Embed Size (px)

Citation preview

Financial & Grants Management Basics: 101

Session Objectives

Learn basic financial and grants management

Review reimbursing, reporting, and

rebudgeting issues

Learn about common audit pitfalls & issues

1. Regulations & Requirements

2. Financial Management Principles

3. Policies and Procedures

5. Administrative Costs

6. Documenting Expenses

7. Cash & In-Kind Match

8. Reimbursing, Reporting, and Rebudgeting

9. Audits and Site Visits

10. Grant Closeout

Grants & Financial

Management Basics: 101

4. Internal Controls

Sessio

n Obje

ctive

s

Regulations & Requirements

5

Nat’l & Community Svc. Act of 1990

Code of Fed. Regulations (CFR)

OMB Circulars (part of CFR)

State & Local Regulations

Notice Of Funding Opportunity

Notice of Grant Award

Proposal & Budget

ProvisionsCertifications and Assurances

Changes to the OMB Circulars

• The OMB Circulars were first published in 1952

• In 2005, grants management circulars were incorporated into the Code of Federal Regulations (CFR)

• The content and information is the same; however, the guidelines were streamlined and changed for consistency

Grant Guidelines

Federal Grant Guidelines

UniversitiesStates, Local, Indian Tribal Governments

Non-Profits Hospitals

Administrative Requirements

§ 45 CFR 2543§ 2 CFR 215

(formerly A-110)

§ 45 CFR 2541 OMB A-102

§ 45 CFR 2543§ 2 CFR 215 (formerly A-110)

§ 45 CFR 2543§ 2 CFR 215

(formerly A-110)

Cost Principles § 2 CFR 220 (formerly A-21)

§ 2 CFR 225 (formerly A-87)

§ 2 CFR 230 (formerly A-122)

§ 45 CFR 74 (HHS regulations)

Audit Requirements OMB A-133 OMB A-133 OMB A-133 OMB A-133

Notes:CFR = Code of Federal Regulations = Organization is subject to A-133 if it expends more than $500,000 of Federal funds in its fiscal year

Locate Grants Management Circulars: www.whitehouse.gov/omb/grants_circulars/

Effective May 11, 2004 and August 31, 2005

When do I use OMB Circulars?

The Circulars provides guidance and requirements relevant to the Federal grants in these areas:

• Cost Principles

• Administrative Requirements

• A-133 Audits

Cost Principles Requirements

• Provide guidance to determine the allowable costs incurred by organizations under Federal grants

• Designed so that Federal awards bear their fair share of costs

• Provide guidance about reimbursement requirements• Provide uniform standards of allowability and

allocation• Encourage consistency of treatment of costs• 54 selected items of cost

Cost Principles

Examples of Costs in CFRs:• Advertising and public relations costs • Compensation for personal services• Memberships, subscriptions, and professional

activity costs• Recruiting costs• Rental costs• Training and education costs• Travel costs

Administrative Requirements

• Provide consistency and uniformity among Federal agencies in the management of grants and cooperative agreements

• Required all Federal agencies to issue a grants management common rule to adopt government-wide terms and conditions

Specific grantmaking requirements for CNCS

are in the CFRs

Administrative Requirements

Examples of items in CFRs:• Pre-award policies• Special award conditions• Purpose of financial and program management• Standards for financial management systems• Cost sharing or matching• Program income

A-133 Audit Requirements

• Provide the standards for obtaining consistency and uniformity among Federal agencies for the audit of organizations expending Federal funds

• Apply to all organizations that expend $500,000 or more of Federal funds in a year

CNCS Grant Provisions

• Are issued by CNCS with the Notice of Grant Award• Are the guiding principles for CNCS-funded grants and

cooperative agreements• Contain program and financial guidelines• Are binding on the grantee and subgrantee in the same

manner• The order of precedence if inconsistencies exists is:

1. Notice of Grant Award

2. AmeriCorps Special Provisions

3. General Provisions

4. Approved Grant Application

CNCS Grant Provision Requirements

Examples of items in the Provisions:• Member Recruitment, Selection, and Exit• Living Allowances, Other In-Service Benefits, and Taxes• Member Records and Confidentiality• Budget and Programmatic Changes• Reporting Requirements• Responsibilities under Grant Administration• Financial Management Standards• Program Income• Safety

