Embed Size (px)

Citation preview

CAFCINTER CAFINAL CA

FINAL CAREVISION NOTES

MAY '19

Strategic Financial Management

Bond Management

/officialjksc Jkshahclasses.com/revision

J.K.SHAH CLASSES FINAL C.A. – FINANCIAL REPORTING

: 1 : REVISION NOTES – MAY ‘19

Q.1. A is willing to purchase a 5 years Rs. 1000 par value bond having a coupon rate of 9%.

A’s required rate of return is 10%. How much A should pay to purchase the bond if it matures at par.

Q.2. A PSU is proposing to sell a 8 years bond of Rs. 1000 at 10% coupon rate per annum.

The bond amount will be amortised equally over its life. If an investor has a minimum required rate of return of 8%, what is the bond’s present value.

Q.3. A 6 years bond of Rs.1000 has an annual rate of interest of 14%. The interest is paid

half yearly. If the required rate of return is 16% what is the value of the bond. Q.4. XYZ Ltd has issued convertible debentures with interest rate of 12%. Every debenture

has an option to convert to 20 equity shares at any time until the date of maturity. Debentures will be redeemed at Rs. Rs. Rs. Rs. 100 on maturity which is after 5 years. An investor normally requires a rate of return of 8% per annum on a 5 year security. As an investor when will you exercise the purchase option if MV of ES is (a) `̀̀̀ 4, (b) `̀̀̀ 5 or (c) `̀̀̀ 6.

Q.5. There is a 9% 5 year bond issue in the market. The issue price is Rs.Rs.Rs.Rs. 90 and the

redemption price is Rs.Rs.Rs.Rs. 105. For an investor with marginal income tax rate of 30% and capital gains tax rate of 10% (assuming no indexation), what is the post-tax yield to maturity?

Q.6. An investor is considering the purchase of the following bond:

Face value Rs.Rs.Rs.Rs. 100 Coupon rate 11% Maturity 3 years i. If he wants a yield of 13% what is the maximum price he should be ready to pay

for the bond? ii. If the bond is selling for Rs.Rs.Rs.Rs. 97.60 what should be his yield?

Q.7. Given a 2 year 8% annual coupon bond with a face value of ` 1000 and with annual

coupon payments that is fully taxable and selling at par and an identical bond that is tax free, what would the yield and price on the tax free bond have to be for an investor in a 35% tax bracket to be indifferent between the two bonds

Q.8. A bond pays Rs.Rs.Rs.Rs. 90 interest annually into perpetuity.

i. What is its value if the current yield is 10% ii. If the current yield changes to 8% and 12% then what is its value.

Q.9. The bonds of Texas Industries of face value ` 100 with 10% coupon paid semiannually

is presently selling at 5% discount on the face value. These bonds will be redeemed at par by equal instalment at the end of 5th and 6th years. The effective tax rate of Texas is 40%. What is the YTM of the bond.

Q.10. An investor purchased at a par a bond with a face value of ` 1000. The bond had 5

years to maturity and a 10% coupon rate. The bond was called two years later for a price of Rs. 1200 after making its second annual interest payment. He then reinvested the proceeds in a bond selling at its face value of ` 1000 with three years to maturity and a 7% coupon rate. What was his actual YTM over the 5 year period.

BOND OF MANAGEMENT

J.K.SHAH CLASSES FINAL C.A. – FINANCIAL REPORTING

: 2 : REVISION NOTES – MAY ‘19

Q.11. An investor acquired at par a bond for ` 1000 that offered a 15% coupon rate. At the time of purchase, the bond had 4 years to maturity. Assuming annual interest payments, calculate his actual yield to maturity if all the interest payments were reinvested in an investment earning 18% per yer. What would his actual yield to maturity be if all interest payments were spent immediately upon receipt.

Q.12. The following data are available for a bond;

Face value `̀̀̀ 1,000 Coupon rate 16% Years to Maturity 6 Redemption value `̀̀̀1,000 Yield to maturity 17%

What are the current market price, duration and volatility of this bond? Calculate the expected market price, if we witness an increase in required yield by 75 basis points.

Q.13. Find the current market price of a bond having face value of `̀̀̀ 1,00,000 redeemable

after 6 years maturity with YTM at 16% payable annually and duration of 4.3202 years. Given 1.166 = 2.4364

Q.14 .(a) Consider two bonds with 5 years to maturity and other with 20 years to maturity.

Both the bonds have a face value of `̀̀̀ 1,00,000 and coupon rate of 8% (with annual interest payments and both are selling at par. Assume that the yields of both of bonds fall to 6%, whether the price of the bond will increase or decrease? What percentage of this increase / decrease comes from a change in the present value of bond’s principal amount and what percentage of this increase / decrease comes from a change in the present value of bond’s interest payment.

(b) Consider a bond selling at its par value of `̀̀̀1000 with 6 years to maturity and a 7% coupon rate (with annual interest payment), what is the bond’s duration?

(c) If the YTM of the bond in (b) above increase to 10%, how it affects the bond’s duration? And why?

(d) Why should the duration of a coupon carrying bond always be less that the time to maturity?.

Q.15. The investment portfolio of a bank is as follows :

Government Bond Coupon rate Purchase rate (FV `̀̀̀ 100)

Duration (years)

GOI 2006 11.68% 106.50 3.50

GOI 2010 7.55% 105.00 6.50

GOI 2015 7.38% 105.00 7.50

GOI 2022 8.35% 110.00 8.75

GOI 2032 7.95% 101.00 13.00

Face value of total investment in Rs.Rs.Rs.Rs. 5 crores in each government bond. Calculate the actual investment in the portfolio. What is a suitable action to churn out investment portfolio in the following scenario: a. Interest rates are expected to lower by 25 basis points b. Interest rates are expected to rise by 75 basis points

Also calculate the revised duration of investment portfolio in each scenario.

J.K.SHAH CLASSES FINAL C.A. – FINANCIAL REPORTING

: 3 : REVISION NOTES – MAY ‘19

Q.16. M/s Transindia Ltd is contemplating calling `̀̀̀ 3 crores of 30 years Rs.Rs.Rs.Rs. 1000 bonds issued 5 years ago with a coupon interest rate of 14%. The bonds have a call price of `̀̀̀

1140 and had initially collected proceeds of `̀̀̀ 2.91 crores due to a discount of `̀̀̀ 30 per bond. The initial floating cost was `̀̀̀ 3,60,000. The company intends to sell `̀̀̀ 3 crores of 12% coupon rate, 25 years bonds to raise funds for retiring the old bonds. It proposes to sell the new bonds at their par value of `̀̀̀1000. The estimated flotation cost

is `̀̀̀ 4,00,000. The company is paying 40% tax and its after tax cost of debt is 8%. As the new bonds must first be sold and their proceeds then used to retire old bonds, the company expects a two months period of overlapping interest during which interest must be paid on both the old and new bonds. What is the feasibility of refunding bonds?

Q.17. The data given below relates to a convertible bond

Face Value `̀̀̀ 250 Coupon rate 12% No of shares per bond 20 Market price of share `̀̀̀ 12 Straight value of bond `̀̀̀235 Market price of convertible bond `̀̀̀ 265

Calculate: a) The stock value of bond b) The percentage of downside risk c) The conversion premium d) The conversion parity price of bond

Q.18. Duration & IMMUNISATION OF PORTFOLIO

A company has to pay Rs. 10 million after 6 years from today. The company wants to fund this obligation today only. The current interest rate in the market is 8%. Two zero coupon bonds are traded in the market on the basis of 8% YTM – one with a 5 year maturity and the other with a 7 year maturity. Suggest the interest rate immunized investment plan. Calculate the total amount to be received from the investments in following three cases :

a. market interest rates remain unchanged throughout the period of 6 years .

b. Market interest rates declines to 6%.

c. Market interest rate rises to 10%.

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 1 : REVISION NOTES – MAY ‘19

Q.1. A company is proposing to set-up a project worth ` 7.5 lacs. The following additional

information is available : (a) The project will result in production of product X as below :

i) First year 10,000 units ii) Second year 20,000 units iii) Third year onwards till the end of eighth year 50,000 units annually.

(b) The company can market the entire production thinking of pricing it at ` 10.50 in the first year and ` 11 in subsequent years.

(c) The estimated relevant cost per unit is ` 8.50 in the first year and ` 8 from the second year onwards.

(d) Life of the machine is estimated to be eight years at the end of which the company expects to sell the equipment for ` 2.5 lacs.

(e) The depreciation is to be calculated as per Income Tax provision at 25%. (f) This project will reduce the cost of certain existing operations at ` 5,000 per

annum uniformly. Discounting rate is 10%. Is the investment worthwhile? Assume tax rate of 52.5%.

Q.2. A large profit making company is considering the installation of a machine to process

the waste produced by one of its existing manufacturing process to be converted into a marketable product. At present, the waste is removed by a contractor for disposal on payment by the company of ` 50 lacs per annum for the next four years. The contract can be terminated upon installation of the aforesaid machine on payment of a compensation of ` 30 lacs before the processing operation starts. This compensation is not allowed as deduction for tax purposes.

