Embed Size (px)

Citation preview

How do Individual, Institutional,and Foreign Investors Win and Lose

in Equity Trades? Evidence fromJapann

KEE-HONG BAEw, TAKESHI YAMADA

¼AND KEIICHI ITO§

wQueen’s University, Kingston, Ontario, Canada¼National University of Singapore, Singapore

§Nomura Securities, Tokyo, Japan

ABSTRACT

We investigate the gains and losses from equity trades of individualinvestors, various institutional investors, and foreign investors in the TokyoStock Exchange. We develop a trade-weighted performance measure andexamine the impact of trading intervals, price spreads, and market timing onperformance. We find that different investor types gain or lose from differentsources. For example, we discover that individual investors have poor markettiming ability but potentially gain during short-run trading intervals as theiraverage sell price is consistently higher than the average purchase price. Incontrast, we find that foreign investors consistently generate gains fromtrade due to good market timing, although their average sell price is lowerthan the average purchase price. Also, we find that foreign investors extractsignificant portion of their gains by trading against Japanese institutionalinvestors when Japanese investors trade before their fiscal-year end.

n We received useful suggestions from participants of The 5th Behavioral Economics Workshopco-sponsored by Aoyama Gakuin University and Osaka University Center for Research inBehavioral Economics. For earlier versions of the paper, we thank Junji Kawahara, SrinivasanSankaraguruswamy, Yasuhiko Tanigawa, participants of the NFA/APFA/FMA Annual Meetings,and seminar participants at the Hong Kong University of Science and Technology, KeioUniversity, Musashi University, Nanyang Technological University, National University ofSingapore, and The University of Hong Kong for helpful comments. We appreciate the effortsof Masato Hirota and Hirotaka Kawai of the Tokyo Stock Exchange in answering our questions oninstitutional details. We appreciate Alisa Larson for excellent editorial assistance. Yamadaacknowledges the support during stay at the Graduate School of International Corporate Strategyof Hitotsubashi University and financial support from the National University of SingaporeAcademic Research Grant R-315-000-047-112. The contents expressed in the paper do not reflectopinions of the institutions with which authors are affiliated.

r 2007 The Authors. Journal compilation r International Review of Finance Ltd. 2007. Published by BlackwellPublishing Ltd., 9600 Garsington Road, Oxford OX4 2DQ, UK and 350 Main Street, Malden, MA 02148, USA.

International Review of Finance, 6:3–4, 2006: pp. 129–155

I. INTRODUCTION

A growing number of empirical studies in recent years have examined thetrading behavior of diverse investor types such as individual investors, variousinstitutional investors, and foreign investors.1 These studies have shown thatthere are significant differences in the trading behavior of various investortypes. However, it is not clear whether the different trading behaviors of variousinvestor types result in significant differences in trade performances. In efficientmarkets, we expect no investor types to perform persistently better or worsethan other investor types. Our paper investigates this issue using data thatinclude trades of all investor types that trade on the Tokyo Stock Exchange(TSE). Our paper not only compares the trading performance of all investortypes across the entire equity market but also measures trading gains and lossesfrom different sources. We examine the impact of trading intervals, pricespreads, and market timing on the trading performance of various investortypes. For this purpose, we develop a trade-weighted measure of tradingperformance using buy and sell volumes.

We raise two issues regarding previous studies that examined the tradeperformance of various investor types (see Section II for a review of priorstudies). First, because different studies have measured trade performancesdifferently, it is difficult to compare results from divergent studies and drawgeneral conclusions. Second, prior studies typically examined single measuresof trade performance in each study. However, some investor types might havepoor market timing in the long run but might generate profits by churningstocks in the short run and compensate for the loss from poor market timing. Ifsuch gains outweigh the losses from poor market timing, these types ofinvestors can continue to participate in a competitive market.

The important result of our paper is that we find some investor types showcomparative advantages in different trading abilities. We find that foreigninvestors consistently have better market timing abilities compared with otherdomestic investors. In fact, we provide evidence that foreign investors cannotmake positive trading gains unless they have good market timing abilitybecause foreign investors buy portfolio of stocks at higher average prices thanthe portfolio of stocks they sell. In contrast, we find that individual investorsoffset losses from poor market timing by selling portfolio of shares atsignificantly higher prices than the purchase prices on average. We find that

1 Among other studies, Choe et al. (1999, 2004) examined trading behavior of various investor

types for the Korean equity market; Grinblatt and Keloharju (2000, 2001), for the Finnish

market; and Hamao and Mei (2001), Kamesaka et al. (2003), and Karolyi (2002), for the Japanese

market. Barber and Odean (2000) and Odean (1999) studied the trading of individual investors

in the United States. Cai et al. (2000), Lakonishok et al. (1992), and Nofsinger and Sias (1999)

studied the trading behavior of US institutional investors. Barber and Odean (2003), Cohen

(1999), Cohen et al. (2002), and Griffin et al. (2003) compared trading behavior of individual

investors and institutional investors. For various markets, Bailey et al. (2007), Brennan and Cao

(1997), Froot, et al. (2001), and Seasholes (2000) examined trading of foreign investors.

International Review of Finance

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007130

individual investors perform better than other investor types for very shorttrading horizons due to the positive price spreads. However, for long-runtrading intervals, we find that the trading gains from market timing dominatethe overall trading performance for various investor types.

One of the interesting aspects of examining equity trades in the TSE duringour observation period (1991–1999) is that foreign investors’ trades significantlyincreased during the period. Because foreign investors do not always have thesame institutional constraints as domestic investors, we are able to examinehow foreign investors and domestic investors interact with each other in theirtrades. We find evidence that foreign investors buy from Japanese domesticinstitutions that sell a large volume of shares possibly for window-dressingpurposes as well as for adjusting their stock ownership near the fiscal year-end(FYE). Our results suggest that foreign investors exploit significant trading gainsfrom domestic institutions that sell shares during the FYE period.

The data from the TSE uniquely suit our objective because the data not onlyrecord buy and sell trades of different investor types but also enable us tocompute trade-weighted average prices of both buy and sell trades for allinvestor types. For each investor type, the trade-weighted average prices reflectthe average selection of stocks traded by each investor type. Also, our data coverportfolio trading across the entire market. Because a sell trade in the marketmust clear every buy trade, we are able to examine the correlations of nettrading gains among all investor groups for the entire market.

This paper is organized as follows. Section II reviews the literature. Section IIIdiscusses the data and provides descriptive statistics on trading by differentinvestor types. Section IV reports correlations of trades among different investortypes, correlations between trades and market returns, and seasonal tradingpatterns. Section V investigates the impacts of trading price spreads, markettiming, and trading frequencies on trade performance for different investortypes. Section VI provides concluding remarks.

II. PRIOR STUDIES OF TRADING PERFORMANCE OF VARIOUSINVESTOR TYPES

Although an extensive number of studies have explored the trading behavior ofvarious investor types, not many studies have addressed their tradingperformances. Among those that have, most studies have found poorperformance of individual investors. For example, Barber and Odean (2000)and Odean (1999) reported that individual investors in the United States tradeexcessively, which results in poor portfolio performance. Barber and Odeanused individual investors’ household portfolio returns and compared themagainst the various benchmarks, including the market portfolio and the multi-factor benchmark. They found that individual investors gain poor net returnsafter adjusting for trading costs. By using market-wide data from the Finnishstock market, Grinblatt and Keloharju (2000) found individual investors do not

How do Investors Win and Lose in Equity Trades?

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007 131

pick future winning stocks better than domestic institutional investors andforeign investors. Cohen (1999) found that individual investors buy stock frominstitutions after price increases and sell to institutions after price decreases inthe United States, which suggests that individual investors are bad markettimers and institutions are good market timers. In a related study, Cohen et al.(2002) examined the interactions between individuals and institutions in theUS stock market and found that institutions profited from the underreaction ofstock prices by buying shares from individuals in response to good cash flownews. A recent paper by Barber et al. (2007) examine trade performances ofindividual investors and various institutional investors using a comprehensivedata from the Taiwan Stock Exchange. They find that individual investors incurtrading losses after costs due to aggressive trading, whereas institutionalinvestors profit from trade after cost. Altogether, previous empirical resultssuggest that individual investors are generally poor performers of equitytrading.

A number of researchers have also compared the performance of foreigninvestors with domestic investors. However, these studies show mixed results.Seasholes (2000) found that foreigners generally perform well compared withdomestic investors in emerging markets. He found that foreign investors’ tradespredict future price movements and earn abnormal profits. Froot et al. (2001)and Froot and Ramadorai (2001) examined international portfolio flows forvarious countries and also found that foreign investors trades forecast futureequity returns relatively well. Karolyi (2002) and Kamesaka et al. (2003) alsoshowed that foreign investors in the Japanese equity market have good marketpredicting ability of the market index.2 In contrast, other studies have shownthat foreign investors do not necessarily have good trade performance.Dahlquist and Robertsson (2004) suggested foreign investors are not necessarilygood at picking future winning stocks for the Swedish market. Choe et al.(2005) suggested that foreign investors do not have a private informationadvantage over Korean individual investors. They showed that individualinvestors have a higher proportion of buy trades than sell trades preceding largeprice movements, whereas foreigners have a higher proportion of buy tradesthan sell trades after the event. They also showed that foreign investors trade atworse prices than individual investors. While Dvorak (2005) found domesticinvestors have an information advantage over foreign investors on average, healso showed evidence that some global brokerages have better informationbecause of their experience and expertise. In sum, the prior studies show thatwhether foreign investors perform better or worse than domestic investors isinconclusive.

