Embed Size (px)

Citation preview

DMB

Dr. Perdana Wahyu Santosa

Delineating

Efficient

Portfolio

Key Concepts and Skills

Combination of Two Risky Assets

Shape of The Portfolio Curve

The Efficient Frontier

Examples and Applications

Combination of Two Risky Assets

1 1 2 2

1

2

The expected return on a portfolio of two assets is given by:

(1)

is the proportion asset 1 in the portfolio

is the proportion asset 2 in the portfolio

is the ex

P

P

R w R w R

where

w

w

R

1

2

pected return on the portfolio

is the expected return on the asset 1

is the expected return on the asset 2

R

R

( )i iE R R

Combination of Two Risky Assets

1 2

2 1

1 1 1 2

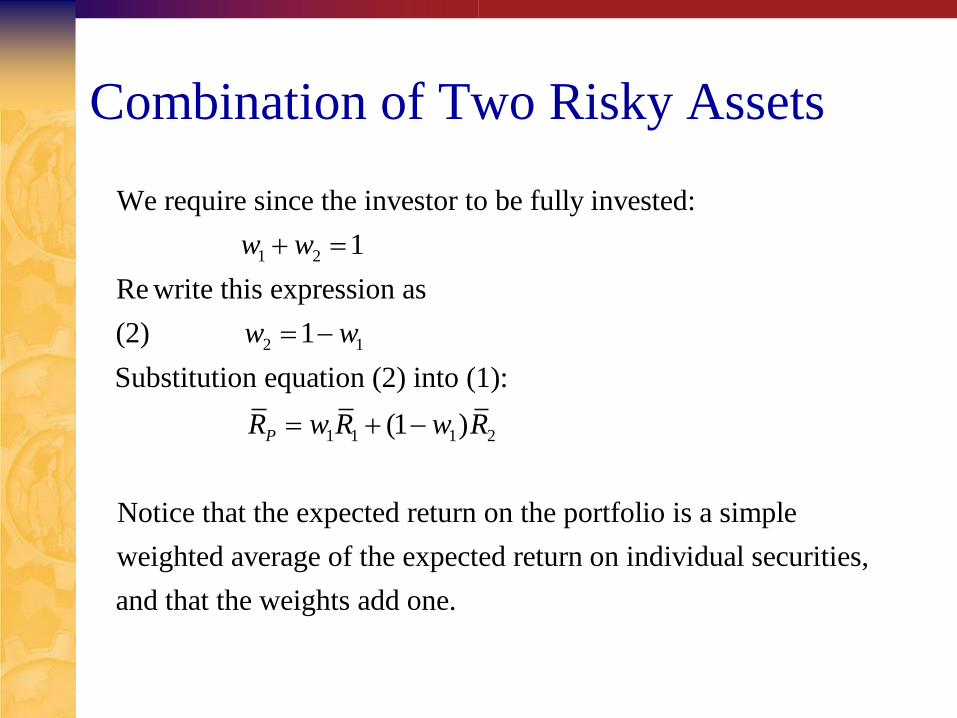

We require since the investor to be fully invested:

1

Re write this expression as

(2) 1

Substitution equation (2) into (1):

(1 )

Notice

P

w w

w w

R w R w R

that the expected return on the portfolio is a simple

weighted average of the expected return on individual securities,

and that the weights add one.

4

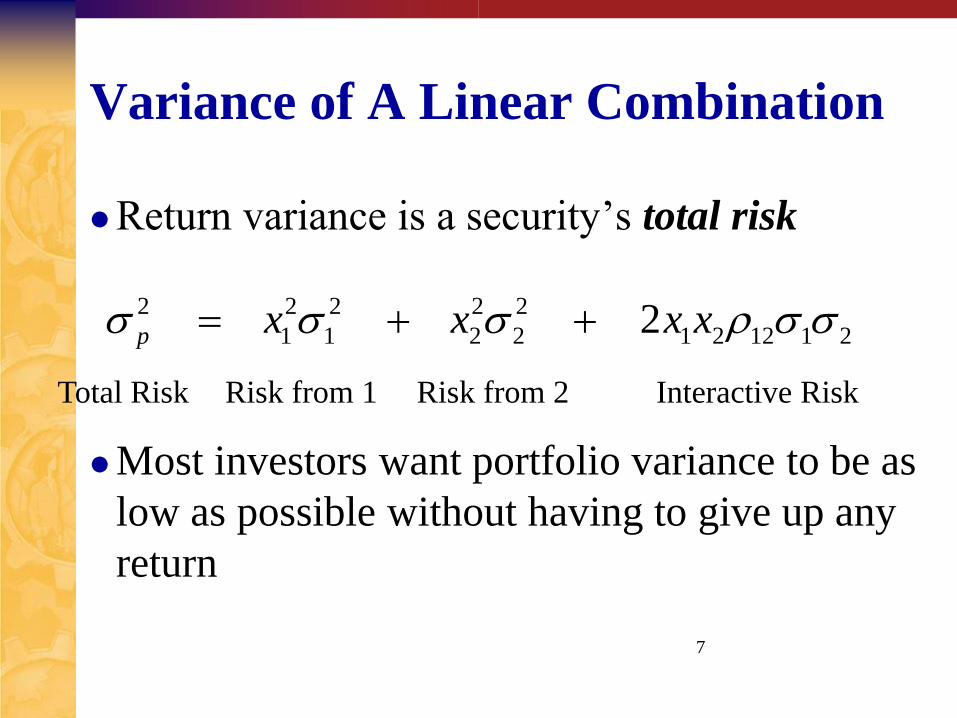

Variance of A Linear Combination

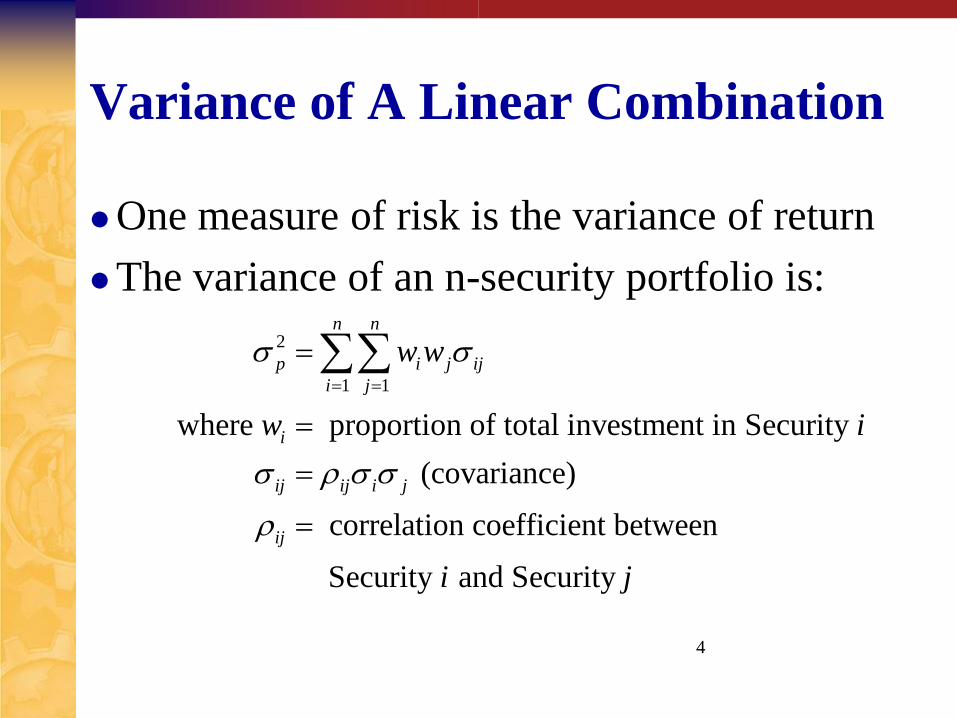

One measure of risk is the variance of return

The variance of an n-security portfolio is:

2

1 1

where proportion of total investment in Security

(covariance)

correlation coefficient between

Security and Security

n n

p i j ij

i j

i

ij ij i j

ij

w w

w i

i j

Combination of Two Risky Assets

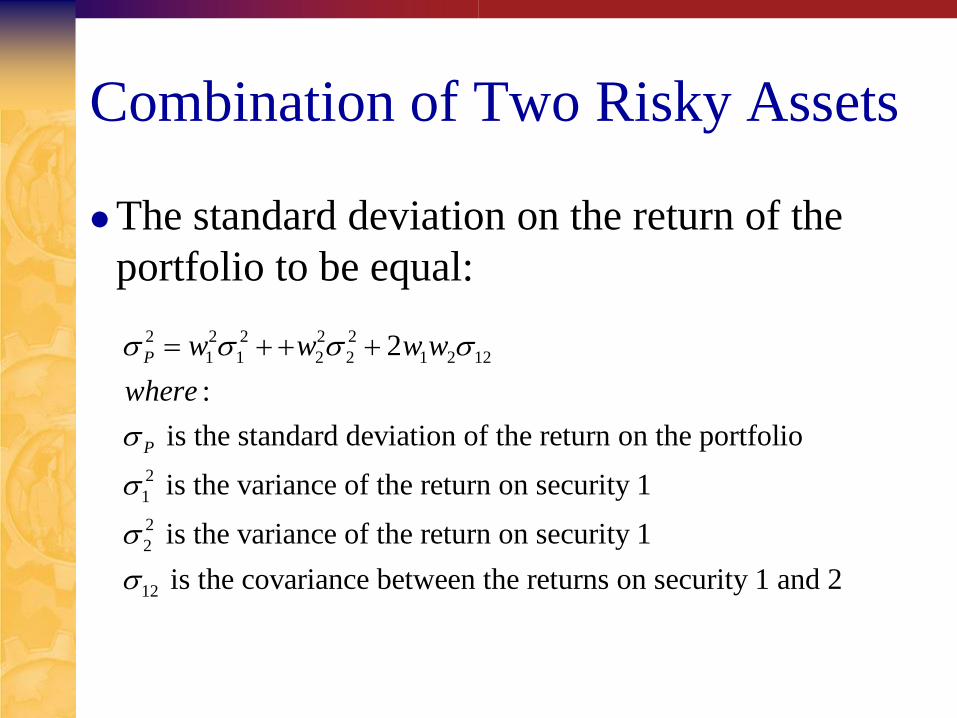

The standard deviation on the return of the

portfolio to be equal:

2 2 2 2 2

1 1 2 2 1 2 12

2

1

2

2

12

2

:

is the standard deviation of the return on the portfolio

is the variance of the return on security 1

is the variance of the return on security 1

is the cov

P

P

w w w w

where

ariance between the returns on security 1 and 2

Combination of Two Risky Assets

22 2 2 2

1 1 1 2 1 1 12

1212 12 12 1 2

1 2

12

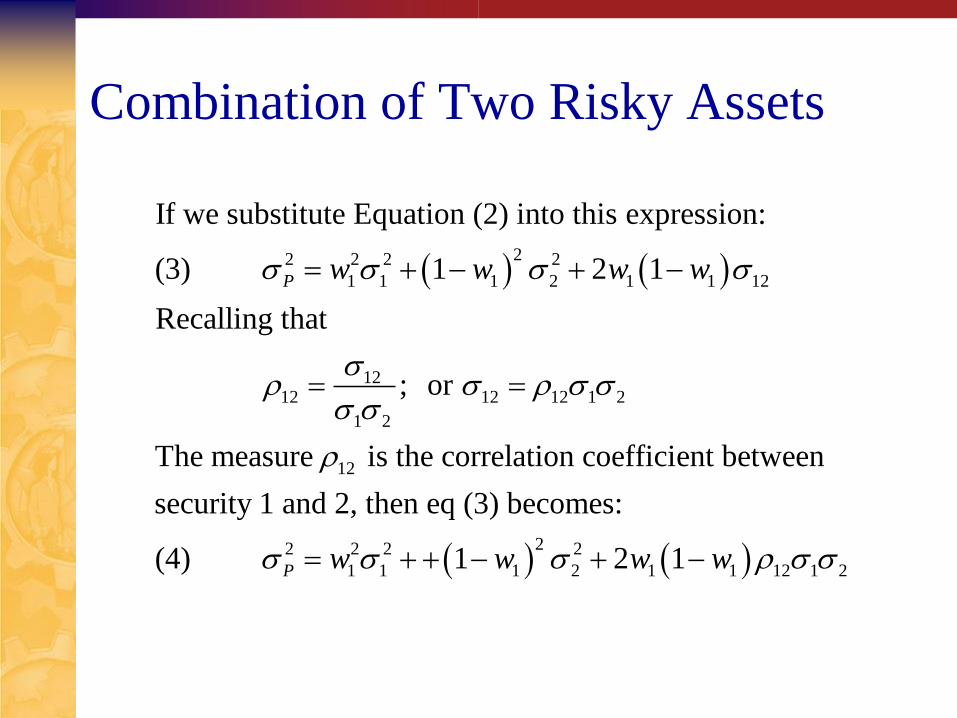

If we substitute Equation (2) into this expression:

(3) 1 2 1

Recalling that

; or

The measure is the correlation coefficient bet

P w w w w

22 2 2 2

1 1 1 2 1 1 12 1 2

ween

security 1 and 2, then eq (3) becomes:

(4) 1 2 1P w w w w

7

Variance of A Linear Combination

Return variance is a security’s total risk

Most investors want portfolio variance to be as

low as possible without having to give up any

return

2 2 2 2 2

1 1 2 2 1 2 12 1 2 2p x x x x

Total Risk Risk from 1 Risk from 2 Interactive Risk

Combination of Two Risky Assets

The standard deviation of the portfolio is not,

in general, a simple-weighted average of the

standard deviation each security.

Some specific cases involving different degrees

of co-movement between securities (covariance

and coefficient of correlation).

A correlation coefficient has: 1 1ij

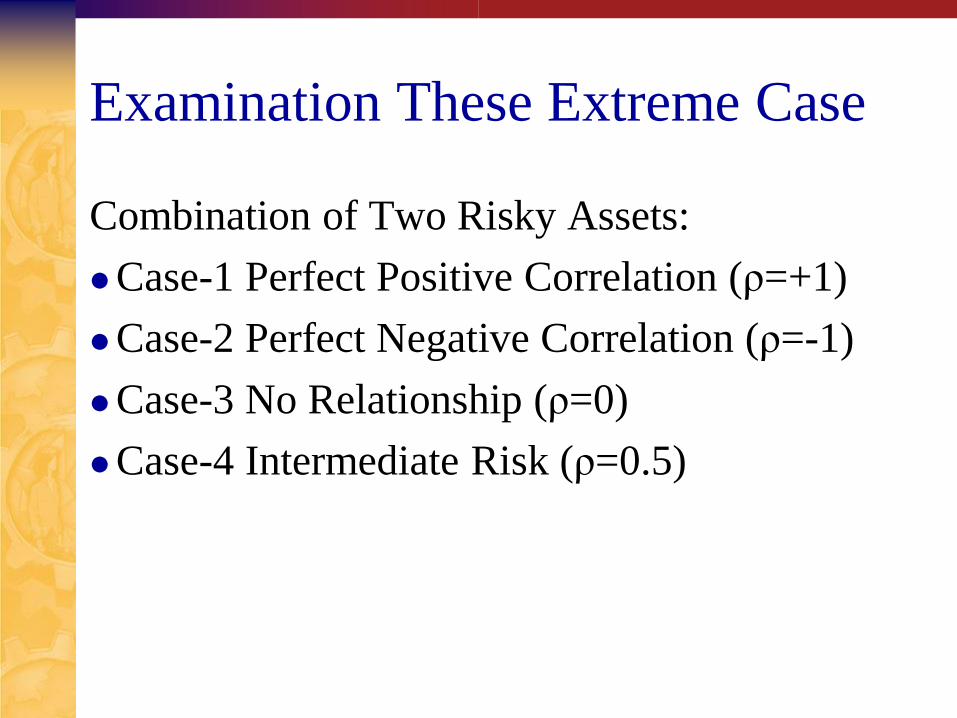

Examination These Extreme Case

Combination of Two Risky Assets:

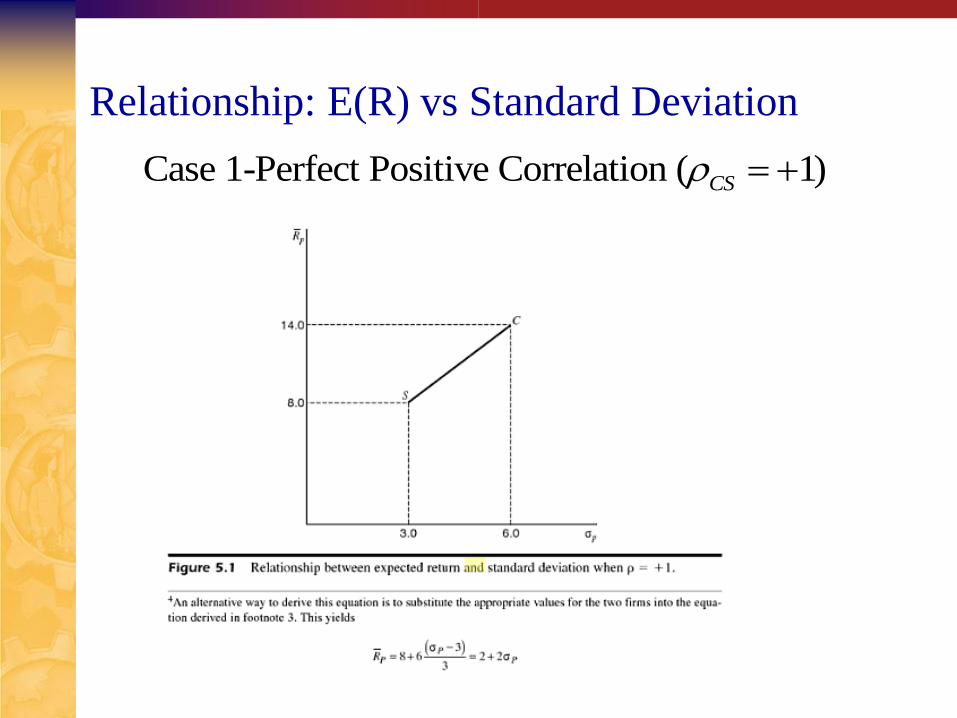

Case-1 Perfect Positive Correlation (ρ=+1)

Case-2 Perfect Negative Correlation (ρ=-1)

Case-3 No Relationship (ρ=0)

Case-4 Intermediate Risk (ρ=0.5)

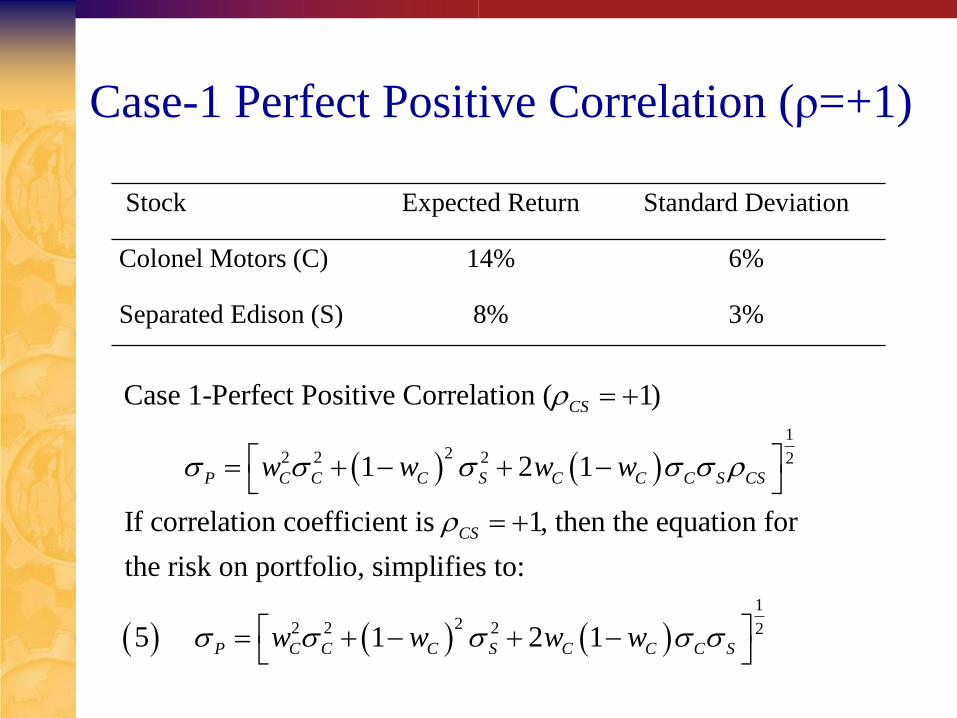

Case-1 Perfect Positive Correlation (ρ=+1)

Stock Expected Return Standard Deviation

Colonel Motors (C) 14% 6%

Separated Edison (S) 8% 3%

122 2 2 2

2

Case 1-Perfect Positive Correlation ( 1)

1 2 1

If correlation coefficient is 1, then the equation for

the risk on portfolio, simplifies to:

5

CS

P C C C S C C C S CS

CS

P C C

w w w w

w

1

22 2 21 2 1C S C C C Sw w w

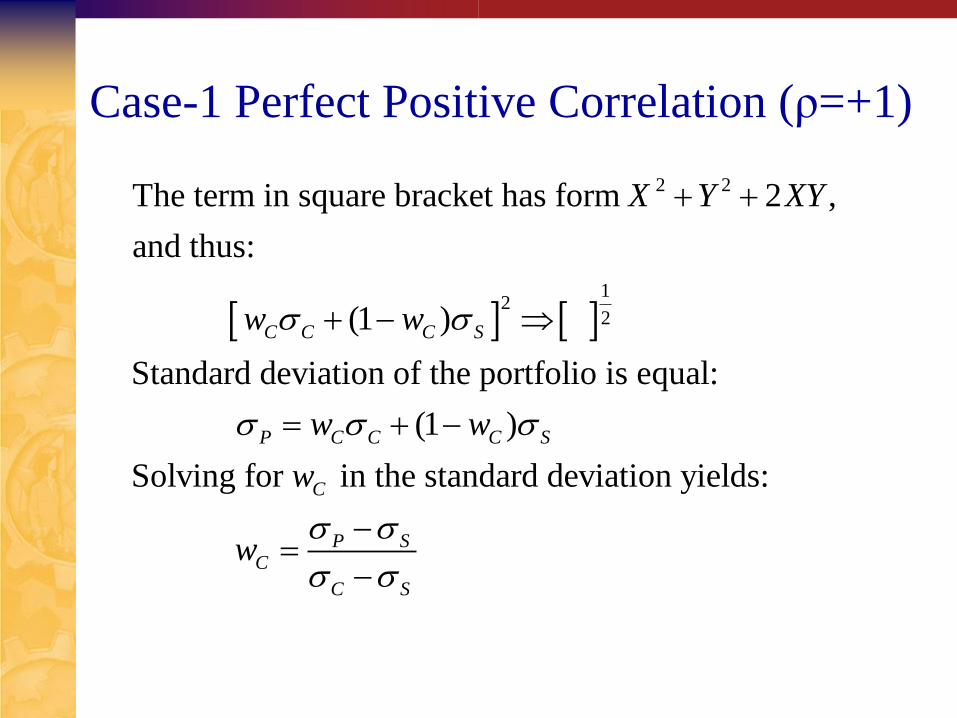

Case-1 Perfect Positive Correlation (ρ=+1)

2 2

12

2

The term in square bracket has form 2 ,

and thus:

(1 )

Standard deviation of the portfolio is equal:

(1 )

Solving for in the standard deviation yie

C C C S

P C C C S

C

X Y XY

w w

w w

w

lds:

P SC

C S

w

Case-1 Perfect Positive Correlation (ρ=+1)

While the expected return on the portfolio is:

(1 )

substitute :

For two stocks under study,

(1 )

Which is the equation of a straight line

P C C C S

P SC

C S

P S P SP C S

C S C S

R w R w R

w

R R R

connecting C and S in

expected return and standard deviation space.

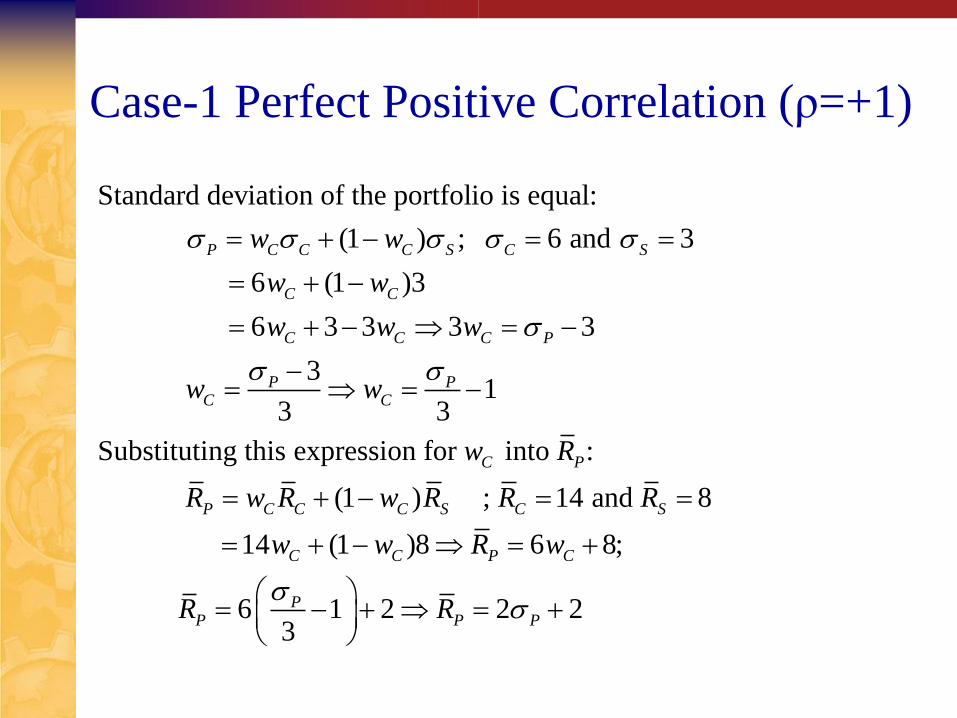

Case-1 Perfect Positive Correlation (ρ=+1)

Standard deviation of the portfolio is equal:

(1 ) ; 6 and 3

6 (1 )3

6 3 3 3 3

3 1

3 3

Substituting this

P C C C S C S

C C

C C C P

P PC C

w w

w w

w w w

w w

expression for into :

(1 ) ; 14 and 8

14 (1 )8 6 8;

6 1 2 2 23

C P

P C C C S C S

C C P C

PP P P

w R

R w R w R R R

w w R w

R R

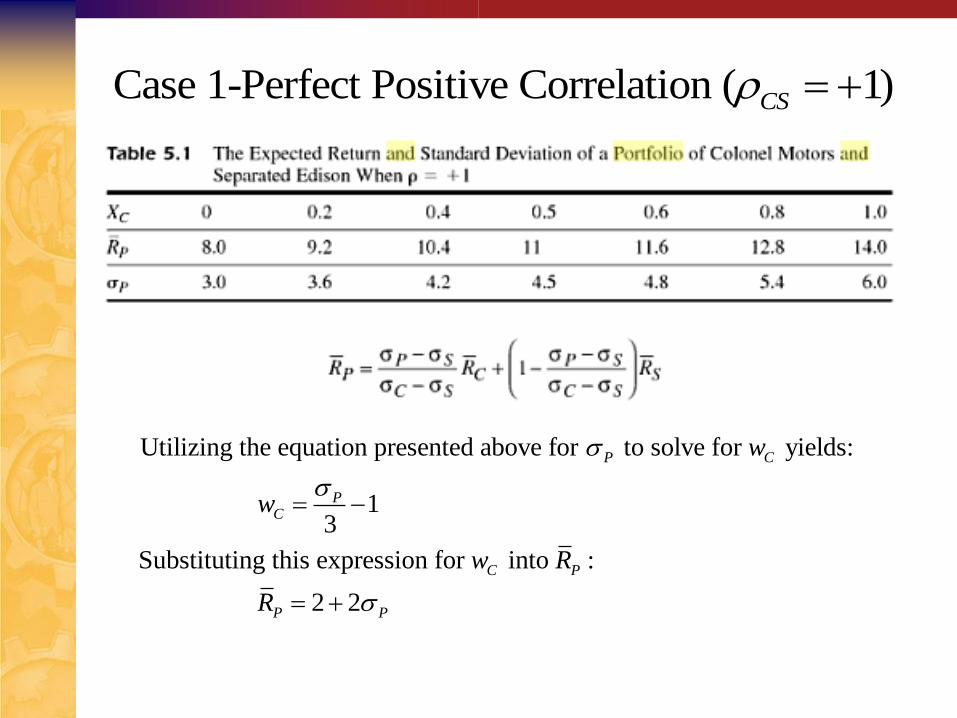

Case 1-Perfect Positive Correlation ( 1)CS

Utilizing the equation presented above for to solve for yields:

13

Substituting this expression for into :

2 2

P C

PC

C P

P P

w

w

w R

R

Relationship: E(R) vs Standard Deviation

Case 1-Perfect Positive Correlation ( 1)CS

Case-2 Perfect Negative Correlation (ρ=-1)

Stock Expected Return Standard Deviation

Colonel Motors 14% 6%

Separated Edison 8% 3%

122 2 2 2

2

Case 2-Perfect Negative Correlation ( 1)

1 2 1

If correlation coefficient is 1, then the equation for

the risk on portfolio, simplifies to:

6

CS

P C C C S C C C S CS

CS

P C C

w w w w

w

1

22 2 21 2 1C S C C C Sw w w

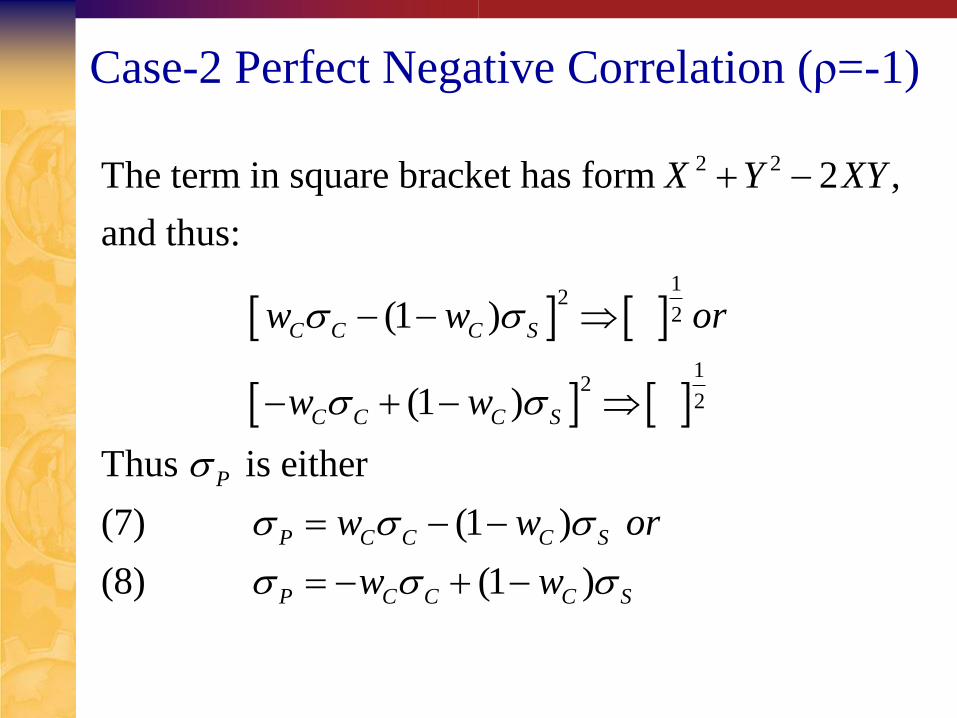

Case-2 Perfect Negative Correlation (ρ=-1)

2 2

12

2

12

2

The term in square bracket has form 2 ,

and thus:

(1 )

(1 )

Thus is either

(7) (1 )

