Embed Size (px)

DESCRIPTION

Very good information stuff

Citation preview

Food Processing Industry - India

December 2009

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

2FOOD PROCESSING INDUSTRY – INDIA.PPT

Executive Summary

Market

Drivers &

Challenges

Competition

�Food processing industry in India is valued at USD 70 bn and is growing at a 14% annual rate

�Diary products, fruits & vegetables and meat processing are the most attractive segments

�Government of India is leading from the front to ensure multi-fold growth in this segment

�Exports in food processing are expected to grow further in the near future

Drivers:

– Increasing consumer spend on

processed foods

– Competitive edge in food

processing

– Government support

– Growth in food processing exports

– Adoption of contract farming

– Increasing food retailing in India

– Growth in terminal markets

Challenges:

– Lack of integrated supply chain and scale

of operations

– Limited use of technology in food

processing

– Low level of penetration in domestic

market

– High taxes on branded agricultural

products

•PepsiCo

•Nestle

•Agro Tech Foods

•Unilever

•Haldirams

•MTR Foods

•Dabur Foods

•Gits Food Products

Major Foreign PlayersMajor Domestic Players

�The sector is highly competitive with many foreign players and large unorganized segment

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

3FOOD PROCESSING INDUSTRY – INDIA.PPT

•Market Overview

•Drivers & Challenges

•Government Initiatives

•Competition

•Key Developments

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

4FOOD PROCESSING INDUSTRY – INDIA.PPT

Food processing is a large sector that covers many activities

like agriculture, horticulture, animal husbandry etc.

Food Processing

Diary Sector

Fruits & Vegetables

Meat & Poultry

Fisheries

Packaged Foods

Beverages

Staples

Processed milk products like butter, cheese, ghee, ice

cream etc.

Raw fruits and vegetables, pulps, canned fruits, juices and

pickles

Cattle, buffaloes, sheep, pigs and poultry

Marine fisheries, frozen and minced fish products

Noodles, vermicelli, tomato ketchup, jam , soups etc.

Carbonated drinks, fruit-based drinks and hot beverages

Sugar, wheat, bread, flour and salt

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

5FOOD PROCESSING INDUSTRY – INDIA.PPT

Food processing industry in India has huge untapped

potential and offers scope for large investments

•Industry is valued at USD 70 bn and is growing

at 14% annually

•India is one of the top producers of milk,

pulses, sugarcane and tea in the world

•Government has taken major initiatives

towards ensuring multi-fold growth in this

sector that has an investment opportunity of

about USD 24 bn by 2015

•Mega Food Parks are coming up in India to

integrate the supply chain and promote food

processing

•States like Andhra Pradesh, Uttar Pradesh and

Madhya Pradesh are highly attractive for food

processing industry

•Huge foreign direct investments have been

made in 2007-08 totalling ~USD 143 mn

Market Overview Market Size & Growth

Source: Ministry of Food Processing Industries, IBEF articles & KPMG Research

10491

8070

0

20

40

60

80

100

120

2009 2010e 2011e 2012e

+14%

USD bn

Market Penetration of Segments

37%Diary Sector

10%Fruits & Vegetables

6% 10%Meat & Poultry

12%Fisheries

3%Packaged Foods

Range 6 – 10%

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

6FOOD PROCESSING INDUSTRY – INDIA.PPT

Diary products and fruits & vegetables are the most

attractive segments for investments

Source: Press articles; Ministry of Food Processing website; IBEF & KPMG research report “Food Processing- market & opportunities”, Apr 2008

Growth

Rate

+15%

Growth

Rate

+20%

Dairy Products

• India is the leading producer of milk in the world, about 108 mn tonnes in 2007

• ~37% of the produced milk is processed and ~676 diary plants are registered with the government

• Growing segments

� Branded butter market is valued at USD 133 mn and is estimated to grow at 8-10% per annum

� Cheese market is valued at USD 110 mn and is growing rapidly in urban areas at about 15%

� Ghee is growing at a rate of 8% annual rate with 24.1% penetration across country

� Ice cream market is valued at USD 199 mn in India and is growing at 20% annual rate

• Other emerging segments include are Ultra Heated Treatment (UHT) and flavored milk

� UHT milk is gaining popularity and the market is estimated at USD 33.4 mn

Fruits and Vegetables (F&V)

• Globally, India is second and third largest producer of vegetables (100 mn tonnes) and fruits (50 mn

tonnes) respectively

� India accounts for 8.4% of the world’s F&V production

• Area under fruit cultivation is about 4.8 mn hectares and that of vegetables is 7.59 mn hectares

• Less than 2% of total vegetables produced are processed commercially in India

• Share of organized sector in fruits processing is ~48%; ~20% of processed F&V are exported

