Embed Size (px)

Citation preview

GPP501: Lecture Sept 19 1 of 21

GPP 501

Microeconomic Analysis for Public Policy

Fall 2017

Given by Kevin Milligan

Vancouver School of Economics

University of British Columbia

Lecture Sept 19th: Supply

GPP501: Lecture Sept 19 2 of 21

Agenda for today:

1. Factors of production

2. Technology and production

3. Supply Curves

4. Market equilibrium

GPP501: Lecture Sept 19 3 of 21

Factors of production

What do we need to make guns/butter/anything?

GPP501: Lecture Sept 19 4 of 21

Factors of production

Labour

Is labour homogenous? Differentiated?

Capital

What is capital?

Land / Air / Nature / Raw materials

Where do these come from? How do we attain the right to use it?

GPP501: Lecture Sept 19 5 of 21

Agenda for today:

1. Factors of production

2. Technology and production

3. Supply Curves

4. Market equilibrium

GPP501: Lecture Sept 19 6 of 21

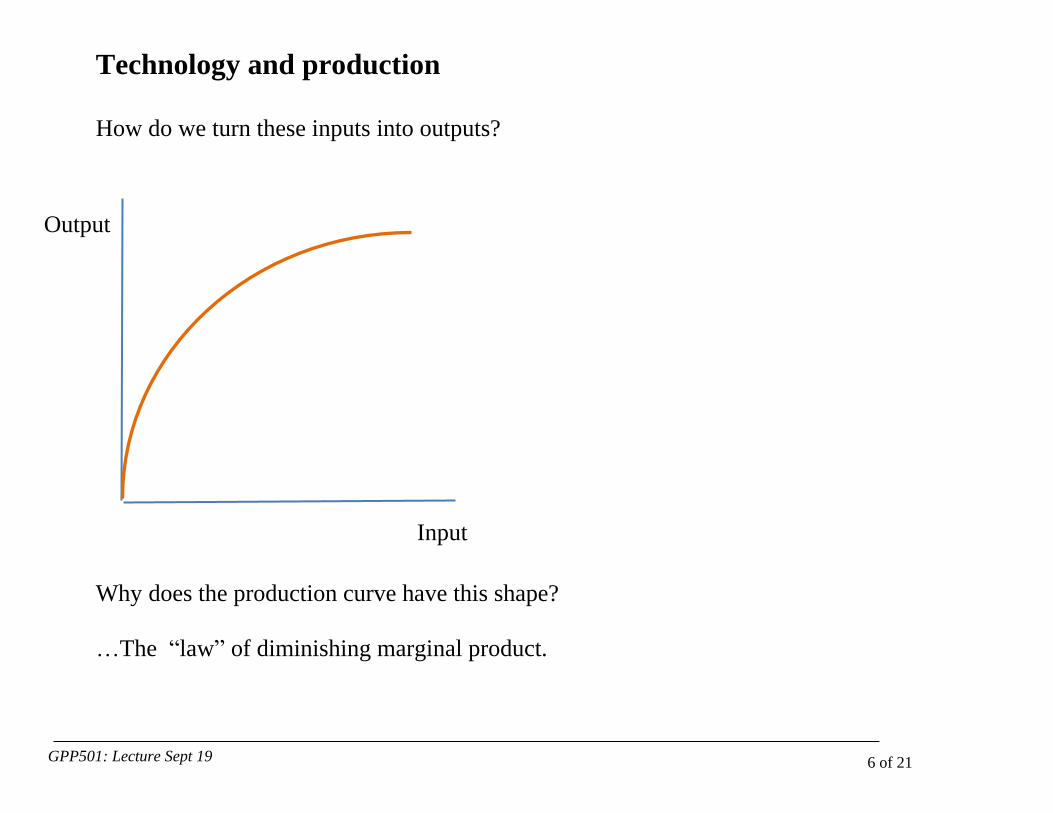

Technology and production

How do we turn these inputs into outputs?

Why does the production curve have this shape?

…The “law” of diminishing marginal product.

