Embed Size (px)

DESCRIPTION

Harnessing the Potential of Digital in Financial Services. Stephen Phillips September 23, 2013. Harnessing the potential of Digital in Financial Services. Context and perspective. Leading Digital practice. Organising for success. Consumers will be more connected with more devices. - PowerPoint PPT Presentation

Citation preview

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent

Harnessing the Potential of Digital in Financial Services

Stephen PhillipsSeptember 23, 2013

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 2130916-Belgium Finance Conference v5STK

Context and perspective

Leading Digital practice

Organisingfor success

Harnessing the potential of Digital in Financial Services

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 3130916-Belgium Finance Conference v5STK

0

20

40

60

80

100%

Broadband internet subscriptions

( % of households )

EU

BRIC

USA

Japan

00 02 04 06 08 10 12 14 16 18 20

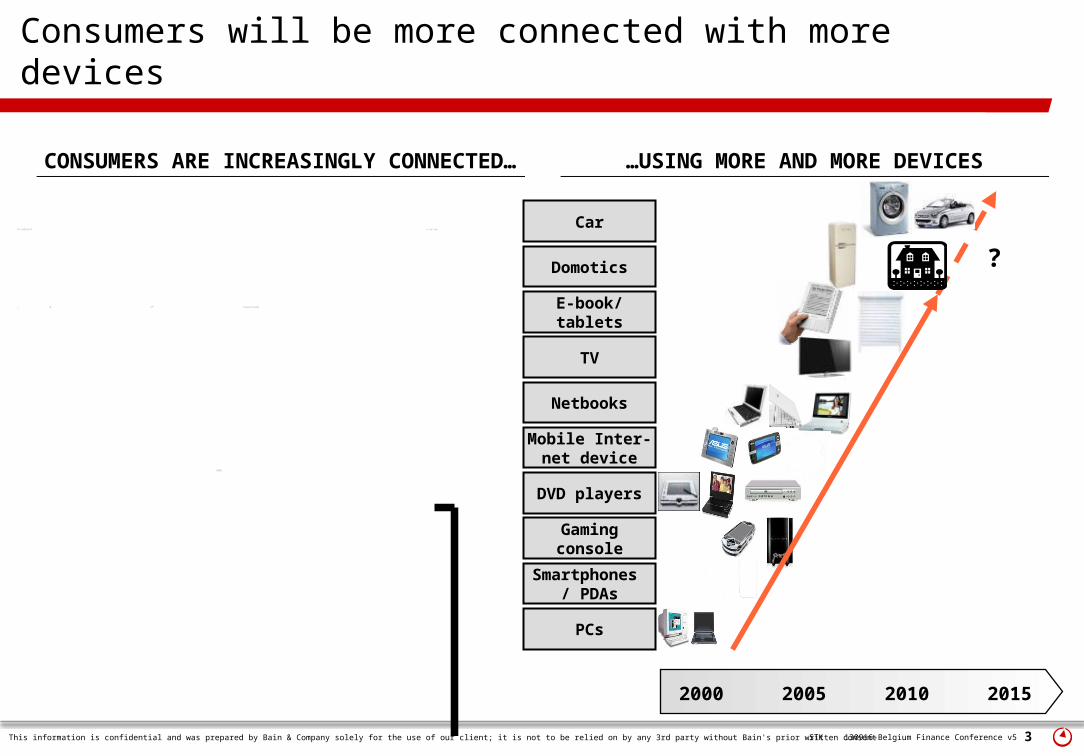

Consumers will be more connected with more devices

2000 2005 2010 2015

PCs

Smartphones / PDAs

Netbooks

Gaming console

TV

Mobile Inter-net device

Car

DVD players

Domotics ?E-book/ tablets

CONSUMERS ARE INCREASINGLY CONNECTED… …USING MORE AND MORE DEVICES

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 4130916-Belgium Finance Conference v5STK

0

20

40

60

80

100%

2002

65

2008

75

2014E

Trad

ition

al

med

ia

Online

media

83

Share of weekly per capita media

consumption ( hours/week )

-1%

10%

( 08-14 )

CAGR

0

1

2

3

4B

2004 2005 2006 2007 2008 2009 2010

Total time spent online in US

(hours/month )

Social media

Search

Content

Communications

Commerce

10%

6%

19%

21%

222%

( 04-09 )

CAGR

ONLINE WILL CONTINUE TO TAKE SHARETOTAL TIME SPENT ON SOCIAL MEDIA

HAS INCREASED DRAMATICALLY

The shift “online” is pronounced, particularly time spent using social media

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 5130916-Belgium Finance Conference v5STK

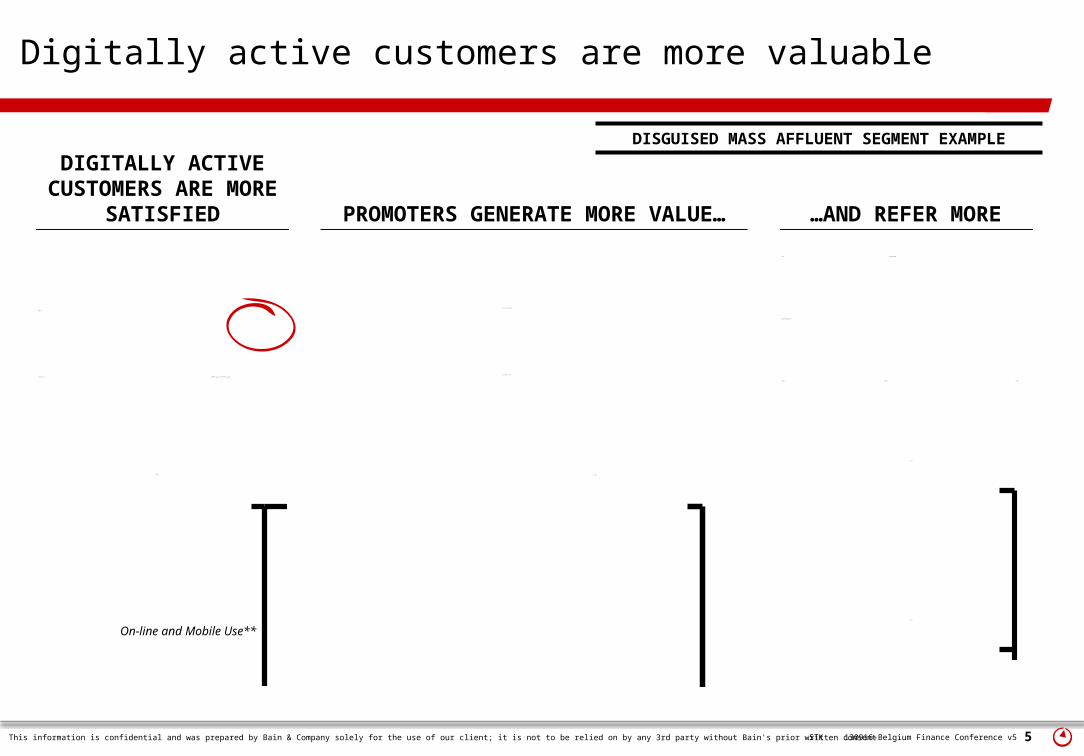

Digitally active customers are more valuable

-40

-30

-20

-10

0%

-36

-21

-12

-2

NPS

(Mass affluent/Affluent )*

None Low Med High

On-line and Mobile Use**

DIGITALLY ACTIVE CUSTOMERS ARE MORE SATISFIED

PROMOTERS GENERATE MORE VALUE…

-2.0

-1.0

0.0

1.0

2.0

Annual

revenue

100

94

78

Revenue

growth

rate

100

-16

-86

Defection

rate

100

88

151

Customer characteristics by NPS score,

indexed to promoter

…AND REFER MORE

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

Net average number of

referrals/ discouragements

per year per customer

Promoter

1.7

0.7

Detractor

-2.9

Passive

DISGUISED MASS AFFLUENT SEGMENT EXAMPLE

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 6130916-Belgium Finance Conference v5STK

