Embed Size (px)

Citation preview

HHOONNGG KKOONNGG・・TTAAIIWWAANN・・KKOORREEAA IINNDDUUSSTTRRYY MMOONNIITTOORR

(2013 First Half Issue) 1st April 2013

?

【Hong Kong】Industrial economy may recover at a moderate pace Hong Kong’s real GDP registered sharp slowdown at 1.4% YoY in 2012. Nevertheless, quarterly figures showed that the economy is improving modestly with GDP hitting the bottom in Q1.

In view of moderate economic re-acceleration in China, Hong Kong economy will likely grow at a gradual pace. Individual consumption related sectors may post stable growth. Market condition of service related sectors are also forecasted to remain healthy. However, constrained by government measures, further rise in property price is unlikely. Price is expected to stay firm at current level.

【Taiwan】Slow recovery in industrial economy is expected Taiwan’s real GDP grew just 1.3% YoY in 2013 because of weak export demand especially in European markets. Nevertheless, real GDP in Q4 bounced back to 3.4% YoY, thanks to recovered exports to Asian markets.

Industrial economy in Taiwan will likely recover moderately. Production of manufacturing industries, in particular electronics and its peripheral sectors, may increase in line with export demand recovery. Individual spending is also improving. However, while LCD production could remain unprofitable and risk of price fall in DRAM is high, recovery in some industries may not be sustainable.

【Korea】Modest recovery in H2 expected but close watch on exchange rates is needed Real GDP in Korea further slowed from 3.6% YoY in 2011 to 2.0% YoY in 2012. Performance was especially unfavorable in H2. Automobile production declined sharply partially due to strong Korean won. Shipbuilding also underwent strict market condition amid weak demand from shipping industry.

Industrial economy in Korea is expected to recover moderately in the second half, with individual consumption currently showing signs of improvement. However, considering that strong Korean won may hurt export competitiveness, hence the sustainability of recovery of Korean automobile and material industries, close monitor on any change in market condition is necessary.

1

Table of Contents

Industry Indicator Latest Data Page

Retail 1. Retail Sales Volumes Jan 2013

Restaurant 2. Restaurant Sales Volumes Dec 2012 2

Hotel 3. Hotel Occupancy / Room Rate Jan 2013

4. Residential Price / Rental Index Jan 2013 3

Real Estate 5. Office Price / Rental Index Jan 2013

Hong Kong

Export 6. Total Exports Jan 2013 4

Automobiles 7. Automobile Production Feb 2013

8. Semiconductor : IC Production Dec 2012 5

9. Semiconductor : Foundry Production Dec 2012 Electronics

10. LCD Production (10inch & Over) Dec 2012 6

Petrochemistry 11. Plastics Production Dec 2012

Taiwan

Retail 12. Retail Sales Volumes Jan 2013 7

Automobiles 13. Automobile Production Feb 2013

Shipbuilding 14. New Ship Completions Jan 2013 8

Steel 15. Crude Steel Production Jan 2013

Petrochemistry 16. Ethylene Production Jan 2013 9

Korea

Retail 17. Retail Sales Volumes Jan 2013 10

Appendix 1 Hong Kong・Taiwan・Korea Macroeconomic Indicators 11

Appendix 2 Monthly Sales Volume of Main Electronic Companies in Taiwan 13

Note: The “FORECAST” period added in this edition is a short-term outlook (about 6 months to 1 year).

This bulletin is issued semi-annually.

2

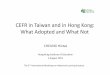

1. <Hong Kong> Retail Sales Volumes Forecast : Sustain mid single digit growth

-20%

-10%

0%

10%

20%

30%

2007 2008 2009 2010 2011 2012 2013 2014

Total Sales: 10.4 (Jan)Department Stores: 0.4 (Jan)Supermarkets: ▲5.3 (Jan)

Note: 1. “Real retail sales volumes” refer to the value adjusted for price changes from actual total sales volume.

2. To avoid the effect of change in sales volumes during the Chinese Lunar New Year, which lies at different period every year, growth rate in January and February of each year is calculated by the average of the two months.

Source: Census and Statistics Dept. HKSAR, Corporate Research Division of BTMU

Total retail sales in volume recorded single digit growth at 7.2% YoY in 2012, a sharp slowdown in comparison to 18.4% YoY in 2011. Retail sales in value were HKD445.4 billion. Some categories posted strong but decelerating growth, with “electrical goods and photographic equipment” and “proprietary medicines and supplies & cosmetics” increasing by 27.6% YoY and 13.3% YoY respectively. Sales growth of “jewellery, watches & clocks and valuable” remained positive but dropped significantly to 2.4% YoY as mainland visitors reined in luxury spending. Deceleration in sales of department stores also became apparent, with growth rate felling from 16.1% YoY in 2011 to 7.5% YoY in 2012.

Outlook: In view that the Chinese economy will re-accelerate at a moderate pace, retail sales volumes in 2013 will likely continue to post positive year-on-year growth. However, a slower growth in comparison to 2011 is expected. Luxury retailing sector will especially be impacted by the shift in spending of mainlanders from luxuries to mid-to-low priced goods. In consequence, retail sales volumes in Hong Kong is forecasted to sustain mid single digit growth in the future one year.

