Embed Size (px)

DESCRIPTION

From Crisis to Recovery In A Multi-Polar World. IMF Regional Economic Outlook October 2010. Dr. Nasser Saidi, Chief Economist & Head of External Relations, DIFC Authority 24 th October 2010. Agenda. Decoupling: Moving ahead, but @ different speeds. - PowerPoint PPT Presentation

Citation preview

From Crisis to Recovery In A Multi-Polar WorldIMF Regional Economic Outlook October 2010

Dr. Nasser Saidi,Chief Economist & Head of External Relations, DIFC Authority

24th October 2010

Agenda

Decoupling: Moving ahead, but @ different speeds

Increasing links with Asia: Trade & Financial Linkages

New Economic Geography Necessitates Policy Reforms

Decoupling: Back to the Forefront• The Oct 2010 WEO forecasts emerging market

economies (EMEs) to grow at 7.1% compared to advanced economies 2.7%.

• Business cycles are becoming more closely linked intra industrial countries & EMEs.

• However, there is a decoupling of business cycles b/n the two groups (Kose, Otrok & Prasad, 2008).

• Decoupling has resulted from increased trade & financial flows between EMEs.

Stylised facts on EMEs:

• Fiscal consolidation + financial sector reforms in years preceding the crisis contributed to resilience to the Great Recession

• Felt the effects of the global crisis later than the advanced economies, but have also recovered more sharply.

• By 2030, Asian GDP is expected to exceed that of the G7 major industrial economies.

Source: IMF WEO, Oct 2010, Llaudes et.al (2010)

-4

-2

0

2

4

6

8

10

Advanced Eco's

MENA

Emerging&DevelopingEco's

Evident Divergence in Economic Growth

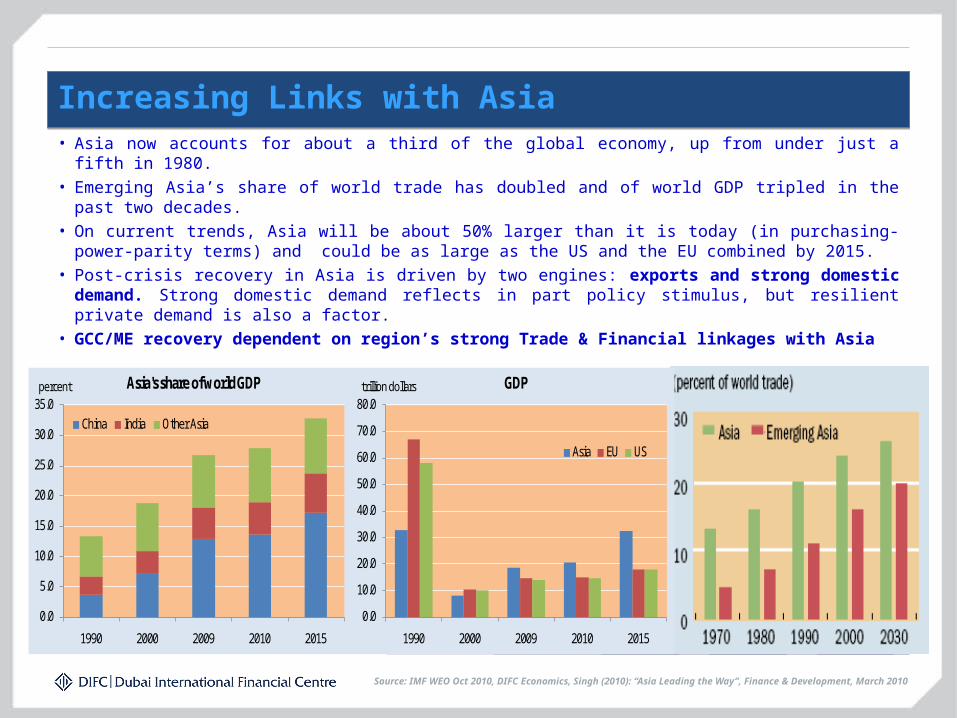

Increasing Links with Asia• Asia now accounts for about a third of the global economy, up from under just a fifth in 1980.

• Emerging Asia’s share of world trade has doubled and of world GDP tripled in the past two decades.