Financial Management Principles

Efficient Accounting System

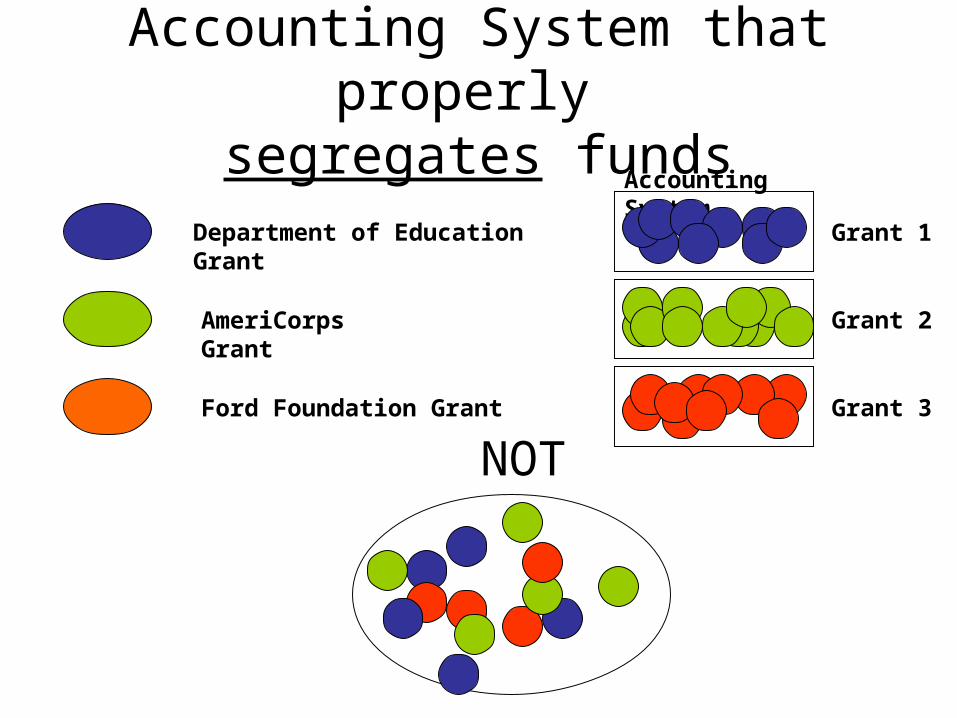

Efficient Accounting System

Accounting System must be capable of:• Distinguishing between grant verses non-grant

related expenditures

• Identifying costs by program year

• Identifying costs by budget category

• Differentiating between direct and indirect costs (administrative costs)

• Accounting for each award/grant separately

Accounting System that properly segregates funds

Department of Education Grant

AmeriCorps Grant

Ford Foundation Grant

Accounting System

Grant 1

Grant 2

Grant 3

NOT

Efficient Accounting System

Accounting System must be capable of:• Distinguishing Federal funds separately from grant

funds• Recording in-kind contribution as both revenues and

expenses• Easily provide management with financial reports at

both the summary or detailed levels• Comparing outlays with budget amounts for each

award (budget vs. actual reports)• Correlating financial reports submitted to CNCS

directly to accounting information and supporting documents

Allowable, Reasonable, Allocable, and Consistent Costs

To be allowable under a grant, costs must: Be reasonable and allocable for the performance of the

award

Conform to grant award limitations or cost principles

Be consistent with policies and procedures that apply to both federally-financed and other activities of the organization

Be given consistent treatment

Be in accordance with Generally Accepted Accounting Principles (GAAP)

Not be included as a cost or used to meet cost sharing or matching requirements of any other federally-financed program

Be adequately documented

Allowable - What does it Mean?

Example – Allowable?

• The Program Director of BEST AmeriCorps program decided to host a very important meeting at his home and serve beer and pizza hoping that everyone would attend.

• The purpose of the meeting was to discuss changes in the new CNCS Grant Provisions that affected the program.

• Because it was a business meeting he decided to charge the cost of the beer and pizza to the AmeriCorps grant, especially since he was providing the use of his home.

Allowable?

A cost is reasonable if:• It does not exceed what a prudent person would do under

the circumstances at the time the decision was made to incur the cost

• Consideration should be given to:

– Whether the cost is ordinary and necessary for the operations of the organization

– The restraints or requirements imposed by generally accepted sound business practices

– Whether the individuals concerned acted with prudence

– Significant deviations from established practices which may unjustifiably increase the award costs

Reasonable - What Does it Mean?

