Embed Size (px)

Citation preview

Enterprise RiskManagement:Frameworks,Elements, andIntegration

Statement onManagementAccounting

FINANCE GOVERNANCE,RISK, AND COMPLIANCE

IMA® would like to acknowledge the work of William G. Shenkir, Ph.D., CPA, and

Paul L. Walker, Ph.D., CPA, both of the McIntire School of Commerce, University of

Virginia who were the authors of this SMA. Thanks also go to Patrick Stroh of

UnithedHealth Group and Jeff Thomson, CMA, of IMA who served as reviewers and

Raef Lawson, Ph.D., CMA, CPA, of IMA who serves as series editor.

Published by

Institute of Management Accountants

10 Paragon Drive, Suite 1

Montvale, NJ 07645

www.imanet.org

Copyright © 2011 by

Institute of Management Accountants

All rights reserved

Enterprise Risk Management

2

TABLE OF CONTENTS

I. Rationale . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4II. Defining Risk and ERM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4III. Scope . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 IV. Total Risk Classification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 V. The Role of the Management Accountant . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6VI. ERM Frameworks: A Global Perspective . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

The Combined Code and Turnbull Guidance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8King II Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8A Risk Management Standard by Federation of European Risk Management Association (FERMA). . . . . . . 8Australian/New Zealand Standard 4360—Risk Management. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8 COSO’s Enterprise Risk Management—Integrated Framework . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9IMA’s “A Global Perspective on Assessing Internal Control over Financial Reporting” . . . . . . . . . . . . . . . . . . . 10Basel II . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12Standard & Poor’s and ERM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

VII. ERM Foundational Elements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12Organizational Context . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Tone at the Top . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12Risk Management Philosophy and Risk Appetite. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12Integrity and Ethical Values. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13Scope and Infrastructure for ERM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Basic Components of ERM Framework . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13Set Strategy and Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13Identify Risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14Assess Risks. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Treat and Control Risks. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Communicate and Monitor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

VIII. Integrating ERM into Ongoing Management Activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20Strategic Planning . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20Balanced Scorecard . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21Budgeting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22Total Quality Management and Six Sigma . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23Business Continuity (Crisis Management) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23Corporate Governance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24The Board and Stock Exchanges . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24Risk Disclosures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Proxy Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24Management’s Discussion and Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2410-K Item 1A—Risk Factor Disclosure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25 Other Voluntary Disclosures. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

IX. Transitioning from SOX to ERM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25X. Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Glossary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26Bibliography . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

TABLE OF EXHIBITS

Exhibit 1: Evolution of Risk Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Exhibit 2: COSO Enterprise Risk Management Framework . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Exhibit 3: COSO Enterprise Risk Components . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Exhibit 4: Core Components of a Risk-Based Approach. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Exhibit 5: A Continuous Risk Management Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Exhibit 6: Risk Identification Techniques . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Exhibit 7: Risk Quantitative and Qualitative Techniques . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Exhibit 8: Subjective Assessment of Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Exhibit 9: Risk Map . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Exhibit 10: Detailed Risk Map . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Exhibit 11: Color-Coded Risk Map . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Exhibit 12: Functional Risk Assessment Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Exhibit 13: Linking Objectives, Events, Risk Assessment, and Risk Response . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Exhibit 14: Strategy, the Balanced Scorecard, and the Budget . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Exhibit 15: Balanced Scorecard and Strategic Risk Assessment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Exhibit 16: Risk/Crisis Acceleration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

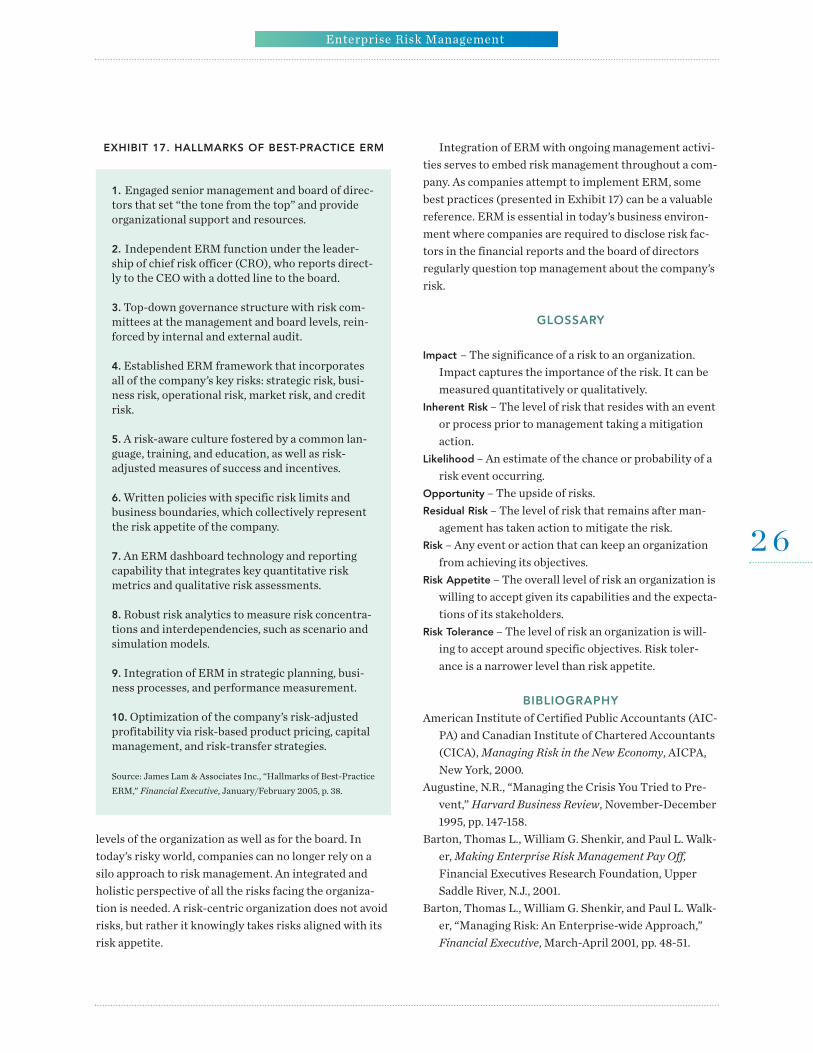

Exhibit 17: Hallmarks of Best-Practice ERM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Enterprise Risk Management

3

I. RATIONALELeadership is about making a difference. If leaders of

organizations in the 21st Century are to make a differ-ence and grow their organizations to greatness, theymust have the capability to navigate in a very risky anddangerous world. Thus, understanding and managing riskhas become imperative for successful leadership oforganizations in today’s world.

A variety of risks confront organizations today, andany one of them could threaten an organization’s successand ultimately lead to a decrease in stakeholder value.The need for greater risk awareness by leaders is drivenby much more than just terrorism. Forces such as global-ization and the geopolitical environment in which organ-izations operate add complexity to business, therebyincreasing risks. Technology and the Internet requirecompanies to rethink their business models, core strate-gies, and target markets. Customers have ever-increasingdemands for customized products and services leading tomore risks. If customer expectations are not met, marketshare and, ultimately, revenue and profits can be signifi-cantly and quickly impacted. Organizations must alsocomply with increased regulations in some cases andderegulation in others, both of which drive risks. Mergersand restructurings are causing organizations to downsizeand undergo changes in management responsibilities,which also creates the potential for enterprise risks. Another important driver for more attention to risk

management is the accounting and reporting deficien-cies, such as unjustified revenue recognition and convo-luted business transactions as found in special purposeentities and backdating of stock options. More complexfinancial instruments such as derivatives are also part ofthe reality today, requiring greater understanding of therisks embedded in such instruments. Given all of theseforces, leaders must have a heightened state of awarenessof the necessity for holistic risk management and for astronger governance structure for their organization.Well-managed organizations have always had some

focus on risk management, but typically it has been on anexposure-by-exposure basis through various risk man-agement silos. For example, the treasury function focuseson risks emanating from foreign currencies, interestrates, and commodities—so called financial risks. Anorganization’s insurance group focuses on hazard riskssuch as fire and accidents. Operating management looksafter various operational risks, and the information tech-

nology group is concerned with security and systemsrisks. The accounting and internal audit function focuseson risks caused by inadequate internal controls andtrends in performance indicators. The general assump-tion is that executive management has their eyes on thebig picture of strategic risks facing the enterprise in theshort term and over the life of the strategic plan. As organizations grow in complexity and serve global

markets, the leadership challenge is to fully understandhow the various organizational units interact and relateand, in turn, how the risks cut across the silos. Instead ofmanaging risk in many individual silos, enterprise riskmanagement (ERM) takes an integrated and holistic per-spective on risks facing an organization. Risk-centricleadership does not mean that the organization will berisk adverse, but that it strives to identify, assess, andmanage risks. When taking risks, the leadership does sointentionally rather than unknowingly. The key is to takecalculated risks across the enterprise and appropriatelymanage and mitigate the risks for the benefit of thestakeholders.

II. DEFINING RISK AND ERMOrganizations are confronted by events that affect the

execution of their strategies and achievement of theirobjectives. These events can have a negative impact(risks), a positive impact (opportunities), or a mix of bothrisk and opportunity. In the 2004 publication EnterpriseRisk Management—Integrated Framework: ExecutiveSummary Framework, the Committee of SponsoringOrganizations of the Treadway Commission (COSO) stat-ed that ERM is: • “A process, ongoing and flowing through an entity• Effected by people at every level of an organization• Applied in strategy setting• Applied across the enterprise, at every level andunit, and includes taking an entity-level portfolioview of risk

• Designed to identify potential events that, if theyoccur, will affect the entity and to manage risk with-in its risk appetite

• Able to provide reasonable assurance to an entity’smanagement and board of directors

• Geared to achievement of objectives in one or moreseparate but overlapping categories.”

Several points to emphasize from this broad defini-

Enterprise Risk Management

4

tion include:• Risk management should be viewed as a core competency; and

• It is part of everyone’s job—whether at the level ofsetting the organization’s strategy, a unit’s objec-tives, or running the daily operations.

Organizations seek to create value for their stakehold-ers, and ERM is implemented with that goal in mind.Accordingly, ERM is:a structured and disciplined approach: It aligns strategy,

processes, technology, and knowledge with the pur-

pose of evaluating and managing the uncertainties the

enterprise faces as it creates value.…It is a truly holis-

tic, integrated, forward-looking, and process-oriented

approach to managing all key business risks and

opportunities—not just financial ones—with the intent

of maximizing shareholder value as a whole.

The authors of this Statement on ManagementAccounting (SMA) have stated in previous publicationsthat the goal of ERM is “to create, protect, and enhanceshareholder value by managing the uncertainties thatcould either negatively or positively influence achieve-ment of the organization’s objectives.” Given that ERM isapplicable to all types of organizations, as noted below,some might prefer to use the term “stakeholder value” inthis definition instead of “shareholder value.”

