Embed Size (px)

Citation preview

Following the ShopperImpact of Recession on the European Grocery Retail Sector

© IGD 2009

Agenda

The economic downturn and its impact on retailers’ economic models

The new shopper landscape

Driving retail value

Following the shopper in the new era

Summary

© IGD 2009

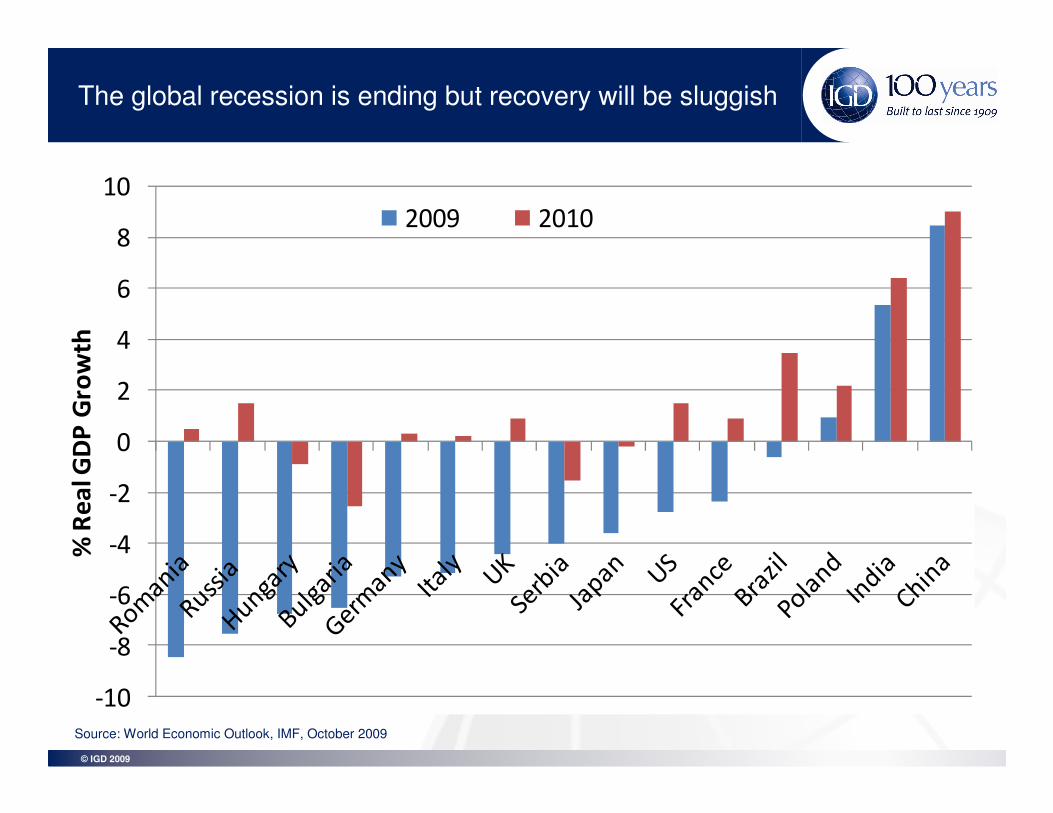

The global recession is ending but recovery will be sluggish

Source: World Economic Outlook, IMF, October 2009

-10

-8

-6

-4

-2

0

2

4

6

8

10

% R

ea

l GD

P G

row

th

2009 2010

© IGD 2009

Shoppers in Europe and the US are feeling the pinch

gas prices fuel bills food prices

savings property value unemployment

Last year…

And this…

© IGD 2009

Overview Key Initiatives for Large Format RetailersA greener supply chain to save cash

The larger retailers (Tesco, Asda, Sainsbury’s, M&S

and Waitrose) are focused on:

Reducing CO2 emissions from the distribution network

and store portfolio

Simplification of replenishment – using Retail Ready

Packaging, consolidation of deliveries

Increasing levels of transport collaboration and efficiency.

