Embed Size (px)

Citation preview

Page 1

Group Presentation

Page 2

Companies

STIAL

SOCOGES

Centrale Laitière du Cap-Bon (CLC)

Centrale Laitière du Nord (CLN)

Centrale Laitière de Sidi-Bouzid (CLSB)

Compagnie Fromagère (CF)

Société des Boissons du Cap-Bon (SBC)

DELTA PLASTIC (DP)

Shareholders

MEDDEB's FamilyGervais DANONE

MEDDEB's FamilyGervais DANONE

MEDDEB's Family

MEDDEB's Family

MEDDEB's Family

MEDDEB's Family

BONGRAIN

MEDDEB's Family

MEDDEB's Family

DELICE Holding subsidiaries

Page 3

Manufacturing premises

2 plants in Boussalem :- CLN

- La Compagnie Fromagère

1 plant inSidi-Bouzid (2014):

- CLSB

5 plants in Soliman :- STIAL- CLC- SBC- DELTAPlastic- CF (Borj Cedria)

Korbous

Soliman

Cap Bon

Sidi Daoud

Kélibia

Korba

Nabeul

Page 4

Main milestones

Creation of STIAL byM. Mohamed

MEDDEB : total

investment of 200K€

- Creation of SOCOGES

- Partnership talks with :

- YOPLAIT

- DANONE

1978 2005-2006

-Strategic partnership withDANONE (50% of STIAL

and SOCOGES acquired by

CGD)-Creation of “CLC” with an

investment of 22 MDT

-Acquisition of "CLN"

-End of partnership with

VIRGIN COLA

Creation of CLSB with total

investment of 24 M€

(expected to reach 35.5 M€

in 2018)

- Creation of SBC

- Creation of Delta Plastic

- Partnership with VIRGIN COLA (franchising contract)

Creation of CF through a

strategic partnership with

BONGRAIN

- Creation of DELICE Holding

- IPO (15% of DH listed)

- Activity launch of CLSB

1997 2011

1993 20082002 2013-2014

Page 5

DELICE Holding structure

Beverage

activity

Milk

activityCheese

activityDistribution

activity

Dairy activity

SBC STIAL CF SOCOGES

DELTA

PLASTICCLSB CLN

DELICE Holding

CLC

Page 6

Business Activities

Page 7

Milk activityRaw milk in Tunisia

Page 8

286 collecting centers

424 000 cows

Annual yield per cow : 4 500 L 120 000 dairy farmers

7 milk production plants

4 yogurt production plants

31 cheese production small plants

The milk production represents 25% of the animal production, 11% of the

agricultural products and 7% of the food production

The national production of raw milk is around 1 200 Millions liters with an

annual average growth rate of 4%

90% of the milk collected by the industry is brought by small dairy farmers

286 Collecting centers with a total collection ability around 2,6 millions liters

42 milk units contribute to the transformation process with a daily

production of 3,4 Millions liters

Milk activityRaw milk in Tunisia

Page 9

National Production

National Collection

1054

638

1090

664

1136

709

1150

745

1200

783

1248

823

2013 2014

Raw milk in Tunisia

National production and collection of milk (million liters)

Page 10

2015*

*Estimates

2010 2011 2012

Source : GIVLAIT

Milk activity

Milk

drinks

(546 ML)

Powdered

milk

(20 ML)

Yogurt

and dairy

(155 ML)

18% 15% 4% 26%

Informal market

and self

consumption

(310 ML)

Cheese

(135 ML)Others

(34 ML)

National production (1200 ML)

74%

Improvement

potential

Total raw milk going to the industry (890 ML)

61% 2%

Milk activityRaw milk in Tunisia

Page 11

2014 Data

Milk activity

Per Capita Consumption PCC

+0,3% +20,1% +3,8% +2,4%

2013 20142011

0,0 0

10

20

30

40

50

100,0

200,0

300,0

400,0

500,0

2012 2015

398 399 479 497 509

* Total UHT milk (1/2 skimmed,

vitamin enriched milk, skimmed

milk and whole milk)

51

55 5759 60

60

70

600,0

700,0

CAGR

+9,7% +3,1%

Annual growth (%)

Volume (liters)