The machine required for carrying out the processing will cost ` 200 lacs to be financed by a loan repayable in 4 equal installments commencing from the end of year 1. The interest rate is 16% per annum. At the end of the 4th year, the machine can be sold for `

20 lacs and the cost of dismantling and removal will be `15 lacs. Sales and direct costs of the product emerging from waste processing for 4 years are

estimated as under :

Year 1 2 3 4

Sales Material consumption Wages Other expenses Factory overheads Depreciation (as per income - tax rules)

322 30 75 40 55 50

322 40 75 45 60 38

418 85 85 54

110 28

413 85

100 70

145 21

Initial stock of materials required before commencement of the processing operations is ` 20 lacs at the start of year 1. The stock levels of materials to be maintained at the end of year 1, 2 and 3 will be ` 55 lacs and the stocks at the end of year 4 will be nil. The storage of materials will utilise space which would otherwise have been rented out for ` 10 lacs per annum. Labour costs include wages of 40 workers, whose transfer to this process will reduce idle time payments of ` 15 lacs, in year 1 and ` 10 lacs in year 2 Factory overheads include apportionment of general factory overheads except to the extent of insurance charges of ` 30 lacs per annum payable on this venture. The company's tax rate is 50%.

CAPITAL BUDGETING

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 2 : REVISION NOTES – MAY ‘19

Present value factors for four years are as under :

Year 1 2 3 4

Present value factors 0.870 0.756 0.658 0.572

Advise the management on the desirability of installing the machine for processing the waste. All calculations should form part of the answer.

Q.3. An automobiles ancillary unit is proposing to set up a manufacturing establishment

whose project cost is ` 320 lacs. The cost of land and buildings included in the project

cost is ` 40 lacs, the breakup of which is as follows :

(`̀̀̀)

Land (4,400 sq. yards) Building (area 25,000 sq. feet)

15 lacs 25 lacs

It is anticipated that in the first 4 years, the profitability will be low due to the time required for cultivating the market. To meet the situation, management is planning to hire factory premises of the same size at Re. 0.80 per square foot per month for the first four years, instead of own buildings. Repairs and maintenance, taxes, etc. will be borne by the landlord.

In the present project, the provision has been made for depreciation at 7% p.a. on original cost of buildings. Provision has also been made for repairs, maintenance, taxes etc., on buildings at ` 1,20,000 p.a.

The annual sales and profit figures as projected in the project report are as follows (`̀̀̀ in lacs)

Year Sales Net profit (NPADIT) Capacity Utilization

I II III IV

200 275 350 450

(-5) 5 10 20

60% 75% 90% 100%

After 4 years, the profit is expected to be steady at ` 40 lacs per annum. Institutional

finance is available upto ` 200 lacs under both the alternatives. (a) You are required to work out the average rate of return for the first four years on

shareholders initial investment, under both the alternatives. (b) If the lease is available for 4 years only, would you recommend leasing the

premises, if it is anticipated that the cost of land will increase by 40% and the cost of construction by 20% at the end of the four year period? For this purpose, opportunity cost of finance may be taken at 10% p.a.

Q.4. Delhi Bridge Construction Company plans to build a bridge over a crossing. The

construction work is expected to last 5 years and will be undertaken by a private sector firm to which ` 100 lacs will be payable at the end of year 1 and ` 50 lacs each at the end of next 4 years.

The annual maintenance cost of the bridge is expected to be ` 10,00,000 at current prices. This cost is expected to increase at 7% p.a. At the end of 15 years after completion, the bridge will require a major repair work requiring materials of `100 lacs and expenses of `100 lacs, both in current prices. The prices of materials are expected to rise at the rate of general inflation for 16 years and constant thereafter but expense cost is expected to rise 6% over the general interest for the first three years and then will increase in line with general inflation rate.

The required rate of return may be taken as 17% p.a. and the life of the bridge may be taken as infinite. Numbers of vehicles using the bridge per day is 20,000 and the toll tax is expected to increase in line with general inflation. Find out the minimum toll tax chargeable per vehicle in the first year of operation so that the investment in bridge may breakeven over its life. (Assumption : All annual cash flows arise on the last day of the year).

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 3 : REVISION NOTES – MAY ‘19

Q.5. A and Co. is contemplating whether to replace an existing machine or to spend money on overhauling it. A and Co. currently pays no taxes. The replacement machine costs ` 90,000 now and requires maintenance of ` 10,000 at the end of each year for eight

years. At the end of eight years, it would have a salvage value of ` 20,000 and would be sold. The existing machines require increasing amounts to maintenance each year and its salvage value falls each year as follows :

Year Maintenance (`̀̀̀) Salvage (`̀̀̀)

Present 1 2 3 4

0 10,000 20,000 30,000 40,000

40,000 25,000 15,000 10,000

0

COC is 15%. When should the machine be replaced? (Annuity for 8 years 4.4873 and at the end of the 8th year 0.3269).

Q.6. A delivery van must be replaced every four years and related cash flow are as under : (Figures in ‘ `̀̀̀ 000)

Age for Van in Years

Year 0 Year 1 Year 2 Year 3 Year 4

Cost of Van Maintenance Cost Repairs Scrap Value

1,500 ---- ---- ----

---- 400 ---- 800

---- 450 100 600

---- 500 200 400

---- 500 400 200

The firm is faced with the decision : Should the van be kept for four years and then scrapped away for ` 2,00,000? Or should it be replaced earlier?

Q.7. Catix Corporation is a divisionalised company and each division has the authority to

make capital expenditure upto ` 2,00,000 without the approval of the corporate headquarters. The corporate controller has determined that the cost of capital for Catix Corporation is 12%. This rate does not include an allowance for inflation, which is expected to occur at an average rate of 8% over the next five years. Catix pays income tax at the rate of 40%. The Electronics Division of Catix is considering the purchase of an automated assembly machine. The divisional controller estimates that if the machine is purchased, two positions will be eliminated yielding a cost saving for wages and employees benefits. However, the machine would require additional supplies and more power would be required to operate the machine. The cost savings and additional cost in current 19x0 prices are as follows : Wages and employee benefit of the two Positions eliminated (` 25,000 each) `̀̀̀ 50,000

Cost of additional supplies `̀̀̀ 3,000 Cost of additional power `̀̀̀ 10,000

The new machine would be purchased and installed at the end of 19x0 at a net cost of ` 80,000. If purchased, the machine would be depreciated @ 25% as per Income Tax Laws. The machine will become technologically obsolete in four years and will have no scrap value at that time.

The Electronics Division compensates for inflation in capital expenditure analysis by adjusting the expected cash flows by an estimated price level index.

The adjusted after tax cash flows are then discounted using the appropriate discount rate.

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 4 : REVISION NOTES – MAY ‘19

The estimated year end index values for each of the next five years are presented below :

Year Year – End Price Index

19x0 19x1 19x2 19x3 19x4 19x5

1.00 1.08 1.17 1.26 1.36 1.47

All operating revenues and expenses occur at the end of the year. You are required to prepare an analysis of the automated assembly machine for the

Electronics Division. Q.8. XYZ Ltd. an infrastructure company is evaluating a proposal to build, operate and

transfer a section of 35 kms. of road at a project cost of ` 200 crores to be financed as follows :

Equity Share Capital of ` 50 crores, loans at the rate of interest of 15% p.a. from financial institutions ` 150 crores. The Project after completion will be opened to traffic and a toll will be collected for a period of 15 years from the vehicles using the road the company is also required to maintain the road during the above 15 years and after the completion of that period, it will be handed over to the Highway authorities at zero value. It is estimated that the toll revenue will be ` 50 crores per annum and the annual toll collection expenses including maintenance of the roads will amount to 5% of the project cost. The company considers to write off the total cost of the project in 15 years on a straight line basis. For Corporate Income - tax purposes the company is allowed to take depreciation @ 10% on WDV basis. The financial institutions are agreeable for the repayment of the loan in 15 equal annual instalments - consisting of principal and interest.

Calculate Project IRR and Equity IRR. Ignore Corporate taxation. Explain the difference in Project IRR and Equity IRR.

CAFCINTER CAFINAL CA

FINAL CAREVISION NOTES

MAY '19

Strategic Financial Management

Mergers & Acquisitions

/officialjksc Jkshahclasses.com/revision

Including Corporate Valuation

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 1 : REVISION NOTES – MAY ‘19

Q.1. A Ltd. is keen or reporting an earning per share of ` 6 after acquiring T Ltd. The

following financial data are given : A Ltd. T Ltd.

EPS Market price per share No. of shares

` 5

` 60

10,00,000

` 5

` 50

8,00,000

There is an exected synergy gain of 5%. What exchange ratio will result in post - merger EPS of ` 6 for A Ltd.?

Q.2. You have been provided the following financial data of two companies :

T Ltd. A Ltd.

Earnings after taxes Equity shares outstanding Earnings per share Price - earnings (P / E) ratio Market price per share

` 7,00,000

2,00,000 3.50

10 times ` 35

` 10,00,000

4,00,000 2.50 14 times

` 35

Company A is acquiring the Company T, exchanging its shares on a one to one basis for Company T's shares. The exchange ratio is based on the market prices of the shares of the two companies. (i) What will be the EPS subsequent to merger ? (ii) What is the change in EPS for the shareholders of companies A and T ? (iii) Determine the market value of the post - merger firm. P.E. Ratio is likely to remain

same. (iv) Ascertain the profits accruing to shareholders of both the firms. (v) T Ltd. wants to be sure that it's shareholders' earnings will not be dimished by the

merger. What should be the exchange ratio in that case? (vi) Determine gain (loss) for shareholders of the two companies after acquisition.

Q.3. T Ltd. and E Ltd. are in the same industry. The former is in negotiation for acquisition of

the latter. Important information about the two companies as per their latest financial statements is given below:

T Ltd. E Ltd.

` 10 Equity shares outstanding Debt: 10% Debentures (` Lakhs) 12.5% Institutional Loan (` Lakhs) Earnings before interest, depreciation and tax (EBIDAT) (` Lakhs) Market Price/share (`)

12 Lakhs

580 --

400.86 220.00

6 Lakhs --

240

115.71 110.00

T Ltd. plans to offer a price for E Ltd., business as a whole which will be 7 times EBIDAT reduced by outstanding debt, to be discharged by own shares at market price.

