Embed Size (px)

DESCRIPTION

Excellence in Leadership December 2012

Citation preview

Strate

gic p

erfo

rma

nce

ma

na

gem

en

tE

xce

llen

ce in

Le

ad

ersh

ipIS

SU

E 4

20

12

Issue 4 | 2012 | £12

the

S T R A T E G I CP E R f o R m A n C Em A n A G E m E n T

issue

How finance is driving effective performance management strategies

Paul Friston, director of group financial control at Marks & Spencer, on how finance

underpins the retailer’s performance

Anders Bouvin, general manager, Handelsbanken UK, on how his bank outperformed in the financial crisis

James Davenport, FD, Innocent Drinks, on how reward packages incentivise

performance

Alexander Maljers, downstream finance performance manager at Shell, on what

performance management means to the oil giant

talents and skills of an organisation’s rising stars (p52).When it comes to managing employee expectations,

Generation Y is reshaping the landscape. James Davenport, finance director at Innocent Drinks, Stephen Purse, FD at Adnams brewers, and George Riding, MENA CFO at business management software specialists SAP, discuss how flexible working, flat-rate bonuses and employee share schemes are helping to enhance staff performance (p54).

As part of CIMA’s celebrations to mark the 20th anniversary of the Balanced Scorecard, the institute launched four new reports, each of which looks at integrating performance management from a different perspective. These range from: employee empowerment in shared service centres; risk management in the intermediary food chain business; the adoption of economic value-added (EVA) in Chinese state-owned enterprises; and improving risk reporting to the board of directors. Each report provides

insights into how organisations are pushing performance management in new directions (p24).

CIMA is strongly aware that tomorrow’s talent is high on the business agenda. With this in mind, the institute recently held a roundtable in conjunction with financial

recruitment experts, Hays, to find out how firms are planning their talent management strategy in light of changing organisational requirements. The clear message is that management accountants are becoming even more integral to the decision-making process in leading companies (p46).

I very much hope that this issue of Excellence in Leadership will be a useful reminder of the importance of fine-tuning the motor of business and, in particular, the value drivers. As Professor Kaplan recently pointed out in his inimitable way, “There ain’t no fixed costs – just inattentive managers.”

At CIMA’s recent celebration to mark the 20th anniversary of the Balanced Scorecard, one of the scorecard’s creators, Professor Bob Kaplan, joked that he wanted the words: “We can’t manage what we don’t measure,” written on his tombstone. In this particular instance, the professor was

discussing ways to improve performance management in public healthcare, but this phrase should be etched at the forefront of every business leader’s mind, whether they are in the public or private sector.

Today, the Balanced Scorecard’s popularity is global. Indeed, it was selected by the editors of the Harvard Business Review as one of the most influential management ideas of the past 75 years. But, of course, there are many devices in the modern business toolbox. In this issue, we ask leading business figures to highlight some of the key performance management challenges they are facing and what tools they are using to overcome them.

Performance management means different things to different organisations. For Alexander Maljers, downstream finance performance manager at Shell, the focus is on ensuring that the petroleum giant achieves end-to-end value optimisation across its operations (p28). Meanwhile, Anders Bouvin, general manager at Handelsbanken UK, reveals how a commitment to customer-focused values has helped the bank to avoid the shockwaves of the global downturn while Rani Awad, CEO of Atlantic FuelEx, illustrates how deft performance management footwork is needed to avoid turbulence in the aviation fuel supply business (p8).

Speaking from the cutting edge of business, Paul Friston, director of group financial control at Marks & Spencer, details how his team is working on a ground-breaking integrated reporting pilot that he believes will make the company’s Plan A strategy for sustainability even more effective (p14). Like many other successful firms, Marks & Spencer has found that part of Plan A’s success is ensuring buy-in from staff.

On a similar theme, Phil Sheridan, managing director of financial recruitment firm Robert Half UK, explains how a performance management strategy that is transparent and tightly linked to the overall goals can help to develop the

Charles Tilley,chief executive, CIMA

foREWoRD

Performance management

‘When it comes to managing employee

expectations, Generation Y is reshaping the landscape’

Excellence in Leadership is the official publication of CIMAplus. For more information visit: www.cimaglobal.com/cimaplus

Cov

er i

mag

e: A

ctio

n Im

ages

. Th

is p

age:

Illu

stra

tion

: Mas

ao Y

amaz

aki/

Du

tch

Un

cle

Excellence in Leadership | Issue 4, 20123

Editorial advisory boardMalinga Arsakularatnechief financial officer, Hemas Holdings

David Blackwoodgroup finance director, Yule Catto & Co

George Ridingchief financial officer, Middle East and north Africa, SAP

Arul Sivagananathanmanaging director, Hayleys BSI

Bogi Nils Bogasonchief financial officer, Icelandair Group

Kai Peterschief executive, Ashridge Business School

Jeff van der Eemschief financial officer, United Biscuits

Jennice Zhufinance director, Unilever China

ConTEnTS

3 Foreword

6 Vital statistics 8 Performance strategies Anders Bouvin, general manager, Handelsbanken UK; Rani Awad, CEO, Atlantic FuelEx; and Dr Kristina Potocnik from the University of Edinburgh Business School, on what performance management means to them

14 Finance makes a mark Marks & Spencer director of group financial control, Paul Friston, FCMA, CGMA, on how finance is driving performance at the retailer

20 Know your customer Author and performance management guru Gary Cokins offers businesses guidance on

On the right KPI road?How to avoid KPIs that damage other parts of the business p38

Getting global How multinational Shell handles global performance management p28

Paying the priceHow salary fits into companies’ reward structures p54

how to better understand their customers

24 Modern performance To mark the 20th anniversary of the Balanced Scorecard, CIMA commissioned four reports into modern-day performance management. We profile the findings

28 A global view Alexander Maljers, downstream finance performance manager at Shell, explains how to obtain a view of performance in a multinational corporation

32 Investing in the future How Hewlett-Packard is partnering with CIMA to create a learning culture at its shared service centres that will reap benefits for years to come

36 Independent partners Independence in business partnering has been the subject of a series of recent CIMA roundtable events. Tanya Barman, CIMA’s head of ethics, provides an update on the dicusssions

38 Best laid plans... Key performance indicators can help an organisation to drive up performance. But it’s important to consider their impact across the whole business

41 Get involved with CIMA

42 Right tools for the job Leading finance chiefs on good performance management

46 Tomorrow’s talent With finance playing an

increasingly important role across organisations, a recent roundtable in partnership with Hays addressed the issue

52 Measure for success Robert Half UK’s Phil Sheridan on creating a motivated workforce through performance management

54 Paying the wayHow salaries fit into today’s reward programmes

60 From CFO to NED Peter Williams, NED of Cineworld Group and Silverstone Holdings, on what CFOs bring to the role of non-executive director

66 CIMA directory

65 Next issue

Excellence in Leadership | Issue 4, 20125

Excellence in Leadership | Issue 4, 2012

CIMA is the Chartered Institute of Management Accountants 26 Chapter Street, London SW1P 4NP 020 7663 5441 www.cimaglobal.com

CIMA contact: CPD manager, CIMA Claire MortonEmail: claire.morton @cimaglobal.com

Excellence in Leadership is published for CIMA by Seven, 3-7 Herbal Hill, London EC1R 5EJ. Tel: 020 7775 7775.