2. <Hong Kong> Restaurant Sales Volumes Forecast: Maintain marginal year-on-year growth

-15%

-10%

-5%

0%

5%

10%

15%

20%

2007 2008 2009 2010 2011 2012 2013 2014

All restaurants: 0.5 (12Q4)Chinese restaurants: ▲0.7 (12Q4)Fast food shops: 1.6 (12Q4)

Note: “Real total retail sales volumes” refer to the value adjusted for price changes from actual total sales volume. Source: Census and Statistics Dept. HKSAR, Corporate Research Division of BTMU

Total restaurant sales in volume slightly declined from the year ago level at ▲0.4% YoY in 2012. Restaurant sales in value were HKD93.7 billion. However, data in Q4 2012 revealed signs of recovery with restaurant sales recording positive growth for the first time in 12 months at 0.5% YoY. Impacted by the increase in number of consumers who tend to spend less for dinning outside, sectors performed differently in 2012. Fast food sector had a relatively favourable year, increasing by 1.2 percentage points to 3.4% YoY; whereas sales of Chinese and non-Chinese restaurants, which normally have high per capita spending, both declined by ▲1.5% YoY.

Outlook: Total restaurant sales in volume in Hong Kong are expected to maintain positive in view that the Hong Kong economy will accelerate moderately. However, such growth will likely be a marginal and slow one as individual spending is not expected to post significant growth. Restaurants and food shops with different per capita spending will continue to perform differently in the future one year.

3

3. <Hong Kong> Hotel Occupancy / Room Rate Forecast: Continue high occupancy

0

500

1,000

1,500

2,000

2007 2008 2009 2010 2011 2012 2013 201460

70

80

90

100

Average achieved hotel roomrate- all hotels: 1,448 (Jan)Occupancy rate: 87 (Jan)(HKD)

(%)

Source: Census and Statistics Dept. HKSAR, Corporate Research Division of BTMU

Occupancy of all hotels stayed at the highest historical level at 89% in 2012. Demand was strong as overnight visitors grew 6.5% YoY, largely from strong growth of mainland overnight visitors that grew 11.1% YoY. They are the largest visitor group accounting for 63.6% of total overnight visitors. Hong Kong, due to its close proximity, is attractive to mainland Chinese in terms of value and quality. Other long-haul and short-haul visitors have actually declined slightly under uncertain global economy. Room supply increased 8.5% in 2012. Despite higher pace of supply, continuous supply shortage situation and high demand led average achieved room rate to grow 9.8% YoY to HK$1,489 per night in 2012.

Outlook: In the future one year, HK will remain attractive to mainland visitors. Visits from other long-short-haul visitors may rise in view of better economic prospects in the global economy. As for supply, future room supply is estimated to grow at a low 5.2% YoY to 71,688 rooms. The tight room supply situation is expected to continue in 2013. Barring any change in government measures related to individual visits from mainland China, occupancy rate is expected to remain firm at a high level.

4. <Hong Kong> Residential Price / Rental Index Forecast: Price to stay at current high level

50

100

150

200

250

300

1997 1999 2001 2003 2005 2007 2009 2011 2013

Price Index (All Grades): 247.2 (Jan)Price Index (Popular Developments): 205.7 (Jan)Rental Index (All): 150.2 (Jan)

<1999=100>

Source: Rating & Valuation Dept. HKSAR, Corporate Research Division of BTMU

Price of large units rose 13.0% and popular developments rose 24.7% in Dec 2012 over Dec 2011; but overall number of transactions dropped ▲3.7% to 81,333 in 2012. Rental index climbed 11.2% YoY in Dec 2012. Introduction of additional taxes etc. by government in October markedly reduced demand from non-residents and led to decline in transaction volume. However, price continued to rise with supports of the low interest rate environment, the current low supply level and steady demand from the local residents.

Outlook: In the future one year, price is expected to be range bound at current level. For now, while there are prevailing positive fundamentals like low supply and low interest rate to support price; however, there are persistent government measures to curb the rising price. Surely, the government is determined to sell more land and will implement more new measures if price continues to rise. Hence further rapid price rise is unlikely. In addition, major banks raised mortgage rate by 0.25% in Mar 2013. While financial impact is minimal but demand sentiment is affected. Also, a major developer offered incentives to promote sales. Price is expected to remain firm at current high level. Rent will continue to rise as a result of increasing demand due to high residential price.

4

5. <Hong Kong>Office Price / Rental Index Forecast: Continue gradual growth in rental

rate

50

100

150

200

250

300

350

400

1997 1999 2001 2003 2005 2007 2009 2011 2013

Price Index (All Grades): 382.7 (Jan)Rental Index (All Grades): 192.4 (Jan)Rental Index (Grade A): 200.8 (Jan)

<1999=100>

Source: Rating and Valuation Dept. HKSAR, Corporate Research Division of BTMU

As a whole, rental of office (all grades) rose 7.1% in Dec 2012 over Dec 2011. The growth was largely supported by rising rental rate in areas outside core CBD Central especially in Island East and Kowloon East. Most are from relocations of cost-sensitive companies in the non-financial and small-medium sectors. Demand for Grade A office in Central CBD was still soft due to its high rental. Some companies remained conservative in expansion amid uncertain outlook. Nevertheless, overall vacancy improved slightly to 4.3% level as of end-2012 as supply was limited.

