Embed Size (px)

Citation preview

Angela Hung

Director, Center for Financial and Economic Decision Making

May 2011

Gender and Financial Education

OECD/INFE Scoping Report on Gender and

Financial Education

• Goal: better identify, understand and respond to gender gaps in financial literacy

• OECD/INFE commissioned RAND to conduct a scoping report on Gender and Financial Education

• Project Framework

• Preliminary evidence on gender differences from OECD/INFE pilot survey on financial literacy

• Preliminary results of the OECD/INFE survey on financial education programmes and gender issues

• Highlights of research and literature on financial education and women

• Next steps and research

OECD/INFE pilot survey on financial literacy

• OECD/INFE developed an internationally comparable survey measuring personal financial literacy.

• Twelve countries from the OECD/INFE are currently pilot testing the questionnaire.

• Core questions cover a mix of knowledge, attitude and financial behaviour based on previous testing and validation, use in other national surveys and correlation with underlying concepts being measured.

Interest Compounding

Suppose you put $100 into a savings account with a guaranteed interest rate of 2% per year. You don’t make any further payments into this account and you don’t withdraw any money…and how much would be in the account at the end of five years? Would it be:

1. More than $110

2. Exactly $110

3. Less than $110

4. Or is it impossible to tell from the information given

Risk Diversification

I would like to know whether you think the following statement is true or false: It is usually possible to reduce the risk of investing in the stock market by buying a wide range of stocks and shares.