Volume / capita (liters)*

BENCHMARK PCC

Source :Nielsen/ tetrapak

Page 12

Estimated

Market 2011 2012 2013 2014

Algeria 53,49 54,08 56,76 58,84

Libya 16,67 21,95 23,42 25,06

Morocco 28,83 29,62 30 30,47

Ireland 129,27 127,33 125,79 124,22

Finland 125,78 125,15 132,92 122,08

CAGR

Milk activity

SKU’s = 17

Page 13

Company

Centrale Laitière du Cap-Bon

CLC

Employees

696

Centrale Laitière du Nord

CLN436

Centrale Laitièrede Sidi Bouzid

CLSB300

Total

employees

1432

Beverage activity

Per Capita Consumption PCC

13 % 9%8%

30%

2010 2011

BENCHMARK PCC

20122009

8,3

8,7 9,1

10,611,3

12,2

13,2

2013

34 37 40 52 63

21%13%

14%

2014 2015*

Annual growth (%)

Volume (liters)

71 81

CAGR

+17%

Volume / capita (liters)*

Source: Nielsen JJ14 & INS 1

Compass Tétrapak 14

Estimated

Page 14

2009 2010 2011 2012 2013 2014

Libya 55,38 61,49 29,92 51,68 71 54,29

Algeria 17,14 19,18 21,62 26,33 26,13 28,09

Egypt 4,85 6,95 8,58 8,86 9,13 9,59

Morocco 3,69 4,24 4,72 5,11 6,02 6,49

Beverage activity

160

160

Société des Boissons du Cap-

Bon

SBC

Total employees

Company

Page 15

Employees SKU’s = 38

Dairy activity

Per Capita Consumption PCC

2008 2009 2010 20112004 2005 2006

88,4

9,310,4 10,7

11,2

17,416,4

15,9

14,6

12,8

11,7

2007 2012 2013 2014 2015 2016 2017

Estimates

2018

18,619,9

21,3

CAGR+7%

CAGR+7%

CAGR+6%

CAGR+7%

Evolution PCC Kg*

BENCHMARK

Source : Nielsen JJ14 & INS 1

Compass Tétrapak 14

France = 36 kg

Saudi Arabia = 28 kg

Spain = 27 kg

Turkey = 26 kg

Algeria = 11 kg

Page 16

Dairy activity

1100

1100

STIAL

Total employees

Company Employees SKU’s = 75

Page 17

Cheese activity

Per Capita Consumption PCC

CAGR

23%

-4%

22%

2013 20142011

0,816

1,198 1,213

2012

871510721 13040

+15%

(kilos)

BENCHMARK PCC

Market

France

Italy

Egypt

South Africa

28

22

10

2

2014

13340

Volume (tons)

Volume / capita2%

2015

Estimates

Annual growth(%)

1,244

Page 18

3%

13681

Cheese activity

Company

170

170

La Compagnie Fromagère

CF

Total employees

Employees SKU’s = 36

Page 19

Packaging activity

Outsourcing Danup bottles production for STIAL

Company

60

60

Delta Plastic

DP

Total employees

Employees

Page 20

Distribution activitySales process

SOCOGES

SBC

Distribution workforce:

- 220 freelance drivers with SOCOGES' tracks

- 20 SOCOGES’ sales platform with own tracks-Retailers spread on whole Tunisian territory

CLN CLC

CLSB

SOCOGES’