E Ltd. is planning to seek one share in T Ltd. for every 2 shares in E Ltd. based on the market price. Tax rate for the two companies may be assumed as 30%.

Calculate and show the following under both alternatives - T Ltd.'s offer and E Ltd.'s plan: (i) Net consideration payable. (ii) No. of shares to be issued by T Ltd. (iii) EPS of T Ltd. after acquisition. (iv) Expected market price per share of T Ltd. after acquisition. (v) State briefly the advantages to T Ltd. from the acquisition.

Calculations (except EPS) may be rounded off to 2 decimals in lakhs.

MERGERS & ACQUISITIONS INCLUDING CORPORATE VALUATION

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 2 : REVISION NOTES – MAY ‘19

Q.4. The shares of Nisha Ltd., are currently being traded for ` 24 per share. The top management together with their families control 40% of the 10 lakh shares outstanding. Sangeeta Ltd. wishes to acquire Nisha Ltd. because of likely synergies. The estimated present value of these synergies is ` 80 lakh. Moreover, Sangeeta feels that the management of Nisha is overpaid. It feels with better management motivation, lower salaries and fewer perks for the top management, approximately ` 4 lakh of expenses per annum can be saved. This would add ` 30 lakh in value to the acquisition. The following additional information is available regarding Sangeeta : Earnings per share ` 4.00 Number of shares outstanding 15 lakh Market price of shares ` 40.00 (a) What is the maximum price per share which Sangeeta can offer to pay for Nisha? (b) What is the minimum price per share at which the management of Nisha will be

willing to give up their controlling interest? Q.5. Following are the financial statements for A Ltd. and B Ltd. for the current financial year.

Both firms operate in the same industry. Balance Sheet

A Ltd. B Ltd.

Total current assets Total fixed assets (net) Total Assets Equity capital (of ` 10 each)

Retained earnings 14% Long term debt Total current liabilities

` 14,00,000 10,00,000

` 10,00,000 5,00,000

24,00,000 15,00,000

10,00,000 2,00,000 5,00,000 7,00,000

8,00,000 ----

3,00,000 4,00,000

24,00,000 15,00,000

Income Statements A Ltd. B Ltd.

Net sales Cost of goods sold Gross profit Operating expenses Interest Earnings before taxes Taxes (50%) Earnings after taxes (EAT) Additional Information : Number of equity shares Dividend payment ratio Market price per share (MPS)

` 34,50,000 27,60,000

` 17,00,000 13,60,000

6,90,000 2,00,000 70,0000

3,40,000 1,00,000 42,000

4,20,000 2,10,000

1,98,000 99,000

2,10,000 99,000

1,00,000

40% ` 40

88,000 60% ` 15

Assume that the two firms are in the process of negotiating a merger through an exchange of equity shares. You have been asked to assist in establishing equitable exchange terms, and are required to : (i) Decompose the share prices of both the firms into EPS and PE components, and

also segregate their EPS figures into return on equity (ROE) and book value / intrinsic value per share (BVPS) components.

(ii) Estimate future EPS growth rates for each firm. (iii) Calculate the post - merger EPS based on an exchange ratio of 0.4 : 1 being

offered by A Ltd. Indicate the immediate EPS accretion or dilution, if any, that will occur for each group of shareholders.

(iv) Based on a 0.4 : 1 exchange ratio, and assuming that A's pre - merger PE ratio will continue after the merger, estimate the post - merger market price. Show the resulting accretion or dilution in pre - merger market prices.

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 3 : REVISION NOTES – MAY ‘19

Q.6. The following information is provided relating to the acquiring company. Efficient Ltd., and the target Company Healthy Ltd.

Efficient Ltd. Healthy Ltd.

No. of shares (F.V. ` 10 each) Market Capitalisation P / E ratio (times) Reserves and Surplus Promoter's Holding (No. of shares)

10.00 lakhs 500.00 lakhs

10.00 300.00 lakhs 4.75 lakhs

7.5 lakhs 750.00 lakhs

5.00 165.00 lakhs 5.00 lakhs

Board of Directors of both the Companies have decided to give a fair deal to the shareholders and accordingly for swap ratio the weights are decided as 40%, 25% and 35% respectively for Earning. Book Value and Market Price of share of each company : (i) Calculate the swap ratio and also calculate Promoter's holding % after acquisition. (ii) What is the EPS of Efficient Ltd., after acquisition of Healthy Ltd.? (iii) What is the expected market price per share and market capitalization of Efficient

Ltd. after acquisition, assuming P/E ratio of Firm Efficient Ltd., remains unchanged.

(iv) Calculate free float market capitalization of the merged firm. Q.7. The following information is relating to Fortune India Ltd., having two division, viz.

Pharma Division and Fast Moving Consumer Goods Division (FMCG Division). Paid up share capital of Fortune India Ltd., is consisting of 3,000 Lakhs equity shares of Re. 1 each. Fortune India Ltd., decided to de - merge Pharma Division as Fortune Pharma Ltd., w.e.f. 1.4.2005. Details of Fortune India Ltd., as on 31.3.2005 and of Fortune Pharma Ltd., as on 1.4.2005 are given below :

Particulars Fortune Pharma Ltd. Fortune India Ltd.

`̀̀̀ `̀̀̀

Outside Liabilities Secured Loans Unsecured Loans Current Liabilities & Provisions Assets Fixed Assets Investments Current Assets Loans & Advances Deferred tax / Miscellaneous Expenses

400 lakh

2,400 lakh 1,300 lakh

7,740 lakh 7,600 lakh 8,800 lakh 900 lakh 60 lakh

3,000 lakh 800 lakh

21,200 lakh

20,400 lakh 12,300 lakh 30,200 lakh 7,300 lakh (200) lakh

Board of Directors of the Company have decided to issue necessary equity shares of Fortune Pharma Ltd., of Re. 1 each, without any consideration to the shareholders of Fortune India Ltd. For that purpose following points are to be considered : 1. Transfer of Liabilities & Assets at Book value. 2. Estimated Profit for the year 2005-06 is ` 11,400 Lakh for Fortune India Ltd. &

` 1,470 lakhs for Fortune Pharma Ltd. 3. Estimated Market Price of Fortune Pharma Ltd. is ` 24.50 per share. 4. Average P/E Ratio of FMCG sector is 42 & Pharma sector is 25, which is to be

expected for both the companies. Calculate :

1. The Ratio in which shares of Fortune Pharma are to be issued to the shareholders of Fortune India Ltd.

2. Expected Market price of Fortune India Ltd. 3. Book Value per share of both the Companies immediately after Demerger.

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 4 : REVISION NOTES – MAY ‘19

Q.8. A Ltd. Wants to value T Ltd. in accordance with Chop Shop method. T Ltd. is carrying out 3 streams of business namely telecom, real estate, toys. The market capitalization of equity shares of T Ltd. is ` 15,200 crores. The other financial details of T Ltd. are as follows :

Particulars Telecom Real Estate Toys Total

Turnover 5000 cr. 4000 cr. 1000 cr. 10000 cr.

Assets 1250 cr. 2000 cr. 1000 cr. 4250 cr.

Net operating profits after tax 1000 cr. 500 cr. 400 cr. 1900 cr.

Industry Statistics

Market Capitalization to Sales 1.65 1.40 0.7

Market Capitalization to Assets 3 4 2

Market Capitalization NOPAT 12 9 11

Q.9. The total value (equity + debt) of two companies, A Ltd. and B Ltd. are expected to

fluctuate according to the state of the economy.

State of the economy Probability Value of A Ltd. ` ` ` ` in lakh

Value of B Ltd. `̀̀̀ in lakh

Rapid growth 0.30 720 1150

Slow growth 0.50 520 750

Recession 0.20 380 600

A Ltd. and B Ltd. currently have a debt of ` 420 lakhs and ` 80 lakhs, respectively. The two companies are deciding for merger. Assuming that no operational synergy is

expected as a result of the merger, you are required to calculate the expected value of debt and equity of the merged company.

Also explain the reasons for any difference that exists from the expected values of debt and equity, if they do not change.

Q.10. Timby Ltd. is in the business of making sports equipment. The company operates from

Thailand. To globalize its operations, Timby has identified Find Toys Ltd. an Indian Company, as a potential takeover candidate. After due diligence of Find Toys Ltd. the following information is available. (a)

(b) The net worth of Find Toys Ltd. (`in lakhs) after considering certain adjustments suggested by the due diligence team reads as under:

Tangible Inventories Receivables Less:Creditors Bank Loans

160 250

750 145 75

971

(415)

Represented by equity shares of `1,000 each 555

Talks for takeover have crystallized on the following: 1. Timby Ltd. will not be able to use Machinery worth ` 75 lakhs which will be

disposed of by them subsequent to take over. The expected realization will be ` 50 lakhs.

2. The inventories and receivables are agreed for takeover of values of `100 and `50 lakhs respectively which is price they will realize on disposal.

Cash Flow Forecasts (`̀̀̀ in crore):

Year 10 9 8 7 6 5 4 3 2 1

Find Toys Ltd. 24 21 15 16 15 12 10 8 6 3

Timby Ltd. 108 70 55 60 52 44 32 30 20 16

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 5 : REVISION NOTES – MAY ‘19

3. The liabilities of Fine Toys Ltd. will be discharged in full on take over along with an employee settlement of `90 lakhs for the employees who are not interested in continuing under the new management.

