings path but

attempt to maximize their forecast accuracy by following firms that do smooth

earnings.

The paper is organized as follows. In Section 2, we describe our research design

and present summary statistics for our survey data. We examine, in Section 3,

analysts’ beliefs regarding the importance of meeting earnings benchmarks, in

Section 4, their beliefs regarding the valuation implications of earnings manage-

ment, and, in Section 5, their beliefs regarding the consequences of earnings

smoothing. Section 6 concludes.

2 Research design, data description, and summary statistics

We collect the opinions of financial analysts via a survey and supplemental

interviews. (‘‘Appendix’’ details our survey design and interview setup.) We draw

heavily on the Graham et al. questionnaire that solicits opinions of CFOs of US

firms to facilitate comparison of CFOs’ and analysts’ perceptions. Asking analysts

to answer the survey questions using a US firm randomly selected from their

portfolios enables us to compare our analyst results with the CFO results of Graham

et al.

We received 306 usable responses (response rate = 48 %). We apply a five-point

scale (coded from -2 to ?2) for most questions and report the average response, the

percentage of responses in categories ?1 and ?2, and the percentage of responses in

categories -1 and -2. Subsequent analyses compare the average answers of our

analyst and the CFO survey in two ways. First, we conduct a standard difference-of-

means t test (referred to in the tables as H0: Difference = 0).1 Because the firm

characteristics of size and industry differ between the CFO and analyst samples, we

regress the response scores of both samples on an analyst dummy that equals one for

observations from our analyst and zero for observations from the CFO sample.

Additional regressors for each regression are dummy variables for revenue (size)

and industry class. The responses being in distinct categories, we use (ordered) logit

regression models. The tables report the significance of the coefficient of the analyst

dummy that represents the size and industry corrected difference between the CFO

and analyst answers (referred to in the tables as H0: Corrected difference b = 0).

We corroborate the survey results and achieve further clarification by means of

the interviews with 21 financial analysts in four institutions, a subset of the

investment banks in our survey.

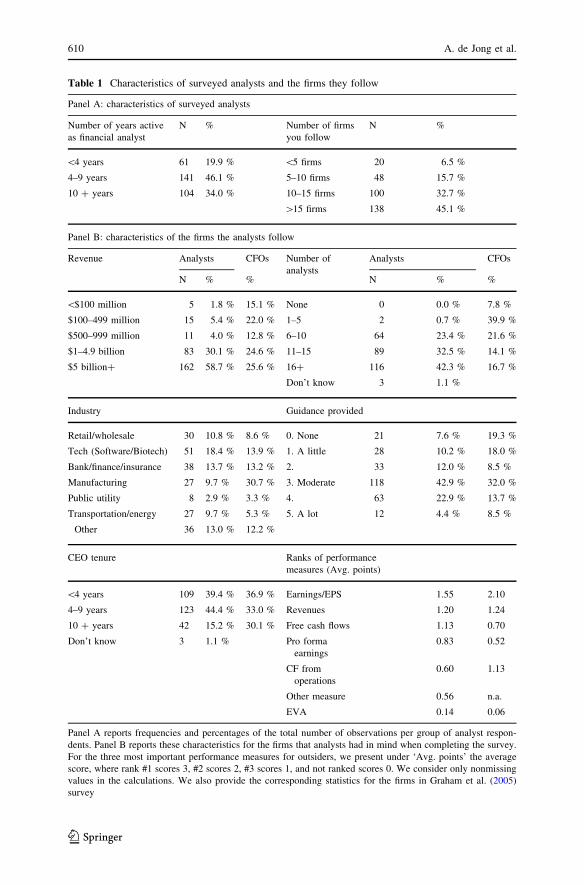

Table 1 Panel A provides summary statistics for the analysts who completed the

survey. We find that 46.1 % have four to 9 years, and 34 % at least 10 years,

experience as financial analysts and that 77.8 % follow at least 10 firms.

1 This analysis requires all observations for public firms in the CFO survey sample. We are grateful to

John Graham, Campbell Harvey, and Shiva Rajgopal for providing us their CFO data.

Survey evidence from financial analysts 609

123

Table 1 Characteristics of surveyed analysts and the firms they follow

Panel A: characteristics of surveyed analysts

Number of years active

as financial analyst

N % Number of firms

you follow

N %

\4 years 61 19.9 % \5 firms 20 6.5 %

4–9 years 141 46.1 % 5–10 firms 48 15.7 %

10 ? years 104 34.0 % 10–15 firms 100 32.7 %

[15 firms 138 45.1 %

Panel B: characteristics of the firms the analysts follow

Revenue Analysts CFOs Number of

analysts

Analysts CFOs

N % % N % %

\$100 million 5 1.8 % 15.1 % None 0 0.0 % 7.8 %

$100–499 million 15 5.4 % 22.0 % 1–5 2 0.7 % 39.9 %

$500–999 million 11 4.0 % 12.8 % 6–10 64 23.4 % 21.6 %

$1–4.9 billion 83 30.1 % 24.6 % 11–15 89 32.5 % 14.1 %

$5 billion? 162 58.7 % 25.6 % 16? 116 42.3 % 16.7 %

Don’t know 3 1.1 %

Industry Guidance provided

Retail/wholesale 30 10.8 % 8.6 % 0. None 21 7.6 % 19.3 %

Tech (Software/Biotech) 51 18.4 % 13.9 % 1. A little 28 10.2 % 18.0 %

Bank/finance/insurance 38 13.7 % 13.2 % 2. 33 12.0 % 8.5 %

Manufacturing 27 9.7 % 30.7 % 3. Moderate 118 42.9 % 32.0 %

Public utility 8 2.9 % 3.3 % 4. 63 22.9 % 13.7 %

Transportation/energy 27 9.7 % 5.3 % 5. A lot 12 4.4 % 8.5 %

Other 36 13.0 % 12.2 %

CEO tenure Ranks of performance

measures (Avg. points)

\4 years 109 39.4 % 36.9 % Earnings/EPS 1.55 2.10

4–9 years 123 44.4 % 33.0 % Revenues 1.20 1.24

10 ? years 42 15.2 % 30.1 % Free cash flows 1.13 0.70

Don’t know 3 1.1 % Pro forma

earnings

0.83 0.52

CF from

operations

0.60 1.13

Other measure 0.56 n.a.

EVA 0.14 0.06

Panel A reports frequencies and percentages of the total number of observations per group of analyst respon-

dents. Panel B reports these characteristics for the firms that analysts had in mind when completing the survey.

For the three most important performance measures for outsiders, we present under ‘Avg. points’ the average

score, where rank #1 scores 3, #2 scores 2, #3 scores 1, and not ranked scores 0. We consider only nonmissing

values in the calculations. We also provide the corresponding statistics for the firms in Graham et al. (2005)

survey

610 A. de Jong et al.

123

Table 1 Panel B provides summary statistics for the firms the analysts used to

complete the survey.2 We ask analysts to provide information on the size, industry,

and number of analysts following the firms they select. Nearly 90 % of these firms

have revenues in excess of $ 1 billion, and 74.8 % are followed by at least 10

analysts. Interestingly, greater importance is attached to analysts for setting stock

price by CFOs of such firms than by CFOs of smaller firms and firms followed by

fewer analysts (Graham et al.). Most of the analysts in our sample indicate that their

firms provide moderate or more than moderate guidance.

To investigate whether earnings management influences investor expectations,

we need to establish a mutual focus on earnings by CFOs and analysts. According to

Graham et al., CFOs believe earnings rather than cash flows to be the most

important performance measure for outsiders. Block’s (1999) survey results provide

preliminary evidence of a preference for earnings by financial analysts. Table 1

Panel B shows the average ranking of importance analysts and CFOs attach to

different performance measures. Consistent with the mutual focus on earnings, both

view earnings as the most important performance measure for outsiders. Revenue is

ranked second most important by analysts and free cash flows third. The interviews

elucidate these analyst preferences. The importance of earnings is largely driven by

investor interest in the EPS number. One analyst explained: ‘‘This is the metric the

investment community has dictated’’, ‘‘When I think of the Street, net income is

most important.’’ Analysts’ client bases thus seem to drive their focus on earnings.