Although several other papers have compared the trading performance ofvarious investor types across the entire equity market (Grinblatt and Keloharju

2 Hamao and Mei (2001) found that foreign investors show insignificant degree of timing ability

in the Japanese stock market during most of the 1980s. On the other hand, Karolyi (2002) and

Kamesaka et al. (2003) used data from the 1990s.

International Review of Finance

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007132

2000; Karolyi 2002; Kamesaka et al. 2003), most of these studies each examinedonly single aspect of equity trading performance. Our paper examines differentsources of trading performances such as trading prices, market timing, andtrading frequencies of various investor types, which provides us with a morecomplete picture of the performance of various investor types in the entireequity market.3

III. DATA AND SUMMARY STATISTICS

A. Data

We use weekly trading data on the First Section of the TSE. The TSE categorizesthe member securities companies’ brokered trades by classifying trades intothose by individuals, foreigners, and institutions. Institutions are furtherclassified into nonfinancial corporations, mutual funds, insurance companies,and banks. The data comprise the volume (i.e., number of shares traded) andthe amount of trade in yen (f) for both buy and sell trades for each investortype. The TSE reports trades that are aggregated across individual stocks for eachinvestor type. The data cover all trades brokered by TSE’s member securitiescompanies that have a capitalization of at least f3 billion. The data also includethe proprietary trades of these securities companies. Altogether, the dataaccount for approximately 90% of trades in the First Section of the TSE.

Among the domestic institutions, professional fund managers undertake theequity trading for mutual funds, insurance companies, and banks. A large partof trades by banks are by trust banks, which manage equity funds that includecorporate pensions.4 The foreign investors category includes both institutionaland individual investors, but most trades are believed to be from professionalfund managers. On the other hand, individual investors and nonfinancialcorporations mostly consist of investors that are not professional fundmanagers (i.e., nonprofessional investors). Particularly, the equity trading bynonfinancial corporations arises not only through corporate asset managementbut also from adjustment of cross-shareholdings in Japanese corporate groups.It is understood among TSE member firms that one of the functions of theproprietary trading of securities companies is to facilitate the execution ofcustomer orders. Therefore, proprietary trades include both liquidity-providingactivity and the autonomous trades of the member securities firms.

3 A recent study by Barber et al. (2007) is among the few studies that examine stock selection as

well as market timing abilities for different investor types.

4 The bank category also includes trading by commercial banks. Although the nature of equity

trading by commercial banks differs from equity trading by professional fund managers of trust

banks, trading by commercial banks is 10% or less of all trades in this category. Data on the

breakdown of bank trades into commercial and trust banks are available only for September

1996 and later.

How do Investors Win and Lose in Equity Trades?

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007 133

Our sample period begins with the first week of January 1991 and ends withthe last week of April 1999. We choose 1991 as the beginning of our observationperiod because the period immediately before 1990 is the so-called ‘asset pricebubble’ period in Japan. Because the Japanese government allowed investors toexecute equity trades outside the stock exchanges after April 1999, we chosethis month as the end of our observation period as our data do not includetrades executed outside the TSE. Unless otherwise noted, all data used in thispaper are from the Nomura Research Institute.

B. Descriptive statistics of trades

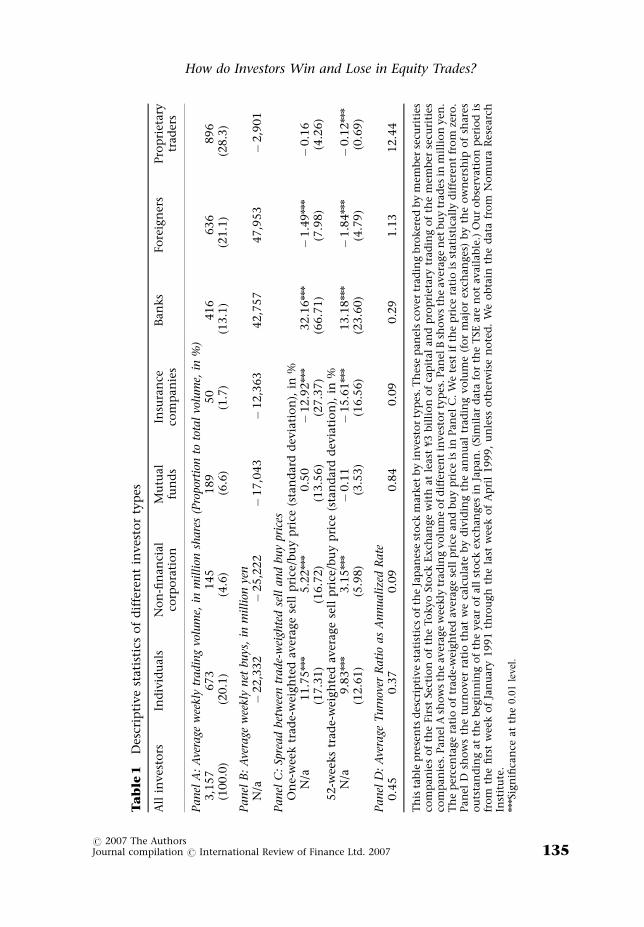

In Table 1, Panel A shows the weekly trading volume of different investor typesand the proportion of that volume to the total trading volume between January1991 and April 1999. Of all investor types, the major traders are the proprietarytraders of securities companies, individuals, foreigners, and banks. Theseinvestors account for between 75% and 80% of the trades. Other investortypes, such as mutual funds, insurance companies, and nonfinancial corpora-tions, account for relatively small shares of the trades. Panel B shows theaverage yen amount of the net buys of different investor types. During ourobservation period, foreign investors and banks were net buyers, and all otherdomestic investors were net sellers on average.

In Table 1, Panel C shows the percentage spread between trade-weightedaverage sell price and trade-weighted average buy price for each investor type(i.e., average sell price/average buy price-1). We calculate the spread for both 1-week trades and accumulated 52-week trades. The 52-week spread has smallerstandard deviations because short-term fluctuations are smoothed out. Fromboth 1-week and 52-week average price spreads, we find that investors such asforeign investors and insurance companies have negative average spreads thatare significantly different from zero, which implies that these investors onaverage lose money from equity turnovers. Other investors such as individualinvestor, nonfinancial corporations and banks have significant positive spreads.Particularly, we find that banks and individual investors have the largestpositive spreads.

In Table 1, Panel D shows the average turnover ratios for each investor type.5

The average turnover of the entire market is 0.45 times per year. The turnoverratio of individual investors (0.37) is lower than the market average.Nonfinancial corporations have a low turnover ratio (0.09), because a largepart of their shares are cross-held among group companies and are not tradedfrequently. Insurance companies also have a low turnover ratio (0.09) as theynaturally have long investment horizons. The turnover ratio of banks (0.29)

5 We calculate the turnover ratio by dividing the annual trading volume (for major exchanges) by

the ownership of shares outstanding at the beginning of the year of all stock exchanges in

Japan. (Similar data for the TSE are not available.) The percentage share of trades for the TSE is

more than eighty-five percent of total trades of all stock exchanges in Japan.

International Review of Finance

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007134

Ta

ble

1D

escr

ipti

ve

stati

stic

so

fd

iffe

ren

tin

ves

tor

typ

es

All

inves

tors

Ind

ivid

uals

No

n-fi

nan

cial

corp

ora

tio

nM

utu

al

fun

ds

Insu

ran

ceco

mp

an

ies

Ban

ks

Fo

reig

ner

sPro

pri

etary

trad

ers

Panel

A:

Ave

rage

wee

kly

tradin

gvo

lum

e,in

million

share

s(P

ropor

tion

toto

tal

volu

me,

in%

)3,1

57

673

145

189

50

416

636

896

(100.0

)(2

0.1

)(4

.6)

(6.6

)(1

.7)

(13.1

)(2

1.1

)(2

8.3

)

Panel

B:

Ave

rage

wee

kly

net

buys

,in

million

yen

N/a

�22,3

32

�25,2

22

�17,0

43

�12,3

63

42,7

57

47,9

53

�2,9

01

Panel

C:

Spre

ad

bet

wee

ntr

ade-

wei

ghte

dse

lland

buy

pri

ces

On

e-w

eek

trad

e-w

eigh

ted

aver

age

sell

pri

ce/b

uy

pri

ce(s

tan

dard

dev

iati

on

),in

%N

/a11.7

5nnn

5.2

2nnn

0.5

0�

12.9

2nnn

32.1

6nnn

�1.4

9nnn

�0.1

6(1

7.3

1)

(16.7

2)

(13.5

6)

(27.3

7)

(66.7

1)

(7.9

8)

(4.2

6)