Group editor Jon WatkinsGroup art director Simon CampbellJunior designer Josh FarleySenior sub editorsGraeme AllenDarren BarrettDeputy chief subChristina Ryder Chief sub editor Steve McCubbinPicture editor Louise Fenerci Picture researcher Alex Ridley Editorial director Peter Dean Managing directorJessica Gibson Creative director Michael Booth Production manager Mike Doukanaris Group publishing director Rachael StilwellCommercial account developmentHilton YoungAdvertising manager Andrew WalkerEmail: [email protected]: 020 7775 5717

Chief executive Sean King Chairman Tim Trotter

© Seven © CIMA

Cover imageAction Images

The contents of this publication are subject to worldwide copyright protection and reproduction in whole or in part, whether mechanical or electronic, is expressly forbidden without the prior written consent of CIMA/Seven. All rights reserved.

Origination by Rhapsody.Printed in the UK by Wyndeham Press Group.

The products and services advertised in Excellence in Leadership are not necessarily endorsed by or connected in any way with CIMA. The editorial opinions expressed in the publication are those of the individual authors and not necessarily those of CIMA or Seven. While every effort has been made to ensure the accuracy of the information in this publication, neither Seven nor CIMA accepts responsibility for errors or omissions.

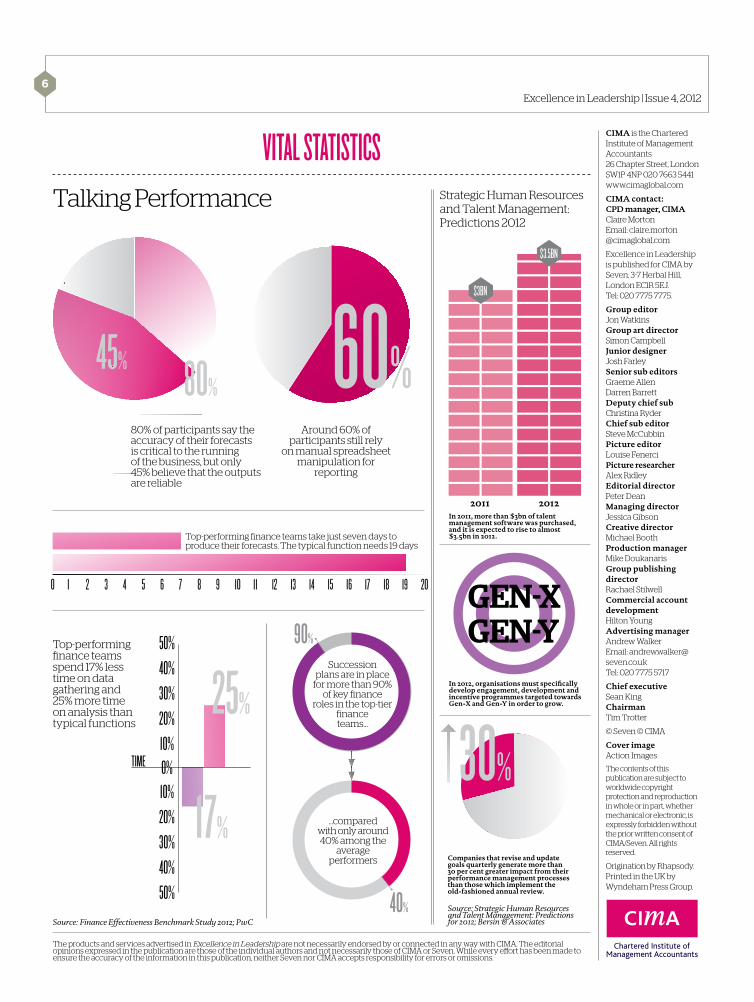

VITAL STATISTICSTalking Performance

Source: Finance Effectiveness Benchmark Study 2012; PwC

6

2011

$3.5BN

$3BN

2012In 2011, more than $3bn of talent management software was purchased, and it is expected to rise to almost $3.5bn in 2012.

Strategic Human Resources and Talent Management: Predictions 2012

Source: Strategic Human Resources and Talent Management: Predictions for 2012; Bersin & Associates

Companies that revise and update goals quarterly generate more than 30 per cent greater impact from their performance management processes than those which implement the old-fashioned annual review.

GEN-XGEN-Y

In 2012, organisations must specifically develop engagement, development and incentive programmes targeted towards Gen-X and Gen-Y in order to grow.

30%

Top-performing finance teams take just seven days to produce their forecasts. The typical function needs 19 days

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 200

60%Around 60% of

participants still rely on manual spreadsheet

manipulation for reporting

Top-performing finance teams spend 17% less time on data gathering and 25% more time on analysis than typical functions

25%

17%

0%10%20%30%

TIME

40%50%

50%40%30%20%10%

Succession plans are in place

for more than 90% of key finance

roles in the top-tier finance teams…

…compared with only around 40% among the

average performers

90%

40%

45% 80%

80% of participants say the accuracy of their forecasts is critical to the running of the business, but only 45% believe that the outputs are reliable

8

Contextis everything

Performance management means different things to different organisations. Anthony Harrington

asked Anders Bouvin, general manager, Handelsbanken UK; Rani Awad, CEO, Atlantic FuelEx;

and Dr Kristina Potocnik from the University of Edinburgh Business School, about their performance

management strategies and what it means to them

Excellence in Leadership | Issue 4, 20129

Theories of performance management come in many guises. Ultimately, it’s all about finding the most appropriate and best available metrics to steer a particular ship through its own patch of ocean. Ideally, those metrics should also be broad enough – to stay with this marine analogy – to allow the officers to keep a weather eye out for any relevant dynamic that might radically impact the vessel’s passage – a passing hurricane, for instance. The following two case studies show just how much the context in which a company is operating, and the way it perceives and defines its strategic mission and the nature of its markets, sets the framework for what

constitutes an appropriate set of performance management metrics. The Swedish Handelsbanken Group was recently rated by Bloomberg as the tenth safest bank

in the world, and the safest in Europe. It quietly and unspectacularly avoided all the elephant traps that so many of the developed world’s banks stumbled into in their mad dash for profits in the run-up to the 2008 global financial crash, and the durability of its business model is – or should be – the envy of its competitors. Atlantic FuelEx, founded by the entrepreneur Rani Awad, has taken just 14 months to be well on the way to being a global player in one of the most competitive markets on earth, as a worldwide provider of aviation fuel services. What makes this market so difficult, as Awad notes, is the simple fact that “fuel is fuel”, and though the volumes are huge, the margins are tiny. This means that success has to be based on more than price. Value add and risk control are the keys to Awad’s business and shape everything that the company does.

Interestingly, what both fuel services and banking have in common is a low mark-up on credit, which means that one large loss caused by one big client going belly up creates a huge hole that can only be plugged by a daunting volume of ordinary business. This makes risk management absolutely vital for both bankers and jet fuel providers and creates a surprising commonality of purpose. Awad has to look to continuously add value in order to grow his business and make his offering more attractive than that of his competitors. But adding value, in the sense of being ready to meet the needs of clients across everything from personal and business banking, is exactly what banking is all about, too. »

Excellence in Leadership | Issue 4, 201210

Bouvin has been with Handelsbanken since 1985 and served as its head of Northern Great Britain and head of Denmark Regional Bank.

Anders BouvinGeneral manager, Handelsbanken UK

What was it that allowed Handelsbanken to sidestep the disasters of the 2007/2008 financial crash? How did the bank manage its way through that crisis and what were the key metrics that management was concerned with during this period?Our philosophy has always been to avoid what you might call “opportunity banking” and to stay focused on one simple principle, which is to keep the customer relationship at the heart of everything we do. It is customary in banking for all banks to claim that they are focused on the client relationship, but there is a world of difference between saying this and doing it. For example, the entire bonus culture, in our view, is inimical to a model that puts the customer at the heart of the relationship.

