Embed Size (px)

Citation preview

Hochschild Mining plc

Sell Side Roundtable

Ignacio Bustamante, CEO

Ramon Barúa, CFO

Isabel Lutgendorf, Head of IR

1

Disclaimer

Some statements contained in this presentation or in documents referred to in it are or may be forward‐

looking statements. Actual results may differ from those expressed in such statements, depending on a

variety of factors.

Past performance of the Company or its shares cannot be relied on as a guide to future performance.

Any forward‐looking information contained in this presentation has been prepared on the basis of a

number of assumptions which may prove to be incorrect, and accordingly, actual results may vary.

This presentation does not constitute, or form part of or contain any invitation or offer to any person to

underwrite, subscribe for, otherwise acquire, or dispose of any shares in Hochschild Mining plc or advise

persons to do so in any jurisdiction, nor shall it, or any part of it, form the basis of or be relied on in any

connection with or act as an inducement to enter into any contract or commitment therefore. No reliance

may be placed for any purpose whatsoever on the information or opinions contained in this document or

on its completeness and no liability whatsoever is accepted for any loss howsoever arising from any use of

this document or its contents otherwise in connection therewith.

Nothing in this presentation is to be

construed as a profit forecast.

This presentation has been prepared in compliance with English law and English courts will have exclusive

jurisdiction over any disputes arising from or connected with this presentation.

2

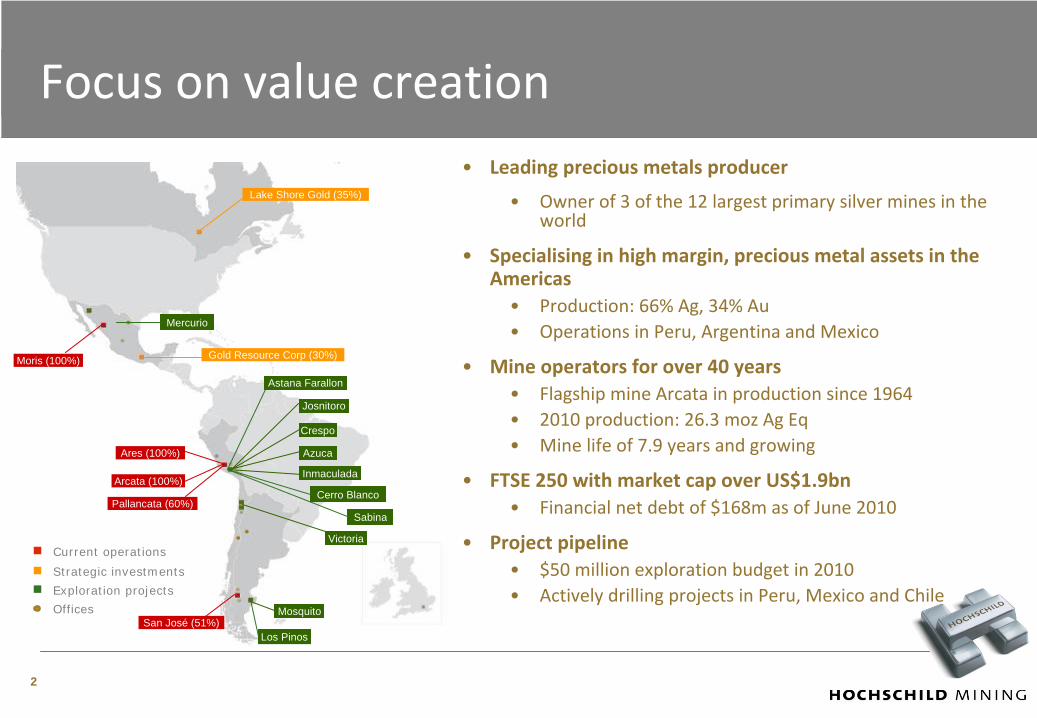

Lake Shore Gold (35%)

Gold Resource Corp (30%)Moris (100%)

Arcata (100%)

Ares (100%)

Pallancata (60%)

San José (51%)

Josnitoro

Crespo

Azuca

Inmaculada

Victoria

Mosquito

Current operations

Strategic investments

Exploration projects

Offices

Astana Farallon

Cerro Blanco

Los Pinos

Sabina

Mercurio

•

Leading precious metals producer

•

Owner of 3 of the 12 largest primary silver mines in the

world

•

Specialising in high margin, precious metal assets in the

Americas•

Production: 66% Ag, 34% Au•

Operations in Peru, Argentina and Mexico

•

Mine operators for over 40 years•

Flagship mine Arcata in production since 1964•

2010 production: 26.3 moz

Ag Eq•

Mine life of 7.9 years and growing

•

FTSE 250 with market cap over US$1.9bn•

Financial net debt of $168m as of June 2010

•

Project pipeline•

$50 million exploration budget in 2010•

Actively drilling projects in Peru, Mexico and Chile

Focus on value creation

3

Mission & Vision

“We

are

a

precious

metals

mining

company

focused

on

the Americas,

working

with

excellence,

social

responsibility

and

the

highest

environmental

and

safety

standards,

achieving

high profitability, sustained growth

and creating shareholder value”

MISSION

VISION

“Become

the

market

leader

in

shareholder

returns,

work environment and safety”

4

HOC social commitment Environment:

•

ISO 14001 Arcata certified. San Jose and Pallancata

to

achieve certification by 1Q11

•

Environmental Management Plan in operations and

projects

•

Constant monitoring through Critical Performance

Indicators

Safety:

•

DNV certification started in 2008, in process to

achieve Level 5 at Arcata, Pallancata

and San Jose

•

Frequency Index currently at 3.7

Community relations:

•

Programmes

focused on health, education and infant

nutrition with an annual US$10m budget

–

Mobile Hospital

–

Over 20 schools and 1,000 students supported

–

Alpaca genetic improvement program

•

Optimise

life of mine at main operations

•

Increase productivity

•

Cost control

‐

Arcata ‐

San José

‐

PallancataCore Assets

Exploration

Corporate Development

•

Fund exploration through largest ever budget

•

Maximise

economies of scale by targeting

opportunities within clusters

•

Strategic project pipeline

•

Focus on early stage projects with high geological

potential and clear path to control

Strategy ‐

pillars for growth

‐

Company

makers

‐

Company

maintainers

‐

Strategic

Investments

1

2

3

5

Current operationsARCATA, Peru SAN JOSÉ, ArgentinaPALLANCATA, Peru

ARES, Peru MORIS, Mexico

GRC, Mexico LAKE SHORE GOLD, Canada

Main operations

Smaller, ageing mines

Strategic investments

1

11.3 MOZ AG EQ 10.3 MOZ AG EQ 9.6 MOZ AG EQ

1.8 MOZ AG EQ3.5 MOZ AG EQ

•Production figures relate to full year 2009 and are based on 100% production • Lakeshore and GRC’s

production targets are based on public data and refer to 2011 (LSG) and the first 12 months of

production (GRC)

150 KOZ AU ‐

Target 70 KOZ AU ‐

Target

6

7

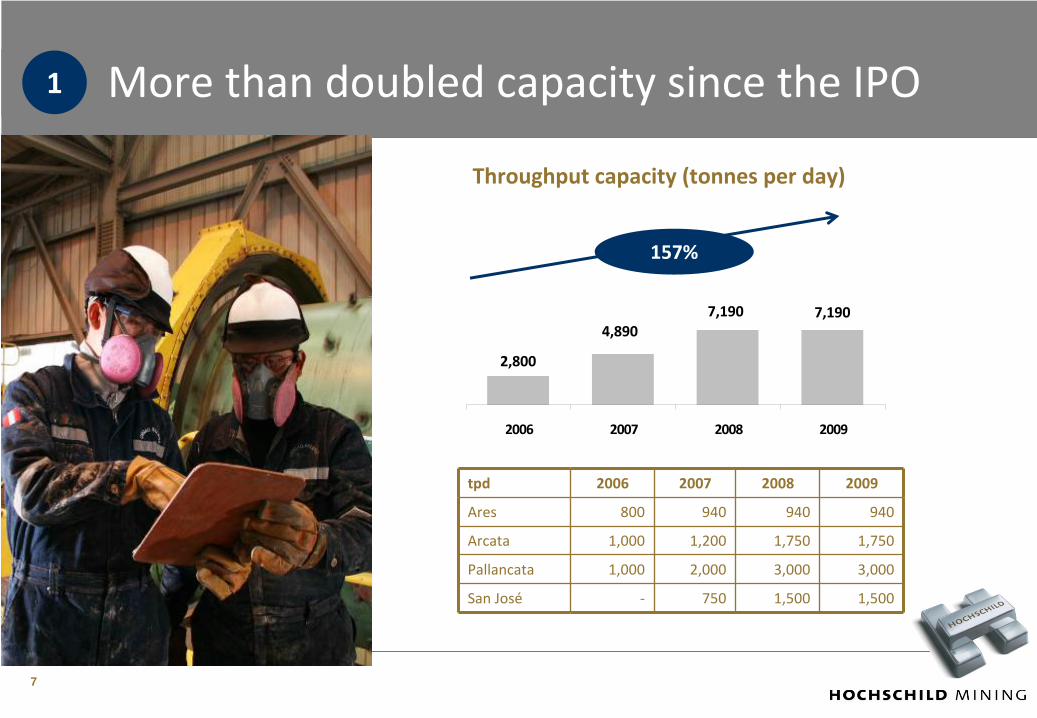

More than doubled capacity since the IPO1

2,800

4,8907,190 7,190

2006 2007 2008 2009

157%

tpd 2006 2007 2008 2009

Ares 800 940 940 940

Arcata 1,000 1,200 1,750 1,750

Pallancata 1,000 2,000 3,000 3,000

San José ‐ 750 1,500 1,500

Throughput capacity (tonnes

per day)