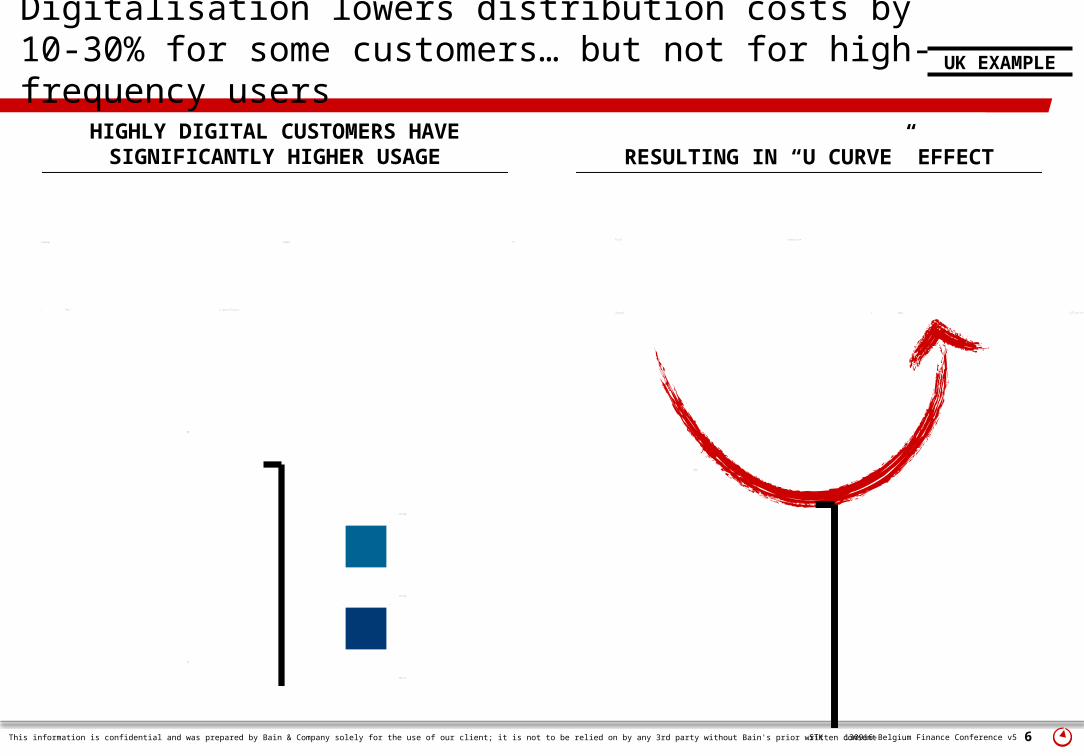

RESULTING IN “U CURVE” EFFECT

Digitalisation lowers distribution costs by 10-30% for some customers… but not for high-frequency users

0

50

100

150

None

100

Low

71

Medium

89

High

136

Total transaction cost by distribution

channel ( Mass affluent/Affluent*; indexed )

0

15

30

45

60

75

90

No digital

17

Low

18

Medium

33

High

88

74% 70% 69% 67%

Average number of uses of channel per quarter

( Mass affluent/Affluent )

Branch ( Transaction )

Branch ( Sales/ Service )

ATM

Phone

Mobile

Online ( Transaction )

Online ( Other )

HIGHLY DIGITAL CUSTOMERS HAVE SIGNIFICANTLY HIGHER USAGE

UK EXAMPLE

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 7130916-Belgium Finance Conference v5STK

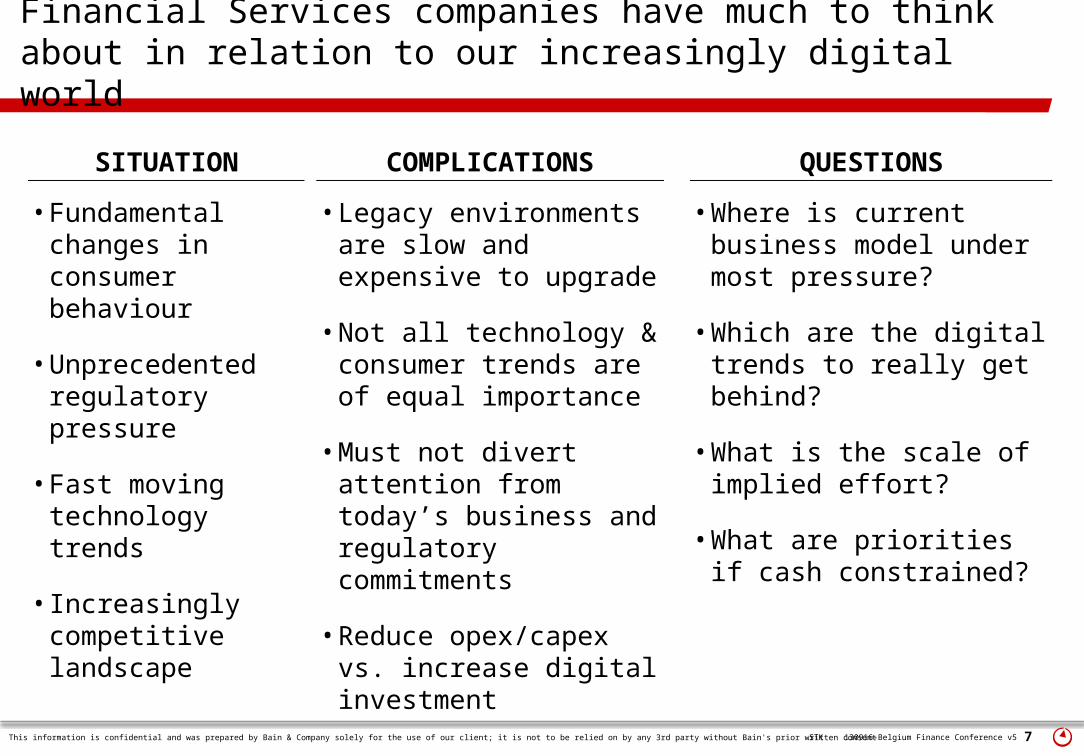

Financial Services companies have much to think about in relation to our increasingly digital world

•Fundamental changes in consumer behaviour

•Unprecedented regulatory pressure

•Fast moving technology trends

•Increasingly competitive landscape

•Legacy environments are slow and expensive to upgrade

•Not all technology & consumer trends are of equal importance

•Must not divert attention from today’s business and regulatory commitments

•Reduce opex/capex vs. increase digital investment

•Where is current business model under most pressure?

•Which are the digital trends to really get behind?

•What is the scale of implied effort?

•What are priorities if cash constrained?

SITUATION COMPLICATIONS QUESTIONS

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 8130916-Belgium Finance Conference v5STK

Context and perspective

Leading Digital practice

Organisingfor success

Harnessing the potential of Digital in Financial Services

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 9130916-Belgium Finance Conference v5STK

0

20

40

60

80

100%

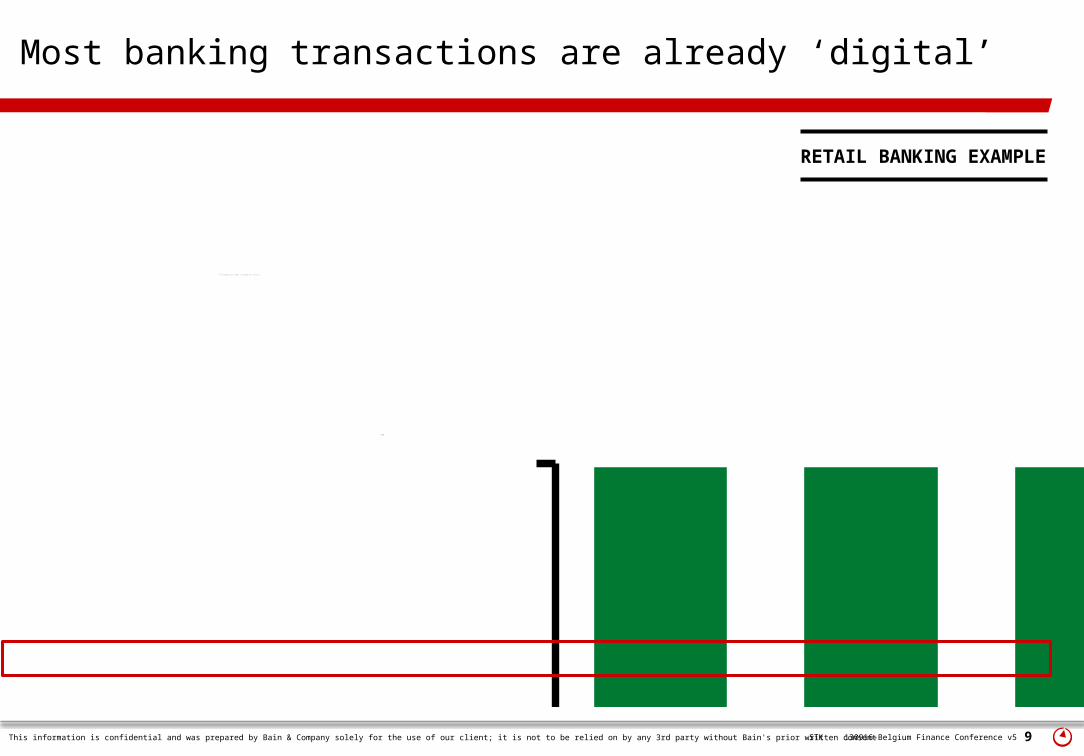

Australia US Korea Canada UK Spain India Mexico Thailand

42% 40% 36% 36% 33%58% 58% 55% 55% 53% 53% 52% 51%

2 1 2 4 19 74 9 8 2 14 10 10

# interactions per customer by country

Germany France China Singapore

% Online and mobile

interactions

No. of respondents

(000s)

Most banking transactions are already ‘digital’

RETAIL BANKING EXAMPLE

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 10130916-Belgium Finance Conference v5STK