If you’re going to reward a manager for meeting a target, then he or she is going to try to meet that target, whether or not it accords with what customers really need and want. You are setting up a tension between what the manager wants, namely a larger bonus, and what the customer wants, which is excellent service. To bring it down to performance management, if you set targets for anything, be it a branch personal loan portfolio, business loan portfolio, or expanding your mortgage book by a certain percentage, or whatever, then people will work to achieve

those targets. If you then reward on the basis of those targets, which is what bonuses are all about, you strongly reinforce the behaviours that will allow management to achieve against those targets. What has this got to do with relationship banking? Not a lot, in our opinion. In fact, it’s easy to see that it actually works against relationship banking. This is why Handelsbanken doesn’t pay bonuses and doesn’t have a bonus culture.

For the same reason, we do not have performance targets that seek to increase this or that specific facet of our portfolio of services to customers. None of those metrics work for us because they are not about nurturing the client/bank relationship. What this meant, in the boom years in the run-up to 2007/2008, was that we looked very staid, and might have seemed to outside commentators to be missing a number of tricks when our competitors were outperforming us by buying large amounts of mortgage-backed securities, which at the time seemed to pay handsome returns, or when our competitors increased their sovereign debt portfolios with massive lending to Portugal, Greece and other peripheral eurozone countries.

We did not join this dash to exploit new opportunities in banking. We stayed focused on our own business model and on our own key metrics, namely building our banking model around the customer. This approach did not change through this whole period and remains the same today.

How do you support your customer relations focus with metrics? What enables you to manage on this basis?The basic philosophy is that if you leave it to branch managers, they are best placed to know who the best customers are in their area. They will develop the long-term relationships with customers, and by focusing on what the customer needs they will, over time, grow their book steadily. So the metric that is most important to us is the branch cost to income ratio. We measure this regularly and have a totally transparent league table. Every branch can see where they are on the cost/income ratio table, relative to all the other branches. There is a clear incentive to move up if your branch is quite far down the league table, and to retain and improve your position if your branch is well placed. As you can see, this is a completely neutral metric as far as prioritising particular products is concerned. By stimulating competition among the branches and giving branch management a free hand to develop client relationships for the long term, branch performance improves over time. This enables us to meet our overall objective, which is to outperform the competition on the key financial metric that really matters to us, namely return on equity. We outperform our competitors on return on equity by being more efficient and having lower costs. This is not about underpaying staff. To attract the best people in banking you have to pay an attractive reward package, but then you get superior returns by retaining »

AnDERS BouVIn

12

customers for the long term by providing them with what they want, not by selling them products they don’t need. We are also very selective in our customer acquisition. We only take on customers that the branch manager feels that he or she can develop a long-term relationship with. We are not about acquiring rapid market share. This simple set of metrics has worked for us for 40 years. We have lower non-performing loans and better return on equity, and lower cost income ratios than the competition, and have had for decades. This model works through all business cycles, through the downturn as well as the boom times.

Other banks tend to fall into the trap of endlessly rethinking and restructuring their business models. We have had the same, consistent model for 40 years, since we moved to it in the 1970s. Before that we had tons of goals. There were so many targets and goals set by head office that everyone found a different subset of goals that suited them and there was no consistency. So we did away with all that and stuck with one overriding goal, return on equity relative to our peers, and at branch level this translates down to the cost income ratio. With that as our yardstick and with a complete focus on developing long-term customer relations, we achieve steady, organic growth year in and year out.

How important was scale to you as a metric when you launched Atlantic FuelEx from your base in Dubai in July 2011?It was a very crucial metric for us. To be a global player in this business you have to have a wide network of relationships with airline carriers and general aviation clients, as well as with both incumbent services and fixed-base operators at airports in a number of countries. If you are dealing with a big jet fuels supplier, your importance to them is directly related to the size of the fuel orders you are placing with them and the quality of the clients they are delivering to from a creditworthiness standpoint. This has a very significant influence on the margin you can get from them. Margins in this industry are very thin and we deal in large quantities of fuel to generate profit. So getting to a sustainable scale that would enable us to maintain our growth was vital.

However, it was just as important, if not more so, for us to carry out very thorough due diligence checking on our potential customers and to monitor their economic health very closely.

So credit management is a fundamental and critical part of this business and is just as important as being excellent on the logistics front. If you say there are going to be fuel trucks on the ground at a particular airport at a particular time, and waiting for a particular flight, that fuel had better be there! Operational efficiency is another dimension that you live or die by in this business.

One of the maxims in the jet fuels business is that “fuel is fuel”, meaning that fuel companies such as yours are supplying direct from the major suppliers, such as Exxon or Total, to a range of incumbent services and fixed-base operators, as well as to carriers. Scale is not enough to differentiate your business, is it?No. Another critical metric for us is value add, and it is something that we strive to make a fundamental part of our proposition to all our clients. This has

Rani AwadCEO, Atlantic FuelEx

Awad was previously the fuel sales manager for Jetex Flight Support for five years before he set up Atlantic FuelEx.

RAnI AWAD

Excellence in Leadership | Issue 4, 2012

Excellence in Leadership | Issue 4, 201213

How solid or deep is the current state of performance management theory?To date, the theory is very pragmatic and, one has to say, very shallowly rooted in theoretical concepts. Any theory needs a definition of its terms, and the definition that we use is that performance management is all about a group of behaviours that contribute to the effectiveness of others in the work group.

That would seem to be a very group-oriented definition. How does it help at the company level where an organisation is looking to enhance the performance of its strategic mission?There are basically three approaches to performance management. At the corporate level, the definition that is most often used is results-based performance. This emphasises outcomes, financial outcomes generally, but also “softer” outcomes, such as developing client

relationships that then go on to deliver financial performance.

Another measure is the behaviours approach that I began outlining, and the third approach is based on traits. It asks what character traits an employee has to have to be successful in this organisation, or more specifically, in this role? What would lead us to expect an enhanced performance from someone in this role? Here you are looking at enduring traits, such as conscientiousness and intelligence. If someone is conscientious and intelligent today, they are likely to be so tomorrow, and a year from today and so on.

The second approach, the behaviours approach, is what you want to work with when it is not absolutely clear how your expectations on the results approach are going to be achieved. You are then looking not just at financial outcomes, but at the specific behaviours that are needed to get to those numbers, at how the work is done.

both a direct economic benefit and a huge knock-on benefit which, in the

end, shows up as better margins from our major fuel suppliers. For example, to win a good-quality carrier client I will want to bring to their attention the fact that while they have two or three options on fuel supply in, say Qatar and the Middle East, they have no good coverage in Sudan or West Africa, where I can help them. So the fact that we extended our operations to Africa at an early stage is very important to us. That goes to the scale issue, but it also goes to improving my proposition to the carrier, since I can do them a bundled deal for their Middle East and Africa business and provide them with comprehensive billing, reporting and fuel usage statistics. But at the same time, winning the carrier’s business improves my standing with the major fuel suppliers. The same thing works with the direct suppliers. Exxon has a range of options in terms of suppliers it can go through to reach Middle East clients, but it is not strong in Africa. So I can give them an added presence there and that can bring me some or all of their Middle East business since we can, again, do a bundled deal. So in this business you always have to look at ways of leveraging value add, while keeping a very close eye on your credit lines and

the general health of your debtors. Value add is not a “metric” so much as it is a philosophy and a shaping approach to business.