(8) (1

C C C S

C C C S

P

P C C C S

P C C C

X Y XY

w w or

w w

w w or

w w

) S

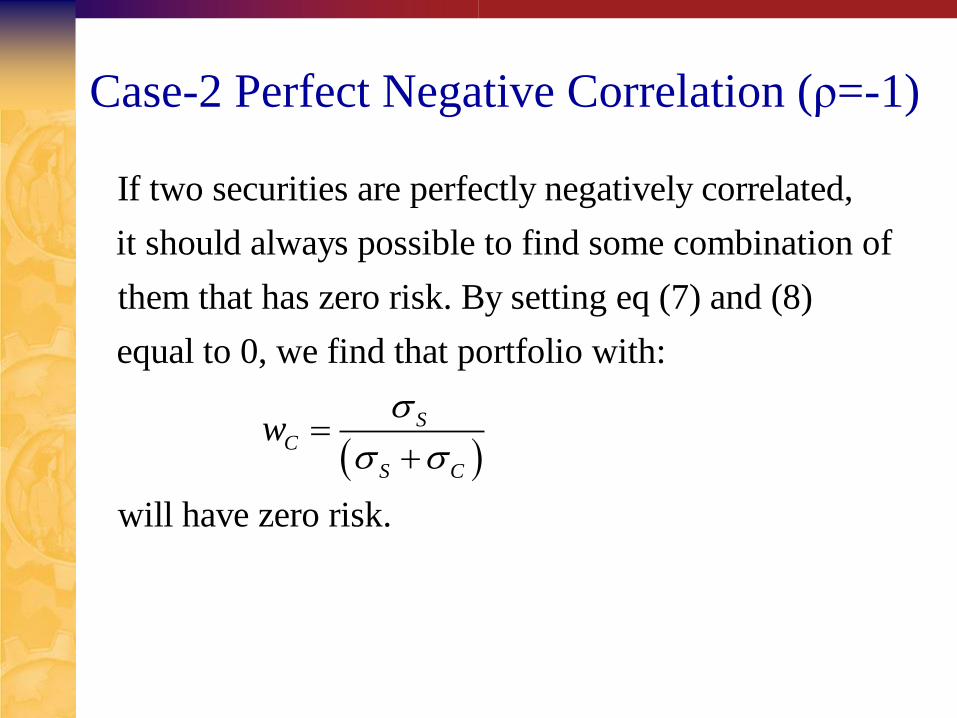

Case-2 Perfect Negative Correlation (ρ=-1)

If two securities are perfectly negatively correlated,

it should always possible to find some combination of

them that has zero risk. By setting eq (7) and (8)

equal to 0, we find that portfolio with:

will have zero risk.

SC

S C

w

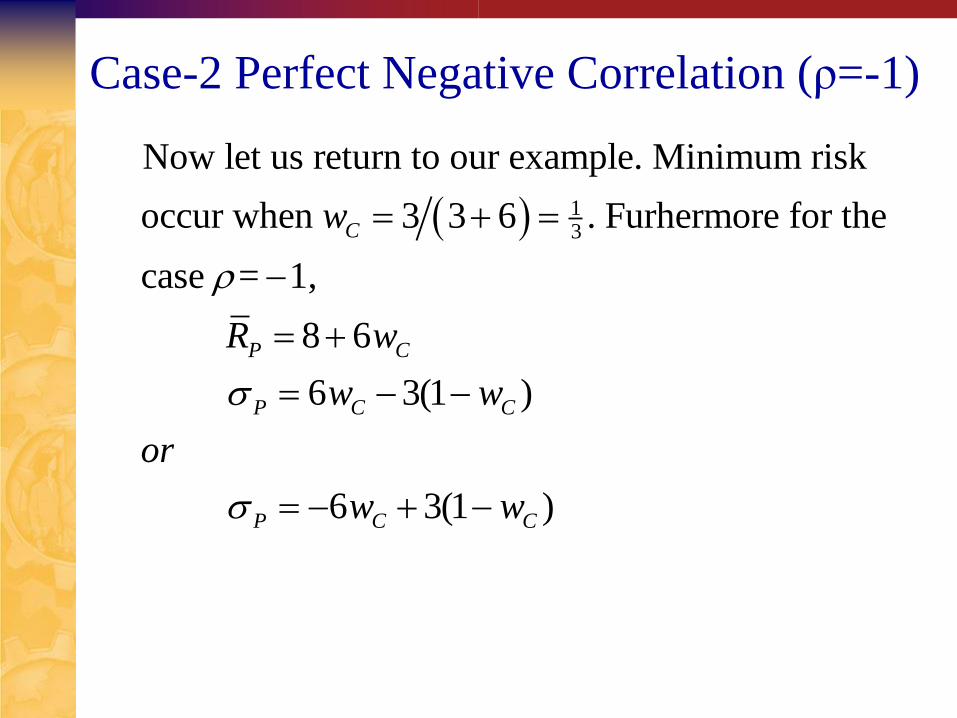

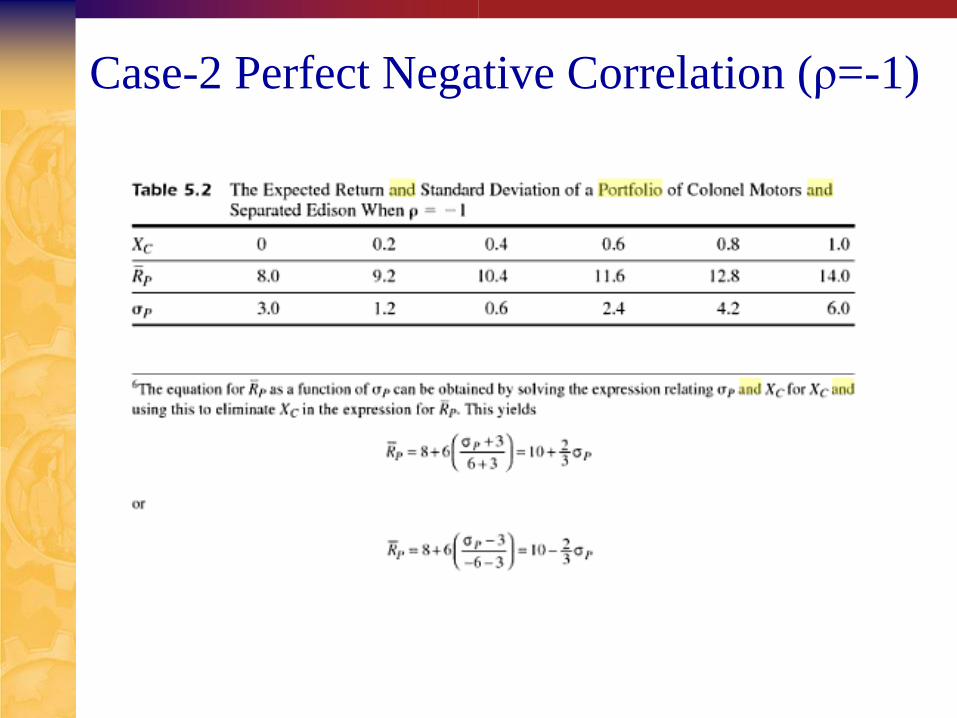

Case-2 Perfect Negative Correlation (ρ=-1)

13

Now let us return to our example. Minimum risk

occur when 3 3 6 . Furhermore for the

case = 1,

8 6

6 3(1 )

6 3(1 )

C

P C

P C C

P C C

w

R w

w w

or

w w

Case-2 Perfect Negative Correlation (ρ=-1)

There are two equation relating to . Only one is

appropriate for any value of . The appropriate equation

to define for any value of is that equation for

which 0.

See Table 5.2 and Figur

P C

C

P C

P

w

w

w

e 5.2

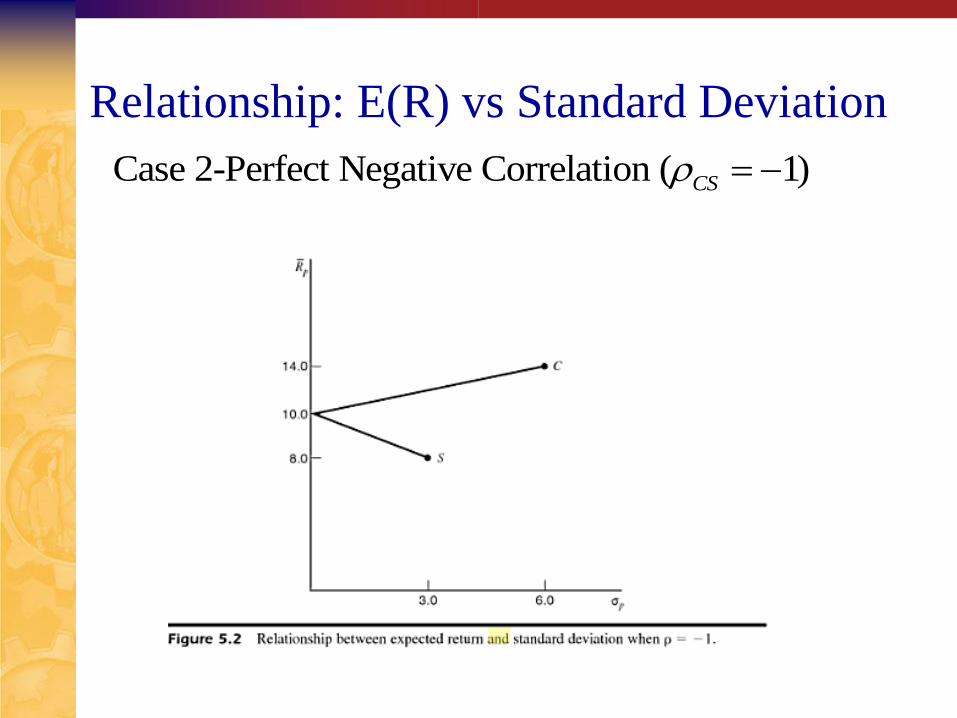

Case-2 Perfect Negative Correlation (ρ=-1)