Output

Input

GPP501: Lecture Sept 19 7 of 21

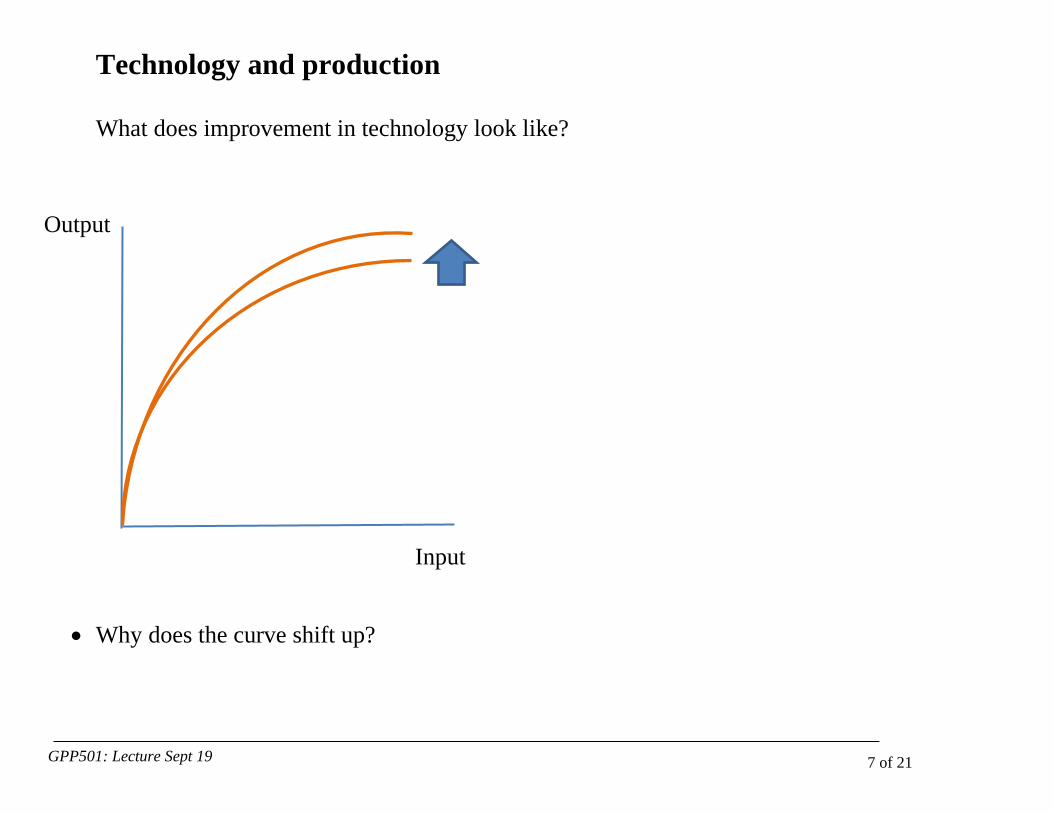

Technology and production

What does improvement in technology look like?

Why does the curve shift up?

Output

Input

GPP501: Lecture Sept 19 8 of 21

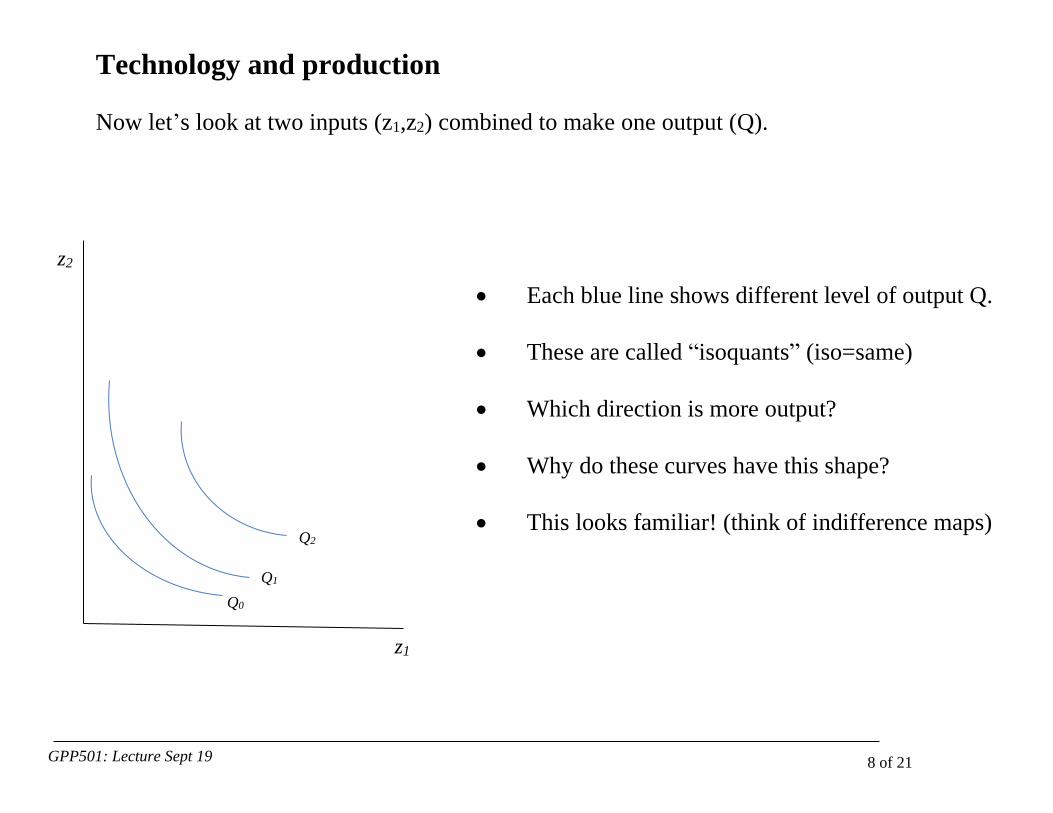

Technology and production

Now let’s look at two inputs (z1,z2) combined to make one output (Q).