Another example is the way we facilitate the use of supplier fuel card schemes across Africa. If you hold a fuel card as a pilot at London Heathrow, you will have no problems getting the job done. But at many African bases, and at numerous other places around the world, fuel sales are done on a strictly cash

basis. We are working very hard with fixed-base operators and incumbent fuel services companies to get them to accept cards from our major fuel partners. We are also looking to get the cards accepted on military bases. That is a strong positive from the point of view of our suppliers, but it also helps the clients since it makes it much easier for pilots to pay. Value add, scale and cash flow, coupled with excellent logistics, is what makes our business tick.

Dr Kristina PotocnikLecturer in the Organisation Studies Group at the University of Edinburgh Business School

The theory of performance management

Gal

lery

Sto

ck, G

etty

Imag

es

14Excellence in Leadership | Issue 1, 2012

14

xxxx

xxxx

xxxx

Excellence in Leadership | Issue 4, 2012

Can accountants save the world?

THE In-DEPTH InTERVIEW

15

Paul Friston, FCMA, CGMA, director of group financial control at Marks & Spencer, on how finance is driving performance at the leading global retailer

The idea that finance holds the key to issues we face today has been gaining currency. Peter Bakker, president of the World Business Council for Sustainable Development, raised it at the 2012 Rio+20 conference on sustainable development and at a Marks & Spencer conference on integrated reporting this year. At the latter, Bakker made every accountant in the room stand up and told them that they can make a difference by making sustainability more measurable and tangible through integrated reporting.

The message clearly resonates with Paul Friston. He has been closely involved with Marks & Spencer’s well-regarded Plan A for sustainability since it was launched in 2007 – especially since he took over as group financial controller in 2011 – and is now working on an integrated reporting pilot that he believes could help make Plan A even more successful.

“Now I have a really diverse team, from commercial decision support through to technical accounting, with about 350 people across the world,” he says. “With the expected growth in »

middle classes around the world, retail consumption will [increase rapidly]. As a large international retailer, we need to account for this and consider how we impact the planet, because resources are finite. There is both an environmental and a commercial rationale.”

When Plan A was launched it made 100 social and environmental commitments to deliver by March 2012. In 2010, M&S updated the plan and added 80 more commitments. It has been widely hailed as a success, both within the company and by commentators in the worlds of both business and social responsibility. The vast majority of Plan A targets have been met or are “on plan”, while only six have been abandoned. And the next phase of the plan has been launched with a range of three- year targets.

ClIMaTE ChaNgE Is IMporTaNTFriston says that while targets around the reduction of energy and waste have an obvious practical impact, other less tangible targets, such as those based on climate change, are equally important.

“We are already seeing the impact of climate change in important areas such as costs and continuity of supply,” he says. “To raise awareness about that and to influence it is important. Because we are ‘own label’, we cover all aspects of the business. The commitments are wide-ranging, so different parts appeal to different areas of the organisation. [Plan A targets on] ethical sourcing, for example, have a big impact on customer interaction.

“We also measure how Plan A resonates with staff – over the five-year period it has become more important to them as they are becoming more socially and

environmentally aware. On the customer side, we have always been clear that they don’t want to pay for something that is ethical or environmentally friendly, so the challenge has been how you can promote the benefits without passing on any additional cost.”

Crucially for finance, the business case for Plan A has grown over the past three years.

Friston says: “My current role has revolved around how to bring the business case for Plan A to life. Within my team is the head of FP&A Suzanne Foley – she sits on the Plan A committee and the Plan A innovation fund [which supports new business ideas]. That is really helping the business to capture and realise the benefits, and get the best return on investments.

“Plan A went from costing us money in year one, to profit neutral in year two. Now, in year five – whether on cost avoidance or true enhancements to profit – it is adding about £105m of profit. Commodity and energy prices have gone up in those five years and so, by limiting our consumption, Plan A has played a bigger part.”

This year, M&S also published the document “The key lessons from the Plan A business case”. “That is to help other organisations and finance professionals think about how we have gone about measuring Plan A,” says Friston. “We want to help others to see that there is a financial benefit, and to upskill so that they can do the same.”

sUCCEss IN sUsTaINaBIlITYFriston says that Plan A has been a huge challenge, but has been more successful than the company could have imagined back in 2007. “That success is a unique selling point and a huge benefit in attracting finance people, who are generally much

more socially aware than they were even five years ago. We didn’t necessarily know how we were going to get there, so it has taken a lot of faith and changing mindsets, but having ambitious and stretching goals has helped us to find solutions.”

“The biggest challenge initially was that not everyone understood the part they had to play,” says Friston. “We had a central team that formulated the ideas and we found very early on that we needed much more ownership, both commercially and financially. So we devolved many of the budgets and expectations to the different areas of the business to try to foster accountability.

“A few Plan A commitments were not achieved, because the landscape is changing. For example, we wanted to double the amount of organic food that we sold. [But because of the economic downturn] demand actually declined.

“The key to success has therefore been to have something that is simple and can be cascaded easily through the organisation – so everyone knows what you are trying to achieve and the part they can play. It also has to be something ambitious, and that you keep coming back to. There will be times when we have to realign how we get there.

“Now that it is so embedded in the culture, everyone is playing their part. That was the biggest cultural shift. We have made sure we had the right KPIs in place, and everyone in the organisation has Plan A as one of their objectives. Senior management have it linked clearly to their bonus targets, so it helps us culturally to make sure that this isn’t just a hobby.

“Also, we now have a clear business case, so there is much more of an appetite, not only from social responsibility but also

THE In-DEPTH InTERVIEW

17

»

from a financial point of view, to keep driving Plan A. We have moved away from seeing it as just about efficiency with our cost base and are starting to see the commercial opportunities. The obvious efficiency was around reducing energy consumption, but we are now finding ways – for example, through eco-products such as our carbon-neutral bra – that get a response from customers and allow us to sell more.”

Plan A has helped M&S win several awards recently, including the CIMA Finance Team of the Year 2011. “We don’t benchmark ourselves against competitors, but the awards are recognition of what we have done,” says Friston. “We make sure we have the right talent within the group, spend a lot of time developing those people, and have used Plan A as a way to motivate and galvanise the team.”

Plan A is now expected to become even more commercial. “We expected to generate profit this year, but it was way ahead of our expectations in 2007,” says Friston. “Now we want to build on that and we have built it more formally into our planning process. Every budget holder will know what the expectation is.

“Monitoring it regularly means you can stop activities that aren’t working and accelerate the ones that are. That has really helped us to drive new thinking, so when it gets to something that you can roll out we would build that into their plans, with any investment required and any benefits we are looking to realise.”

Of course, good sustainability strategy does not always guarantee profits. Though it has performed well over the past few years, Marks & Spencer net profits dipped in the financial year ending in 2012.

Friston says: “Our underlying profits last year were flat against the backdrop of a more challenging UK market. But in terms of our long-term strategy, Plan A helped generate an extra £105m last year, so it is definitely helping towards our results rather than distracting from our core operation.”

“We have a very large CIMA population within the finance group,” says Friston. “Their skills help to bring the technical elements of accounting together with the commercial side. We are a very commercial business and we want people in finance that help drive that.

“We have added value around the Plan A business case and there are a number of key things that I have helped to bring with my CIMA experience, such as what costs should be included. For example, you know what is a sunk cost compared to a cost that would be a true consequence of Plan A.”

Having a robust baseline is crucial, he says. “It is about knowing where you are measuring from and to, and measuring investment by having the right hurdle rates in place. Plan A hasn’t had softer hurdle rates, we have treated it like any other business initiative and looked for the same return on investment – which is generally 12-15 per cent. We also look at whole life-cycle costing, trying to move away from measuring just the initial outlay.”

Bringing it back to Bakker’s point about integrated reporting, Friston says: “Lastly, we feed all that into an integrated reporting approach. We are part of a pilot on how to bring our Plan A report and our annual report and accounts together in an integrated view of how we are driving

value through to shareholders, both socially and financially.

