Embed Size (px)

Citation preview

Ethanol as a Household Fuel in Madagascar World Bank Final Revisions, June 2011 Project Gaia Responses to Peer Review Questions

Ethanol program Submitted by Harry Stokes and Brady Luceno

1. More detail on recommendations for moving forward: what are the phases, who leads each phase? Suggested phases: a) initiation (R&D); (b) piloting (demonstration, awareness‐raising, capacity‐building); (c) mass propagation (promote entrepreneurs, policy and regulatory measures, standards, access to financing, etc.). Should We Proceed?

The study indicates that it is appropriate to move forward with a pilot phase and incremental scale‐up because the social and economic benefits are shown to far outweigh the financial costs, while, at the same time, the financial feasibility of producing ethanol on a small scale and cooking with ethanol are within range of feasibility, e.g. competitiveness with existing fuels and stoves. Pilot study and measured scale‐up will be essential to test the financial feasibility and determine in what ways and under what circumstances small scale ethanol for cooking will not be feasible or can be made to be more feasible.

Has the Small Scale Production Model Failed?

Small scale distributed ethanol production for fuel use has been discussed and experimented with in Europe and the U.S. since the time of Henry Ford and the Model T, which Henry Ford had designed to run on ethanol1. Both the Germans and the Japanese developed ethanol fuel capability during World War II when their supplies of petroleum fuels ran short2. Brazil built upon this work in the 1950s when it launched its PróAlcool program, which has now resulted in a fuel ethanol economy of enormous national and worldwide importance. During a critical period in the development of PróAlcool, there was an intense debate in Brazil whether to base the production capacity for fuel ethanol on small scale farm‐based production or on large scale industrialized production3. A few key policy decisions by the Brazilian Government tipped the balance in favor of large scale with vital financial incentives encouraging large scale production and penalizing small scale production, but many small producers remained in operation producing for the cachaça if not the fuel market and their technology and expertise was passed on to a new generation of researchers and practitioners who continued to demonstrate and

1 Blume 2007. 2 Kovarik, William. 2008. Ethanol’s First Century – Fuel Blending and Substitution Programs in Europe, Asia, Africa and Latin America, XVI International Symposium on Alcohol Fuels. (On the web at www.radford.edu/wkovarik. 3 Horta 2008

make advances in small scale ethanol manufacture, resulting in the emergence of advocates such as Marcelo Guimarães Mello4, Juarez de Souza e Silva5, Antonio Pedro Machado6, Geraldo Lopes de Carvalho Filho7, Luiz Augusto Horta Nogueira8 and many others. These are practitioners and academics, coming from industry and university teaching and research.

The decision early in PróAlcool to tilt the balance to large scale, which established a trend to further consolidation to very large scale, left many questions about what was the better strategy, and the proponents of small scale in Brazil continue today to make their case, which this study has found to have special interest for Madagascar and Africa.

Meanwhile, the argument for small scale, farm‐based ethanol production has carried on in the U.S. as well, with many farmers developing their own distilleries, despite regulatory barriers put in place in the 1920s and the difficulties that exist in accessing the automotive fuel market. The USDA has clearly shown an interest in small scale ethanol and has sponsored a number of case studies, as has also been done with government sponsorship in Brazil. More information, economic and financial case studies and testing of new equipment and technologies goes on today in small scale ethanol production. The common belief has been that fuel ethanol is feasible only when produced on a large scale, but in fact the issue has not been settled and it remains very much an open question. Thus it is important to note that small scale ethanol production as a feasible production model has not been shown not to work—even in the West—and has not been disproved, nor has it “failed.” It has simply never really been tried on a wide scale, only in individual demonstrations, from which a number of studies have come, with the majority of them showing promising results (Blume 2007; Ortega 2006, etc.)9.

One of the clearest spokespersons for the small scale production model was Deon Hulett of lndustria e Gornircio Ltda, Piracicaba, Brazil, writing in the Proceedings of the South African Sugar Technologists' Association in June, 1981. He stated that:

Farmers could become self‐sufficient in liquid fuel requirements provided tractors, trucks, etc. could use alcohol as fuel. Surplus alcohol, alternatively the whole output

4 Couto, Regina. 2009. Tapping the potential of Brazil’s PróAlcool movement for the household energy sector. Boiling Point 56, HEDON. See also Mello, Marcelo Guirmarães et al., 2001. BIOMASSA – Energia dos Trópicos em Minas Gerais, ed. LabMídia/Fafich, Belo Horizonte. See also: http://www.scribd.com/doc/10258917/A-Producao-de-Etanol-Em-Microdestilarias-UNICAMP-2006 5 Silva, Juarez de Souza, 2007. Produção de Álcool Combustível na Fazenda e em Sistema Cooperativo. Ed. CENTEV/UFV, Viçosa. 6 Idem. 7 Idem. 8 Luiz Augusto Horta Nogueira is editor of the Brazilian Government’s “Green Book,” Sugarcane-based bioethanol: energy for sustainable development, produced by BNDES and CGEE in 2008. 9 Ortega, Enrique, Watanabe, Marcos and Cavalett, Otavio. 2006. Production of Ethanol in Micro and Mini-Distilleries. Laboratory of Ecological Engineering FEA, Unicamp.

7‐12‐11 2

of the plant, could be sold to Brazil's Government purchasing authority at a price which would yield an attractive return on investment.

He defined the task in a very clear way. Micro distilleries are not just scaled‐down large plants; they are small plants engineered for simplicity, efficiency and size:

The manufacturers of the very large fuel alcohol distilleries . . . consider that the minimum size of the plant which can be operated economically is the 120,000 litres per day unit. They also offer plants as small as 10,000 to 5,000 litres per day units but few of these exist because these smaller plants prove to be very expensive . . . . They are simply scaled‐down versions of the larger plants.

With the onset of the world oil crisis, serious shortages of fuel in the country and irregular supplies to the farmers . . . the possibility of producing an ultra simple and comparatively inexpensive distillery which could be installed easily on any farm was investigated and it was found to be feasible provided a different technology was used. The result was the introduction of the MlCRO distillery which in Brazil is defined as a small factory producing hydrated ethyl alcohol at a rate of less than 5,000 litres per day.

He also described the political situation in Brazil, which proponents of this approach faced:

It was natural . . . to expect an immediate "anti" reaction from the big manufacturers and the Government, and the cry of “impossible” and “not viable" was soon heard! The Government refused to consider or accept the MICRO for its inclusion in the PRO‐ALCOOL financial assistance scheme, so that it meant that anyone considering a MICRO would have to bear the cost himself.

He listed the advantages, which are as relevant today as they were in 1981, and which have been demonstrated and explained since by other researchers and developers of micro distilleries10:

Advantages of the MICRO vs. the Bigger Plants

1. Decentralization of job opportunities and a better spread of income helping to settle labour in the rural areas. 2. Considerable economy in fuel due to a reduction of the transport of both cane and alcohol. 3. Greater national security due to decentralization of fuel production points in the country and the resultant flexibility of production. 4. Simplicity of operation obviating the need for highly qualified personnel. 5. An investment cost per litre of alcohol of approximately one third of that of the bigger conventional plant. For the same initial investment as that of one 120,000 litre per day

10 A recent example is a Brazilian study that used the Usinas Sociais Inteligentes (USI) micro distillery, discussed in this report, as the object of its study. See: Rosado Júnior Adriano Garcia, Coelho, Hilton Machado and Feil, Norton Ferreira. 2008. Análise da viabilidade econômica da produção de bio-etanol em microdestilarias. Universidade Federal do Rio Grande do Sul.

7‐12‐11 3

conventional distillery, one hundred and forty‐seven (147) MICRO distilleries, producing a total of 352,000 litres per day, can be installed.11

These advantages are of interest for Madagascar and Africa. Point 5, the assertion that the investment cost per liter of micro plant is one third that of a large, conventional plant, is especially significant. The examination provided in this report (see Section 2.4.2) appears to bear this out.

Discussion on Phases

Phase 1: Initiation (Research & Development)

Much R&D has already been performed with micro distilleries and with the CleanCook ethanol stove, which was chosen as the alcohol stove in the Component A field studies of this report. Project Gaia, Inc. with partners continues to test and develop the CleanCook stove, although it considers the model used in the studies fully commercial12. Other developers of ethanol stoves will surely pilot test stoves in the Malagasy market and throughout Africa. It is likely that one commercially successful stove will lead to at least several in the market.