4. Timby Ltd. will invest a sum of `150 lakhs for upgrading the Plant of Find Toys Ltd.

on takeover. A further sum of `50 lakhs will also be incurred in the second year to revamp the machine shop floor of Find Toys Ltd.

5. The Anticipated Cash Flows (in `crore) post takeover are as follows: Year 1 2 3 4 5 6 7 8 9 10 18 24 36 44 60 80 96 100 140 200

You are required to advice the management the maximum price which they can pay per share of Find Toys Ltd. if a discount factor of 20 per cent is considered appropriate.

Q.11. AB Ltd., is planning to acquire and absorb the running business of XY Ltd. The

valuation is to be based on the recommendation of merchant bankers and the consideration is to be discharged in the form of equity shares to be issued by AB Ltd. As on 31.3.2006, the paid up capital of AB Ltd. consists of 80 lakhs shares of ` 10 each.

The highest and the lowest market quotation during the last 6 months were ` 570 and ` 430. For the purpose of the exchange, the price per share is to be reckoned as the average of the highest and lowest market price during the last 6 months ended on 31.3.2006.

XY Ltd.'s Balance Sheet as at 31.3.2006 is summarised below :

`̀̀̀ in lakhs

Sources Share Capital

20 lakhs equity shares of ` 10 each fully paid 10 lakhs equity shares of ` 10 each ` 5 paid

Loans

200 50 100

Total 350

Uses Fixed Assets (Net) Net Current Assets

150 200

Total 350

An independent firm of merchant bankers engaged for the negotiation, have produced the following estimates of cash flows from the business of XY Ltd. :

Year ended By way of `̀̀̀ lakhs

31.3.07 31.3.08 31.3.09 31.3.10 31.3.11

after tax earnings for equity do do do do terminal value estimate

105 120 125 120 100 200

It is the recommendation of the merchant banker that the business of XY Ltd., may be valued on the basis of the average of (i) Aggregate of discounted cash flows at 8% and (ii) Net assets value. Present value factors at 8% for years. 1 - 5 : 0.93 0.86 0.79 0.74 0.68

You are required to : (i) Calculate the total value of the business of XY Ltd. (ii) The number of shares to be issued by AB Ltd.; and (iii) The basis of allocation of the shares among the shareholders of XY Ltd.

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 6 : REVISION NOTES – MAY ‘19

Q.12. Chennai Limited and Kolkata Limited have agreed that Chennai Limited will take over the business of Kolkata Limited with effect from 31st March, 2009. It is agreed that : (i) 10,00,000 shareholders of Kolkata Limited will receive shares of Chennai Limited. The swap ratio is determined on the basis of 26 weeks average market prices of

shares of both the companies. Average price have been worked out at ` 50 and ` 25 for the shares of Chennai Limited and Kolkata Limited respectively.

(ii) In addition to (i) above shareholders of Kolkata Limited will be paid cash based on the projected synergy that will arise on the absorption of the business of Kolkata Limited by Chennai Limited. 50% of the projected benefits will be paid to the shareholders of Kolkata Limited.

The following projection has been agreed upon by the management of both the companies.

Year ended 31.3. Benefit

2010 2011 2012 2013 2014

(in ` Lakhs) 50 75 90 100 105

The benefit is estimated to grow at the rate of 2% after 2014 perpetually. It has been further agreed that a discount rate of 20% should be used to calculate the

cash that the holder of each share of Kolkata Limited will receive. (i) Calculate the cash that holder of each share of Kolkata Limited will receive. (ii) Calculate the total purchase consideration. [Discounting factor : Discounting rate 20% : 1 year. 833, 2 year. 694, 3 year. 579,

4 year. 482, 5 year. 402, 6 year. 335; Discounting rate 18%; 1 year. 842, 2 year. 718,3 year. 609, 4 year. 516, 5 year. .437, 6 year. 370; Discounting rate 16% : 1 year. 862, 2 year. 743, 3 year. 641, 4 year. 552, 5 year. .476, 6 year. 410]

Q.13. Adonis Ltd., makes thermal clothing for winter sports and outdoor work, and is

considering acquiring Sking Ltd. which manufactures and sells ski clothing. Sking Ltd. is about one quarter of Adonis size and manufactures its entire product line in a small rented factory on a mountaintop in Manali. It costs about 10,00,000 a year in overhead to operate in the factory. Adonis Ltd. produces its output in a less popular in North but more popular north - east locations. Its factory has at least 50% excess capacity. Adonis plan is to acquire Sking Ltd., and combine production operations in its north - eastern factory, but otherwise run the companies separately.

Sking Ltd. beta is 2.0, Treasury bills currently yield 5% and the Nifty Index is yielding 9%. The corporate income tax rate for both firms is 40%. Because Sking Ltd. will no longer be maintaining its own production facilities, it can be assumed that only a minimal amount of cash will have to be reinvested. This amount is estimated at 1,00,000 per year.

The financial information for Sking Ltd. is as follows :

Revenue EAT Depreciation

` 1,25,00,000 ` 13,00,000

` 6,00,000

(a) Calculate the appropriate discount rate for evaluating the Sking Ltd. acquisition. (b) Determine the annual cash flow expected by Adonis Ltd. from Sking Ltd. if the

acquisition is made (considering the synergy). (c) Calculate the value of the acquisition to Adonis Ltd. assuming the benefits last for

(1) five years, (2) 10 years, and (3) 15 years. (d) Sking Ltd. has 2,50,000 shares outstanding. Calculate the maximum price Adonis

Ltd. should be willing to pay per share to acquire the firm under the three assumptions in part C.

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 7 : REVISION NOTES – MAY ‘19

(e) If Adonis Ltd. is willing to assume the benefits of the Sking Ltd. acquisition will last indefinitely without growth, what should it be willing to pay per share?

(f) Assume that the cash flow from the Sking Ltd. acquisition grows at 10% from its initial value for one year and then grows at 5% indefinitely (starting in the third year). Calculate the value of the firm and the implied stock price under these conditions. Use a terminal value at the beginning of the period of 5% growth. What price premium is implied in Rupees and as a percent of market price if Sking Ltd. stock is currently selling at ` 62?

Q.14. Zed Ltd. is considering the immediate purchase of some or all, of the shares of one of

two firms Red Ltd. and Yellow Ltd. Both Red and Yellow have 1,00,000 equity shares issued and neither company has any debt capital outstanding.

Both firms are expected to pay a dividend in 1 years’ time, Red's expected dividend amounting to ` 3 per share and Yellow's being ` 2.70 per share. Dividends will be paid annually and are expected to increase over time. Red's dividends are expected to display perpetual growth at a compound rate of 6 per cent per annum. Yellow's dividend will grow at a high annual compound rate of 331/3% until a dividend of ` 6.40 per share is reached in year 4.

Thereafter Yellow's dividend will remain constant. If Zed is able to purchase all the equity capital of either firm then the reduced

competition would enable Zed to save some advertising and administrative costs which would amount to ` 2,25,000 per annum indefinitely and, in year 2, to sell some office space for ` 8,00,000. These benefits and savings would only occur if a complete takeover were to be carried out. Zed would change some operations of any company completely taken over. The details are : (i) In case of Red : No dividend would be paid until year 2. Year 3 dividend would be

` 2.50 per share and dividends would then grow at 10% per annum indefinitely. (ii) In case of Yellow : No change in total dividends in years 1 to 4, but after year 4

dividend growth would be 25% per annum compound until year 7. Thereafter, annual dividends would remain constant at the year 7 amount per share.

An appropriate discount rate for the risk inherent in all the cash flows mentioned is 15%. You are required to present. (i) The valuation per share for a minority investment in each of the firms, Red and

Yellow, which would provide the investor with a 15% rate of return. (ii) The maximum amount per share which Zed should consider paying for each

company in the event of a complete takeover. Q.15. Y Ltd. which is specialized in manufacturing garments is planning for expansion to

handle a new contract which it expects to obtain. An investment bank have approached the company and asked whether the Co. had considered venture Capital financing. In 2001, the company borrowed ` 100 lacs on which interest is paid at 10% p.a. The Company shares are unquoted and it has decided to take your advice in regard to the calculation of value of the Company that could be used in negotiations using the following available information and forecast.

Company’s forecast turnover for the year to 31st March, 2005 is ` 2,000 lacs which is mainly dependent on the ability of the Company to obtain the new contract, the chance for which is 60%, turnover for the following year is dependent to some extent on the outcome of the year to 31st March, 2005. Following are the estimated turnovers and probabilities:

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 8 : REVISION NOTES – MAY ‘19

Year - 2005 Year - 2006

Turnover `̀̀̀ (in lacs)

Prob. Turnover `̀̀̀ (in lacs)

Prob.

2,000

1,500

1,200

0.6 0.3 0.1

2,500 3,000 2,000 1,800 1,500 1,200

0.7 0.3 0.5 0.5 0.6 0.4

Operating costs inclusive of depreciation are expected to be 40% and 35% of turnover respectively for the years 31st March, 2005 and 2006. Tax is to be paid at 30%. It is assumed that profits after interest and taxes are free cash flows. Growth in earnings is expected to be 40% for the years 2007, 2008 and 2009 which will fall to 10% each year after that. Industry average cost of equity (net of tax) is 15%.

Q.16. A valuation done of an established company by a well-known analyst has estimated a

value of ` 500 lakhs, based on the expected free cash flow for next year of ` 20 lakhs and an expected growth rate of 5%.

While going through the valuation procedure, you found that the analyst has made the mistake of using the book values of debts & equity in his calculation. While you do not know the book value weights he used, you have been provided with the following information: (i) Company has a cost of equity of 12% (ii) After tax cost of debt is 6% (iii) The market value of equity is three times the book of equity, while the market

value of debt is equal to the book value of debt. You required to estimate the correct value of the company.

