Embed Size (px)

Citation preview

EY Taxation of Investment Funds Symposium 201411 September 2014

Page 1

WELCOME!

Investment Structures

Page 3

Investment Fund Structures

Traditional investment pooling vehicles:► Commercial Trusts

► Unit Trusts ► Mutual Fund Trusts

► Corporations► Mutual Fund Corporations

Specific products:► Exchange Traded Funds (ETFs)

Page 4

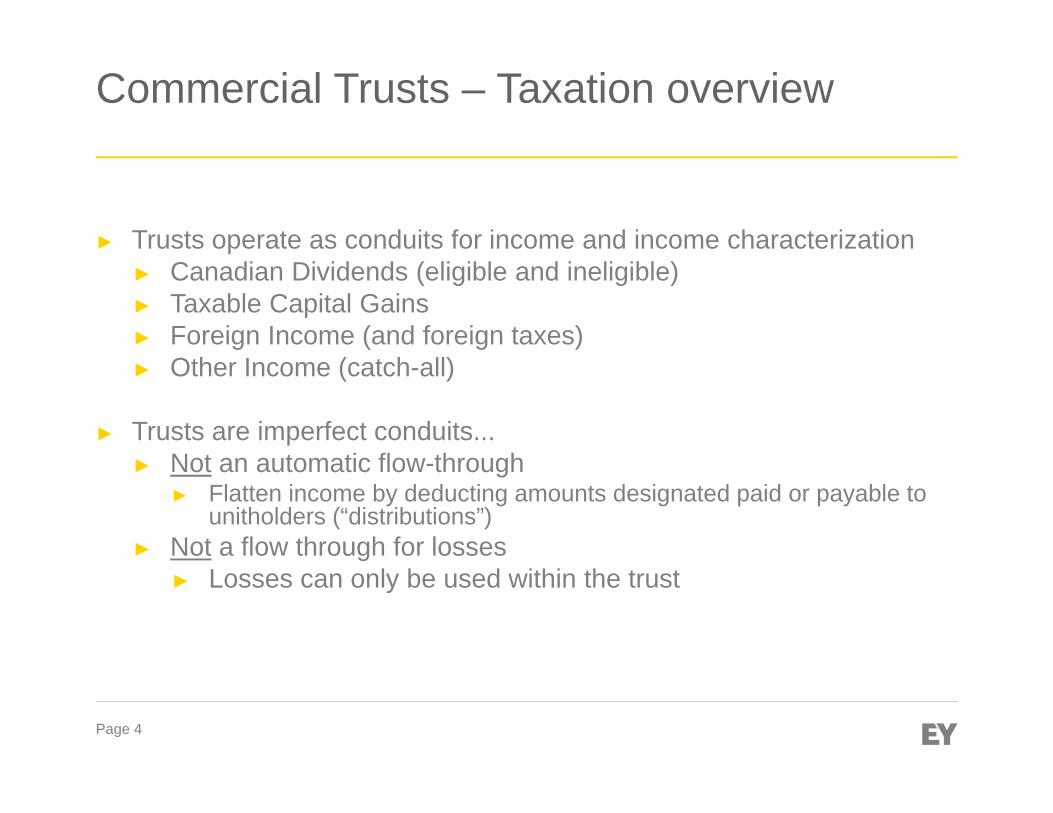

Commercial Trusts – Taxation overview

► Trusts operate as conduits for income and income characterization► Canadian Dividends (eligible and ineligible)► Taxable Capital Gains► Foreign Income (and foreign taxes)► Other Income (catch-all)

► Trusts are imperfect conduits...► Not an automatic flow-through

► Flatten income by deducting amounts designated paid or payable to unitholders (“distributions”)

► Not a flow through for losses► Losses can only be used within the trust

Page 5

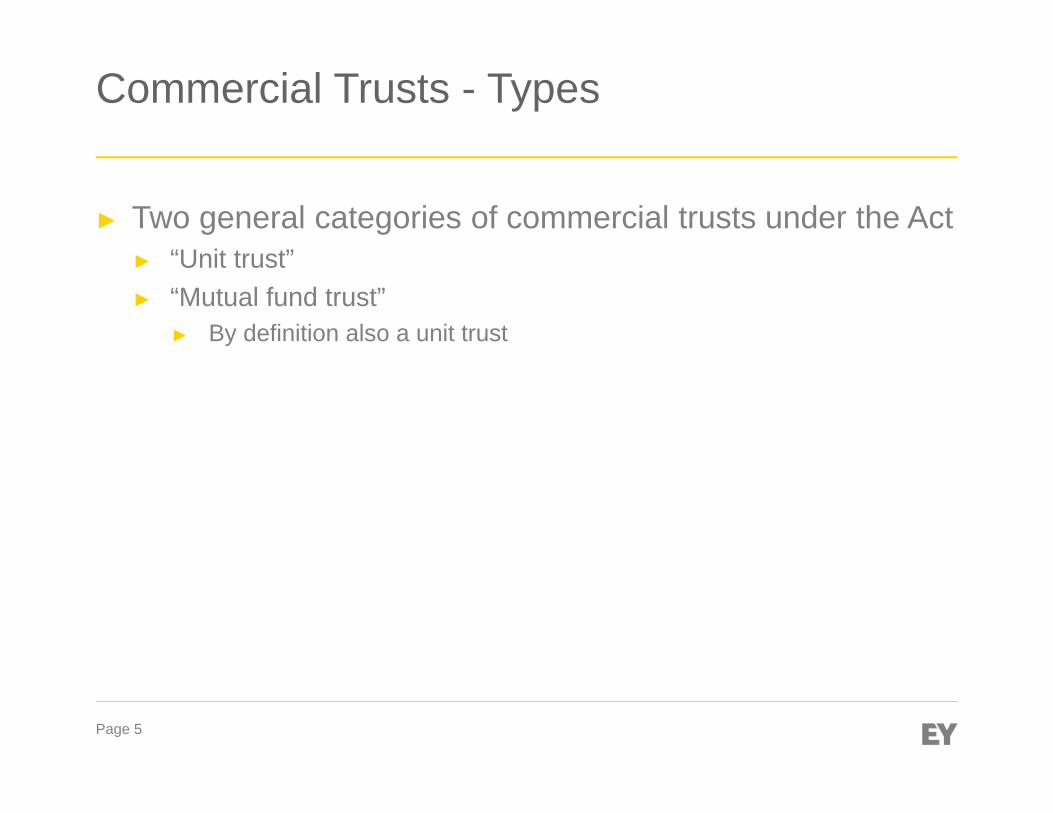

Commercial Trusts - Types

► Two general categories of commercial trusts under the Act► “Unit trust” ► “Mutual fund trust”

► By definition also a unit trust

Page 6

Unit Trusts – Open-ended

► Qualifies as an open-ended unit trust if, at any time:1. it is an inter vivos trust;

2. the interest of each beneficiary is described by reference to units of the trust, and

3. at least 95% of the fair market value of all issued units of the trust are units that have conditions attached thereto requiring the trust to accept, at the demand of the holder thereof and at the price determined and payable in accordance with the conditions, the surrender of units that are fully paid

Page 7

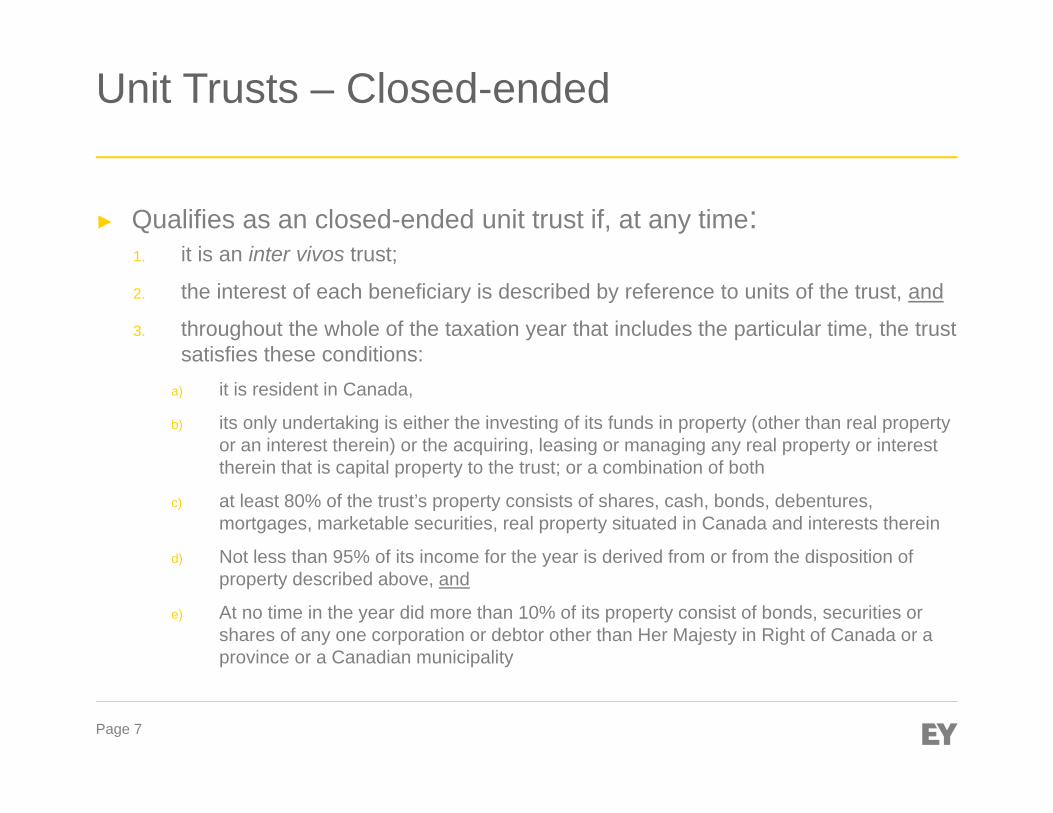

Unit Trusts – Closed-ended

► Qualifies as an closed-ended unit trust if, at any time:1. it is an inter vivos trust;

2. the interest of each beneficiary is described by reference to units of the trust, and

3. throughout the whole of the taxation year that includes the particular time, the trust satisfies these conditions:

a) it is resident in Canada,

b) its only undertaking is either the investing of its funds in property (other than real property or an interest therein) or the acquiring, leasing or managing any real property or interest therein that is capital property to the trust; or a combination of both

c) at least 80% of the trust’s property consists of shares, cash, bonds, debentures, mortgages, marketable securities, real property situated in Canada and interests therein

d) Not less than 95% of its income for the year is derived from or from the disposition of property described above, and

e) At no time in the year did more than 10% of its property consist of bonds, securities or shares of any one corporation or debtor other than Her Majesty in Right of Canada or a province or a Canadian municipality

Page 8

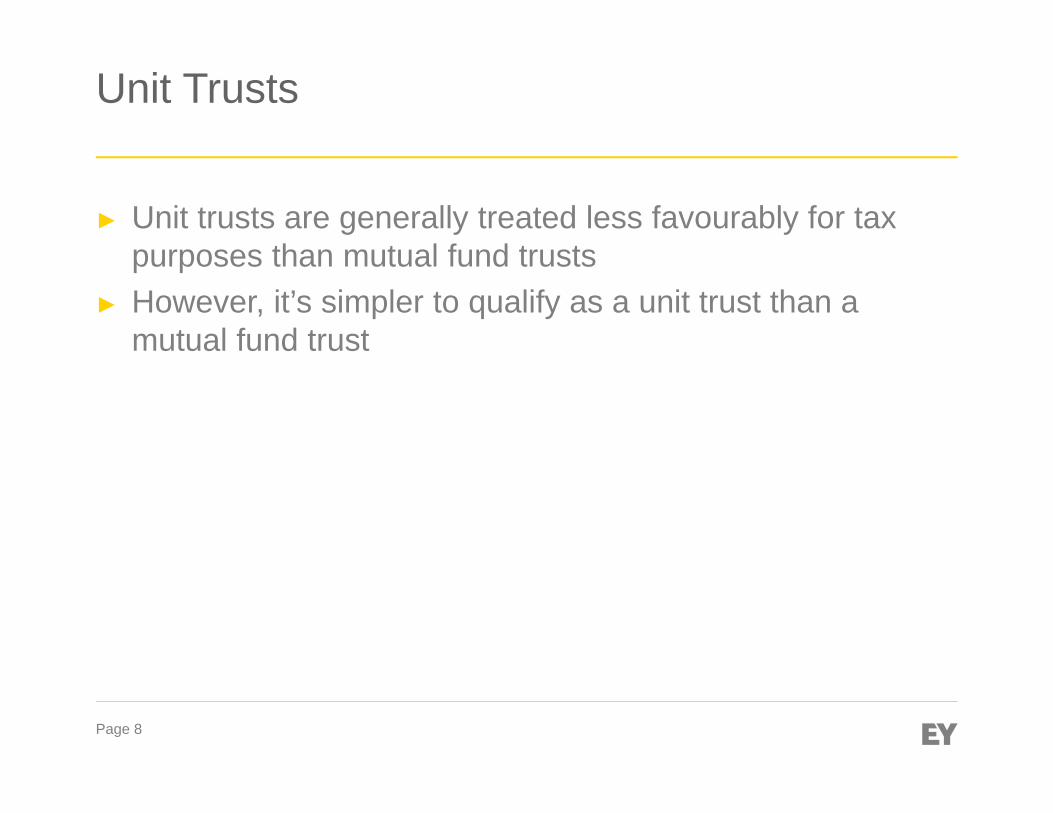

Unit Trusts

► Unit trusts are generally treated less favourably for tax purposes than mutual fund trusts

► However, it’s simpler to qualify as a unit trust than a mutual fund trust

Page 9

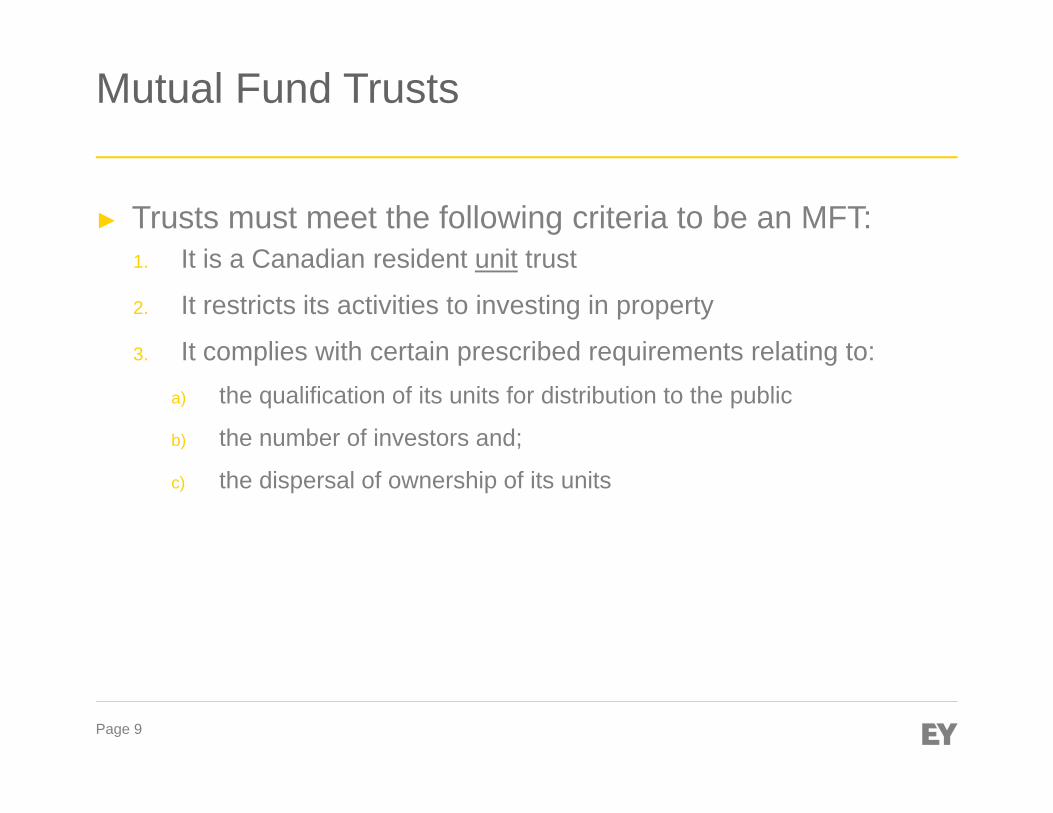

Mutual Fund Trusts

► Trusts must meet the following criteria to be an MFT:1. It is a Canadian resident unit trust

2. It restricts its activities to investing in property

3. It complies with certain prescribed requirements relating to:a) the qualification of its units for distribution to the public

b) the number of investors and;

c) the dispersal of ownership of its units

Page 10

Mutual Fund Trusts – RequirementsInvesting in property

► Only undertaking must be the investing of its funds in property► In addition to typical investments, CRA views that acceptable activities include

► Futures, forwards, options on commodities, stocks, bonds and FX

► Securities lending, repos, shorts

► The Act does not provide any guidance in interpreting the investing undertaking requirement and the courts do not appear to have addressed this issue.

► The requirement appears in certain other provisions in the Act dealing with such issues as provisions concerning unit trusts, mortgage investment corporations and MFCs. So that, CRA’s interpretation of these contexts may provide some guidance on the way it would apply the requirement in determining MFT status.

Page 11

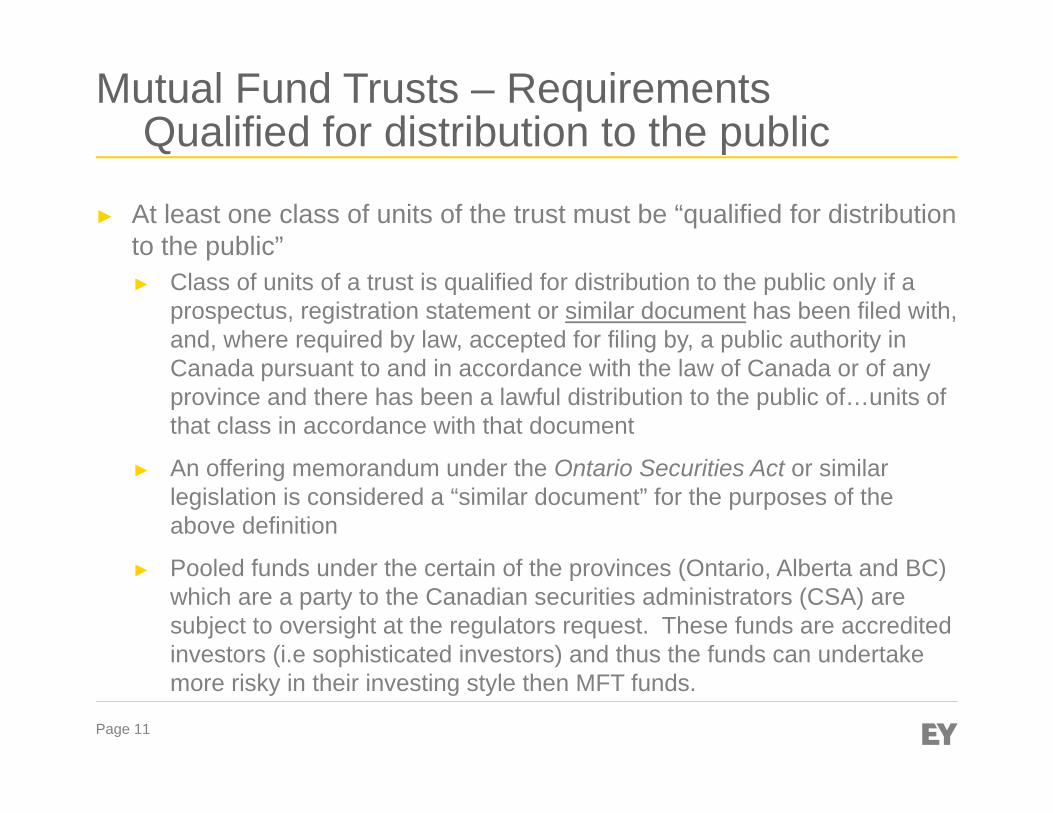

Mutual Fund Trusts – RequirementsQualified for distribution to the public

► At least one class of units of the trust must be “qualified for distribution to the public”► Class of units of a trust is qualified for distribution to the public only if a

prospectus, registration statement or similar document has been filed with, and, where required by law, accepted for filing by, a public authority in Canada pursuant to and in accordance with the law of Canada or of any province and there has been a lawful distribution to the public of…units of that class in accordance with that document

► An offering memorandum under the Ontario Securities Act or similar legislation is considered a “similar document” for the purposes of the above definition

► Pooled funds under the certain of the provinces (Ontario, Alberta and BC) which are a party to the Canadian securities administrators (CSA) are subject to oversight at the regulators request. These funds are accredited investors (i.e sophisticated investors) and thus the funds can undertake more risky in their investing style then MFT funds.

