Embed Size (px)

Citation preview

Chapter 4Statement of Cash Flows

When a company prepares a complete set of financial statements, it includes a statement of cash flows with the income statement, balance sheet, and retained earnings statement. 1 A statement of cash flows is a financial statement that displays a business’s cash receipts and cash disbursements for a period according to categories of business activities—operating activities, financing activities, and investing activities. The statement shows the reader the business’s cash sources and how the business used the cash during the period. Readers use this information in answering such questions as: “Why did the company pay little or no cash dividends when it had significant net income?” or, “How did the company finance the purchase of new plant assets?” This chapter presents a discussion of the statement of cash flows, including its usefulness, and describes techniques for preparing the statement.

LEARNING OBJECTIVES

1. Explain the purpose of a statement of cash flows.2. Describe the operating, investing, and financing classifications of cash flow activities.3. Explain how to prepare a statement of cash flows.4. Analyze accrual basis accounting information to determine the effects on cash flows.5. Describe the indirect method of reporting cash flows from operating activities.6. Understand the underlying relationship between net income and cash flows.7. Describe the relationship between accounting income and cash flows and the concepts of quality and persistence of earnings8. Prepare a statement of cash flows using a worksheet (Appendix SCF-A).

1 “Statement of Cash Flows,” Statement of Financial Accounting Standards No. 95 (Stamford, Conn.; FASB, 1987), par. 3.

Copyright © 2003, Robert G. May Page 1

LO 1 PURPOSE OF A STATEMENT OF CASH FLOWS

The accounting profession has identified information about a business’s cash flows as an objective of financial reporting as indicated by the following paragraph:

Financial reporting should provide information to help present and potential investors and creditors and other users in assessing the amounts, timing, and uncertainty of prospective cash receipts from dividends or interest and the proceeds from the sale, redemption, or maturity of securities or loans. The prospects for those cash receipts are affected by an enterprise’s ability to generate enough cash to meet its obligations when due and its other cash operating needs, to reinvest in operations, and to pay cash dividends. 2

Accountants designed the statement of cash flows to meet this objective by assisting investors, creditors, and other readers of the financial statements in assessing such factors as follow:

• The business’s ability to generate positive cash flows in future periods

• The business’s ability to meet its obligations and to pay dividends• Reasons for differences between the amount of net income and the

related cash flows from operations• Both the cash and noncash aspects of the business’s investing and

financing activities for the period.3

Complete Set of Financial Statements

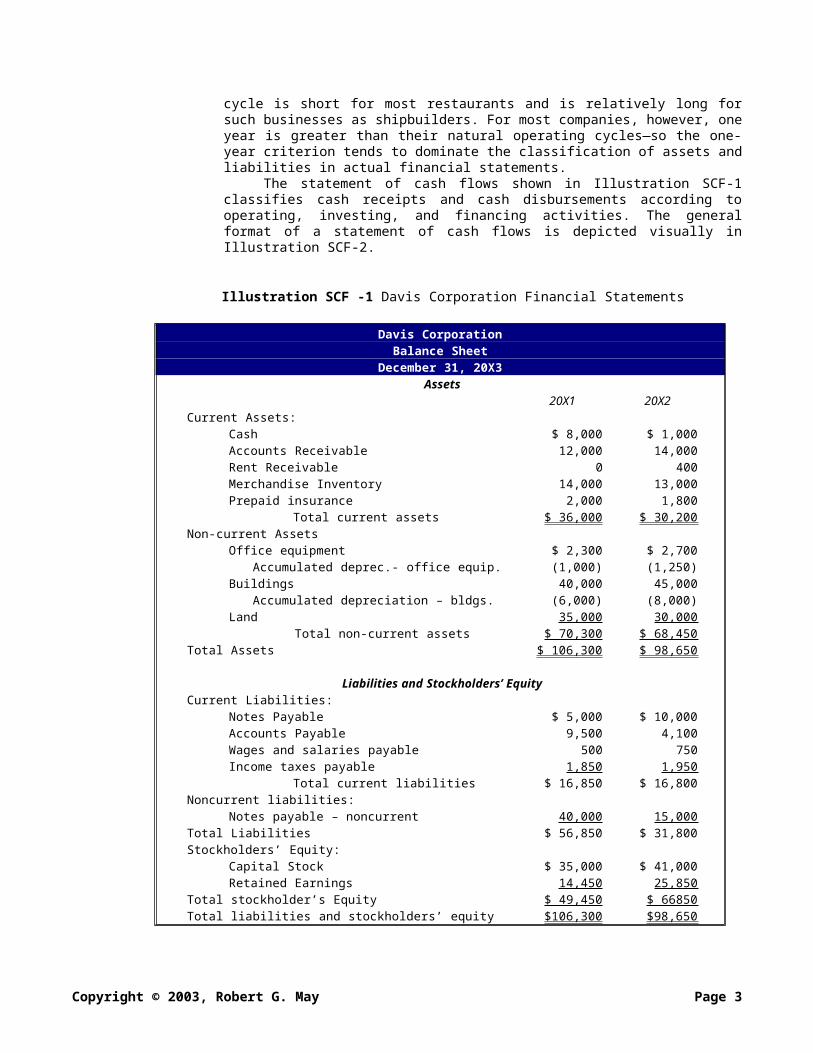

Illustration SCF-1 presents a complete set of financial statements for the Davis Corporation. The financial statements presented include a comparative balance sheet for 20X1 and 20X2, an income statement for 20X2, a retained earnings statement for 20X2, and a statement of cash flows for 20X2. Notice that in the balance sheet, assets and liabilities are classified as current and non-current. These classifications relate directly to cash flows for most companies in that current assets are those assets that will be converted to another form (usually realized in the form of cash) within one year or one operating cycle, whichever is longer. All other assets are non-current. Current liabilities are those that will be settled (usually paid) within one year or one operating cycle, whichever is longer. All other liabilities are non-current. The operating cycle of a business is the typical length of time from the acquisition of the inputs for its production process to the collection of cash from customers. This cycle is short for most restaurants and is relatively long for such businesses as shipbuilders. For most companies, however, one year is greater than their natural operating cycles—so the one-year criterion tends to dominate the classification of assets and liabilities in actual financial statements.

2 “Objectives of Financial Reporting by Business Enterprises,” Statement of Financial Accounting Concepts, No. 1(Stamford, Conn.: FASB, 1978), par 373 Ibid., par 5.

Copyright © 2003, Robert G. May Page 2

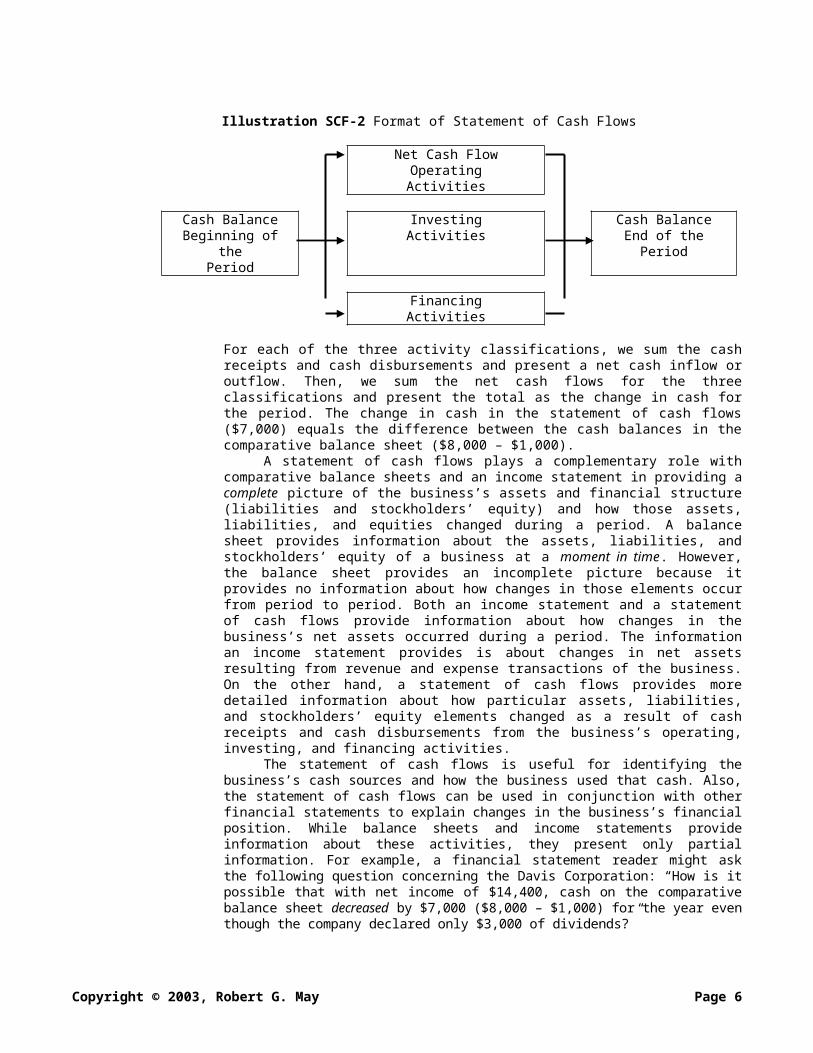

The statement of cash flows shown in Illustration SCF-1 classifies cash receipts and cash disbursements according to operating, investing, and financing activities. The general format of a statement of cash flows is depicted visually in Illustration SCF-2.

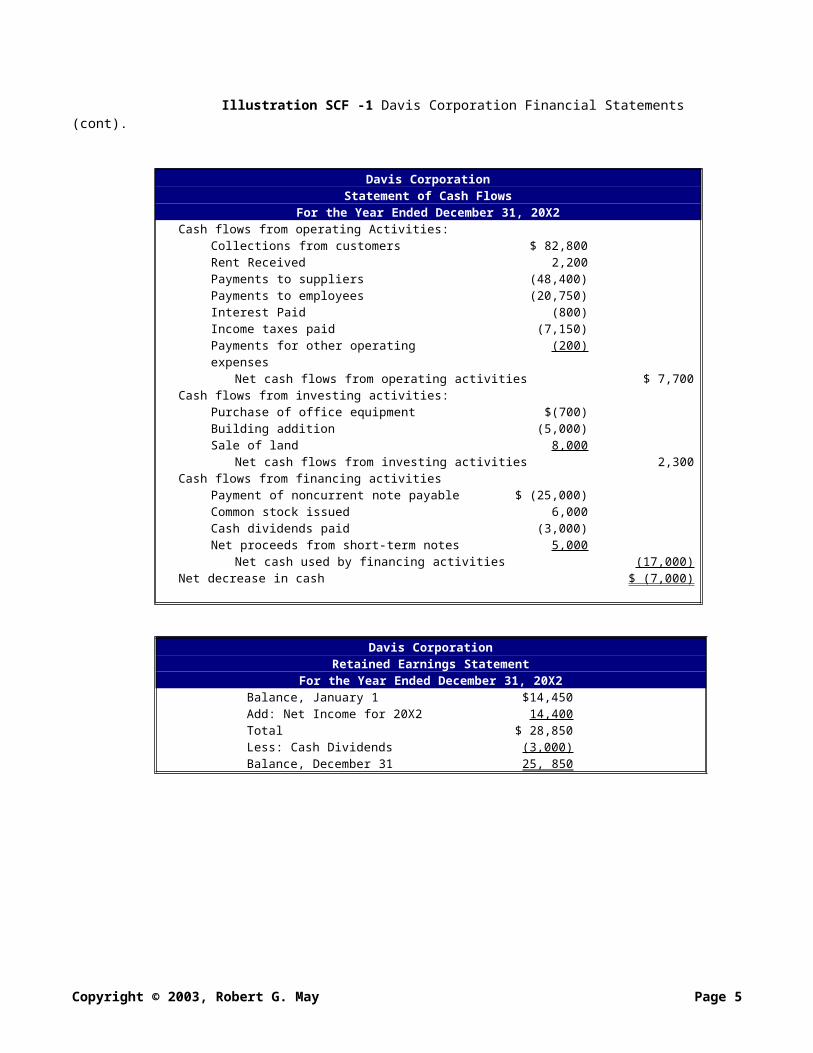

Illustration SCF -1 Davis Corporation Financial Statements

Davis CorporationBalance Sheet

December 31, 20X3Assets

20X1 20X2Current Assets:

Cash $ 8,000 $ 1,000Accounts Receivable 12,000 14,000Rent Receivable 0 400Merchandise Inventory 14,000 13,000Prepaid insurance 2,000 1,800

Total current assets $ 36,000 $ 30,200Non-current Assets

Office equipment $ 2,300 $ 2,700Accumulated deprec.- office equip. (1,000) (1,250)

Buildings 40,000 45,000Accumulated depreciation – bldgs. (6,000) (8,000)

Land 35,000 30,000Total non-current assets $ 70,300 $ 68,450

Total Assets $ 106,300 $ 98,650

Liabilities and Stockholders’ EquityCurrent Liabilities:

Notes Payable $ 5,000 $ 10,000Accounts Payable 9,500 4,100Wages and salaries payable 500 750Income taxes payable 1,850 1,950

Total current liabilities $ 16,850 $ 16,800Noncurrent liabilities:

Notes payable – noncurrent 40,000 15,000Total Liabilities $ 56,850 $ 31,800Stockholders’ Equity:

Capital Stock $ 35,000 $ 41,000Retained Earnings 14,450 25,850

Total stockholder’s Equity $ 49,450 $ 66850Total liabilities and stockholders’ equity $106,300 $98,650

Copyright © 2003, Robert G. May Page 3

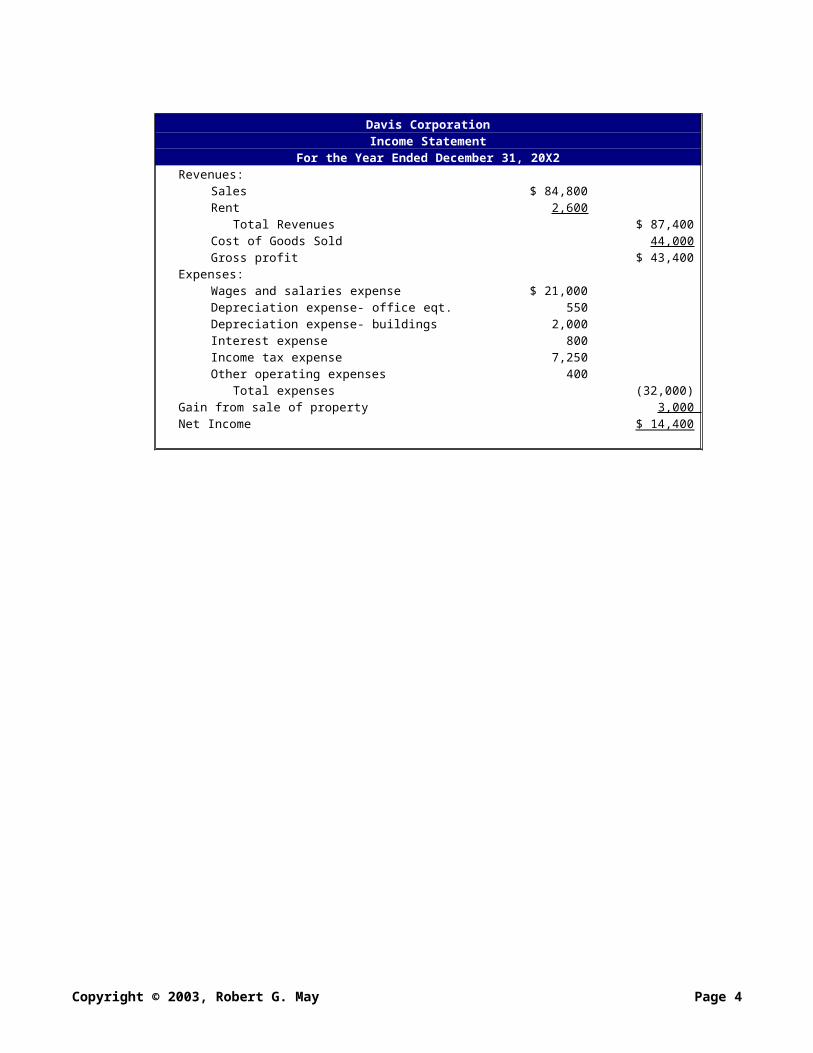

Davis CorporationIncome Statement

For the Year Ended December 31, 20X2Revenues:

Sales $ 84,800Rent 2,600 Total Revenues $ 87,400Cost of Goods Sold 44,000Gross profit $ 43,400

Expenses:Wages and salaries expense $ 21,000Depreciation expense- office eqt. 550Depreciation expense- buildings 2,000Interest expense 800Income tax expense 7,250Other operating expenses 400 Total expenses (32,000)

Gain from sale of property 3,000 Net Income $ 14,400

Illustration SCF -1 Davis Corporation Financial Statements (cont).

