Embed Size (px)

Citation preview

Exploring the performanceeffects of key-supplier

collaborationAn empirical investigation into Swiss

buyer-supplier relationships

Daniel CorstenKuehne-Institute for Logistics, University of St Gallen, St Gallen, Switzerland, and

Jan FeldeHilti Corporation, Schaan, Principality of Liechtenstein

Abstract

Purpose – To examine the conditions under which the proposed benefits of collaboration between afirm and its suppliers will occur.

Design/methodology/approach – This paper examines buyer-supplier relationships from the pointof view of the buying firm. The paper is based on a Swiss sample of OEM-supplier relationships. Theresearch question is empirically tested employing a sample of 135 Swiss buyer-supplier relationshipsand using structured equation modelling as well as multi-group comparison to test forquasi-moderation effects. In this paper it is investigated under which condition collaboration withkey suppliers is beneficial for buyers. By linking collaboration with key performance measures andcontrasting its effects with relational constructs like trust and dependence it is hoped to add to thegrowing literature on inter-organizational relationships in supply chain contexts.

Findings – The results demonstrate that supplier collaboration has a positive effect on buyerperformance both in terms of innovative capability and financial results. As expected, trust anddependence play an important role in supplier relationships.

Research limitations/implications – This research is based on a single country (Switzerland)multi-industry study. Generalizability to other industries or countries may be limited.

Practical implications – Supplier relationships need governance modes that balance control andrelational elements. Relationship controlling is an important element in building successful supplierrelationships. In order to be able to reap the benefits of collaboration for the entire company, thepurchasing department needs incentives that support relationship building. Managers leading apurchasing department can learn what structural elements and processes are necessary to obtainoptimal benefits from their supply base.

Originality/value – From a manager’s viewpoint, this paper will provide additional insight intowhen and how collaboration can improve financial performance, enhance innovation, and reducetransaction costs..

Keywords Purchasing, Governance, Switzerland, Trust, Innovation, Financial performance

Paper type Research paper

Exploring the effects of key-supplier collaboration in Swiss buyer-supplierrelationshipsThe collaborative management of key-supplier relationships is an important aspect ofphysical distribution and logistics management as two recent special issues of this

The Emerald Research Register for this journal is available at The current issue and full text archive of this journal is available at

www.emeraldinsight.com/researchregister www.emeraldinsight.com/0960-0035.htm

Swiss buyer-supplier

relationships

445

Received May 2004Accepted November 2004

International Journal of PhysicalDistribution & Logistics Management

Vol. 35 No. 6, 2005pp. 445-461

q Emerald Group Publishing Limited0960-0035

DOI 10.1108/09600030510611666

journal (2003) confirm. Indeed, over the last decades, interest in collaborativerelationships has surged. Hoyt and Huq (2000), for instance, argue that closerbuyer-supplier relationships have evolved over the past two decades from transactionprocesses based on arms-length agreements to collaborative processes based on trustand information sharing and that collaborative buyer-supplier relationships play animportant role in an organization’s ability to respond to dynamic and unpredictablechange. Recent empirical research shows that information sharing in relationshipsincreases financial performance (Droge and Germain, 2000) and that collaboration withexternal supply chain entities increases internal collaboration which in turn improvesservice performance (Stank et al., 2001). It is now commonplace for companies todedicate engineers to key suppliers to learn about their systems, procedures, andprocesses in order to improve communication, reduce errors, and enhance capabilities(Dyer, 1996). Despite – or because – of these developments, there is an increasingfeeling that collaborative buyer-supplier relationships can be “too close for comfort”,particularly with powerful parties (Macdonald, 1995).

In this paper, we will investigate under which condition collaboration with keysuppliers is beneficial for buyers. By linking collaboration with key performancemeasures and contrasting its effects with relational constructs like trust anddependence we hope to add to the growing literature on inter-organizationalrelationships in supply chain contexts. From a manager’s viewpoint, this paper willprovide additional insight into when and how collaboration can improve financialperformance, enhance innovation, and reduce transaction costs.

Conceptual frameworkCollaboration has been a subject of academic debate for an extended period of time.The advantages of close ties with a firm’s suppliers have been highlighted in thecontext of lean management and the Keiretsu model of supplier relationships (Womacket al., 1990) as well as in the alliance literature (Dyer et al., 2001). There is a growingconsensus that collaboration is a specific form of relational exchange (Cannon andPerreault, 1999) which implies “creating value together” (Kanter, 1994). Collaborationhas been referred to as a process requiring “a high level of purposeful cooperation”(Spekman, 1988) and has been conceptualized as the creation of joint processes throughsubstantial investments into co-specialized assets (Dyer, 1996), or simply, “joint action”(Heide and John, 1990). Recently there has been an increasing stream of – largelyconceptual – research on supplier relations in the German literature (Backhaus andBueschgen, 1999; Belz and Muhlmeyer, 2001; Otto and Kotzab, 2003). While empiricalresearch on supplier relations in Switzerland and Germany is scarce (notable exceptioninclude Quayle (2002), Wagner (2001), Szwejczewski (2001) and Corsten (2004)) existingstudies suggest that there are no major differences between supplier relationshippractices in Switzerland, Germany and the rest of Europe.

In this study, we largely follow Heide and John (1990) and define collaboration asjoint action in buyer-supplier relationships and focus on collaborative product andprocess development processes. While suppliers of commodity materials maysometimes negatively influence performance, for example, if they fail to deliver ontime, the performance effects of key-suppliers, i.e. suppliers who supply strategicproducts which are high in value, scarce, or contribute considerably to a buyer’s

IJPDLM35,6

446

performance (Kraljic, 1983) are substantial – both to the advantage or disadvantage ofa buyer. Hence, we focus on the relationships of buyers and their key-suppliers.

In the management and logistics literature collaboration has been linked to a widevariety of benefits such as higher quality and lower costs (Larson, 1994), delivery (Artz,1999) and logistics service performance (Stank et al., 2001), the opportunity to expandproduct and service offerings, the ability to share risks (Parkhe, 1993) and overallperformance (Hewett and Bearden, 2001). Collaboration has also been associated withother relational constructs. Marketing scholars have found that, for instance,dependence (Heide and John, 1988) and trust (Kumar et al., 1995) influence collaborativesuccess. The common assumption is often that collaboration and other relationalconstructs reduce transaction costs and lead to improved business performance. But isthis always true?

While the argument that collaboration leads to improved outcomes typically goesundisputed, there is mounting evidence that not all collaborative efforts are successful.The literature is also rich in examples where collaboration is linked to negativeoutcomes: asset co-specialization is costly and increases the vulnerability toopportunism by the exchange partner (Williamson, 1985). By collaborating closelywith one customer a firm may forego the chance to build economies of scale andachieve a low-cost position (Dyer, 1996). Closer collaboration with a supplier has beenlinked to dependence for knowledge as the buyer may gradually lose the capabilities tobuild and specify the products outsourced (Fine and Whitney, 1996). Particularly in aturbulent environment, relying on a single supplier can be an extremely risky strategy(Singh and Mitchell, 1996).

All together, theoretical arguments and empirical evidence do not paint a clearpicture if and under which conditions supplier collaboration leads to improvedperformance for a buyer. A variety of possible counter-indications leave managers ofbuying firms without guidance when and why to collaborate with their suppliers.