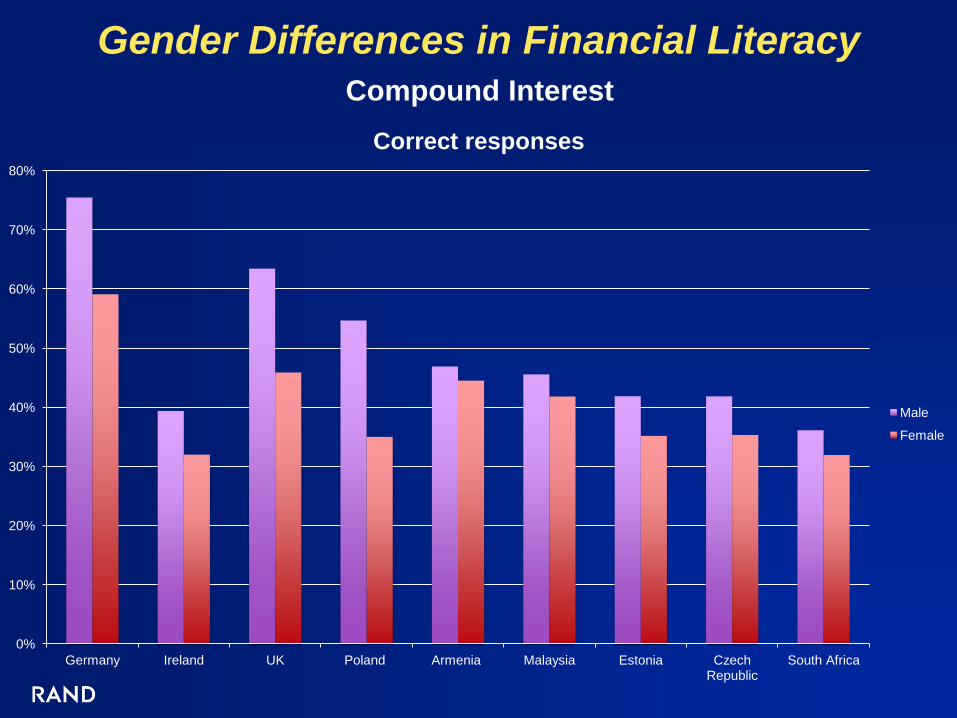

Gender Differences in Financial Literacy

Compound Interest

0%

10%

20%

30%

40%

50%

60%

70%

80%

Germany Ireland UK Poland Armenia Malaysia Estonia Czech Republic

South Africa

Correct responses

Male

Female

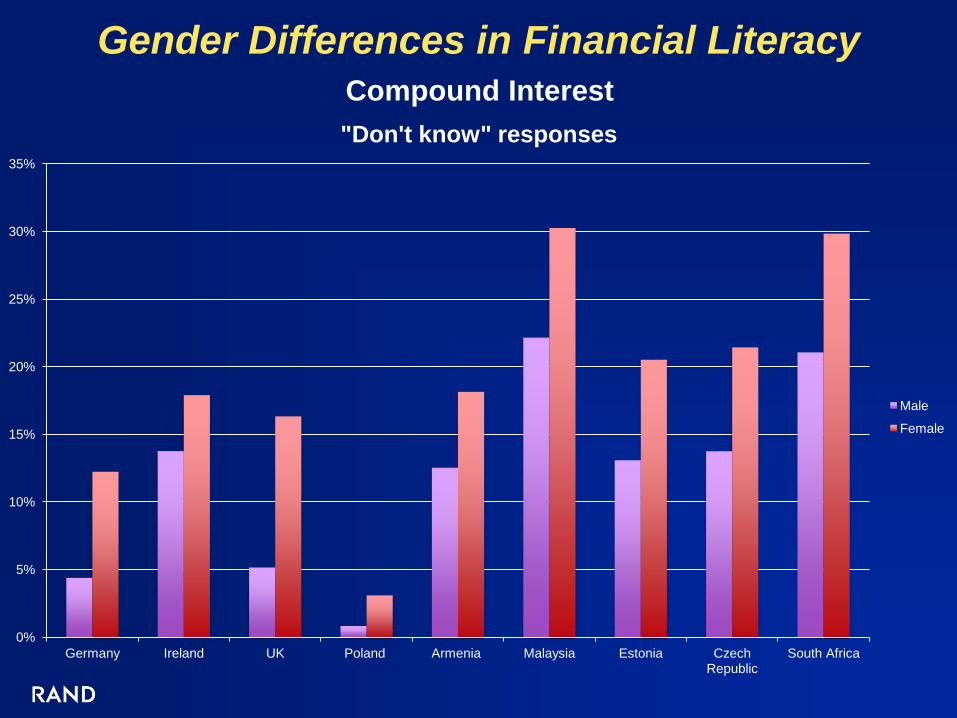

Gender Differences in Financial Literacy

Compound Interest

0%

5%

10%

15%

20%

25%

30%

35%

Germany Ireland UK Poland Armenia Malaysia Estonia Czech Republic

South Africa

"Don't know" responses

Male

Female

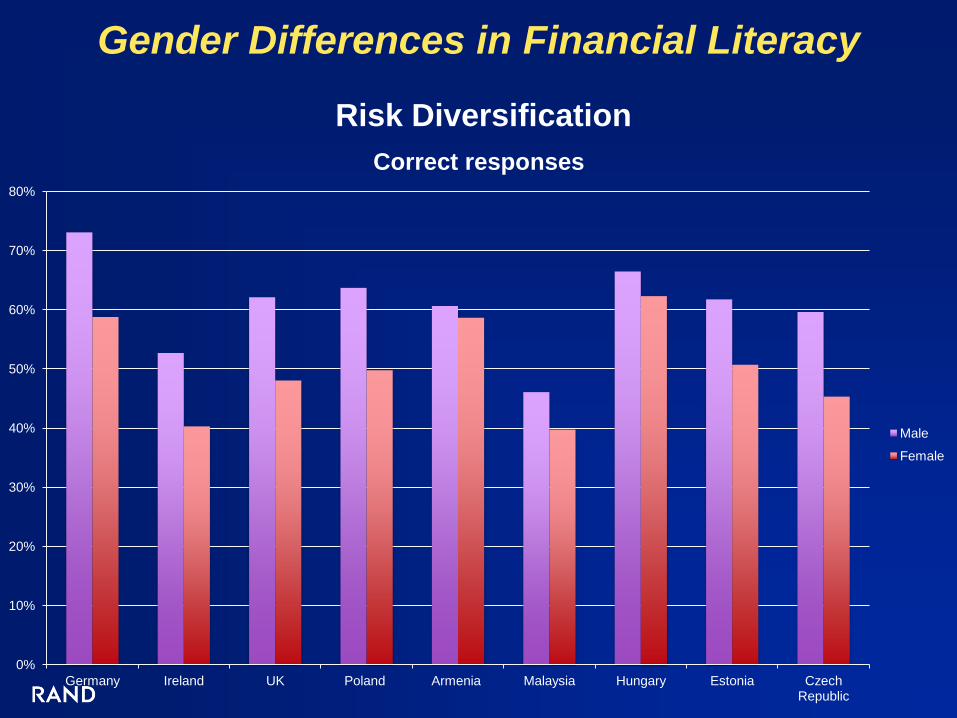

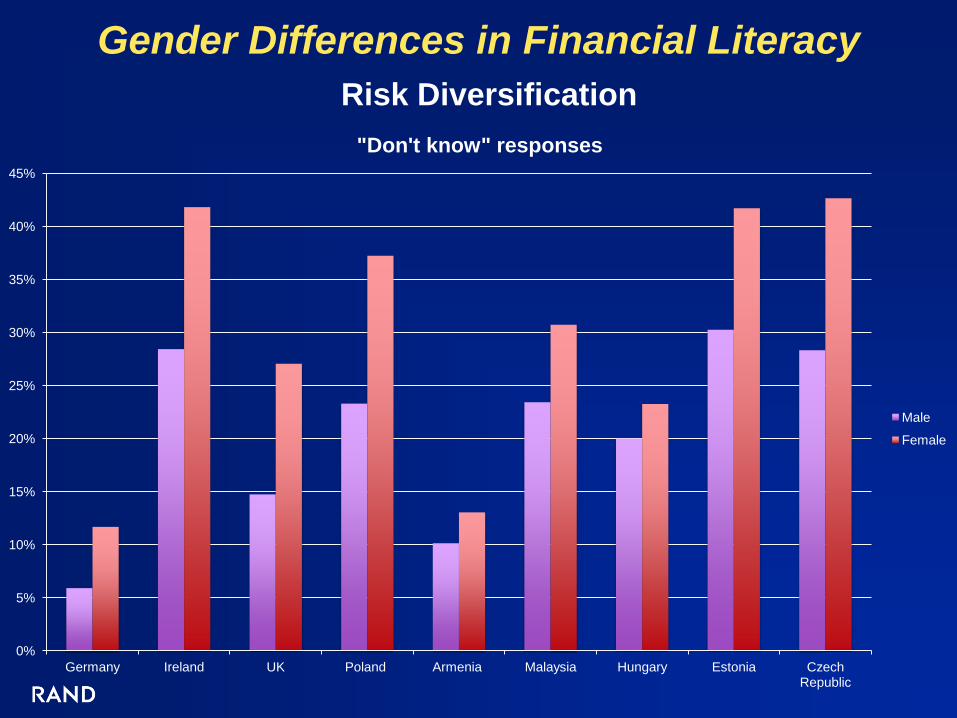

Gender Differences in Financial Literacy

Risk Diversification

0%

10%

20%

30%

40%

50%

60%

70%

80%

Germany Ireland UK Poland Armenia Malaysia Hungary Estonia Czech Republic

Correct responses

Male

Female

Gender Differences in Financial Literacy

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Germany Ireland UK Poland Armenia Malaysia Hungary Estonia Czech Republic

"Don't know" responses

Male

Female

Risk Diversification

OECD/INFE member survey on financial

education programmes and gender issues

• Survey sent to INFE members on:

• the perception of gender gaps in financial literacy in respondent countries

• the level and type of policy concern

• details of financial education programmes conducted in the last 5 years addressing these issues.

INFE Member Survey Preliminary Results

• We received responses from 15 countries:

•Australia

•Belgium

•Chile

•Denmark

•Estonia

•India

•Lebanon

•New Zealand

•Poland

•Portugal

•Serbia

•Singapore

•Slovenia

•Spain

•Turkey

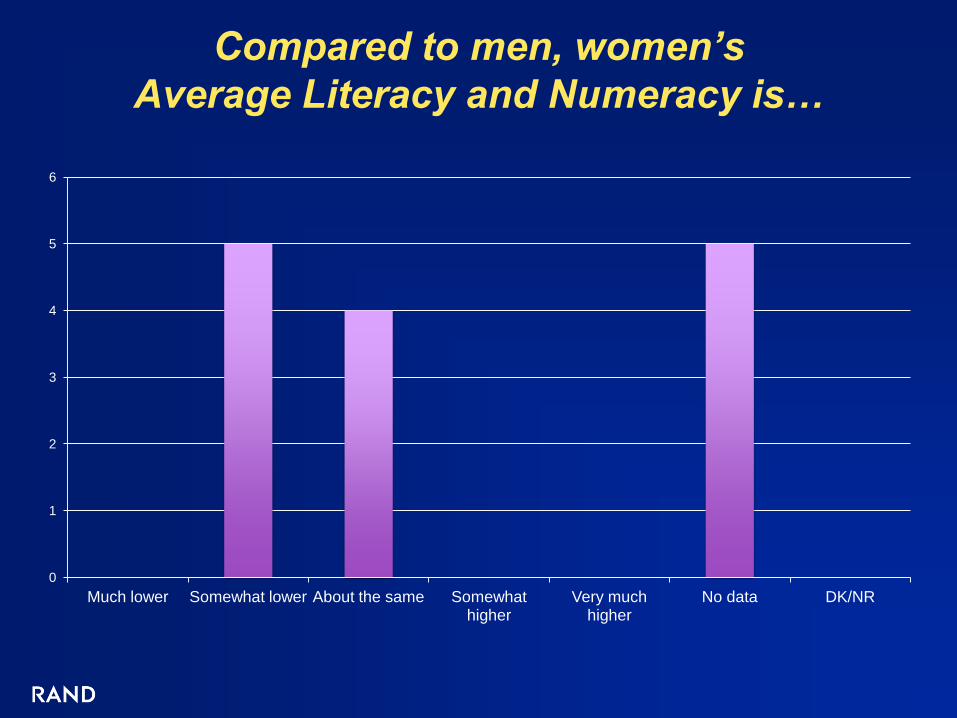

Compared to men, women’s

Average Literacy and Numeracy is…

0

1

2

3

4

5

6

Much lower Somewhat lower About the same Somewhat higher

Very much higher

No data DK/NR

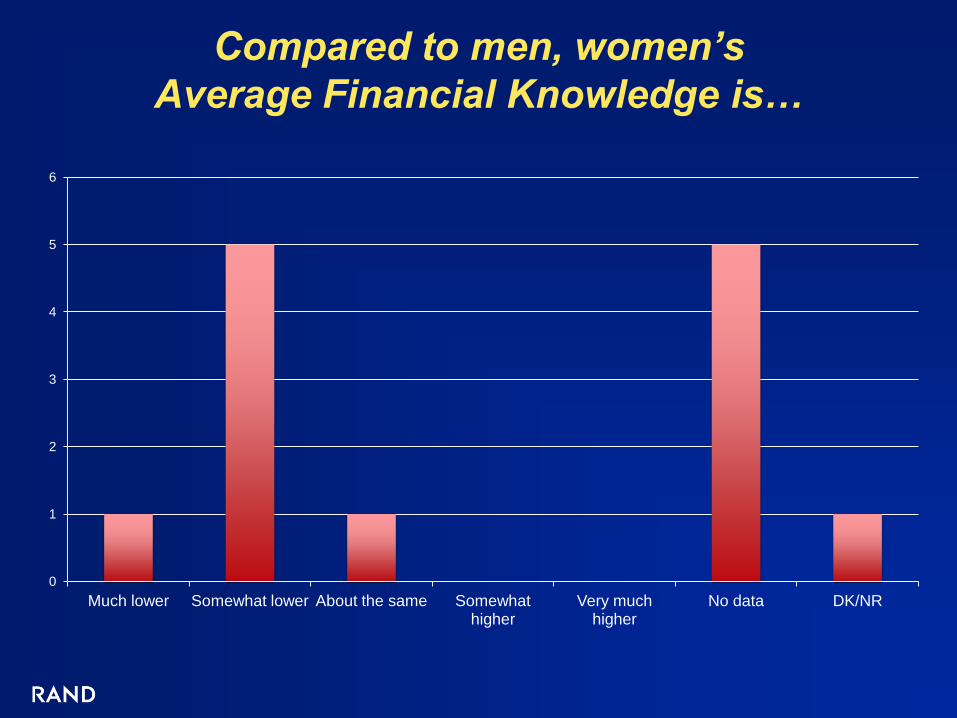

Compared to men, women’s

Average Financial Knowledge is…

0

1

2

3

4

5

6

Much lower Somewhat lower About the same Somewhat higher

Very much higher

No data DK/NR

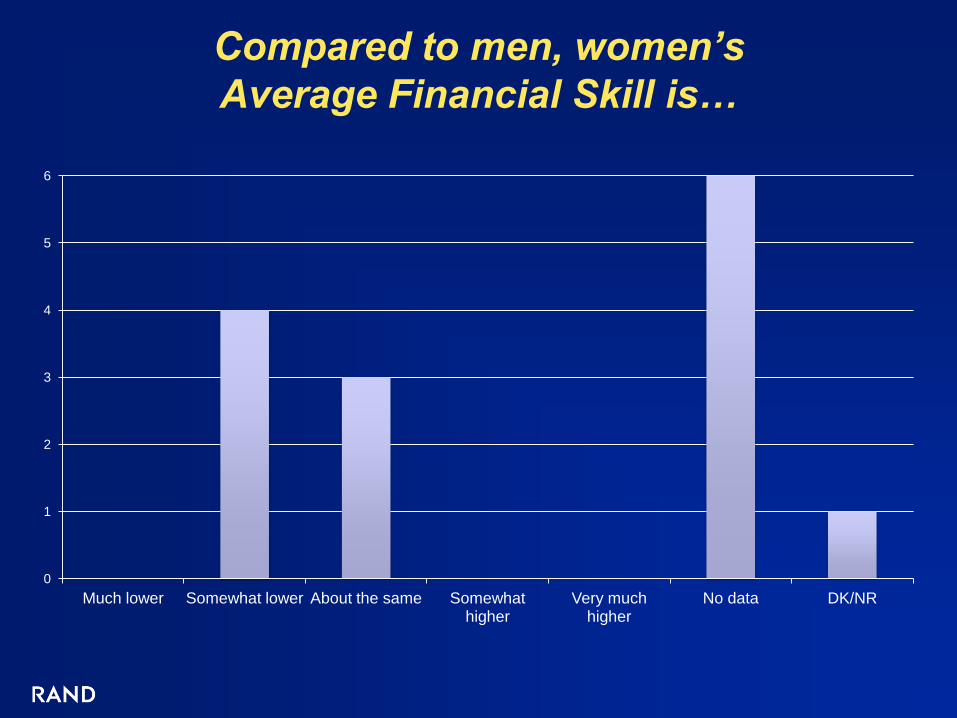