� Mango and its other products alone constitute 50% of the total F&V exports

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

7FOOD PROCESSING INDUSTRY – INDIA.PPT

Meat processing is less penetrated in India and fisheries are

majorly export oriented

Source: Press articles; Ministry of Food Processing website; IBEF & KPMG research report “Food Processing- market & opportunities”, Apr 2008

Meat & Poultry

• India has the largest livestock population (470 mn) globally (50% of buffaloes and 16% of goats)

• Processing of meat in India is licensed under MFPO (Meat Food Products Order) act, 1973

� Registered under MFPO are 3,600 slaughter houses, 9 modern abattoirs and 171 meat processing units

• About 5 mn tonnes of meat is produced per year in India

� Per head consumption of fresh and processed meat is as low as 1.5 kg in India against world average of 35.5 kg

• Majority of animals in India are not bred for meat, the processing percentage for meat is as follows

– Buffaloes (11%), Cattle (6%), Sheep (33%), Goat (38%)

• The annual poultry production in India is 450 mn broilers and 33 bn eggs growing at 20% and 16%

� Major poultry exports are to Maldives, Oman , Japan, Malaysia, Indonesia and Singapore

Fisheries

• Fisheries sector is classified in to marine, in-land and aquaculture and India ranks third in fish

production in the world, it also ranks second in in-land fish production

• About 60% production comes from marine resources and fish processing in to canned and frozen

forms and is primarily targeted for export markets

� Frozen shrimp contributes to 34.62% of exports in terms of volume and 63.5% in value

• India has about 369 freezing units with daily processing capacity of 10,226 tonnes and 499 frozen

storage units with a capacity of 134,767 tonnes

Growth

Rate

+10%

Growth

Rate

+20%

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

8FOOD PROCESSING INDUSTRY – INDIA.PPT

Packaged foods, beverages and staples are restricted to

urban areas, characterized by high volumes and low margins

Source: Press articles; Ministry of Food Processing website; IBEF & KPMG research report “Food Processing- market & opportunities”, Apr 2008

Packaged Foods

• Packaged foods primarily includes ready-to-eat snacks, chips, namkeen, bakery products etc.

� India has around 60,000 bakeries; 20,000 traditional food units

• Growing segments

� Noodles growing at over 15% annually and branded noodles is estimated to be 230 mn servings/yr

� Soups market is at a nascent stage and is valued at USD 14 mn

� Confectionaries market pegged at USD 484.3 mn while biscuit market at USD 373.4 mn growing at 5.7% & 7.5%

� Biscuit market is estimated to be USD 373.4 mn and is growing at 7.5%

� Culinary products is growing at 18-20% per annum, also tomato ketchups and jams at 20% per annum

Beverages

• Primarily comprises non-alcoholic beverages like aerated soft drinks, fruit juices and hot beverages

• 100 plants across India under aerated soft drinks segment and exports in soft drinks are valued at

USD 156 mn per annum; attracted highest foreign direct investments valued at more than USD 1 bn

• India is the largest tea producer in the world accounting for 28% of global production and 5th

largest coffee producer accounting for 4% of total production in the world

Growth

Rate

+8%

Growth

Rate

+27%

• Second largest wheat producer globally with an output of 70 mn tonnes valued at USD 195 mn

• Bread production is growing at 7.5% and organized market accounts for ~55% of the market

• 10,000 pulse mills with 14 mn tonnes milling capacity per annum

Growth

Rate

+85%

Beverages

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

9FOOD PROCESSING INDUSTRY – INDIA.PPT

•Market Overview

•Drivers & Challenges

•Government Initiatives

•Competition

•Key Developments

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

10FOOD PROCESSING INDUSTRY – INDIA.PPT

Drivers & Challenges

Increasing food retailing in India

Adoption of contract farming

Growth in terminal markets

Increasing consumer spend on

processed foods

Growth in food processing exports

Drivers

Competitive edge in food processing

Government support

High taxes on branded agricultural

products

Low level of penetration in domestic

market

Lack of integrated supply chain and

scale of operations

Challenges

Limited use of technology in food

processing

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

11FOOD PROCESSING INDUSTRY – INDIA.PPT

Rising disposable income and increasing spend on food will

boost the processed food market in India

• In the last 5 years an increase in per capita disposable income of 8% has led to an increase in

per capita consumption expenditure on food by over 20%

• Consumption of primary and secondary processed foods has grown rapidly over the past few

years owing to the following factors:

� Four-fold growth in size of households in middle to very rich segment

� Increase in the youth (age group 15 – 25) in the country

� Growing migration of population from rural to urban India

• In agro-products, fruits & vegetables is the largest consumption category accounting for 50% of

the total consumption

Increasing consumer spend on processed foods Impact

70%

Agri-products

30%

Milk & milk products,

meat & marine products

66%Primary & secondary

processed foods

34%Others

Source: FICCI - E&Y study “‘Flavours of Incredible India – Opportunities in the Food Industry’, Oct 2009

Expenditure on Food by Indian Consumers

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12FOOD PROCESSING INDUSTRY – INDIA.PPT

Low cost of production, favourable conditions and

government support gives India a competitive edge

• India has a competitive edge in food processing as it has the largest irrigated land and livestock

population in the world

• India is also the largest producer of milk, tea and pulses and is one of the leading countries in

the production of fruits and vegetables

• India is a favorable market to set-up large low cost production base with effective utilization of

available cheap workforce

• Cost of production in India is 40% lower than many of the locations in Europe and about 10-15%

lower to that of United Kingdom

Competitive edge in food processing

• The government of India has taken several initiatives to promote investments in this sector

• 100% FDI as well as technology transfer is allowed in this sector and grants are given by the

government for setting up common facilities in Agro Food Park

• Institutional and credit support is provided for new industries in fruits & vegetables and income

tax rebate is allowed for 100% of profits for first 5 years and 25% for next 5 years

• Central excise duty on meat, poultry and fish is reduced to 8%, customs duty on packaging

machines has also fallen

• Custom duty on food processing machinery and its parts is reduced from 7.5% to 5%

• Custom duty on packaging machinery is reduced from 15% to 5% and on reefer vans from 20%

to 10%

• Diary machineries are completely exempted from central excise duty

Government support

Impact

Source: Ministry of Food Processing Industries, India; Indian Brand Equity Foundation report 2008

Impact

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

13FOOD PROCESSING INDUSTRY – INDIA.PPT

Exports of processed food and the adoption of contract

farming will drive the market

1.74 1.930.670.790

2

4

1.292.08

2003-04

1.30

1.97

2004-05

1.48

3.22

2005-06

2.001.26

3.26

2006-07

1.72

3.65

2007-08

Fruits & Vegetables

Diary, Poultry &

Meat Products

+15%mn metric

tonne

• Exports from India in food processing sector is growing every year at a significant rate

• Processed foods contribute to about 5% of the total exports from India

• Targets set by the government are will be a major driving force for the market

Growth in food processing exports Impact

Source: APEDA (Agricultural and Processed Food Products Export Development Authority) India report; Financial express “Contract farming did no good to farmers, says

IIM-A study”

Food Processing Exports Growth in Volume

• In contract farming

� Food processors gets into an agreement with the farmer who is contracted for planting a particular crop and

produce an agreed yield of certain quality at a pre-agreed price

� The food processor provides the required support in terms of technology and training to the farmer so as to

get the agreed results

• This eliminates the supply shocks for farmer and generates steady source of income and assures

good quality farm inputs, to the processor, which is crucial in this business

• This model minimizes risks for processors and producers and is expected to lead to a larger

demand for processed food due to the enhancement of quality of the food processed

Adoption of contract farming ImpactISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

14FOOD PROCESSING INDUSTRY – INDIA.PPT

Growing food retail formats and outlets in India is a major

driving force for processed food products

Increasing food retailing in India

• The Indian consumers have various outlets in the neighbourhood to purchase food products

• Food retailing formats are growing in India ranging from neighbourhood stores, supermarkets,

hypermarkets to cash and carry stores

• All these outlets contribute to the growth in food trade and hence many corporate houses are

moving to food retail

• HUL, ITC and Dabur has already forayed in to this space and are planning to increase their

outlets and have a pan-India coverage

• Established players are planning to tap the backward linkages and expand their geographies

� Players include Reliance Fresh, More, Spencer’s Daily, Food Bazaar, Subhiksha, Food World, Nilgiris etc.

• The food retail business in India is growing at a 30% annual rate, thereby providing huge scope

for food processing players to reach end-users

• Government of India is also promoting this business by allowing 51% FDI by single brand

companies and in future plans to increase this limit in order to promote food processing

industry

• There is also a growing trend of franchising food retail outlets in India especially the quick serve

joints like KFC, McDonald’s, Pizza Hut, Nirula’s etc. which enables deep penetration in less time

Source: Chilli Breeze article “Food Retail in India – Growth, Growth and More Growth”; Business Line “Food retailing needs to perfect franchise recipe “, Apr 2009