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 1 : REVISION NOTES – MAY ‘19

Q.1. ABC Ltd. is a construction company following a residual dividend policy. The total

capital budget for next year can be ` 20 lakhs, ` 30 lakhs or ` 40 lakhs. The forecasted

level of potential retained earnings next year is ` 20 lakhs. The optimal/target capital structure is debt ratio of 40%. Compute the amount of the dividend and dividend payout ratio for each of the 3 capital expenditure amounts.

Q.2. Vouge Ltd. maintains a capital structure of 70% debt and 30% equity. The profit after

tax for the current year is ` 60,000. (i) How much capital expenditure can be incurred without raising fresh issue (a) If the

company adopts the residual approach and does not bother about capital structure? (b) If the company adopts the residual approach and bothers about the capital structure?

(ii) If the company plans to spend ` 1,50,000 in the upcoming year as capital expenditure, what dividend will it be in a position to pay if it follows the (a) residual approach and believes in not maintaing its capital structure intact? (b) residual approach and believes in maintaing its capital structure?

Q.3. Calculate the value of the share from the following information : Profit of the company ` 290 crores Equity capital of company ` 1,300 crores Par value of share ` 40 each Debt ratio of company 0.27 Long run growth rate of the co. 8% Beta 0.1 Risk free interest rate 8.7% Market returns 10.3% Capital expenditure per share ` 47 Depreciation per share ` 39 Change in working capital ` 3.45 per share Q.4. CMC plc has an all-common-equity capital structure. If has 200,000 share of ` 2 par

value equity shares outstanding. When CMC’s founder, who was also its research director and most successful inventor, retired unexpectedly to settle down in the South Pacific in late 2005, CMC was left suddenly and permanently with materially lower growth expectations and relatively few attractive new investment opportunities. Unfortunately, there was no way to replace the founder’s contributions to the firm. Previously, CMC found it necessary to plough back most of its earnings to finance growth, which averaged 12% per year. Future growth at a 5% rate is considered realistic; but that level would call for an increase in the dividend payout. Further, it now appears that new investment projects with at least the 14% rate of return required by CMC’s shareholders (ke = 14%) would amount to only ` 800,000 for 2006 in

comparison to a projected ` 2,000,000 of net income. If the existing 20% dividend payout were continued, retained earnings would be ` 16,00,000 in 2006, but, as noted, investments that yield the 14% cost of capital would amount to only ` 800,000. The one encouraging thing is that the high earnings from existing assets are expected to continue, and net income of ` 20,00,000 is still expected for2006. Given the dramatically changed circumstances. CMC’s board is reviewing the firm’s dividend policy.

DIVIDEND POLICY

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 2 : REVISION NOTES – MAY ‘19

(a) Assuming that the acceptable 2006 investment projects would be financed entirely by earnings retained during the year, calculate DPS in 2006, assuming that CMC uses the residual payment policy.

(b) What payout ratio does your answer to part a imply for 2006? (c) If a 60 % payout ratio is adopted and maintained for the foreseeable future, what is

your estimate of the present market price of the equity share? How does this compare with the market price that should have prevailed under the assumptions existing just before the news about the founder’s retirement? If the two values of P0 are different. Comment on why?

(d) What would happen to the price of the share if the old 20% payout were continued? Assume that if this payout is maintained, the average rate of return on the retained earnings will fall to 7.5% and the new growth rate will be G = (1.0- Payout ratio) × (ROE) = (1.0 – 0.2) (7.5%) = (0.8) (7.5%) = 6.0%.

Q.5. A Ltd. has earning of ` 4 per share this year. Dividend per share last year was ` 1.50

suppose the target pay-out ratio is 60% & the adjustment rate is 50%, what would be the dividend per share for the current year under Lintner's Model.

Q.6. The target payout ratio for Jupiter Ltd. is 0.4. The dividend per share for the current

year is ` 14. The dividend per share in previous year was ` 12. The Adjustment ratio is 0.60. The number of equity shares outstanding in the company is 10,00,000. If the P/E multiple is 9, applying Lintner Model of dividend policy to the company, compute the market capitalization of the company.

Q.7. Ghanshyam Limited is relatively a new company in the industry of automobiles. The

earnings per share of a company is ` 30 and dividend payout ratio is 60%. If the share

price of the company is ` 56 whereas cost of capital and internal rate of return is 15% and 18% respectively. What is the multiplier applicable to the company according to the Graham and Dodd model?

Q.8. ABC Ltd. has a capital of ` 10 lakhs in equity shares of ` 100 each. The shares are

currently quoted at par. The company proposes declaration of a dividend of ` 10 per share at the end of the current financial year. The capitalisation rate for the risk class to which the company belongs is 12%.

What will be the market price of the share at the end of the year if (i) A dividend is not declared? (ii) A dividend is declared?

Assuming that the company pays the dividend and has net profits of ` 5,00,000 and makes new investments of `10 lakhs during the period, how many new shares must be issued ? Use the M.M. model.

Q. 7. Diamond Engineering Company has 10,00,000 equity shares outstanding at the start of the

accounting year 2003. The ruling market price per share is ` 150. The Board of Directors of the Company contemplates declaring ` 8 share as dividend at the end of the current year. The rate

of Capitalization appropriate to the risk-class to which the company belongs is 12%. (a) Based on Modigliani-Miller Approach, calculate the market price per share of the company

when the contemplated dividend is (i) declared and (ii) not declared. (b) How many new shares are to be issued by the company at the end of the accounting year

on the assumption that the Net Income for the year is ` 2 crores? Investment budget is ` 4 crores and (i) the above dividends are distributed and (ii) they are not distributed.

(c) Show that the total market value of the shares at the end of the accounting year will remain the same whether dividends are either distributed or not distributed. Also find out the current market value of the firm under both situations.

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 1 : REVISION NOTES – MAY ‘19

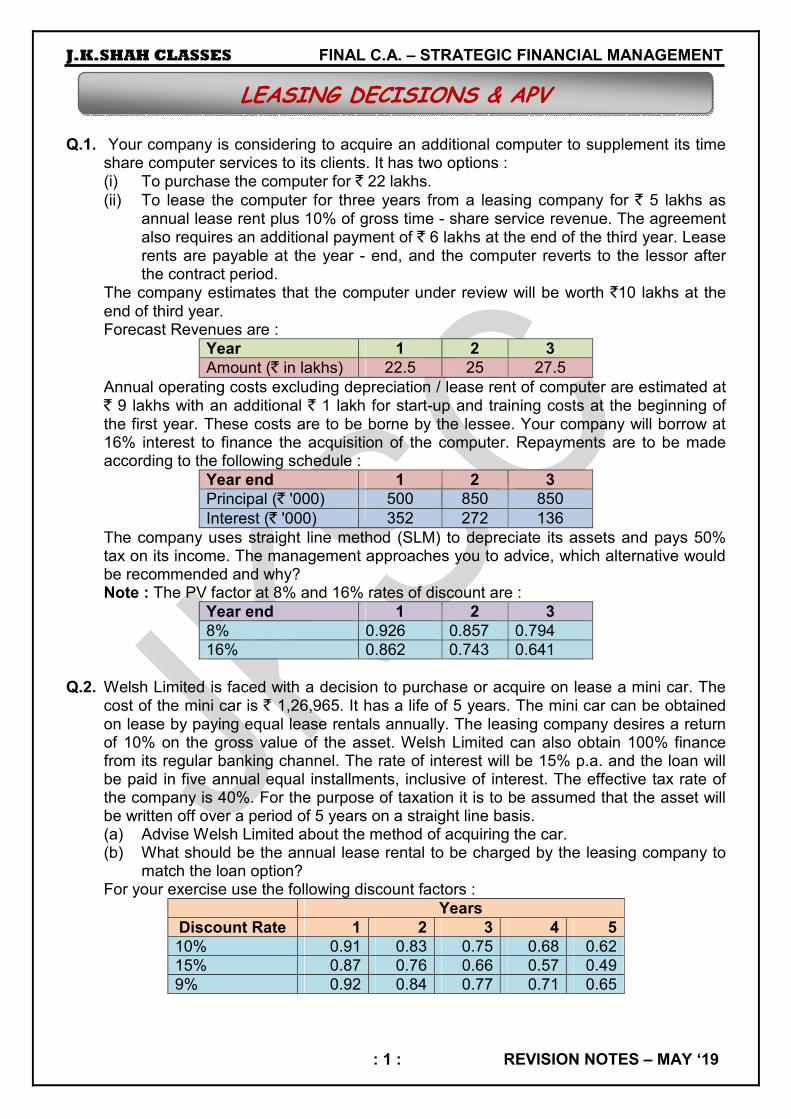

Q.1. Your company is considering to acquire an additional computer to supplement its time

share computer services to its clients. It has two options : (i) To purchase the computer for ` 22 lakhs.

(ii) To lease the computer for three years from a leasing company for ` 5 lakhs as annual lease rent plus 10% of gross time - share service revenue. The agreement also requires an additional payment of ` 6 lakhs at the end of the third year. Lease rents are payable at the year - end, and the computer reverts to the lessor after the contract period.

The company estimates that the computer under review will be worth `10 lakhs at the end of third year.

Forecast Revenues are :

Year 1 2 3

Amount (` in lakhs) 22.5 25 27.5

Annual operating costs excluding depreciation / lease rent of computer are estimated at ` 9 lakhs with an additional ` 1 lakh for start-up and training costs at the beginning of the first year. These costs are to be borne by the lessee. Your company will borrow at 16% interest to finance the acquisition of the computer. Repayments are to be made according to the following schedule :

Year end 1 2 3

Principal (` '000) 500 850 850

Interest (` '000) 352 272 136

The company uses straight line method (SLM) to depreciate its assets and pays 50% tax on its income. The management approaches you to advice, which alternative would be recommended and why?