Compared to men, women’s

Average Financial Skill is…

0

1

2

3

4

5

6

Much lower Somewhat lower About the same Somewhat higher

Very much higher

No data DK/NR

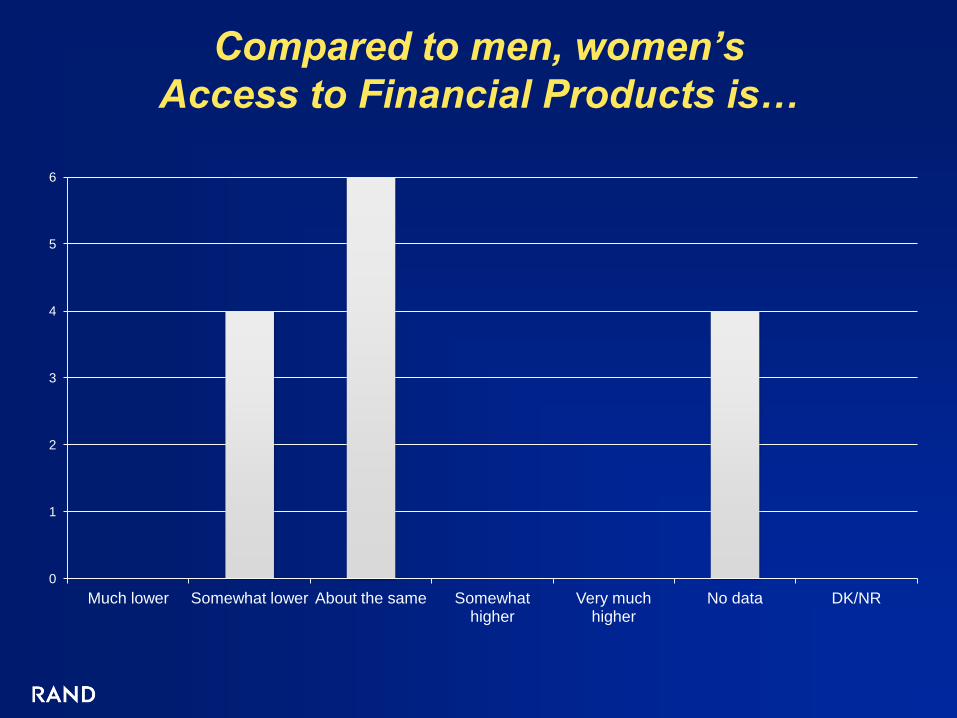

Compared to men, women’s

Access to Financial Products is…

0

1

2

3

4

5

6

Much lower Somewhat lower About the same Somewhat higher

Very much higher

No data DK/NR

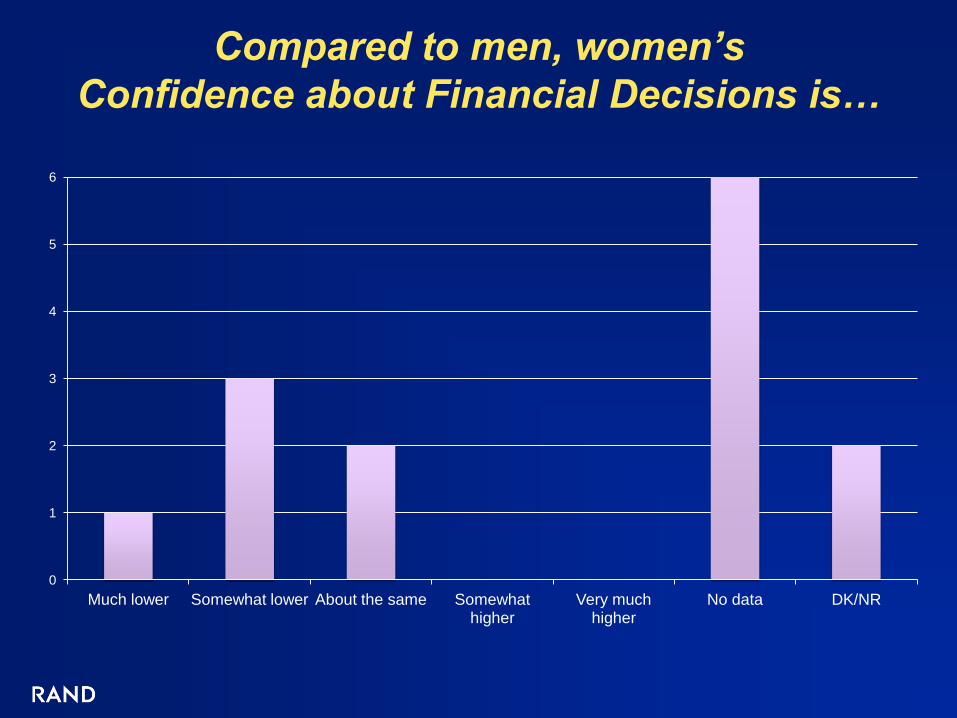

Compared to men, women’s

Confidence about Financial Decisions is…

0

1

2

3

4

5

6

Much lower Somewhat lower About the same Somewhat higher

Very much higher