“We want to be at the forefront of that and help with thought leadership. We are already well advanced with our two reports and want to help our stakeholders and shareholders understand how to use the information from both.”

“Integrated reporting will help because everything that gets measured gets managed. Rewarding someone for delivery against something gives it focus. If stakeholders and shareholders see all the information together, they will start holding the board to account,” says Friston.

Another aspect that has helped cascade the message about Plan A to departments is the fact that many CIMA members working in M&S are in embedded teams around the organisation. “They are able to work closely with the business to drive this agenda – it is not just the central finance team,” says Friston. “We have a very active business-partnering finance function that touches the whole organisation. They have become an effective and influential group. The commercial areas, for example, would rather have more people supporting them than less, which is a good sign that the business partners are adding value.”

Friston’s ambition does not stop there, though. He adds that: “The next stage of Plan A will involve embedding it further in how we do things. We have an ambition to be the world’s most sustainable retailer by 2015. After that the benchmark will just keep rising.”

Excellence in Leadership | Issue 4, 2012

THE In-DEPTH InTERVIEW

19

Friston left City University with an MA in property valuation and law and joined Marks & Spencer on the finance graduate programme in 1996. In 2009, he became director of M&S Pension Trust Ltd and in 2011 was appointed director of group financial control for M&S.

PAuL fRISTon

Jam

es P

faff

14Excellence in Leadership | Issue 1, 2012

Optimising customer profitability and value

20

Gal

lery

Sto

ck

»

Excellence in Leadership | Issue 4, 201221

Author and performance management guru Gary Cokins profiles the pressures on businesses to better understand their customers and, if they do, the

performance improvements that can be achieved…

Much of a company’s marketing budget is typically based on faith that its spending will somehow grow the business. There is an old, rumoured quote from a company president stating: “I am certain that half the money I am spending on advertising is wasted. The trouble is, I don’t know which half.” This expresses a concern and applies

to many marketing programmes, in addition to general advertising. Marketing spends money in certain areas and the company hopes for a financial return. Senior management has had unquestioned views that marketing and advertising is something that you must spend money on – but how much money? How much is too much? Where are the highest returns and what should you avoid? Which customers should you target? And which not?

Business is no longer just about increasing sales. It’s about increasing the profitability from sales. It’s not enough to simply measure gross margin profitability for sales of products and standard service lines. Companies should instead start to identify the differences in the cost-to-serve between different types of customers (called the fully loaded costs of serving a customer). Activity-based costing (ABC) is required to measure these costs for products, services, channels and customers. This effort will help them get a full picture of where their businesses are making or losing money. Superior companies provide a differentiated customer experience to different types of customers in order to drive loyalty and gain a competitive advantage.

The budget expenditures for the marketing and sales functions should be subject to the same intense examination of the chief operating officer (COO) and chief financial officer (CFO) as any other spending programme. Many marketing functions rely on imperfect metrics, anecdotes and history that may have been a result of unusual occurrences that are unlikely to be repeated. How marketing spends money is critical, but it should be treated as a scarce resource to be aimed at generating the highest long-term profits. This means the need for answering questions such as: “Which type of customer is attractive to newly acquire, retain, grow or win back? And which types are not? How much should we optimally spend on attracting, retaining, growing or recovering the types of customers we want?”

Excellence in Leadership | Issue 4, 201223

GARy CoKInSCokins is an internationally recognised expert, speaker and author in advanced cost management and performance improvement systems and holds an MBA from Northwestern University’s Kellogg School of Management. He began his management consulting career with Deloitte Consulting before moving to KPMG, where he was trained on activity-based costing by Harvard Business School professors Robert S Kaplan and Robin Cooper. From 1997 until recently, he was in business development with SAS, a leading provider of enterprise performance management and business analytics and intelligence software.

1 Customer retention

It is generally more expensive to acquire a new customer than it is to retain an existing one – and satisfied existing customers are not only likely to buy more but also “spread the word” to others, such as a referral service. Existing customers are free. They have already been acquired.

2 A shift in the source for competitive advantage In the past, companies focused on building products and selling them to every potential prospect. But many products or service lines are one-size-fits-all and have become commodity-like. Consequently, as products and service lines become commodities, where competitors offer comparable ones, then the importance of customer service rises. There is an unarguable shift from product-driven differentiation towards service-based differentiation. That is, as differentiation from product advantages is reduced or neutralised, the customer relationship grows in importance. This trend has given rise to many marketing organisations focusing on segment, service and channel programmes, as opposed to traditional, product-focused initiatives.

3 One-to-one marketing Technology is being hailed as an enabler to: (1) identify customer segments, and (2) tailor marketing offers and service propositions to individual customers (or segments). There is now a shift from mass marketing products a seller believes it can sell to a much better understanding of each customer’s unique preferences and what they can afford.

4 Expanded product diversity, variation and customisation As product and service lines proliferate, such as new colours or sizes, it results in complexity. As a result, more indirect expenses (i.e. overhead costs) are needed to manage the complexity; therefore indirect expenses are increasing at a relatively faster rate than direct expenses. With indirect expenses growing as a component of an organisation’s expense structure, the managerial

accounting practices typically require enhancing. Activity-based costing provides this enhancement.

5 Power shift to customers The internet is shifting power – irreversibly – from sellers to buyers. This is a one-time event happening in our lifetime. Thanks to the internet, consumers and purchasing agents can explore more shopping options more efficiently and quickly compare prices among dozens of suppliers. They can also more easily and quickly educate themselves. This shift in power from sellers to buyers is placing relentless pressure on suppliers. Supplier shakeouts and consolidations are constant.

The combination and convergence of these pressures and additional customer satisfaction and loyalty pressures mean that suppliers must pay much more attention to their customers. This means providing more and better products and services to one’s existing customer base, as well as carefully targeting future customers.

Earning, not just buying, customer loyalty is now mandatory. There is an unchallenged belief that focusing solely on increasing sales dollars will eventually lead companies to reduced profitability. What matters is a mind-shift from pursuing increased sales volume at any cost to pursuing profitable sales volume – smart sales growth. If each customer’s value is not known, then you are more likely to be misallocating resources by under-serving the more valuable customers, and vice versa.

ThE CFo shoUld sErvE ThE CMo aNd ThE salEs dIrECTorThe CFO can and should work more closely with the chief marketing officer (CMO) and sales directors to measure and report the non-financial, Balanced Scorecard key performance indicators that impact or reflect customers’ total experience and satisfaction. Progressive CFOs understand how customer experience drivers achieve strategic objectives and indirectly influence financial results.

Ultimately, managerial accounting measures, which are typically product-based and retrospective, should extend to become forward-looking, value- based measures. Evaluating customers requires calculating prospective metrics that, when acted on intelligently, truly convert to bottom-line earnings and shareholder wealth.

The day is coming that the CFO function must now turn its attention from operations and cost control to support the CMO and sales director. The objective is to develop and monitor strategies that will assist cost planning and are customer-centric to grow the customer base, its loyalty, its revenue and the company’s brand.

The perfect storm is creating turbulence for sales and marketing management.

In the past ten years, five major forces have converged that place immense pressure on companies, particularly on business-to-consumer ones, to better understand their customers and what it costs to serve different types:

24

To mark the anniversary, scorecard creators Professor Robert Kaplan and Dr David Norton attended a series of events that saw the launch of a number of CIMA and CGMA reports on performance management. Here, we look at the key findings from those reports...

