Embed Size (px)

Citation preview

First Half Year 2012 Results – Analyst presentation24 August 2012

2

Forward-looking statement

This document contains statements of a forward-looking nature, based on currently available plans

and forecasts. Given the dynamics of the markets and the environments of the 31 countries in which

Vopak renders logistics services, the company cannot guarantee the accuracy and completeness of

forward-looking statements.

Unforeseen circumstances include, but are not limited to, exceptional income and expense items,

unexpected economic, political and foreign exchange developments, and possible changes to IFRS

reporting rules.

Statements of a forward-looking nature issued by the company must always be assessed in the

context of the events, risks and uncertainties of the markets and environments in which Vopak

operates. These factors could lead to actual results being materially different from those expected.

HY1 2012 results 24 August 2012

3

Contents

Achievements

Business environment and strategy update

Business performance

Results per division

Investments and financing

Outlook

HY1 2012 results 24 August 2012

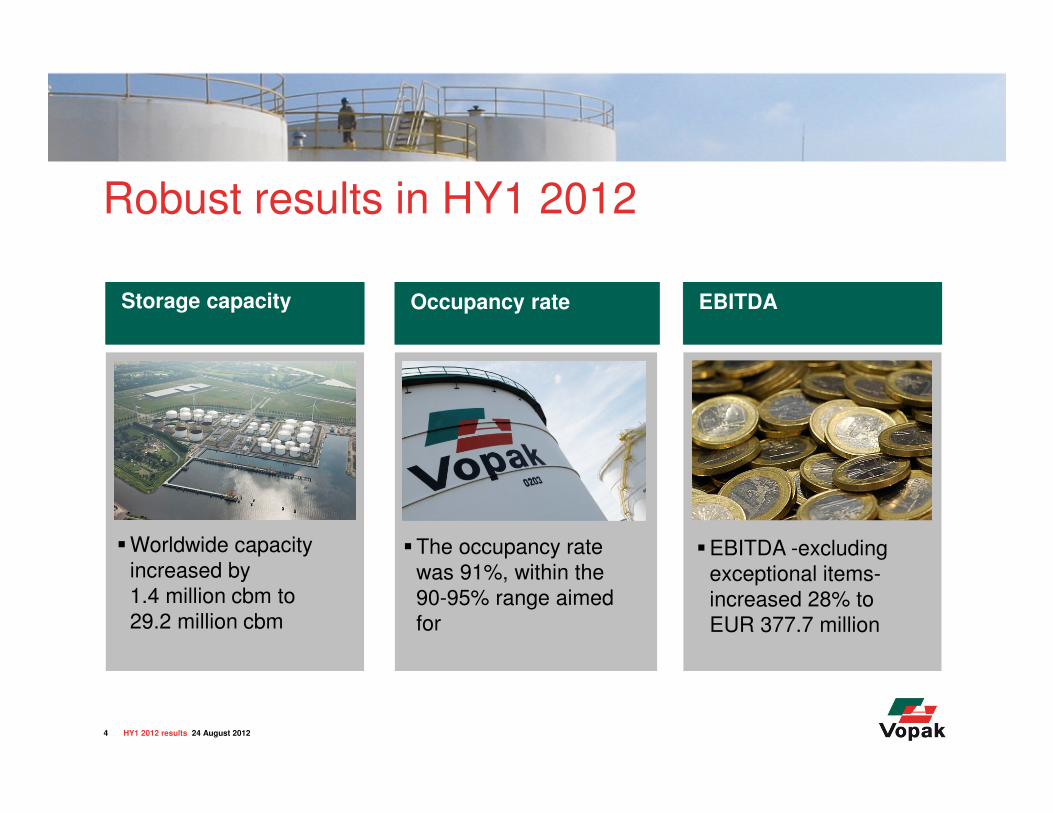

Robust results in HY1 2012

4

EBITDAOccupancy rateStorage capacity

�Worldwide capacity

increased by

1.4 million cbm to

29.2 million cbm

�The occupancy rate

was 91%, within the

90-95% range aimed

for

�EBITDA -excluding

exceptional items-

increased 28% to

EUR 377.7 million

HY1 2012 results 24 August 2012

Personal and process safety

5

-50%

HY1 2012

0.6

HY1 2011

1.2

HY1 2010

1.8

The lost time injury rate (LTIR) Total injuries leading to lost time per million hours worked