Page 12

Mutual Fund Trusts – Grandfathering Rules for “old” Unit Trusts

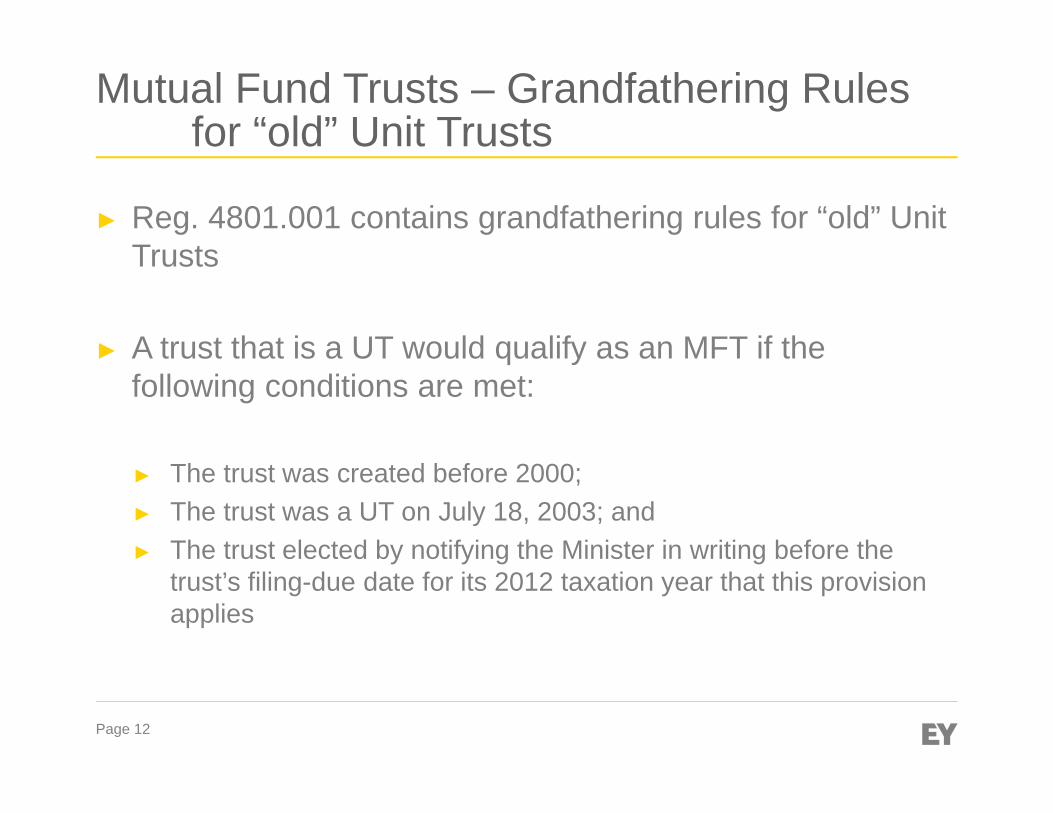

► Reg. 4801.001 contains grandfathering rules for “old” Unit Trusts

► A trust that is a UT would qualify as an MFT if the following conditions are met:

► The trust was created before 2000;► The trust was a UT on July 18, 2003; and► The trust elected by notifying the Minister in writing before the

trust’s filing-due date for its 2012 taxation year that this provision applies

Page 13

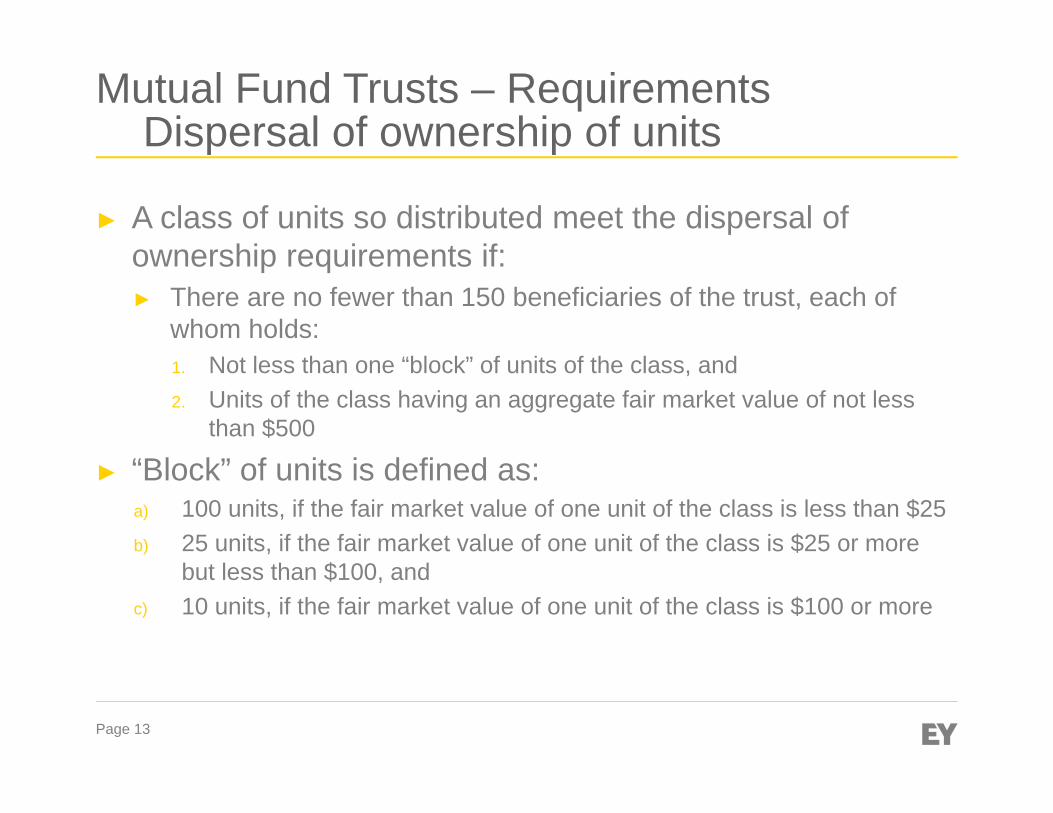

Mutual Fund Trusts – RequirementsDispersal of ownership of units

► A class of units so distributed meet the dispersal of ownership requirements if:► There are no fewer than 150 beneficiaries of the trust, each of

whom holds:1. Not less than one “block” of units of the class, and2. Units of the class having an aggregate fair market value of not less

than $500

► “Block” of units is defined as:a) 100 units, if the fair market value of one unit of the class is less than $25b) 25 units, if the fair market value of one unit of the class is $25 or more

but less than $100, andc) 10 units, if the fair market value of one unit of the class is $100 or more

Page 14

Benefits of Mutual Fund Trusts

► Access to the Capital Gains Refund Mechanism (CGRM)► Exempt from classification as a “financial institution” ► Elect for December 15th year end► Guaranteed subsection 39(4) election re: gains on

“Canadian Securities”► Exempt from Alternative Minimum Tax► Exempt from XII.2 special tax on Designated Beneficiaries

(i.e. non-residents)► Least restrictive conditions to obtain status of registered

investments

Page 15

Benefits of Mutual Fund Trusts

► Ordinarily not “taxable Canadian property” to non-resident investors

► Automatically a “qualified investment” eligible to be held by deferred plans ► RRSPs, RRIFs, DPSPs, RSDPs, RESPs and TFSAs

Page 16

Election to be a Mutual Fund Trust – Year of inception

► Certain benefits afforded under the Act require a trust to be a Mutual Fund Trust throughout a taxation year

► Although the trust will not meet the dispersal of ownership test at inception, it may be deemed to be a Mutual Fund Trust throughout the first taxation year if:► It meets all of the prescribed requirements to be an Mutual Fund

Trust before the 91st day after the end of its first taxation year, and

► The trust makes an election in its T3 return for its first taxation year

Page 17

Deemed to be a Mutual Fund Trust – Year of termination

► In year of termination, fund likely to lose Mutual Fund Trust status and therefore would not be considered to be an MFT throughout the year

► Act deems the fund to be a Mutual Fund Trust throughout the year if:1. The trust was a Mutual Fund Trust at the beginning of the year2. At any time in the year the trust ceased to be an Mutual Fund

Trust because:a) failed to meet the redemption requirement in order to be an open-

ended unit trustb) failed to comply with the dispersal requirementsc) it ceased to exist

3. The trust would otherwise have been a Mutual Fund Trust throughout the period it was in existence

Page 18

Mutual Fund Corporations – Taxation overview

► Mutual Fund Corporations operate as partial conduits for income and income characterization► Canadian Dividends► Taxable Capital Gains

► Mutual Fund Corporations are imperfect conduits...► Not a flow-through for:

► Foreign Income► Other Income (i.e. Interest)

► Not an automatic flow-through► Flow through by payment of taxable and capital gains dividends

► Not a flow through for losses► Losses can only be used within corporation

Page 19

Mutual Fund Corporations – Taxation overview► Legally formed as a corporate entity

► Stand alone ► Split share ► Corporate class

► Corporate class structures can offer multiple classes of shares as separate funds► Tax free switching by investor between classes► Can invest direct or fund on fund- be careful of where expenses are incurred

► Taxed as a single legal entity despite treatment as separate “funds”► Co-mingling of tax attributes across classes► Must develop equitable means of sharing tax attributes across classes

► Residual income is subject to high rate tax at full general rate of 38% (i.e. no general rate reduction)► Inefficient tax integration

Page 20

Mutual Fund Corporations - Qualifying

Qualifying as a “mutual fund corporation” under the Act1. The only undertaking of the corporation is investing its funds in property (shares,

trusts, debt, cash etc.)2. At least 95% of the fair market value of all outstanding shares are redeemable by

the holder3. Corporation is a “public corporation” as defined in Act

► Public corporation includes a corporation which has a class of share (the “qualifying shares”) with the following:► Minimum of 150 shareholders of “equity shares” (i.e. commons) OR► Minimum of 300 shareholders of “non-equity shares” (i.e. preferred)► Each shareholder holds a block of 100 shares worth a minimum of $500 in

total► The class is issued pursuant to a prospectus or similar document (i.e.

offering memorandum)

Page 21

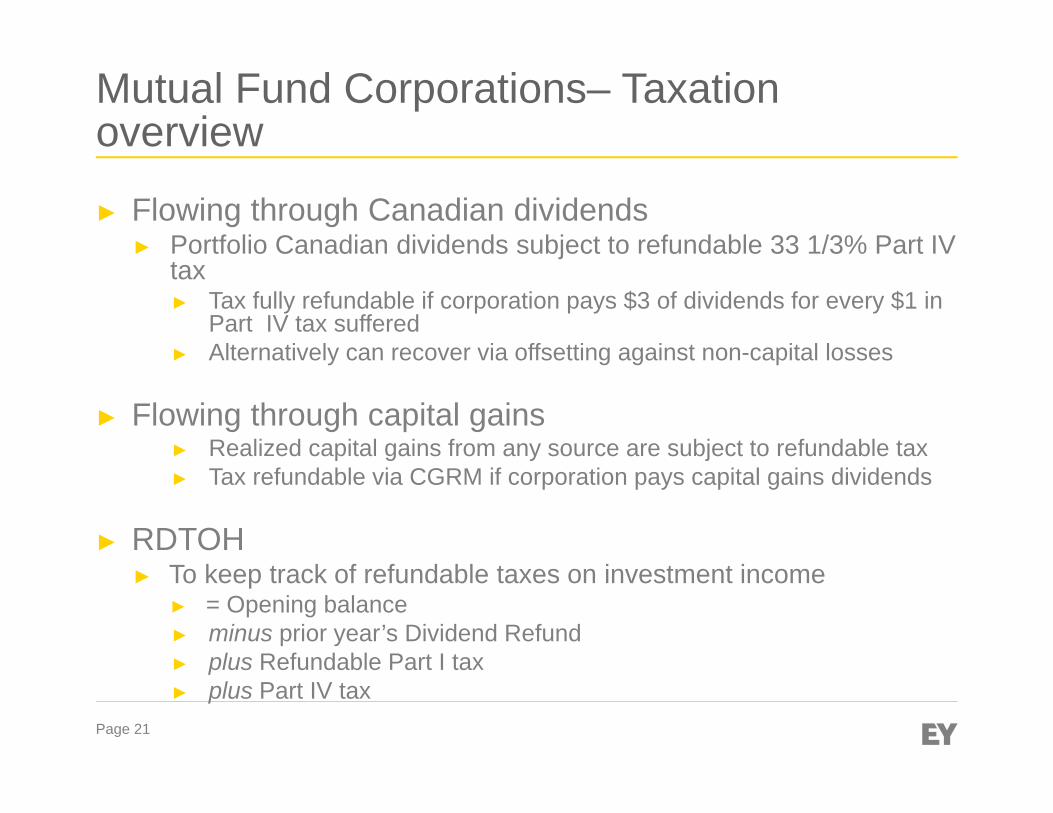

Mutual Fund Corporations– Taxation overview

► Flowing through Canadian dividends► Portfolio Canadian dividends subject to refundable 33 1/3% Part IV

tax► Tax fully refundable if corporation pays $3 of dividends for every $1 in

Part IV tax suffered► Alternatively can recover via offsetting against non-capital losses

► Flowing through capital gains► Realized capital gains from any source are subject to refundable tax ► Tax refundable via CGRM if corporation pays capital gains dividends

► RDTOH ► To keep track of refundable taxes on investment income

► = Opening balance► minus prior year’s Dividend Refund► plus Refundable Part I tax► plus Part IV tax

Page 22

Mutual Fund Corporations- Corporate Class

► Viewed as tax efficient because of:► Tax deferred switching between classes► Tax favoured distributions: Canadian dividends , capital gains,

ROC

► May invest in underlying trusts► Often desirable to have a corporate class version of trust► Preferable for tax exempt investors to be in trust version

► Challenge in determining character of income from underlying fund prior to year end distributions► Can pay capital gains 60 days after year end► Dividends must be payable at year end and paid within 60 days

► Suspended losses apply at corporate level

Page 23

Exchange Traded Funds

► Fund traded on a stock exchange► Act does not define Exchange Traded Funds

► Simply Mutual Fund Trusts

► Benefits for investors ► Trades like stocks► Opportunity to buy and sell throughout the day► Generally, lower MERs due to lower fund costs

► Offer opportunity to trade indices or underlying investments ► Active managed ETFs may also involve the use of derivatives

Page 24

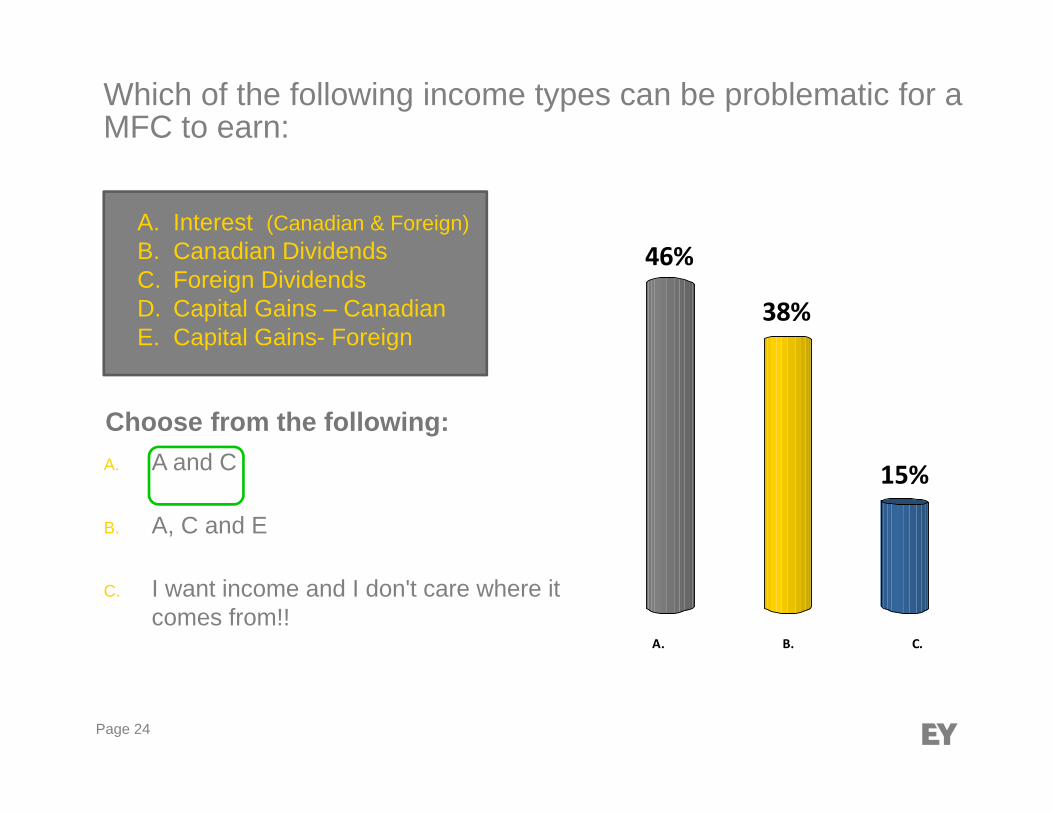

Which of the following income types can be problematic for a MFC to earn:

A. B. C.

46%

15%

38%

Choose from the following:

A. Interest (Canadian & Foreign)B. Canadian DividendsC. Foreign DividendsD. Capital Gains – CanadianE. Capital Gains- Foreign

A. A and C

B. A, C and E

C. I want income and I don't care where it comes from!!

Page 25

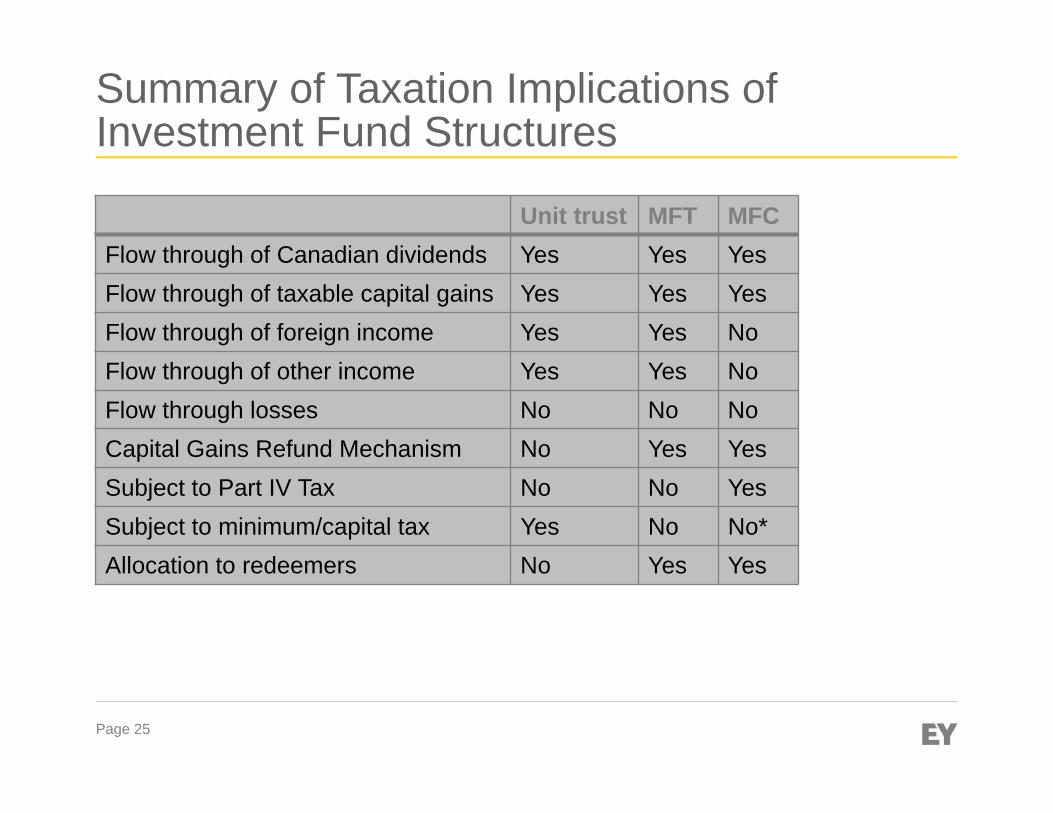

Summary of Taxation Implications of Investment Fund Structures

Unit trust MFT MFCFlow through of Canadian dividends Yes Yes YesFlow through of taxable capital gains Yes Yes YesFlow through of foreign income Yes Yes NoFlow through of other income Yes Yes NoFlow through losses No No NoCapital Gains Refund Mechanism No Yes YesSubject to Part IV Tax No No YesSubject to minimum/capital tax Yes No No*Allocation to redeemers No Yes Yes

Income Types & Tax Treatment

Page 27

Income Types & Tax Treatment

► Certain types of income earned by a fund may retain its character when distributed to the individual unitholder

► Example: If an MFT earns Canadian dividend income and capital gains, it may pay out this income to its unit holders without losing its characterization

► This is similar to a partnership.

Page 28

Income Types & Tax Treatment – Cont’d

► Taxable Canadian Dividends

► MFC – may deduct dividend income for tax purposes but will be subject to Part IV tax, which will be refunded when the MFC pays taxable dividends.

► MFT / UT – Taxable dividends are eligible for the dividend tax credit. Distributions by an MFT may retain their character when paid to unit holders.

► Individuals – Preferential tax treatment on taxable Canadian dividends due to dividend tax credit mechanism

Page 29

Income Types & Tax Treatment – Cont’d

► Taxable Capital Gains

► MFC – Only 50% of capital gain is taxable. Capital losses may only be offset against capital gains. MFCs may distribute its net capital gains to shareholders

► MFT – Only 50% of capital gain is taxable. Capital losses may only be offset against capital gains. MFTs may distribute its net capital gains to beneficiaries and required distribution may be reduced by the CGRM

► UT – Consistent with MFT, except UTs are not eligible for the CGRM

Page 30

Income Types & Tax Treatment – Cont’d

► Taxable Capital Gains (cont.)

► Individuals – Only 50% of capital gain is taxable. Capital losses may only be offset against capital gains

► Other items of note: Subsection 39(4) election whereby every Canadian security will be considered capital property

Page 31

Income Types & Tax Treatment – Cont’d

► Definition of Capital Property► Any properties of which any gains and losses from disposition

would qualify as capital gains or losses.► Example: securities, debt indentures, precious metals (not held as

business inventories)

► Definition of Canadian Securities ► Examples: Units in a MFT or shares of the capital stocks of a corporation

resident in Canada

Page 32

Income Types & Tax Treatment – Cont’d

► Returns of Capital (“ROC”)

► Non-Deductible when a fund returns its capitals to unitholders or shareholders, but also not taxable when received

► ACB of investment should be reduced by ROC, which will increase capital gains or reduce capital losses realized upon disposition.

► If ACB is reduced to nil, any subsequent ROC would trigger capital gains.

Page 33

Income Types & Tax Treatment – Cont’d

► Returns of Capital (“ROC”) – MFCs

► Distribution of ROC should reduce Capital Gain Dividend Account, thereby reducing the amount of tax-free capital dividend that can be distributed to shareholders

► Paid-in-capital of shares of MFC would be reduced by ROC as well.

Page 34

Income Types & Tax Treatment – Cont’d

► Foreign Source Income

► Example: distribution of foreign trusts / partnerships, interest income on bonds / debt instruments issued by foreign banks, dividend income on capital stocks of foreign entities.

► MFC/Individuals – Foreign source income is fully taxable

► MFT/UT – Foreign source income is fully taxable (net of amount distributed)

► Foreign tax credits can be claimed on foreign tax paid.

Page 35

Income Types & Tax Treatment – Cont’d

► Other Income

► MFC/Individuals – Other income is fully taxable

► MFT/UT – Other income is fully taxable (net of amount distributed)

Page 36

30%

70%A. True

B. False

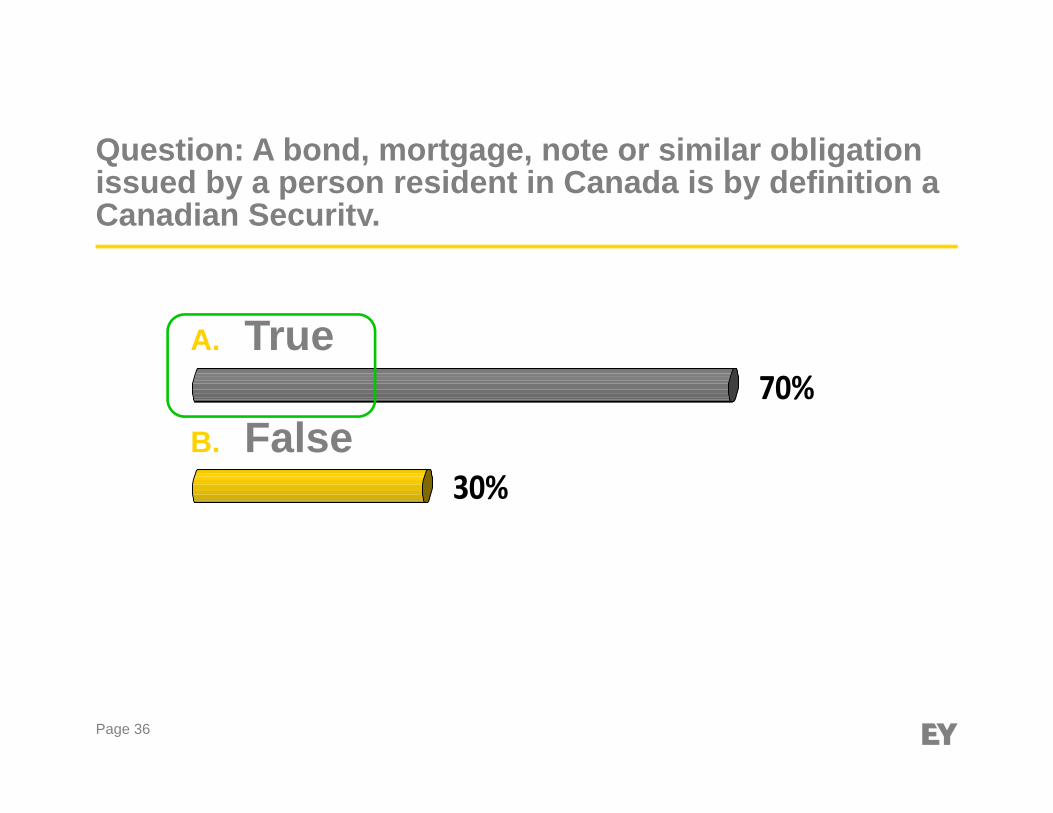

Question: A bond, mortgage, note or similar obligation issued by a person resident in Canada is by definition a Canadian Security.