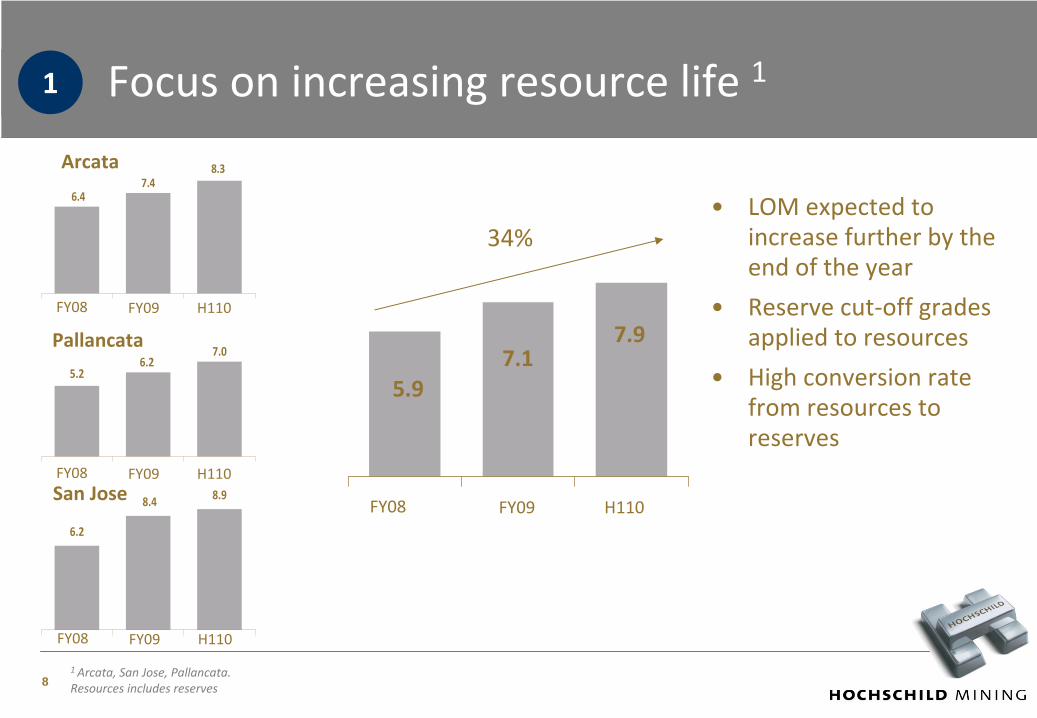

7.9

5.97.1

FY08 H110FY09

•

LOM expected to increase further by the

end of the year

•

Reserve cut‐off grades applied to resources

•

High conversion rate from resources to

reserves

7.0

5.26.2

8.9

6.2

8.4

Arcata

Pallancata

San Jose

34%

FY08 H110FY09

FY08 H110FY09

FY08 H110FY09

7.46.4

8.3

Focus on increasing resource life 11

81 Arcata, San Jose, Pallancata. Resources includes reserves

Exploration – existing strategy is successful

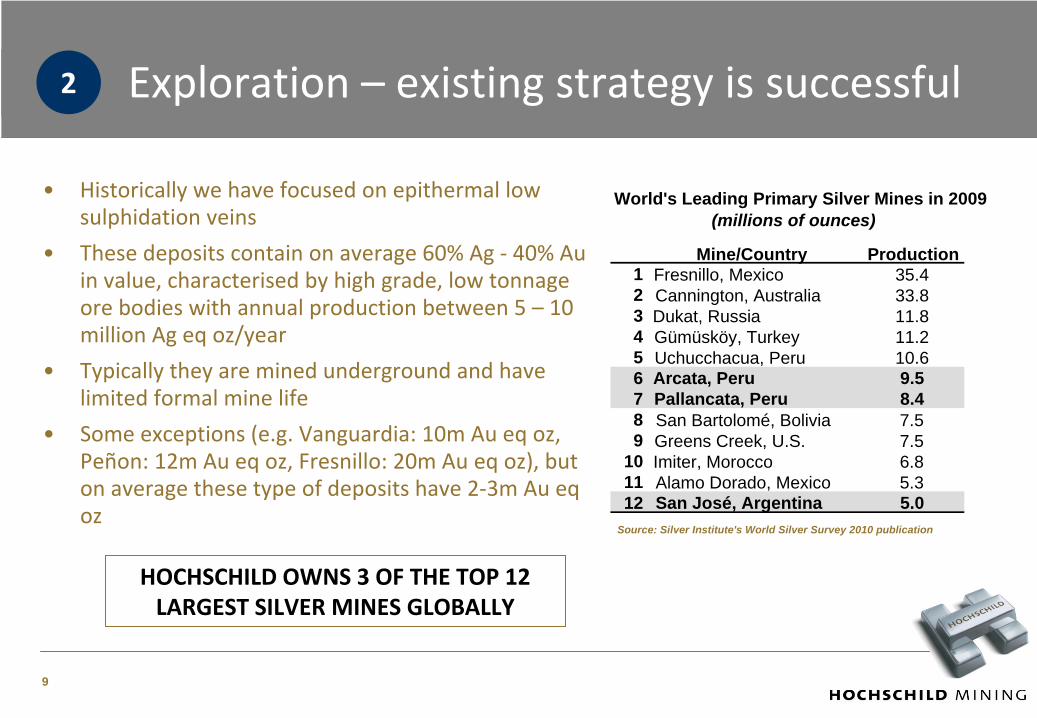

•

Historically we have focused on epithermal low

sulphidation veins

•

These deposits contain on average 60% Ag ‐

40% Au

in value, characterised

by high grade, low tonnage

ore bodies with annual production between 5 – 10

million Ag eq

oz/year

•

Typically they are mined underground and have

limited formal mine life

•

Some exceptions (e.g. Vanguardia: 10m Au eq

oz,

Peñon: 12m Au eq

oz, Fresnillo: 20m Au eq

oz), but

on average these type of deposits have 2‐3m Au eq

ozSource: Silver Institute's World Silver Survey 2010 publication

Mine/Country Production1 Fresnillo, Mexico 35.42 Cannington, Australia 33.83 Dukat, Russia 11.84 Gümüsköy, Turkey 11.25 Uchucchacua, Peru 10.66 Arcata, Peru 9.57 Pallancata, Peru 8.48 San Bartolomé, Bolivia 7.59 Greens Creek, U.S. 7.5

10 Imiter, Morocco 6.811 Alamo Dorado, Mexico 5.312 San José, Argentina 5.0

(millions of ounces)World's Leading Primary Silver Mines in 2009

2

HOCHSCHILD OWNS 3 OF THE TOP 12

LARGEST SILVER MINES GLOBALLY

9

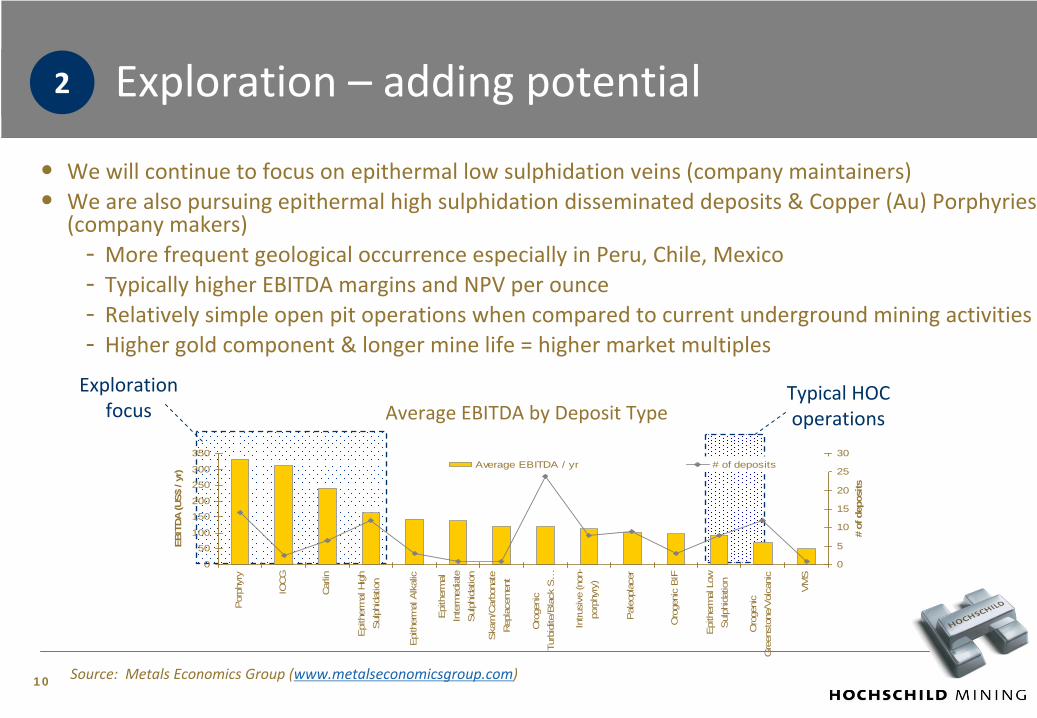

Exploration –

adding potential

•

We will continue to focus on epithermal low sulphidation veins (company maintainers)•

We are also pursuing epithermal high sulphidation disseminated deposits & Copper (Au) Porphyries

(company makers)‐

More frequent geological occurrence especially in Peru, Chile, Mexico

‐

Typically higher EBITDA margins and NPV per ounce‐

Relatively simple open pit operations when compared to current underground mining activities

‐

Higher gold component & longer mine life = higher market multiples

2

Average EBITDA by Deposit TypeExploration

focusTypical HOC

operations

0

50

100

150

200

250

300

350

Por

phyr

y

IOC

G

Car

lin

Epi

ther

mal

Hig

hS

ulph

idat

ion

Epi

ther

mal

Alk

alic

Epi

ther

mal

Inte

rmed

iate

Sul

phid

atio

n

Ska

rn/C

arbo

nate

Rep

lace

men

t

Oro

geni

cTu

rbid

ite/B

lack

S…

Intru

sive

(non

-po

rphy

ry)

Pal

eopl

acer

Oro

geni

c B

IF

Epi

ther

mal

Low

Sul

phid

atio

n

Oro

geni

cG

reen

ston

e/V

olca

nic

VM

S

EBIT

DA (U

S$ /

yr)

