Embed Size (px)

Citation preview

GLOBAL PHARMACEUTICAL AND BIOTECHNOLOGY REPORT 2016

A CLE ARWATER INTERNAT IONAL HEALTHCARE REPORT

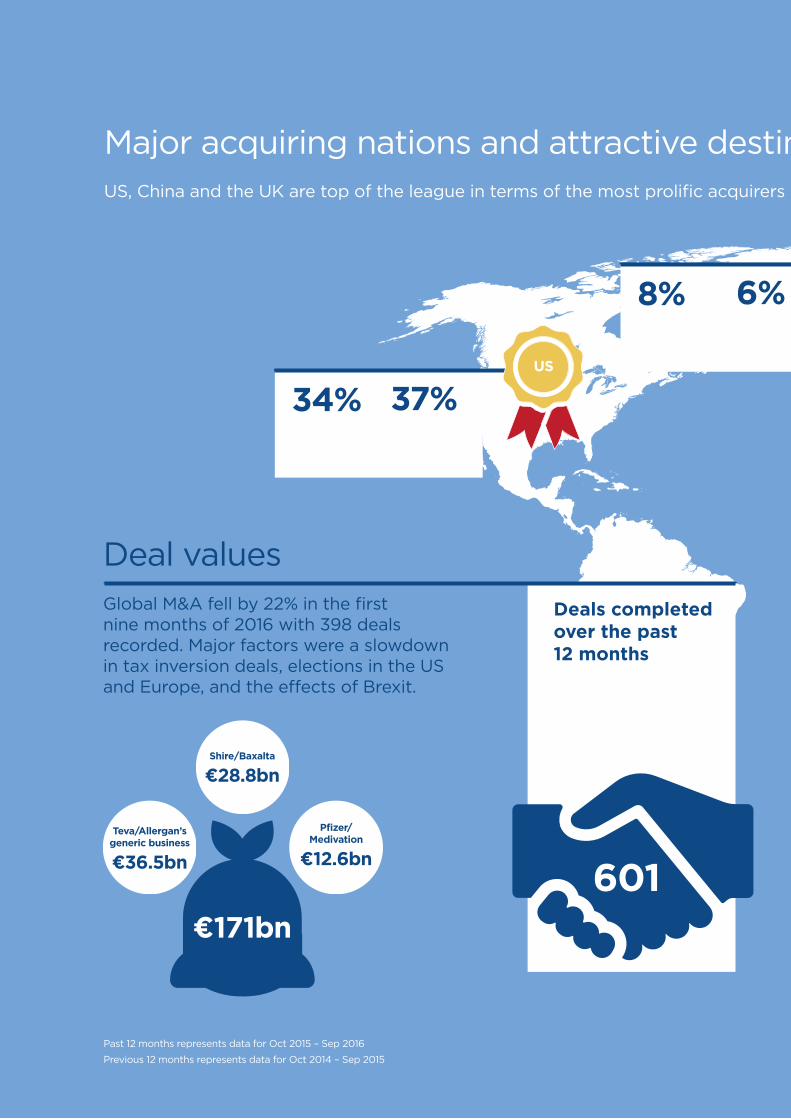

Major acquiring nations and attractive destinations

Deal values

US, China and the UK are top of the league in terms of the most prolific acquirers and favourite target destinations over the past 12 months.

Global M&A fell by 22% in the first nine months of 2016 with 398 deals recorded. Major factors were a slowdown in tax inversion deals, elections in the US and Europe, and the e�ects of Brexit.

34% deals as acquiring nation

37% as target destination

US

8% deals as acquiring nation

6% as target destination

UK

10% deals as acquiring nation

11% as target destination

China

€171bn

Teva/Allergan’s generic business

€36.5bn

Shire/Baxalta

€28.8bn

Pfizer/Medivation

€12.6bn

Deals completed over the past 12 months

A 12% decrease on the previous 12-month figure

601

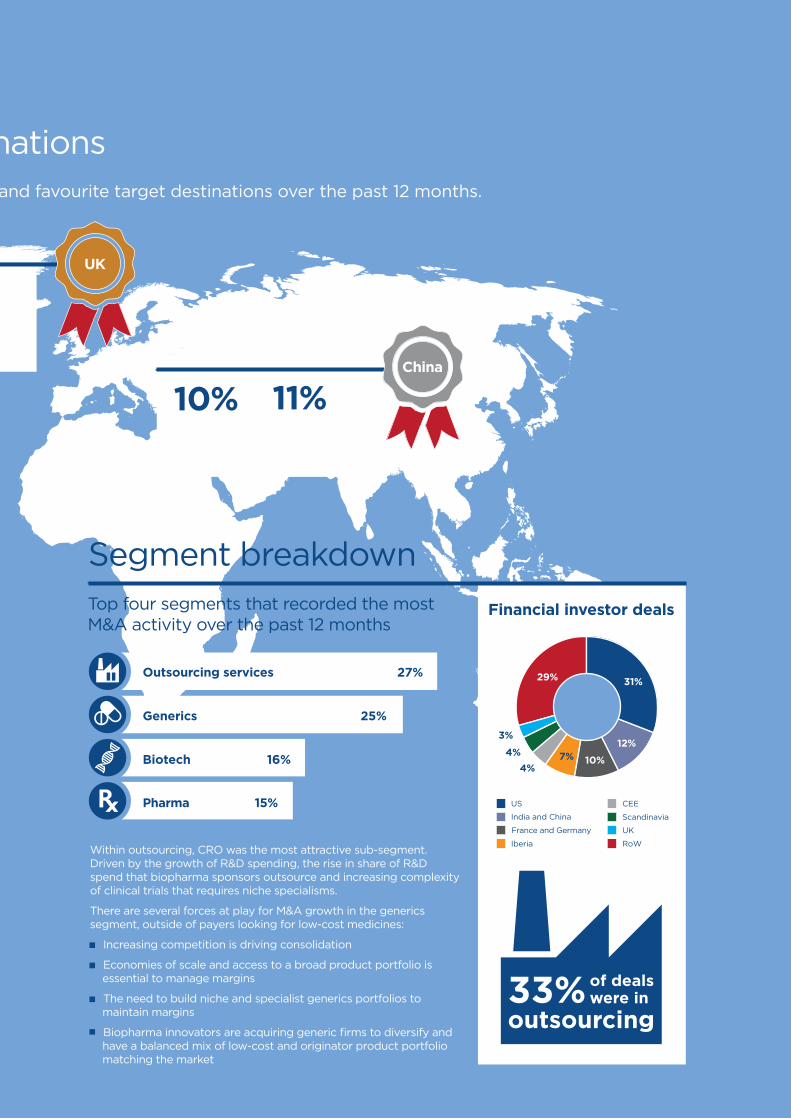

Segment breakdown Top four segments that recorded the most M&A activity over the past 12 months

Outsourcing services 27%

Generics 25%

Biotech 16%

Pharma 15%

Within outsourcing, CRO was the most attractive sub-segment. Driven by the growth of R&D spending, the rise in share of R&D spend that biopharma sponsors outsource and increasing complexity of clinical trials that requires niche specialisms.

There are several forces at play for M&A growth in the generics segment, outside of payers looking for low-cost medicines:

Increasing competition is driving consolidation

Economies of scale and access to a broad product portfolio is essential to manage margins

The need to build niche and specialist generics portfolios to maintain margins

Biopharma innovators are acquiring generic firms to diversify and have a balanced mix of low-cost and originator product portfolio matching the market

Past 12 months represents data for Oct 2015 – Sep 2016

Previous 12 months represents data for Oct 2014 – Sep 2015

4%

4%

3%

US CEE

UK

29% 31%

12%

10%7%

Financial investor deals

India and China

France and Germany

Iberia RoW

Scandinavia

33% outsourcing

of deals were in

Major acquiring nations and attractive destinations

Deal values

US, China and the UK are top of the league in terms of the most prolific acquirers and favourite target destinations over the past 12 months.

Global M&A fell by 22% in the first nine months of 2016 with 398 deals recorded. Major factors were a slowdown in tax inversion deals, elections in the US and Europe, and the e�ects of Brexit.

34% deals as acquiring nation

37% as target destination

US

8% deals as acquiring nation

6% as target destination

UK

10% deals as acquiring nation

11% as target destination

China

€171bn

Teva/Allergan’s generic business

€36.5bn

Shire/Baxalta

€28.8bn

Pfizer/Medivation

€12.6bn

Deals completed over the past 12 months

A 12% decrease on the previous 12-month figure

601

Segment breakdown Top four segments that recorded the most M&A activity over the past 12 months

Outsourcing services 27%

Generics 25%

Biotech 16%

Pharma 15%

Within outsourcing, CRO was the most attractive sub-segment. Driven by the growth of R&D spending, the rise in share of R&D spend that biopharma sponsors outsource and increasing complexity of clinical trials that requires niche specialisms.

There are several forces at play for M&A growth in the generics segment, outside of payers looking for low-cost medicines:

Increasing competition is driving consolidation

Economies of scale and access to a broad product portfolio is essential to manage margins

The need to build niche and specialist generics portfolios to maintain margins

Biopharma innovators are acquiring generic firms to diversify and have a balanced mix of low-cost and originator product portfolio matching the market

Past 12 months represents data for Oct 2015 – Sep 2016

Previous 12 months represents data for Oct 2014 – Sep 2015

4%

4%

3%

US CEE

UK

29% 31%

12%

10%7%

Financial investor deals

India and China

France and Germany

Iberia RoW

Scandinavia

33% outsourcing

of deals were in

4 GLOBAL PHARMACEUT I C AL AND B I OTEC H NOLOG Y R EP ORT 20 16

Welcome

The total deals inked by pharma & biotech companies in the first nine months of 2016 indicate a decline in deal volume by 22% compared to 2015. This, however, is not surprising given the state of markets and the withdrawal of many serial acquirers. The Brexit ripple effect across Europe, the slowdown in tax inversion practices, and elections in the US and Europe have slowed down the pace of M&A activity in 2016.