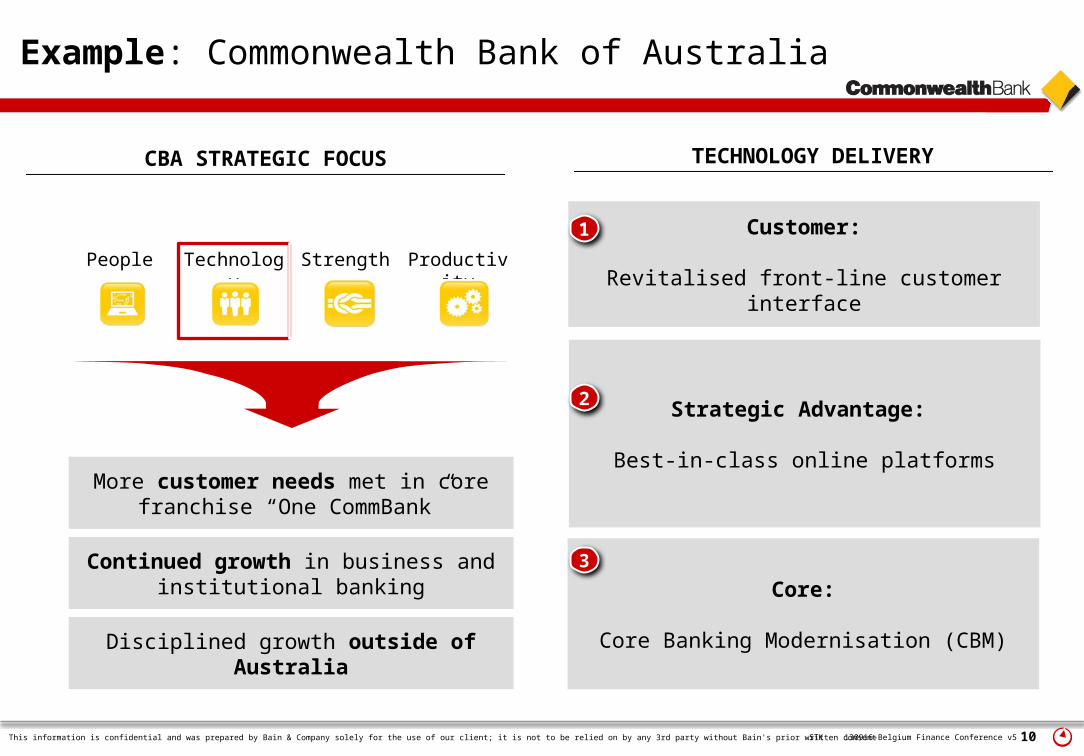

Example: Commonwealth Bank of Australia

People Technology Strength Productivity

More customer needs met in core franchise “One CommBank”

Continued growth in business and institutional banking

Disciplined growth outside of Australia

CBA STRATEGIC FOCUS TECHNOLOGY DELIVERY

Customer:

Revitalised front-line customer interface

Strategic Advantage:

Best-in-class online platforms

Core:

Core Banking Modernisation (CBM)

1

2

3

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 11130916-Belgium Finance Conference v5STK

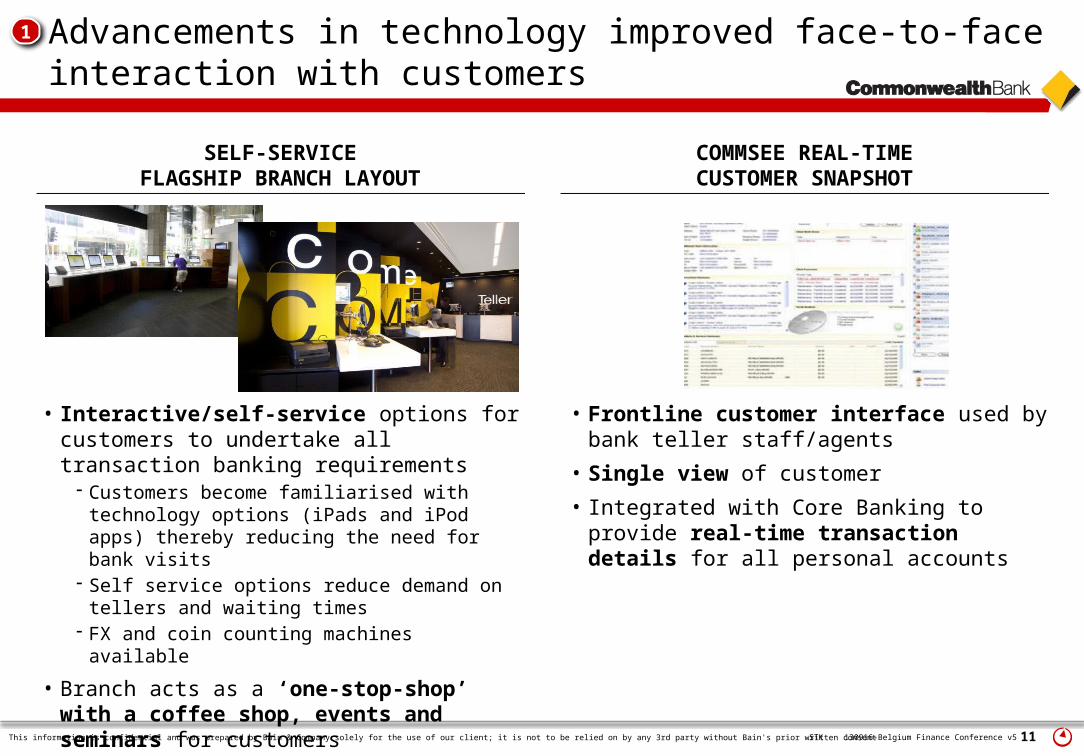

Advancements in technology improved face-to-face interaction with customers

1

SELF-SERVICEFLAGSHIP BRANCH LAYOUT

COMMSEE REAL-TIMECUSTOMER SNAPSHOT

• Interactive/self-service options for customers to undertake all transaction banking requirements

- Customers become familiarised with technology options (iPads and iPod apps) thereby reducing the need for bank visits

- Self service options reduce demand on tellers and waiting times

- FX and coin counting machines available• Branch acts as a ‘one-stop-shop’ with a

coffee shop, events and seminars for customers

• Frontline customer interface used by bank teller staff/agents

• Single view of customer• Integrated with Core Banking to provide

real-time transaction details for all personal accounts

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 12130916-Belgium Finance Conference v5STK

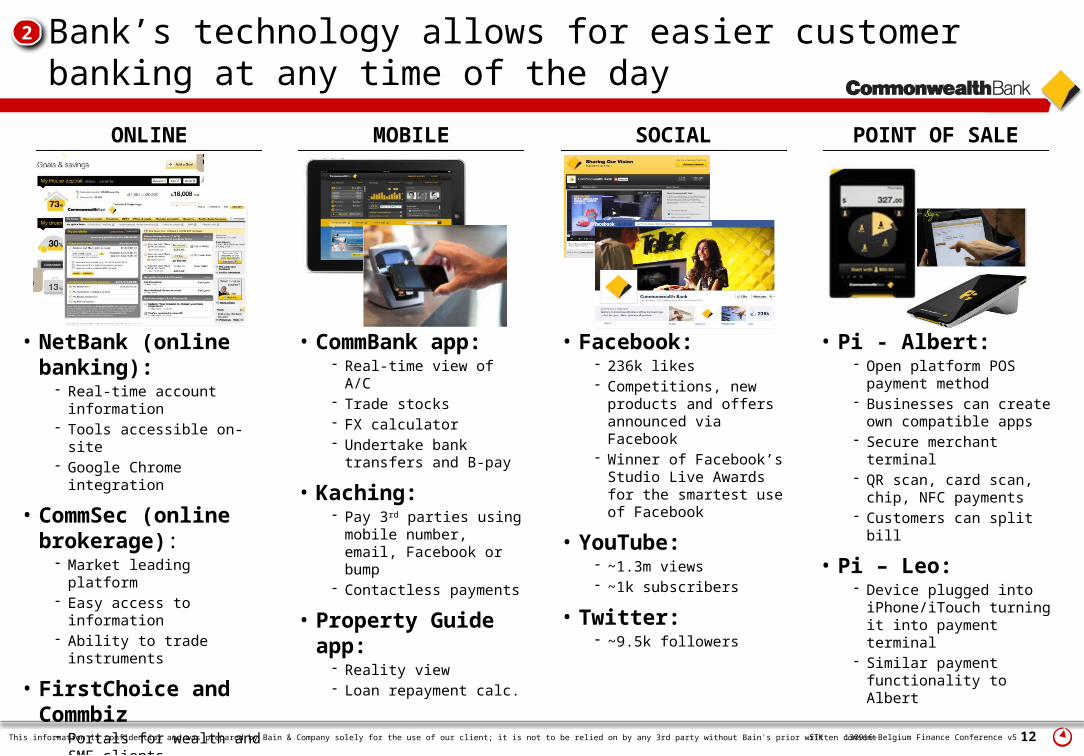

Bank’s technology allows for easier customer banking at any time of the day

2

ONLINE MOBILE SOCIAL POINT OF SALE

• NetBank (online banking):

- Real-time account information

- Tools accessible on-site- Google Chrome

integration

• CommSec (online brokerage):

- Market leading platform- Easy access to information- Ability to trade

instruments

• FirstChoice and Commbiz

- Portals for wealth and SME clients

• CommBank app:- Real-time view of A/C- Trade stocks - FX calculator- Undertake bank

transfers and B-pay

• Kaching:- Pay 3rd parties using

mobile number, email, Facebook or bump

- Contactless payments

• Property Guide app:

- Reality view- Loan repayment calc.