These conjectures support empirical evidence that suggests that share prices behave

as if the market is fixated on earnings rather than cash flows (Sloan 1996).

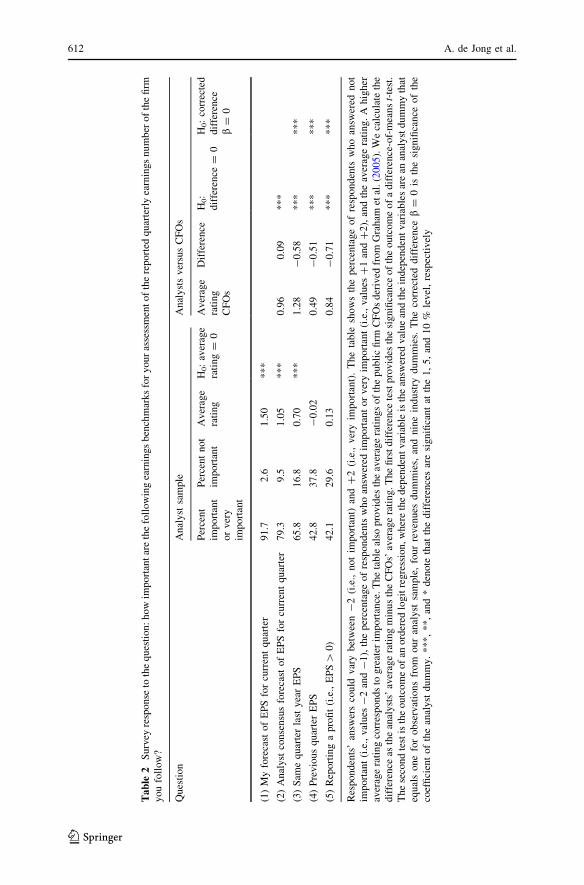

To confirm that analysts have the same benchmark in mind as CFOs answering

questions about meeting/missing earnings benchmarks and earnings management to

reach a benchmark, we ask the analysts about the importance of different

benchmarks to their assessment of firms’ reported quarterly earnings. Table 2

compares the analysts’ and CFOs’ responses.

Not surprisingly, analysts attach the greatest importance to their own forecasts

(i.e., 91.7 % agree or strongly agree). A more important result for our subsequent

analyses is that both analysts and CFOs, with average ratings of 1.05 and 0.96,

respectively, agree that consensus of analyst forecasts is an important evaluation

benchmark. The difference between the two ratings is not significant after

controlling for size and industry. For analysts, the third most important benchmark

is the EPS from the same quarter in the previous year.

3 Analysts’ beliefs regarding the importance of meeting earnings benchmarks

We first examine the analysts’ beliefs regarding the consequences of meeting or

missing earnings benchmarks with respect to the firm’s stock price. A number of

studies suggest that the market views meeting and beating earnings benchmarks as

important. Investors reward firms that meet and beat earnings benchmarks and

2 To facilitate comparison with the CFO sample in Graham et al., we also present the characteristics of

their CFO sample.

Survey evidence from financial analysts 611

123

Ta

ble

2S

urv

eyre

spo

nse

toth

eq

ues

tio

n:

ho

wim

po

rtan

tar

eth

efo

llo

win

gea

rnin

gs

ben

chm

ark

sfo

ry

ou

ras

sess

men

to

fth

ere

po

rted

qu

arte

rly

earn

ings

nu

mb

erof

the

firm

yo

ufo

llo

w?

Ques

tion

Anal

yst

sam

ple

Anal

yst

sver

sus

CF

Os

Per

cen

t

imp

ort

ant

or

ver

y

imp

ort

ant

Per

cen

tn

ot

imp

ort

ant

Av

erag

e

rati

ng

H0:

aver

age

rati

ng

=0

Av

erag

e

rati

ng

CF

Os

Dif

fere

nce

H0:

dif

fere

nce

=0

H0:

corr

ecte

d

dif

fere

nce

b=

0

(1)

My

fore

cast

of

EP

Sfo

rcu

rren

tquar

ter

91.7

2.6

1.5

0***

(2)

Anal

yst

conse

nsu

sfo

reca

sto

fE

PS

for

curr

ent

quar

ter

79.3

9.5

1.0

5***

0.9

60.0

9***

(3)

Sam

eq

uar

ter

last

yea

rE

PS

65

.81

6.8

0.7

0*

**

1.2

8-

0.5

8*

**

**

*

(4)

Pre

vio

us

qu

arte

rE

PS

42

.83

7.8

-0

.02

0.4

9-

0.5

1*

**

**

*

(5)

Rep

ort

ing

ap

rofi

t(i

.e.,

EP

S[

0)

42

.12

9.6

0.1

30

.84

-0

.71

**

**

**

Res

po

nd

ents

’an

swer

sco

uld

var

yb

etw

een

-2

(i.e

.,n

ot

imp

ort

ant)

and

?2

(i.e

.,ver

yim

port

ant)

.T

he

table

show

sth

eper

centa

ge

of

resp

onden

tsw

ho

answ

ered

not

imp

ort

ant

(i.e

.,v

alu

es-

2an

d-

1),

the

per

cen

tag

eo

fre

spo

nd

ents

wh

oan

swer

edim

po

rtan

to

rv

ery

imp

ort

ant

(i.e

.,v

alu

es?

1an

d?

2),

and

the

aver

age

rati

ng

.A

hig

her

aver

age

rati

ng

corr

esp

on

ds

tog

reat

erim

po

rtan

ce.

Th

eta

ble

also

pro

vid

esth

eav

erag

era

tin

gs

of

the

pu

bli

cfi

rmC

FO

sd

eriv

edfr

om

Gra

ham

etal

.(2

00

5).

We

calc

ula

teth

e

dif

fere

nce

asth

ean

aly

sts’

aver

age

rati

ng

min

us

the

CF

Os’

aver

age

rati

ng

.T

he

firs

td

iffe

ren

cete

stp

rov

ides

the

sig

nifi

can

ceo

fth

eo

utc

om

eo

fa

dif

fere

nce

-of-

mea

ns

t-te

st.

Th

ese

con

dte

stis

the

ou

tco

me

of

ano

rder

edlo

git

regre

ssio

n,w

her

eth

ed

epen

den

tv

aria

ble

isth

ean

swer

edv

alu

ean

dth

ein

dep

end

ent

var

iab

les

are

anan

aly

std

um

my

that

equ

als

on

efo

ro

bse

rvat

ion

sfr

om

ou

ran

aly

stsa

mp

le,

fou

rre

ven

ues

du

mm

ies,

and

nin

ein

du

stry

du

mm

ies.

Th

eco

rrec

ted

dif

fere

nce

b=

0is

the

sign

ifica

nce

of

the

coef

fici

ent

of

the

anal

yst

du

mm

y.

**

*,

**

,an

d*

den

ote

that

the

dif

fere

nce

sar

esi

gn

ifica

nt

atth

e1

,5

,an

d1

0%

lev

el,

resp

ecti

vel

y

612 A. de Jong et al.

123

punish those that fall short of them (e.g., Athanasakou et al. 2011; Skinner and

Sloan 2002), and firms that meet earnings benchmarks consistently over time are

priced at a premium (Barth et al. 1999; Kasznik and McNichols 2002); especially

when such premium is viewed as an indicator of future performance (Bartov et al.