52-w

eeks

trad

e-w

eigh

ted

aver

age

sell

pri

ce/b

uy

pri

ce(s

tan

dard

dev

iati

on

),in

%N

/a9.8

3nnn

3.1

5nnn

�0.1

1�

15.6

1nnn

13.1

8nnn

�1.8

4nnn

�0.1

2nnn

(12.6

1)

(5.9

8)

(3.5

3)

(16.5

6)

(23.6

0)

(4.7

9)

(0.6

9)

Panel

D:

Ave

rage

Turn

over

Rati

oas

Annualize

dR

ate

0.4

50.3

70.0

90.8

40.0

90.2

91.1

312.4

4

Th

ista

ble

pre

sen

tsd

escr

ipti

ve

stati

stic

so

fth

eJa

pan

ese

sto

ckm

arket

by

inves

tor

typ

es.T

hes

ep

an

els

cover

trad

ing

bro

ker

edb

ym

ember

secu

riti

esco

mp

anie

so

fth

eFir

stSe

ctio

no

fth

eTo

kyo

Sto

ckExch

an

ge

wit

hat

least

f3

bil

lio

no

fca

pit

al

an

dp

rop

riet

ary

trad

ing

of

the

mem

ber

secu

riti

esco

mp

anie

s.Pan

elA

sho

ws

the

aver

age

wee

kly

trad

ing

vo

lum

eo

fd

iffe

ren

tin

ves

tor

typ

es.Pan

elB

sho

ws

the

aver

age

net

bu

ytr

ad

esin

mil

lio

nyen

.T

he

per

cen

tage

rati

oo

ftr

ad

e-w

eigh

ted

aver

age

sell

pri

cean

db

uy

pri

ceis

inPan

elC

.W

ete

stif

the

pri

cera

tio

isst

ati

stic

all

yd

iffe

ren

tfr

om

zero

.Pan

elD

sho

ws

the

turn

over

rati

oth

at

we

calc

ula

teb

yd

ivid

ing

the

an

nu

al

trad

ing

vo

lum

e(f

or

maj

or

exch

an

ges

)b

yth

eo

wn

ersh

ipo

fsh

ares

ou

tsta

nd

ing

at

the

beg

inn

ing

of

the

yea

ro

fall

sto

ckex

chan

ges

inJa

pan

.(S

imil

ar

data

for

the

TSE

are

no

tavail

ab

le.)

Ou

ro

bse

rvati

on

per

iod

isfr

om

the

firs

tw

eek

of

Jan

uary

1991

thro

ugh

the

last

wee

ko

fA

pri

l1999,

un

less

oth

erw

ise

no

ted

.W

eo

bta

inth

ed

ata

fro

mN

om

ura

Res

earc

hIn

stit

ute

.nnnSi

gn

ifica

nce

at

the0.01level.

How do Investors Win and Lose in Equity Trades?

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007 135

reflects the low turnover of commercial banks, as their shareholdings are part ofthe cross-holdings of corporate groups (i.e., keiretsu). However, trust banks,whose trading volume is around 90% of the entire trading volume in the Bankscategory, have higher turnover because they are professional fund managers.For example, after 1997, when a breakdown of the data is available, the averageturnover ratio of trust banks is 0.60 per year, compared with 0.14 per year forcommercial banks. Foreigners and mutual funds have higher turnover than themarket average (1.13 for foreigners, 0.84 for mutual funds). The turnover ratioof proprietary traders (12.44) is the highest among all investor types, which isnot surprising given the liquidity-providing role of proprietary traders.

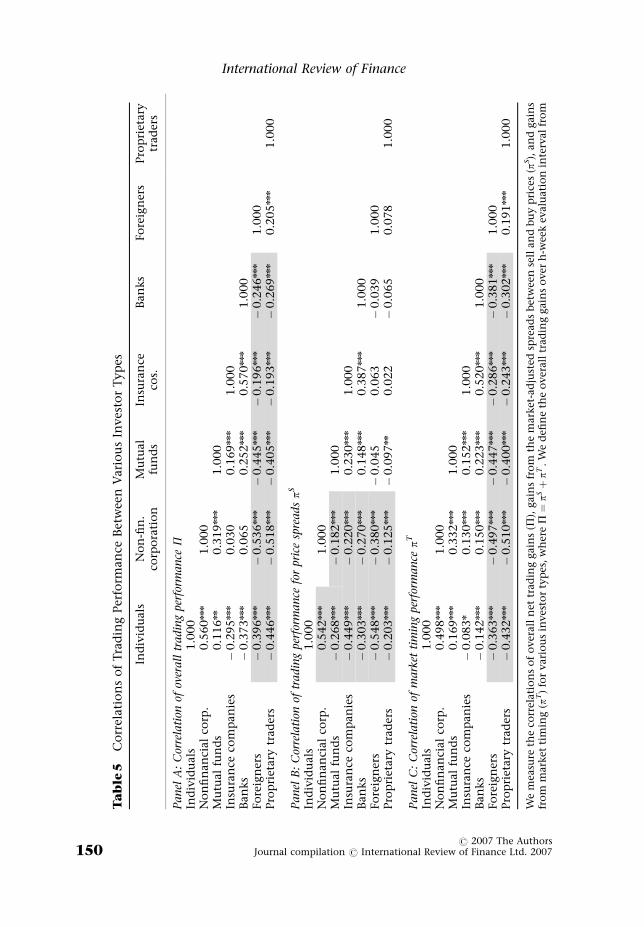

IV. CORRELATIONS AND PATTERNS OF TRADE AMONG INVESTORTYPES

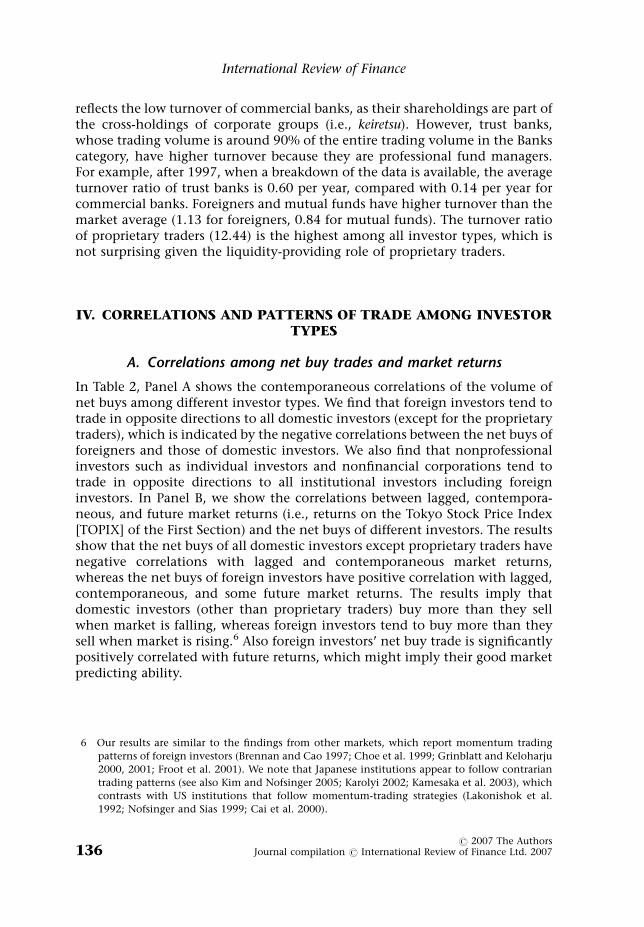

A. Correlations among net buy trades and market returns

In Table 2, Panel A shows the contemporaneous correlations of the volume ofnet buys among different investor types. We find that foreign investors tend totrade in opposite directions to all domestic investors (except for the proprietarytraders), which is indicated by the negative correlations between the net buys offoreigners and those of domestic investors. We also find that nonprofessionalinvestors such as individual investors and nonfinancial corporations tend totrade in opposite directions to all institutional investors including foreigninvestors. In Panel B, we show the correlations between lagged, contempora-neous, and future market returns (i.e., returns on the Tokyo Stock Price Index[TOPIX] of the First Section) and the net buys of different investors. The resultsshow that the net buys of all domestic investors except proprietary traders havenegative correlations with lagged and contemporaneous market returns,whereas the net buys of foreign investors have positive correlation with lagged,contemporaneous, and some future market returns. The results imply thatdomestic investors (other than proprietary traders) buy more than they sellwhen market is falling, whereas foreign investors tend to buy more than theysell when market is rising.6 Also foreign investors’ net buy trade is significantlypositively correlated with future returns, which might imply their good marketpredicting ability.

6 Our results are similar to the findings from other markets, which report momentum trading

patterns of foreign investors (Brennan and Cao 1997; Choe et al. 1999; Grinblatt and Keloharju

2000, 2001; Froot et al. 2001). We note that Japanese institutions appear to follow contrarian

trading patterns (see also Kim and Nofsinger 2005; Karolyi 2002; Kamesaka et al. 2003), which

contrasts with US institutions that follow momentum-trading strategies (Lakonishok et al.

1992; Nofsinger and Sias 1999; Cai et al. 2000).