Only time will tell what impact the shock result of the US election will have amid fears that more protectionist trade policies may restrict access to the US pharma market.

Given that global M&A was again dominated by the US in 2016 this becomes even more significant. The US remains both the top acquirer and the most popular target for M&A activity in the pharma and biotech space.

For instance we have recently seen Quintiles Transnational's merger with IMS Health; Cambrex's acquisition of API manufacturer Pharmacore; and the sale of Actavis' generic assets and operations in the UK and Ireland to Accord Healthcare.

Meanwhile a recent trend has been the acquisition of biotech firms by pharma companies to strengthen their market share, and this has continued this year. Shire spent €28.9bn on buying Baxalta and €5.9bn on Dyax Corp, while Pfizer recently completed its €12.6bn acquisition of Medivation. Other deals include AbbVie’s €5.5bn acquisition of Stemcentrx, and AstraZeneca’s €3.6bn purchase of Acerta Pharma and €2.4bn acquisition of ZS Pharma.

General M&A activity has remained strong in recent weeks. For instance, Elanco acquired Boehringer Ingelheim Vetmedica Inc, and AstraZeneca announced that MedImmune, its global biologics research and development arm, had entered into a licensing agreement with Allergan for the global rights to MEDI2070.

In this report we take an in-depth look at the performance of different markets globally, while also capturing the segments within the pharma & biotech sector that are likely to witness the strongest growth over the next few years.

We hope you enjoy the read.

4

@CWICF

/company/clearwater-international-corporate-finance

Meet the team

Ramesh Jassal International Head of Healthcare, UK +44 845 052 0374 [email protected]

Franc Kaiser Partner, China + 86 21 6341 0699 x 850 [email protected]

Louise Kamp Nørbæk Associate Director, Denmark +45 40 17 86 90 [email protected]

Philippe Guezenec Partner, France +33 1 53 89 0504 [email protected]

Markus Otto Partner, Germany +49 611 360 39 24 [email protected]

John Curtin Partner, Ireland +353 1 517 58 42 [email protected]

Rui Miranda Partner, Portugal +351 918 766 799 [email protected]

Miguel Ángel Lorenzo Director, Spain +34 659 094 041 [email protected]

ContentsGLOBAL MARKET 6

Major deal drivers

Highlights

Top 10 global deals

US 12

UK 14

IRELAND 17

IBERIA 18

FRANCE AND GERMANY 20

SCANDINAVIA 22

CEE 24

INDIA AND CHINA 25

RECENT CLEARWATER INTERNATIONAL DEALS 27

For the purposes of this report, we have quoted all figures in Euros using the following average exchange rates:

Oct 2015 – Sep 2016 USD to EUR: 0.901 Oct 2014 – Sep 2015 USD to EUR: 0.873 Oct 2015 – Sep 2016 GBP to EUR: 1.287 Oct 2014 – Sep 2015 GBP to EUR: 1.348 Oct 2015 – Sep 2016 CNY to EUR: 0.138 Oct 2014 – Sep 2015 CNY to EUR: 0.140 Oct 2015 – Sep 2016 INR to EUR: 0.013 Oct 2014 – Sep 2015 INR to EUR: 0.014

This report is published by Clearwater International Editors: Ruth Farrington and Jim PendrillDesign: www.creative-bridge.comSubscription: [email protected] part of this publication may be reproduced or used in any form without prior permission of Clearwater International

A CL E A RWA TE R IN TE RN A T ION A L HE A L THCA RE REPORT 5

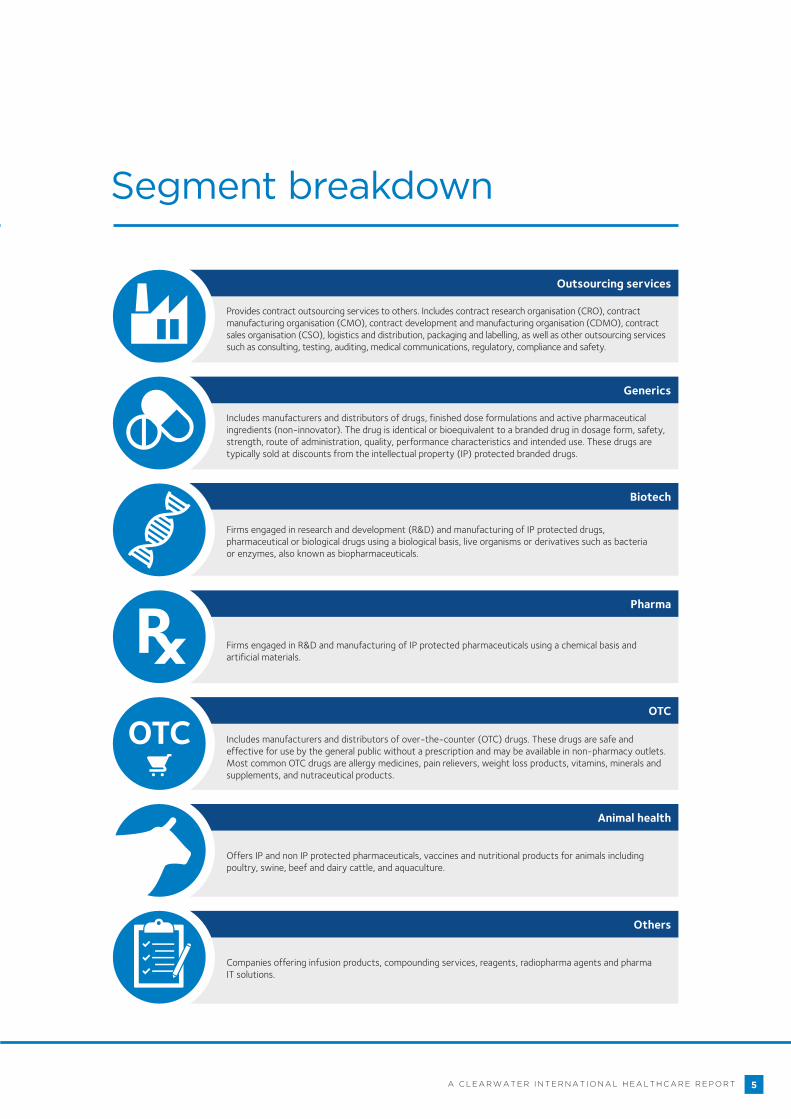

Segment breakdown

Others

Companies offering infusion products, compounding services, reagents, radiopharma agents and pharma IT solutions.

Animal health

Offers IP and non IP protected pharmaceuticals, vaccines and nutritional products for animals including poultry, swine, beef and dairy cattle, and aquaculture.

OTC

Includes manufacturers and distributors of over-the-counter (OTC) drugs. These drugs are safe and effective for use by the general public without a prescription and may be available in non-pharmacy outlets. Most common OTC drugs are allergy medicines, pain relievers, weight loss products, vitamins, minerals and supplements, and nutraceutical products.

Pharma

Firms engaged in R&D and manufacturing of IP protected pharmaceuticals using a chemical basis and artificial materials.

Biotech

Firms engaged in research and development (R&D) and manufacturing of IP protected drugs, pharmaceutical or biological drugs using a biological basis, live organisms or derivatives such as bacteria or enzymes, also known as biopharmaceuticals.

Generics

Includes manufacturers and distributors of drugs, finished dose formulations and active pharmaceutical ingredients (non-innovator). The drug is identical or bioequivalent to a branded drug in dosage form, safety, strength, route of administration, quality, performance characteristics and intended use. These drugs are typically sold at discounts from the intellectual property (IP) protected branded drugs.

Outsourcing services

Provides contract outsourcing services to others. Includes contract research organisation (CRO), contract manufacturing organisation (CMO), contract development and manufacturing organisation (CDMO), contract sales organisation (CSO), logistics and distribution, packaging and labelling, as well as other outsourcing services such as consulting, testing, auditing, medical communications, regulatory, compliance and safety.

Global market

Global M&A witnessed a slowdown in 2016 after posting record numbers of deals in 2014 and 2015. In the first nine months of 2016, global M&A was down 22%, compared with 2015, with total deal value falling from €271bn to €138bn.

Stringent regulatory changes, a slowdown in tax inversion practices and other macro events and uncertainties - including the Brexit vote and US and European elections - have caused M&A activity to move at a steady pace.

However, after a slow start to the year deal volumes are expected to rebound in the latter part of 2016. The past 12 months have seen an at-par performance in terms of deal volume, but lower values than the preceding 12 months.

Oct 14 - Sep 15

Oct 15 - Sep 16

Deal count 684 601

Total value (€bn) 304 171

So far 2016 has recorded 398 deals in the pharma & biotech market, with the most activity taking place in the outsourcing services sector.

6

M&A acquirer by country

Over the past year the US has been the most prolific acquirer and led the way with 34% of total closed transactions, compared to 32% in the preceding 12 months. China represented 10%, followed by the UK (8%).

In terms of acquisition targets, the US again led the way with 37% of total global M&A activity, followed by China (11%) and the UK (6%).

Apart from the US, the UK and Ireland have emerged as attractive target destinations as companies, mainly based in the US, relocate their headquarters to countries with lower corporate taxes.

This practise, known as ‘tax inversion’, has been a major driver of cross-border transactions in recent years. However, the US government has now curbed the practice by passing legislation that limits the size of the foreign entity. One of the deal casualties was the collapse of Pfizer and Allergan’s €134bn merger in April 2016.

The patent cliff also led to a new wave of mega-mergers and consolidation in the pharma & biotech sector. In the last 12 months we have seen 24 deals above the €1bn transaction value mark.