• On current trends, Asia will be about 50% larger than it is today (in purchasing-power-parity terms) and could be as large as the US and the EU combined by 2015.

• Post-crisis recovery in Asia is driven by two engines: exports and strong domestic demand. Strong domestic demand reflects in part policy stimulus, but resilient private demand is also a factor.

• GCC/ME recovery dependent on region’s strong Trade & Financial linkages with Asia

Source: IMF WEO Oct 2010, DIFC Economics, Singh (2010): “Asia Leading the Way”, Finance & Development, March 2010

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

1990 2000 2009 2010 2015

China India Other Asia

Asia's share of world GDPpercent

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

1990 2000 2009 2010 2015

Asia EU US

GDPtrillion dollars

GCC Increasing Links with Asia: Trade• Crisis led to sharp downturns in the more

export-oriented economies of Asia

• But, recent data (H1-2010) suggest that GCC-Asia trade has bounced back to pre-crisis levels (Q3 2008).

• Asia is currently the GCC’s largest trade partner in exports (23.5% of total GCC trade);

• Asia is second trade partner (26.3%) to EU (28%) in GCC imports.

• Within Asia, India and China have the largest share of trade with the GCC.

• Gulf countries increasingly integrated into Asia global supply chain: e.g. oil, gas, aluminum

• Increasingly important role of infrastructure & trade logistics in increasing connectedness & growing intra-industry trade