• Facebook:- 236k likes- Competitions, new

products and offers announced via Facebook

- Winner of Facebook’s Studio Live Awards for the smartest use of Facebook

• YouTube:- ~1.3m views- ~1k subscribers

• Twitter:- ~9.5k followers

• Pi - Albert:- Open platform POS

payment method - Businesses can create

own compatible apps- Secure merchant

terminal- QR scan, card scan, chip,

NFC payments- Customers can split bill

• Pi – Leo:- Device plugged into

iPhone/iTouch turning it into payment terminal

- Similar payment functionality to Albert

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 13130916-Belgium Finance Conference v5STK

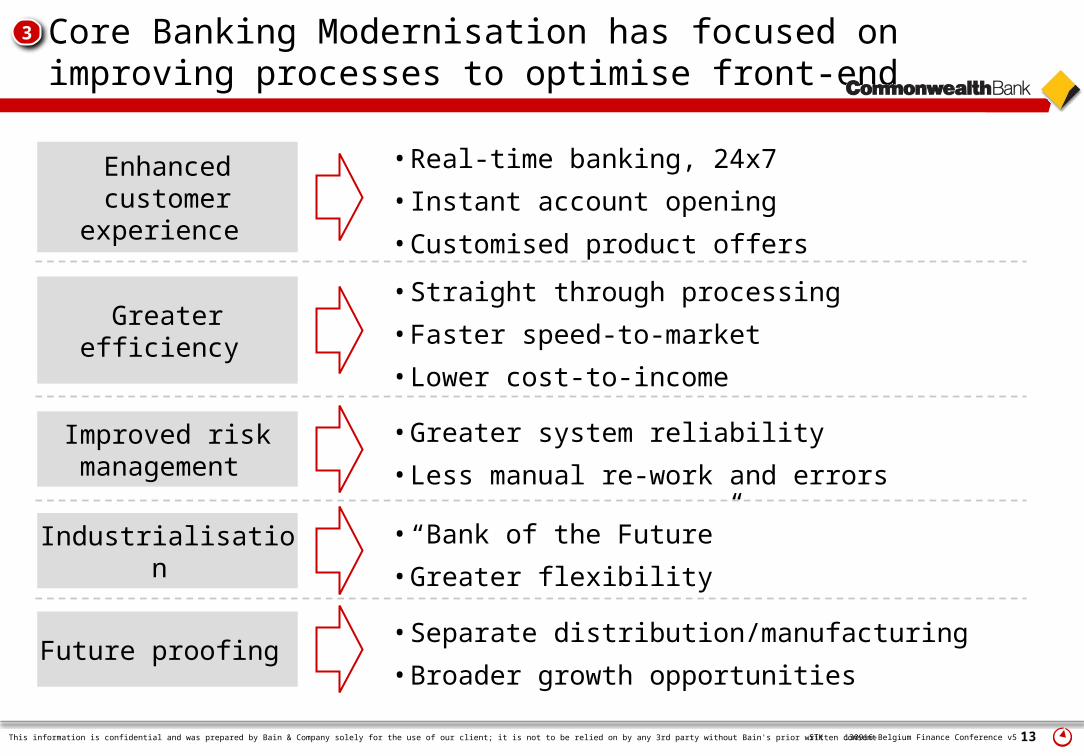

Core Banking Modernisation has focused on improving processes to optimise front-end

3

Enhanced customer

experience

Greater efficiency

Improved risk management

Industrialisation

Future proofing

•Real-time banking, 24x7 •Instant account opening •Customised product offers •Straight through processing •Faster speed-to-market •Lower cost-to-income •Greater system reliability •Less manual re-work and errors

•“Bank of the Future” •Greater flexibility •Separate distribution/manufacturing •Broader growth opportunities

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 14130916-Belgium Finance Conference v5STK

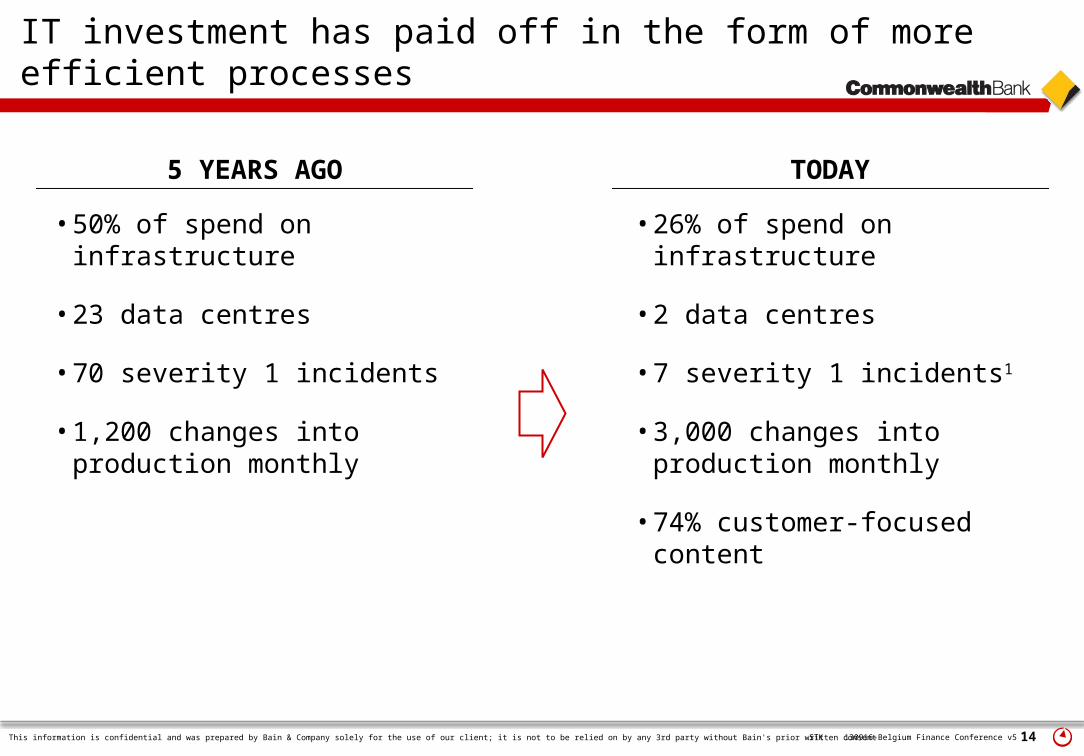

IT investment has paid off in the form of more efficient processes

5 YEARS AGO TODAY

•50% of spend on infrastructure

•23 data centres

•70 severity 1 incidents

•1,200 changes into production monthly

•26% of spend on infrastructure

•2 data centres

•7 severity 1 incidents1

•3,000 changes into production monthly

•74% customer-focused content

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 15130916-Belgium Finance Conference v5STK

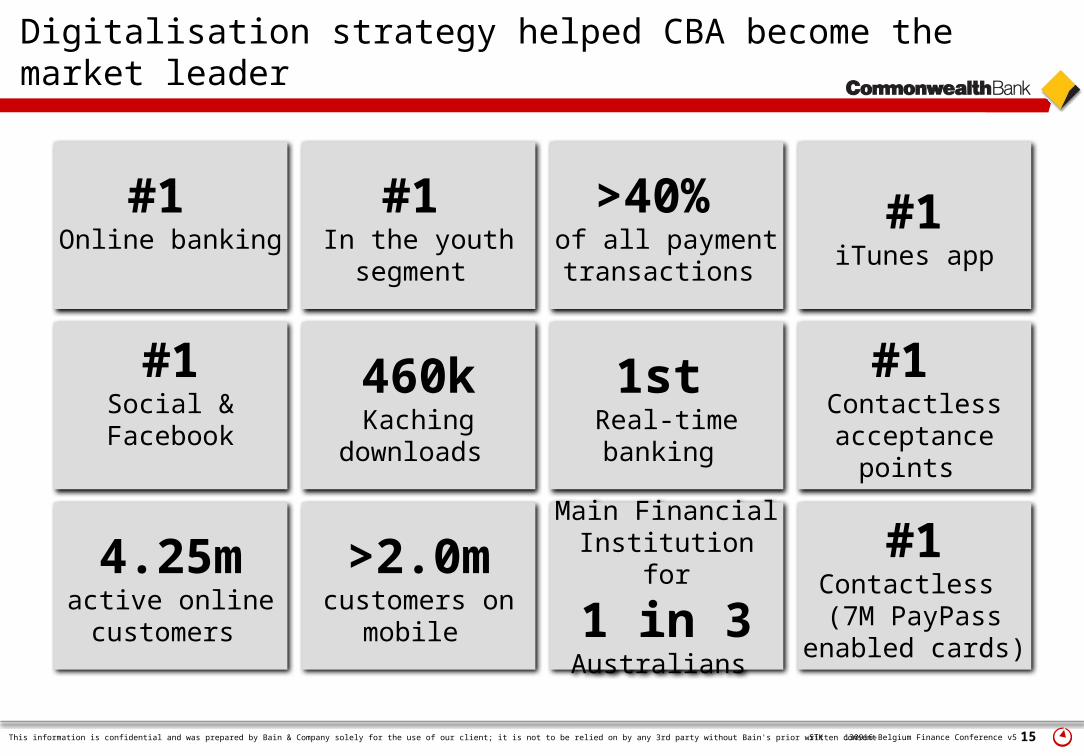

Digitalisation strategy helped CBA become the market leader

#1 Online banking

#1 In the youth

segment

>40% of all payment transactions

#1iTunes app

#1Social &

460k Kaching

downloads

1st Real-time banking

#1 Contactless acceptance

points

4.25m active online customers

>2.0m customers on

mobile

Main Financial Institution for1 in 3 Australians

#1 Contactless (7M PayPass

enabled cards)

