Embed Size (px)

Citation preview

i

Earned Income Credit

ii

ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER.

Purchase of a course includes a license for one person to use the course materials. Absent specific

written permission from the copyright holder, it is not permissible to distribute files containing course materials or printed versions of course materials to individuals who have not purchased the course. It is also not permissible to make the course materials available to others over a computer network, Intranet, Internet, or any other storage, transmittal, or retrieval system. This document is designed to provide general information and is not a substitute for professional advice in specific situations. It is not intended to be, and should not be construed as, legal or accounting advice which should be provided only by professional advisers.

iii

Contents

Introduction to The Course ..................................................................................................... 1 Learning Objectives ............................................................................................................... 1

Chapter 1 – Earned Income Credit Rules ................................................................ 2 Introduction ......................................................................................................................... 2 Learning Objectives ............................................................................................................... 2 Eligibility to Receive EIC ......................................................................................................... 2

EIC Rules Applicable to Everyone ......................................................................................... 2 Adjusted Gross Income Limits ........................................................................................... 2 Valid Social Security Number Required ............................................................................... 3 Tax Filing Status .............................................................................................................. 3 Citizenship or Residency ................................................................................................... 3 Foreign Earned Income .................................................................................................... 4 Investment Income ......................................................................................................... 4 Earned Income ................................................................................................................ 4

EIC Rules That Apply Only if the Taxpayer Has a Qualifying Child ............................................. 4 Relationship, Age, Residence and Joint Return Tests ............................................................ 4

The Relationship Test .................................................................................................... 4 The Age Test ................................................................................................................ 5

Student Defined ......................................................................................................... 5 Permanently and Totally Disabled Defined ..................................................................... 6

The Residency Test ....................................................................................................... 6 Exception for U.S. Military Stationed Outside the U.S. .................................................... 6

The Joint Return Test .................................................................................................... 6 Child Must Have Valid Social Security Number .................................................................. 6

Qualifying Child of More than One Person Rule .................................................................... 7 Tiebreaker Rules ........................................................................................................... 7

Qualifying Child of Another Taxpayer Rule .......................................................................... 7 EIC Rules That Apply if Taxpayer Does Not Have a Qualifying Child .......................................... 8

The Age Rule .................................................................................................................. 8 Death of Spouse During Year .......................................................................................... 8

The Dependent of Another Person Rule .............................................................................. 8 The Qualifying Child of Another Taxpayer Rule .................................................................... 8 The Main Home Rule ........................................................................................................ 9

Figuring the Amount of the Earned Income Credit ..................................................................... 9 Calculating Earned Income for EIC Purposes .......................................................................... 9

Taxpayers Not Self-Employed, Statutory Employees, Clergy or Church Employees ................... 9 Self-Employed Taxpayers, Statutory Employees, Clergy and Church Employees .....................11

Summary ............................................................................................................................15 Chapter Review ...................................................................................................................15

Chapter 2 – Earned Income Credit Errors ............................................................. 17 Introduction ........................................................................................................................17 Learning Objectives ..............................................................................................................17 Incidence of Earned Income Credit Errors................................................................................17 Factors Leading to Earned Income Credit Errors .......................................................................18 Estimated Revenue Impact of Earned Income Credit Errors .......................................................18 Common Earned Income Credit Errors ....................................................................................19

Earned Income Credit Errors Involving Qualifying Children .....................................................19 Qualifying Child Requirements ..........................................................................................19

When a Child is Disabled ...............................................................................................20 Avoiding Qualifying Child Earned Income Credit Errors ........................................................20

iv

Earned Income Credit Errors Involving a Client’s Filing Status .................................................20 Single Filing Status .........................................................................................................21 Head of Household Filing Status .......................................................................................21

Married Persons Living Apart .........................................................................................21 Avoiding Filing Status Earned Income Credit Errors .............................................................22

Earned Income Credit Errors Involving Income Reporting .......................................................22 Avoiding Income Reporting Earned Income Credit Errors .....................................................23

Earned Income Credit Errors Involving Social Security Numbers ..............................................24 Avoiding Social Security Number Earned Income Credit Errors .............................................24

Summary ............................................................................................................................24 Chapter Review ...................................................................................................................25

Chapter 3 - EIC Disallowance ............................................................................... 26 Introduction ........................................................................................................................26 Learning Objectives ..............................................................................................................26 IRS Efforts to Reduce Improper EIC Payments .........................................................................26 Claiming EIC after Disallowance .............................................................................................26

IRS Form 8862 Timing .......................................................................................................26 Filing IRS Form 8862 .........................................................................................................27

Exceptions .....................................................................................................................27 Client Consequences of EIC Disallowance ................................................................................27

Disallowance Due to Reckless or Intentional Disregard of EIC Rules .........................................27 Disallowance Due to Fraud..................................................................................................28

Summary ............................................................................................................................28 Chapter Review ...................................................................................................................28

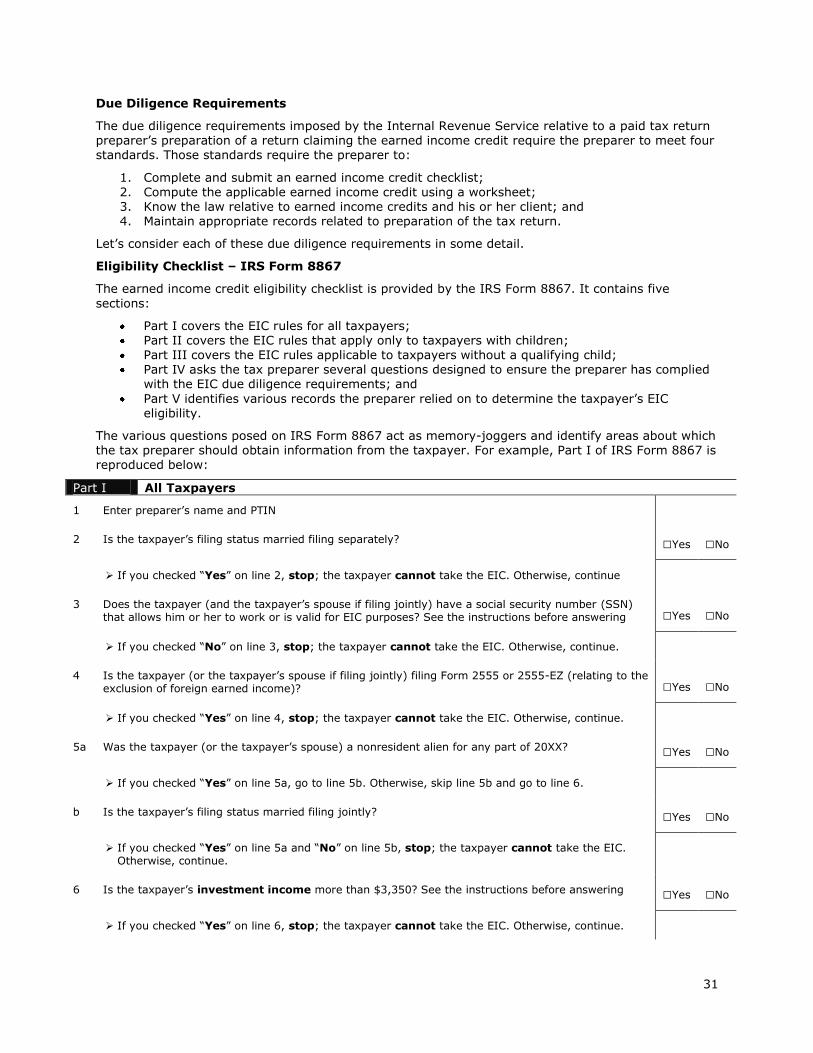

Chapter 4 - EIC Due Diligence .............................................................................. 30 Introduction ........................................................................................................................30 Learning Objectives ..............................................................................................................30 Tax Preparer Due Diligence a Statutory Requirement – IRC §6695 .............................................30 Due Diligence Requirements ..................................................................................................31

Eligibility Checklist – IRS Form 8867 ....................................................................................31 Due Diligence Questions to Ask to Avoid Qualifying Child Errors ...........................................32 Eligibility Checklist Best Practices .....................................................................................32

EIC Computation ...............................................................................................................33 Computation Best Practices..............................................................................................33

Know the Law and the Client ...............................................................................................33 When Should a Preparer Ask Additional Questions – Examples .............................................33 Knowledge Requirement Best Practices .............................................................................34

Record Maintenance ...........................................................................................................34 Record Maintenance Best Practices ...................................................................................35

Failure to Meet Due Diligence Requirements ............................................................................35 Consequences for the Tax Return Preparer ...........................................................................35 Consequences for the Preparer’s Employer ...........................................................................36

Summary ............................................................................................................................36 Chapter Review ...................................................................................................................37

Answers to Chapter Review Questions ................................................................. 38 Chapter 1 ............................................................................................................................38 Chapter 2 ............................................................................................................................39 Chapter 3 ............................................................................................................................41 Chapter 4 ............................................................................................................................42

Glossary ............................................................................................................... 45

Index ................................................................................................................... 47

Appendix A – Worksheet A ................................................................................... 48

Appendix B – Worksheet B ................................................................................... 49

1

Introduction to The Course

The Earned Income Credit (EIC) is a refundable tax credit that has a significant impact on United States revenue. In fact, EIC claims in any year generally total more than $60 billion.