International Review of Finance

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007136

Ta

ble

2C

orr

elati

on

sam

on

gth

en

etb

uy

vo

lum

eso

fd

iffe

ren

tin

ves

tor

typ

esan

dm

ark

etre

turn

s

Ind

ivid

uals

No

nfi

nan

cial

corp

ora

tio

nM

utu

al

fun

ds

Insu

ran

ceco

s.B

an

ks

Fo

reig

ner

sPro

pri

etary

trad

ers

Panel

A:

Cor

rela

tion

ofnet

buy

volu

mes

Ind

ivid

uals

1.0

00

No

nfi

nan

cial

corp

.0.3

50nnn

1.0

00

Mu

tual

fun

ds

�0.1

15n

0.2

82nnn

1.0

00

Insu

ran

ceco

mp

an

ies

�0.3

14nnn

0.2

20nnn

0.1

19nn

1.0

00

Ban

ks

�0.1

16nn

0.3

57nnn

0.3

35nnn

0.4

42nnn

1.0

00

Fo

reig

ner

s�

0.4

10nnn

�0.5

71nnn

�0.3

13nnn

�0.2

01nnn

�0.5

33nnn

1.0

00

Pro

pri

etary

trad

ers

�0.2

98nnn

�0.4

17nnn

�0.3

51nnn

�0.2

24nnn

�0.5

02nnn

0.0

31

1.0

00

Panel

B:

Cor

rela

tion

bet

wee

nla

gged

,co

nte

mpor

aneo

us,

and

futu

reT

OPIX

retu

rns

(r)

and

net

buy

volu

me

r t�

4�

0.0

32

�0.0

62

�0.0

26

�0.0

76

�0.0

39

0.1

02nn

�0.0

14

r t�

3�

0.0

15

�0.0

72

�0.0

65

�0.1

23nn

�0.1

29nnn

0.1

62nnn

0.0

17

r t�

2�

0.0

37

�0.1

23nn

�0.1

21nn

�0.0

66

�0.1

66nnn

0.2

10nnn

0.0

41

r t�

1�

0.0

02

�0.1

92nnn

�0.2

74nnn

�0.1

96nnn

�0.2

68nnn

0.2

50nnn

0.1

50nnn

r t�

0.1

96nnn

�0.5

36nnn

�0.2

19nnn

�0.1

98nnn

�0.3

08nnn

0.3

26nnn

0.3

56nnn

r t1

10.0

13

�0.0

35

�0.0

64

�0.0

84n

�0.0

33

0.0

76

�0.0

11

r t1

2�

0.0

72

�0.1

15nn

�0.0

71

�0.0

55

�0.0

86n

0.1

42nnn

0.0

68

r t1

30.0

04

�0.0

43

�0.0

66

�0.0

52

�0.0

19

0.0

84nn

�0.0

23

r t1

4�

0.0

06

�0.0

21

�0.0

13

�0.0

25

�0.1

10

0.0

75

0.0

49

Pan

elA

sho

ws

the

Pea

rso

nco

rrel

atio

no

fth

en

etb

uy

vo

lum

esam

on

gd

iffe

ren

tin

ves

tor

typ

es.

Pan

elB

sho

ws

the

corr

elat

ion

bet

wee

nm

arket

retu

rns

an

dth

en

etb

uy

vo

lum

eso

fvari

ou

sin

ves

tor

typ

es.

Th

ed

ata

com

pri

seth

en

etbu

yvo

lum

eso

fth

eFir

stSe

ctio

no

fth

eTo

kyo

Sto

ckExch

an

ge

that

are

bro

ker

edb

ym

ember

secu

riti

esco

mp

anie

sw

ith

at

least

f3

bil

lio

no

fca

pit

alan

dth

en

etbu

yvo

lum

eso

fth

ep

rop

riet

ary

trad

ing

div

isio

no

fth

em

emb

erco

mp

an

ies.

We

com

pu

tem

ark

etre

turn

sas

wee

kly

log

pri

cech

an

ges

fro

mth

eT

OPIX

.T

he

sam

ple

per

iod

isfr

om

the

firs

tw

eek

of

Jan

uary

1991

thro

ugh

the

last

wee

ko

fA

pri

l1999.

Th

esa

mp

leco

mp

rise

s435

ob

serv

ati

on

s.nSi

gn

ifica

nce

at

the0.10

level

.nnSignificance

atthe0.05

level

.nnnSignificance

atthe0.01

level

.

How do Investors Win and Lose in Equity Trades?

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007 137

B. Seasonal trading patterns: FYE effect

Several studies have found seasonal trading patters in the Japanese equitymarket during the FYE period. Bremer and Kato (1996) reported that stocks withgains in Japan have higher turnover in March. Kato and Loewenstein (1995)suggested that overall increase in trading volumes of most domestic institutionsaround the FYE could reflect the temporary stock ownership adjustments ofgroup company (keiretsu) firms.7 In our paper, we examine if seasonal tradingpatterns near the FYE affect the trading performance of various investor types.Therefore, in this section we investigate if there are any seasonal patterns of buyand sell trades for different investor types.

We estimate the following regression model for volumes of each investortype:

Volumet ¼ aþX12

j¼1bjMonthDumj;t þ e

t

where X12

j¼1wjbj ¼ 0: ð1Þ

Volumet denotes buy or sell volume data in week t, and MonthDumj, t is a dummyvariable that takes the value of 1 if Volumet is from month j and zero otherwise.The intercept measures the average volume, and bj measures the deviation fromthe average volume for month j. The weight, wj, is the proportion of month j inthe sample. Because we constrain the weighted sum of 12 monthly coefficientsto be zero in the estimation procedure, each coefficient indicates the monthlydeviation from the average volume for the observation period, which is theintercept.

Panels A and B in Table 3 show that during the period from January throughMarch, most domestic institutions sell more than they buy compared withother periods. We find that the sell volume of domestic institutions, particularlythat of banks, is greatest in March. Whereas the adjustments of stock holdingsby institutional investors explain the increase in the overall trading around theFYE (Kato and Loewenstein 1995), a unique Japanese corporate accounting rulemight partly explain the sell trading patterns of domestic institutional investorsbefore the FYE. Under this accounting rule, capital gain is realized andrecognized as income only if the shares are sold. Observers of the Japaneseequity market point to the fact that this rule motivates domestic institutions tosell shares to realize capital gains and to window-dress their profits during the

7 He et al. (2004) showed that US institutions, particularly investment advisors who act as

external managers such as mutual funds, tend to sell loser stock at year-end to window-dress

their portfolios. Ng and Wang (2004) also observed similar year-end trading patterns for small

stocks that are held by US institutions.

International Review of Finance

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007138

Ta

ble

3Se

aso

nali

tyo

fb

uy

an

dse

llvo

lum

esb

yin

ves

tor

typ

es

Ind

ivid

uals

No

nfi

nan

cial

corp

ora

tio

ns

Mu

tual

fun

ds

Insu

ran

ceco

s.B

an

ks

Fo

reig

ner

sPro

pri

etary

trad

ers

Panel

A:

Seaso

nality

inbuy

volu

mes

Inte

rcep

t339.8

48nnn

60.1

19nnn

85.3

29nnn

16.2

34nnn

220.8

80nnn

348.7

07nnn

446.1

64nnn

Jan

uary

�53.6

40n

�10.2

69n

�17.7

79nn

�2.2

69

�59.7

51nnn

�33.5

67

�86.9

81nnn

Feb

ruary

76.7

30nn

14

.76

9nnn

3.0

56

7.7

08nnn

�12.6

27

40.0

48

54.2

72n

Marc

h1

14

.17

8nnn

37

.53

9nnn

13.3

26

14

.97

1nnn

45

.03

7nnn

11

1.5

60nnn

13

4.6

64nnn

Ap

ril

14

7.7

72nnn

13.3

50nn

18.3

29nn

�3.9

38nn

50

.61

6nnn

40.1

79

64.0

24nn

May

�28.3

84

�10.6

38n

6.7

37

�5.2

90nnn

�5.0

26

�36.1

42

�30.2

81

Jun

e�

17.0

93

�3.2

91

16.9

11n

�1.0

00

22.9

62

9.8

37

22.8

92

July

�49.1

41

�13.3

42nn

�0.5

01

�2.9

73

�18.9

68

�28.8

75

�38.5

82

Au

gu

st�

46.0

48

�10.3

18n

�12.3

54

�3.8

14nn

�24.9

94n

�14.5

28

�46.5

30

Sep

tem

ber

�11.6

72

6.5

75

10.8

03

�0.4

76

18.9

81

�4.7

58

66.5

34nn

Oct

ob

er�

71.3

55nn

�12.3

82nn

�0.8

09

�0.8

69

�15.2

22

�29.3

27

�53.9

90nnn

No

vem

ber

�49.8

45

�9.8

47n

�21.3

89nn

�0.4

25

1.9

84

�41.2

54

�63.9

59nn

Dec

emb

er.