Cutting the amount of waste sent to landfill

Reducing the quantity of packaging and carrier bag use

Use of intermodal transport – rail, canal and river barges

The development of more eco-friendly stores

Cutting water consumption

© IGD 2009

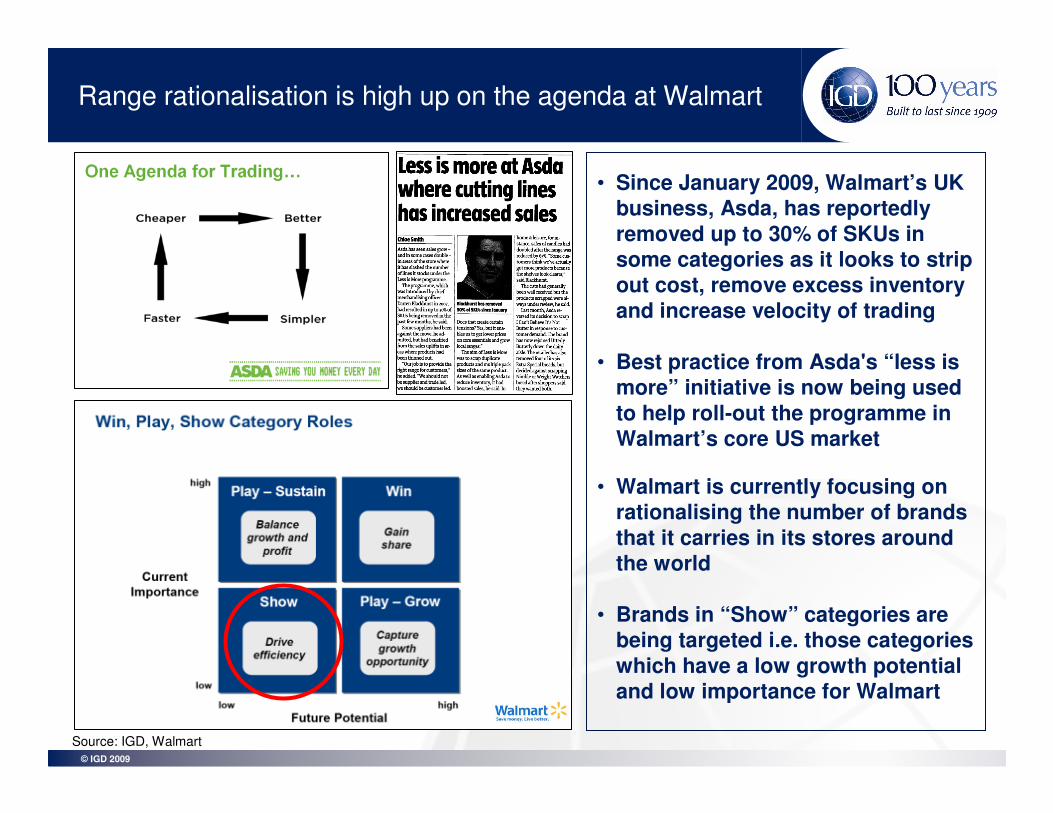

Range rationalisation is high up on the agenda at Walmart

• Since January 2009, Walmart’s UK business, Asda, has reportedly removed up to 30% of SKUs in some categories as it looks to strip out cost, remove excess inventory and increase velocity of trading

• Best practice from Asda's “less is more” initiative is now being used to help roll-out the programme in Walmart’s core US market

• Walmart is currently focusing on rationalising the number of brands that it carries in its stores around the world

• Brands in “Show” categories are being targeted i.e. those categories which have a low growth potential and low importance for Walmart