EIC claims are also increasing in both number and amount1. In the ten year period ending in 2010, the

number of EIC claims increased from 19.6 million to 27.4 million, an increase of 39.8%. Not only had the number of claims for EIC increased over the period, the average credit per family also increased by 28.8%, from $1,704 at the beginning of the period to $2,194 in the year the 10-year period ended. The combination of an increased number of EIC claims coupled with an increase in the average credit caused the total amount of EIC claimed to skyrocket by 82.3% over the period from $33.4 billion to $60.9 billion.

In a recent year, 147.4 million individual federal tax returns were filed, and 24.4 million—16.6% of

individual taxpayers—claimed the Earned Income Credit. Based on that percentage, it would not be unexpected that approximately one taxpayer in every six may claim the EIC.

Learning Objectives

Upon completion of this course, you should be able to:

Apply the earned income credit rules to determine if a taxpayer is eligible for the tax credit; Identify the common errors committed in connection with the earned income credit;

Describe the consequences of the IRS’ disallowance of the earned income credit; and Recognize the tax return preparer’s EIC due diligence requirements.

1 Source: Internal Revenue Service, Statistics of Income Division, Table 1, Individual Income Tax Returns: Selected Income and Tax Items for Tax Years 1999 – 2011. http://www.irs.gov/uac/SOI-Tax-Stats-Historical-Table-1

2

Chapter 1 – Earned Income Credit Rules

Introduction

The earned income credit—usually referred to simply as “EIC” or “EITC”—is a tax credit for certain low-income working taxpayers who meet income, filing status and other requirements. Eligibility to claim the credit requires, among other things, that the taxpayer have an earned income and also have an adjusted gross income (AGI) that is below a specified level. The applicable AGI level generally changes annually.

EIC is a refundable credit and, accordingly, it is available to eligible taxpayers regardless of whether or

not they have a federal income tax liability.

Learning Objectives

When you have completed this chapter, you should be able to:

Recognize the EIC eligibility rules that apply to all taxpayers; Identify the EIC eligibility rules applicable to taxpayers who have a qualifying child; List the EIC eligibility rules that apply to taxpayers who do not have a qualifying child; and

Recognize how the EIC for which an eligible taxpayer qualifies is determined.

Eligibility to Receive EIC

In order to receive EIC, the taxpayer must meet certain requirements. Furthermore, the rules vary depending on whether the taxpayer has a qualifying child. Thus, the applicable EIC rules fall into three categories:

Rules that apply to everyone; Rules that apply if the taxpayer has a qualifying child; and

Rules that apply if the taxpayer does not have a qualifying child.

EIC Rules Applicable to Everyone

Determining whether a taxpayer qualifies for EIC begins with the seven rules that apply to everyone

whether or not the taxpayer has a qualifying child. If the taxpayer meets all the seven rules that apply to everyone, the taxpayer must then meet the additional rules that apply a) if the taxpayer has a qualifying child or b) if the taxpayer does not have a qualifying child.

The rules for everyone relate to:

1. Adjusted gross income (AGI) limits—the taxpayer’s AGI cannot exceed specified levels based on filing status;

2. Social Security number—the taxpayer must have a valid SSN; 3. Tax filing status—taxpayers whose filing status is married filing separate are ineligible for EIC; 4. Citizenship or residency; 5. Foreign earned income—excluded foreign earned income will cause a taxpayer to be ineligible

for EIC; 6. Investment income—investment income cannot exceed a specified amount; and 7. Earned income—an eligible taxpayer must work and receive earned income.

If the taxpayer does not meet all seven of the rules applicable to everyone, the taxpayer cannot

receive the earned income credit.

Adjusted Gross Income Limits

To meet the rule concerning adjusted gross income limits, a taxpayer must have an AGI that is less

than the maximum amount for his or her filing status and number of qualifying children. The applicable AGI limits generally change each year and, for 2015 and 2016, are as shown in the following chart:

3

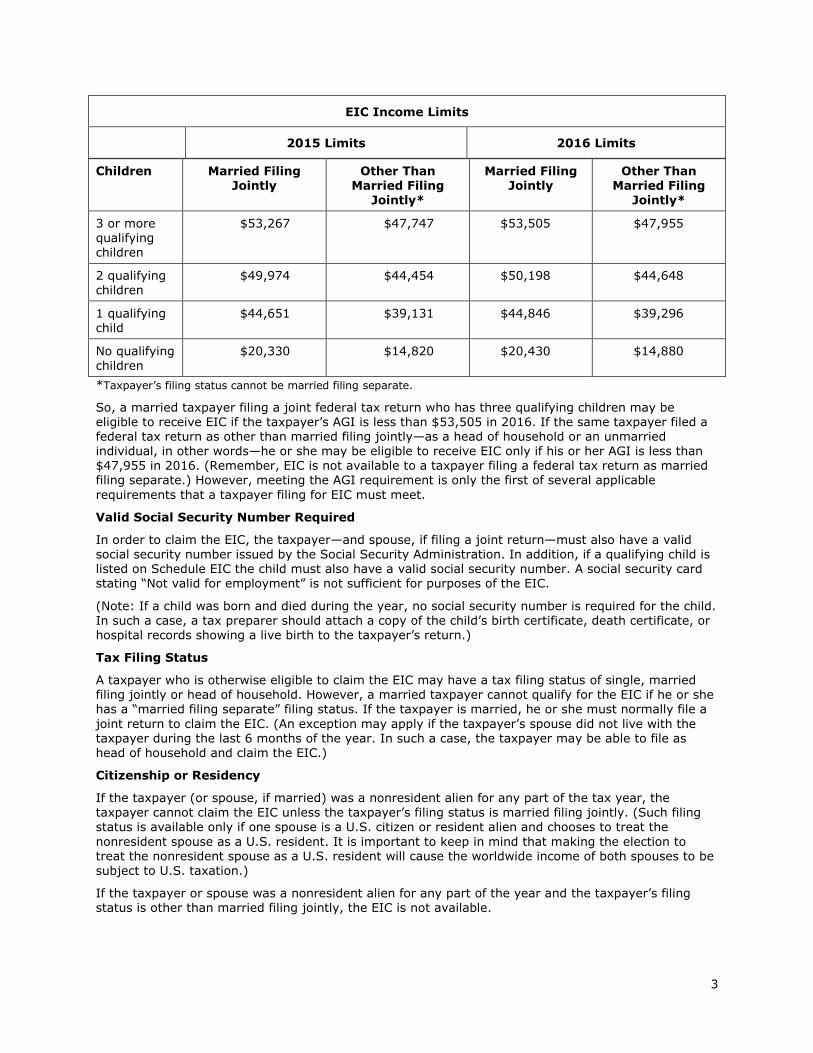

EIC Income Limits

2015 Limits 2016 Limits

Children Married Filing Jointly

Other Than Married Filing

Jointly*

Married Filing Jointly

Other Than Married Filing

Jointly*

3 or more qualifying children

$53,267 $47,747 $53,505 $47,955

2 qualifying children

$49,974 $44,454 $50,198 $44,648

1 qualifying child

$44,651 $39,131 $44,846 $39,296

No qualifying children

$20,330 $14,820 $20,430 $14,880

*Taxpayer’s filing status cannot be married filing separate.

So, a married taxpayer filing a joint federal tax return who has three qualifying children may be eligible to receive EIC if the taxpayer’s AGI is less than $53,505 in 2016. If the same taxpayer filed a federal tax return as other than married filing jointly—as a head of household or an unmarried individual, in other words—he or she may be eligible to receive EIC only if his or her AGI is less than $47,955 in 2016. (Remember, EIC is not available to a taxpayer filing a federal tax return as married filing separate.) However, meeting the AGI requirement is only the first of several applicable

requirements that a taxpayer filing for EIC must meet.

Valid Social Security Number Required

In order to claim the EIC, the taxpayer—and spouse, if filing a joint return—must also have a valid social security number issued by the Social Security Administration. In addition, if a qualifying child is listed on Schedule EIC the child must also have a valid social security number. A social security card

stating “Not valid for employment” is not sufficient for purposes of the EIC.

(Note: If a child was born and died during the year, no social security number is required for the child. In such a case, a tax preparer should attach a copy of the child’s birth certificate, death certificate, or hospital records showing a live birth to the taxpayer’s return.)

Tax Filing Status

A taxpayer who is otherwise eligible to claim the EIC may have a tax filing status of single, married filing jointly or head of household. However, a married taxpayer cannot qualify for the EIC if he or she has a “married filing separate” filing status. If the taxpayer is married, he or she must normally file a

joint return to claim the EIC. (An exception may apply if the taxpayer’s spouse did not live with the taxpayer during the last 6 months of the year. In such a case, the taxpayer may be able to file as head of household and claim the EIC.)

Citizenship or Residency

If the taxpayer (or spouse, if married) was a nonresident alien for any part of the tax year, the

taxpayer cannot claim the EIC unless the taxpayer’s filing status is married filing jointly. (Such filing status is available only if one spouse is a U.S. citizen or resident alien and chooses to treat the

nonresident spouse as a U.S. resident. It is important to keep in mind that making the election to treat the nonresident spouse as a U.S. resident will cause the worldwide income of both spouses to be subject to U.S. taxation.)

If the taxpayer or spouse was a nonresident alien for any part of the year and the taxpayer’s filing status is other than married filing jointly, the EIC is not available.