Performance management: 20 years after the Balanced Scorecard

Excellence in Leadership | Issue 4, 201225

»

This report looks at the consequences of applying performance management systems in the context of shared service centres.

Performance management frameworks tend to begin with strategy. They then rely on measures to drive organisational performance by communicating goals through a top-down process. This begins at executive director level. The Balanced Scorecard model suggests that the route to organisational performance lies in appropriate performance measures. This is because management is not possible without measurement. However, recent studies offer an alternative view. They suggest that performance management is about finding a variety of ways of working to encourage commitment and constructive behaviour. Performance measurement is a part of the story, but is not the whole story.

This research considers these two contrasting views. The focus is on shared service centres (SSCs), which are designed to encourage an entrepreneurial mind-set and new working practices. It found that in order to achieve excellent performance, SSCs are attempting to steer a course through a number of competing forces. One of the fundamental arguments for the creation of SSCs lies in their potential to standardise and streamline business processes, saving costs and potentially providing a better service. All of the case study organisations are engaging with management techniques such as Lean

and Six Sigma. In an economic environment characterised recently by volatility, and where advances in technology and management are taking place at an increasing rate, the research found that the need also arises for adaptability and flexibility to be built into business processes in order to facilitate rapid response.

In addition, highly competitive marketplaces have created the need for a continuous improvement of systems in order to keep pace with competitors.

The researchers did not encounter clear and neat alignment of performance measures from operations to strategy. Strategy was typically communicated from the top of the organisations, but it was not explicitly connected to performance measures. Hundreds of different performance measures can exist at an operational level, but few are routinely reported upwards. Instead, effective leadership in SSCs is largely about empowering employees and increasing the extent to which they identify with their organisation. This was analysed in terms of a Performance Management Mix, which combines “managing through people” with “managing by the numbers”.

The approach of “managing through people” has involved the SSCs in new ways of working. One CEO described his role as essentially about “winning the hearts and minds” of the SSC staff and making them feel empowered. Individuals within SSCs invest considerable time and effort in

frequent communications with their teams and with customers. A significant part of the process standardisation includes managing the customers’ expectations and negotiating their compliance with the new system.

Rather than finding a systematic cascade of strategy maps of increasing detail as they moved down the organisations, the researchers found in the SSCs complex web of relationships linking processes, SSC people, internal and external customers and wider social institutions. Instead of being translated into a series of detailed performance measures, strategy statements from the top of the organisation are translated in facilitating frameworks such as the Network Rail “4Cs” model, which looked at cash, cycle time reduction, compliance and customer service to drive continuous improvement. These models provide a frame of reference and a vocabulary within which employees can discuss performance.

However, the frameworks do not provide detailed guidance on the performance measures to be chosen. This choice is frequently made by team leaders and managers in negotiation with the individuals concerned. In this way, employees are empowered and motivated and the senior managers keep an overall check on the aggregate effect of the individual choices through monitoring and by engaging in a series of benchmarking programmes and peer-to-peer networking.

RElEvANCE REGAiNEd? PERfORmANCE mANAGEmENT iN ShAREd SERviCE CENTRES Professor Lin Fitzgerald, Dr Rhoda Brown, Rosamund Chester Buxton, Ian Herbert, Ruth King and Dr Laurie McAulay – Loughborough University

To download the report visit:http://tinyurl.com/a46rh8l

‘SSCs are attempting to steer a course through a number of competing forces’

Ala

my

Excellence in Leadership | Issue 4, 201226

This research sought to understand the extent to which performance measurement systems in food supply chains might be incomplete and inadequately balanced.

Intermediary food businesses operate in a highly competitive marketplace where demand is volatile and net margins are low (typically around 2% of turnover). The grower-packers and small manufacturers in this study face worries about survival and long-term profitability because of the high risks centred on: • Loss of customer through the

“promiscuous” chasing of lower prices, even when ability to supply exists.

• Refusal of product by customer. • Loss of reputation. • Loss of supply through weather, disease

or contamination.• Relative ease of substitution in the market

of both product and supplier.Unlike the bigger manufacturing firms,

these businesses rely on the quality of produce, products and customer service to achieve some competitive advantage.

Performance measures are used extensively within the intermediaries and cover internal processes; quality; customer profitability; delivery to customers; and staff

development and finance. In terms of negotiation with retailers, quality and delivery specifications are set by the retailer/caterer.

Financial and risk measures are rarely discussed, except price, where again negotiations centre on quality and delivery. With suppliers, intermediaries did develop relationships that involved wider discussions about risk and price, especially where they wanted to retain the services of the best growers. Asked what drove the strategic plans of the intermediary, one director replied: “Quality, integrity and provenance in the marketplace in the UK. We can’t afford to pay any more money than anyone else, but we need to attract the best 25 per cent of the growers.”

Key findings• The main risk in this research was commercial risk, which includes the risk of losing customers or suppliers at relatively short notice for reasons other than their own inability to supply or meet requirements. It appears that retailers want the assurance of quality and delivery that comes from long-term relationships, but at prices that come from competitive trading markets.

• Intermediary food companies play a crucial, pivotal role in attempting to align strategic and operational planning in the industry. In order to develop the relationships that make planning and negotiation more effective, and to ensure their own survival, they show best practice by delivering on time, in full, and to specification to the retailer, creating value, developing relationships with suppliers based on constant communication and business support, and by providing some protection for suppliers against commercial risk.

• Elements of the Balanced Scorecard approach were evident, even though no examples of full scorecards were presented, suggesting that the influence of the approach has extended beyond major multinationals. Performance measurement through the supply chain is based primarily on non-financial measures relating to quality, customer service and learning. Financial measures are used within the intermediary measures, but only price is discussed between supply chain partners, restricting the scope of negotiations and maintaining the monopsony in which a very small number of retail buyers are able to drive prices down.

PERfORmANCE mEASuREmENT ANd RiSk mANAGEmENT iN iNTERmEdiARY fOOd ChAiN BuSiNESSESProfessor Lisa Jack, Portsmouth Business School, UK; Associate professors Juan M. Ramon-Jeronimo and Raquel Florez-Lopez, Pablo Olavide University (Spain)

This project investigated the design and implementation of performance measurement systems (PMS) based on economic value added (EVA) in China’s state-owned enterprises (SOEs).

EVA implementation has been mainly studied in Western companies from the perspective of improving economic efficiency. This report took a different angle, however, looking at the motives of EVA adoption and the impact on the design and implementation in a major emerging

economy. The study found evidence that evolutionary change is achieved in Chinese state-owned enterprises by staged performance measurement system development, in which economic value added is introduced gradually.

It also revealed that this design is driven by the intertwined motives of legitimacy and efficiency, and has provided a mechanism to achieve a balance between maintaining stability and promoting changes in a company’s management practice.

Some changes were observed, including an improved awareness of the cost of capital, a greater willingness for investing in research and development, and an improved asset and operation efficiency.

The study also concluded that the extent of the impact was variable among the companies and is largely determined by the motives behind implementing EVA, and the level of management effort.

Imposed by the State-owned Assets Supervision and Administration

ECONOmiC vAluE-AddEd AdOPTiON iN ChiNA’S STATE-OwNEd ENTERPRiSES: A CASE Of EvOluTiONARY ChANGEDr Pingli Li, Middlesex University Business School, UK; and Professor Guliang Tang and Dr Narisa Dai, University of International Business and Economics, PRC

To download the report visit:http://tinyurl.com/av9fhoj

To download the report visit:http://tinyurl.com/bqqmn6b

Excellence in Leadership | Issue 4, 201227

Excellence in Leadership | Issue 4, 2012

Commission of the State Council (SASAC), a new EVA-based performance assessment policy has been introduced to the 129 Chinese SOEs under the direct administration of central government since 2010. Established by the State Council in 2003, SASAC at the national level handles the state’s ownership interests, as well as regulation and supervision of central SOEs. This EVA initiative was applauded by Erik Stern, the director of Stern Stewart and Co, as a change that “could end up having an impact on China that rivals that of Premier Deng’s 1978 reforms”.

