Embed Size (px)

Citation preview

EAT & DRINK LONDON

Eat & Drink London INSIGHT INTO THE PROPERTY MARKET THAT SERVES LONDON’S FOOD AND BEVERAGE SECTOR

2 3

EAT & DRINK LONDON

3

EAT & DRINK LONDON

RESEARCH SCOPE

70%dining

30%drinking

400+independents

70+branded offers

570outlets

12locations

WELCOMEEat & Drink London is a new Colliers International research study which provides unique insights into the property market that serves London’s rapidly evolving food and beverage sector. To create this groundbreaking research, we have identified 12 locations across the Capital where the proliferation of restaurants and bars is booming.

Each of our studies will focus on an established location and also one that is on the upgrade.

In this report we look at Mayfair, the epicentre of fine dining in London, and also the emerging dining scene around Middlesex Street E1 – an area which is emblematic of the revolution in the eating and drinking scene around the Square Mile and its fringes.

We hope you find this research useful and would be delighted to discuss its findings with you.

Cover image: Kingly Court at Carnaby StreetThis page: Wahaca on Charlotte Street

2

5

EAT & DRINK LONDON

4

THE RENTAL LANDSCAPE

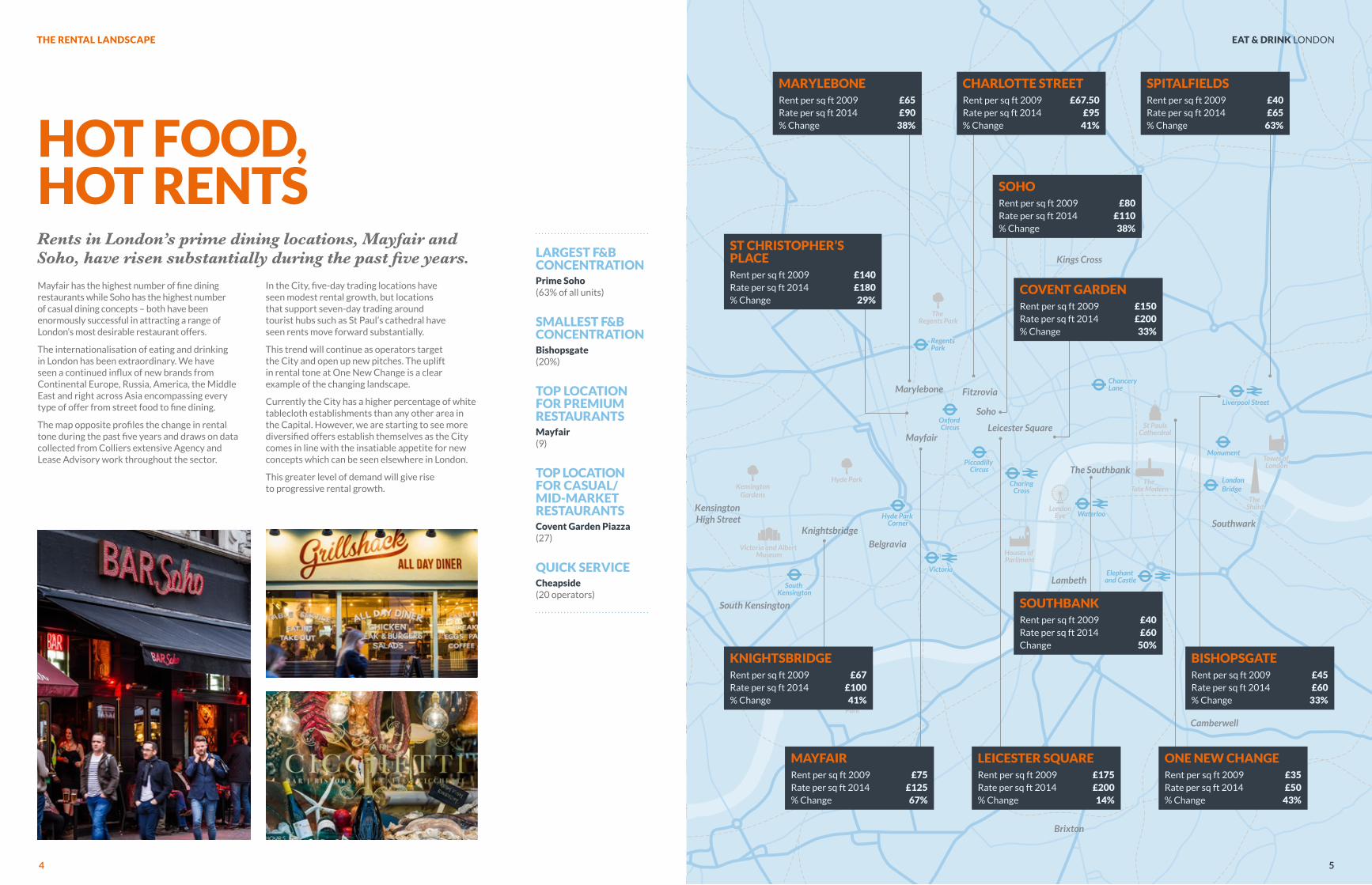

HOT FOOD, HOT RENTS

Mayfair has the highest number of fine dining restaurants while Soho has the highest number of casual dining concepts – both have been enormously successful in attracting a range of London’s most desirable restaurant offers.

The internationalisation of eating and drinking in London has been extraordinary. We have seen a continued influx of new brands from Continental Europe, Russia, America, the Middle East and right across Asia encompassing every type of offer from street food to fine dining.

The map opposite profiles the change in rental tone during the past five years and draws on data collected from Colliers extensive Agency and Lease Advisory work throughout the sector.

In the City, five-day trading locations have seen modest rental growth, but locations that support seven-day trading around tourist hubs such as St Paul’s cathedral have seen rents move forward substantially.

This trend will continue as operators target the City and open up new pitches. The uplift in rental tone at One New Change is a clear example of the changing landscape.