2002; Kasznik and McNichols 2002). That the market reward is lower, or even

absent, for firms that meet or beat analysts’ forecasts as a result of earnings or

expectations management (e.g., Athanasakou, et al. 2011; Bartov et al. 2002;

Gleason and Mills 2008), however, suggests that the market at least partially

accounts for CFO discretion when targeting earnings benchmarks.

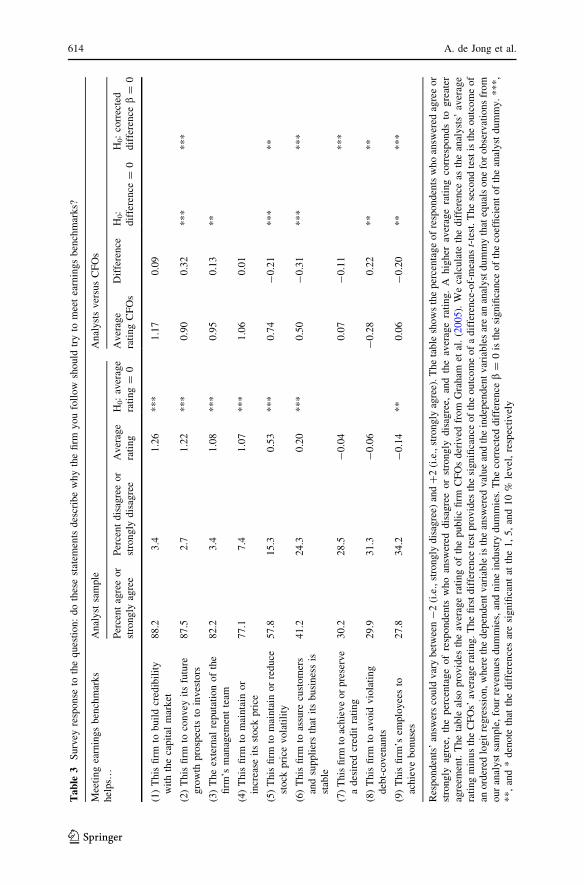

The results of the analyst survey reported in Table 3 support the importance of

stock-price-related motivations for meeting earnings benchmarks. We see that

88.2 % of the analysts believe that meeting earnings benchmarks helps firms build

credibility with capital markets, and 87.5 % believe that it helps to convey the

firm’s future growth prospects to investors. Analysts also agree that meeting

benchmarks helps to maintain or increase stock price (i.e., 77.1 %) and reduce stock

price volatility (57.8 %). We find by comparing their answers that analysts and

CFOs are of the same opinion regarding stock-price-related motivations for meeting

earnings benchmarks, but the analysts’ answers about long-term growth and

credibility suggest that they further believe that meeting short-term earnings

benchmarks can have long-term consequences.

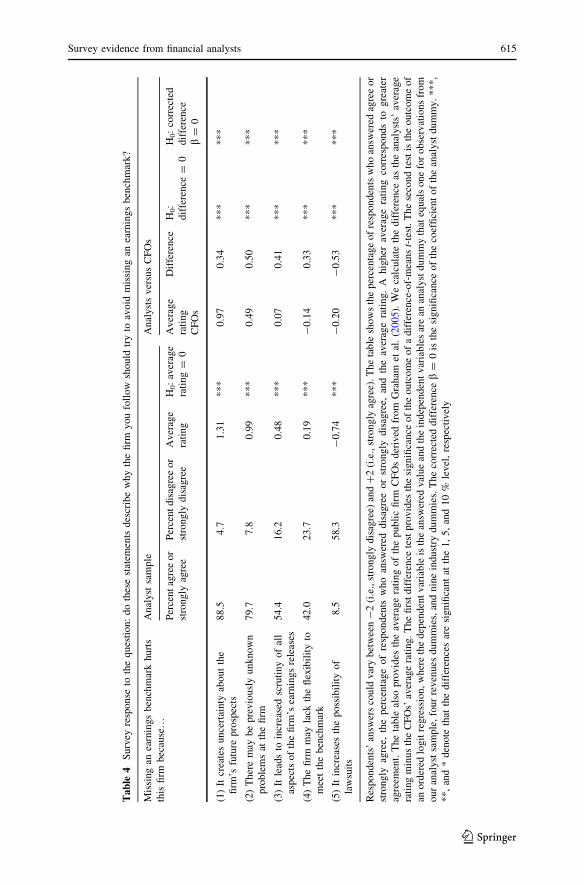

Additional supportive evidence for this view is provided by analysts’ responses

to questions regarding why firms should try to avoid missing earnings benchmarks.

As can be seen in Table 4, 88.5 % of the analysts agree with the statement that

missing earnings benchmarks creates uncertainty about firms’ future prospects.

Eighty percent of analysts believe that failure to meet earnings benchmarks is an

indication of previously unknown problems in a firm, and 42 % believe that a firm

might lack the flexibility to meet the benchmark. Our interview results suggest that

lack of flexibility relates to earnings management; firms with earnings below

benchmark are expected to manage their earnings to be just above the benchmark.

Hence missing the benchmark indicates either lack of flexibility or a gap between

earnings and benchmark that is too great to be bridged by earnings management.

Although these results suggest that analysts anticipate severe problems with firms

that miss benchmarks, our interviews indicate that missed benchmarks are viewed in a

more sophisticated way by analysts. Stated one: ‘‘If a firm misses [its] number, it does

not necessarily change the outlook for the business.’’ Most analysts carefully examine

management’s explanations for missed benchmarks. In evaluating these explanations,

the credibility of the motivation determines the magnitude of the negative impact.

Analysts verify the assumptions for their valuation models’ key value drivers. Missed

benchmarks, especially if they alter analysts’ assessment of long-term cash flows, are

considered negative. The interview results are consistent with analyst survey responses,

indicating that missed benchmarks lead to increased scrutiny (54.4 % agree). That

CFOs score much lower on this question indicates that they do not believe that missed

benchmarks incur increased scrutiny of all aspects of their firms’ earnings releases.

The external reputation of the management team can be an incentive for CFOs to

meet earnings benchmarks. Previous studies (e.g., DeFond and Park 1999; Farrell

and Whidbee 2003; Puffer and Weintrop 1991) show that managers whose firms do

Survey evidence from financial analysts 613

123

Ta

ble

3S

urv

eyre

spo

nse

toth

eq

ues

tio

n:

do

thes

est

atem

ents

des

crib

ew

hy

the

firm

yo

ufo

llo

wsh

ould

try

tom

eet

earn

ings

ben

chm

ark

s?

Mee

tin

gea

rnin

gs

ben

chm

ark

s

hel

ps…

An

aly

stsa

mple

An

alyst

sv

ersu

sC

FO

s

Per

cen

tag

ree

or

stro

ng

lyag

ree

Per

cen

td

isag

ree

or

stro

ng

lyd

isag

ree

Av

erag

e

rati

ng

H0:

aver

age

rati

ng

=0

Av

erag

e

rati

ng

CF

Os

Dif

fere

nce

H0:

dif

fere

nce

=0

H0:

corr

ecte

d

dif

fere

nce

b=

0

(1)

This

firm

tobuil

dcr

edib

ilit

y

wit

hth

eca

pit

alm

ark

et

88

.23

.41

.26

**

*1

.17

0.0

9

(2)

Th

isfi

rmto

con

vey

its

futu

re

gro

wth

pro

spec

tsto

inv

esto

rs

87

.52

.71

.22

**

*0

.90

0.3

2*

**

**

*

(3)

Th

eex

tern

alre

pu

tati

on

of

the

firm

’sm

anag

emen

tte

am

82

.23

.41

.08

**

*0

.95

0.1

3*

*

(4)

Th

isfi

rmto

mai

nta

ino

r

incr

ease

its

sto

ckp

rice

77

.17

.41

.07

**

*1

.06

0.0

1

(5)

Th

isfi

rmto

mai

nta

ino

rre

du

ce

sto

ckp

rice

vo

lati

lity

57

.81

5.3

0.5

3*

**

0.7

4-

0.2

1*

**

**

(6)

Th

isfi

rmto

assu

recu

stom

ers

and

sup

pli

ers

that

its

bu

sin

ess

is

stab

le

41

.22

4.3

0.2

0*

**

0.5

0-

0.3

1*

**

**

*

(7)

This

firm

toac

hie

ve

or

pre

serv

e

ad

esir

edcr

edit

rati

ng

30

.22

8.5

-0

.04

0.0

7-

0.1

1*

**

(8)

Th

isfi

rmto

avo

idv

iola

tin

g

deb

t-co

ven

ants

29

.93

1.3

-0

.06

-0

.28

0.2

2*

**

*

(9)

Th

isfi

rm’s

emplo

yee

sto

achie

ve

bonuse

s

27

.83

4.2

-0

.14

**

0.0

6-

0.2

0*

**

**

Res

po

nd

ents

’an

swer

sco

uld

var

yb

etw

een

-2

(i.e

.,st

rong

lyd

isag

ree)

and

?2

(i.e

.,st

rongly

agre

e).