Each blue line shows different level of output Q.

These are called “isoquants” (iso=same)

Which direction is more output?

Why do these curves have this shape?

This looks familiar! (think of indifference maps)

z1

z2

Q1

Q0

Q2

GPP501: Lecture Sept 19 9 of 21

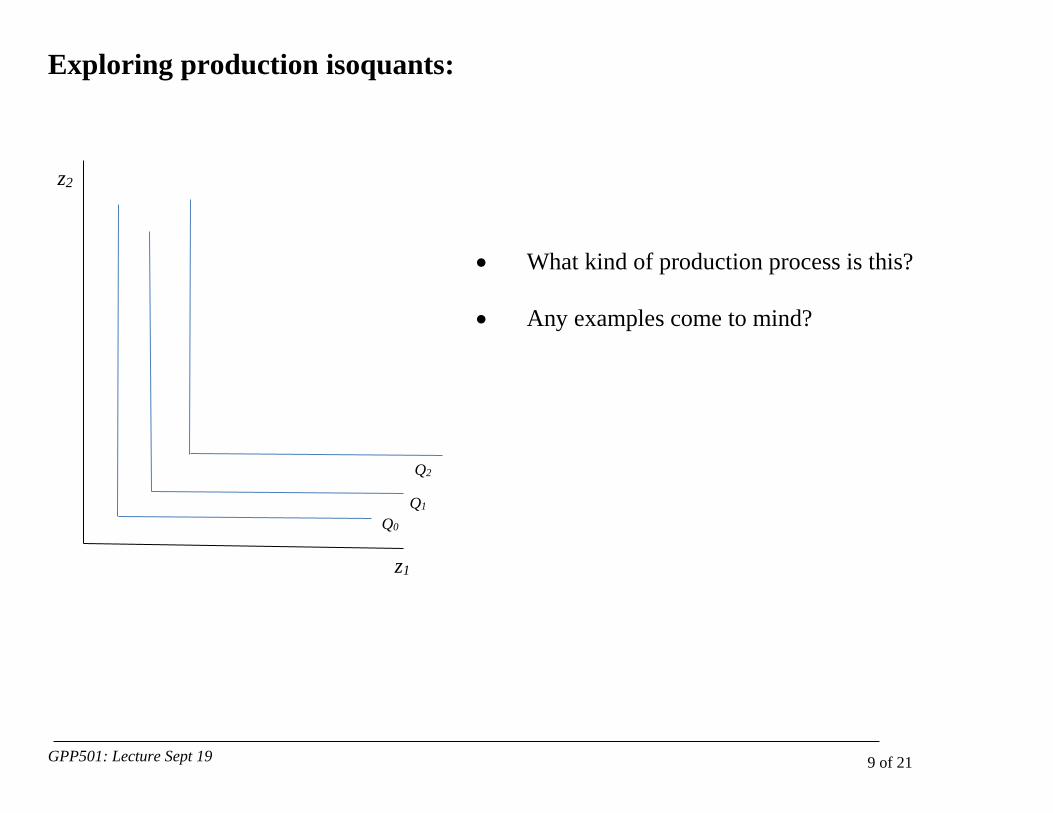

Exploring production isoquants:

What kind of production process is this?

Any examples come to mind?