�29.6

49

�5.2

79

�16.0

73n

�2.7

02

0.6

92

�23.7

97

�23.9

13

Ad

just

edR

20.0

84

0.1

31

0.0

26

0.1

63

0.0

75

0.0

40

0.0

84

Wald

test

50.6

9nnn

76.6

2nnn

22.4

0nn

95.4

6nnn

46.3

2nnn

29.0

5nnn

50.9

3nnn

Panel

B:

Seaso

nality

inse

llvo

lum

esIn

terc

ept

333.0

45nnn

84.5

69nnn

103.3

03nnn

33.8

99nnn

195.4

83nnn

315.1

68nnn

449.9

28nnn

Jan

uary

�48.8

08n

�12.3

25n

�21.3

56nn

�0.8

48

�29.2

55n

�41.3

64n

�113.6

68nnn

Feb

ruary

53.8

17n

30

.96

8nnn

22.6

45nn

15

.21

4nnn

42

.94

9nnn

0.7

37

14.7

94

Marc

h8

5.2

20nnn

59

.73

1nnn

38

.00

1nnn

19

.04

1nnn

10

4.9

65nnn

25.0

92

13

9.7

01nnn

Ap

ril

13

6.8

13nnn

1.0

38

25.4

26nn

�5.0

89

22.4

56

41.2

41n

11

0.0

86nnn

May

�18.9

67

�20.3

83nnn

�2.9

22

�0.9

47

�17.3

44

�19.9

58

�30.7

00

Jun

e�

5.0

87

�12.7

31n

9.6

07

�6.9

84

�9.9

90

22.5

43

61.0

80nn

July

�36.0

31

�20.4

17nnn

�2.3

59

�6.5

77

�20.8

88

�25.8

32

�34.4

66

How do Investors Win and Lose in Equity Trades?

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007 139

Ta

ble

3(c

onti

nued

)

Ind

ivid

uals

No

nfi

nan

cial

corp

ora

tio

ns

Mu

tual

fun

ds

Insu

ran

ceco

s.B

an

ks

Fo

reig

ner

sPro

pri

etary

trad

ers

Au

gu

st�

33.8

10

�9.8

96

�19.4

39n

�8.0

92nn

�22.3

67

�13.7

02

�59.0

13nn

Sep

tem

ber

�9.1

34

19.3

85nn

1.3

49

�4.4

22

14.5

51

5.0

85

48.7

79

Oct

ob

er�

45.3

23

�20.8

88nnn

�17.8

10

�9.2

09nn

�41.0

92nn

8.1

72

�63.3

03nn

No

vem

ber

�44.9

83

�13.2

10n

�23.6

19nn

�1.2

50

�40.8

94nn

12.9

29

�75.7

56nn

Dec

emb

er.

�49.0

34

�5.2

76

�12.5

07

7.2

07n

�11.6

31

�13.2

32

4.0

40

Ad

just

edR

20.0

65

0.1

99

0.0

56

0.0

87

0.1

15

�0.0

04

0.1

22

Wald

test

41.3

7nnn

118.6

0nnn

36.7

5nnn

52.2

1nnn

67.2

6nnn

9.3

471.0

2nnn

Th

ista

ble

pre

sen

tsth

ese

aso

nal

patt

ern

so

fb

uy

an

dse

llvo

lum

eso

fd

iffe

ren

tin

ves

tor

typ

es.

We

esti

mate

the

foll

ow

ing

regre

ssio

nm

od

elfo

rvo

lum

eso

fea

chin

ves

tor

typ

e:

Vol

um

e t¼

aþX 1

2

j¼1b j

Mon

thD

um

j;tþe t;

wh

ere

X 12

j¼1

wjb

j¼

0:

Vol

um

e td

eno

tes

bu

yo

rse

llvo

lum

ed

ata

inw

eek

t,an

dM

onth

Dum

j,tis

ad

um

my

var

iab

leth

at

takes

the

valu

eo

fo

ne

ifV

olum

e tis

fro

mm

on

thjan

dze

roo

ther

wis

e.T

he

inte

rcep

tm

easu

res

the

aver

age

vo

lum

ean

db j

mea

sure

sth

ed

evia

tio

nfr

om

the

aver

age

vo

lum

efo

rm

on

thj.

Th

ew

eigh

t,w

j,is

the

pro

po

rtio

no

fm

on

thjin

the

sam

ple

.V

olu

me

data

are

inw

eekly

freq

uen

cyan

dco

ver

trad

eso

nth

eFir

stSe

ctio

no

fth

eTo

kyo

Sto

ckExch

an

ge.

Th

esa

mp

lep

erio

dis

fro

mJa

nu

ary

1991

thro

ugh

Ap

ril

1999.

Th

esa

mp

leco

mp

rise

s435

ob

serv

ati

on

s.M

arc

his

hig

hli

gh

ted

bec

au

seth

een

do

fM

arc

his

the

fisc

al

yea

r-en

dfo

rm

ost

Jap

anes

eco

mp

anie

s.nSi

gn

ifica

nce

at

the0.10

level

.nnSignificance

atthe0.05

level

.nnnSignificance

atthe0.01

level

.Si

gn

ifica

nt

case

sat

the0.01

level

wit

hp

osi

tive

coef

fici

ents

are

inb

old

chara

cter

s.

International Review of Finance

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007140

FYE period (see Bremer and Kato 1996).8 Our results in Table 3 are consistentwith this explanation. In contrast, foreign investors are significant buyers inMarch (see Panel A), whereas their sell volume in Panel B does not show anysignificant seasonal patterns. Foreign investors, who do not need to follow thesame tax and accounting rules as domestic investors, could purchase shares atbetter terms before the FYE and improve their trading performance, whereasdomestic institutional investors might sell shares at unfavorable conditions.Individual investors also tend to buy more than they sell in March, which isconsistent with the fact that individual investors do not have any specialincentives to sell shares before end-March.

One might argue that foreign investors buy shares in March before the FYEbased on information. However, because most public information related to thelatest financial reports become available after April, information-based tradingmight not explain the large buy trades of foreign investors in March. Also, theinformation story cannot explain the greater buy trades of individual investorsin March as most individual investors only have access to public information.Therefore, our results suggest that foreign investors and some individualinvestors are timing their buy trades before the FYE when domestic institutionssell their shares.

V. TRADING PRICES, MARKET TIMING, AND TRADING INTERVALS

In this section, we examine trading gains and losses of various investor types. InSection V.A, we develop a new trading performance measure and explain thetest methodology. In Section V.B, we present the results.

A. Performance measures and test methodology

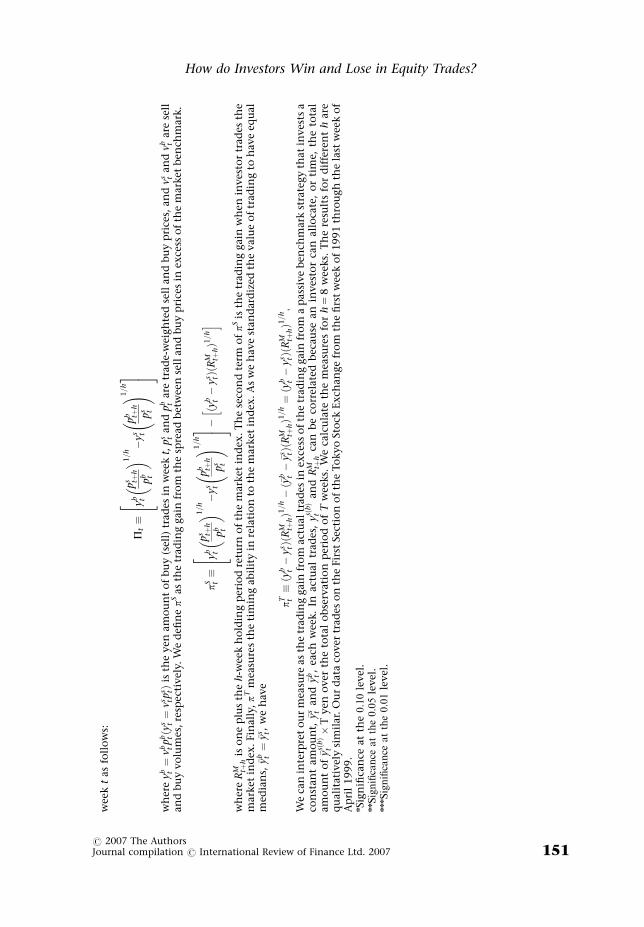

We develop a performance metric that gauges the net trading gains of securitiestrading. We define the net trading gains as net cash inflows generated by trades.Specifically, we define the gains as net cash inflows that increase the level ofportfolio holdings after adjusting for trade size and the number of shares traded.Because trade sizes as well as the level of net buy trades are different for variousinvestor types, we create a standardized measure that compares tradingperformances between different investor types. We assume that investorinitially buys (sells) the portfolios of shares during week t and subsequentlysells (buys) the same number of shares during week t1h. Given the samenumber of shares traded, trade performance is determined by the spread

8 A widely used accounting rule is called teikaho, under which a company or financial institution

can choose between cost or market price, whichever is lower, to value its asset. Particularly,

cross-held shares among keiretsu companies have low acquisition costs if they were purchased at

issue many years previously, which gives the companies greater incentives to sell these shares

when they need to increase profits. Under the new accounting standards that became effective

in fiscal year 2001, securities holdings must be valued at market prices.