III. SCOPEThis SMA provides an overview of the ERM process

and frameworks. ERM frameworks can be adapted to fit the specifics of the organization’s culture and can beimplemented in large or small organizations, service or manufacturing businesses, profit, not-for-profit, or private entities. The information in this SMA provides management

accountants and others interested in implementing ERMwith:• A definition of ERM;• A classification of various risks;• An understanding of the roles and responsibilitiesof management accountants in ERM projects;

• An overview of ERM frameworks from several dif-ferent professional organizations around the world;

• A discussion of the foundational elements of ERM;• Suggestions of how ERM can enhance on-goingmanagement activities; and

• Ideas for adding value to the Sarbanes-Oxley (SOX)

404 compliance requirement by employing a risk-based approach to identify, test, and document keyinternal controls to assure investors on the quality ofthe firm’s financial statements and related disclosures.

The information in this SMA provides an overview foran organization considering implementation of ERM.This document is not intended to provide a comprehen-sive discussion of ERM. Other sources, such as thoseidentified in the bibliography, should also be consulted.

IV. TOTAL RISK CLASSIFICATIONTaking the perspective of the total entity, risks may be

classified in a variety of risk frameworks. One frequentlyused framework is:• Strategic Risk: examples include risks related tostrategy, political, economic, regulatory, and globalmarket conditions; also could include reputationrisk, leadership risk, brand risk, and changing cus-tomer needs.

• Operational Risks: risks related to the organization’shuman resources, business processes, technology,business continuity, channel effectiveness, cus-tomer satisfaction, health and safety, environment,product/service failure, efficiency, capacity, andchange integration.

• Financial Risks: includes risks from volatility in for-eign currencies, interest rates, and commodities;also could include credit risk, liquidity risk, andmarket risk.

• Hazard Risk: risks that are insurable, such as naturaldisasters; various insurable liabilities; impairmentof physical assets; terrorism.

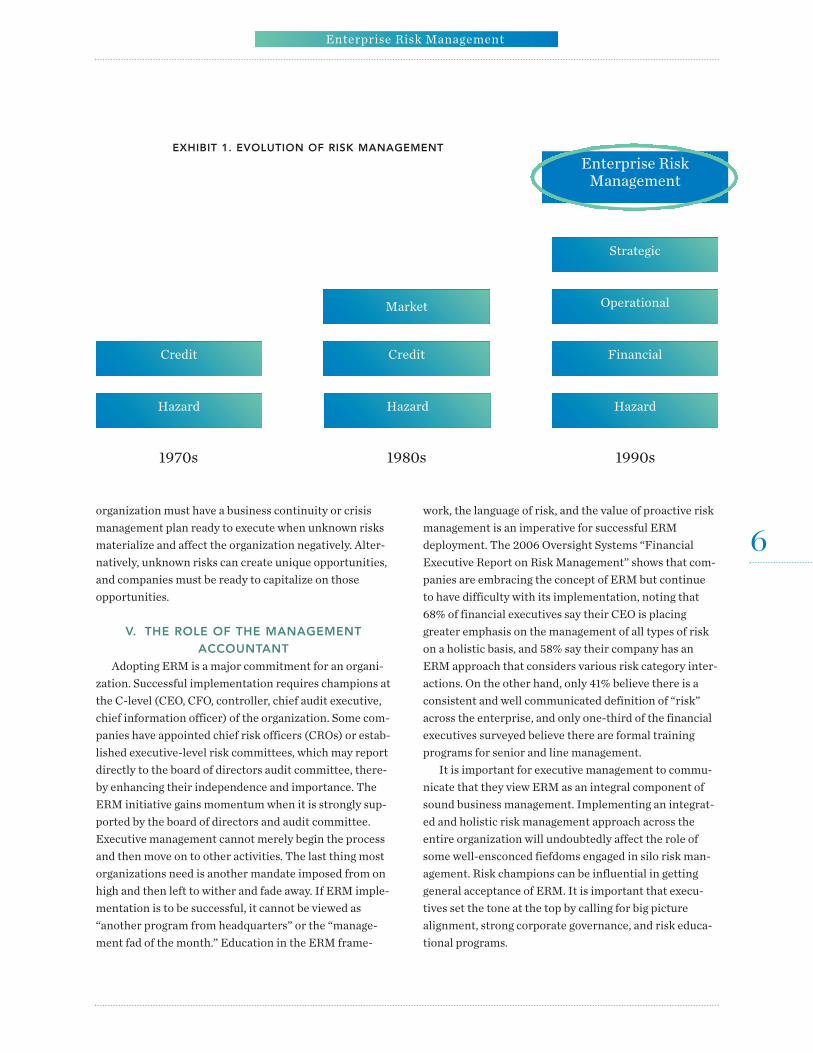

As noted in Exhibit 1: Evolution of Risk Management,traditional risk management generally focused on finan-cial risk and hazard risk. Approaching risk from an enter-prise-wide perspective began to be considered andimplemented in the 1990s. This holistic risk approachshould enable management to identify most of the keyrisks that confront the organization. Implementing ERM,however, does not mean that an organization will be ableto anticipate every risk that could result in loss of stake-holder value. The limitation of ERM is captured in theaphorism: “There are known knowns, known unknowns,and unknown unknowns.” In the ERM process, knownrisks will be identified, and some previously unknownrisks will become known. Even with a robust process,however, some unknown risks will not be identified. The

Enterprise Risk Management

5

organization must have a business continuity or crisismanagement plan ready to execute when unknown risksmaterialize and affect the organization negatively. Alter-natively, unknown risks can create unique opportunities,and companies must be ready to capitalize on thoseopportunities.

V. THE ROLE OF THE MANAGEMENTACCOUNTANT

Adopting ERM is a major commitment for an organi-zation. Successful implementation requires champions atthe C-level (CEO, CFO, controller, chief audit executive,chief information officer) of the organization. Some com-panies have appointed chief risk officers (CROs) or estab-lished executive-level risk committees, which may reportdirectly to the board of directors audit committee, there-by enhancing their independence and importance. TheERM initiative gains momentum when it is strongly sup-ported by the board of directors and audit committee.Executive management cannot merely begin the processand then move on to other activities. The last thing mostorganizations need is another mandate imposed from onhigh and then left to wither and fade away. If ERM imple-mentation is to be successful, it cannot be viewed as“another program from headquarters” or the “manage-ment fad of the month.” Education in the ERM frame-

work, the language of risk, and the value of proactive riskmanagement is an imperative for successful ERMdeployment. The 2006 Oversight Systems “FinancialExecutive Report on Risk Management” shows that com-panies are embracing the concept of ERM but continueto have difficulty with its implementation, noting that68% of financial executives say their CEO is placinggreater emphasis on the management of all types of riskon a holistic basis, and 58% say their company has anERM approach that considers various risk category inter-actions. On the other hand, only 41% believe there is aconsistent and well communicated definition of “risk”across the enterprise, and only one-third of the financialexecutives surveyed believe there are formal trainingprograms for senior and line management.It is important for executive management to commu-

nicate that they view ERM as an integral component ofsound business management. Implementing an integrat-ed and holistic risk management approach across theentire organization will undoubtedly affect the role ofsome well-ensconced fiefdoms engaged in silo risk man-agement. Risk champions can be influential in gettinggeneral acceptance of ERM. It is important that execu-tives set the tone at the top by calling for big picturealignment, strong corporate governance, and risk educa-tional programs.

Enterprise Risk Management

6

Enterprise Risk Management

Strategic

Operational

Financial

HazardHazardHazard

Credit Credit

Market

1970s 1980s 1990s

EXHIBIT 1. EVOLUTION OF RISK MANAGEMENT

The management accountant can make major contri-butions to moving the organization from silo risk man-agement (or no meaningful risk management process atall) to an integrated and holistic approach. In the migra-tion from a counter of wealth to assisting in the creationof wealth (i.e., independent strategic business partner),the management accountant in the “new” era of thefinance organization is increasingly being asked to serveon, if not lead, cross-functional teams to implement criti-cal enterprise-wide initiatives. ERM provides a wealth ofopportunities for the management accountant to helpimplement a disciplined, systematic process to maximizethe value of the enterprise. Some specific activities wherethe skills and competencies of the management account-ing professional can be useful in ERM implementationinclude:• Serve as a champion for ERM, supporting thechange from risk management in silos to ERM;

• Help to resolve conflict between supporters of ERMand traditional risk management approaches;

• Educate others in the organization of the ERMprocess;

• Provide expertise to operational management onthe organization’s ERM framework and process;

• Serve on cross-functional and diverse ERM committees;

• Assist executive and operational management inanalyzing and quantifying the organization’s riskappetite and risk tolerances for individual units;

• Assist in implementing ERM within the financefunction;

• Provide information to operational management toassist in risk identification;

• Perform benchmarking studies for use in risk identification;

• Gather best practice information on ERM;• Assist in quantifying impact and likelihood of indi-vidual risk on risk maps;

• Assist in identifying and estimating costs and bene-fits of various risk mitigation alternatives, andcoach management in responding to risks;

• Design reports to monitor risks and develop finan-cial and nonfinancial metrics to evaluate the effec-tiveness of risk mitigation (treatment) actions;

• Advise management on integrating ERM with thebalanced scorecard and budgeting process;

• Participate in development of business continuity

(crisis management) plans;• Advise on risk disclosures in the SEC Form 10-Kand the annual report;

• Serve as a champion for strong corporate gover-nance incorporating ERM; and

• Coach management on the value of extending SOX404 compliance to encompass ERM, including busi-ness process owners and other operational func-tions conducting a holistic assessment of risksimpacting achievement of their business objectives.

Once executive management has decided to embarkon implementing ERM, it is in the enlightened self- interest of management accountants to do what they canto keep the project moving. An effective ERM implemen-tation provides a context for management accountants toperform their duties and responsibilities knowing thatpeople at all levels of the organization are aware of riskwhile doing their work and are held accountable for howthey manage risks.

VI. ERM FRAMEWORKS: A GLOBAL PERSPECTIVE

ERM is a globally accepted and growing field. As aresult, a number of risk frameworks and statements havebeen published by professional organizations around theworld. Some of the publications urge businesses to usethese frameworks. Other risk frameworks have a “complyor explain why not” approach. Still other frameworks arelegally mandated or implied in their respective country.Some of the documents were written by guidance-settingorganizations such as COSO, while others were writtenby individuals with a wide range of backgrounds, includ-ing insurance, government, safety, and engineering. Thedifferent backgrounds lead to very different approachesin these risk frameworks. Some lean toward financialreporting and internal control, and others lean towardmanagement, corporate governance, and accountability.Ambitiously, some even try to cover every possible aspectof risk. Still, enterprise risk management frameworks arevaluable tools. They usually provide a diagram orapproach that includes the steps necessary for ERMimplementation in addition to providing guidance andexamples. In this section, the following ERM frameworksare briefly discussed:• The Combined Code and Turnbull Guidance• King II Report• A Risk Management Standard by the Federation of

Enterprise Risk Management

7

European Risk Management Association (FERMA)• Australian/New Zealand Standard 4360—RiskManagement

• COSO’s Enterprise Risk Management—IntegratedFramework

• IMA’s “A Global Perspective on Assessing InternalControl over Financial Reporting” (ICoFR)

• Basel II• Standard & Poor’s and ERM

THE COMBINED CODE AND TURNBULL GUIDANCE

In the United Kingdom, the Financial ReportingCouncil published the Combined Code on Corporate Gov-ernance (the Code) in 2003. Although the Code is notspecifically labeled as an ERM framework, it does havemany similar aspects, and “risk” is mentioned more than100 times. The Code states that the role of the board is toprovide a framework of effective control so that risk isassessed and managed. The board is also required toreview the effectiveness of controls, including all controlsover financial, operational, and compliance areas as wellas risk management systems.In 2005, the Financial Reporting Council also pub-

lished Internal Control—Revised Guidance for Directorson the Combined Code, which is a revision of the Turnbullreport first published in 1999. This guidance assumesthat a company’s board uses a risk-based approach tointernal control. The guidance suggests that to assess acompany’s risk and control processes, the following ele-ments must be reviewed: • Risk assessment;• Control environment and control activities;• Information and communication; and• Monitoring.The guidance offers sample questions that could be

used to assess the effectiveness of risk and controlprocesses. Questions related to risk assessment focus onthe presence of clear objectives, effective direction onrisk assessment, measurable performance targets, identi-fication and assessment of all risks on an ongoing basis,and a clear understanding of acceptable risks.