Note : The PV factor at 8% and 16% rates of discount are :

Year end 1 2 3

8% 0.926 0.857 0.794

16% 0.862 0.743 0.641

Q.2. Welsh Limited is faced with a decision to purchase or acquire on lease a mini car. The

cost of the mini car is ` 1,26,965. It has a life of 5 years. The mini car can be obtained on lease by paying equal lease rentals annually. The leasing company desires a return of 10% on the gross value of the asset. Welsh Limited can also obtain 100% finance from its regular banking channel. The rate of interest will be 15% p.a. and the loan will be paid in five annual equal installments, inclusive of interest. The effective tax rate of the company is 40%. For the purpose of taxation it is to be assumed that the asset will be written off over a period of 5 years on a straight line basis. (a) Advise Welsh Limited about the method of acquiring the car. (b) What should be the annual lease rental to be charged by the leasing company to

match the loan option? For your exercise use the following discount factors :

Years

Discount Rate 1 2 3 4 5

10% 0.91 0.83 0.75 0.68 0.62

15% 0.87 0.76 0.66 0.57 0.49

9% 0.92 0.84 0.77 0.71 0.65

LEASING DECISIONS & APV

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 2 : REVISION NOTES – MAY ‘19

Q.3. Kuber Leasing Ltd. Is in the process of making out a proposal to lease certain equipment to a user – manufacturer. The cost of the equipment is expected to be ` 10 lakhs and the primary period of lease is to be 10 years. Kuber Ltd. gives you the following additional information :

• SLM over 10 years period is acceptable under the Income – tax Act.

• The current effective tax rate is 40% and is expected to lower to 30% from the beginning of the 6th year of lease.

• Cut off rate is 10%.

• Lessees need to pay 1% of the value of the asset as lease management and processing fee.

• Annual lease rentals are to be collected at the beginning of the year. Compute annual lease rent. Q.4. (a) The pre – tax expected rate of return for the Hypothetical Industries Ltd. (HIL) is 24

per cent for a five year non – cancellable lease. The annual lease rental would be stepped at 10 per cent over the period. Compute the lease rental per ` 1,000.

(b) Assume that the lease rentals are deferred for the first two years. Compute the lease rentals per ` 1,000.

(c) The lease rentals will be stepped up by 25 per cent and then by 40 per cent and subsequently stepped down in the reverse order in the fifty year. Compute the lease rental per ` 1,000.

Q.5. GMBH Ltd. is in software development business. It has recently been awarded a

contract from an Asian country for computerization of its all offices and branches spread across the country. This will necessitate acquisition of a super computer at a total cost of `10 crores. The expected life of computer is 5 years. The scrap value is estimated at `5 crore. However, this value could even be much lower depending upon the developments taken place in the field of computer technology.

A leasing company has offered a lease contract will total lease of `1.5 crore per annum for 5 years payable in advance will all maintenance costs being borne by lesee.

The other option available is to purchase the computer by taking loan from the bank with variable interest payment payable semi – annually in arrears at a margin of 1% per annum above MIBOR. The MIBOR forecast to be at a flat rate of 2.4% for each 6 month period, for the duration of loan.

Tax rate applicable to corporation is 30%. For taxation purpose, depreciation on computer is allowed at 20% as per WDV method, with a delay of 1 year between the tax depreciation allowance arising and deduction from tax paid.

You are required to calculate : (a) Compound annualized post tax cost of debt. (b) NPV of lease payment Vs. purchase decisions at discount rate of 4% and 5%. (c) The break – even post – tax cost of debt at which corporation will be indifferent

between leasing and purchasing the computer. (d) Which option should be opted for?

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 1 : REVISION NOTES – MAY ‘19

Q.1. Determine the Risk Adjusted Net Present Value of the following projects :

A B C

Net cash outlays (`) Project life Annual cash inflow (`) Coefficient of Variation

1,00,000 5 years 30,000

0.4

1,20,000 5 years 42,000

0.8

2,10,000 5 years 70,000

1.2

The company selects the risk – adjusted rate of discount on the basis of the Coefficient of Variation:

Coefficient of Variation

Risk adjusted rate of discount rate of discount

Present value factor 1 to 5 years at risk adjusted

0.0 10% 3.791

0.4 12% 3.605

0.8 14% 3.433

1.2 16% 3.274

1.6 18% 3.127

2.0 22% 2.864

More than 2.0 25% 2.689

Q.2. ABC and Co. is considering two mutually exclusive machines X and Y. The company

uses a Certainty Equivalent approach to evaluate the proposals. The estimated cash flow and certainty equivalents for both machines are as follows :

Machine X Machine Y

Year Cash flow Certainty Equivalent Cash flow Certainty Equivalent

0 1 2 3 4

` - 30,000 15,000 15,000 10,000 10,000

1.00 0.95 0.85 0.70 0.65

` - 40,000 25,000 20,000 15,000 10,000

1.00 0.90 0.80 0.70 0.60

Which machine should be bought, if the risk free discount rate is 5 per cent? Q.3. XYZ Ltd. is evaluating two equal size mutually exclusive proposals X and Y for which

the respective cash flows together with associated probabilities are as follows :

Project X Project Y

Cash Flows (`̀̀̀) Probabilities Cash Flows (`̀̀̀) Probabilities

2,000 0.3 1,000 0.1

4,000 0.4 3,000 0.1

6,000 0.3 5,000 0.4

7,000 0.3

9,000 0.1

Find out the risks of the proposals in terms of the standard deviation and coefficient of variation.

RISK ANALYSIS

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 2 : REVISION NOTES – MAY ‘19

Q.4. A company is considering investing in a new product with an expected life of three years. It is estimated that if the demand for the product is favourable in the first year, then it is certain to be favourable in the subsequent years. And if it is low in the first year, it would remain low in years 2 and 3. The company feels that cash flows over time are perfectly correlated. The cost of the project is ` 50,000 and the possible cash flows for three years are :

Year 1 Year 2 Year 3

Cash flow Probability Cash flow Probability Cash flow Probability

---- 0.10 ` 5,000 0.15 ---- 0.15

` 10,000 0.20 20,000 0.20 ` 7,500 0.20

20,000 0.40 35,000 0.30 15,000 0.30

30,000 0.20 50,000 0.20 22,500 0.20

40,000 0.10 65,000 0.15 30,000 0.15

Assume a risk free discount rate of 5 per cent. Calculate the expected value and standard deviation of the probability distribution of possible net present values. Assuming a normal distribution, what is the probability of the project providing a net present value of (i) zero or less (ii) ` 15,000 or more?

Q.5. A firm has an investment proposal, requiring an outlay of ` 40,000. The investment

proposal is expected to have 2 year's economic life with no salvage value. In year I there is a 0.4 probability that cash inflow after tax will be ` 25,000 and 0.6 probability that cash inflow after tax will be ` 30,000. The probabilities assigned to cash inflows after tax for the year II are as follows : The Cash inflow year I ` 25,000 ` 30,000 The Cash inflow year II Probability Probability ` 12,000 0.2 ` 20,000 0.4 ` 16,000 0.3 ` 25,000 0.5

` 22,000 0.5 ` 30,000 0.1 The firm uses a 10% discount rate for this type of investment. Required :

(a) Construct a decision tree for the proposed investment project. (b) What net present value will the project yield if worst outcome is realised? What is

the probability of occurrence of this NPV? (c) What will be the best and the probability of that occurrence? (d) Will the project be accepted? (10% Discount factor 1 year 0.909 2 year 0.826)

Q.6. A company in the North of a country is engaged in the manufacture and installation of a

new leisure activity. Progress has been made in creating a market. A short lease on its existing temporary premises will expire at the end of this year and will not be renewable.

Market research has shown that the demand for new installation is likely to end after a further eight years. In this period it is foreseen that in the first four years there is a 70% chance that new work will be mainly in the south. Thereafter there is a forecast reversal of demand source with a 60% chance of most new work originating in the north.

No suitable rented accommodation is available. The cost of premises is ` 3,00,000 in the north and ` 4,00,000 in the south. Of these sums, 20% is the cost of land and the remainder the cost of specialised buildings. The buildings will have no further use after eight years. The land is assumed to retain its original value and will be sold when it is no longer required for the project.

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 3 : REVISION NOTES – MAY ‘19

To relocate after four years would involve dismantling and re - erecting buildings, a loss of business during the changeover, staff transfers and variations in the cost of services. The overall cost at the end of year four would be :

North to south ` 1,50,000 South to north ` 1,00,000

The annual net cash flow for the company is expected to be `1,20,000. The extra cost of transport and communication expense would reduce this annual income by ` 40,000 a year if the premises were located in the area away from the major business.

The cost of capital to the company is 12% per annum. You are required, from the information given, to :

(a) Prepare a decision tree of the options open to the company ; (b) Decide on a net present value (NPV) basis which option is the most attractive

financially. Q.7. A company is considering a project involving the outlay of ` 3,00,000 which it estimates

will generate cash flows over its two - year life with the probabilities shown below.