Relationship: E(R) vs Standard Deviation

Case 2-Perfect Negative Correlation ( 1)CS

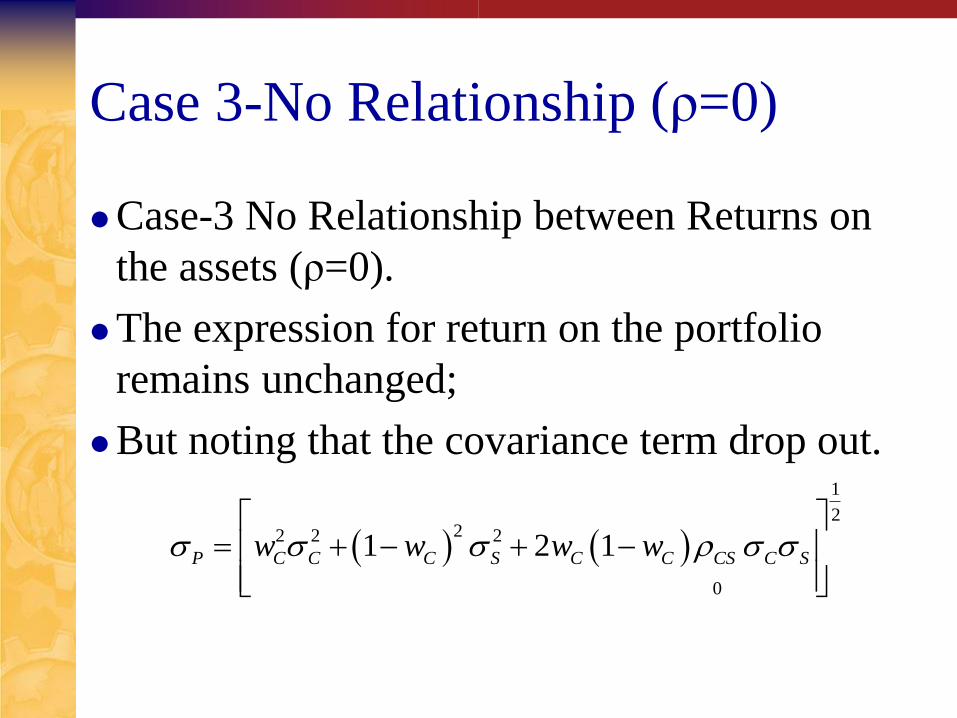

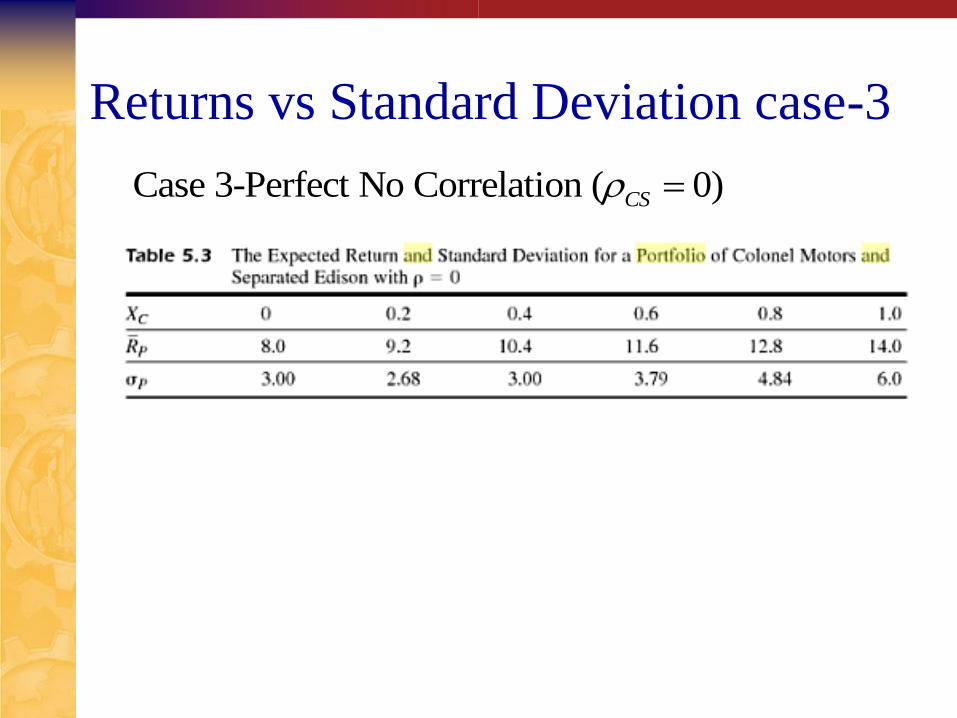

Case 3-No Relationship (ρ=0)

Case-3 No Relationship between Returns on

the assets (ρ=0).

The expression for return on the portfolio

remains unchanged;

But noting that the covariance term drop out.

1

222 2 2

0

1 2 1P C C C S C C CS C Sw w w w

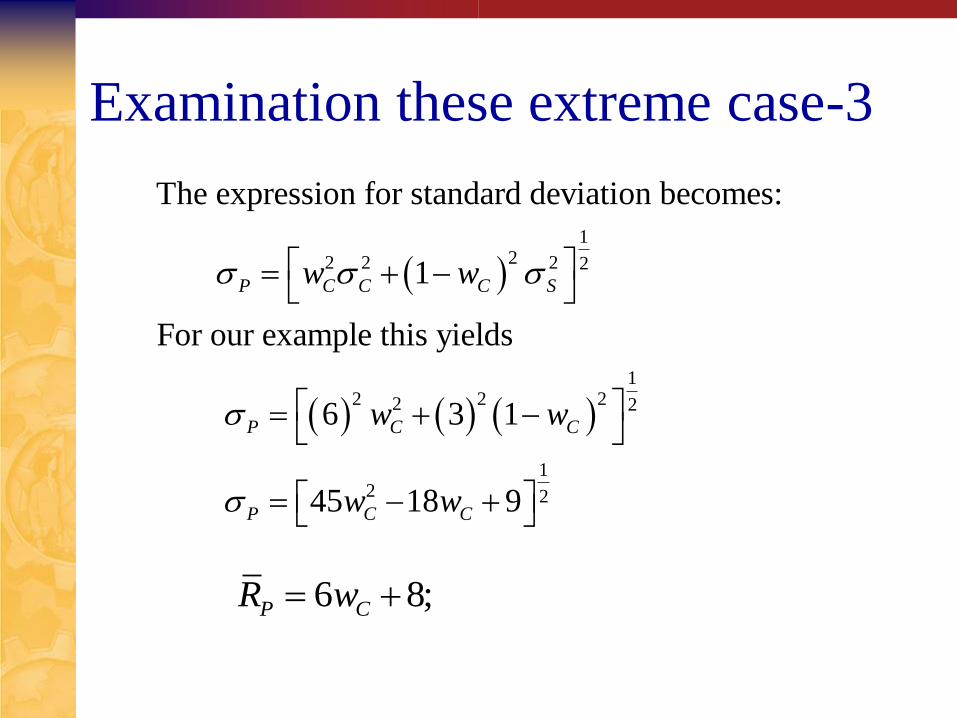

Examination these extreme case-3

122 2 2 2

12 2 22 2

12 2

The expression for standard deviation becomes:

1

For our example this yields

6 3 1

45 18 9

P C C C S

P C C

P C C

w w

w w

w w

6 8; P CR w

Returns vs Standard Deviation case-3

Case 3-Perfect No Correlation ( 0)CS

The Minimum Risk

1

22 2 2 2

The portfolio has minimum risk!. The portfolio can be found

in general by looking at the equation for risk:

1 2 1

To find the value of that minimize, take the deriv

P C C C S C C C S CS

C

w w w w

w

2 2 2

122 2 2 2

ative of it

with respect to , set derivative equal zero, and solve for :

2 2 2 2 41

21 2 1

C C

C C C C S C S CS C C S CSP

C

C C C S C C C S CS

w w

w w w

ww w w w

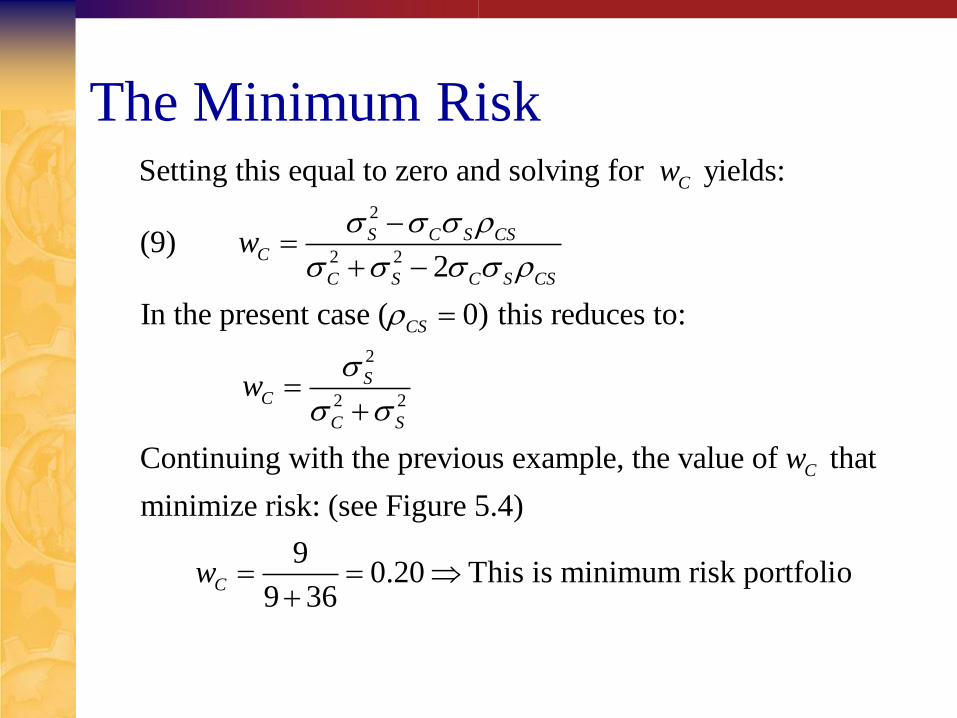

The Minimum Risk

2

2 2

2

2 2

Setting this equal to zero and solving for yields:

(9) 2

In the present case ( 0) this reduces to:

Continuing with the previous exampl

C

S C S CSC

C S C S CS

CS

SC

C S

w

w

w

e, the value of that

minimize risk: (see Figure 5.4)

9 0.20 This is minimum risk portfolio

9 36

C

C

w

w

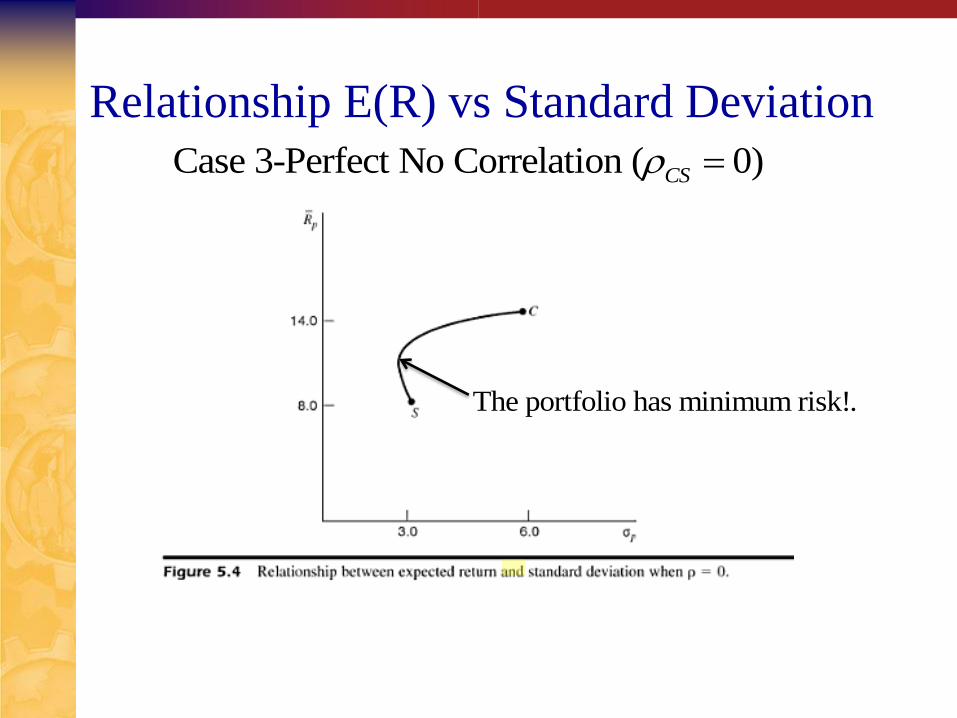

Relationship E(R) vs Standard Deviation

Case 3-Perfect No Correlation ( 0)CS

The portfolio has minimum risk!.