This study successfully piloted two micro distilleries, one in Ambositra and one in Vatomandry. While micro distilleries have been extensively tested, run and studied in Brazil, the U.S. and diverse countries including Colombia, the Dominican Republic, Italy and India, they should be further tested and developed in Madagascar. This is not because the equipment and processes are mysterious, but because they need to be more fully understood by practitioners. In so doing, innovations and adaptations will emerge. Economical running of these plants is of necessity; how this is done can be demonstrated over and over again only to good effect.

Several companies consulted in this study desire to build their plants in Africa and provide the technical support necessary to train local owners and operators in how to build, operate and maintain these plants. This includes Usinas Sociais Inteligentes (USI) of Brazil and Blume Distillation, LLC of the U.S. These are but two.

For Madagascar it is likely, because of the capacity that already exists with Tany Meva, the Institut Supérieur Polytechnique Madagascar (ISPM), and within industry, given Madagascar’s long involvement with ethanol production, that micro distillery projects will originate as “home‐grown” projects; indeed, they already have. It is also recommended

11 Block quotes are from Hulett, Deon. 1981. The Development of a Micro Distillery for Fuel Alcohol in Brazil. Proceedings of the South African Sugar Technologists’ Association, June 1981. 12 Project Gaia, Inc. and Dometic Group.

7‐12‐11 4

that experienced advanced micro distillery suppliers be invited to the country to build prototype plants, which can then be studied and replicated by local developers.

The outside company may need to provide only the distillation module, allowing the local developer to source equipment from local or regional markets. In addition to the distillation module, other important equipment includes an efficient boiler that burns low‐grade fuel, heat transfer and cooling equipment, electronic controls, the computers to monitor and regulate them, small, efficient ethanol engines and various other applications. The front‐end of the plant, the fermentation trains, and the backend of the plant, fuel storage and co‐product handling, can be sourced locally.

Madagascar should watch what develops elsewhere in Africa with micro distilleries and stoves. This is an activity that could be led by Tany Meva and ISPM. A USI distillery has just been purchased in Nigeria for Oyo State, with assistance from the Nigerian federal government13. The development team has also purchased 1,000 CleanCook stoves to use the ethanol that will be produced. This project will be closely watched. The World Bank has funded the development of a micro distillery in Ethiopia under the Biomass Energy Initiative for Africa (BEIA) program. This is to be implemented by the Gaia Association. Several new small distilleries are already operating in Africa. These projects offer excellent case studies for Madagascar.

A vital focus of the additional study needed on micro distilleries in Africa concerns the production and supply of feedstock to the micro distillery. Any micro distillery project should have a strong agricultural component, with Agricultural Extension or the Ministry of Agriculture involved. The International Institute of Tropical Agriculture in Ibadan, part of the CGIAR network, will be involved with the Oyo State project. Growing, providing and preparing feedstock for the micro distillery is as important as fermentation, distillation and of use of products.

Another vital focus is government policy development. The Malagasy government should assist directly in technology transfer, knowledge sharing and reduction of barriers to commercialization. The PróAlcool in Brazil was developed over many years with the help of a comprehensive list of incentives. Development of ethanol fuel in Madagascar will be greatly speeded by the government’s engagement on the policy and regulatory levels14 Addressing land tenure issues may be one area where government policy reform can have a big effect.

13 Facilitated by Project Gaia, Inc. This is the National Biotechnology Development Agency (NABDA) project. 14 For a discussion on policies to promote biofuel development, see Horta Nogueira, Luiz Augusto, ed. 2008. Sugarcane-based Bioethanol – Energy for Sustainable Development, BNDES and CGEE, Chapter 8, Section 4.

7‐12‐11 5

Phase 2: Commercialize Ethanol Fuel & Stoves (demonstration, awareness raising, capacity building); Phase 3: Mass Propagation (promote entrepreneurs, policy & regulatory measures, standards, incentives and subsidies, and access to financing, etc.)

The easiest pathway to commercialization is to start small and build incrementally. This is possible with a “micro distillery plus stoves” approach. If a commercial start‐up begins with a scale of 1,000 liters per day, this is 4,200 tons of sugarcane consumed in one year, 1,000 stoves sold in one year, and 360,000 liters of fuel sold in one year. One sees the relative importance of the feedstock and the ethanol fuel to the stoves. For every stove sold, 4 tons of sugarcane are harvested and 360 liters of ethanol are sold.

Providing financing opportunities for building and operating micro distilleries may be the most effective way to reduce financial impediments to creating an ethanol fuel market in Madagascar. If the micro distillery can be built locally, the equity required, at 20%, may be in the range of $5,000 to $10,000. To import and install one of the advanced systems from Brazil, the equity requirement would be quite a bit higher at $20,000 to $30,000. The ROI on the more expensive, imported system may be quite good, however, because the efficiency and productivity are high. The National Development Bank of Brazil has repeatedly stated its willingness to offer finance for these systems.

Import duties will be a critical issue. Many countries provide incentives for importing machinery and equipment for value added processing or manufacturing either tax free or at greatly reduced rates. Madagascar does not have a clear program in this regard. Bringing in the best prototype equipment to start a small scale ethanol production industry is very important. Tax holidays on equipment and machinery can be justified for agricultural and industrial development reasons, for import substitution and for the reason of creating a biofuels economy. Several national priorities come together to support the creation of incentives by government and financiers.

Introducing the CleanCook stove or other high quality stoves offers the same benefits as introducing advanced micro distillery equipment. Getting high quality prototype equipment into local commerce will stimulate innovation and the development of “home grown” solutions. Dometic Group, the manufacturer of the CleanCook, has offered to the prospective local manufacturer the option of shipment of stove parts for local assembly, partly for the reason of avoiding high tariff barriers, with the local manufacturer taking over manufacture as capacity is built. This approach would enable the local manufacturer to adapt the stove body and pot supports to local needs, while retaining the Dometic stove burner technology. Dometic understands that it cannot make locally appropriate stoves for many different countries in one central plant in Europe. Therefore, it is willing to share the technology to responsible partners so that its stove technology can be adapted to local

7‐12‐11 6

needs and stove sales can increase. Dometic has no experience in Madagascar; therefore, it needs a responsible local partner to assist it in negotiating the Malagasy market. Since Madagascar would not necessarily be a market that Dometic would enter, Malagasy authorities must realize that companies like Dometic need to be attracted to their market.

While there are very few high performing ethanol stove on the market today anywhere in the world that are capable of heavy duty cooking, there are many examples of good micro distilleries operating in many different countries. These micro distilleries are “stick built,” e.g. built one at a time. The opportunity exists to build modular micro distilleries on an “assembly line” basis, and this in fact is what both USI in Brazil and Blume Distillation LLC in the U.S. are planning to do. As the number of units built increases, presumably the price of equipment would come down. Equipment for a smaller unit would match equipment for a larger unit, except for the distillation tower itself, and equipment could be assembled in series to increase plant size, to a point where resizing is necessary for efficiency and cost.

This same approach could be taken for building micro distilleries in Madagascar. The opportunity exists for a local industry to produce micro distilleries for many applications, whether on the farm or in built up areas where waste streams exist that could be used to produce ethanol. The know‐how for this could come through ISPM from France, from Italy, from elsewhere in Europe, or from Brazil, the U.S., the Dominican Republic, Mauritius or India. Understanding of micro scale distillation is widely shared.

The ideal composition of a team to start a commercial project around ethanol stoves and fuel is a local investor with sufficient resources to provide project equity, a local bank, a development bank willing to assist with loan capital at a preferred rate, and technical support from academic, non‐profit and development organizations like Tany Meva to provide advice and expertise on the technologies and project planning. Such facilitating organizations could also be the link to outside expertise on stoves, distilleries and agronomics. The partner also needs to have access to a civil engineer, a process engineer or chemist familiar with fermentation and distillation, and to an agronomist familiar with the crops that will provide the substrate for the ethanol manufacture.

Ways in which this team could be assisted to implement their first‐of‐a‐kind business include:

1. Funding and planning assistance to complete a business and financing plan (estimated cost is less than $10,000)

2. Access to financing at preferred rates (estimated cost over 5 years is less than $30,000)

7‐12‐11 7

3. Assistance with importing machinery and equipment (little or no cost)

4. At least a temporary holiday on tariffs to promote technology transfer (estimated cost less than $35,000)

5. At least a temporary holiday on VAT for the sale of stoves and fuel (estimated cost less than $10,000 for the first year of operation).

6. Recognition in government of the cross‐cutting nature of the enterprise, with engagement by the ministries of Revenue, Agriculture, Energy, Industry and Health (little or no cost).