Davis CorporationStatement of Cash Flows

For the Year Ended December 31, 20X2Cash flows from operating Activities:

Collections from customers $ 82,800Rent Received 2,200Payments to suppliers (48,400)Payments to employees (20,750)Interest Paid (800)Income taxes paid (7,150)Payments for other operating expenses

(200)

Net cash flows from operating activities $ 7,700Cash flows from investing activities:

Purchase of office equipment $(700)Building addition (5,000)Sale of land 8,000

Net cash flows from investing activities 2,300Cash flows from financing activities

Payment of noncurrent note payable $ (25,000)Common stock issued 6,000Cash dividends paid (3,000)Net proceeds from short-term notes 5,000

Net cash used by financing activities (17,000)Net decrease in cash $ (7,000)

Copyright © 2003, Robert G. May Page 4

Davis CorporationRetained Earnings Statement

For the Year Ended December 31, 20X2 Balance, January 1 $14,450Add: Net Income for 20X2 14,400Total $ 28,850Less: Cash Dividends (3,000)Balance, December 31 25, 850

Illustration SCF-2 Format of Statement of Cash Flows

Net Cash FlowOperatingActivities

Cash BalanceBeginning of the

Period

InvestingActivities

Cash BalanceEnd of the Period

FinancingActivities

For each of the three activity classifications, we sum the cash receipts and cash disbursements and present a net cash inflow or outflow. Then, we sum the net cash flows for the three classifications and present the total as the change in cash for the period. The change in cash in the statement of cash flows ($7,000) equals the difference between the cash balances in the comparative balance sheet ($8,000 – $1,000).

A statement of cash flows plays a complementary role with comparative balance sheets and an income statement in providing a complete picture of the business’s assets and financial structure (liabilities and stockholders’ equity) and how those assets, liabilities, and equities changed during a period. A balance sheet provides information about the assets, liabilities, and stockholders’ equity of a business at a moment in time. However, the balance sheet provides an incomplete picture because it provides no information about how changes in those elements occur from period to period. Both an income statement and a statement of cash flows provide information about how changes in the business’s net assets occurred during a period. The information an income statement provides is about changes in net assets resulting from revenue and expense transactions of the business. On the other hand, a statement of cash flows provides more detailed information about how particular assets, liabilities, and stockholders’ equity elements changed as a result of cash receipts and cash disbursements from the business’s operating, investing, and financing activities.

The statement of cash flows is useful for identifying the business’s cash sources and how the business used that cash. Also, the statement of cash flows can be used in conjunction with other financial statements to explain changes in the business’s financial position. While balance sheets and income statements provide information about these activities, they present only partial information. For example, a financial statement reader might ask the following question concerning the Davis Corporation: “How is it possible that with net income of $14,400, cash on the comparative balance sheet decreased by

Copyright © 2003, Robert G. May Page 5

$7,000 ($8,000 – $1,000) for the year even though the company declared only $3,000 of dividends?”

Interpreting the Statement of Cash Flows

An examination of the statement of cash flows reveals the following response: even though net income is $14,400, operating activities actually generated net cash flows of only $7,700. Also, investing activities generated net cash flows of $2,300, resulting from the sale of land less the purchase of new assets. Finally, financing activities used net cash of $16,700, resulting from the net effects of issuing common stock, paying off debt of $25,000, paying the $3,000 cash dividends, and increasing short-term borrowings. The net effect of these transactions is a $7,000 decrease in cash for the year. Overall, rather than paying greater dividends, Davis Corporation paid off a large portion of its long-term debt. Certainly, such a detailed analysis of Davis Corporation would be difficult without the statement of cash flows.

LO 2 CLASSIFICATION OF CASH FLOWS

As you see in Illustration SCF-1, the statement of cash flows classifies the business’s cash receipts and cash payments according to the categories of operating, investing, and financing activities.

Operating Activities

A business’s normal operations result in both cash receipts and cash disbursements. Cash receipts result from selling merchandise and providing services. Cost of goods sold, expenses directly associated with providing services, and other operating expenses result in cash disbursements. The revenues and expenses reported in the income statement, however, do not coincide with the cash receipts and cash disbursements. Under GAAP, we prepare the income statement on an accrual basis, which means we record the revenues when earned and expenses when incurred. The receipts and payments of cash for these revenues and expenses may occur in either an earlier or later period than the period in which we report the revenues and expenses.

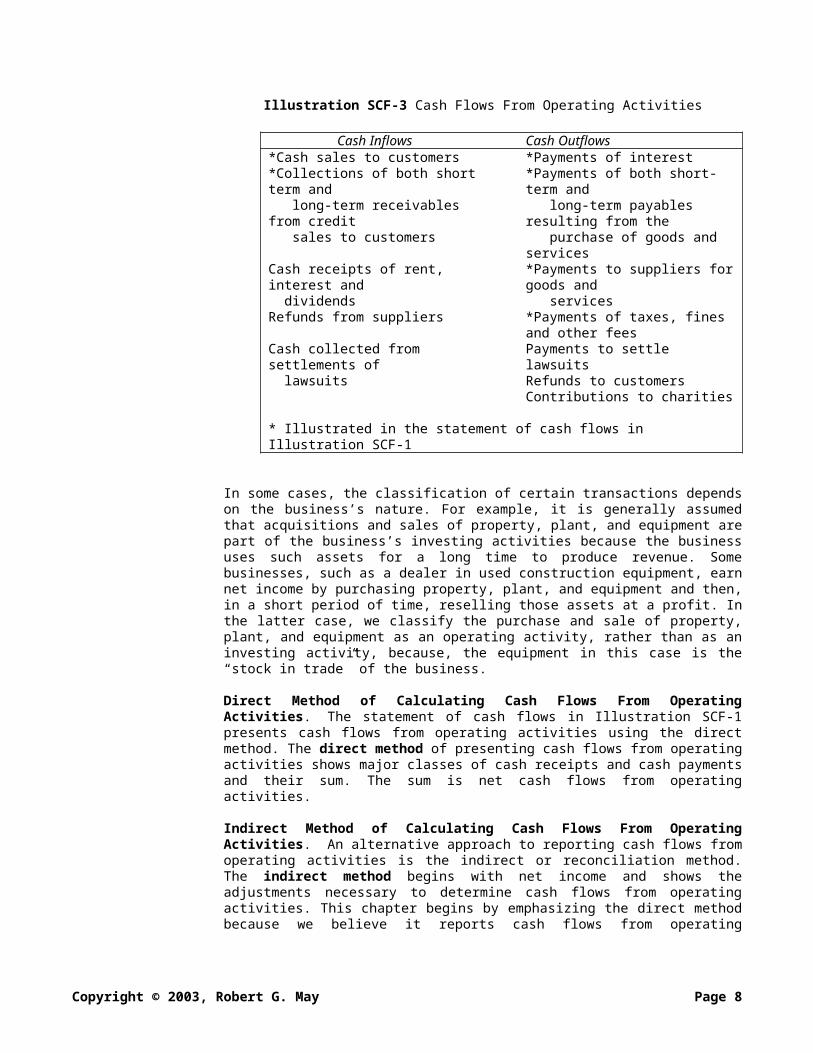

All transactions and events that are not classified as either investing or financing activities are classified as operating activities. Cash flows from operating activities generally are the cash effects of the transactions—selling or producing goods or providing services—included to determine net income. Illustration SCF-3 presents a listing of the types of transactions that are classified as operating activities for the statement of cash flows.

Copyright © 2003, Robert G. May Page 6

Illustration SCF-3 Cash Flows From Operating Activities

Cash Inflows Cash Outflows*Cash sales to customers *Payments of interest*Collections of both short term and long-term receivables from credit sales to customers

*Payments of both short-term and long-term payables resulting from the purchase of goods and services

Cash receipts of rent, interest and dividends

*Payments to suppliers for goods and services

Refunds from suppliers *Payments of taxes, fines and other fees

Cash collected from settlements of lawsuits

Payments to settle lawsuitsRefunds to customers

Contributions to charities

* Illustrated in the statement of cash flows in Illustration SCF-1

In some cases, the classification of certain transactions depends on the business’s nature. For example, it is generally assumed that acquisitions and sales of property, plant, and equipment are part of the business’s investing activities because the business uses such assets for a long time to produce revenue. Some businesses, such as a dealer in used construction equipment, earn net income by purchasing property, plant, and equipment and then, in a short period of time, reselling those assets at a profit. In the latter case, we classify the purchase and sale of property, plant, and equipment as an operating activity, rather than as an investing activity, because, the equipment in this case is the “stock in trade” of the business.

Direct Method of Calculating Cash Flows From Operating Activities. The statement of cash flows in Illustration SCF-1 presents cash flows from operating activities using the direct method. The direct method of presenting cash flows from operating activities shows major classes of cash receipts and cash payments and their sum. The sum is net cash flows from operating activities.

Indirect Method of Calculating Cash Flows From Operating Activities. An alternative approach to reporting cash flows from operating activities is the indirect or reconciliation method. The indirect method begins with net income and shows the adjustments necessary to determine cash flows from operating activities. This chapter begins by emphasizing the direct method because we believe it reports cash flows from operating activities more clearly. We illustrate the indirect method later in the chapter.

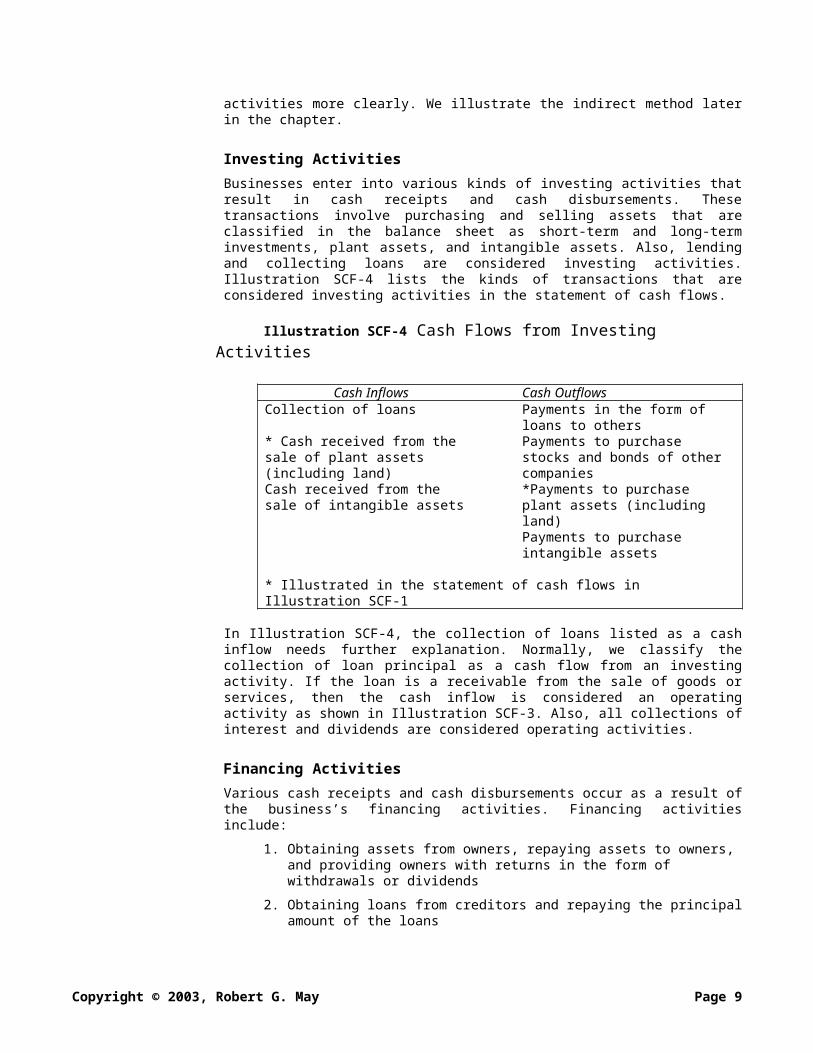

Investing Activities

Businesses enter into various kinds of investing activities that result in cash receipts and cash disbursements. These transactions involve purchasing

Copyright © 2003, Robert G. May Page 7

and selling assets that are classified in the balance sheet as short-term and long-term investments, plant assets, and intangible assets. Also, lending and collecting loans are considered investing activities. Illustration SCF-4 lists the kinds of transactions that are considered investing activities in the statement of cash flows.

Illustration SCF-4 Cash Flows from Investing Activities

Cash Inflows Cash OutflowsCollection of loans Payments in the form of loans

to others* Cash received from the sale of plant assets (including land)

Payments to purchase stocks and bonds of other companies

Cash received from the sale of intangible assets

*Payments to purchase plant assets (including land)Payments to purchase intangible assets

* Illustrated in the statement of cash flows in Illustration SCF-1

In Illustration SCF-4, the collection of loans listed as a cash inflow needs further explanation. Normally, we classify the collection of loan principal as a cash flow from an investing activity. If the loan is a receivable from the sale of goods or services, then the cash inflow is considered an operating activity as shown in Illustration SCF-3. Also, all collections of interest and dividends are considered operating activities.

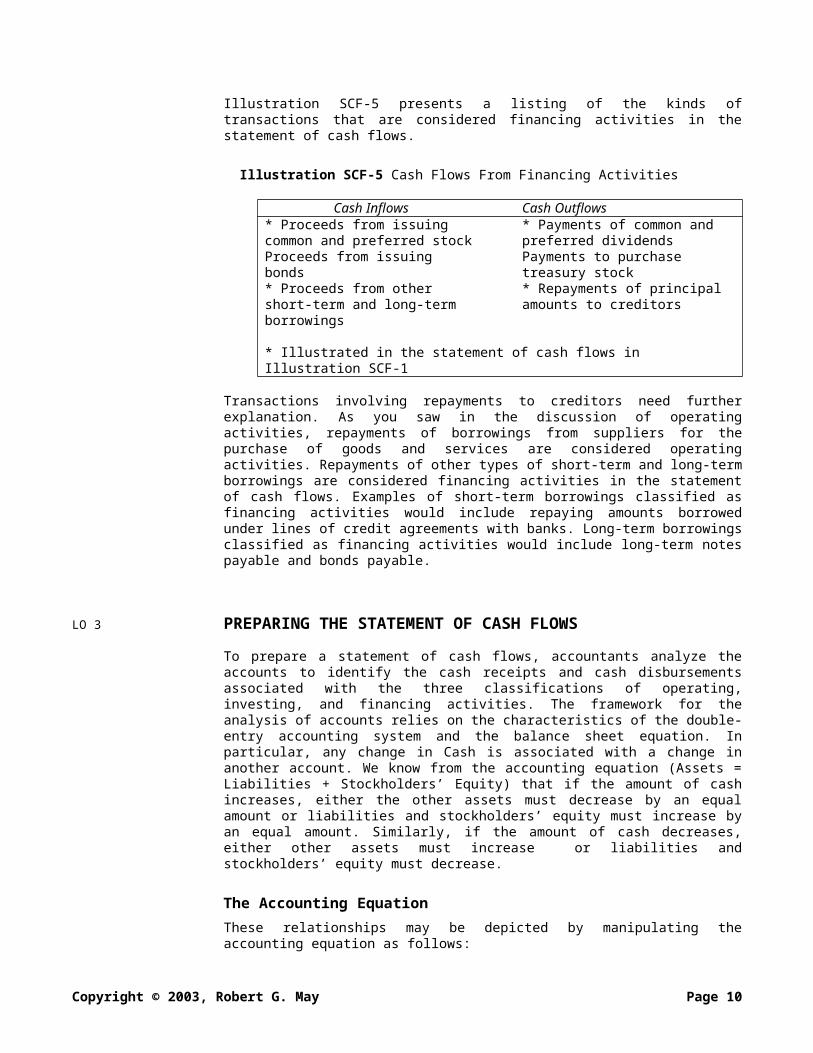

Financing Activities

Various cash receipts and cash disbursements occur as a result of the business’s financing activities. Financing activities include:

1. Obtaining assets from owners, repaying assets to owners, and providing owners with returns in the form of withdrawals or dividends

2. Obtaining loans from creditors and repaying the principal amount of the loans

Illustration SCF-5 presents a listing of the kinds of transactions that are considered financing activities in the statement of cash flows.