IFRS for Investment Funds

Page 38

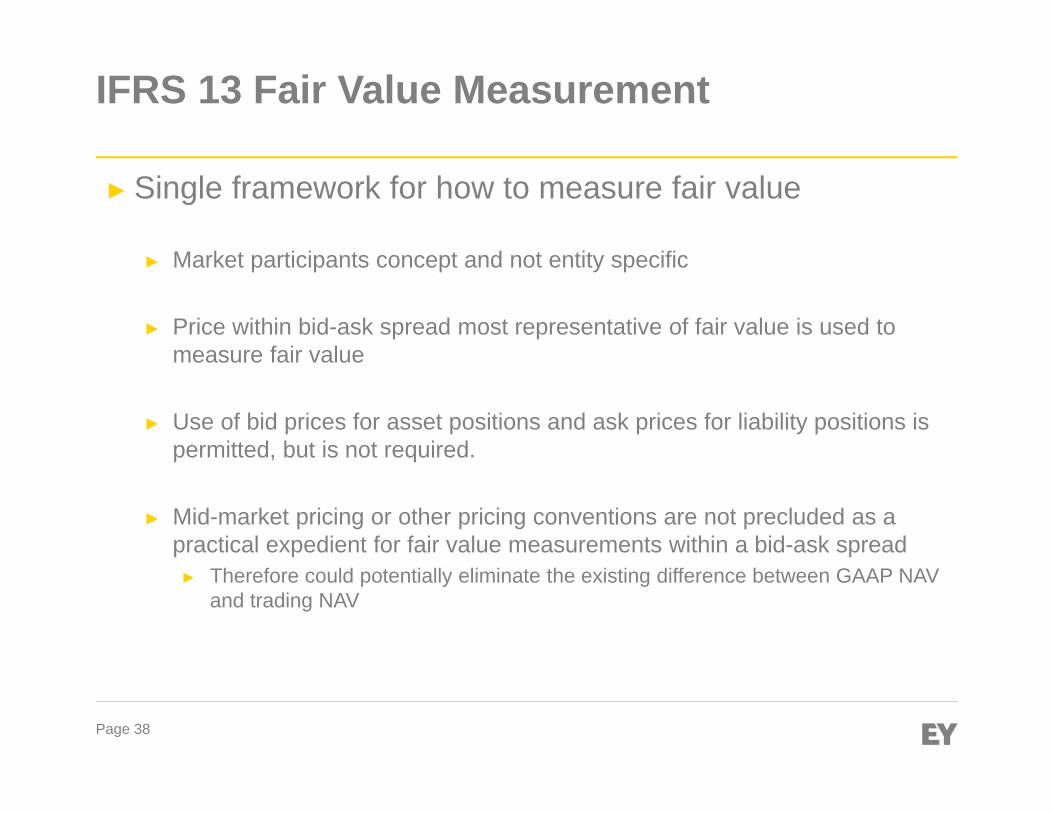

IFRS 13 Fair Value Measurement

► Single framework for how to measure fair value

► Market participants concept and not entity specific

► Price within bid-ask spread most representative of fair value is used to measure fair value

► Use of bid prices for asset positions and ask prices for liability positions is permitted, but is not required.

► Mid-market pricing or other pricing conventions are not precluded as a practical expedient for fair value measurements within a bid-ask spread► Therefore could potentially eliminate the existing difference between GAAP NAV

and trading NAV

Page 39

IFRS 13 Fair Value Measurement

► Implications

► Potential change in valuation technique (bid vs last trade) for publicly traded investments on transition to IFRS

► Assess whether other investments are impacted on adoption of IFRS 13

► Opening balance sheet and comparative year FS will need to be restated for any changes in fair value measurement, including notes disclosure that are impacted

► Additional fair value disclosure requirements under IFRS 13, particularly around level 3 instruments

Page 40

IFRS 13 Fair Value Measurement

► Tax Implications

► The formula for “capital gains redemption” in the CGRM formula incorporates the unrealized gains remaining in the trust (which presumably will become subject to tax when triggered, i.e. – realized)

► Such unrealized gains are based on the fair market values of the securities remaining in the MFT or MFC

► Under CGAAP, funds were likely using the end of day closing price to determine FMV for securities, which was by default used for the purposes of the “capital gains redemption” formula

► The Act does not prescribe methodology for measurement of unrealized gains utilized for purposes of the CGRM formula. The Act generally requires settlement price for determining gains and losses.

► Consideration for use of closing prices rather then mid-point for CGRM purposes. This may result in variance in CGRM result.

Page 41

IAS 18 – Revenue Recognition: Interest Income

Key Issues and potential impact

► IAS 18 specifically states that interest is to be recognized using the effective interest method as set out in IAS 39

► The use of effective interest method is not specifically required in IAS 39 for funds that record their financial instruments at fair value through profit and loss

► If interest income is required to be disclosed separately on the financial statements due to NI 81-106 disclosure requirements, interest would have to be calculated and presented in accordance with the effective interest method

► The regulator accepts interest income on investments to be disclosed as interest income for distribution purpose, with an explicit description of what it means, to avoid confusion that the amount is effective interest.

Page 42

IAS 18 – Revenue Recognition: Interest Income

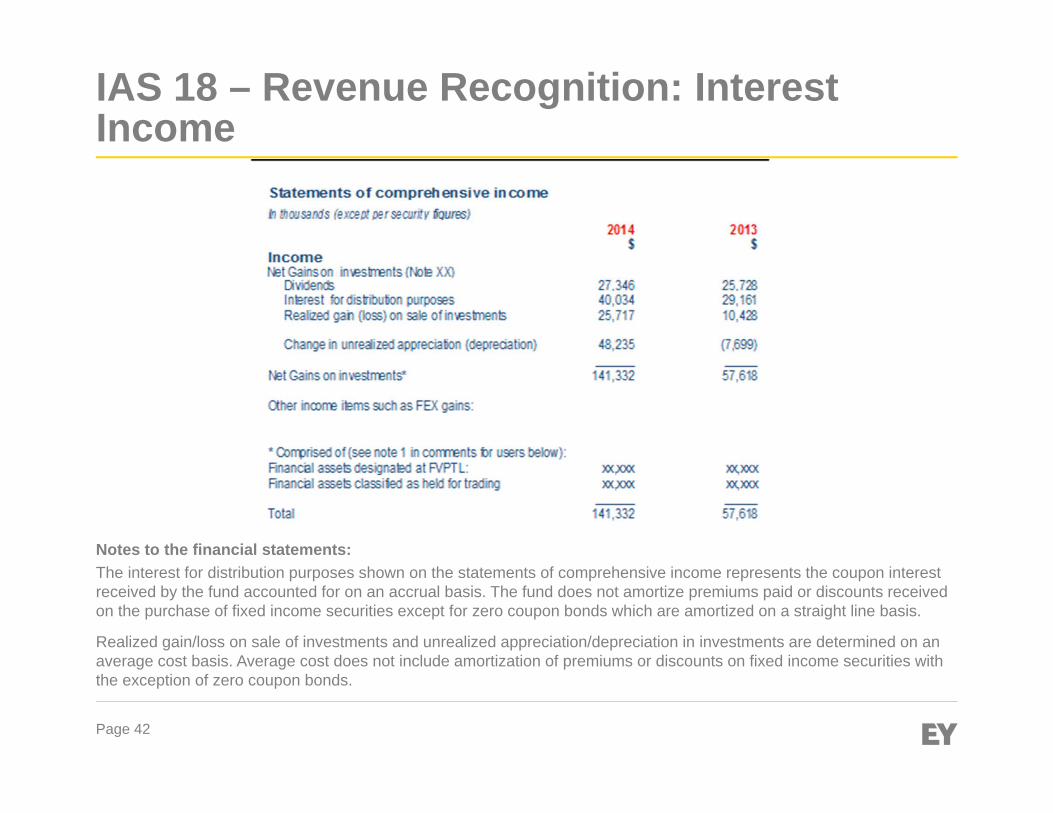

Notes to the financial statements:The interest for distribution purposes shown on the statements of comprehensive income represents the coupon interest received by the fund accounted for on an accrual basis. The fund does not amortize premiums paid or discounts received on the purchase of fixed income securities except for zero coupon bonds which are amortized on a straight line basis.

Realized gain/loss on sale of investments and unrealized appreciation/depreciation in investments are determined on an average cost basis. Average cost does not include amortization of premiums or discounts on fixed income securities with the exception of zero coupon bonds.

Page 43

IAS 18 – Revenue Recognition: Interest Income

Tax Implications

► Bonds purchased at a discount► Effective interest rate is greater than the cash coupon payment► Accretion of the carrying value of the bond/”pull-to-par” effect is taxable

► Bonds purchased at a premium► Effective interest rate is less than the cash coupon payment► Grind of the carrying value of the bond/”pull-to-par” effect is NOT

deductible in reducing the cash coupon payment

Page 44

IAS 7 - Cash Flow Statements

Statement of Cash Flows► A Statement of Cash Flows will be required for all funds as part of the complete set

of financial statements. IAS 7 contains the detailed requirements for this statement

► IAS 7 requires the presentation of information about the changes in cash of an entity according to operating, investing and financing by means of a statement of cash flows

► Allow for direct or indirect method

► Need to identify the non-cash components in all accounts in order to properly present the cash movement

► Also need to separately disclose interest and dividends received and paid, taxes paid and non-cash investing and financing transactions

Dividend Tax Credits

Page 46

► Background

► A fund may earn dividend income from investing in the shares of a corp.

► Distributions received by a Canadian resident are generally income from a trust, unless a deeming provision applies

► One provision in the ITA allows a trust to distribute dividend income it has received as dividend distributions out to the beneficiaries of the trust (i.e. – unitholders)

► The purpose of the gross-up and dividend tax credit mechanism is to achieve integration and avoid double-taxation

Dividend Tax Credits

Page 47

► Key Considerations

► Foreign dividend income does not qualify for the DTC

► Eligible dividends and ineligible dividends have different gross-up and DTC factors► If subsequent information from payer corporation indicates ineligible dividends

were paid, then T3 returns and slips must be amended

► A fund may be able to optimize the income retained in the trust without attracting tax by allocating expenses against dividend income

Dividend Tax Credits

Page 48

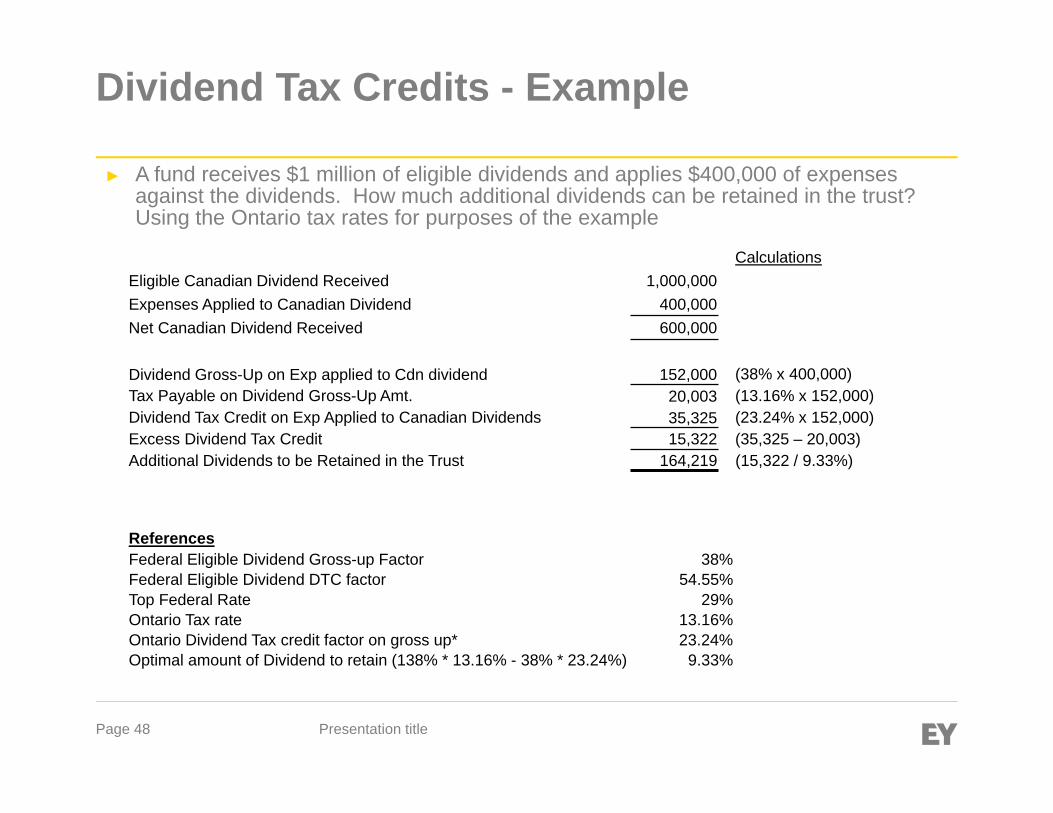

Dividend Tax Credits - Example

CalculationsEligible Canadian Dividend Received 1,000,000 Expenses Applied to Canadian Dividend 400,000 Net Canadian Dividend Received 600,000

Dividend Gross-Up on Exp applied to Cdn dividend 152,000 (38% x 400,000)Tax Payable on Dividend Gross-Up Amt. 20,003 (13.16% x 152,000)Dividend Tax Credit on Exp Applied to Canadian Dividends 35,325 (23.24% x 152,000)Excess Dividend Tax Credit 15,322 (35,325 – 20,003)Additional Dividends to be Retained in the Trust 164,219 (15,322 / 9.33%)

Presentation title

ReferencesFederal Eligible Dividend Gross-up Factor 38%Federal Eligible Dividend DTC factor 54.55%Top Federal Rate 29%Ontario Tax rate 13.16%Ontario Dividend Tax credit factor on gross up* 23.24%Optimal amount of Dividend to retain (138% * 13.16% - 38% * 23.24%) 9.33%

► A fund receives $1 million of eligible dividends and applies $400,000 of expenses against the dividends. How much additional dividends can be retained in the trust? Using the Ontario tax rates for purposes of the example

Page 49

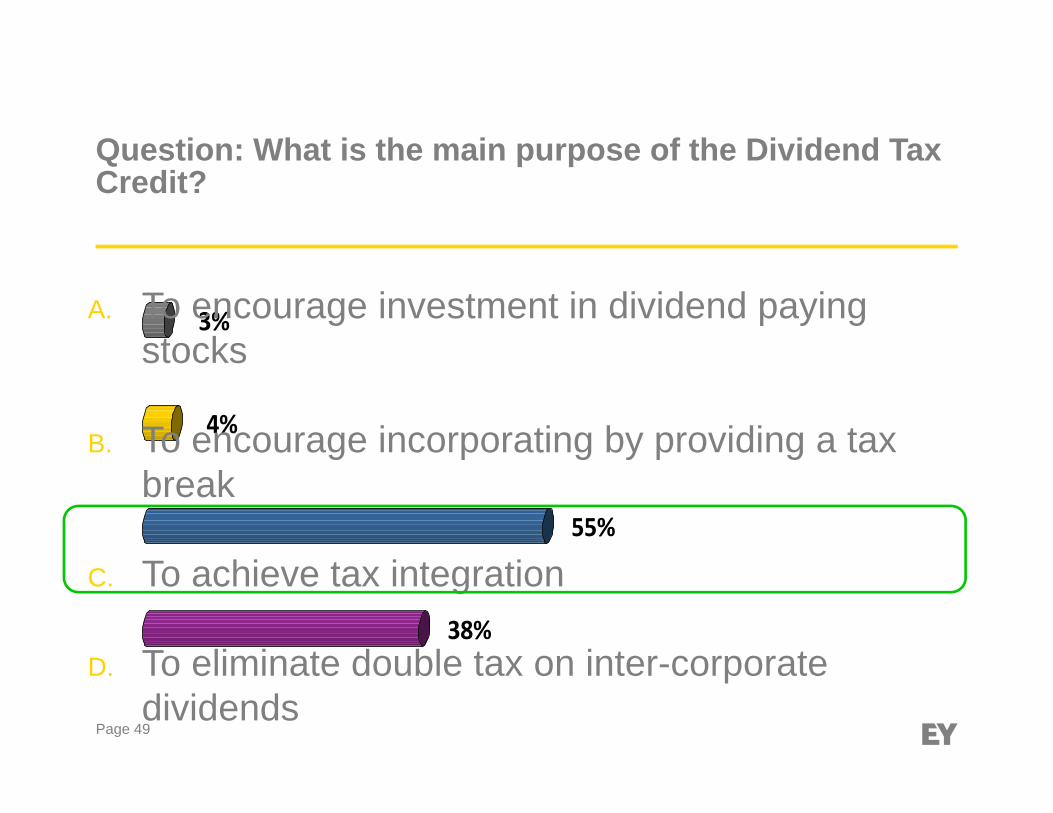

38%

55%

4%

3%A. To encourage investment in dividend paying stocks

B. To encourage incorporating by providing a tax break

C. To achieve tax integration

D. To eliminate double tax on inter-corporate dividends

Question: What is the main purpose of the Dividend Tax Credit?

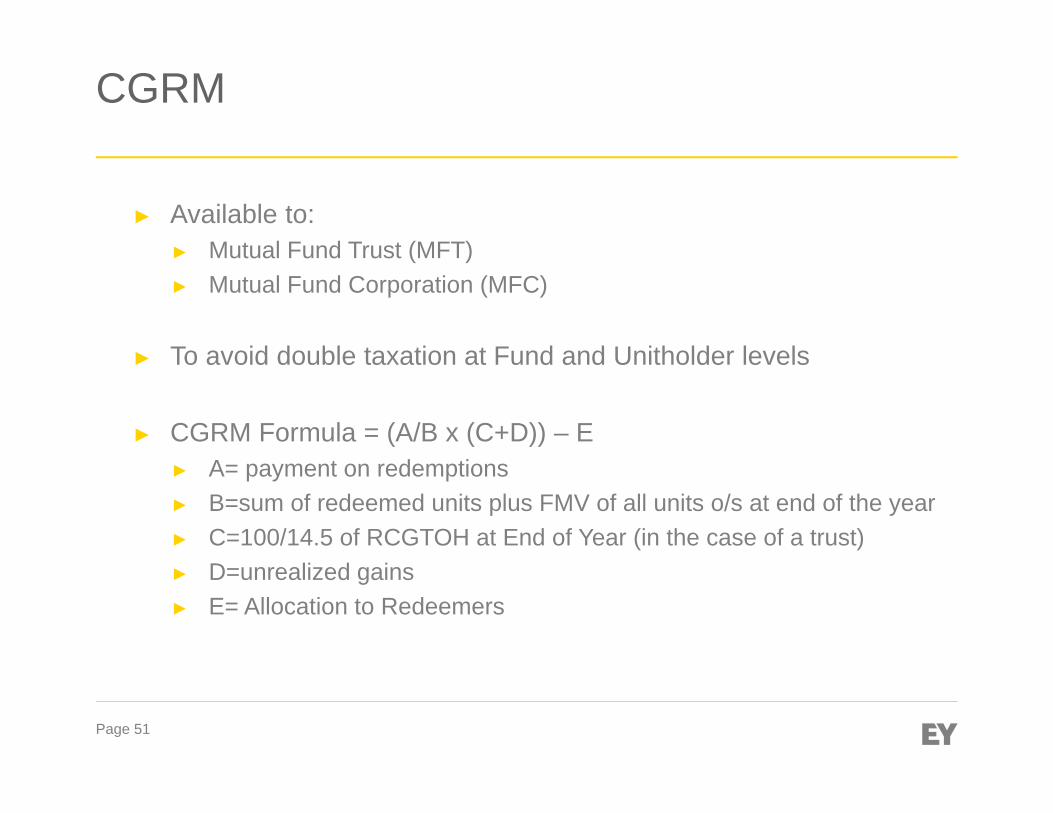

Capital Gains Refund Mechanism (“CGRM”)

Page 51

CGRM

► Available to:► Mutual Fund Trust (MFT)► Mutual Fund Corporation (MFC)

► To avoid double taxation at Fund and Unitholder levels

► CGRM Formula = (A/B x (C+D)) – E► A= payment on redemptions► B=sum of redeemed units plus FMV of all units o/s at end of the year► C=100/14.5 of RCGTOH at End of Year (in the case of a trust)► D=unrealized gains► E= Allocation to Redeemers

Page 52

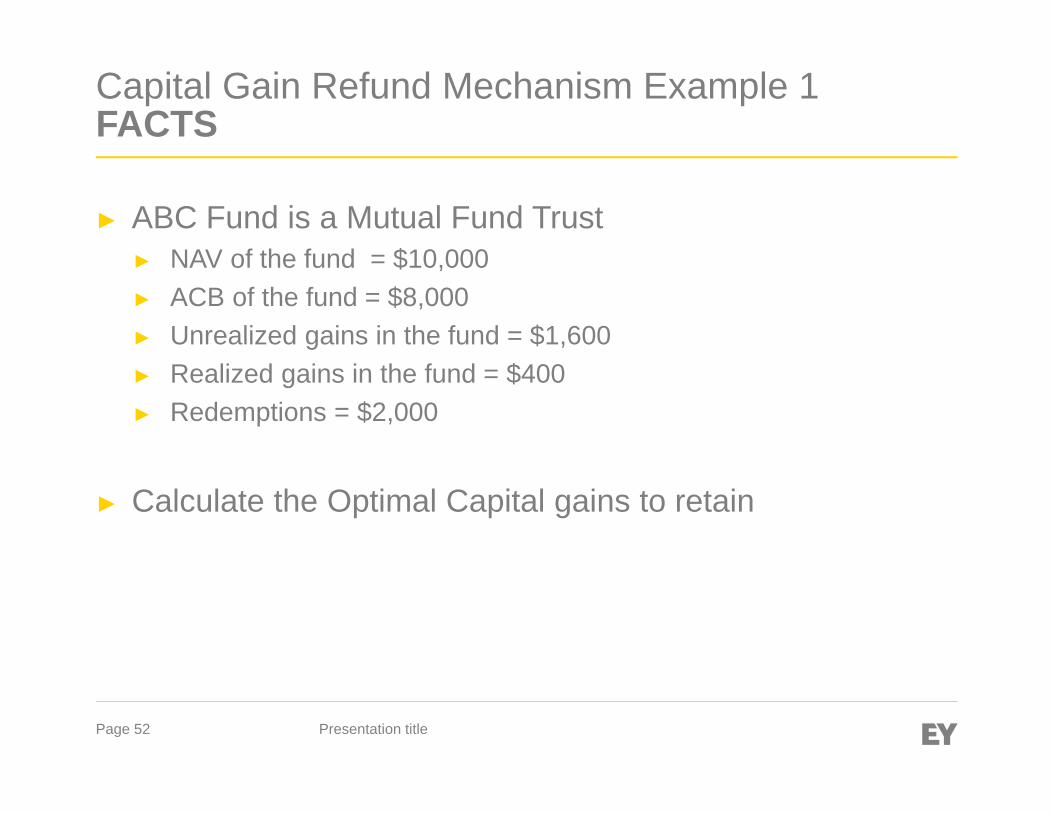

Capital Gain Refund Mechanism Example 1FACTS

► ABC Fund is a Mutual Fund Trust► NAV of the fund = $10,000 ► ACB of the fund = $8,000► Unrealized gains in the fund = $1,600► Realized gains in the fund = $400► Redemptions = $2,000