The total cost of this package of incentives is $85,000, not all of which is borne by the same sponsor. Some combination of these incentives could be quite helpful for the first several start‐ups.

Creating the right environment for this sector to grow could include the following policy interventions from government:

1. Recognition of ethanol as a fuel, not only a chemical or pharmaceutical, and regulation of ethanol as a fuel

2. As a corollary to the above, policy making across the energy sector with ethanol fuel as part of the bigger picture; using incentives rather than laws or mandates to help pick the winners

3. Recognition that beverage ethanol is an entirely different product, industry and market

4. Intellectual property protection for patented technology

5. Engagement in the planning and regulation of the fuel supply chain to assure safety, integrity and economy of the fuel

6. Certification of quality stoves. Stoves should carry a government seal and be clearly differentiated from inferior products sold in the market. Obviously, it would be best to keep as many of these inferior, often dangerous stoves out of the market altogether. Bad stoves can retard the introduction and uptake of good stoves.

7. Government to play an advocacy role in promoting clean fuels and their many benefits.

7‐12‐11 8

Are Subsidies Needed?

The Fuel

Creating a conducive business environment in which micro distilleries and the use of ethanol for cooking can grow is a much cheaper way to promote ethanol than subsidies.

Ethanol itself is intrinsically cheap to manufacture. Most of the value in the ethanol (>50%) is transferred back to the farmer as payment for his crop. In Madagascar, sugar cane prices are generally low ($8 to $15 per ton) because of low farm labor costs. This is comparable to Brazil. Other costs in the manufacture of ethanol are small, with energy inputs and capital cost of the equipment being the most important. If the investment cost in the equipment can be kept down—removing tariffs on imported equipment for example—and if energy efficient technology is selected and used (a good boiler, a well‐designed furnace), then the costs involved in the production of ethanol, other than the cost of the feedstock, are very small.

With energy and investment costs kept down, there is ample opportunity for the sale price of the ethanol to be kept low, while still paying a fair price to the farmer for his/her sugarcane. Thus, the cost of the ethanol does not need to be subsidized to the consumer because the ethanol is already cheap enough—possibly as cheap as the price of charcoal15.

Subsidies on the fuel are expensive to government because the subsidy is paid on every liter sold. Tax holidays and government‐sponsored programs to assist in the set‐up of efficient, affordable micro distilleries come with costs, but these are one‐time costs to get the distiller into business. If he has been assisted in building an efficient distillery without unnecessary cost in the equipment, he/she will produce an abundance of cheap ethanol over many years.

Supply chain is the other cost of any significance in the fuel. If the supply chain can be kept short, with the minimum of “middlemen” who must take their share of profit, then the cost of the fuel will be less. If micro distilleries are serving a geographically concentric market, it is quite conceivable that there would be no middlemen. The ethanol could be dispensed from a pump at the micro distillery gate, and residents of the town or village served could

15 In fuel cost studies Project Gaia has conducted in Nairobi, Kenya, and in Haiti, where the daily cost of charcoal is quite high, in the range of $0.50 or greater, it appears that ethanol would already be the cheaper fuel. Please see: Boiling Point 59, Bringardner, Patrick, et al., 2011. Using emergency interventions for sustainable development: Jumpstarting the transition from woodfuels to liquid biofuels and efficient agriculture. Available at http://www.hedon.info/View+Article&itemId=11884.

7‐12‐11 9

walk or take local conveyance, whether daily or weekly, to the distillery to direct‐purchase their ethanol.

This would not work for urban markets, but for these markets, the ethanol could go directly in liter bottles in crates (for example) to certified fuel sellers who would sell direct to the customer. Or, it could be transported in a converted kerosene tank truck and bottled at the fuel‐seller’s establishment. Ethanol as a fuel is more efficient to ship than fuelwood or charcoal and easier to store. If redundant “middlemen” can be kept out of the supply chain, the opportunity for running a supply chain with less cost in it than the traditional wood or charcoal supply chain is real.

The Stove

Ethanol stoves should be built with quality materials that withstand corrosion. Corrosion can destroy a mild steel stove within month, even a stove that is painted. The CleanCook stove currently comes in two iterations, an all‐stainless‐steel stove, with high quality stainless, or a stove with a baked finish aluminum body, a galvanized steel heat shield (inside the body) and burner parts of stainless steel. These stoves have an estimated 10‐year and 6‐year life respectively. As these stoves are made on an automated assembly line, most of the cost of the stove is in the materials or in the capital cost of the tools to make the stoves. As the numbers of stoves produced increases, the capital cost of production contained in each stove will decrease. The cost of materials may decrease but only slightly. A one‐burner CleanCook is likely to eventually reach the cost of 35 EUR. Today the cost is in the neighborhood of 40 EUR for the aluminum‐bodied stove and 50 EUR for the all‐stainless stove. Most of the cost of the stove is in the material used for fabrication.

As other ethanol stoves come into the market, attracted by the availability of ethanol fuel, it is likely that the stoves that work well, with good heat output, fuel efficiency, convenient handling, durability and safety, will not be cheap. They may cost out above $20, $30 or $40 USD, or more. Most consumers, to purchase a quality stove, will need access to financing to do so. They will need to be able to buy the stove over time—6 months, 12 months, 18 months.

If the stove is durable, with a multi‐year life, it should be well suited for financing. A stove with a 6‐month life can hardly be financed over 6 months, and certainly not over 12 months. A stove with a 6‐ or 10‐year life can be financed over a year or 18 months. If the consumer is able to enjoy the use of the stove for a reasonable period of time after it is fully paid for, he or she will be much more likely to purchase it.

An amortization schedule for a stove might look like this:

7‐12‐11 10

Without Carbon Finance

Loan Summary $45.00 Principal amount $4.14 Monthly Principal & Interest $49.64 Total of 12 Payments $4.64 Total Interest Paid

Amortization Schedule 18.5% Month Interest Principal Balance

1 $0.69 $3.44 $41.56 2 $0.64 $3.50 $38.06 3 $0.59 $3.55 $34.51 4 $0.53 $3.60 $30.91 5 $0.48 $3.66 $27.25 6 $0.42 $3.72 $23.53 7 $0.36 $3.77 $19.76 8 $0.30 $3.83 $15.93 9 $0.25 $3.89 $12.04

10 $0.19 $3.95 $8.09 11 $0.12 $4.01 $4.07 12 $0.06 $4.07 $0.00

With Carbon Finance

Amortization Schedule 18.5% Month Interest Principal Balance

1 $0.54 $2.68 $32.32 2 $0.50 $2.72 $29.60 3 $0.46 $2.76 $26.84 4 $0.41 $2.80 $24.04 5 $0.37 $2.85 $21.19 6 $0.33 $2.89 $18.30 7 $0.28 $2.93 $15.37 8 $0.24 $2.98 $12.39 9 $0.19 $3.03 $9.36

10 $0.14 $3.07 $6.29 11 $0.10 $3.12 $3.17 12 $0.05 $3.17 $0.00

Loan Summary $35.00 Principal amount $10.00 Carbon Finance input $3.22 Monthly Principal & Interest $38.61 Total of 12 Payments $3.61 Total Interest Paid

One can see from these examples that a financed stove can be affordable, even at a purchase price, as in this example, of $45.00.

Carbon finance is helpful but in these examples carbon finance at $10 per stove is not nearly as important to the consumer as his/her opportunity to finance the purchase of the stove.

Positing a daily fuel cost ‘going rate’ (e.g. a fuel cost for any fuel bought) of $0.30, with a monthly cost of $9.00, the monthly amortization rate for the stove is one‐third to one‐half the monthly fuel cost. This helps to illustrate that the fuel cost is a much more significant

7‐12‐11 11

expense than stove cost—even when the stove costs $45 and must be micro financed at 18.5%.

The reason that the fuel cost is manageable for the consumer is that it is a small cost once a day, not a big cost all at once. But that said, the difference in a fuel cost of $0.50 and $0.40, for example, represents a huge economy over time—in this instance $36.50 over one year, which is nearly the cost of a stove.

Because ethanol is an intrinsically cheap fuel—cheap to make under normal, e.g. widely prevailing circumstances—it should not have to be subsidized, as kerosene and LPG once were in many national markets and still are today in such places like India. If ethanol fuel can be brought cheaply to the market, with the added help of a short and economical supply chain, then it is possible that there will be enough economy in the fuel to provide a cross subsidy for the stove. If $0.05 is placed in the fuel to pay for the stove, then the cost of a $45 stove to the consumer would be $27 if the subsidy is collected over one year and $9 if collected over two years. The cost of the stove can “disappear” if the fuel, if there is enough economy in the fuel to permit this.