Illustration SCF-5 Cash Flows From Financing Activities

Cash Inflows Cash Outflows* Proceeds from issuing common and preferred stock

* Payments of common and preferred dividends

Proceeds from issuing bonds Payments to purchase treasury stock

* Proceeds from other short-term and long-term borrowings

* Repayments of principal amounts to creditors

* Illustrated in the statement of cash flows in Illustration SCF-1

Copyright © 2003, Robert G. May Page 8

Transactions involving repayments to creditors need further explanation. As you saw in the discussion of operating activities, repayments of borrowings from suppliers for the purchase of goods and services are considered operating activities. Repayments of other types of short-term and long-term borrowings are considered financing activities in the statement of cash flows. Examples of short-term borrowings classified as financing activities would include repaying amounts borrowed under lines of credit agreements with banks. Long-term borrowings classified as financing activities would include long-term notes payable and bonds payable.

LO 3 PREPARING THE STATEMENT OF CASH FLOWS

To prepare a statement of cash flows, accountants analyze the accounts to identify the cash receipts and cash disbursements associated with the three classifications of operating, investing, and financing activities. The framework for the analysis of accounts relies on the characteristics of the double-entry accounting system and the balance sheet equation. In particular, any change in Cash is associated with a change in another account. We know from the accounting equation (Assets = Liabilities + Stockholders’ Equity) that if the amount of cash increases, either the other assets must decrease by an equal amount or liabilities and stockholders’ equity must increase by an equal amount. Similarly, if the amount of cash decreases, either other assets must increase or liabilities and stockholders’ equity must decrease.

The Accounting Equation

These relationships may be depicted by manipulating the accounting equation as follows:

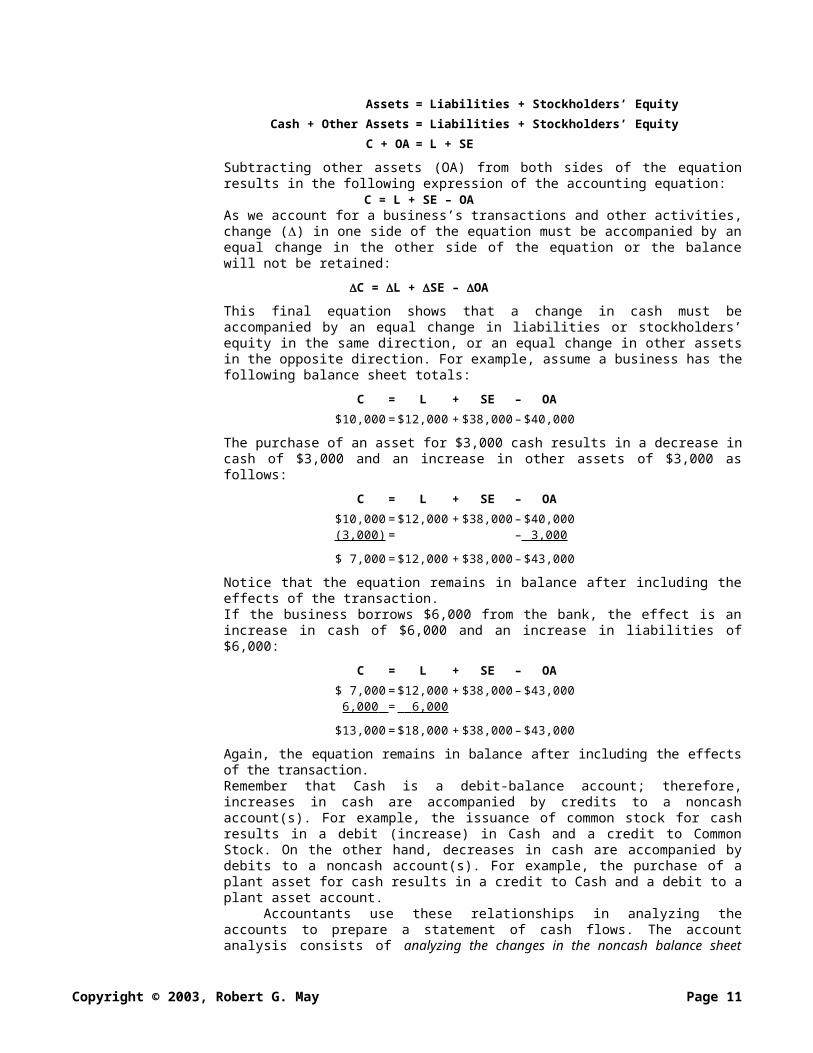

Assets = Liabilities + Stockholders’ Equity

Cash + Other Assets = Liabilities + Stockholders’ Equity

C + OA = L + SE

Subtracting other assets (OA) from both sides of the equation results in the following expression of the accounting equation:

C = L + SE – OAAs we account for a business’s transactions and other activities, change () in one side of the equation must be accompanied by an equal change in the other side of the equation or the balance will not be retained:

C = L + SE – OA

This final equation shows that a change in cash must be accompanied by an equal change in liabilities or stockholders’ equity in the same direction, or an equal change in other assets in the opposite direction. For example, assume a business has the following balance sheet totals:

C = L + SE – OA

$10,000=$12,000 + $38,000 – $40,000

The purchase of an asset for $3,000 cash results in a decrease in cash of $3,000 and an increase in other assets of $3,000 as follows:

Copyright © 2003, Robert G. May Page 9

C = L + SE – OA

$10,000=$12,000 + $38,000 – $40,000(3,000) = – 3,000

$ 7,000 =$12,000 + $38,000 – $43,000

Notice that the equation remains in balance after including the effects of the transaction.If the business borrows $6,000 from the bank, the effect is an increase in cash of $6,000 and an increase in liabilities of $6,000:

C = L + SE – OA

$ 7,000 =$12,000 + $38,000 – $43,0006,000 = 6,000

$13,000=$18,000 + $38,000 – $43,000

Again, the equation remains in balance after including the effects of the transaction.Remember that Cash is a debit-balance account; therefore, increases in cash are accompanied by credits to a noncash account(s). For example, the issuance of common stock for cash results in a debit (increase) in Cash and a credit to Common Stock. On the other hand, decreases in cash are accompanied by debits to a noncash account(s). For example, the purchase of a plant asset for cash results in a credit to Cash and a debit to a plant asset account.

Accountants use these relationships in analyzing the accounts to prepare a statement of cash flows. The account analysis consists of analyzing the changes in the noncash balance sheet accounts to explain the changes in cash for the period. The account analysis is complicated by the fact that not all changes in noncash accounts result in a cash inflow or outflow. For example, the purchase of a building by incurring a mortgage payable does not have an immediate effect on cash. Also, depreciation expense does not involve an entry to Cash. To prepare the statement of cash flows, the accountant must sort through the changes in the noncash balance sheet accounts and identify those transactions and events that change the noncash accounts and involve cash receipts and disbursements.

Sources of Information

To perform the account analysis used to construct a Cash Flows Statement, the accountant should have the following sources of information:

• Comparative balance sheet. The accountant needs a balance sheet for the end of the current period and a balance sheet for the end of the previous period to determine the net change in Cash and the noncash balance sheet accounts for the period.• Income statement. The accountant uses an income statement for the current period to determine the cash flows from operating activities. The income statement provides information about the revenue and expenses for the period, including noncash expenses such as depreciation.• Summary transaction data. The accountant can obtain summary information about the components of changes in account balances by analyzing the general ledger T-accounts. The summary information about transactions is needed because the comparative balance sheet only shows the net changes in the various account balances. For example, a $1,000

Copyright © 2003, Robert G. May Page 10

increase in Equipment may be the result of a purchase of equipment costing $1,000, or the result of a $2,000 purchase and the disposal of equipment that originally cost $1,000. Acquisitions and dispositions of plant assets are shown as separate investment activities in a statement of cash flows.

LO 4 PREPARING A STATEMENT OF CASH FLOWS—AN ILLUSTRATION

In Illustration SCF-1, the statement of cash flows for Davis Corporation is presented. Following is a discussion of how we developed that statement from the company’s accrual basis records.

In addition to the company’s financial statements, shown in Illustration SCF-1, we derived the following information from analyzing Davis Corporation’s accounts:

1. Prepaid Insurance is related to “Other operating expenses” shown on the income statement.

2. New office equipment was purchased at a cost of $700.3. Worn-out and fully depreciated office equipment was discarded. The

equipment cost $300 when purchased.4. A new storage room was added to the building at a cost of $5,000.5. Depreciation expense, office equipment, is $550.6. Depreciation expense, building, is $2,000.7. Land that cost $5,000 was sold for $8,000, resulting in a gain of

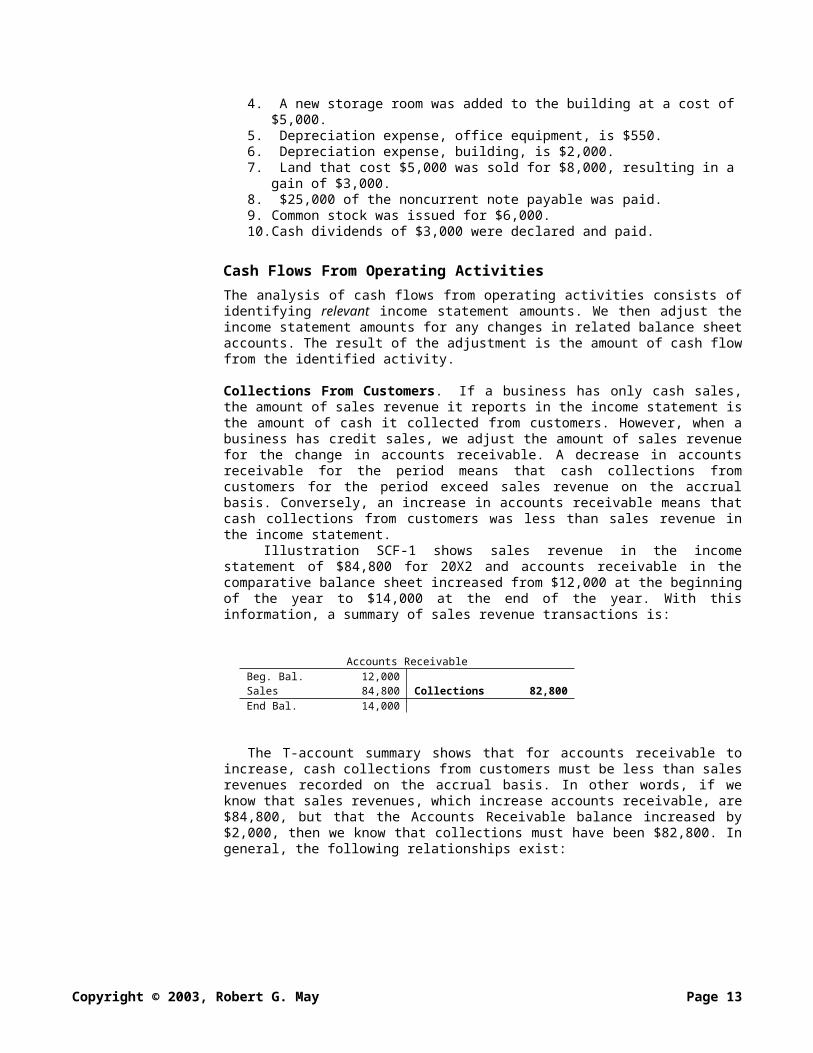

$3,000.8. $25,000 of the noncurrent note payable was paid.9. Common stock was issued for $6,000.10. Cash dividends of $3,000 were declared and paid.

Cash Flows From Operating Activities

The analysis of cash flows from operating activities consists of identifying relevant income statement amounts. We then adjust the income statement amounts for any changes in related balance sheet accounts. The result of the adjustment is the amount of cash flow from the identified activity.

Collections From Customers. If a business has only cash sales, the amount of sales revenue it reports in the income statement is the amount of cash it collected from customers. However, when a business has credit sales, we adjust the amount of sales revenue for the change in accounts receivable. A decrease in accounts receivable for the period means that cash collections from customers for the period exceed sales revenue on the accrual basis. Conversely, an increase in accounts receivable means that cash collections from customers was less than sales revenue in the income statement.

Illustration SCF-1 shows sales revenue in the income statement of $84,800 for 20X2 and accounts receivable in the comparative balance sheet increased from $12,000 at the beginning of the year to $14,000 at the end of the year. With this information, a summary of sales revenue transactions is:

Accounts Receivable

Copyright © 2003, Robert G. May Page 11

Beg. Bal. 12,000Sales 84,800 Collections 82,800End Bal. 14,000

The T-account summary shows that for accounts receivable to increase, cash collections from customers must be less than sales revenues recorded on the accrual basis. In other words, if we know that sales revenues, which increase accounts receivable, are $84,800, but that the Accounts Receivable balance increased by $2,000, then we know that collections must have been $82,800. In general, the following relationships exist:

– Increase in Accounts Receivable

Cash Collections from Customers = Sales Revenues or

+ Decrease in Accounts Receivable

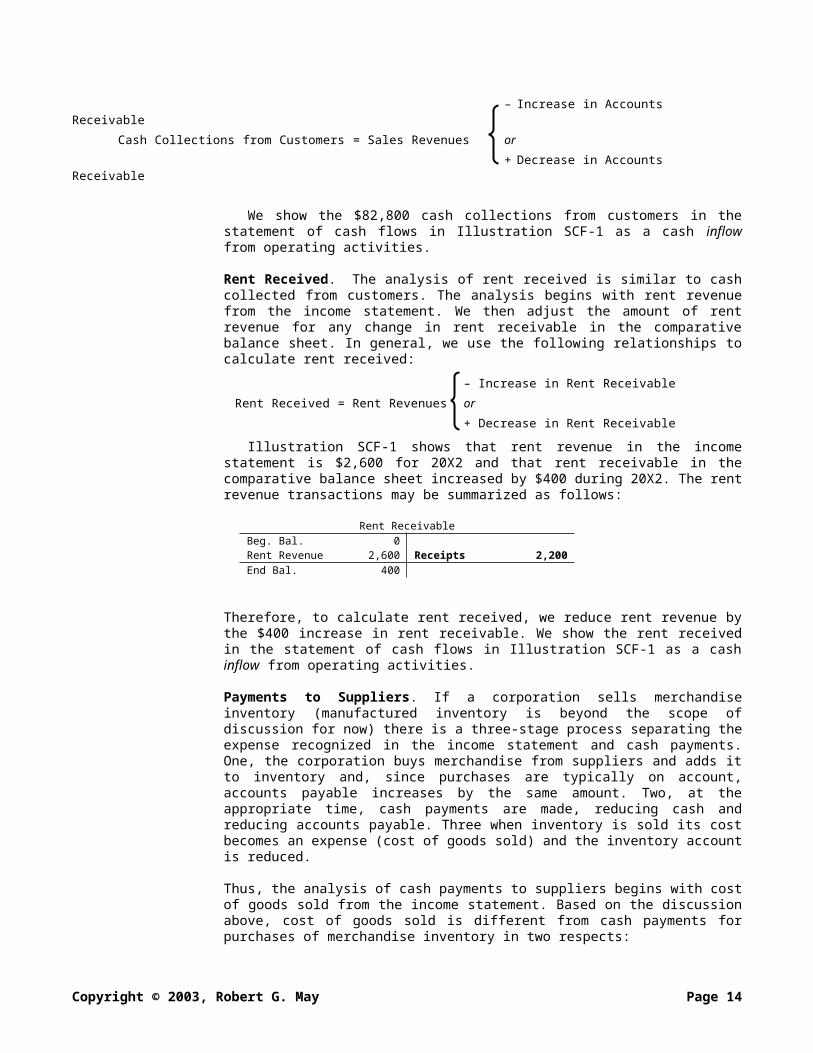

We show the $82,800 cash collections from customers in the statement of cash flows in Illustration SCF-1 as a cash inflow from operating activities.