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 16130916-Belgium Finance Conference v5STK

Context and perspective

Leading Digital practice

Organisingfor success

Harnessing the potential of Digital in Financial Services

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 17130916-Belgium Finance Conference v5STK

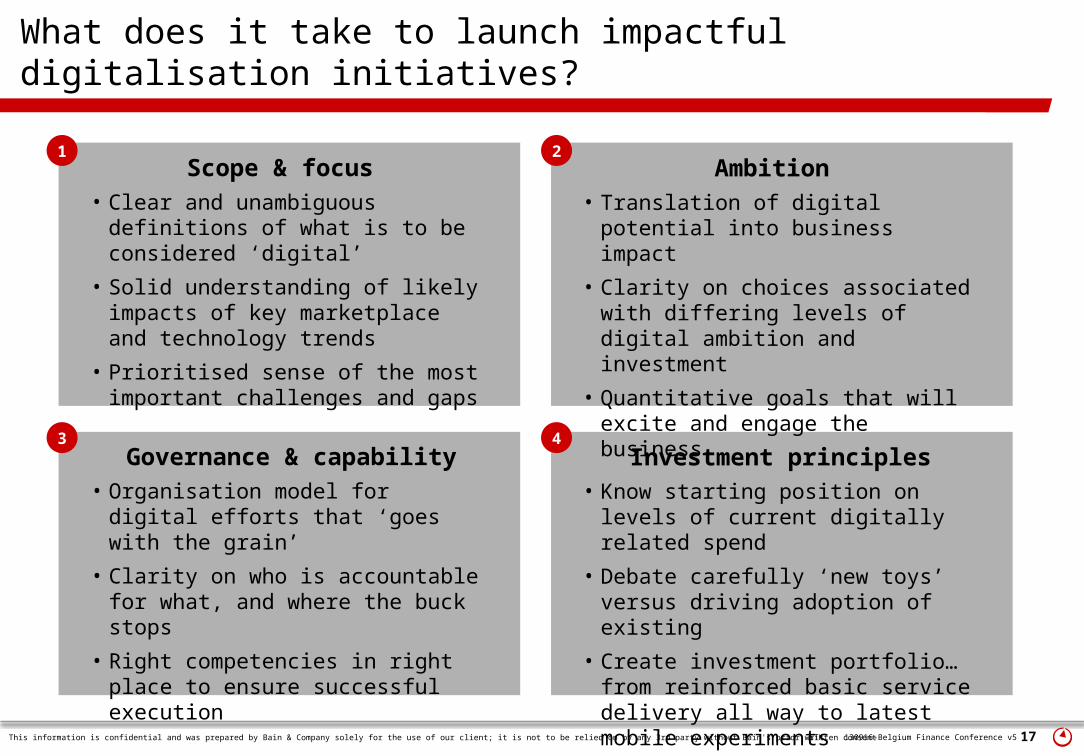

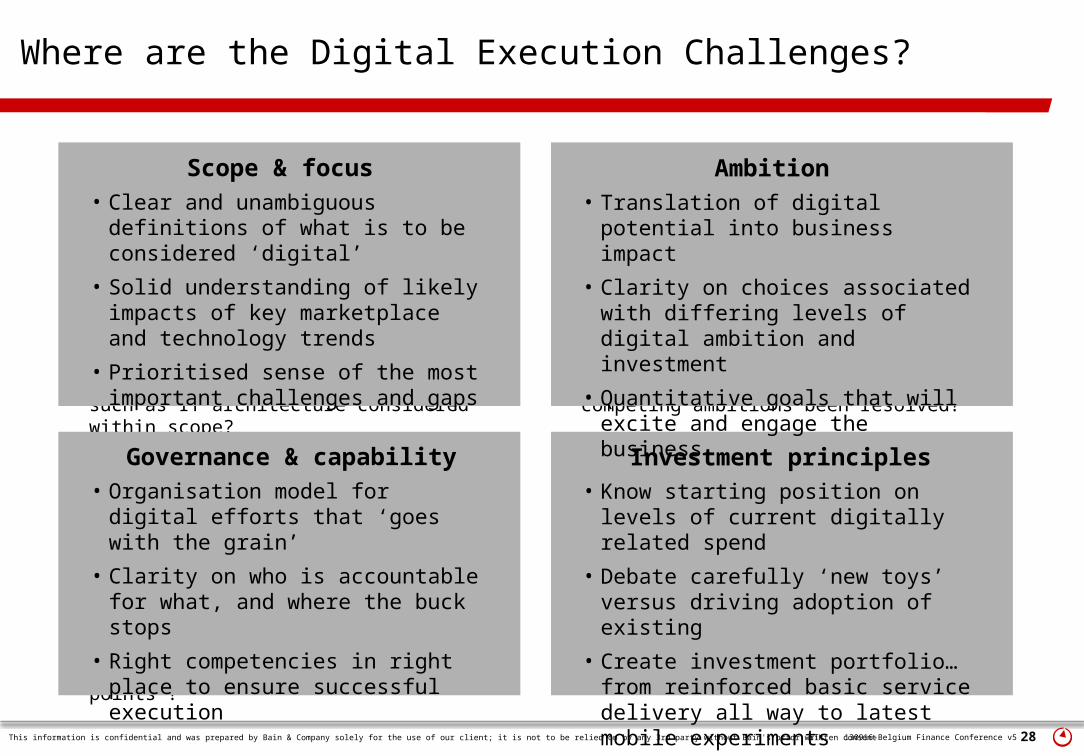

What does it take to launch impactful digitalisation initiatives?

Scope & focus Ambition

Governance & capability Investment principles

• Clear and unambiguous definitions of what is to be considered ‘digital’

• Solid understanding of likely impacts of key marketplace and technology trends

• Prioritised sense of the most important challenges and gaps

• Translation of digital potential into business impact

• Clarity on choices associated with differing levels of digital ambition and investment

• Quantitative goals that will excite and engage the business

• Organisation model for digital efforts that ‘goes with the grain’

• Clarity on who is accountable for what, and where the buck stops

• Right competencies in right place to ensure successful execution

• Know starting position on levels of current digitally related spend

• Debate carefully ‘new toys’ versus driving adoption of existing

• Create investment portfolio… from reinforced basic service delivery all way to latest mobile experiments

1 2

3 4

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 18130916-Belgium Finance Conference v5STK

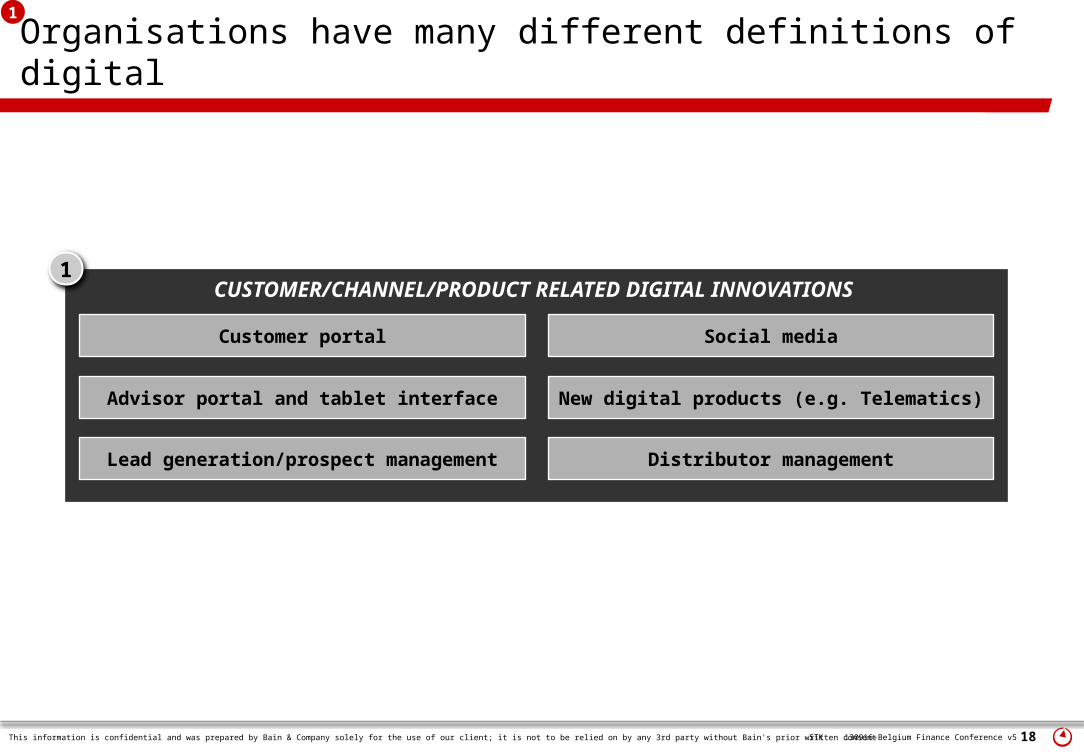

CUSTOMER/CHANNEL/PRODUCT RELATED DIGITAL INNOVATIONS

Customer portal

Advisor portal and tablet interface

Lead generation/prospect management

Organisations have many different definitions of digital

Social media

New digital products (e.g. Telematics)

Distributor management

1

1

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 19130916-Belgium Finance Conference v5STK

INCLUDE BROADER SET OF APPLICATIONS?