US

Others

China

UK

India

Canada

France

34%

34%

10%

8%

6%

4%4%

GLOBAL PHARMACEUT I C AL AND B I OTEC H NOLOG Y R EP ORT 20 16

A CL E A RWA TE R IN TE RN A T ION A L HE A L THCA RE REPORT 7

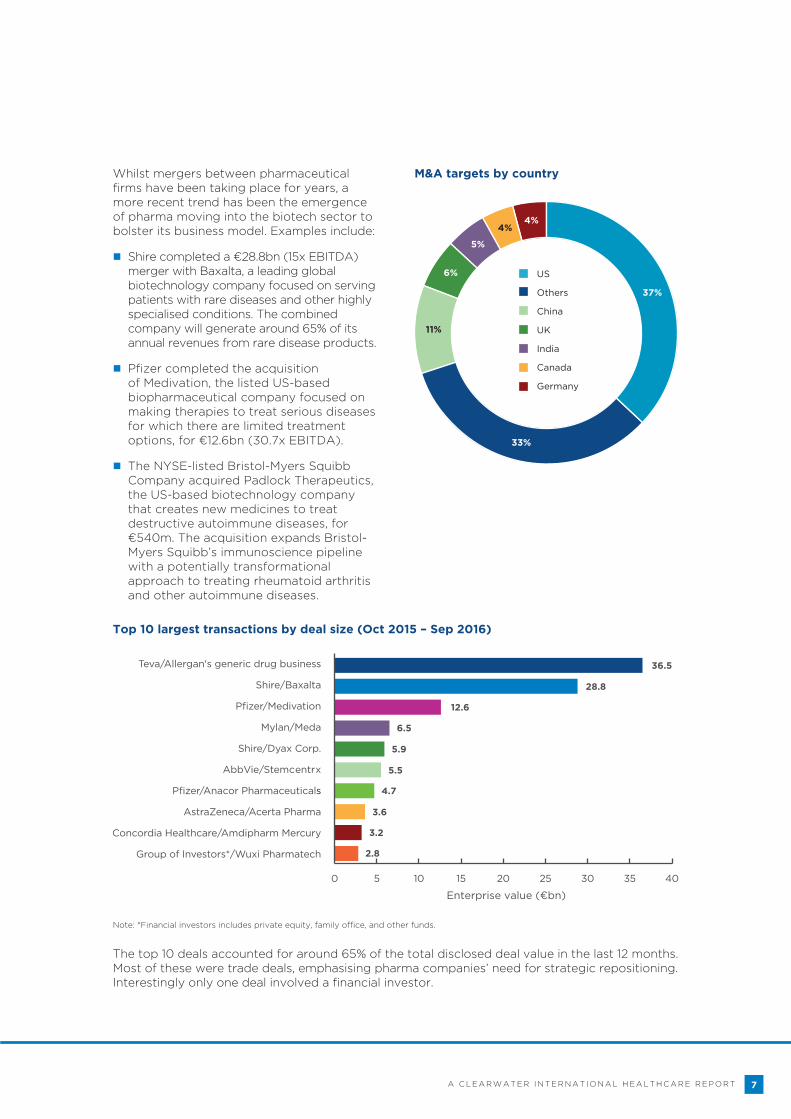

Whilst mergers between pharmaceutical firms have been taking place for years, a more recent trend has been the emergence of pharma moving into the biotech sector to bolster its business model. Examples include:

Shire completed a €28.8bn (15x EBITDA) merger with Baxalta, a leading global biotechnology company focused on serving patients with rare diseases and other highly specialised conditions. The combined company will generate around 65% of its annual revenues from rare disease products.

Pfizer completed the acquisition of Medivation, the listed US-based biopharmaceutical company focused on making therapies to treat serious diseases for which there are limited treatment options, for €12.6bn (30.7x EBITDA).

The NYSE-listed Bristol-Myers Squibb Company acquired Padlock Therapeutics, the US-based biotechnology company that creates new medicines to treat destructive autoimmune diseases, for €540m. The acquisition expands Bristol-Myers Squibb’s immunoscience pipeline with a potentially transformational approach to treating rheumatoid arthritis and other autoimmune diseases.

Top 10 largest transactions by deal size (Oct 2015 – Sep 2016)

Note: *Financial investors includes private equity, family office, and other funds.

The top 10 deals accounted for around 65% of the total disclosed deal value in the last 12 months. Most of these were trade deals, emphasising pharma companies’ need for strategic repositioning. Interestingly only one deal involved a financial investor.

M&A targets by country

37%

33%

11%

6%

5%

4%4%

US

Others

China

UK

India

Canada

Germany

36.5

28.8

12.6

6.5

5.9

5.5

4.7

3.6

3.2

2.8

Enterprise value (€bn)

8

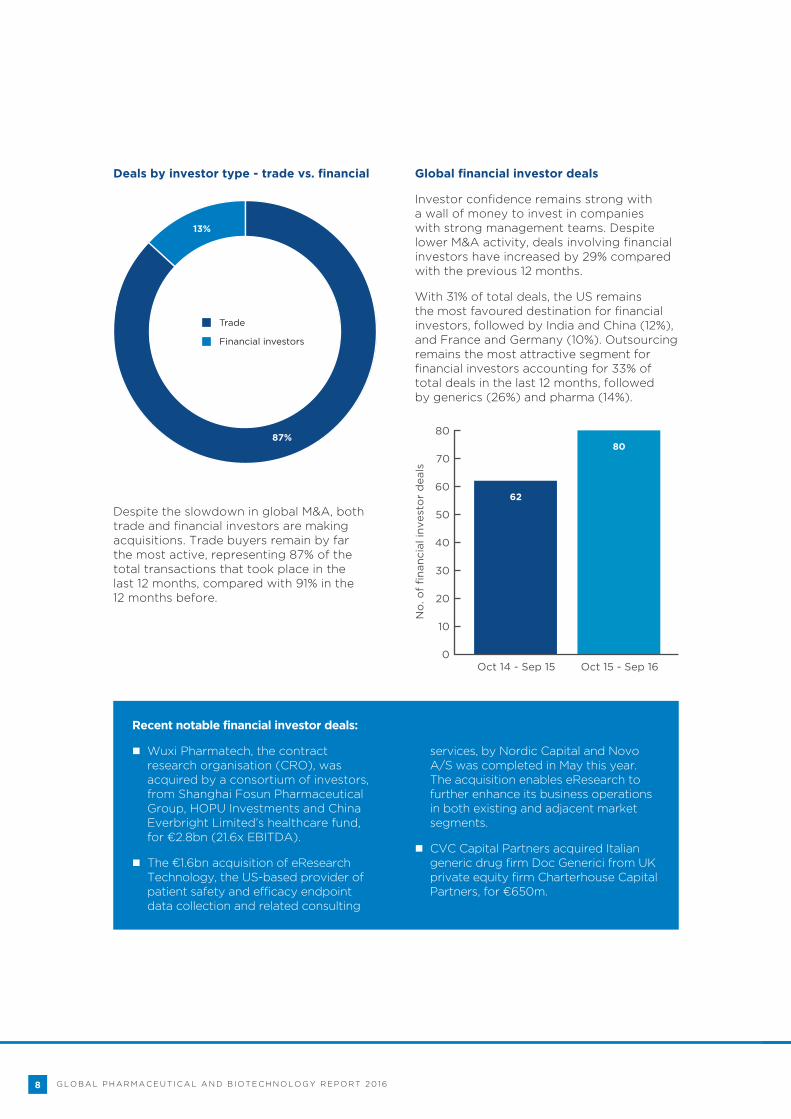

Deals by investor type - trade vs. financial

Despite the slowdown in global M&A, both trade and financial investors are making acquisitions. Trade buyers remain by far the most active, representing 87% of the total transactions that took place in the last 12 months, compared with 91% in the 12 months before.

Recent notable financial investor deals:

Wuxi Pharmatech, the contract research organisation (CRO), was acquired by a consortium of investors, from Shanghai Fosun Pharmaceutical Group, HOPU Investments and China Everbright Limited’s healthcare fund, for €2.8bn (21.6x EBITDA).

The €1.6bn acquisition of eResearch Technology, the US-based provider of patient safety and efficacy endpoint data collection and related consulting

services, by Nordic Capital and Novo A/S was completed in May this year. The acquisition enables eResearch to further enhance its business operations in both existing and adjacent market segments.

CVC Capital Partners acquired Italian generic drug firm Doc Generici from UK private equity firm Charterhouse Capital Partners, for €650m.

Trade

Financial investors

0

10

20

30

40

50

60

70

80

Oct 14 - Sep 15 Oct 15 - Sep 16

No

. of

fina

ncia

l inv

esto

r d

eals

Global financial investor deals

Investor confidence remains strong with a wall of money to invest in companies with strong management teams. Despite lower M&A activity, deals involving financial investors have increased by 29% compared with the previous 12 months.

With 31% of total deals, the US remains the most favoured destination for financial investors, followed by India and China (12%), and France and Germany (10%). Outsourcing remains the most attractive segment for financial investors accounting for 33% of total deals in the last 12 months, followed by generics (26%) and pharma (14%).

