Embed Size (px)

Citation preview

Delaware State Housing Authority

Homeownership Loan ProgramsLender Training

DSHA is committed to follow all aspects of the Fair Housing Act in our efforts to promote responsible homeownership and obtaining competitive and safe financing for same.

Agenda• Overview of Mortgage Products• DSHA Product Structure • Homeownership Product Definitions• Downpayment & Closing Cost Assistance Products• Compliance Review and Guidelines• Compliance File Delivery• Eligible Loan Products• Allowable Fees• Loan Flow• Registration/Loan Reservation Process• Pipeline Tracking• Program Documents• SMAL and Advantage 4 Closing Process• Closed Loan Delivery• Housekeeping Items

3

Overview of DSHA Mortgage Programs

DSHA Mortgage loan products are designed to enable income‐qualified families to achieve the dream of homeownership.

Advantages for DSHA borrowers include:– At or below‐market interest rates– Downpayment Assistance Options– First mortgage programs are 30 year fixed rate

When DSHA funds are used to finance mortgage loans, certain criteria are required including:– Loan Size or Purchase Price limits– Income limits– Owner‐occupancy requirements– Restricted to properties located in Delaware

4

Current Products Offered

Welcome Home Loans Mortgages For First‐Time Homebuyers

Home Again LoansMortgages for Repeat Homebuyers

5

DSHA DefinitionsWelcome Home Product‐ First‐Time Homebuyer Definition:

– A person who has not had an ownership interest in his/her principalresidence at any time during the last three years prior to the closingdate.• Mobile homes not permanently affixed to the ground are notconsidered real estate; the owner would be eligible for first‐timehomebuyer rates.

Qualified Veterans as defined in 38 USC Section 101, are exempt from the First‐Time Home Buyer requirement.– Must provide a copy of their DD 214 Form demonstrating military discharge or release under conditions other than dishonorable.

Home Again Product – For Homebuyers who do not meet the First‐Time Homebuyer definition.

6

Eligible Loan Products

• FHA– 203(b); 203(b)(2); 234(c); 223(e); 203(ks) and other acceptable FHA products.

• VA– Originated and guaranteed in accordance with VA guidelines under 1810 and 181A.

• USDA Rural Housing Service Loans– Originated and guaranteed in accordance with USDA guidelines.

• Fannie Mae Conventional: HFA Preferred product onlyo MI and No MI options available

7

Advantage 4Advantage 4 provides a grant equal to 4% of the first mortgage amount and is applied toward required downpayment and closing costs, and then principle reduction:

• Welcome Home and Home Again loans with Advantage 4 rates• Standard 1st Mortgage documents• No repayment is ever required from the borrower• No additional lien is recorded on the property

HFA provided downpayment assistance funds are considered borrower’s own funds for the purposes of qualifying agency LTV and CLTV limits.

Funds must be provided at closing by DSHA.

8

Second Mortgage Assistance Loan (SMAL)

• Available on income and purchase price qualified DSHA Homeownership Loans.

• Loan amounts up to $8,000.• Funds must be used toward downpayment and settlement costs. • 3% Simple interest. • Repayment is deferred for 30‐years, or until the first mortgage is refinanced, or the property is sold or transferred; whichever comes first.

• The SMAL is secured by a second lien against the property.

9

SMAL – Special Rehab

• Available only for income and purchase price qualified DSHA borrowers using the FHA 203ks program.

• Loan amounts up to $10,000.• Funds must be used toward downpayment and settlement costs. • 3% Simple interest. • Repayment is deferred for 30‐years, or until the first mortgage is refinanced, or the property is sold or transferred; whichever comes first.

• The SMAL – Special Rehab is secured by a second lien against the property.

10

Second Mortgage Assistance Loan (SMAL) and SMAL – Special Rehab

Additional Requirements• These products are only available in conjunction with a DSHA first mortgage product.

– Household income and purchase price limits are the same as for the Delaware First‐Time Homebuyer. Tax Credit program.

– All borrowers must participate in a U.S. Department of Housing and Urban Development (HUD)‐approved housing counseling product/home ownership education.

11

Rates for Second Mortgage Assistance Loans

• Can be used with either Welcome Home and Home Again loans.• SMAL and Advantage 4 cannot be combined.

HFA‐provided downpayment assistance funds are considered borrower’s own funds for the purposes of qualifying agency LTV and

CLTV limits. Funds must be provided at closing by DSHA.

*Rates and terms are subject to change.

12

SMAL Registration• Lender reserves the SMAL using DSHA’s MITAS On‐line system.• Once the Reservation is completed, the Lender prints the Reservation Confirmation.

• SMAL loans are subject to TRID. To assist Lenders, DSHA will generate and mail the Loan Estimate directly to borrowers to insure the LE disclosure timeframes are met. Lenders can view the SMAL loan reservation in Mitas to confirm DSHA has mailed the Loan Estimate.

• Once approved, the Lender must fax a SMAL Wire Request to DSHA. Once processed the SMAL loan status will be made “Active” at which time the SMAL Note, Mortgage and Closing Disclosure will be made available through Mitas.

• It is the Lender’s responsibility to make sure the SMAL Closing Disclosure is provided to the Borrower and maintain documentation that TRID timeframes have been met.

13

DSHA Forms – SMAL Loans

• At Application– SMAL Mortgagor’s Affidavit

• Prior to Closing– SMAL Wire Request Worksheet– SMAL Note (prefilled document can be printed from MITAS once loan has been made “Active”)

– SMAL Mortgage (prefilled document can be printed from MITAS once loan has been made “Active”)

– SMAL Closing Disclosure (available to print from Mitas once DSHA processes lender’s wire request). Lender is responsible to comply with TRID timeframes to provide this to the borrower and document compliance.

14

SMAL vs. Advantage 4

15

SMAL(Second Mortgage)

ADVANTAGE 4(Grant)

1st Mortgage Amount $200,000.00 $200,000.00

Interest Rate 4.50% 5.50%

Term (months) 360 360

P & I Payment $1,013.37 $1,135.58

DPA Provided $8,000.00 $8,000.00

Repayment Amount* $15,424.38 $0.00

* Assumes no payments made during 30 year deferment period.

DSHA Compliance Review

There are three components of Compliance Review:

1. Income2. Purchase Price or Loan Limit3. First‐Time or Repeat Homebuyer Status

16

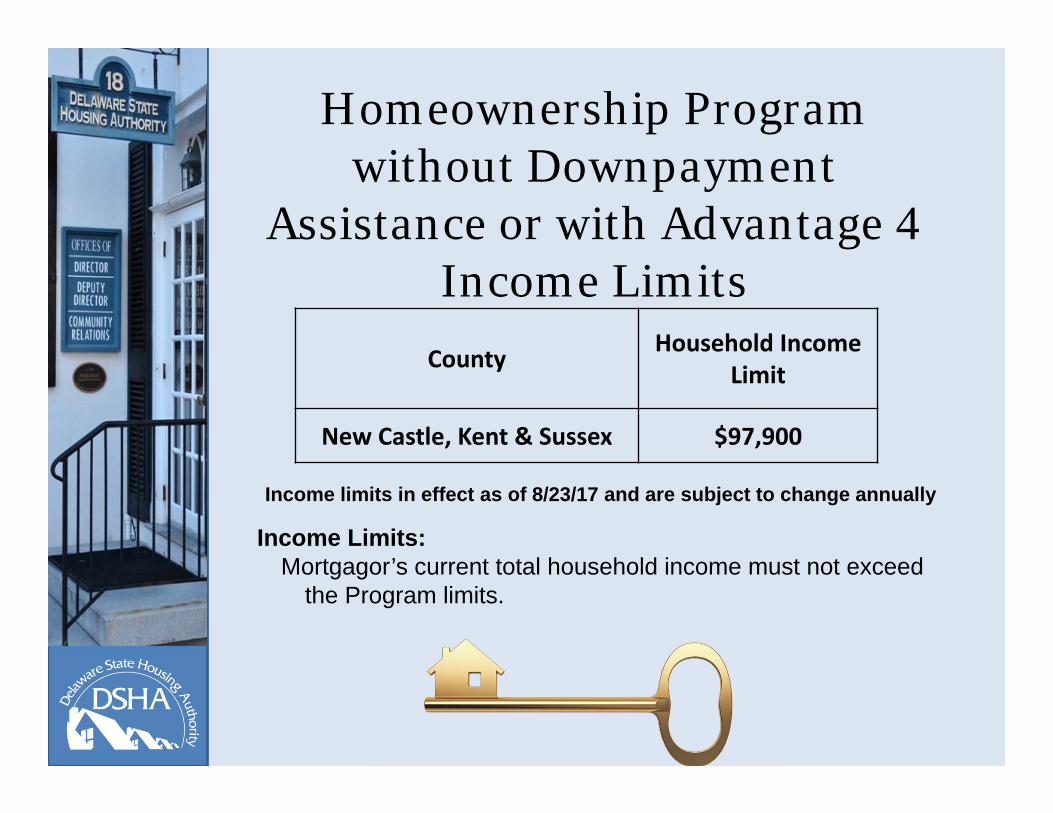

Homeownership Program without Downpayment

Assistance or with Advantage 4 Income Limits

17

County Household Income Limit

New Castle, Kent & Sussex $97,900

Income Limits:Mortgagor’s current total household income must not exceed

the Program limits.

Income limits in effect as of 8/23/17 and are subject to change annually

Homeownership Loans without Downpayment Assistance or with

Advantage 4 Loan Limits

18

Income Limits:Mortgagor’s loan amount must not exceed the program limits.

Loan limits in effect as of 8/23/17 and are subject to change.

County Loan Limit

Kent, New Castle & Sussex $417,000

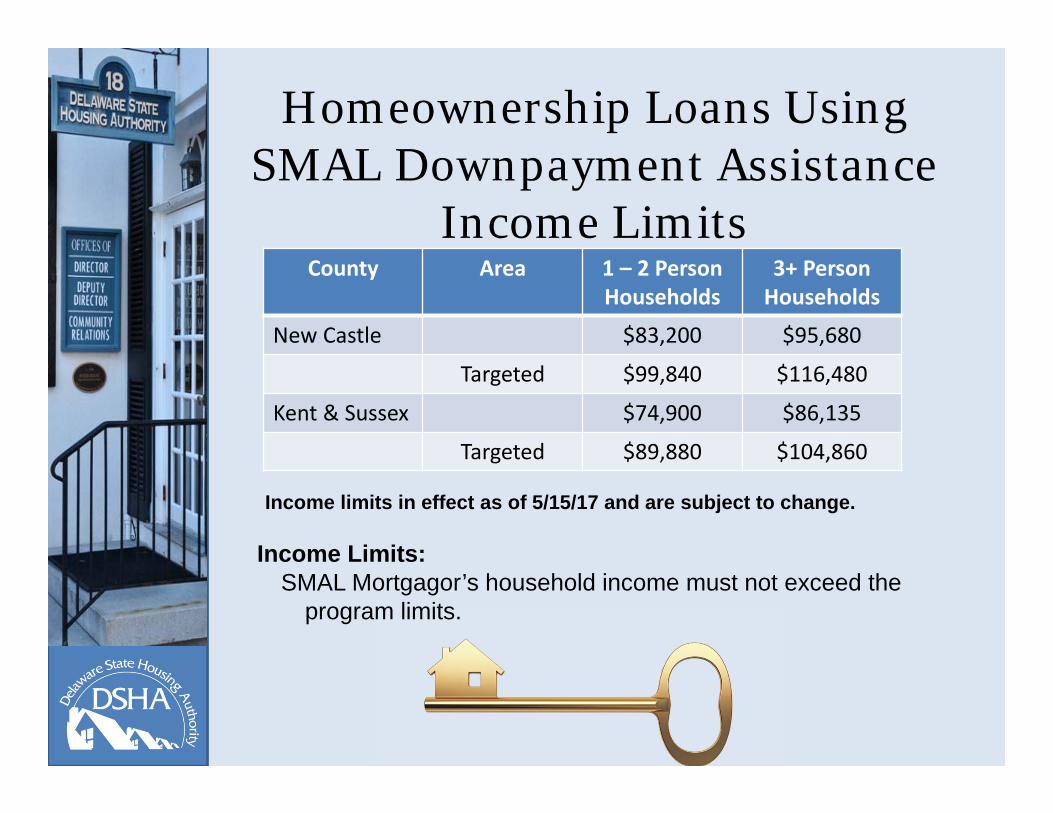

Homeownership Loans Using SMAL Downpayment Assistance

Income Limits

19

Income Limits:SMAL Mortgagor’s household income must not exceed the

program limits.

Income limits in effect as of 5/15/17 and are subject to change.

County Area 1 – 2 Person Households

3+ Person Households

New Castle $83,200 $95,680

Targeted $99,840 $116,480

Kent & Sussex $74,900 $86,135

Targeted $89,880 $104,860

SMAL Program Purchase Price Limits

20

Income Limits:Mortgagor’s purchase price must not exceed the program

limits.

Purchase price limits in effect as of 5/15/17 and are subject to change.

Property Location by County

Purchase Price Limit

1 Unit 2 Unit 3 Unit 4 Unit

New Castle County $349,411 $447,283 $540,690 $671,938

Kent County $248,098 $317,655 $383,962 $477,135

Sussex County $291,176 $372,752 $450,552 $559,933

Compliance Income Calculation

The DSHA income calculation can and probably will be different than the underwriting income used for loan qualification purposes.

• Income calculated is the gross pay and any additional income, including all mortgagors and anyone over the age of 18 that will be living in the property.

• All forms of income will be used including:– Overtime, Bonus, SSI, Disability Income, Pension, Retirement, Child Support/Alimony, Seasonal/Part‐Time jobs, Self‐Employment, Interest and Dividend Income, Rental Income, Gambling and Lottery Winnings, Public Assistance, etc.

– Additional income such as bonuses, commissions, shift differential and over time are averaged over a 12‐month period.

Note: DSHA will include all income that appears on the 1003 when determining total household income.