0

5

10

15

20

25

30

# of

dep

osits

Average EBITDA / yr # of deposits

Source: Metals Economics Group (www.metalseconomicsgroup.com)10

-

25

50

75

100

Sukh

ayba

rat

Kem

ess

Cen

tral

Pier

ina

Wha

rfAn

govi

aM

orila

Bron

zew

ing

Rub

y H

illLa

Coi

paC

orra

les

Ree

fton

Kals

aka

Bogo

so/P

res

Lega

Dem

biG

edab

ekLa

Lib

erta

d ItyBe

rezi

tovo

yeSa

n An

dres

C C

reek

-La

verto

nVo

roLe

fa C

orrid

orKu

mto

rBo

nikr

oLa

Her

radu

raEl

Cha

nate

Nor

th M

ara

El C

astill

oPe

njom

Cha

tree

Mar

icun

gaSo

leda

d-Sa

diol

a H

illSa

mira

Hill

Ahaf

oH

idde

nSi

guiri

Cha

pada

Bodd

ingt

onC

hoco

Nav

acha

bAn

daco

lloSu

kari

Mid

delv

eiM

aika

inzo

loto

Bere

znya

ki

Reserve LOM Resource LOM

-

25

50

75

100

Anta

pite

Ishi

huin

caM

arth

aSh

ila-P

aula

Dia

blito

San

Topi

aQ

uiru

vilc

aC

olom

bia

Ares

Julc

ani

Rec

uper

adM

ina

Palla

ncat

aPi

men

ton

Gua

naju

ato

Kettl

e R

-BEn

cant

ada

Pogo

Arca

taN

. Sen

ora

Gua

nace

viEl

Pen

onSa

n Jo

seG

uana

juat

o LaSa

n M

artin

Co-

OSi

lver

Zaru

ma

Cay

llom

aR

ossi

Troy

Min

eG

reen

sC

ubo-

La C

iene

gaSa

n D

imas

Mor

ococ

haFr

esni

lloH

uaro

nLu

cky

Bola

nos

Reserve LOM Resource LOM

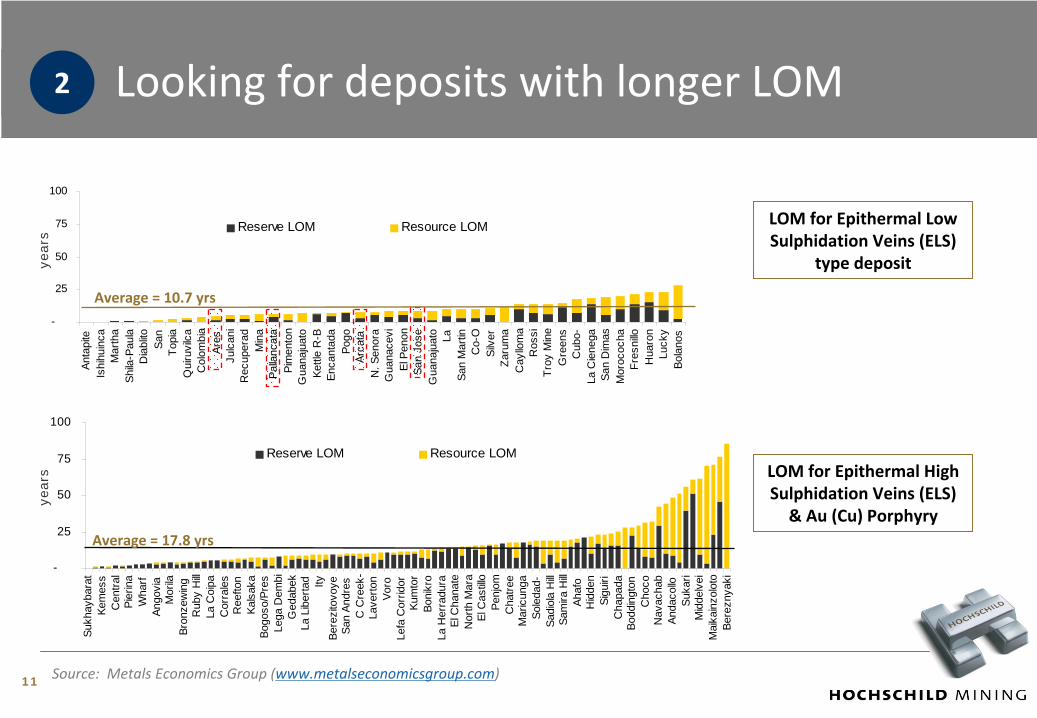

11

Average = 10.7 yrs

LOM for Epithermal Low

Sulphidation Veins (ELS)

type deposit

Average = 17.8 yrs

LOM for Epithermal High

Sulphidation Veins (ELS)

& Au (Cu) Porphyry

year

sye

ars

Source: Metals Economics Group (www.metalseconomicsgroup.com)

Looking for deposits with longer LOM 2

12

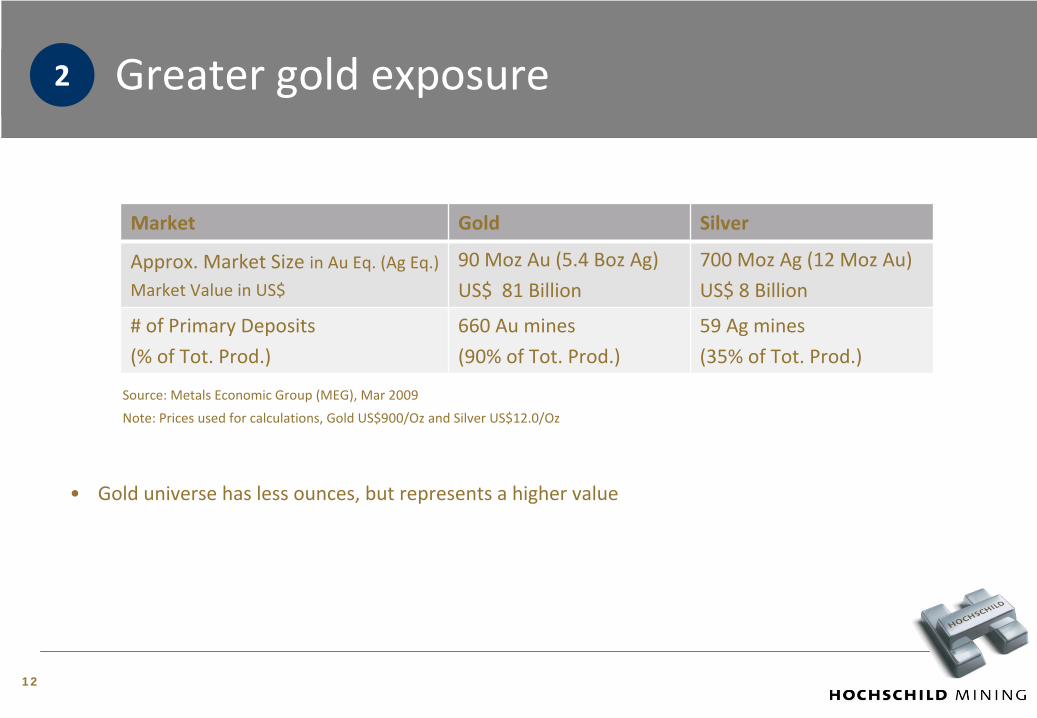

Market Gold Silver

Approx. Market Size in Au Eq. (Ag Eq.)Market Value in US$

90 Moz

Au (5.4 Boz

Ag)

US$ 81 Billion

700 Moz

Ag (12 Moz

Au)

US$ 8 Billion

# of Primary Deposits

(% of Tot. Prod.)

660 Au mines

(90% of Tot. Prod.)

59 Ag mines

(35% of Tot. Prod.)

•

Gold universe has less ounces, but represents a higher value

Source: Metals Economic Group (MEG), Mar 2009

Note: Prices used for calculations, Gold US$900/Oz and Silver US$12.0/Oz

Greater gold exposure2

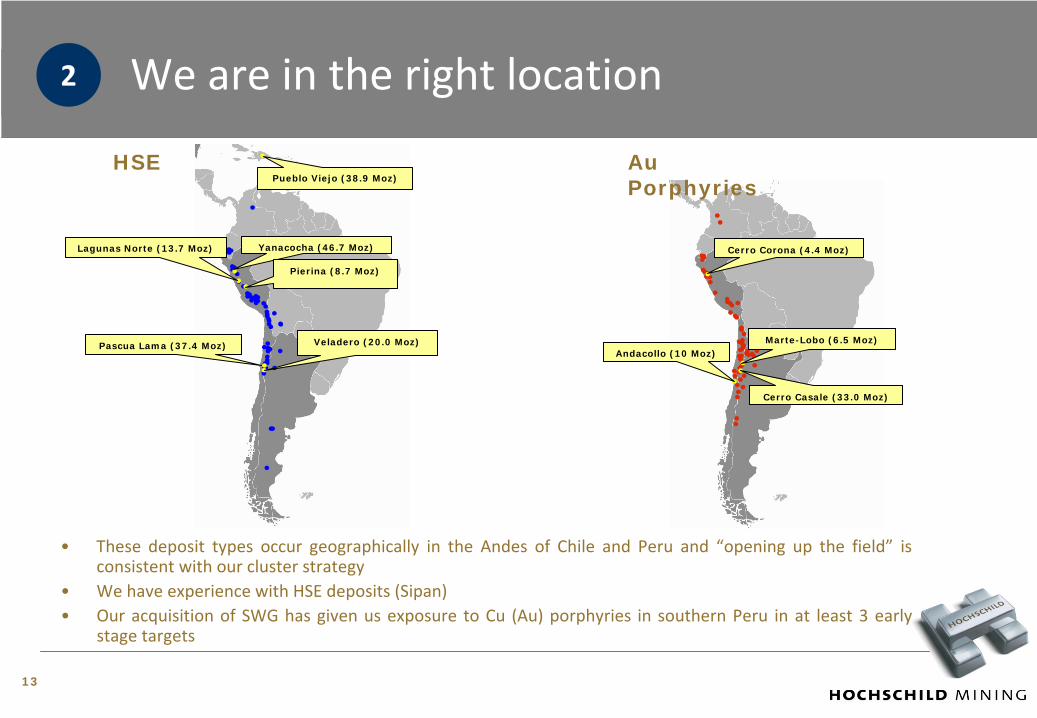

•

These

deposit

types

occur

geographically

in

the

Andes

of

Chile

and

Peru

and

“opening

up

the

field”

is

consistent with our cluster strategy

•

We have experience with HSE deposits (Sipan)•

Our

acquisition

of

SWG

has

given

us

exposure

to

Cu

(Au)

porphyries

in

southern

Peru

in

at

least

3

early

stage targets

We are in the right location

Au Porphyries

Cerro Corona (4.4 Moz)