Rent Received. The analysis of rent received is similar to cash collected from customers. The analysis begins with rent revenue from the income statement. We then adjust the amount of rent revenue for any change in rent receivable in the comparative balance sheet. In general, we use the following relationships to calculate rent received:

– Increase in Rent Receivable

Rent Received = Rent Revenues or

+ Decrease in Rent Receivable

Illustration SCF-1 shows that rent revenue in the income statement is $2,600 for 20X2 and that rent receivable in the comparative balance sheet increased by $400 during 20X2. The rent revenue transactions may be summarized as follows:

Rent ReceivableBeg. Bal. 0Rent Revenue 2,600 Receipts 2,200End Bal. 400

Therefore, to calculate rent received, we reduce rent revenue by the $400 increase in rent receivable. We show the rent received in the statement of cash flows in Illustration SCF-1 as a cash inflow from operating activities.

Payments to Suppliers. If a corporation sells merchandise inventory (manufactured inventory is beyond the scope of discussion for now) there is a three-stage process separating the expense recognized in the income statement and cash payments. One, the corporation buys merchandise from suppliers and adds it to inventory and, since purchases are typically on account, accounts payable increases by the same amount. Two, at the appropriate time, cash payments are made, reducing cash and reducing accounts payable. Three when inventory is sold its cost becomes an expense (cost of goods sold) and the inventory account is reduced.

Copyright © 2003, Robert G. May Page 12

Thus, the analysis of cash payments to suppliers begins with cost of goods sold from the income statement. Based on the discussion above, cost of goods sold is different from cash payments for purchases of merchandise inventory in two respects:

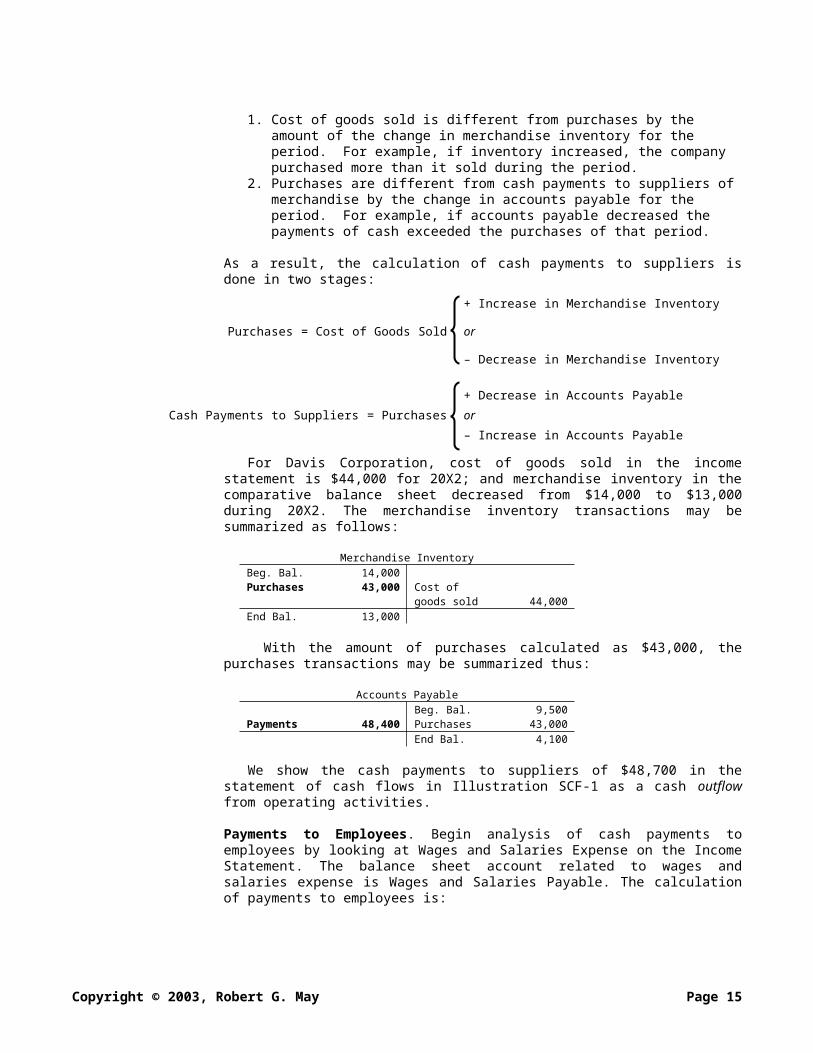

1. Cost of goods sold is different from purchases by the amount of the change in merchandise inventory for the period. For example, if inventory increased, the company purchased more than it sold during the period.

2. Purchases are different from cash payments to suppliers of merchandise by the change in accounts payable for the period. For example, if accounts payable decreased the payments of cash exceeded the purchases of that period.

As a result, the calculation of cash payments to suppliers is done in two stages:

+ Increase in Merchandise Inventory

Purchases = Cost of Goods Sold or

– Decrease in Merchandise Inventory

+ Decrease in Accounts Payable

Cash Payments to Suppliers = Purchases or

– Increase in Accounts Payable

For Davis Corporation, cost of goods sold in the income statement is $44,000 for 20X2; and merchandise inventory in the comparative balance sheet decreased from $14,000 to $13,000 during 20X2. The merchandise inventory transactions may be summarized as follows:

Merchandise InventoryBeg. Bal. 14,000Purchases 43,000 Cost of

goods sold 44,000End Bal. 13,000

With the amount of purchases calculated as $43,000, the purchases transactions may be summarized thus:

Accounts PayableBeg. Bal. 9,500

Payments 48,400 Purchases 43,000End Bal. 4,100

We show the cash payments to suppliers of $48,700 in the statement of cash flows in Illustration SCF-1 as a cash outflow from operating activities.

Payments to Employees. Begin analysis of cash payments to employees by looking at Wages and Salaries Expense on the Income Statement. The balance sheet account related to wages and salaries expense is Wages and Salaries Payable. The calculation of payments to employees is:

Copyright © 2003, Robert G. May Page 13

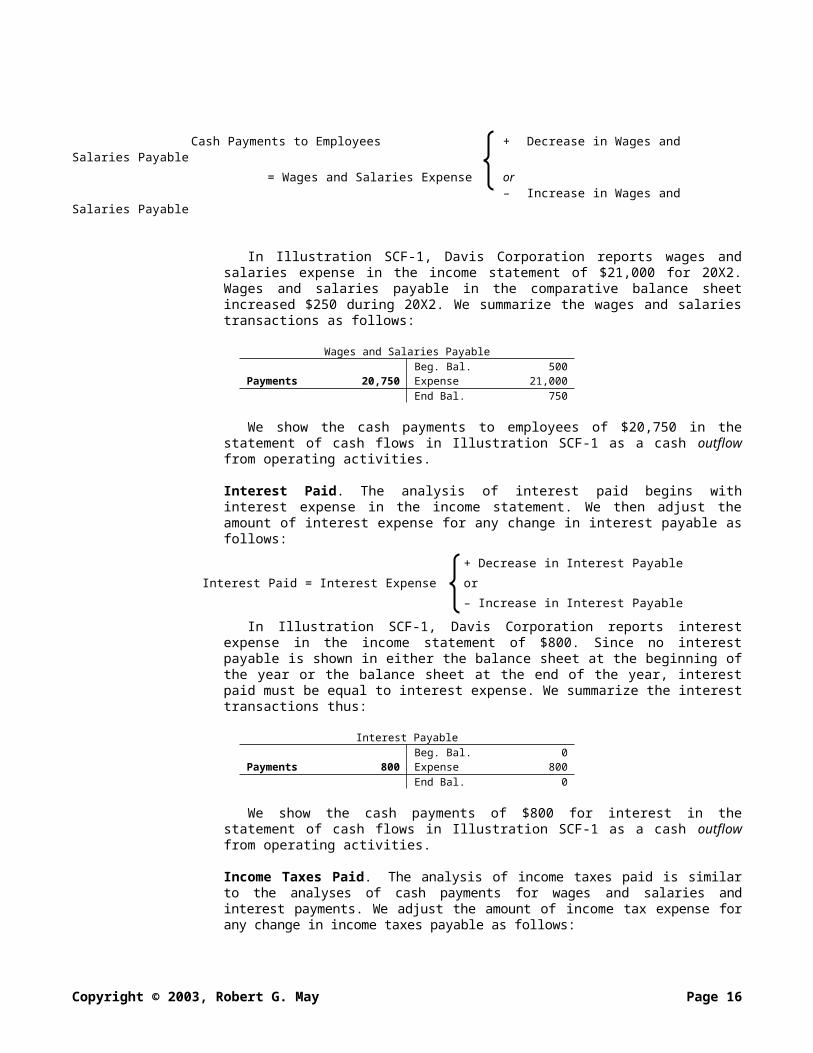

Cash Payments to Employees + Decrease in Wages and Salaries Payable

= Wages and Salaries Expense or– Increase in Wages and Salaries

Payable

In Illustration SCF-1, Davis Corporation reports wages and salaries expense in the income statement of $21,000 for 20X2. Wages and salaries payable in the comparative balance sheet increased $250 during 20X2. We summarize the wages and salaries transactions as follows:

Wages and Salaries PayableBeg. Bal. 500

Payments 20,750 Expense 21,000End Bal. 750

We show the cash payments to employees of $20,750 in the statement of cash flows in Illustration SCF-1 as a cash outflow from operating activities.

Interest Paid. The analysis of interest paid begins with interest expense in the income statement. We then adjust the amount of interest expense for any change in interest payable as follows:

+ Decrease in Interest Payable

Interest Paid = Interest Expense or

– Increase in Interest Payable

In Illustration SCF-1, Davis Corporation reports interest expense in the income statement of $800. Since no interest payable is shown in either the balance sheet at the beginning of the year or the balance sheet at the end of the year, interest paid must be equal to interest expense. We summarize the interest transactions thus:

Interest PayableBeg. Bal. 0

Payments 800 Expense 800End Bal. 0

We show the cash payments of $800 for interest in the statement of cash flows in Illustration SCF-1 as a cash outflow from operating activities.

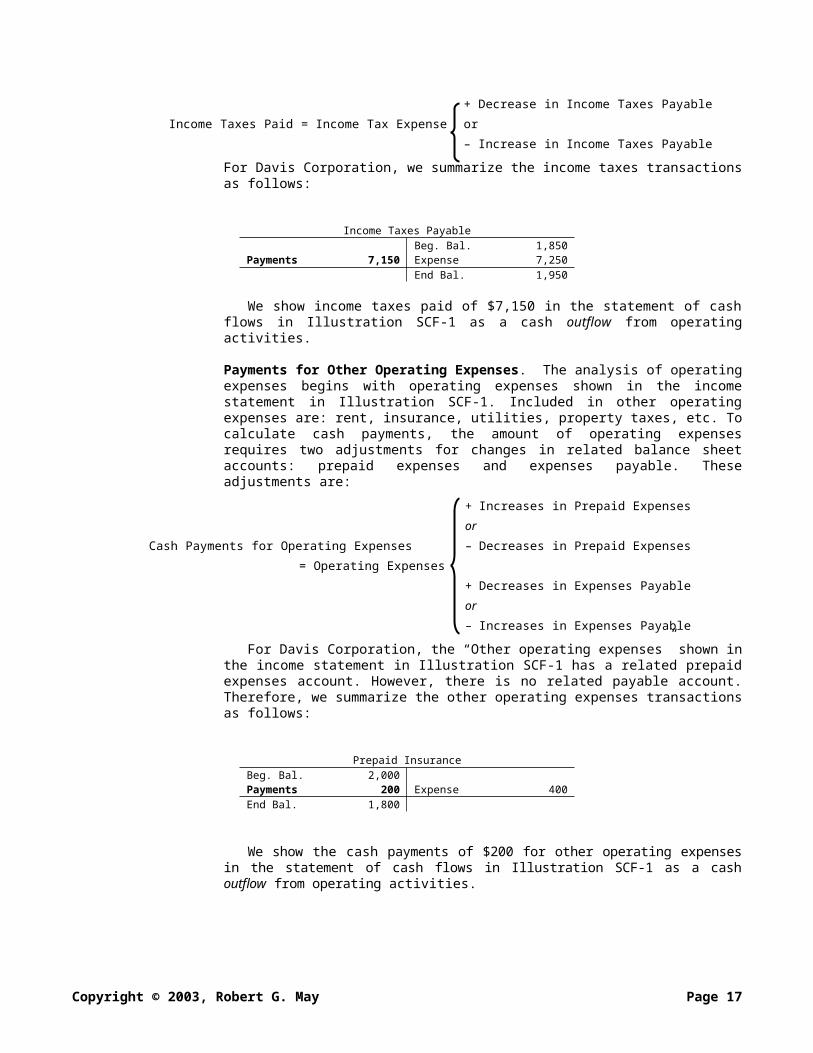

Income Taxes Paid. The analysis of income taxes paid is similar to the analyses of cash payments for wages and salaries and interest payments. We adjust the amount of income tax expense for any change in income taxes payable as follows:

+ Decrease in Income Taxes Payable

Income Taxes Paid = Income Tax Expense or

– Increase in Income Taxes Payable

For Davis Corporation, we summarize the income taxes transactions as follows:

Copyright © 2003, Robert G. May Page 14

Income Taxes PayableBeg. Bal. 1,850

Payments 7,150 Expense 7,250End Bal. 1,950

We show income taxes paid of $7,150 in the statement of cash flows in Illustration SCF-1 as a cash outflow from operating activities.

Payments for Other Operating Expenses. The analysis of operating expenses begins with operating expenses shown in the income statement in Illustration SCF-1. Included in other operating expenses are: rent, insurance, utilities, property taxes, etc. To calculate cash payments, the amount of operating expenses requires two adjustments for changes in related balance sheet accounts: prepaid expenses and expenses payable. These adjustments are:

+ Increases in Prepaid Expenses

or

Cash Payments for Operating Expenses – Decreases in Prepaid Expenses

= Operating Expenses

+ Decreases in Expenses Payable

or

– Increases in Expenses Payable

For Davis Corporation, the “Other operating expenses” shown in the income statement in Illustration SCF-1 has a related prepaid expenses account. However, there is no related payable account. Therefore, we summarize the other operating expenses transactions as follows:

Prepaid InsuranceBeg. Bal. 2,000Payments 200 Expense 400End Bal. 1,800

We show the cash payments of $200 for other operating expenses in the statement of cash flows in Illustration SCF-1 as a cash outflow from operating activities.

Elements of the Income Statement Unrelated to Operating Cash Flows

If you review the income statement in Illustration SCF-1, you will note that we have not used all of its components to construct cash flows from operations. In particular, we have not used the gain from sale of property (land) and the two depreciation expense amounts.

Gain From Sale of Property (Land). Gains and losses that appear in the financial statements may be associated with investing and financing activities. For example, a loss on the early retirement of corporate debt is a financing loss that tells us the cash paid to retire the debt exceeded its

Copyright © 2003, Robert G. May Page 15

carrying value. Each gain or loss must be analyzed separately and associated with the correct cash-flow activity. In the Davis Corporation example, the income statement shows a gain on sale property (land) of $3,000. Thus, we know that land was sold for $3,000 more than its carrying value and a gain (income) was earned on the sale. The gain from the sale of land is not analyzed in determining cash flows from operating activities because we classify cash received from the sale of plant assets as an investing activity (as shown in Illustration SCF-4). We analyze this gain below in the discussion of investing activities.

Income Statement Items Unrelated to Cash Transactions. Depreciation expense is another matter. Depreciation does relate to operations, but it does not relate to cash expended. The cash expended or received for plant and equipment is expended or received in connection with its acquisition and disposition, respectively. These are investment activities. Depreciation represents the use of the plant and equipment in operations and, while it appears in the income statement, it is unrelated to cash. Some other non-cash components of income that you will see in corporate income statements are deferred tax expense and equity in the earnings of unconsolidated affiliated companies. You need not worry now about the details of these expense and income items, just be aware that they exist.

Cash Flows From Investing Activities

The statement of cash flows in Illustration SCF-1 shows that in 20X2, Davis Corporation had three cash flows resulting from investing activities.