sales

platform

Retailers

Hypermarkets

STIAL

CF

Page 21

Company

SOCOGES

Employees

-

Total employees -

DELICE Holding Key Figures

Page 22

Economic Environment

Page 23

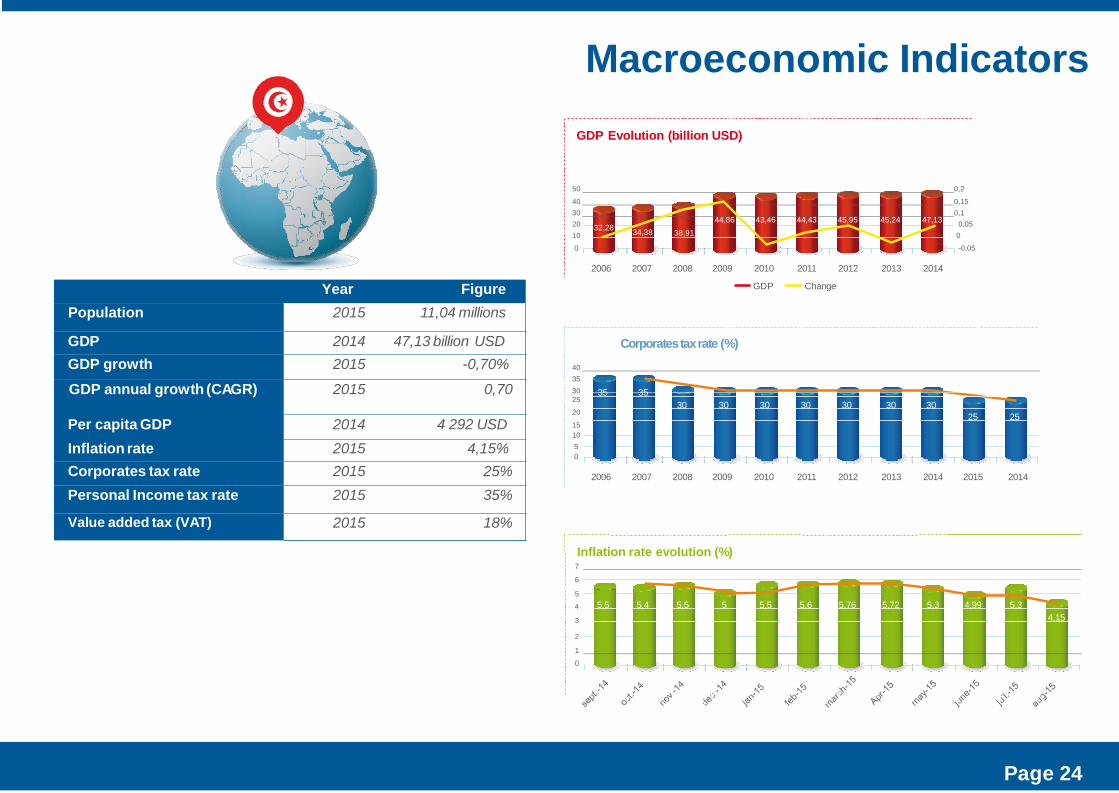

Macroeconomic Indicators

Corporatestaxrate (%)

2006

30

25

20

15

10

5

0

25 25

40

35

30 30 30 30 30 30 30

35 35

2007 2008 2009 2010 2011 2012 2013 2014 2015 2014

Inflation rate evolution (%)7

6

5

4

3

2

1

0

5,5 5,4 5,5 5 5,5 5,6 5,76 5,72 5,3 4,99 5,3

4,15

GDP Evolution (billion USD)

2006 2007 2011

Change

2012

20

10

0

2014

34,38 38,910,05

0

-0,05

50 0,2

40 0,15

30 0,1

2008 2009 2010

GDP

2013

32,2844,86 43,46 44,43 45,95 45,24 47,13

Page 24

Year Figure

Population 2015 11,04 millions

GDP 2014 47,13 billion USD

GDP growth 2015 -0,70%

GDP annual growth (CAGR) 2015 0,70

Per capita GDP 2014 4 292 USD

Inflation rate 2015 4,15%

Corporates tax rate 2015 25%

Personal Income tax rate 2015 35%

Value added tax (VAT) 2015 18%

Beverage Activity

Page 25

Beverage activity

27 160

22,5% 14,8% 8,6% 29,7%

33 269

38 17941 481

2 602

3,2% 118,0% -27,7% 28,9%

2 684

5 850

4 228

5 450

Net income

CAGR = 20%

RevenuesCAGR = 19%

Operating income

CAGR = 30%

Margin’s Evolution

Operating margin = Operating Income / Total revenues Net margin = Net income/ Total revenues