21

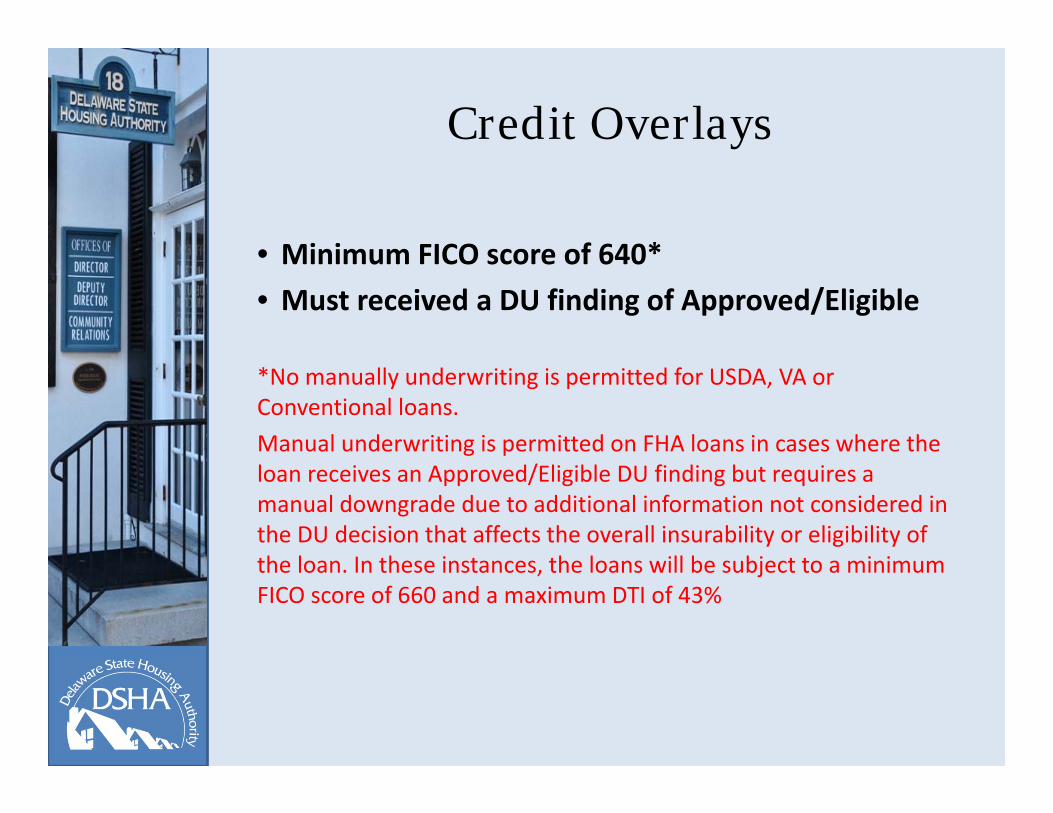

Credit Overlays

• Minimum FICO score of 640* • Must received a DU finding of Approved/Eligible

*No manually underwriting is permitted for USDA, VA or Conventional loans.Manual underwriting is permitted on FHA loans in cases where the loan receives an Approved/Eligible DU finding but requires a manual downgrade due to additional information not considered in the DU decision that affects the overall insurability or eligibility of the loan. In these instances, the loans will be subject to a minimum FICO score of 660 and a maximum DTI of 43%

22

FHA, VA, USDA Eligible Properties

Owner Occupied Residential Properties• Single Family Units and Town Houses• Agency Approved Condominiums for FHA, VA or USDA only

– Please refer to Section 4.4 of the Seller’s Guide for specific guidelines

• Planned Unit Developments (PUD’s)• 1‐4 Unit Properties (meeting DSHA purchase price limits and Agency guidelines for the loan product being originated)

Properties Not Allowed:• Manufactured homes• Rental homes• Co‐ops• Investment properties• Recreational, vacation, or second homes

23

FHA 203(ks)• The FHA 203(ks) product is intended to facilitate uncomplicated rehabilitation and/or improvements to a home for which plans, consultants, engineers and/or architects are not required. – 203(ks) rehabilitation amount is limited to $35,000, eligible improvements are limited to improvements such as energy efficiencies and cosmetic improvements that are not structural changes to the property. Refer to HUD for more details on allowable uses.

– FHA 203ks may access the SMAL – Special Rehab program that provides up to $10,000 for down payment and closing costs.

24

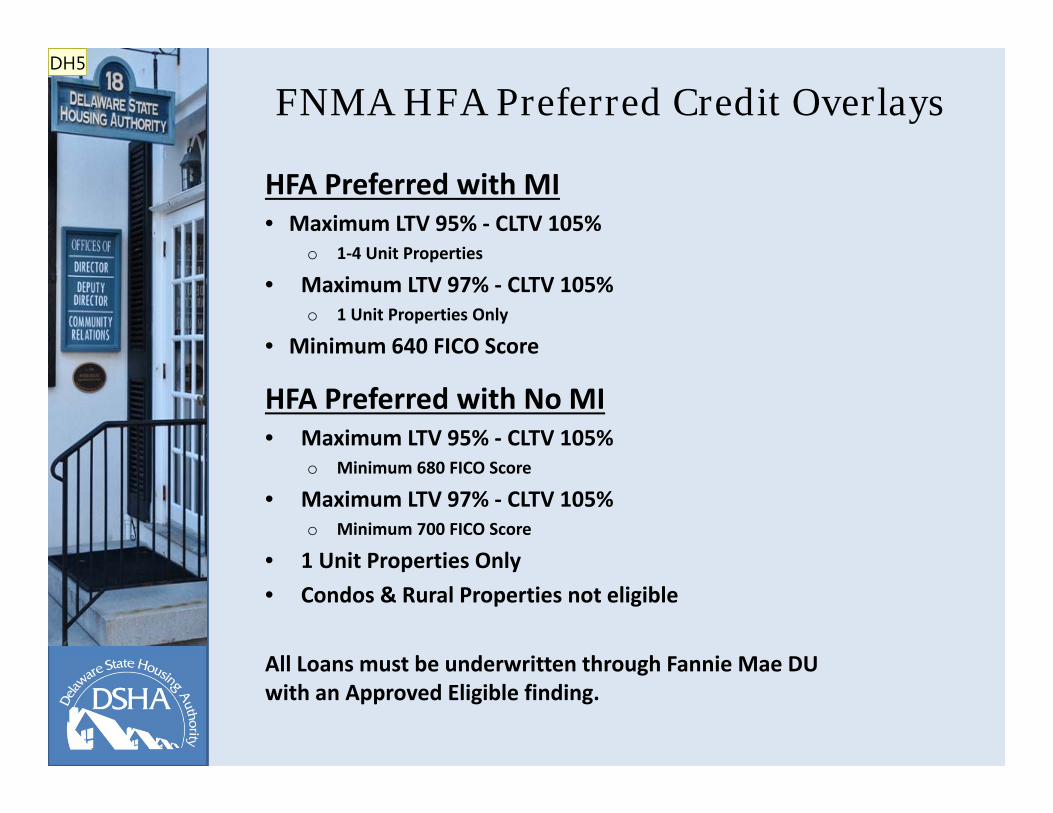

FNMA HFA Preferred Credit Overlays

HFA Preferred with MI• Maximum LTV 95% ‐ CLTV 105%

o 1‐4 Unit Properties

• Maximum LTV 97% ‐ CLTV 105% o 1 Unit Properties Only

• Minimum 640 FICO Score

HFA Preferred with No MI• Maximum LTV 95% ‐ CLTV 105%

o Minimum 680 FICO Score

• Maximum LTV 97% ‐ CLTV 105% o Minimum 700 FICO Score

• 1 Unit Properties Only• Condos & Rural Properties not eligible

All Loans must be underwritten through Fannie Mae DU with an Approved Eligible finding.

25

DH5

Slide 25

DH5 I re-worked this whole page. Doreen Haugh, 8/17/2017

FNMA HFA Preferred Eligible Properties

Eligible Properties ‐ Owner Occupied Residential Properties

• Single Family Units and Town Houses• Planned Unit Developments (PUD’s)

Ineligible Properties• Condominiums on loans with No MI• Multiple Unit Properties• Vacation/Second Homes• Co‐ops• Investment/Rental Units• Manufactured Homes