Impact

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

15FOOD PROCESSING INDUSTRY – INDIA.PPT

Development of terminal markets creating linkages with

aggregators and logistics providers

• Terminal market is an assembly and trading place for agricultural commodities

� The produce is either sold to end consumer or food processor, packaged for export or stored in a cold

storage for future disposal

� The infrastructure of terminal markets include electronic auctioning facility, pre-cooling, cold storage,

ripening chambers, grading packaging facilities, processing units and other allied infrastructures like banks,

post office etc

� These terminal markets operate on a hub and spoke model with market being the hub and collection centers

which are located close to the production areas act as spokes

• In order to integrate the domestic produce with retail chains the government of India is

promoting terminal markets

� It plans to set-up 8 terminal markets with an investment of USD 131 mn

– Cities under consideration are Mumbai, Nashik, Nagpur, Chandigarh, Rai, Patna, Bhopal and Kolkata

� 21 more terminal markets are proposed for future

• This will allow the market to develop due to stronger integration between food producers and

processors

Growth in terminal markets Impact

100

100

125

Area Required (Acres)

750

1000

3000

Handling Capacity

(Metric Tonne)

12Nagpur

13Nashik

43-54Mumbai

Project Cost (USD mn)Terminal Markets

Source: Maharashtra State Agricultural Marketing Board “Projects: Terminal Markets”, IBEF and other press articles

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

16FOOD PROCESSING INDUSTRY – INDIA.PPT

Small scale of operations and limited use of technology are

the major challenges for this sector

• Due to lack of proper value chain for food processing in India, produce worth USD 10 bn is

wasted every year in India

• Nearly 20-25% of the fruits & vegetables production in India is lost in spoilage at various stages

of harvesting

• Lack of technology, poor quality of seeds and planting material is one of the reasons for this,

scale of operations is also a key factor

• About 90% of the units are small scale and hence does not reap the benefits of economies of

scale, this also applies to land holdings

• A proper integrated supply chain is needed along with scale of operations to improve efficiency

in this sector

Lack of integrated supply chain and scale of operations

• Food processing in India is majorly a manual process with limited use of technology like pre-

cooling facilities for vegetables

• Technology plays a major role for storing fruits & vegetables for a long period in order to enable

further processing

• There are about 3600 licensed slaughter-houses in India but due to lack of technology, meat

processing is low in India considering the large animal population available in the country

• India has to bring in modern technology for food processing in order to improve process

efficiency and quality of end product

Limited use of technology in food processing

Impact

Source: IBEF report 2008; igovernment article “India to set up 30 food parks”, May 2008

ImpactISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

17FOOD PROCESSING INDUSTRY – INDIA.PPT

Low penetration levels in domestic market and high taxes

on branded products affects this industry

• The penetration levels in the domestic market are low in India because majority of processing

units are export oriented

• Share of ghee in branded milk products is still as low as 2%, penetration of culinary products is

13.3% with major emphasis is given to sales in cities

• Packaged biscuits consumption is as low as 0.48% in India while it is about 4% in the US

• India has large untapped domestic potential

Low level of penetration in domestic market Impact

Source: Economic Times “Food processing can create more jobs”, Jul 2009; igovernment article “India to set up 30 food parks”, May 2008; Yahoo news “High taxes hitting

food processing sector: Assocham” Nov 2009

020

4060

8080%

Brazil

70%

Malaysia

40%

Philippines

5%

78%

China

30%

Thailand India

%

Processing % of Food Produced Across Countries

• Besides 12.5% of value-added tax, branded processed products are subject to a 2% central sale

tax and also attract local entry tax and octroi up to 4%

• On the other hand, unbranded products are in many cases exempted from tax or often taxed at

a 4% confessional rate, this is adversely affecting the competitiveness of the sector

High taxes on branded agricultural products Impact

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

18FOOD PROCESSING INDUSTRY – INDIA.PPT

•Market Overview

•Drivers & Challenges

•Government Initiatives

•Competition

•Key Developments

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

19FOOD PROCESSING INDUSTRY – INDIA.PPT

Key Initiatives

Vision 2015

Tax Benefits Mega Food Parks Scheme

Financial SupportManpower Training

Trends

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

20FOOD PROCESSING INDUSTRY – INDIA.PPT

Government expects a 100 fold growth in food processing in

line with the high growth experienced by service sector

• The main priorities for the government in this sector is to encourage and increase food processing activities

• It expects to create 10 mn jobs by 2015 in the food processing sector in India

• It plans to promote partnership between agricultural and industrial sectors, to help farmers move up the

value chain

Government Initiatives

Source: Ministry of Food Processing India; Economic Times Interview with Food-processing minister “Food processing can create more jobs”, Jul 2009; The Financial