Outlook: In 2013, overall rental is expected to improve gradually. Demand for office space is likely to rise in line with the expected better economic outlook in HK. PMI is improving and hiring expectations are also rising. While future demand is also subjected to the influence of current uncertain global economy especially in Europe, there are positive factors. Current vacancy rate is low and future supply is limited. Hence, rental is likely to improve at a moderate pace. Impacted by new government measures announced in Feb 2013, by which stamp duty rates on property transactions are raised and charging of stamp duty are advanced, office price is expected to trend downward at a gradual pace.

6. <Hong Kong>Total Exports Forecast: Faster growth in 2013

0

50

100

150

200

250

300

350

2007 2008 2009 2010 2011 2012 2013 2014-30%

-20%

-10%

0%

10%

20%

30%

40%

Total Exports: 305 (Jan)YoY Growth Rate: 17.6 (Jan)(HKD billion)

Note: To avoid the effect of change in sales volumes during the Chinese Lunar New Year, which lies at different period every year, growth rate in January and February of each year is calculated by the average value of the two months. Source: Census and Statistics Dept. HKSAR, Corporate Research Division of BTMU

Total exports grew 2.9% YoY to HKD3,434.3 billion in 2012, a sharp slowdown from 10.1% YoY in 2011. Exports to major destination mainland China grew just 6.3% YoY (vs 9.3% YoY in 2011). Exports to large demand markets, the US and Japan, grew 2.3% YoY and 6.5% YoY respectively but exports to EU areas dropped significantly at ▲7.0% YoY. Demand conditions in the US improved but remained soft. Growth in Japan was due to after-quake effect. Situations in the EU were weak as debt issues continued to be uncertain. By sector, while telecommunication equipment and office machine grew strongly, the largest electrical/electronic sector decelerated and apparel sector declined.

Outlook: Total exports are expected to post faster growth in 2013 compared with that in 2012. Exports of major trade partner China is widely projected to improve, growing at around 8% YoY, with expectation of moderate re-acceleration of the Chinese economy. Exports to the US may slowly improve in view of better economic outlook. Product wise, exports of IT goods, especially telecommunication equipments, are expected to grow with introduction of new smart phone models by major brands.

5

7. <Taiwan>Automobile Production Forecast: Improve and ensure positive

growth

0

5

10

15

20

25

30

35

40

2007 2008 2009 2010 2011 2012 2013 2014-100%

-50%

0%

50%

100%

150%

200%

250%

300%

Commercial Vehicle (CV) Production: 2.2 (Feb)Passenger Vehicle (PV) Production: 15.8 (Feb)YoY Grow th (CV Production): ▲52.3 (Feb)YoY Grow th (PV Production): ▲30.3 (Feb)(th units)

Source: CEIC Data Co., Ltd. , Corporate Research Division of BTMU

Automobile production declined by ▲1.2% YoY to 339,000 units in 2012. Due to the export-oriented nature of its economy, individual spending in Taiwan has been volatile to fluctuation in global economy. In 2012, consumer sentiment was constrained by the uncertain economic condition in Europe and slower growth of the Chinese economy. Coupled with gasoline price rise, domestic demand fell sharply by ▲5.4 % YoY. On the other hand, exports recorded rapid growth at 29.4% YoY, thanks to large demand from Near and Middle East markets.

Outlook: Automobile production in Taiwan is expected to improve in 2013. The export-oriented economy of Taiwan may gradually recover in line with the anticipated re-acceleration of Chinese economy. Currently, around 3.2 million automobiles in Taiwan are at the end of their product lif cycle. This may help improve domestic demand to a more stable trend. Exports may also grow steadily with Japanese automakers scheduling production increase in Taiwan to cope with increasing demand from Near and Middle East markets. Given the above positive factors, automobile production in Taiwan is likely to ensure single digit growth against year ago level.

8. <Taiwan> Semiconductor : IC Production Forecast: Flat previous year’s level at best

0

50

100

150

200

250

300

2007 2008 2009 2010 2011 2012 2013 2014-100%

-50%

0%

50%

100%

150%

200%

IC Production Value: 96.7 (Dec)YoY Ave. Unit Price Grow th: ▲4.6 (Dec)YoY Production Grow th: 16.7 (Jan)(NTD 100mn)

Source: CEIC Data Co., Ltd. , Corporate Research Division of BTMU

IC production, constrained by the persistently low demand of major product DRAM, declined by 18.8% YoY to NTD134.9 billion in 2012. DRAM price picked up and significantly improved most recently with production cuts by manufacturers. Nevertheless, demand for DRAM remained soft and showed no sign of recovery as demand of the major customer PC sector declined against previous year’s level. DRAM manufacturers continued to record loss as a result.