CUSTOMER/CHANNEL/PRODUCT RELATED DIGITAL INNOVATIONS

Customer portal

Advisor portal and tablet interface

Lead generation/prospect management

Enterprise components

Business support solutionsPolicy systems

Organisations have many different definitions of digital

Social media

New digital products (e.g. Telematics)

Data management

Distributor management

1

2

1

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 20130916-Belgium Finance Conference v5STK

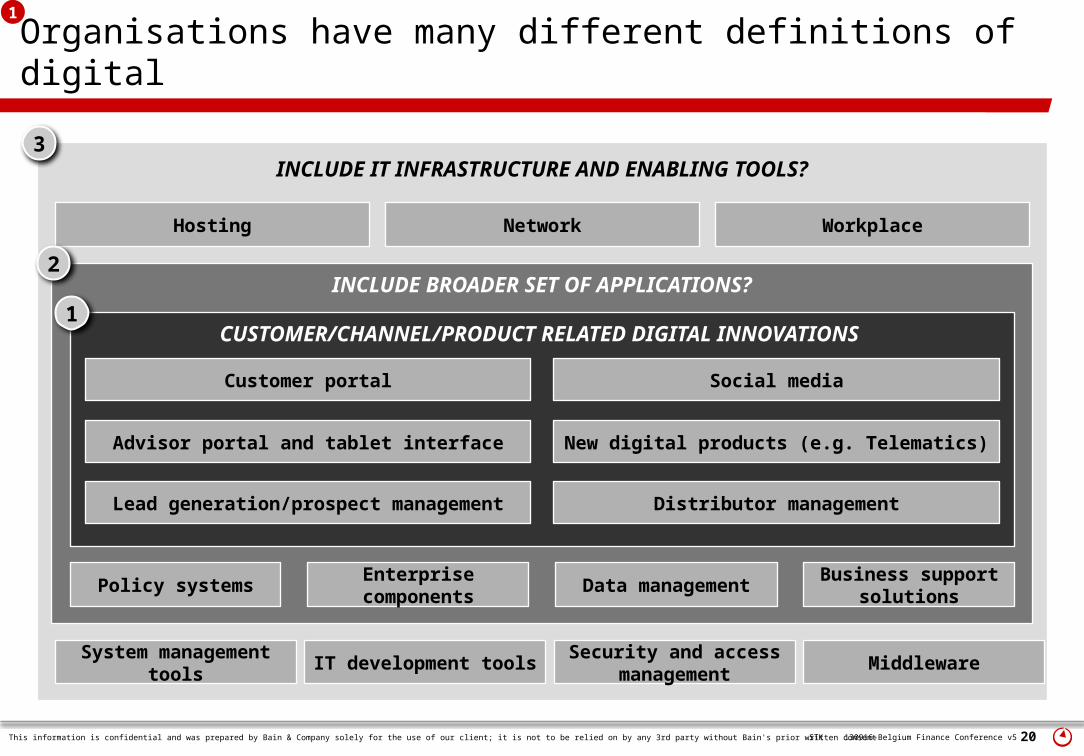

Hosting Network Workplace

INCLUDE BROADER SET OF APPLICATIONS?

CUSTOMER/CHANNEL/PRODUCT RELATED DIGITAL INNOVATIONS

Customer portal

Advisor portal and tablet interface

Lead generation/prospect management

Enterprise components

Business support solutionsPolicy systems

System management tools IT development tools Security and access

management

Organisations have many different definitions of digital

INCLUDE IT INFRASTRUCTURE AND ENABLING TOOLS?

Social media

New digital products (e.g. Telematics)

Data management

Distributor management

Middleware

1

2

3

1

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 21130916-Belgium Finance Conference v5STK

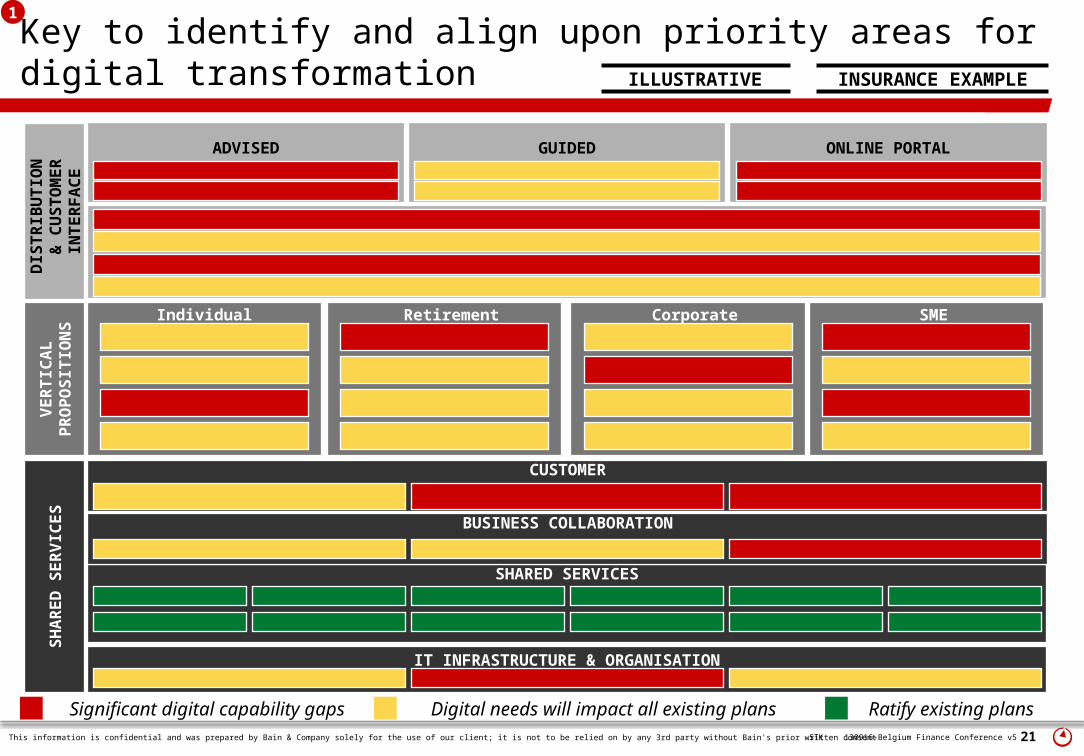

Key to identify and align upon priority areas for digital transformation

Digital needs will impact all existing plans Significant digital capability gaps Ratify existing plans

CUSTOMER

SHAR

ED S

ERVI

CES

SHARED SERVICES

IT INFRASTRUCTURE & ORGANISATION

BUSINESS COLLABORATION

GUIDED

VERT

ICAL

PR

OPO

SITI

ON

S Individual Retirement Corporate SME

ONLINE PORTALADVISED

DIS

TRIB

UTI

ON

&

CU

STO

MER

IN

TERF

ACE

ILLUSTRATIVE INSURANCE EXAMPLE

1

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 22130916-Belgium Finance Conference v5STK