62

80

13%

87%

GLOBAL PHARMACEUT I C AL AND B I OTEC H NOLOG Y R EP ORT 20 16

A CL E A RWA TE R IN TE RN A T ION A L HE A L THCA RE REPORT 9

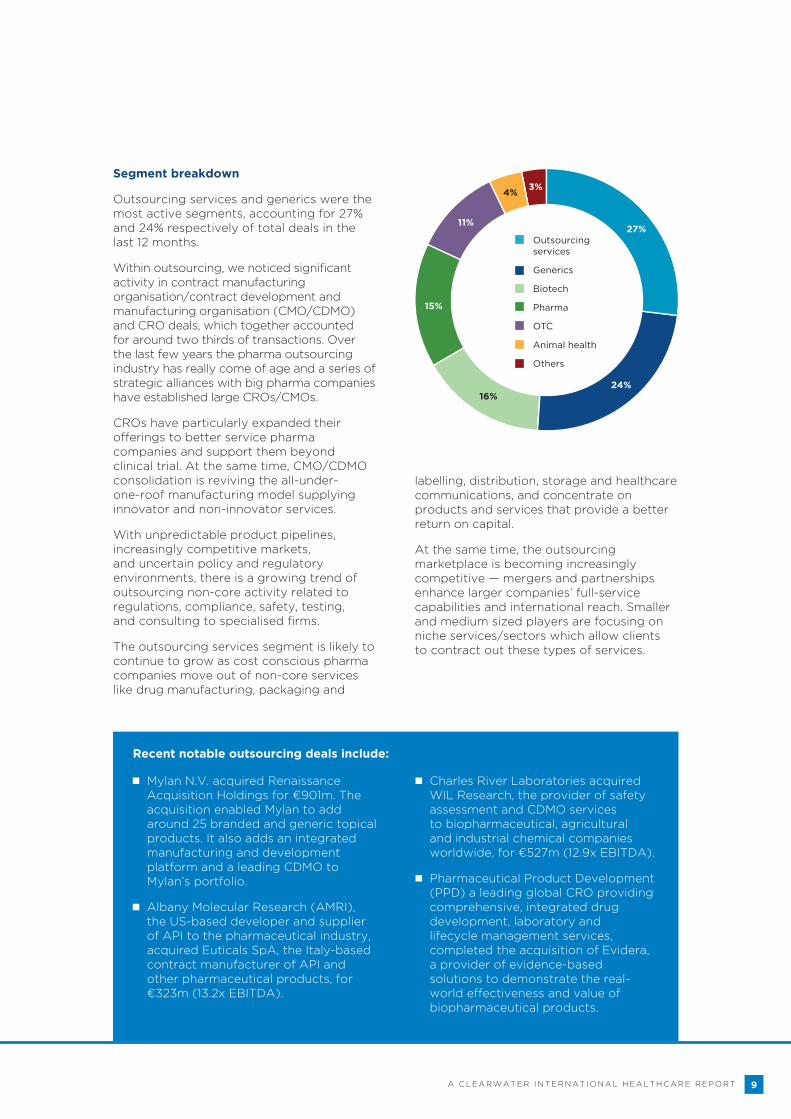

Segment breakdown

Outsourcing services and generics were the most active segments, accounting for 27% and 24% respectively of total deals in the last 12 months.

Within outsourcing, we noticed significant activity in contract manufacturing organisation/contract development and manufacturing organisation (CMO/CDMO) and CRO deals, which together accounted for around two thirds of transactions. Over the last few years the pharma outsourcing industry has really come of age and a series of strategic alliances with big pharma companies have established large CROs/CMOs.

CROs have particularly expanded their offerings to better service pharma companies and support them beyond clinical trial. At the same time, CMO/CDMO consolidation is reviving the all-under-one-roof manufacturing model supplying innovator and non-innovator services.

With unpredictable product pipelines, increasingly competitive markets, and uncertain policy and regulatory environments, there is a growing trend of outsourcing non-core activity related to regulations, compliance, safety, testing, and consulting to specialised firms.

The outsourcing services segment is likely to continue to grow as cost conscious pharma companies move out of non-core services like drug manufacturing, packaging and

Mylan N.V. acquired Renaissance Acquisition Holdings for €901m. The acquisition enabled Mylan to add around 25 branded and generic topical products. It also adds an integrated manufacturing and development platform and a leading CDMO to Mylan’s portfolio.

Albany Molecular Research (AMRI), the US-based developer and supplier of API to the pharmaceutical industry, acquired Euticals SpA, the Italy-based contract manufacturer of API and other pharmaceutical products, for €323m (13.2x EBITDA).

Charles River Laboratories acquired WIL Research, the provider of safety assessment and CDMO services to biopharmaceutical, agricultural and industrial chemical companies worldwide, for €527m (12.9x EBITDA).

Pharmaceutical Product Development (PPD) a leading global CRO providing comprehensive, integrated drug development, laboratory and lifecycle management services, completed the acquisition of Evidera, a provider of evidence-based solutions to demonstrate the real-world effectiveness and value of biopharmaceutical products.

Recent notable outsourcing deals include:

Outsourcing services

Generics

Biotech

Pharma

OTC

Animal health

Others

27%

24%16%

15%

11%

4%3%

labelling, distribution, storage and healthcare communications, and concentrate on products and services that provide a better return on capital.

At the same time, the outsourcing marketplace is becoming increasingly competitive — mergers and partnerships enhance larger companies’ full-service capabilities and international reach. Smaller and medium sized players are focusing on niche services/sectors which allow clients to contract out these types of services.

10

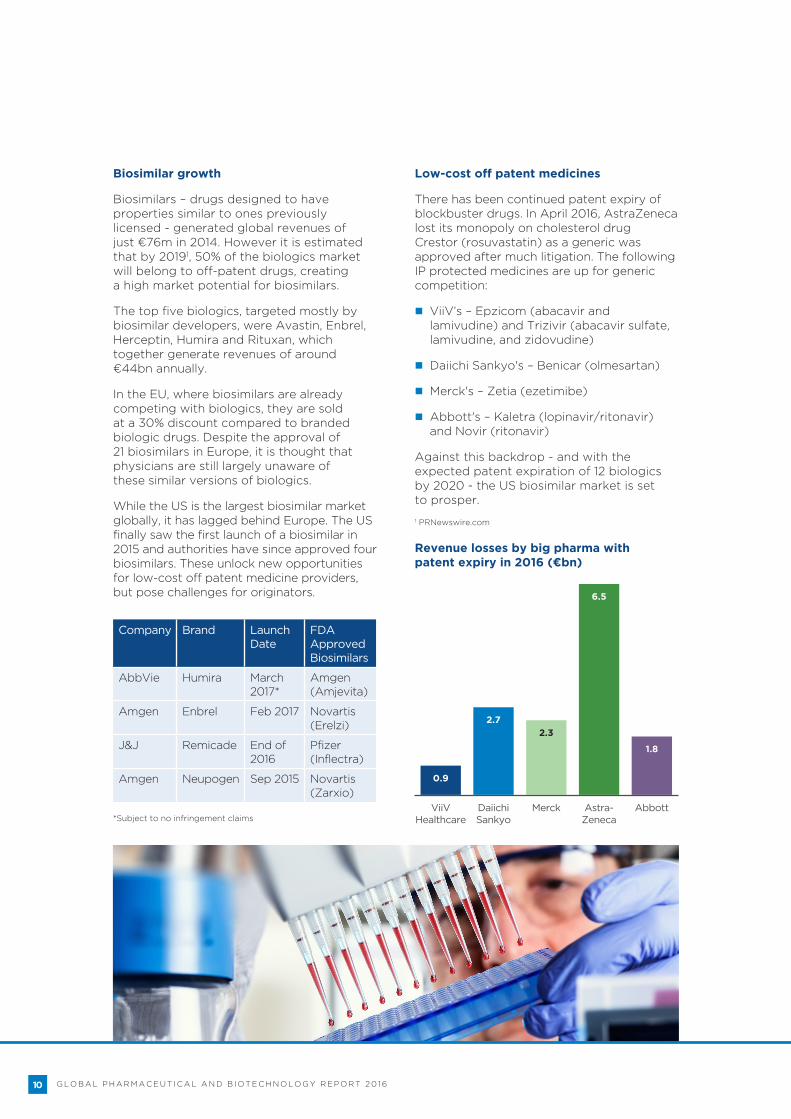

Biosimilar growth

Biosimilars – drugs designed to have properties similar to ones previously licensed - generated global revenues of just €76m in 2014. However it is estimated that by 20191, 50% of the biologics market will belong to off-patent drugs, creating a high market potential for biosimilars.

The top five biologics, targeted mostly by biosimilar developers, were Avastin, Enbrel, Herceptin, Humira and Rituxan, which together generate revenues of around €44bn annually.

In the EU, where biosimilars are already competing with biologics, they are sold at a 30% discount compared to branded biologic drugs. Despite the approval of 21 biosimilars in Europe, it is thought that physicians are still largely unaware of these similar versions of biologics.

While the US is the largest biosimilar market globally, it has lagged behind Europe. The US finally saw the first launch of a biosimilar in 2015 and authorities have since approved four biosimilars. These unlock new opportunities for low-cost off patent medicine providers, but pose challenges for originators.

GLOBAL PHARMACEUT I C AL AND B I OTEC H NOLOG Y R EP ORT 20 16

Company Brand Launch Date

FDA Approved Biosimilars

AbbVie Humira March 2017*

Amgen (Amjevita)

Amgen Enbrel Feb 2017 Novartis (Erelzi)

J&J Remicade End of 2016

Pfizer (Inflectra)

Amgen Neupogen Sep 2015 Novartis (Zarxio)

*Subject to no infringement claims

Low-cost off patent medicines

There has been continued patent expiry of blockbuster drugs. In April 2016, AstraZeneca lost its monopoly on cholesterol drug Crestor (rosuvastatin) as a generic was approved after much litigation. The following IP protected medicines are up for generic competition:

ViiV’s – Epzicom (abacavir and lamivudine) and Trizivir (abacavir sulfate, lamivudine, and zidovudine)

Daiichi Sankyo's – Benicar (olmesartan)

Merck's – Zetia (ezetimibe)

Abbott's – Kaletra (lopinavir/ritonavir) and Novir (ritonavir)

Against this backdrop - and with the expected patent expiration of 12 biologics by 2020 - the US biosimilar market is set to prosper.