How do Investors Win and Lose in Equity Trades?

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007 141

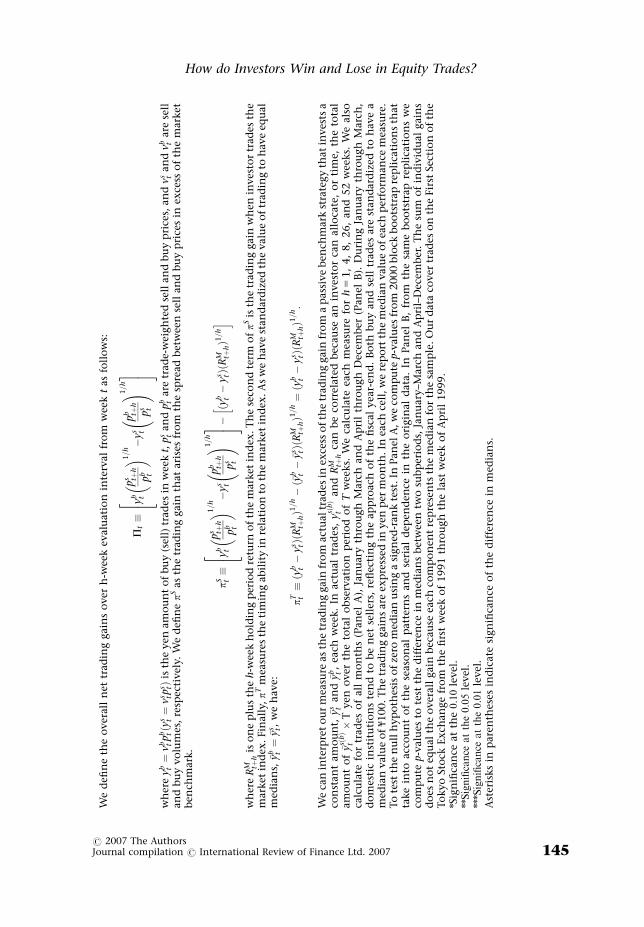

between trade-weighted buy and sell prices. We also standardize the yenamount of buy and sell trades so that the net buy trade (buy minus sell trade) forthe observation period is zero. Therefore, the trade performance is alsodetermined by the allocation (or the timing) of trades over a specified period.An investor could achieve better market timing performance if he/she allocatedmore buy trades than sell trades before increases in market returns. We definethe overall net trading gains over h-week trading horizon as follows:

Pt � ybt

pstþh

pbt

� �1=h

�yst

pbtþh

pst

!1=h24

35 ð2Þ

where ybt ¼ vb

t pbt ðys

t ¼ vst p

stÞ is the yen amount of buy (sell) trades in week t, ps

t andpb

t are trade-weighted sell and buy prices, and vst and vb

t are sell and buy volumes,respectively. The yen amount of buy and sell trades are adjusted to have thesame median values. We use the median instead of the mean because trades areknown to have skewed distributions. This measure assumes that the investorbuys vb

t shares (sells vst shares) at week t and sells (buys) the same volume of

shares at week t1h, but allowing for different selections of shares for each trade.We can interpret

pstþh

pbt

andpb

tþh

pst

as the intertemporal spreads of trade-weightedaverage prices, which reflect the stock selection as well as the trade weights ofshares each investor type chooses to trade.9 Our definition of stock selectionrefers to the choice of stocks that investors choose to buy and sell, whereas theconventional definition used for portfolio performance measurement refers tothe selection of stocks that investors decide to hold in their portfolios at thebeginning of the holding period.

Our performance measure has the following implications. If our overall nettrading gain is positive (negative), P 4 0 (o 0), it implies that the net cash flowfrom trade at time t and t1h increases (decreases) the level of the underlyingportfolio under the assumption that the same number of shares are traded attime t and t1h. In this regard, we analyze net gains that arise from trades ofmarginal investors but not profits that arise from changes in the valuation ofportfolio holdings that might not be actually traded. We decompose P into twocomponents, net-trading gains arising from price spreads and those arising frommarket timing. We define pS as the net trading gains that arise due to(intertemporal) price spreads in excess of trading the market benchmark:

pSt � yb

t

pstþh

pbt

� �1=h

�yst

pbtþh

pst

!1=h24

35� ðyb

t � yst ÞðRM

tþhÞ1=h

h ið3Þ

where RMtþh is one plus the rate of return of the market index over an h-week

interval. As the second term, ðybt � ys

t ÞðRMtþhÞ

1=h, is the net trading gains wheninvestor trades the market index, pS measures the excess gains that arises wheninvestors trade portfolio of stocks that is different from the market portfolio.

9 Using the notation in this section, the contemporary spread between trade-weighted average

sell price and buy price in Table 1, Panel C is ðpst=p

bt � 1Þ � 100.

International Review of Finance

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007142

We compute pT to measure timing ability in relation to the market index. Aswe have standardized the value of trading to have equal medians, �yb

t ¼ �yst , we

have:

pTt � ðyb

t � yst ÞðRM

tþhÞ1=h � ð�yb

t � �yst ÞðRM

tþhÞ1=h ¼ ðyb

t � yst ÞðRM

tþhÞ1=h: ð4Þ

We can interpret pT as the net trading gains from actual trades in excess of thenet gains from a passive strategy that trades a constant amount, �yb

t and �yst , each

week. In actual trades, ysðbÞt and RM

tþh can be correlated because an investor canallocate, or time, the trades over a period.10 A larger pT implies better timingperformance because the investor buys (sells) before the market returnincreases (decreases). Our timing measure is similar to the portfolio perfor-mance measure developed by Grinblatt and Titman (1993). Because the originalGrinblatt–Titman measure uses the changes in portfolio weights in place oftrades, the interpretation of our measure is slightly different than theirs. In sum,we can express the overall trading profit as a summation of the abovecomponents:

Pt ¼ pSt þ pT

t : ð5Þ

Based on this performance measure, we are able to conduct a test against thenull hypothesis, H0:Pt 5 0. For net gains arising from price spreads, we havethe null hypothesis, H0 : pS

t ¼ 0, which implies that an investor trades themarket benchmark portfolio. For profits arising from market timing, we havethe null hypothesis, H0 : pT

t ¼ 0.We calculate these measures for h 5 1, 4, 8, 26, and 52 weeks over the total

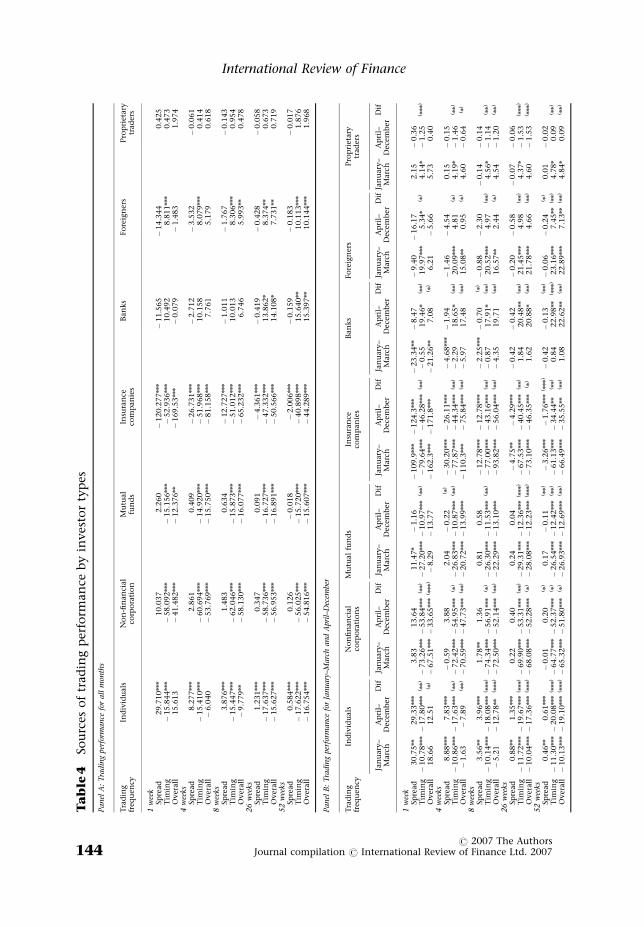

observation period. By comparing the net trading gains for different tradingintervals, we can determine the effect of turnover period on the net gains. Toenable comparisons between trading gains for different trading intervals, allnumbers are expressed in yen per month. In each cell in Table 4, we report themedian net trading gains for each investor type and test the null hypothesis ofzero median using the nonparametric signed-rank test. The sum of the net gainsdoes not equal the overall gains because each component represents the medianfor the sample.

We compute the p-values of the signed-rank test statistics using a blockbootstrap method. We cannot use the conventional standard errors for thesigned-rank tests as the standard signed-rank test assumes independent data. Aswe use overlapping observations, we introduce serial dependence in theperformance measures. Also, we expect seasonal patterns in the performancemeasures arising from seasonal patterns in buy and sell trades (see Section IV.B).Therefore, we use a block bootstrap method which resamples the data in blocksto maintain the serial dependence and periodicity (i.e., seasonality) in the

10 If we use the mean trades to standardize both buy and sell trades, the expectation of pT is the

covariance between trade today and the future market returns, covðybt � ys

t ;RMtþhÞ.