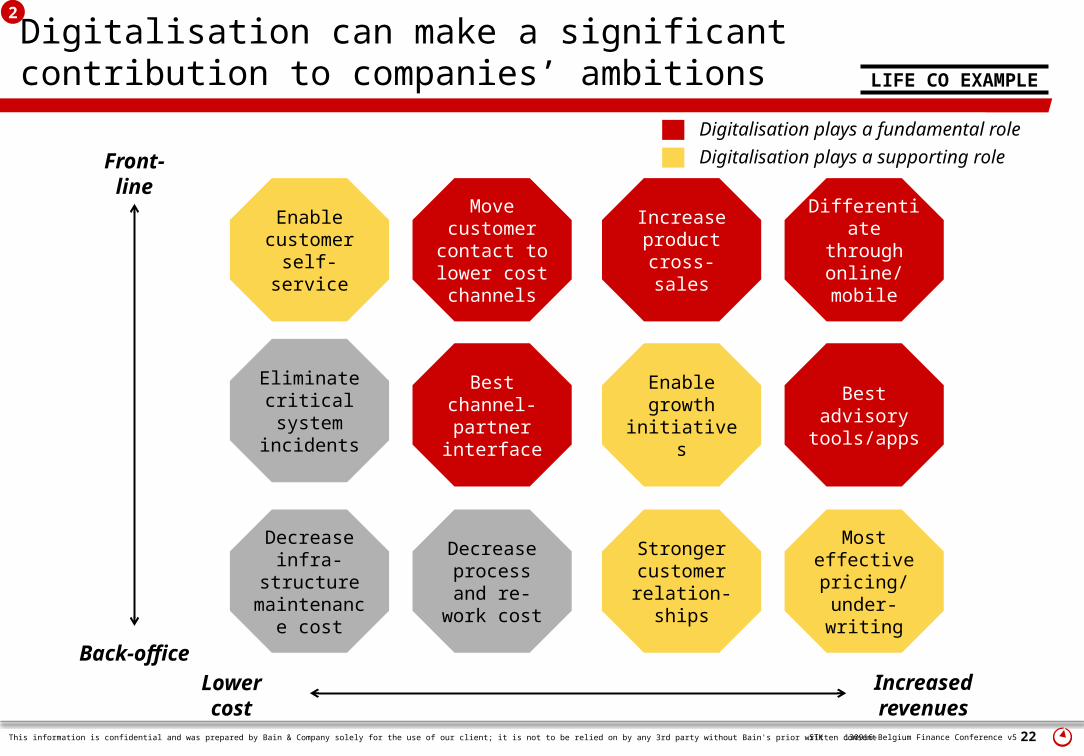

Digitalisation can make a significant contribution to companies’ ambitions

Back-office

Front-line

Increasedrevenues

Lowercost

Differentiate through

online/ mobile

Increase product

cross-sales

Best advisory

tools/apps

Decrease process and re-work cost

Move customer contact to lower cost channels

Decrease infra-

structure maintenanc

e cost

Enable growth

initiatives

Most effective pricing/ under-writing

Eliminate critical system

incidents

Stronger customer relation-

ships

Best channel-partner

interface

Enable customer

self-service

Digitalisation plays a fundamental roleDigitalisation plays a supporting role

LIFE CO EXAMPLE

2

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 23130916-Belgium Finance Conference v5STK

0

20

40

60

80

100%

Other

Div

este

d

trans

actio

ns

WM

Financial

Other

Mixed deposit

Cash withdrawal < X

Cash withdrawal > X

Cross entry

Cash deposit

XM

Non

financial

Cust.

enquiry

YM

# transactions (Y1 )

Card status

Card order

Card activation

Sales

ZM

Total = XXXM

0

XXXM

A Y3

EOY

B C D E Y4

EOY

Target

Gap

# non-self service transactions

Y1

Start

point

Y3

Forecast

Y6

Strategic

view

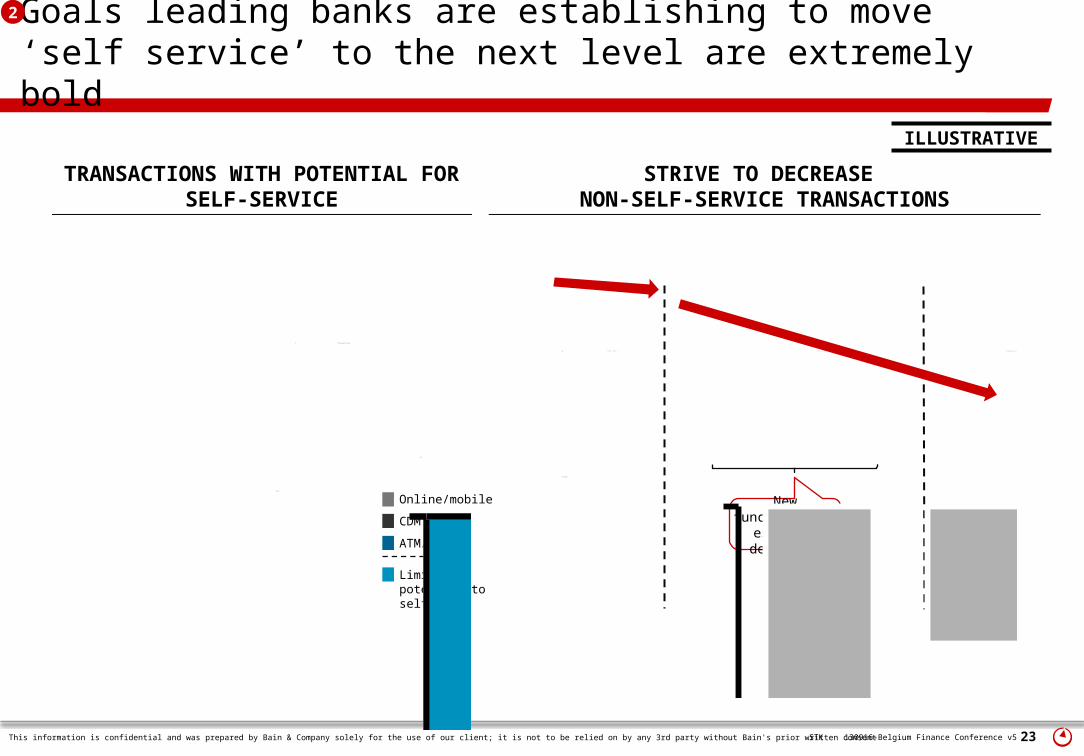

Goals leading banks are establishing to move ‘self service’ to the next level are extremely bold

STRIVE TO DECREASE NON-SELF-SERVICE TRANSACTIONS

WHAT HAS BEEN DONE WHAT CAN BE DONE IN 2013 BEYOND 2013

TRANSACTIONS WITH POTENTIAL FOR SELF-SERVICE

New functionalities

being delivered

Potential toself-serve via:Online/mobile

CDM onlyATM/CDM

Limited potential to self-serve

ILLUSTRATIVE

2

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 24130916-Belgium Finance Conference v5STK

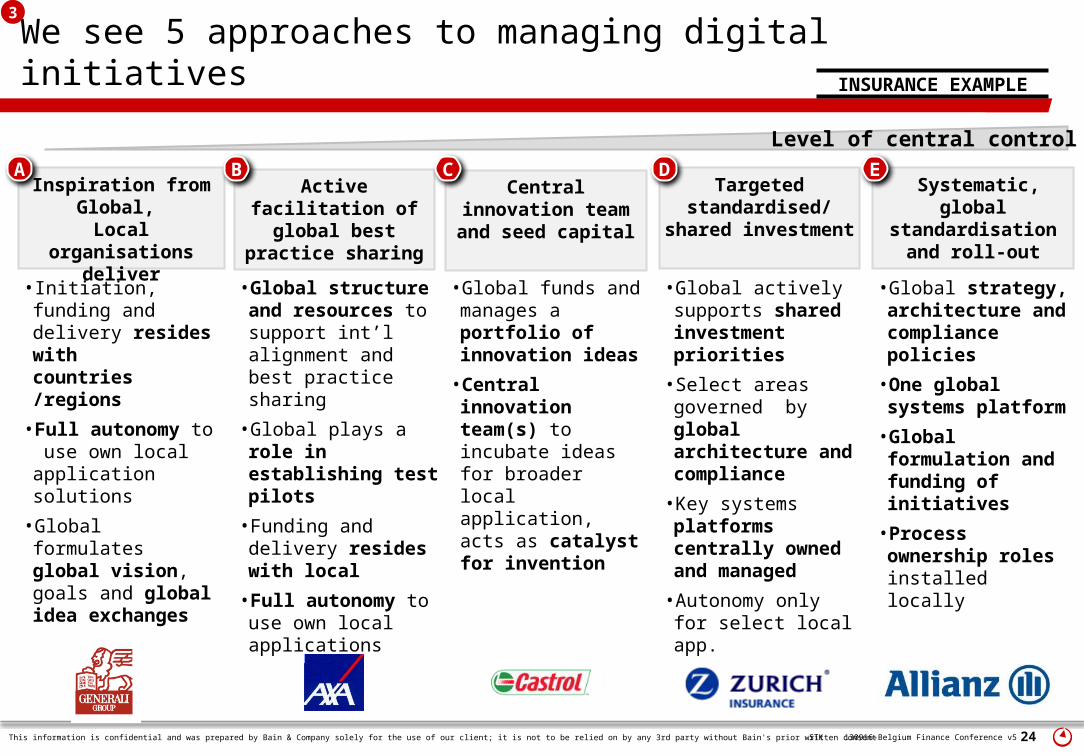

We see 5 approaches to managing digital initiatives

Inspiration from Global,

Local organisations deliver

Central innovation team and seed capital

Active facilitation of global best

practice sharing

•Initiation, funding and delivery resides with countries /regions

•Full autonomy to use own local application solutions

•Global formulates global vision, goals and global idea exchanges

Targeted standardised/

shared investment

Systematic, global

standardisation and roll-out

•Global funds and manages a portfolio of innovation ideas

•Central innovation team(s) to incubate ideas for broader local application, acts as catalyst for invention

•Global structure and resources to support int’l alignment and best practice sharing

•Global plays a role in establishing test pilots

•Funding and delivery resides with local

•Full autonomy to use own local applications

•Global actively supports shared investment priorities

•Select areas governed by global architecture and compliance

•Key systems platforms centrally owned and managed

•Autonomy only for select local app.