26

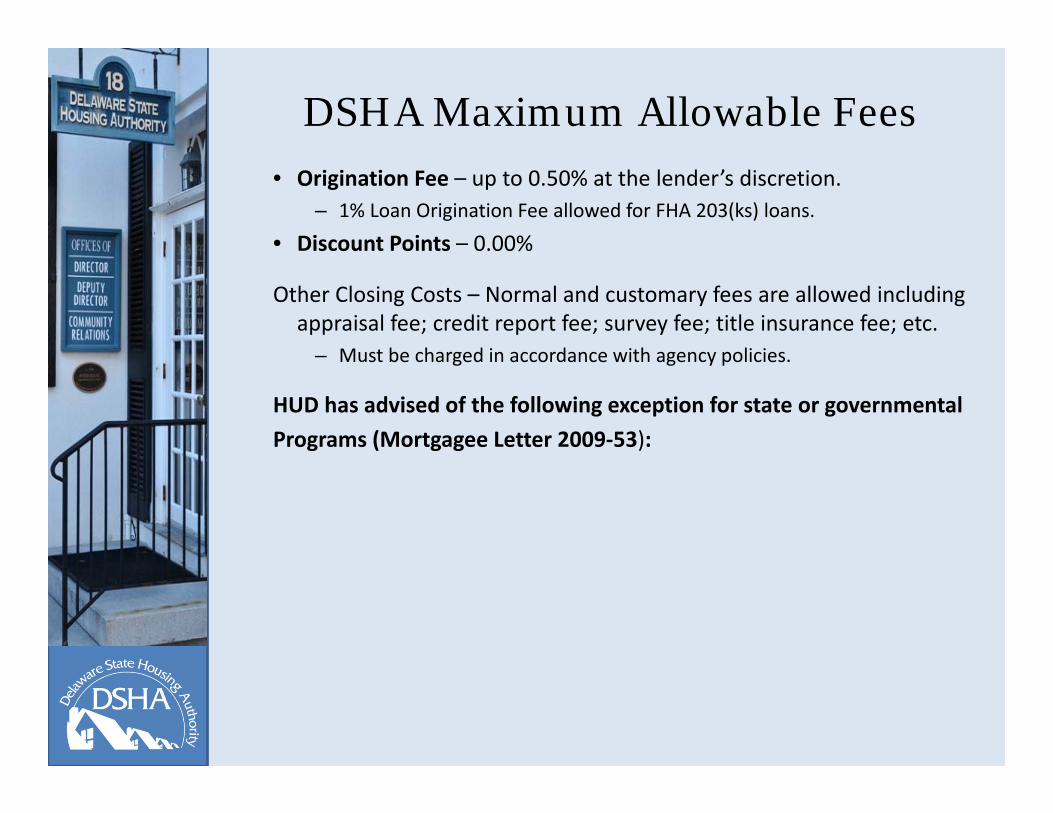

DSHA Maximum Allowable Fees• Origination Fee – up to 0.50% at the lender’s discretion.

– 1% Loan Origination Fee allowed for FHA 203(ks) loans.

• Discount Points – 0.00%

Other Closing Costs – Normal and customary fees are allowed including appraisal fee; credit report fee; survey fee; title insurance fee; etc.

– Must be charged in accordance with agency policies.

HUD has advised of the following exception for state or governmental Programs (Mortgagee Letter 2009‐53):

27

DSHA Forms

All DSHA program specific forms are available on DSHA’s Lender Resource website at Lenders.DeStateHousing.com under the Homeownership Program Documents tab.

DSHA training presentations, important links & contacts, Mitas user tips, as well as a calendar of holidays and scheduled closings are also available on the Lenders Resource Website.

28

Loan Flow

1. Lender pre‐qualifies homebuyer per DSHA and Agency guidelines.

1. Lender registers loan(s) through DSHA’s Mitas Online Reservation System at https://MITAS.destatehousing.com

2. Lender uploads compliance file to DSHA for eligibility review: • Income• Homebuyer Status

o Qualified Veteran (if applicable)

• Purchase Price/Acquisition Cost3. Once “Committed”, Lender closes loan and delivers

closed purchase file to Lakeview for funding.1. If using SMAL funds, lender submits the Wire Request

Worksheet to request funds 7 business days prior to settlement, 24 hours for Advantage 4 wires . DSHA will wire funds to closing.

29

Loan Flow (continued)

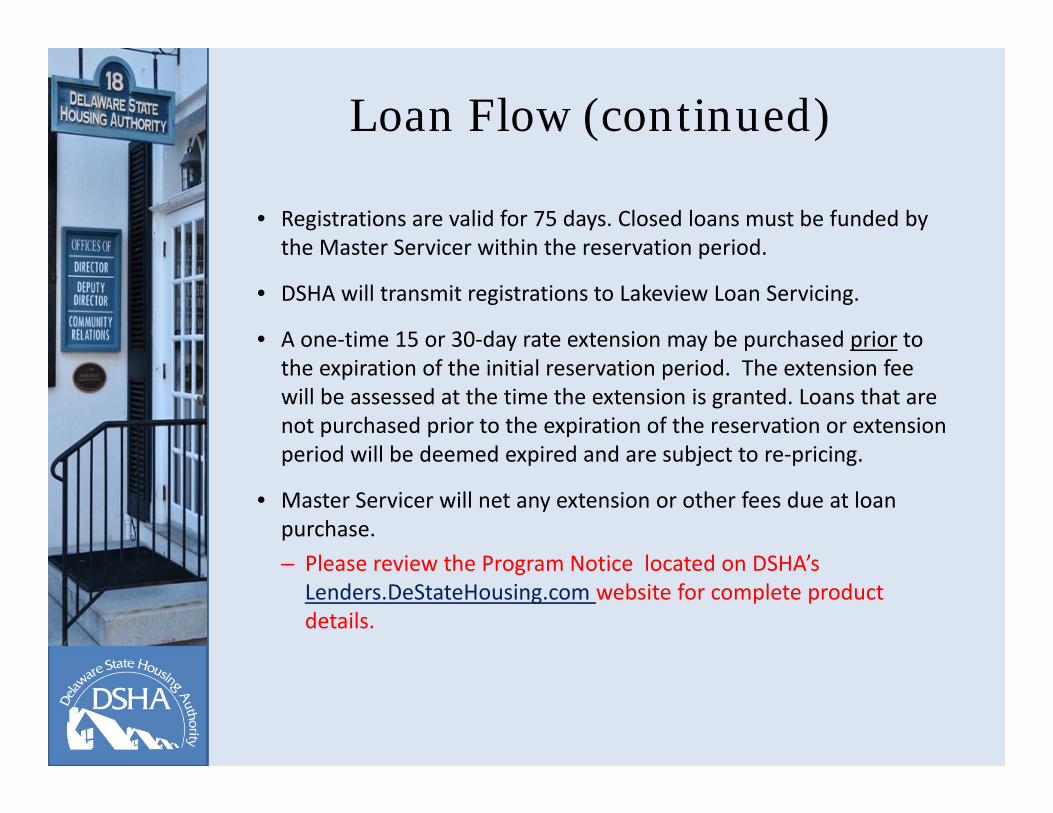

• Registrations are valid for 75 days. Closed loans must be funded by the Master Servicer within the reservation period.

• DSHA will transmit registrations to Lakeview Loan Servicing.

• A one‐time 15 or 30‐day rate extension may be purchased prior to the expiration of the initial reservation period. The extension fee will be assessed at the time the extension is granted. Loans that are not purchased prior to the expiration of the reservation or extension period will be deemed expired and are subject to re‐pricing.

• Master Servicer will net any extension or other fees due at loan purchase. – Please review the Program Notice located on DSHA’s Lenders.DeStateHousing.com website for complete product details.

30

Pre-Closing Compliance File Delivery

• The Compliance Package for each loan must be uploaded to DSHA at least 3 business days before closing. Borrowers requesting SMAL funds must be delivered earlier to provide sufficient time for Compliance Review and the Closing Disclosures to be provided to borrower. The Closing Disclosure will be available to print once the SMAL Wire Request is processed by DSHA.

Note: Incomplete loan files are not placed in the queue for compliance review until all outstanding conditions have been satisfied. Therefore, it is of no benefit to submit an incomplete package ahead of time.

– Please use the Transmittal of Loan Documentation for Compliance, located on the Correspondent Lending Website.

– The $75 compliance review fee will be netted from the purchase wire or billed to lender if the loan does not close under the DSHA product.