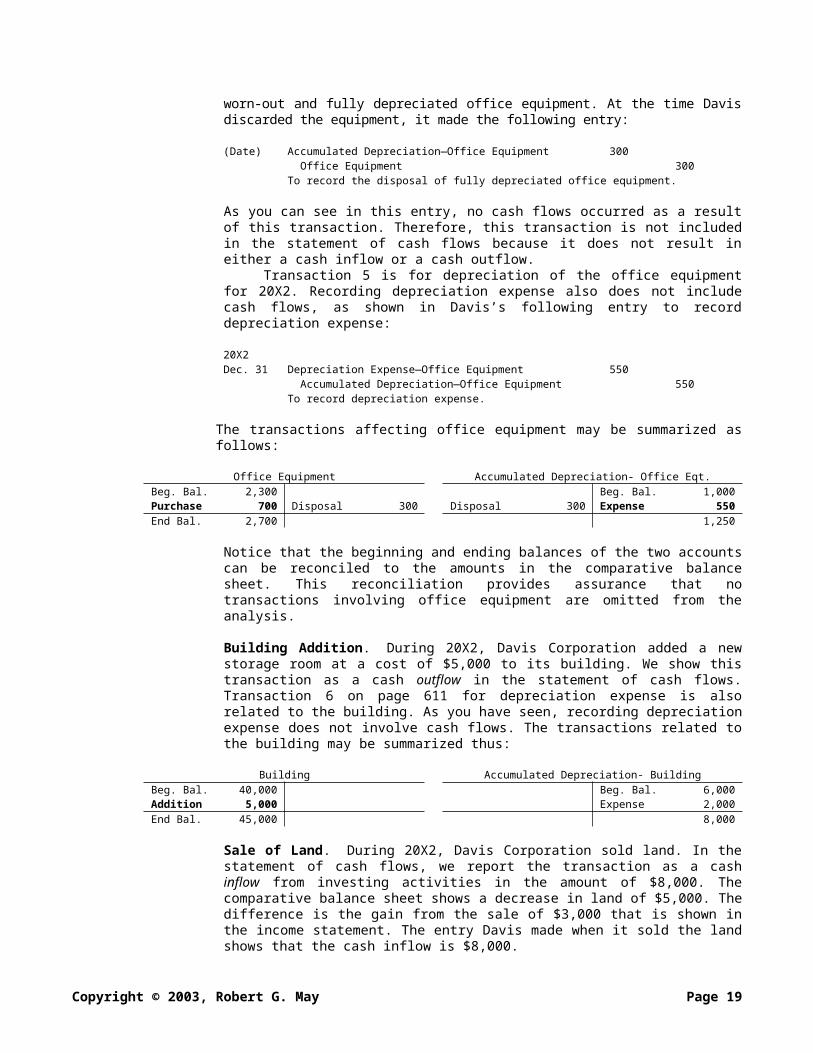

Purchase of Office Equipment. During 20X2, Davis Corporation purchased new office equipment at a cost of $700. In the statement of cash flows, this amount is shown as a cash outflow from investing activities. The listing of information obtained from analyzing the accounts, however, shows that office equipment was affected by three transactions described in Items 2, 3 and 5 at the beginning of this illustration. Transaction 2 is the purchase of new office equipment described above, and Transaction 3 is the discarding of worn-out and fully depreciated office equipment. At the time Davis discarded the equipment, it made the following entry:

(Date) Accumulated Depreciation—Office Equipment 300 Office Equipment 300To record the disposal of fully depreciated office equipment.

As you can see in this entry, no cash flows occurred as a result of this transaction. Therefore, this transaction is not included in the statement of cash flows because it does not result in either a cash inflow or a cash outflow.

Transaction 5 is for depreciation of the office equipment for 20X2. Recording depreciation expense also does not include cash flows, as shown in Davis’s following entry to record depreciation expense:

Copyright © 2003, Robert G. May Page 16

20X2Dec. 31 Depreciation Expense—Office Equipment 550

Accumulated Depreciation—Office Equipment 550To record depreciation expense.

The transactions affecting office equipment may be summarized as follows:

Office Equipment Accumulated Depreciation- Office Eqt.Beg. Bal. 2,300 Beg. Bal. 1,000Purchase 700 Disposal 300 Disposal 300 Expense 550End Bal. 2,700 1,250

Notice that the beginning and ending balances of the two accounts can be reconciled to the amounts in the comparative balance sheet. This reconciliation provides assurance that no transactions involving office equipment are omitted from the analysis.

Building Addition. During 20X2, Davis Corporation added a new storage room at a cost of $5,000 to its building. We show this transaction as a cash outflow in the statement of cash flows. Transaction 6 on page 611 for depreciation expense is also related to the building. As you have seen, recording depreciation expense does not involve cash flows. The transactions related to the building may be summarized thus:

Building Accumulated Depreciation- BuildingBeg. Bal. 40,000 Beg. Bal. 6,000Addition 5,000 Expense 2,000End Bal. 45,000 8,000

Sale of Land. During 20X2, Davis Corporation sold land. In the statement of cash flows, we report the transaction as a cash inflow from investing activities in the amount of $8,000. The comparative balance sheet shows a decrease in land of $5,000. The difference is the gain from the sale of $3,000 that is shown in the income statement. The entry Davis made when it sold the land shows that the cash inflow is $8,000.

(Date) Cash 8,000 Land 5,000 Gain from Sale of Property 3,000To record the sale of property.

The transaction involving land is shown in the accounts as follows:

LandBeg. Bal. 35,000 Sale 5,000End Bal. 30,000

Cash Flows From Financing Activities

For 20X2, Davis Corporation reports four cash flow transactions from financing activities.

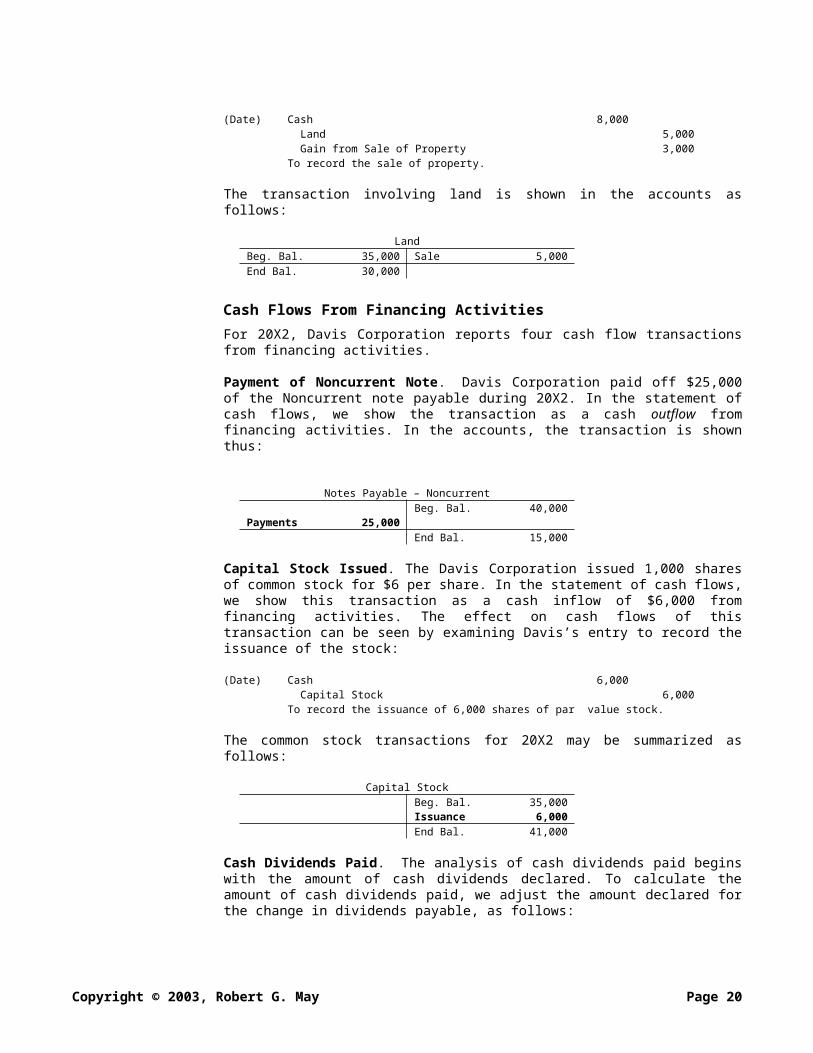

Payment of Noncurrent Note. Davis Corporation paid off $25,000 of the Noncurrent note payable during 20X2. In the statement of cash flows, we show the transaction as a cash outflow from financing activities. In the accounts, the transaction is shown thus:

Copyright © 2003, Robert G. May Page 17

Notes Payable – NoncurrentBeg. Bal. 40,000

Payments 25,000End Bal. 15,000

Capital Stock Issued. The Davis Corporation issued 1,000 shares of common stock for $6 per share. In the statement of cash flows, we show this transaction as a cash inflow of $6,000 from financing activities. The effect on cash flows of this transaction can be seen by examining Davis’s entry to record the issuance of the stock:

(Date) Cash 6,000 Capital Stock 6,000To record the issuance of 6,000 shares of par value stock.

The common stock transactions for 20X2 may be summarized as follows:

Capital StockBeg. Bal. 35,000Issuance 6,000End Bal. 41,000

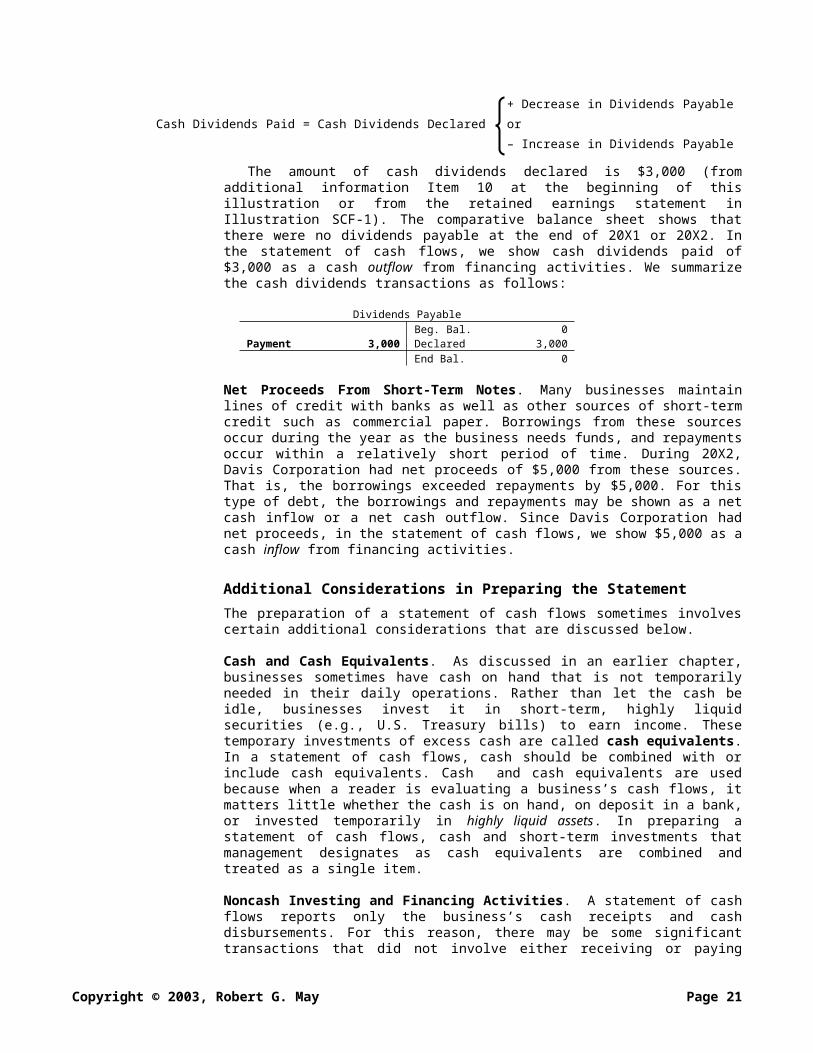

Cash Dividends Paid. The analysis of cash dividends paid begins with the amount of cash dividends declared. To calculate the amount of cash dividends paid, we adjust the amount declared for the change in dividends payable, as follows:

+ Decrease in Dividends Payable

Cash Dividends Paid = Cash Dividends Declared or

– Increase in Dividends Payable

The amount of cash dividends declared is $3,000 (from additional information Item 10 at the beginning of this illustration or from the retained earnings statement in Illustration SCF-1). The comparative balance sheet shows that there were no dividends payable at the end of 20X1 or 20X2. In the statement of cash flows, we show cash dividends paid of $3,000 as a cash outflow from financing activities. We summarize the cash dividends transactions as follows:

Dividends PayableBeg. Bal. 0

Payment 3,000 Declared 3,000End Bal. 0

Net Proceeds From Short-Term Notes. Many businesses maintain lines of credit with banks as well as other sources of short-term credit such as commercial paper. Borrowings from these sources occur during the year as the business needs funds, and repayments occur within a relatively short period of time. During 20X2, Davis Corporation had net proceeds of $5,000 from these sources. That is, the borrowings exceeded repayments by $5,000. For this type of debt, the borrowings and repayments may be shown as a net cash inflow or a net cash outflow. Since Davis Corporation had net proceeds, in the statement of cash flows, we show $5,000 as a cash inflow from financing activities.

Copyright © 2003, Robert G. May Page 18

Additional Considerations in Preparing the Statement

The preparation of a statement of cash flows sometimes involves certain additional considerations that are discussed below.

Cash and Cash Equivalents. As discussed in an earlier chapter, businesses sometimes have cash on hand that is not temporarily needed in their daily operations. Rather than let the cash be idle, businesses invest it in short-term, highly liquid securities (e.g., U.S. Treasury bills) to earn income. These temporary investments of excess cash are called cash equivalents. In a statement of cash flows, cash should be combined with or include cash equivalents. Cash and cash equivalents are used because when a reader is evaluating a business’s cash flows, it matters little whether the cash is on hand, on deposit in a bank, or invested temporarily in highly liquid assets. In preparing a statement of cash flows, cash and short-term investments that management designates as cash equivalents are combined and treated as a single item.

Noncash Investing and Financing Activities. A statement of cash flows reports only the business’s cash receipts and cash disbursements. For this reason, there may be some significant transactions that did not involve either receiving or paying cash. Some common examples of noncash investing and financing transactions include the following:

1. Acquiring assets by assuming liabilities. A business may purchase land and buildings by assuming a mortgage payable.

2. Acquiring assets by issuing stock. A company may purchase assets such as plant assets and intangible assets by issuing preferred or common stock directly to the seller.

3. Exchanges of non-monetary assets. Companies commonly trade one asset to another company or individual for a more desirable asset.

4. Issuance of stock to repay loans. A company may repay a loan by issuing preferred or common stock to the creditor.

To present a complete picture of the business’s investing and financing activities, significant noncash investing and financing transactions are presented in a separate schedule following the statement of cash flows or in the notes to the financial statements. Other noncash transactions such as stock dividends, stock splits, and appropriations of retained earnings are neither investing nor financing activities and are not reported in the schedule of noncash investing and financing activities. Information about these noncash transactions is generally reported in the retained earnings statement or in schedules and notes explaining changes in stockholders’ equity.

LO 5 ALTERNATIVE PRESENTATION OF CASHFLOWS FROM OPERATING ACTIVITIES

Although the direct method of representing cash flows from operations illustrated above is the preferred method, most companies actually use an indirect method. The indirect method of reporting cash flows from operating activities begins with net income and adjusts for items that are

Copyright © 2003, Robert G. May Page 19

included in net income but do not affect cash flows from operating activities. There are three types of adjustments to net income.

Noncash Expenses

Certain expenses that are included in net income do not result in a cash outflow. The primary noncash expenses are depreciation and amortization. The offsetting entry for these expenses is to an accumulated depreciation account and to an intangible asset account, respectively. The cash flows associated with these transactions occur at the time of purchase and disposal of the related assets and are classified then as investing activities.

Adjustments to Convert Revenues and Expenses to the Cash Basis

Revenues and expenses are recognized on the accrual basis at times that may be different than the time of the related cash flows. The adjustments to net income for these items involve analyzing changes in receivables, inventories, prepaid expenses, and payables that are related to revenues and expenses.

Nonoperating Items

Gains and losses from investing and financing transactions are included in net income, but the transactions are not considered operating activities. These gains and losses are from disposals of non-current assets and settlements of long-term liabilities. These transactions are considered investing and financing activities. Therefore, the gains and losses associated with these transactions should be removed from net income in calculating cash flows from operating activities.