Express “Food processing min plans Rs 1,200-crore VC fund” Sep 2009

Vision 2015

• Tripling the size of industry from the current USD 70 bn to nearly 210 bn

• Raising the level of processing of perishables from 6% to 20%

• Increasing value addition from 20% to 35%

• Enhancing India’s share in the global food trade from 1.5% to 3%

Financial

Support

• Provides an investment opportunity of USD 24 bn

• Plans to set up a dedicated venture capital fund to support the investment

requirements

� The venture capital fund would be set up with a corpus of about USD 250 mn by Apr 2010

� Fund could be either a government initiative or under public-private-partnership model

• Participation from NABARD, IDBI, SIDBI, other banks and the private sector is

expected

• Plans to approach RBI to include food processing under the priority sector

lending

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

21FOOD PROCESSING INDUSTRY – INDIA.PPT

India to emerge as regional hub for food processing through

the Mega Food Parks Scheme by the government

Mega Food

Parks Scheme

(MFPS)

• Government plans on establishing 30 mega food parks in all states enabling

integration of the fruit and vegetable sector from farm gate to the retail outlet

� Operations towards developing 10 parks has begun

� All parks are expected to be established by 2015

• Government is supporting these parks by providing a portion of total capital

investment subject to a maximum of USD 11 bn

• It also plans to extend special economic zone benefits to food parks

Tax Benefits

• Government is planning to declare a tax holiday for all food processing units

• It also plans to extend 100% depreciation benefit for infrastructure projects in

the sector from first year onwards

• Plan for rationalization of duties for the industry

Manpower

Training

• Government plans to design a curriculum for skill development programmes in

consultation with HRD ministry, Labour ministry and institutions

• Plans to collaborate with aid agencies like World Bank and Asian Development

Bank to raise funds for running large-scale skill development programmes

• Prepare a blueprint for Skill Development Mission and collaborate with

Industrial Training Institutes (ITI) to focus on training the workers at various

levels of food processing

Source: Ministry of Food Processing India; Economic Times Interview with Food-processing minister “Food processing can create more jobs”, Jul 2009

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

22FOOD PROCESSING INDUSTRY – INDIA.PPT

•Market Overview

•Drivers & Challenges

•Government Initiatives

•Competition

•Key Developments

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

23FOOD PROCESSING INDUSTRY – INDIA.PPT

Indian food processing sector is highly competitive with

many foreign players in the market

• A highly competitive market with many domestic

players and their MNC counterparts fighting for

market share

� Competitive pricing, expansions, aggressive advertising

campaigns and efficient packaging are the strategies used

by firms to gain market share

• More players are planning to tap the mass market in

basic foods like fruits & vegetables, meat & poultry

and fisheries

Competition Segments Share

Source: D&B articles “Emerging SMEs of India- Food Processing”; IBEF report “Food Processing- market & opportunities”, Apr 2008; Press articles

80%Packaged Foods

77%Beverages

50%Staple Foods

48%Fruits & Vegetables

15%Diary Sector

5%Meat & Poultry

Segment-wise Organized Share

Other products

24%

Diary Products 5%

Staples

11%

Beverages

20%

Meat, Fish,

Fruits,Vegetables,

Oil40%

Food Processing Units in Organized Sector

174,296Rice Mills + Modernized Rice Mills

725Solvent Extract

429Sugar Mills

266Milk Products

656Sweetened and Aerated Water

171Meat Processing

5293Food and Vegetable

568Fish Processing

516Flour Mills

Note: Based on latest available data from the Ministry

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

24FOOD PROCESSING INDUSTRY – INDIA.PPT

Major Domestic Players (1/6)

• Dabur foods is a 100% subsidiary of Dabur India. Started in 1997 with the launch of packaged

fruit juices

• The company caters to beverages and culinary segment with products including fruit juices,

lemon drink , cooking pastes, coconut milk, tomato ketchup, corn flour etc.

• Major brands include Real, activ, BuRRst, HOMMADE, LEMONEEZ, CAPSICO etc.

• In addition to the retail sales, Dabur Foods is looking at increasing institutional sales to

hotels, restaurants and caterers

Financials:

• Turnover of Dabur Foods in 2005 was USD 27.9 mn

Dabur Foods

• Nusli Wadia group and Groupe Danone, a French food company, share 48.5% promoter

holding equally in Britannia

• Leading player in organized biscuit market with about 30% market share

• Plans to strengthen its position by launching new products and improving volumes and

introducing variants of the existing products

Financials:

• Annual sales turnover of USD 565.2 mn in 2008

Britannia

Business DescriptionCompany

Source: Company Websites and Articles Note: This list is not exhaustive

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

25FOOD PROCESSING INDUSTRY – INDIA.PPT

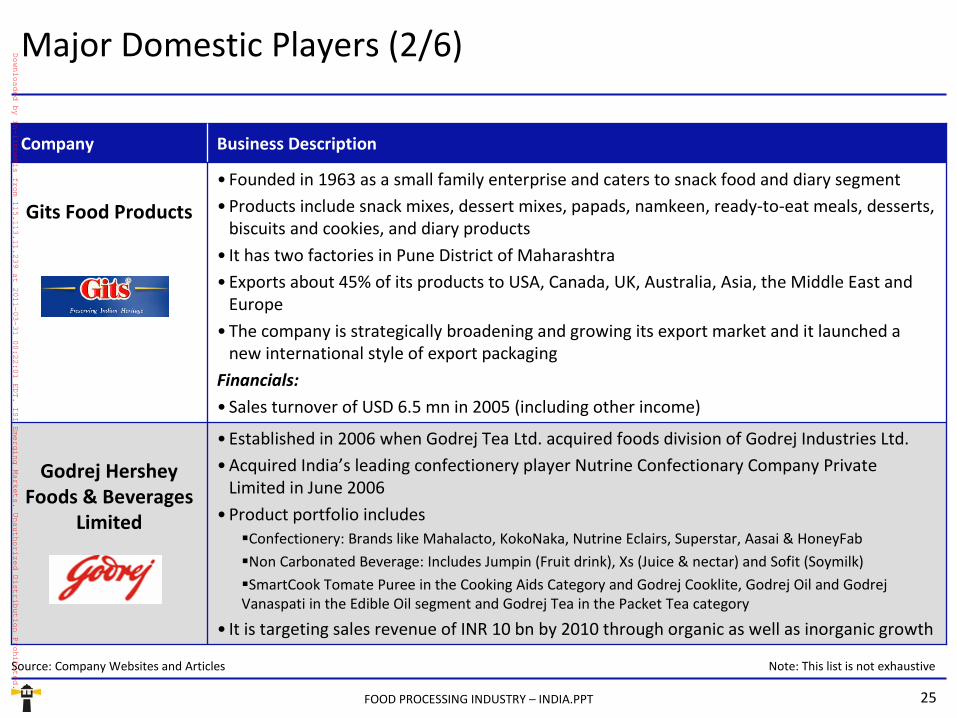

Major Domestic Players (2/6)

• Established in 2006 when Godrej Tea Ltd. acquired foods division of Godrej Industries Ltd.

• Acquired India’s leading confectionery player Nutrine Confectionary Company Private

Limited in June 2006

• Product portfolio includes

�Confectionery: Brands like Mahalacto, KokoNaka, Nutrine Eclairs, Superstar, Aasai & HoneyFab

�Non Carbonated Beverage: Includes Jumpin (Fruit drink), Xs (Juice & nectar) and Sofit (Soymilk)

�SmartCook Tomate Puree in the Cooking Aids Category and Godrej Cooklite, Godrej Oil and Godrej

Vanaspati in the Edible Oil segment and Godrej Tea in the Packet Tea category

• It is targeting sales revenue of INR 10 bn by 2010 through organic as well as inorganic growth

Godrej Hershey

Foods & Beverages

Limited

• Founded in 1963 as a small family enterprise and caters to snack food and diary segment

• Products include snack mixes, dessert mixes, papads, namkeen, ready-to-eat meals, desserts,

biscuits and cookies, and diary products

• It has two factories in Pune District of Maharashtra

• Exports about 45% of its products to USA, Canada, UK, Australia, Asia, the Middle East and

Europe

• The company is strategically broadening and growing its export market and it launched a

new international style of export packaging

Financials:

• Sales turnover of USD 6.5 mn in 2005 (including other income)

Gits Food Products

Business DescriptionCompany

Source: Company Websites and Articles Note: This list is not exhaustive

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

26FOOD PROCESSING INDUSTRY – INDIA.PPT

Major Domestic Players (3/6)

• Started in 1936, as a shop in Bikaneer, expanded to Delhi in 1982 and to USA in 1993

• It caters to snack food products like namkeen, syrup, sweets, crushes, chips and papads

• Major presence in North India and especially New Delhi

• Also exports its products to countries like US, UK, Canada, Australia, Singapore and UAE

• Follows competitive pricing strategy and caters to Indian palette with labour intensive

products

Haldirams

• Established in 1946

• It is is India's largest food products marketing organisation

• The company has a range of products in various segments namely Cheese, UHT milk, ghee,

milk powders, sweetened condensed milk, curd products, ice-creams and confectionary

• Exports its products to USA, Gulf Countries and Singapore

• It plans on expanding its outlets “Amul Parlour” from 4,000 to 10,000 by 2010.