31

Compliance Review Package Requirements-Delivery

Complete the Transmittal of Loan Documentation For Compliance Review Checklist and Stacking Sheet and upload it along with all of the required documentation using the Mitas Secure Document Upload function. This should be done as a single upload.

Tracking Your Loan Pipeline in MITAS

• Lenders should use MITAS to see status of files delivered to DSHA for Compliance Review for any Compliance Review conditions and DSHA staff assigned to file.

• Lenders should cancel reservations of any "dead loans“ prior to reservation expiration to avoid non-cancellation penalty fees.

Lenders should cancel all inactive Mortgage Loan reservations as soon as possible through the Mitas On-line website or be assessed a non-cancellation penalty.Penalties for non-cancellation are: • $300 for 1st mortgages; and • $100 for 2nd mortgages There is no penalty if the lender cancels the loan online prior to the expiration of the reservation or the loan is purchased within reservation period. Cancelled loans may not be re-registered for a DSHA loan for a time period of 60 days after the original expiration date or the purchased extension date, whichever is later.

Lender should monitor pipeline for expiring reservations.

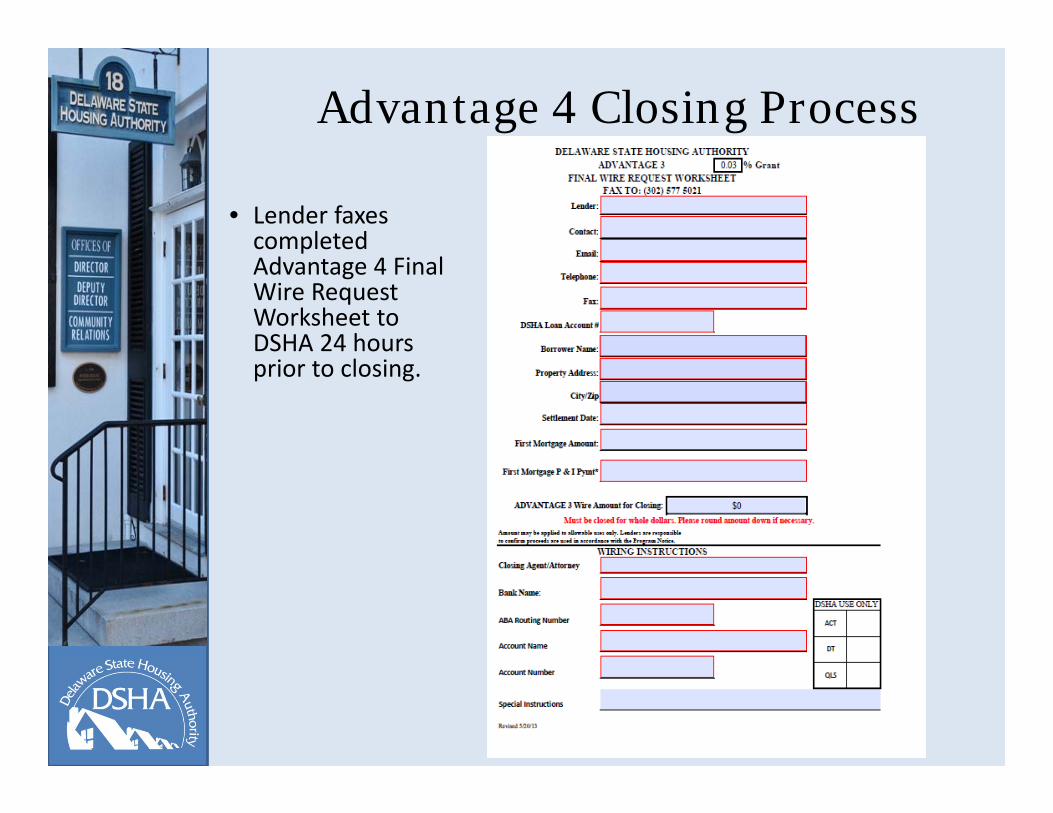

Advantage 4 Closing Process

• Lender faxes completed Advantage 4 Final Wire Request Worksheet to DSHA 24 hours prior to closing.

35

SMAL Closing Process

• Lender faxes Final Wire Request to DSHA 7 business days or more prior to closing.

• Lender pulls the Closing Disclosure, Note and Mortgage from the MITAS On‐line system once the SMAL loan is updated to an “Active” status by DSHA staff.

36

SMAL Closing Process

Lender must use the SMAL Closing Disclosure provided by DSHA. The form can be downloaded by the lender once DSHA changes the loan from a “Committed” to an “Active” status.

37

Document Original Copy NotesClosing Disclosure X Signed copy.

SMAL Mortgage Note XOriginal borrower signature(s) and witness signature.

SMAL Mortgage X Signed Certified True Copy.

SMAL Borrower’s Affidavit

X Signed copy.

SMAL Delivery Requirements for Loan Purchase

Closed Loan Delivery

Closed loans must be delivered and purchased by Lakeview within the 75 day reservation period (90 or 105 days based on whether a 15 or 30

day extension was purchased).

39

Housekeeping Items

• Please insure you are providing your borrowers with the current versions of our Disclosures located on the Lender’s Resource Center website: Lenders.DeStateHousing.com

• When submitting conditions, please try and wait until you have all of the conditions and submit them together.

Housekeeping Items• When making changes to a committed loan, please note on a coversheet the specific changes being requested.

• When completing the Mortgagor’s Affidavit provide a full 3 year residence history with the property owner’s name an address.

• Conventional HFA Preferred loans may have a Homebuyer Education requirement even if not using SMAL.

Housekeeping Items• Reservations follow the borrower not the property. If a property falls through, a new property can be substituted, so do not rush to cancel the Reservation or the borrower will be subject to a lock‐out period of 60 days from the Reservation Expiration Date.

• Program changes to reservations are subject to the higher of the rates in effect at the time of reservation or the time the change is processed by DSHA.

Recent DSHA Enhancements• Loans with SMAL /Tax Credits can be reserved simultaneously.

• Increased Income and Loan Size Limits

• Lender Resource Website - Lenders.destatehousing.com

• Delaware First-Time Homebuyer Tax Credit

• Advantage 4 – 1st Mortgage options with 4% grant

• Comprehensive Lender Pipeline Reporto Allows lender’s pipeline across all products to be viewed in

one consolidated pipeline report.

• Secure Document Upload through the MITAS systemo Reduces cost and delivery time for submission of

Compliance Review Packages and Compliance Review Pending Conditions.

Delaware State Housing Authority

Delaware First-Time Homebuyer Tax Credit

The Delaware First-Time Homebuyer Tax Credit Team

45

Delaware State Housing Authority (DSHA) has partnered with Hilltop Securities, Inc. to support lenders, realtors, and homebuyers to market, educate, and administer DSHA’s Delaware First‐Time Homebuyer Tax Credit.

o DSHA – will provide:• Lender Training• Delaware First‐Time Homebuyer Tax Credit Marketing• Delaware First‐Time Homebuyer Tax Credit Processing

o Hilltop Securities, Inc.– will provide:• Delaware First‐Time Homebuyer Tax Credit Issuance to

Homebuyer• General Reporting• IRS Annual Lender Reports• Homebuyer Annual Letter

DE Tax Credit Program Income Limits

46

Income Limits:Mortgagor’s household income must not exceed the program

limits.

Income limits in effect as of 5/15/17 and are subject to change.