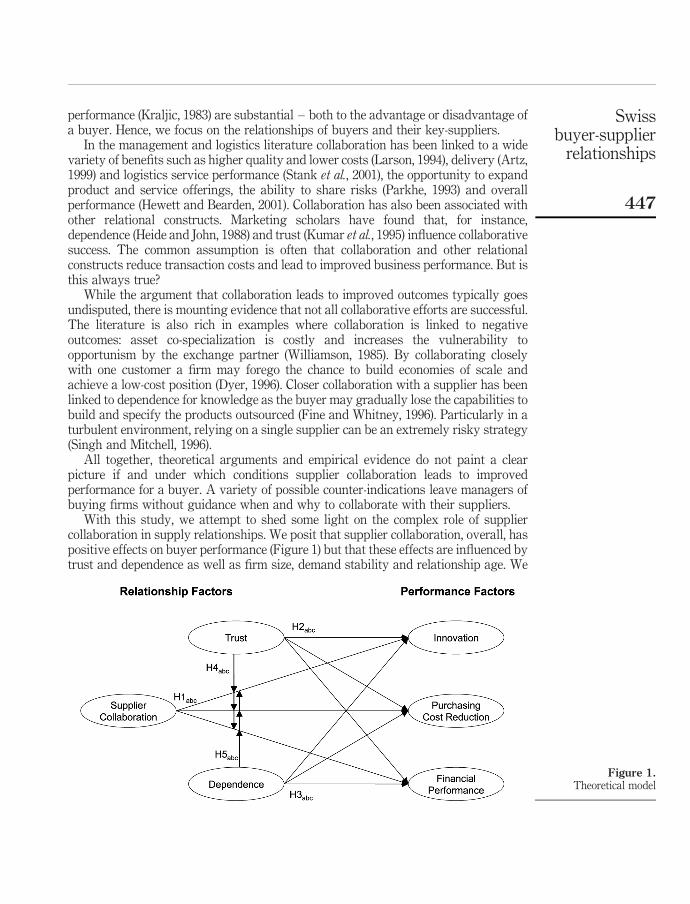

With this study, we attempt to shed some light on the complex role of suppliercollaboration in supply relationships. We posit that supplier collaboration, overall, haspositive effects on buyer performance (Figure 1) but that these effects are influenced bytrust and dependence as well as firm size, demand stability and relationship age. We

Figure 1.Theoretical model

Swissbuyer-supplier

relationships

447

report on an empirical study, which tests these predictions across a sample of 135Swiss buyer-supplier relationships.

Given our objective to assess comprehensively whether buyers benefit fromcollaboration with suppliers, we pursue a broad-based assessment of buyerperformance from three different perspectives – innovation, purchasing costreduction, and financial performance.

Innovation is central to a company’s success as it allows the company to achievetemporary monopoly positions and thus generate superior rents. Hence, innovation is aprerequisite to long-term survival and growth of the firm. Schumpeter (1942) notes thatthe competition that “comes from the new commodity, the new technology, the newsource of supply” is stronger than the competition among firms with similar productsand technologies. In many industries, innovation is often created collaboratively in anetwork of firms (Powell, 1998) particularly among medium sized firms (Jorde andTeece, 1990). By evaluating and finally selecting suppliers the purchasing function hasa strong influence on the innovation performance of the firm. Suppliers may contributeto firm innovation by performing R&D of its own and thus absorbing some of the R&Dcosts the buying firm would have to incur normally. Moreover, suppliers may havevaluable knowledge of production and fulfillment processes that may influence firmperformance. Finally, suppliers can transfer ideas for better products and features thatcould enable the buying firm to enhance products itself. We thus define innovationsuccess as the level of product and process improvements in conjunction with reducedR&D expenses compared to other supplier relationships.

For a buying firm purchasing costs include the costs for coordinating with thesupplier, especially in respect to ordering and transportation (Cannon and Homburg,2001; Williamson, 1985). From a total cost perspective, purchasing costs are animportant determinant of supplier performance (Ellram, 1995). We thus includecommunication, transportation and ordering costs as a performance measure.

Particularly in industrial companies, where key-suppliers often influence overallproduct success, measures of return on assets and sales have gained prominence asmeasures of performance (Droge and Germain, 2000). We thus define financialperformance as the return on assets, return on sales, and the improvement of bothmeasures compared to industry average.

Effects of supplier collaboration on buyers’ performanceScholars have demonstrated that relationships are often the most important source ofnew ideas and information (von Hippel, 1988). Supplier collaboration facilitates thesharing of tacit and explicit knowledge and enhances knowledge creation andinnovation spillover from the supplier (Inkpen, 1996). Furthermore, suppliers play animportant scout function in the innovation process (Walter et al., 2003). Collaborationreduces purchasing cost by lowering contracting cost, frequent communication,improved coordination, and a joint approach to operational problem-solving (Scannellet al., 2000; Cannon and Homburg, 2001). Key suppliers can have considerable impacton the overall well-being of a firm. For example, the top ten suppliers of the UKDepartment for Work and Pensions account for over 50 percent of the total purchasingvolume (Office, 2004). Taken together, improved innovation performance and lower

IJPDLM35,6

448

purchasing costs through key-supplier collaboration should be reflected in a betterfinancial performance of the buying firm. We hypothesize:

H1. The higher a buyer’s level of collaboration with a supplier, (a) the higher abuyer’s innovation level, (b) the lower a buyer’s purchasing cost, and (c) thehigher a buyer’s financial performance.

Effects of trust on buyers’ performanceTrust is sometimes referred to as a “psychological state comprising the intention toaccept vulnerability based upon positive expectations of the intentions or behavior ofanother” (Rousseau et al., 1998). Trust implies that one believes the partner will standby its word, not take unexpected actions with a negative impact on the firm (Andersonand Narus, 1990), fulfil promised role obligations, and conform to the norms ofcooperative behavior (Cannon and Perreault, 1999).

Trust or related constructs such as openness and transparency have been found tohave a positive effect on innovation as knowledge sharing becomes more frequent andricher in content (Hamel, 1991). Trust lowers purchasing cost with a supplier as thelevel of control and costly safeguards against supplier opportunism can be loweredgradually (Ghoshal and Moran, 1996). Furthermore, purchasing cost decreases throughimproved coordination, information quality and process reliability (Zaheer et al., 1998).We posit:

H2. The higher a buyer’s level of trust in a supplier (a) the higher a buyer’sinnovation level, (b) the lower a buyer’s purchasing cost, and (c) the higher abuyer’s financial performance.

Effects of dependence on buyers’ performanceDependence is often referred to as the reliance on actions of another party to achievecertain goals or gratification (Emerson, 1962). Because dependence causes thedependent party to change its behavior in favor of the party depended upon, exercisingthe inherent power is normally not necessary (Provan and Gassenheimer, 1994).

While dependence is mostly defined as the replaceability in terms of marketrelevance (Kumar et al., 1995), recently it has been argued that dependence onsupplier’s knowledge is more eminent. It may diminish a buyer’s capabilities todevelop, specify and ultimately even to evaluate new technologies, a dynamic whichmay eventually deteriorate a buyer’s innovativeness (Fine and Whitney, 1996).Dependence of a buyer may encourage a powerful supplier to divert profits from thebuyer resulting in a negative relationship between dependence and financialperformance for the buyer (Heide and John, 1988).