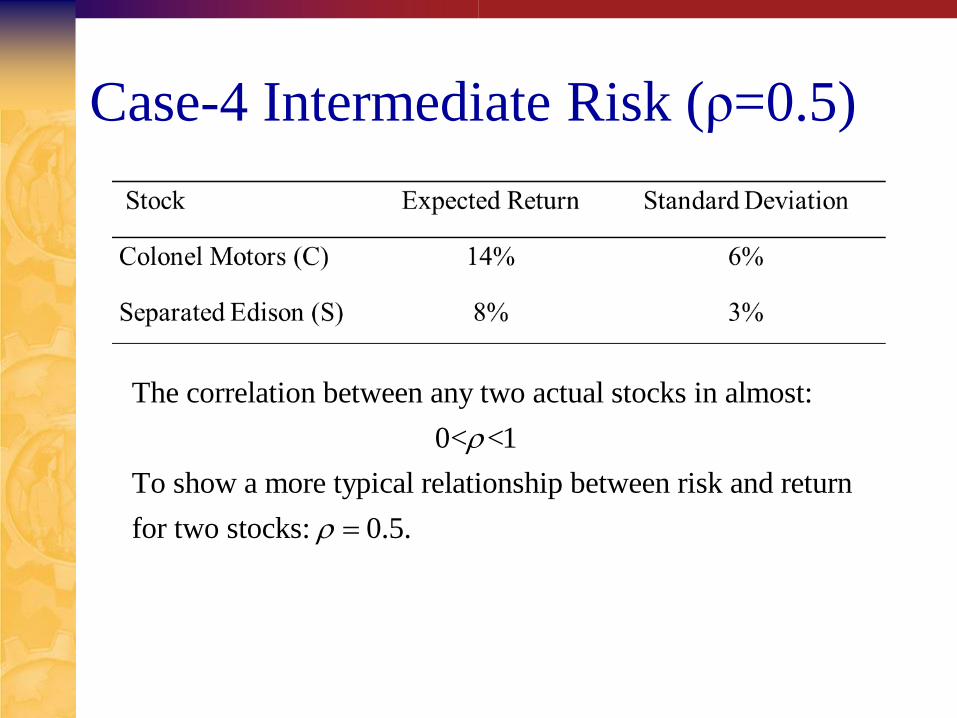

Case-4 Intermediate Risk (ρ=0.5)

The correlation between any two actual stocks in almost:

0< <1

To show a more typical relationship between risk and return

for two stocks: 0.5.

Case-4 Intermediate Risk (ρ=0.5)

12

122 2 2 2

12 2 22 21

2

2

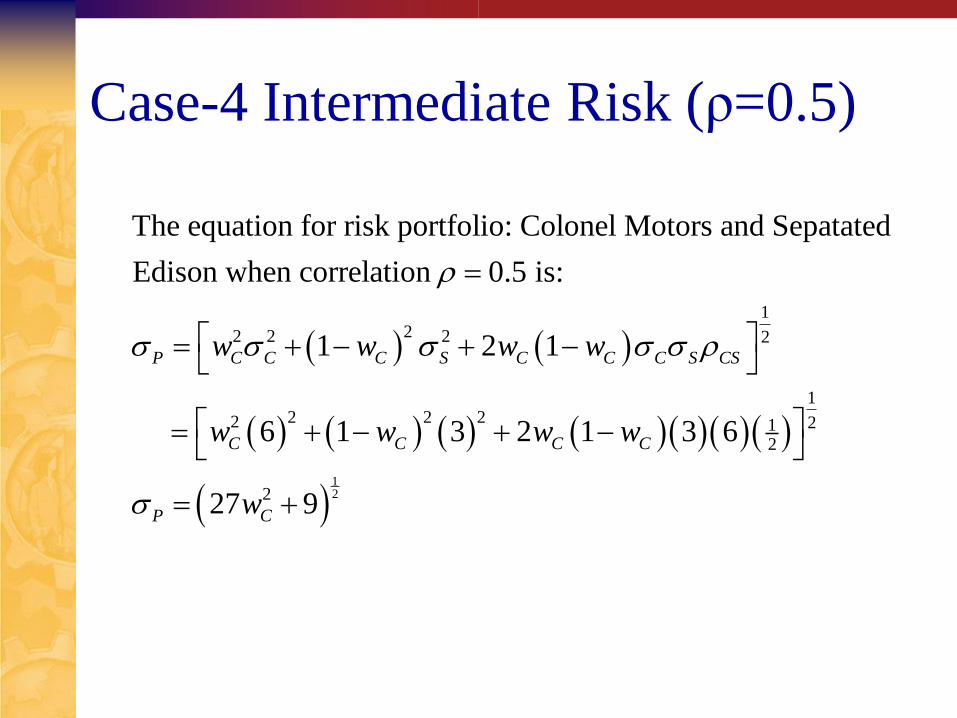

The equation for risk portfolio: Colonel Motors and Sepatated

Edison when correlation 0.5 is:

1 2 1

6 1 3 2 1 3 6

27 9

P C C C S C C C S CS

C C C C

P C

w w w w

w w w w

w

The Minimum Risk

2

2 2

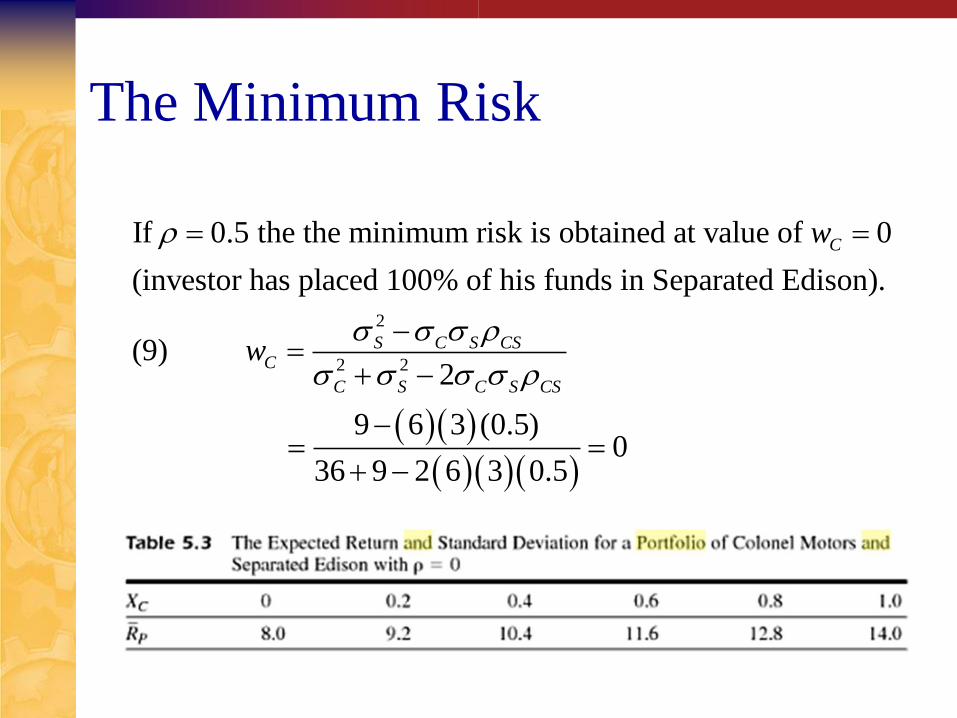

If 0.5 the the minimum risk is obtained at value of 0

(investor has placed 100% of his funds in Separated Edison).

(9) 2

9 6 3 (0.5)

36 9 2 6 3 0.

C

S C S CSC

C S C S CS

w

w

0

5

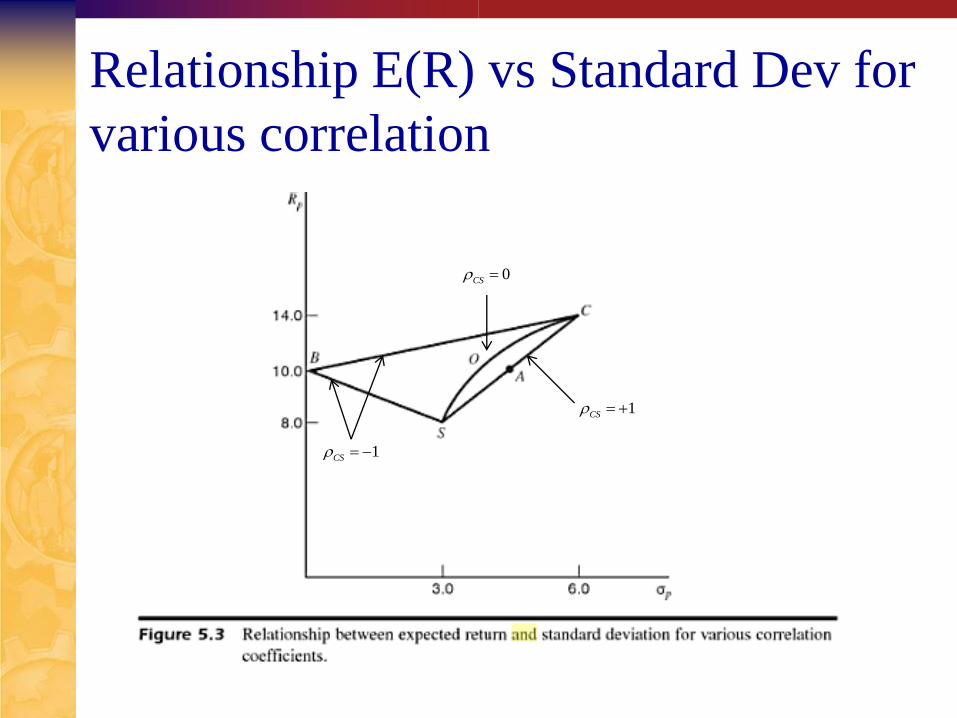

Relationship E(R) vs Standard Dev for

various correlation

1CS

0CS

1CS

Some insights into portfolio

First, we have noted that the lower (closer to -1) the

correlation coefficient between assets, all other

attributes held constant, the higher the payoff of

diversification.

Second, combination of two assets can never have

more risk than that found on a straight line connecting

the two assets.