Example – Reasonable?• BEST AmeriCorps program needs 5 laptop computers for the

program so that members can learn basic computer skills. • When deciding on the model that would best suit its needs, the

Program Director received three price quotes on various models and two were within the same general price range of $650 - $700. However, one laptop appealed to him most – it met all of the necessary specifications plus being the “techie” he was it had many other “nice to have” features, such as built in webcam and mobile broadband, a 21” Hi-Def widescreen, and 8 built-in speakers and a subwoofer.

• Although the basic models were adequate, the more appealing one was $2,999, on sale, and came in crimson red, the BEST AmeriCorps program’s team color, so the Program Director ordered 5 of these laptop computers.

Reasonable?

A cost is allocable:• Based on its relative benefits received• If it is treated consistently with other costs incurred for the

same purpose in like circumstances and if it:– It is incurred specifically for the award

– Benefits both the award and other work and can be distributed in reasonable proportion to the benefits received or

– Is necessary to the overall operation of the organization

Any cost allocable to a particular award may not be shifted to other Federal awards

to overcome funding deficiencies, or to avoid restrictions imposed by law or by the

terms of the award

Allocable - What Does it Mean?

Example – Allocable?

• When the crimson red laptops finally arrived, the Program Director found that funds allocated for supplies for the BEST AmeriCorps program were fully expended.

• Although the laptops were to be used only for the AmeriCorps program, BEST had another CNCS funded program through a Learn & Serve America program, so the Program Director told the accountant to charge the cost to the Learn & Serve America program since CNCS was also funding that program.

Allocable?

Grantees must be consistent in assigning costs:

• Whether a direct cost or an indirect cost

• Regardless of the source of funding, i.e., federally or non-federally sponsored activities, and

• Following written cost allocation plan, as applicable

Key wording in the cost principles:

• Consistent with that paid for similar work in the organization’s other activities

• Distributed to awards and other activities in a consistent pattern

• The organization must follow a consistent, equitable procedure

• Charges must be consistent with those normally allowed in like circumstances in the organization’s non-Federally-sponsored activities

Consistent - What Does it Mean?

Example – Consistently Applied?

• The BEST AmeriCorps program was running low on office supplies and postage stamps.

• Since the Program Director couldn’t wait any longer for the office manager to provide the supplies, he purchased them and charged them to the AmeriCorps grant.

Consistently Applied?

Policies & Procedures

Policies & Procedures

• Policies and procedures are a set of written documents that describe an organization's policies for operation – “what is to be done” the procedures necessary to fulfill the policies – “how it is to be

completed”

• All staff must be familiar with these documents• Documents must be kept up-to-date• Documents should explain the rationale and include

principal transactions and completed forms• Documents must incorporate Federal and CNCS grant

regulations and provisions

Policies & Procedures

• Required by Federal grant regulations

• Non-profit organizations have additional requirements – Form 990 submitted to IRS

• Other Key Policies & Procedures to document

• AmeriCorps Programs

CD provided in 2008

See Grantee Central

See Handout

Helpful guide and handbook for developing Policies and Procedures

Internal Controls

Are You an Internal Control User?

When you leave home in the morning to go to work,

do you lock the doors to your house? _____________

If you do, that's your own "internal control" to safeguard the assets you own in your home

Congratulations, you are an internal control user!!

Why Have Internal Controls?

• Improve accountability to customers – CNCS, trustees, funders, public

• Help organization achieve performance & budget targets

• Improve reliability of financial reporting

• Improve compliance with laws & regulations

• Prevent loss of resources & public assets

• Prevent loss of public trust

• Reduce legal liability

Who is Responsible?

Everyone within the organization has some role in internal controls

Roles vary depending upon level of responsibility: • Executives establish the presence of integrity, ethics,

competence and a positive control environment

• Directors and department heads have oversight responsibility for internal controls within their units

• Managers and supervisory personnel are responsible for executing control policies and procedures at the detail level within their specific unit

• Each individual within a unit is to be cognizant of proper internal control procedures associated with their specific job responsibilities

Elements of Internal Controls

Internal control systems operate at different levels of effectiveness

Determining effectiveness is based on an assessment of whether these 5 components are present and functioning:

1. Control Environment – sets the tone of an organization

2. Risk Assessment – identifying & analyzing internal and external risk

3. Control Activities – management’s directives carried out through policies and procedures

4. Information and Communication – providing timely information to the right people down, across, and up

5. Monitoring – assessing the quality of the system’s performance over time

Administrative Costs

DefinitionsSpecific expenses related to theoperations of a specific projectDirect Costs

Indirect/Administrative

Costs

General expenses related to overall administration of anorganization receiving CNCS funds

Expenses incurred for common or joint objectives and cannot be readily identifiable with a specific project or cost objective

What are Direct Costs?