Source: IGD, Walmart

© IGD 2009

Asda Innovation: Prefilled Display Boxes

1. More space per product

2. Better availability

3. Signposting of lower price points, link-saves and ladder deals.

4. Ease of replenishment for high volume lines

© IGD 2009

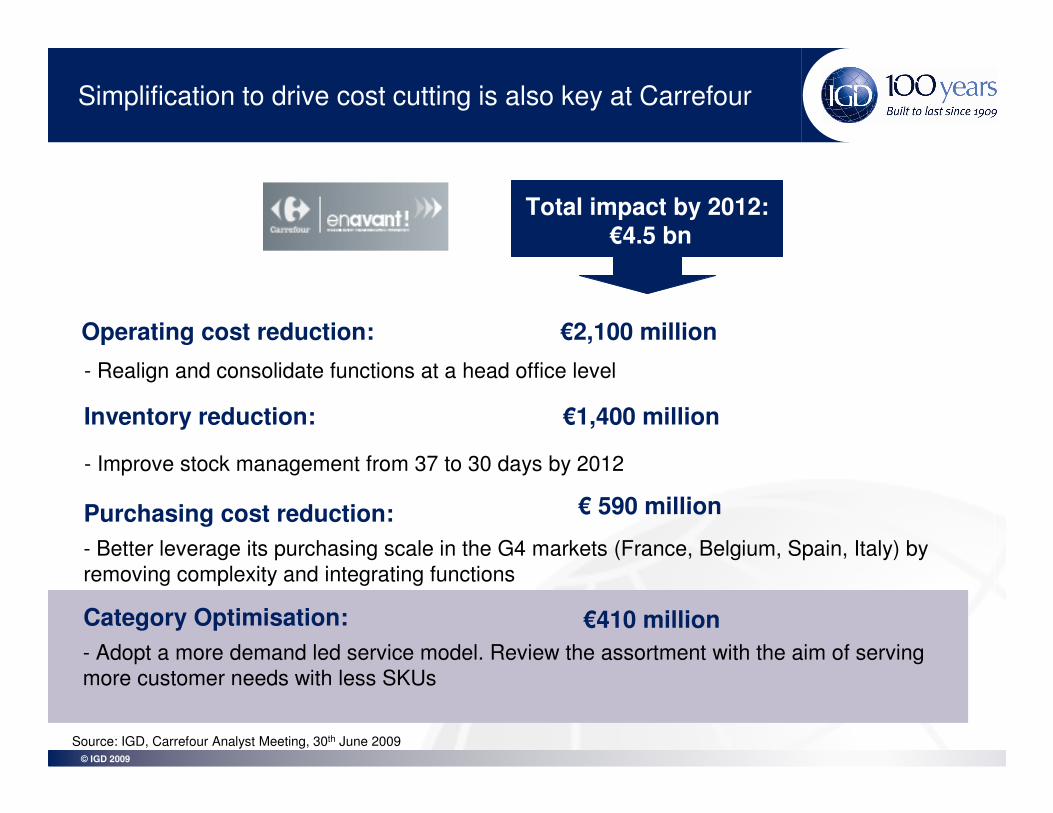

Simplification to drive cost cutting is also key at Carrefour

Category Optimisation:

Inventory reduction: €1,400 million

Operating cost reduction: €2,100 million

€410 million

Purchasing cost reduction:

Total impact by 2012:€4.5 bn

- Improve stock management from 37 to 30 days by 2012

- Realign and consolidate functions at a head office level

- Adopt a more demand led service model. Review the assortment with the aim of serving

more customer needs with less SKUs

- Better leverage its purchasing scale in the G4 markets (France, Belgium, Spain, Italy) by