by own employees and contractors

-11%

HY1 2012

2.5

HY1 2011

2.8

HY1 2010

3.7

Process Incidents

Number of incidents

Total Injury RateTotal injuries per million hours worked by own employees

-25%

HY1 2012

66

HY1 2011

88

HY1 2010

63

HY1 2012 results 24 August 2012

6

Contents

Achievements

Business environment and strategy update

Business performance

Results per division

Investments and financing

Outlook

HY1 2012 results 24 August 2012

Global product trends drive Vopak’s markets

Oil products Chemical products Biofuels & VegoilsLNG

� Global crude oil

trade business

� Europe’s gasoline

surplus and deficit

for middle distillates

� Closures of some

less competitive

refineries in the

Atlantic Basin

� Increasing demand

in Asia and lower

demand in Europe

� Feedstock

advantage in Middle

East

� Gulf re-emerges due

to shale gas

� Flows between US-

Brazil-Europe-Asia

� Market is expected to

grow

� Impact of annual

harvest and

regulatory

uncertainties

� A globalizing natural

gas market with new

business models

� LNG growth due to

imbalances, security

of supply and

environmental push

7 HY1 2012 results 24 August 2012

Assets Coryton Houston VlaardingenSmall scale LNG

Example of growth project

8

Focused strategy and disciplined execution

Customer LeadershipOperational Excellence

Our Sustainability Foundation

• Excellent People

• Health and Safety

Our ability to construct,

operate and maintain

our terminals to

deliver our service at

competitive costs

Our ability to create

a relationship

with our customers

Our ability to find or

identify the right location

for our terminals

Growth Leadership

• Environment Care

• Responsible Partner

HY1 2012 results 24 August 2012

Global products trends resulting in company growth through healthy demand for storage capacity Capacity developments

In mln cbm

* Including net change at various terminals (including decommissioning).** Including the acquisition of the assets of the former Coryton refinery (UK) by means of a strategic consortium.

+5.3**

+1.4

31-12-2014

34.5

Acquisition

0.5

New terminals

3.8

Expansions

1.0

30-06-2012

29.2

Acquisition

0.1

New terminals

0.1

Expansions*

1.2

31-12-

2011

27.8

HY1 2012 results 24 August 2012 9

10

A’dam Westpoort 2 (100%)

582,000 cbm; oil products

Tianjin Lingang (50%)

95,300 cbm; chemicals

Note: Above examples not representative of all projects completed in HY1 2012.

Zhangjiagang (100%)

55,600 cbm; chemicals

Gothenburg (100%)

60,000 cbm; oil products

Commissioned

Acquired

Fujairah (33.3%)

611,000 cbm; oil products

HY1 2012 results 24 August 2012

Projects commissioned HY1 2012Storage capacity increased by 1.4 million cbm

Commissioned

(Joint Venture)

11

Under construction

Pengerang (44%)

1,278,000 cbm; oil products

Europoort (100%)

400,000 cbm; oil products

Eemshaven (50%)

660,000 cbm; oil products

Hainan (49%)

1,350,000 cbm; oil products

Algeciras (80%)

403,000 cbm; oil products

* Including the acquisition of the assets of the former Coryton refinery (UK) by means of a strategic consortium. Note: Above examples not representative of all projects under construction.