• Allowable direct expenses for members, e.g., living allowances and insurance costs

• Costs for staff who train, place, or supervise• Member’s benefit programs• Evaluations of programs• Supplies and Facility costs • Travel

What are Administrative Costs?

• Accounting, auditing, contracting, budgeting, and general legal services

• Facility occupancy costs, e.g., rent, utilities, insurance, taxes, and maintenance

• General liability insurance that protects the organization (not directly related to a program)

• Director’s and Officer’s liability insurance• Depreciation on building & equipment• Office Supplies• General & Administrative salaries & wages

What cannot be included as Administrative Costs?

≠ Bad debts ≠ Entertainment costs ≠ Fines and penalties ≠ Fundraising ≠ Interest on borrowed capital ≠ Lobbying ≠ Relocation Costs≠ Taxes

CNCS 5% Administrative Rate

Administrative costs are limited by statute: Costs cannot exceed 5% of total Corporation share Grantees may charge up to 5% of the total CNCS

funds expended, provided that the grantee’s administrative match does not exceed 10% of all direct costs

CaliforniaVolunteers Guidelines: 4% = Subgrantee 1% = CaliforniaVolunteers

Use the CNCS “fixed 5%”Option 1

Federally Approved Indirect Cost Rate

Option 2Use the Federally approved Indirect Cost Rate

Obtaining a Federally ApprovedIndirect Cost Rate

1. Can my organization have an indirect cost rate? • Yes. If your organization is a direct recipient of

Federal grant funds

• No. If your organization receives only pass-through Federal grant funds, then your organization is limited to using the 5% and 10% fixed rates stipulated for CNCS grants

Documenting Administrative Costs

1. Using the CNCS 5% Rate (45 CFR 2540.110)

• Not subject to supporting cost documentation• “Not Auditable”? If direct costs charged to CNCS are

questioned, and deemed unallowable:– Payback funds for disallowed direct costs– Payback funds for administrative costs claimed based on the

disallowed direct costs

• Unreimbursed indirect costs may be applied to meeting operational matching requirements

2. Using a Federally Approved Indirect Cost Rate• Must maintain related supporting

documentation for audit• Charges are based on documented expenses

Documenting Expenses

AllowableAllocable

ReasonableConsistently Applied

Document, Document, Document

Why Retain Documentation?

• To track incoming information

• To review information

• To provide historical evidence

• To provide evidence of accomplishments

• To assist during the audit or site visit

Documentation Basics

Establish a written record retention policy

See Handout

Defining Source Documentation • Physical information:

– Hard copy– Soft copy: CD, flash drive, server, microfilm

• Source: – Internal to the organization– External sources

• Benefits supports a value, cost, or performance criteria relative to the grant

CaliforniaVolunteers may request this during site visits or desk reviews

• Signed timesheets with supervisory approval

• Quarterly payroll returns (941)

• Payroll register

• Personnel file with salary/wage information

• Employment contract

• Cancelled checks

• Direct deposit schedule

Salary

Key Documentation Issue

See Handout

Reimbursements, Reporting & Rebudgeting

Reimbursement is made based on actual expenses

Reimbursements may not be for estimated, unauthorized, or unallowable expenses

Invoices must be for approved and budgeted expenditures that programs have already incurred

No advances allowed

Reimbursements

Subgrantees/Programs must submit:

• 3 Copies = CaliforniaVolunteers Invoice Form

(CV 100)

• 3 Copies = Periodic Expense Report (PER)

Reimbursements

CaliforniaVolunteers allows monthly or quarterly reimbursement but program must designate which method it will use

Must also have up-to-date and current:

1. Member hours in WBRS

2. PERs

3. FSRs

4. Program Reports

Must also demonstrate compliance with program

operations, i.e., no outstanding corrective action

Reimbursements

AmeriCorps Grant Provisions“Financial management systems must be capable of distinguishing expenditures attributable to this grant from expenditures not attributable to this grant. The systems must be able to identify costs by programmatic year and by budget category and to differentiate between direct and indirect costs or administrative costs.”