Source: IMF DOTS, DIFC Economics

0

5000

10000

15000

20000

25000

30000

35000

Q1

20

00

Q3

20

00

Q1

20

01

Q3

20

01

Q1

20

02

Q3

20

02

Q1

20

03

Q3

20

03

Q1

20

04

Q3

20

04

Q1

20

05

Q3

20

05

Q1

20

06

Q3

20

06

Q1

20

07

Q3

20

07

Q1

20

08

Q3

20

08

Q1

20

09

Q3

20

09

Q1

20

10

GCC: Rising Role of India & China

China India Korea

USD mn

0100002000030000400005000060000700008000090000

Q1

20

00

Q3

20

00

Q1

20

01

Q3

20

01

Q1

20

02

Q3

20

02

Q1

20

03

Q3

20

03

Q1

20

04

Q3

20

04

Q1

20

05

Q3

20

05

Q1

20

06

Q3

20

06

Q1

20

07

Q3

20

07

Q1

20

08

Q3

20

08

Q1

20

09

Q3

20

09

Q1

20

10

Asia EU US Japan

GCC's Growing Links with Asia

Major Trading Partners of the GCC - Exports

Asia, 14.1 Africa, 3.4Middle East exclu. Intra-

GCC, 2.2

EU, 11.3

US, 10.6Japan, 23.3

Other Advanced

Economies, 20.8

Others, 9.92000

Asia, 23.5

Africa, 3.0

Middle East exclu. Intra-

GCC, 4.2EU, 6.7

US, 6.8Japan, 17.9

Other Advanced

Economies, 20.4

Others, 10.92009

Asia’s rising share in exports

Source: IMF DOTS, DIFC Economics

Major Trading Partners of the GCC - Imports

Source: IMF DOTS, DIFC Economics

Asia, 14.2 Africa, 1.4

Middle East exclu. Intra-GCC, 11.7

EU, 33.2US, 13.0

Japan, 10.1

Other Advanced

Economies, 20.6

Others, 6.02000

Asia, 26.3

Africa, 1.2

Middle East exclu. Intra-

GCC, 2.9

EU, 28.0

US, 10.3

Japan, 6.2

Other Advanced

Economies, 17.2

Others, 5.9 2009

GCC’s Major Import Partners – the EU and Asia dominate

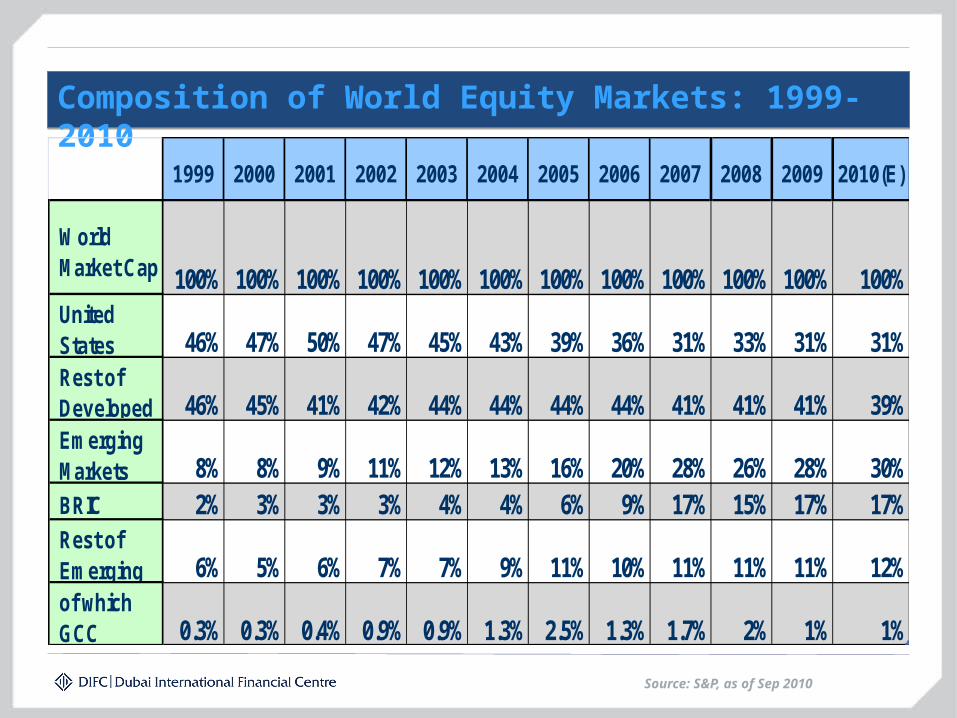

Composition of World Equity Markets: 1999-2010

Source: S&P, as of Sep 2010

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010(E)

World Market Cap 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%United States 46% 47% 50% 47% 45% 43% 39% 36% 31% 33% 31% 31%Rest of Developed 46% 45% 41% 42% 44% 44% 44% 44% 41% 41% 41% 39%Emerging Markets 8% 8% 9% 11% 12% 13% 16% 20% 28% 26% 28% 30%BRIC 2% 3% 3% 3% 4% 4% 6% 9% 17% 15% 17% 17%Rest of Emerging 6% 5% 6% 7% 7% 9% 11% 10% 11% 11% 11% 12%of which GCC 0.3% 0.3% 0.4% 0.9% 0.9% 1.3% 2.5% 1.3% 1.7% 2% 1% 1%