Assets Coryton (33.3%)

500,000 cbm; oil products

HY1 2012 results 24 August 2012

Acquired (Joint Venture)

Various projects under constructionTotal storage capacity under construction 5.3 million cbm*

Under construction

(Joint Venture)

Strengthening competitive position of services to our customers

12 HY1 2012 results 24 August 2012

Sa

fety

Eff

icie

nc

y

Vopak expects to achieve

its 2013 outlook of

EUR 725-800 million

EBITDA in 2012

It is Vopak’s ambition to realize an EBITDA of

EUR 1 billion in 2016The year of 400 years of

entrepreneurship

15

Contents

Achievements

Business environment and strategy update

Business performance

Results per division

Investments and financing

Outlook

HY1 2012 results 24 August 2012

Robust results in HY1 2012

16

HY1 2012

91

HY1 2011

92

2010

93

2009

94

2008

95

2007

96

2006

94

Occupancy rate

In percent

90-95%

28.3

2008

27.1

2007

21.8

2006

21.2

+3.7

HY1 2012

29.2

HY1 2011

25.5

2010

28.8

2009

Storage capacity

In mln cbm

2011

+28%

HY1 2012

377.7

598.2 636.0

297.3513.4

295.3

340.7300.9

2009 20102008

429.3

2007

369.5

2006

314.1

EBITDA Development*

In EUR mln

* Excluding exceptional items; including net result from Joint VenturesHY1 2012 results 24 August 2012

17

Financial performance is fuelled by different value drivers

Occupancy improvements

2003-06 2007-09 2010-2011 2012 >

Operational efficiency gains

Capacity expansion

PresentNear PastPastPresent/

Future

Playing field between 90 - 95%

HY1 2012 results 24 August 2012

18

Q2

90

Q1

93

Q4

94

Q3

93

Q2

93

Q1

92

Q4

92

Q3Q2

93

Q1

93

Q4

9293

Q3

93

Q2

95

Q1

95

Q4

95

Q3

94

Q2

95

Q1

96

’07

96

’06

94

’05

92

’04

84

Occupancy rate

In percent

90-95%

Healthy occupancy rates between 90-95%

2008 2009 2010 2011 2012

HY1 2012 results 24 August 2012

Vopak is well positioned to maintain healthy EBIT(DA) margins

19

EBIT(DA) Margin*

In percent

Focus on logistic efficiency improvements for our clients

has led to increased EBIT(DA) margins

* Excluding exceptional items; excluding net result from Joint Ventures.

EBIT Margin

EBITDA Margin

HY1 2012 results 24 August 2012

0

10

20

30

40

50

2004 2005 2006 2007 2008 2009 2010 2011 2012HY1 2012

20

Development of storage capacity

34.5

21.4

13.1

2013

32.7

20.9

11.8

2012

30.0

20.4

9.6

HY1 2012

29.2

20.4

8.8

2011

27.8

19.7

8.1

2010

28.8

18.3

10.5

2009

+5.3*+1.4

+7.9

2014

28.3

18.1

10.2

2008

27.1

17.5

9.6

2007

21.8

16.7

5.1

2006

21.2

15.8

5.4

2005

20.4

15.5

4.9

2004

20.2

15.1

5.1

2003

19.9

15.1

4.8

Storage capacity

In mln cbm

Subsidiaries

Joint Ventures

* Including the acquisition of the assets of the former Coryton refinery (UK) by means of a strategic consortium.

Note: for the Joint Ventures 100% of the storage capacity is included.HY1 2012 results 24 August 2012

Solid financial performance

21

EBIT*

In EUR million 648.1

+16%

HY1 2012HY1 2011

561.1

Revenues

In EUR million

* Including net result from Joint Ventures.** Attributable to holders of ordinary shares; including net result from Joint Ventures.Note: Excluding exceptional items.

279.9

+28%

HY1 2012HY1 2011

217.9

Earnings per share**

In EUR169.5

+37%

HY1 2012HY1 2011

123.5

Net profit**

In EUR million1.33

+37%

HY1 2012HY1 2011

0.97

HY1 2012 results 24 August 2012

All regions contribute to the 16% revenue increase

22

+19%

HY1 2012

78.4

HY1 2011

65.9

North America

Note: Revenues in EUR millions.