z1

z2

Q1

Q0

Q2

GPP501: Lecture Sept 19 10 of 21

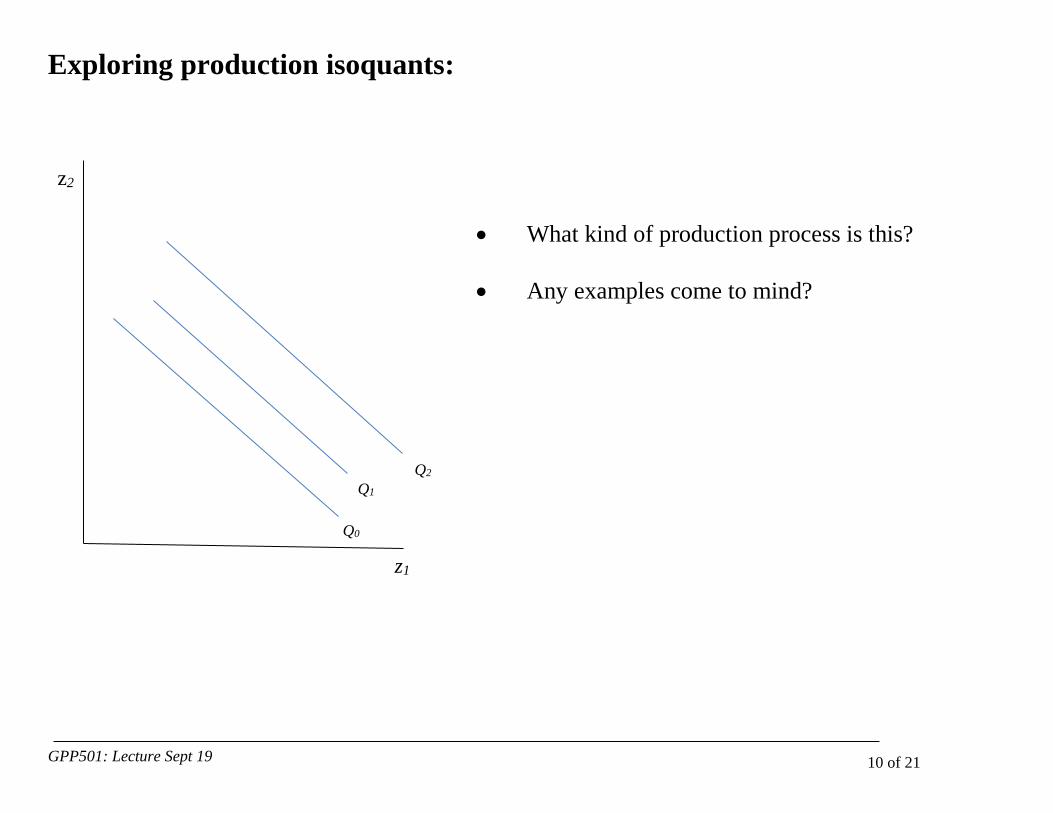

Exploring production isoquants:

What kind of production process is this?

Any examples come to mind?

z1

z2

Q1

Q0

Q2

GPP501: Lecture Sept 19 11 of 21

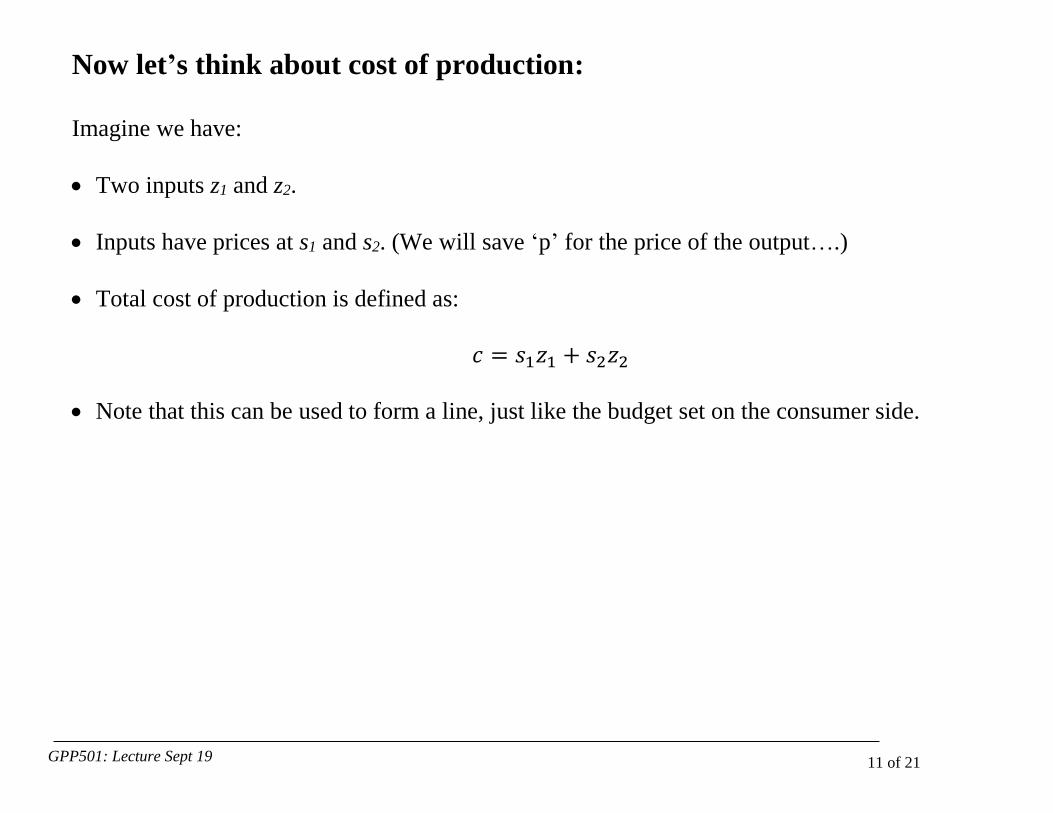

Now let’s think about cost of production:

Imagine we have:

Two inputs z1 and z2.

Inputs have prices at s1 and s2. (We will save ‘p’ for the price of the output….)

Total cost of production is defined as:

𝑐 = 𝑠1𝑧1 + 𝑠2𝑧2

Note that this can be used to form a line, just like the budget set on the consumer side.