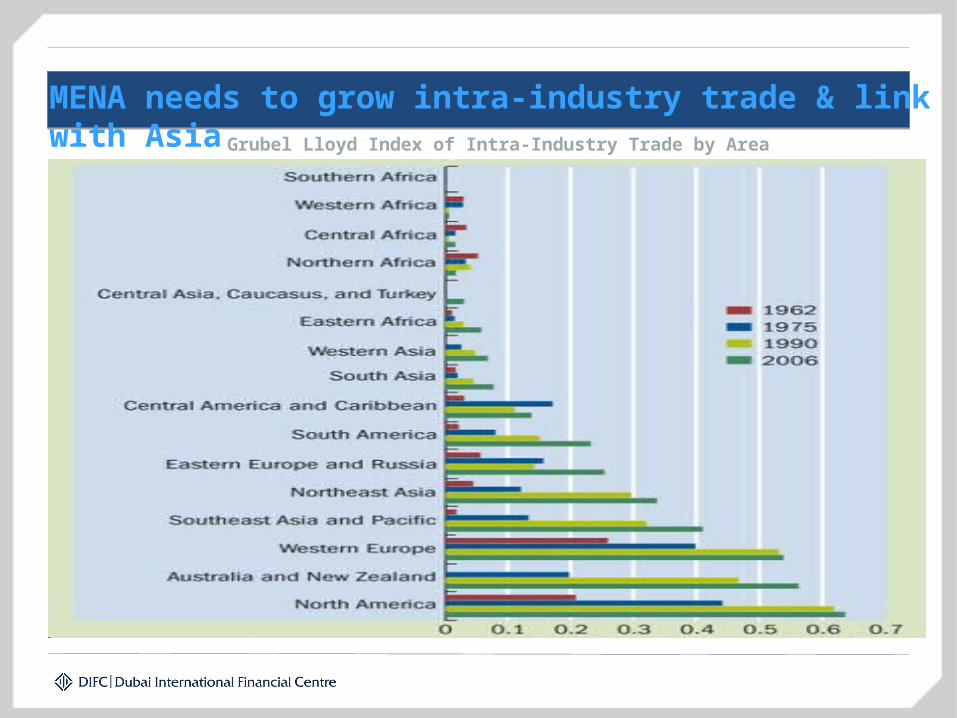

MENA needs to grow intra-industry trade & link with AsiaGrubel Lloyd Index of Intra-Industry Trade by Area

Policy Reform I: Re-Orient Trade & Investment Policies

•GCC/ME should re-orient Trade, Investment & Financial linkages towards Asia:• Free Trade & Investment Agreements with China, India, ASEAN• Chiang Mai Agreement

•Strengthen financial linkages by:• Linking Stock Exchanges• Integrating Payment systems• Regulatory & Supervisory Agreements: e.g. DFSA MRA with Malaysia

•DIFC signed MOU with Hong Kong Monetary Authority and currently in the process of developing close relations with major financial centres with EMEs in Asia, Africa. LATAM

•Move towards a ‘spider-web’ of financial markets away from ‘hub-spoke’ model

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

European Union

United States

Japan Newly indus. Asia

Asia Western Hemi

MENA

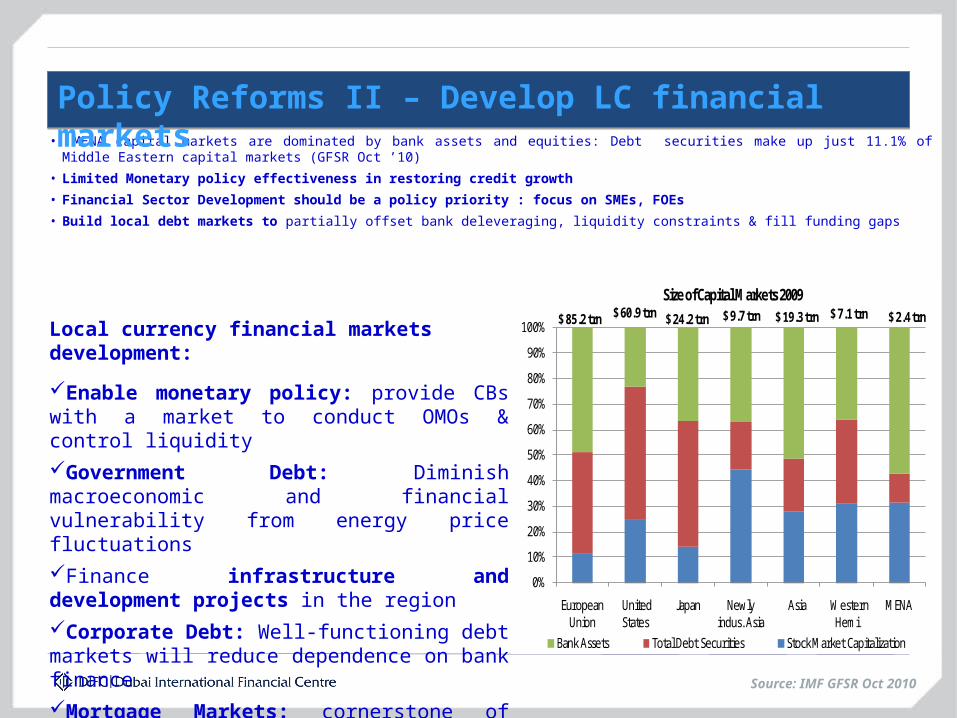

Bank Assets Total Debt Securities Stock Market Capitalization

Size of Capital Markets 2009$ 85.2 trn $ 60.9 trn $ 24.2 trn $ 9.7 trn $ 19.3 trn $ 7.1 trn $ 2.4 trn

• MENA capital markets are dominated by bank assets and equities: Debt securities make up just 11.1% of Middle Eastern capital markets (GFSR Oct ’10)