The Indirect Method—An Illustration

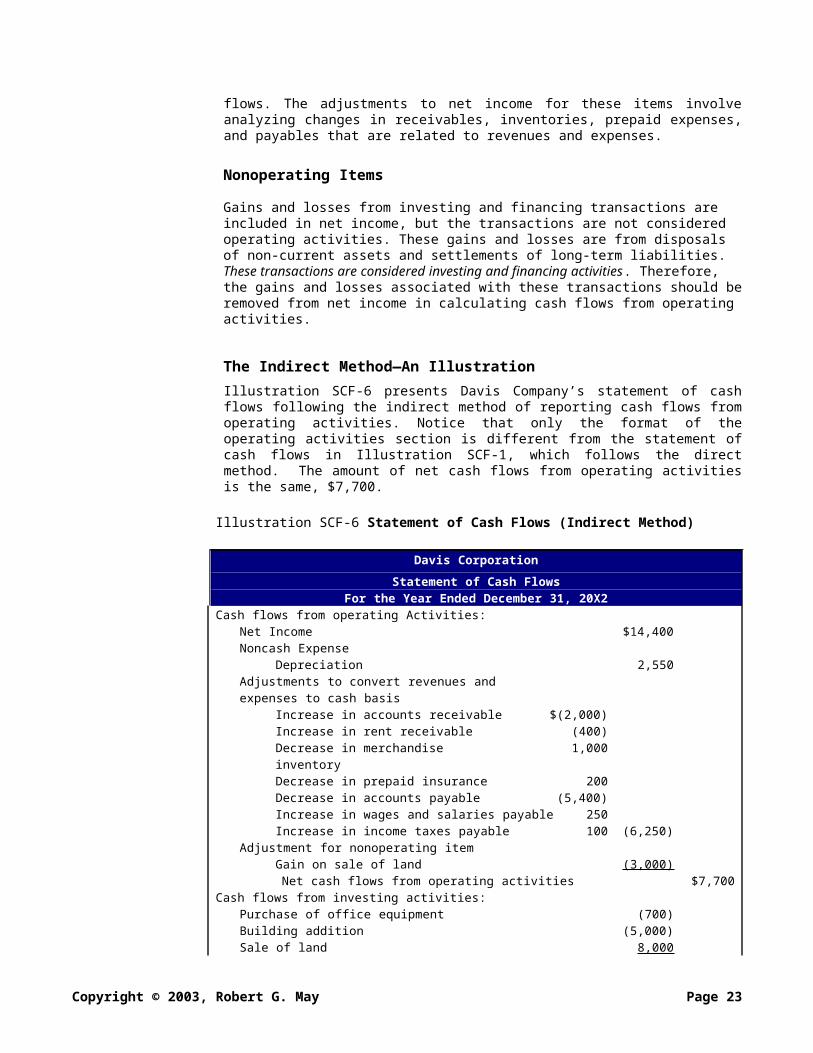

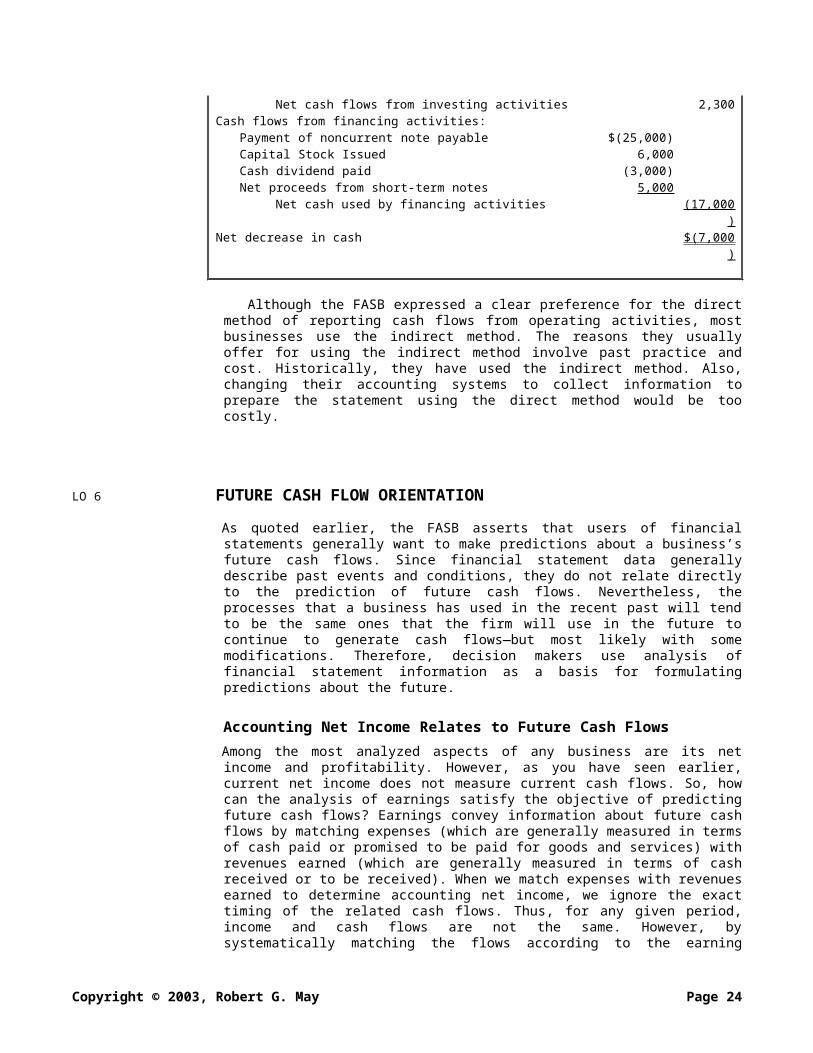

Illustration SCF-6 presents Davis Company’s statement of cash flows following the indirect method of reporting cash flows from operating activities. Notice that only the format of the operating activities section is different from the statement of cash flows in Illustration SCF-1, which follows the direct method. The amount of net cash flows from operating activities is the same, $7,700.

Illustration SCF-6 Statement of Cash Flows (Indirect Method)

Davis Corporation

Statement of Cash FlowsFor the Year Ended December 31, 20X2

Cash flows from operating Activities:Net Income $14,400Noncash Expense

Depreciation 2,550Adjustments to convert revenues and expenses to cash basis

Increase in accounts receivable $(2,000)Increase in rent receivable (400)

Copyright © 2003, Robert G. May Page 20

Decrease in merchandise inventory

1,000

Decrease in prepaid insurance 200Decrease in accounts payable (5,400)Increase in wages and salaries payable 250Increase in income taxes payable 100 (6,250)

Adjustment for nonoperating itemGain on sale of land (3,000)

Net cash flows from operating activities $7,700Cash flows from investing activities:

Purchase of office equipment (700)Building addition (5,000)Sale of land 8,000

Net cash flows from investing activities 2,300Cash flows from financing activities:

Payment of noncurrent note payable $(25,000)Capital Stock Issued 6,000Cash dividend paid (3,000)Net proceeds from short-term notes 5,000

Net cash used by financing activities (17,000)

Net decrease in cash $(7,000)

Although the FASB expressed a clear preference for the direct method of reporting cash flows from operating activities, most businesses use the indirect method. The reasons they usually offer for using the indirect method involve past practice and cost. Historically, they have used the indirect method. Also, changing their accounting systems to collect information to prepare the statement using the direct method would be too costly.

LO 6 FUTURE CASH FLOW ORIENTATION

As quoted earlier, the FASB asserts that users of financial statements generally want to make predictions about a business’s future cash flows. Since financial statement data generally describe past events and conditions, they do not relate directly to the prediction of future cash flows. Nevertheless, the processes that a business has used in the recent past will tend to be the same ones that the firm will use in the future to continue to generate cash flows—but most likely with some modifications. Therefore, decision makers use analysis of financial statement information as a basis for formulating predictions about the future.

Accounting Net Income Relates to Future Cash Flows

Among the most analyzed aspects of any business are its net income and profitability. However, as you have seen earlier, current net income does not measure current cash flows. So, how can the analysis of earnings satisfy the objective of predicting future cash flows? Earnings convey information about future cash flows by matching expenses (which are generally measured in terms of cash paid or promised to be paid for goods and services) with revenues earned (which are generally measured in terms of cash received

Copyright © 2003, Robert G. May Page 21

or to be received). When we match expenses with revenues earned to determine accounting net income, we ignore the exact timing of the related cash flows. Thus, for any given period, income and cash flows are not the same. However, by systematically matching the flows according to the earning process, earnings tend to convey the long-run (average) cash-generating ability of the current earning process.

In fact, we can make the following generalizations about cash flows and net income:1. Over the life of a business, accounting net income equals cash flows from

all sources, except borrowings and repayments of debt and transactions with owners. In other words, lifetime income approximately equals cash flows from operations and investment activities—the cash flows the business generates for itself (not from owners and creditors).

2. Therefore, over the life of the business, average income (per period) approximately equals average cash flows from operations and investment activities. In other words, average income is an approximation of average cash flows per period.

3. If a business continues in operation indefinitely, providing the same volume of goods and services at the same prices and using the same inputs at the same prices, current income is an approximation of the average net cash flows per period the business will generate in the future.This latter concept may seem naive, since the future is never the same

as the present or past. Yet, financial statement analysts can directly build on this concept to forecast the future. First, the analyst will want to evaluate net income to determine how well it approximates steady-state future cash flows. We call this the income persistence problem. Next, the analyst may wish to judge the net income for any bias management introduces by choosing particular accounting principles and methods. We call this the income quality problem. Finally, the analyst must predict how a particular firm’s future will be different from its past and adjust net income to achieve a better prediction of the actual (non-steady-state) future. Thus, successful analysts, who are able to produce the best forecasts, are the ones who have the best insight into the future.

Persistence and Quality of Income

In this course, we cannot cover all there is to know about forecasting a company’s future. We can, however, teach you the concepts an analyst needs to form the platform for a forecast of future earnings and cash flows. Income persistence is the tendency for a component of income to continue in future periods under steady-state (no change) assumptions. Income quality is the degree to which management does not exercise or does not have the opportunity to manipulate the firm’s income to paint an optimistic picture of ongoing income.

Income Persistence. Income statements are formatted to segregate income components or segments with regard to their persistence. That is, such components of income as gains and losses, income (loss) from discontinued operations, so-called extraordinary items, and the effects of certain accounting changes are clearly identified separately from regular revenues and expenses in corporate income statements. This alerts analysts to treat them differently in thinking about the base-lines for forecasts of future income and cash flows.

Copyright © 2003, Robert G. May Page 22

Quality of Income. Quality of income is much spoken about among financial analysts, but it is difficult to describe concisely how to analyze it. One thing is clear, however. If management tries to manipulate the amount of net income, analysts cannot rely on the net income figure to the same extent that they could if management remained neutral. How can management manipulate income? In a surprising variety of ways. First, management can select among GAAP those principles that produce the desired effect on income but do not fit the circumstances as well as other principles. In later chapters you will see many cases of alternative ways of accounting for the same assets, liabilities, revenues and expenses. Each of management’s choices, if not the most appropriate in the circumstances, may bias net income. Second, management makes numerous estimates and judgments in applying GAAP. For example, management ultimately is responsible for estimating the useful lives of plant assets. Management can systematically over- and underestimate in the directions that have desired effects on income. Finally, management can engage in outright fraud or deception. The most common intentional deception in financial reporting is overstating revenues. Methods range from recording the subsequent year’s sales early—as revenue of the current year—to shipping goods before year-end to customers that did not order them (and recording the sales returns in the subsequent year when the goods are returned).

The difficulty in analyzing quality of income is that, if management is manipulating income, they do not openly disclose their actions. In the financial reports of companies, notes to the financial statements disclose the accounting methods and many of the estimates used—but often only in broad terms. However, professional analysts follow companies for years, observe the judgments that their managers make, and compare them to peer firms and their managers. Over time, companies gain reputations for high or low quality earnings and analysts make adjustments accordingly.

Keep in mind these dual qualities of earnings—persistence and quality—as we examine various accounting principles to handle the great variety of business transactions and events. Keep in mind as well, the relationship between accounting net income and cash flows.

SUMMARY

Explain the purpose of a statement of cash flows. The primary purpose of a statement of cash flows is to provide information about the business’s cash receipts and cash disbursements during a period. A secondary objective of the statement is to provide information about the business’s investing and financing activities during a period. Classifying cash flows in the statement into categories of operating, investing, and financing activities serve these two purposes.

Describe the operating, investing, and financing classifications of cash flow activities. Cash receipts and cash disbursements from operating activities are the cash effects of revenue and expense transactions. Investing activities include transactions that involve acquiring and disposing of productive assets, investing in securities, and investing in intangible assets. Financing activities include transactions with stockholders (owners) and creditors.

Copyright © 2003, Robert G. May Page 23

Explain how to prepare a statement of cash flows. To prepare a statement of cash flows, accountants analyze the accounts to identify the cash receipts and cash disbursements associated with operating, investing, and financing activities. The information accountants use includes comparative balance sheets, income statements, and additional information from the business’s accounts.Analyze accrual basis accounting information to determine the effects on cash flows. In preparing the statement of cash flows, we adjust income statement amounts for the differences between the timing of related cash flows and the timing of revenue and expense recognition under accrual accounting.

Describe the indirect method of reporting cash flows from operating activities. The indirect method begins with net income and adjusts for items that are included in net income but did not affect cash flows from operating activities. These adjustments are for noncash expenses, adjustments to convert revenues and expenses to the cash basis, and nonoperating items.

Describe the relationship between accounting income and cash flows and the concepts of quality and persistence of earnings. Over the life of a business, accounting net income equals cash flows from all sources, except borrowings and repayments of debt and transactions with owners. In other words, lifetime income approximately equals cash flows from operations and investment activities—the cash flows the business generates for itself (not from owners and creditors). Persistence of earnings refers to the degree that various components of income such as gains and losses will tend to repeat themselves in the future. Quality of earnings refers to the possible bias in earnings introduced by management’s choice among GAAP and systematic under and overestimation in the application of GAAP.

APPENDIX SCF-A: USING A WORKSHEET TO PREPARE THE STATEMENT OF CASH FLOW

For complex situations involving numerous adjustments, accountants also use a worksheet to facilitate the preparation of the statement of cash flows. In this Appendix, we give a comprehensive example to illustrate the use of a worksheet for preparing a statement of cash flows. The worksheet we demonstrate is for the indirect method for cash flows from operating activities. We chose this approach because of its widespread use in the business world. A similar worksheet method could be used for the direct method.

LO 6 PREPARING THE WORKSHEET

The worksheet used to prepare Davis Corporation’s statement of cash flows is presented in Illustration SCF-7. The worksheet consists of nine columns. The first column lists the names of the accounts and changes in cash. The remaining eight columns list the dollar amounts of the account balances, their changes and letter references to link related changes. The worksheet

Copyright © 2003, Robert G. May Page 24

simply consolidates the balance sheet T-accounts into one place, with each line across representing a horizontal T-account. We use the following steps in preparing the worksheet:

1. Enter the beginning balances of the balance sheet accounts in the first two debit-credit columns, and enter the ending balances in the last two debit-credit columns.

2. Note that we have left many lines between the entry for the beginning cash balance and the ending cash balance where we have, in effect, built the cash-flow statement. You should start out leaving these lines blank and then gradually fill them as you do the analysis of non-cash accounts.

3. After entering the account balances, sum the debits and credits to make sure that they are equal. If the debits and credits are not equal, you have made an error in entering the data in the worksheet. Before proceeding, locate and correct the error(s).

4. Enter relevant components of the changes in accounts in the Account Analysis columns. These entries (1) represent changes in the account balances and (2) allow the determination of cash flows from operating, investing, and financing activities, which are listed at the top of the worksheet. Recall that any credit change to a non-cash account balance is a possible increase in cash and any debit is a possible decrease in cash. For some changes in account balances, more than one entry is necessary to explain the change. For example, in Illustration SCF-7, two entries are needed to explain the $400 increase in office equipment: (1) a $700 debit (Entry f) and (2) a $300 credit (Entry g). Notice that the two entries net to a $400 debit, which explains the $400 increase in office equipment from a balance of $2,300 at December 31, 20X1, to $2,700 at December 31, 20X2. Remember: The data for the entries come from the income statement, statement of retained earnings, supplemental information and analysis of the general ledger accounts.

The entries on the worksheet summarize the effects of the various transactions that changed the account balances during the period. For example, Entry (g) is a debit to Accumulated Depreciation—Office Equipment and a credit to Office Equipment. For every entry representing a change in one account balance, there is an offsetting entry (or entries) to other accounts of equal amount. Some of these offsetting entries involve an increase or a decrease in cash. In those cases, we enter the changes in cash in the available lines at the top of the worksheet in the proper activity category of the statement of cash flows. It is helpful to use a computer spreadsheet program to implement the worksheet because you will be able to adjust the number of rows explaining the change in cash to accommodate the operating, investing and financing cash-flow format..