Cash flows for project Year 1

Cash flow Probability

`̀̀̀

1,00,000 2,00,000 3,00,000

0.25 0.50 0.25

1.00

Year 2 If cash flow in Year 1 is : there is a probability of :

that cash flow in Year 2 will be:

`̀̀̀ `̀̀̀

1,00,000 0.25 0.50 0.25

Nil 1,00,000 2,00,000

1.00

2,00,000 0.25 0.50 0.25

1,00,000 2,00,000 3,00,000

1.00

3,00,000 0.25 0.50 0.25

2,00,000 3,00,000 3,50,000

1.00

All cash flows should be treated as being received at the end of the year. The company has a choice of undertaking this project at either of two sites (A or B)

whose costs are identical and are included in the above outlay. In terms of the technology of the project itself, the location will have no effect on the outcome.

If the company chooses sits B, it has the facility to abandon the project at the end of the first year and to sell the site to an interested purchaser for ` 1,50,000. This facility is not available at site A.

The company's investment criterion for this type of project is 10% DCF. Its policy would be to abandon the project on site B and to sell the site at the end of the year 1 if its expected future cash flows for year 2 were less than the disposal value.

Required : (a) Calculate the NPV of the project on site A.

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 4 : REVISION NOTES – MAY ‘19

(b) (i) Explain, based on the data given, the specific circumstances in which the company would abandon the project on site B.

(ii) Calculate the NPV of the project on site B taking account of the abandonment facility.

(c) Calculate the financial effect of the facility for abandoning the project on site B stating whether it is positive or negative.

Ignore tax and inflation. Q.8. An investor has two alternative proposals for evaluation on the basis of the following

information:

Project A Project B

Cash inflows Probability Cash inflows Probability

` 75,000

` 25,000

0.6 0.4

` 52,500 1

His utility function states that he will get utilities of 6, 4, 2 and 1 from the first ` 25,000,

second ` 25,000, third ` 25,000 and the fourth ` 25,000 respectively. Evaluate the proposals with and without utility function.

Q.9. TMC is a venture capital financier. It received a proposal for financing requiring an

investment of ` 45 crores which returns ` 600 crores after 6 years, if succeeds. However, it may be possible that the project may fail at any time during the six years.

The following table provide the estimates of probabilities of the failure of the projects.

Year 1 2 3 4 5 6

Probability of failure 0.28 0.25 0.22 0.18 0.18 0.10

In the above table, the probability that the project fails in the second year is given that it has survived throughout year 1. Similarly, for year 2 and so forth.

TMC is considering an equity investment in the project. The beta of this type of project is 7. The market return and risk free rate of return are 8% and 6% respectively.

You are required to compute the expected NPV of the venture capital project and advice of TMC.

: 6 :

J. K. SHAH CLASSES FINAL C.A. - STRATEGIC FINANCIAL MANAGEMENT

REVISION NOTES – MAY ‘19

TABLE : AREAS UNDER THE STANDARD NORMAL CURVE FROM 0 TO Z.

Z .00 .01 .02 .03 .04 .05 .06 .07 .08 .09

.0 .0000 .0040 .0080 .0120 .0160 .0199 .0239 .0279 .0319 .0359

.1 .0398 .0438 .0478 .0517 .0557 .0596 .0636 .0675 .0714 .0753

.2 .0793 .0832 .0871 .0910 .0948 .0987 .1026 .1064 .1103 .1141

.3 .1179 .1217 .1255 .1293 .1331 .1368 .1406 .1443 .1480 .1517

.4 .1554 .1591 .1628 1664 .1700 .1736 .1772 .1808 .1844 .1879

.5 .1915 .1950 .1985 .2019 .2054 .2088 .2123 .2157 .2190 .2224

.6 .2257 .2291 .2324 .2357 .2389 .2422 .2454 .2486 .2518 .2549

.7 .2580 .2612 .2642 .2673 .2704 .2734 .2764 .2794 .2823 .2852

.8 .2881 .2910 .2939 .2967 .2995 .3023 .3051 .3078 .3106 .3133

.9 .3159 .3186 .3212 .3238 .3264 .3289 .3315 .3340 .3365 .3389

1.0 .3413 .3438 .3461 .3485 .3508 .3531 .3554 .3577 .3599 .3621

1.1 .3643 .3665 .3686 .3708 .3729 .3749 .3770 .3790 .3810 .3830

1.2 .3849 .3869 .3888 .3907 .3925 .3944 .3962 .3980 .3997 .4015

1.3 .4032 .4049 .4066 .4082 .4099 .4115 .4131 .4147 .4162 .4177

1.4 .4192 .4207 .4222 .4236 .4251 .4265 .4279 .4252 .4306 .4319

1.5 .4332 .4345 .4357 .4370 .4382 .4394 .4406 .4418 .4429 .4441

1.6 .4452 .4463 .4474 .4484 .4495 .4505 .4515 .4525 .4535 .4545

1.7 .4554 .4564 .4573 .4582 .4591 .4599 .4608 .4616 .4625 .4633

1.8 .4641 .4649 4656 .4664 .4671 .4678 .4686 .4693 .4699 .4706

1.9 4713 .4719 .4726 .4732 .4738 .4744 .4750 .4756 .4761 .4767

2.0 4772 .4778 .4783 .4788 .4793 .4798 .4803 4808 .4812 .4817

2.1 .4821 4826 .4830 .4834 .4838 .4842 .4846 .4850 .4854 .4857

2.2 4861 4864 .4868 .4871 .4875 .4878 .4881 .4884 .4887 4890

2.3 .4893 .4896 .4898 .4901 .4904 .4906 .4909 .4911 .4913 .4916

2.4 .4918 .4920 .4922 .4925 .4927 .4931 .4931 .4932 .4934 .4936

2.5 .4938 .4940 .4941 .4943 .4945 .4946 .4948 .4949 .4951 .4952

2.6 .4953 .4955 .4956 .4957 .4959 .4960 .4961 .4962 .4963 .4964

2.7 4965 .4966 .4967 .4968 .4969 .4970 .4971 .4972 .4973 .4974

2.8 .4974 .4975 .4976 .4977 .4977 .4978 .4979 .4979 .4980 .4981

2.9 .4981 .4982 .4982 .4983 .4984 .4984 .4985 .4985 .4986 .4986

3.0 .49865 .4987 .4987 .4988 .4988 .4989 .4989 .4989 .4990 .4990

4.0 .4999683

IIIustration: For Z = 1.72, shaded area is .4573 out of total area of 1.

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 1 : REVISION NOTES – MAY ‘19

Foreign currency and foreign exchange : • In the context of India, any currency other than Indian rupees is foreign currency. • Foreign exchange includes currency, drafts, bills, letters of credits and traveler cheques

which are denominated and ultimately payable in foreign currencies What is a foreign exchange market : • The foreign exchange market is a decentralized worldwide market. • The participants in the foreign exchange market include central banks, commercial

banks, brokers etc. • The central banks monitor market movements and sentiments and intervene according to

government policy. • The function of buying and selling of foreign currencies in India is performed by

authorized dealers / moneychangers appointed by the RBI. • The foreign exchange department of the major banks are linked across the world on a 24

hour basis. • Major commercial centers are London, Amsterdam, Frankfurt, Milan, Paris, New York,

Toronto, Bahrain, Tokyo, Hong Kong and Singapore. Briefly describe the functions of a foreign exchange market : • Purchasing power is transferred across different countries which will enhance the

feasibility of international trade and overseas investments • The foreign exchange market acts as a central focal point wherein prices of various

currencies are discovered. • Enables the investors to hedge or minimize their risks • Enables the traders to arbitrage any inequalities • Provides an investment / trading avenue to entities who are willing to expose themselves

to this risk. What are the Determinants of Exchange rate

FOREIGN EXCHANGE RISK MANAGEMENT

Interest rate parity

Purchasing Power Parity

Balance of payment position

Government Intervention

Market Expectation

Overseas Investment

Speculation

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 2 : REVISION NOTES – MAY ‘19

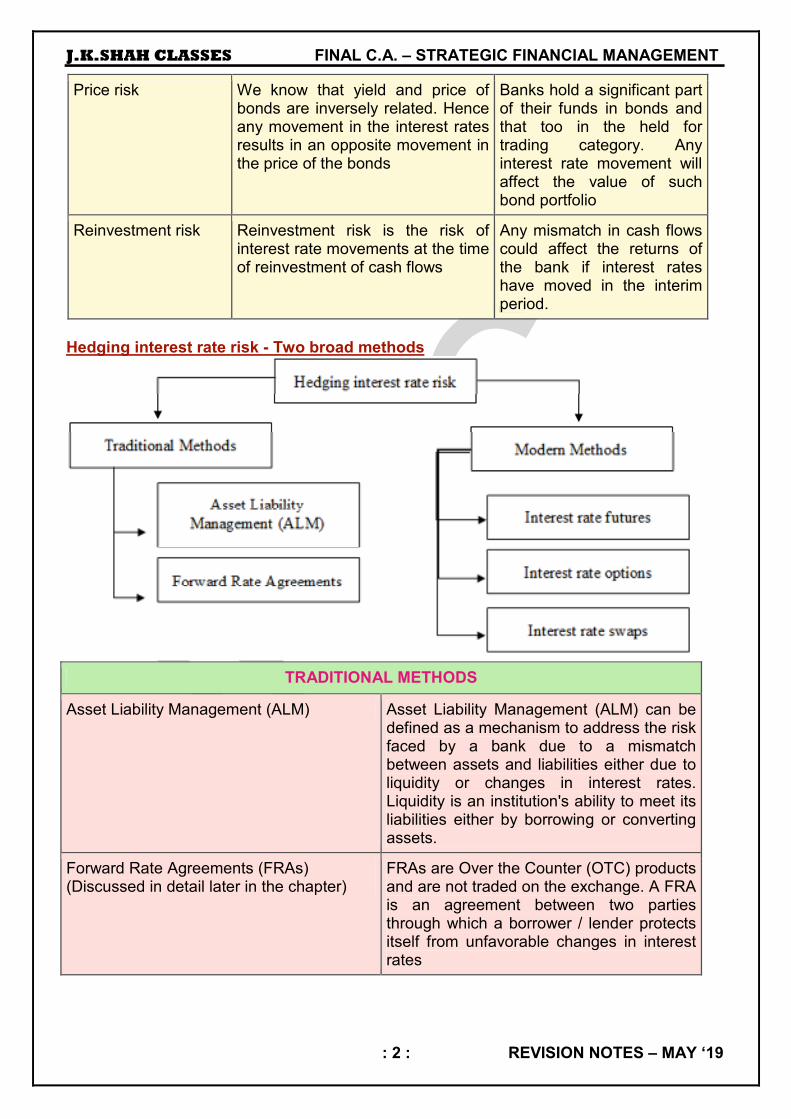

A. Interest Rate Parity theorem: (IRP)

As per IRP “the size of the forward premium (or discount) should be equal to the interest rate differential between the two countries concerned”. When IRP exists, covered interest arbitrage is not feasible because any interest rate differential advantage will be offset by the discount on the forward rate. Thus, the act of covered interest arbitrage would a return that is no higher that what would be generated by a domestic investment.