• Limited Monetary policy effectiveness in restoring credit growth

• Financial Sector Development should be a policy priority : focus on SMEs, FOEs

• Build local debt markets to partially offset bank deleveraging, liquidity constraints & fill funding gaps

Source: IMF GFSR Oct 2010

Policy Reforms II – Develop LC financial markets

Local currency financial markets development:

Enable monetary policy: provide CBs with a market to conduct OMOs & control liquidity

Government Debt: Diminish macroeconomic and financial vulnerability from energy price fluctuations

Finance infrastructure and development projects in the region

Corporate Debt: Well-functioning debt markets will reduce dependence on bank finance

Mortgage Markets: cornerstone of housing finance

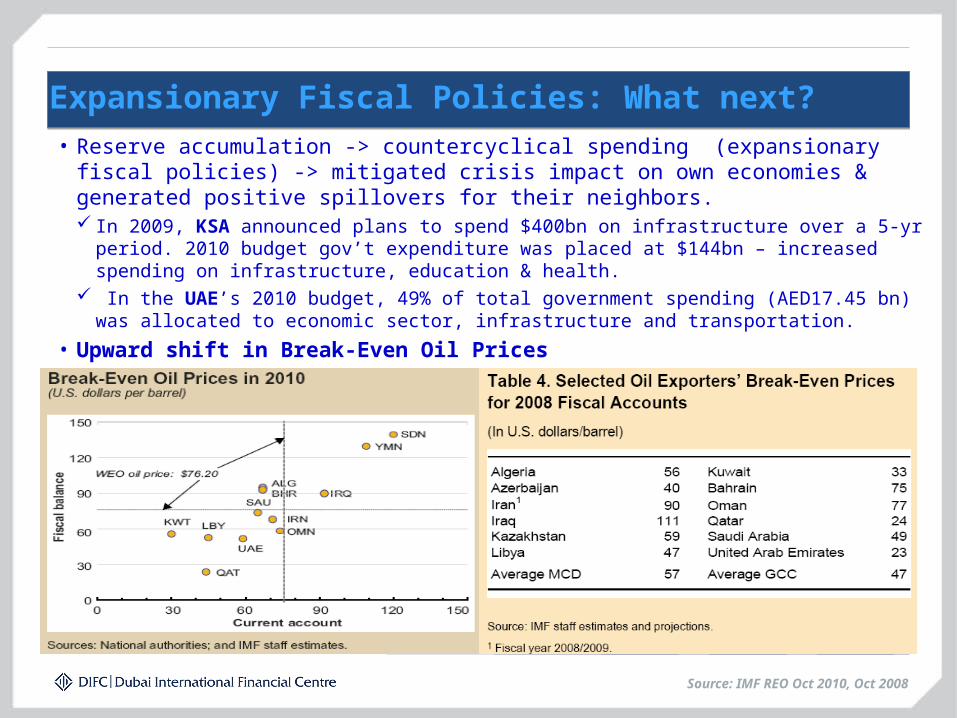

Expansionary Fiscal Policies: What next?

Source: IMF REO Oct 2010, Oct 2008

• Reserve accumulation -> countercyclical spending (expansionary fiscal policies) -> mitigated crisis impact on own economies & generated positive spillovers for their neighbors. In 2009, KSA announced plans to spend $400bn on infrastructure over a 5-yr period. 2010 budget

gov’t expenditure was placed at $144bn – increased spending on infrastructure, education & health. In the UAE’s 2010 budget, 49% of total government spending (AED17.45 bn) was allocated to

economic sector, infrastructure and transportation.

• Upward shift in Break-Even Oil Prices

Policy Reforms III: Rev. Diversification + Pvt Sec Participation

• Fiscal stimulus/counter-cyclical spending => major driver of recovery

• But: Increase in Structural Non-Oil Deficits

• Economic diversification dependent on increased private participation by SMEs and FOEs

• Policy reforms required including:

Fiscal policy focus on non-oil deficits

Review distorting fuel subsidies

Revenue diversification: GCC-wide VAT

Decrease Cost of Doing Business;

Attract private sector participation;

Infrastructure development (through PPPs).