Currently the City has a higher percentage of white tablecloth establishments than any other area in the Capital. However, we are starting to see more diversified offers establish themselves as the City comes in line with the insatiable appetite for new concepts which can be seen elsewhere in London.

This greater level of demand will give rise to progressive rental growth.

Rents in London’s prime dining locations, Mayfair and Soho, have risen substantially during the past five years. LARGEST F&B

CONCENTRATIONPrime Soho (63% of all units)

SMALLEST F&B CONCENTRATIONBishopsgate (20%)

TOP LOCATION FOR PREMIUM RESTAURANTSMayfair (9)

TOP LOCATION FOR CASUAL/MID-MARKET RESTAURANTSCovent Garden Piazza (27)

QUICK SERVICECheapside (20 operators)

Lambeth

Belgravia

Mayfair

Marylebone Fitzrovia

Southwark

South Kensington

Kensington High Street

Brixton

Camberwell

Soho

Holloway

Leicester Square

Knightsbridge

The Southbank

Kings Cross

The Regents Park

The Shard

Tower of London

Hyde ParkKensington

Gardens

BatterseaPark

The Tate Modern

St PaulsCatherdral

LondonEye

Houses of Parliment

Victoria and Albert Museum

Hyde Park Corner

Victoria

CharingCross

Piccadilly Circus

Oxford Circus

Regents Park

ChanceryLane

London Bridge

Monument

South Kensington

Waterloo

Elephant and Castle

Liverpool Street

Kings Cross St Pancras

Hyde Park Corner

Victoria

CharingCross

Piccadilly Circus

Oxford Circus

Regents Park

ChanceryLane

London Bridge

Monument

South Kensington

Waterloo

Elephant and Castle

Liverpool Street

Kings Cross St Pancras

BISHOPSGATERent per sq ft 2009 £45Rate per sq ft 2014 £60% Change 33%

MAYFAIRRent per sq ft 2009 £75Rate per sq ft 2014 £125% Change 67%

KNIGHTSBRIDGERent per sq ft 2009 £67 Rate per sq ft 2014 £100% Change 41%

LEICESTER SQUARERent per sq ft 2009 £175Rate per sq ft 2014 £200% Change 14%

SOHORent per sq ft 2009 £80Rate per sq ft 2014 £110% Change 38%

SPITALFIELDSRent per sq ft 2009 £40Rate per sq ft 2014 £65% Change 63%

MARYLEBONERent per sq ft 2009 £65Rate per sq ft 2014 £90% Change 38%

CHARLOTTE STREETRent per sq ft 2009 £67.50Rate per sq ft 2014 £95% Change 41%

SOUTHBANKRent per sq ft 2009 £40Rate per sq ft 2014 £60 Change 50%

ST CHRISTOPHER’S PLACERent per sq ft 2009 £140Rate per sq ft 2014 £180% Change 29%

COVENT GARDENRent per sq ft 2009 £150Rate per sq ft 2014 £200% Change 33%

ONE NEW CHANGERent per sq ft 2009 £35Rate per sq ft 2014 £50% Change 43%

5

EAT & DRINK LONDON

6

PLANNING CAN BE THE KEY TO MAYFAIR

Its restaurant market is currently enjoying unprecedented levels of demand despite rents spiralling upwards.