223.6

HY1 2012HY1 2011

185.7

+20%

Netherlands

+16%

174.1

HY1 2012HY1 2011

150.3

Asia

+11%

51.7

HY1 2012HY1 2011

46.5

Latin America

+7%

HY1 2012HY1 2011

110.6 117.8

EMEA

HY1 2012 results 24 August 2012

648.1

+16%

HY1 2011 HY1 2012

561.1

Revenues

EBIT excluding exceptional items increased by 28% to EUR 279.9 million

23

EBIT excl. exceptional items 217.9

Exceptional gain (loss) 117.5

EBIT incl. exceptional items 335.4

Net result Joint Ventures 167.2

Operating profit 168.2

279.9

0.0

279.9

56.6

223.3

HY1 2011

In EUR mln

HY1 2012

In EUR mln

Delta

In percent

33%

-66%

-17%

28%

Net profit excl. exceptional items* 123.5 169.5 37%

HY1 2012 results 24 August 2012

* Attributable to holders of ordinary shares.

Except from Latin America, all regions contribute to the 28% EBIT increase

24

HY1 2012

19.8

HY1 2011

16.9

+17%

North America

+38%

HY1 2012

94.2

HY1 2011

68.2

Netherlands

+15%

HY1 2012

107.2

HY1 2011

93.6

Asia

-7%

HY1 2012

12.7

HY1 2011

13.7

Latin America

+14%

HY1 2012

52.3

HY1 2011

45.7

EMEA

HY1 2012 results 24 August 2012

+28%

HY1 2012

279.9

HY1 2011

217.9

EBIT

Global LNG

HY1 2012

10.7

HY1 2011

-3.6

Note: EBIT in EUR million; excluding exceptional items; including net result from Joint Ventures

Net result of Joint Ventures increases with 34%, mainly due to Global LNG

25

0.0

HY1 2012

-100%*

1.2

HY1 2011

North America

0.6

HY1 2012

+20%

0.5

HY1 2011

Netherlands

+3%

HY1 2012

15.815.3

HY1 2011

Asia

+67%

HY1 2012

0.3

HY1 2011

0.5

Latin America

HY1 2012

26.4

HY1 2011

25.9

+2%

EMEA

HY1 2012 results 24 August 2012

56.6

+34%

HY1 2012HY1 2011

42.2

Net result of JVs

Global LNG

HY1 2012

13.4

HY1 2011

-1.0

* Due to the sale of Vopak’s 20% equity stake in BORCO (Bahamas).Note: Net result Joint Ventures in EUR million; Excluding exceptional items.

26

Revenues

HY1 2012

648.1

+16%

HY1 2011

561.1

Revenues Subsidiaries

HY1 2012

830.1

+21%685.9

HY1 2011

EBITDAEBITDASubsidiaries and net result from Joint Ventures

* Vopak consolidated including proportional consolidation of joint ventures in tank storage activities.Note: In million EUR; Excluding exceptional items.