1 PRNewswire.com

Revenue losses by big pharma with patent expiry in 2016 (€bn)

0.9

2.72.3

6.5

1.8

ViiV Healthcare

Daiichi Sankyo

Merck Astra-Zeneca

Abbott

A CL E A RWA TE R IN TE RN A T ION A L HE A L THCA RE REPORT 11

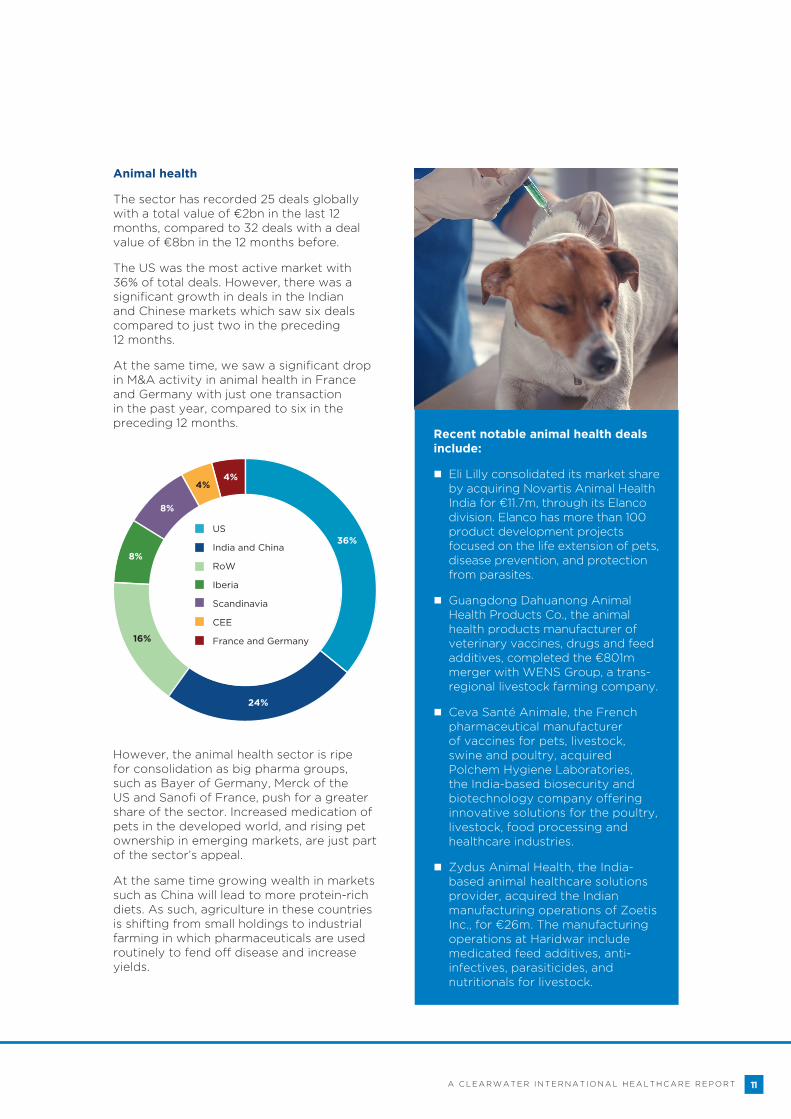

However, the animal health sector is ripe for consolidation as big pharma groups, such as Bayer of Germany, Merck of the US and Sanofi of France, push for a greater share of the sector. Increased medication of pets in the developed world, and rising pet ownership in emerging markets, are just part of the sector’s appeal.

At the same time growing wealth in markets such as China will lead to more protein-rich diets. As such, agriculture in these countries is shifting from small holdings to industrial farming in which pharmaceuticals are used routinely to fend off disease and increase yields.

US

India and China

RoW

Iberia

Scandinavia

CEE

France and Germany

36%

24%

16%

8%

8%

4%4%

Recent notable animal health deals include:

Eli Lilly consolidated its market share by acquiring Novartis Animal Health India for €11.7m, through its Elanco division. Elanco has more than 100 product development projects focused on the life extension of pets, disease prevention, and protection from parasites.

Guangdong Dahuanong Animal Health Products Co., the animal health products manufacturer of veterinary vaccines, drugs and feed additives, completed the €801m merger with WENS Group, a trans-regional livestock farming company.

Ceva Santé Animale, the French pharmaceutical manufacturer of vaccines for pets, livestock, swine and poultry, acquired Polchem Hygiene Laboratories, the India-based biosecurity and biotechnology company offering innovative solutions for the poultry, livestock, food processing and healthcare industries.

Zydus Animal Health, the India-based animal healthcare solutions provider, acquired the Indian manufacturing operations of Zoetis Inc., for €26m. The manufacturing operations at Haridwar include medicated feed additives, anti-infectives, parasiticides, and nutritionals for livestock.

Animal health

The sector has recorded 25 deals globally with a total value of €2bn in the last 12 months, compared to 32 deals with a deal value of €8bn in the 12 months before.

The US was the most active market with 36% of total deals. However, there was a significant growth in deals in the Indian and Chinese markets which saw six deals compared to just two in the preceding 12 months.

At the same time, we saw a significant drop in M&A activity in animal health in France and Germany with just one transaction in the past year, compared to six in the preceding 12 months.

12

US market2016 so far has recorded 152 deals with a combined value of around €114bn.

We have seen 225 deals worth €127bn in the last 12 months, compared to 229 deals worth €222bn in the previous 12-month period. Continued low interest rates and the intention of big pharma to buy biotech and smaller firms to bolster their pipelines were the main reasons for deal activity.

Major deal drivers

Cheap debt financing has particularly pushed the pharma deal environment in the US. Corporate debt offerings have become the go-to option for pharmaceutical companies looking to fund deals. Some debt financed pharma and biotech deals include: Pfizer’s acquisition of Hospira; Actavis’ acquisition of Allergan; Teva’s acquisition of Allergan’s generic business; and Valeant’s acquisition of Salix Pharmaceuticals.

Apart from consolidation and mega mergers, pharma companies are also looking for therapeutics and smaller biotech companies through targeted acquisitions and partnerships designed to strengthen innovative drug portfolios. Pfizer's acquisition of Anacor and Bristol-Myers Squibb's acquisition of Padlock Therapeutics exemplify this trend.

Deals by investor type - trade vs. financial

Trade buyers constituted the biggest share, representing 89% of total transactions in the last 12 months, a slight decline compared to 93% in the previous 12-month period. Despite lower M&A activity, investor confidence remains strong in the US market, and we recorded 25 deals compared with 17 deals in the previous 12 months.

0

5

10

15

20

25

Oct 14 - Sep 15 Oct 15 - Sep 16

17

25

No

. of

fina

ncia

l inv

esto

r d

eals

PaxVax, the US-based vaccine company that develops and commercialises vaccine candidates against various infectious diseases, was acquired by Cerberus Capital Management for €95m.

Sofinnova Partners, the France-based venture capital firm, and Novo, the Denmark-based private equity firm, acquired stakes in RGenix, the US-based cancer therapeutics company focused on the discovery and development of novel cancer drugs, for €30m.

Cinven, the UK private equity firm, announced it is acquiring BioClinica from two other buyout firms, Water Street Healthcare Partners and JLL Partners, for €1.1bn. The sale underscores private equity’s appetite for CROs that have benefited in recent years from pharmaceutical companies' drive to cut costs, reduce clinical trial times and expand their research and development presence globally.

Some notable financial investor deals include:

GLOBAL PHARMACEUT I C AL AND B I OTEC H NOLOG Y R EP ORT 20 16

A CL E A RWA TE R IN TE RN A T ION A L HE A L THCA RE REPORT 13

Segment breakdown

Outsourcing services (27%) and biotech (23%) accounted for half of the deals completed in the last 12 months. Of the outsourcing deals, 44% were related to CRO, 18% to CMO/CDMO, and 28% deals were related to the sub-segment which includes companies providing other outsourcing services such as consulting, testing, auditing, certification, medical communications, regulatory, compliance, and safety.

Oncology is a particular growth segment. Deals in the sector have gained prominence and the market is projected to more than double by 2022, with global revenues expected to increase from €75bn in 2015 to €168bn.

Recent deals include AbbVie’s acquisition of the US-based cancer drug biotech firm Stemcentrx for €5.5bn, and Jazz Pharmaceuticals’ €1.4bn acquisition of Celator Pharmaceuticals, the listed US-based oncology-focused biopharmaceutical company.

Notable transactions:

Shire plc acquired the rare disease specialist Dyax Corp. for €5.9bn, securing Shire’s hereditary angioedema portfolio. Its lead fast track, breakthrough therapy and orphan drug-designated Phase III-ready product, DX- 290, is considered to have blockbuster potential.

Pfizer acquired Anacor Pharmaceuticals, the US-based developer of small-molecule therapeutics, for €4.7bn. Anacor’s drugs will complement Pfizer’s line-up of inflammation and immunology products.

Bristol-Myers Squibb acquired Cardioxyl Pharmaceuticals, the US-based biotechnology company focused on the discovery and development of novel therapeutic agents for the treatment of cardiovascular diseases, for €1.9bn.

AstraZeneca acquired ZS Pharma Inc. for €2.4bn to bolster its cardiovascular and metabolic disease portfolio through accessing ZS-9, a possible best-in-class speciality treatment for hyperkalaemia.

Germany's Boehringer Ingelheim Corp. completed the sale of Roxane Labs, the US speciality generics company, to UK-based Hikma Pharmaceuticals for €1.6bn. Hikma becomes the sixth largest player in the US generics market by value and the third largest supplier of generic injectables by volume.

Private investment company Ardian, in collaboration with GHO Capital and the management team, acquired the US-based outsourcer and life-sciences scientific communications company Envision Pharma.

27%

23%19%

13%

10%

4%4%

Outsourcing services

Biotech

Pharma

OTC

Generics

Animal health

Others

14

UK market

Europe is the second largest pharma & biotech market, led by the UK, France and Germany. In terms of acquisition targets, the UK has seen 34 deals in the last 12 months – a decrease of 24% compared to the previous 12 months. As an acquirer nation the UK remained quite active, sealing 49 deals compared to 48 in the preceding 12-month period.