► Calculate the Optimal Capital gains to retain

Presentation title

Page 53

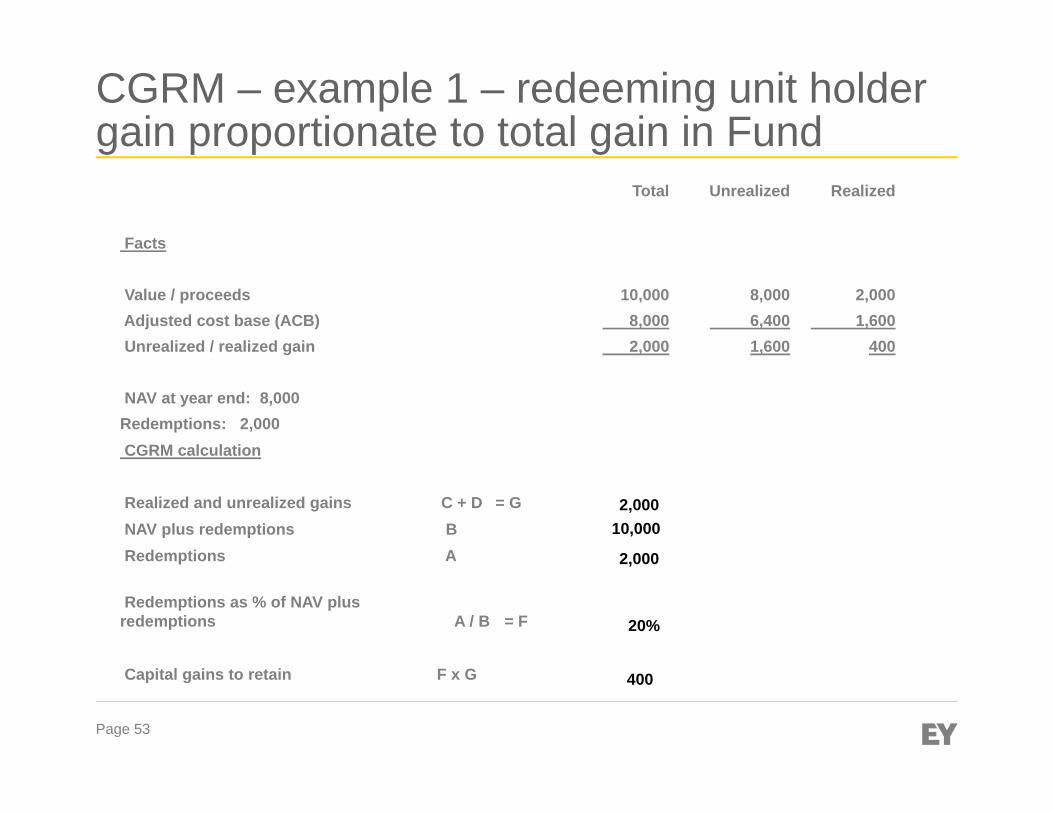

CGRM – example 1 – redeeming unit holder gain proportionate to total gain in Fund

Total Unrealized Realized

Facts

Value / proceeds 10,000 8,000 2,000 Adjusted cost base (ACB) 8,000 6,400 1,600 Unrealized / realized gain 2,000 1,600 400

NAV at year end: 8,000Redemptions: 2,000CGRM calculation

Realized and unrealized gains C + D = GNAV plus redemptions BRedemptions A

Redemptions as % of NAV plus redemptions A / B = F

Capital gains to retain F x G

2,00010,000

2,000

20%

400

Page 54

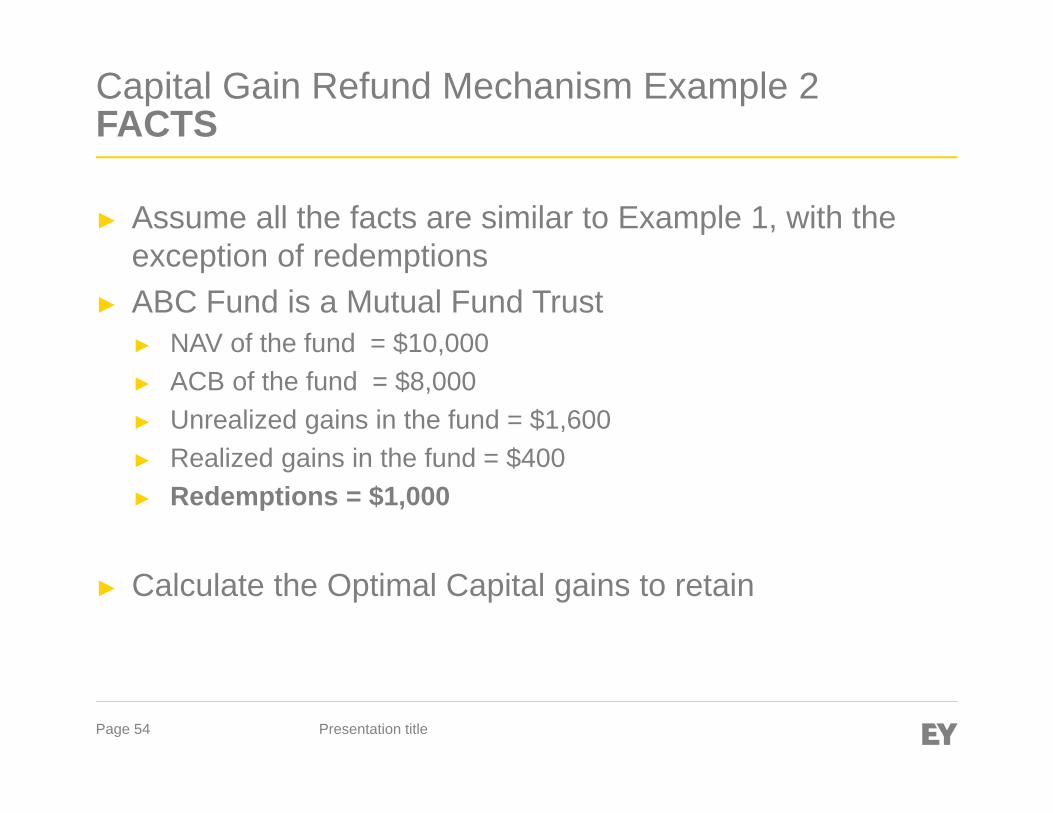

Capital Gain Refund Mechanism Example 2FACTS

► Assume all the facts are similar to Example 1, with the exception of redemptions

► ABC Fund is a Mutual Fund Trust► NAV of the fund = $10,000 ► ACB of the fund = $8,000► Unrealized gains in the fund = $1,600► Realized gains in the fund = $400► Redemptions = $1,000

► Calculate the Optimal Capital gains to retain

Presentation title

Page 55

CGRM – example 2 – redeeming gain less than total realized gains

Total Unrealized Realized

Facts

Value / proceeds 10,000 8,000 2,000Adjusted cost base (ACB) 8,000 6,400 1,600 Unrealized / realized gain 2,000 1,600 400 F

NAV at year end: 9,000Redemptions: 1,000CGRM calculation

Realized and unrealized gains C + D = GNAV plus redemptions BRedemptions A

Redemptions as % of NAV plus redemptions A / B = H

Capital gains to retain H x G = ICapital gains to distribute F- I

2,00010,0001,000

10%

200200

Page 56

Capital Gain Refund Mechanism Example 3FACTS

► Scenario A & B show the interaction of CGRM and Allocation to redeemers.

► For each of Scenario A & B, assume the following attributes:► NAV of the fund = $200 ► ACB of the fund = $100► Realized gains in the fund = $100► Redemptions = $200

► In Scenario A the fund will utilize the CGRM and in Scenario B the fund will utilize the Allocation to Redeemer mechanism.

► Compare the results of using each approach

Presentation title

Page 57

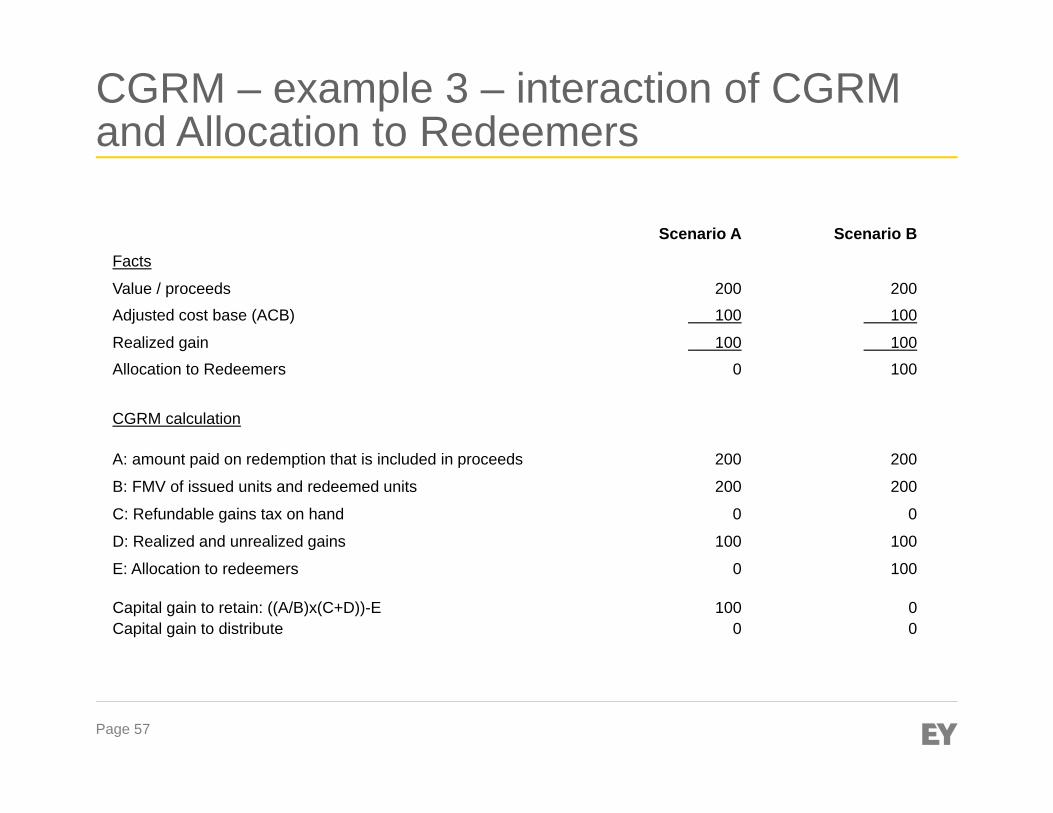

CGRM – example 3 – interaction of CGRM and Allocation to Redeemers

Scenario A Scenario BFacts

Value / proceeds 200 200

Adjusted cost base (ACB) 100 100

Realized gain 100 100

Allocation to Redeemers 0 100

CGRM calculation

A: amount paid on redemption that is included in proceeds 200 200

B: FMV of issued units and redeemed units 200 200

C: Refundable gains tax on hand 0 0

D: Realized and unrealized gains 100 100

E: Allocation to redeemers 0 100

Capital gain to retain: ((A/B)x(C+D))-E 100 0Capital gain to distribute 0 0

Page 58

CGRM vs. ATR

► In practice, many funds utilize CGRM, Allocation to Redeemers (ATR), or a combination of both methods, depending on policy and benefits derived from each methodology

► In certain funds, the CGRM will not produce the desired result, and the use of ATR may be preferential. ► A fund with an overall accrued loss on its portfolio at year-end► CGRM may not be preferential where a fund is in an unrealized

gain position at year-end which is lower than the total amount of gains realized by investors who redeemed during the year.

Presentation title

Page 59

Refundable capital gains tax

► RCGTOH► Where MFC or MFT has paid tax on capital gains

► Example: CGs underdistributed ► Carried forward as refundable capital gains tax on hand

► Capital gains refund► RCGTOH refundable to the extent of:

► MFT – 14.5% of capital gains redemptions► MFC - 14% of capital gains redemptions and capital gains dividends► Similar provincial portion

► MFC - Capital gains dividend► Elect on dividends paid within 60 days of year end► Cannot exceed balance of Capital gains dividend account

► Cumulative realized CGs less CG dividends paid and grossed-up capital gains refunds before that time

Page 60

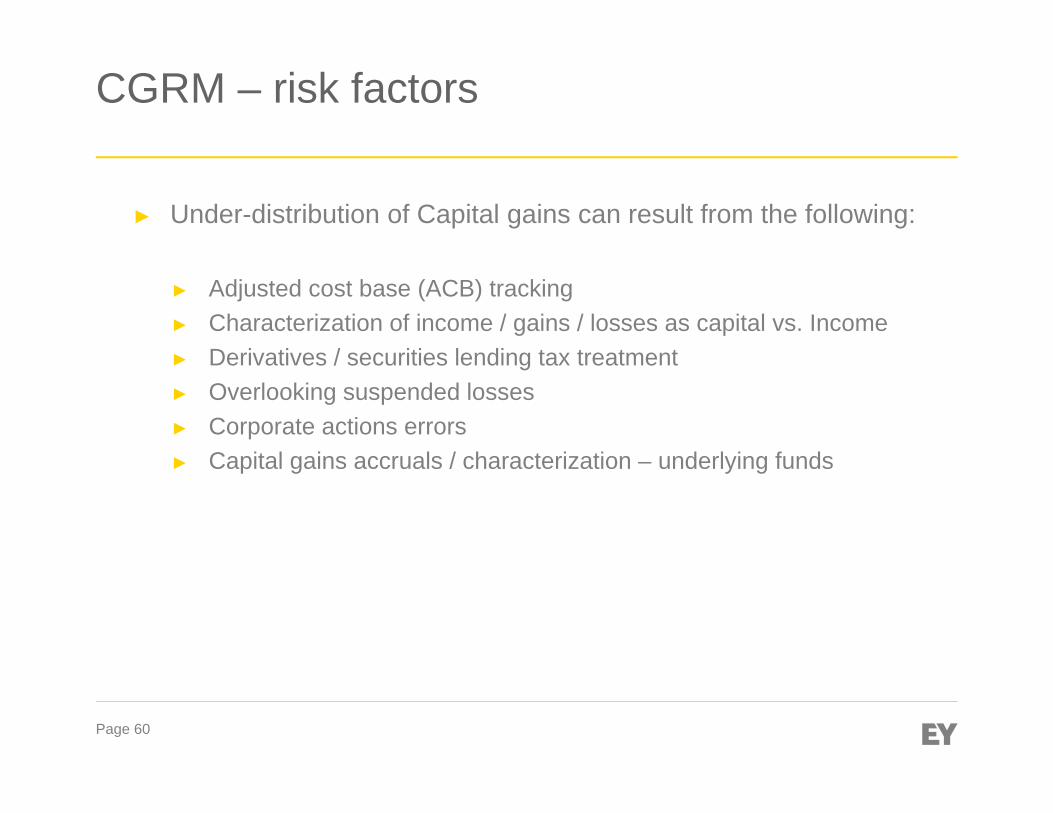

CGRM – risk factors

► Under-distribution of Capital gains can result from the following:

► Adjusted cost base (ACB) tracking► Characterization of income / gains / losses as capital vs. Income► Derivatives / securities lending tax treatment► Overlooking suspended losses ► Corporate actions errors► Capital gains accruals / characterization – underlying funds

Page 61

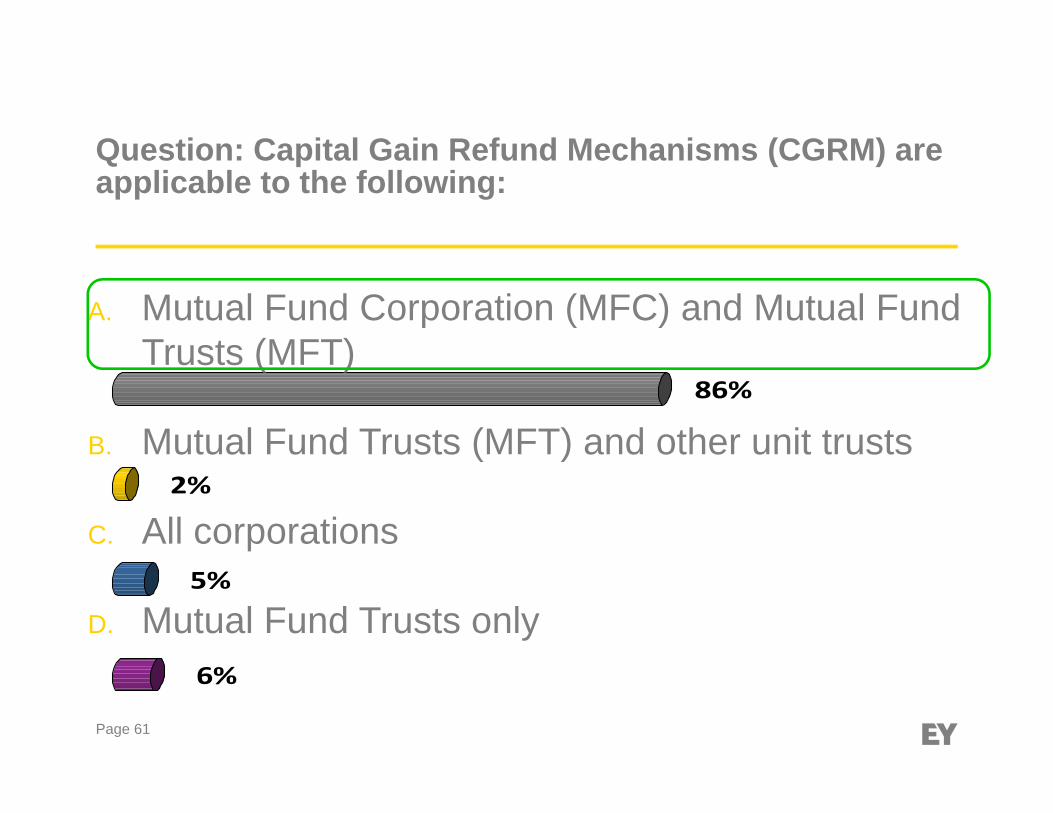

6%

5%

2%

86%

A. Mutual Fund Corporation (MFC) and Mutual Fund Trusts (MFT)

B. Mutual Fund Trusts (MFT) and other unit trusts

C. All corporations

D. Mutual Fund Trusts only

Question: Capital Gain Refund Mechanisms (CGRM) are applicable to the following:

Special Topics

Stop Loss, Suspended Losses, SLAs, Trust Loss Restriction Events

Page 63

Stop Loss

Page 64

Stop Loss Rules

► The stop loss rules are intended to prevent certain taxpayers from receiving tax-free dividends while simultaneously claiming a loss on the sale of the security► Example: A Co receives a dividend of $10 from B Co. Absent the stop

loss rules, A Co should receive the inter-corporate dividend tax free. B Co’s value is now reduced by $10 and A Co sells its share of B Co. A Co would realizes a $10 loss on the sale.

► Who is subject to stop loss rules?► Trust (other than mutual fund trust)► Corporation (including mutual fund corporation)► Partnerships► Individuals

Page 65

Stop Loss Rules

► Generally, where the stop loss rules apply, the loss on the disposition of shares is reduced by the deductible portions of dividends received.

► Note that some dividends may be excluded where certain conditions are met:

► the dividend was paid on a share owned for a least 365 days before the disposition

► the corporation/trust (other than a MFT), alone or with persons/ beneficiaries not dealing at arm's length with, did not own more than 5% of the issued shares of any class of the payor corporation at the time the dividend was received.

Page 66

Stop Loss Rules

► The stop loss mechanisms vary by recipient type (trust, partnership, corporation) and whether the shares were held as capital property or as inventory

► Proposed section 112(8) has stop loss provisions where a synthetic disposition has been entered into

Page 67

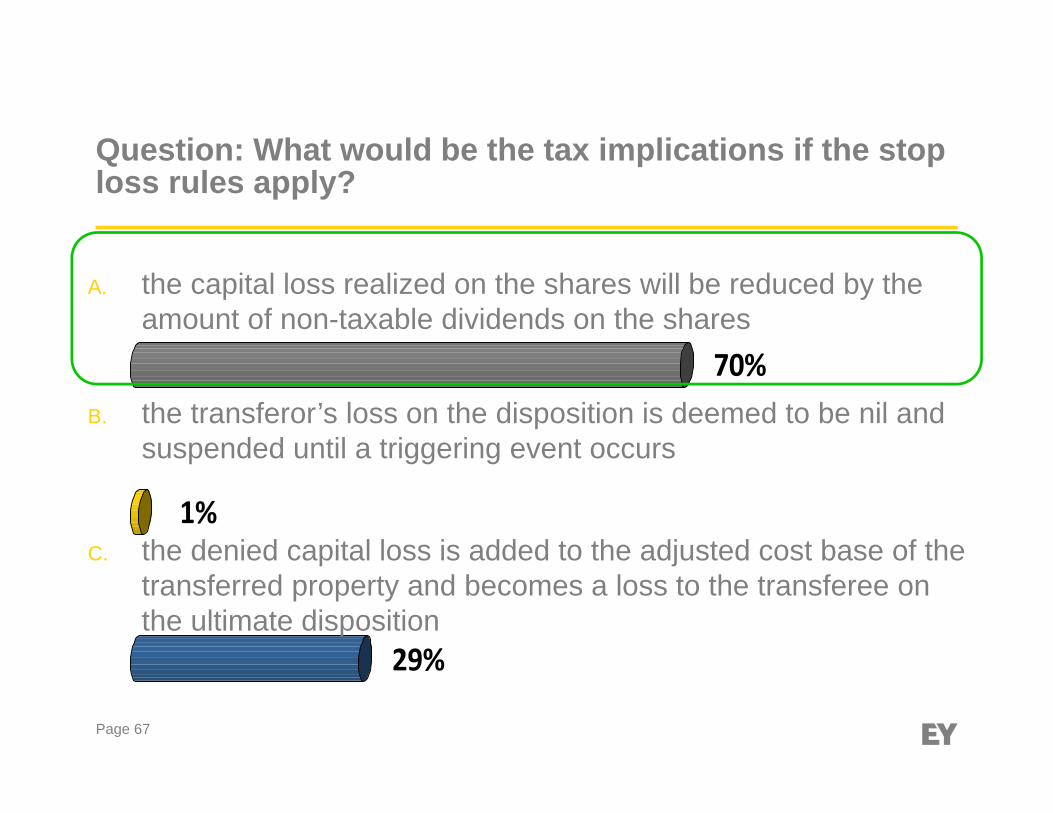

29%

1%

70%

A. the capital loss realized on the shares will be reduced by the amount of non-taxable dividends on the shares

B. the transferor’s loss on the disposition is deemed to be nil and suspended until a triggering event occurs

C. the denied capital loss is added to the adjusted cost base of the transferred property and becomes a loss to the transferee on the ultimate disposition

Question: What would be the tax implications if the stop loss rules apply?