No data DK/NR

Compared to men, women’s…

0

1

2

3

4

5

6

Much lower Somewhat lower

About the same

Somewhat higher

Very much higher

No data DK/NR

Average Literacy and Numeracy

Average Financial Knowledge

Average Financial Skill

Access to Financial Products

Confidence About Financial Decisions

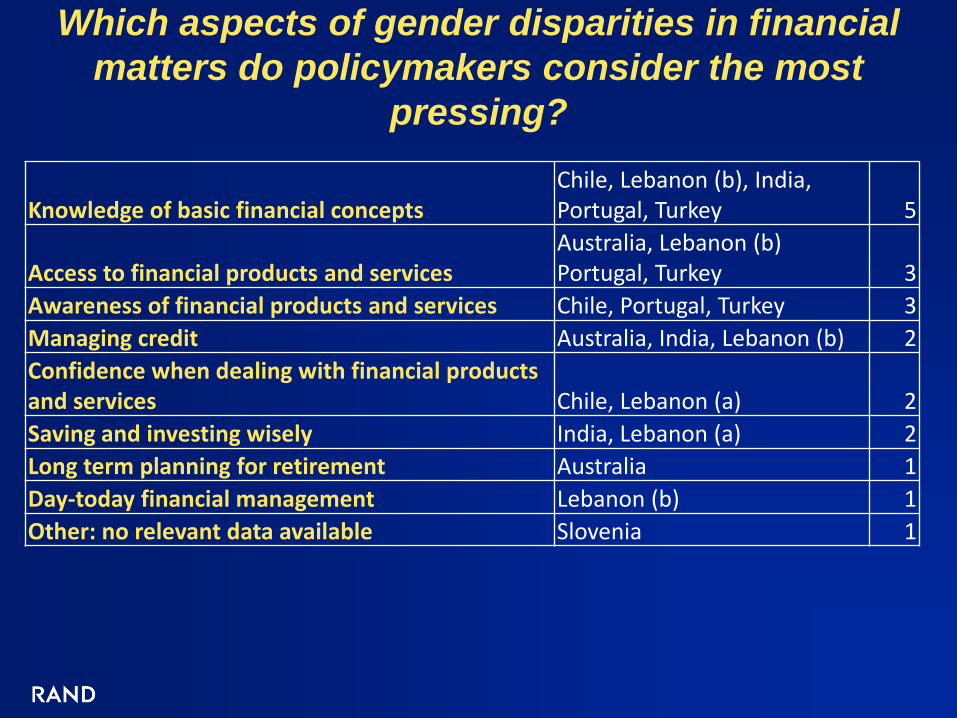

Which aspects of gender disparities in financial

matters do policymakers consider the most

pressing?

Knowledge of basic financial concepts Chile, Lebanon (b), India, Portugal, Turkey 5

Access to financial products and services Australia, Lebanon (b) Portugal, Turkey 3

Awareness of financial products and services Chile, Portugal, Turkey 3

Managing credit Australia, India, Lebanon (b) 2

Confidence when dealing with financial products and services Chile, Lebanon (a) 2

Saving and investing wisely India, Lebanon (a) 2

Long term planning for retirement Australia 1

Day-today financial management Lebanon (b) 1

Other: no relevant data available Slovenia 1

Are there specific groups

of women who have a particularly pressing need for

improved financial literacy?

Low-income Australia, Chile, India, Lebanon (a), New Zealand, Portugal, Spain, Turkey 8