Based on the concept of residual income (RI) and trademarked by Stern Stewart & Co in the 1980s, EVA is defined as adjusted operating income minus a capital charge. The academic research examining the use of RI has mainly compared the performance of firms having adopted RI to those that have not, but has produced mixed results.

One of the factors contributing to the

mixed results may be that distinguishing RI companies from others has been solely on the basis of RI use in forming compensation plans. From their field work in five Finnish companies, Malmi and Ikäheimo (2003) found that the use of value-based measures does not lead to management control mechanisms in their purest form. Similarly, McLaren’s (2005) CIMA-sponsored investigation into the use of EVA in three companies in New Zealand found that EVA has not entirely replaced traditional measures, so its use is not “all or nothing”. They argue that the different application may be due to different motives for adoption.

In the context of Chinese SOEs, the motive of introducing EVA could be regarded literally as pursuing economic efficiency, since the main objectives of EVA implementation are to increase returns on capital and strengthen risk control for the interests of state as shareholders, as claimed

by SASAC. However, SASAC and the sector of SOEs are under not just economic, but also social and political pressures for restructure and privatisation.

The criticisms on SASAC’s roles and SOE achievement have never abated. One recent example of these criticisms is the heated debates in 2012 on whether SOEs should be privatised, which was triggered by the World Bank’s report “China 2030”. Within this context, should there be other motives for SASAC to introduce the EVA initiative? How would those motives affect the design and implementation of the initiatives? What impact does the new system have on decision-making in the companies? Answers to these questions will have theoretical and practical implications.

Aiming to address the above research questions, the researchers investigated the design and implementation of EVA-based initiatives in China’s central SOEs by means of case studies.

Since the board of directors holds the ultimate responsibility for a company’s success or failure, board members should be adequately informed about the company’s performance and risks. That was the driver behind this CGMA research project into integrating risk into performance.

Surprisingly, the report states that there has been relatively little academic research on what information boards of directors actually receive in order to fulfil their strategic monitoring role. Furthermore, whereas performance-related reporting benefits from a long-standing research tradition in management accounting literature, relatively limited attention has been paid to its integration with risk – especially in relation to boards as receivers and users of that information.

This project responds to earlier calls for research that extends beyond the use of accounting information for decision-making by managers to examine how other actors interface with management accounting.

The main objectives of this research were to:

• Document and analyse how performance and risk are integrated in management reporting to the board of directors.

• Identify leading practices of enhancing performance management with risk to enable board members to perform their strategic monitoring role.

The case studies provide evidence of significant variation in companies’ risk reporting practices, both in terms of the content and the structural aspects of risk reporting. The researchers’ main findings were as follows: • They observed that boards generally seem

to be very aware of the importance of considering risks in their decisions and in their performance evaluations. Board members tend to perform their own implicit assessment of strategic risks when they discuss new strategic initiatives. Such board risk assessments are usually not formalised, but are part of the regular discussions on long-term strategy and potential uncertainties related to that strategy.

• With respect to integration of risk and

performance in strategic decision-making, the researchers found that it is common practice by management to identify and report risks to the board as a part of M&A proposals, business development plans, or strategic reviews. Such integrated reporting typically comes on top of the specialised reporting that focuses specifically on (operational) risks.

• Through the involvement of the internal auditor in risk management, the integration between risk and performance is also in the audit reports that go to the board of directors. On the board side it is the audit committee that is most frequently in charge of the risk management, which also adds to an integrated view on both risk and performance.

• In most companies the researchers observed that risks are viewed not only in a negative light (i.e. as a threat), but also from a positive perspective (i.e. as value-creating opportunities). The reporting on risks is thus closely intertwined with reporting on potential opportunities, in this sense providing a close integration between risk and performance.

iNTEGRATiNG RiSk iNTO PERfORmANCEProfessor Dr. ir. Regine Slagmulder, Vlerick Business School

To download the report visit:http://tinyurl.com/bm5ntx3

28

Gaining a global view of performance

What does performance management mean to a major global corporation, and how does it measure performance across its operations?

Alexander Maljers, downstream finance performance manager at Shell,

offers some insight…

Performance management means different things to different organisations. What does it look like within Shell?Performance management is as broad or as narrow as you want to make it. To take an extreme view, everything we do is done to manage performance. However, when I talk about it in terms of my role at Shell, performance management means that I focus on planning, measuring and appraising performance.

At Shell, we start by setting a strategy and determining where the business wants to go to in the long term – and what the strategic objectives are of the business. That is absolutely key in terms of performance management: always start with the strategy as it gives each business their long-term targets.

Based on our strategy, we make shorter term plans, and these translate into detailed operational targets, and measure our performance against those targets. These operational targets are aligned across the organisation: starting with sales targets and budgets at the lowest organisational level, rolling up to the overall targets for the whole of downstream. Targets are always consistent, but not necessarily focused on the same metrics. As an example, at downstream we focus on cash generation, but

for a sales manager we translate that cash target into targets for sales volumes, pricing and direct costs.

With reporting, it’s very important to have one consistent set of numbers across the business and it’s essential to make sure that businesses cannot tweak their own data.

What are the most challenging aspects of performance management?The most difficult part is driving accountability through the appraisal process. There are several dilemmas. Do you stick to backward-looking discussions or do you make them forward-looking?; do you focus on processes or restrict yourself to outcome KPIs?; how do you identify the most appropriate and effective KPIs?

Also, a lot depends on the personality of the manager and the context in which he or she operates. How much edge does the manager want to bring into the conversation? Some managers prefer to put everything out on the table, while others choose to focus on particular areas. All can generate different results.

I also want to highlight that across all of the businesses, safety comes first, and so tracking non-financial safety metrics is part of our role. »

29

31Excellence in Leadership | Issue 4, 201234

Maljers is downstream finance performance manager. He has a planning team, a reporting team and a financial management reporting to him and has been with Shell for 20 years.ALExAnDER mALjERS

So how do you manage the appraisal process at Shell?We have an appraisal framework that is consistent across the organisation: it starts with the RDS appraisal with the Board, then the downstream appraisal with the CEO, all the way down the organisation, say to cluster GM or refinery manager. The appraisals always consist of a standard data set and a number of special topics that are relevant at that time. The more senior appraisals are quarterly and lower down the organisation more often, and we look at a mix of lagging KPIs (e.g. cash, expenditure, earnings) and leading KPIs (e.g. supply/demand forecasts).

We don’t try to create actions from appraisals or have action trackers in place, as it should really be about how the business is doing against its strategy and targets. It is expected that managers would have plans in place to improve performance where it falls short on these criteria. Therefore action planning is the exception.

It’s very important for us as a large organisation to have a consistent business plan and objectives across the company, rather than business areas or individuals working in silos and in different ways. Although we are a huge organisation, we have the same molecules flowing through our entire business. The molecule you buy at a filling station, for example, has easily been “handled” by 10-12 parts of the organisation on its way to reaching you. So that end-to-end value optimisation is absolutely critical and the appraisals should look to include that angle.

What shifts have we seen in performance management over the past five or so years?I think the end-to-end talking and thinking in performance management is coming much more to the forefront now, for a number of reasons. The world has become more complex, Enterprise Resource Planning is now able to give you a full picture of the end-to-end value and, culturally, we are no longer as country-based as we used to be – we are global, with global functions and a globally optimised supply chain. In addition, we are in a period of single-point accountability, with individuals looking after a business. Appraisal discussions now typically include only four key people, which allows for really focused discussions.