HY1 2012

377.7

+28%295.3

HY1 2011

438.2

+34%

HY1 2012

327.7

HY1 2011

HY1 2012 results 24 August 2012

IFRS equity accounting Proportionate consolidation*

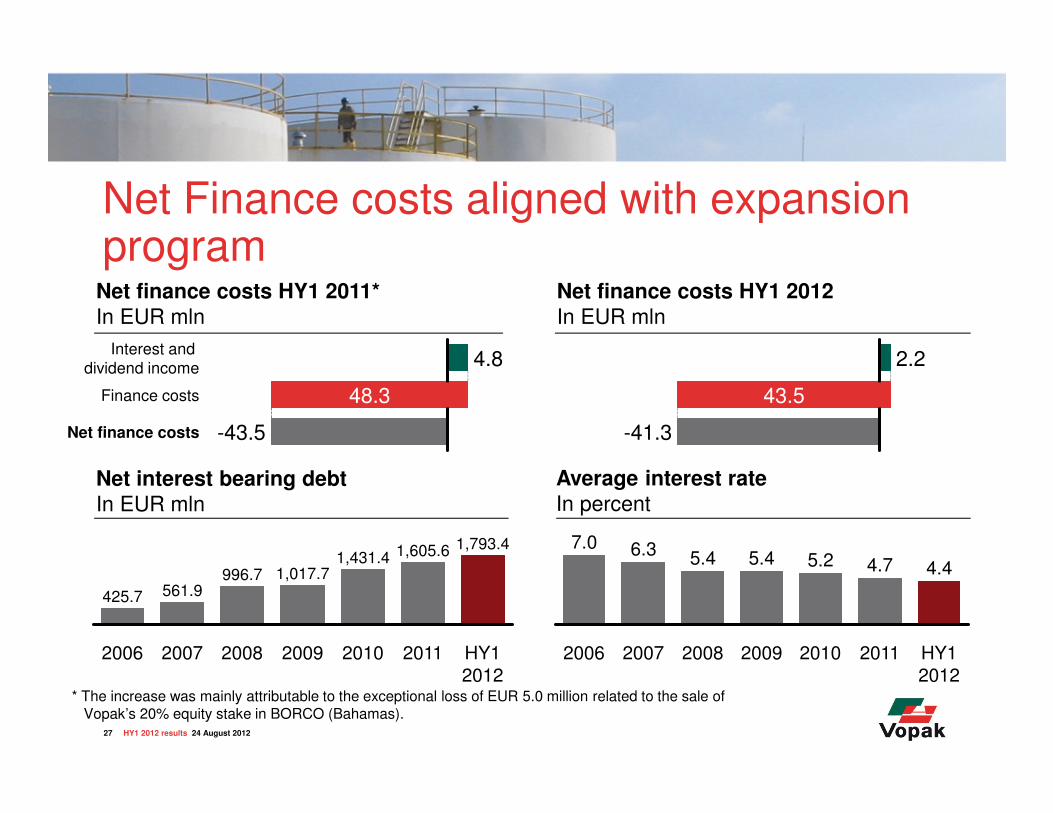

Net Finance costs aligned with expansion program

27

-43.5Net finance costs

4.8

48.3Finance costs

Interest and

dividend income

Net finance costs HY1 2011*

In EUR mln

43.5

-41.3

2.2

4.4

HY1 2012

2011

4.7

2010

5.2

2009

5.4

2008

5.4

2007

6.3

2006

7.0

Average interest rate

In percent

1,431.4

2010

1,605.6

20112009

1,017.7

2008

996.7

2007

561.9

2006

425.7

HY1 2012

1,793.4

Net interest bearing debt

In EUR mln

Net finance costs HY1 2012

In EUR mln

* The increase was mainly attributable to the exceptional loss of EUR 5.0 million related to the sale of Vopak’s 20% equity stake in BORCO (Bahamas).

HY1 2012 results 24 August 2012

Effective tax rate HY1 2012

28

Effective Tax Rate

In percent

+49%30.3

45.2

HY1 2012HY1 2011

TaxIn EUR mln

0.018.9 18.9

HY1 2012HY1 2011

8.9

10.0

� In 2011, EUR 108.5 million of book

gain on the sale of our 20% equity

stake in BORCO (Bahamas) was

exempted for tax purposes

� Excluding exceptional items, the

effective tax rate for HY1 2011

amounted to 18.9%

HY1 2012 results 24 August 2012

Sources and uses of cash in HY1 2012

29

Net Cash position

30/06/2012*

-9.7

FX

1.3

Other

financing

activities

210.9

Dividend

paid in

cash**

110.1

Derivatives

settlement

9.9

Disposals

19.2

Invest-

ments

296.6

Tax paid

20.9

Net finance

costs paid

34.7

Gross

operating

cash flow

298.1

Net Cash position 1/1/2012*

-67.0

Consolidated Statement of Cash Flows

In EUR mln

* Including bank overdrafts.** Including dividend paid in cash on financing preference shares.