2011 2012

Operating margin

2013 2014

Net margin

2015*

* Estimation

10,3 %11,1 %

8,1 %

9,6 %

14,6 % 15 %

10,2 % 10,1 %

18,5 %

15,3 %

2013 20142011* Estimation

2012

2013 20142011

* Estimation

2012

53 795

2015* 2015*

2015*

2 804

31,2% 91,6% -13,8% 33,0%

3 680

7 051 6 075

2013 20142011

* Estimation

2012

Capital value = 2600 Kdt

8 077

Page 26

Dairy Activity

Page 27

Dairy activity

195 157

18,5% 14,6% 8,3% 8,5%

231 302

265 023287 068

25 500

19,7% 16,9% 17,2% 13,9%

30 518

35 687

41 837

47 654

Net Income

CAGR = 17%

RevenuesCAGR = 12%

Operating Income

CAGR = 13%

Margin’s evolution

2011 2013 2014 2015*

* Estimation

19,0 %19,2 %

13,2 %

13,1 %

19,3 %19,6 %

14,6 % 15,3%

19,0 %

13,5 %

2012

Operating

margin

Net margin

2013 20142011

* Estimation

2012

2013 20142011 2012

37 152

19,7% 13,0% 10,4% 9,9%

44 487

50 285

55 528

2013 20142011

* Estimation

20122015*

311 436

2015*

61 042

2015*

* Estimation

Page 28

Packaging Activity

Page 29

Packaging activity

2 245

42,7% 23,3% 2,2% 14,0%

3 203

3 9504 035

598

42,8% -40,5% -11,4% 22,2%

854

508450

Net IncomeCAGR = -2%

RevenuesCAGR = 20%

Margin’s evolution

2011 2013

Operating IncomeCAGR = 1%

1 147

2014

* Estimation

30,0 %

35,8 %

26,6 %26,7 %

14,7 %15,1 %

11,2 % 12 %

21,1 %

12,9 %

2012

Operating

margin

Net margin

2013 20142011

* Estimation

2012

2013 20142011

* Estimation

2012

674

70,2% -27,2% -28,7% 16,5%

835

595

2013 20142011

* Estimation

20122015*

2015*

4 598

2015*

693

2015*

550

Page 30

Cheese Activity

Page 31

Cheese activity

5 554153,7% -15,2% 50,6% 21,0%

14 088

11 950

17 999

Net Income

RevenuesCAGR = 41%

Operating Income

Margin’s evolution

2011 2012 2013 2014 2015*

-31,9%

1,9 %

-0,3 %

-37,6 %

-4,4 %

4,8 %

0,2 %

-10,3 %

-5,1 %

-8,3 %

OperatingMargin

Net margin

2013 20142011

* Estimation

2012 -1 773

* Estimation

115,4% -324,2% -30,7% 230,4%

273

-612

-800

2013 20142011

2012

-2 086

97,9% -2156,8% -86,0% 101,8%

-44

-993

-1 847

33

2013 20142011 2012

2015*

21 774

2015*

1 043

2015*

* Estimation

Page 32

* Estimation

Distribution Activity

Page 33

Distribution activity

507 088

14,0% 9,2% 14,0% 12,4%

578 196

631 112

719 576

Net Income

RevenuesCAGR = 12%

Operating Income

Margin’s evolution

2011 2012 2013 2014 2015*

-0,4%

-0,3 %

-0,3 %

-0,5 %

-0,6 %-0,8 %

-0,8 %-0,9 %

-0,4 %

-0,4 %

Operatingmargin

Net margin

2013 20142011

* Estimation

2012

-2 633

25,3% -31,4% -136,0% -25,8%

-1 967

-2 585

-6 100

2013 20142011 2012

-2 251

32,6% -60,7% -77,6% -43,4%

-1 517

-2 438

-4 331

-6 209

2013 2014 2015*2011 2012

2015*

809 041

-7674

2015*

* Estimation

Page 34

* Estimation

* Estimation

Milk Activity

Page 35

Milk activity

286 046

6,3% 12,1% 18,0% 19,5%

304 090

340 960

402 474

5 474

50,8% 210,4% -68,4% 24,9%

8 255 8 100

Net Income

CAGR = 17%

RevenuesCAGR = 14%

Operating Income

CAGR = 11%

Margin’s evolution

2011 2012

Operating

2014

* Estimation

3,7 % 3,7 %

2,7 %1,9 %

3,3 % 3,4 %

2,0 % 2,1 %

7,5 %

2,8 %

margin

2013

Net margin

2013 20142011

* Estimation

2012

2013 20142011 2012

10 723

4,3% -13,1% 35,6% 24,3%

11 179

9 709

13 162

2013 20142011

* Estimation

2012

25 626

2015*

481 053

2015*

16 356

2015*

10 119

* Estimation

Page 36

2013 capital value = 17 644 Kdt