Page 68

Suspended Losses

Page 69

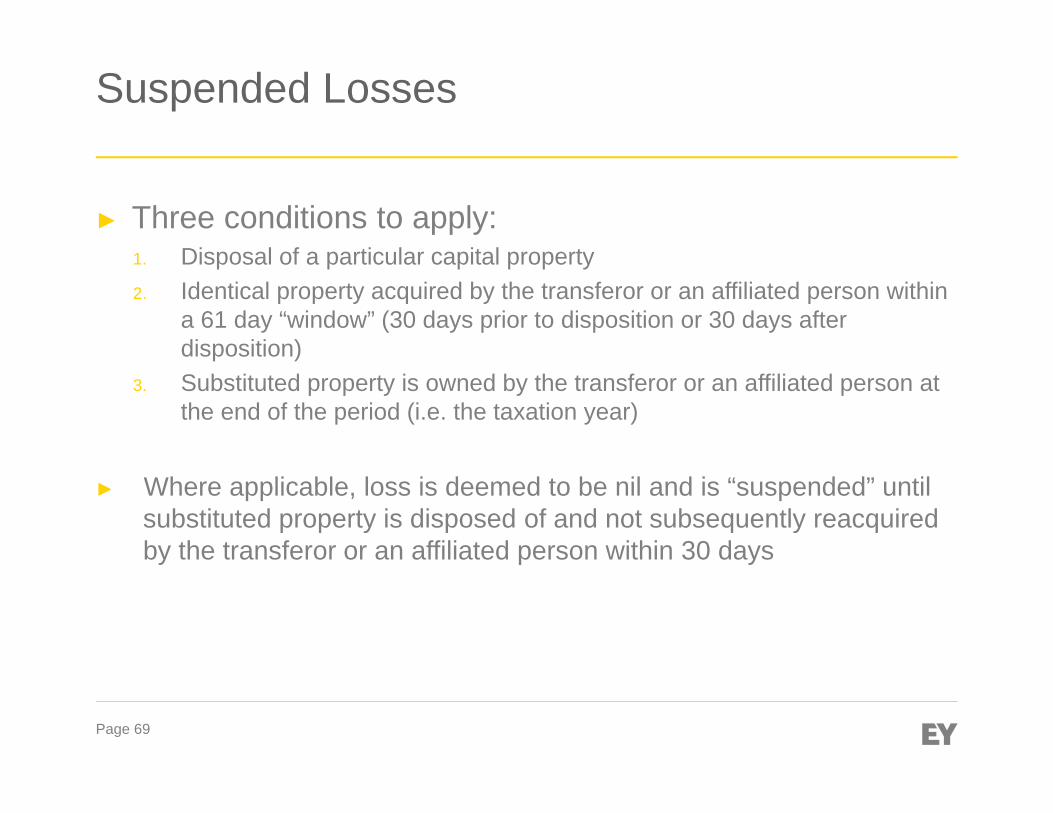

Suspended Losses

► Three conditions to apply:1. Disposal of a particular capital property2. Identical property acquired by the transferor or an affiliated person within

a 61 day “window” (30 days prior to disposition or 30 days after disposition)

3. Substituted property is owned by the transferor or an affiliated person at the end of the period (i.e. the taxation year)

► Where applicable, loss is deemed to be nil and is “suspended” until substituted property is disposed of and not subsequently reacquired by the transferor or an affiliated person within 30 days

Page 70

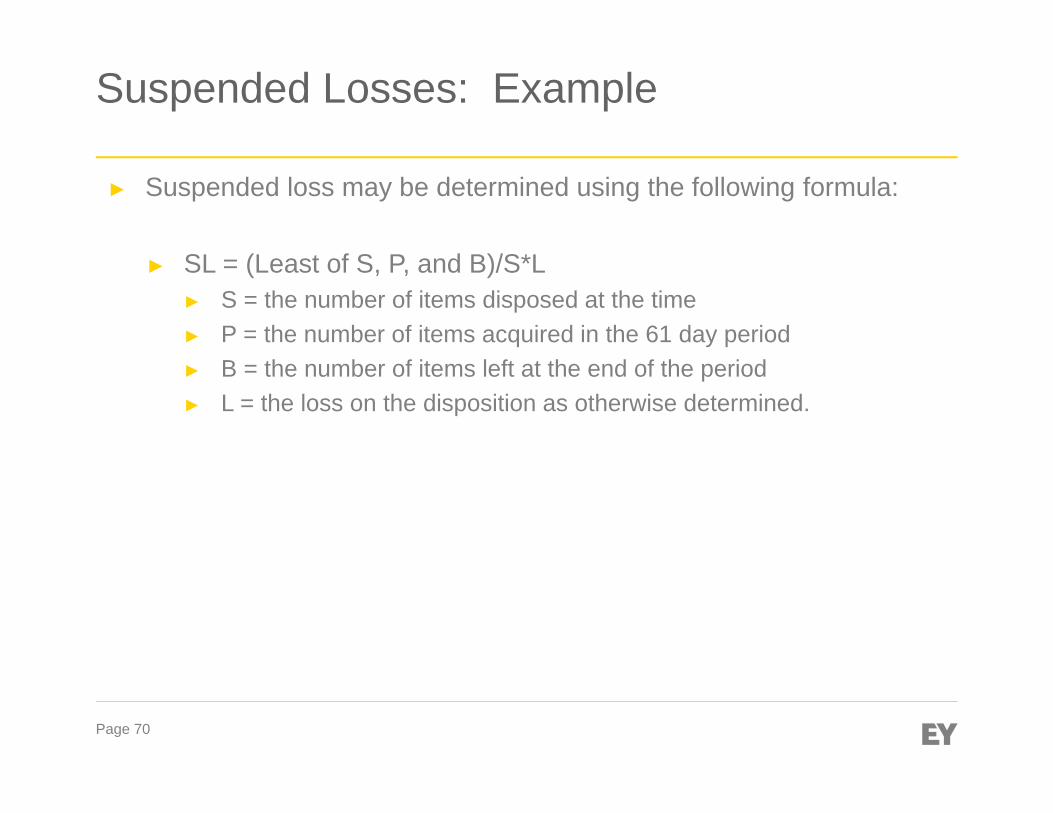

Suspended Losses: Example

► Suspended loss may be determined using the following formula:

► SL = (Least of S, P, and B)/S*L► S = the number of items disposed at the time► P = the number of items acquired in the 61 day period► B = the number of items left at the end of the period► L = the loss on the disposition as otherwise determined.

Page 71

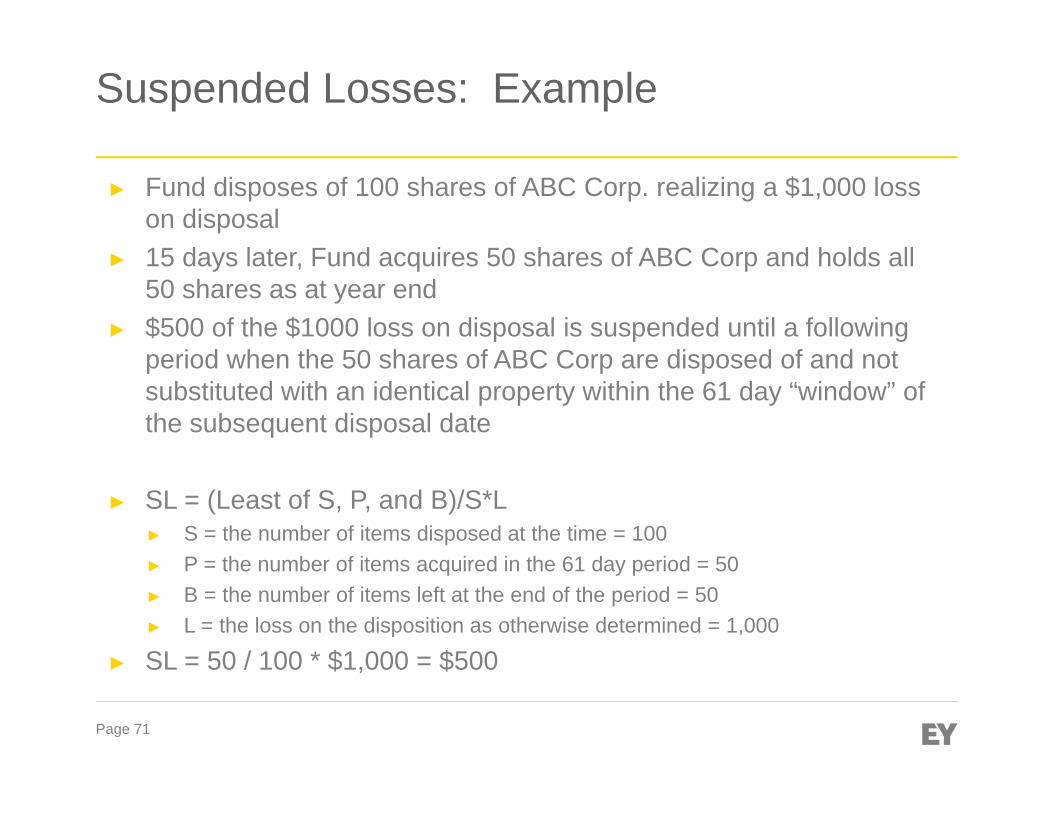

Suspended Losses: Example

► Fund disposes of 100 shares of ABC Corp. realizing a $1,000 loss on disposal

► 15 days later, Fund acquires 50 shares of ABC Corp and holds all 50 shares as at year end

► $500 of the $1000 loss on disposal is suspended until a following period when the 50 shares of ABC Corp are disposed of and not substituted with an identical property within the 61 day “window” of the subsequent disposal date

► SL = (Least of S, P, and B)/S*L► S = the number of items disposed at the time = 100► P = the number of items acquired in the 61 day period = 50► B = the number of items left at the end of the period = 50► L = the loss on the disposition as otherwise determined = 1,000

► SL = 50 / 100 * $1,000 = $500

Page 72

Securities Lending Arrangements

Page 73

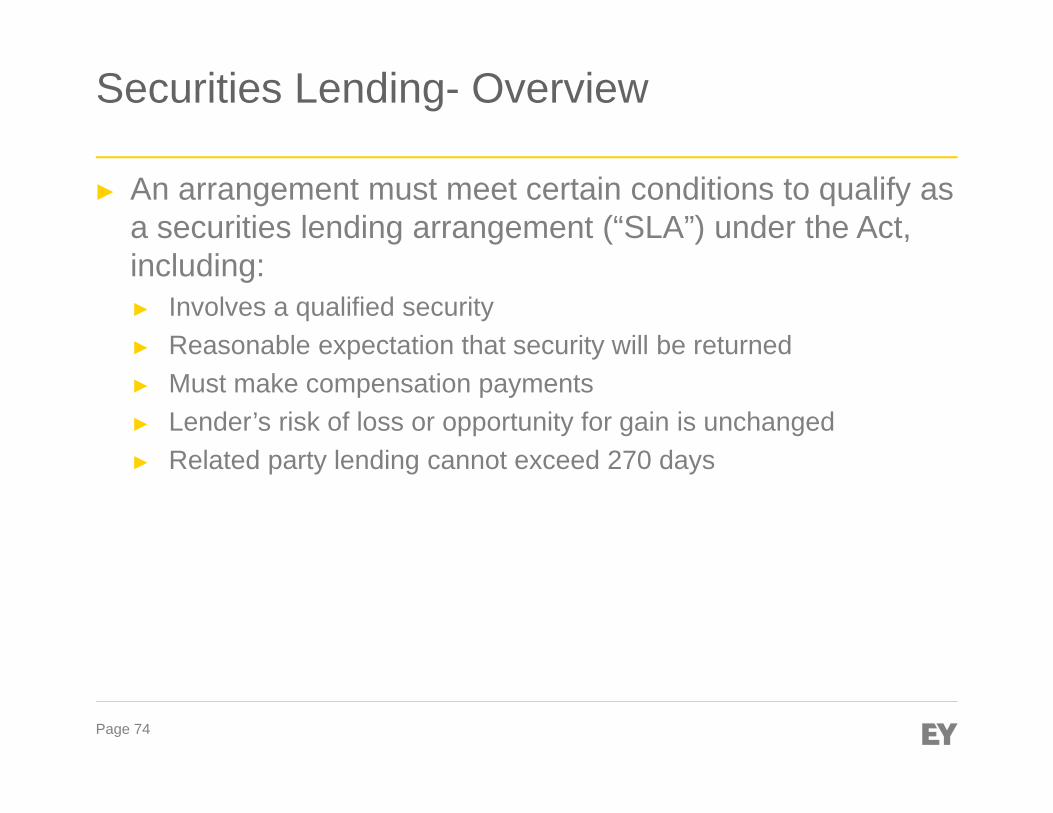

Securities Lending- Overview

► Act contains a specific regime to govern lending of certain securities:► Publicly traded equities (including warrants, rights, options) ► Publicly traded trust units► Debt of public traded entities

► Applies to domestic and foreign issuances

► Does not apply to commodities

Page 74

Securities Lending- Overview

► An arrangement must meet certain conditions to qualify as a securities lending arrangement (“SLA”) under the Act, including:► Involves a qualified security► Reasonable expectation that security will be returned► Must make compensation payments► Lender’s risk of loss or opportunity for gain is unchanged► Related party lending cannot exceed 270 days

Page 75

Securities Lending- Lender issues

► Funds may lend to enhance yields by earning interest► Lender is deemed not to have disposed of the lent security► Borrow fees or income on re-invested cash collateral fully taxable► Compensation payments received retain character of the

underlying payment► Dividends, trust distributions or interest► Generally a lender should be in same position as if held and received

income directly

Page 76

Securities Lending- Borrower issues

► Certain funds may borrow to cover short positions ► Compensation payments are generally deductible, except:

► Trusts are limited to deducting Canadian dividend compensation payments to the extent of long Canadian dividends received

► Where foreign shorts are held on income account, dividend compensation expense is not limited in its deductibility.

► Where foreign shorts are held on capital account, foreign dividend expenses are only deductible against foreign dividend income of the same security.

Page 77

Securities Lending- Borrower issues

► Security lending expenses are generally deductible, except:► Where shorts (domestic or foreign) are held on income account,

security lending expense is not limited in its deductibility ► Where shorts (domestic or foreign) are held on capital account,

security lending expense is not deductible against any income, and does not reduce ACB► Partnerships pass through to determine deductibility at partner level

► Withholding tax applies to dividend compensation payments to non-residents, even over foreign equities

► Borrow fees generally deductible and characterized as interest for withholding tax purposes

Page 78

Securities Lending- Other issues

► Securities regulators worldwide looking to put securities lending “on-exchange”

► Emergence of central counterparties (“CCPs”) ► CCPs act as principal to both borrower and lender► Participants are approved members► Reduces counterparty risk► Currently no Canadian resident CCP

► Canadians must go through US or foreign resident CCP

► Canadian tax regime may give adverse results with non-resident CCP

Page 79

77%

23%A. Yes

B. No

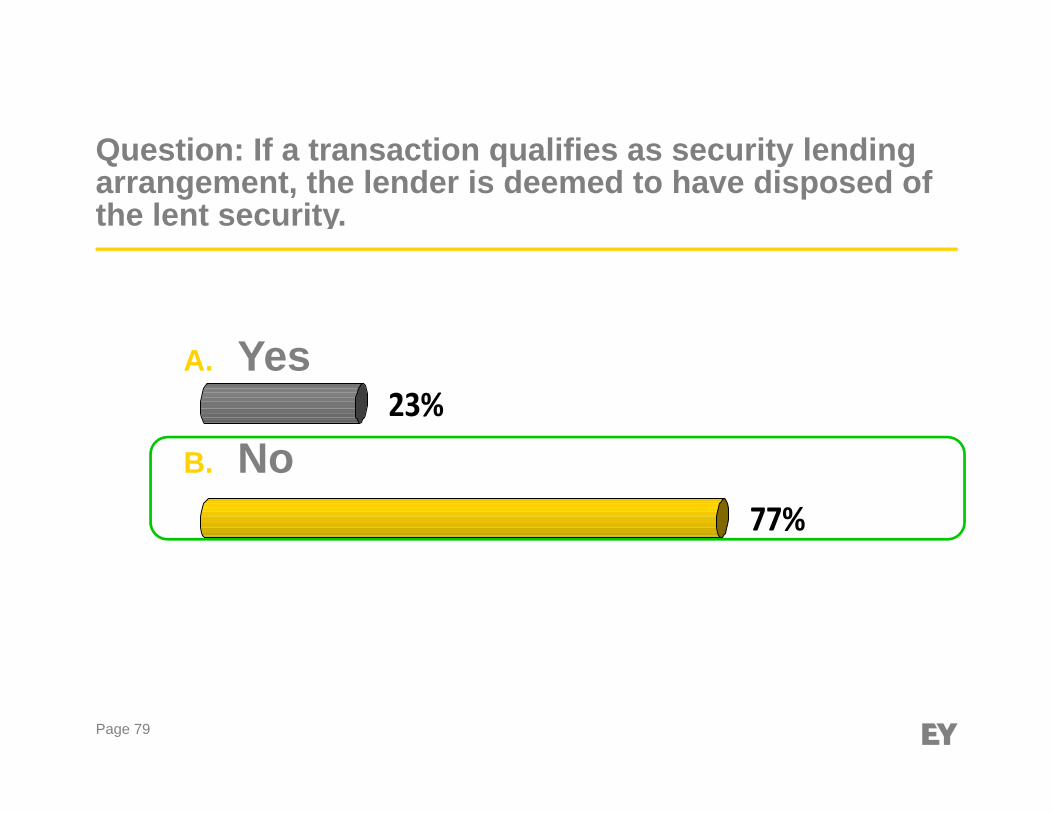

Question: If a transaction qualifies as security lending arrangement, the lender is deemed to have disposed of the lent security.

Page 80

Trust Loss Restriction Event

Page 81

Trust Loss Restriction Event

► New legislation from Federal Budget 2013 results in the application of the acquisition of control rules to trusts► Legislation enacted on December 12, 2013, with retroactive

application to March 21, 2013

► Occurs when a beneficiary, either directly or indirectly (i.e. – through a partnership), and either alone or in combination with affiliated persons, acquires a greater than 50% interest in the FMV of all interest or capital of a trust► Such a beneficiary is called a “majority-interest beneficiary under

the ITA

Page 82

Trust Loss Restriction Event

► Situations where a Trust Loss Restriction Event (“TLRE”) could occur:

► ETFs: a single designated broker dealer holds a greater than 50% interest in the ETF, however short the time period, in its capacity as a market maker for the ETF

► Fund on Fund: where a top fund’s beneficial interest exceeds 50%

► Non-NI 81-102 Fund: In such non-regulated funds, the investment capital may not be widely held as in “regular” NI 81-102 MFTs

► New Fund launched after March 20, 2013

Page 83

Trust Loss Restriction Event

► Tax Implications of a TLRE► Deemed year-end to occur at the beginning of the day (i.e. – the

end of the prior day), unless otherwise elected by the taxpayer

► Realization of all accrued losses (i.e. – capital losses, property losses)

► Limitation of Losses: Capital losses realized prior to the TLRE, including those capital losses realized on accrued losses previously, will not be available for carryforward after the TLRE

► Limitation of Losses: Non-capital losses may be carried forward to the extent income or profits from the same or similar business that gave rise to the losses

Page 84

Trust Loss Restriction Event

► Tax Implications of a TLRE► Limitation of Losses: Property losses will not be available for

carryforward

► Business loss vs. property loss is a question of fact

► In order to minimize the quantum of capital and property losses which may otherwise expire following a TLRE, certain elections may be made to increase the respective tax basis of certain property held by the trust up to the amount of any accrued gains in respect of that property

Page 85

Trust Loss Restriction Event

► Tax Implications of a TLRE

► Qualifying as an MFT: a trust may need to meet the requirements sooner than mid-March of the following calendar year (assuming the trust will elect a December 15 taxation year)

Page 86

Trust Loss Restriction Event

► Business Implications of a TLRE

► Managers and administrators should consider processes and procedures to identify the risk/occurrence of a TLRE

► If a TLRE has occurred, measure the tax risk and undertake actions to minimize losses

► Determine of declarations of trust allow for additional, “non-routine” (i.e. – not monthly, quarterly, or annually) distributions to minimize tax exposure in the trust

Page 87

18%

82%A. Yes

B. No

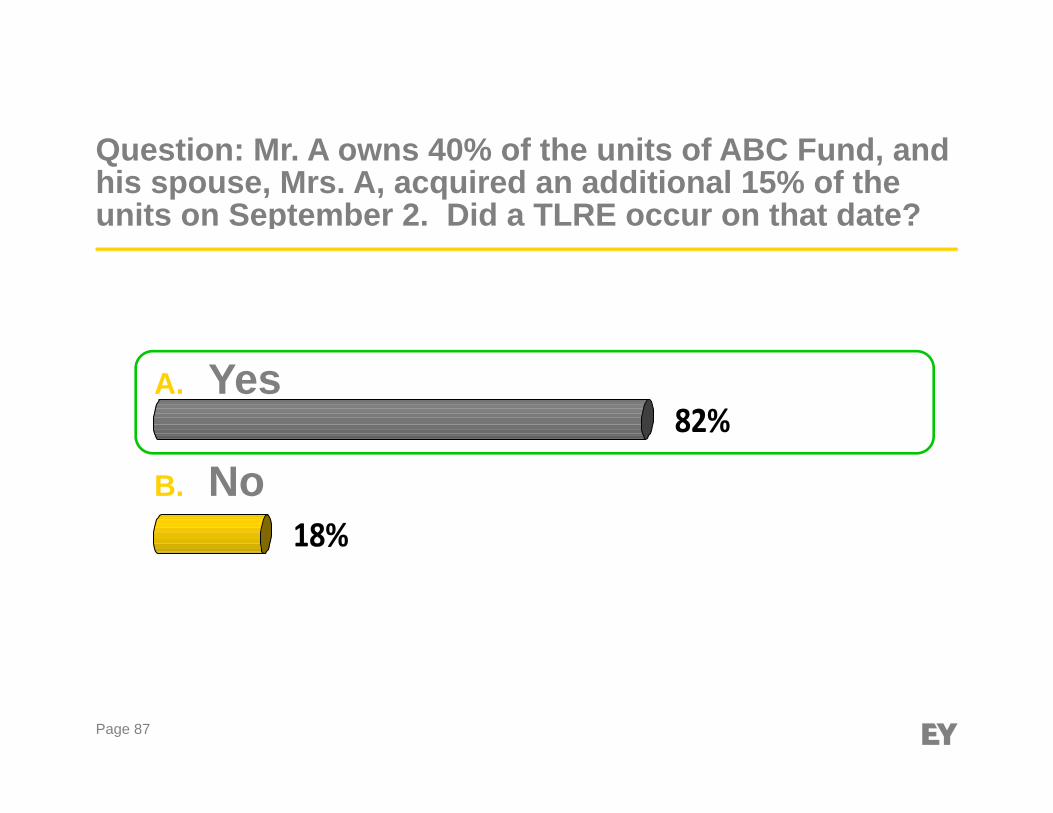

Question: Mr. A owns 40% of the units of ABC Fund, and his spouse, Mrs. A, acquired an additional 15% of the units on September 2. Did a TLRE occur on that date?

Page 88

70%

30%A. Yes

B. No

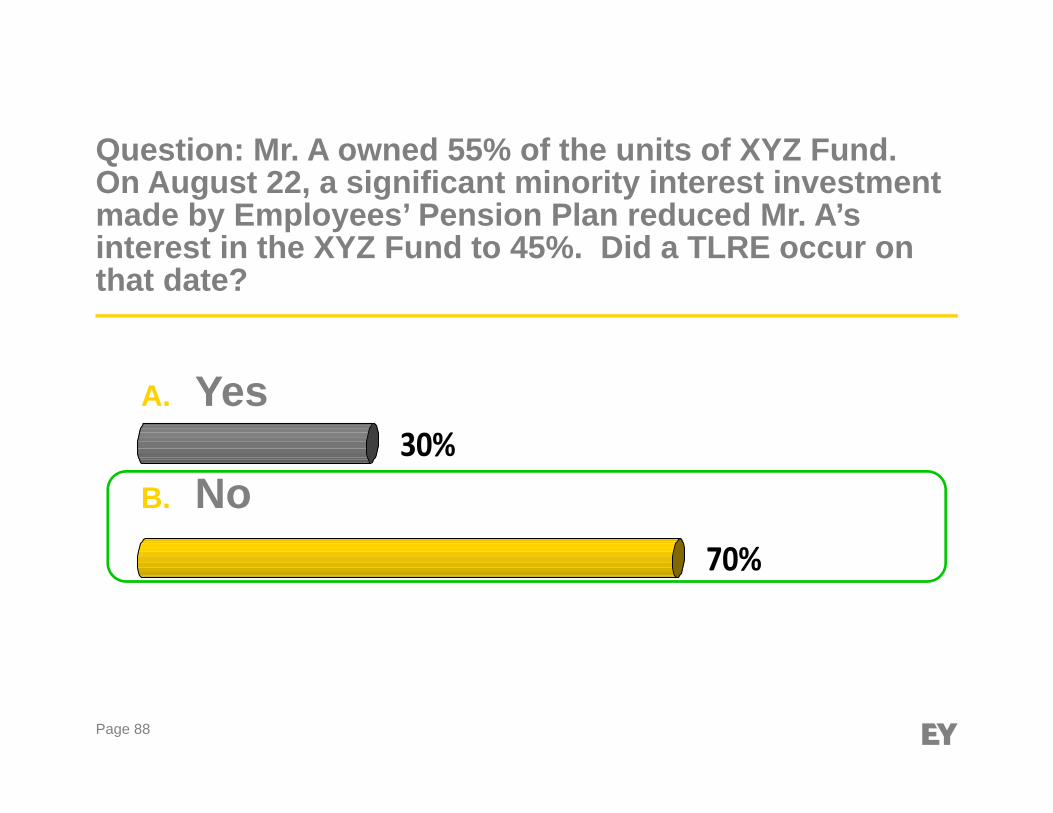

Question: Mr. A owned 55% of the units of XYZ Fund. On August 22, a significant minority interest investment made by Employees’ Pension Plan reduced Mr. A’s interest in the XYZ Fund to 45%. Did a TLRE occur on that date?