The advantage of a durable stove made of stainless steel or other high quality materials is that its life of 6, 10 or more years allows it to earn both cross subsidy finance and carbon finance for the life of the stove. If the cross subsidy in the fuel pays for the stove in 3 years, nevertheless, the stove in consuming fuel for many more years beyond 3, and the owner of the stove is paying fuel cross subsidy for those additional years. That excess cross subsidy can then be said to be available to pay for another stove. The same is true for carbon offsets or carbon finance. If the stove earns offsets in years 1‐3 to pay for the stove, yet it is also earning in years 4‐10 to pay for other stoves. Stove developers may argue for a mild steel stove that can be sold for $15. This provides an argument for a high quality stainless steel stove that may cost $45 or $55 but last for 10 years or more.

If a fuel seller has as his or her business both the selling of fuel and stoves, then he or she can take advantage of the fuel to sell the stove, provided the fuel has been brought to market economically.

An example of this financing model was constructed for Haiti, using the actual cost of kerosene and charcoal fuels in Haiti, the cost of a charcoal, a kerosene and an ethanol CleanCook stove, and a projected cost for ethanol if shipped from Brazil. It shows the

7‐12‐11 12

ethanol stove to be the cheaper stove by far, because there is enough savings in the ethanol fuel to dramatically reduce operating cost16.

Operating Costs of Stoves: Haiti Example (Peaks Show Stove Replacements)

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

$50.00

1 7 13 19 25 31 37 43 49 55 61 67 73Months

Cos

t per

Mon

th

Ethanol Stove Carbon FinanceCharcoal Stove

Kerosene StoveEthanol Stove No Carbon Finance

Should the Stove be Subsidized?

In light of the above, does a relatively expensive stove have to be financed for a lower income demographic, if all of these financial tools are available?

If subsidies are to be added to a program to promote rapid uptake of ethanol fuel and the stoves necessary to burn it, then the subsidy should be applied to the stove rather than to the fuel. There are several reasons for this, as follows:

1. A subsidy is paid once per stove, while the subsidy is paid on each increment of fuel. For a 10‐year stove, a subsidy on fuel would be paid more than 3,600 times. If a $10 or $20 subsidy is paid on the stove, this makes a meaningful difference. If the same subsidy is applied to the fuel, it would not be meaningful. Stated another way, subsidizing the stove is much cheaper than subsidizing the fuel.

2. For a clean fuel program to stand on its own and ultimately be sustainable, the cost of the fuel must be competitive with other fuels. Creating artificial fuel pricing is likely to be unsustainable. This is demonstrated by the fact that most African countries have of necessity deregulated their fuels. Having gone through

16 Boiling Point 59, Bringardner, Patrick, et al., 2011. Using emergency interventions for sustainable development: Jumpstarting the transition from woodfuels to liquid biofuels and efficient agriculture. Available at http://www.hedon.info/View+Article&itemId=11884.

7‐12‐11 13

the painful process of kerosene deregulation, why would a government choose to regulate the price of another fuel by use of subsidies?

3. If a subsidy can enable the purchase of a better stove, this will produce gains in efficiency, durability, safety, air quality and so on. There is no virtue in a cheap stove. Assuming rational pricing, cheap stoves are less likely to deliver the same benefits as more expensive stoves.

4. Stoves are the essential condition to drawing ethanol fuel into the household market. Without stoves in the hands of consumers, ethanol producers cannot sell their ethanol to the household. If an ethanol stove fuel market exists, it is likely that the ethanol producer can fund or finance his/her business and get into production. Thus, distilleries can be established and spread on an entrepreneurial basis. Stoves, in contrast, must be marketed and sold to consumers. Consumers must weigh short term against longer term benefits and costs. The high initial cost of a stove is likely to discourage the decision to purchase. A subsidy on the purchase price of the stove is a marketing tool that will encourage the sale of stoves. It also reduces the barrier that the high purchase price poses for many consumers, with or without financing. Using the finance model shown above, a $45 stove with a $20 subsidy reduces the monthly payment to $2.30. The interest the consumer pays on the micro loan is less than $2.60.

5. The subsidy on the stove may be able to be phased out as the business matures and many stoves enter the market.

There is a compelling analogy to be made between the mobile phone business and a business of stoves and fuel sales. The telephone handset is subsidized by the sale of airtime, just as stoves would be subsidized by the sale of fuel. If one accepts this analogy, then an examination of how the mobile phone business has matured over 20 years could be instructive. There are many millions of mobile phones in operation today even in the poorest countries. The use of mobile phones has skyrocketed in Madagascar17. Handsets were originally sold very cheaply or even given away. Today handsets are sold at retail prices and many handsets with added features and functionality are sold at prices typical of developed economies. There is a booming business not just in airtime but also in hardware.

As more stoves come into the market, the cost of the stove will fall. The stove will become a recognized consumer appliance; it will attract more attention and be

17 UNData for Madagascar: Mobile phones. Available at http://data.un.org/Search.aspx?q=Madagascar.

7‐12‐11 14

accorded more importance in the choices that consumers make. As Africa’s growing middle class18 buys more stoves, the earnings on fuel that stoves in use generate will help to underwrite the marketing and sales of more stoves into the market. If fully paid stoves are earning fuel cross subsidy and perhaps even carbon offsets, this is income available to a stove and fuel business to push more stoves into the market. The mobile phone industry grew rapidly because there was a large pent‐up need in the market, because they had a product that really worked, and because a business model was created using the sale of many small, cheap units daily to pay for the sale of the expensive infrastructure, which was also units of sale but which could not serve as a profit center until there were enough handsets in the market to reach critical mass. Now the handsets for the most part carry themselves. But the industry still uses cheap, subsidized handsets to enter new markets, including poor markets. They are not afraid to service markets where consumers earn just a few dollars a day, because they know that the consumers will prioritize their spending and buy what works.

Uptake of Cell Phones in Madagascar 1993 to 2008 as a % of Population

0%

5%

10%

15%

20%

25%

30%

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Year

18 For an informative report on Africa’s rising middle class, see: Ncube, Mthuli, et al. 2011. The Middle of the Pyramid: Dynamics of the Middle Class in Africa. AfDB Market Brief, April 20, 2011.

7‐12‐11 15

Thus if direct subsidies are to be used, the appropriate place to put them would be on the stove, not on the fuel. If the mobile phone industry is a useful analogy, the subsidies would eventually be able to be phased out, at least for most consumers.

2. Geographic targeting: does it make sense to start with urban/peri‐urban market? Pro: richer, more concentrated, greater environmental impact. Con: further from feedstock source.

Ethanol as a liquid fuel is an efficient way to concentrate and transport energy over distances to market. It can occupy the same role that kerosene has historically, in this regard. Therefore, ethanol can be produced in proximity to its feedstock and transported to urban markets, where roads exist that can accommodate small or large tanker trucks. Tanker transport to market may be most suitable for large scale ethanol production.

Tanker trucks come in 2,000, 5,000, 10,000 and up to 40,000 liter sizes; the latter is a tandem rig where one cab pulls two tankers.

Unlike large plants, small and micro scale distilleries can be located close‐in to urban areas because they can use dedicated small sources of feedstock and may not require large production bases. Micro scale distilleries can be situated on small areas of land with minimal buffers to other uses. One to two hectares of land are ample for a 2,000 to 5,000 liter/day distillery. Thus, a distillery could be located at a food processing center (such as fruit canning or coffee or rice milling). Provided waste is collected and managed properly, a distillery could be supported from the unsold produce of an urban market. This ethanol would be readily available to its geographically proximate urban or suburban area. But it would be only a very limited supply of ethanol, serving a tiny fraction of a potentially large market.

Where a rural micro distillery can be established based upon good feedstock opportunities, the ethanol from this distillery would best serve a geographically proximate market. This might be a village or town where population density is conducive to efficient delivery of the fuel. But under the right circumstances, fuel does not have to be delivered. Consumers can come to the distillery to purchase the ethanol from a metered pump located at the distillery.

Depending on the size of a retail stove and fuel business, it is probably most feasible to begin the commercialization of stoves and ethanol fuel in the urban and peri‐urban markets. These markets have the advantage of more developed infrastructure, which will help in establishing supply chains. Urban and peri‐urban markets also offer the advantage of engaging with other retailers that have already established consumer bases and supply chains. Purchasing power and the comparative cost of other fuels will also be higher. Ethanol may find a competitive edge vis‐à‐vis other fuels.

