Embed Size (px)

Citation preview

BUSINESS &. FINANCE

Eye on the Future Chemical industry officials find rising costs put cr imp in earn ings —but not in expansion plans

Vv HEN CHEMICAL COMPANIES eye their current problems and take a look at future prospects, they often find they have mu<;h t h e same outlook. This was underscored last week, when top-level executives of three leading chemical firms rpiit tHeir companies' operations in the spotlight for the benefit of financial analysts i n Cleveland, Ohio. All three firins-Dow, Diamond Alkali, and Hooker Electrochemical—see no slackening in sales or i n expansion spending. But risiag costs, both for day-to-day operation and for getting new plants into profitable production, may very likely pat: a l i d on higher earnings, at least for awhile.

Diamond Alkal i president John A. Sargent a.dmits that results in this year's first quarter—when Diamond's profits slipped t o 84 cents a share from $1.02 earned a. year before—were quite disappointing. Current operations, he hastens "to add , are somewhat more encouraging. But Sargent sees 1957 as a year "of consolidation and preparation of a base for future growth." Unless demand increases from producers of consumer goods (which take about 90% of Diamond's ou tpu t ) , "we do not anticipate that earnings will exceed 1956," hie told t he annual convention of the National Federation of Financial Analysts Societies. " In fact, we will be hard pressed to avoid a modest decline."

• More for the Future. One burden on Diamond's current earnings is its construction program. The company has earmarked more than $20 million in capital spending for this year alone, plans to invest between $60 million and $80 million b y the end of 1960. Most of this rrioney will go to expand output of Diamond's cirrrent product lines and to modernize its Painesville, Ohio, plant and boost s o d a ash capacity there. Outlays will be broken down on a divisional basis as follows:

Electro chemicals 3 8 % Chlorin*ated products 26% Soda products 14% Plastics 6.5% Cementt-coke 6% Chromium chemicals 6% Silicate, detergent, calcium 3.5%

Although the costs incident to its construction program are a drag on earnings, Diamond is optimistic about long-range benefits. It is setting its sights on a sales volume of $160 million to $180 million by 1960. (Last year the company grossed $121 million.) Looking even further ahead, chairman Raymond F. Evans sees sales of about $250 million by 1965 if Diamond merely holds onto its present position in the industry. And if it can maintain its recent growth rate, volume could hit $350 million by then.

• Fighting Against Costs. Hooker, too, is fighting an upstream battle against rising costs. Chairman R. Lindley Murray estimates that increased expenses, coupled with higher depreciation charges and nonrecurring items, "cost us about 25 cents a share in 1956" compared with 1955. "It now appears that the corresponding figure for 1957 against 1956 will be around 20 cents a share," he adds.

Hooker's first-quarter sales were down slightly from the same period of 1956, largely as a result of lower production and inventorv reductions by customers. "The pickup has not developed as much or as soon as we had expected," Murrays admits, "but we believe that our actual sales for the year will show a small increase over 1956."

About 80% of the $15 million or

more Hooker has slated for capital expenditures in each of the next five years will go to increase production, sales, and efficiency. The remainder will be spent on improvements aimed at giving better products and service to customers. Spending will be broken down this way among various Hooker plants:

Niagara Falls, Ν. Υ. 4 0 % Durez (two plants) 22% Oldbury (two plants) 12% Montague, Mich. 12% Tacoma, Wash. 2% North Vancouver, B. C. 12% A large share of the expansion pro

gram will be used to up Hooker's capacity for such basic products as caustic soda, chlorine, potash, phosphates, and chlorates—much of which will go for Hooker's own use.

• Burden of Capital Spending. Dow sank $150 million into new plant and property during its fiscal year just ended and may spend even more in the year ahead, president Leland Doan told the security analysts' meeting. With depreciation charges expected t o add up to about $85 million in the current fiscal year—and as much as $100 million by fiscal 1961—Dow does not expect to need outside financing to carry out its expansion program.