removing complexity and integrating functions

€ 590 million

Source: IGD, Carrefour Analyst Meeting, 30th June 2009

© IGD 2009

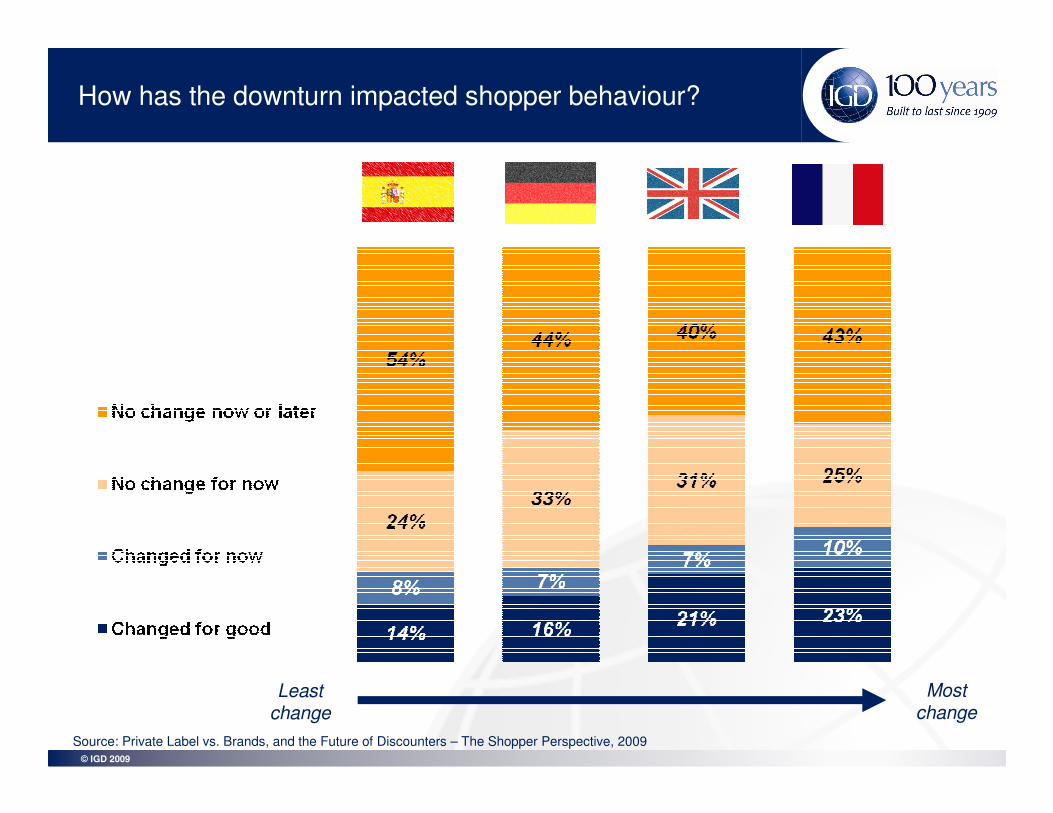

How has the downturn impacted shopper behaviour?

Least

change

Most

change

Source: Private Label vs. Brands, and the Future of Discounters – The Shopper Perspective, 2009

© IGD 2009

New behaviour will persist according to retailers

“A whole new consumer generation will

come out of this … so no-one should

hold their breath waiting for things to

go back to the way they were.”

Andy Bond, CEO of Asda Walmart

© IGD 2009

Saving money…..the sustainable way to live

Sainsbury’s (UK)

John Lewis (UK)

Morrisons (UK)

Whole Foods Market (US)