4

Foreign Earned Income

The Earned Income Credit is designed to assist low-income earners and cannot be claimed by a taxpayer who excludes foreign earned income from his or her gross income subject to U.S. taxation. Thus, a taxpayer is ineligible for the EIC if he or she files Form 2555, Foreign Earned Income, or Form

2555-EZ, Foreign Earned Income Exclusion. These forms are used to exclude income earned in foreign countries from the taxpayer’s gross income or to exclude a foreign housing amount.

Investment Income

Paying the EIC to a taxpayer with substantial investment earnings is inconsistent with its intended purpose of providing assistance to low-income earners. Accordingly, a taxpayer eligible for EIC cannot receive more than a minimal amount of investment income.

The EIC rules require that the 2016 investment income of a taxpayer eligible for EIC cannot be greater

than $3,400. If the taxpayer’s 2016 investment income is greater than $3,400, the taxpayer is ineligible for the EIC.

Earned Income

A taxpayer eligible for the EIC must work and have earned income. If the taxpayer is married and files a joint return, the requirements of the earned income rule are met provided at least one spouse works and has earned income.

The income that qualifies as “earned income” includes:

Wages, salaries, tips and other taxable employee pay; Net earnings from self-employment; and Gross income received by the taxpayer as a statutory employee.

Although earned income generally excludes non-taxable pay, a taxpayer can elect to include non-taxable combat pay in earned income for purposes of the EIC.

EIC Rules That Apply Only if the Taxpayer Has a Qualifying Child

If the taxpayer meets all the EIC eligibility rules applicable to all filers—the rules just discussed, in other words—then proceed to the next step. The appropriate next step depends on whether or not the taxpayer has a qualifying child. We will turn our attention now to the rules that apply to a taxpayer

who has met the EIC rules that apply to everyone and has a qualifying child.

Thus, in addition to meeting the EIC rules that apply to everyone, a taxpayer who has a qualifying child must meet certain other rules in order to be eligible to receive the EIC. The rules that a taxpayer with a qualifying child must also meet are:

1. The relationship, age, residence and joint return tests; 2. The qualifying child of more than one person rule; and 3. The qualifying child of another taxpayer rule.

Let’s look at each of these additional rules.

Relationship, Age, Residence and Joint Return Tests

A taxpayer’s child is a qualifying child for purposes of the EIC if the child meets four tests and, unless

the child was born and died in the year, has a valid Social Security number. The four tests the child must meet are:

The relationship test; The age test; The residency test; and The joint return test.

All four tests must be met. If the taxpayer does not meet all four tests, the child is not a qualifying

child for purposes of the EIC.

The Relationship Test

To meet the relationship test, a qualifying child must be the taxpayer’s:

5

Son, daughter, stepchild, foster child, or a descendant—the taxpayer’s grandchild or great

grandchild, for example—of any of them; or Brother, sister, half brother, half sister, stepbrother, stepsister, or a descendant—a taxpayer’s

niece or nephew, for example—of any of them.

Although many of the relationships mentioned above are fairly obvious, the definition of a foster child, for purposes of the EIC, should be noted. A “foster child” is one placed with the taxpayer by an authorized placement agency or by judgment, decree, or other order of any court of competent jurisdiction. A child left with the taxpayer by its parent would not be a foster child as the term is used in connection with the EIC; the child must be placed with the taxpayer by a placement agency or the court.

The Age Test

To meet the age test, a qualifying child must be:

Younger than age 19 at the end of the tax year and younger than the taxpayer (or the taxpayer’s spouse if filing jointly);

Younger than age 24 at the end of the tax year, a student, and younger than the taxpayer (or

the taxpayer’s spouse if filing jointly); or Permanently and totally disabled at any time during the tax year, regardless of age.

For example, a taxpayer’s child who became age 19 during the tax year would not meet the age test since a qualifying child is one who is younger than age 19 at the end of the year unless he or she was a student or permanently and totally disabled during the year. Similarly, a 23 year-old student living with her brother and sister-in-law, both of whom are younger than 23, would not be a qualifying child since at least one of the couple with whom she is living must be older than the student in order for her to meet the age test to be a qualifying child. However, if either the taxpayer or spouse was age 24 or older, the 23 year-old student would meet the age test.

Student Defined

Since meeting one of the age tests depends on the qualifying child being a student, it is important to understand how a student is defined for purposes of the EIC. To qualify as a student, the child must be, during some part of each of any five calendar months during the calendar year either:

1. A full-time student, i.e. one considered to be a full-time student by the school being attended, provided the school has a – a) Regular teaching staff,

b) Course of study, and c) Regular student body; or

2. A student taking a full-time, on-farm training course given by a – a) School described in 1. above, or b) State, county or local government.

The five calendar months of study during the calendar year required under the definition of a student

need not be consecutive months nor does the child need to have been a student for the entire month.

Furthermore, the definition of school is very broad. Thus, a school, for purposes of the EIC, includes:

An elementary school; A junior or senior high school; A college or university; or

A technical, trade, or mechanical school.

Despite the broad definition of “school,” certain types of training do not meet the criteria for the EIC.

Accordingly, taking the following types of training would not qualify the child as a student:

On-the-job training courses; Correspondence schools; and Schools offering courses only through the internet.

6

Permanently and Totally Disabled Defined

A child who is permanently and totally disabled is not required to meet the age test for EIC purposes. For a child to be considered permanently and totally disabled, as that term is used in connection with the EIC, two requirements must be met:

1. The child must be unable to engage in any substantial gainful activity because of a – a) Physical condition, or b) Mental condition; and

2. A doctor must determine the condition – a) Has lasted continuously for at least a year, b) Can be expected to last continuously for at least a year, or c) Can lead to death.

The Residency Test

In addition to meeting the relationship and age tests, a child must also meet the residency test. To meet the residency test, a qualifying child must have lived with the taxpayer in the United States for more than half of the year. “United States” means the 50 states and the District of Columbia.

However, the term does not include Puerto Rico or U.S. possessions.

The home at which the child lives with the taxpayer may be any location—including a homeless shelter

or other type of dwelling—in which the taxpayer regularly lives.

A child who was born or who died during the year is treated, for purposes of the EIC, as having lived with the taxpayer for more than half the year if the taxpayer’s home was the child’s home for more than half the time the child was alive during the year.

The child’s temporary absence from the taxpayer’s home due to special circumstances should be considered as time the child lived with the taxpayer. Such special circumstances include:

Illness;

School attendance; Business; Vacation; Military service; and

Detention in a juvenile facility.

Exception for U.S. Military Stationed Outside the U.S.

Although the residency test specifies that the residence at which the child resides with the taxpayer

must be within the United States, an exception applies to U.S. military personnel stationed outside the United States. U.S. military personnel who are on extended active duty stationed outside the United States are deemed to live in the United States during that duty period for purposes of the EIC.

The term “extended active duty” means duty for an indefinite period or for a period of more than 90 days. Once the taxpayer begins serving extended active duty, he or she is still considered to have been on extended active duty even if the taxpayer does not actually serve more than 90 days.

The Joint Return Test

The last test that a child must meet to be considered a “qualifying” child is the joint return test. To meet the joint return test the child cannot file a joint return for the tax year, except when filing the child’s filing a joint tax return is only to claim a refund.

However, even if the child does not file a joint tax return, the child cannot be the taxpayer’s qualifying child, for purposes of the EIC, if the child was married at the end of the year unless:

The taxpayer can claim an exemption for the child; or

The reason the taxpayer cannot claim an exemption for the child is that the taxpayer let the child’s other parent claim the exemption.

Child Must Have Valid Social Security Number

Unless the child was born and died during the year, he or she must have a valid social security number. Thus, a taxpayer cannot claim the EIC based on having a qualifying child if:

7

The child’s social security number is missing from the taxpayer’s return or is incorrect;

The child’s social security card says “Not valid for employment” and was issued for use in obtaining a federally funded benefit; or

The child has either of the following rather than a social security number –

o An individual taxpayer identification number (ITIN), which is issued to a noncitizen who cannot obtain a social security number, or

o An adoption taxpayer identification number (ATIN), issued to adopting parents who cannot get a social security number for the child being adopted until the adoption is final.

If a taxpayer has more than one child and only one of the children has a valid social security number, the taxpayer can use only the child with the valid social security number to claim the EIC.

Qualifying Child of More than One Person Rule

It is possible that a child may meet the tests to be a qualifying child of more than one person. However, even if a child meets the tests to be a qualifying child of more than one person, only one person is permitted to treat the child as a qualifying child for purposes of the EIC.

Thus, only that person is permitted to use the child as a qualifying child to take all the following tax

benefits, assuming the taxpayer is eligible for each benefit:

The exemption for the child;

The child tax credit; Head of household filing status; The credit for child and dependent care expenses; The exclusion for dependent care benefits; and The EIC.

The other person cannot take any of these benefits based on the same qualifying child. Accordingly, the taxpayer and the other person cannot divide these tax benefits between themselves based on the

same child. In the event the taxpayer and another person both meet the qualifying child tests, the tiebreaker rules are used to determine which person can treat the child as a qualifying child.