GPP501: Lecture Sept 19 12 of 21

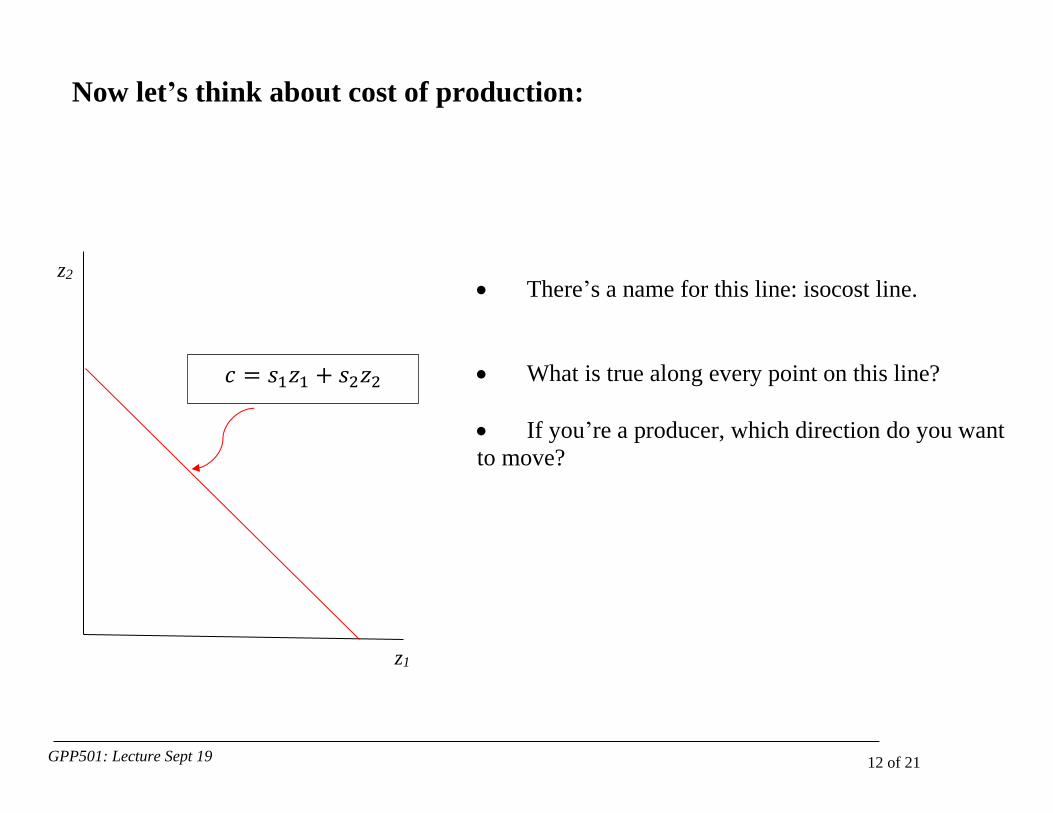

Now let’s think about cost of production:

There’s a name for this line: isocost line.

What is true along every point on this line?

If you’re a producer, which direction do you want

to move?