Demand in Mayfair is almost exclusively from the premium/fine dining segment of the market and is now being predominantly led by new international concepts looking for representation in London. Around two thirds of recent lettings in prime Mayfair locations have been to international operators.

Berkeley Street has quickly become a particularly favoured pitch for international restaurant concepts with a new and exciting line up emerging to join Novikov and Nobu.

This influx has driven up the entry costs and enabled landlords to be extremely selective when accepting new offers. The marketing of the former NatWest bank building on Berkeley Square vividly illustrated this when Caprice Holdings had to beat off competition from 17 other high quality operators for the prominent corner unit at a rent of £1.1m.

In these circumstances, it’s not surprising that leases are changing hands for multi-million pound premiums. Historically the level of premium that was paid for a lease was predicated on a multiple of net profit. However, in such a fiercely competitive market this correlation no longer applies: operators are

essentially prepared to pay substantial ‘key money’ purely to get a foothold in Mayfair.

Where new leases are being granted the prevailing rental tone is around 67% higher than five years ago.

With demand high and supply tightening, a robust approach to planning is increasingly important to securing the right property.

Westminster Council’s Unitary Development Plan stipulates that new leisure uses of over 500 sq metres can only be granted in exceptional circumstances. This has historically been tough to challenge but there are now signs that there is more scope for securing a change of use.

A recent planning appeal decision in Grosvenor Square made it clear that a large restaurant should be granted consent as the UDP policies were deemed to be outdated in the light of the new national guidance in the National Planning Policy Framework. Westminster was unable to identify specific harm arising from the proposal and so the much-vaunted ‘presumption in favour of sustainable development’ prevailed.

The message for operators and landlords who want to unlock the restaurant or leisure potential of Mayfair properties is that they need to have access to advice which encompasses both the A3 occupational market and also planning strategy.

There are many new locations that are developing a burgeoning eating and drinking scene in London, but the sheer quality of the Mayfair offer remains unequalled.

• Unprecedented levels of operator demand driven by international market entrants

• Prime rents up by 67% in past five years

• Berkeley Street establishing new status as prime pitch

• Robust approach to planning can unlock site potential

• Substantial premiums becoming the norm as demand continues to outweigh supply

• Gordon Ramsay takes lease on the former The Living Room in Heddon Street at £115 per sq ft

• Café Pushkin, Bocconcino and Caprice Holdings receive A3 planning consent for their new outlets

• Russian restaurateur Arkady Novikov acquires the Dover Street Wine Bar for a reported £1.6m premium

A TASTER

6

SPOTLIGHT MAYFAIR EAT & DRINK LONDON

MAYFAIR BY NUMBERS

22% are casual/

mid-market category

67% of the drinks

offers serve alcohol

56% of food operators were

premium/fine dining

33% of the drinks

offers are cafes

28% were quick

service

of Mayfair units surveyed are traded by a food & beverage operator Food Offers Drinks-led

Branded operators

Independent (<5 branches)

7

8 9

EAT & DRINK LONDONON THE UP

MIDDLESEX STREET E1

But today if you’re peckish and on the eastern fringe of the City there are good reasons to check out the eateries of Middlesex Street.

An area that can boast a street called Frying Pan Alley is always going to have potential for the food business. It has been steadily attracting hip independent and multiple retailers along with bar and restaurant operators and is following the lead set by development in and around Spitalfields Market.

The location has developed a tremendous demographic cross-section. ‘City types’ mingle with a younger set drawn from new student accommodation developments while the residential towers being built around Aldgate are bringing an influx of new affluent permanent residents.

As a consequence, the area around Middlesex Street has become a 6-7 day trading location – in contrast to the majority of Square Mile where bar and restaurant opening tends to still be confined to the working week.

The initial focus for A3 operators in the eastern City fringe was for representation in Spitalfields Market or Shoreditch, but as competition for sites increased so demand has spread to Middlesex Street, Widegate Street, Artillery Lane, Steward Street and Strype Street creating an upward pressure on rents.

Earlier this year Honest Burger paid an open market rent of £55 per sq ft to secure its outlet on Widegate Street while Byron’s Steward Street rent review was settled at nearly £63 per sq ft.

Another influence is the nearby Devonshire Square estate which has become a focus for foodies with a regular world food market and Mark Hix becoming the latest arrival in the square alongside fellow super chef, Marco Pierre White.