The

table

show

sth

eper

centa

ge

of

resp

onden

tsw

ho

answ

ered

agre

eor

stro

ng

lyag

ree,

the

per

cen

tag

eo

fre

spo

nd

ents

wh

oan

swer

edd

isag

ree

or

stro

ng

lyd

isag

ree,

and

the

aver

age

rati

ng

.A

hig

her

aver

age

rati

ng

corr

esp

ond

sto

gre

ater

agre

emen

t.T

he

tab

leal

sop

rov

ides

the

aver

age

rati

ng

of

the

pu

bli

cfi

rmC

FO

sd

eriv

edfr

om

Gra

ham

etal

.(2

00

5).

We

calc

ula

teth

ed

iffe

ren

ceas

the

anal

yst

s’av

erag

e

rati

ng

min

us

the

CF

Os’

aver

age

rati

ng

.T

he

firs

td

iffe

ren

cete

stp

rov

ides

the

sign

ifica

nce

of

the

ou

tco

me

of

ad

iffe

ren

ce-o

f-m

eans

t-te

st.

Th

ese

con

dte

stis

the

ou

tco

me

of

anord

ered

logit

regre

ssio

n,

wher

eth

edep

enden

tvar

iable

isth

ean

swer

edval

ue

and

the

indep

enden

tvar

iable

sar

ean

anal

yst

dum

my

that

equal

sone

for

ob

serv

atio

ns

fro

m

ou

ran

aly

stsa

mple

,fo

ur

rev

enu

esd

um

mie

s,an

dn

ine

indu

stry

du

mm

ies.

Th

eco

rrec

ted

dif

fere

nce

b=

0is

the

sign

ifica

nce

of

the

coef

fici

ent

of

the

anal

yst

du

mm

y.

**

*,

**,

and

*den

ote

that

the

dif

fere

nce

sar

esi

gnifi

cant

atth

e1,

5,

and

10

%le

vel

,re

spec

tivel

y

614 A. de Jong et al.

123

Ta

ble

4S

urv

eyre

spo

nse

toth

eq

ues

tio

n:

do

thes

est

atem

ents

des

crib

ew

hy

the

firm

yo

ufo

llo

wsh

ould

try

toav

oid

mis

sin

gan

earn

ings

ben

chm

ark

?

Mis

sing

anea

rnin

gs

ben

chm

ark

hu

rts

this

firm

bec

ause

…A

nal

yst

sam

ple

An

alyst

sv

ersu

sC

FO

s

Per

cen

tag

ree

or

stro

ng

lyag

ree

Per

cen

td

isag

ree

or

stro

ng

lyd

isag

ree

Av

erag

e

rati

ng

H0:

aver

age

rati

ng

=0

Av

erag

e

rati

ng

CF

Os

Dif

fere

nce

H0:

dif

fere

nce

=0

H0:

corr

ecte

d

dif

fere

nce

b=

0

(1)

Itcr

eate

su

nce

rtai

nty

abo

ut

the

firm

’sfu

ture

pro

spec

ts

88

.54

.71

.31

**

*0

.97

0.3

4*

**

**

*

(2)

Th

ere

may

be

pre

vio

usl

yu

nk

no

wn

pro

ble

ms

atth

efi

rm

79

.77

.80

.99

**

*0

.49

0.5

0*

**

**

*

(3)

Itle

ads

toin

crea

sed

scru

tin

yo

fal

l

asp

ects

of

the

firm

’sea

rnin

gs

rele

ases

54

.41

6.2

0.4

8*

**

0.0

70

.41

**

**

**

(4)

Th

efi

rmm

ayla

ckth

efl

exib

ilit

yto

mee

tth

eb

ench

mar

k

42

.02

3.7

0.1

9*

**

-0

.14

0.3

3*

**

**

*

(5)

Itin

crea

ses

the

po

ssib

ilit

yo

f

law

suit

s

8.5

58

.3-

0.7

4*

**

-0

.20

-0

.53

**

**

**

Res

po

nd

ents

’an

swer

sco

uld

var

yb

etw

een

-2

(i.e

.,st

rong

lyd

isag

ree)

and

?2

(i.e

.,st

rongly

agre

e).

The

table

show

sth

eper

centa

ge

of

resp

onden

tsw

ho

answ

ered

agre

eor

stro

ng

lyag

ree,

the

per

cen

tag

eo

fre

spo

nd

ents

wh

oan

swer

edd

isag

ree

or

stro

ng

lyd

isag

ree,

and

the

aver

age

rati

ng

.A

hig

her

aver

age

rati

ng

corr

esp

onds

tog

reat

er

agre

emen

t.T

he

tab

leal

sop

rov

ides

the

aver

age

rati

ng

of

the

pu

bli

cfi

rmC

FO

sd

eriv

edfr

om

Gra

ham

etal

.(2

00

5).

We

calc

ula

teth

ed

iffe

ren

ceas

the

anal

yst

s’av

erag

e

rati

ng

min

us

the

CF

Os’

aver

age

rati

ng

.T

he

firs

td

iffe

ren

cete

stp

rov

ides

the

sign

ifica

nce

of

the

ou

tco

me

of

ad

iffe

ren

ce-o

f-m

eans

t-te

st.

Th

ese

con

dte

stis

the

ou

tco

me

of

anord

ered

logit

regre

ssio

n,

wher

eth

edep

enden

tvar

iable

isth

ean

swer

edval

ue

and

the

indep

enden

tvar

iable

sar

ean

anal

yst

dum

my

that

equal

sone

for

ob

serv

atio

ns

fro

m

ou

ran

aly

stsa

mple

,fo

ur

rev

enu

esd

um

mie

s,an

dn

ine

indu

stry

du

mm

ies.

Th

eco

rrec

ted

dif

fere

nce

b=

0is

the

sign

ifica

nce

of

the

coef

fici

ent

of

the

anal

yst

du

mm

y.

**

*,

**,

and

*den

ote

that

the

dif

fere

nce

sar

esi

gnifi

cant

atth

e1,

5,

and

10

%le

vel

,re

spec

tivel

y

Survey evidence from financial analysts 615

123

not meet analyst forecasts are more likely to be replaced. As can be seen in Table 3,

82.2 % of the analysts agree that firms should achieve earnings benchmarks for the

external reputation of the firm’s management team. The interviews corroborate the

relevance of this perspective. Nearly all the analysts explained that, benchmarks

being strongly based on previous expectations provided by management teams,

meeting benchmarks demonstrates the capabilities of the managers. Meeting

forecasts, observed one analyst, ‘‘provides a signal about the management team.

They should know what is going on in their own firm.’’