Reimbursements

Record in-kind contribution as both revenues and expenses

AmeriCorps Grant Provisions“A living allowance is not a wage. Programs must not pay a living allowance on an hourly basis. Programs should pay the living allowance in regular increments, such as weekly or bi-weekly, paying an increased increment only on the basis of increased living expenses such as food, housing, or transportation. Payments should not fluctuate based on the number of hours served in a particular time period, and must cease when a member concludes a term of service.”

Reimbursements

No “lump sum” if member completes term earlyNo “lump sum” if member starts late, e.g., “make up” missed payments

30 Days = Target Date– Reimbursement may take up to 45 days

Reimbursement requests received after due date will be processed in the following monthDelays Occur Because:

– Incomplete or incorrect invoices– Insufficient match– Missing documentation– Failure to update member hours in WBRS or to

correctly submit them– Failure to submit Progress Report

Payments from CaliforniaVolunteers

Key Elements of Financial Reporting

• Prepare all financial reports with information from the organization’s accounting system

• Review and reconciliation the information to ensure accuracy prior to report submission

• Files must have the proper documentation to support all information reported in financial reports

• Submit all reports on time

Reporting Requirements

1. Periodic Expense Report (PER) • Due to CaliforniaVolunteers office by the

25th day of the each month or quarter• Must be submitted via hard copy• 3 copies of the PER are required• Required documents include: PER and

invoice cover sheet

Failure to submit the PER on time will result in reimbursement delays

Reporting Requirements

2. Financial Status Report (FSR) • Due to CaliforniaVolunteers office by the 15th day

after the end of the reporting period• Must be submitted via hard copy• One (1) copy of the FSR is required• Required documents include:

• Program Income Form• Submission of all PERs for reporting period

Prior to the due date1. By e-mail, request an extension

2. Provide reason why an extension is needed

3. State expected date of completion

PERs and FSRs– Submit extension request to Grants

Management Associate (Jesse Delis)

Late Reports?

Program Income

Program Income Form• There are 2 alternatives to use program income:

1. Additive – added to funds committed to the program and used to further program objectives

2. Deductive – deducted from total allowable costs of the program to determine the net allowable costs for which the Federal share is based

Program Income

• Gross Program Income – All funds collected as a direct result of grant funded-activities

• Net Program Income – The amount after deducting costs associated with generating the income

• All Program Income must be used for grant-related purposes

• Program Income and the supporting documentation is “auditable”

Key Reporting Issues

• Program Income– These were the common errors found on the

April 30, 2009 Program Income Forms• Program Income used as match was erroneously

reported as Program Income– Corrective Action: If all your program income was used

as match, your Program Income Form should be blank

• Program Income Form was not submitted at the same time as the FSR

– Corrective Action: Submit the FSR and the Program Income Form at the same time, not separately

CaliforniaVolunteers must receive written approval from CNCS for these budgetary changes:

– Specific costs requiring approval under the cost principles, such as:• Overtime pay, rearrangement and alternation costs, and pre-

award costs

– Purchases of equipment over $5,000 using CNCS funds, unless specified in the approved application and budget

– Changes in the cumulative budget line items that amount to 10% or more of the total budget, unless the CNCS share is $100,000 or less• The total budget includes both the CNCS and grantee shares

• Grantees may transfer funds among approved direct costs categories when the cumulative amount of such transfers do not exceed 10% of the total budget

Rebudgeting

CaliforniaVolunteersKey Rebudgeting Issues

• Budget changes are made before CaliforniaVolunteers approved the change

• Adequate written justification was not provided• Budget Revision Request Form was incomplete• Inadequate monitoring of budget throughout the

year resulted in major budget changes at year-end, instead of periodically throughout the year

CaliforniaVolunteersRebudgeting Requests

Submit a Budget Revision Request Form (CV 200)• Narrative justification – explain why a redistribution of funds is

needed• Spreadsheet with the original CNCS share budget, proposed

budget, and difference between two budgets• Spreadsheet with the original Subgrantee share budget,

proposed budget, and difference between two budgets• Must be signed by the Program Director and faxed to

CaliforniaVolunteers Program Associate• Program Associate reviews it and approves program changes

and the Grants Management Associate reviews it for fiscal accuracy

• CaliforniaVolunteers will either approve or deny – wait to take action only after receiving approval

Your budget = estimate of expected costs• Estimates may change as the program is

implemented

• Review budget monthly

• Request budget revisions promptly

• Do not wait until last month of year to request budget modification

Rebudgeting Pointers

Federal Audits:OIG and A-133

What is an Audit

Examines a Corporation program or activity1. Financial Audits

• Audits of costs incurred on grants and contracts, indirect costs, and internal controls

2. Performance Audits• Audits of economy and efficiency of programs

– Measure achievement of desired results or benefits

Office of Inspector General

What’s the OIG Audit Process?