Finally, Finding the minimum risk of portfolio

(variance) when two assets combined in a portfolio.

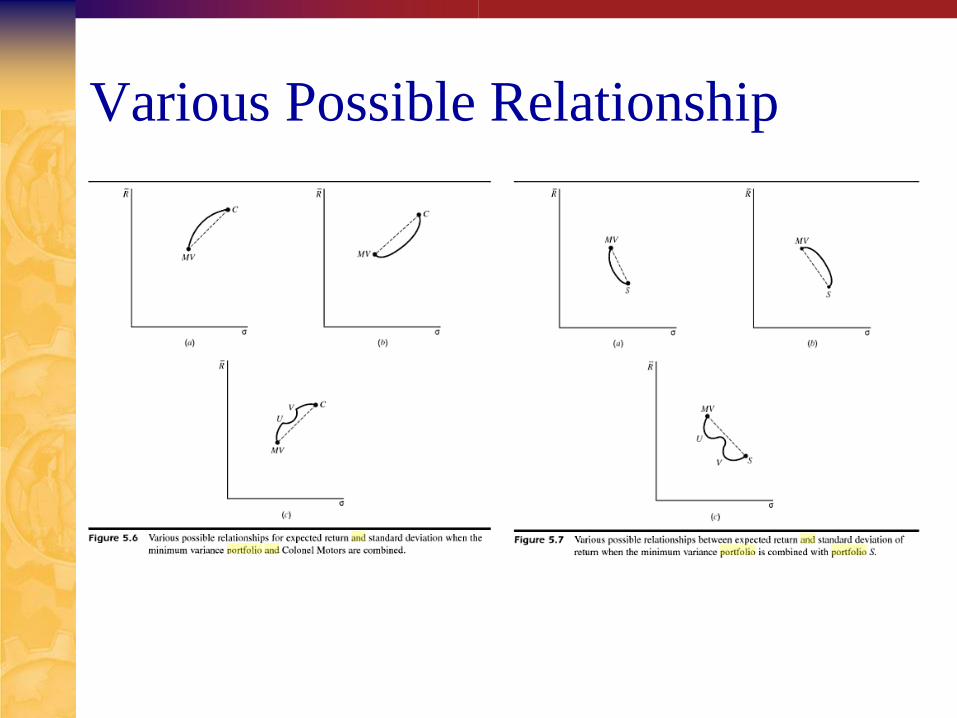

Various Possible Relationship

The efficient frontier (No short sales)

Risk Averter?

We reasoned that an investor would prefer

more return to less risk and would prefer less

risk to more.

Set of portfolio:

Offered a bigger return for the same risk, or

Offered a lower risk for the same return

Indentified all portfolio an investor could

consider holding.

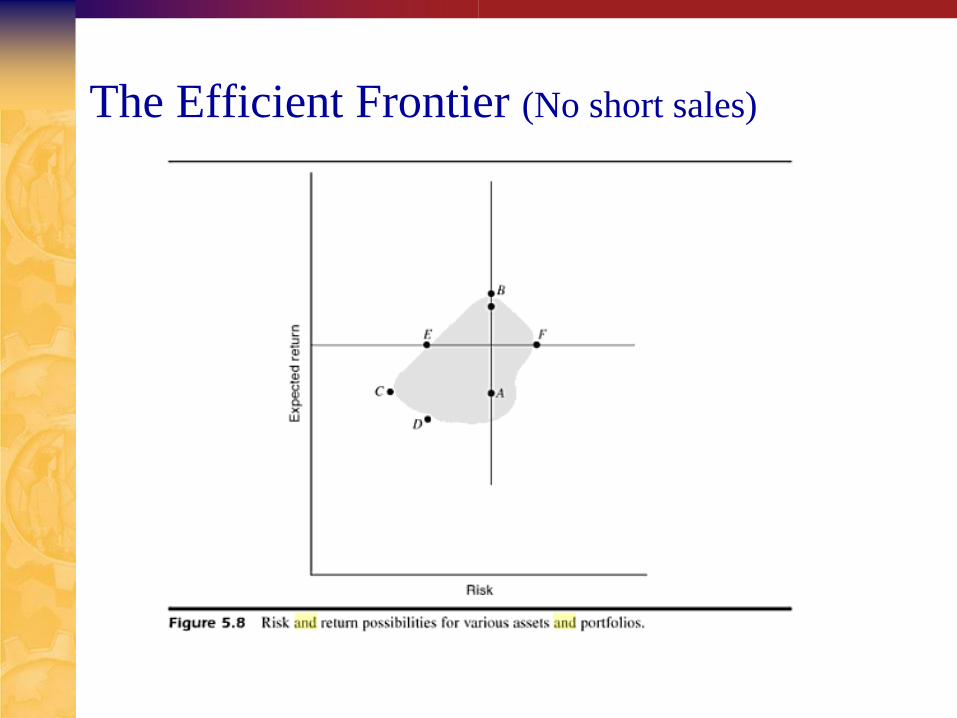

The Efficient Frontier (No short sales)

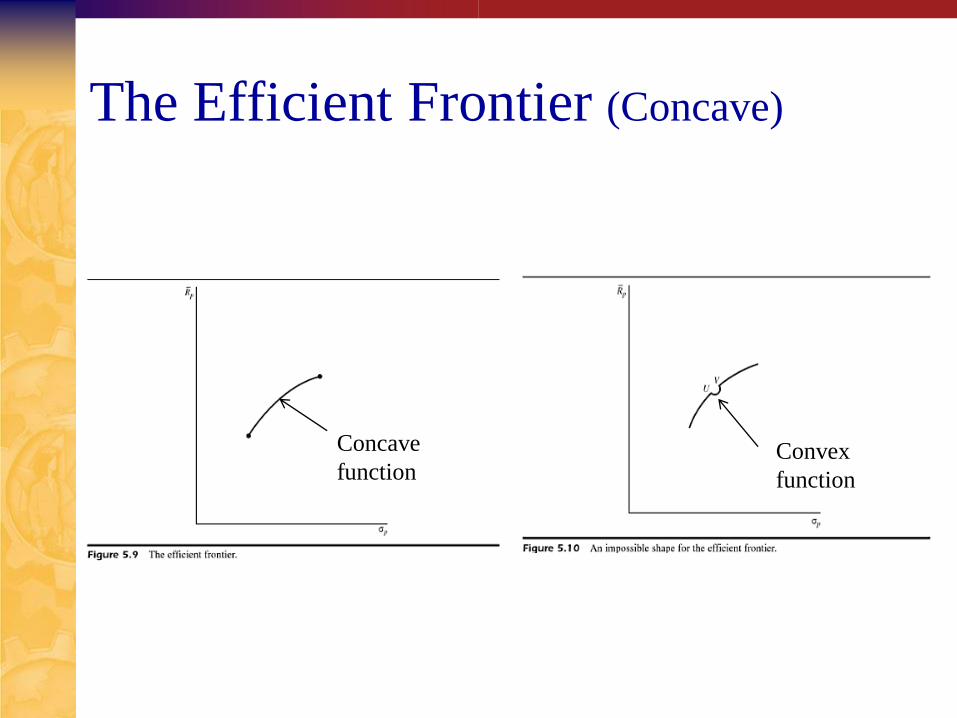

The Efficient Frontier (Concave)

Concave

function Convex

function

The Efficient Frontier

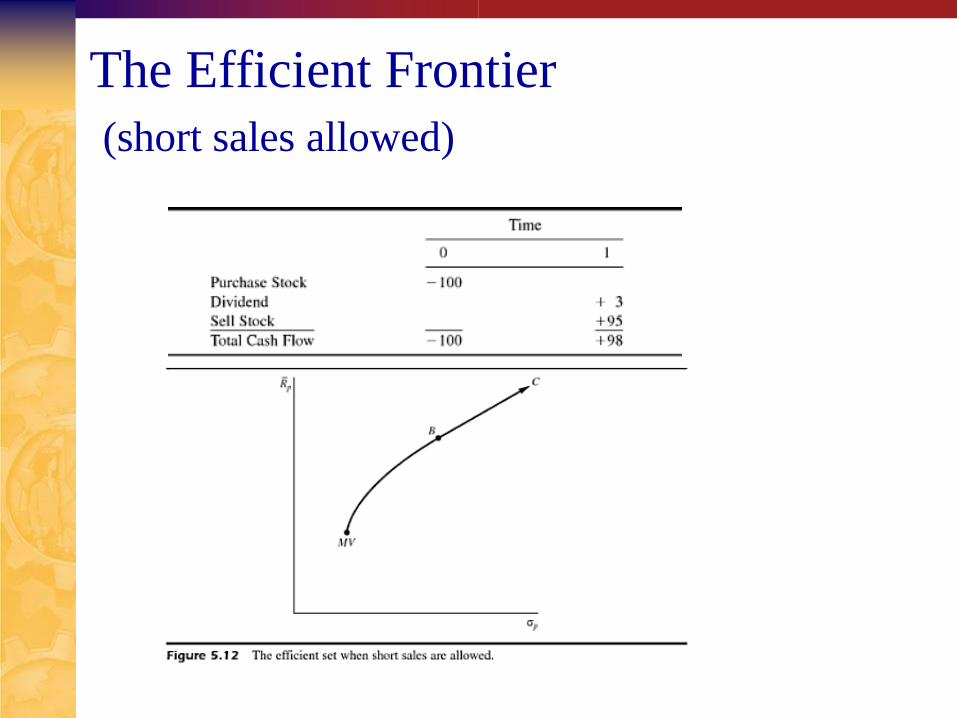

(short sales allowed)