z1

z2

𝑐 = 𝑠1𝑧1 + 𝑠2𝑧2

GPP501: Lecture Sept 19 13 of 21

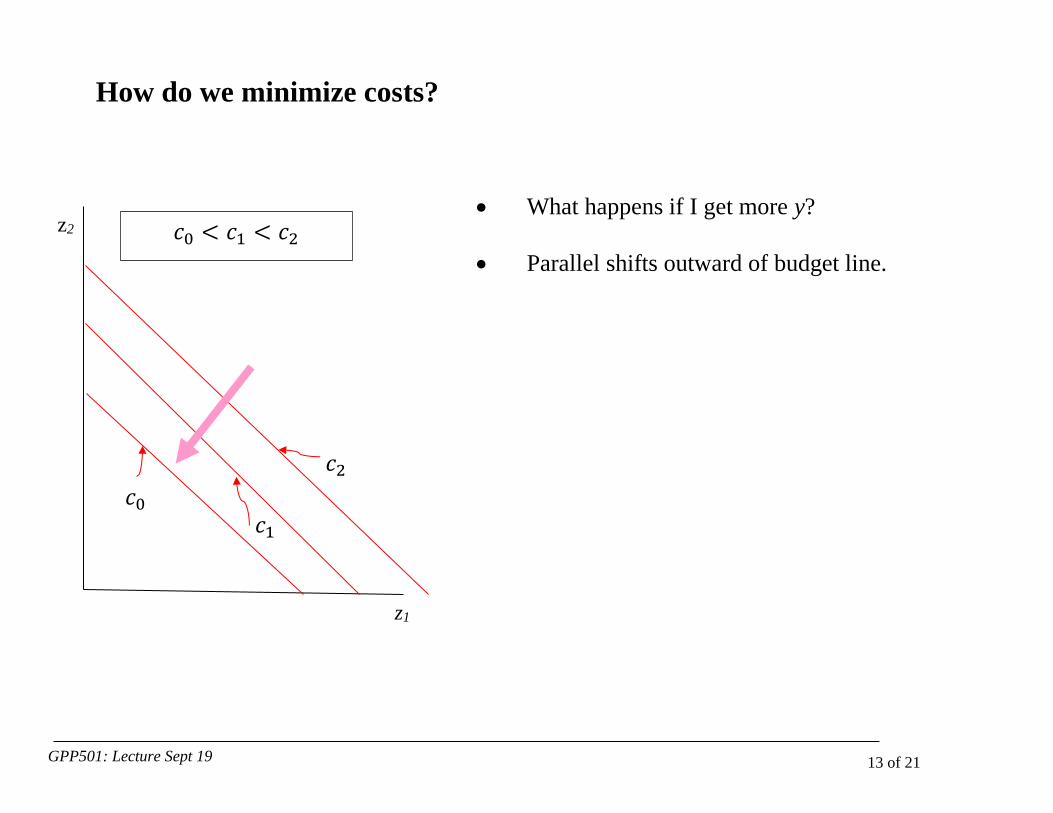

How do we minimize costs?

What happens if I get more y?

Parallel shifts outward of budget line.

z1

z2 𝑐0 < 𝑐1 < 𝑐2

𝑐0 𝑐1

𝑐2

GPP501: Lecture Sept 19 14 of 21

Agenda for today:

1. Factors of production

2. Technology and production

3. Supply Curves

4. Market equilibrium

GPP501: Lecture Sept 19 15 of 21

Putting isoquants and isocost curves together

What happens when we combine our diagrams?

Draw up the isoquants that we can make given our technology.

What is the cheapest way to make each quantity of production?

o Find the lowest cost curve on each isoquant.

Let’s give this a shot!

GPP501: Lecture Sept 19 16 of 21

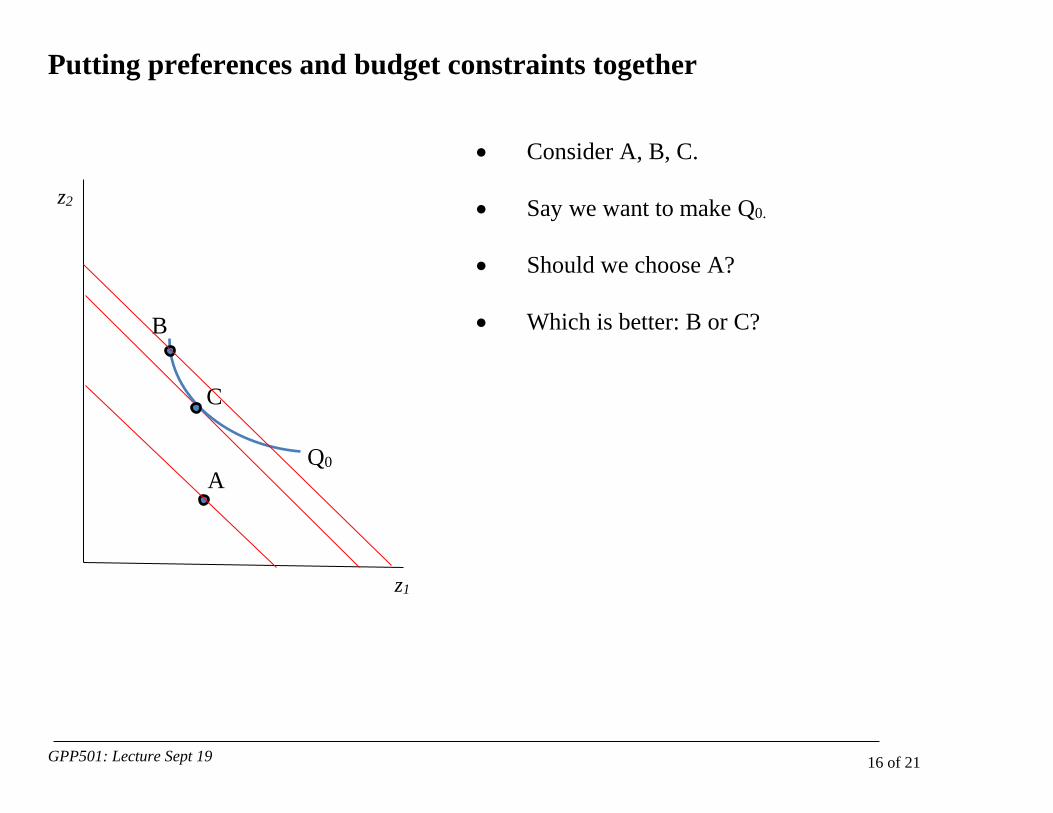

Putting preferences and budget constraints together

Consider A, B, C.

Say we want to make Q0.

Should we choose A?