Marte-Lobo (6.5 Moz)Andacollo (10 Moz)

Cerro Casale (33.0 Moz)

HSEPueblo Viejo (38.9 Moz)

Yanacocha (46.7 Moz)Lagunas Norte (13.7 Moz)

Pierina (8.7 Moz)

Pascua Lama (37.4 Moz) Veladero (20.0 Moz)

13

2

141414

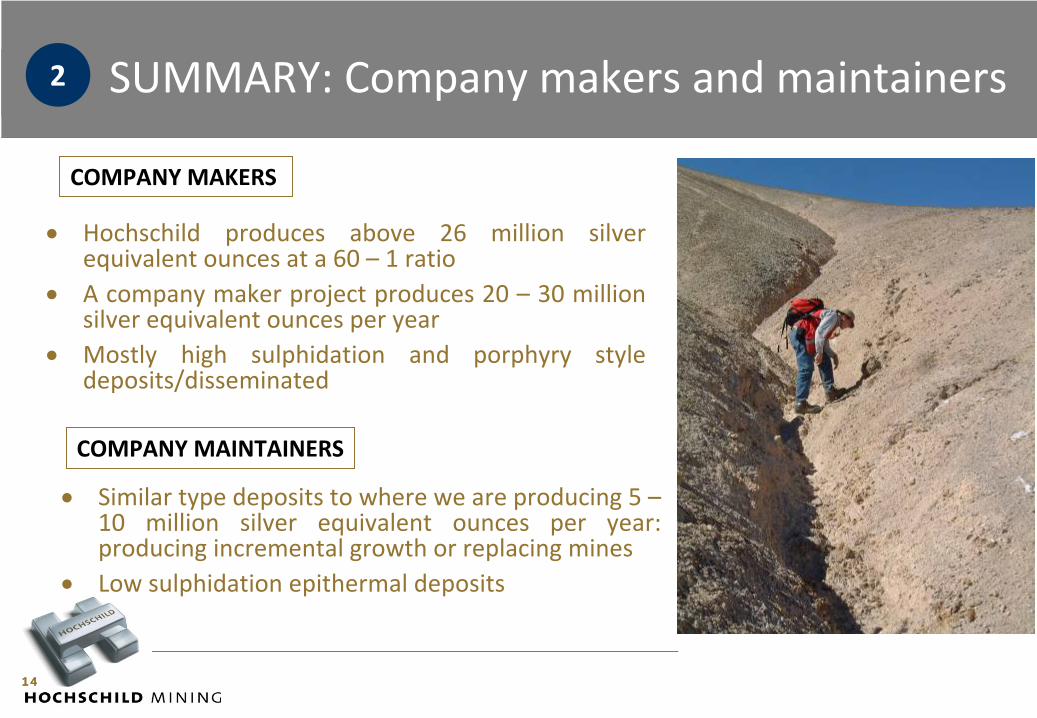

SUMMARY: Company makers and maintainers

•

Hochschild

produces

above

26

million

silver equivalent ounces at a 60 – 1 ratio

•

A company maker project produces 20 – 30 million silver equivalent ounces per year

•

Mostly

high

sulphidation

and

porphyry

style deposits/disseminated

COMPANY MAKERS

COMPANY MAINTAINERS

•

Similar type deposits to where we are producing 5 – 10

million

silver

equivalent

ounces

per

year:

producing incremental growth or replacing mines•

Low sulphidation epithermal deposits

2

1515

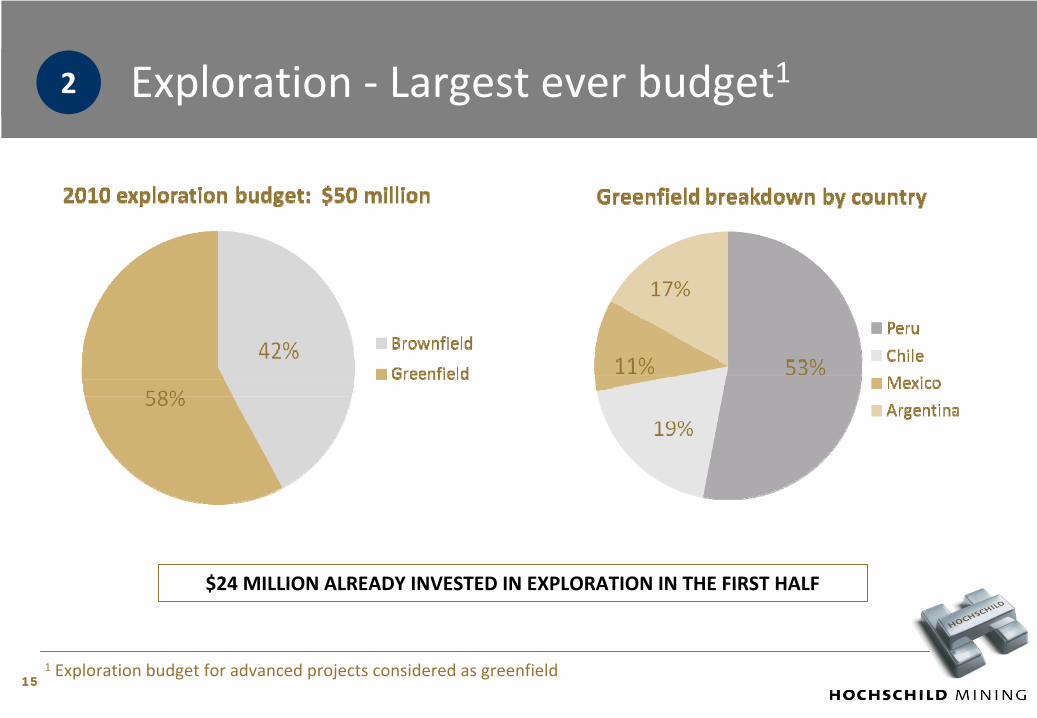

Exploration ‐

Largest ever budget12

$24 MILLION ALREADY INVESTED IN EXPLORATION IN THE FIRST HALF

1

Exploration

budget

for

advanced

projects

considered

as greenfield

16

Greenfield

•

27

geologists

who

collectively

hold 15 postgraduate degrees

•

23

support

staff

to

ensure

our

geologists focus on exploration

Brownfield

•

40

geologists

who

collectively

hold 10 postgraduate degrees

•

8

support

staff

to

ensure

our

geologists focus on exploration

A solid team2

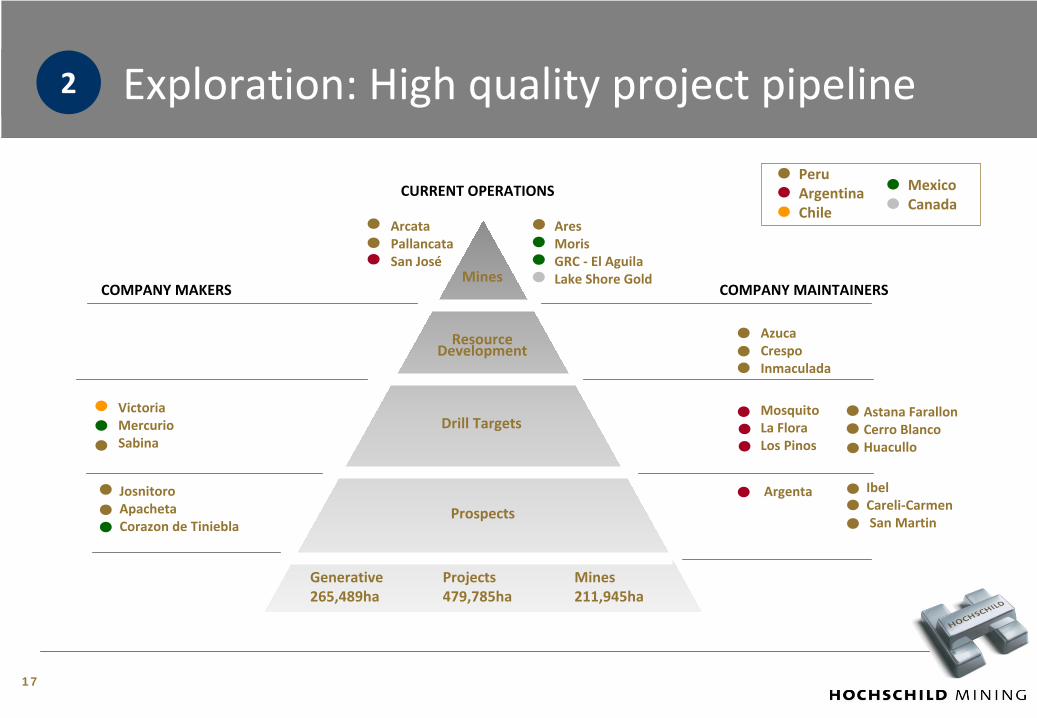

Exploration: High quality project pipeline

JosnitoroApachetaCorazon de Tiniebla

IbelCareli‐CarmenSan Martin

CURRENT OPERATIONS

ArcataPallancataSan José

VictoriaMercurioSabina

Projects479,785ha

Prospects

Drill Targets

Resource

Development

Mines

AresMorisGRC ‐

El AguilaLake Shore Gold

COMPANY MAINTAINERS

AzucaCrespoInmaculada

MosquitoLa FloraLos Pinos

Astana FarallonCerro BlancoHuacullo

COMPANY MAKERS

Argenta

PeruArgentinaChile

MexicoCanada

Mines211,945ha

Generative265,489ha

2

17

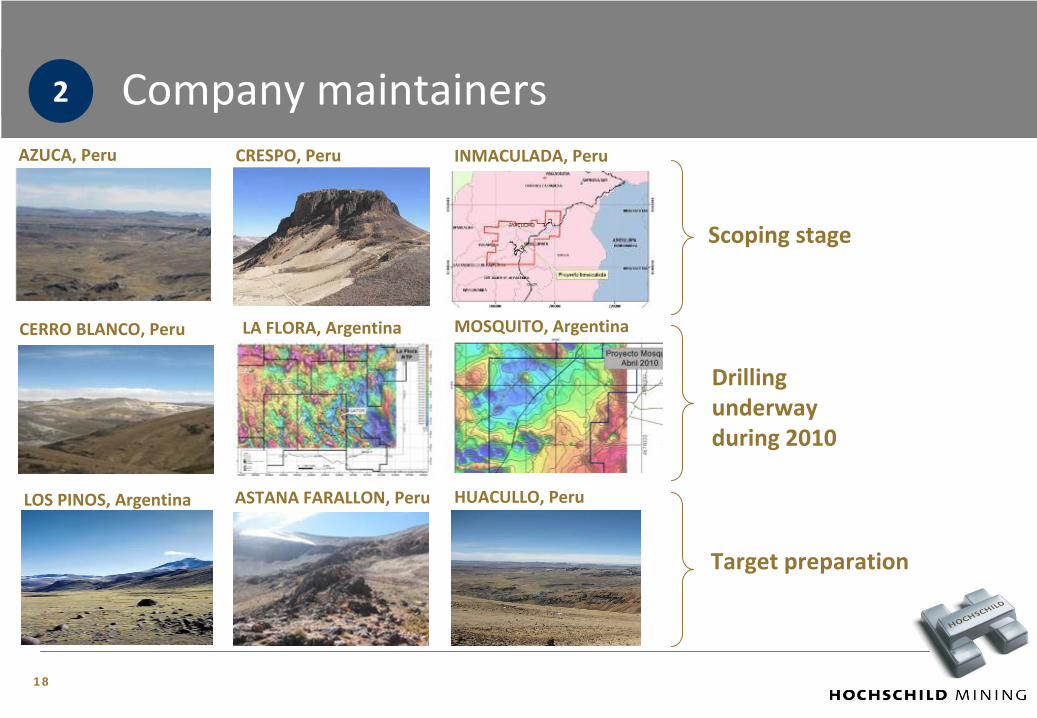

Company maintainers AZUCA, Peru CRESPO, Peru

MOSQUITO, Argentina

INMACULADA, Peru

Scoping stage

2

LA FLORA, Argentina

ASTANA FARALLON, Peru

CERRO BLANCO, Peru

Drilling underwayduring 2010

Target preparation

18

LOS PINOS, Argentina HUACULLO, Peru

1919

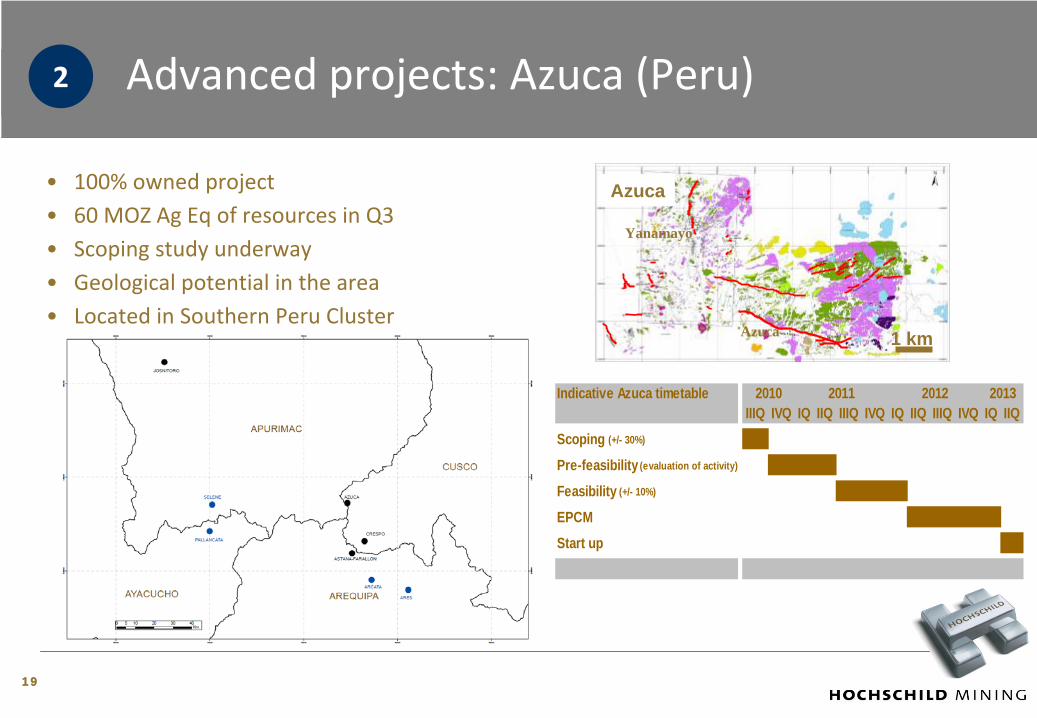

•

100% owned project

•

60 MOZ Ag Eq

of resources in Q3

•

Scoping study underway

•

Geological potential in the area

•

Located in Southern Peru Cluster

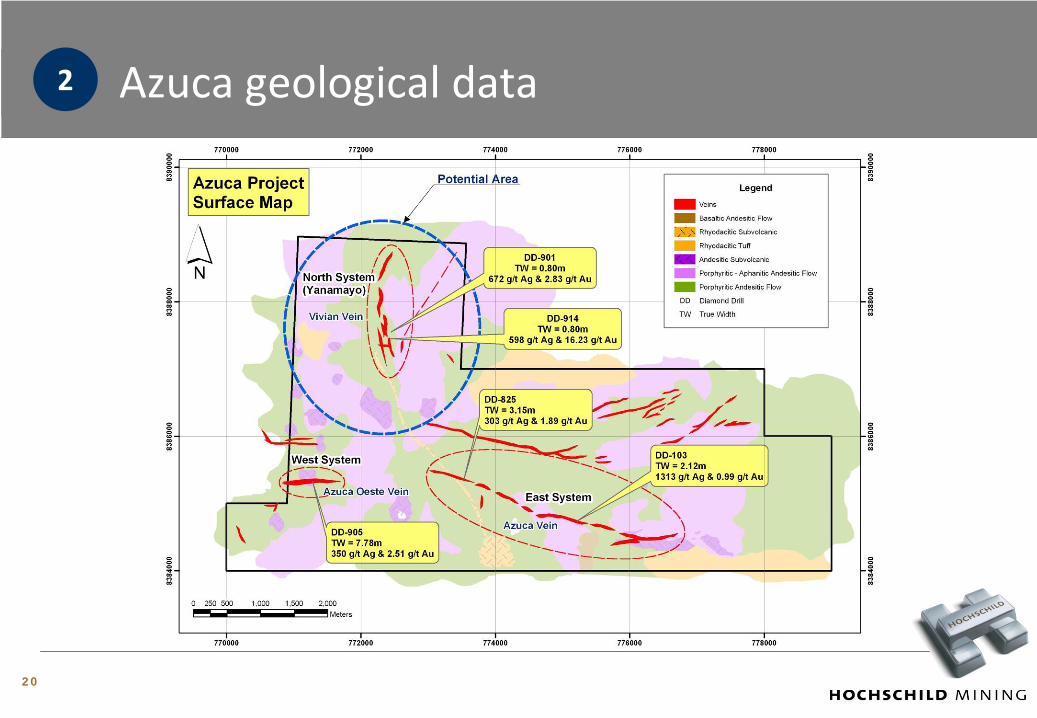

Advanced projects: Azuca

(Peru)

1 km

Azuca

Azuca

Yanamayo

2

Indicative Azuca timetable 2010 2011 2012 2013IIIQ IVQ IQ IIQ IIIQ IVQ IQ IIQ IIIQ IVQ IQ IIQ

Scoping (+/- 30%)

Pre-feasibility (evaluation of activity)

Feasibility (+/- 10%)

EPCMStart up

20

Azuca

geological data2

21

•

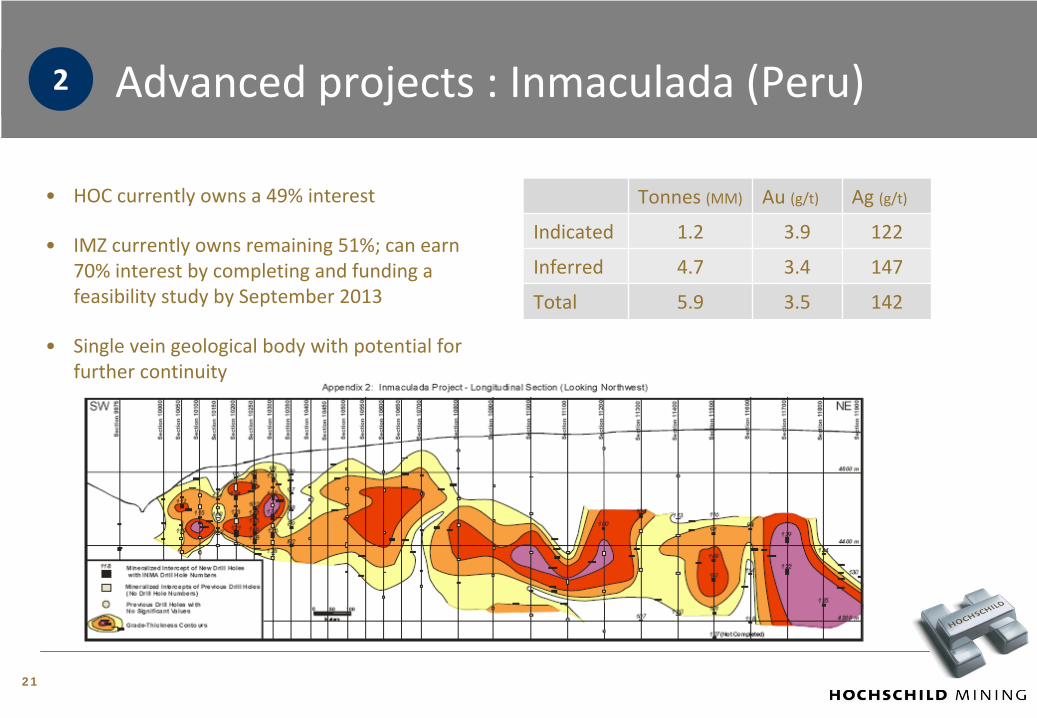

HOC currently owns a 49% interest

•

IMZ currently owns remaining 51%; can earn

70% interest by completing and funding a

feasibility study by September 2013

•

Single vein geological body with potential for

further continuity

Tonnes

(MM) Au (g/t) Ag (g/t)