KING II REPORT

The King Report on Corporate Governance for SouthAfrica (King II Report) was published in 2002 to promotecorporate governance. This report has five sections:• Board and directors;

• Risk management;• Internal audit;• Integrated sustainability reporting; and• Accounting and auditing.The King II Report also includes an appendix on “risk

management and internal controls.”According to this report, the board is responsible for

the risk management process and its effectiveness. Theboard should:• Set risk strategy policies;• Assess the risk process;• Assess the risk exposures, such as physical andoperational risks, human resource risks, technologyrisks, business continuity and disaster recovery,credit and market risks, and compliance risks;

• Review the risk management process and signifi-cant risks facing the company; and

• Be responsible for risk management disclosures.

A RISK MANAGEMENT STANDARD BY FEDERATION

OF EUROPEAN RISK MANAGEMENT ASSOCIATION

(FERMA)

A consortium of U.K. organizations, including theInstitute of Risk Management, the Association of Insur-ance and Risk Managers, and the National Forum forRisk Management in the Public Sector, published A RiskManagement Standard (RMS) in 2004. The RMS repre-sents best practices that companies can compare them-selves against to determine how well they are doing in theprescribed areas. It is not a lengthy document, but it doesprovide a risk management process, which includes:• Linkage to the organization’s strategic objectives;• Risk assessment, which the RMS breaks down intorisk analysis, risk identification, risk description,risk estimation, and risk evaluation;

• Risk reporting;• Decision;• Risk treatment;• Residual risk reporting; and • Monitoring.

AUSTRALIAN/NEW ZEALAND STANDARD 4360—

RISK MANAGEMENT

Australia and New Zealand formed a joint technicalcommittee composed of representatives from numerousorganizations to publish two documents on risk manage-ment in 2004. The committee is diverse and includes

Enterprise Risk Management

8

groups that focus on computers, customs, insurance,defense, emergency management, safety, securities, andaccounting, among many others. This diverse backgroundleads to a different approach than is seen in other frame-works. The first document, initially published in 1999, istitled Risk Management (the Standard). The second com-panion document, Risk Management Guidelines (the Guid-ance), provides insights on implementing the Standard. The Standard can be applied to any type of organiza-

tion and to any project or product. It attempts to factor inboth the upside and downside of risk. Although the Stan-dard specifies the elements of risk management, it is notintended to enforce uniformity. Its objective is to provideguidance in several areas, some of which are: a basis fordecision making, better risk identification, gaining value,resource allocation, improved compliance, and corporategovernance. The Standard’s risk management processincludes establishing the context, identifying risks, ana-lyzing risks, evaluating risks, and treating risks. The Guidance document elaborates on each element

of the risk management process. For example, for the

step “establishing the context,” the commentary focuseson understanding an organization’s objectives and itsexternal and internal stakeholders. As another example,the Guidance provides commentary on “criteria” forestablishing the context, which include the kinds of con-sequences and the definition of likelihood. The commen-tary on criteria further includes detailed case examples ofcriteria and the related objectives.

COSO’S ENTERPRISE RISK MANAGEMENT—

INTEGRATED FRAMEWORK

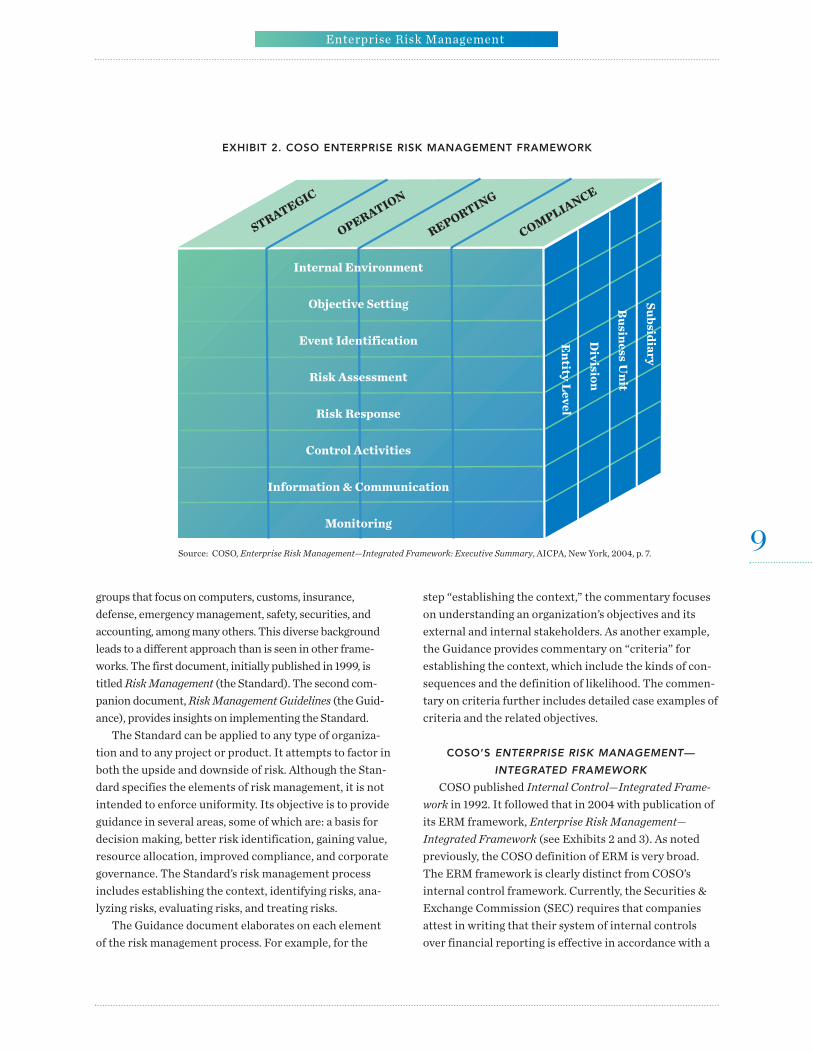

COSO published Internal Control—Integrated Frame-work in 1992. It followed that in 2004 with publication ofits ERM framework, Enterprise Risk Management— Integrated Framework (see Exhibits 2 and 3). As notedpreviously, the COSO definition of ERM is very broad.The ERM framework is clearly distinct from COSO’sinternal control framework. Currently, the Securities &Exchange Commission (SEC) requires that companiesattest in writing that their system of internal controlsover financial reporting is effective in accordance with a

Enterprise Risk Management

9

Subsidiary

Bu

siness U

nit

Division

En

tity Level

Internal Environment

Objective Setting

Event Identification

Risk Assessment

Risk Response

Control Activities

Information & Communication

Monitoring

STRATEGIC

OPERATION

R

EPORTING

COMPLIANCE

EXHIBIT 2. COSO ENTERPRISE RISK MANAGEMENT FRAMEWORK

Source: COSO, Enterprise Risk Management—Integrated Framework: Executive Summary, AICPA, New York, 2004, p. 7.

“suitable” framework such as COSO’s 1992 internal con-trol framework. Interestingly, the 2004 COSO ERM guid-ance is arguably more suitable for achieving the SEC’sgoal of developing and deploying “top-down, risk-based”management assessment guidance that helps lower thecosts associated with SOX 404 compliance. The COSOERM framework notes that internal control is a part ofERM.The COSO ERM framework has eight interrelated

components (see Exhibit 3). According to COSO’s ERMframework, internal environment refers to the tone ofthe organization, its risk appetite, and elements such asoversight by the board. The framework states that com-panies must set objectives at the strategic level and mustidentify the risks and opportunities that impact the enti-ty. Risks must then be assessed, and a response to the riskmade—avoidance, reduction, sharing, or possibly accept-ance. Clearly, COSO’s ERM framework is one of the most

comprehensive frameworks. COSO also published a volume of application tech-

niques to supplement the framework. This documentprovides examples to assist companies in implementingERM. For example, the application techniques related tothe internal environment component show sample riskmanagement philosophy statements and illustrativecodes of conduct. Other examples are given for each ofthe framework’s components.

IMA’S “A GLOBAL PERSPECTIVE ON ASSESSING

INTERNAL CONTROL OVER FINANCIAL

REPORTING”

IMA developed a risk-based framework to assist com-pany management in better cost-effective compliancewith SOX 404 requirements. Titled “A Global Perspectiveon Assessing Internal Control over Financial Reporting”(ICoFR), it includes self-assessments by CFOs and busi-

Enterprise Risk Management

1 0

INTERNAL ENVIRONMENTRisk Management Philosophy – Risk Appetite – Board of Directors – Integrity and Ethical Values – Commitment to Competence –

Organizational Structure – Assignment of Authority and Responsibility – Human Resource Standards

OBJECTIVE SETTINGStrategic Objectives – Related Objectives – Selected Objectives – Risk Appetite – Risk Tolerances

EVENT IDENTIFICATIONEvents – Influencing Factors – Event Identification Techniques –

Event Interdependencies – Event Categories – Distinguishing Risks and Opportunities

RISK ASSESSMENTInherent and Residual Risk – Establishing Likelihood and Impact – Data Sources –

Assessment Techniques – Event Relationships

RISK RESPONSEEvaluating Possible Responses – Selected Responses – Portfolio View

CONTROL ACTIVITIESIntegration with Risk Response – Types of Control Activities – Policies and Procedures –

Controls Over Information Systems – Entity Specific

INFORMATION AND COMMUNICATIONInformation – Communication

MONITORINGOngoing Monitoring Activities – Separate Evaluations – Reporting Deficiencies

Source: COSO, Enterprise Risk Management—Integrated Framework: Executive Summary, AICPA, New York, 2004, p. 2.