H3. The higher a buyer’s level of dependence on a supplier, (a) the lower a buyer’sinnovation level, (b) the lower a buyer’s purchasing cost, and (c) the lower abuyer’s financial performance.

Quasi-moderating effects of trust and dependenceIn addition, we argue that the relationship between collaboration and performance isinfluenced by trust and dependence. Following accepted methodological procedures

Swissbuyer-supplier

relationships

449

(Sharma et al., 1981), we simultaneously posit direct and quasi-moderating effects oftrust and dependence in relation to collaboration and the proposed outcomes.

Trust in a supplier enhances the overall effects of collaboration for a buyer as itserves as an additional safeguard against opportunism (Artz, 1999). Trust results in ahigher capacity for collaboration, adaptation, and commitment, which eliminatesfrictions in day-to-day operations, leads to better coordination, which will result inimproved financial performance (Wicks et al., 1999). Moreover, since the emergence oftrust requires intensive socialization which facilitates the exchange of tacit knowledge,trust-based collaborations create redundant and overlapping knowledge bases thatenhance the potential for innovation (Nonaka and Takeuchi, 1995). Since trust reducesthe uncertainty of a partner’s actions and other relational risks, it discounts the“interest” rates for relational investments, encouraging partners to engage incollaborative actions because of an increase in the perceived rate of relational returns(Madhok, 1995).

H4. Under conditions of high trust (as compared to low trust), the relationship ofcollaboration to (a) innovation will be higher, (b) purchasing costs will belower, and (c) financial performance will be higher.

Contrary to the effects in trust-based collaborations, a buyer’s dependence on asupplier negatively affects the overall effects of collaboration. Dependence has beenfound to lead to higher conflict (Kumar et al., 1995), which in turn impedes the flow ofknowledge and erects operational barriers. Collaboration under dependence will beinherently unstable, as the dependent partner may look for alternative sources ofsupply, willing to defect as soon as a window of opportunity opens up. A supplier whoknows that the focal firm is dependent may limit her knowledge transfer initiativestrying to maintain or even widen the knowledge gap. The powerful supplier may easilyshift cost towards the buyer and extract additional profits from the relationship.

H5. Under conditions of high dependence (as compared to low dependence), therelationship of collaboration to (a) innovation will be lower, (b) purchasingcosts will be higher, and (c) financial performance will be lower.

MethodResearch setting and data collection procedureSwitzerland was the research setting. Switzerland forms together with Germany,Austria, and the Netherlands the Germanic Europe Cluster which differs significantlyfrom other clusters on relevant societal culture dimensions. According to Gupta et al.(2002) it is characterized by higher practices of performance orientation, uncertaintyavoidance, future orientation, and assertiveness than many other regional clusters. Theregion is also characterized by relatively low levels of institutional collectivism, groupand family collectivism, gender egalitarianism, and humane orientation and mediumlevels of power distance. Surface area and population vary greatly within the clusterand Switzerland, neighboured by Germany, France, Italy, Austria and Liechtensteinand located at the mountainous center of Europe, ranks the smallest regarding surfacearea (41,000 km2) and population (7.2 million). In addition, its people shows an ethnicmake-up of German (65 percent), French (18 percent) and Italian (10 percent) with

IJPDLM35,6

450

corresponding cultural, religious and economic differences. Perhaps surprisingly, thestudy by Szabo (2002) does not reveal substantial differences between Switzerland andthe rest of the Germanic cluster, neither on a societal culture nor leadership dimensionsuggesting that Switzerland does not differ on important aspects of this study.

A mail survey was selected to examine the effects of supplier collaboration,dependence, and trust on buyer performance. A list of all 894 member firms of theSwiss Association of Purchasing and Material’s Management (SVME) was obtainedand questionnaires, promising confidentiality of responses, and including a cover letterexplaining the purpose of the study were sent out. Three letters were returnedundeliverable. Subsequent e-mail and telephone follow-ups led to multiple waves ofreturned questionnaires and eventually, to a total of 140 questionnaires. Fivequestionnaires containing too many missing values were dropped from the finalsample. Thus, 135 usable responses were received, resulting in a response rate of 15.1percent.

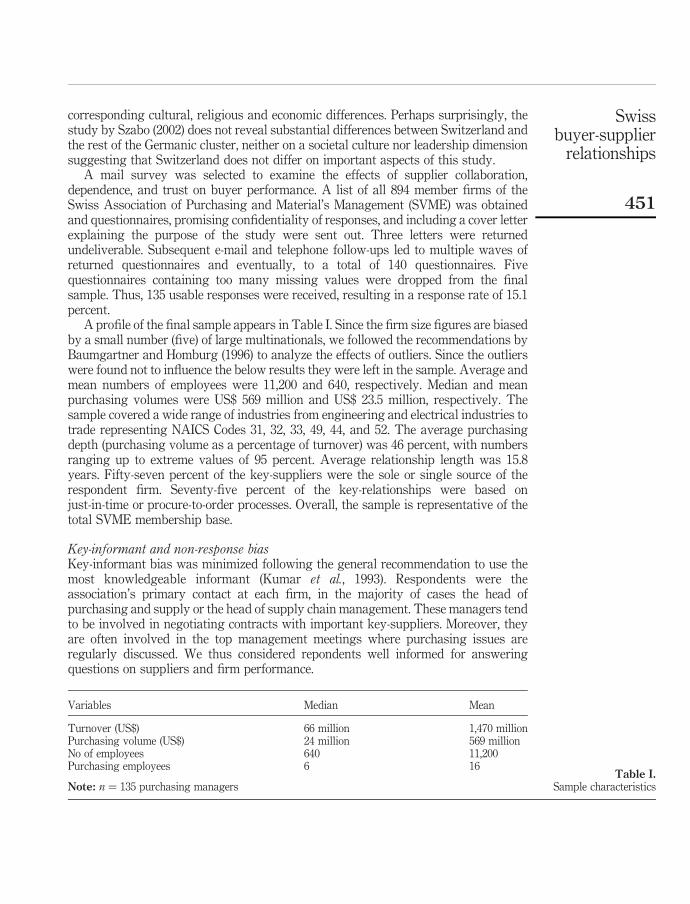

A profile of the final sample appears in Table I. Since the firm size figures are biasedby a small number (five) of large multinationals, we followed the recommendations byBaumgartner and Homburg (1996) to analyze the effects of outliers. Since the outlierswere found not to influence the below results they were left in the sample. Average andmean numbers of employees were 11,200 and 640, respectively. Median and meanpurchasing volumes were US$ 569 million and US$ 23.5 million, respectively. Thesample covered a wide range of industries from engineering and electrical industries totrade representing NAICS Codes 31, 32, 33, 49, 44, and 52. The average purchasingdepth (purchasing volume as a percentage of turnover) was 46 percent, with numbersranging up to extreme values of 95 percent. Average relationship length was 15.8years. Fifty-seven percent of the key-suppliers were the sole or single source of therespondent firm. Seventy-five percent of the key-relationships were based onjust-in-time or procure-to-order processes. Overall, the sample is representative of thetotal SVME membership base.