Indicated 1.2 3.9 122

Inferred 4.7 3.4 147

Total 5.9 3.5 142

Advanced projects : Inmaculada

(Peru)2

Company makers

MERCURIO, Mexico SABINA, Peru VICTORIA, Chile

Drilling in progress

2

JOSNITORO, Peru CORAZON DE TINIEBLAS, Mexico APACHETA, Peru

Permits and

approvals underway

Mercur io

Sombrerete

Fresnillo

22

101.9m @ 0.91g/t Au , 57 g/t Ag102m @ 0.43 g/t Au, 34 g/t Ag

0 250 500m

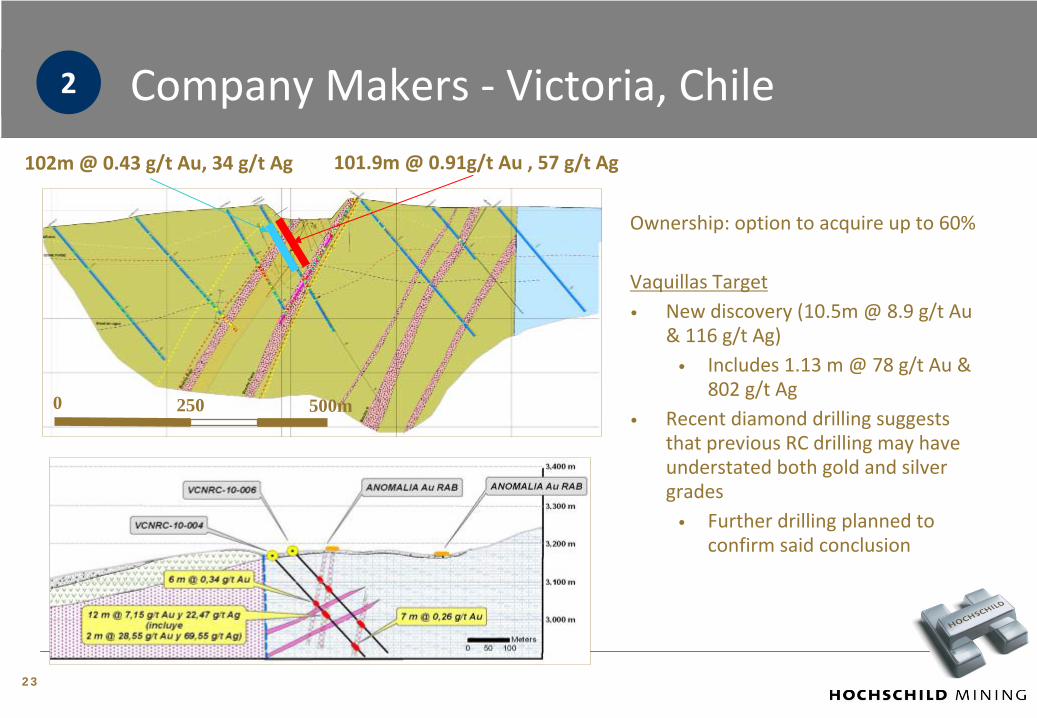

Company Makers ‐

Victoria, Chile

Ownership: option to acquire up to 60%

Vaquillas

Target•

New discovery (10.5m @ 8.9 g/t

Au

& 116 g/t

Ag)•

Includes 1.13 m @ 78 g/t

Au &

802 g/t

Ag•

Recent diamond drilling suggests

that previous RC drilling may have

understated both gold and silver

grades•

Further drilling planned to

confirm said conclusion

2

23

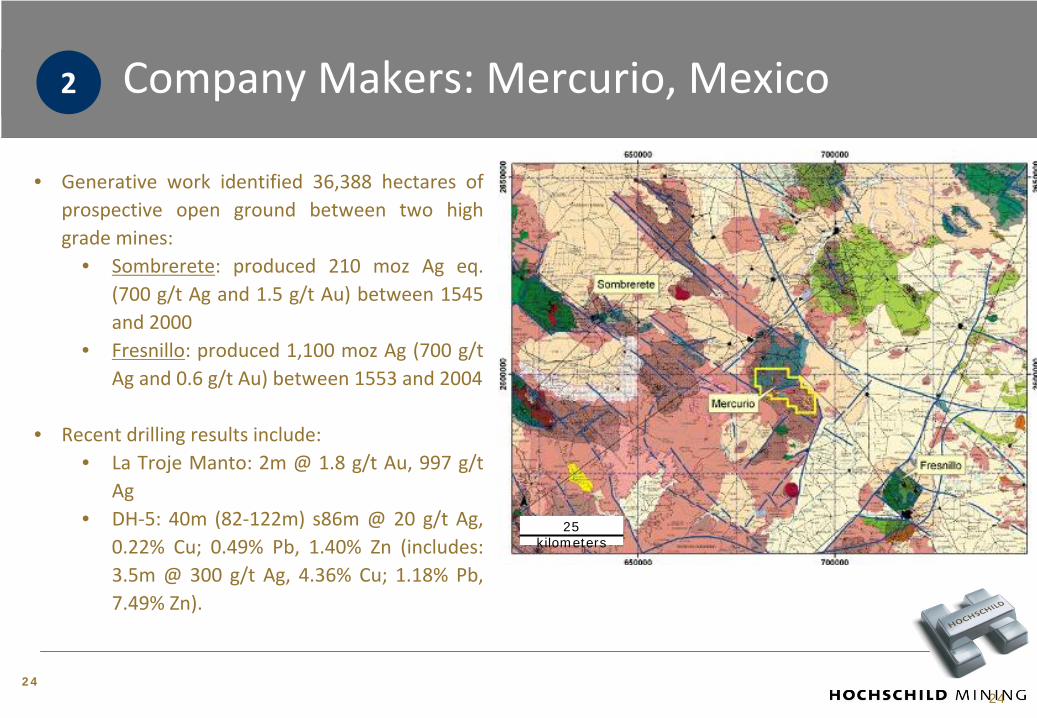

Company Makers: Mercurio, Mexico

24

2

24

• Generative

work

identified

36,388

hectares

of

prospective

open

ground

between

two

high

grade mines:• Sombrerete:

produced

210

moz

Ag

eq.

(700

g/t

Ag and

1.5

g/t

Au)

between

1545

and 2000 • Fresnillo:

produced

1,100

moz

Ag

(700

g/t

Ag and 0.6 g/t

Au) between 1553 and 2004

• Recent drilling results include:• La

Troje

Manto:

2m

@

1.8

g/t

Au,

997

g/t

Ag• DH‐5:

40m

(82‐122m)

s86m

@

20

g/t

Ag,

0.22%

Cu;

0.49%

Pb,

1.40%

Zn

(includes:

3.5m

@

300

g/t

Ag,

4.36%

Cu;

1.18%

Pb,

7.49% Zn).