Financials:

• Annual sales turnover of USD 1.5 bn in 2008-09

Gujarat

Cooperative Milk

Marketing

Federation (Amul)

Business DescriptionCompany

Source: Company Websites and Articles Note: This list is not exhaustive

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

27FOOD PROCESSING INDUSTRY – INDIA.PPT

Major Domestic Players (4/6)

• Established in 1989

• Product portfolio includes staples, ready to eat Indian curries, cook-in sauces, cooking paste

to spices, seasoning and frozen food

• Marketing their products by tying up with the major retail chains not just in the domestic

market but in the international markets

• Presently boasts of a distribution network of more than 200 thousand retail outlets, 100

super distributors and 600 stockists

• Exports its products to USA, UK, Dubai, Canada, Japan, Australia, Singapore and other

European countries.

Financial

• Net in FY ’08 stood at INR 6.4 bn

Kohinoor Foods Ltd

• Entered the branded & packaged foods business in 2001with its Kitchens of India brand

• Expanded to other brands namely Aashirvaad, Sunfeast, mint-o, Candyman and Bingo!

• Its product portfolio includes staples, biscuit, confectionary, snack foods and packet food in

the ready-to-eat format

• It has presence in USA, Canada, Switzerland, Mauritius and Germany

Financials

• Gross turnover was INR 231 bn in 2008-09

ITC Ltd.

Business DescriptionCompany

Source: Company Websites and Articles Note: This list is not exhaustive

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

28FOOD PROCESSING INDUSTRY – INDIA.PPT

Major Domestic Players (5/6)

• Top five processed food companies in India, MTR is an ISO 9002 and a HACCP certified

company

• Recently MTR is acquired by Orkla, a Norway-based company for USD 80 mn

• It caters to snack foods and ice cream products including ready-to-eat curries and rice, ready-

to-cook gravies, frozen foods, ice creams, instant snack and dessert mixes, spices, pickles etc.

• About 10% of the total sales comes from export market

• MTR which is established in south is developing its brand in the west and north India markets

• It also plans to expand its product line rapidly

Financials:

• Annual turnover of USD 40.6 mn in 2008

MTR Foods

• Set up in 1974 under the Operation Flood Programme and is now a wholly owned company

of the National Dairy Development Board

• Product portfolio includes liquid milk, dahi, ice creams, cheese and butter, Dhara range of

edible oils and the Safal range of fresh fruits & vegetables, frozen vegetables and fruit juices

at a national

• Recently developed a state-of-the-art fruit processing plant at Bangalore with fruit handling

capacity of around 250 MT per day

Mother Dairy

Business DescriptionCompany

Source: Company Websites and Articles Note: This list is not exhaustive

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

29FOOD PROCESSING INDUSTRY – INDIA.PPT

Major Domestic Players (6/6)

• Established in 1971

• Major market presence in the meat and poultry segment

Financials

• Net sales pegged at INR 5.2 bn for FY ‘08

Venkys’ India Ltd.

• Major brands include Frooti, Appy Classic in fruit-based drinks; Bailley in packaged drinking

water; Mintrox and ButterCup in confectionaries

• Parle Agro’s flagship product Mango Frooti has 75% market share in fruit based drinks

• Parle Agro has entered snack market recently with the launch of its brand Hippo

• It started Hippo with 5 flavours and plans a bigger portfolio in snacks segment

• Broad strategy is backward integration and aggressive media campaign during product

launches

Financials:

• Plans to increase its revenues from USD 206.6 mn to USD 761.3 by 2011

Parle Agro

Business DescriptionCompany

Source: Company Websites and Articles Note: This list is not exhaustive

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

30FOOD PROCESSING INDUSTRY – INDIA.PPT

Major Foreign Players (1/2)

• HUL is India’s largest FMCG firm with 51.55% stake holding from parent company Unilever

• Caters to Food and Beverages segment with products like jam, salt, wheat flour, soup, tea,

coffee and ice creams

• Major brands include Broke Bond and Lipton in Tea, Bru in coffee, Kwality Wall’s in ice

cream, Kissan jam, Knorr soup and Annapurna salt and wheat flour

• Foods segment contributes to 20% of the total HUL sales

• HUL divested its non-core businesses and focussed on its food business for driving growth

Financials:

• Annual sales turnover of USD 940 mn for HUL Foods segment in FY 2008-09

Hindustan Unilever

Limited

• Affiliated to ConAgra Foods Inc, USA which is a major foods company in the world

• ConAgra Foods along with Tiger Brands of South Africa holds a majority stake of 52.3% in

Agro Tech Foods Ltd, through CAG Tech Holdings

• A major player in edible oil and branded foods in India, it has a flagship brand Sundrop

• Product portfolio includes edible oil, vanaspati, atta, popcorn, french fries and green peas