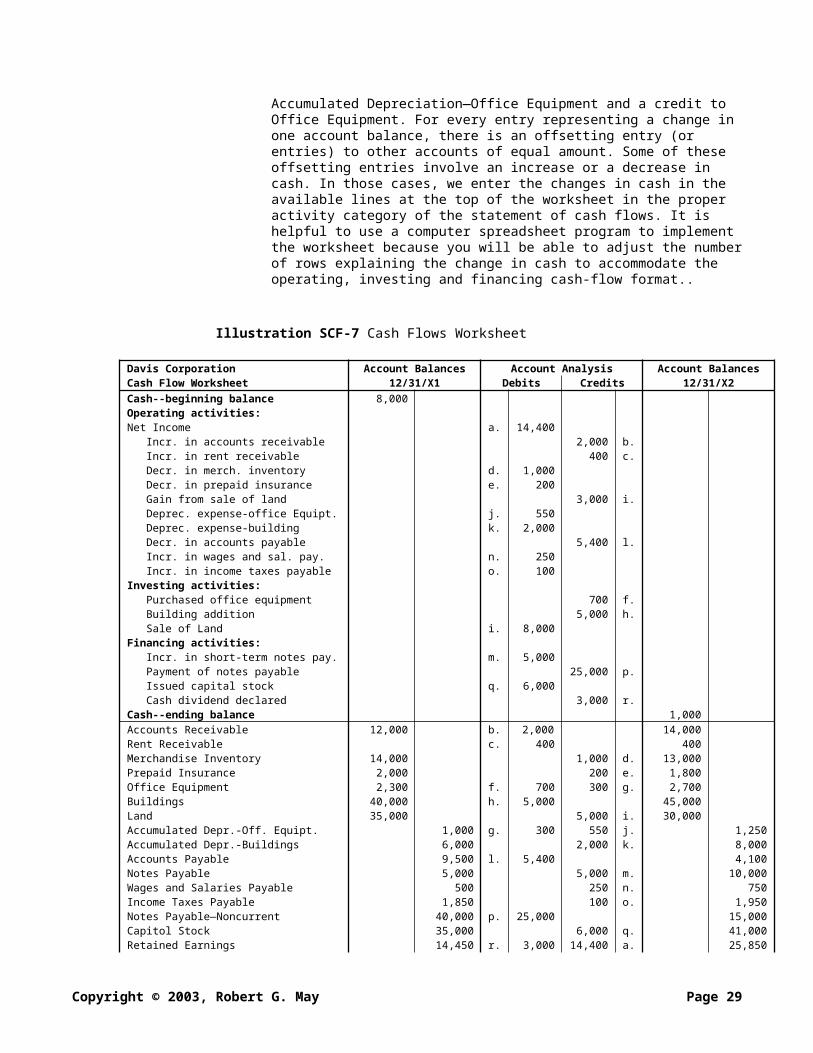

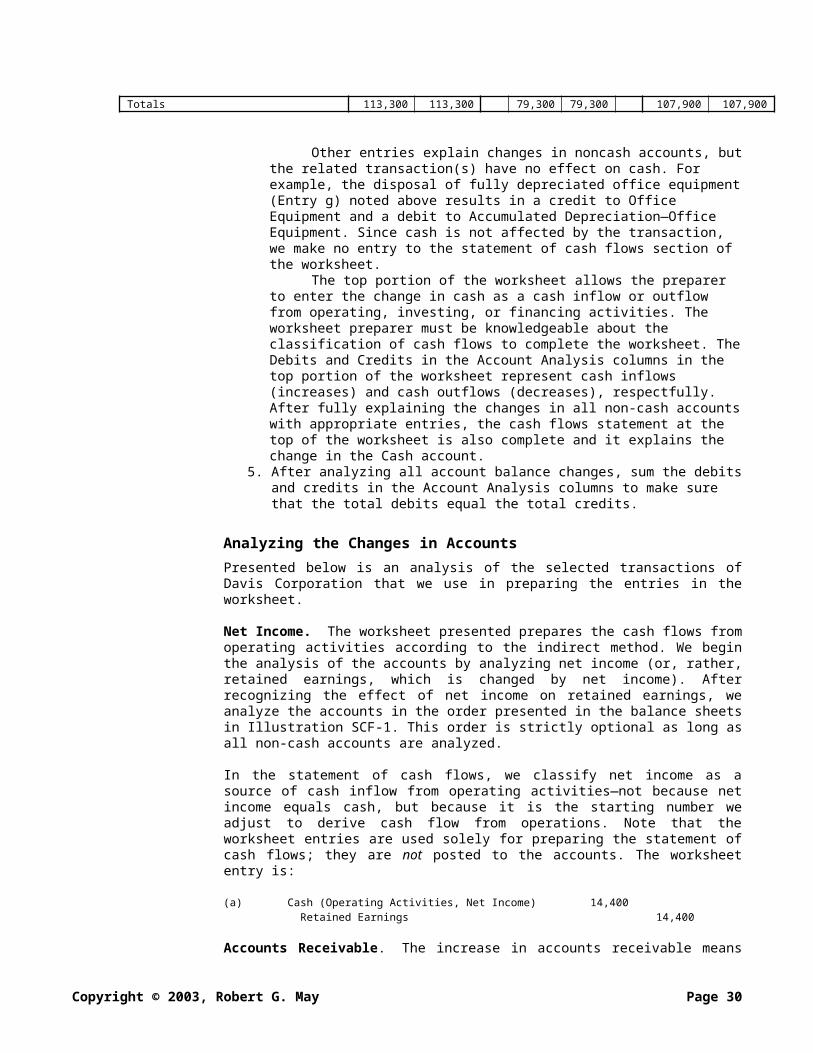

Illustration SCF-7 Cash Flows Worksheet

Davis Corporation Account Balances Account Analysis Account BalancesCash Flow Worksheet 12/31/X1 Debits Credits 12/31/X2Cash--beginning balance 8,000 Operating activities: Net Income a. 14,400 Incr. in accounts receivable 2,000 b. Incr. in rent receivable 400 c.

Copyright © 2003, Robert G. May Page 25

Decr. in merch. inventory d. 1,000 Decr. in prepaid insurance e. 200 Gain from sale of land 3,000 i. Deprec. expense-office Equipt. j. 550 Deprec. expense-building k. 2,000 Decr. in accounts payable 5,400 l. Incr. in wages and sal. pay. n. 250 Incr. in income taxes payable o. 100 Investing activities: Purchased office equipment 700 f. Building addition 5,000 h. Sale of Land i. 8,000 Financing activities: Incr. in short-term notes pay. m. 5,000 Payment of notes payable 25,000 p. Issued capital stock q. 6,000 Cash dividend declared 3,000 r. Cash--ending balance 1,000 Accounts Receivable 12,000 b. 2,000 14,000 Rent Receivable c. 400 400 Merchandise Inventory 14,000 1,000 d. 13,000 Prepaid Insurance 2,000 200 e. 1,800 Office Equipment 2,300 f. 700 300 g. 2,700 Buildings 40,000 h. 5,000 45,000 Land 35,000 5,000 i. 30,000 Accumulated Depr.-Off. Equipt. 1,000 g. 300 550 j. 1,250Accumulated Depr.-Buildings 6,000 2,000 k. 8,000Accounts Payable 9,500 l. 5,400 4,100Notes Payable 5,000 5,000 m. 10,000Wages and Salaries Payable 500 250 n. 750Income Taxes Payable 1,850 100 o. 1,950Notes Payable—Noncurrent 40,000 p. 25,000 15,000Capitol Stock 35,000 6,000 q. 41,000Retained Earnings 14,450 r. 3,000 14,400 a. 25,850Totals 113,300 113,300 79,300 79,300 107,900 107,900

Other entries explain changes in noncash accounts, but the related transaction(s) have no effect on cash. For example, the disposal of fully depreciated office equipment (Entry g) noted above results in a credit to Office Equipment and a debit to Accumulated Depreciation—Office Equipment. Since cash is not affected by the transaction, we make no entry to the statement of cash flows section of the worksheet.

The top portion of the worksheet allows the preparer to enter the change in cash as a cash inflow or outflow from operating, investing, or financing activities. The worksheet preparer must be knowledgeable about the classification of cash flows to complete the worksheet. The Debits and Credits in the Account Analysis columns in the top portion of the worksheet represent cash inflows (increases) and cash outflows (decreases), respectfully. After fully explaining the changes in all non-cash accounts with appropriate entries, the cash flows statement at the top of the worksheet is also complete and it explains the change in the Cash account.

5. After analyzing all account balance changes, sum the debits and credits in the Account Analysis columns to make sure that the total debits equal the total credits.

Analyzing the Changes in Accounts

Presented below is an analysis of the selected transactions of Davis Corporation that we use in preparing the entries in the worksheet.

Copyright © 2003, Robert G. May Page 26

Net Income. The worksheet presented prepares the cash flows from operating activities according to the indirect method. We begin the analysis of the accounts by analyzing net income (or, rather, retained earnings, which is changed by net income). After recognizing the effect of net income on retained earnings, we analyze the accounts in the order presented in the balance sheets in Illustration SCF-1. This order is strictly optional as long as all non-cash accounts are analyzed.

In the statement of cash flows, we classify net income as a source of cash inflow from operating activities—not because net income equals cash, but because it is the starting number we adjust to derive cash flow from operations. Note that the worksheet entries are used solely for preparing the statement of cash flows; they are not posted to the accounts. The worksheet entry is:

(a) Cash (Operating Activities, Net Income) 14,400 Retained Earnings 14,400

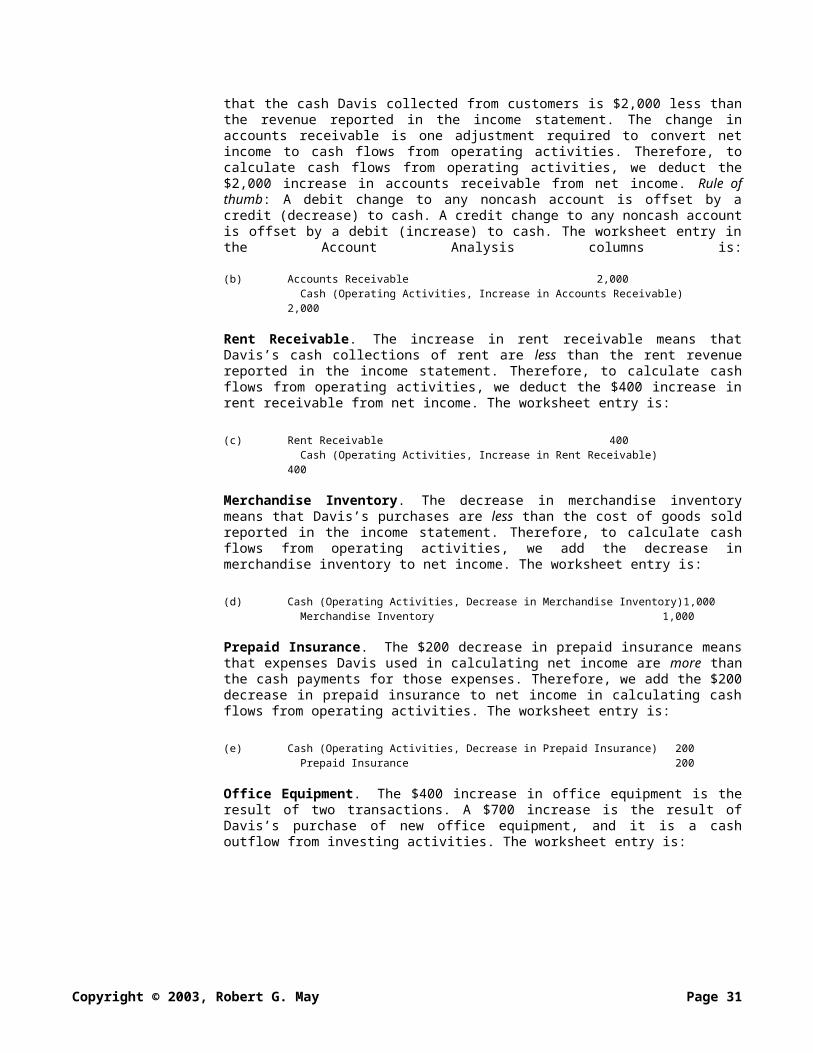

Accounts Receivable. The increase in accounts receivable means that the cash Davis collected from customers is $2,000 less than the revenue reported in the income statement. The change in accounts receivable is one adjustment required to convert net income to cash flows from operating activities. Therefore, to calculate cash flows from operating activities, we deduct the $2,000 increase in accounts receivable from net income. Rule of thumb: A debit change to any noncash account is offset by a credit (decrease) to cash. A credit change to any noncash account is offset by a debit (increase) to cash. The worksheet entry in the Account Analysis columns is:

(b) Accounts Receivable 2,000 Cash (Operating Activities, Increase in Accounts Receivable) 2,000

Rent Receivable. The increase in rent receivable means that Davis’s cash collections of rent are less than the rent revenue reported in the income statement. Therefore, to calculate cash flows from operating activities, we deduct the $400 increase in rent receivable from net income. The worksheet entry is:

(c) Rent Receivable 400 Cash (Operating Activities, Increase in Rent Receivable) 400

Merchandise Inventory. The decrease in merchandise inventory means that Davis’s purchases are less than the cost of goods sold reported in the income statement. Therefore, to calculate cash flows from operating activities, we add the decrease in merchandise inventory to net income. The worksheet entry is:

(d) Cash (Operating Activities, Decrease in Merchandise Inventory)1,000 Merchandise Inventory 1,000

Prepaid Insurance. The $200 decrease in prepaid insurance means that expenses Davis used in calculating net income are more than the cash payments for those expenses. Therefore, we add the $200 decrease in

Copyright © 2003, Robert G. May Page 27

prepaid insurance to net income in calculating cash flows from operating activities. The worksheet entry is:

(e) Cash (Operating Activities, Decrease in Prepaid Insurance) 200 Prepaid Insurance 200

Office Equipment. The $400 increase in office equipment is the result of two transactions. A $700 increase is the result of Davis’s purchase of new office equipment, and it is a cash outflow from investing activities. The worksheet entry is:

(f) Office Equipment 700 Cash (Investing Activities, Purchase of Office Equipment) 700

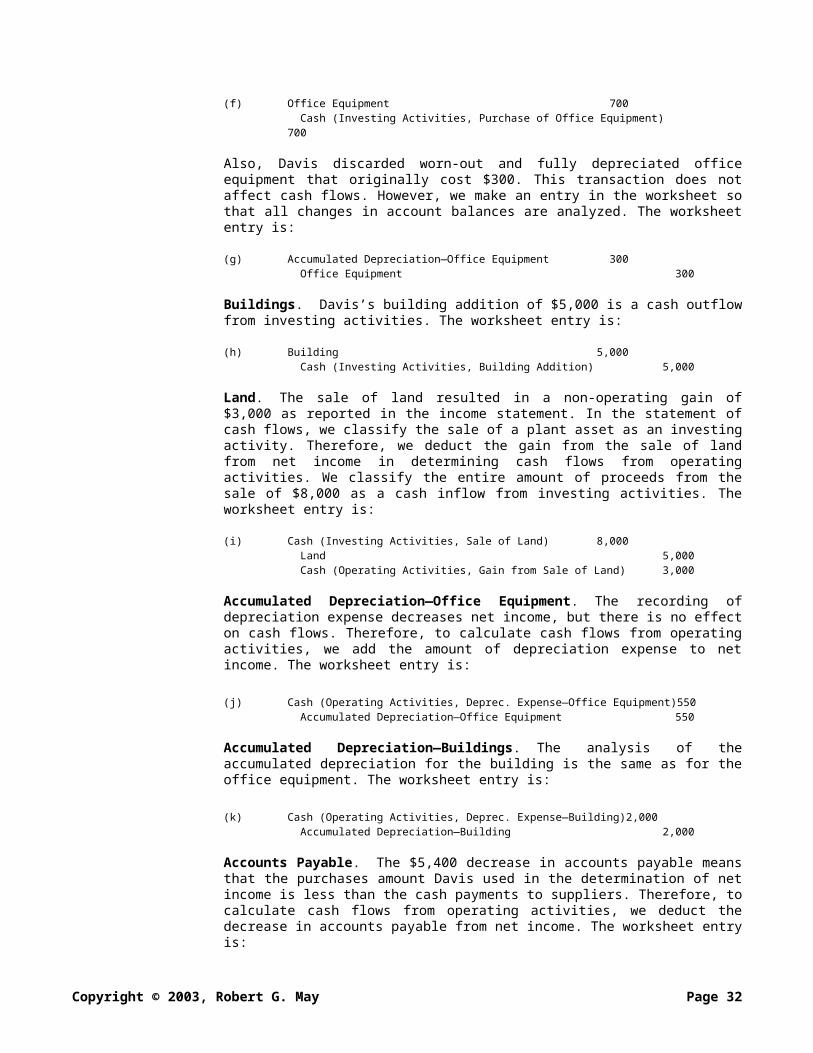

Also, Davis discarded worn-out and fully depreciated office equipment that originally cost $300. This transaction does not affect cash flows. However, we make an entry in the worksheet so that all changes in account balances are analyzed. The worksheet entry is:

(g) Accumulated Depreciation—Office Equipment 300 Office Equipment 300

Buildings. Davis’s building addition of $5,000 is a cash outflow from investing activities. The worksheet entry is:

(h) Building 5,000 Cash (Investing Activities, Building Addition) 5,000

Land. The sale of land resulted in a non-operating gain of $3,000 as reported in the income statement. In the statement of cash flows, we classify the sale of a plant asset as an investing activity. Therefore, we deduct the gain from the sale of land from net income in determining cash flows from operating activities. We classify the entire amount of proceeds from the sale of $8,000 as a cash inflow from investing activities. The worksheet entry is:

(i) Cash (Investing Activities, Sale of Land) 8,000 Land 5,000 Cash (Operating Activities, Gain from Sale of Land) 3,000

Accumulated Depreciation—Office Equipment. The recording of depreciation expense decreases net income, but there is no effect on cash flows. Therefore, to calculate cash flows from operating activities, we add the amount of depreciation expense to net income. The worksheet entry is:

(j) Cash (Operating Activities, Deprec. Expense—Office Equipment)550 Accumulated Depreciation—Office Equipment 550

Accumulated Depreciation—Buildings. The analysis of the accumulated depreciation for the building is the same as for the office equipment. The worksheet entry is:

Copyright © 2003, Robert G. May Page 28

(k) Cash (Operating Activities, Deprec. Expense—Building) 2,000 Accumulated Depreciation—Building 2,000

Accounts Payable. The $5,400 decrease in accounts payable means that the purchases amount Davis used in the determination of net income is less than the cash payments to suppliers. Therefore, to calculate cash flows from operating activities, we deduct the decrease in accounts payable from net income. The worksheet entry is:

(l) Accounts Payable 5,400 Cash (Operating Activities, Decrease in Accounts Payable) 5,400

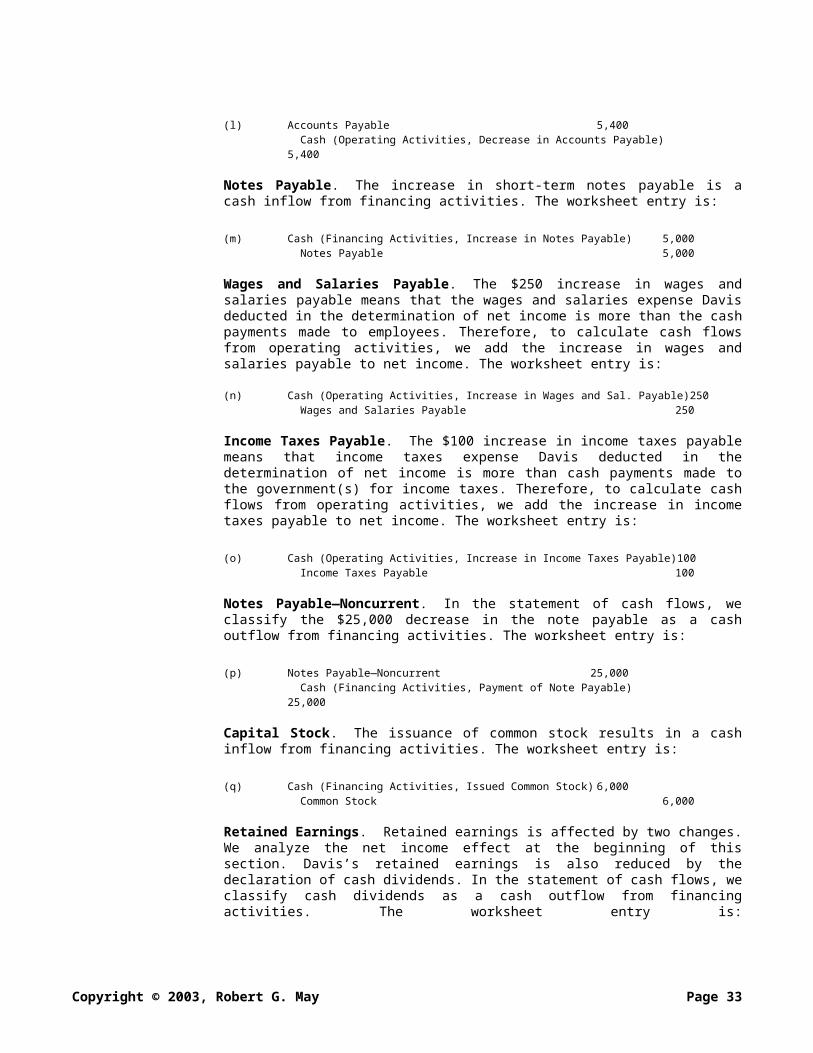

Notes Payable. The increase in short-term notes payable is a cash inflow from financing activities. The worksheet entry is:

(m) Cash (Financing Activities, Increase in Notes Payable) 5,000 Notes Payable 5,000

Wages and Salaries Payable. The $250 increase in wages and salaries payable means that the wages and salaries expense Davis deducted in the determination of net income is more than the cash payments made to employees. Therefore, to calculate cash flows from operating activities, we add the increase in wages and salaries payable to net income. The worksheet entry is:

(n) Cash (Operating Activities, Increase in Wages and Sal. Payable)250 Wages and Salaries Payable 250

Income Taxes Payable. The $100 increase in income taxes payable means that income taxes expense Davis deducted in the determination of net income is more than cash payments made to the government(s) for income taxes. Therefore, to calculate cash flows from operating activities, we add the increase in income taxes payable to net income. The worksheet entry is:

(o) Cash (Operating Activities, Increase in Income Taxes Payable)100 Income Taxes Payable 100

Notes Payable—Noncurrent. In the statement of cash flows, we classify the $25,000 decrease in the note payable as a cash outflow from financing activities. The worksheet entry is:

(p) Notes Payable—Noncurrent 25,000 Cash (Financing Activities, Payment of Note Payable) 25,000

Capital Stock. The issuance of common stock results in a cash inflow from financing activities. The worksheet entry is:

(q) Cash (Financing Activities, Issued Common Stock) 6,000 Common Stock 6,000

Retained Earnings. Retained earnings is affected by two changes. We analyze the net income effect at the beginning of this section. Davis’s retained earnings is also reduced by the declaration of cash dividends. In

Copyright © 2003, Robert G. May Page 29

the statement of cash flows, we classify cash dividends as a cash outflow from financing activities. The worksheet entry is:

(r) Retained Earnings 3,000 Cash (Financing Activities, Cash Dividend Declared) 3,000

Preparing the Statement

When all cash accounts have been analyzed, the debit and credit changes should be totaled to be sure that they balance in total. Also, the debit and credit changes in the cash account should be separately totaled. The difference in the totals should be equal to the change in the cash account for the period. In this case they do with a net credit of $7,000. After the worksheet is complete, all the information needed to prepare the statement of cash flows is contained in the top portion of the worksheet. The statement prepared according to the indirect method is presented in Illustration SCF-6.

REVIEW PROBLEM

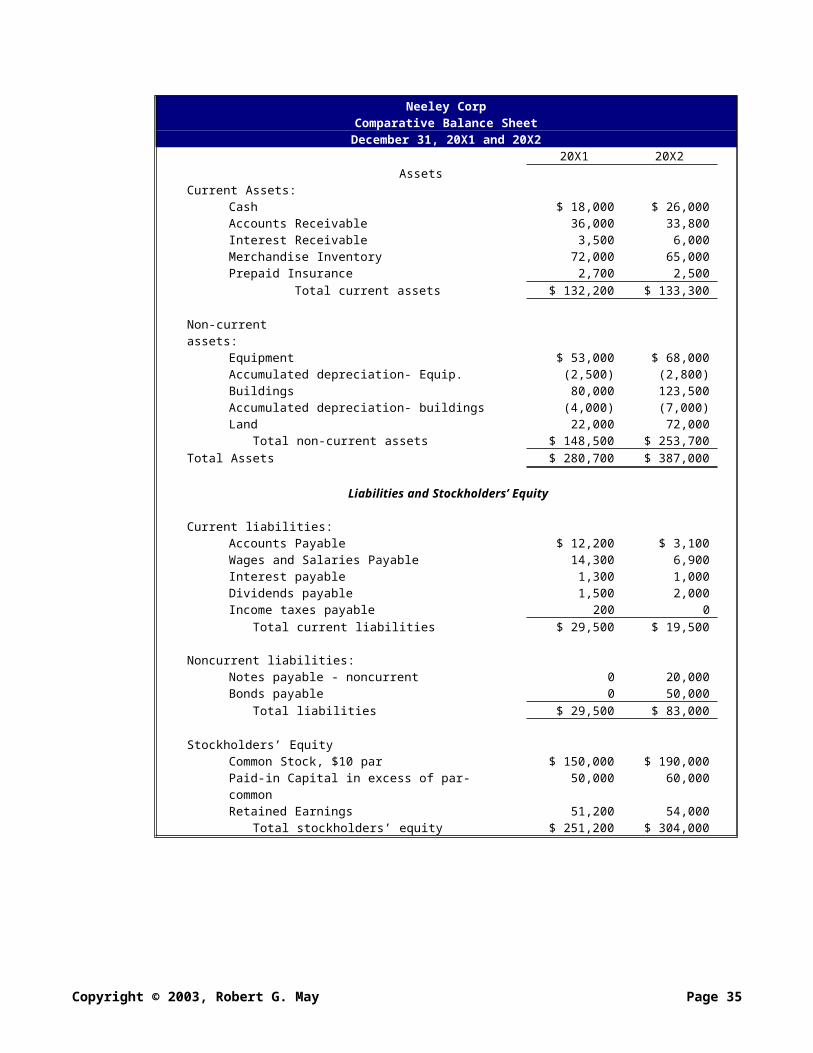

Prepare a statement of cash flows using the direct method for the Neeley Corp. from the financial statements and additional information that follow:

Copyright © 2003, Robert G. May Page 30

Neeley CorpComparative Balance SheetDecember 31, 20X1 and 20X2

20X1 20X2Assets

Current Assets:Cash $ 18,000 $ 26,000Accounts Receivable 36,000 33,800Interest Receivable 3,500 6,000Merchandise Inventory 72,000 65,000Prepaid Insurance 2,700 2,500

Total current assets $ 132,200 $ 133,300

Non-current assets:

Equipment $ 53,000 $ 68,000Accumulated depreciation- Equip. (2,500) (2,800)Buildings 80,000 123,500 Accumulated depreciation- buildings (4,000) (7,000)Land 22,000 72,000

Total non-current assets $ 148,500 $ 253,700Total Assets $ 280,700 $ 387,000

Liabilities and Stockholders’ Equity

Current liabilities:Accounts Payable $ 12,200 $ 3,100Wages and Salaries Payable 14,300 6,900Interest payable 1,300 1,000Dividends payable 1,500 2,000Income taxes payable 200 0

Total current liabilities $ 29,500 $ 19,500

Noncurrent liabilities:Notes payable - noncurrent 0 20,000Bonds payable 0 50,000

Total liabilities $ 29,500 $ 83,000

Stockholders’ EquityCommon Stock, $10 par $ 150,000 $ 190,000Paid-in Capital in excess of par- common

50,000 60,000

Retained Earnings 51,200 54,000Total stockholders’ equity $ 251,200 $ 304,000

Copyright © 2003, Robert G. May Page 31

Neeley Corp.Income Statement

For the Year Ended December 31, 20X2Revenues:

Sales $ 90,000Interest 4,200

Total Revenue $ 94,200Cost of goods sold 68,000Gross profit $ 26,200Expenses:

Wages and Salaries expense $ 10,100Depreciation expense-equipment 1,500Depreciation expense–buildings 3,000Interest expense 1,700Income taxes expense 1,000Insurance expense 2,800

Total expenses (20,100)Loss from sale of equipment

(800)

Net Income $ 5,300

Neeley Corp.Retained Earnings Statement

For the Year Ended December 31, 20X2Balance, January 1 $ 51,200Add: Net Income 5,300Total $56,500Less: Cash dividends declared 2,500Balance, December 31 $ 54,000

Additional Information:1. Equipment was purchased for $20,000 cash.2. Equipment with a cost of $5,000 and a book value of $3,800 was sold for $3,000.3. An addition to the building was added at a cost of $43,500. The addition was

paid for in cash.4. Borrowed $70,000 cash by issuing a $20,000 10% note payable and $50,000 of

bonds.5. Acquired land with a fair value of $50,000 by exchanging 4,000 shares of

common stock for the land.

SOLUTION:

Planning and Organizing Your Work1. Analyze the change in each balance sheet account to determine the cash inflows

and cash outflows. You may find it helpful to analyze the account changes by using T-accounts as demonstrated in the chapter.

2. Make note of changes in balance sheet accounts resulting from noncash investing and financing activities.

3. Classify each cash flow as resulting from operating, investing, or financing activities.

4. Prepare the statement of cash flows in the proper format.5. Prepare the supplementary schedule for noncash investing and financing

activities.

Copyright © 2003, Robert G. May Page 32

Neeley Corp.Statement of Cash Flows

For the Year Ended December 31, 20X2Cash flows from operating Activities:

Collections from customers (1) $ 92,200Interest received (2) 1,700Payments to suppliers (3) (70,100)Payments to employees (4) (17,500)Interest Paid (5) (2,000)Income taxes paid (6) (1,200)Payments for insurance (7) (2,600)

Net cash flows from operating activities $ 500Cash flows from investing activities:

Purchase of equipment (8) $ (20,000)Sale of equipment (given) 3,000Building addition (9) (43,500)

Net cash flows used in investing activities (60,500)Cash flows from financing activities

Issue of 10% note payable (10) $ 20,000Issue of bond payable (11) 50,000Cash dividend paid (12) (2,000)

Net cash used by financing activities 68,000Net decrease in cash $

8,000

Schedule of noncash investing and financing activitiesPurchase of land in exchange for common stock (13) $ 50,000

(1) Accounts Receivable (2) Accounts PayableBeg Bal. 36,000 Beg Bal. 3,500Sales 90,000 Receipt 92,200 Interest Rev 4,200 Receipt 1,700End Bal. 33,800 End Bal. 6,000

(3) Merchandise Inventory (3) Accounts PayableBeg Bal. 72,000 Beg. Bal. 12,200

Purchases 61,000Cost of Goods sold 68,000 Payments 70,100 Purchases 61,000

End Bal. 65,000 End Bal. 3,100

(4) Wages and Salaries Payable (5) Interest PayableBeg. Bal. 14,300 Beg. Bal. 1,300

Payments 17,500Wages andSalary Exp. 10,100 Payments 2,000

Interest Expense. 1,700

End Bal. 6,900 End Bal. 1,000

(6) Income Taxes Payable (7) Prepaid InsuranceBeg. Bal. 200 Beg. Bal. 2,700

Payments 1,200Income taxes Expense

1,000Payments 2,600

Insurance Expense 2,800

End Bal. 0 End Bal. 2,500

(8) Equipment (9) BuildingsBeg. Bal. 53,000 Beg. Bal. 80,000Purchases 20,000 Sold 5,000 Purchases 43,500End Bal. 68,000 End Bal. 123,500

(10) Notes Payable-Noncurrent (11) Bonds PayableBeg Bal. 0 Beg Bal. 0Receipt 20,000 Receipt 50,000End Bal. 20,000 End Bal. 50,000

(12) Dividends Payable (13) LandBeg. Bal. 1,500 Beg. Bal. 22,000

Payments 2,000 Declared 2,500 Acquired 50,000End Bal. 2,000 End Bal. 72,000

Copyright © 2003, Robert G. May Page 33

(13) Common Stock (13) Paid-in Capital in excess of ParBeg Bal. 150,000 Beg Bal. 0Issued for Land 40,000