25 kilometers

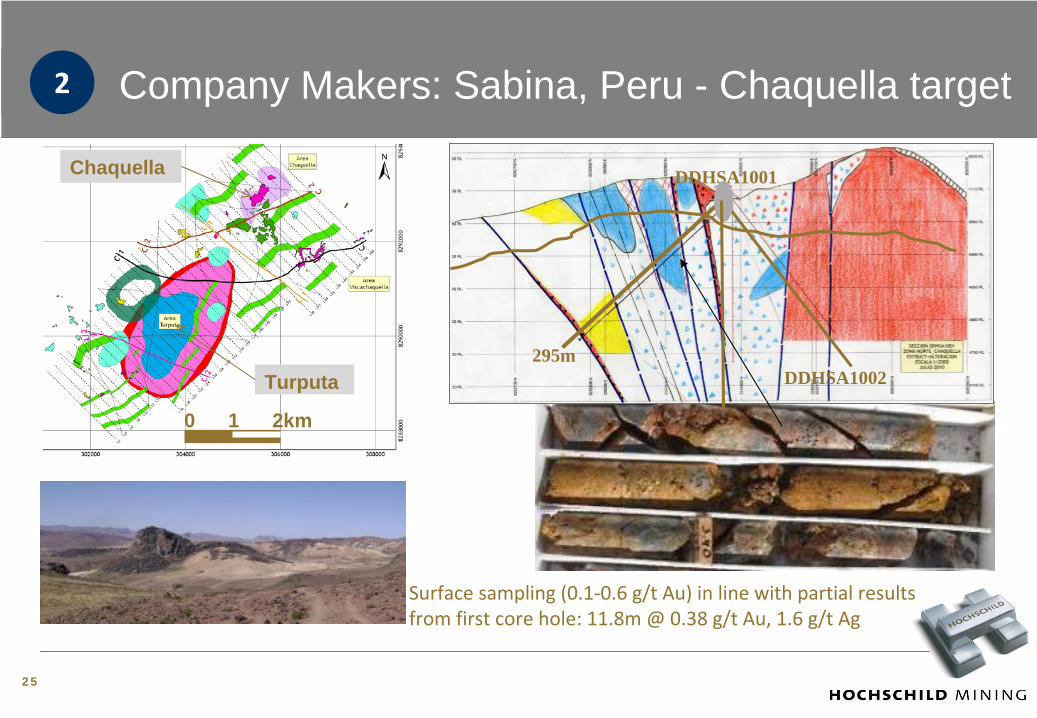

Company Makers: Sabina, Peru - Chaquella target

Surface sampling (0.1‐0.6 g/t

Au) in line with partial results

from first core hole: 11.8m @ 0.38 g/t

Au, 1.6 g/t

Ag

295m

DDHSA1001

DDHSA1002

Chaquella

Turputa

0 1 2km

2

25

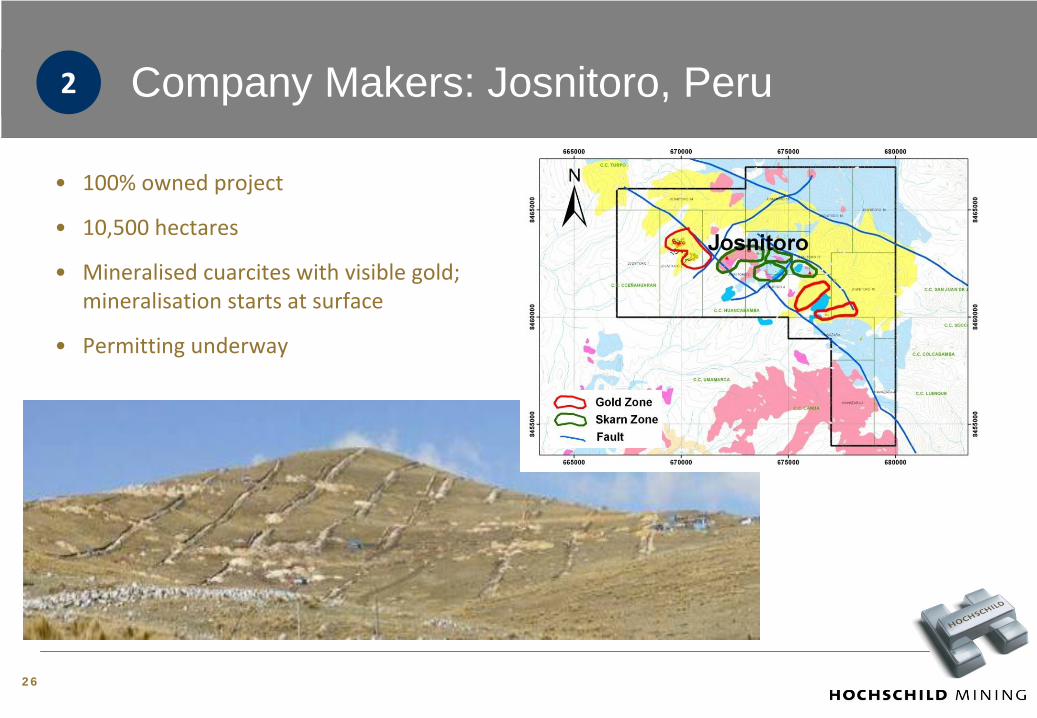

Company Makers: Josnitoro, Peru2

26

•

100% owned project

•

10,500 hectares

•

Mineralised cuarcites

with visible gold;

mineralisation starts at surface

•

Permitting underway

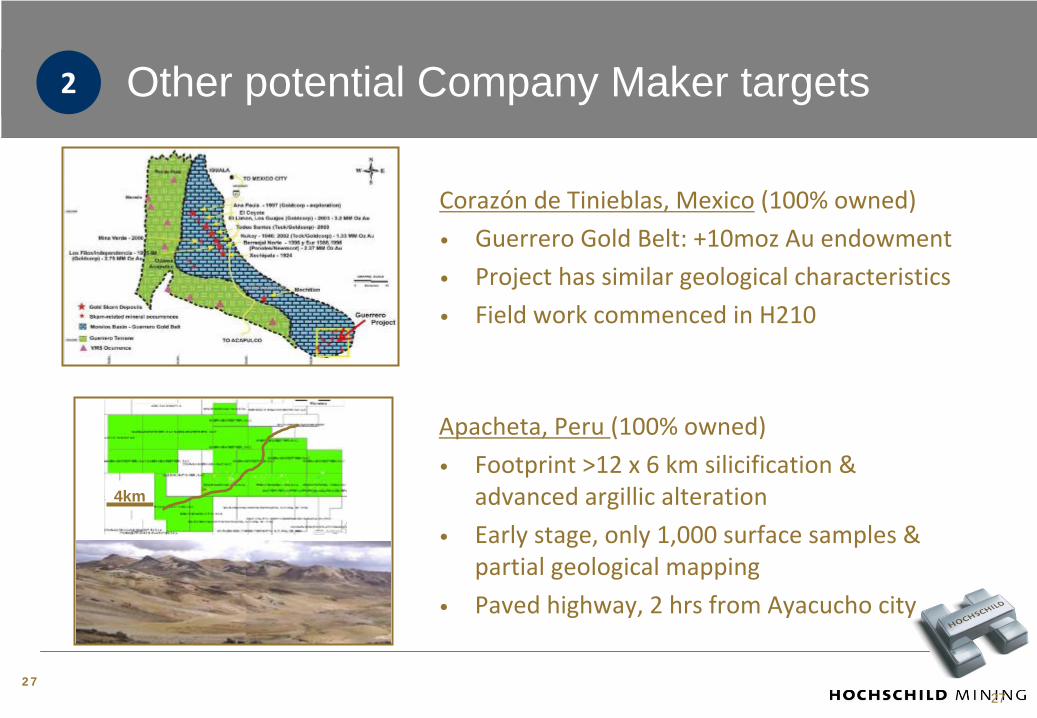

Other potential Company Maker targets

27

Corazón

de Tinieblas, Mexico

(100% owned)

•

Guerrero Gold Belt: +10moz Au endowment

•

Project has similar geological characteristics

•

Field work commenced in H210

Apacheta, Peru (100% owned)