But rising capital outlays have held down earnings. Doan estimates that Dow upped sales to a record $625 million in the year ended May 31 from a volume of $565 million in fiscal 1956. Earnings he puts at somewhere above $50 million, compared with last year's net of nearly $60 million.

Dow and the chemical industry as a whole is not making enough money, adds treasurer Carl Gerstacker; earnings per share of common stock have not increased as fast as they should. And because of the expenses involved in expansion, Gerstaker believes Dow's earnings may tend to stabilize for awhile. •

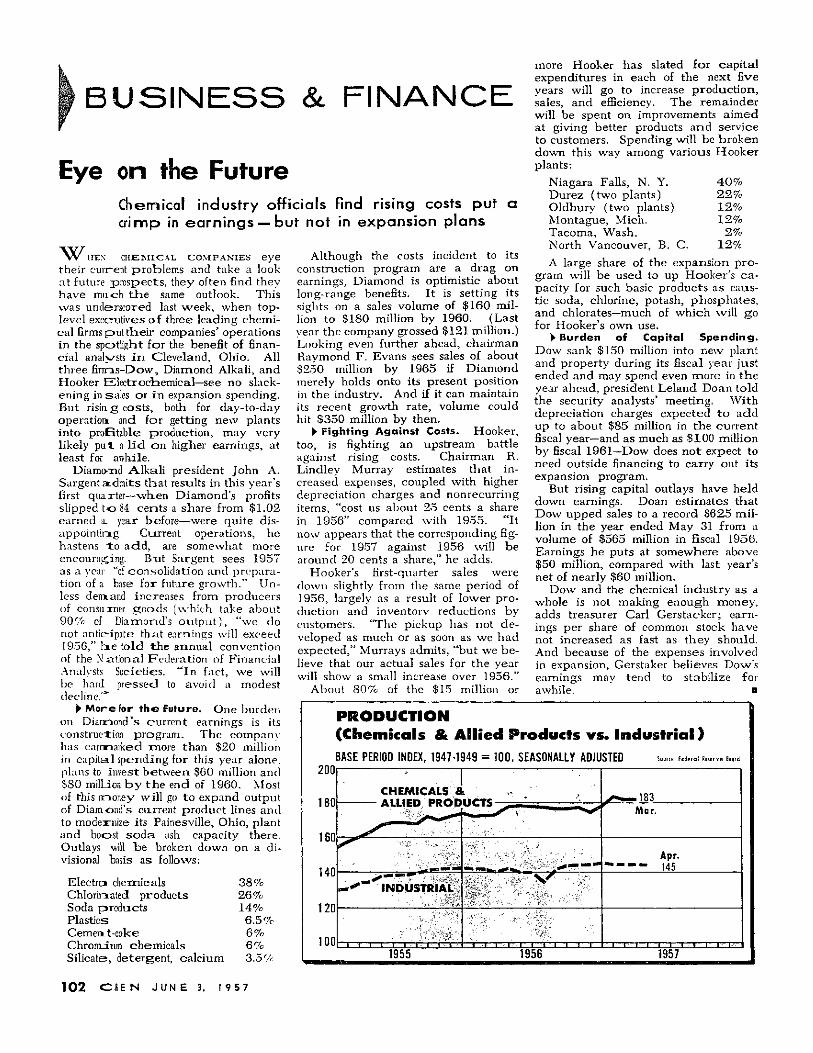

200|

PRODUCTION (Chemicals & Al l ied Products vs· Industr ie! ) BASE PERIOD INDEX, 1947-1949 = 100. SEASONALLY ADJUSTED Source. Federal Reserve Board

120

100,

CHEMICALS & ALLIED PRODUCTS

U ^ - * INDUSTRIAL

1 1 i l 1955

f i l l l Z 1956

t I I I 1957

- ι , ιί!-μί

1 0 2 GSE Ν JUN Ε 3. I 9 5 7