Key-informant and non-response biasKey-informant bias was minimized following the general recommendation to use themost knowledgeable informant (Kumar et al., 1993). Respondents were theassociation’s primary contact at each firm, in the majority of cases the head ofpurchasing and supply or the head of supply chain management. These managers tendto be involved in negotiating contracts with important key-suppliers. Moreover, theyare often involved in the top management meetings where purchasing issues areregularly discussed. We thus considered repondents well informed for answeringquestions on suppliers and firm performance.

Variables Median Mean

Turnover (US$) 66 million 1,470 millionPurchasing volume (US$) 24 million 569 millionNo of employees 640 11,200Purchasing employees 6 16

Note: n ¼ 135 purchasing managersTable I.

Sample characteristics

Swissbuyer-supplier

relationships

451

To account for non-response bias, we compared our sample and the population of theSVME regarding the industry structure as well as early with late respondents(Armstrong and Overton, 1977). The first 75 percent of returned questionnaires weredefined as early respondents and the last 25 percent as late (Li and Calantone, 1998).Using two-tailed t-tests, we compared early with late respondents on all constructs andthe descriptive variables shown above. Since no significant differences ð p , 0:10Þwere observed, non-response bias does not appear to be a problem although a morestringent test would have been to compare respondents with non-respondentsfollowing the procedures suggested by Mentzer and Flint (1997).

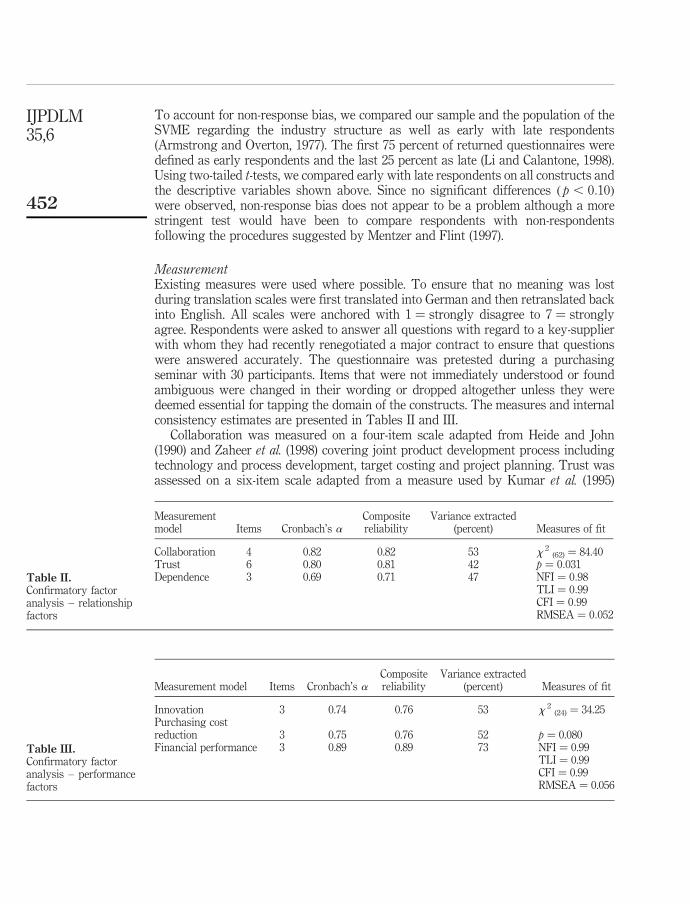

MeasurementExisting measures were used where possible. To ensure that no meaning was lostduring translation scales were first translated into German and then retranslated backinto English. All scales were anchored with 1 ¼ strongly disagree to 7 ¼ stronglyagree. Respondents were asked to answer all questions with regard to a key-supplierwith whom they had recently renegotiated a major contract to ensure that questionswere answered accurately. The questionnaire was pretested during a purchasingseminar with 30 participants. Items that were not immediately understood or foundambiguous were changed in their wording or dropped altogether unless they weredeemed essential for tapping the domain of the constructs. The measures and internalconsistency estimates are presented in Tables II and III.

Collaboration was measured on a four-item scale adapted from Heide and John(1990) and Zaheer et al. (1998) covering joint product development process includingtechnology and process development, target costing and project planning. Trust wasassessed on a six-item scale adapted from a measure used by Kumar et al. (1995)

Measurement model Items Cronbach’s aCompositereliability

Variance extracted(percent) Measures of fit

Innovation 3 0.74 0.76 53 x 2(24) ¼ 34.25

Purchasing costreduction 3 0.75 0.76 52 p ¼ 0.080Financial performance 3 0.89 0.89 73 NFI ¼ 0.99

TLI ¼ 0.99CFI ¼ 0.99RMSEA ¼ 0.056

Table III.Confirmatory factoranalysis – performancefactors

Measurementmodel Items Cronbach’s a

Compositereliability

Variance extracted(percent) Measures of fit

Collaboration 4 0.82 0.82 53 x 2(62) ¼ 84.40

Trust 6 0.80 0.81 42 p ¼ 0:031Dependence 3 0.69 0.71 47 NFI ¼ 0:98

TLI ¼ 0:99CFI ¼ 0:99RMSEA ¼ 0:052

Table II.Confirmatory factoranalysis – relationshipfactors

IJPDLM35,6

452

assessing the supplier’s honesty and benevolence. Dependence was measured on athree-item scale adapted from Kumar et al. (1995) covering a supplier’s replaceability, abuyer’s resource dependence, and a supplier’s influence on a firm’s overall success.

Buyer’s performance was measured with three three-item scales. The scale forinnovation was adapted from Gilley and Rasheed (2000) and covers improved productand process innovation as well as a decrease in research and development expense.The scale for purchasing cost reduction was inspired by Cannon and Homburg (2001)encompassing coordination, ordering and transportation costs. The financialperformance scale was adapted from Droge and Germain (2000) and Gilley andRasheed (2000) and assesses, over a period of three years, the return on sales and assetsas well as a more general statement on the improvement of financial results. All itemsare listed in the Appendix.

Reliability and validityFor the full sample, we conducted exploratory factor analyses to purify the scales.Items with loadings of less than 0.40 on the intended factor and/or cross-loadings withother factors of more than 0.35 were deleted unless they were essential for tapping theconstruct domain. Other items were deleted because of low variance and the possibilityof multiple interpretations. All scales were close or exceeded the recommended level of0.70 for Cronbach’s a providing evidence of reliability.

We estimated two measurement models for exogenous (i.e. collaboration, trust, anddependence) and endogenous (i.e. innovation, purchasing cost reduction, and financial)variables. Tests for uni-dimensionality, convergent validity, and discriminant validityof the measures were conducted separately for each model following therecommendations of Anderson and Gerbing (1988). The items representing eachconstruct were subjected to a series of confirmatory factor analyses via the AMOS 4.01software package (Arbuckle, 1999).