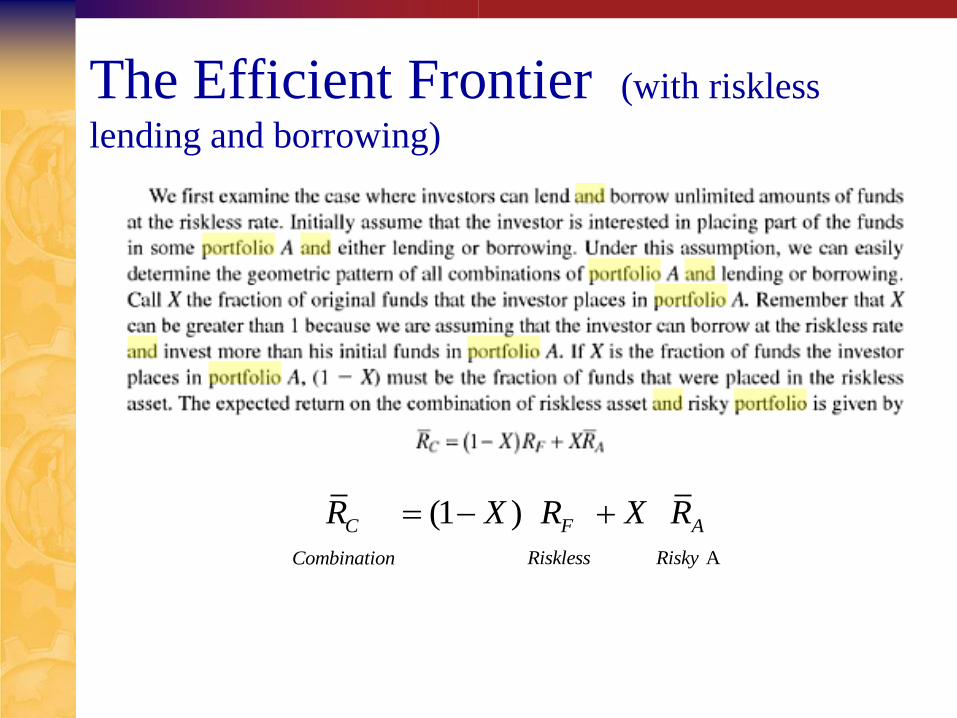

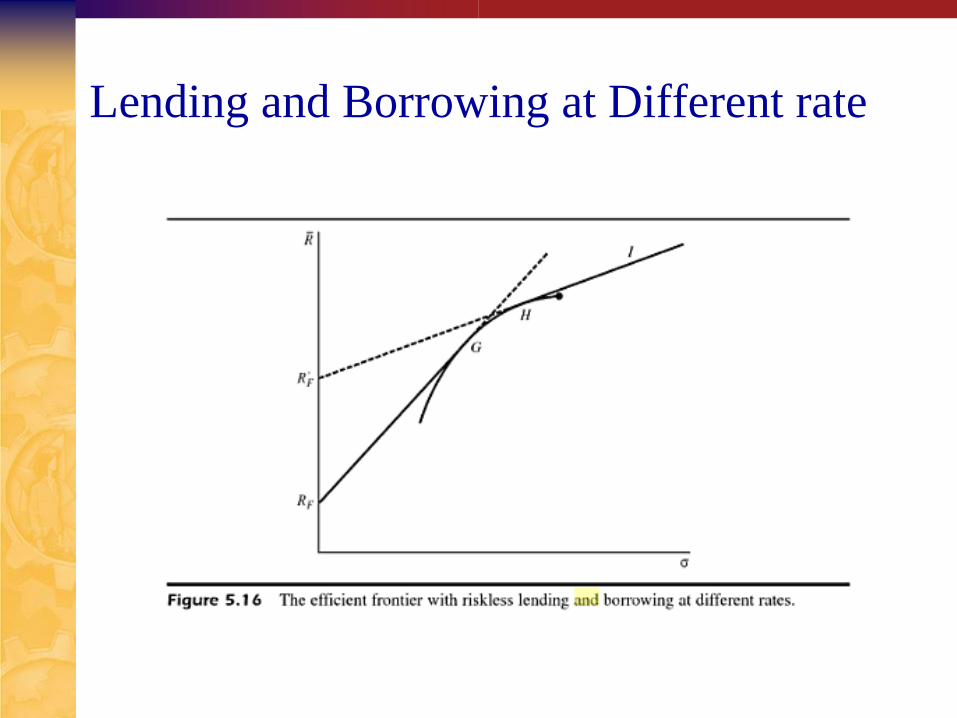

The Efficient Frontier (with riskless

lending and borrowing)

A

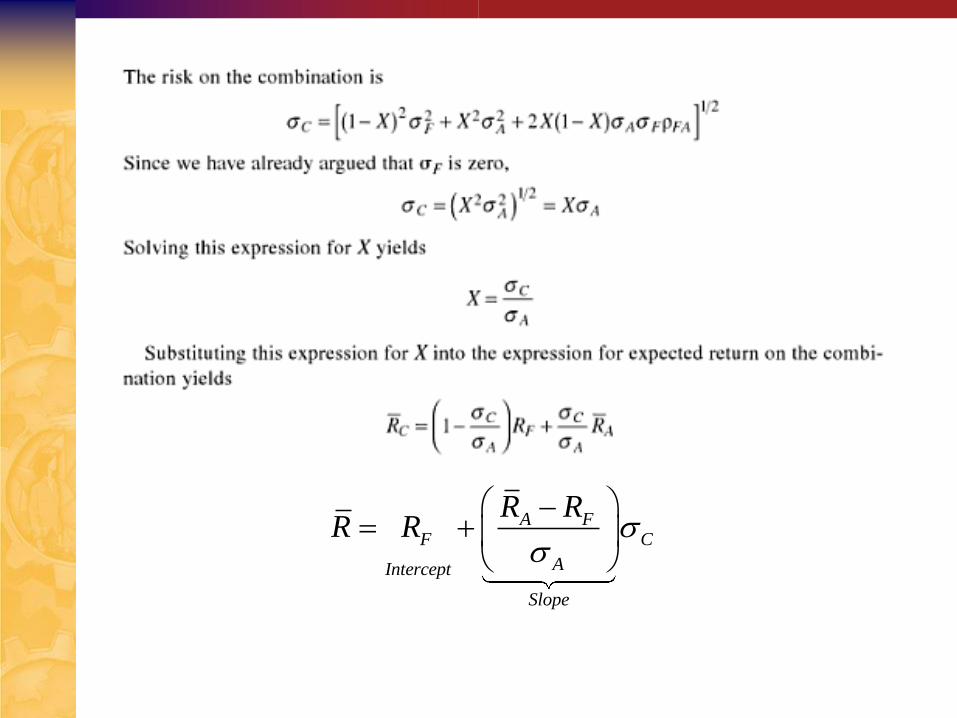

(1 )C F A

Riskless RiskyCombination

R X R X R

A FF C

AIntercept

Slope

R RR R

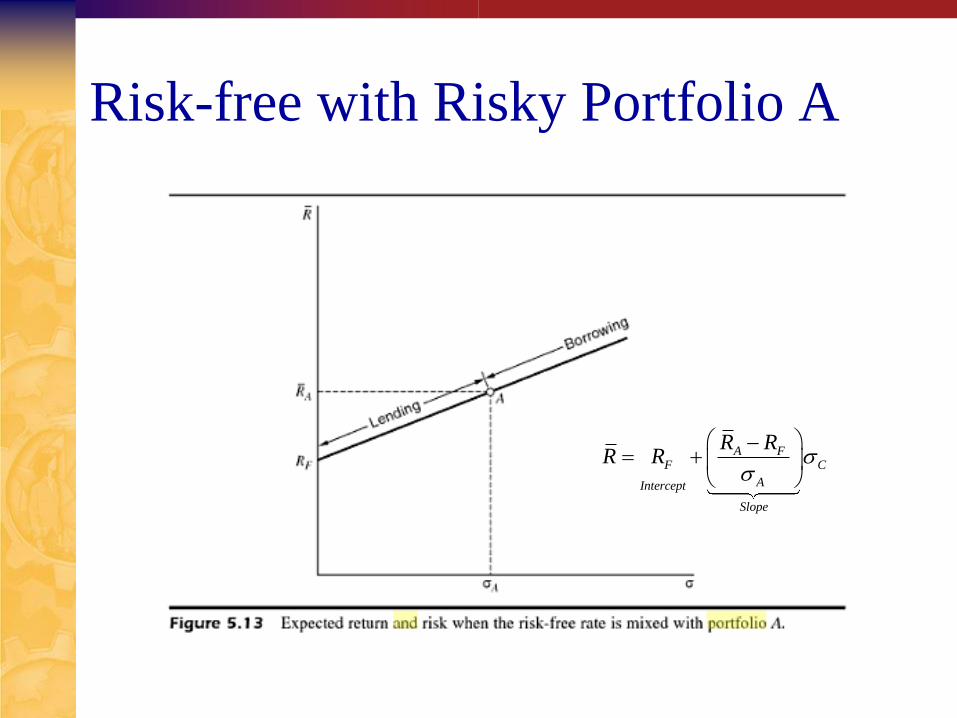

Risk-free with Risky Portfolio A

A FF C

AIntercept

Slope

R RR R

Lending and Borrowing at Different rate

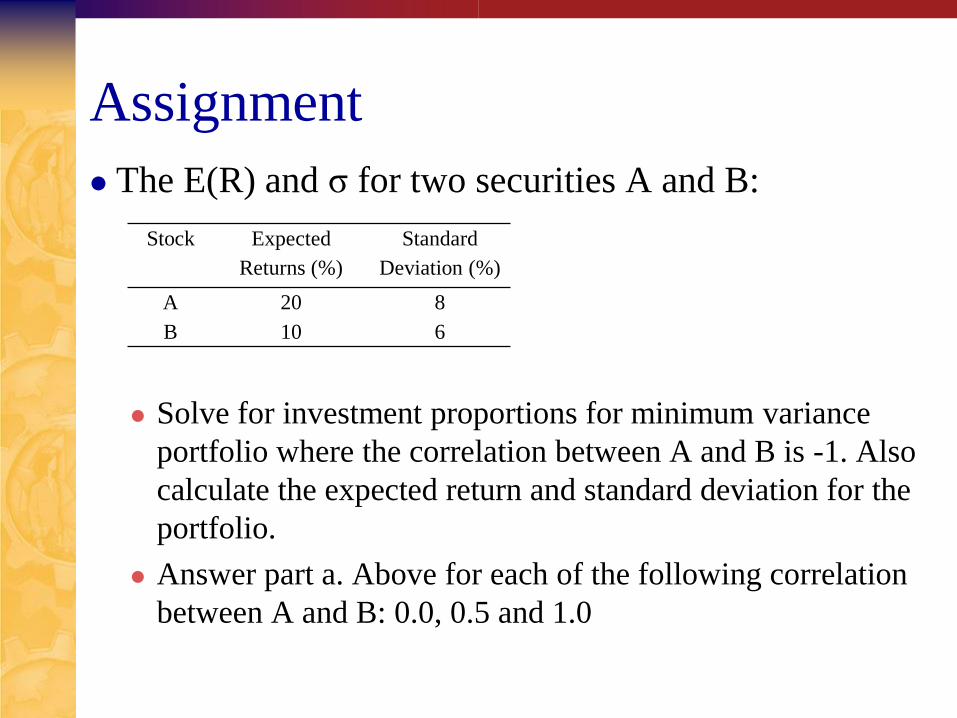

Assignment

The E(R) and σ for two securities A and B:

Solve for investment proportions for minimum variance

portfolio where the correlation between A and B is -1. Also

calculate the expected return and standard deviation for the

portfolio.

Answer part a. Above for each of the following correlation

between A and B: 0.0, 0.5 and 1.0

Stock Expected

Returns (%)

Standard

Deviation (%)

A 20 8

B 10 6

References

Elton, E.J, Gruber, M.J, et al (2003) Modern Portfolio

Theory and Investment Analysis, 6th Ed, Willey

International.

Brealy & Myers (2008) Principle of Corporate

Finance, 7th Ed, McGraw-Hill, USA

Martin, John.D et al (1988) Theory of Finance:

Evidence & Applications, The Dryden Press, NY.