© IGD 2009

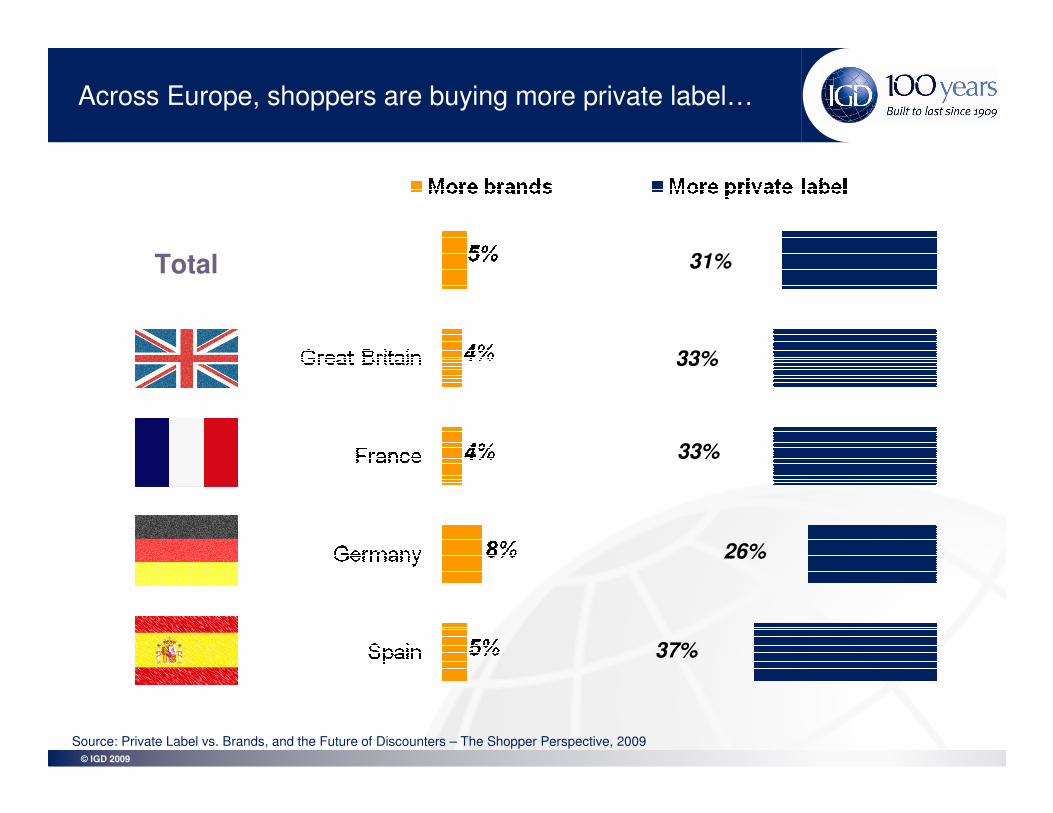

Across Europe, shoppers are buying more private label…

33%

33%

26%

37%

Total 31%

Source: Private Label vs. Brands, and the Future of Discounters – The Shopper Perspective, 2009