County Area 1 – 2 Person Households

3+ Person Households

New Castle $83,200 $95,680

Targeted $99,840 $116,480

Kent & Sussex $74,900 $86,135

Targeted $89,880 $104,860

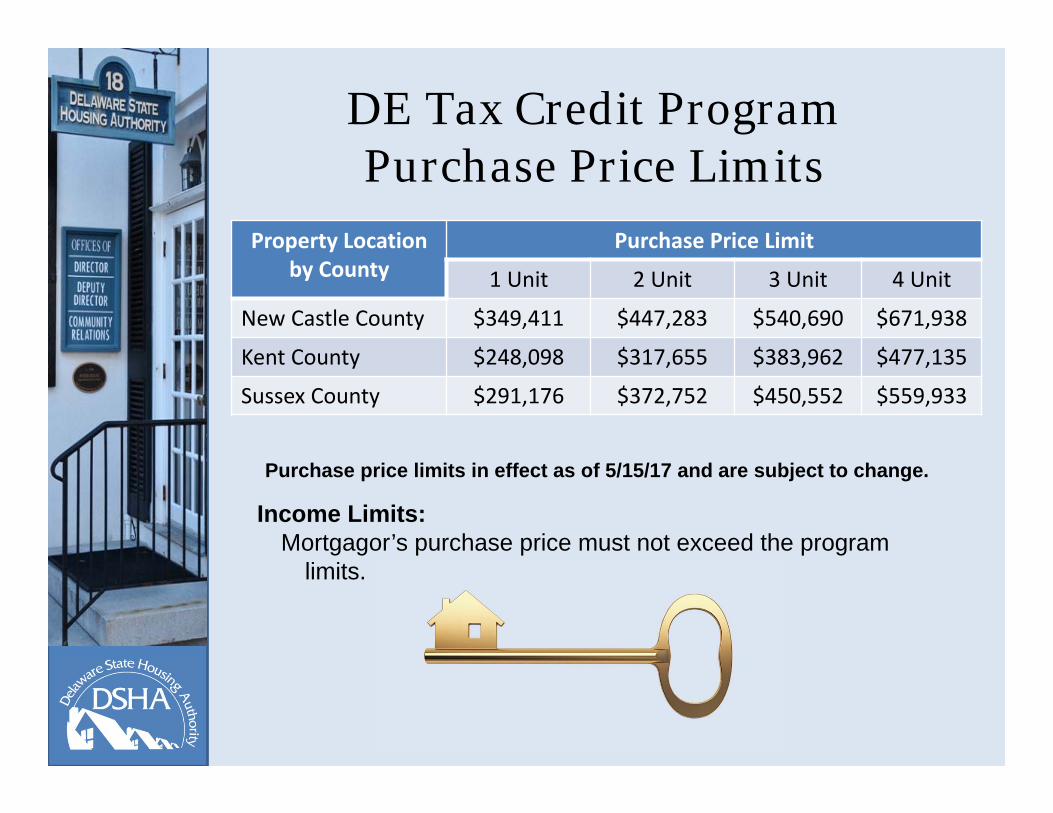

DE Tax Credit Program Purchase Price Limits

47

Income Limits:Mortgagor’s purchase price must not exceed the program

limits.

Purchase price limits in effect as of 5/15/17 and are subject to change.

Property Location by County

Purchase Price Limit

1 Unit 2 Unit 3 Unit 4 Unit

New Castle County $349,411 $447,283 $540,690 $671,938

Kent County $248,098 $317,655 $383,962 $477,135

Sussex County $291,176 $372,752 $450,552 $559,933

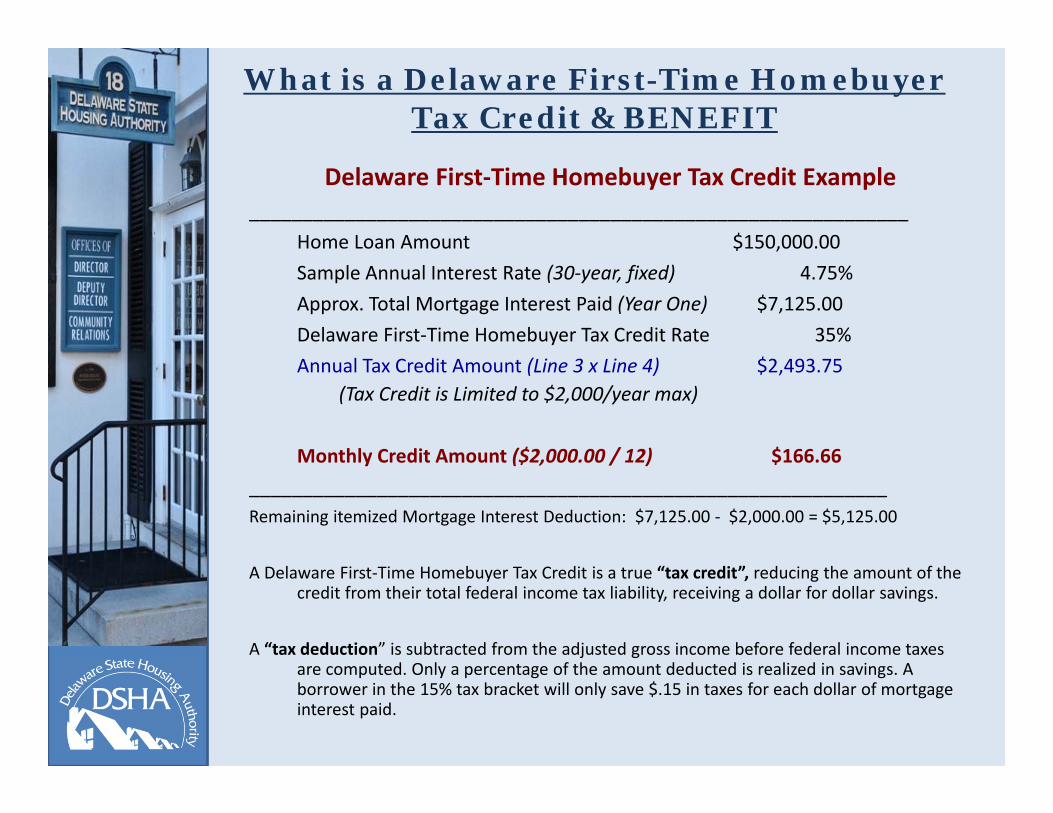

What is a Delaware First-Time Homebuyer Tax Credit and What are the Benefits?

o A Delaware First‐Time Homebuyer Tax Credit is a federal income tax credit designed to assist people to better afford individual ownership of housing.

o The Delaware First‐Time Homebuyer Tax Credit provides an annual tax credit up to $2,000 to qualifying homebuyers for the original term of their mortgage, as long as they live in the property and have a mortgage. The annual credit is calculated by taking the annual mortgage interest paid multiplied by the Delaware First‐Time Homebuyer Tax Credit rate of 35% which has been established by DSHA.

o The tax credit is applied to the federal income tax liability of the Delaware First‐Time Homebuyer Tax Credit certificate holder. There must be a tax liability to claim the credit.

o Delaware First‐Time Homebuyer Tax Credit calculation example to follow.

Delaware First‐Time Homebuyer Tax Credit Example______________________________________________________________

Home Loan Amount $150,000.00Sample Annual Interest Rate (30‐year, fixed) 4.75%Approx. Total Mortgage Interest Paid (Year One) $7,125.00Delaware First‐Time Homebuyer Tax Credit Rate 35%Annual Tax Credit Amount (Line 3 x Line 4) $2,493.75

(Tax Credit is Limited to $2,000/year max)

Monthly Credit Amount ($2,000.00 / 12) $166.66____________________________________________________________Remaining itemized Mortgage Interest Deduction: $7,125.00 ‐ $2,000.00 = $5,125.00

A Delaware First‐Time Homebuyer Tax Credit is a true “tax credit”, reducing the amount of the credit from their total federal income tax liability, receiving a dollar for dollar savings.

A “tax deduction” is subtracted from the adjusted gross income before federal income taxes are computed. Only a percentage of the amount deducted is realized in savings. A borrower in the 15% tax bracket will only save $.15 in taxes for each dollar of mortgage interest paid.