In the wake of Brexit, dealmaking in the industry has slowed down a little, but it is too early to make any firm conclusions. Much of the M&A is happening within specialised companies that have good domestic reach and international upside, and this is evident from companies which are currently exploring possible sales options.

These include: Martindale Pharma, the drug-maker which provides medicines used in emergency rooms and which recently bought Viridian Pharma, another UK-based firm, to expand its product portfolio; drug-maker Morningside Pharmaceuticals, which makes generic medicines for the NHS and international markets; and Ziarco Pharma, the biotechnology company whose investors include Pfizer’s venture capital arm. GW Pharmaceuticals is also rumoured to be considering bids.

Deals by investor type - trade vs. financial

Trade buyers constituted the majority of deals, accounting for 94% of the total transactions in the last 12 months compared to 91% in the previous 12 months.

In comparison, financial investor interest seemed to dwindle with only two deals in the last 12 months compared to four in the previous 12-month period. Quotient Clinical, the UK-based pharmaceutical drug development service provider, was acquired by GHO Capital Partners from Bridgepoint Development Capital, for €212m. And Synova Capital exited from its investment in Kinapse to private equity firm HgCapital for €13m, realising a return of 16.1x.

Segment breakdown

The outsourcing services and pharma segments have accounted for 64% of closed deals in the last 12 months. Within outsourcing, we noticed significant activity in CRO (69%) and CMO/CDMO (15%), together accounting for 84% of total outsourcing deals.

2016 has seen a strong start with 20 deals so far.

0

1

2

3

4

Oct 14 - Sep 15 Oct 15 - Sep 16

4

2

No

. of

fina

ncia

l inv

esto

r d

eals

Outsourcing services

Pharma

Generics

Biotech

OTC

38%

26%

18%

15%

3%

GLOBAL PHARMACEUT I C AL AND B I OTEC H NOLOG Y R EP ORT 20 16

A CL E A RWA TE R IN TE RN A T ION A L HE A L THCA RE REPORT 15

Notable transactions:

Vectura merged with Skyepharma in a €568m (11.6x EBITDA) deal that will create an industry-leading specialist in inhalation devices for people with respiratory diseases such as asthma. Their respective product portfolios and areas of expertise - including dry powder inhalers, pressurised metered dose inhalers and nebulisers for asthma patients and other airways-related illnesses - are complementary.

Akarna Therapeutics, the biopharmaceutical company, was acquired by Allergan, for €45m. Allergan obtains rights to AKN-083, Akarna’s lead product candidate for the potential treatment of non-alcoholic steatohepatitis (NASH) and other liver diseases.

Pharmaceutical Product Development (PPD), the US-based CRO, together with Jaguar Holding Company Luxembourg S.a.r.l., acquired Synexus, a clinical research company with expertise in patient recruitment, for €229m (16.2x EBITDA). Earlier this year Synexus acquired US-based Research Across America, expanding its reach to over 79 million potential patients.

Merck & Co., the listed US-based company, acquired IOmet Pharma, the UK-based developer of novel small molecules for the treatment of cancer, for €360m.

Novartis Pharma acquired all the remaining rights of biological therapeutic Ofatumumab from GlaxoSmithKline for €931m.

Genzyme, the Sanofi company, acquired the rare cancer therapy Caprelsa from AstraZeneca for €270m, in a deal designed to bolster the Genzyme endocrinology portfolio. Caprelsa is an oral kinase inhibitor for symptomatic or progressive medullary thyroid carcinoma in patients.

Sinclair IS Pharma sold its non-aesthetics business to Alliance Pharma for €170m (14.7x EBITDA). The transaction includes wound and skin care products and other hospital products.

NASDAQ-listed Concordia Healthcare acquired Amdipharm Mercury for €3.2bn. The acquisition enables Concordia to become a leading international speciality pharmaceutical company with commercial reach in over 100 countries.

Clinigen Group, the specialty pharmaceutical company, acquired Link Healthcare, a specialist pharmaceutical and medical technology business, for €129m (23.8x EBITDA).

Brexit

The Brexit vote in June 2016 has led to considerable uncertainty in the sector. A loss of regulatory harmonisation across Europe and new tariff charges, for instance, could increase production costs and delay the entry of new drugs into the UK market.

These changes can potentially threaten drug makers' margins and could push major global players to prioritise investment operations elsewhere. However, it is too early to make any firm conclusions as to the true impact until formal negotiations over Brexit begin.

16

“The UK has a strong pedigree in contract outsourcing, generics, R&D and manufacturing complex innovator and non-innovator pharma and biopharmaceuticals, and the market is an attractive and strong source of M&A activity in the mid-market. Combined with the scarcity level of these types of assets, the UK will continue to be a very contested market…it is a good time to sell.”

Ramesh Jassal, Head of Healthcare, Clearwater International, UK

GLOBAL PHARMACEUT I C AL AND B I OTEC H NOLOG Y R EP ORT 20 16

A CL E A RWA TE R IN TE RN A T ION A L HE A L THCA RE REPORT 17

“Ireland has a fundamentally strong position as a hub for global biotechnology and pharmaceutical companies. The majority of large international manufacturers have invested heavily in facilities and a thriving indigenous sector has developed. While we will see more mega deals into the future, the rationale for future M&A will need to be based on sound commercial logic and not be solely driven through potential tax efficiencies.”

John Curtin, Partner, Clearwater International, Ireland

Irish marketIreland is a leading pharmaceutical and biotechnology location with nine of the 10 largest pharmaceutical companies in the world having a significant presence in the country, including Allergan, Novartis and Perrigo.

Pharmaceutical products make up half of total Irish goods exports by value and the country is the eighth largest producer and fifth largest exporter of pharmaceutical products globally, and the largest net exporter of pharmaceutical products in Europe.

Ireland has developed a reputation as an attractive hub for pharma and biotech companies due to the friendly foreign direct investment structures, a highly educated workforce, and a competitive tax regime. The country also has a strong network of indigenous pharma and biotech companies that have been developed through its strong clinical and academic research ecosystem.

M&A activity

In recent years the high value of transactions in the market has been particularly driven by tax inversions with international pharmaceutical companies taking advantage of attractive corporate tax rates to acquire Irish domiciled companies.

However, over the past 12 months we have seen just 15 deals by Irish companies, a decrease of 42% compared to the preceding 12 months. Total deal value fell from €81.6bn to just €10.3bn.

Despite the slowdown in M&A activity, Irish big pharma companies like Allergan and Shire continue to strengthen their market share through biotech and pipeline deals. For instance, Allergan acquired Kythera Biopharmaceuticals, the US-based biopharmaceutical aesthetic product research company for €1.9bn, and also

Therapeutics Inc., the US-based clinical-stage biotechnology company developing therapies for dermatology and medical aesthetics.

There were six deals in which Irish companies were the target, compared to seven deals in the preceding 12 months.

Notable transactions:

Baxter Healthcare, the UK company that develops, manufactures, and markets products for the treatment of hemophilia, immune disorders, infectious diseases, and other chronic conditions, acquired Fannin Compounding, the manufacturer of compounded medicines, from Fannin, a DCC plc company.

Fastnet Equity, which last year announced a switch of focus from oil exploration to pharmaceuticals, acquired orphan drug development firm Amryt Pharmaceuticals, for €38m.

NYSE-listed Spark Therapeutics acquired Genable Technologies, the bio-pharmaceutical company that develops gene therapies for the treatment of genetic diseases. Genable was spun out of Trinity College Dublin and had been partnering with Spark to develop gene therapies to treat inherited diseases.

4D Pharma plc acquired Tucana Health, the biotech company that investigates the use of microbiome signatures to aid the diagnosis and treatment of diseases, for €14m.

18

Iberian market

The Iberian pharma & biotech sector is on a consolidation spree. Out of the 15 deals recorded in the Iberia region, seven featured acquirers also located within the region.

Outsourcing services gained particular traction, accounting for seven of the total closed transactions in the last 12 months. Of these, five were related to CMO/CDMO and CRO. We also saw a significant fall in generics transactions, falling from eight to three.

Spain

During 2015 the Spanish internal pharma market grew significantly due mainly to a rise in public spending boosted by the introduction of new therapies to treat Hepatitis C. Sales in pharmacies have also increased leading to a total increase in

pharma sales of 10.6%, compared with 2014, with total revenues reaching €15.6bn.

The increase has not been even across all segments. Sales of branded medicines have remained constant while average prices have suffered a small decrease. However, generics sales have increased by 3.6% with a price rise of 2.4%. Imports grew at a rate of 15.4%, while export levels increased by 7.9% to €11.1bn.

This increase in price is a consequence of the growing demand for prevention products, as well as strong marketing campaigns carried out by large consumer health corporations. The development of new product portfolios, mainly in the food supplements segment, has also driven up prices.

There were 15 deals in the pharma & biotech sector in the last 12 months with 80% of acquisition targets located in Spain and 20% in Portugal.

“Interestingly, we recorded six financial investor deals, compared to just one in the preceding 12 months, indicating high investor confidence in Iberia’s pharma & biotech market.”

Miguel Ángel Lorenzo, Director, Clearwater International, Spain

Notable transactions:

Apax Partners, the UK-based private equity firm, acquired Invent Farma, a developer and manufacturer of Active Pharmaceutical Ingredients (APIs) and pharmaceuticals specialities, for €221m (8.8x EBITDA). The deal shows PE interest in the European generics and contract outsourcing market.

Euromed, the producer of herbal extracts and natural active substances for pharmaceutical, health food and cosmetics, was acquired by The Riverside Company, the US PE firm, from Meda AB, the Sweden-based

pharmaceutical company, for €82m (5.0x EBITDA).

An undisclosed investment vehicle acquired a 69.6% stake in Laboratorios Farmaceuticos ROVI SA, the pharma outsourcer, for €492m.