© IGD 2009

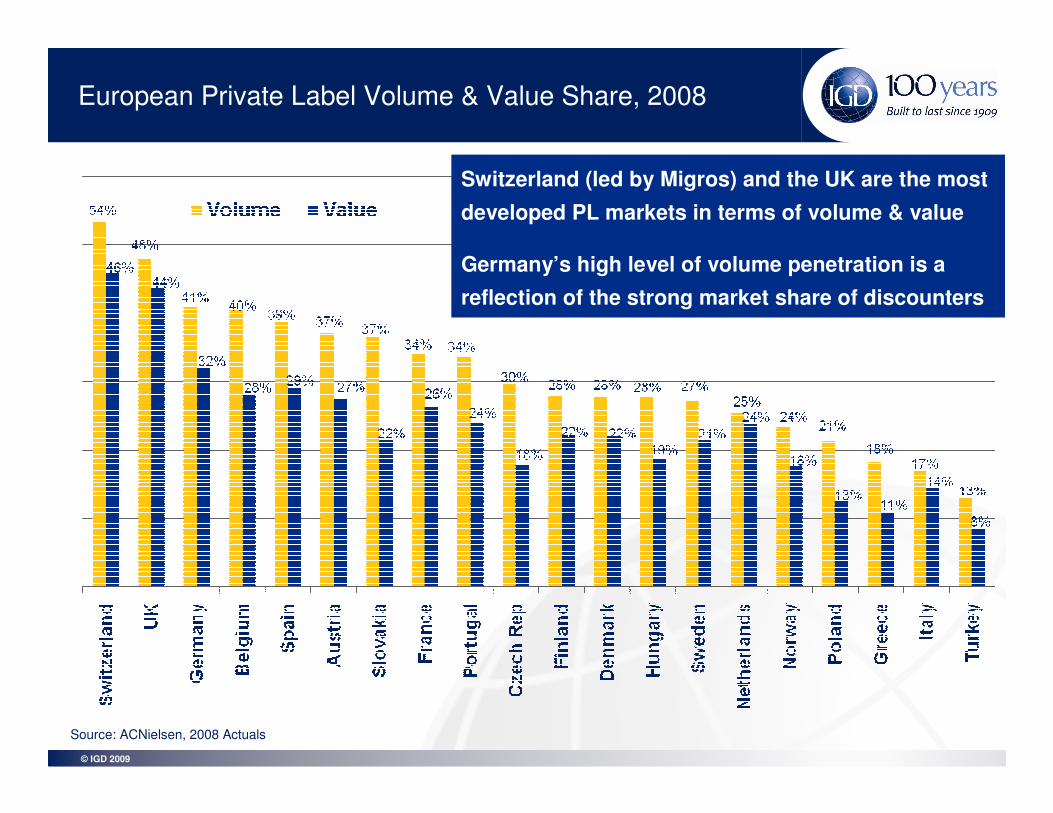

European Private Label Volume & Value Share, 2008

Switzerland (led by Migros) and the UK are the most

developed PL markets in terms of volume & value

Germany’s high level of volume penetration is a

reflection of the strong market share of discounters

Source: ACNielsen, 2008 Actuals

© IGD 2009

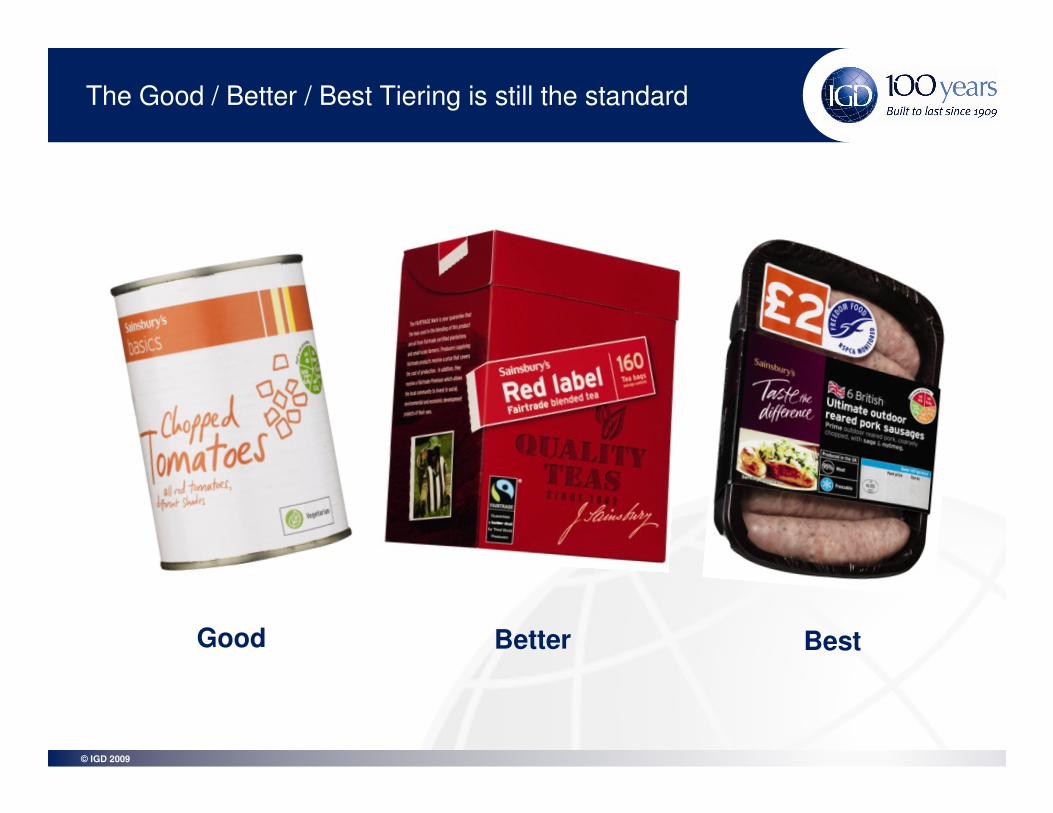

The Good / Better / Best Tiering is still the standard

Good BestBetter

© IGD 2009

Shoppers are looking for value and values

VALUE VALUES

TRUST

PROVENANCE

PACK SIZE

ETHICSSUSTAINABILITY

PERFORMANCE

PROMOTIONS

PRICE

Source: IGD, 2009

© IGD 2009

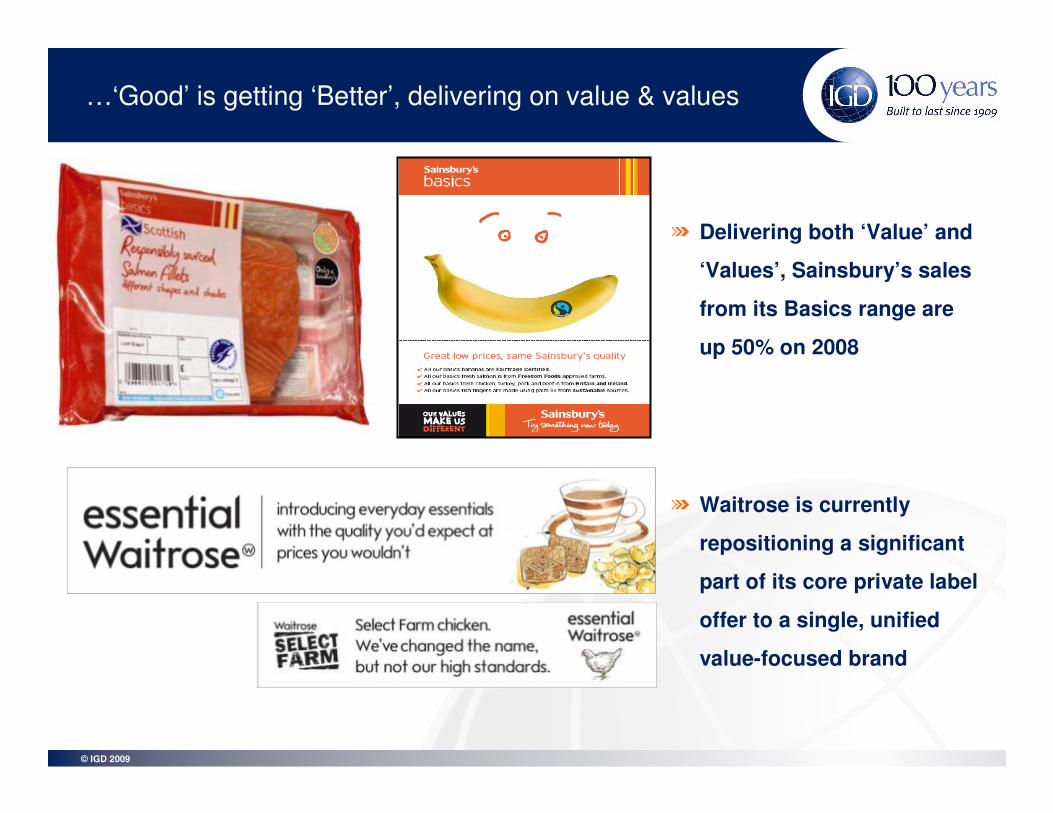

…‘Good’ is getting ‘Better’, delivering on value & values

Delivering both ‘Value’ and

‘Values’, Sainsbury’s sales

from its Basics range are

up 50% on 2008

Waitrose is currently

repositioning a significant

part of its core private label

offer to a single, unified

value-focused brand

© IGD 2009

Tip Value Range at Real, Metro Group

Value ranges have been re-engineered to boost credentialsBetter packaging and reformulation to improve the quality / value equation

In 2008/2009, value ranges

have been at the heart of

retailers’ strategies

The new value ranges have

similar designs:

• crisper photography &

white background

• a high level of product

reformulation

© IGD 2009

Rewe, Germany, Aug 09 Carrefour, France, June 09 Target, USA, June 09

Source: IGD Retail Analysis

In-Store bold displays encourage trial at POS

© IGD 2009

Canada (Loblaws)

USA(Publix)

UK(Sainsbury’s)

Retailers’ “switch and save” campaigns drive PL growth

© IGD 2009

• Premium ranges help strengthen a retailers’ brand and proposition

• Premium and value-added PL also benefit from the ‘eating-in’ trend in recessionary times

Ahold, Stop & Shop, USA Carrefour Premium Range, Belgium

Both ends of the private label spectrum flourishPremium ranges are increasingly instrumental in fresh food categories

© IGD 2009

Private label plays a central role in marketing campaigns

© IGD 2009

Value

Standard

Finest

“Discount”

(Launched September 2008)

The Discount Brands range is c. 20% cheaper

than Tesco standard PL and approximately

twice the cost of Tesco Value

30% of Tesco shoppers are now regularly buying

into the Discount Brands range

Tesco has created a new tier to counteract discounters...