Bowen et al. (1995) and Burgstahler and Dichev (1997) argue that firms with

higher earnings can get better terms of trade with stakeholders like customers,

suppliers, and lenders because higher earnings can enhance their reputation for

fulfilling the stakeholders’ claims. Meeting earnings benchmarks can have the same

implications. Our results show that 41.2 % of the analysts view assurance of a stable

business to customers and suppliers to be an important reason for meeting earnings

benchmarks. CFOs attach more importance than analysts suggest to the stakeholder

motivation for meeting earnings benchmarks. Analyst client bases that consist

mainly of one type of stakeholder, investors, might explain their different view. One

alternative view is that analysts do not fully account for CFOs’ stakeholder-related

incentives to meet earnings benchmarks. Consistent with the CFOs’ answers,

analysts do not believe earnings benchmarks to be important with respect to credit

ratings, debt covenants, employee bonuses, and the potential for lawsuits.

Overall, our analysis of analysts’ opinions relative to those of the CFOs indicates

that analysts share CFOs’ beliefs regarding the importance of meeting earnings

benchmarks. We further show that, although they claim to seek reasons for missed

benchmarks and to believe that benchmarks missed for temporary reasons should

not have severe consequences for firm valuation, analysts’ answers regarding

missing/meeting earnings benchmarks suggest that they develop a negative view of

firms that miss short-term earnings targets. A possible explanation for this negative

view, corroborated by our interviews, is that analysts are aware of CFOs’ discretion

to manage earnings to a benchmark.

4 Analysts’ beliefs regarding the valuation implications of earningsmanagement

Empirical evidence suggests that firms use either accounting (i.e., accruals) or real

actions to reduce the probability of missing earnings benchmarks.3 Market rewards

that accrue to firms that meet earnings benchmarks4 depend on the actions taken to

3 See, for example, Ayers et al. (2006) for evidence on using accruals earnings management to meet

earnings benchmarks. See, for example, Bartov (1993) and Dechow and Sloan (1991) for earlier work and

Cohen et al. (2010), Hribar et al. (2006), and Roychowdhury (2006) for more recent work on using real

earnings management to meet benchmarks. Zang (2012) shows that real earnings management and

accruals-based earnings management act as substitutes.4 Note however that benefits are short-lived. Bhojraj et al. (2009) show that, on a three-year horizon,

firms that miss their benchmark but do not manage earnings (real, accruals, or both) tend to outperform

firms that achieve their benchmark by means of earnings management.

616 A. de Jong et al.

123

meet those benchmarks. Rewards are greater, for example, for firms that meet

consensus analyst forecasts by means of real earnings management than for firms

that use accruals management (Chen et al. 2010). Whereas firms that use accruals

management (Bartov et al. 2002) or classification shifting to meet benchmarks earn

a lower, but positive, premium (Athanasakou et al. 2011), the market reaction ceases

to be positive for firms that reduce tax expenses (Gleason and Mills 2008).

Moreover, firms that meet analyst earnings forecasts through share repurchases,

even though doing so helps to forestall extreme declines in share price, tend to be

discounted by analysts (Hribar et al. 2006). In their review, Dechow et al. (2010)

suggest that different responses to earnings management in relation to target beating

may be explained by the fact that some types of earnings management are more

easily detected than others.

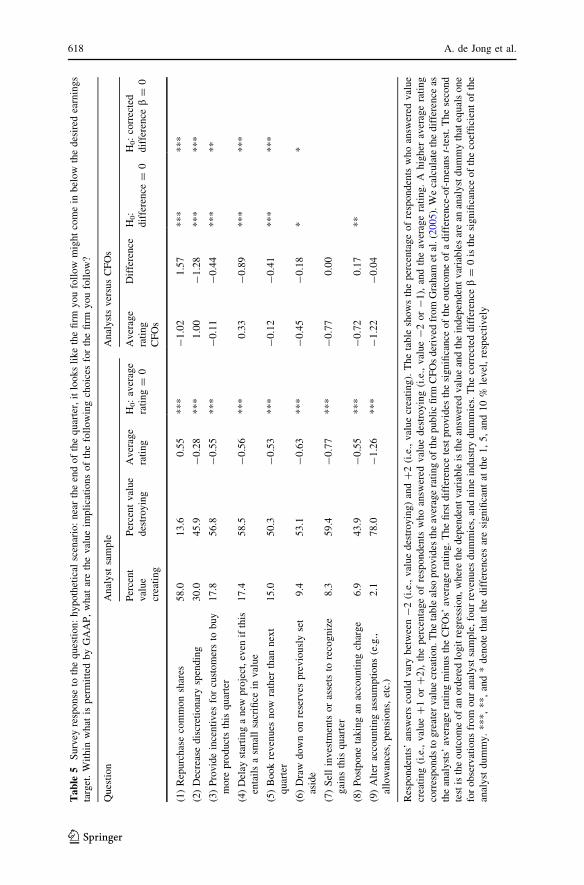

Table 5 reports analysts’ answers to the question regarding the perceived value

implications of employing various within-GAAP earnings management actions to

achieve earnings targets. In comparing analysts’ with CFOs’ answers, it should be

noted that Graham et al. ask CFOs which of the choices their firms might make

rather than the value implications of the choices.

We find that analysts believe that, share repurchases excepted, most types of

earnings management are value destroying. Our results further indicate that,

analysts view real actions more positively than accruals actions to meeting earnings

targets. The top four of the most value-enhancing/least value-destroying choices are

repurchasing common shares (ranked 1), decreasing discretionary spending (ranked

2), providing incentives for customers to buy more products in the present quarter

(ranked 3), and delaying the start of a new project, even if doing so entails a small

sacrifice in value (ranked 4), all of which are real actions. Excepting the decision to

sell investments or assets to recognize gains in the present quarter (ranked 7), the

bottom of the list contains accruals actions.

A comparison of analysts’ responses and the CFO results of Graham et al. reveals

a remarkable correspondence between the actions CFOs might make and the value

implications as perceived by analysts. Although CFOs’ preference for real earnings

management is not surprising,5 analysts’ positive view of real earnings management

is, especially given the impact of real earnings management on firms’ actual cash

flows. One explanation for analysts’ positive view is that they perceive attaining the

earnings benchmark by means of real earnings management to be a positive signal

of future firm performance (e.g., Bartov et al. 2002; Chen et al. 2010).

Three real earnings management actions CFOs are willing to take are considered

by analysts to be value destroying. As noted above, this inconsistency may be

occasioned by the different questions asked to CFOs and analysts. Our results

indicate that the first action, share repurchasing, although viewed by analysts as the

most value-enhancing action firms can take to meet earnings targets (average rating

5 The Graham et al. interviews clarify CFOs’ preference in terms of fear of legal action should regulators

suspect earnings management, which is more apparent with accruals than with real actions. Even when

earnings choices are made within GAAP, regulators can construe the choices to constitute earnings

management with managerial intent to obscure true economic performance (Dechow and Skinner 2000).

The consequences of being targeted for financial misrepresentation are severe for both firm and managers

(Karpoff et al. 2008a, b).

Survey evidence from financial analysts 617

123

Ta

ble

5S

urv

eyre

spo

nse

toth

eq

ues

tio

n:

hy

poth

etic

alsc

enar

io:

nea

rth

een

do

fth

eq

uar

ter,

itlo

ok

sli

ke

the

firm

yo

ufo

llo

wm

igh

tco

me

inb

elow

the

des

ired

earn

ing

s

targ

et.

Wit

hin

wh

atis

per

mit

ted

by

GA

AP

,w

hat

are

the

val

ue

imp

lica

tio

ns

of

the

foll

ow

ing

cho

ices

for

the

firm

yo

ufo

llo

w?