B. Purchasing power parity (Inflation) theorem

• Difference in inflation rates between two countries is considered as the most important factor for variations in exchange rates.

• If domestic inflation is high, it means domestic goods are costlier than foreign goods. This results in higher imports creating more demand for foreign currency, making it costlier. (In other words the value of domestic currency will decline).

• If a basket of goods cost Rs470 in India and $10 in US then it is quite natural that the exchange rate should be Rs47/$1

• PPP theory can be expressed by the formula: PPPr = Spot rate (1+rh)

(1+rf) where rh is inflation rate at home; rf is the inflation rate of foreign country

Weakness of PPP theory : It is not only inflation, which affects foreign currency movements. PPP ignores substitution effects – i.e. instead of importing goods might be substituted. C. Balance of payments position : • The BOP position has a big impact on the value of a nation’s currency. • A big or consistent deficit would mount a pressure on the currency of a nation as

deficits require payments in foreign currency. • In the case of a fixed currency rate scenario – the local currency would be devalued

thereby making imports costlier and exports cheaper. • However in the free rate scenario a big or consistent deficit would be a forewarning

for depreciation of a nations currency

D. Government intervention : At times the government would intervene by purchasing or selling foreign exchange to

control pressures on the nation’s currency. F. Market expectation : Market expectation as regards interest rates, inflation, taxes, BOP positions etc would

affect the foreign exchange rates. G. Overseas investment : Overseas Investment flows have an impact of foreign exchange rate. E.g. if US

investments in India increases there would be dollar inflows putting downward pressure on dollar in India.

H. Speculation : Speculators including treasury managers of banks, by virtue of their buying and selling,

tend to influence the rates.

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 3 : REVISION NOTES – MAY ‘19

I. International Fisher Effect (IFE)

IFE uses interest rate rather than inflation rate differentials to explain why exchange rate change over time, but it is closely related to Purchasing Power Parity theory because interest rates are often highly co-related with inflation rates.

According to IFE “ nominal risk free interest rate contain a real rate of return and anticipated inflation”. This mean if investors of all countries required the same real rate of return, interest rate differentials between countries may be the result of differentials in expected inflation

What do you mean by Direct and Indirect quotes :

Direct quotes:

• Number of units of the domestic currency per unit of foreign currency

• E.g. 1$ = Rs 49.50 is a dollar direct quote of an Indian rupee in India. However the same quote when quoted in US is not a direct quote for an American.

Indirect quotes:

• Number of units of a foreign currency per fixed number of domestic currency;

• E.g. Rs 100 = $0.2245

What is Two way quotes

Bid price and offer price

• Bid is the price at which a dealer is willing to buy another currency and offer is the rate at which he is willing to sell the currency.

• E.g. a quote of Rs /$ is Rs42,50 / 42.55 it means that the dealer will buy $ at Rs 42.50 and sell dollar at 42.55

Spreads

• Spread is the difference between the bid rate and the offer rate and usually represents the profit margins that a dealer expects to make.

What is meant by Cross currency rates

• In India all buy and sell transactions are routed through the US $.

• Hence all deals involving any other currency would necessarily involve converting in US$ and then converting the US$ into INR.

• Thus if an Indian importer wishes to buy Yen he would first have to sell rupees and buy dollar; then he would sell dollar and buy yen.

• The banker would obtain the Yen / $ rate from Singapore or Tokyo and then apply the Rs /$ rate to determine the amount of rupees required to buy the desired Yen.

Spot rate, Forward rate, cash rate and Tom rate :

1. Spot rate : Rate quoted for transactions that will settled two business days from the transaction date (T+2)

2. Forward rate : Rate quoted for transactions that will be settled beyond two business days at a mutually agreed rate and date.

3. Cash rate : Rate quoted for transactions that will settled on the same day (T+0)

4. Tom rate : Rate quoted for transactions that will be settled in one business day form the date of transaction (T+1)

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 4 : REVISION NOTES – MAY ‘19

What is Appreciation and depreciation of currency : (A) Appreciation:

• A currency is said to have appreciated if it is able to purchase more of the other currency.

• E.g. if Rs /$ is 1$ = Rs45 and it changes to 1$ = Rs46 then dollar is said to have appreciated.

(B) Depreciation : • A currency is said to have depreciated if it is able to purchase less of the other

currency. • E.g. if Rs /$ is 1$ = Rs45 and it changes to 1$ = Rs44 then dollar is said to have

depreciated and rupee appreciated. What do mean by Premium and discount : • Premium :

➢ A currency is said to be at a premium if it is more expensive in the forward than in the spot

➢ If Rs / $ spot is 44.95/45.00 and 3 month forward is 45.2045.25 we say that dollar is at a premium

• Discount

➢ A currency is said to be at a discount when it is quoting higher in the spot and cheaper in the forward.

Briefly describe Arbitrage and the kinds of arbitrage operations Arbitrage means buying in one market & selling in another to take advantage of price differential For example a customer can make profits by purchase of dollars in one market where it is available at a cheaper rate and sell the dollars in another market (directly or through other currencies) at a higher rate. There are three types of arbitrages that are dominant in the market : 1. Geographical arbitrage : Buying currency in say London market & selling it in say

Tokyo 2. Triangular arbitrage : Involves three currencies and three markets (also known as

three point arbitrage) 3. Spot - forward Arbitrage (also known as Interest rate arbitrage) If the spot rate +

interest is greater or less than the forward rate there exists an arbitrage potential.

What are the various foreign currency accounts maintained by Banks : 1. Nostro Account : Nostro means “our account with you” Nostro account is the account maintained by the Bank in India with the bank

abroad. E.g. PNB may maintain a bank account with Citibank, New York. Such account

would obviously in dollars. All foreign exchange transactions routed through Nostro Accounts.The concept of Nostro Account and Exchange Position is explained in details towards the end of the notes.

2. Vostro Account : Vostro means “your account with us”. E.g. Citibank New York may maintain a Rupee account with SBI 3. Loro Account : Loro means “their account with you” E.g. SBI has an account with Citibank New York. When Syndicate Bank refers to

this account in any correspondence with Citibank New York it would refer it as Loro account.

J.K.SHAH CLASSES FINAL C.A. – STRATEGIC FINANCIAL MANAGEMENT

: 5 : REVISION NOTES – MAY ‘19

Nostro Account and Exchange Position Explained.

Nostro Account refers to “Our Account with you”. For example if Bank of Baroda maintains a Dollar Account with CITIBANK (US), Bank of Baroda will refer it to as Nostro A/c : Citibank(US) meaning our account with Citibank. A Nostro A/c is a current account - no interest is earned on the balance kept in the account; but if the account is overdrawn then interest is charged.

The account is prepared in the books of the bank in which the account is maintained.A Nostro a/c is very similar to a passbook maintained by a customer in a bank - Hence actual inflow of foreign currency will be credited to the account and outflow will be debited.

Terms used with reference to Nostro A/c

Telegraphic Transfer (TT) - A mode of immediate transfer of funds (earlier done through telegrams / telex - now done online)

TT issuance / TT Sale / TT remittance: Suppose a customer of Bank of Baroda requires BoB to transfer immediately $100,000 to his associate in US. He will pay the Rupee equivalent to BoB (India) and BoB will instruct CITIBANK (US) to hand out $100,000 to the associate. In such a case CITIBANK (US) after handing out $100,000 will debit the Nostro A/c

TT payment / TT Purchase: Mr.Rastogi (a US citizen) remits $10,000 to his brother Ram in India. Ram will approach BoB which will hand out the Rupee equivalent of $10,000. BoB in turn will receive $10,000 from Mr Rastogi’s banker. Hence in this case $10,000 will be credited to the Nostro A/c

DD Payment / Encashment of DD/ DD Purchase: Desi Indian Ltd receives a DD of $5000 issued in its favour from Washington. Desi Indian Ltd will approach BoB to encash the DD - BoB will hand over the Rupee Equivalent of $5,000 and in turn will encash the DD of $5000. Hence the Nostro A/c will be credited.

DD issuance: Mr Bharat of New Delhi approaches BoB to get a DD issued for $1000 in favour of a supplier payable at Boston (USA). The Bank charges Rs.68000 and issues the DD. This transaction won’t be entered in the Nostro A/c on the date of issuance of DD. It will be entered on the day the amount of DD is paid. On that day the Nostro A/c will be debited with $1000