How do Investors Win and Lose in Equity Trades?

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007 143

Ta

ble

4So

urc

eso

ftr

ad

ing

per

form

an

ceb

yin

ves

tor

typ

es

Panel

A:

Tra

din

gper

form

ance

for

all

mon

ths

Tra

din

gfr

equ

ency

Ind

ivid

uals

No

n-fi

nan

cial

corp

ora

tio

nM

utu

al

fun

ds

Insu

ran

ceco

mp

an

ies

Ban

ks

Fo

reig

ner

sPro

pri

etary

trad

ers

1w

eek

Spre

ad

29.7

10nnn

10.0

37

2.2

60

�120.2

77nnn

�11.5

65

�14.3

44

0.4

25

Tim

ing

�15.8

44nnn

�58.0

92nnn

�15.1

56nnn

�52.9

36nnn

10.4

92

8.8

11nnn

0.4

73

Over

all

15.6

13

�41.4

82nnn

�12.3

76nn

�169.5

3nnn

�0.0

79

�1.4

83

1.9

74

4w

eeks

Spre

ad

8.2

77nnn

2.8

61

0.4

09

�26.7

31nnn

�2.7

12

�3.5

32

�0.0

61

Tim

ing

�15.4

10nnn

�60.6

94nnn

�14.9

20nnn

�51.9

68nnn

10.1

58

8.0

79nnn

0.4

14

Over

all

�6.0

40

�53.7

69nnn

�15.7

50nnn

�81.1

58nnn

7.7

61

5.1

79

0.6

18

8w

eeks

Spre

ad

3.8

76nnn

1.4

83

0.6

34

�12.7

27nnn

�1.0

11

�1.7

67

�0.1

43

Tim

ing

�15.4

47nnn

�62.0

46nnn

�15.8

73nnn

�51.0

12nnn

10.0

13

8.3

06nnn

0.9

54

Over

all

�9.7

79nn

�58.1

30nnn

�16.0

77nnn

�65.2

32nnn

6.7

46

5.9

93nn

0.4

78

26

wee

ksSp

read

1.2

31nnn

0.3

47

0.0

91

�4.3

61nnn

�0.4

19

�0.4

28

�0.0

58

Tim

ing

�17.6

37nnn

�58.7

36nnn

�16.7

27nnn

�47.3

32nnn

13.8

62n

8.3

74nn

0.6

73

Over

all

�15.6

27nnn

�56.9

53nnn

�16.8

91nnn

�50.5

66nnn

14.1

08n

7.7

31nn

0.7

19

52

wee

ksSp

read

0.5

84nnn

0.1

26

�0.0

18

�2.0

06nnn

�0.1

59

�0.1

83

�0.0

17

Tim

ing

�17.6

22nnn

�56.0

25nnn

�15.7

20nnn

�40.8

98nnn

15.6

40nn

10.1

13nnn

1.8

76

Over

all

�16.7

54nnn

�54.8

16nnn

�15.6

07nnn

�44.2

89nnn

15.3

97nn

10.1

44nnn

1.9

68

Panel

B:

Tra

din

gper

form

ance

for

January

–Marc

hand

Apri

l–D

ecem

ber

Tra

din

gfr

equ

ency

Ind

ivid

uals

No

nfi

nan

cial

corp

ora

tio

ns

Mu

tual

fun

ds

Insu

ran

ceco

mp

an

ies

Ban

ks

Fo

reig

ner

sPro

pri

etary

trad

ers

Jan

uary

–M

arc

hA

pri

l–D

ecem

ber

Dif

Jan

uary

–M

arc

hA

pri

l–D

ecem

ber

Dif

Jan

uary

–M

arc

hA

pri

l–D

ecem

ber

Dif

Jan

uary

–M

arc

hA

pri

l–D

ecem

ber

Dif

Jan

uary

–M

arc

hA

pri

l–D

ecem

ber

Dif

Jan

uary

–M

arc

hA

pri

l–D

ecem

ber

Dif

Jan

uary

–M

arc

hA

pri

l–D

ecem

ber

Dif

1w

eek

Spre

ad

30.7

5nn

29.3

3nnn

3.8

313.6

411.4

7n

�1.1

6�

109.9

nnn�

124.3

nnn

�23.3

4nn�

8.4

7�

9.4

0�

16.1

72.1

5�

0.3

6T

imin

g�

10.7

8nnn�

17.8

0nnn

( nn)�

73.2

6nnn�

53.8

4nnn

( nn)�

27.2

0nnn�

10.9

7nnn

( nn)�

79.6

4nnn�

46.2

8nnn

( nn)�

0.5

519.4

6n

( nn)

19.9

7nnn

5.3

4n

( n)

4.1

4n

�1.2

5( nnn)

Over

all

18.6

612.5

1( n

)�

67.5

1nnn�

33.6

5nnn

( nnn)�

8.2

9�

13.7

7�

162.3

nnn�

171.8

nnn

�21.2

6nn

7.0

8( n

)6.2

1�

5.6

65.7

30.4

04

wee

ksSp

read

8.8

8nnn

7.8

3nnn

�0.5

93.8

82.0

4�

0.2

2( n

)�

30.2

0nnn�

26.1

1nnn

�4.6

8nnn�

1.9

4�

1.4

6�

4.5

40.1

5�

0.1

5T

imin

g�

10.8

6nnn�

17.6

3nnn

( nn)�

72.4

2nnn�

54.9

5nnn

( n)�

26.8

3nnn�

10.8

7nnn

( nn)�

77.8

7nnn�

44.3

4nnn

( nn)�

2.2

918.6

5n

( nn)

20.0

9nnn

4.8

1( n

)4.1

9n

�1.4

6( nn)

Over

all

�1.6

3�

7.8

9( nn)�

70.5

9nnn�

47.7

3nnn

( nn)�

20.7

2nnn�

13.9

9nnn

�110.3

nnn

�75.8

4nnn

( nn)�

5.9

717.4

8( nn)

15.0

8nn

0.9

5( n

)4.6

0�

0.6

4( n

)

8w

eeks

Spre

ad

3.5

6nn

3.9

6nnn

1.7

8nn

1.3

60.8

10.5

8�

12.7

8nnn�

12.7

8nnn

�2.2

5nnn�

0.7

0( n

)�

0.8

8�

2.3

0�

0.1

4�

0.1

4T

imin

g�

10.1

4nnn�

18.0

8nnn

( nnn)�

74.3

4nnn�

56.9

1nnn

( n)�

26.3

0nnn�

11.5

3nnn

( nn)�

77.0

0nnn�

43.1

6nnn

( nn)�

0.8

717.9

1n

( nn)

20.5

2nnn

4.9

7( nn)

4.5

6n

�1.1

4( nn)

Over

all

�5.2

1�

12.7

8nn

( nnn)�

72.5

0nnn�

52.1

4nnn

( nn)�

22.2

9nnn�

13.1

0nnn

�93.8

2nnn�

56.0

4nnn

( nn)�

4.3

519.7

1( nn)

16.5

7nn

2.4

4( n

)4.5

4�

1.2

0( nn)

26

wee

ksSp

read

0.8

8nn

1.3

5nnn

0.2

20.4

00.2

40.0

4�

4.7

5nn

�4.2

9nnn

�0.4

2�

0.4

2�

0.2

0�

0.5

8�

0.0

7�

0.0

6T

imin

g�

11.7

2nnn�

19.6

7nnn

( nnn)�

69.9

0nnn�

53.3

1nnn

( nn)�

29.3

1nnn�

12.3

6nnn

( nnn)�

67.5

3nnn�

40.4

5nnn

( nn)

1.8

420.4

8nn

( nn)

21.4

5nnn

4.9

8( nn)

4.3

7n

�1.5

3( nnn)

Over

all�

10.0

4nnn�

17.3

6nnn

( nnn)�

68.0

8nnn�

52.2

8nnn

( n)�

28.0

8nnn�

12.2

3nnn

( nnn)�

73.1

0nnn�

46.3

5nnn

( n)

1.6

220.8

8n

( nn)

21.7

8nnn

4.6

6( nn)

4.6

0�

1.5

3( nnn)

52

wee

ksSp

read

0.4

6nn

0.6

1nnn

�0.0

10.2

0( n

)0.1

7�

0.1

1( nn)

�3.2

6nnn

�1.7

6nnn

( nnn)�

0.4

2�

0.1

3( nn)�

0.0

6�

0.2

4( n

)0.0

1�

0.0

2T

imin

g�

11.3

0nnn�

20.0

8nnn

( nnn)�

64.7

7nnn�

52.3

7nnn

( n)�

26.5

4nnn�

12.4

2nnn

( nn)�

61.1

3nnn�

34.4

4nn

( nn)

0.8

422.9

8nn

( nnn)

23.1

6nnn

7.4

5nn

( nn)

4.7

8n

0.0

9( nn)