• Plans to diversify its product portfolio and enter new markets with focus on product and

brand differentiation

Financials:

• Annual sales turnover of branded foods segment was USD 117.1 mn in 2007

Agro Tech Foods

Business DescriptionCompany

Source: Company Websites and Articles Note: This list is not exhaustive

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

31FOOD PROCESSING INDUSTRY – INDIA.PPT

Major Foreign Players (2/2)

• Started in 1959 as Food Specialities by Nestle SA which has 51% stake holding

• It caters to diary products, beverages and snack foods with products including instant coffee,

condensed milk, diary whitener, infant food, chocolates and confectionaries

• Nestle India is planning to launch new products in all its product segments

Financials:

• Annual sales turnover of USD 965.5 mn in 2008

Nestle India

• PepsiCo started its operations in India in the year 1989

• Caters to beverages and snack foods including soft drinks, fruit juice and chips

• It has 43 bottling plants in India, and it’s Frito Lay foods division has 3 plants

• PepsiCo is planning to invest USD 200 mn to set-up four new plants out of which 3 would be

for beverages and one for foods

• Major focus is on high volume scales, it is planning to set-up new greenfield plants and is

looking for new franchisee bottlers

PepsiCo

Business DescriptionCompany

Source: Company Websites and Articles Note: This list is not exhaustive

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

32FOOD PROCESSING INDUSTRY – INDIA.PPT

•Market Overview

•Drivers & Challenges

•Government Initiatives

•Competition

•Key Developments

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

33FOOD PROCESSING INDUSTRY – INDIA.PPT

Key Developments

Indian Farmers Fertiliser Cooperative Limited (IFFCO) to set-up a farm-based food processing SEZ with an

investment of USD 512.7 mn at Nellore, Andhra Pradesh.

Feb 2009

India’s largest sea food processing plant with a daily capacity of 40 ton has come up at Jankia, 50kms from

Bhubaneswar. The unit has a cold storage capacity of 1800 ton per day.

Sep 2009

An Indo-French joint working group (JWG) on agriculture is set-up to promote co-operation and France is

ready to help Indian food processing sector with latest technology.

Oct 2009

Government to provide food processing training to 500,000 women in collaboration with industrial training

institutes (ITI) as part of its efforts to create 10 mn jobs by 2015.

Aug 2009

PepsiCo to invest USD 200 mn to set-up 4 new greenfield projects and expect them to be operational by

2012. One of the 4 would be for making food products while other 3 would be for making beverages.

Nov 2009

World’s largest food park to come up in Haridwar, Uttarakhand state. It is called Patanjali Food and Herbal

Park and will have 32 processing units for fruits & vegetable products.

Apr 2009

Date Development

Source: Press articles

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

34FOOD PROCESSING INDUSTRY – INDIA.PPT

Thank you for the attention

About Netscribes

Netscribes is a knowledge-consulting and solutions firm with clientele across the globe. The company’s expertise spans areas of investment &

business research, business & corporate intelligence, content-management services, and knowledge-software services. At its core lies a true

value proposition that draws upon a vast knowledge base. Netscribes is a one-stop shop designed to fulfil clients’ profitability and growth

objectives.

The Food Processing - India report is a part of Research on India’s Food and Beverage Industry

series.

For more detailed information or customized research requirements please contact:

Disclaimer: This report is published for general information only. Although high standards have been used the preparation, Research on India,

Netscribes (India) Pvt. Ltd. or “Netscribes” is not responsible for any loss or damage arising from use of this document. This document is the

sole property of Netscribes (India) Pvt. Ltd. and prior permission is required for guidelines on reproduction.

Natasha Mehta, CFAPhone: +65 8448 0449

E-Mail: [email protected]

Gagan Uppal

Phone: +91 98364 71499

E-Mail: [email protected]

Research on India is a product of Netscribes (India) Pvt. Ltd. Research on India is dedicated to disseminating information and providing quick

insights on “hot” industries in India and other emerging markets. Track our new releases and major updates in these industries on

ISIEmergingMarketsPDF in-iimbemis from 115.113.11.239 on 2011-03-31 00:22:01 EDT. DownloadPDF.

Downloaded by in-iimbemis from 115.113.11.239 at 2011-03-31 00:22:01 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

![[PPT]Food Processing Industry - E-R Impreseimprese.regione.emilia-romagna.it/internazionalizzazione/eventi/... · Web viewMarket Assessment of Food and Food Processing Industry](https://img.dokumen.tips/doc/110x75/5ab1da0e7f8b9a6b468d0849/pptfood-processing-industry-e-r-viewmarket-assessment-of-food-and-food-processing.jpg)