ProA Capital de Inversiones, the Spain-based PE firm, acquired a majority stake in Suanfarma SA, the biopharmaceutical developer, for €25m. It also acquired Avizorex Pharma SL, the dry eye syndrome therapy research services provider, for an estimated €25m.

GLOBAL PHARMACEUT I C AL AND B I OTEC H NOLOG Y R EP ORT 20 16

A CL E A RWA TE R IN TE RN A T ION A L HE A L THCA RE REPORT 19

Portugal

Pharma sales totalled €2.8bn in 2014 with generics accounting for 22%1 of total sales. The recession and debt crisis has led to substantial growth in the generics market over the last few years, particularly in terms of volume. Indeed, the development of generic drugs has been the cornerstone of a series of government austerity measures to reduce healthcare spending.

Notable transactions:

Lusosuan, the manufacturer of antibiotics and pharmaceutical ingredients, acquired an 85.4% stake in CIPAN, the manufacturer of pharmaceutical preparations.

Medifarma S.A., the Peru-based developer and manufacturer of pharmaceutical products and drugs, acquired Portuguese outsourcer and manufacturer of finished dosage forms Laboratorios Atral from Atral Cipan SGPS.

“For the last decade the market has been adjusting to changes on pricing and reimbursement applied by the government, and the need for consolidation has created M&A opportunities for international pharmaceutical groups already present in the market. The adjustments will continue to have an effect on the industry and M&A opportunities will arise, especially in the mid-market.”

Afonso Lima, Associate, Clearwater International, Portugal

1 European Federation of Pharmaceutical Industries and Associations: The Pharmaceutical Industry in Figures

2020

French and German markets2016 has seen 32 deals in the pharma & biotech sector with 14 acquisition targets located in France and 18 in Germany.

Total deal count has declined by 27% with 41 deals in the last 12 months, compared to 56 over the previous year. With 22 (54%) cross-border deals, US and UK-based companies were the most active acquirers. There were eight deals by financial investors, an increase of 33% compared to the preceding 12 month period.

France

France is the second largest European market and one of the world’s largest consumers of pharmaceutical products. The market is expected to grow by 0.7% CAGR, from €40bn in 2014 to €42bn by 20201, mostly due to an increasing focus on generic drugs. The market will also be boosted by the ageing population, tax incentives, a skilled workforce, and high public healthcare expenditure.

Until a few years ago most of the drug R&D and production was carried out by the largest French pharma companies, but this trend is now shifting. For instance, in 2015 French biotech companies had more products in development in their pipeline than the four largest pharma players combined—Sanofi, Ipsen, Servier and Pierre Fabre.

Over the past 10 years the French biotech R&D market has emerged as the leading European market, exemplified by the number of companies listed on the Euronext market. From just a handful in 2006 with a combined market cap below €500m, the market now has more than 50 life sciences companies listed with a combined market cap of more than €10bn.

In terms of M&A, France has recorded 18 deals worth €1.6bn in the last 12 months, compared to 27 deals worth €1.4bn in the preceding 12-month period.

Notable transactions:

Ethypharm, the pharmaceutical company that specialises in pain and addiction treatment, was acquired by PAI Partners, for €750m (12.5x EBITDA).

NASDAQ-listed Avalanche Biotechnologies acquired Annapurna Therapeutics, the gene therapy company focused on discovering and developing new therapeutic products, for €98m.

Onxeo S.A. acquired DNA Therapeutics and its signal-interfering DNA (siDNA) repair technology and lead product candidate AsiDNA, for €28m. The acquisition shows Onxeo’s commitment

to developing novel orphan oncology drugs which position the company at the forefront of scientific research for rare cancers.

Recipharm AB, the listed Sweden-based CDMO, acquired Kaysersberg Pharmaceuticals, the owner and operator of pharmaceutical manufacturing facilities, from Alcon, for €18m.

Porsolt SAS, the preclinical in-vivo efficacy and safety CRO, acquired Fluofarma, a company focused on the provision of cell-based assays and in-vitro screening services.

GLOBAL PHARMACEUT I C AL AND B I OTEC H NOLOG Y R EP ORT 20 16

A CL E A RWA TE R IN TE RN A T ION A L HE A L THCA RE REPORT 21

Germany

Germany has the largest pharmaceutical industry output in Europe with sales of approximately €50.4bn (+5.3% YOY growth). The revenues are largely export-driven with around 66% of sales generated abroad. The market is characterised by a strong R&D competency and a large number of clinical trials.

Generic drugs account for 81% of value and 36% of the volume of the pharma market, while branded products hold the remainder. In the distribution channel pharmacy prescribed medicine accounts for 87% of sales with OTC medicine the remainder.

There has been significant M&A activity in generics with five deals in the last 12 months compared to just two in the preceding 12-month period. This year has also seen a number of smaller sized transactions. For instance, Irish pharmaceutical company Amryt Pharmaceuticals acquired Birken AG, the pharmaceutical products manufacturer, and Sompharmaceuticals SA, the Switzerland-based anti-tumour medicines and diagnostic preparations developer, for €38m.

Notable transactions:

7Life, a subsidiary of ProSiebenSat.1 Media, the German media company, acquired a 92% stake in Windstar Medical, the provider of private label and branded pharmaceuticals, for €80m (10.0x EBITDA).

Apax Partners, the UK PE firm, acquired neuraxpharm Arzneimittel, the manufacturer of generic medicines for treating disorders of the central nervous system.

Charles River Laboratories acquired Oncotest GmbH, the contract oncology research services provider, for €36m (11.0x EBITDA).

Market outlook

The local market is expected to grow at a slower rate due to pricing restrictions. However, the cumulative sales of German companies might experience higher growth rates due to strong exposure to foreign markets.

“We see M&A potential particularly in the mid-market segment as research-oriented German companies are seen as targets for international pharmaceutical companies.”

Markus Otto, Partner, Clearwater International, Germany

1 PharmaVoice.com

2222

Scandinavian marketSo far in 2016 there have been 13 deals in the region – predominantly in Sweden.

There have been 18 deals in Scandinavia in the last 12 months with the majority of the acquisition targets located in Sweden (67%), followed by Denmark (22%) and Norway (11%).

The OTC segment registered six deals in the last 12 months, compared to just three in the previous 12-month period due to increasing adoption rates of OTC drugs.

Sweden

The Swedish life science industry consists of 1,5001 companies within pharma, biotech and medtech. Of these, around 800 are engaged in R&D programmes in the country.

Generics have held a low revenue share of around 15% over the last few years due to their low prices, but the prices of branded products with high-volume sales fell between 80% and 95% over the same time period following patent expiries.

This depicts the level of price competition between generics manufacturers. This will somewhat restrict the market’s growth and lead to a stagnation in terms of innovation

at pharmaceutical and biotechnology companies which are now unable to post handsome profits. However, this trend works well for Sweden as it needs to cut its healthcare costs.

In the last 12 months we recorded 12 deals, the same as in the previous 12-month period. There was significant growth in the biotech and OTC segments.

Norway

A particular growth market is aquatic health products serving aquaculture which has been rising at 7–8% annually and is worth around €450m. This growth rate is faster than the overall livestock segment, which is growing at 6% CAGR, and the animal segment, which is growing at 5% CAGR.

NYSE-listed Zoetis Inc. acquired PHARMAQ Holding, the Norway-based leading aquatic health group, for €689m (33x EBITDA). Acquiring PHARMAQ strengthens Zoetis’ core livestock business, giving the company a market-leading presence in this fast growing segment.

Notable transactions:

Mylan acquired Meda AB, the Sweden-based generic and OTC drugs manufacturer and wholesaler, for €6.5bn (13.3x EBITDA). The deal opens up a number of new opportunities for Mylan, such as significantly expanding its OTC presence and accelerating its expansion into markets such as China, Southeast Asia, Russia and the Middle East. The deal makes the combined company a leader in the global respiratory and allergy market.

Cormorant Pharmaceuticals, the Sweden-based developer of therapeutics including the HuMax- IL8 antibody programme for the treatment of cancer and rare diseases, was acquired by Bristol-Myers Squibb, for €468m. The acquisition broadens Bristol-Myers Squibb’s oncology pipeline focus in tumour microenvironment and combination therapy.

GLOBAL PHARMACEUT I C AL AND B I OTEC H NOLOG Y R EP ORT 20 16

A CL E A RWA TE R IN TE RN A T ION A L HE A L THCA RE REPORT 23

Denmark

Due to strong historical roots, the Danish pharmaceutical and biotechnology industry is one of the world’s leaders. Major industry players include Novo Nordisk, Lundbeck, Leo Pharma, AlkAbelló, GenMab, and Bavarian Nordic. In 2015 the country saw exports of medicinal products reach 13.5% of total Danish exports – making it the country’s largest export industry. Paired with more than €1.5bn in R&D investments, the pharmaceutical industry is also the country’s largest private research area, in one of the most R&D intensive countries in the world.

Medicon Valley is home to the Danish life science industry and one of Europe’s top three clusters for biotech innovation alongside Cambridge in the UK and Basel in Switzerland. The Danish biotechnology cluster is a particularly dominant world player within enzymes, accounting for more than 70% of total production. Denmark is now home to more than 160 dedicated biotech companies and more than 300 biotech service providers.

In the last 12 months we have recorded four transactions, two of them by financial investors.

Notable transactions:

LEO Pharma, the Danish pharmaceutical company focused on developing and manufacturing dermatology and parenteral treatments of thromboembolism, acquired the global dermatology business of Japan-based Astellas Pharma, for €675m.

US-based Savara Pharmaceuticals acquired Serendex Pharmaceuticals, the developer of drugs to treat respiratory diseases through inhalation.

An investor group comprising of Lundbeckfonden and Novo A/S, acquired a 43% stake in IO Biotech ApS, the manufacturer of biological products, for €10.7m.