7‐12‐11 16

This study has shown that ethanol production tends to be within reach of the major urban markets in Madagascar, but a more in depth assessment of ethanol feedstocks, including a bio‐mapping study to identify current and potential feedstock lands and materials (by‐product and waste inventories) would be beneficial to determine where opportunities lie. The Government of Brazil has conducted bio‐mapping studies in Mozambique and Senegal and is considering providing this service to other countries in Africa19.

Industrial production of ethanol in Madagascar is set to increase steadily over the next five years. If a portion of this supply could be made available in bulk for household cooking, urban households would be the first target market for this ethanol.

In rural areas, woody biomass will continue to dominate household energy use for some time to come. The smoke, dirt, discomfort and health risks, as well as the inconvenience and lack of efficiency involved with using solid fuels, will eventually make competitively priced ethanol an attractive fuel even for rural households, where fuels are purchased. Component A of this report shows that a major concern for most households is the speed of cooking. Efficiency and time saved are key advantages of the CleanCook stove and ethanol fuel. Time savings as well as cleanliness and convenience are benefits that will motivate consumer decisions first in urban and peri‐urban households but eventually also in rural households.

19 For the bio mapping study performed by the Getulio Vargas Foundation for the Government of Senegal, see http://www.fgv.br/fgvprojetos/novoprojetos/arq_site/972.pdf. Cite as: Getulio Vargas Foundation. 2010. Biofuel Production in the Republic of Senegal | Stage 1: Feasibility Study.

7‐12‐11 17

3. More on policy context required for next phases: duty‐free import of stoves etc.

Supportive government policy that will promote technology transfer will be of critical importance. We would recommend that the results of this study be used to encourage the Government of Madagascar (GOM) to provide at least a temporary tax holiday (two to five years) on the importation of stoves and microdistillery equipment. An initial number of stoves should be imported to Madagascar to quickly build a market for locally produced ethanol. This will provide a commercial demonstration. Local production of stoves will follow. Small scale programs can be built incrementally by their very nature. Yet it is often difficult to get started. If the GOM can assist with helping commercial interests to get started, every indication is that the program will grow steadily.

Please see above (response # 1) for additional discussion on policy options available to government.

Importing “seed” stoves offers to a prospective manufacturer a way of testing the commercial market without incurring the investment risk of building stoves first, ahead of any proof of market. Investors want to see stoves in operation and ethanol fuel in use prior to making a commitment. Experience in other countries is no substitute for experience in Madagascar. Even if the investor is confident in the stove itself, he or she will want answers to the following questions:

1. Will consumers like cooking with ethanol? 2. Will consumers like the ethanol stove? 3. How much will consumers pay for the stove? 4. How much will consumers pay for the fuel—how does it compare with fuels we

already know? 5. Where will the ethanol fuel come from—can I make it, will others make it? If I

make the stoves, will there be fuel to run them?

While introducing a new appliance into the market might be easy enough, this is more challenging because of the need to prove the fuel and pull it into the market.

The early regulation of the ethanol stove and fuel in Madagascar will determine the way in which this alternative is developed and whether it prospers or not. There are many examples of nascent alcohol fuels industries having been destroyed by the lack of attention or misguided policy by government. In the U.S. in the early 1860s a burgeoning lamp oil industry based on alcohol produced in thousands of farm‐scale distilleries was destroyed overnight by a tax placed on alcohol that did not distinguish between beverage and fuel alcohol20. Brazil, in the 1950s,

20 Kovarik, Bill. 1998. "Henry Ford, Charles F. Kettering and the Fuel of the Future," Automotive History Review, Spring 1998, No. 32, p. 7 - 27. Available at http://www.radford.edu/~wkovarik/papers/fuel.html.

7‐12‐11 18

enacted a comprehensive program of incentives and policies to build its PróAlcool program21. Today in Madagascar excessive and cumbersome duties and taxes incurred when bringing the new ethanol stoves in for testing hindered this research project, delaying it and making it more costly. Commercial start‐ups are fragile and cannot afford uncertainty, delay and added cost. They may not require subsidy for their products, but they may need the avoidance of cost to get started.

We recommend that the Ministry of Energy and the Ministry of Finance and Budget work together to ease technology transfer to Madagascar. The Ministry of Energy, through its renewable energy policy, can determine types of technologies that should benefit from tax and duty waivers22. When this study looked at the performance of the few existing domestically produced ethanol stoves, it determined that a stove produced outside the country should be brought in for the study. This was not a recommendation against developing locally made stoves; on the contrary, it was a recommendation for a technology that should be used for local development. Bringing new technologies in will help local stoves to develop and evolve. This will help to ensure that Malagasy consumers have access to stoves as good as or better than any stoves in the world. It also helps to guarantee the success of the local ethanol industry. There are notable examples of failed ethanol stoves and it is imperative that an inferior stove not set back the development of ethanol fuel23.

To get good technologies in, the GOM should grant favorable trade and tax treatment at least on a temporary basis. Exemption from taxes such as VAT or sales tax would also help a project to reach scale once the technology is in use in the country. When the products are fully commercialized, VAT can be returned.

To import the stoves for this study, each stove incurred customs duties, VAT, Gasy Net fees, airport agency fees, and customs agency fees. This increased the cost of the stoves by 350%. Moreover, the process was staff‐intensive and time consuming. Five months were required to get 147 stoves through customs. Part of this was the time required to receive a response from the Ministry of Finance and Budget on the matter of duty exemption, which was denied even though one of the two deliveries of stoves was actually donated by the manufacturer.

21 Horta, et al. 2008. Evolution of Bioethanol Fuel in Brazil, Chapter 6. Sugarcane-Based Bioethanol – Energy for Sustainable Development. BNDES and CGEE. pp. 148-150. 22 To avoid abuses with tariff and duty waivers, such waivers should be granted in connection with specific government policy, such as renewable energy development policy. In the past, it has been acknowledged that abuses have occurred, as in “Category 7” tax exemptions for “reason of state.” See: WT/TPR/S/197, or World Trade Organization, Trade Policy Review, S197, pp. 36. Available at: www.wto.org/english/tratop_e/tpr_e/s197-03_e.doc. 23 When ORIGO, the CleanCook prototype, entered the European and US markets in 1978-1980, it gradually displaced the alcohol Primus stove, which is now no longer available in these markets. The gelfuel stove has set back the effort in Africa to develop alcohol fuels because of the general dissatisfaction by consumers of this stove.

7‐12‐11 19

A step that caused delays in the technology transfer was the registration of imported goods on Madagascar’s Gasynet website, also known as Malagasy Community Network. All international trade to and from Madagascar must be registered on the Gasynet system which is a public‐private partnership. This system is relatively new to Madagascar and is not yet working smoothly. It can be ambiguous or unclear what documents are needed for the shipment of goods. It is very difficult to obtain technical assistance, and for any unusual or unique circumstance, the Gasynet system proves inflexible. The importation of the ethanol stoves was not made easier by the Gasynet system24.