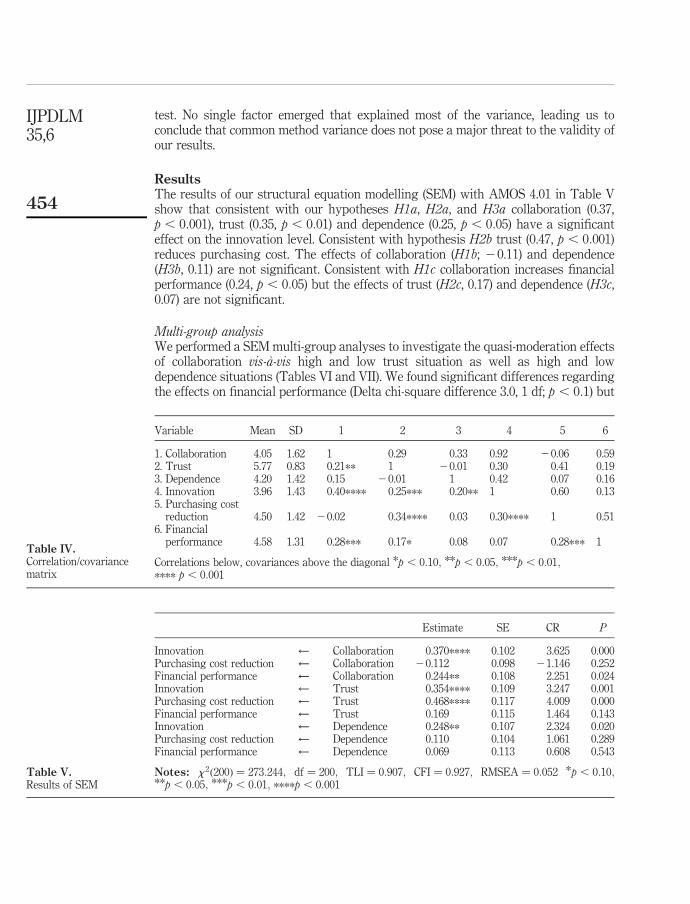

Our results are presented in Tables II and III. The chi-square is significant for boththe exogenous (84, df ¼ 62; p ¼ 0:031) and the endogenous model (34, df ¼ 24;p ¼ 0:080). In addition, and given the limitations of our sample size, we estimated a setof generally recommended fit measures (Garver and Mentzer, 1999). For both theexogenous (NFI 0.976, TLI 0.993, CFI 0.995, RMSEA 0.044) and endogenous model (NFI0.989, TLI 0.994, CFI 0.997, RMSEA 0.056) the fit measures suggest a good fit of thedata to the models. Table IV shows the factor correlation matrix. We tested fordiscriminant validity using the procedures suggested by Anderson and Gerbing (1988)and Fornell and Larcker (1981). All the correlations between the constructs weresignificantly below 1 ð p , 0:001Þ and from the covariance’s f-matrix we observed thatthe correlations between any construct plus/minus twice the standard error did notinclude 1. In addition, the 15 squared correlation coefficients, i.e. shared variancesamong all possible pairs of constructs were substantially lower than the averagevariance extracted for the constructs.

Common method variance can be a problem in survey-based research if bothdependent and independent variables are perceptual measures. Because most firms inour sample were privately held, independent estimates of firm performance were notavailable. However, during questionnaire design, we followed the recommendations byPodsakoff and Organ (1986) and, in addition, post hoc performed Harmann’s one factor

Swissbuyer-supplier

relationships

453

test. No single factor emerged that explained most of the variance, leading us toconclude that common method variance does not pose a major threat to the validity ofour results.

ResultsThe results of our structural equation modelling (SEM) with AMOS 4.01 in Table Vshow that consistent with our hypotheses H1a, H2a, and H3a collaboration (0.37,p , 0:001), trust (0.35, p , 0:01) and dependence (0.25, p , 0:05) have a significanteffect on the innovation level. Consistent with hypothesis H2b trust (0.47, p , 0:001)reduces purchasing cost. The effects of collaboration (H1b; 20.11) and dependence(H3b, 0.11) are not significant. Consistent with H1c collaboration increases financialperformance (0.24, p , 0:05) but the effects of trust (H2c, 0.17) and dependence (H3c,0.07) are not significant.

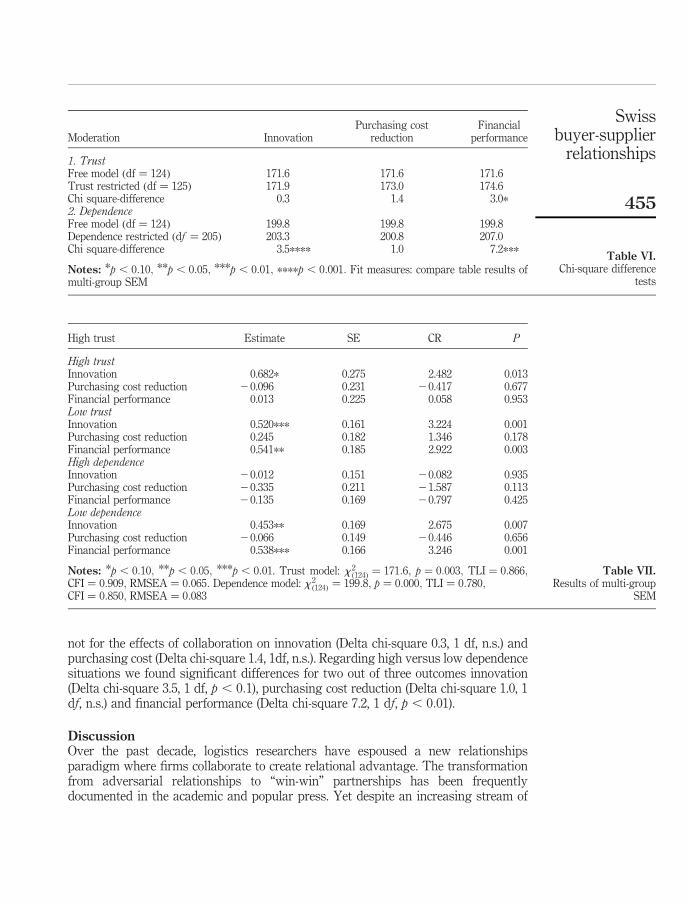

Multi-group analysisWe performed a SEM multi-group analyses to investigate the quasi-moderation effectsof collaboration vis-a-vis high and low trust situation as well as high and lowdependence situations (Tables VI and VII). We found significant differences regardingthe effects on financial performance (Delta chi-square difference 3.0, 1 df; p , 0:1) but

Estimate SE CR P

Innovation ˆ Collaboration 0.370**** 0.102 3.625 0.000Purchasing cost reduction ˆ Collaboration 20.112 0.098 21.146 0.252Financial performance ˆ Collaboration 0.244** 0.108 2.251 0.024Innovation ˆ Trust 0.354**** 0.109 3.247 0.001Purchasing cost reduction ˆ Trust 0.468**** 0.117 4.009 0.000Financial performance ˆ Trust 0.169 0.115 1.464 0.143Innovation ˆ Dependence 0.248** 0.107 2.324 0.020Purchasing cost reduction ˆ Dependence 0.110 0.104 1.061 0.289Financial performance ˆ Dependence 0.069 0.113 0.608 0.543

Notes: x 2ð200Þ ¼ 273:244; df ¼ 200; TLI ¼ 0:907; CFI ¼ 0:927; RMSEA ¼ 0:052 *p , 0:10;**p , 0:05; ***p , 0:01; ****p , 0:001

Table V.Results of SEM

Variable Mean SD 1 2 3 4 5 6

1. Collaboration 4.05 1.62 1 0.29 0.33 0.92 20.06 0.592. Trust 5.77 0.83 0.21** 1 20.01 0.30 0.41 0.193. Dependence 4.20 1.42 0.15 20.01 1 0.42 0.07 0.164. Innovation 3.96 1.43 0.40**** 0.25*** 0.20** 1 0.60 0.135. Purchasing cost

reduction 4.50 1.42 20.02 0.34**** 0.03 0.30**** 1 0.516. Financial

performance 4.58 1.31 0.28*** 0.17* 0.08 0.07 0.28*** 1

Correlations below, covariances above the diagonal *p , 0:10; **p , 0:05; ***p , 0:01;

**** p , 0:001

Table IV.Correlation/covariancematrix

IJPDLM35,6

454

not for the effects of collaboration on innovation (Delta chi-square 0.3, 1 df, n.s.) andpurchasing cost (Delta chi-square 1.4, 1df, n.s.). Regarding high versus low dependencesituations we found significant differences for two out of three outcomes innovation(Delta chi-square 3.5, 1 df, p , 0:1), purchasing cost reduction (Delta chi-square 1.0, 1df, n.s.) and financial performance (Delta chi-square 7.2, 1 df, p , 0:01).