What is a Delaware First-Time Homebuyer Tax Credit & BENEFIT

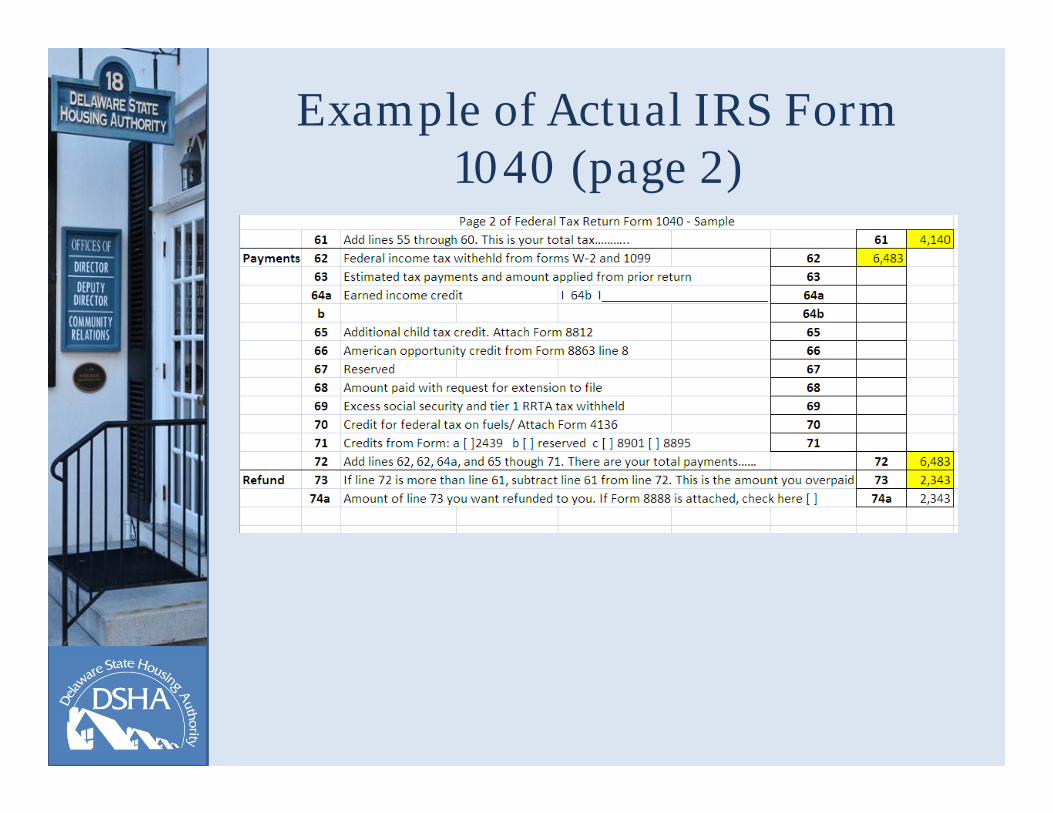

Example of Actual IRS Form 1040 (page 2)

How a Homebuyer Uses The Delaware First-Time Homebuyer Tax Credit

Actual Example based on prior scenario.

Borrower may also itemize remaining $5,125.00 of mortgage interest paid.

DSHA encourages homebuyers to contact their tax advisor or employer to help them with the necessary tax forms and, if they so choose, to properly adjust

their tax withholding.

Adjusted Gross Income $42,132.00

Withholdings & Tax Payments $6,483.00

Tax Liability $4,140.00

Refund $2,343.00

Tax Credit (up to $2,000) $1,797.00

Revised Tax Refund $4,140.00

What is a Delaware First-Time Homebuyer Tax Credit and What are the Benefits?

o The annual maximum $2,000 tax credit may be used by a lender to assist the homebuyer in qualifying for a mortgage loan, following agency underwriting guidelines:

Note: DSHA will include all income that appears on the 1003 when determining total household income.

o The Delaware First‐Time Homebuyer Tax Credit has the potential of saving the homebuyer thousands of dollars over the life of the loan.

How a Homebuyer Uses The Delaware First-Time Homebuyer Tax Credit

o Borrower claims the credit with their annual federal income tax return using IRS Form 8396.

o The credit may be claimed for the original term of the loan as long as the home is their principal residence. The borrower must have tax liability to benefit from the annual credit in any given year.

o The borrowers may, if they choose, adjust their W‐4s to reflect the anticipated credit.

o If the amount of the Delaware First‐Time Homebuyer Tax Credit credit exceeds the Delaware First‐Time Homebuyer Tax Credit holder’s tax liability, reduced by any other personal credits for the tax year, the unused portion of the credit can be carried forward to the next three tax years or until used, whichever comes first. The homebuyer will have to keep track of the unused credit each year. The current year credit is applied first and then the oldest amount of unused credit applied next.

DSHA encourages homebuyers to contact their tax advisor or employer to help them with the necessary tax forms and, if they so choose, to properly adjust their tax

withholding.

Basic Delaware First-Time Homebuyer Tax Credit Requirements

o If using a DSHA Welcome Home loan, the rate, term, of the first mortgage loan is determined by first mortgage product and whether or not the borrower is using DSHA downpayment and closing cost assistance. For lenders not using a DSHA Welcome Home loan, the rate, term, and type of mortgage loan is determined by the lender.

o Only first mortgages qualify for the Delaware First‐Time Homebuyer Tax Credit Program.

o Delaware First‐Time Homebuyer Tax Credit may be used with all DSHA’s products, including Second Mortgage Assistance Loan (SMAL) and Welcome Home Advantage 3.

Delaware First-Time Homebuyer Tax Credit Eligibility Requirements

Simply put, any homebuyer eligible for a Welcome Home loan whose income and purchase price does not exceed the Tax Credit limits will qualify for the Delaware First‐Time Homebuyer Tax Credit.

Everyone who signs the Mortgage must sign the affidavits.

Delaware First-Time Homebuyer Tax Credit Process

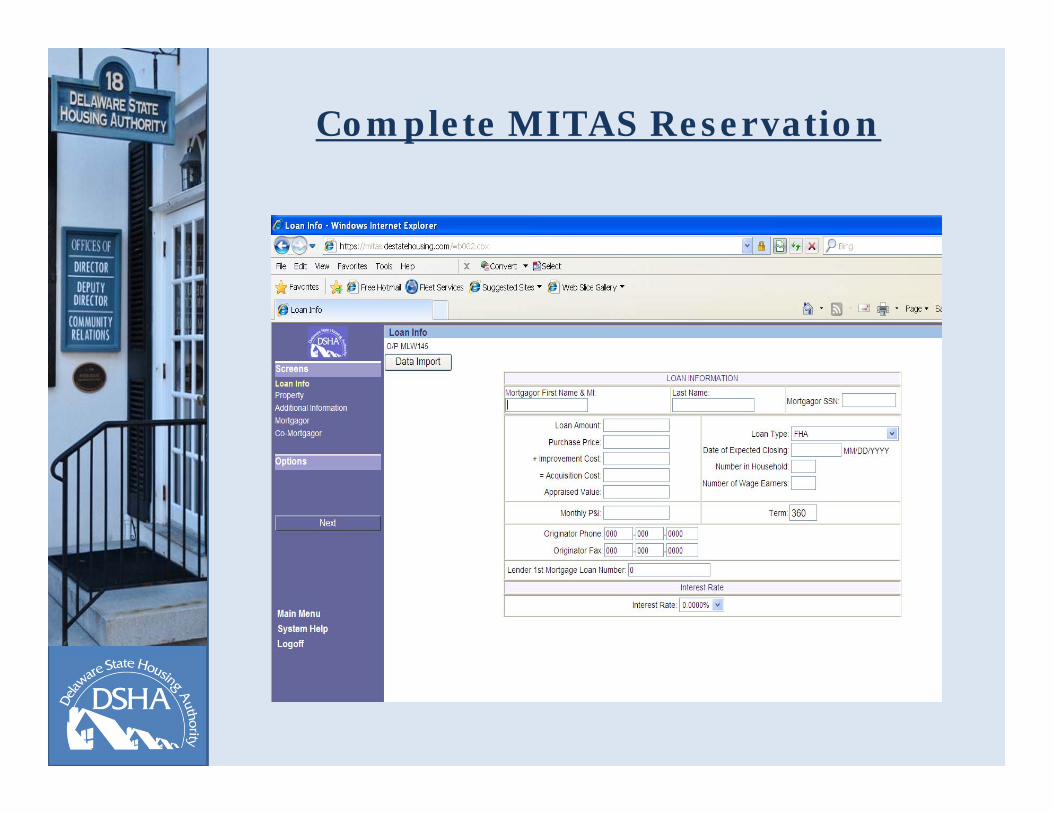

Step 1o Reserve –Delaware First‐Time Homebuyer Tax Credit Funds via the

MITAS online reservation system.