Fund Mergers

Page 90

Fund Mergers – Typical legal steps

► Terminating Fund (T-Fund) transfers its property to Continuing Fund (C-Fund)► Retain enough cash (or other property value) to settle liabilities► T-Fund takes back units of C-Fund as consideration for the

property transferred

► T-Fund transfers the C-Fund units to its unitholders as proceeds of redemption of all T-Fund units► T-Fund is dissolved

► A taxable event to T-Fund and its unitholders ► Or undertaken on a Tax-Deferred basis► Where certain conditions met

Page 91

Tax-deferred mergers

► Tax-Deferred Fund Merger rules► MFT’s to merge► MFC convert to MFT ► NOT available for MFT to convert to MFC

► Possible uses► Merge Funds where new Manager► Combine two or more similar Funds► Merge out small/declining Funds► Increase size of Fund to diversify► Reduce fixed administrative costs / MER%

Page 92

Qualifying exchange

► T-Fund must be either MFT or MFC► Not available for Pooled Funds or other Unit trusts

► T-Fund must transfer substantially all property to MFT► Not to MFC► Could be new MFT / election to be MFT from beginning of year

► Must redeem all T-Fund units within 60 days► Cannot be consideration for T-Fund units on redemption other than

C-Fund units (except cash where statutory right of dissent)

► Must file joint election► Within 6 months of transfer time / Minister may extend► Minister may accept joint election to amend or revoke election

Page 93

Tax implications and Considerations

► On a tax deferred merger, the following is true for a continuing fund: ► Can elect the merger to occur at a cost between ACB and FMV► Unused losses expire► CGRM can be utilized► Year end on termination date

► On a taxable merger, the following is true for a continuing fund:► Include property at FMV ► Unused losses do not expire► No year end on termination date

Presentation title

Page 94

Tax implications and Considerations (cont..)

► On a tax deferred merger, the following is true for a terminating fund: ► Can elect the merger to occur at a cost between ACB and FMV► Unused losses expire► CGRM can be utilized► Year end on termination date

► On a taxable merger, the following is true for a continuing fund:► Recognize accrued losses or gains► Unused losses expire► Year end on termination date

Presentation title

Corporate Actions

Page 96

What is a Corporate Action?

► A corporate action is an event initiated by a company, typically a public company, that affect a security holding.

► Companies use corporate actions to achieve financial and non-financial objectives.

► Some examples that affect the securities (equity or debt) issued by the companies include:► One company may takeover, or be taken over by, another

company;► A division may be spun off into a new corporation of a company;► A corporation may undertake a stock split or share consolidation;► Capital may be reorganized.

Page 97

Why do Funds care?

► Funds typically hold equity and debt instruments of corporations in their portfolio.

► The fund is a shareholder of various corporations.► Corporate actions may have a financial impact on the

shareholder.► Tax consequences are typically significant and complex.

Page 98

Why do Funds care?

► The Fund’s income or adjusted cost base (ACB) of the instrument may be impacted by the Corporate Action.

► Funds typically distribute income out to unit-holders to limit taxation in the Fund.

► Incorrect interpretation of a Corporate Action can result in a distribution error within the Net Asset Value (NAV) of the Fund and understated tax liability to the Fund or unit-holders.

Page 99

Why do Funds care?

► Tax information of the investor implications surrounding foreign corporate actions is often non-Canadian.

► Canada Revenue Agency (CRA) will typically respect the legal nature of the foreign transaction.

► Understanding the legal character of each step in a corporate action and local corporate laws will minimize errors for the shareholder.

Page 100

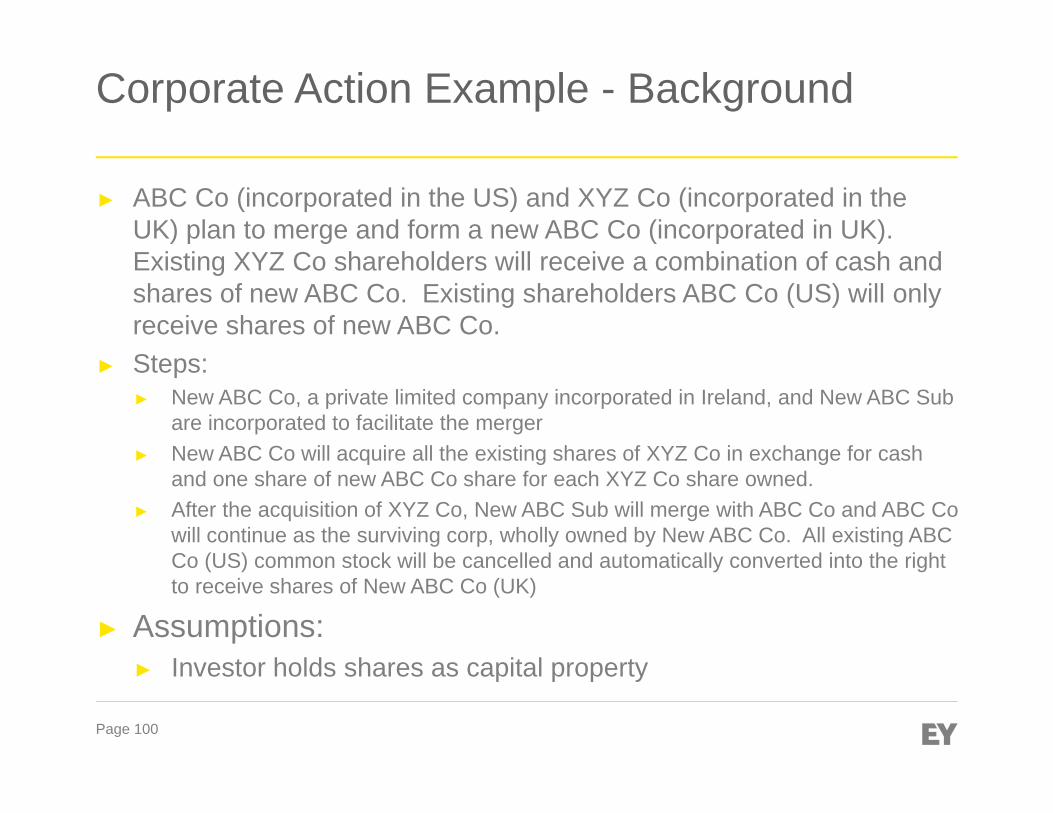

Corporate Action Example - Background

► ABC Co (incorporated in the US) and XYZ Co (incorporated in the UK) plan to merge and form a new ABC Co (incorporated in UK). Existing XYZ Co shareholders will receive a combination of cash and shares of new ABC Co. Existing shareholders ABC Co (US) will only receive shares of new ABC Co.

► Steps:► New ABC Co, a private limited company incorporated in Ireland, and New ABC Sub

are incorporated to facilitate the merger► New ABC Co will acquire all the existing shares of XYZ Co in exchange for cash

and one share of new ABC Co share for each XYZ Co share owned. ► After the acquisition of XYZ Co, New ABC Sub will merge with ABC Co and ABC Co

will continue as the surviving corp, wholly owned by New ABC Co. All existing ABC Co (US) common stock will be cancelled and automatically converted into the right to receive shares of New ABC Co (UK)

► Assumptions:► Investor holds shares as capital property

Page 101

Corporate Action Example

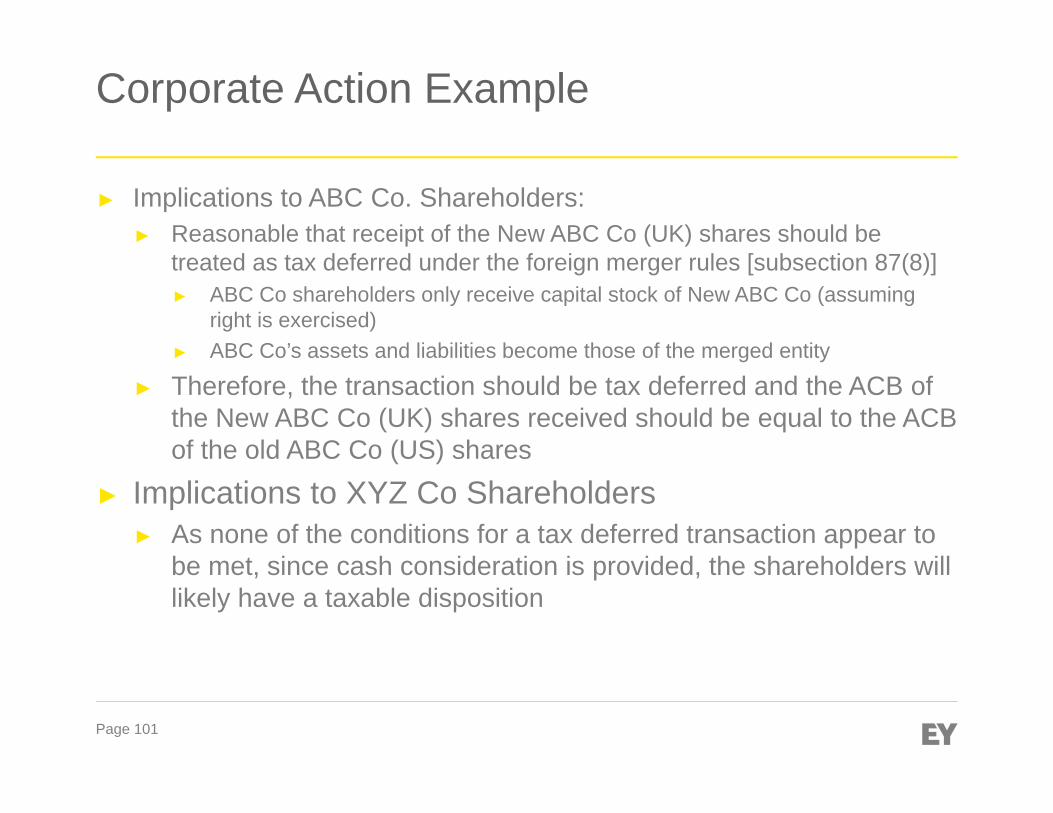

► Implications to ABC Co. Shareholders:► Reasonable that receipt of the New ABC Co (UK) shares should be

treated as tax deferred under the foreign merger rules [subsection 87(8)]► ABC Co shareholders only receive capital stock of New ABC Co (assuming

right is exercised)► ABC Co’s assets and liabilities become those of the merged entity

► Therefore, the transaction should be tax deferred and the ACB of the New ABC Co (UK) shares received should be equal to the ACB of the old ABC Co (US) shares

► Implications to XYZ Co Shareholders► As none of the conditions for a tax deferred transaction appear to

be met, since cash consideration is provided, the shareholders will likely have a taxable disposition

Page 102

Typical Transactions and Tax overview

Typical Transactions 85 85.1 85.1(5) 86 86.1 87 87(8) 51 51.1 15(1)Domestic Merger x xDomestic Acquisition x xDomestic Spin off xDomestic Reorganization of Capital xDomestic Share /Debt Exchange x x x x xForeign Merger xForeign Acquisition xForeign Spin off xForeign Reorganization of Capital xConversion of capital property x x x xRights Issuance xFroeign Share Exchange x x

Income tax Act sections

Page 103

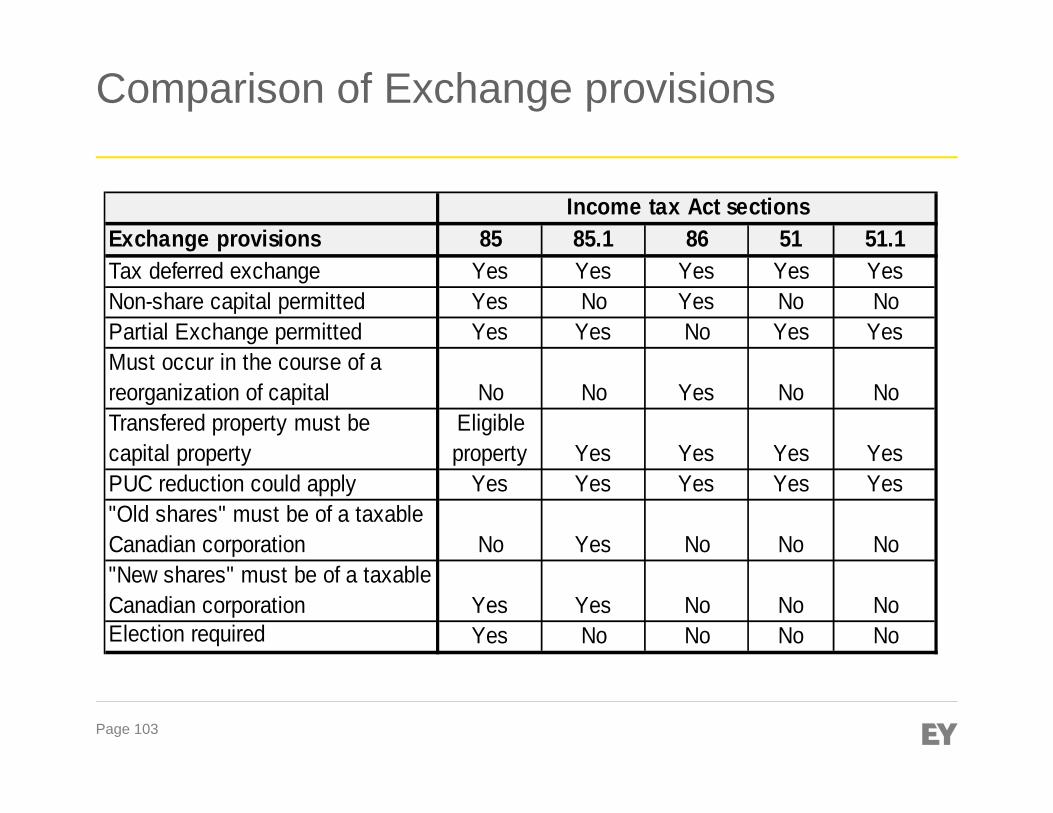

Comparison of Exchange provisions

Exchange provisions 85 85.1 86 51 51.1Tax deferred exchange Yes Yes Yes Yes YesNon-share capital permitted Yes No Yes No NoPartial Exchange permitted Yes Yes No Yes YesMust occur in the course of a reorganization of capital No No Yes No NoTransfered property must be capital property

Eligible property Yes Yes Yes Yes

PUC reduction could apply Yes Yes Yes Yes Yes"Old shares" must be of a taxable Canadian corporation No Yes No No No"New shares" must be of a taxable Canadian corporation Yes Yes No No NoElection required Yes No No No No

Income tax Act sections

Page 104

Thank You!

Page 105 Presentation title

Income vs. capital: an economic perspective to determining taxation characterizationSeptember 2014

Page 107

Income vs capital characterization

► Background: setting the stage:

► What is the issue/problem

► Solutions:

► Legal

► Economic (statistical and qualitative)

► What tax law says

► Economic analysis to support characterization

► Economic tests and examples

► Application examples

► Questions

Page 108

What is the issue/problem

► Distributions to unit holders can be taxed on income or capital account

► For the majority of funds, the capital gain characterization option for distributions is not a straightforward choice and can be challenged by tax authorities

► The capital gain characterization need to be supported if selected:► Court case decisions

► Economic analysis

► Why can we do it?

► Legal precedents can be sited

► Various supporting qualitative and quantitative data are readily available

► Have pure income funds for comparison purposes

► Can easily construct various hypothesis, criteria and tests

Page 109

What is the issue/problem

► To support the capital gain characterization of fund distributions, the following four general hypotheses need to be tested, primarily based on the central concept of the “adventure in the nature of trade”:

1. A fund’s unit (= underlying portfolio assets) is an investment asset with a long-term holding period

2. A fund’s management does not act as a trader of its portfolio assets and does not attempt to time the market on a regular basis

3. Unit holders on average do not act as traders of fund units when buying, holding, and selling these units

4. Fund units can serve as a hedging vehicle.

Page 110

Income vs capital characterization- what tax law says

► The ITA requires a taxpayer to determine if property is being held as inventory or on capital account. It is far from unambiguous

► The ITA has certain deeming provisions which impose characterization on certain property under s 39 (i.e DFA, ECE, Canadian resource property, insurance policies, etc)

► ITA s. 54 addresses computation of capital gains and losses

► Other charging provisions address limitations in respect of expenses, NOLs & NCLs (i.e. s.18(1)(b), s.20, s. 40, 44, 54 & s. 111)

► ITA ss. 39(4) election – provides for capital gains treatment for eligible taxpayer and only on Canadian securities

Page 111

Income vs capital characterization- what CRA says

► IT-346R

► For taxpayers who have transactions in commodities connected with their business, the trading of commodities would be on account of income

► Also applies for taxpayers with special (insider) information

► Taxpayers whose prime or only business activity is trading – income treatment

► Speculators – gains or losses are on capital account

► IT-479R

► A taxpayer may be able to report gains and losses on transactions in commodities or commodity futures as being of an income nature and gains and losses on transactions in securities as being of a capital nature or vice versa

► 9412945

► Generally gains and losses resulting from transactions in commodities by mutual fund trusts are considered to be an adventure in the nature of trade

Page 112

Income vs capital characterization- what CRA says

► 2004-008197

► Mutual fund trust invests in gold and silver physical assets and certificates – held as investment not for speculation

► CRA: question of fact – CRA is still of the opinion that transactions in commodities or commodity related instruments should generally be treated as ordinary income

► 2008-0292461E5

► Corporation purchases commodity for long-term investment – no other business activities

► CRA: question of fact – where a corporation’s primary, principal, main or only activity is transacting in commodities, any gains or losses would be subject to income treatment (business income or adventure in the nature of trade)

Page 113

Income vs capital characterization- what CRA says

► 2010-0381521E5

► Individual purchases commodity (emeralds) and intends to re-invest gains and purchase more commodities

► Where property (emeralds) acquired by a taxpayer is of such a nature or such magnitude that it could not produce income by virtue of its ownership and the only purpose of the acquisition was a subsequent sale of the property, the presumption is that the purchase and sale was an adventure or concern in the nature of trade

► 2010-0355871I7(E)

► underscores the importance of demonstrating linkage how the derivative instrument is to be used for hedging the underlying transaction in order to determine taxation characterization.

Page 114

Income vs capital characterization- what CRA says

► 2011-0392061E5

► Reference to speculators in IT-346 is not intended to cover persons who carry on a business of transacting in commodity futures – those persons should be taxable on income account

► Gains and losses resulting from transactions in commodities by mutual fund corporations or trusts are, generally, considered to be derived from an adventure in the nature of trade and consequently, on income account

Page 115

Income vs capital characterization- what the courts have said

► MNR v. Taylor, 56 DTC 1125 (Ex. Ct.)

► Purchase and sale of 1,500 tons of lead

► Was it an adventure in the nature of trade?

► Is the transaction of the same kind and carried on in the same way as a transaction of an ordinary trader or dealer in property of the same kind?

► Court: was an adventure in the nature of trade

► Nature and quantity – not of an investment nature

Page 116

Income vs capital characterization- what the courts have said

► Wisdom v. Chamberlain (1968), 45 TC 92 (UK C.A.)

► Sale of silver bullion was a profit from adventure in the nature of trade (hedging strategy)

► Transaction entered into on a short-term basis for the purpose of making a profit out of the purchase and sale of a commodity

► Southco Holdings and Management Ltd et al v MNR, 75 DTC 162 (TRB)

► Company purchased and sold gold (forced transaction) within 15 months –claimed capital gain

► Crown: gold only has value when it is sold

► TRB: inconceivable that the taxpayer would buy gold in such a quantity without intention of reselling it at a profit at the earliest opportunity – adventure in the nature of trade

Page 117

Income vs capital characterization- what the courts have said

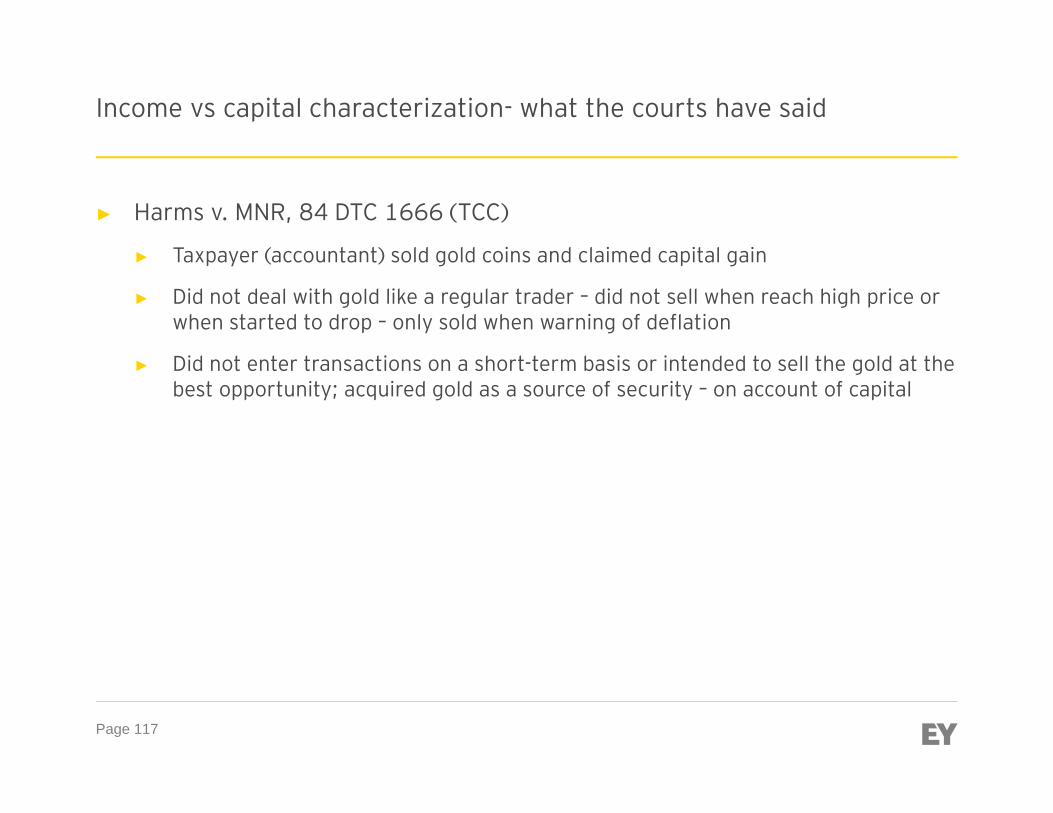

► Harms v. MNR, 84 DTC 1666 (TCC)

► Taxpayer (accountant) sold gold coins and claimed capital gain

► Did not deal with gold like a regular trader – did not sell when reach high price or when started to drop – only sold when warning of deflation

► Did not enter transactions on a short-term basis or intended to sell the gold at the best opportunity; acquired gold as a source of security – on account of capital

Page 118

Economic Analysis - Overview

► The economic analysis can be used to support the arguments raised in court cases:

► Apply the underlying general principles articulated by the courts

► Perform behavioral and economic assessment of the facts.

► The feasibility and economic analysis to test the application of capital vs income hypotheses includes several phases:

► Stage 1: Review background information and behavioural / procedural facts.

► Stage 2: Establish economic hypotheses and design economic tests to assess the income/capital gains characterization;

► Stage 3: Undertake qualitative and quantitative economic analysis and assess whether capital gain or income characterization should be applied;

Page 119

Economic Analysis – Focus Points

Focus points of economic support:

► The capital characterization support revolves around the concept of the “adventure in the nature of trade”:

► Regular operating business vs. investment activity

► Price risk and profit taking behavior

► Asset properties and use

► Questions to ask:

► Did the fund behave as an ordinary asset trader would do?

► Did asset trading represent ordinary business activities of the fund?

► What are the nature and properties of managed asset(s)?

► What was the purpose of asset purchases and how did the asset buyer benefit from asset holdings other than by reselling the asset at a profit?