Outlook: Demand for DRAM is expected to be weak in 2013 as production of the major customer PC sector will only see marginal growth. Despite expectations of sluggish demand in the first half of the year, which is partially due to low-season effect, some manufacturers have started to increase production given the current improvement in price. DRAM price may deteriorate again as a result. In the second half, DRAM demand should pick up on the back of seasonal demand and production of PC installed with new CPU (Haswell); but such growth in demand is unlikely to be sustainable in the mid-long term. Besides, risk of oversupply continues to be high as investment on device density enhancement is inevitable to improve competitiveness. Given the sluggish market situation in major DRAM sector, IC production value in Taiwan is expected to maintain previous year’s level at best.

6

9. <Taiwan> Semiconductor : Foundry Production Forecast: Stable trend expected

0

100

200

300

400

500

600

2007 2008 2009 2010 2011 2012 2013 2014-80%

0%

80%

160%

240%

320%

400%

Foundry Wafer Production Value (8 Inch & Below): 155 (Dec)Foundry Wafer Production Value (12 Inch & Above): 355 (Dec)YoY Growth in Production Units (8 Inch & Below): 17.5 (Dec)YoY Growth in Production Units (12 Inch & above): 16.6 (Dec)YoY Growth in Production Value (8 Inch & Below): 19.2 (Dec)YoY Growth in Production Value (12 Inch & above): 20.4 (Dec)

(NTD 100mn)

Source: CEIC Data Co., Ltd, Corporate Research Division of BTMU

Foundry production in value increased 15.7% YoY to NTD630.4 billion in 2012. Production in Q1 declined from the year ago level due to gloomy global economy and low yield rates of high-tech products; however, it picked up and continued double digit growth after Q2 with large demand for communication chips for smart phones and tablets. Impact from production adjustment by major smart phone manufacturer to the industry is small as a whole. Production of foundry manufacturers is on a firm trend with the strong demand for high-tech products (28nm process).

Outlook: Foundry demand is expected to grow in 2013, with major smart phone manufacturers launching new models in the first half. Semi-conductor manufacturers have also become more reliant on foundry products given the larger investments on advanced technologies (device density enhancement). On the other hand, supply may remain tight as some major foundry manufacturers still face difficulties in improving yield rate of high-tech products. As a result, foundry price and production value is forecasted to remain stable in 2013.

10. <Taiwan> LCD Production (10 Inch & Over) Forecast: Maintain positive but slow growth

0

250

500

750

1,000

2007 2008 2009 20102011 2012 2013 2014-100%

-50%

0%

50%

100%

150%

200%

250%

300%

LCD Production Value (10 Inch & Over): 518 (Dec)YoY Ave. Unit Price Growth: 11.7 (Dec)YoY Growth (Production Units): 10.3 (Dec)

(NTD 100mn)

Source: CEIC Data Co. ,Ltd. , Corporate Research Division of BTMU

LCD production in value increased by 16.1% YoY to NTD670.4 billion in 2012. Despite weak demand for the major product LCD TV and traditional PCs in the global market, overall production was driven by strong LCD TV demand in China and recorded over 30%’s year on year growth for 2 consecutive quarters. Nevertheless, major manufacturers continued to report loss in Oct-Dec 2012, showing no sign of recovery in profitability.

Outlook: TV manufacturer in China has started to reduce LCD procurement due to high inventory level resulted by over procurement in 2012. Coupled with the low seasonal demand, current (Q1 2013) market condition is sluggish. Nevertheless, overall LCD production value in 2013 is expected to increase in line with strong LCD TV demand in China and improving LCD TV demand in global market. However, as demand for LCD TV in China will eventually peak out and Chinese LCD manufacturers is determined to raise their production capacity to a considerably high level, LCD industry is in high risk of oversupply and re-deterioration in price. As a result, LCD production value in Taiwan is expected to maintain positive but slow growth in 2013.

7

11. <Taiwan> Plastics Production Forecast: Maintain moderate improvement

0

100

200

300

400

500

2007 2008 2009 2010 2011 2012 2013 2014-60%

-30%

0%

30%

60%

90%

PVC Production: 60 (Dec)ABS Production: 98 (Dec)PS Production: 71 (Dec)PP Production: 96 (Dec)LDPE Production: 40 (Dec)YoY Plastics Production Grow th: ▲0.9 (Dec)(th tons)

Source: CEIC Data Co., Ltd. , Corporate Research Division of BTMU

Plastics production in Taiwan fell by 1.8% YoY to 4,386 thousand tons in 2012. This was mainly due to decline in export markets, resulting from fragile economic performance in US and EU, and slower growth in Asian economies. On the supply side, repeated fire accidents which led to production cuts of major petrochemical producers in Taiwan also caused lower plastics output last year. Nevertheless, supported by demand recovery mainly in Asian markets, most plastics product prices have bottomed out in Q4 2012. This could help improve plastics production.

Outlook: Demand for plastics products are expected to increase moderately on the back of improving domestic demand due to better economic prospect in Taiwan economy. Exports to major market China will also recover with anticipated robust market condition in manufacturing, infrastructure and construction sectors. Risk of accidents is also reduced given the stricter safety requirements. Benefiting from the above factors, production of plastics products, in particular PVC used by infrastructure and construction sectors, is expected to recover at a moderate pace. Consequently, profitability of Taiwanese petrochemical producers is likely to improve in 2013, but close monitor on price is needed as price may fall due to eased supply-demand situation.