Ques

tion

Anal

yst

sam

ple

Anal

yst

sver

sus

CF

Os

Per

cen

t

val

ue

crea

tin

g

Per

cen

tv

alue

des

troy

ing

Av

erag

e

rati

ng

H0:

aver

age

rati

ng

=0

Av

erag

e

rati

ng

CF

Os

Dif

fere

nce

H0:

dif

fere

nce

=0

H0:

corr

ecte

d

dif

fere

nce

b=

0

(1)

Rep

urc

has

eco

mm

on

shar

es5

8.0

13

.60

.55

**

*-

1.0

21

.57

**

**

**

(2)

Dec

reas

ed

iscr

etio

nar

ysp

endin

g3

0.0

45

.9-

0.2

8*

**

1.0

0-

1.2

8*

**

**

*

(3)

Pro

vid

ein

cen

tiv

esfo

rcu

sto

mer

sto

bu

y

mo

rep

rod

uct

sth

isq

uar

ter

17

.85

6.8

-0

.55

**

*-

0.1

1-

0.4

4*

**

**

(4)

Del

ayst

arti

ng

an

ewp

roje

ct,

even

ifth

is

enta

ils

asm

all

sacr

ifice

inv

alu

e

17

.45

8.5

-0

.56

**

*0

.33

-0

.89

**

**

**

(5)

Boo

kre

ven

ues

no

wra

ther

than

nex

t

qu

arte

r

15

.05

0.3

-0

.53

**

*-

0.1

2-

0.4

1*

**

**

*

(6)

Dra

wd

ow

no

nre

serv

esp

rev

iou

sly

set

asid

e

9.4

53

.1-

0.6

3*

**

-0

.45

-0

.18

**

(7)

Sel

lin

ves

tmen

tso

ras

sets

tore

cog

niz

e

gai

ns

this

qu

arte

r

8.3

59

.4-

0.7

7*

**

-0

.77

0.0

0

(8)

Po

stp

on

eta

kin

gan

acco

un

tin

gch

arg

e6

.94

3.9

-0

.55

**

*-

0.7

20

.17

**

(9)

Alt

erac

cou

nti

ng

assu

mp

tio

ns

(e.g

.,

allo

wan

ces,

pen

sio

ns,

etc.

)

2.1

78

.0-

1.2

6*

**

-1

.22

-0

.04

Res

po

nd

ents

’an

swer

sco

uld

var

yb

etw

een

-2

(i.e

.,v

alu

ed

estr

oy

ing

)an

d?

2(i

.e.,

val

ue

crea

ting).

The

table

show

sth

eper

centa

ge

of

resp

onden

tsw

ho

answ

ered

val

ue

crea

ting

(i.e

.,val

ue

?1

or

?2),

the

per

centa

ge

of

resp

onden

tsw

ho

answ

ered

val

ue

des

troyin

g(i

.e.,

val

ue

-2

or

-1

),an

dth

eav

erag

era

tin

g.

Ah

igh

erav

erag

era

tin

g

corr

esp

on

ds

tog

reat

erv

alu

ecr

eati

on

.T

he

tab

leal

sop

rov

ides

the

aver

age

rati

ng

of

the

pu

bli

cfi

rmC

FO

sd

eriv

edfr

om

Gra

ham

etal

.(2

00

5).

We

calc

ula

teth

ed

iffe

ren

ceas

the

anal

yst

s’av

erag

era

ting

min

us

the

CF

Os’

aver

age

rati

ng

.T

he

firs

td

iffe

ren

cete

stp

rov

ides

the

sig

nifi

can

ceo

fth

eo

utc

om

eo

fa

dif

fere

nce

-of-

mea

ns

t-te

st.

Th

ese

con

d

test

isth

eoutc

om

eof

anord

ered

logit

regre

ssio

n,

wher

eth

edep

enden

tvar

iable

isth

ean

swer

edval

ue

and

the

indep

enden

tv

aria

ble

sar

ean

anal

yst

dum

my

that

equ

als

on

e

for

ob

serv

atio

ns

fro

mo

ur

anal

yst

sam

ple

,fo

ur

rev

enu

esd

um

mie

s,an

dn

ine

ind

ust

ryd

um

mie

s.T

he

corr

ecte

dd

iffe

ren

ceb

=0

isth

esi

gn

ifica

nce

of

the

coef

fici

ent

of

the

anal

yst

du

mm

y.

**

*,

**

,an

d*

den

ote

that

the

dif

fere

nce

sar

esi

gn

ifica

nt

atth

e1

,5

,an

d1

0%

lev

el,

resp

ecti

vel

y

618 A. de Jong et al.

123

equals 0.55), is not favored by CFOs as an option for meeting earnings targets

(average rating equals -1.02). In the interviews, analysts attribute the value effect

of repurchasing to (1) a signal of underpriced stock and (2) repayment of free cash

flows. It is not obvious why a repurchase transaction designed merely to meet

earnings expectations might enhance value. Perhaps analysts are positive about

share repurchases because they are easier to detect, a conjecture consistent with the

market discounting of firms that meet earnings benchmarks by repurchasing shares

(Hribar et al. 2006). The ease with which this type of earnings management can be

unraveled might account for CFOs’ reluctance to take this action.

The two other types of real earnings management for which analysts’ and CFOs’

attitudes differ are reduction in discretionary spending and delay of new projects.

Although analysts, on average, find these two options (with average ratings of

-0.28 and -0.56, respectively) to be value-destroying, CFOs view the actions (with

average ratings of 1.00 and 0.33, respectively) as acceptable for meeting

benchmarks. In contrast to the share repurchasing option, CFOs might prefer these

actions because they are less detectable by analysts and other market participants.

For their part, analysts might be unwilling to admit that they cannot detect

discretionary spending cuts or delayed project initiations undertaken for the sake of

meeting benchmarks.

5 Analysts’ beliefs regarding the consequences of smoothing earnings

There is considerable evidence that many firms smooth their earnings path (see, for

example, Barth et al. 1999, Beidleman 1973; Hand 1989; Myers et al. 2007). In

interviews conducted by Graham et al., CFOs maintain that earnings volatility is

directly related to missing consensus analyst forecasts as earnings benchmarks,

thereby occasioning uncertainty among market participants about firm value. In this

section, we examine how analysts view the consequences of smoothing and whether

they believe firms should sacrifice value to smooth earnings.

5.1 Consequences for firms that smooth their earnings path

Empirical evidence relating earnings smoothing to firm pricing value is mixed.

Although some studies find earnings smoothing to be negatively associated with

cost of equity (Francis et al. 2004) and positively with share price (e.g., Myers et al.

2007; Ronen and Sadan 1981), the positive effect on share price disappears when a

string of earnings increases ends (Myers et al. 2007). Moreover, McInnis’s (2010)

application of asset pricing techniques shows no relation between earnings

smoothness and returns. This finding is in line with Verrecchia’s (2010) view that,

because their motivation is associated with perceived greater wealth, managers’

preference for smooth earnings paths is heuristic.6 Earnings smoothing can also

6 Supporting evidence is the following text from Graham et al. (p. 47): ‘‘Without exception, every CFO

we spoke with prefers a smoother earnings path to a bumpier one, even if the underlying cash flows are

the same.’’

Survey evidence from financial analysts 619

123

Ta

ble

6S

urv

eyre

sponse

toth

eques

tion:

ifth

efi

rmyou

foll

ow

would

smooth

its

earn

ings

pat

h,

what

would

be

the

conse

quen

ces?

Ifth

efi

rmth

atI

foll

ow

wo

uld

smo

oth

its

earn

ing

sp

ath…

An

alyst

sam

ple

An

aly

sts

vs.