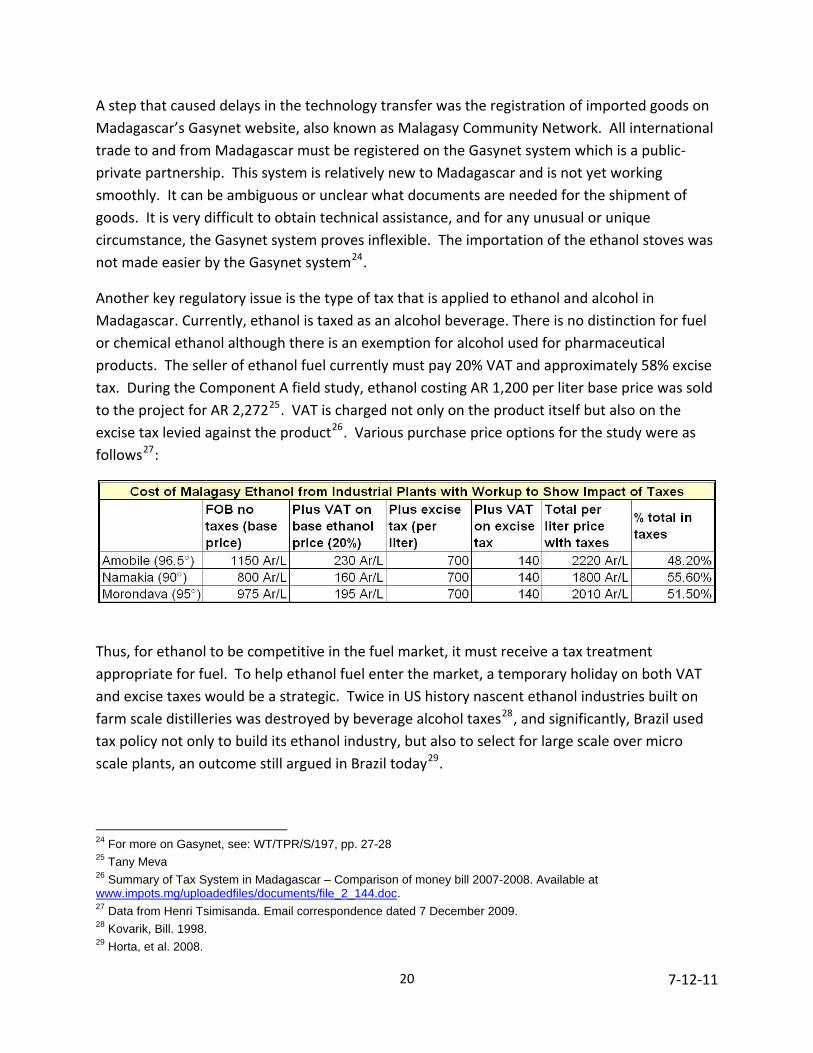

Another key regulatory issue is the type of tax that is applied to ethanol and alcohol in Madagascar. Currently, ethanol is taxed as an alcohol beverage. There is no distinction for fuel or chemical ethanol although there is an exemption for alcohol used for pharmaceutical products. The seller of ethanol fuel currently must pay 20% VAT and approximately 58% excise tax. During the Component A field study, ethanol costing AR 1,200 per liter base price was sold to the project for AR 2,27225. VAT is charged not only on the product itself but also on the excise tax levied against the product26. Various purchase price options for the study were as follows27:

Thus, for ethanol to be competitive in the fuel market, it must receive a tax treatment appropriate for fuel. To help ethanol fuel enter the market, a temporary holiday on both VAT and excise taxes would be a strategic. Twice in US history nascent ethanol industries built on farm scale distilleries was destroyed by beverage alcohol taxes28, and significantly, Brazil used tax policy not only to build its ethanol industry, but also to select for large scale over micro scale plants, an outcome still argued in Brazil today29.

24 For more on Gasynet, see: WT/TPR/S/197, pp. 27-28 25 Tany Meva 26 Summary of Tax System in Madagascar – Comparison of money bill 2007-2008. Available at www.impots.mg/uploadedfiles/documents/file_2_144.doc. 27 Data from Henri Tsimisanda. Email correspondence dated 7 December 2009. 28 Kovarik, Bill. 1998. 29 Horta, et al. 2008.

7‐12‐11 20

4. Subsidies: the public good provides justification for public support in initial phases, but what to subsidize? Provide arguments for subsidizing investments in stoves/distilleries rather than fuel. How best to allocate subsidies for stoves and/or distilleries?

The great opportunity of ethanol as a household fuel is that it can be produced cheaply, at a price that is competitive or near competitive with fuels in Madagascar that are purchased. Current pricing information shows the price of ethanol to be slightly higher than charcoal but cheaper than kerosene and LPG. As such, the daily purchase of fuel would not require a subsidy to get its start in the market. In fact, it is recommended not to subsidize ethanol fuel but rather to allow it to develop in competition with other unsubsidized fuels. It is recommended to subsidize the technology purchases necessary to make and use ethanol cheaply and efficiently. If lessons can be drawn from the past 60 years, national cooking fuel subsidy programs are enormously expensive and eventually have to be abandoned. It could be argued that the subsidy of kerosene and LPG in various markets actually retarded the development of other clean fuel options like ethanol. Development of a fully commercial ethanol fuel market from the outset will protect consumers from the eventual shock of government withdrawing its subsidy. What government can do to assist the new fuel market is to avoid injecting cost into it while it is young and fragile. Ethanol as a fuel must be differentiated from ethanol for other uses, and if possible, taxes should be removed or reduced on ethanol fuel to assist it in getting into market.

Subsidies could have a very positive effect on the uptake of stoves. These subsidies could be offered during an initial growth period and be phased out when ethanol stove and fuel businesses begin to reach critical mass (sufficient sales to survive and reinvest). Subsidies could also be provided to microdistillery technology and operations in the form of tax credits or holidays—especially for advanced technology coming in from outside. This promotes technology transfer. Most of this new equipment would eventually be produced locally.

Experience of LPG Subsidies in Brazil: From 1950 to 2001 the Brazilian federal government regulated the final price of LPG to consumers. In 2001, the LPG fuel subsidies were removed, which corrected the price distortion but dramatically increased (essentially doubled) the price of fuel for consumers. In order to regulate the LPG subsidy, the Government had created excessive standards and procedures in the distribution system, which discouraged investment and competition.30 Subsidizing the fuel caused other problems, including waste. Studies found that subsidized fuel was being used for inappropriate purposes, such as heating swimming pools and saunas, simply because it was so cheap. It was also being used in vehicles fitted to burn LPG. This represented a big expense for the government which expended around $100

30 Lucon, Coelho, & Goldemberg. “LPG in Brazil: lessons and challenges”. Energy for Sustainable Development. Volume VIII No. 3. Sept 2004.

7‐12‐11 21

million USD annually to subsidize the fuel. It is estimated that the Brazilian government spent approximately $8.235 billion between 1973 and 2011 on LPG subsidies. Additionally, studies found that nearly half of the energy used in an LPG stove was being wasted, heating air and stove parts, but not the pot and the food. Once the subsidy had ended, many users reverted to using their traditional wood and charcoal stoves. Project Gaia found this to be so in its studies in 2006‐2007 in three locations in Minas Gerais State31.

Experience of LPG Subsidies in Senegal: In the 1970’s Senegal began a “butanisation” program to promote the use of LPG as a cooking fuel in the home. In the beginning, import duties and tariffs were waived on the stoves; however, the program did not take off, initially, it was thought, because the government failed to promote the LPG program. In a second try to penetrate the market, Senegal moved to a direct fuel subsidy32. The success of the program seems to be attributable to the discounts on fuel but also to the fact that families could purchase fuel in smaller quantities (2.75kg or 6 kg). Annual domestic consumption of LPG rose from 3,000 tons in 1974 to 100,000 tons in 2000, almost all of which was sold in the smallest cylinders (2.75 kg) for household consumption. In 1998 the government began reducing the subsidy by 20% per year until 2002 when it was completely eliminated. At present, LPG prices are affordable to many homes since the private sector has taken over the fuel supply and competition has helped to control the price. LPG is now the primary cooking fuel in 71% of urban households33.

Experience of Kerosene Subsidies in Nigeria: A study in Nigeria showed that when the government removed fuel subsidies, the national poverty level increased. The report also highlights that the way in which government deals with subsidies—and the removal of subsidies—can greatly affect the lowest‐income brackets. The report states that subsidy removal can have a disproportionate effect on urban vs. rural households34.

Experience of Kerosene Subsidies in Africa: Over the last decade, there has been much written on petroleum product subsidies as international prices of oil experienced first lows, then highs. The rebound of petroleum prices had a direct effect on government policies on subsidies. Spikes in oil prices made government fuel subsidies in many countries grossly unaffordable. These countries do not have an exit strategy from public debt, and In order to weigh the benefits of subsidizing fuel, it is interesting to note that one IMF report showed that in Africa 45% of all kerosene subsidies accrue to the top two income quintiles. As international fuel 31 For Project Gaia studies on cooking in rural and village Brazil, see www.projectgaia.com. See also: http://www.projectgaia.com/files/BrazilPilotFinalReport0107.pdf. 32 Schlag, Nicolai & Zuzarte, Fiona. “Market Barriers to Clean Cooking Fuels in Sub-Saharan Africa: A Review of Literature”. Working Paper. Stockholm Environment Institute (SEI). April 2008. Page 11. 33 Schlag and Zuzarte. 2008. 34 Nwafor, Manson; Ogujiuba, Kannayo; Asogwa, Robert. “Does Subsidy Removal Hurt the Poor?” International Development Research Centre (IDRC). Feb 2006.

7‐12‐11 22

prices are on the rise, it is prudent to measure the success in fuel subsidies in reaching the “bottom of the pyramid”. Also, the international community has recently targeted the reform of fossil fuel subsidies as part of a larger effort to confront global warming.35 As seen in the Kenya example, Governments can play an effective role in subsidies, without inflating the prices of the fuel. In Kenya, the Government removed only the taxes from kerosene which rendered the fuel close enough to the price of charcoal to offer a competitive alternative. Many consumers in urban areas switched to kerosene, which by 2008 was used in 56% of all urban homes. The price of LPG is heavily weighted with taxes and distribution charges, which can account for 60% of the total fuel price, as experienced in Tanzania.