EXHIBIT 3. COSO ENTERPRISE RISK COMPONENTS

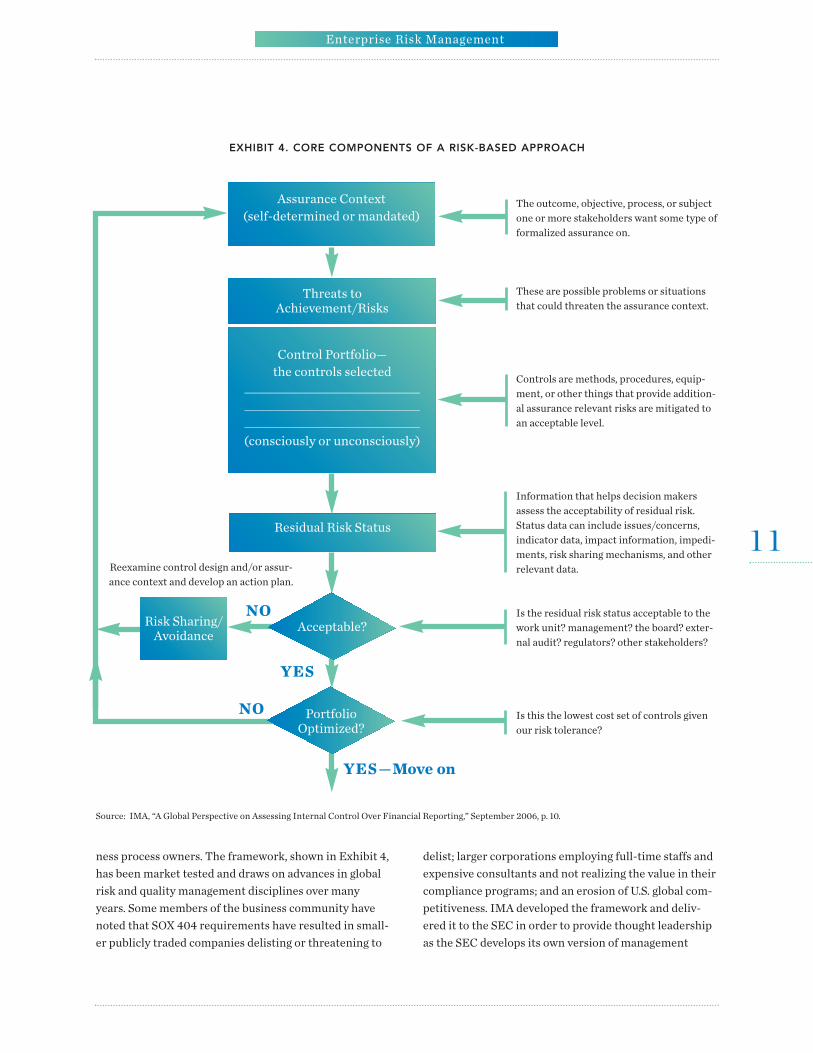

ness process owners. The framework, shown in Exhibit 4,has been market tested and draws on advances in globalrisk and quality management disciplines over manyyears. Some members of the business community havenoted that SOX 404 requirements have resulted in small-er publicly traded companies delisting or threatening to

delist; larger corporations employing full-time staffs andexpensive consultants and not realizing the value in theircompliance programs; and an erosion of U.S. global com-petitiveness. IMA developed the framework and deliv-ered it to the SEC in order to provide thought leadershipas the SEC develops its own version of management

Enterprise Risk Management

1 1

The outcome, objective, process, or subjectone or more stakeholders want some type offormalized assurance on.

These are possible problems or situationsthat could threaten the assurance context.

Controls are methods, procedures, equip-ment, or other things that provide addition-al assurance relevant risks are mitigated toan acceptable level.

Information that helps decision makersassess the acceptability of residual risk. Status data can include issues/concerns,indicator data, impact information, impedi-ments, risk sharing mechanisms, and otherrelevant data.

Is the residual risk status acceptable to thework unit? management? the board? exter-nal audit? regulators? other stakeholders?

Is this the lowest cost set of controls givenour risk tolerance?

Assurance Context(self-determined or mandated)

Threats to Achievement/Risks

Control Portfolio—the controls selected

__________________________________________________________________________________________(consciously or unconsciously)

Residual Risk Status

Acceptable?Risk Sharing/Avoidance

PortfolioOptimized?

Reexamine control design and/or assur-ance context and develop an action plan.

YES

YES—Move on

NO

NO

EXHIBIT 4. CORE COMPONENTS OF A RISK-BASED APPROACH

Source: IMA, “A Global Perspective on Assessing Internal Control Over Financial Reporting,” September 2006, p. 10.

assessment guidance, which many hope will address theimplementation issues associated with SOX 404 compli-ance in the more than three years since the Sarbanes-Oxley Act was passed. ICoFR heavily relies on advances in global risk man-

agement, including how to “treat” risks once an “assur-ance context” has been established with appropriatebusiness objectives. The assurance context as it relates toSOX 404 is materially fault-free financial statementsenabled by an effective system of internal controls. Therisk-based framework works equally well with other busi-ness contexts/applications, however, such as businesscontinuity planning, operations management, and costoptimization. The ICoFR framework also relies on tradi-tional Total Quality Management (TQM) principles. Forexample, once the assurance context has been establishedand the initial control portfolio is selected to address“threats to achievement” of objectives, the residual riskthat remains is quantifiable (e.g., by analysis of historicalerror rates) and tested against preestablished bounds.This helps determine if the risk is acceptable or not.

BASEL II

The Basel Committee on Banking Supervision updat-ed its original Basel Accord with Basel II and its relatednew framework. The framework is designed to improvethe international banking system and make it stronger.The framework is focused on maintaining consistent cap-ital adequacy requirements among banks. A key ideabehind the framework is that banks should match capitalto the actual level of risks and to set minimum capitallevels. The framework applies to “internationally activebanks” and has three pillars: minimum capital require-ments, supervisory review, and market discipline.

STANDARD & POOR’S AND ERM

Standard & Poor’s (S&P) has already started to incor-porate a company’s ERM practice into the S&P rating ofthe company. S&P currently applies this rating to bothfinancial institutions and insurers. Its framework forevaluating ERM at banks includes a review of ERM poli-cies, ERM infrastructure, and ERM methodology. ERMpolicies should address risk culture, appetite, and strate-gy; control and monitoring; and disclosure and aware-ness. ERM infrastructure covers risk technology,operations, and risk training. ERM methodology refers tocapital allocation, model vetting, and valuation methods.

The framework for evaluating insurers includes anassessment of risk management culture, risk controls,emerging risk management, risk and capital models, andstrategic risk management. S&P rates an insurer as weak,adequate, strong, or excellent. An adequate rating wouldmean an insurer has “fully functioning risk control sys-tems in place for all major risks.”

VII. ERM FOUNDATIONAL ELEMENTSThe essential components of most ERM frameworks

are similar. They differ in the language used to describethe components in the ERM process as well as in thenumber of specific steps. In implementing ERM, a com-pany may want to adapt a generic framework to fit its cul-ture, management philosophy, capabilities, needs,industry, and size. This section discusses the organiza-tional context for ERM and the basic components in ageneric ERM framework.

ORGANIZATIONAL CONTEXT

An effective ERM implementation requires an organi-zational context that includes: • Tone at the top;• Risk management philosophy and risk appetite;• Integrity and ethical values; and• Scope and infrastructure for ERM.

Tone at the TopA necessary condition for effective ERM implementa-

tion is the tone set by the board of directors and top man-agement, who are ultimately responsible for riskmanagement. A board with a majority of independentdirectors should regularly seek executive management’sresponses to these questions: “What are the company’stop risks? What is their time horizon? And what is beingdone to manage them?” The board discussion aroundthese questions sends a message to top management thatthe board recognizes that any organization is vulnerableto risk, and they expect top management to maintain aneffective risk management process. In turn, the impor-tance that top management places on effective ERM inits decisions sends a message to the entire organization.Again, if the organization’s risk committee and chief riskofficer report directly to the audit committee of theboard of directors, this signals the importance of ERM.

Risk Management Philosophy and Risk AppetiteThe core of a company’s risk management philosophy

Enterprise Risk Management

1 2

is how it views risks and considers them when makingdecisions. Management seeks to create value by growingthe company, and the risk management philosophyserves as a control over which risks are acceptable in pur-suing growth opportunities. An organization usually can-not pursue all the numerous opportunities for growththat may be envisioned and must choose those that fallwithin its risk appetite and tolerance.An organization’s risk management philosophy is

manifested in its risk appetite, which reflects how muchrisk the company can optimally handle given its capabili-ties and the expectation of its various stakeholders. Thecompany’s capabilities in terms of the core competenciesof its people, technology, and capital are key determi-nants of the amount of risk it can accept overall relativeto business and stakeholder objectives. The company’srisk appetite influences its culture, strategic decisions,and operating style. The company’s stakeholders—share-holders, executives, employees, and others—have expec-tations concerning the organization’s appropriateamount of risk, and, thus, they also influence the settingof the risk appetite. Companies should understand andbe fully aware of the risk appetite of all stakeholders ifthey wish to deliver optimal results.While risk appetite is a broad, entity-wide concept,

risk tolerance has a narrower focus. An organization mayhave different risk tolerances for its various operatingunits, but when the individual risk tolerances are com-bined, they should fall within the overall risk appetite setby top management and the board. This is the essence ofERM, which is an integrated, holistic view of risks, incontrast with a silo approach to risk management. Addi-tionally, risk mitigation under ERM takes an enterpriseperspective rather than inefficiently mitigating risksindependently.

Integrity and Ethical ValuesManagement’s uncompromising commitment to

integrity and ethical behavior in all areas of decisionmaking are prerequisites to implementing effective ERM.If employees sense that management is cutting cornersand not setting an example for acceptable behavior, theywill likely follow suit and develop the same attitude aboutright and wrong, putting the organization’s reputation atrisk. An organization’s reputation takes years to build butcan be diminished quickly by unethical behavior. Reputa-tion risk is recognized as one of the major risks that

organizations must manage proactively. Formal codes of conduct that are constantly rein-

forced through training programs serve to set boundariesfor all employees as to what is unacceptable behavior.Under SOX, the SEC was directed to set rules that requirea company to disclose if it has adopted a code of ethics orexplain why it does not. This disclosure requirementenhances the internal environment supporting ERMimplementation.

Scope and Infrastructure for ERMIn launching an ERM initiative, the scope of the effort

should be stated clearly. Some organizations initially rollout their ERM effort in a specific operating unit andbeta-test the framework they are using before imple-menting it across the company. In addition, a decisionmust be made on the risk infrastructure from a gover-nance and leadership accountability perspective. Will theeffort be overseen by a chief risk officer (CRO), the CFO,an ERM advisory committee, or some combination? ACRO supported by a cross-functional risk advisory com-mittee is one approach. Regardless of the approach, risksidentified are owned by the operating units, not the CROor a risk committee. Also, the ERM effort will not succeedwithout champions at the C-level supporting the riskinfrastructure and a major, enterprise-wide educationeffort on the ERM methodology.