CF

Os

Per

cen

tag

ree

or

stro

ng

ly

agre

e

Per

cen

td

isag

ree

or

stro

ng

ly

dis

agre

e

Av

erag

e

rati

ng

H0:

aver

age

rati

ng

=0

Av

erag

e

rati

ng

CF

Os

Dif

fere

nce

H0:

dif

fere

nce

=0

H0:

corr

ecte

d

dif

fere

nce

b=

0

(1)

Itw

ou

ldb

eea

sier

top

red

ict

this

firm

’sfu

ture

earn

ing

s

83

.08

.51

.01

**

*0

.99

0.0

2

(2)

Th

isfi

rmw

ou

ldb

ele

ssri

sky

56

.72

2.3

0.3

7*

**

1.1

8-

0.8

1*

**

**

*

(3)

Th

isfi

rmw

ou

ldas

sure

cust

om

ers/

sup

pli

ers

that

bu

sin

ess

isst

able

43

.82

4.9

0.1

7*

**

0.6

1-

0.4

4*

**

**

*

(4)

Th

isfi

rmw

ou

ldre

du

ceth

ere

turn

that

inves

tors

dem

and

42

.22

5.9

0.1

6*

**

0.5

5-

0.3

9*

**

**

*

(5)

Th

isfi

rmw

ou

ldp

rom

ote

are

pu

tati

on

for

tran

spar

ent

and

accu

rate

report

ing

35

.13

3.3

-0

.06

0.3

2-

0.3

8*

**

**

*

(6)

This

firm

would

achie

ve

or

pre

serv

e

ad

esir

edcr

edit

rati

ng

34

.22

0.6

0.1

0*

0.2

1-

0.1

1*

**

(7)

Th

isfi

rmw

ou

ldco

nv

eyh

igh

erfu

ture

gro

wth

pro

spec

ts

22

.63

8.4

-0

.22

**

*0

.42

-0

.64

**

**

**

(8)

Th

isfi

rmw

ou

ldcl

arif

ytr

ue

eco

no

mic

per

form

ance

19

.94

2.4

-0

.32

**

*-

0.0

5-

0.2

7*

**

**

*

Res

po

nd

ents

’an

swer

sco

uld

var

yb

etw

een

-2

(i.e

.,st

rong

lyd

isag

ree)

and

?2

(i.e

.,st

rongly

agre

e).

The

table

show

sth

eper

centa

ge

of

resp

onden

tsw

ho

answ

ered

agre

eor

stro

ng

lyag

ree,

the

per

cen

tag

eo

fre

spo

nd

ents

wh

oan

swer

edd

isag

ree

or

stro

ng

lyd

isag

ree,

and

the

aver

age

rati

ng

.A

hig

her

aver

age

rati

ng

corr

esp

onds

tog

reat

er

agre

emen

t.T

he

tab

leal

sop

rov

ides

the

aver

age

rati

ng

of

the

pu

bli

cfi

rmC

FO

sd

eriv

edfr

om

Gra

ham

etal

.(2

00

5).

We

calc

ula

teth

ed

iffe

ren

ceas

the

anal

yst

s’av

erag

e

rati

ng

min

us

the

CF

Os’

aver

age

rati

ng

.T

he

firs

td

iffe

ren

cete

stp

rov

ides

the

sign

ifica

nce

of

the

ou

tco

me

of

ad

iffe

ren

ce-o

f-m

eans

t-te

st.

Th

ese

con

dte

stis

the

ou

tco

me

of

anord

ered

logit

regre

ssio

n,

wher

eth

edep

enden

tvar

iable

isth

ean

swer

edval

ue

and

the

indep

enden

tvar

iable

sar

ean

anal

yst

dum

my

that

equal

sone

for

ob

serv

atio

ns

fro

m

ou

ran

aly

stsa

mple

,fo

ur

rev

enu

esd

um

mie

s,an

dn

ine

indu

stry

du

mm

ies.

Th

eco

rrec

ted

dif

fere

nce

b=

0is

the

sign

ifica

nce

of

the

coef

fici

ent

of

the

anal

yst

du

mm

y.

**

*,

**,

and

*den

ote

that

the

dif

fere

nce

sar

esi

gnifi

cant

atth

e1,

5,

and

10

%le

vel

,re

spec

tivel

y

620 A. de Jong et al.

123

reduce the cost of debt and enhance trade terms with suppliers and customers

(Trueman and Titman 1988), help to realize bonus targets (Healy 1985), and protect

managers’ jobs (Fudenberg and Tirole 1995).

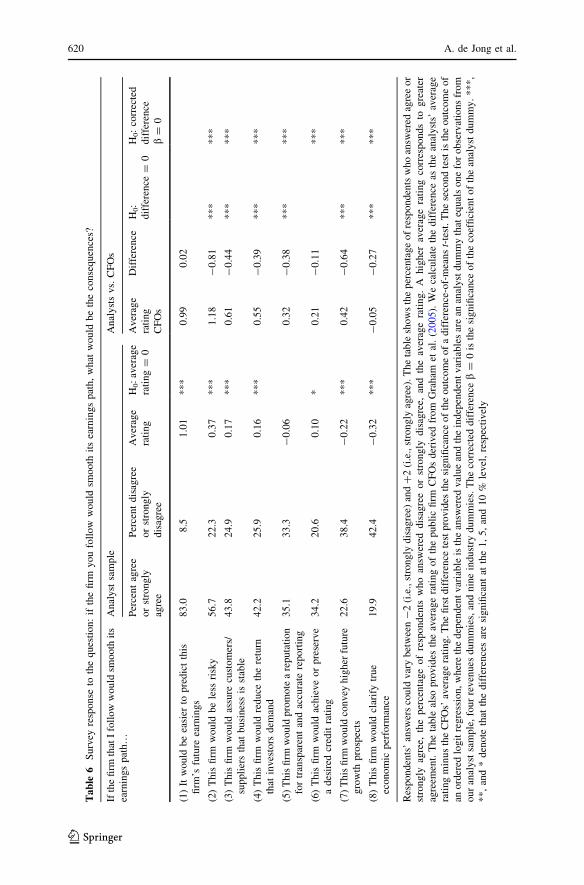

Analysts’ opinions regarding the consequences of earnings smoothing for the

firms they follow are reported in Table 6.

Our main result is that analysts believe in smoothing earnings to reduce

perceived firm riskiness. Smoothed earnings are perceived by 83 % of the analysts

to be easier to predict, by 56.7 % to be less risky, and by 42.2 % to characterize

firms with a lower required return. As one interviewee put it, ‘‘Smoothing lifts the

valuation because it increases predictability, which reduces volatility…. A little bit

makes sense.’’ Although analysts share CFOs’ beliefs regarding these statements,

CFOs’ significantly higher average rating of perceived riskiness and required returns

of firms with smooth earnings paths suggest a more optimistic appraisal of the

consequences of smoothing.

We find disagreement between analysts and CFOs on two consequences of

earnings smoothing. First, a smooth earnings path is perceived to be more

informative of firms’ growth prospects by CFOs (average rating = 0.42) but not by

analysts (average rating = -0.22). Second, the average rating of analysts who find

earnings smoothing to promote firms’ reputation for transparency and accurate

reporting is -0.06, while that of CFOs is 0.32. Thus smoothing is acknowledged by

analysts to make earnings more predictable, but it is not expected to reduce

information asymmetries.

The interviews also surfaced the argument that earnings smoothing substitutes a

black box for what is happening in firms. ‘‘In the long run,’’ explained one analyst,

‘‘it helps their stock price because of predictability, but it hurts our ability to see

what the fair value is.’’ This statement corresponds with analysts’ disagreement with

the survey statement that firms clarify true economic performance by smoothing

earnings (average rating = -0.32). Another interviewee summarized the pros and

cons of smoothing succinctly with the following observation: ‘‘We do not want

them to smooth, but we love smooth earnings paths.’’ Smooth earnings paths,

because analysts associate them with higher firm value, are liked by analysts and

bumpy earnings paths that are smoothed disliked because they impede assessment

of the businesses and,hence the ability to deliver reliable reports.7 We infer from

this paradoxical finding that analysts are not always able to detect CFOs’ earnings

smoothing.