It makes measurement and accountability much more straightforward despite the growing complexity of the business. Around ten years ago it wouldn’t have been unusual to step into an appraisal discussion and see 12 to 15 people involved.

How has finance’s role and influence grown during this time?In Shell, strategy sits within finance, and finance owns the performance management processes. Finance drives the planning, and ensures the integrity of the numbers. In every appraisal discussion the finance leaders will sit next to their business leaders, where they bring discipline to the appraisal discussions about the business and, increasingly, bring edge to the business conversations. The finance people can do that because they ask the right questions about why things are working or not. Finance is already playing a greater role than the traditional accountant did in the past and I see that becoming an even deeper partnering role in the future. That’s also why we split our organisation into business finance and finance operations.

Do you feel today’s performance management model will still be fit for purpose in five to ten years’ time, or will this fast-changing business world require a change in the coming years?At Shell, the model we use and the way it is working is robust in the set-up. However, there are a number of areas where we should continue to improve. We could still enhance our ability to hold individuals accountable – we are a massive organisation, with a long value chain, so we want to be able to find out exactly where performance needs to be improved, and who hasn’t played their part.

Looking forward, it’s fair to say that we can expect the speed of performance management to improve. As we develop tools that are increasingly real-time, then the speed at which we can carry out performance management and analysis will become faster.

In addition, I would expect some of the things we are trying out to be more embedded by then. For example, I would expect a sales manager in a region to be able to see instantly everything that is happening in their area, and presented in a way that is useful for them and allows them to react quickly – creating a more direct ability to change things, thus becoming even more reactive to customer demands.

Get

ty Im

ages

32

s the role of the finance function continues to expand and finance professionals become increasingly influential in driving organisations’ strategies, companies are increasingly looking at ways to equip their finance staff with the skills

and experience needed to fill these roles.At the heart of the debate is the role played

by internal shared service centres (SSCs) and the staff working in them – which role SSCs should play in the overall finance function and business, how staff working in them can advance their own skills and careers, and how they will evolve over time.

US multinational Hewlett-Packard (HP) recently launched a new finance, learning and skills portal. The Global Business Services University hosts a wide range of learning material to help staff at its internal SSC to develop their skills.

The university includes a raft of CIMA learning material – 1,600-plus hours of e-learning content – which HP says will give its staff the opportunity to “increase their finance and managerial capabilities”.

Jon Watkins asked V Ravichandran, senior vice president GBS at HP, about the company’s commitment to developing skills among those working in its SSC, why it has chosen to partner with CIMA and, ultimately, how the university will drive performance in the organisation as a whole.

Why have you decided to partner the HP GBS University with a management accountancy body? As HP moves to improve domain expertise within the organisation, there is a need to partner with professional bodies in finance, supply chain and human resources, etc.

What opportunities will this partnership deliver to your finance staff in the short and longer term?I was in Poland recently and talked about this partnership with my team there. They were thrilled. My staff, and not just finance staff, see this as a huge, positive step taken by HP from an employee career perspective. They see this partnership as the first step in creating a knowledge-based organisation. In the long run, my staff see this as an enabler to creating a learning organisation that will add significant value to HP and its business units (BUs).

Does such a move reflect a shift in the skill levels and capabilities within SSCs generally over recent years?Yes, it does. As shared services move higher in their maturity curve, the cost arbitrage factor reduces in importance and customers look for more value-added services. This requires different skill sets and capabilities that many shared service organisations have started building. Apart from this, the expectations of customers regarding the shared service organisation they use is changing to be more driven by business outcomes than output. This means that both skill levels and the capability build need to be different from what they were earlier.

What are the career prospects for ambitious accountants in service centres, and how will the partnership help drive those opportunities? As customer expectations change, career opportunities improve. Shared service organisations are now not just creating people management roles, but roles that need deep domain knowledge and expertise. In the finance space, Global

Excellence in Leadership | Issue 4, 201233

Investing in the future

Get

ty Im

ages

Multinational Hewlett-Packard has created an online “university” to help staff at its internal

shared service centre grow their own finance skills and knowledge. Ultimately, it hopes it will

drive performance across the organisation

Excellence in Leadership | Issue 4, 2012

»

Business Services (GBS) has moved from being a transaction service provider to an organisation that helps close the books of accounts, handles complex reconciliations and cross-border transactions, is building taxation expertise and handles complex reporting, as well as business finance expertise.

We also have forensic accountants, SOX auditors and asset protection services in our SSC. Over the past ten years we have grown in our maturity to provide process expertise to the finance function of HP. This means that our staff have to be professionally qualified to be able to handle the complexity. We are looking to this partnership to give us that.

Do you hope that the partnership will help your accountants develop a better understanding of the drivers of cost risk and value in the business? As I stated earlier, the need to understand business finance, risk and compliance and how all these impact business outcomes is only increasing. The CIMA qualification is very well suited to get our accountants to better appreciate these aspects of business.

In your view, are finance service centres becoming process service centres?Yes. This is true. Over the past ten years, GBS has provided process management capabilities to the finance function. In fact, all major IT project roll-outs and process roll-outs have happened through the use of GBS. Today, GBS owns most of the finance processes of HP.

How essential is it for organisations to expand their finance skill sets today, and to encourage their finance people to gain a broader understanding of the business, to become business partners and to develop the knowledge to make non-finance decisions?Customer expectations have changed and businesses are asking for more outcome-driven services. This means that finance professionals should understand the fundamentals of the businesses they support and be able to add value in business decision-making. A business leader needs to understand his/her numbers extremely well.

It is essential to have finance acumen to succeed in business so expanding finance skill sets is a must for any organisation.

Specifically, how can accountants in SSCs develop close working relationships with their counterparts in distant BUs?This is done through partnering to ensure that the objectives of the BUs and their outcomes become the performance indicators of the SSCs. What is measured is what gets done. So if the outcomes of both the BU and the SSC are intertwined, they will work with each other. Of course, nothing can replace collaboration and the collaborative skills that are needed in today’s geographically dispersed organisations.

How do you hope it will impact the long-term performance of the organisation as you increase the skills and abilities within the finance shared services centre?The services coming out of the SSC will be more contextual and will enable businesses to make decisions. Long term, the focus will be more on data analytics and how information is provided from these SSCs that will drive decision-making within business units.

What sort of results and changes do you hope to see across the SSC in the next three to five years as a result of this partnership?A significant improvement in the quality of services in the finance and risk functions. I am also expecting that the quality of information provided for critical decision-making will improve significantly. Process automation and process re-engineering will improve and this will result in a highly skilled, leaner finance organisation that enables the business to sell more and customers to be able to reach out to global organisations more conveniently.

Why have you chosen to partner with CIMA specifically?CIMA is the leading management accounting body in the world. It is truly a professional qualification. I am a proud member of CIMA and having gone through the rigour, I know the benefits that this qualification can bring to an organisation.

35Excellence in Leadership | Issue 4, 201234

Ravichandran was managing director – India, global e:business operations at HP before taking on his current role.

VRAVICHAnDRAn

With business ethics making front page news, CIMA has been holding roundtable events with

senior finance executives to discuss independence in business partnering. Tanya Barman, head of ethics

at CIMA, summarises the key messages

36

Independent

partners

D rawing on discussions in London, Singapore, Warsaw and Johannesburg, we found a number of similarities, both in challenges and in ways of embedding

good practice. But there were also key regional differences.