Tiebreaker Rules

When more than one person has the same qualifying child, the tiebreaker rules apply. The tiebreaker

rules are as follows:

If only one of the persons is the parent of the child, the child is the qualifying child of the parent;

If the parents file a joint return together and can claim the child as a qualifying child, the child is treated as the qualifying child of the parents;

If the parents do not file a joint return together but both parents claim the child as a qualifying child, the IRS will treat the child as the qualifying child of the parent – o With whom the child lived for the longer period of time during the year, or o Who had the higher adjusted gross income for the year if the child lived with each parent

for the same amount of time; If no parent can claim the child as a qualifying child, the child is treated as the qualifying child

of the person who had the highest adjusted gross income for the year; and If a parent can claim the child as a qualifying child but no parent does, the child is treated as

the qualifying child of the person who had the highest AGI for the year, but only if that person’s AGI is higher than the highest AGI of any of the child’s parents who can claim the child.

Qualifying Child of Another Taxpayer Rule

A taxpayer cannot claim the EIC if he or she is a qualifying child of another taxpayer. A taxpayer is considered a qualifying child of another person only if all of the following are true:

The taxpayer is the other person’s son, daughter, stepchild, grandchild, or foster child; The taxpayer is the brother, sister, half-brother, half-sister, stepbrother, or stepsister (or a

child or grandchild of the brother, sister, half-brother, etc.) of the other person; The taxpayer was –

8

o Under age 19 at the end of the tax year and younger than the other person (or

spouse, if the other person files jointly), o Under age 24 at the end of the tax year, a student, and younger than the other person

(or spouse, if the other person files jointly), or

o Permanently and totally disabled, regardless of age; The taxpayer lived with the other person in the United States for more than half of the year;

and The taxpayer is not filing a joint return for the year (or is filing a joint return only as a claim

for a refund).

If taxpayer #1 meets the criteria to be the qualifying child of taxpayer #2, taxpayer #1 cannot claim the EIC even if taxpayer #2 does not claim the EIC or meet all the rules to claim the EIC. For

example, suppose Barbara, a taxpayer, and Barbara’s child lived with Barbara’s mother. If Barbara meets the relationship, age, residency and joint return tests, she is considered the qualifying child of her mother. Accordingly, Barbara’s mother—assuming she meets all other requirements—can claim the EIC. Since Barbara is the qualifying child of her mother, she cannot claim the EIC whether or not Barbara’s mother cannot or does not claim the EIC.

EIC Rules That Apply if Taxpayer Does Not Have a Qualifying Child

A taxpayer may claim the EIC without a qualifying child, provided the taxpayer meets all the rules that apply to everyone and all the following rules that apply to taxpayers without qualifying children. The EIC rules applicable to a taxpayer with no qualifying child are:

1. The age rule; 2. The dependent of another person rule; 3. The qualifying child of another taxpayer rule; and 4. The main home rule.

The Age Rule

A taxpayer claiming the EIC must be at least age 25 but less than age 65 at the end of the tax year. If the taxpayer is married filing a joint return, either the taxpayer or spouse must be at least age 25 but under age 65 at the end of the year. Either spouse, i.e. the husband or wife, may satisfy the age test as long as one of the spouses does. If neither the taxpayer nor spouse is at least age 25 but under

age 65, the taxpayer cannot claim the EIC.

Death of Spouse During Year

A surviving spouse filing a joint return with a deceased spouse who died during the tax year meets the age test if the deceased spouse was at least age 25 but under age 65 at the time of death.

The Dependent of Another Person Rule

A taxpayer claiming the EIC cannot be the dependent of another person, regardless of whether or not the other person actually claimed the taxpayer as a dependent. Thus, if someone else can claim the taxpayer (or the taxpayer's spouse, if filing a joint return) as a dependent, the taxpayer cannot claim

the EIC, even if the other person did not actually claim the taxpayer as a dependent.

The Qualifying Child of Another Taxpayer Rule

A taxpayer claiming the EIC cannot be a qualifying child of another taxpayer. As noted earlier, a taxpayer is a qualifying child of another person if all the following are true:

The taxpayer is the other person’s son, daughter, stepchild, grandchild, or foster child; The taxpayer is the brother, sister, half-brother, half-sister, stepbrother, or stepsister (or a

child or grandchild of the brother, sister, half-brother, etc.) of the other person;

The taxpayer was – o Under age 19 at the end of the tax year and younger than the other person (or

spouse, if the other person files jointly), o Under age 24 at the end of the tax year, a student, and younger than the other person

(or spouse, if the other person files jointly), or o Permanently and totally disabled, regardless of age;

The taxpayer lived with the other person in the United States for more than half of the year;

and

9

The taxpayer is not filing a joint return for the year (or is filing a joint return only as a claim

for a refund).

The Main Home Rule

Under the main home rule, a taxpayer claiming the EIC must have lived in the United States more

than half the year. A taxpayer will meet this rule only if he or she lived in the 50 states or the District of Columbia for more than half the year. It does not include Puerto Rico or U.S. possessions. The rule does not require that a taxpayer actually reside in a traditional home; instead, a taxpayer who lived in one or more homeless shelters in the United States for more than half the year will also meet the rule.

U.S. military personnel stationed outside the United States on extended active duty are considered to live in the United States during that duty period for purposes of the EIC.

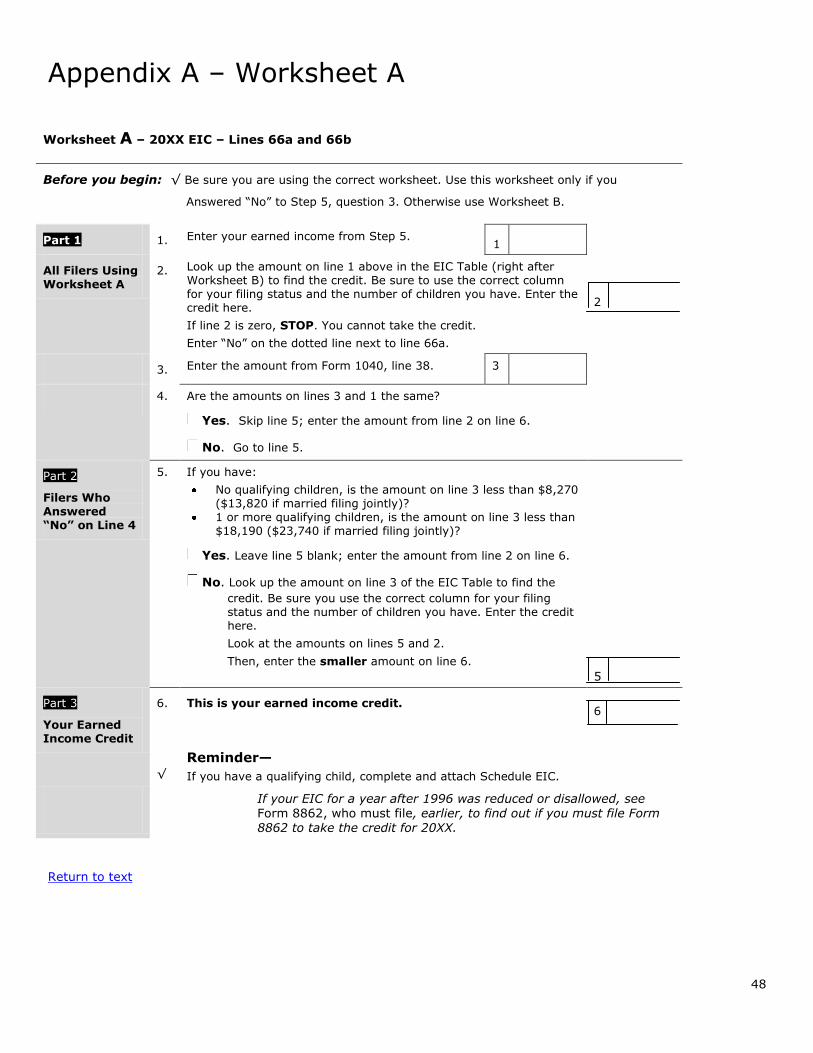

Figuring the Amount of the Earned Income Credit

If the taxpayer meets all of the rules applicable to his or her claiming EIC, the next step is figuring the amount of EIC. Determining the earned income credit is done on either EIC Worksheet A (Appendix A) or EIC Worksheet B (Appendix B).

EIC Worksheet A is used if the taxpayer was not self-employed at any time during the tax year and was not a member of the clergy, a church employee who files Schedule SE, or a statutory employee filing schedule C or C-EZ.

EIC Worksheet B is used if the taxpayer was self-employed at any time during the year or was a member of the clergy, a church employee who files schedule SE or a statutory employee filing schedule C or C–EZ.

The instructions for IRS Form 1040 “Lines 66a and 66b” walk you through the EIC rules—the rules for all filers, for filers with a qualifying child and for filers without a qualifying child—just discussed.

Calculating Earned Income for EIC Purposes

In Step 5 of those Form 1040 EIC instructions, the taxpayer’s earned income for EIC purposes is

calculated. That calculation begins with inserting the total of the taxpayer’s wages, salaries, tips, etc. that appears on Form 1040, line 7. From that line 7 number, various amounts are then deducted to determine the taxpayer’s earned income for purposes of the EIC. If the taxpayer received nontaxable combat pay, the taxpayer may elect to include that nontaxable combat pay in earned income for EIC

purposes. However, electing to include the combat pay in earned income may increase or decrease the EIC.

The amount deducted from the total of the taxpayer’s wages, salaries, tips, etc. that appears on Form

1040 line 7 is the total of the following if included on line 7:

Taxable scholarships or fellowship grants not reported on Form W-2; Amounts received for work performed by the taxpayer while an inmate in a penal institution;

and Amounts received as a pension or annuity from a nonqualified deferred compensation plan or

nongovernmental section 457 plan.