Page 120

Economic Analysis – Focus Points

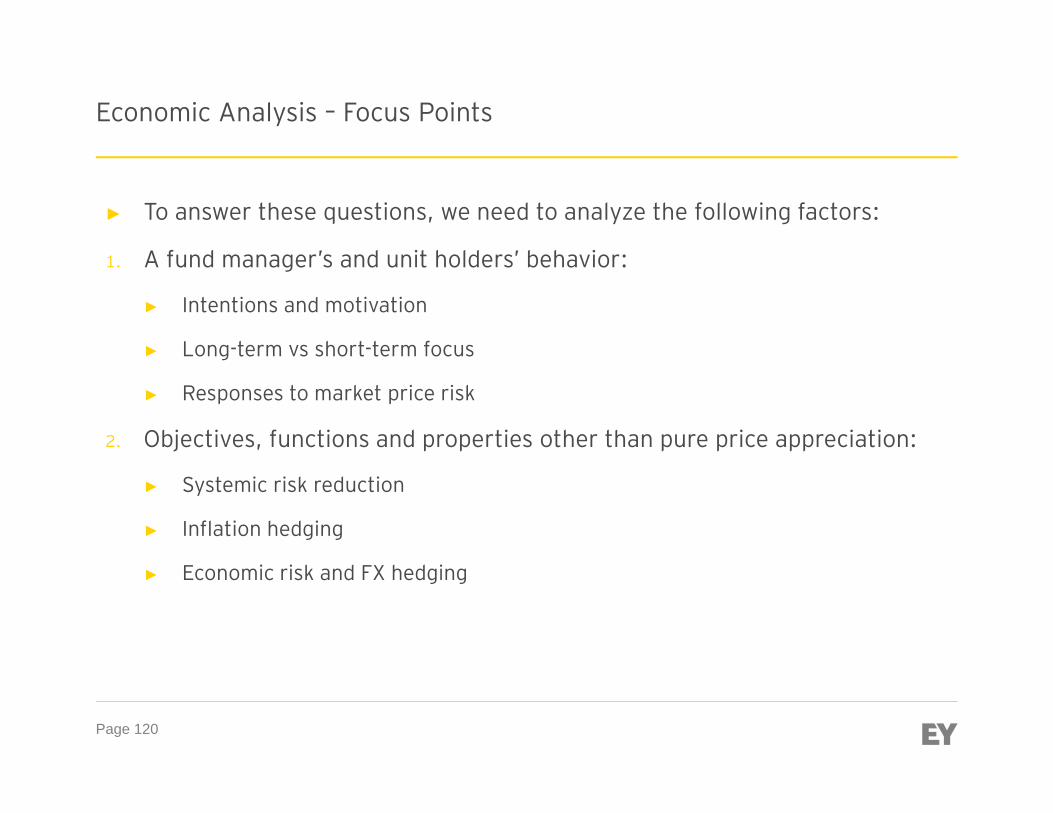

► To answer these questions, we need to analyze the following factors:

1. A fund manager’s and unit holders’ behavior:

► Intentions and motivation

► Long-term vs short-term focus

► Responses to market price risk

2. Objectives, functions and properties other than pure price appreciation:

► Systemic risk reduction

► Inflation hedging

► Economic risk and FX hedging

Page 121

Economic Analysis – Tools of the Trade

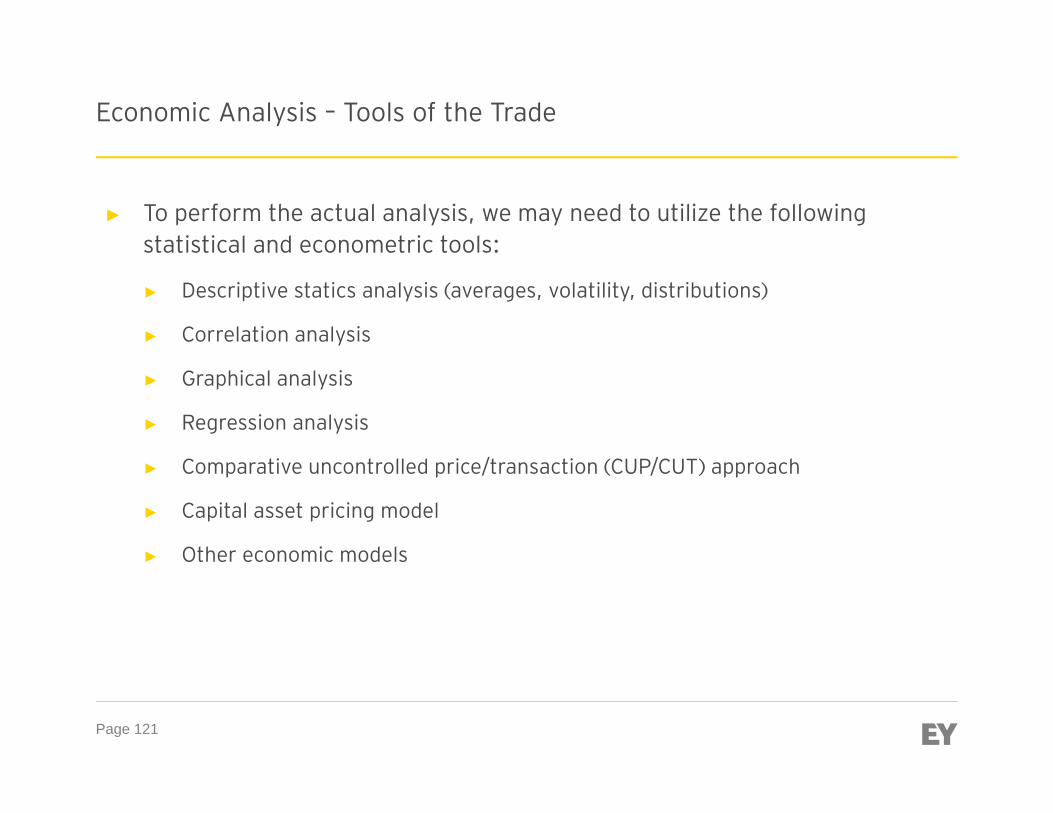

► To perform the actual analysis, we may need to utilize the following statistical and econometric tools:

► Descriptive statics analysis (averages, volatility, distributions)

► Correlation analysis

► Graphical analysis

► Regression analysis

► Comparative uncontrolled price/transaction (CUP/CUT) approach

► Capital asset pricing model

► Other economic models

Page 122

► At this stage, we perform preliminary feasibility assessment to conclude whether it makes sense to proceed with the economic analysis:

► Collect information; analyze the facts and circumstances; and have discussions with portfolio managers to understand whether the fund behaves as an ordinary trader:

► Did the fund sell their asset positions at the best opportunity?

► Was the fund required to sell its assets positions on a regular basis to meet income generation or financing requirements.

► Review of the fund’s trading restrictive provisions and penalties on early terminations by unit holders

► Analyze asset or portfolio properties:

► What was the purpose of asset purchases and how did the asset buyer benefit from asset holdings other than by reselling the asset position at a profit?

Stage 1. Preliminary Review and Assessment

Page 123

► At these stages, the economic hypotheses and tests are defined and applied to test and validate the capital gain characterization.

► The focus is on:

► Fund’s behavior

► Unit holders’ behavior

► Qualitative and quantitative asset properties

Stages 2 and 3. Overview of Hypotheses and Tests

Page 124

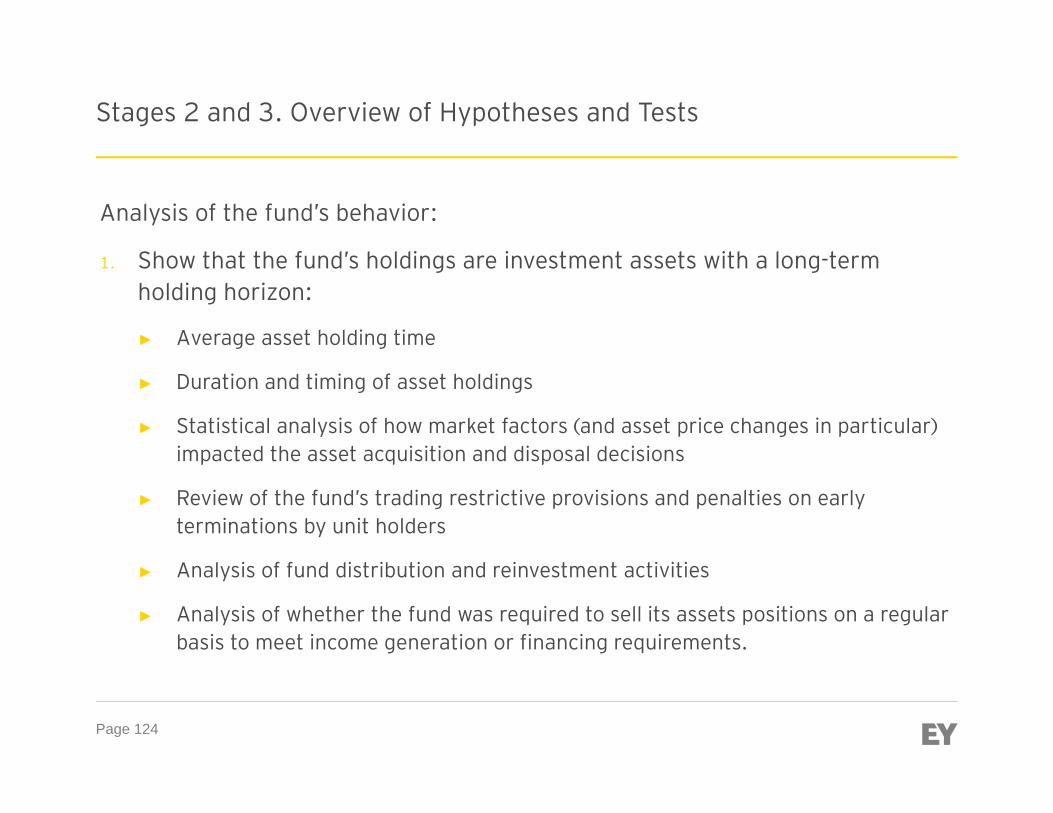

Analysis of the fund’s behavior:

1. Show that the fund’s holdings are investment assets with a long-term holding horizon:

► Average asset holding time

► Duration and timing of asset holdings

► Statistical analysis of how market factors (and asset price changes in particular) impacted the asset acquisition and disposal decisions

► Review of the fund’s trading restrictive provisions and penalties on early terminations by unit holders

► Analysis of fund distribution and reinvestment activities

► Analysis of whether the fund was required to sell its assets positions on a regular basis to meet income generation or financing requirements.

Stages 2 and 3. Overview of Hypotheses and Tests

Page 125

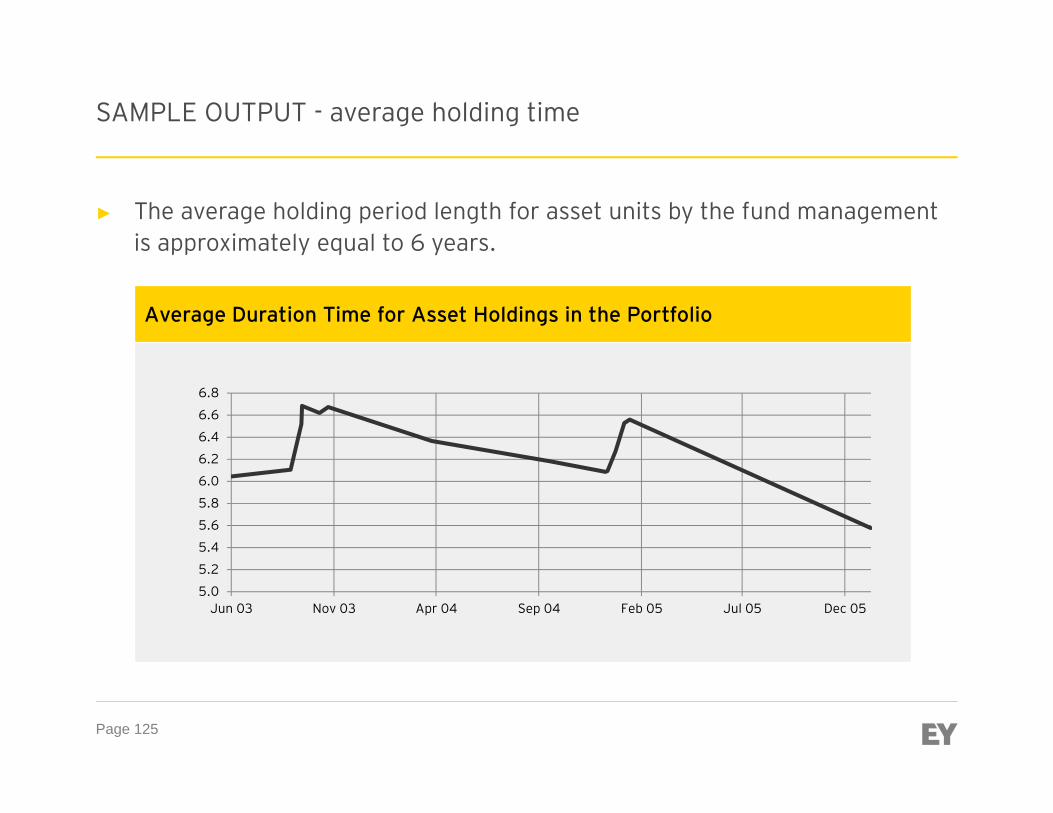

► The average holding period length for asset units by the fund management is approximately equal to 6 years.

Average Duration Time for Asset Holdings in the Portfolio

5.0

5.2

5.4

5.6

5.8

6.0

6.2

6.4

6.6

6.8

Jun 03 Nov 03 Apr 04 Sep 04 Feb 05 Jul 05 Dec 05

SAMPLE OUTPUT - average holding time

Page 126

Analysis of the fund’s behavior (continued):

2. The fund’s management did not act as a trader and did not attempt to time the asset price markets:

► Benchmarking analysis based on market comparables (other funds, indices, futures markets, etc.) that we know that their characterization of distributions to unit holders are on income

► Holding duration tests

► Reinvestment behavior analysis

Stages 2 and 3. Overview of Hypotheses and Tests

Page 127

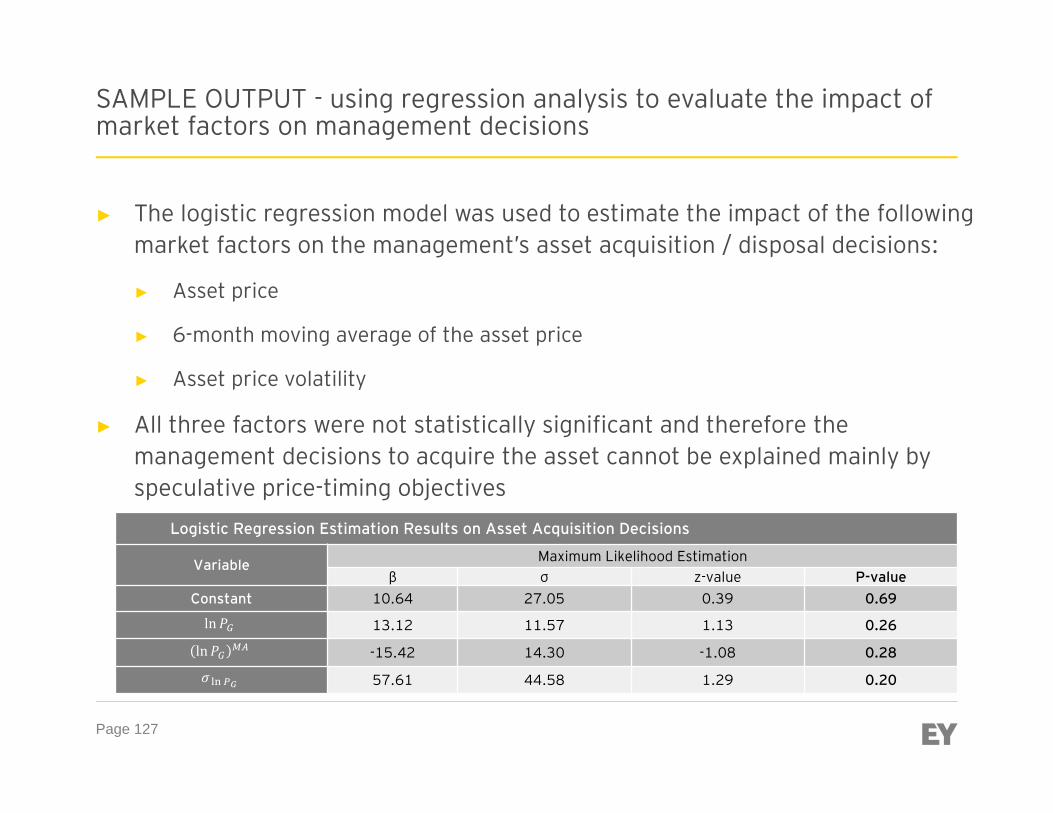

► The logistic regression model was used to estimate the impact of the following market factors on the management’s asset acquisition / disposal decisions:

► Asset price

► 6-month moving average of the asset price

► Asset price volatility

► All three factors were not statistically significant and therefore the management decisions to acquire the asset cannot be explained mainly by speculative price-timing objectives

Logistic Regression Estimation Results on Asset Acquisition Decisions

Variable Maximum Likelihood Estimationβ σ z-value P-value

Constant 10.64 27.05 0.39 0.69

ln 13.12 11.57 1.13 0.26

ln -15.42 14.30 -1.08 0.28

57.61 44.58 1.29 0.20

SAMPLE OUTPUT - using regression analysis to evaluate the impact of market factors on management decisions

Page 128

Analysis of the fund’s behavior (continued):

3. Show that the fund’s target assets, as part of the fund’s asset portfolio, deliver non-price benefits to the fund and unit holders:

► Correlation and timing models (i.e., regression analysis & benchmarking)

► CAPM and beta tests

► Portfolio risk reduction and other efficiency considerations

► Hedge against the risk of deterioration in economic conditions and asset values

4. Analysis of disposition motives by the fund’s management:

► Analysis of distribution patterns and motives

► Redemption requests by unit holders

► Portfolio rebalancing

► Liquidity management considerations

Stages 2 and 3. Overview of Hypotheses and Tests

Page 129

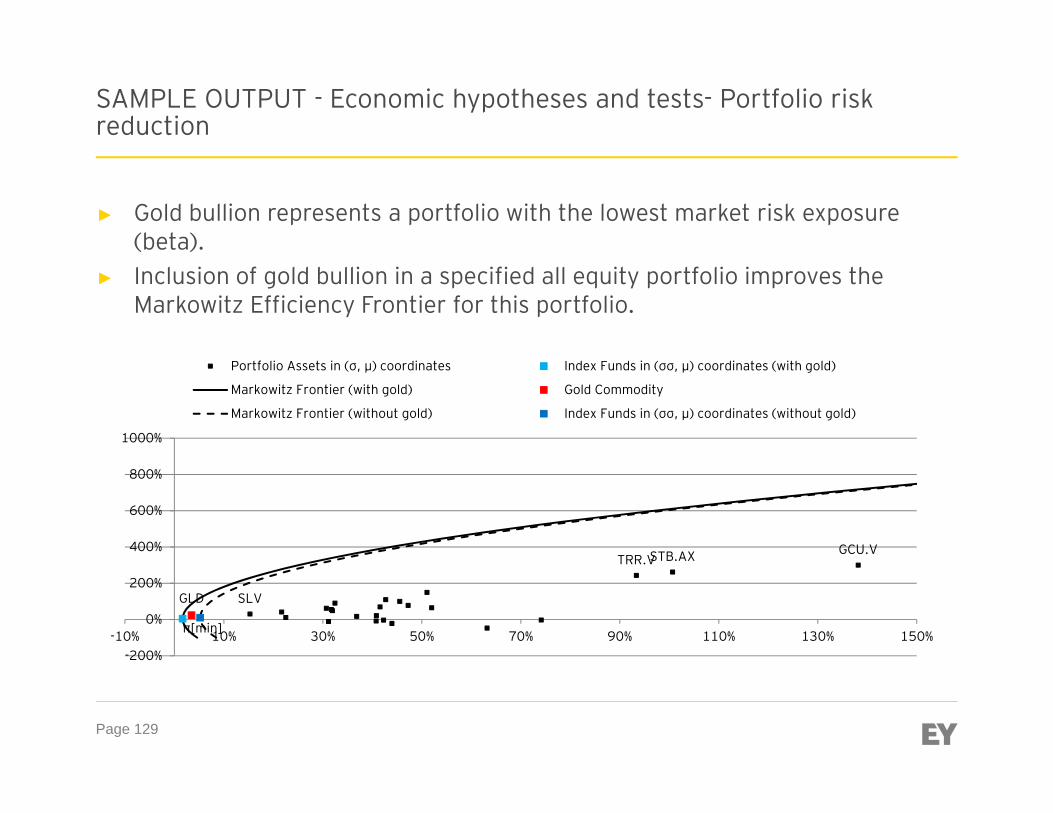

► Gold bullion represents a portfolio with the lowest market risk exposure (beta).

► Inclusion of gold bullion in a specified all equity portfolio improves the Markowitz Efficiency Frontier for this portfolio.

GCU.VSTB.AXTRR.V

SLV

π[min]

GLD

-200%

0%

200%

400%

600%

800%

1000%

-10% 10% 30% 50% 70% 90% 110% 130% 150%

Portfolio Assets in (σ, μ) coordinates Index Funds in (σσ, μ) coordinates (with gold)

Markowitz Frontier (with gold) Gold Commodity

Markowitz Frontier (without gold) Index Funds in (σσ, μ) coordinates (without gold)

SAMPLE OUTPUT - Economic hypotheses and tests- Portfolio risk reduction

Page 130

Analysis of the unit holders’ behavior:

► Average share holding periods

► Duration and timing of positions

► Statistical analysis on correlations between asset price behavior and unit holders’ share acquisition and disposal decisions

Stages 2 and 3. Overview of Hypotheses and Tests

Page 131

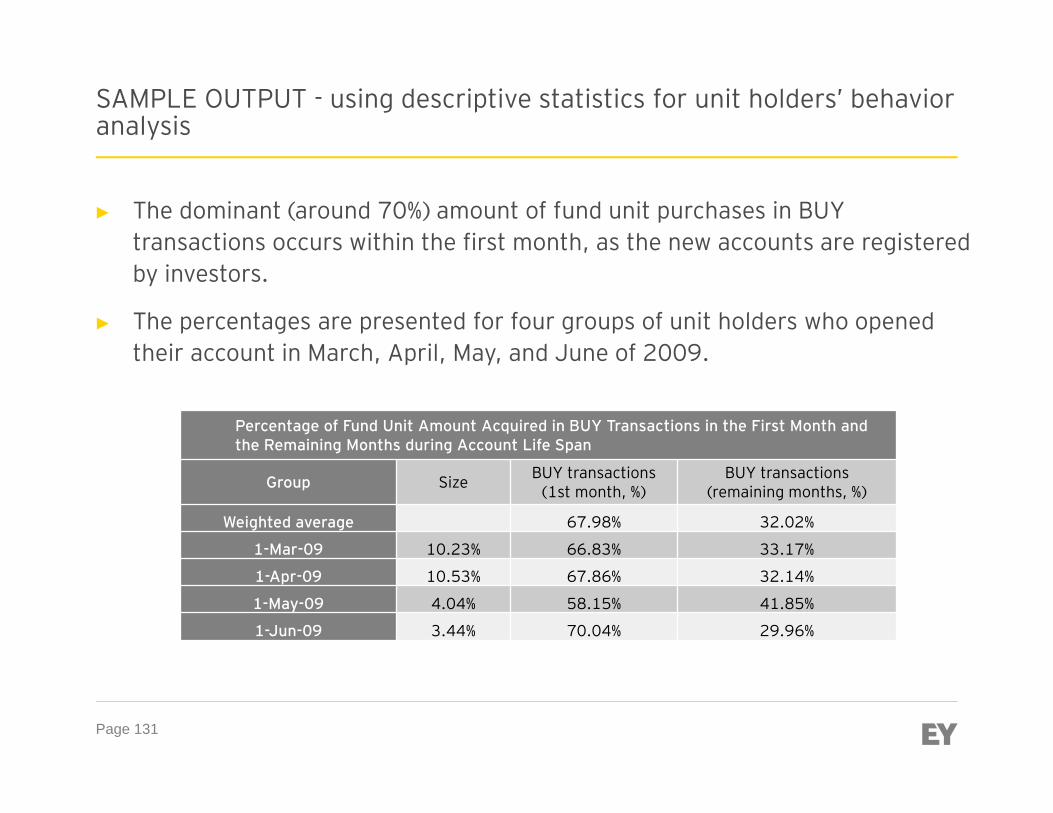

► The dominant (around 70%) amount of fund unit purchases in BUY transactions occurs within the first month, as the new accounts are registered by investors.