© IGD 2009

Premium Ranges Health & Sustainability

Quality Awards Focus on Fresh

‘Gourmet’, Aldi Germany

‘Luxury For All, Lidl UK

Discounters continue to broaden their appeal

Carbon footprint, Hofer, Austria

Leaderprice, France

Lidl, Germany

© IGD 2009

Aldi UK – TV Advertising

Celebrity Chef Phil Vickery

Lidl Germany – TV advertising

A trio of Celebrity Chefs

Discounters trial new media strategies to build their image

© IGD 2009

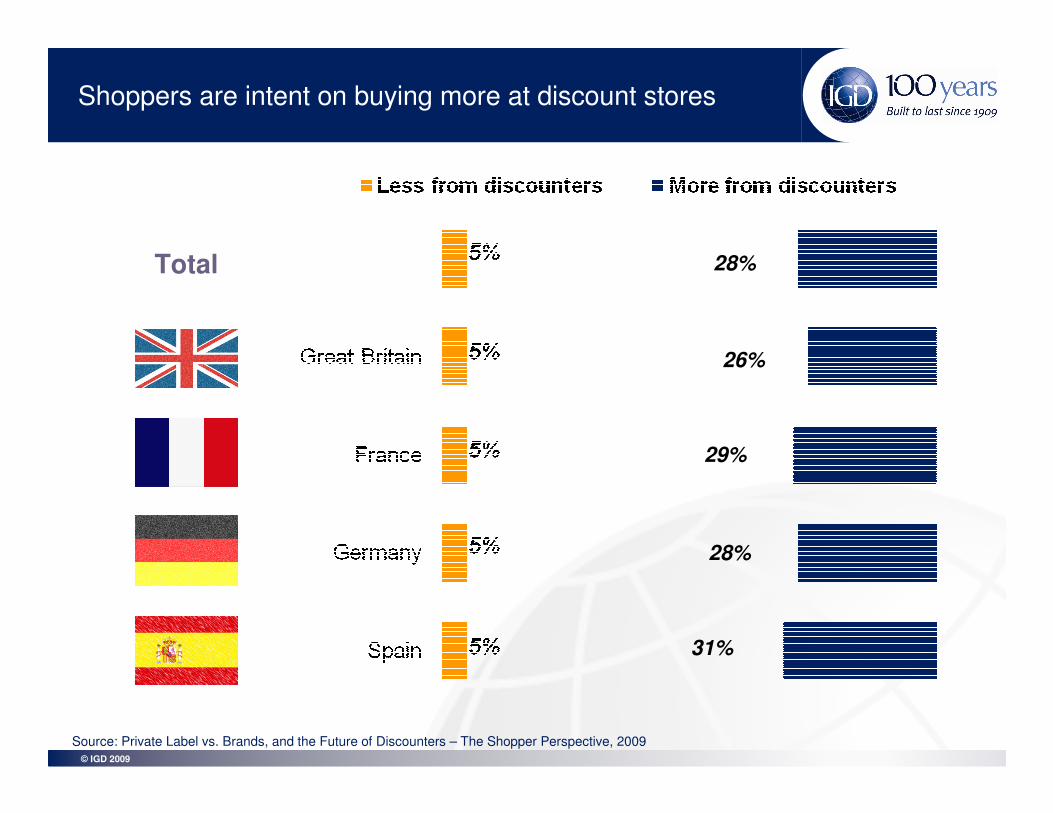

Shoppers are intent on buying more at discount stores

26%

29%

28%

31%

Total 28%

Source: Private Label vs. Brands, and the Future of Discounters – The Shopper Perspective, 2009

© IGD 2009

Is it all because of the downturn?

Buying more Begun to make changes to save money in downturn

Both

Private Label

Discounters

Source: IGD 2009 - % of French, German, British and Spanish shoppers

14%14% 13%

15%16% 12%

© IGD 2009

Following the shopper…

“We make no apology for being on the side of the consumer.”

“Our main focus is to delight our customers every day so we can become their preferred retailer.”

“When our buyers in China are buying products nine

months in advance, we will give them a phone, they will take a picture of the product and email it to customers, and

1,000 customers will vote on whether we buy it”.

Richard Brasher, Tesco

Lars Olofsson, Carrefour

Rick Bendel, Walmart

© IGD 2009

Embracing new technological platforms

© IGD 2009

7 key themes for your business

The downturn has changed behaviours and created opportunities. New behaviours

could become permanent, and new sticky loyalties formed

Value has come to the fore, and price competition will continue through the recovery

Retailers and manufacturers are seeking routes to reduce their cost bases - more

efficient operating models to support a demand-led assortment

Discount retailers continue to grow, and continue to evolve. It has become a mature

channel – manage it as such – though one that continues to provokes response

Private label has been an area of significant investment for many retailers – and there

are no signs of this investment reducing. Shoppers recognise the improvement

Customers are seeking value and values, and are prepared to change for them. A new

language may be needed to talk to shoppers with, tackling the ‘big picture’

Shoppers won’t “revert to type” as conditions improve, so follow the shopper, and

remember ‘perception is reality’

2

3

4

5

6

1

7