1. Notification Letter in writing

2. Entrance Conference • To provide audit scope and objectives

3. Survey Phase (planning phase) • To obtain grantee’s background, mission,

resources, responsibilities, key personnel, operating systems and controls

What’s the OIG Audit Process?

4. Develop the Audit Program• A set of procedures for auditors to follow

5. Field Work• Auditors complete the audit following the

procedures in the audit program

6. Exit Conference• A verbal briefing of auditor’s findings work with the

opportunity to confirm information, ask questions, and obtain clarifying information

What’s the OIG Audit Process?

7. Draft Report• Issued to the auditee and Corporation officials a

request to provide written comments in 30 days

8. Corporation & Grantee Response• The Corporation and Grantee each respond in writing to

the draft report and comments are published in the final report

9. Final Report• Issued after reviewing auditee’s and Corporation’s

comments with complete description of findings and recommendations for corrective action

Common Pitfalls & Issues7 Main Areas:

1. Member Eligibility

2. Member Files & Records

3. Member Costs

4. Match

5. Reports

6. Administrative Areas

7. General Management See Handout

OIG HotlineOIG HotlineReport suspected fraud, waste, or abuseReport suspected fraud, waste, or abuse

All Information is confidentialAll Information is confidential

You can remain anonymousYou can remain anonymous

1-800-452-82101-800-452-8210oror

[email protected]@cncsig.govWebsite: Website: www.cncsig.gov

Grant Closeout

CaliforniaVolunteers:Annual Closeout Procedures

CaliforniaVolunteers closes all subgrants on an annual basis:

1. Fiscal Activities

2. Program Activities

Program staff and Fiscal staff must coordinate Closeout activities

CaliforniaVolunteers Annual AmeriCorps Closeout Procedures

Fiscal Activities

1. Final Reimbursement Invoices - Due within 60 days of grant termination

• Review all obligations to ensure all expenses have been paid

• Final invoices will only be processed for payment after the program submits all required documentation attesting to the completeness of member records and the retention site

• Errors in reimbursement requests (over or under) discovered after closeout must be brought to the attention of the Commission ASAP for resolution

2. Final PER = Due within 60 days of grant end3. FSR = Due by April 15th following end of grant

Program Activities

There are 7 steps needed to complete the programmatic closeout of your grant. They are:

1. Verification of complete and accurate entry of member time logs into WBRS for each AmeriCorps member in your program

2. Verification that all Exit Forms have been entered into WBRS for all AmeriCorps members in your program

3. Print out a program reconciliation report from WBRS to verify that all members have been exited with appropriate education award

CaliforniaVolunteers Annual AmeriCorps Closeout Procedures

Program Activities 4. Review of all member files and submission of Member Files

Closeout Certification Form

5. Completion of final Progress Report

• Due 15th day after the program end date

6. Submission of printed final Progress Report, signed and dated by Program Director

7. Submission of cover letter, on letterhead, that steps 1-6 are completed, including information where files will be stored and the process for document retrieval in the event of an audit

CaliforniaVolunteers Annual AmeriCorps Closeout Procedures

Final Grant Closeout

CaliforniaVolunteers must:

1. Pay outstanding obligations

2. Close subgrants

3. Ensure FFR and PSC-272 are equal

4. Enter final FFR in eGrants

5. Submit closeout documents to CNCS

6. Return unobligated funds

CV cannot fix problems or return funds after funds have been returned to the Federal Government

Final Grant Closeout

Subgrantee must:

1. Submit Final FSR

2. Submit Equipment Inventory Form

3. Submit Residual Supplies Form

4. Submit Progress Report

CNCS: Deobligating Funds

• CNCS will deobligate any authorized grant funds not drawn down at the end of the project period

• Deobligation reduces the amount of authorized funds to equal the amounts disbursed and drawn down for the grantee and its subgrantees

• Grantees do not have access to deobligated funds

CNCS: Subsequent Audit

• CaliforniaVolunteers and CNCS retain right to conduct a subsequent audit or other review of a grant – closeout does not change this right

• Notice of audit may extend the 3 year record retention requirement

Subgrantees and Grantee must:

• Retain all records for 3 years from when the Commission (grantee) submits the final FSR

• Requirement is included in the CNCS Grant Provisions

Questions?Questions?