BASIC COMPONENTS OF ERM FRAMEWORK

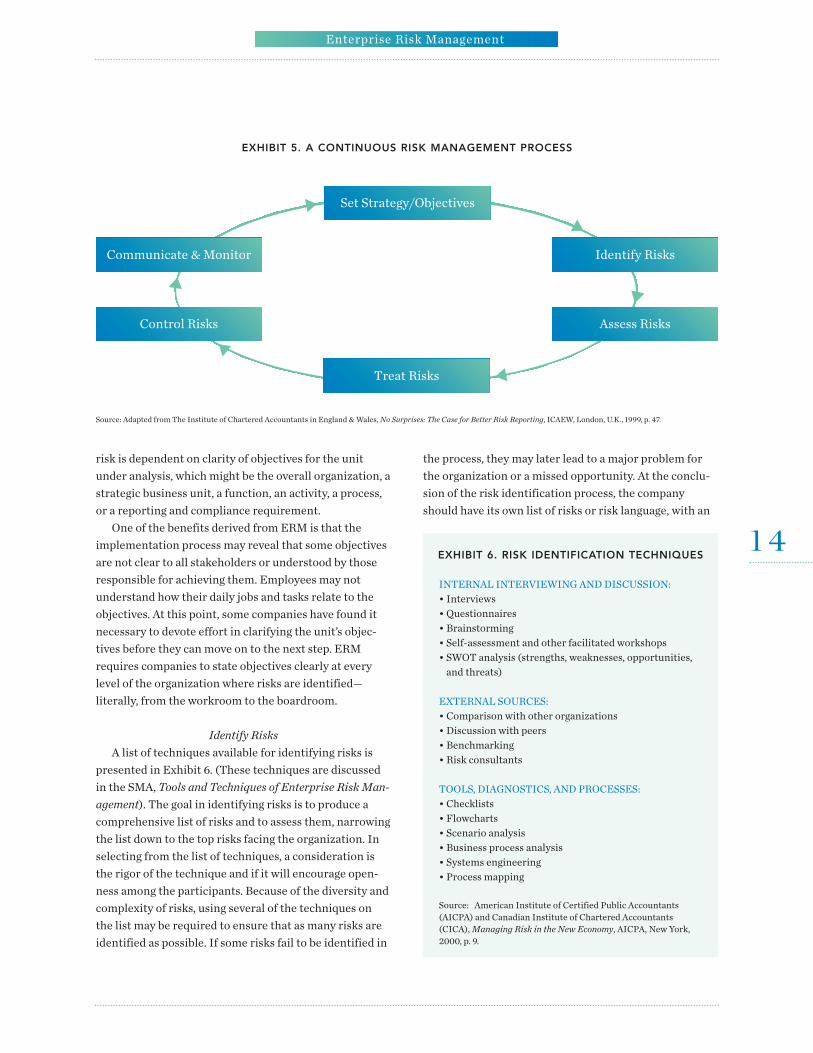

The basic components found in most ERM frame-works are (see Exhibit 5):• Set strategy and objectives,• Identify risks,• Assess risks,• Treat risks,• Control risks, and• Communicate and monitor.

Set Strategy and ObjectivesThe first step in the ERM framework requires an

understanding and clarity of strategy and objectives. Theopportunities that a company decides to pursue are artic-ulated in its strategy and objectives. Risks are the eventsor actions that jeopardize the achievement of the strategyand related objectives. On the up side, a holistic andproactive understanding of risk can lead to new or previ-ously unidentified opportunities. The identification of

Enterprise Risk Management

1 3

risk is dependent on clarity of objectives for the unitunder analysis, which might be the overall organization, astrategic business unit, a function, an activity, a process,or a reporting and compliance requirement. One of the benefits derived from ERM is that the

implementation process may reveal that some objectivesare not clear to all stakeholders or understood by thoseresponsible for achieving them. Employees may notunderstand how their daily jobs and tasks relate to theobjectives. At this point, some companies have found itnecessary to devote effort in clarifying the unit’s objec-tives before they can move on to the next step. ERMrequires companies to state objectives clearly at everylevel of the organization where risks are identified— literally, from the workroom to the boardroom.

Identify RisksA list of techniques available for identifying risks is

presented in Exhibit 6. (These techniques are discussedin the SMA, Tools and Techniques of Enterprise Risk Man-agement). The goal in identifying risks is to produce acomprehensive list of risks and to assess them, narrowingthe list down to the top risks facing the organization. Inselecting from the list of techniques, a consideration isthe rigor of the technique and if it will encourage open-ness among the participants. Because of the diversity andcomplexity of risks, using several of the techniques onthe list may be required to ensure that as many risks areidentified as possible. If some risks fail to be identified in

the process, they may later lead to a major problem forthe organization or a missed opportunity. At the conclu-sion of the risk identification process, the companyshould have its own list of risks or risk language, with an

Enterprise Risk Management

1 4

Set Strategy/Objectives

Identify Risks

Assess Risks

Communicate & Monitor

Control Risks

Treat Risks

EXHIBIT 5. A CONTINUOUS RISK MANAGEMENT PROCESS

Source: Adapted from The Institute of Chartered Accountants in England & Wales, No Surprises: The Case for Better Risk Reporting, ICAEW, London, U.K., 1999, p. 47.

EXHIBIT 6. RISK IDENTIFICATION TECHNIQUES

INTERNAL INTERVIEWING AND DISCUSSION:• Interviews• Questionnaires• Brainstorming• Self-assessment and other facilitated workshops• SWOT analysis (strengths, weaknesses, opportunities,and threats)

EXTERNAL SOURCES:• Comparison with other organizations• Discussion with peers• Benchmarking• Risk consultants

TOOLS, DIAGNOSTICS, AND PROCESSES:• Checklists• Flowcharts• Scenario analysis• Business process analysis• Systems engineering• Process mapping

Source: American Institute of Certified Public Accountants(AICPA) and Canadian Institute of Chartered Accountants(CICA), Managing Risk in the New Economy, AICPA, New York,2000, p. 9.

agreement on the meaning of each one. This list is theorganization’s inherent risks, and once mitigation actionsare determined, what remains are residual risks. In identifying risks, one view is to start with a blank

sheet of paper and develop the list of inherent risks byapplying of one or several of the techniques in Exhibit 6.

Alternatively, a list of risks or a risk universe can be pro-vided to those participating in the identification process.They, in turn, use this list to identify the risks relevant tothe organization. Some combination of these twoapproaches also may be used to develop a comprehensivelist of risks.

Enterprise Risk Management

1 5

QUALITATIVE:

Risk identification

Risk rankings

Risk maps

Risk maps with impact and likelihood

Risks mapped to objectives or divisions

Identification of risk correlations

QUALITATIVE/QUANTITATIVE:

Validation of risk impact

Validation of risk likelihood

Validation of correlations

Risk corrected revenues

Gain/loss

Tornado charts

Scenario analysis

Benchmarking

Net present value

Traditional measures

QUANTITATIVE:

Probabilistic techniques:

Cashflow at risk

Earnings at risk

Earnings distributions

EPS distributions

LEVEL OF DIFFICULTY AND AMOUNT OF DATA REQUIRED

EXHIBIT 7. RISK QUANTITATIVE AND QUALITATIVE TECHNIQUES

Qualitative and Quantitative Approaches to Assessment and Measurement

BRAINSTORMING OUTPUT

SURVEY RESPONSES TOTAL

Risks: 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Score

Sample Risk #1 3 1 1 1 1 1 1 1 1 1 1 1 1 1 1 17

Sample Risk #2 2 1 1 1 2 1 1 1 1 1 1 1 1 2 1 18

Sample Risk #3 2 1 2 1 2 1 2 1 1 1 1 1 1 1 1 19

Sample Risk #4 3 1 1 1 1 1 1 1 2 2 2 1 1 1 1 20

Sample Risk #5 3 1 2 1 1 2 1 2 1 2 1 1 1 1 1 21

Sample Risk #6 2 1 1 1 2 2 1 1 2 2 1 1 1 1 2 21

Sample Risk #7 3 2 3 1 1 1 1 1 2 1 2 1 2 1 1 23

Sample Risk #8 2 2 2 1 2 2 2 1 1 1 1 1 1 2 2 23

Sample Risk #9 3 2 1 1 2 2 1 1 2 1 1 2 2 2 2 25

Sample Risk #10 2 2 3 2 1 2 3 3 3 2 1 2 3 2 1 32

1 = very important 2 = somewhat important 3 = not important

EXHIBIT 8. SUBJECTIVE ASSESSMENT OF RISK

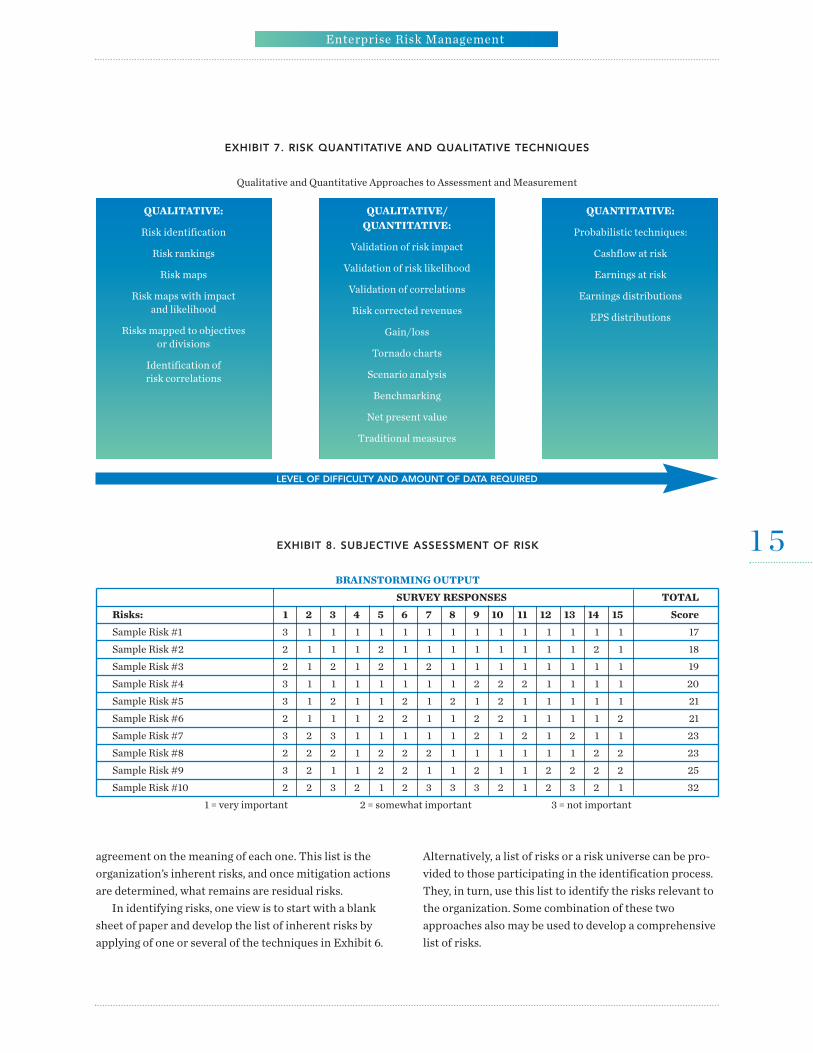

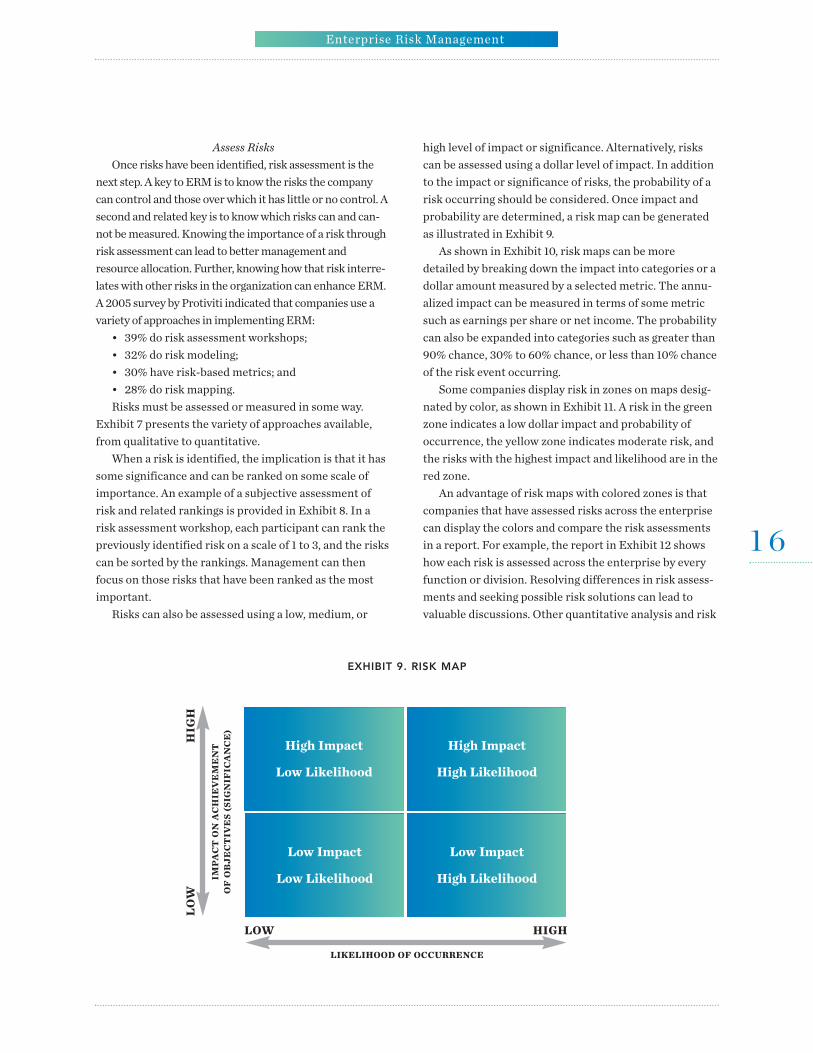

Assess RisksOnce risks have been identified, risk assessment is the

next step. A key to ERM is to know the risks the companycan control and those over which it has little or no control. Asecond and related key is to know which risks can and can-not be measured. Knowing the importance of a risk throughrisk assessment can lead to better management andresource allocation. Further, knowing how that risk interre-lates with other risks in the organization can enhance ERM.A 2005 survey by Protiviti indicated that companies use avariety of approaches in implementing ERM:• 39% do risk assessment workshops;• 32% do risk modeling;• 30% have risk-based metrics; and• 28% do risk mapping.Risks must be assessed or measured in some way.

Exhibit 7 presents the variety of approaches available,from qualitative to quantitative.When a risk is identified, the implication is that it has

some significance and can be ranked on some scale ofimportance. An example of a subjective assessment ofrisk and related rankings is provided in Exhibit 8. In arisk assessment workshop, each participant can rank thepreviously identified risk on a scale of 1 to 3, and the riskscan be sorted by the rankings. Management can thenfocus on those risks that have been ranked as the mostimportant. Risks can also be assessed using a low, medium, or

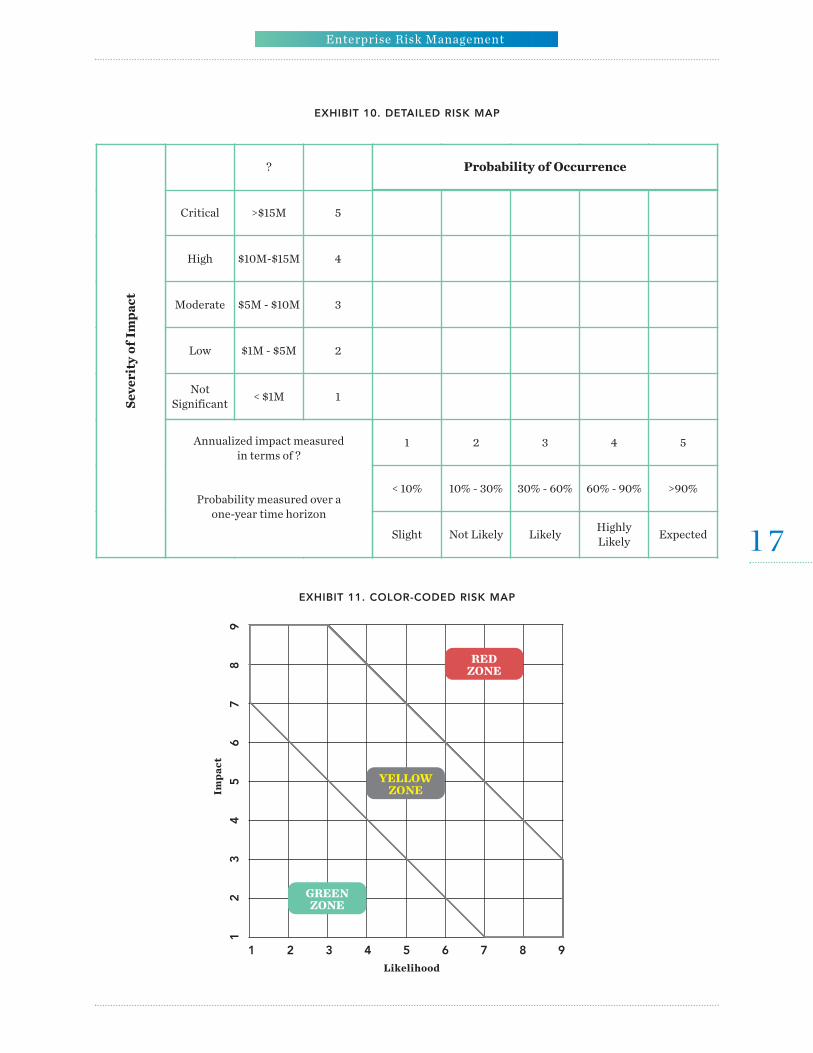

high level of impact or significance. Alternatively, riskscan be assessed using a dollar level of impact. In additionto the impact or significance of risks, the probability of arisk occurring should be considered. Once impact andprobability are determined, a risk map can be generatedas illustrated in Exhibit 9.As shown in Exhibit 10, risk maps can be more

detailed by breaking down the impact into categories or adollar amount measured by a selected metric. The annu-alized impact can be measured in terms of some metricsuch as earnings per share or net income. The probabilitycan also be expanded into categories such as greater than90% chance, 30% to 60% chance, or less than 10% chanceof the risk event occurring. Some companies display risk in zones on maps desig-

nated by color, as shown in Exhibit 11. A risk in the greenzone indicates a low dollar impact and probability ofoccurrence, the yellow zone indicates moderate risk, andthe risks with the highest impact and likelihood are in thered zone.An advantage of risk maps with colored zones is that

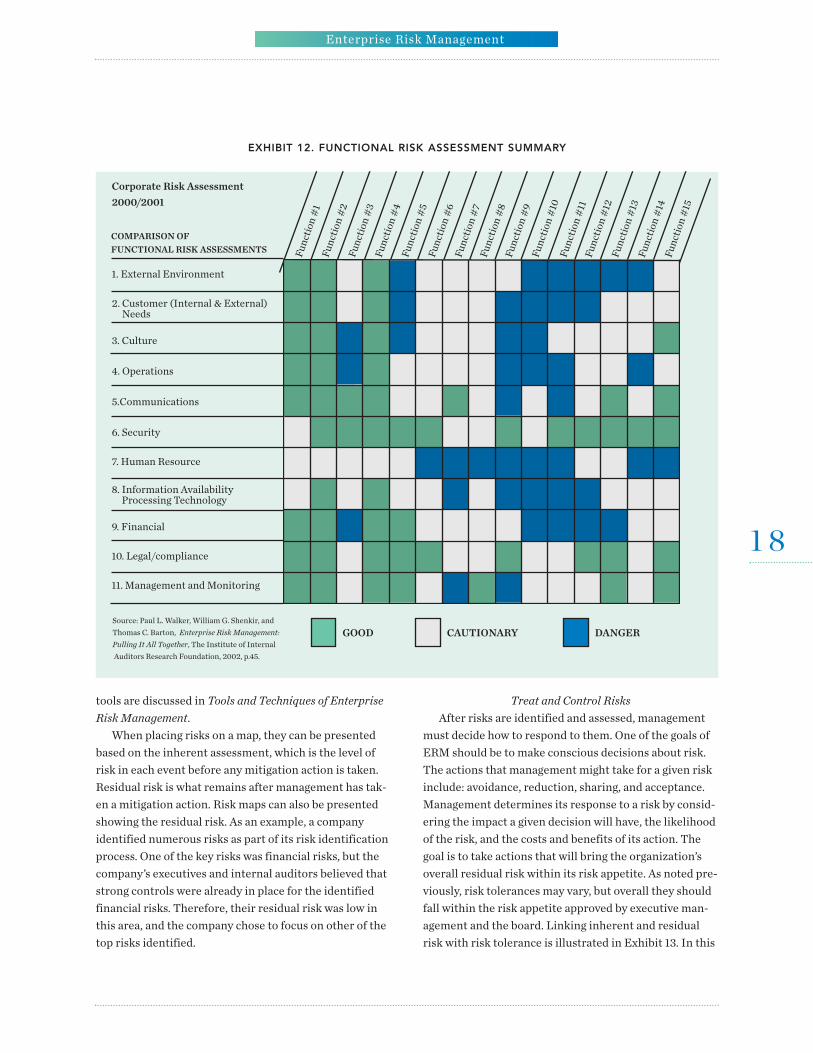

companies that have assessed risks across the enterprisecan display the colors and compare the risk assessmentsin a report. For example, the report in Exhibit 12 showshow each risk is assessed across the enterprise by everyfunction or division. Resolving differences in risk assess-ments and seeking possible risk solutions can lead tovaluable discussions. Other quantitative analysis and risk

Enterprise Risk Management

1 6

EXHIBIT 9. RISK MAP

High Impact

Low Likelihood

High Impact

High Likelihood

Low Impact

Low Likelihood

Low Impact

High Likelihood

LIKELIHOOD OF OCCURRENCE

LOW HIGH

IMPACT ON ACHIEVEMENT

OF OBJECTIVES (SIGNIFICANCE)

LOW

HIGH

Enterprise Risk Management

1 7

?

Critical >$15M 5

High $10M-$15M 4

Moderate $5M - $10M 3

Low $1M - $5M 2

Not Significant

< $1M 1

1 2 3 4 5

< 10% 10% - 30% 30% - 60% 60% - 90% >90%

Slight Not Likely LikelyHighly Likely

Expected

Annualized impact measured in terms of ?

Probability measured over a one-year time horizon

Probability of Occurrence

Severity of Impact

EXHIBIT 10. DETAILED RISK MAP

1 2 3 4 5 6 7 8 9Likelihood

Impact

1

2

3

4

5

6

7

8

9

REDZONE

YELLOWZONE

GREENZONE

EXHIBIT 11. COLOR-CODED RISK MAP

tools are discussed in Tools and Techniques of EnterpriseRisk Management. When placing risks on a map, they can be presented

based on the inherent assessment, which is the level ofrisk in each event before any mitigation action is taken.Residual risk is what remains after management has tak-en a mitigation action. Risk maps can also be presentedshowing the residual risk. As an example, a companyidentified numerous risks as part of its risk identificationprocess. One of the key risks was financial risks, but thecompany’s executives and internal auditors believed thatstrong controls were already in place for the identifiedfinancial risks. Therefore, their residual risk was low inthis area, and the company chose to focus on other of thetop risks identified.