The result of that calculation, plus the amount of nontaxable combat pay (if the taxpayer elects to include it), is the taxpayer’s earned income for EIC purposes.

Taxpayers Not Self-Employed, Statutory Employees, Clergy or Church Employees

The earned income total just calculated may or may not be modified, depending on the taxpayer’s

employment status. If the taxpayer is not a) self-employed, b) a statutory employee filing Schedule C or C-EZ or c) a member of the clergy or person with church employee income filing Schedule SE, the earned income amount is not modified for purposes of the EIC. Instead, it should simply be entered on

Worksheet A in Part 1, box 1.

Part 1 1. Enter your earned income from Step 5. 1

All Filers Using Worksheet A

2. Look up the amount on line 1 above in the EIC Table (right after Worksheet B) to find the credit. Be sure to use the correct column for your filing status and the number of children you have. Enter the

10

credit here.

If line 2 is zero, STOP. You cannot take the credit.

Enter “No” on the dotted line next to line 66a.

2

3. Enter the amount from Form 1040, line 38. 3

4. Are the amounts on lines 3 and 1 the same?

Yes. Skip line 5; enter the amount from line 2 on line 6.

No. Go to line 5.

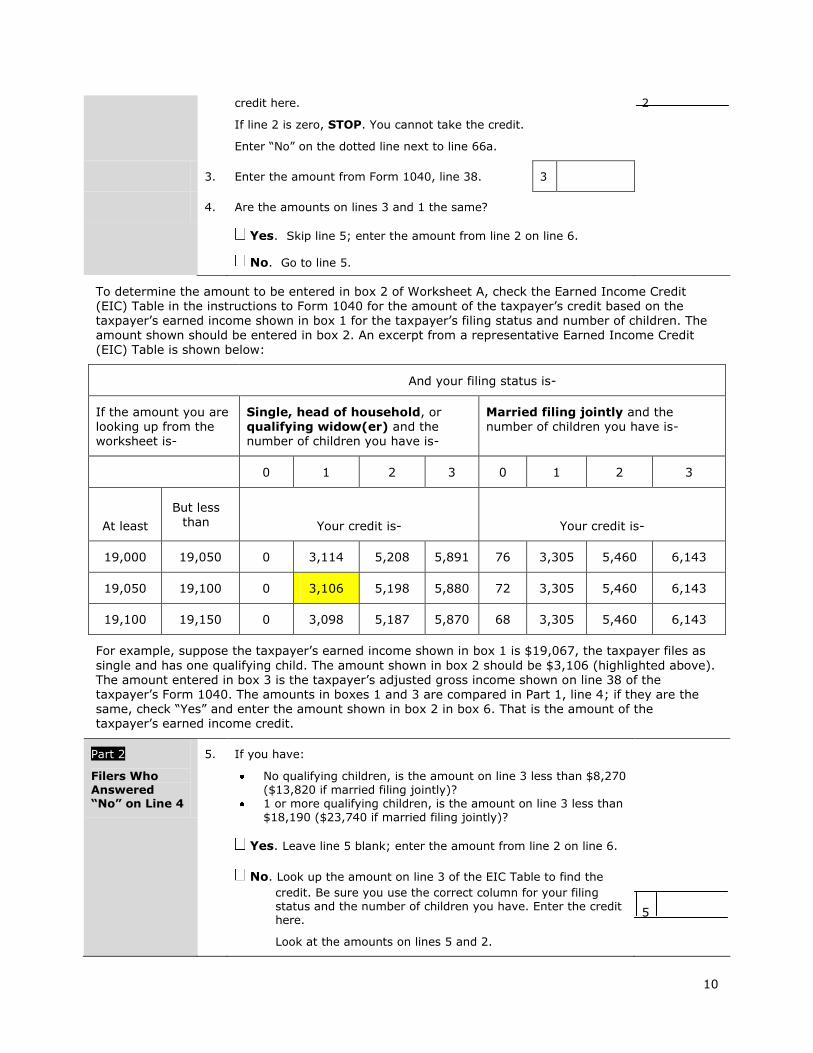

To determine the amount to be entered in box 2 of Worksheet A, check the Earned Income Credit (EIC) Table in the instructions to Form 1040 for the amount of the taxpayer’s credit based on the taxpayer’s earned income shown in box 1 for the taxpayer’s filing status and number of children. The amount shown should be entered in box 2. An excerpt from a representative Earned Income Credit

(EIC) Table is shown below:

And your filing status is-

If the amount you are looking up from the worksheet is-

Single, head of household, or qualifying widow(er) and the number of children you have is-

Married filing jointly and the number of children you have is-

0 1 2 3 0 1 2 3

At least

But less than

Your credit is-

Your credit is-

19,000 19,050 0 3,114 5,208 5,891 76 3,305 5,460 6,143

19,050 19,100 0 3,106 5,198 5,880 72 3,305 5,460 6,143

19,100 19,150 0 3,098 5,187 5,870 68 3,305 5,460 6,143

For example, suppose the taxpayer’s earned income shown in box 1 is $19,067, the taxpayer files as

single and has one qualifying child. The amount shown in box 2 should be $3,106 (highlighted above). The amount entered in box 3 is the taxpayer’s adjusted gross income shown on line 38 of the taxpayer’s Form 1040. The amounts in boxes 1 and 3 are compared in Part 1, line 4; if they are the same, check “Yes” and enter the amount shown in box 2 in box 6. That is the amount of the taxpayer’s earned income credit.

Part 2

Filers Who Answered “No” on Line 4

5. If you have:

No qualifying children, is the amount on line 3 less than $8,270 ($13,820 if married filing jointly)?

1 or more qualifying children, is the amount on line 3 less than $18,190 ($23,740 if married filing jointly)?

Yes. Leave line 5 blank; enter the amount from line 2 on line 6.

No. Look up the amount on line 3 of the EIC Table to find the

credit. Be sure you use the correct column for your filing status and the number of children you have. Enter the credit here.

Look at the amounts on lines 5 and 2.

5

11

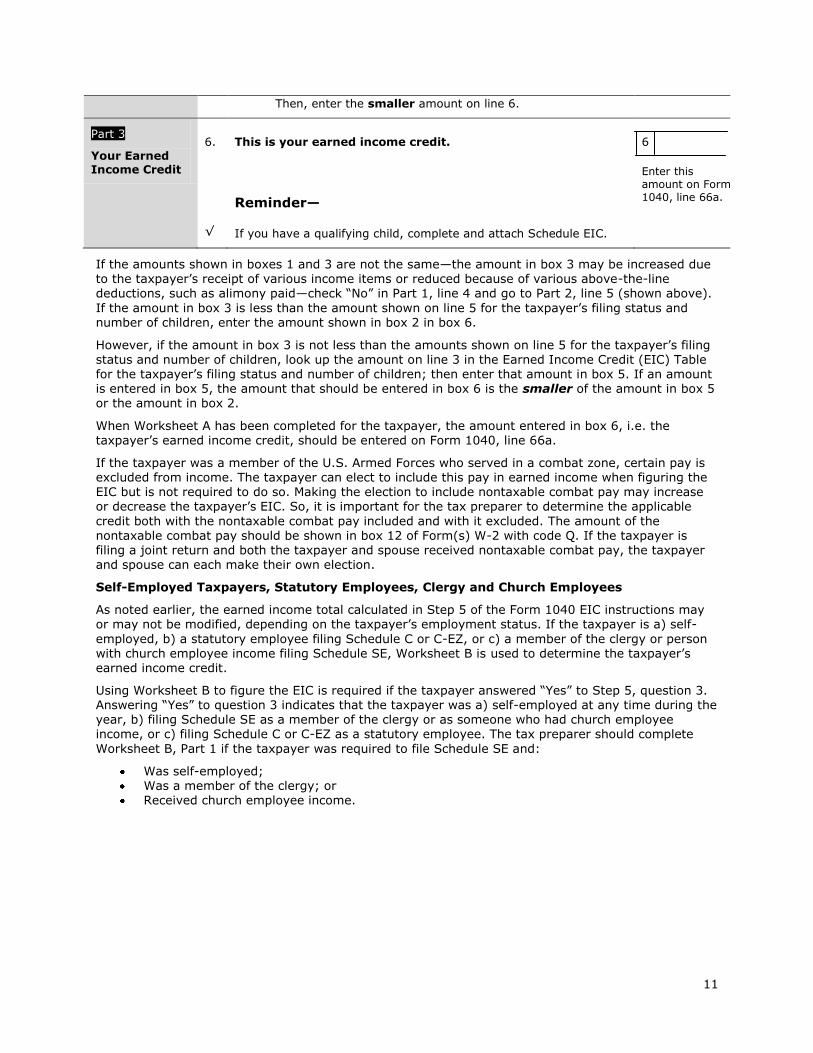

Then, enter the smaller amount on line 6.

Part 3

Your Earned Income Credit

6.

√

This is your earned income credit.

Reminder—

If you have a qualifying child, complete and attach Schedule EIC.

6

Enter this amount on Form 1040, line 66a.

If the amounts shown in boxes 1 and 3 are not the same—the amount in box 3 may be increased due to the taxpayer’s receipt of various income items or reduced because of various above-the-line deductions, such as alimony paid—check “No” in Part 1, line 4 and go to Part 2, line 5 (shown above).