DiscussionOver the past decade, logistics researchers have espoused a new relationshipsparadigm where firms collaborate to create relational advantage. The transformationfrom adversarial relationships to “win-win” partnerships has been frequentlydocumented in the academic and popular press. Yet despite an increasing stream of

Moderation InnovationPurchasing cost

reductionFinancial

performance

1. TrustFree model ðdf ¼ 124Þ 171.6 171.6 171.6Trust restricted ðdf ¼ 125Þ 171.9 173.0 174.6Chi square-difference 0.3 1.4 3.0*2. DependenceFree model ðdf ¼ 124Þ 199.8 199.8 199.8Dependence restricted ðdf ¼ 205Þ 203.3 200.8 207.0Chi square-difference 3.5**** 1.0 7.2***

Notes: *p , 0:10; **p , 0:05; ***p , 0:01; ****p , 0:001: Fit measures: compare table results ofmulti-group SEM

Table VI.Chi-square difference

tests

High trust Estimate SE CR P

High trustInnovation 0.682* 0.275 2.482 0.013Purchasing cost reduction 20.096 0.231 20.417 0.677Financial performance 0.013 0.225 0.058 0.953Low trustInnovation 0.520*** 0.161 3.224 0.001Purchasing cost reduction 0.245 0.182 1.346 0.178Financial performance 0.541** 0.185 2.922 0.003High dependenceInnovation 20.012 0.151 20.082 0.935Purchasing cost reduction 20.335 0.211 21.587 0.113Financial performance 20.135 0.169 20.797 0.425Low dependenceInnovation 0.453** 0.169 2.675 0.007Purchasing cost reduction 20.066 0.149 20.446 0.656Financial performance 0.538*** 0.166 3.246 0.001

Notes: *p , 0:10; **p , 0:05; ***p , 0:01. Trust model: x 2ð124Þ ¼ 171:6; p ¼ 0:003; TLI ¼ 0:866;

CFI ¼ 0:909; RMSEA ¼ 0:065: Dependence model: x 2ð124Þ ¼ 199:8; p ¼ 0:000; TLI ¼ 0:780;

CFI ¼ 0:850; RMSEA ¼ 0:083

Table VII.Results of multi-group

SEM

Swissbuyer-supplier

relationships

455

research on collaboration, studies that take a balanced view on the positive andnegative effects of collaboration are still small in number. Taken as a whole, the resultsof our study support the notion that supplier collaboration is beneficial for buyer firms.However, the influence of trust and dependence on collaborative success is complex.Despite – or because – of the recent interest in collaboration among academics andpractitioners alike, collaboration is often seen as inherently positive, encouragingmanagers to engage in collaboration without taking into account the contingencies ofcollaborative success. Thus, our study adds to the logistics literature with a morenuanced assessment of the role of collaboration in relational exchange.

Theoretical implicationsOverall, collaboration, trust and – surprisingly – dependence enhance the buyer’sinnovation level. The truthful exchange of tacit knowledge and explicit informationtends to enhance the innovation success for a buying company even whencollaborating with powerful suppliers. In addition, trust reduces the purchasing costand collaboration improves financial outcomes of buyers. It seems as if the fruits offaithful joint value creation off-set the initial investments into joint processes toincrease business results.

Surprisingly, the effect of collaboration on financial performance is stronger underconditions of low trust compared to high trust. We speculate that the safeguardingeffect of collaboration is stronger in low trust situations where the risks of opportunismare high and joint actions ensure harmonized processes and capabilities. In high trustsituations incentives are more aligned and the protective effect of collaboration seemsto be substantially lower. An alternative explanation is that in collaborativerelationship high trust can be detrimental because too much trust can lead “too closefor comfort” (Macdonald, 1995) and to vulnerability towards a supplier. Somewhatcounterintuitively, we find that collaboration has a stronger effect on innovation andfinancial performance in the context of low vis-a-vis high dependence. We suspectpowerful buyers benefit even more from collaboration because they dominate thepartnership and may dispose of alternative sources of supply.

Implications for managersSupplier collaboration is not always a guaranteed road to improving firm performance.Before entering a long-term relationship, a buying firm needs to decide what objectivesshe pursues with a particular relationship. Segmenting suppliers can help to decidewhat the right relationship is for each supplier. Only once the objectives are clear and apotential group of collaboration suppliers has been identified, should a firm moveforward and invest in deepening selected relationships. Collaboration needs to beembedded in a wider set of governance mechanisms that should include relationshipcontrolling, dependence monitoring and trust building. Finding the right balance ofgovernance modes – both control-type and relational – is often more difficult thansetting-up the necessary collaborative processes. In collaborative relationshipscomplex trade-offs must be considered because the benefits of collaboration do notcome for free. Relationship controlling should focus not on a single performancemeasure but should employ a balanced approach taking into consideration innovation,purchasing costs, and financial performance.

IJPDLM35,6

456

Innovation and overall financial performance are rarely used to evaluate thepurchasing department. In order to overcome potential obstacles en route tocollaboration with key-suppliers the performance measures used to evaluatepurchasing need to be changed. A balanced-scorecarding approach (Kaplan andNorton, 1996) to supplier collaboration whereby the multiple indicators for the variousstrategic goals are employed, may help achieve collaborative success. A first step couldbe to give purchasing a voice on the management board that is equal to the increasingleverage held by purchasing managers. In addition, top management needs to take aninterest in the decisions that are taken in the purchasing department. Departmentthinking leads to decisions that are sub-optimal for the whole enterprise. One potentialarea for further research could be the influence of various performance measures on theperformance on the buying department and the enterprise as a whole.

LimitationsOur study is based on a cross-sectional sample in Switzerland which is positivebecause the results are more representative than industry-specific studies. However,big differences are known to exist between industries and to influence the results. Dueto the limited number of firms in each industry, we were unable to perform ouranalyses on a per industry basis. It would be desirable to perform similar studies in anumber of industries to be able to compare the results.

It would be particularly interesting to study the link between collaboration and thebuying but also the supplying firm’s archival performance or investigate the influenceof mutual dependence. However, given the fact that most of the companies in oursample are privately held and the information required has to be considered highlyconfidential, we were unable to obtain real performance data. Nevertheless, a link toreal performance measures, e.g. item prices, would be desirable to increase the validityof results in future studies.

References

Anderson, J.C. and Gerbing, D.W. (1988), “Structural equation modeling in practice: a review andrecommended two-step approach”, Psychological Bulletin, Vol. 103 No. 3, pp. 411-23.