Over

all�

10.1

3nnn�

19.1

0nnn

( nnn)�

65.3

2nnn�

51.8

0nnn

( n)�

26.9

3nnn�

12.6

9nnn

( nn)�

66.4

9nnn�

35.5

5nn

( nn)

1.0

822.6

2nn

( nn)

22.8

9nnn

7.1

3nn

( nn)

4.8

4n

0.0

9( nn)

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007144

International Review of Finance

We

defi

ne

the

over

all

net

trad

ing

gain

so

ver

h-w

eek

evalu

ati

on

inte

rval

fro

mw

eek

tas

foll

ow

s:

Pt�

yb t

ps tþ

h

pb t

�� 1=h�

ys t

pb tþ

h

ps t

! 1=

h2 4

3 5w

her

ey

b t¼

vb tp

b tðy

s t¼

vs tp

s tÞis

the

yen

am

ou

nt

of

bu

y(s

ell)

trad

esin

wee

kt,

ps t

an

dp

b tare

trad

e-w

eigh

ted

sell

an

db

uy

pri

ces,

an

dv

s tan

dv

b tare

sell

an

db

uy

vo

lum

es,

resp

ecti

vel

y.W

ed

efin

epS

as

the

trad

ing

gain

that

ari

ses

fro

mth

esp

read

bet

wee

nse

llan

db

uy

pri

ces

inex

cess

of

the

mar

ket

ben

chm

ark

.

pS t�

yb t

ps tþ

h

pb t

�� 1=h�

ys t

pb tþ

h

ps t

! 1=

h2 4

3 5 �ðy

b t�

ys tÞð

RM tþ

hÞ1=h

hi

wh

ere

RM tþ

his

on

ep

lus

the

h-w

eek

ho

ldin

gp

erio

dre

turn

of

the

mark

etin

dex

.T

he

seco

nd

term

ofpS

isth

etr

ad

ing

gain

wh

enin

ves

tor

trad

esth

em

arket

ind

ex.Fin

all

y,pT

mea

sure

sth

eti

min

gab

ilit

yin

rela

tio

nto

the

mark

etin

dex

.A

sw

eh

ave

stan

dar

diz

edth

evalu

eo

ftr

ad

ing

toh

ave

equ

al

med

ian

s,� y

b t¼

� ys t,

we

have:

pT t�ðy

b t�

ys tÞð

RM tþ

hÞ1=h�ð� y

b t�

� ys tÞð

RM tþ

hÞ1=h¼ðy

b t�

ys tÞð

RM tþ

hÞ1=h:

We

can

inte

rpre

to

ur

mea

sure

as

the

trad

ing

gain

fro

mact

ual

trad

esin

exce

sso

fth

etr

ad

ing

gain

fro

ma

pass

ive

ben

chm

ark

stra

tegy

that

inves

tsa

con

stan

tam

ou

nt,

� ys t

an

d� y

b t,

each

wee

k.

Inact

ual

trad

es,

ysð

bÞ

tan

dR

M tþh

can

be

corr

elat

edbec

au

sean

inves

tor

can

all

oca

te,

or

tim

e,th

eto

tal

am

ou

nt

of

� ysð

bÞ

t�

Tyen

over

the

tota

lo

bse

rvati

on

per

iod

of

Tw

eeks.

We

calc

ula

teea

chm

easu

refo

rh

51,

4,

8,

26,

an

d52

wee

ks.

We

als

oca

lcu

late

for

trad

eso

fall

mo

nth

s(P

an

elA

),Ja

nu

ary

thro

ugh

Marc

han

dA

pri

lth

rou

gh

Dec

emb

er(P

anel

B).

Du

rin

gJa

nu

ary

thro

ugh

Marc

h,

do

mes

tic

inst

itu

tio

ns

ten

dto

be

net

sell

ers,

refl

ecti

ng

the

ap

pro

ach

of

the

fisc

alyea

r-en

d.

Bo

thb

uy

an

dse

lltr

ad

esare

stan

dard

ized

toh

ave

am

edia

nvalu

eo

ff100.T

he

trad

ing

gain

sare

exp

ress

edin

yen

per

mo

nth

.In

each

cell

,w

ere

po

rtth

em

edia

nvalu

eo

fea

chp

erfo

rman

cem

easu

re.

To

test

the

nu

llh

yp

oth

esis

of

zero

med

ian

usi

ng

asi

gn

ed-r

ank

test

.In

Pan

elA

,w

eco

mp

ute

p-v

alu

esfr

om

2000

blo

ckb

oo

tstr

ap

rep

lica

tio

ns

that

take

into

acc

ou

nt

of

the

seaso

nal

patt

ern

san

dse

rial

dep

end

ence

inth

eo

rigin

ald

ata

.In

Pan

elB

,fr

om

the

sam

ebo

ots

trap

rep

lica

tio

ns

we

com

pu

tep-v

alu

esto

test

the

dif

fere

nce

inm

edia

ns

bet

wee

ntw

osu

bp

erio

ds,

Jan

uary

–Marc

han

dA

pri

l–D

ecem

ber

.T

he

sum

of

ind

ivid

ual

gain

sd

oes

no

teq

ual

the

over

all

gain

bec

au

seea

chco

mp

on

ent

rep

rese

nts

the

med

ian

for

the

sam

ple

.O

ur

data

cover

trad

eso

nth

eFir

stSe

ctio

no

fth

eTo

kyo

Sto

ckExch

an

ge

fro

mth

efi

rst

wee

ko

f1991

thro

ugh

the

last

wee

ko

fA

pri

l1999.

nSi

gn

ifica

nce

at

the0.10

level

.nnSignificance

atthe0.05

level

.nnnSignificance

atthe0.01

level

.A

ster

isks

inp

are

nth

eses

ind

icate

sign

ifica

nce

of

the

dif

fere

nce

inm

edia

ns.

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007 145

How do Investors Win and Lose in Equity Trades?

original sample, as resampling of the data using conventional bootstrap methodinevitably will destroy information included in the sequence of the originaldata.11 To determine the block size for bootstrapping, we first examine the serialdependence of performance measures by fitting an ARMA model after adjustingfor seasonality.12 We find that the maximum lag length among all performancemeasures is 5 weeks. To bootstrap time series data with seasonality, Politis(2003) proposed a method to resample the data in periodic blocks. Our naturalperiodic block length is 52 weeks because our data has monthly patterns. As the52 weeks block length subsumes the serial dependence of 5 weeks identified bythe ARMA model, we randomly resample the original data with replacement inblock length of 52 weeks. As we test the null hypothesis of zero median, wesubtract the median value from the original sample to generate the bootstrapdistribution under the null hypothesis. We conduct 2000 replications for eachcase.

B. Results

In Table 4, Panel A, our result shows that the overall net trading gain, P, for 1week trading interval is greatest for individual investors, which is due to thelarge trading gain arising from price spreads for short trading intervals. Forinitial buy and sell trades, both having median value of f100, average individualinvestors generate a median trading profit of f15.61 for turning over the samenumber of shares 1 week subsequent to the initial trade.13 On the other hand,our result shows that individual investors had a median trading loss of f16.75 ifthey turned over the same number of shares 52 weeks later. Although thepositive gains from the intertemporal price spreads for individual investorscould partly reflect higher risk premium of (possibly smaller) stocks preferred byindividual investors, they reflect the positive spread difference between thetrade-weighted sell and buy prices (see Table 1, Panel C). The positive pricespreads for individual investors might reflect the investors’ disposition to sellwinning investments and hold onto losing investments. Our result is alsoconsistent with the findings by Barber and Odean (2000) for US individualinvestors that show positive abnormal return for short-term round-trip trades.As trading intervals become longer, our result shows that the overall tradinggain of individual investors worsens. Because gains from price spreads becomesrelatively smaller for longer trading intervals, trading losses arising from poormarket timing dominates the overall performances for longer trading intervals.We also observe a similar pattern of trading performances for nonfinancial

11 For general discussion on block bootstrap methods, see Davison and Hinkley (1997).

12 We use the Minimum Information Criterion Method that estimates ARMA with various lag

lengths and tentatively identify the order of the process. See Box et al. (1994).

13 In effect, the median net initial trade is zero yen as we assume each investor type buys and sells

100 yen each. After 1 week, investor sells and buys the same numbers of shares as the initial

trade and generates a median trading gain of 15.61 yen.

International Review of Finance

r 2007 The AuthorsJournal compilation r International Review of Finance Ltd. 2007146

corporations, although their trading gains from price spreads are notstatistically significant.

In contrast, we find that foreign investors have negative trading perfor-mances (while not statistically significant) arising from intertemporal pricespreads. As foreign investors have significant negative price spreads (see Table 1,Panel C), a short-term turnover of their portfolios would not be a sustainabletrading strategy in the long run. In effect, we find that foreign investors havepositive performances arising from good market timing that largely offset thelosses arising from negative price spreads.

Although banks have relatively large positive contemporaneous spreadsbetween sell prices and buy prices (see Table 1, Panel C), we do not find anypositive performance arising from intertemporal price spreads, which must bedue to banks’ poor price spread performance relative to the market movements.However, our result shows that banks have positive market timing perfor-mances that generate significant and positive overall trading gains for longertrading intervals.