12. <Taiwan> Retail Sales Volumes Forecast: Re-accelerate at a gradual pace

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2007 2008 2009 2010 2011 2012 2013 2014-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Retail Sales: 3,319 (Jan)YoY Growth: ▲1.8 (Jan)(NTD 100mn)

Source: CEIC Data Co., Ltd. , Corporate Research Division of BTMU

Retail sales volumes grew 2.4% YoY to NTD3813.1 billion, a slower growth in comparison to 6.3% YoY in 2011. Unemployment rate remained stable at low level. However, consumer sentiment was affected by uncertain employment environment due to increasing no-pay leaves; and continuous decrease in real GDP growth since first half of 2012. Growth in retail sales volumes slowed down as a result. Consumer sentiment index has also continued to fall after reaching its peak in Mar 2012. Sectors saw different growth pace in 2012, with convenience stores rose 2.1 percentage points to 8.8% YoY while department stores drop 4.0 percentage points to 3.6% YoY and super markets drop 1.4 percentage points to 5.9% YoY.

Outlook: Consumer sentiment index in Taiwan has been improving gradually since the beginning of 2013, revealing signs of recovery in consumer sentiment due to better economy. Given that unemployment rate remains stable at a low level, retail sales volume in Taiwan is expected to remain healthy and re-accelerate at a modest pace.

8

13. <Korea>Automobile Production Forecast: Marginal positive growth

0

5

10

15

20

25

30

35

40

45

50

2007 2008 2009 2010 2011 2012 2013 2014-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

Commercial Vehicle (CV) Production: 3.1 (Feb)Passenger Vehicle (PV) Production: 30.7 (Feb)YoY Grow th (CV Production): ▲13.2 (Feb)YoYGrow th (PV Production): ▲20.4 (Feb)(10th units)

Source: CEIC Data Co., Ltd. , Corporate Research Division of BTMU

Automobile production in Korea declined by ▲2.1% YoY to 4.56 million units in 2012. Domestic demand declined by ▲4.3% YoY as affected by dropping consumer sentiment, increasing household debt and economic slowdown. Exports also decelerated rapidly in the second half with stronger Korean won. While exports to the largest US market increased by 18.0% YoY as supported by the recovery in US market and FTA, exports to other major markets such as South America, EU and Asia experienced substantial decline. The fall in South America was partially attributed by tax rise for imported cars in Brazil.

Outlook: Automobile production in Korea is likely to register marginal positive growth in 2013, supported mainly by exports while domestic demand is expected to remain subdued due to still soft consumer sentiment on durable goods. Despite weak demand from EU, export is expected to be driven by demand from US and emerging markets. Recently, major Korean automakers have increased production capacity in overseas such as Asia and other Europe countries. Therefore, export growth directly from Korea is expected to be moderate in the mid-long term.

14. <Korea> New Ship Completions Forecast: Unfavorable market condition amid persistent decline in new ship

0

20

40

60

80

100

120

140

160

180

2007 2008 2009 2010 2011 2012 2013 2014-80%

-40%

0%

40%

80%

120%

160%

200%

240%

280%

Container Ship Completion: 49.4 (Jan)Bulk Carrier Completion: 10.3 (Jan)LPG/PNG & General Cargo Carrier Completion: 45.3 (Jan)Oil Tanker Completion: 12.8 (Jan)YoY Growth (Container Ship): 37.4 (Jan)YoY Growth (Bulk Carrier): ▲65.7 (Jan)YoY Growth (LPG/PNG & General Cargo Carrier): 256.3 (Jan)YoY Growth (Oil tanker): ▲29.9 (Jan)

(10th tons)

Source: CEIC Data Co., Ltd. , Corporate Research Division of BTMU

New ship completion dramatically dropped by 26.2 percentage points to ▲12.9% YoY (12.4 million tons) in 2012. Bulker and oil tanker completions fell deeply by ▲52.8% YoY and ▲21.8% YoY respectively. Container ship completion sustained positive growth but growth pace dropped sharply by 20.2 percentage points to 6.7% YoY. LPG/LNG carrier is the only sector increased sharply by 40.6% YoY, backed by strong demand for alternative energy. Under an overall sluggish market environment, volume of new contracts and orderbook of Korean players were downed by ▲45.3% YoY and ▲21.9% YoY. Overall new building price index also fell ▲9.2% YoY to the lowest record level since 2004.

Outlook: New ship completion is likely to continue to drop in 2013 given the decline in new contracts and orderbook. Demand for bulker and oil tanker is likely to be low due to lingering oversupply. To a certain extent, it is similar for container ship. On the other hand, LPG/LNG carrier is expected to attract steady demand. As a whole, Korean shipbuilders will face unfavourable market condition amid current low price level, small number of new contracts and impact of strong Korean Won.