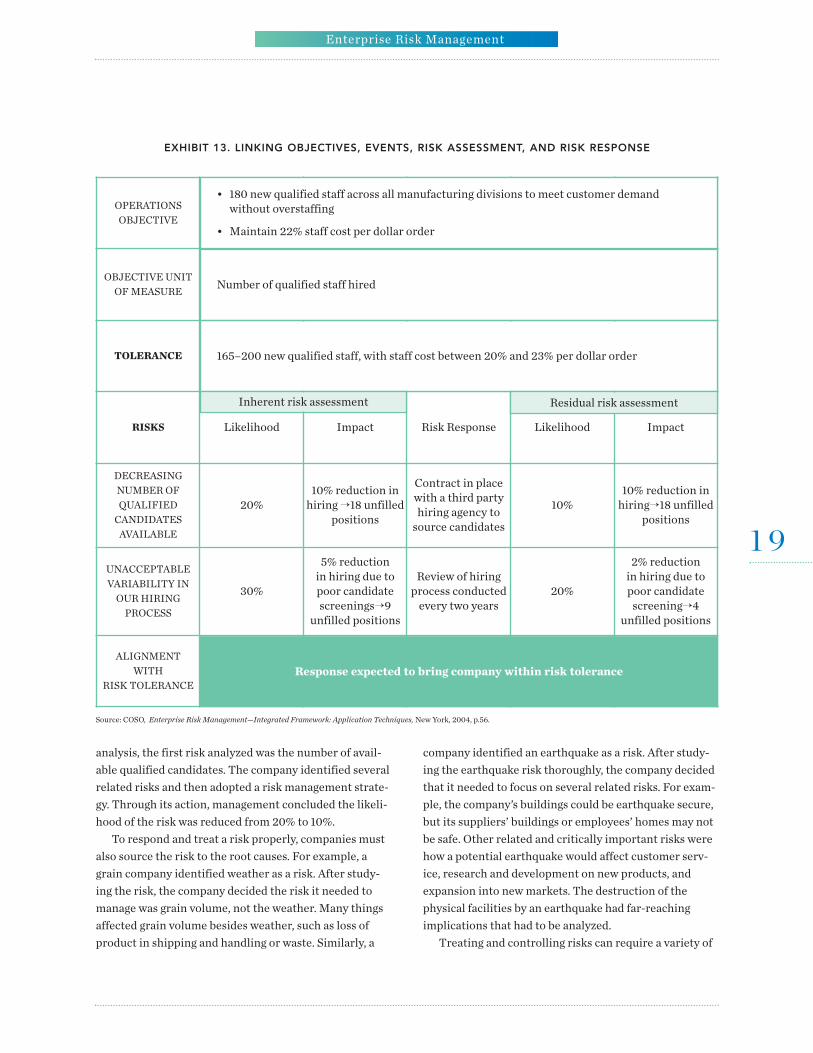

Treat and Control RisksAfter risks are identified and assessed, management

must decide how to respond to them. One of the goals ofERM should be to make conscious decisions about risk.The actions that management might take for a given riskinclude: avoidance, reduction, sharing, and acceptance.Management determines its response to a risk by consid-ering the impact a given decision will have, the likelihoodof the risk, and the costs and benefits of its action. Thegoal is to take actions that will bring the organization’soverall residual risk within its risk appetite. As noted pre-viously, risk tolerances may vary, but overall they shouldfall within the risk appetite approved by executive man-agement and the board. Linking inherent and residualrisk with risk tolerance is illustrated in Exhibit 13. In this

Enterprise Risk Management

1 8

Source: Paul L. Walker, William G. Shenkir, and

Thomas C. Barton, Enterprise Risk Management: Pulling It All Together, The Institute of InternalAuditors Research Foundation, 2002, p.45.

1. External Environment

2. Customer (Internal & External)Needs

3. Culture

4. Operations

5.Communications

6. Security

7. Human Resource

8. Information Availability Processing Technology

9. Financial

10. Legal/compliance

11. Management and Monitoring

Function #1

Function #2

Function #3

Function #4

Function #5

Function #6

Function #7

Function # 8

Function #9

Function #10

Function #11

Function #12

Function #13

Function #14

Function #15

COMPARISON OF FUNCTIONAL RISK ASSESSMENTS

Corporate Risk Assessment2000/2001

GOOD CAUTIONARY DANGER

EXHIBIT 12. FUNCTIONAL RISK ASSESSMENT SUMMARY

analysis, the first risk analyzed was the number of avail-able qualified candidates. The company identified severalrelated risks and then adopted a risk management strate-gy. Through its action, management concluded the likeli-hood of the risk was reduced from 20% to 10%. To respond and treat a risk properly, companies must

also source the risk to the root causes. For example, agrain company identified weather as a risk. After study-ing the risk, the company decided the risk it needed tomanage was grain volume, not the weather. Many thingsaffected grain volume besides weather, such as loss ofproduct in shipping and handling or waste. Similarly, a

company identified an earthquake as a risk. After study-ing the earthquake risk thoroughly, the company decidedthat it needed to focus on several related risks. For exam-ple, the company’s buildings could be earthquake secure,but its suppliers’ buildings or employees’ homes may notbe safe. Other related and critically important risks werehow a potential earthquake would affect customer serv-ice, research and development on new products, andexpansion into new markets. The destruction of thephysical facilities by an earthquake had far-reachingimplications that had to be analyzed. Treating and controlling risks can require a variety of

Enterprise Risk Management

1 9

OPERATIONSOBJECTIVE

OBJECTIVE UNITOF MEASURE

TOLERANCE

RISKS Likelihood Impact Risk Response Likelihood Impact

DECREASING NUMBER OF QUALIFIED CANDIDATESAVAILABLE

20%10% reduction inhiring �18 unfilled

positions

Contract in placewith a third partyhiring agency tosource candidates

10%10% reduction inhiring�18 unfilled

positions

UNACCEPTABLEVARIABILITY INOUR HIRINGPROCESS

30%

5% reduction in hiring due topoor candidatescreenings�9

unfilled positions

Review of hiringprocess conductedevery two years

20%

2% reduction in hiring due topoor candidatescreening�4

unfilled positions

ALIGNMENT WITH

RISK TOLERANCE

• 180 new qualified staff across all manufacturing divisions to meet customer demand without overstaffing

• Maintain 22% staff cost per dollar order

Number of qualified staff hired

165–200 new qualified staff, with staff cost between 20% and 23% per dollar order

Inherent risk assessment Residual risk assessment

Response expected to bring company within risk tolerance

EXHIBIT 13. LINKING OBJECTIVES, EVENTS, RISK ASSESSMENT, AND RISK RESPONSE

Source: COSO, Enterprise Risk Management—Integrated Framework: Application Techniques, New York, 2004, p.56.

actions. For example, companies can implement newpolicies and controls, purchase derivatives, hire newmanagement, or implement new training programs. Thisvariety of risk treatment approaches is why ERM is amuch broader concept than financial reporting and inter-nal control risk. Of course, companies can still just acceptand bear the risk if doing so is in alignment with its stake-holders’ expectations. For example, some airlines havemore aggressive approaches to managing the risk of fuelprice increases and decreases than do others.An insurance and financial services company discov-

ered its sales force had slowly become out of control. Topromote sales, the sales force developed their own train-ing material that was not authorized by the company. Thesales force was increasingly dishonest with customersand told them to ignore notices from the company aboutpremiums. Further, they asked customers to sign blankwithdrawal forms, which allowed the sales team to with-draw funds from the customers’ accounts. Simultaneous-ly, the company also faced risks related to industry trendsthat indicated a shrinking market in one of their keyproduct areas. It is probable that the broader industrytrends and declining market were the root cause of thepressure on the sales force and marketing areas. Thecompany responded by hiring a new CEO with expertisein areas into which the company wanted to expand. Addi-tionally, the company adopted new sales and marketingpolicies to control the risk of the sales force misleadingcustomers by using unauthorized advertising and train-ing material. The company also implemented customersupport lines to help resolve disputes with customers andengaged independent industry organizations to verifywith customers that they were knowledgeable aboutwhat they had purchased.

Communicate and MonitorOrganizations are generally involved in distributed

risk taking as each operating unit faces risk in pursuingits profit objectives and goals to grow its piece of thebusiness. The desired outcome for ERM is not thatorganizations become risk adverse, but that proactive,risk-based decision making is fostered at all levels of theorganization and managers knowingly and intentionallytake risk while utilizing appropriate risk indicators.Accordingly, communication of risk-related informationmust flow down, across, and up the organization. As illus-trated in Exhibit 12, summary reports of risk assess-

ments at the division or function level provide seniormanagement with valuable information on how middlemanagement views the top risks facing the organization. Ongoing monitoring with key performance indicators

(KPIs) and key risk indicators (KRIs) occurs in well man-aged organizations as a normal course of conductingbusiness. Under ERM, monitoring is enhanced by incor-porating information on risk identification and assess-ment and identifying the owners of specific risks.Monitoring is discussed further in the next section.

VIII. INTEGRATING ERM INTO ONGOINGMANAGEMENT ACTIVITIES

The business environment is constantly changing.Consequently, implementing ERM is a continuousprocess much like the organization’s strategy that ERMhelps to achieve. Sustaining ERM requires constantattention by C-level executives, and integration intoongoing management initiatives stresses its importanceto associates at all levels. When ERM is seen as soundbusiness management rather than “the management fadof the month,” it becomes an integral part of the organi-zation’s DNA. Some of the opportunities for integratingERM in ongoing management activities include:• Strategic planning;• Balanced scorecard (BSC);• Budgeting;• Total Quality Management and Six Sigma;• Business continuity (crisis management);• Corporate governance; and • Risk disclosures.The relationship between strategic planning, the bal-

anced scorecard, and budgeting is shown in Exhibit 14.

STRATEGIC PLANNING

The COSO definition of ERM states that ERM is part ofstrategy setting. ERM and strategy setting should beviewed as complementing each other and not as independ-ent activities. If strategy is formulated without identifyingthe risks embedded in the strategy and assessing and man-aging those risks, the strategy is incomplete and at risk offailure. Similarly, if ERM does not begin with holisticallyidentifying risks related to the company’s strategy, theeffort will be incomplete by failing to identify some veryimportant risks. Mismanagement of strategic risks hasbeen shown to be the cause for loss of major shareholdervalue, as pointed out by the following two studies:

Enterprise Risk Management

2 0

A study by Mercer Management Consulting analyzedthe value collapses in the Fortune 1,000 during 1993-1998. The analysis found that 10% of the Fortune1,000 lost 25% of shareholder value within a one-month period. Mercer traced the collapses back totheir root causes and found that 58% of the losseswere triggered by strategic risk, 31% by operationalrisk, and 6% by financial risk. Hazard risk did notcause any of the decrease in shareholder value. Amore recent study by Booz Allen Hamilton analyzed1,200 firms during 1999-2003 with market capitaliza-tions greater than $1 billion. The poorest performerswere identified as companies that trailed the lowest- performing index for that period, which was the S&P500. The primary events triggering the loss of share-holder value were strategic and operational failures.Of the 360 worst performers in the study, 87% ofvalue destruction suffered by these companies relat-ed to strategic and operational mismanagement.