HY1 2012 results 24 August 2012

FX translation-effect on EBIT

30 HY1 2012 results 24 August 2012

Total 2.3

Non allocated 0.0

Latin America 0.2

North America 1.6

Asia 2.2

EMEA (1.7)

2009In EUR mln

25.9

(0.8)

3.2

2.6

17.4

3.5

2010In EUR mln

2.6

0.1

(0.7)

(1.6)

5.4

(0.6)

2011In EUR mln

10.0

(0.3)

0.1

1.1

8.2

0.9

HY1 2012In EUR mln

Consequences IAS 19 Employee BenefitsEffect on comparative figures 2012 as a result of application amendment in 2013

31

Total effect on Equity attributableto owners of parent at 30 June 2012 -167.0

Net result recognized through

statement of income in HY1 20121.5

Total recognized directly in equitythrough Other comprehensive income -168.5

Income tax 31.7

Actuarial gains and losses

in HY1 2012123.9

Income tax 31.1

Actuarial gains and losses

at 1 January 2012107.4

Total effect on equityIn EUR mln

HY1 2012 results 24 August 2012

� Removal 10% corridor approach

(higher volatility in net pension

liability)

� Weighted average discount rate

reduced from 4.68% to 4.26%*

� Only service and net finance

cost in P&L (rest of changes in

other comprehensive income)

� Change of discount rate for the

expected returns on plan assets

(generally lower rate than used

under current IAS 19)* From 31 December 2011 to 30 June 2012.

32

Contents

Achievements

Business environment and strategy update

Business performance

Results per division

Investments and financing

Outlook

HY1 2012 results 24 August 2012

33

Q2 2012

48.3

Q1 2012

45.9

Q4 2011

46.2

Q3 2011

41.9

Q2 2011

34.7

Q1 2011

33.5

EBIT*

In EUR million

* Including net result from Joint Ventures; excluding exceptional items.

Storage capacityIn mln cbm

Occupancy rateIn percent

Netherlands- New oil storage capacity came on stream in Amsterdam Westpoort- Lower occupancy rates in crude and gasoil storage

HY1 2012 results 24 August 2012

HY1 2012HY1 2011

185.7 +20%223.6

9093-3pp

HY1 2012HY1 2011 HY1 2012HY1 2011

7.2 +22%8.8

RevenuesIn EUR million

+38%

34

28.2

Q2 2012Q1 2012

24.1

Q4 2011

23.3

Q3 2011

23.9

Q2 2011

23.3

Q1 2011

22.4

* Including net result from Joint Ventures; excluding exceptional items.

EMEA- New oil storage capacity came on stream in Fujairah- Lower occupancy rates at chemical terminals in Belgium

HY1 2012 results 24 August 2012

Storage capacityIn mln cbm

Occupancy rateIn percent

HY1 2012HY1 2011

110.6 117.8+7% 8890

-2pp

HY1 2012HY1 2011

9.0+10%

HY1 2012HY1 2011

8.2

EBIT*

In EUR million

RevenuesIn EUR million

+14%

35

Q2 2012Q1 2012

53.6

Q4 2011

46.7

Q3 2011

45.0 53.6

Q2 2011

46.2

Q1 2011

47.4

* Including net result from Joint Ventures; excluding exceptional items.

Asia- Continuous growth in Asia- Currency translation gain of EUR 8.2 million on EBIT

HY1 2012 results 24 August 2012

Storage capacityIn mln cbm

Occupancy rateIn percent

+16%150.3174.1

HY1 2012HY1 2011

95950pp

HY1 2012HY1 2011

+7%6.8

HY1 2012

7.3

HY1 2011

EBIT*

In EUR million

RevenuesIn EUR million

+15%

36

9.2

Q2 2012Q1 2012

10.6

Q4 2011

8.9

Q3 2011

8.0

Q2 2011

7.1

Q1 2011

9.8

North America- Higher occupancy rates - Improvements in markets for biofuels and chemicals

HY1 2012 results 24 August 2012

Storage capacityIn mln cbm

Occupancy rateIn percent

+19%

HY1 2012HY1 2011

65.978.4

9691+5pp

HY1 2012HY1 2011

0%2.3

HY1 2012HY1 2011

2.3

* Including net result from Joint Ventures; excluding exceptional items.