Anderson, J.C. and Narus, J.A. (1990), “A model of distributor firm and manufacturer firmworking partnerships”, Journal of Marketing, Vol. 54 No. 1, pp. 42-58.

Arbuckle, J.L. (1999), AMOS 4.01, Small Waters Corp., Chicago, IL.

Armstrong, J.S. and Overton, T.S. (1977), “Estimating nonresponse bias in mail surveys”, Journalof Marketing Research, Vol. 14 No. 3, pp. 396-402.

Artz, K.W. (1999), “Buyer-supplier performance: the role of asset specificity, reciprocalinvestments and relational exchange”, British Journal of Management, Vol. 10 No. 2,pp. 113-26.

Backhaus, K. and Bueschgen, J. (1999), “The paradox of unsatisfying but stable relationships – alook at German car suppliers”, Journal of Business Research, Vol. 46, pp. 245-57.

Baumgartner, H. and Homburg, C. (1996), “Applications of structural equation modelling inmarketing and consumer research: a review”, International Journal of Research inMarketing, Vol. 13 No. 2, pp. 139-61.

Belz, C. and Muhlmeyer, J. (2001), Key Supplier Management, Thexis, St Gallen.

Swissbuyer-supplier

relationships

457

Cannon, J.P. and Homburg, C. (2001), “Buyer-supplier relationships and customer firm costs”,Journal of Marketing, Vol. 65 No. 1, pp. 29-43.

Cannon, J.P. and Perreault, W.D. (1999), “Buyer-seller relationships in business markets”, Journalof Marketing Research, Vol. 36 No. 4, pp. 439-60.

Corsten, D. (2004), Efficient Consumer Response Adoption, Haupt, Bern.

Droge, C. and Germain, R. (2000), “The relationship of electronic data interchange with inventoryand financial performance”, Journal of Business Logistics, Vol. 21 No. 2, pp. 209-30.

Dyer, J.H. (1996), “Does governance matter? Keiretsu alliances and asset specificity as sources ofJapanese competitive advantage”, Organization Science, Vol. 7 No. 6, pp. 649-66.

Dyer, J.H., Kale, P. and Singh, H. (2001), “How to make strategic alliances work”, SloanManagement Review, Vol. 42 No. 4, pp. 37-43.

Ellram, L.M. (1995), “Total cost of ownership”, International Journal of Physical Distribution &Logistics Management, Vol. 25 No. 8, pp. 4-23.

Emerson, R.M. (1962), “Power-dependence relations”, American Sociological Review, Vol. 27 No. 1,pp. 31-41.

Fine, C.H. and Whitney, D.E. (1996), “Is the make-buy decision process a core competence?”,research paper, MIT, Cambridge, MA.

Fornell, C. and Larcker, D.F. (1981), “Evaluating structural equation models with unobservablevariables and measurement error”, Journal of Marketing Research, Vol. 18 No. 1, pp. 39-50.

Garver, M.S. and Mentzer, J.T. (1999), “Logistics research methods: employing structuralequation modeling to test for construct validity”, Journal of Business Logistics, Vol. 20No. 1, pp. 33-57.

Ghoshal, S. and Moran, P. (1996), “Bad for practice: a critique of transaction cost theory”,Academy of Management Review, Vol. 21 No. 1, pp. 13-47.

Gilley, K.M. and Rasheed, A. (2000), “Making more by doing less: an analysis of outsourcing andits effects on firm performance”, Journal of Management, Vol. 26 No. 4, pp. 763-90.

Gupta, V., Hanges, P.J. and Dorfman, P. (2002), “Cultural clusters: methodology and findings”,Journal of World Business, Vol. 37, pp. 11-15.

Hamel, G. (1991), “Competition for competence and inter-partner learning within internationalstrategic alliances”, Strategic Management Journal, Vol. 12, pp. 83-103.

Heide, J.B. and John, G. (1988), “The role of dependence balancing in safeguardingtransaction-specific assets in conventional channels”, Journal of Marketing, Vol. 52 No. 1,pp. 20-35.

Heide, J.B. and John, G. (1990), “Alliances in industrial purchasing: the determinants of jointaction in buyer-supplier relationships”, Journal of Marketing Research, Vol. 27 No. 1,pp. 24-36.

Hewett, K. and Bearden, W.O. (2001), “Dependence, trust, and relational behavior on the part offoreign subsidiary marketing operations: implications for managing global marketingoperations”, Journal of Marketing, Vol. 65 No. 4, pp. 51-66.

Hoyt, J. and Huq, F. (2000), “From arms-length to collaborative relationships in the supply chain”,International Journal of Physical Distribution & Logistics Management, Vol. 30 No. 9,pp. 750-64.

Inkpen, A.C. (1996), “Creating knowledge through collaboration”, California ManagementReview, Vol. 39 No. 1, pp. 123-40.

IJPDLM35,6

458

Jorde, T.M. and Teece, D.J. (1990), “Innovation and cooperation: implications for competition andantitrust”, Journal of Economic Perspectives, Vol. 4 No. 3, pp. 75-96.

Kanter, R.M. (1994), “Collaborative advantage: the art of alliances”, Harvard Business Review,Vol. 72 No. 4, pp. 96-108.

Kaplan, R.S. and Norton, D.P. (1996), The Balanced Scorecard: Translating Strategy into Action,Harvard Business School Press, Boston, MA.

Kraljic, P. (1983), “Purchasing must become supply management”, Harvard Business Review,Vol. 61 No. 5, pp. 109-17.

Kumar, N., Stern, L.W. and Anderson, J.C. (1993), “Conducting interorganizational research usingkey informants”, Academy of Management Journal, Vol. 36 No. 6, pp. 1633-51.

Kumar, N., Scheer, L.K. and Steenkamp, J-B.E.M. (1995), “The effects of perceivedinterdependence on dealer attitudes”, Journal of Marketing Research, Vol. 32 No. 3,pp. 348-56.

Larson, P.D. (1994), “An empirical study of inter-organizational functional integration and totalcosts”, Journal of Business Logistics, Vol. 15 No. 1, pp. 153-69.

Li, T. and Calantone, R.J. (1998), “The impact of market knowledge competence on new productadvantage: conceptualization and empirical examination”, Journal of Marketing, Vol. 62No. 4, pp. 13-29.

Macdonald, S. (1995), “Too close for comfort? The strategic implications of getting close to thecustomer”, California Management Review, Vol. 37 No. 4, pp. 8-27.

Madhok, A. (1995), “Revisiting multinational firms’ tolerance for joint ventures: a trust-basedapproach”, Journal of International Business Studies, Vol. 26 No. 1, pp. 117-37.

Mentzer, J.T. and Flint, D.J. (1997), “Validity in logistics research”, Journal of Business Logistics,Vol. 18 No. 1, pp. 199-216.

Nonaka, I. and Takeuchi, H. (1995), The Knowledge-Creating Company: How Japanese CompaniesCreate the Dynamics of Innovation, Oxford University Press, New York, NY.

Office, N.A. (2004), Improving Procurement, report by the Comptroller and Auditor General, Vol.HC 361-II.

Otto, A. and Kotzab, H. (2003), “Does supply chain management really pay? Six perspectives tomeasure the performance of managing a supply chain”, European Journal of OperationalResearch, Vol. 144 No. 2, pp. 306-20.