Source: IMF REO, Oct 2010

2006 2007 2008 2009 2010f 2011fBH -28.3 -29.6 -31.9 -34.3 -34.8 -32.1KW -30.3 -27.7 -76.1 -69.8 -69.9 -70.6OM -54.5 -47.5 -54.8 -52 -58.1 -56.3QA -40.6 -30.7 -20.4 -9.3 -17.4 -23.4KSA -44.8 -51.3 -49.8 -63.4 -65.7 -61.2UAE -13.7 -14.2 -27.9 -37.3 -31.8 -22.9GCC -37.8 -39.9 -46.9 -53.5 -54.6 -51.1

General Government Non-Oil Fiscal Balance (% of non-oil GDP)

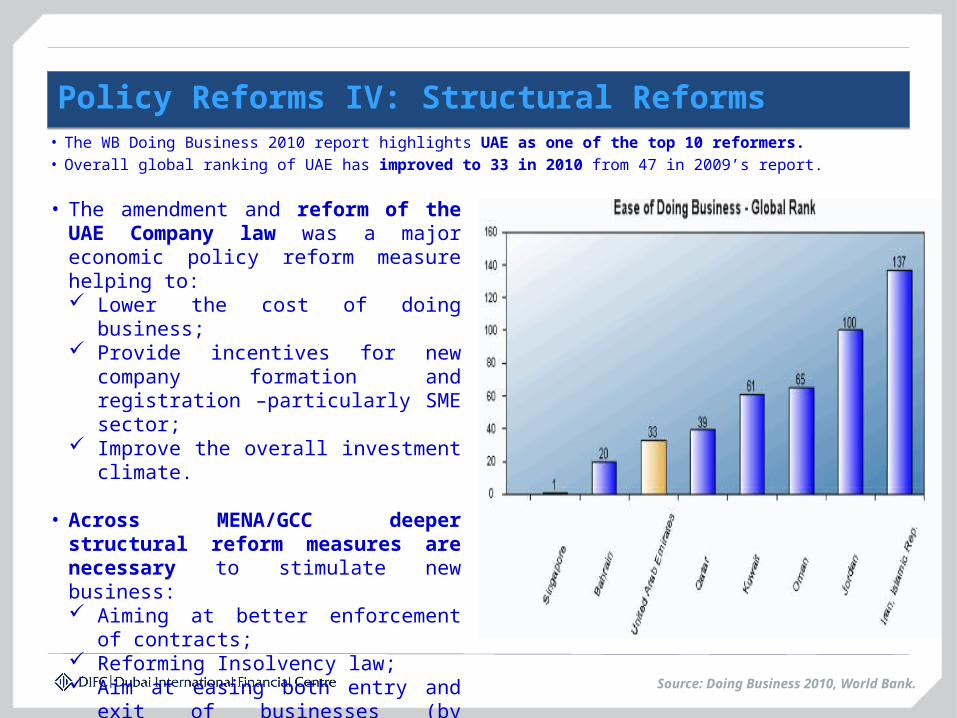

Policy Reforms IV: Structural Reforms

Source: Doing Business 2010, World Bank.

• The WB Doing Business 2010 report highlights UAE as one of the top 10 reformers.• Overall global ranking of UAE has improved to 33 in 2010 from 47 in 2009’s report.

• The amendment and reform of the UAE Company law was a major economic policy reform measure helping to: Lower the cost of doing business; Provide incentives for new company

formation and registration –particularly SME sector;

Improve the overall investment climate.

• Across MENA/GCC deeper structural reform measures are necessary to stimulate new business: Aiming at better enforcement of

contracts; Reforming Insolvency law; Aim at easing both entry and exit of

businesses (by reducing cost and minimizing uncertainty).

Summing Up: Policy Priorities to sustain recovery

New Silk Road requires shift in trade, investment & financial policies towards Asia and EMEs

Engage in design of new International Financial Architecture, Policy & Regulation

Develop Local Currency Financial Markets

Access to Finance for SMEs & FOEs

Fiscal Reform: Revenue diversification/ Expenditure rationalisation

Increased Private Sector Participation

Infrastructure Development through Public-Private Partnerships

Insolvency/ Bankruptcy & Creditor Rights frameworks

Thank You!