Complete MITAS Reservation

Delaware First-Time Homebuyer Tax Credit Process

o Lenders will submit the Delaware First‐Time Homebuyer Tax Credit Compliance Review Package via electronic upload through the Mitas reservation system.

o If using a DSHA 1st Mortgage, DSHA will use the upload on the primary mortgage. o If requesting a “Stand Alone” tax credit, the Compliance Review Package will need to

be uploaded to that record in Mitas.

o DSHA will review for eligibility. If the borrower is eligible, the Reservation will be moved to a Committed status and DSHA will issue the following:

• Delaware First‐Time Homebuyer Tax Credit Approval Letter• Delaware First‐Time Homebuyer Tax Credit Closing Package

Checklist (example to follow)• Delaware First‐Time Homebuyer Tax Credit Closing Affidavit

o Submissions that are incomplete or contain errors will be moved to status of “Pending‐Conditions Posted”. Lender must review and submit items requested within 10 days or the reservation will be cancelled.

Fees and Costs

• The fees collected at closing are: – $350 for Delaware First‐Time Homebuyer Tax

Credit Application/Closing Package Review – 1% of the total loan amount.

(The 1% fee will be waived for borrowers using a DSHA Welcome Home loan.)

• Fees can be paid by the buyer, seller, etc., as allowed by FHA, VA, USDA, conventional and/or investor guidelines.

Delaware First-Time Homebuyer Tax Credit Process

• The lender closes the loan. After closing, send Hilltop Securities, Inc. all of the required items listed on the Hilltop Securities closing package checklist along with applicable fees. Original documents are not required. Hilltop Securities will review the closing package documents and if complete, issue the certificate to the buyer.

Delaware First-Time Homebuyer Tax Credit Servicing

o In January of the following year, lender submits IRS form 8329 for all Delaware First‐Time Homebuyer Tax Credits issued in the prior calendar year. Hilltop Securities will complete the form and forward to each lender for filing. It is the responsibility of the lender to review the report for accuracy prior to filing.

o Also in January, Hilltop Securities will send homebuyers receiving a Delaware First‐Time Homebuyer Tax Credit in the prior tax year a reminder letter and information on how to file.

o Homebuyers who refinance their first mortgage loan can continue to claim the tax credit by contacting Hilltop Securities and requesting re‐issuance of the certificate.

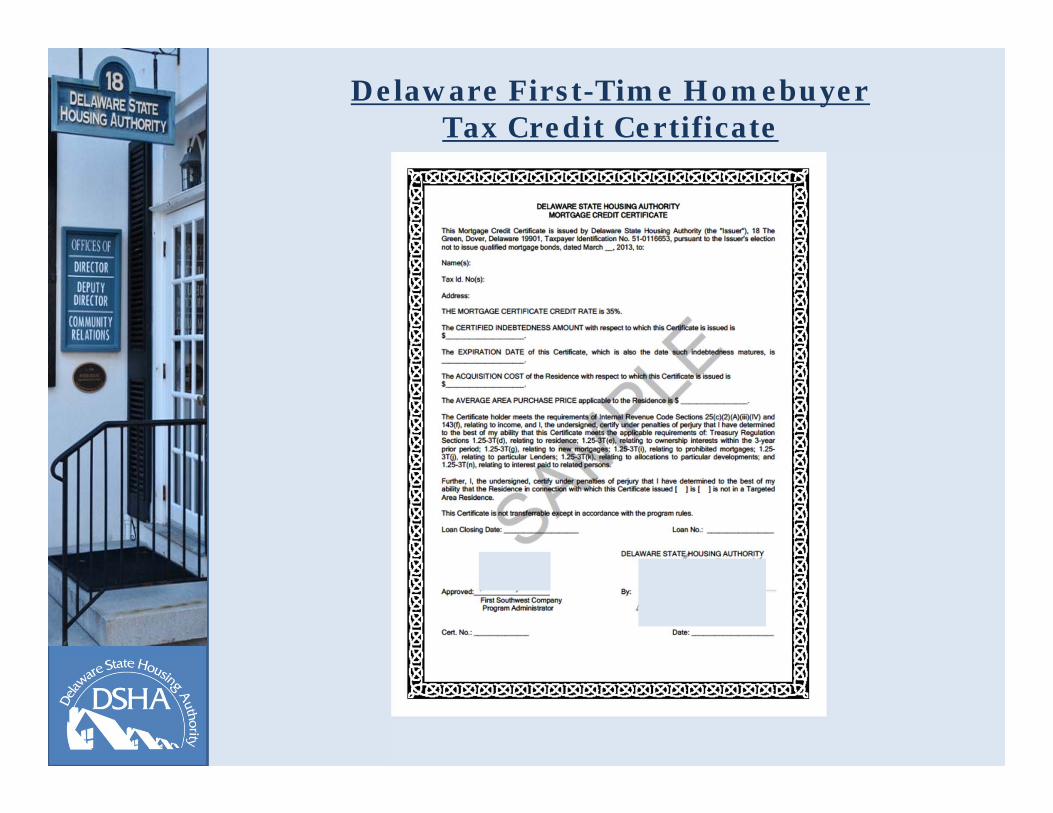

Delaware First-Time Homebuyer Tax Credit Certificate

Summary

There are two Main Benefits to the Homebuyer:

1. Provides a federal tax credit up to $2,000 a year for up to 30 years as long as the homebuyer occupies the home and has a mortgage.

2. Can help qualify the homebuyer which results in increased buyer capacity to qualify for the mortgage loan.

General eMail Address: [email protected]

Mailing Address: Hilltop Securities, Inc.1201 Elm Street, Suite 3500Dallas, Texas 75270

Contact:Lori Wood 214‐953‐4231 [email protected]

Additional services available from Hilltop Securities:• Realtor, Lender, Builder and Outreach, Education and Training• Present at First‐Time Homebuyer Seminars• Marketing Materials

Hilltop Securities, Inc. Contact Information

DSHA Originations Contacts

Lender Resource Website: Lenders.DeStateHousing.com

65

Telephone: 302-577-5001Fax: 302-577-5021

Housing Finance Manager Lender Support

Karen FlowersOffice ManagerInitial Package Review‐Pending Conditions

Lisa McCloskeyMortgage Finance Officer IICompliance Review/Lender Support

Pamela SpencerHousing Mortgage Loan Officer 1Compliance Review/Lender Support

DSHA Post Closing Contacts

Brian RosselloHousing Finance ManagerPost Closing

Enid BeltranMortgage Loan Officer IIPost Closing

Carol OrzechowskiAdministrative Assistant II Document Control

66

Telephone: 302-577-5001Fax: 302-577-5021