•Global strategy, architecture and compliance policies

•One global systems platform

•Global formulation and funding of initiatives

•Process ownership roles installed locally

Level of central controlA CB D E

3

INSURANCE EXAMPLE

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 25130916-Belgium Finance Conference v5STK

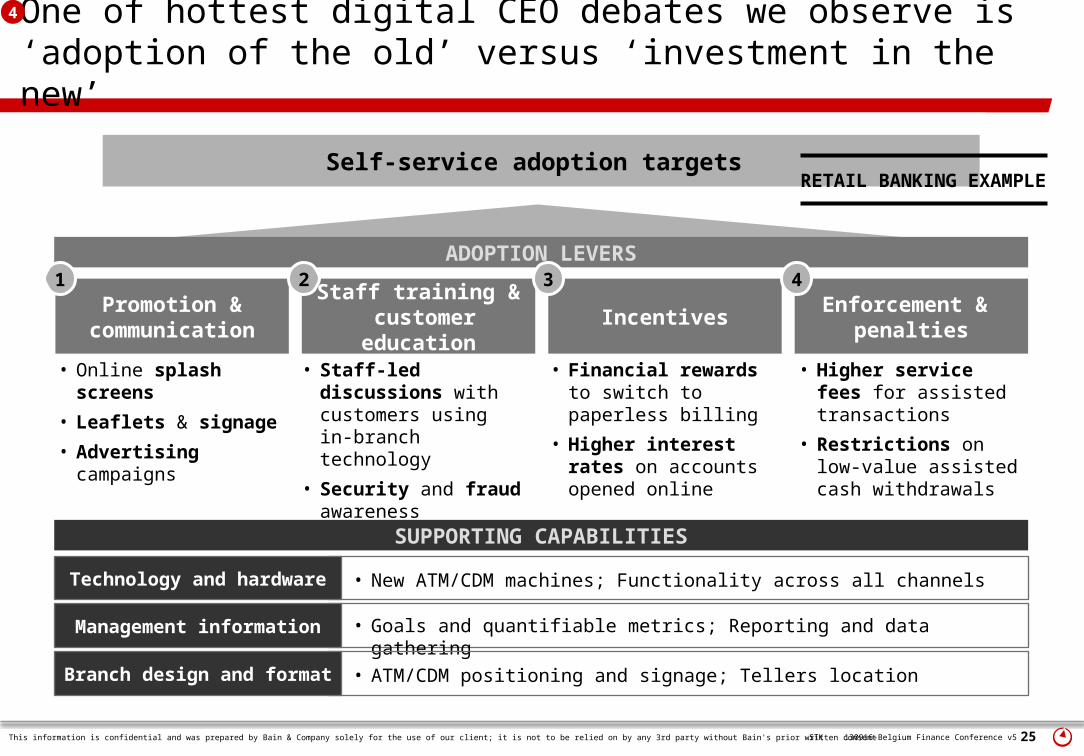

One of hottest digital CEO debates we observe is ‘adoption of the old’ versus ‘investment in the new’

Technology and hardware

Promotion & communication

Staff training & customer education

Incentives Enforcement & penalties

• Online splash screens

• Leaflets & signage• Advertising

campaigns

• Staff-led discussions with customers using in-branch technology

• Security and fraud awareness campaigns

• Financial rewards to switch to paperless billing

• Higher interest rates on accounts opened online

• Higher service fees for assisted transactions

• Restrictions on low-value assisted cash withdrawals

Technology and hardware • New ATM/CDM machines; Functionality across all channels

ADOPTION LEVERS

SUPPORTING CAPABILITIES

1 2 3 4

Self-service adoption targets

Technology and hardwareManagement information • Goals and quantifiable metrics; Reporting and data gathering

Technology and hardwareBranch design and format • ATM/CDM positioning and signage; Tellers location

RETAIL BANKING EXAMPLE

4

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 26130916-Belgium Finance Conference v5STK

Part of digitalisation budgets must improve IT service quality basics to satisfy increasingly demanding clients

0

250

500

750

1 000

1 250

S1 S2 S3 S4 S5 S6 S7

S8

S9

S10 S11

S12

S13 S14 S15 S16 S17 S18 S19 S20 S21 S22 S23 S24 S25 S26 S27 S28 S29 S30 S31 S32 S33 S34 S35 S36 S37 S38 S39 S40 S41 S42 S43 S44

Critical business applications

(S# )

Average monthly minutes downtime

(Y1 )

Down time target

RETAIL INSURANCE EXAMPLE

4

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 27130916-Belgium Finance Conference v5STK

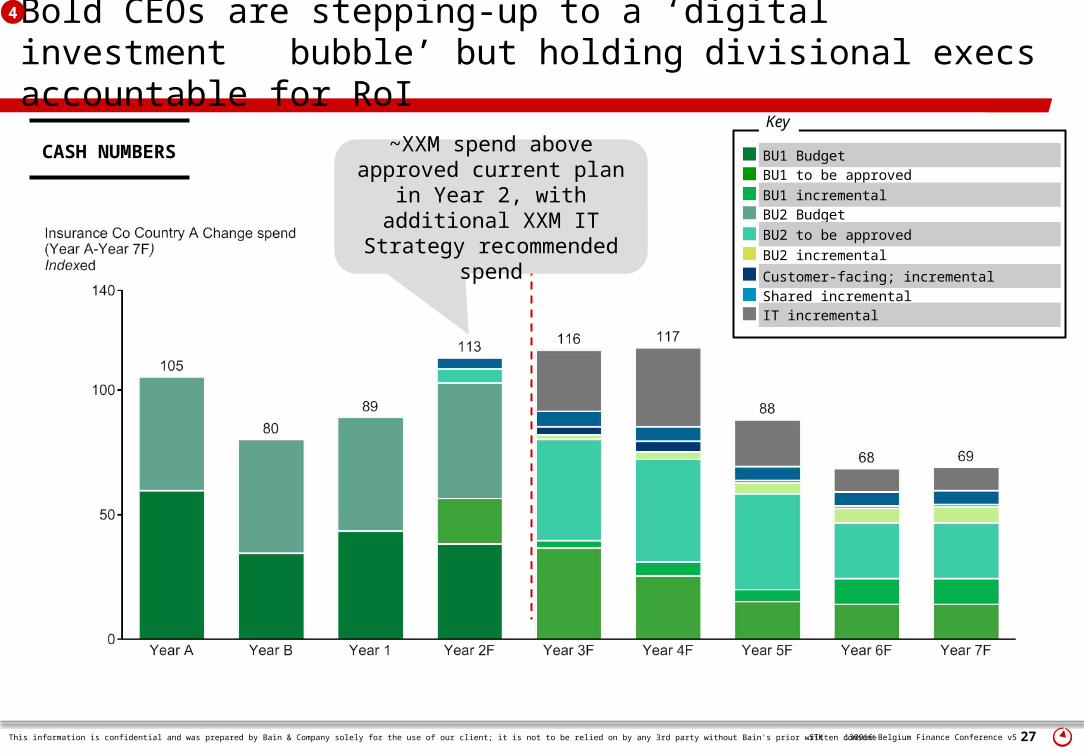

Bold CEOs are stepping-up to a ‘digital investment bubble’ but holding divisional execs accountable for RoI

CASH NUMBERS BU1 Budget

BU1 to be approved

BU2 BudgetBU2 to be approved

BU1 incremental

BU2 incrementalCustomer-facing; incrementalShared incrementalIT incremental

Key

~XXM spend above approved current plan in

Year 2, with additional XXM IT Strategy recommended

spend

4

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 28130916-Belgium Finance Conference v5STK

Where are the Digital Execution Challenges?

Scope & focus•Are you working with clear and ambiguous definition(s) of what digital means?

•Are SL’s digital efforts ‘go to market’ and distribution focused or do they extend to product and policy space?

•Are infrastructural prerequisites such as IT architecture considered within scope?

Ambition•Is there agreed linkage from SLs stated business ambitions through to the role that digital capabilities must play?

•To what extent have these requirements been driven down into concrete KPIs?

•How have any conflicts between competing ambitions been resolved?

Governance & capability•What are the role and associated decision accountabilities in different geographies?

•To what extent are country and product groups aligned and engaged with digital efforts?

•What, if any, have been resourcing and capability related ‘pinch points’?

Investment principles•Is there a clear point-of-departure factbase on current SL digital expenditure?

•How are Divisional executives being held accountable RoI on their share of the transformation investment?

•Will further waves of investment be required?

Scope & focus Ambition

Governance & capability Investment principles

• Clear and unambiguous definitions of what is to be considered ‘digital’

• Solid understanding of likely impacts of key marketplace and technology trends

• Prioritised sense of the most important challenges and gaps

• Translation of digital potential into business impact

• Clarity on choices associated with differing levels of digital ambition and investment

• Quantitative goals that will excite and engage the business

• Organisation model for digital efforts that ‘goes with the grain’

• Clarity on who is accountable for what, and where the buck stops

• Right competencies in right place to ensure successful execution

• Know starting position on levels of current digitally related spend

• Debate carefully ‘new toys’ versus driving adoption of existing

• Create investment portfolio… from reinforced basic service delivery all way to latest mobile experiments