When formulating the company’s strategy, top man-agement analyzes its strategic alternatives and identifiesevents that could threaten their achievement. As therisks embedded in each strategic alternative are identi-fied and placed on a risk map, the alternative can be eval-uated against the organization’s capabilities and how italigns with the risk appetite. Some strategies might beoutside the risk appetite of the company, and a decision ismade not to pursue them—a decision to avoid the risk.Other strategies may be very risky but can be managedand monitored carefully and, thus, will be pursued—adecision to accept the risk. Another strategy may be risky,

but the decision is made to pursue it through a joint ven-ture—a decision to share the risk. Still another alterna-tive strategy with considerable risk embedded in it mightbe pursued incrementally—a decision to reduce the risk.Strategy formulation is enhanced by ERM because risksare identified and the strategic alternatives are assessedgiven the company’s risk appetite. In turn, without a wellarticulated strategy, the foundation for implementingERM is insufficient. Viewing the two together forms thebasis for a strategy-risk-focused organization. For exam-ple, the front-end of the strategy formulation process istypically an environmental scan. Performed comprehen-sively, this scan reveals risks and opportunities.

BALANCED SCORECARD

The balanced scorecard (BSC) is a tool for communi-cating and cascading the company’s strategy throughoutthe organization. The conventional BSC captures thecompany’s strategy in four key perspectives:• Customer;• Internal;• Innovation and learning; and• Financial.Combining the BSC with ERM can enhance perfor -

mance management. In the BSC, objectives are identifiedfor each of the perspectives, and, as noted previously,ERM begins with an understanding of objectives. Foreach BSC perspective, metrics (KPIs) are selected andstretch targets are set. ERM adds value to the BSCthrough the identification of events (risks) that couldstand in the way of achieving the targets in each of thefour perspectives. By monitoring the KPIs, management

Enterprise Risk Management

2 1

Strategy

Balanced ScorecardBudget

Operations

Revise theStrategy

Review

Revise theScorecard

Allocate

EXHIBIT 14. STRATEGY, THE BALANCED SCORECARD, AND THE BUDGET

can assess how effectively their risk mitigation efforts areworking. In effect, the KPIs for each perspective alsoserve as key risk indicators (KRIs), although they are notinitially selected for that purpose. For example, if a targetfor customer satisfaction is not achieved, it suggests thatsome risks related to the item exist. The same metric canbe used for monitoring both strategy and risk. The conventional BSC can be integrated with ERM to

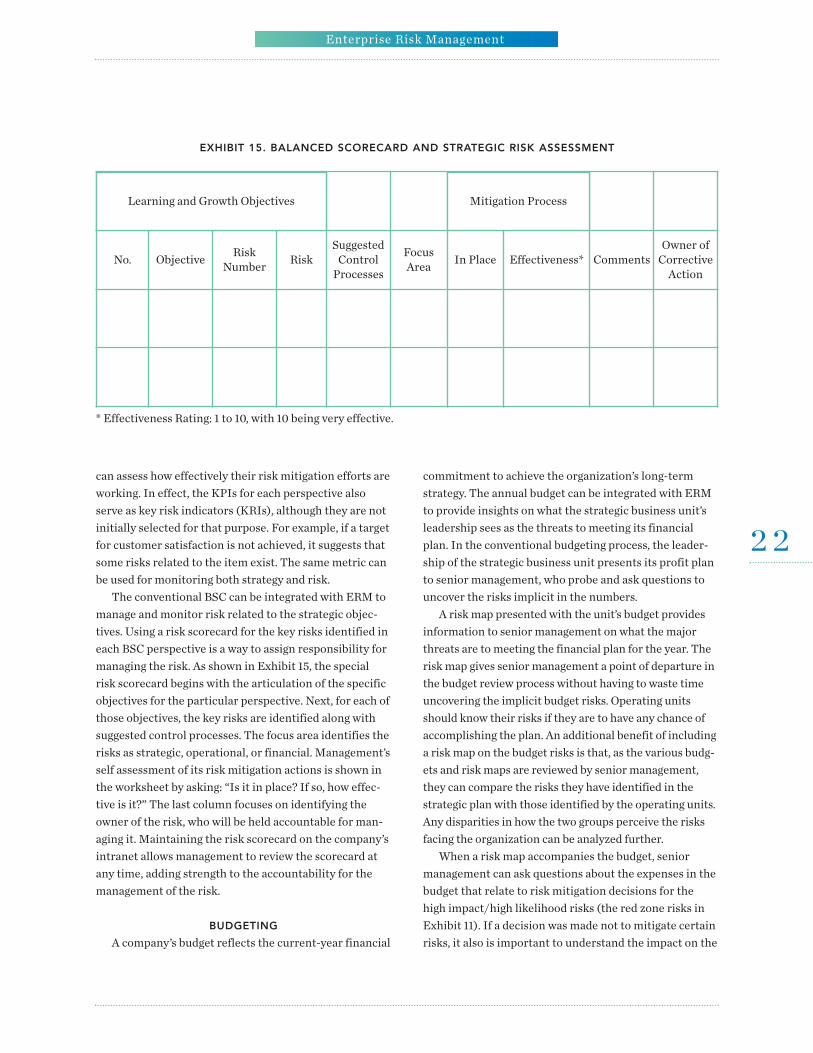

manage and monitor risk related to the strategic objec-tives. Using a risk scorecard for the key risks identified ineach BSC perspective is a way to assign responsibility formanaging the risk. As shown in Exhibit 15, the specialrisk scorecard begins with the articulation of the specificobjectives for the particular perspective. Next, for each ofthose objectives, the key risks are identified along withsuggested control processes. The focus area identifies therisks as strategic, operational, or financial. Management’sself assessment of its risk mitigation actions is shown inthe worksheet by asking: “Is it in place? If so, how effec-tive is it?” The last column focuses on identifying theowner of the risk, who will be held accountable for man-aging it. Maintaining the risk scorecard on the company’sintranet allows management to review the scorecard atany time, adding strength to the accountability for themanagement of the risk.

BUDGETING

A company’s budget reflects the current-year financial

commitment to achieve the organization’s long-termstrategy. The annual budget can be integrated with ERMto provide insights on what the strategic business unit’sleadership sees as the threats to meeting its financialplan. In the conventional budgeting process, the leader-ship of the strategic business unit presents its profit planto senior management, who probe and ask questions touncover the risks implicit in the numbers. A risk map presented with the unit’s budget provides

information to senior management on what the majorthreats are to meeting the financial plan for the year. Therisk map gives senior management a point of departure inthe budget review process without having to waste timeuncovering the implicit budget risks. Operating unitsshould know their risks if they are to have any chance ofaccomplishing the plan. An additional benefit of includinga risk map on the budget risks is that, as the various budg-ets and risk maps are reviewed by senior management,they can compare the risks they have identified in thestrategic plan with those identified by the operating units.Any disparities in how the two groups perceive the risksfacing the organization can be analyzed further. When a risk map accompanies the budget, senior

management can ask questions about the expenses in thebudget that relate to risk mitigation decisions for thehigh impact/high likelihood risks (the red zone risks inExhibit 11). If a decision was made not to mitigate certainrisks, it also is important to understand the impact on the

Enterprise Risk Management

2 2

No. ObjectiveRisk

NumberRisk

SuggestedControlProcesses

Focus Area

In Place Effectiveness* CommentsOwner ofCorrectiveAction

Learning and Growth Objectives Mitigation Process

EXHIBIT 15. BALANCED SCORECARD AND STRATEGIC RISK ASSESSMENT

* Effectiveness Rating: 1 to 10, with 10 being very effective.

unit’s cost structure by taking that action. Another rele-vant issue is to understand to what extent the cost of mit-igating or accepting a risk has been built into the price ofthe product or service. ERM coupled with the budgetreview process can enrich a discussion and lead to a bet-ter understanding of the threats standing in the way ofmaking budget.

TOTAL QUALITY MANAGEMENT AND SIX SIGMA

Quality initiatives focus on improving the efficiencyand effectiveness of detailed processes. ERM requiresclarity of objectives at all levels of the enterprise, and theobjectives of specific processes can be addressed by uti-lizing quality tools and methodologies. When an organi-zation has implemented a quality initiative, informationis available on detailed processes. In turn, this informa-tion can be evaluated within the larger context of theenterprise to identify risks in an ERM implementation.Also, quality initiatives can provide information on plan-ning the mitigation action for a process risk. The processrisk owner and source of the risks should be identifiedwhen implementing the quality initiative. This informa-tion should be insightful in treating the inherent riskwith some control mitigation action. Once the control isimplemented, the gap between the inherent risk andresidual risk should be clearly evident.

BUSINESS CONTINUITY (CRISIS MANAGEMENT)

Regardless of how robust effort of risk identification

is, some unknown risks will remain unknown at the endof the process. A company prepares for these unknownrisks through its business continuity, or crisis manage-ment, plan—an essential element of the ERM process.A crisis is a point at one end of a continuum, with risks

at the other end. With Internet-based new media likebloggers, message boards, chat rooms, e-mail lists, andindependent news websites, a company must be preparedto recognize a crisis and respond swiftly to contain itbefore damage is done to its reputation and brands. Acompany will need to “play war games” to test the crisismanagement plan and ensure that all the key employeesknow their roles. In addition, an essential part of thepreparation is communication about the plan to theentire work force in advance of a crisis.When a crisis occurs, it does not evolve in a linear

way: If it is not recognized quickly and if efforts are notmade to contain it, a series of reactions and events inother areas either within and/or outside the organiza-tion may be triggered. Exhibit 16 shows the “triggeringor ballooning” impact of a crisis and how it may developexponentially. As an example, a major company soldsome contaminated product in two countries thatcaused some users to become ill. A failure by the com-pany to recognize the crisis quickly led the governmentsof the two countries to pull the product from storeshelves. After some delay, the CEO traveled from theU.S. to the countries and eventually apologized publicly.The damage was done, however, as the company’s stock

Enterprise Risk Management

2 3

EXHIBIT 16. RISK/CRISIS ACCELERATION

A. Risk Occurrence B. Crisis Occurrence—Gathering Storm

C. Crisis Occurrence—Catastrophic Force

LIKELIHOOD ACCELERATION ACCELERATION

IMPACT

MASS

MASS

Source: Paul L. Walker, William G. Shenkir, and Thomas C. Barton, Enterprise Risk Management: Pulling It All Together, The Institute of Internal Auditors Research Foundation, 2002, p.100.

price fell, and the CEO was eventually replaced.

CORPORATE GOVERNANCE

ERM ties in closely with corporate governancebecause it:• Improves information flows between the companyand the board regarding risks;

• Enhances discussions of strategy and the relatedrisks between executives and the board;

• Monitors key risks by accountants and manage-ment with reports to the board;

• Identifies acceptable levels of risks to be taken andassumed;

• Focuses management on the risks identified;• Improves disclosures to stakeholders about riskstaken and risks yet to be managed;

• Reassures the board that management no longermanages risk in silos; and

• Knows which of the organization’s objectives is atgreatest risk.