Blackstone owns the 630,000 sq ft Devonshire Square estate and is now delivering a strategy to improve the tenant mix and make the square a seven-days-a-week destination.

Against this backdrop of improvement, our data indicates that top A3 rental levels in the Middlesex Street area have increased by more than 50% in the past five years. This uplift has been achieved ahead of the 2018 arrival of the new Crossrail station at Whitechapel which will bring a further boost to the area.

We believe that with major new local development, existing high-quality environments such as Devonshire Square, and a rapidly improving demographic profile, Middlesex Street and its environs will continue on an upward trajectory as a place to eat and drink in London.

Not very long ago, if you’d found yourself in Middlesex Street you might have been en route to Petticoat Lane market or heading to Brick Lane for a curry.

8

• Fresh development and revitalised schemes such as Devonshire Square are leading a eating and drinking renaissance in the area

• Exciting existing operators including The Breakfast Club, Grapeshots, La Tagliata and the William Ale & Cider House are encouraging new concepts to come to the area

• The area is developing into a seven-days-a week trading environment

• Top rents have risen by c50% in the past five years

• Residential development around Aldgate is bringing new permanent affluent residents while Crossrail will transform access

• The restaurant units at Helical Bar’s new Artillery Lane development are being marketed at c.£60 per sq ft on best space

• 11 Artillery Passage: unit let to Ottolenghi at c.£60 per sq ft

A TASTER

9

EAT & DRINK LONDON

FRESH DEVELOPMENT AND REVITALISED SCHEMES SUCH AS DEVONSHIRE SQUARE ARE LEADING A NEW EATING AND DRINKING SCENE IN THE AREA

COLLIERS INTERNATIONAL

10

CHAINS VS INDYS

NATIONAL COVERAGE, LONDON SPECIALISM

It is one of the most innovative and diverse parts of the UK economy, and our service covers casual dining and fine dining restaurants, themed and branded bars, traditional pubs, gastro pubs and nightclubs through to coffee shops and grab-and-go ‘street food’ outlets.

The combined approach of our Agency and Lease Advisory teams, who have exhaustive market knowledge, has proven successful in securing the best possible outcomes for our landlord and occupier clients throughout Central London.

An integral part of our offer is the Central London Lease Advisory Team which has a proven track record of negotiating the best possible outcomes for our landlord and occupier clients. Working closely alongside its Central London Agency colleagues, the team has complete market coverage.

Meticulous market research is at the heart of the Colliers service and we are able to produce targeted market perspectives which relate to the specific needs of clients.

Through its Agency, Lease Advisory and specialist Licensed & Leisure teams, Colliers International provides a comprehensive service across the UK food, beverage and leisure market.

DAN TAYLORHead of Central London Retail Lease Advisory

020 7344 6871 [email protected]

MARK CHARLTONHead of Research & Forecasting

020 7487 1720 [email protected]

ROSS KIRTONDirector – Agency, Licensed & Leisure

020 7487 [email protected]

CONTACTS

CHAINS VS INDYS WHO’S DOING WHAT AND WHERELondon offers a magnificent diversity of places to eat and drink but the split between independent operators and branded chains is very different depending on where you are in the capital.

It will be fascinating to see how this mix changes over time…

90%

TOP LOCATIONS FOR…

Prime Soho

Regent St

Charlotte St

Independent Operators

81%

79%

One New Change

Covent Garden

Spitalfields

Branded Chain Operators

58%

45%

41%

SPLIT BETWEEN CHAIN AND INDEPENDENT OPERATORS ACROSS RESEARCH SAMPLE

28% Chains

72% Independent

CITY VS SOHO

Independent Chain

55%

45%

91%

9% City Soho

11

COLLIERS INTERNATIONAL | LONDON 50 GEORGE STREET LONDON W1U 7GA | UK

+44 20 7935 4499

WWW.COLLIERS.COM/UK

Designed and produced by THE GROUP www.completelygroup.com

This report gives information based primarily on Colliers International data, which may be helpful in anticipating trends in the property sector. However, no warranty is given as to the accuracy of, and no liability for negligence is accepted in relation to, the forecasts, figures or conclusions contained in this report and they must not be relied on for investment or any other purposes. This report does not constitute and must not be treated as investment or valuationadvice or an offer to buy or sell property. (Nov 2014) © 2014 Colliers International. Colliers International is the licensed trading name of Colliers International Property Advisers UK LLP which is a limited liability partnership registered in England and Wales with registered number OC385143. Our registered office is at 50 George Street, London W1U 7GA