9

15. <Korea> Crude Steel Production Forecast: Moderate improvement

0

100

200

300

400

500

600

700

2007 2008 2009 2010 2011 2012 2013 2014-30%

-20%

-10%

0%

10%

20%

30%

40%

Crude Steel Production: 575 (Jan)

YoY Growth: ▲0.4 (Jan)(10th tons)

Source: CEIC Data Co., Ltd. , Corporate Research Division of BTMU

Crude steel production in Korea increased by just 1.2% YoY in 2012 to 69.32 million tons. It was partially due to slowdown in steel demand from domestic shipbuilding and automobile sectors amid weakening demand. Besides, steel exports were affected by slower economic growth in China and gloomy economy in Europe. On the supply side, although some steel makers have restructured their factories by shutting down hot-rolling mills and small blast furnaces, the industry continued to undergo oversupply condition. Coupled with weakness in steel product prices, profitability of Korean crude steel makers were affected in 2012.

Outlook: Domestic demand in 2013 is expected to sustain positive growth driven by anticipated moderate rise in automobile production. Besides, there could be a mild increase in steel exports in relation to improving infrastructure investments in China. Hence, crude steel production in Korea is expected to improve modestly. On the supply side, while some steel makers plan to reduce production, there will be only one new blast furnace coming on stream. As a result, overall capacity growth is likely to be minimal and supply-demand balance could stabilize this year. Also, steel price may bottom out in H1. In view of better industrial environment, profitability of steel makers in Korea may see marginal recovery.

16. <Korea> Ethylene Production Forecast: Continue positive growth

0

10

20

30

40

50

60

70

80

2007 2008 2009 2010 2011 2012 2013 2014-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Ethylene Production: 72.4 (Jan)YoY Growth: 5.4 (Jan)(10th tons)

Source: CEIC Data Co., Ltd. , Corporate Research Division of BTMU

Ethylene production in Korea grew by 8.8% YoY to 8.08 million tons in 2012. It was mainly because major petrochemical producers ramped up their ethylene capacities last year; and demand for ethylene was pushed up by inventory stocking amid upsurge in crude oil price. Besides, moderate re-acceleration of the Chinese economy also helped boost export demand for ethylene to a certain extent. As a result, ethylene price in Korea bounced back since middle of the year to reach USD1,195/ton in December 2012.

Outlook: The outlook of Korean petrochemical market is optimistic in 2013. On the demand side, there are signs of recovery in downstream polyethylene markets, backed by the improvement in construction, property and packaging sectors especially in China and the US. In addition, ethylene production in Korea is expected to be driven by exports and register high single digit growth, given its high product quality and high cost competitiveness supported by large operating scale. On the supply side, ethylene capacity additions in the world could be lower than expected as some expansion projects have been proponed to 2014. Profitability of Korean ethylene providers could pick up in 2013 as the stable supply-demand balance and price trend should be sustainable.

10

17. <Korea> Retail Sales Volume Forecast: Accelerate at a moderate pace

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2007 2008 2009 2010 2011 2012 2013 2014-5%

0%

5%

10%

15%

20%

25%

30%

Retail Sales: 28,554 (Jan)YoY Growth: ▲2.1 (Jan)(KRW bn)

Source: CEIC Data Co., Ltd. , Corporate Research Division of BTMU

Retail sales value grew 4.1% YoY to KRW349 trillion in 2012. It was a slowdown from 9.4% YoY in 2011 due to soft consumer sentiment as economy was slow. Large discount stores registered sharp slowdown as affected by regulatory measures on new shops opening, business days, operating hours and etc. Sales growth of department stores was constrained partially by contracted private spending on luxuries. However, convenience stores recorded strong sales growth at 18.3% YoY supported by the rise of one-person household and ease of access. Not-in-store (internet and home-shopping) sales increased by 11.0% YoY due to attractive pricing.

Outlook: Given that recent consumer sentiment index in Korea has continued to edge up to the level higher than the standard value, retail sales value as a whole may gradually improve in line with recovering economy to post positive growth. However, sectors are expected to register different growth pace. While large discount stores may possibly face further slowdown due to tighter regulatory measures, internet and home shopping sales are likely to continue high growth pace.

11

Appendix 1 Hong Kong Macroeconomic Indicators

09 10 11 12 12/1Q 12/2Q 12/3Q 12/4QReal GDP (%) ▲2.5 6.8 4.9 1.4 0.8 1.0 1.4 2.5Industrial Production (%) ▲8.3 3.5 0.7 n.a. ▲1.6 ▲2.9 ▲0.1 n.a.Retail Sales (%) 0.6 18.3 24.9 9.8 15.8 10.3 5.8 7.5Consumer Price Index (%) 0.5 2.4 5.3 4.1 5.2 4.2 3.1 3.8Visitor arrival (%) 0.3 21.8 16.4 16 15.6 15.3 17.7 15.1

China (%) 6.5 26.3 23.9 24.2 21.1 24.5 26.8 24.2US & Europe (%) ▲6.2 9.3 2.9 1.3 6.4 3.0 ▲2.2 ▲1.6Others (%) ▲8.5 16.3 3.8 ▲1.4 3.8 ▲2.0 ▲3.0 ▲3.9

Trade Balance(HKDbillion) ▲223.3 ▲333.8 ▲427.3 ▲477.8 ▲98.5 ▲123.1 ▲121.3 ▲134.7Export Growth (%) ▲12.6 22.8 10.1 2.9 ▲1.5 1.8 3.8 7.0Import Growth (%) ▲11.0 25.0 11.9 3.9 0.7 2.1 4.5 8.1