“Healthcare and biotechnology M&A activity is likely to continue as several of the large national players have expressed their interest in acquisitions. Also, inbound M&A activity will continue as global players acquire new programmes to their pipelines from innovative Danish biotech companies.”

Louise Kamp Nørbæk, Associate Director, Clearwater International, Denmark

1 SwedenBIO: The Swedish Drug Development Pipeline 2015

2424

CEE marketPoland, Romania, Hungary and the Czech Republic are the most promising CEE markets based on market size and potential revenue. They are host to a number of developed companies like Zentiva (Sanofi), Gedeon Richter, Polpharma, Egis and other subsidiaries of larger multinational corporations.

Poland is the largest pharma market in the CEE region valued at €8bn–10bn, while other CEE countries continue to witness growth in the sector as a result of improving macroeconomic environments.

Romania is likely to be the region’s fastest-growing economy with a predicted 4.5% growth rate, followed by Poland and Slovakia with 3.2%. Croatia, Estonia, Hungary and Slovenia are expected to witness 2.0% growth rates.

The region also serves as a contract manufacturing and research hub. There are currently some 1,618 clinical trials in phases I-III within this region. The leading CRO locations are Poland with 682; Czech Republic with 505; and Hungary with 431 ongoing trials.

M&A activity

There was a slight decrease in deal volumes over the past 12 months with 14 deals compared to 17 deals in the previous 12 months. Outsourcing was the largest segment accounting for half the deals, compared to 24% in the previous 12 months.

Acquisition targets were primarily from Poland (seven), followed by the Czech Republic (four) and Slovenia, Estonia and Croatia with one each.

The OTC market is growing dynamically, consistent with a global trend for OTC sales to grow faster in developing markets as disposable incomes increase. Due to the socioeconomic impetus, pharmaceutical companies operating in these countries have turned their focus to the OTC market segment in a strategic way. This is, to an extent, a response to the genericisation of many top-selling molecules, leading to considerable price cuts and a challenging regulatory environment.

Notable transactions:

Valosun, the Czech Republic-based probiotics manufacturer, was acquired by Walmark, a major consumer healthcare player in the CEE region with a leading position in dietary supplements. The acquisition extends its presence in digestive health and strengthens its position in female urinary health.

Pelion acquired a stake in Poland-based Pharmena, the dermo-cosmetics manufacturer. Pharmena sells skin and hair care products under the Dermena, Allerco, and other brands. It is also involved in the production and sale of dietary supplements.

In an outsourcing deal Kantar Health, the US-based leading global healthcare consulting and market research firm, acquired CEEOR, the research and consulting firm that operates across Europe. The firm specialises in delivering real-time competitive intelligence data, analytical solutions, and advisory and implementation services to the pharmaceutical, biotechnology and healthcare industries.

Marifarm, proizvodnja in storitve d.o.o., the Slovenia-based pharmaceuticals producer, was acquired by Arterium, the Ukraine-based company that manufactures, markets, sells and distributes original and generic pharmaceutical products, antibacterial drugs, and herbal-based and veterinary medications, for €7m.

Poland-based Maspex Wadowice Group, a producer and seller of food products and beverages, acquired Sequoia Sp. z o.o., the Poland-based vitamin and generic drug maker.

GLOBAL PHARMACEUT I C AL AND B I OTEC H NOLOG Y R EP ORT 20 16

A CL E A RWA TE R IN TE RN A T ION A L HE A L THCA RE REPORT 25

“The domestic market continues to see healthy growth of 12-15% and is expected to maintain these growth rates in the near term. Large players are re-evaluating their growth strategies, with some companies refocusing on the domestic market or acquiring companies and products in the export market.”

Prashant Jain, Director, o3 Capital, India

Indian and Chinese markets2016 so far has recorded 49 deals with a combined value of €2.1bn.

India and China together saw 89 deals in the last 12 months compared with 99 in the previous 12-month period. China accounted for 66 deals worth €10.9bn, while India recorded the remaining 23 deals worth €1.2bn. Domestic players were clearly on an acquisition spree as 91% of the targets were acquired by companies located within the two countries.

India

The pharmaceuticals market is the third largest in volume and thirteenth largest in terms of value. The market is expected to grow at a CAGR of 15%, from €26bn in 20151 to €48bn by 2020.

With a 70% market share (in terms of revenue), generic drugs form the largest segment of the market, followed by OTC and patented drugs. India is also the largest manufacturer of generic drugs globally, with generics accounting for 20% of global exports in terms of volume.

By 2020, India is likely to be among the top three pharmaceutical markets by incremental growth and sixth largest market globally in absolute size. Production costs are significantly lower than in the US and many countries in Europe which gives India a competitive advantage.

The biotech industry, comprising of about 800 companies, was valued at €4.4bn in 2015. It holds around 2% share of the global market.

Driven by growing demand, intensive R&D activities and strong government initiatives, the growth in the biotech sector is likely to continue. It is expected to grow from €6bn in 2015 to €10bn by 2017 – a CAGR of 29%. The bio pharmaceutical segment accounted for the largest share of the biotech industry, with 62% of total revenue in 2015, followed by contract outsourcing (18%) and bio-agri (14%).

Notable transactions:

Strides Arcolab acquired Shasun Pharmaceuticals, the manufacturer of APIs, intermediates and formulations for €243m (11.7x EBITDA). This creates a vertically integrated pharma company with presence in regulated markets’ finished dosages, emerging markets’ branded generics, institutional businesses, APIs, and outsourcing services.

Take Solutions, the life sciences technology provider, acquired Manipal

Acunova from the US-based private equity fund, OrbiMed in order to boost its life sciences technology business. Take Solutions will gain technological expertise and key clients in the field of research in biosimilars, stem cell therapy and in developing diagnostic imaging devices.

Swedish CDMO Recipharm AB acquired a 74% stake in Nitin Lifesciences, the sterile injectables CMO, for €93m (12.4x EBITDA).

China

China is the world's largest producer of pharma ingredients and the world’s second largest pharma market. The market size is expected to account for €142bn worldwide in 20162.

Population growth and increasing medical needs make it the world’s largest producer and exporter of pharmaceutical ingredients. Covering 40% of the global API production, the pharma market presents huge growth opportunities.

With the government’s increasing investment in healthcare and R&D, China presents great opportunities for innovative products and technologies, and collaboration between international and domestic pharmaceutical companies.

Low prices with good quality and bulk production are the main advantages for China being a global leader in API production. At present, a majority of Chinese manufacturers are looking into deepening ties with European and Indian markets by investing in APIs, generics,

biologics, biosimilars, finished formulation and packaging.

Interestingly China has seen some mid-sized local companies formulating aggressive overseas expansion plans. These cash-rich companies, some fuelled by recent IPOs, are starting to invest into product development and registration overseas as well as acquiring European or American players, and will further elevate the Chinese outbound investment trend.

In addition, to alleviate weak local portfolios, local pharma companies are in-licensing a high volume of international assets. At the same time, many international pharma players, including generics makers, are looking to support growth in the Chinese market by buying local companies. Rather than expanding local portfolios, their objectives are the addition of local production capacity, regulatory expertise and market access.

Notable transactions:

Shaanxi Bicon Pharmaceutical Group Holding, the pharmaceuticals manufacturing holding company, was acquired by Jiangsu Jiujiujiu Technology, the developer and distributor of pharmaceutical intermediates and nitrogen fertilizer, for €1.4bn.

Guizhou Chitianhua acquired the entire share capital of Guizhou Salvage Pharmaceutical, the manufacturer and wholesaler of pharmaceutical preparations, for €317m.

LianYunGang HuangHai Machinery acquired Changchun Changsheng Biotechnology, the biological vaccines manufacturer, from Wuhu Zhuorui Innovation Investment Management Centre, for €978m.

China Resources Sanjiu Medical & Pharmaceutical acquired the entire share capital of Kunming Shenghuo Pharmaceutical, the manufacturer and wholesaler of pharmaceutical preparations, for €255m.

“The Chinese pharma market continues to consolidate both horizontally and vertically, driven by a domestic market that is growing at a moderate pace of 6–7% year on year.”

Franc Kaiser, Partner, InterChina Partners, China

2626

1 IBEF: Indian Pharmaceutical Industry2 CPhI.com

GLOBAL PHARMACEUT I C AL AND B I OTEC H NOLOG Y R EP ORT 20 16

A CL E A RWA TE R IN TE RN A T ION A L HE A L THCA RE REPORT 27

Recruitment and CSO services to pharmaceutical and healthcare clients

Clearwater International advised Chase on its recapitalisation, with investment provided by Vespa Capital

Chase Search and Selection

Pharmaceutical company

Clearwater International advised Merz Pharma on the sale of Merz Dental to SHOFU

Merz Pharma

Fast-growing manufacturer, distributor and seller of prescription and OTC products

Clearwater International advised the shareholders of Peckforton on the sale to Abbey Pharma

Peckforton

Chinese manufacturer of pharmaceuticals

Clearwater International advised Group Uriach on its investment

Sunlight Pharma

Leading sports nutrition products business

Clearwater International advised the company on its cross-border sale to Glanbia

Nutramino

Manufacturer of protein purification products used in discovery and development

Clearwater International advised Unilever on the sale to Life Technologies Corporation

BAC BV

Leading laboratory service provider

Clearwater International advised palero capital on the sale of Lausitzer Analytik Gmbh to SYNLAB

Lausitzer Analytik GmbH

Spanish pharmaceutical group involved in the development and production of generic drugs

Clearwater International advised the shareholders of Farmalider on the sale

Farmalider

Undertakes registration and marketing of generic pharmaceuticals

Clearwater International advised Neolab on its sale to DCC plc

Neolab

WWW.CLE ARWATERINTERNAT IONAL .COM

CHINA • DENMARK • FRANCE • GERMANY • IRELAND • PORTUGAL • SPAIN • UK • US