If the amount in box 3 is less than the amount shown on line 5 for the taxpayer’s filing status and number of children, enter the amount shown in box 2 in box 6.

However, if the amount in box 3 is not less than the amounts shown on line 5 for the taxpayer’s filing status and number of children, look up the amount on line 3 in the Earned Income Credit (EIC) Table for the taxpayer’s filing status and number of children; then enter that amount in box 5. If an amount is entered in box 5, the amount that should be entered in box 6 is the smaller of the amount in box 5 or the amount in box 2.

When Worksheet A has been completed for the taxpayer, the amount entered in box 6, i.e. the taxpayer’s earned income credit, should be entered on Form 1040, line 66a.

If the taxpayer was a member of the U.S. Armed Forces who served in a combat zone, certain pay is excluded from income. The taxpayer can elect to include this pay in earned income when figuring the EIC but is not required to do so. Making the election to include nontaxable combat pay may increase or decrease the taxpayer’s EIC. So, it is important for the tax preparer to determine the applicable

credit both with the nontaxable combat pay included and with it excluded. The amount of the nontaxable combat pay should be shown in box 12 of Form(s) W-2 with code Q. If the taxpayer is filing a joint return and both the taxpayer and spouse received nontaxable combat pay, the taxpayer and spouse can each make their own election.

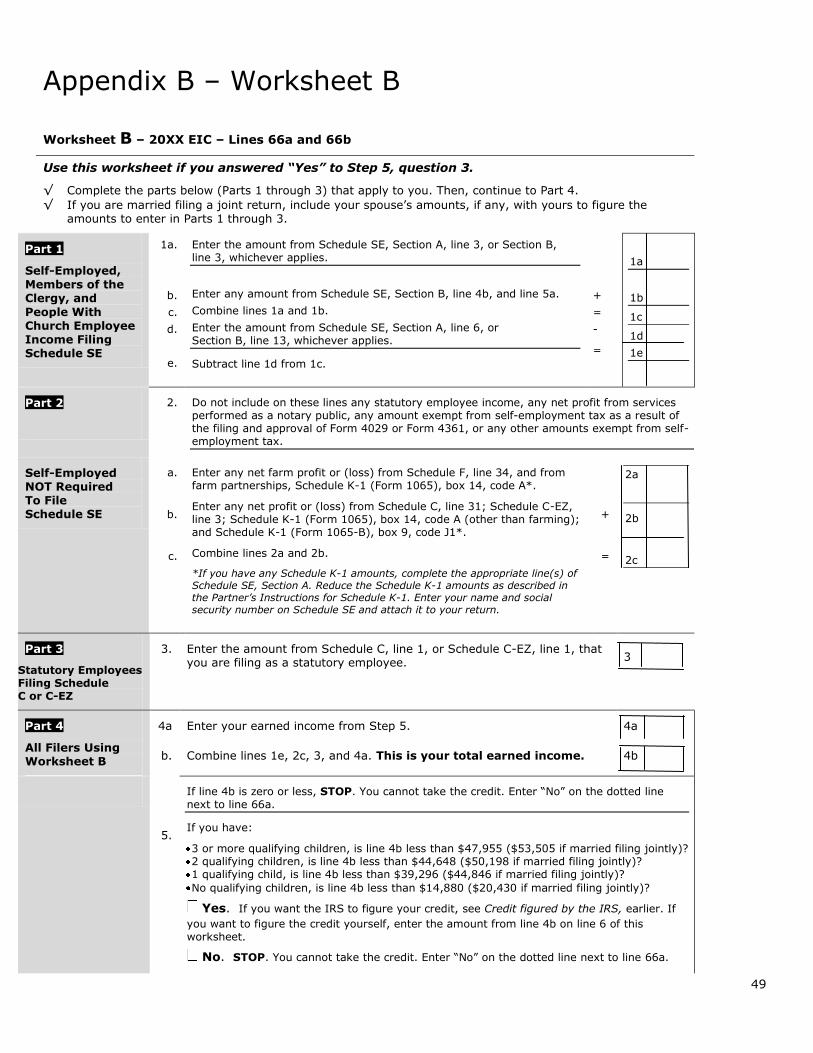

Self-Employed Taxpayers, Statutory Employees, Clergy and Church Employees

As noted earlier, the earned income total calculated in Step 5 of the Form 1040 EIC instructions may or may not be modified, depending on the taxpayer’s employment status. If the taxpayer is a) self-

employed, b) a statutory employee filing Schedule C or C-EZ, or c) a member of the clergy or person with church employee income filing Schedule SE, Worksheet B is used to determine the taxpayer’s earned income credit.

Using Worksheet B to figure the EIC is required if the taxpayer answered “Yes” to Step 5, question 3. Answering “Yes” to question 3 indicates that the taxpayer was a) self-employed at any time during the year, b) filing Schedule SE as a member of the clergy or as someone who had church employee income, or c) filing Schedule C or C-EZ as a statutory employee. The tax preparer should complete

Worksheet B, Part 1 if the taxpayer was required to file Schedule SE and:

Was self-employed; Was a member of the clergy; or Received church employee income.

12

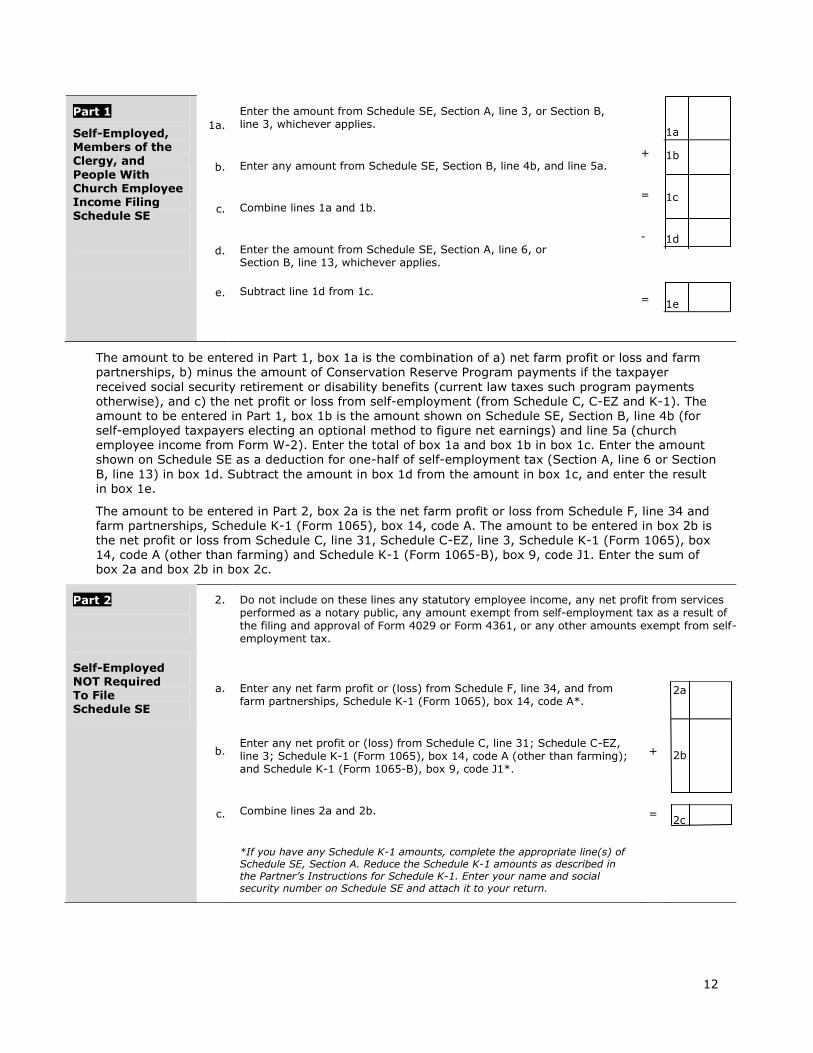

Part 1

Self-Employed, Members of the Clergy, and

People With Church Employee Income Filing Schedule SE

1a.

b.

c.

d.

e.

Enter the amount from Schedule SE, Section A, line 3, or Section B, line 3, whichever applies.

Enter any amount from Schedule SE, Section B, line 4b, and line 5a.

Combine lines 1a and 1b.

Enter the amount from Schedule SE, Section A, line 6, or Section B, line 13, whichever applies.

Subtract line 1d from 1c.

+

=

-

=

1a

1b

1c

1d

1e

The amount to be entered in Part 1, box 1a is the combination of a) net farm profit or loss and farm partnerships, b) minus the amount of Conservation Reserve Program payments if the taxpayer

received social security retirement or disability benefits (current law taxes such program payments otherwise), and c) the net profit or loss from self-employment (from Schedule C, C-EZ and K-1). The amount to be entered in Part 1, box 1b is the amount shown on Schedule SE, Section B, line 4b (for self-employed taxpayers electing an optional method to figure net earnings) and line 5a (church employee income from Form W-2). Enter the total of box 1a and box 1b in box 1c. Enter the amount shown on Schedule SE as a deduction for one-half of self-employment tax (Section A, line 6 or Section

B, line 13) in box 1d. Subtract the amount in box 1d from the amount in box 1c, and enter the result in box 1e.