Parkhe, A. (1993), “Strategic alliance structuring: a game theoretic and transaction costexamination of interfirm cooperation”, Academy of Management Journal, Vol. 36 No. 4,pp. 794-829.

Podsakoff, P.M. and Organ, D.W. (1986), “Self-reports in organizational research: problems andprospects”, Journal of Management, Vol. 12 No. 4, pp. 531-44.

Powell, W.W. (1998), “Learning from collaboration: knowledge networks in the biotechnologyand pharmaceutical industries”, California Management Review, Vol. 40 No. 3, pp. 228-40.

Provan, K.G. and Gassenheimer, J.B. (1994), “Supplier commitment in relational contractexchanges with buyers: a study of interorganizational dependence and exercised power”,Journal of Management Studies, Vol. 31 No. 1, pp. 55-68.

Quayle, M. (2002), “Purchasing policy in Switzerland: an empirical study of sourcing”,Thunderbird International Business Review, Vol. 44 No. 2, pp. 205-36.

Swissbuyer-supplier

relationships

459

Rousseau, D.M., Sitkin, S.B., Burt, R.S. and Camerer, C. (1998), “Not so different after all: across-discipline view of trust”, Academy of Management Review, Vol. 23 No. 3, pp. 393-404.

Scannell, T.V., Vickery, S.K. and Droge, C.L. (2000), “Upstream supply chain management andcompetitive performance in the automotive supply industry”, Journal of Business Logistics,Vol. 21 No. 1, pp. 23-48.

Schumpeter, J.A. (1942), Capitalism, Socialism and Democracy, Harper Brothers, New York, NY.

Sharma, S., Durand, R.M. and Gur-Arie, O. (1981), “Identification and analysis of moderatorvariables”, Journal of Marketing Research, Vol. 18 No. 3, pp. 291-300.

Singh, K. and Mitchell, W. (1996), “Precarious collaboration: business survival after partners shutdown or form new partnerships”, Strategic Management Journal, Vol. 17 No. 7, pp. 99-115.

Spekman, R.E. (1988), “Strategic supplier selection: understanding long-term buyerrelationships”, Business Horizons, Vol. 31 No. 4, pp. 75-81.

Stank, T.P., Keller, S.B. and Daugherty, P.J. (2001), “Supply chain collaboration and logisticalservice performance”, Journal of Business Logistics, Vol. 22 No. 1, pp. 29-48.

Szabo, E.E.A. (2002), “The Germanic Europe Cluster: where employees have a voice”, Journal ofWorld Business, Vol. 37, pp. 55-68.

Szwejczewski, M.E.A. (2001), “Supplier management in German manufacturing companies”,International Journal of Physical Distribution & Logistics Management, Vol. 31 No. 5,pp. 354-73.

von Hippel, E. (1988), The Sources of Innovation, Oxford University Press, New York, NY.

Wagner, S.M. (2001), Strategisches Lieferantenmanagement in Industrieunternehmen, PeterLang, Frankfurt.

Walter, A., Muller, T.A., Helfert, G. and Ritter, T. (2003), “Functions of industrial supplierrelationships and their impact on relationship quality”, Industrial Marketing Management,Vol. 32, pp. 159-69.

Wicks, A.C., Berman, S.L. and Jones, T.M. (1999), “The structure of optimal trust: moral andstrategic implications”, Academy of Management Review, Vol. 24 No. 1, pp. 99-116.

Williamson, O.E. (1985), The Economic Institutions Of Capitalism, The Free Press, New York,NY.

Womack, J.P., Jones, D.T. and Roos, D. (1990), The Machine that Changed the World: The Story ofLean Production, Rawson Associates, New York, NY.

Zaheer, A., McEvily, B. and Perrone, V. (1998), “Does trust matter? Exploring the effects ofinterorganizational and interpersonal trust on performance”, Organization Science, Vol. 9No. 2, pp. 141-59.

IJPDLM35,6

460

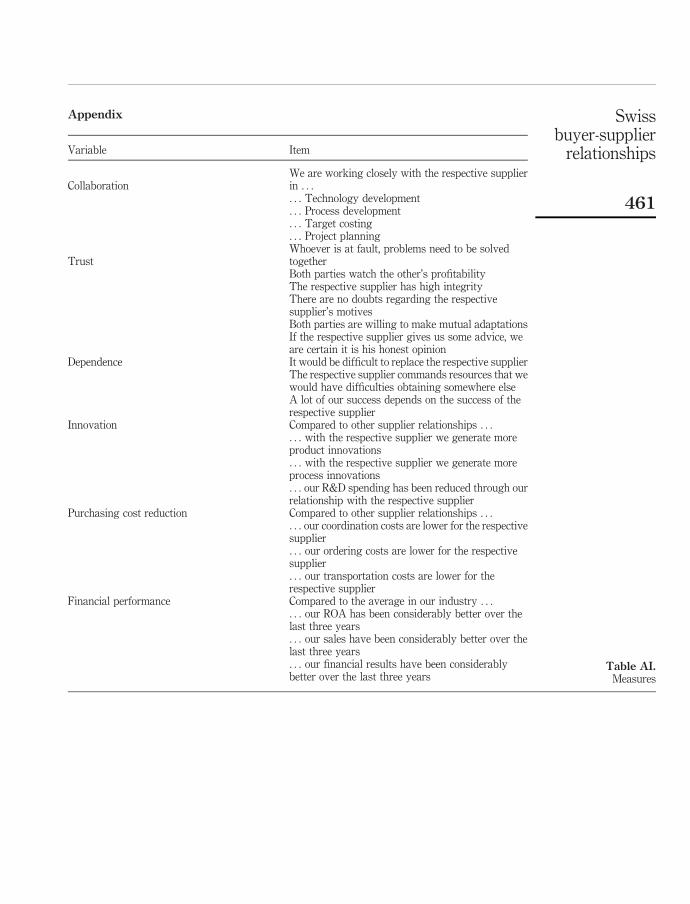

Appendix

Variable Item

CollaborationWe are working closely with the respective supplierin . . .. . . Technology development. . . Process development. . . Target costing. . . Project planning

TrustWhoever is at fault, problems need to be solvedtogetherBoth parties watch the other’s profitabilityThe respective supplier has high integrityThere are no doubts regarding the respectivesupplier’s motivesBoth parties are willing to make mutual adaptationsIf the respective supplier gives us some advice, weare certain it is his honest opinion

Dependence It would be difficult to replace the respective supplierThe respective supplier commands resources that wewould have difficulties obtaining somewhere elseA lot of our success depends on the success of therespective supplier

Innovation Compared to other supplier relationships . . .. . . with the respective supplier we generate moreproduct innovations. . . with the respective supplier we generate moreprocess innovations. . . our R&D spending has been reduced through ourrelationship with the respective supplier

Purchasing cost reduction Compared to other supplier relationships . . .. . . our coordination costs are lower for the respectivesupplier. . . our ordering costs are lower for the respectivesupplier. . . our transportation costs are lower for therespective supplier

Financial performance Compared to the average in our industry . . .. . . our ROA has been considerably better over thelast three years. . . our sales have been considerably better over thelast three years. . . our financial results have been considerablybetter over the last three years

Table AI.Measures

Swissbuyer-supplier

relationships

461