•

Footprint >12 x 6 km silicification

& advanced argillic

alteration

•

Early stage, only 1,000 surface samples & partial geological mapping

•

Paved highway, 2 hrs from Ayacucho city

4km

2

27

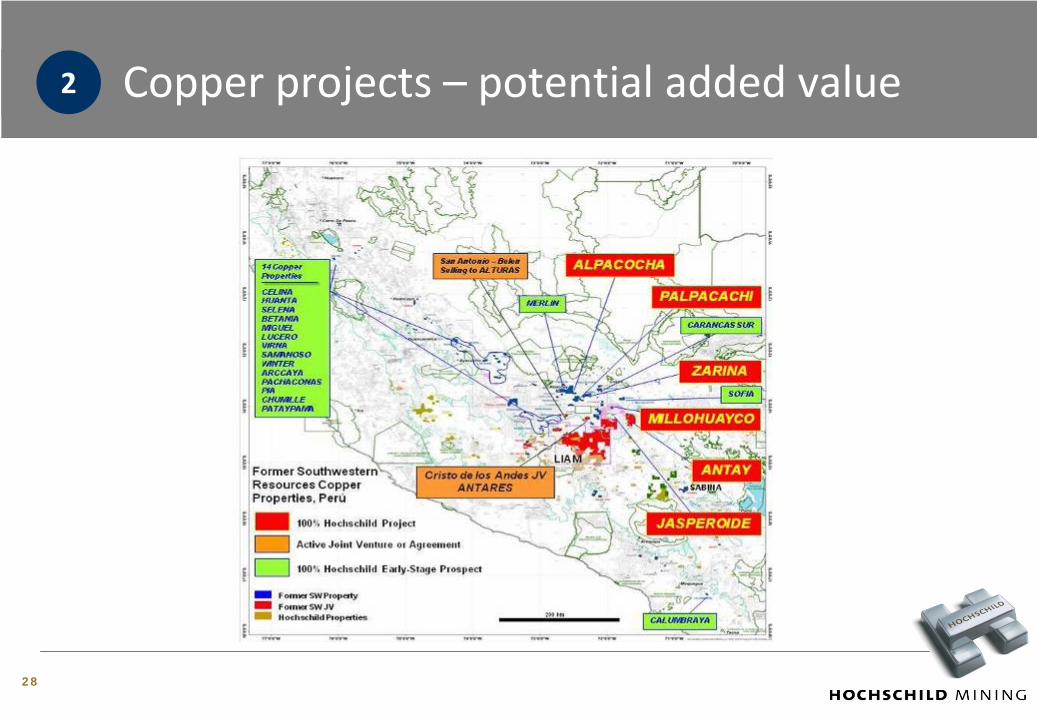

Copper projects –

potential added value

28

2

29

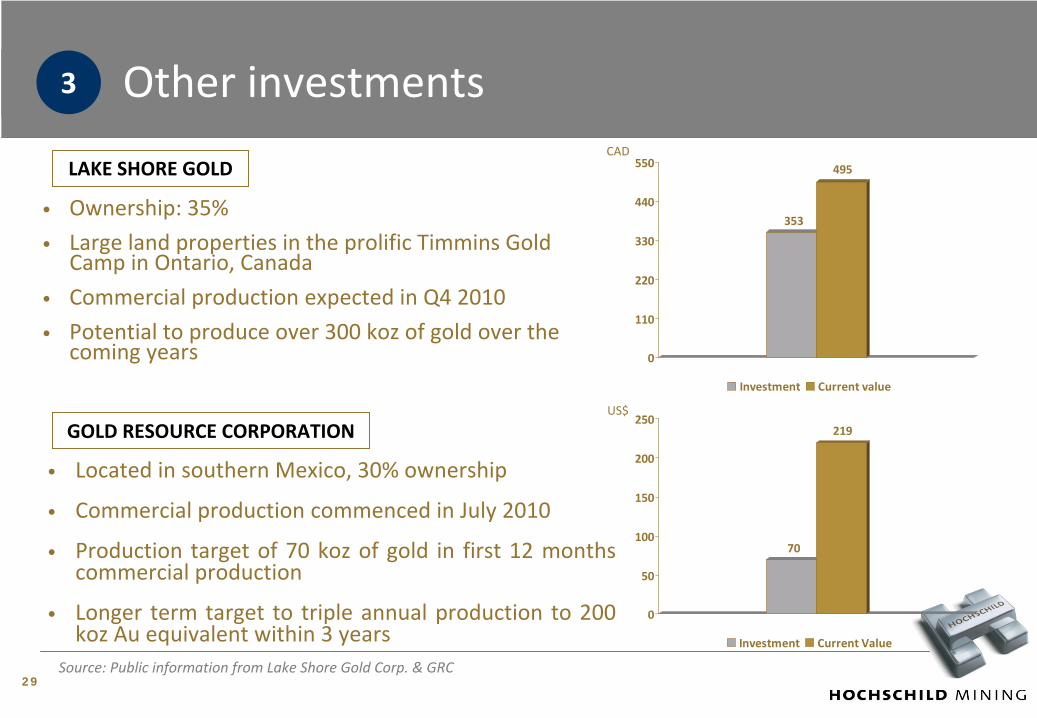

•

Ownership: 35%

•

Large land properties in the prolific Timmins Gold

Camp in Ontario, Canada

•

Commercial production expected in Q4 2010

•

Potential to produce over 300 koz

of gold over the

coming years

Source: Public information from Lake Shore Gold Corp. & GRC

Other investments 3

•

Located in southern Mexico, 30% ownership

•

Commercial production commenced in July 2010

•

Production

target

of

70

koz

of

gold

in

first

12

months

commercial production

•

Longer

term

target

to

triple

annual

production

to

200

koz

Au equivalent within 3 years

LAKE SHORE GOLD

GOLD RESOURCE CORPORATION

353

495

0

110

220

330

440

550

Investment Current value

70

219

0

50

100

150

200

250

Investment Current Value

CAD

US$

30

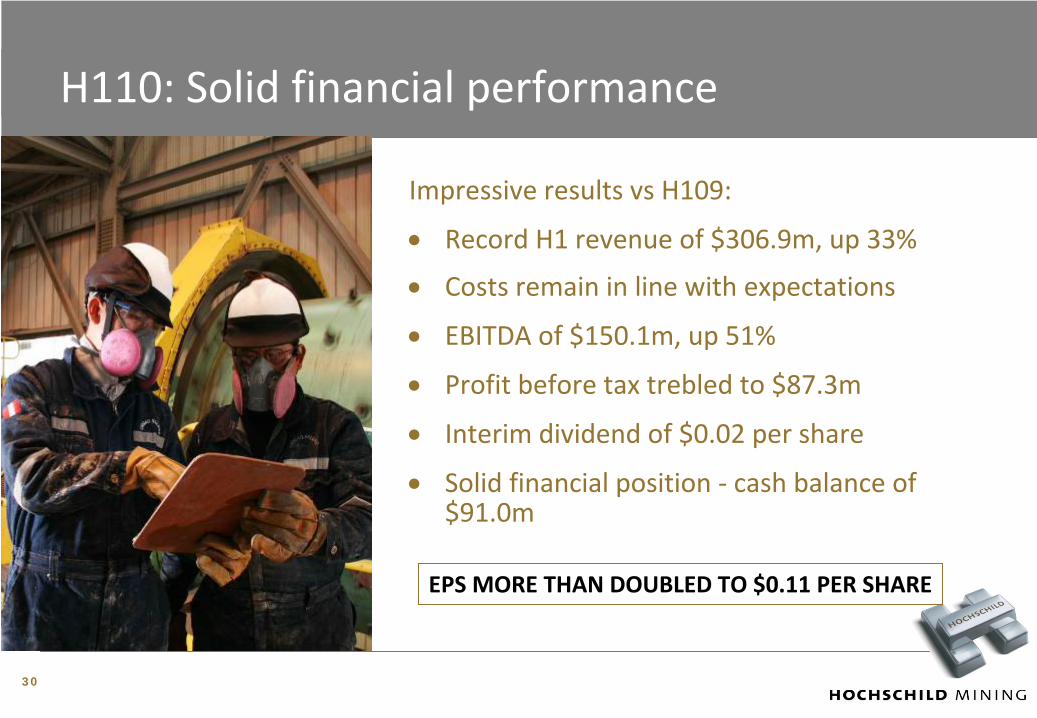

H110: Solid financial performance

Impressive results vs

H109:

•

Record H1 revenue of $306.9m, up 33%

•

Costs remain in line with expectations

•

EBITDA of $150.1m, up 51%

•

Profit before tax trebled to $87.3m

•

Interim dividend of $0.02 per share

•

Solid financial position ‐

cash balance of $91.0m

EPS MORE THAN DOUBLED TO $0.11 PER SHARE

3131

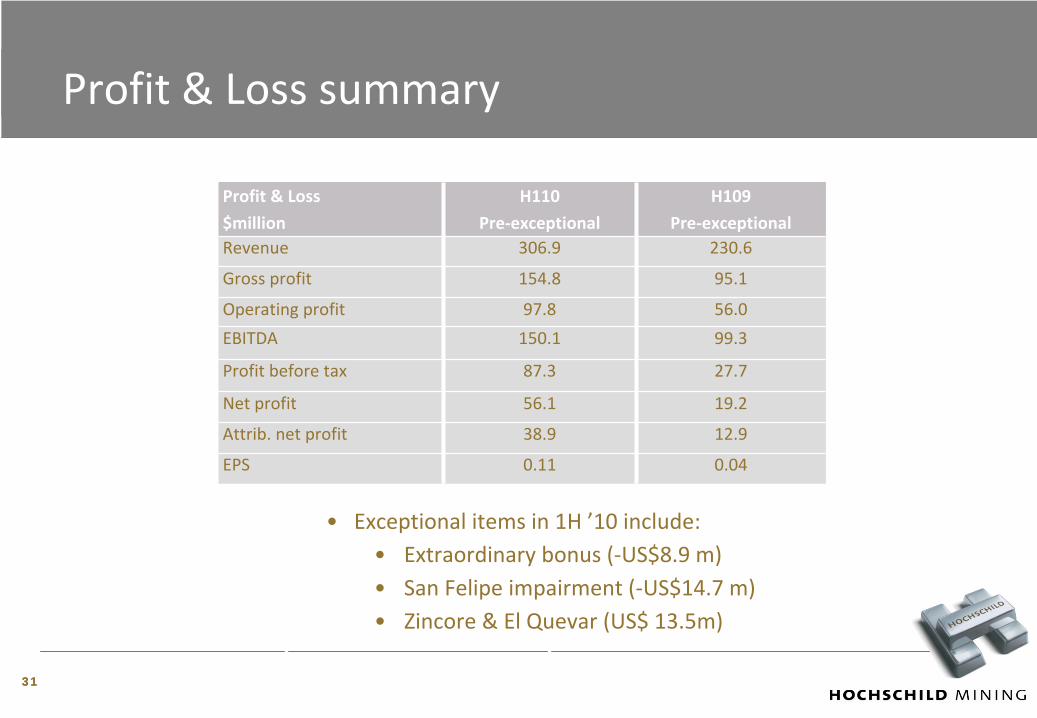

Profit & Loss summary

Profit & Loss

$million

H110

Pre‐exceptional

H109

Pre‐exceptionalRevenue 306.9 230.6

Gross profit 154.8 95.1

Operating profit 97.8 56.0

EBITDA 150.1 99.3

Profit before tax 87.3 27.7

Net profit 56.1 19.2

Attrib. net profit 38.9 12.9

EPS 0.11 0.04

•

Exceptional items in 1H ’10 include:•

Extraordinary bonus (‐US$8.9 m)

•

San Felipe impairment (‐US$14.7 m)

•

Zincore

& El Quevar

(US$ 13.5m)

3232

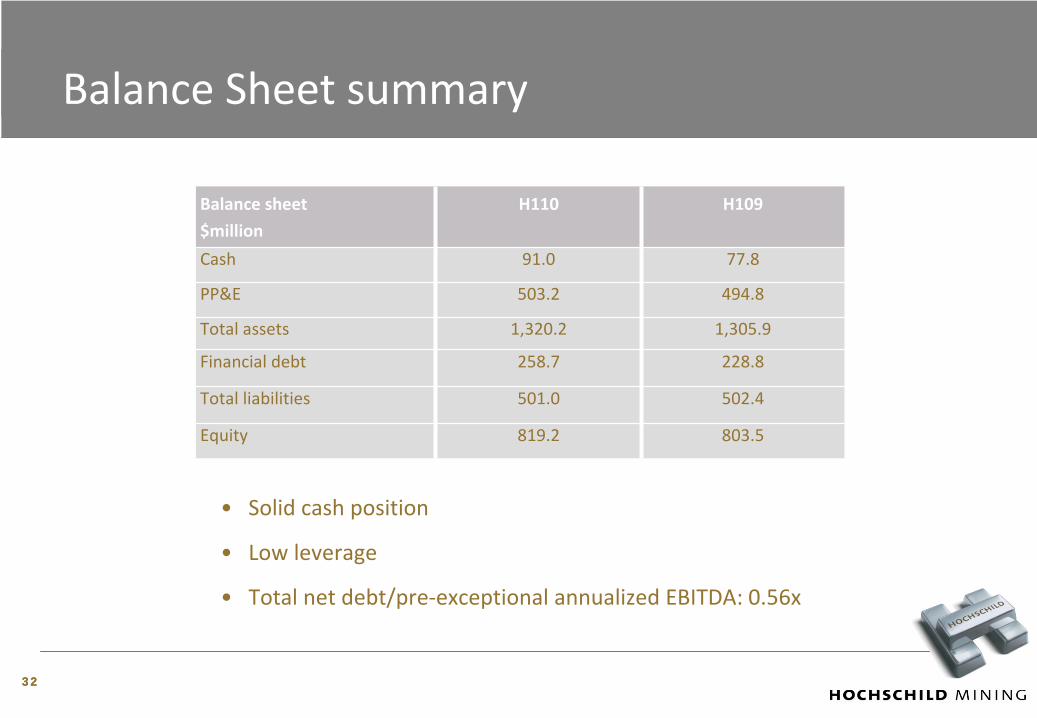

Balance Sheet summary

Balance sheet

$million

H110 H109

Cash 91.0 77.8

PP&E 503.2 494.8

Total assets 1,320.2 1,305.9

Financial debt 258.7 228.8

Total liabilities 501.0 502.4

Equity 819.2 803.5

•

Solid cash position

•

Low leverage

•

Total net debt/pre‐exceptional annualized EBITDA: 0.56x

High potential for value creation

•

LOM increased by 34% since 2009

•

Azuca

approaching pre‐feasibility stage

•

Robust project pipeline in premium mining locations

•

Strategic investments delivering shareholder value

•

Impressive financial results and solid balance sheet

•

Strong precious metals prices

33

34

Appendix

CONTACT US

Isabel Lutgendorf

Head of Investor Relations

+44 207 907 2934

![Hochschild (co)homology and Koszul duality - arXiv · 2015. 12. 8. · arXiv:1405.2247v2 [math.KT] 6 Dec 2015 Hochschild (co)homology and Koszul duality Estanislao Herscovich ∗](https://img.dokumen.tips/doc/110x75/60bce131fe07f4245000d5a2/hochschild-cohomology-and-koszul-duality-arxiv-2015-12-8-arxiv14052247v2.jpg)