The amount to be entered in Part 2, box 2a is the net farm profit or loss from Schedule F, line 34 and farm partnerships, Schedule K-1 (Form 1065), box 14, code A. The amount to be entered in box 2b is the net profit or loss from Schedule C, line 31, Schedule C-EZ, line 3, Schedule K-1 (Form 1065), box 14, code A (other than farming) and Schedule K-1 (Form 1065-B), box 9, code J1. Enter the sum of box 2a and box 2b in box 2c.

Part 2

2. Do not include on these lines any statutory employee income, any net profit from services performed as a notary public, any amount exempt from self-employment tax as a result of the filing and approval of Form 4029 or Form 4361, or any other amounts exempt from self-employment tax.

Self-Employed NOT Required To File Schedule SE

a.

b.

c.

Enter any net farm profit or (loss) from Schedule F, line 34, and from farm partnerships, Schedule K-1 (Form 1065), box 14, code A*.

Enter any net profit or (loss) from Schedule C, line 31; Schedule C-EZ, line 3; Schedule K-1 (Form 1065), box 14, code A (other than farming); and Schedule K-1 (Form 1065-B), box 9, code J1*.

Combine lines 2a and 2b.

*If you have any Schedule K-1 amounts, complete the appropriate line(s) of Schedule SE, Section A. Reduce the Schedule K-1 amounts as described in the Partner’s Instructions for Schedule K-1. Enter your name and social security number on Schedule SE and attach it to your return.

+

=

2a

2b

2c

13

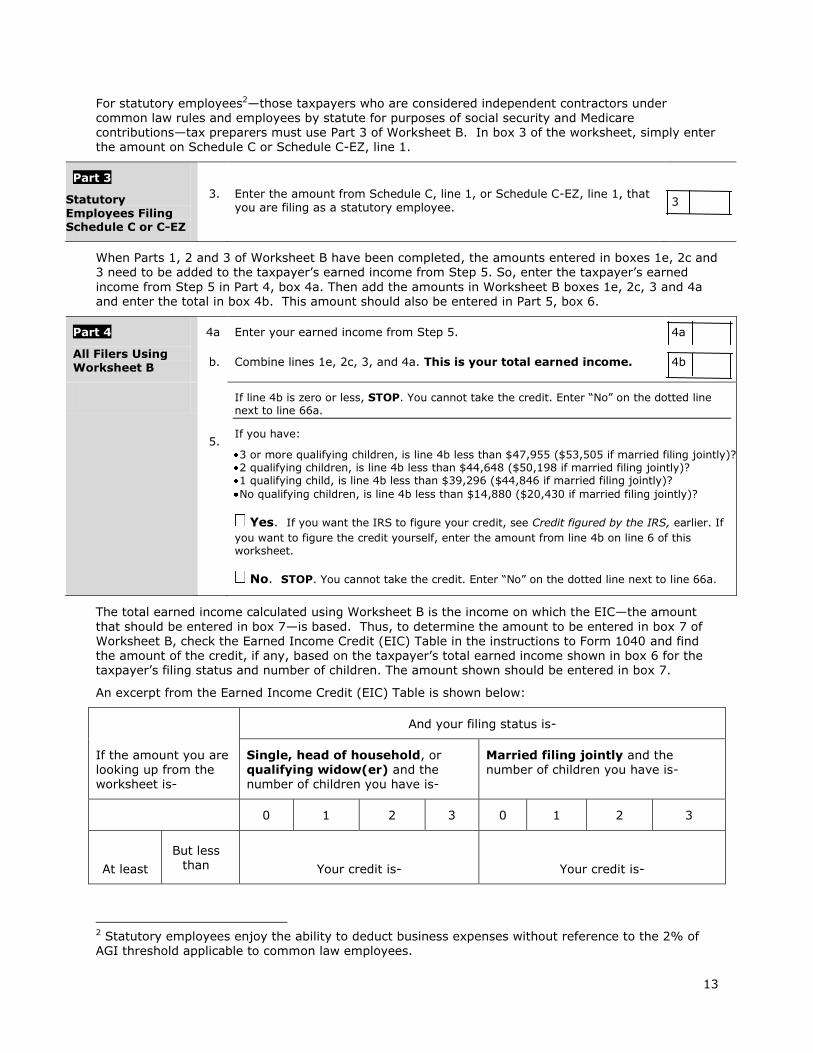

For statutory employees2—those taxpayers who are considered independent contractors under

common law rules and employees by statute for purposes of social security and Medicare contributions—tax preparers must use Part 3 of Worksheet B. In box 3 of the worksheet, simply enter the amount on Schedule C or Schedule C-EZ, line 1.

Part 3

Statutory Employees Filing Schedule C or C-EZ

3. Enter the amount from Schedule C, line 1, or Schedule C-EZ, line 1, that you are filing as a statutory employee.

3

When Parts 1, 2 and 3 of Worksheet B have been completed, the amounts entered in boxes 1e, 2c and 3 need to be added to the taxpayer’s earned income from Step 5. So, enter the taxpayer’s earned

income from Step 5 in Part 4, box 4a. Then add the amounts in Worksheet B boxes 1e, 2c, 3 and 4a and enter the total in box 4b. This amount should also be entered in Part 5, box 6.

Part 4

All Filers Using Worksheet B

4a

b.

Enter your earned income from Step 5.

Combine lines 1e, 2c, 3, and 4a. This is your total earned income.

4a

4b

5.

If line 4b is zero or less, STOP. You cannot take the credit. Enter “No” on the dotted line next to line 66a.

If you have:

3 or more qualifying children, is line 4b less than $47,955 ($53,505 if married filing jointly)? 2 qualifying children, is line 4b less than $44,648 ($50,198 if married filing jointly)? 1 qualifying child, is line 4b less than $39,296 ($44,846 if married filing jointly)?

No qualifying children, is line 4b less than $14,880 ($20,430 if married filing jointly)?

Yes. If you want the IRS to figure your credit, see Credit figured by the IRS, earlier. If

you want to figure the credit yourself, enter the amount from line 4b on line 6 of this worksheet.

No. STOP. You cannot take the credit. Enter “No” on the dotted line next to line 66a.

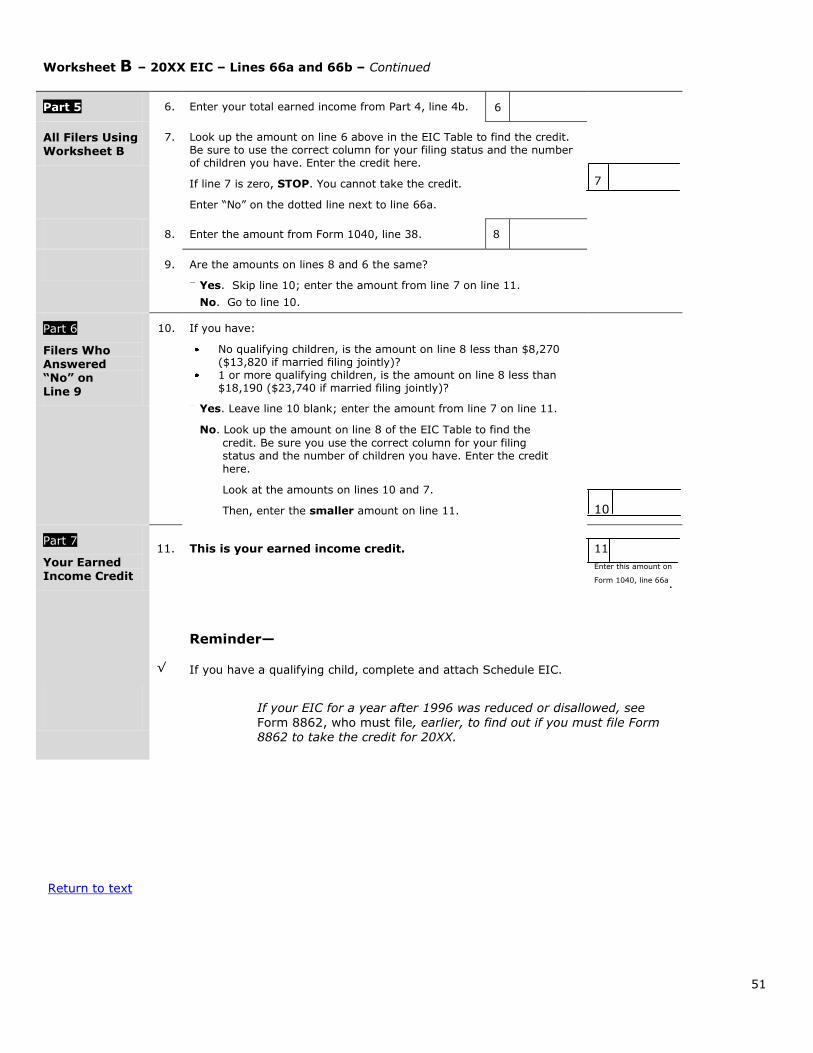

The total earned income calculated using Worksheet B is the income on which the EIC—the amount

that should be entered in box 7—is based. Thus, to determine the amount to be entered in box 7 of Worksheet B, check the Earned Income Credit (EIC) Table in the instructions to Form 1040 and find the amount of the credit, if any, based on the taxpayer’s total earned income shown in box 6 for the taxpayer’s filing status and number of children. The amount shown should be entered in box 7.

An excerpt from the Earned Income Credit (EIC) Table is shown below:

And your filing status is-

If the amount you are looking up from the worksheet is-

Single, head of household, or qualifying widow(er) and the number of children you have is-

Married filing jointly and the number of children you have is-

0 1 2 3 0 1 2 3

At least

But less than

Your credit is-

Your credit is-

2 Statutory employees enjoy the ability to deduct business expenses without reference to the 2% of AGI threshold applicable to common law employees.