25.9 75.1 73.7 n.a. 73.7 ▲9.7 ▲58.0 40.0

2,558 2,687 2,854 3,173 2,946 2,950 3,012 3,17321,873 23,035 18,434 22,657 20,556 19,442 20,840 22,657

Unemployment Rate (%) 5.3 4.3 3.4 n.a. 3.4 3.2 3.3 3.3Exchange Rate (HKD/USD) 7.752 7.769 7.784 7.757 7.760 7.762 7.756 7.751Exchange Rate (JPY/HKD) 12.07 11.29 10.24 10.29 10.23 10.32 10.14 10.48

Govt. Consolidated A/C (HKDbillion)Foreign Reserve (USD'00 mil)Stock Market (HSI 1964=100)

Note: % means a year-on-year growth rate. The quarterly figures of tined area are cumulative total of the year while the others are figures of the quarter. Foreign exchange reserves and stock value are figures at term-end. Exchange rate is the average rate of the given period. Source: CEIC Data Co., Ltd., Corporate Research Division of BTMU

Taiwan Macroeconomic Indicators

09 10 11 12 12/1Q 12/2Q 12/3Q 12/4QReal GDP (%) ▲1.8 10.8 4.1 1.3 0.6 ▲0.1 0.7 3.7Industrial Production (%) ▲8.1 26.9 5.0 ▲0.1 ▲4.5 ▲1.3 1.5 4.2Retail Sales (%) 1.6 6.6 6.5 2.4 1.6 3.7 2.6 1.8Consumer Price Index (%) ▲0.9 1.0 1.4 1.9 1.3 1.7 3.0 1.8Trade Balance (NTD'00 mil) 9,517 7,133 7,612 8,688 1,610 1,571 2,435 3,073 Export Growth (%) ▲16.2 29.0 4.4 ▲1.6 ▲2.7 ▲3.3 0.9 ▲1.3

Electronic Products (%) ▲9.3 30.5 2.5 ▲3.5 ▲6.1 ▲4.5 ▲0.2 ▲3.5 Import Growth (%) ▲23.8 38.0 4.2 ▲3.0 ▲4.5 ▲3.7 ▲0.1 ▲3.7

2,555 3,072 2,639 2,229 510 1,093 1,587 2,229

Growth (%) 8.3 20.2 ▲14.1 ▲15.5 ▲11.9 ▲16.6 ▲17.8 ▲15.5

18.8 24.8 21.8 28.5 7.5 16.2 21.6 28.5

Growth (%) ▲1.0 31.7 ▲11.8 30.4 39.8 35.2 31.8 30.43,482 3,820 3,855 4,032 3,939 3,912 3,980 4,0328,188 8,973 7,072 7,700 7,933 7,296 7,715 7,700

Unemployment Rate (%) 5.9 5.2 4.4 4.2 4.2 4.2 4.3 4.2Exchange Rate (NTD/USD) 33.03 31.49 29.40 29.58 29.70 29.62 29.84 29.15Excjamge Rate (JPY/NTD) 2.83 2.79 2.71 2.70 2.67 2.70 2.64 2.79

Foreign Reserve (USD'00 mil)Stock Market (TSEW 1966=100)

Outward Direct Inv. in China (No. of Projects)

Outward Direct Inv. in China (USD'00 mil)

Note: % means a year-on-year growth rate. The number of direct investments is counted on contract base while direct investments are counted by utilized amount. The quarterly figures of tined area are cumulative total of the year while the others are figures of the quarter. Foreign exchange reserves and stock value are figures at term-end. Exchange rate is the average rate of the given period. Source: CEIC Data Co., Ltd. , Corporate Research Division of BTMU

12

Korea Macroeconomic Indicators

09 10 11 12 12/1Q 12/2Q 12/3Q 12/4QReal GDP (%) 0.3 6.3 3.6 2.0 2.9 2.3 1.5 1.6Industrial Production (%) ▲0.7 16.6 6.9 2.0 2.9 2.4 ▲0.1 3.0Retail Sales (%) 4.0 9.6 8.4 3.3 4.4 3.8 1.7 3.5Consumer Price Index (%) 2.8 2.9 4.0 2.2 3.0 2.4 1.6 1.7Trade Balance (USD'00 mil) 404 412 308 283 12 97 75 99 Export Growth (%) ▲13.9 28.3 19.0 ▲1.3 2.9 ▲1.7 ▲5.8 ▲0.4

Machinery (%) ▲15.7 29.5 21.7 ▲6.7 0.7 ▲0.6 ▲15.7 ▲12.0Electrical & Electronic Products (%) ▲4.5 26.9 2.7 0.2 ▲4.0 ▲4.2 1.0 7.8

Import Growth (%) ▲25.8 31.6 23.3 ▲0.9 7.8 ▲2.9 ▲6.9 ▲1.1

3,131 3,108 2,707 2,863 714 743 645 761

Growth (%) ▲16.4 ▲0.7 ▲12.9 5.8 23.7 12.2 ▲5.6 ▲3.1

114.8 130.7 136.7 162.6 23.5 47.6 40.9 50.6

Growth (%) ▲2.0 13.8 4.6 18.9 17.0 41.7 84.4 ▲16.92,700 2,916 3,064 3,270 3,160 3,124 3,220 3,2701,683 2,051 1,826 1,997 2,014 1,854 1,996 1,997