5. Discussion of competition with ethanol export market: how will this affect the domestic fuel market? What is the likelihood and impact of requirement for 5% of industrially distilled ethanol to be sold on domestic market? Is 35c per liter higher than world price for ethanol? In which case will it attract imports?

World Trade in Ethanol

World ethanol prices increased by more than 30% in 2010, driven by rising demand, by the current high price of sugar, by the impact of the high price of corn in the U.S., and by strong world energy, e.g. oil, prices. This situation contrasts sharply with 2007‐2008 when ethanol prices did not follow the pace of related commodity price increases and ethanol was down. It is always important to note that the world price of ethanol is cyclical and is influenced by factors unrelated to the cost of production, including oil prices, competition with sugar, feedstock prices and production in the dominant markets (Brazil and the U.S.) and rising demand. In 2010, the U.S. became for the first time a net exporter of ethanol, while exports from Brazil were down sharply in a context of high raw sugar prices, lower cane production and relatively more competition from corn‐based ethanol than in previous years36.

Madagascar’s Export Market

The export market for Madagascar’s ethanol is to the east, to China, India and the Asia‐Pacific region. The market is dominated by its region’s big players and is a different setting entirely than the market on the Atlantic side of Africa. Nor is Madagascar’s ethanol likely to find its way to Europe, unless to France.

35Coady, David; Gillingham, Robert; Ossowski, Rolando; Piotrowski, John; Tareq, Shamsuddin; and Tyson, Justin.“Petroleum Product Subsidies: Costly, Inequitable, and Rising”.Staff Position Note. International Monetary Fund (IMF). Feb 2010. 36 OECD-FAO Agricultural Outlook 2011-2020 – Biofuels. Available at: http://www.oecd.org/document/0/0,3746,en_36774715_36775671_47877696_1_1_1_1,00.html

7‐12‐11 23

Ethanol sold for export from Madagascar’s large distilleries will always sell for more than what the domestic price of ethanol should be. The regional commodity market is different from the domestic fuel market. The commodity market requires bulk or size to compete advantageously; it is cyclical, and it can be uneven and unpredictable. The domestic fuel market for ethanol, once firmly established, will be stable, predictable (influenced by forces within Madagascar), reliable and while not always as profitable for the producer as the export market, nevertheless profitable overall because it can sell ethanol well above the cost to produce it, and, moreover, adds value to the domestic economy, produces jobs, tax revenues and produces associated business revenues within the economy where it is being sold. For a large producer to be able to sell into both markets, the commodity market and the domestic fuel market, provides security and redundancy for the large producer.

If Madagascar’s large scale ethanol is being produced by Chinese owners for a dedicated market in China, it may be difficult to determine what the sale price of the ethanol to China really is. If the ethanol is going out on tender or on the spot market, it might sell for from $0.35 to $0.85/liter, bulk, depending on the time of year, the amount of ethanol for sale, its quality, and the contract negotiated. The Asia‐Pacific ethanol market is priced above other markets because India’s fuel blending program has increased regional demand and because there is increasing demand in China. As the hugely dominant consumers in the region, India and China are the drivers. A great deal of new capacity is coming on rapidly in China and throughout the region, which may stabilize or beat down ethanol prices37. After its spike in 2009‐2010, sugar prices are dropping and this will influence ethanol production and pricing in 2011‐2013. As noted above, the commodity price of ethanol is cyclical, as are all commodity prices, and this will remain true in this region, where the fate of ethanol traders is in the hands of dominant players. Pakistan is a significant producer in the region in its own right but much of Pakistan’s ethanol is traded west to the U.K.

According to F.O. Licht, some 2011 internationally traded ethanol prices are:

Chinese market: $1.04 to $1.08 per liter hydrous Thai market: $0.80 to $0.85 per liter anhydrous Brazil export: $0.70 to $0.76 U.S. Spot market sales: $0.71 to $0.7438

Madagascar’s Domestic Fuel Market

It is hoped that ethanol produced in the large distilleries could be put into the market for FOB plant $0.25 to $0.30. This is quite feasible if production costs are where they should be, once 37 Celanese, a U.S. chemical company, has a 200,000 annual ton ethanol-from-coal plant under construction in China. This is 250 million liters destined for chemical markets. (From F.O. Licht, see following citation.) 38 F.O. Licht’s World Ethanol and Biofuels Report, v. 9, No. 20, 22.6.11.

7‐12‐11 24

the plants are modernized and the plantations repaired and well managed. This could give ethanol a retail price of $0.35 per liter. The GOM can keep ethanol fuel price down by not charging excise tax or value added tax on the fuel. This need be only a temporary measure, designed to encourage ethanol fuel to take hold. It could be phased out in 5 years.

Five percent of industrial plant ethanol into the domestic market is not a lot of ethanol. For the foreseeable future, this would be something in the range of 2.5 million annual liters, sufficient to support about 7,000 stoves. While this is not a large amount of ethanol for the demand that will be created in the domestic market, it gives the GOM the opportunity to affect the local ethanol fuel market price; if the government is able to obtain a “tithing” of ethanol otherwise destined for export, at a price influenced or set by government, this could be used to create a benchmark price in the nascent ethanol stove fuel market, to which other producers, small or large, would be to some extent obliged to calibrate their pricing. The Government of Madagascar would be setting by example the price for ethanol fuel for cooking—high enough to be profitable, low enough to be affordable. It can also directly regulate prices, but direct market control could have undesirable consequences. By setting a benchmark, the government would encourage ethanol from other sources to meet or beat the $0.35 benchmark.

A requirement from the GOM to its industrial sugar and ethanol industry, undergoing privatization, to sell ethanol in the domestic market is not an unreasonable one, especially if a good market can be created. This requirement is in line with what other governments are considering and in some cases doing, including governments on the receiving end of trade—those of developed countries, which are putting in place sustainability criteria for imported ethanol39. These criteria generally include a requirement that some of the ethanol produced in the country of origin remain there to provide social and economic benefit. Off‐setting imported fuels or wood and charcoal does both. A requirement of 10% local share is quite reasonable.

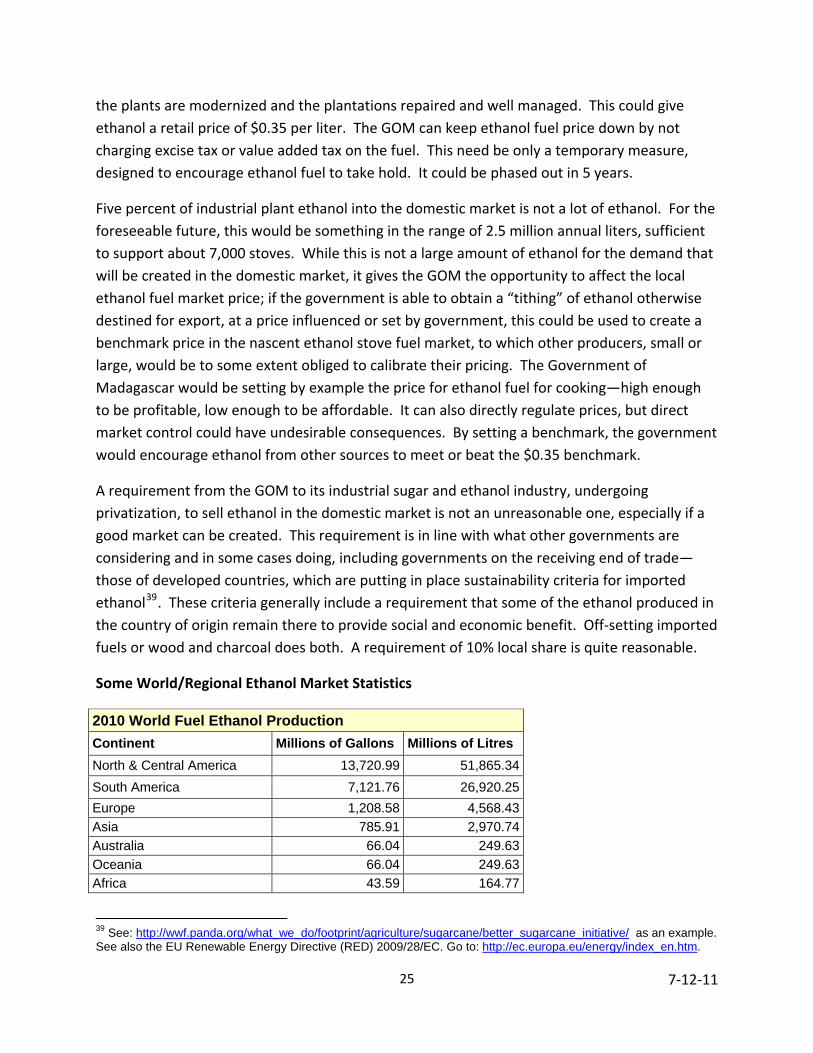

Some World/Regional Ethanol Market Statistics

2010 World Fuel Ethanol Production Continent Millions of Gallons Millions of Litres North & Central America 13,720.99 51,865.34South America 7,121.76 26,920.25Europe 1,208.58 4,568.43Asia 785.91 2,970.74Australia 66.04 249.63Oceania 66.04 249.63Africa 43.59 164.77

39 See: http://wwf.panda.org/what_we_do/footprint/agriculture/sugarcane/better_sugarcane_initiative/ as an example. See also the EU Renewable Energy Directive (RED) 2009/28/EC. Go to: http://ec.europa.eu/energy/index_en.htm.