Which is better: B or C?

z1

z2

C

B

A Q0

GPP501: Lecture Sept 19 17 of 21

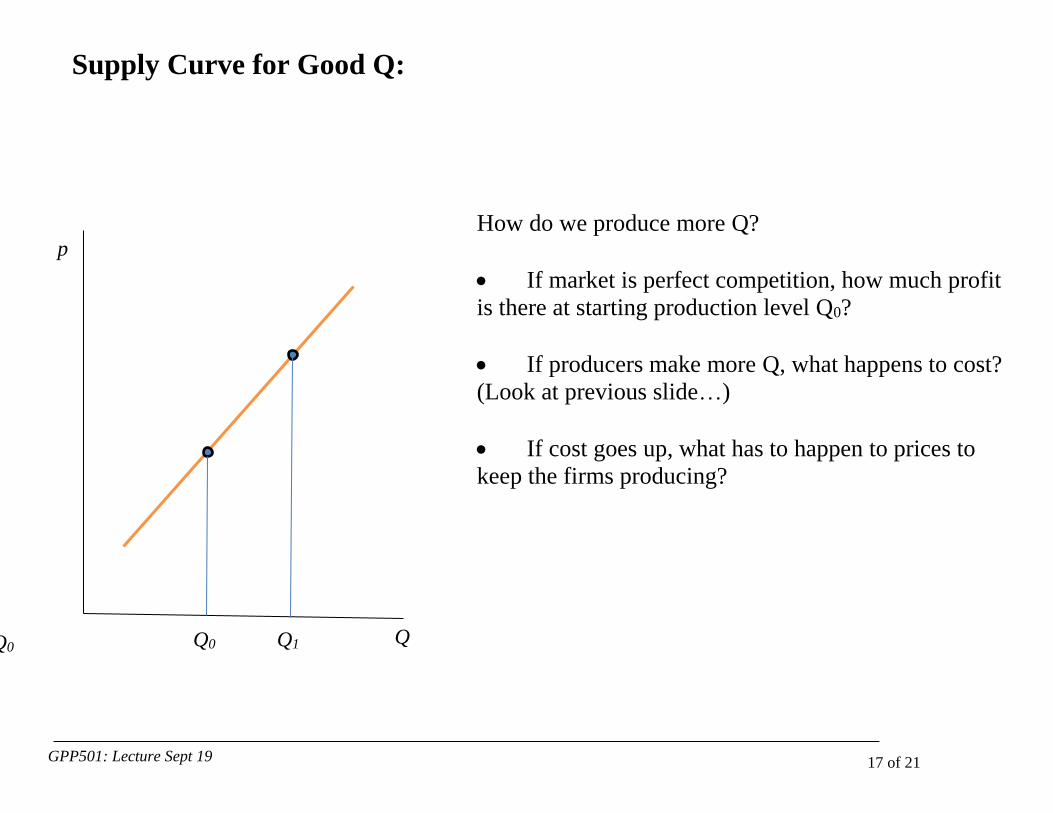

Supply Curve for Good Q:

How do we produce more Q?

If market is perfect competition, how much profit

is there at starting production level Q0?

If producers make more Q, what happens to cost?

(Look at previous slide…)

If cost goes up, what has to happen to prices to

keep the firms producing?

Q

p

Q0 Q0 Q1

GPP501: Lecture Sept 19 18 of 21

Agenda for today:

1. Factors of production

2. Technology and production

3. Supply Curves

4. Market equilibrium

GPP501: Lecture Sept 19 19 of 21

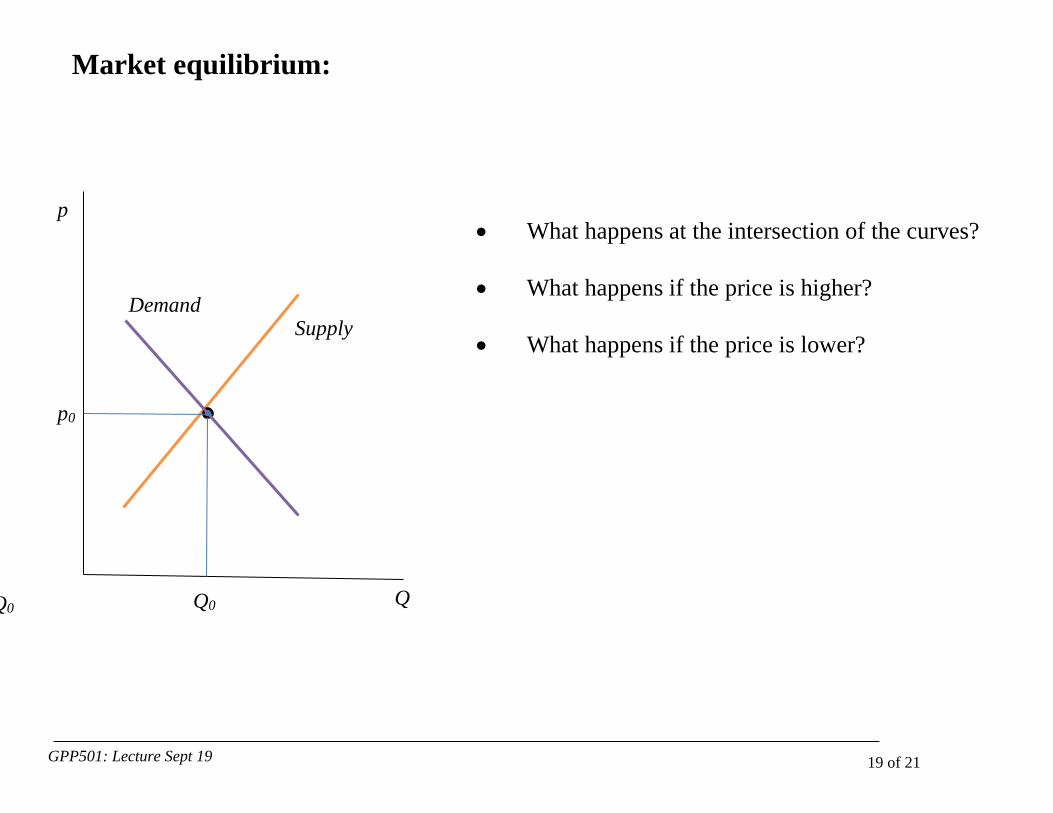

Market equilibrium:

What happens at the intersection of the curves?

What happens if the price is higher?

What happens if the price is lower?

Q

p

Q0 Q0

p0

Supply

Demand

GPP501: Lecture Sept 19 20 of 21

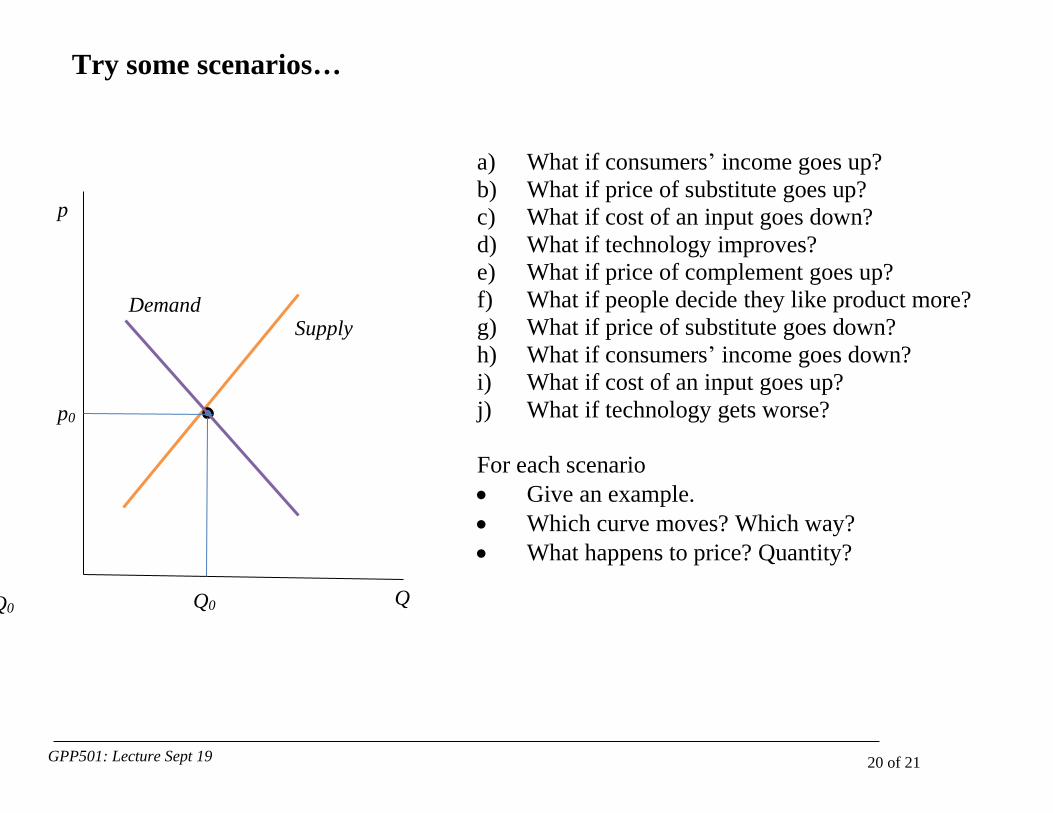

Try some scenarios…

a) What if consumers’ income goes up?

b) What if price of substitute goes up?

c) What if cost of an input goes down?

d) What if technology improves?

e) What if price of complement goes up?

f) What if people decide they like product more?

g) What if price of substitute goes down?

h) What if consumers’ income goes down?

i) What if cost of an input goes up?

j) What if technology gets worse?

For each scenario

Give an example.

Which curve moves? Which way?

What happens to price? Quantity?

Q

p

Q0 Q0

p0

Supply

Demand

GPP501: Lecture Sept 19 21 of 21

For next time…

Read through Green, Riddell, and St-Hilaire (2016).

Just pages 1-24!

Available here.