EBIT*

In EUR million

RevenuesIn EUR million

+17%

37

Q2 2012

5.3

Q1 2012

7.4

Q4 2011

7.5

Q3 2011

7.0

Q2 2011

6.4

Q1 2011

7.3

* Including net result from Joint Ventures; excluding exceptional items.

Latin America- New chemical storage capacity came on stream in Mexico- Lower occupancy rates in Brazil

HY1 2012 results 24 August 2012

Storage capacityIn mln cbm

Occupancy rateIn percent

51.7+11%

HY1 2012HY1 2011

46.5 8892-4pp

HY1 2012HY1 2011

1.00%

HY1 2012HY1 2011

1.0

EBIT*

In EUR million

RevenuesIn EUR million

-7%

38

Contents

Achievements

Business environment and strategy update

Business performance

Results per division

Investments and financing

Outlook

HY1 2012 results 24 August 2012

Capital disciplined growth: Total investments

39

~775-900

2,108

HY2 2012-

2014

~400

2009-

HY1 2012

1,514

2006-2008

Total Investments 2006-2014

In million EUR

Sustaining Capex**

* Yearly sustaining Capex is EUR 150-200 million. ** Including remaining equity share in Joint Ventures; excluding our part of Capex related to the upgrading of

the assets of the former Coryton refinery (UK).Note: Total Capex related to 4.8 mln cbm under construction is ~EUR 1.5 bln.

Expansion Capex*

~375-500297

711

565535

800

446

268

HY1

2012

201120102009200820072006

Total investments 2006-HY1 2012

In million EUR

HY1 2012 results 24 August 2012

Capital disciplined growth: Strategic finance

40

0

1

2

3

4

5

2011

2.65

2010

3.75

2.63

2009

2.23

2008

2.54

2007

1.71

2006

1.61

2005

1.76

2004

2.20

2003*

2.42

HY1 2012

2.70

Net senior debt : EBITDA ratio

* Based on Dutch GAAP.Note: Private placements and syndicated revolving credit facility per year-end 2011.

Maximum Ratio under current US PP program

Maximum Ratio under other PP programs and

syndicated revolving credit facility

Access to Capital Markets

�Syndicated Revol-

ving Credit Facility (EUR 1.2 billion)

�SGD and JPY

Private Placements(SGD 435 million and JPY 20 billion)

�US Private

Placements (EUR 856.7 million)

HY1 2012 results 24 August 2012

41

Contents

Achievements

Business environment and strategy update

Business performance

Results per division

Investments and financing

Outlook

HY1 2012 results 24 August 2012

Outlook assumptions

Note: width of the boxes do not represent actual percentages.42

~x% Share of EBIT

Solid

Oil products Chemicals Biofuels & Vegoils LNG

Robust

~60%

Steady Solid

<1%

Mixed

~17.5-20%

Industrial terminals

~12.5% ~7.5-10%

2011

~60-65% ~2.5-5%~17.5-20% ~7.5-10% ~5-7.5%

2013

HY1 2012 results 24 August 2012

Vopak expects to achieve its 2013 outlook of EUR 725-800 million EBITDA in 2012

43

377.7

2012

725-800

2011

636.0

2010

598.2

2009

513.4

2008

429.3

2007

369.5

2006

314.1

2005

262.5

2004

231.8

2013

725-800

EBITDA Development and outlookIn EUR million

Note: Excluding exceptional items; including net result from Joint Ventures

Historical results

Outlook

HY1 2012 results 24 August 2012

It is Vopak’s ambition to realize an EBITDA of

EUR 1 billion in 2016The year of 400 years of

entrepreneurship

Royal Vopak

Westerlaan 10 Tel: +31 10 4002911

3016 CK Rotterdam Fax: +31 10 4139829

The Netherlands www.vopak.com