7‐12‐11 25

Recent Ethanol Production Capacity Expansion (millions of gallons) Country 2010 2009 2008 2007 % Growth USA 13,230.00 10,600.00 9000 6498.6 204%Brazil 6,921.54 6577.89 6472.2 5019.2 138%European Union 1,176.88 1039.52 733.6 570.3 206%China 541.55 541.55 501.9 486 111%Canada 356.63 290.59 237.7 211.3 169%Thailand 435.2 89.8 79.2 549%Colombia 83.21 79.29 74.9 111%India 91.67 66 52.8 174%Australia 56.8 26.4 26.4 215%

In Thailand, ethanol production is expected to grow by 1.5 billion liters to reach 2.2 billion liters by 2020.

(OECD‐FAO 2011)

Source for both tables: F.O. Licht as presented by the Renewable Fuels Assoc. (RFA)40

Ethanol and biodiesel prices to 2020

The ethanol prediction is based on Brazilian ethanol Sao Paolo ex‐distillery.

The biodiesel price is the producer price in Germany, net of tariffs.

OECD‐FAO Agricultural Outlook 2011‐2020

Development of the World Ethanol Market (OECD‐FAO 2011)41

40 Available at: http://www.ethanolrfa.org/pages/statistics 41 OECD and FAO Secretariats. Available at http://dx.doi.org/10.1787/888932426467.

7‐12‐11 26

6. State role: importance of state in controlling illegal forest degradation, which will increase relative attractiveness of ethanol.

Beginning in the 1980s, the Government of Madagascar began promoting efforts to reverse environmental degradation and protect biodiversity and natural resources. The government has pursued this work in partnership with multi‐national donors, government agencies and non‐governmental organizations. The year 2008 marked the conclusion of the 15‐year National Environmental Action Plan (NEAP), the Malagasy state’s central effort to conserve the country’s forests and biodiversity42. The results of the environmental program, while uneven, have nevertheless been significant and have led to an approach to environmental action that may yet yield results: to put a greater emphasis on the link between rural poverty, environmental degradation and the need to develop livelihoods43.

Since 2009, the government has also been engaged with conservation NGOs in several “Reduced Emissions from Deforestation and Forest Degradation” (REDD) pilot projects led by a national working group. Both the NEAP and REDD projects represent Madagascar’s strategy for protecting the country’s forests and biodiversity.

The GOM has shown its predisposition for linking rural livelihoods and forest protection44. Obviously it is easier for the GOM to make the argument to its people for protection of forests if this can be linked to economic well being. The argument has been that populations that can derive their livelihood from the forest will, under the right circumstances, also protect the forest. There may in fact be an additional economic cause‐and‐effect argument to make. Farms and forests coexist in a tight economic and spatial relationship. If small farmers are able to prosper on land available to them around the forests, while the forests are themselves protected, then the pressures on forest resources may be lessened. This could be true not just in a general sense but also specifically, if agriculture is able to develop the capability to produce fuel rather than go to the forest for it.

There are studies about the relationship between agricultural productivity/prosperity and deforestation. These have been expressed in Environmental Kuznets Curves45. While it is 42 Freudenberger, Karen. 2010. Paradise Lost—Lessons from 25 Years of USAID Environment Programs in Madagascar, International Resource Group and USAID. 43Razafindralambo, G. and L. Gaylord. 2008. Madagascar : National Environmental Action Plan. In : PNDR. 2008. MfDR Principles in Action : Sourcebook on Emerging Good Practices, pp.75-82. (cf: www.mfdr.org/sourcebook )44 Winterbottom, Robert. 2005. Support Sustainable Environment and Forest Ecosystems Management in Madagascar – Report on an Action Plan to Improve Governance in the Forestry Sector. USAID. See Issues and Findings, pp 27. See also: Freudenberger, Karen. 2010. Discussions on Community Based Natural Resource Management, Integrated Conservation and Development Projects, REDD and Payments for Ecosystem Services, pps 48-65. 45 Bhattarai, Madhu S. 2004. Agricultural and Forest Landuse Changes, and the Environmental Kuznets Curve for Deforestation: Available at: http://www.fao.org/fileadmin/user_upload/rome2007/docs/Agriculture_Forest_Landuse_Changes.pdf.

7‐12‐11 27

beyond the scope of this response to examine those studies, it is enough to say that there may be evidence that healthy farm economies do better with forest protection than struggling farm economies. Better‐off farmers may make better environmental decisions. European, American and now the Brazilian farm economy might be cases in point, with recovery of forests advancing in each of these economies46.

Whether or not there is a strong enough case to be made for the link between prospering farmers and improved forest protection, or whether or not this dynamic would work for Madagascar, nevertheless, if forest protection and agricultural development are linked by regulations and programs—carrots and sticks—this could increase the likelihood of desired outcomes. Helping farmers to succeed and make money from their crops can be linked with their requirement to be good stewards. This requirement was established in the U.S. following the Great Depression, which saw both an economic and environmental collapse in American agriculture. Today, the majority of assistance programs available to small farmers in the U.S. are linked to environmental stewardship requirements—often specifically focused on water quality and revegetation (grasses) or reforestation47.

Micro distilleries could be part of a package that permits the farmer to do more with his or her land, plant different kinds of crops that are well suited for degraded soils needing to be restored, earn more from the crops produced and replace cash‐earning activities such as charcoal making and selling with ethanol fuel distillation. If farmers are able to add value to what they produce by processing it to higher value products, and sell it into a good cash market, this may remove the necessity of going to the forest to earn income.

Thus, farm enterprises may be made to help reduce deforestation. By linking farm scale development of ethanol fuel to specific forest stewardship actions, the results may be better. The link is organic; production and use of ethanol in place of woodfuels will help to reduce pressure on the forest, especially if some farmers and their families move away from charcoal production and sale to the production and sale of a cleaner, higher value fuel.

Strengthening the farm economy by giving farmers the know‐how and tools to produce ethanol fuel may thus be a good co‐strategy along with forest protection and enforcement. Giving farmers access to lucrative fuel markets with their planted crops creates a new and well paying opportunity for them. It is also a good employment generator. Because micro scale ethanol resembles, at least in scale, the way in which charcoal is made and sold, the transition from

46 Freudenberger, Karen. 2010. She reports on some failures in Integrated Conservation and Development Projects (ICDP) where farmers strengthened with economic development programs engaged in tavy, while poorer farmers did not. The lesson is that enforcement and accountability must be part of any ICDP or similar program. 47 US National Conservation District history, see: http://www.nacdnet.org/about/districts/history.phtml.

7‐12‐11 28

charcoal making to ethanol distilling may not be too big a leap. Some farmers will be able to make it. Some already have if they are operating a toaka gasy still.

Developing an alcohol fuel industry that is small scale, dispersed, relying on good agricultural practices and land use choices, is a cross‐cutting activity that touches many national development objectives. If employment can be created and money made with the responsible production and use of ethanol fuel, this offers a positive rather than an enforcement oriented (or negative) approach to diverting human demands away from the forests.

The need for clean cooking fuel can thus be used to strengthen forest protection programs. It can also be used to strengthen agriculture. Considering the health and quality of life benefits that derive from clean fuels and stoves, and the fact that ethanol fuel can underpin agricultural economic development and forest resource protection, the GOM should embrace the ethanol stove program as a way to pursue multiple objectives. This could be done within the context of the existing NEAP and REDD programs.

7‐12‐11 29