Unemployment Rate (%) 3.7 3.7 3.4 3.2 3.8 3.3 3.0 2.8Exchange Rate (KRW/USD) 1276.2 1,156.8 1,107.8 1,126.5 1,130.8 1,152.7 1,133.0 1,090.1Exchange Rate (JPY/KRW) 13.64 13.21 13.92 14.13 14.27 14.40 14.41 13.44

Inward Direct Investment(No. of Permitted Projects)

Inward Direct Investment(USD'00 mil)

Stock Market (KOSPI,1980=100)Foreign Reserve (USD'00 mil)

Note: % means a year-on-year growth rate. The quarterly figures are the figure of that period. Foreign exchange reserves and stock value are figures at term-end. Exchange rate is the average rate of the given period. Source: CEIC Data Co., Ltd. , Corporate Research Division of BTMU

13

Appendix 2

Two foundry manufacturers (pre-process manufacturing) Three DRAM manufacturers

0

100

200

300

400

500

600

700

2007 2008 2009 2010 2011 2012 2013-100%

-50%

0%

50%

100%

150%

200%

Sales (Jan): 569YoY Growth (Jan): 33(NTD 100mn)

0

50

100

150

200

250

300

350

400

2007 2008 2009 2010 2011 2012 2013-100%

-50%

0%

50%

100%

150%

200%

250%

300%

Sales (Jan): 57YoY Growth (Jan): 24(NTD '00mil)

Four LCD manufacturers Four laptop PC manufacturers

0

500

1,000

1,500

2007 2008 2009 2010 2011 2012 2013-100%

-50%

0%

50%

100%

150%

200%

Sales (Jan): 753YoY Growth (Jan): 28(NTD '00mil)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2007 2008 2009 2010 2011 2012 2013-40%

-20%

0%

20%

40%

60%

80%

100%

Sales (Jan): 2,150YoY Growth (Jan): 14(NTD '00mil)

Four motherboard manufacturers Four EMS manufacturers

0

150

300

450

600

750

900

1,050

1,200

2007 2008 2009 2010 2011 2012 2013-90%

-60%

-30%

0%

30%

60%

90%

120%

150%

Sales (Jan): 560YoY Growth (Jan): 77(NTD '00mil)

0500

1,0001,5002,0002,5003,0003,5004,0004,5005,000

2007 2008 2009 2010 2011 2012 2013-30%

0%

30%

60%

90%

120%

150%

180%

Sales (Jan): 3,434YoY Growth (Jan): 19(NTD '00mil)

Note: Foundry: TSMC, UMC, DRAM: Nanya, Powerchip, ProMOS, LCD: AU Optronics, Chi Mei Innolux, CPT, Hannstar, Laptop PC: Quanta, Compal, Inventec, Wistron, Motherboard: Elite, Asustek, Giga Byte, Micro-Star, EMS: Hon Hai Precision, Lite-On, BenQ, Mitac Source: Statement of accounts of the above companies, Corporate Research Division of BTMU

14

【BTMU Network in Hong Kong・Taiwan・Korea】 《 Hong Kong 》 《 Taiwan 》

《 Korea 》

Seoul

Taipei

Hong Kong

Kowloon

East Tsim Sha Tsui

This report is intended only for information purposes and is not intended to constitute an offer or solicitation to buy or sell securities or any other products. Contents of the report are information as at 1st Apr 2013 and are subject to change without notice. This report has not been prepared to provide legal, taxational, financial, market-judgmental, or any other advises on propriety of any transactions. In taking any action, each reader is requested to act on the basis of his or her own judgment upon consulting certified lawyers, accountants or other professionals regarding the accuracy, validity and reliability of information appeared in this report. Bank of Tokyo-Mitsubishi UFJ is regulated by the Financial Services Authority. Copyright © The Bank of Tokyo-Mitsubishi UFJ, Limited 2013 No part of this publication may be reproduced, stored in a retrieval system or transmitted without the prior written permission of The Bank of Tokyo-Mitsubishi UFJ Limited. Publisher: The Bank of Tokyo – Mitsubishi UFJ, Ltd. Corporate Research Division (Hong Kong)

6/F., AIA Central, 1 Connaught Road Central, Hong Kong

Tomoo Nishina(仁科 知夫) (852)2249 -3030 [email protected] Bee Yen Ooi(黄 美艶) 2249 3028 [email protected] Daisuke Ikeda(池田 大輔) 2249 3033 [email protected] Eric So(蘇 慶平) 2821 3413 [email protected] William Cheung(張 偉明 ) 2821 3422 [email protected] Takehiro Takehara(竹原 毅洋) 2249 3078 [email protected] Tomoko Matsuura(松浦 知子) 2249 3031 [email protected] Jessica H.K. Kim(金 恵敬) 2821 3406 [email protected] Shota Matsuzawa(松澤 翔太) 2821 3402 [email protected]

Branch

Sub-Branch

Representative Office