This finding also suggests that analysts are forced to trade off incentives to

maximize forecast accuracy, with a possible reputation loss from overlooking

earnings management. On the one hand, analysts aim to limit their reputational risk

from overlooking earnings management by following firms that do not smooth their

earnings paths; on the other hand, analysts have incentives to maximize forecast

accuracy by following firms with smooth earnings paths.

7 Although our survey does not distinguish between whether smoothing is sustainable, this distinction is

crucial to determine the usefulness of smoothing. If CFOs are good at predicting future performance and

smooth to reflect the average level of expected performance, this can help analysts’ assessment of these

firms’ businesses. But if they smooth temporarily in the face of erratic and declining performance and

they have to take a subsequent big write-down, this does impede analysts’ assessment.

Survey evidence from financial analysts 621

123

5.2 Sacrificing value to avoid bumpy earnings paths

Analysts’ answers to the question of how much value CFOs should sacrifice to avoid

a bumpy earnings path are presented in Table 7 for discrete levels of value sacrifice.

Only one third of the analysts believe firms should not sacrifice value to avoid a

bumpy earnings path. ‘‘I don’t think firms should be that short-sighted,’’ remarked

one analyst. ‘‘The firm may experience a short-term dislocation in the stock price,

but over time they will get credit for having the credibility.’’ About half of the

analysts believe firms should sacrifice a small amount of money to avoid a bumpy

earnings path and 13.2 % (i.e., 12.1 % plus 1.1 %) believe that firms should make a

moderate to large sacrifice. These results suggest that most analysts recognize the

advantages of a smooth earnings path.

We investigate the consistency of the analysts’ responses (in an unreported

regression analysis). In this analysis, we explain the value sacrifice by using the

answers to the questions on the consequences of smoothing (as in Table 6). We

estimate eight ordered logit regressions, adding to each one of eight answers to the

question on the consequences of smoothing (e.g., ‘‘this firm would be less risky’’),

and control for guidance, analyst tenure, portfolio size, firm size, and industry. The

coefficients of the expected consequences are always positive and significant at the

1 % level, which indicates that the more positive analysts’ answers are regarding

Table 7 Survey response to the question: how large a sacrifice in value should the firm you follow make

to avoid a bumpy earnings path?

Analyst

sample

Analysts versus CFOs

Percent of

respondents

Percent of

respondents

CFOs

Difference H0:

difference = 0

H0: corrected

difference

b = 0

None 33.5 5.5 27.9 *** ***

Small sacrifice 53.3 33.6 19.8 *** ***

Moderate sacrifice 12.1 46.9 -34.8 *** ***

Large sacrifice 1.1 14.0 -12.9 *** ***

H0: corrected

difference all groups

(b) = 0

-2.318***

Respondents’ answers could vary between 0 (i.e., none) and ?3 (i.e., large sacrifice). The table shows the

percentage of respondents per answer. The table also provides the percentage of respondents of the public

firm CFOs derived from Graham et al. (2005). We calculate the difference as the analysts’ average rating

minus the CFOs’ average rating. The first difference test provides the significance of the outcome of a

difference-of-means t-test. The second test is the outcome of a binary logit regression, where the

dependent variable is a dummy that equals one if the analyst provided that value as the answer (e.g., for

the answer no sacrifice in value, the dummy is one if the analyst checked ‘‘none’’ and zero otherwise).

The independent variables are an analyst dummy that equals one for observations from our analyst

sample, four revenues dummies, and nine industry dummies. The corrected difference b = 0 is the

significance of the coefficient of the analyst dummy. The corrected difference of all groups is the analyst

coefficient and its significance of an ordered logit regression with the same independent variables as the

previous regression but with the value of the answer that ranges from 0 to 3 as the dependent variable.

***, **, and * denote that the differences are significant at the 1, 5, and 10 % level, respectively

622 A. de Jong et al.

123

their perceived consequences of smoothing, the more likely they are to recommend

larger value sacrifices.

We observe a distinct contrast when we compare with those of the CFOs our

results regarding the question of how much value CFOs should sacrifice to avoid

bumpy earnings. Willingness to make a moderate to large sacrifice is expressed by

60.9 % (i.e., 46.9 % plus 14 %) of the CFOs, compared to 13.2 % of the analysts

who recommend that firms make such sacrifices. The CFOs, claiming ‘‘the market

hates uncertainty,’’ provide share-price related arguments for sacrificing value for a

smooth earnings path (Graham et al., p. 49). This greater willingness to sacrifice

value might be explained by their more optimistic view of the consequences of

smooth earnings paths.

6 Conclusion

Survey evidence reported in Graham et al. suggests that CFOs believe that earnings

management can enhance investor perception of firm value. We survey 306

financial analysts and interview 21 of them to gain insight to their views on earnings

management. We then compare their views with those of the public firm CFOs

derived from the survey data used by Graham et al. to examine whether analysts’

views are in line with those of CFOs.

We first investigate analysts’ beliefs regarding the importance of meeting

earnings benchmarks and demonstrate that analysts generally share the CFOs’

beliefs. We further find that analysts are aware of the CFOs’ discretion in

managing earnings. We examine analysts’ beliefs regarding the value implications

of using different earnings management techniques to reach a benchmark and

document that analysts perceive all earnings management techniques, save share

repurchases, to be value destroying. Interestingly, CFOs, although reluctant to

repurchase shares, are willing to take actions viewed by analysts as value

destroying (including decreasing discretionary spending); this preference might be

explained by analysts’ inability to detect certain earnings management techniques.

Finally, we describe analysts’ beliefs regarding the consequences of earnings

smoothing and find that analysts believe smoothing earnings to reduce the

perceived riskiness of the firm to other stakeholders and to be worth a small

sacrifice in value.

Although our research provides novel insights into analysts’ and investors’

perceptions of firm value, we cannot provide conclusive answers regarding its

implications for actual or intrinsic value. We demonstrate that analysts endorse, to

a degree, CFOs’ value-destroying decision to smooth earnings and manage

earnings to benchmarks. This is because the enhanced investor perception of firm

value that may accrue to these decisions can have real consequences for intrinsic

value, as in reducing a firm’s financing costs. CFOs, in corporate financial

reporting decisions, might balance the negative effects of sacrificing economic

value and positive effects of enhanced investor perception of firm value. Because

our survey evidence cannot measure the net value effects, we leave this issue for

further research.

Survey evidence from financial analysts 623

123

Acknowledgments We thank Anna Gold, Alan Goodacre, Reggy Hooghiemstra, Nancy Huyghebaert,

Teye Marra, Marlene Plumlee, Shiva Rajgopal, Rui Shen, Mathijs van Dijk, Marcel van Rinsum, Yulia

Veld-Merkoulova, and seminar participants at K. U. Leuven, Rotterdam School of Management Erasmus

University, University of Antwerp, University of Groningen, and University of Stirling for helpful

comments. We are grateful to John Graham, Campbell Harvey, and Shiva Rajgopal for providing their

CFO survey data to us. Finally, we are grateful to the financial analysts who took the time to fill out our

survey or to be interviewed by us. The paper was previously entitled ‘‘The demand for corporate financial

reporting: a survey among financial analysts’’.

Appendix 1: Survey and interview design

Survey design

During the period of July to October 2007, we approached the heads of the equity

research departments of 11 of the world’s largest investment banks. Upon

guaranteeing to their compliance departments anonymity for the participating

banks and sell-side analysts, all institutions agreed to participate. Heads of equity

research departments dispatched e-mails requesting that their analysts participate

and providing the link to the survey website. Each institution informed us of the

number of sell-side analysts approached. The total was 638, with a median of 68 per

bank. We offered respondents a copy of the results and donated to a charity of the

respondents’ choice $10 for each completed survey. Responses with fewer than 10

answers were automatically deleted. The 306 usable responses received during the