► The percentages are presented for four groups of unit holders who opened their account in March, April, May, and June of 2009.

Percentage of Fund Unit Amount Acquired in BUY Transactions in the First Month and the Remaining Months during Account Life Span

Group Size BUY transactions (1st month, %)

BUY transactions (remaining months, %)

Weighted average 67.98% 32.02%

1-Mar-09 10.23% 66.83% 33.17%

1-Apr-09 10.53% 67.86% 32.14%

1-May-09 4.04% 58.15% 41.85%

1-Jun-09 3.44% 70.04% 29.96%

SAMPLE OUTPUT - using descriptive statistics for unit holders’ behavior analysis

Page 132

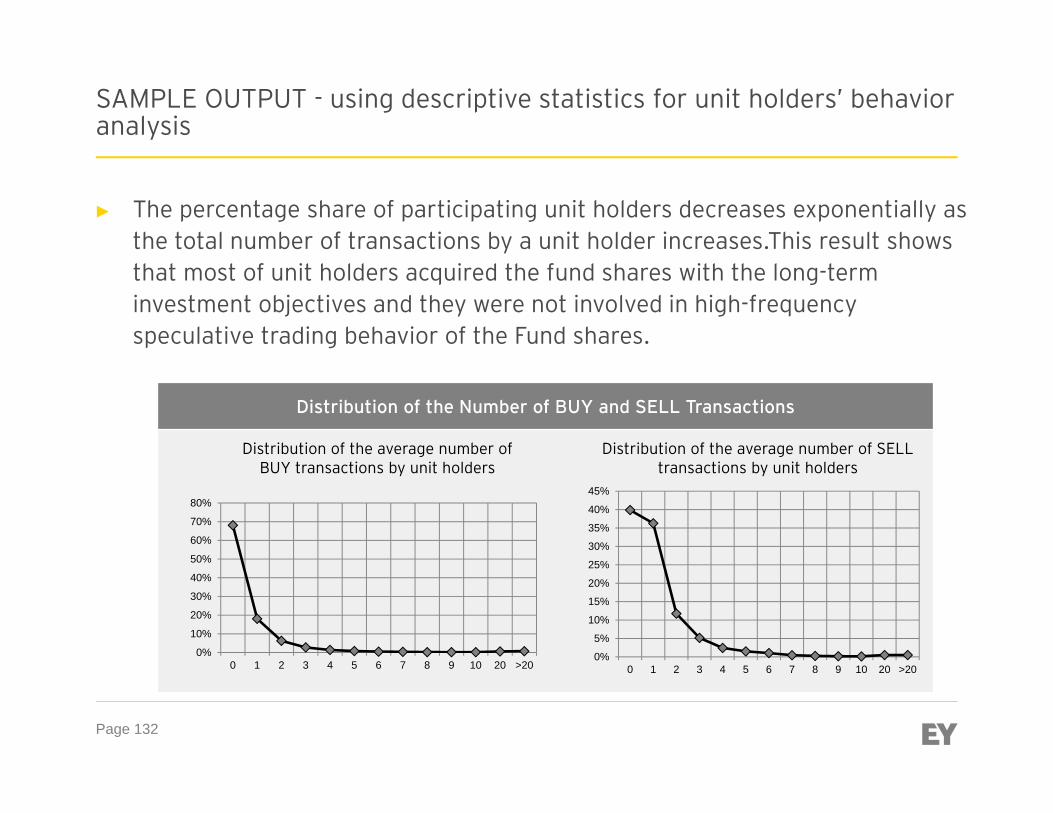

► The percentage share of participating unit holders decreases exponentially as the total number of transactions by a unit holder increases.This result shows that most of unit holders acquired the fund shares with the long-term investment objectives and they were not involved in high-frequency speculative trading behavior of the Fund shares.

Distribution of the Number of BUY and SELL Transactions

0%

10%

20%

30%

40%

50%

60%

70%

80%

0 1 2 3 4 5 6 7 8 9 10 20 >200%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0 1 2 3 4 5 6 7 8 9 10 20 >20

Distribution of the average number of SELLtransactions by unit holders

Distribution of the average number of BUY transactions by unit holders

SAMPLE OUTPUT - using descriptive statistics for unit holders’ behavior analysis

Page 133

Analysis of asset properties:

► Asset hedging functions:

► Inflation risk

► FX risk

► Economic risk

► Systemic risk reduction

► Any other non-price considerations?

Stages 2 and 3. Overview of Hypotheses and Tests

Page 134

Good possible candidates for capital gain characterization:

► Commodity funds

► Fixed income funds

► Market index funds

► Value equity funds

Applications

Page 135

Other considerations:

► Whole asset portfolio vs. portfolio components

► Operating income (dividends/interest/rental payments) vs. capital gain components

► Characterization of accompanying derivatives

► Characterization of the underlying asset

► Functional analysis of hedging strategy

► Characterization caps: under- and overhedging

Applications

Challenges of Structuring New Investment Fund Products

Page 137

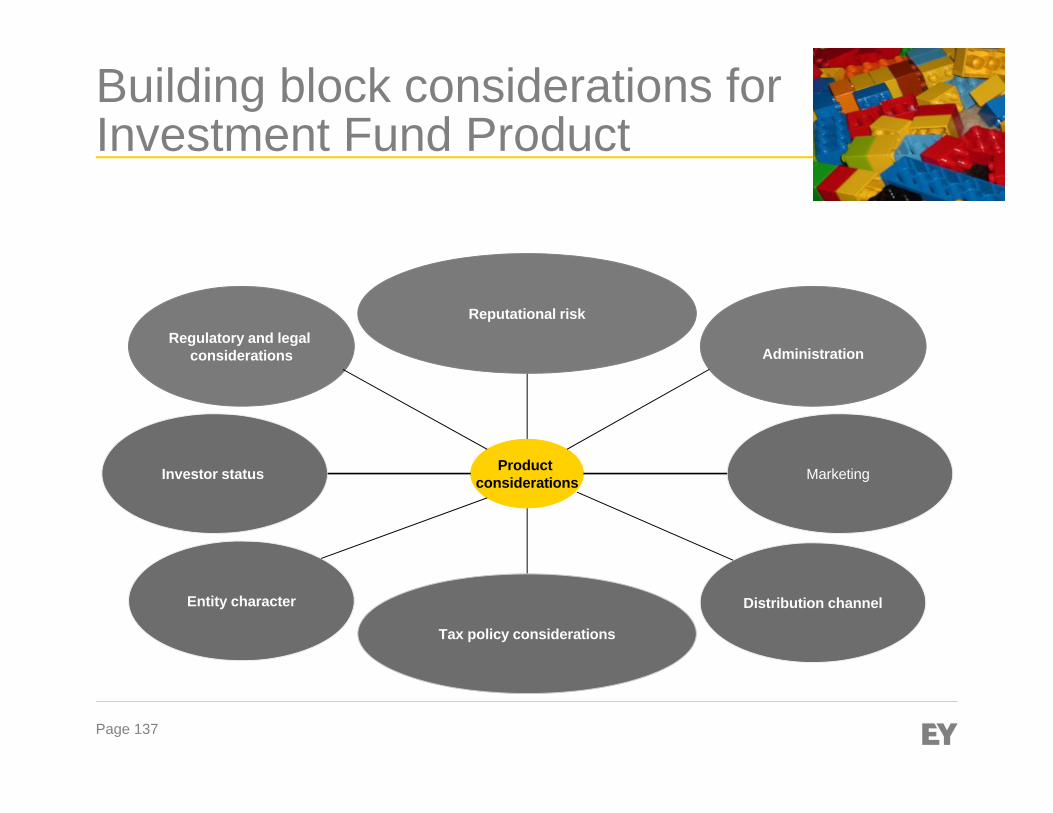

Building block considerations for Investment Fund Product

Product considerations

Regulatory and legal considerations

Reputational risk

Administration

Tax policy considerations

Distribution channel

Marketing Investor status

Entity character

Canada–United States Enhanced Tax Information ExchangeAgreement Implementation Act and Enhanced International Information Reporting-Where are we now?

Taxation of Investment Funds Symposium

11 September 2014

Page 139

Agenda

► Canadian Developments► Global Developments► Key Dates for Canadian Financial Institutions (FIs)► What we have and what is outstanding► Treatment of Canadian Financial Institutions► Sponsoring Entity and Sponsored Investment Entities► Nominee and Client Name Accounts► Portfolio Managers ► OECD Common Reporting Standard ► Moving Forward: Actions Steps to Consider

Page 140

Canadian Developments

► The Canadian government signed a Model 1 IGA on February 5, 2014 (the “Canada IGA”)► Canadian government has signed an Intergovernmental Agreement with the US

government under which it agrees to introduce FATCA-like procedures into Canadian law and, in return, the US government will allow a reduction of the level of effort required to comply

► As such, Canadian financial institutions will have to follow the requirements outlined in the Canada IGA, related implementing legislation and guidance

► Rules to be applied in Canada may be different for branches and entities operating outside of Canada

► Bill C-31 received Royal Assent on June 20, 2014 ► Contains new Part XVIII of the Income Tax Act-i.e. domestic Canadian

legislation to implement the requirements of the Canada IGA (the “Canadian Implementing Legislation”)

Page 141

Canadian Developments (cont’d)

► On June 23 2014, CRA released Guidance on Enhanced Financial Accounts Information Reporting – Part XVIII of the Income Tax Act (the “Canadian Guidance Notes”)► “Notice” issued by CRA regarding calendar years 2014 and 2015 (i.e. transition

period)

Page 142

Global Developments

► IGA Update► To date, over 100 jurisdictions are treated as having an IGA in effect

► Russia is not part of this list

► OECD Common Reporting Standard► On July 21, 2014, the Organization for Economic Co-operation and

Development (OECD) published the Standard for Automatic Exchange of Information in Tax Matters (the “Standard”).► The Standard consists of:

► Model Competent Authority Agreement (“CAA”) and ► The Common Reporting Standard (“CRS”)► There are also extensive commentaries and guidance on technical

solutions for information exchange► Many countries have already agreed to early adoption in 2016► Canada is expected to adopt the CRS

Page 143

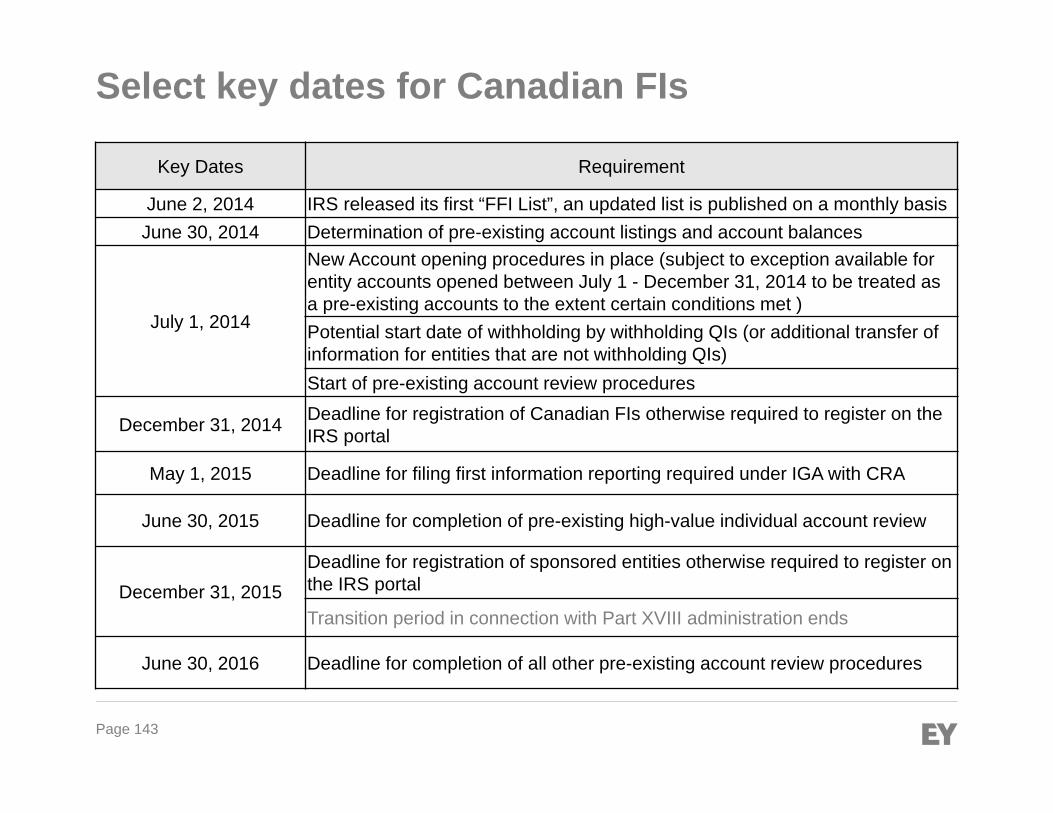

Select key dates for Canadian FIs

Key Dates Requirement

June 2, 2014 IRS released its first “FFI List”, an updated list is published on a monthly basisJune 30, 2014 Determination of pre-existing account listings and account balances

July 1, 2014

New Account opening procedures in place (subject to exception available for entity accounts opened between July 1 - December 31, 2014 to be treated as a pre-existing accounts to the extent certain conditions met )Potential start date of withholding by withholding QIs (or additional transfer of information for entities that are not withholding QIs)Start of pre-existing account review procedures

December 31, 2014 Deadline for registration of Canadian FIs otherwise required to register on the IRS portal

May 1, 2015 Deadline for filing first information reporting required under IGA with CRA

June 30, 2015 Deadline for completion of pre-existing high-value individual account review

December 31, 2015Deadline for registration of sponsored entities otherwise required to register on the IRS portal

Transition period in connection with Part XVIII administration ends

June 30, 2016 Deadline for completion of all other pre-existing account review procedures

Page 144

What we have and what is outstanding

► What we have:► Final FATCA regulations issued January 2013► “Technical corrections” issued in September 2013► Final and temporary regulations revising and further clarifying the final

FATCA regulations issued February 20, 2014 and Regulations to co-ordinate the FATCA Regulations with existing US rules

► Final FFI agreement (Revenue Procedure 2014-13) and “Updated” Final FFI Agreement (Revenue Procedure 2014-38)

► Amended QI Agreement (Revenue Procedure 2014-39)► Notice 2013-43 – Revised Timeline and Other Guidance Regarding the

Implementation of FATCA► IRS Notice 2014-33 – Further Guidance on the Implementation of FATCA

and Related Withholding Provisions► Final forms and instructions for IRS Forms W-9, W-8BEN, W-8BEN-E, W-

8IMY, W-8EXP, W-8ECI ► Final forms and instructions for IRS Forms 1042 and 1042-S

Page 145

What we have and what is outstanding (cont’d)► What we have (continued)

► Final forms and instructions for IRS Form 8966, used to report US owners of foreign accounts or entities

► Three versions of the Model 1 IGA and two versions of Model 2 IGA► Multiple Intergovernmental Agreements (“IGAs”) that have been signed

and a list of countries that have agreed in substance to signing an IGA► OECD CAA and CRS► Canada US IGA issued February 5, 2014 with FAQs, legislative proposals

and explanatory notes► The Canadian Implementing Legislation► Canadian Guidance Notes (dated June 20, 2014)► Certain countries, such as the UK, that have issued FATCA implementing

regulations

Page 146

What we have and what is outstanding (cont’d)► What we have (continued)

► Instructions for the Requester of Forms W-8BEN, W-8BEN-E, W-8ECI, and W-8IMY

► Instructions for using the IRS Portal on which foreign financial institutions (FFIs) will register their FATCA status and other FATCA information

► Form 8957 and instructions for those who are unable to register using the portal► CRA 2015 XML specifications for Part XVIII Information Return► A generally applicable effective date of 1 July 2014 date for FATCA account

onboarding procedures and withholding to the extent required

► What is outstanding:► Canadian instructions on how to complete and file a Part XVIII Information Return –

International Exchange of Information on Financial Accounts slips and summary (under development)

Page 147

Treatment of Canadian Financial Institutions

► To be an Canadian FI under the Canadian Implementing Legislation, an entity must be► A Financial Institution as defined under the Canada IGA► A “listed financial institution” as defined under the Canadian

Implementing Legislation

► A Financial Institution as defined under the Canada IGA includes:► Depository Institutions► Custodial Institutions► Specified Insurance Companies; and ► Investment Entities

Page 148

Treatment of Canadian Financial Institutions (cont’d)

► A “listed financial institution” is defined as:a) an authorized foreign bank within the meaning of section 2 of the Bank Act in

respect of its business in Canada, or a bank to which that Act applies;b) a cooperative credit society, a savings and credit union or a caisse populaire

regulated by a provincial Act;c) an association regulated by the Cooperative Credit Associations Act;d) a central cooperative credit society, as defined in section 2 of the Cooperative

Credit Associations Act, or a credit union central or a federation of credit unions or caisses populaires that is regulated by a provincial Act other than one enacted by the legislature of Quebec;

e) a financial services cooperative regulated by An Act respecting financial services cooperatives, R.S.Q., c. C-67.3, or An Act respecting the Mouvement Desjardins, S.Q. 2000, c. 77;

f) a life company or a foreign life company to which the Insurance Companies Actapplies or a life insurance company regulated by a provincial Act;

g) a company to which the Trust and Loan Companies Act applies;h) a trust company regulated by a provincial Act;

Page 149

Treatment of Canadian Financial Institutions (cont’d)

► A “listed financial institution” is defined as (cont’d):i) a loan company regulated by a provincial Act;j) an entity authorized under provincial legislation to engage in the business

of dealing in securities or any other financial instruments, or to provide portfolio management, investment advising, fund administration or fund management, services;

k) an entity that is represented or promoted to the public as a collective investment vehicle, mutual fund, exchange traded fund, private equity fund, hedge fund, venture capital fund, leveraged buyout fund, or similar investment vehicle that is established to invest or trade in financial assets and that is managed by an entity referred to in the immediately preceding bullet;

l) an entity that is a clearing house or clearing agency; orm) a department or an agent of Her Majesty in right of Canada or of a province that is

engaged in the business of accepting deposit liabilities.

Page 150

Treatment of Canadian Financial Institutions (cont’d)► CRA has provided additional guidance regarding the types of entities that

would be included in paragraphs (j) and (k) of the “listed financial institution” definition

Page 151

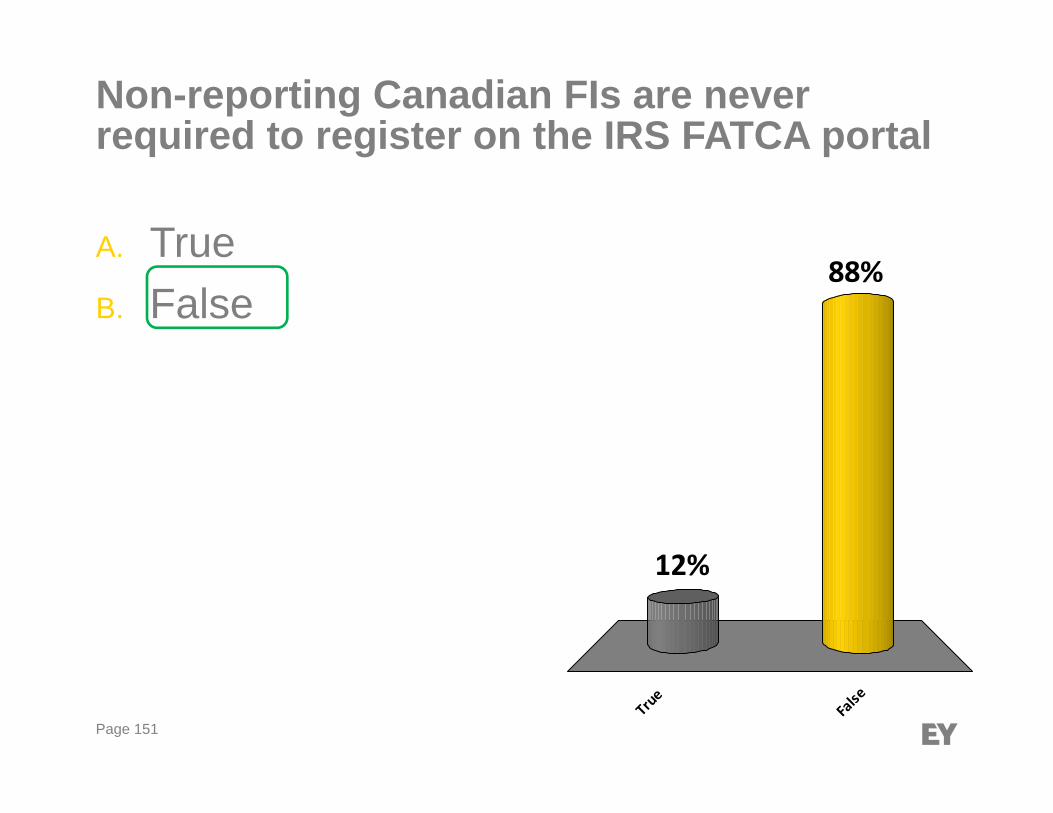

Non-reporting Canadian FIs are never required to register on the IRS FATCA portal

A. TrueB. False

True

False

88%

12%

Page 152

Sponsoring Entity and Sponsored Investment Entities ► The sponsoring entity provisions outlined in the Canada IGA are expected

benefit many fund managers and families of funds► Annex II of the Canada IGA provides that a Canadian FI will be treated as a

non-reporting Canadian FI if the FI meets all of these conditions:a) It is an investment entity established in Canada that is not a qualified

intermediary, withholding foreign partnership, or withholding foreign trust pursuant to relevant U.S. Treasury Regulations; and

b) An entity has agreed with the Financial Institution to act as a sponsoring entity for the Financial Institution AND

c) The sponsoring entity complies with the following requirements:i. The sponsoring entity is authorized to act on behalf of the Financial Institution

(such as a fund manager, trustee, corporate director, or managing partner) to fulfill applicable registration requirements on the IRS FATCA registration website;

Page 153

Sponsoring Entity and Sponsored Investment Entities (cont’d)► The sponsoring entity requirements (cont.)

ii. The sponsoring entity has registered as a sponsoring entity with the IRS on the IRS FATCA registration website;

iii. If the sponsoring entity identifies any U.S. Reportable Accounts with respect to the Financial Institution, the sponsoring entity registers the Financial Institution pursuant to applicable registration requirements on the IRS FATCA registration website on or before the later of December 31, 2015 and the date that is 90 days after such a U.S. Reportable Account is first identified;

iv. The sponsoring entity agrees to perform, on behalf of the Financial Institution, all due diligence, reporting, and other requirements (including providing to any immediate payor the information described in subparagraph 1(e) of Article 4 of the Agreement), that the Financial Institution would have been required to perform if it were a Reporting Canadian Financial Institution;

v. The sponsoring entity identifies the Financial Institution and includes the identifying number of the Financial Institution (obtained by following applicable registration requirements on the IRS FATCA registration website) in all reporting completed on the Financial Institution’s behalf; and

vi. The sponsoring entity has not had its status as a sponsor revoked.

Page 154

Sponsoring Entity and Sponsored Investment Entities (cont’d)

► separate registrations on the IRS FATCA portal are required by a sponsoring entity that is an FI in its own right

Page 155

Dealers and funds are both liable for account documentation, due diligence and information reportingA. TrueB. False

True

False

19%

81%

Page 156

Nominee and Client Name Accounts

► The Canadian Guidance Notes provide clarification with respect to the documentation and reporting responsibilities for accounts held in nominee name and client name

Nominee Accounts► Dealers that hold client units of a fund in nominee name will be responsible for

documenting the underlying client

► Fund is responsible for documenting the nominee (e.g. the dealer)

Client Name Accounts► Investment fund units held in client name will be a financial account to the fund as

well as the dealer

► Therefore both the fund and dealer are responsible for the documentation, due diligence and information reporting

Page 157

Nominee and Client Name Accounts (cont’d)

► Mutual fund dealers, exempt-market dealers, and other investment dealers have due diligence and reporting obligations in connection with the financial accounts they maintain

► CRA expects dealers to perform the due diligence and account classification