Youth Australia, Chile, India, Lebanon(a) and (b), Portugal, Turkey 7

Elderly Australia, Chile, New Zealand, Portugal, Turkey 5

Unbanked/Underbanked Chile, India, Lebanon (a) Portugal, Turkey 5

Solo mothers Australia, Lebanon (a) 2

Immigrants Australia, Spain 2

Ethnic minorities New Zealand, Spain 2

Other: Women with disabilities Lebanon (a), New Zealand 2

Employees Lebanon (b),Portugal, Turkey 2

Recently-separated/widowed/divorced New Zealand 1

Other: Women in remote areas New Zealand 1

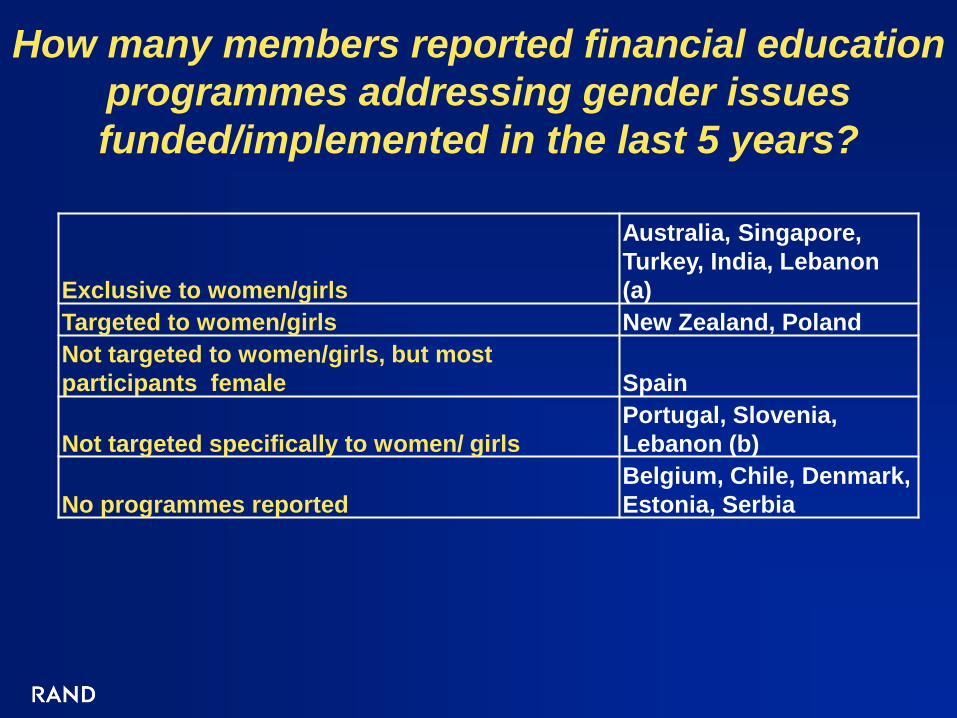

How many members reported financial education

programmes addressing gender issues

funded/implemented in the last 5 years?

Exclusive to women/girls

Australia, Singapore,

Turkey, India, Lebanon

(a)

Targeted to women/girls New Zealand, Poland

Not targeted to women/girls, but most

participants female Spain

Not targeted specifically to women/ girls

Portugal, Slovenia,

Lebanon (b)

No programmes reported

Belgium, Chile, Denmark,

Estonia, Serbia

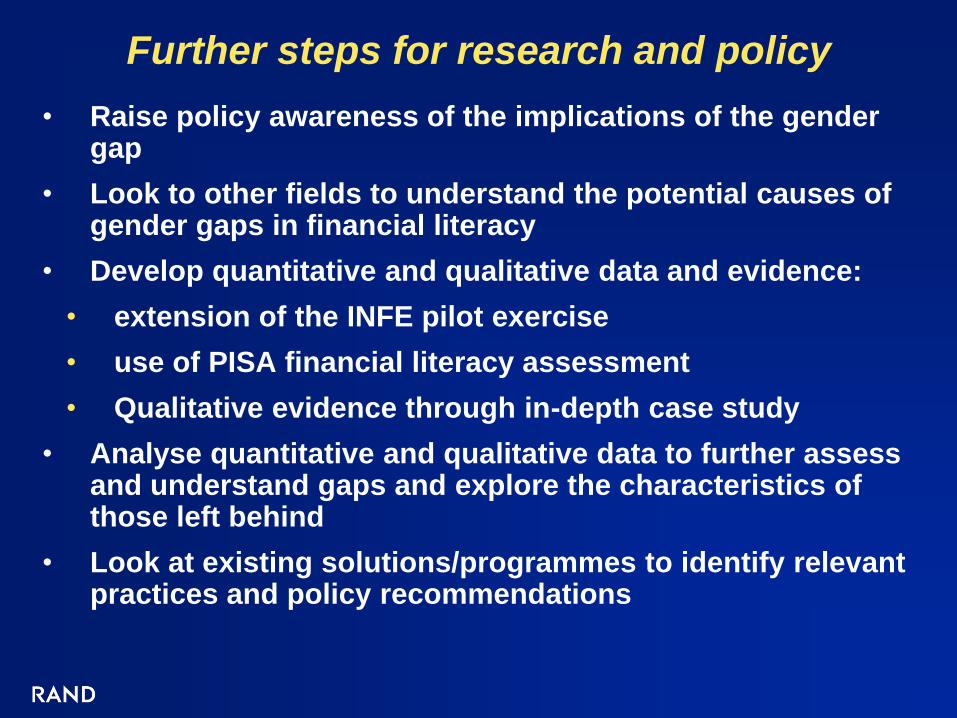

Further steps for research and policy

• Raise policy awareness of the implications of the gender gap

• Look to other fields to understand the potential causes of gender gaps in financial literacy

• Develop quantitative and qualitative data and evidence:

• extension of the INFE pilot exercise

• use of PISA financial literacy assessment

• Qualitative evidence through in-depth case study

• Analyse quantitative and qualitative data to further assess and understand gaps and explore the characteristics of those left behind

• Look at existing solutions/programmes to identify relevant practices and policy recommendations