2015

Consolidated Performance

Page 37

Human Resources

Page 38

Human resources

Headcount evolution

20142012

Headcount evolution and high skilled staff

2013 20142012

Men Headcount

Women Headcount

High skilled staff ratio

HR Policy

Human capital management and development

Fairness and transparency

Harmonious and fair remuneration policy

Training plans to develop competencies

Performance management

Page 39

2013

Total headcount

+70 +466

CAPEX

Page 40

CAPEX

CAPEX in KDT

Page 41

Activity 2015 * 2014 2013

* Estimated

Beverage activity 2 300 12 384 2 890

Dairy activity 14 463 9 357 8 294

Packaging activity 10 176 698

Cheese activity 300 1 045 10 603

Distribution activity 4 396 4 524 5 541

Milk activity 14 200 33 280 40 909

TOTAL CAPEX 35 669 * 60 766 68 935

Financial Statements

Page 42

Income allocation

Income allocation (TND)

Retained earnings -1 600 944

Income 2014 39 017 383

Page 43

Available income

Legal reserves

37 416 439

-1 870 822

Distributable profits 35 545 617

Dividends -35 140 647

Retained earnings 404 970

640 millimes/share

Consolidated Statements

Page 44

Consolidated income statements

Page 45

Consolidated income statement

20 000

0

40 000

92 69060 000

80 000

100 000

120 000

140 000

25 002 25 826

74 009

8 417 3 118

16,3%17,3%

19,0%13,8%

19,7%

38,9%

1 548 586

-93,4%

-6,7%3,3%

2070

NET INCOME VARIATION 2014 VS 2013

%In

co

me

an

nu

alin

cre

ase

2014

vs.

2013

6 386

Page 46

Financial Indicators

Page 47

Financial indicators

In 2014 , the debt to equity and debt to revenues ratios has been relatively steady and reached

respectively 18.5% and 17%.

Net financial debt has increased by 33% to support investment efforts

Page 48

2014 2013 %

Net financial debt 112 84 +33%

Debt /equity 18,5% 14,4%

Debt/revenues 17% 14,7%

2015 Q3 KPI’s

Page 49

2015 Q3 KPI’sKPI’s as of

30.09.2015 vs

30.09.2014

Consolidated

revenues

Production in

value

Debt structure

543 906 Kdt

+10%

575 815 Kdt 140 220 Kdt

Consolidated revenues YTD (kDT)

600 000

500 000

400 000 +10%

300 000

200 000

100 000

30.09.2014 30.09.2015

400 000

300 000

200 000

100 000

600 000

500 000

30.09.2014 30.09.2015

Production in value YTD (kDT)

+18%

45 000

40 000

35 000

30 000

25 000

20 000

15 000

10 000

30.09.2014 30.09.2015

Inventories (kDT)

120 000

110 000

100 000

140 000

130 000

150 000

30.09.2014 30.09.2015

Debt structure (kDT)

The revenues’ increase has

been driven by a relatively more

important growth pace for the

beverage and cheese activities.

Milk and dairy segments’

revenues had respectively

grown by 7.5% and 6.5%.+89%-5%

Page 50

+18% -5%

DELICE Holding Share

Page 51

DELICE Holding shareEvolution of the DELICE Holding share

6000

DH / Tunindex

Overall yield : 7,7%

Highest : 16,91 TD

Lowest : 14,02 TD

Tunindex

Page 52

DH

5800

5600

5400

52005000

18

16

14

12

4800 10

4600 8

4400

4200 6

4000 4

DELICE Holding share

Page 53

Stock market indicators

Libellé 2014* 2015**

Highest(DT) 15,589 16,905

Lowest(DT) 14,023 14,000

Closing price(DT) 14,551 15,68

Yield

DH 3,77% 0,89%

Tunindex 10,76% 2,43%

Market cap(MDT) 798,9 806,4

Number of traded shares 1 154 465 3 502 946

Traded Volumes (MDT) 17,7 56,4

Foreign shares 4,13% 9,05%

* since 08/10/2014

** as of 06/10/2015

Thank you