14

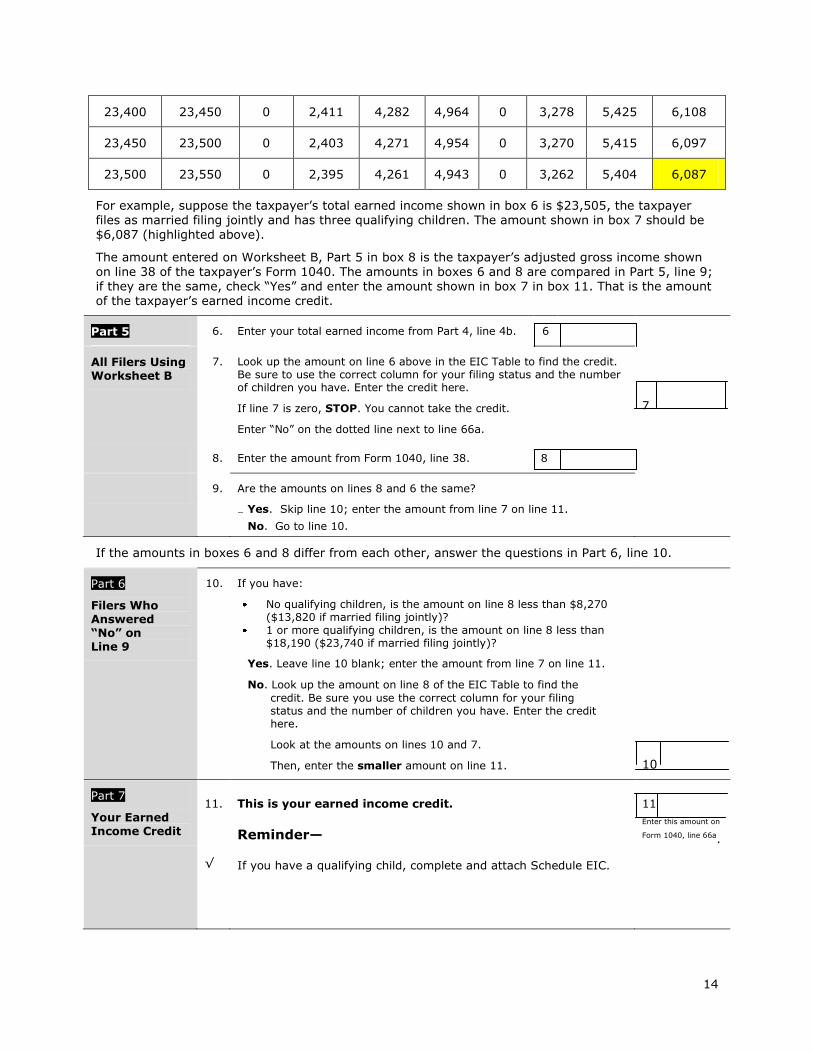

23,400 23,450 0 2,411 4,282 4,964 0 3,278 5,425 6,108

23,450 23,500 0 2,403 4,271 4,954 0 3,270 5,415 6,097

23,500 23,550 0 2,395 4,261 4,943 0 3,262 5,404 6,087

For example, suppose the taxpayer’s total earned income shown in box 6 is $23,505, the taxpayer files as married filing jointly and has three qualifying children. The amount shown in box 7 should be $6,087 (highlighted above).

The amount entered on Worksheet B, Part 5 in box 8 is the taxpayer’s adjusted gross income shown on line 38 of the taxpayer’s Form 1040. The amounts in boxes 6 and 8 are compared in Part 5, line 9; if they are the same, check “Yes” and enter the amount shown in box 7 in box 11. That is the amount of the taxpayer’s earned income credit.

Part 5 6. Enter your total earned income from Part 4, line 4b. 6

All Filers Using Worksheet B

7. Look up the amount on line 6 above in the EIC Table to find the credit. Be sure to use the correct column for your filing status and the number of children you have. Enter the credit here.

If line 7 is zero, STOP. You cannot take the credit.

Enter “No” on the dotted line next to line 66a.

7

8. Enter the amount from Form 1040, line 38. 8

9. Are the amounts on lines 8 and 6 the same?

Yes. Skip line 10; enter the amount from line 7 on line 11.

No. Go to line 10.

If the amounts in boxes 6 and 8 differ from each other, answer the questions in Part 6, line 10.

Part 6

Filers Who Answered “No” on Line 9

10. If you have:

No qualifying children, is the amount on line 8 less than $8,270 ($13,820 if married filing jointly)?

1 or more qualifying children, is the amount on line 8 less than $18,190 ($23,740 if married filing jointly)?

Yes. Leave line 10 blank; enter the amount from line 7 on line 11.

No. Look up the amount on line 8 of the EIC Table to find the

credit. Be sure you use the correct column for your filing status and the number of children you have. Enter the credit here.

Look at the amounts on lines 10 and 7.

Then, enter the smaller amount on line 11.

10

Part 7

Your Earned Income Credit

11.

√

This is your earned income credit.

Reminder—

If you have a qualifying child, complete and attach Schedule EIC.

11

Enter this amount on

Form 1040, line 66a.

15

If the answer to the questions on line 10 is “Yes,” enter the amount previously entered in box 7 into

box 11. However, if the answer to the questions posed in line 10 is “No,” look up the earned income credit in the EIC Table for the taxpayer’s filing status and number of children using the amount shown in box 8 and put the amount of credit shown in the Table in box 10. If the resulting amounts in boxes

7 and 10 differ from one another, enter the smaller amount in box 11. That is the amount of the taxpayer’s earned income credit.

The amount of any applicable EIC is entered in the appropriate line of the taxpayer's return. (Line 66a on IRS Form 1040.)

Summary

The rules that apply to claiming the earned income credit fall into three categories: a) rules that apply to everyone, b) rules that apply if the taxpayer has a qualifying child, and c) rules that apply if the

taxpayer does not have a qualifying child.

Under the EIC rules that apply to everyone, whether or not having a qualifying child a) the taxpayer’s AGI cannot exceed specified levels based on filing status, b) the taxpayer must have a valid social security number, c) a taxpayer eligible to claim the EIC cannot be married filing separate, d) if the

taxpayer (or spouse, if married) was a nonresident alien for any part of the tax year, the taxpayer cannot claim the EIC unless the taxpayer’s filing status is married filing jointly, e) a taxpayer

excluding foreign earned income is ineligible to claim the EIC, f) the investment income of a taxpayer eligible to claim the EIC cannot exceed a specified amount, and g) a taxpayer otherwise eligible to claim the EIC must work and receive earned income.

If a taxpayer who meets the EIC rules applicable to all filers has a qualifying child, the qualifying child must also meet certain rules. Those rules require that the child a) be a son, daughter, stepchild, foster child, brother, sister, half brother, half sister, stepbrother or stepsister of the taxpayer, or a descendant of any of them, b) be younger than age 19 at the end of the year and younger than the

taxpayer or taxpayer’s spouse, younger than age 24 if a student and younger than the taxpayer or taxpayer’s spouse, or permanently and totally disabled regardless of age, c) have lived with the taxpayer in the U.S. for more than half the year, and d) not have filed a joint tax return for the year except to claim a refund. In addition, a child cannot be the qualifying child of more than one person even if the child meets the tests to be a qualifying child of more than one person. In the event the taxpayer and another person both meet the qualifying child tests, the tiebreaker rules are used to

determine which person can treat the child as a qualifying child. Lastly, a taxpayer cannot claim the

EIC if he or she is a qualifying child of another taxpayer.

The EIC rules that apply to a taxpayer with no qualifying child are: a) the age rule pursuant to which, a taxpayer claiming the EIC must be at least age 25 but less than age 65 at the end of the year, b) the dependent of another person rule, under which a taxpayer cannot be the dependent of another person, c) the qualifying child of another taxpayer rule, under which a taxpayer cannot be a qualifying child of another taxpayer, and d) the main home rule under which a taxpayer claiming the EIC must

have lived in the United States more than half the year.

If the taxpayer meets all the rules applicable to his or her claiming EIC, the amount of EIC for which the taxpayer is eligible is determined using EIC Worksheet A—for taxpayers who were not self-employed, not a member of the clergy, not a church employee who files Schedule SE, nor a statutory employee filing schedule C or C-EZ—or EIC Worksheet B for those taxpayers who can be included in one of those categories.

Chapter Review

1. Susan has three qualifying children and files her federal income tax return as married filing separate. In order to qualify for EIC in 2016, she must have an AGI of less than:

A. $53,505

B. $47,955

C. Susan is ineligible for EIC

D. $14,880

16

2. Arthur is married to a nonresident alien who lives in Mexico City. Under what circumstances could

he be eligible for the earned income credit based on 2016 income?

A. Only if he files a federal tax return as married filing jointly

B. Only if the taxpayer was also a nonresident alien for part of the year

C. Only if the taxpayer’s spouse agreed that her foreign income would be subject to U.S. taxation

D. Under no circumstances would the taxpayer be eligible for EIC

3. Shirley and Carl are raising three children: their daughter’s son, Carl’s brother and a child placed with them by its parent. How many qualifying children do they have under the relationship test for purposes of the earned income credit?

A. They have no qualifying children under the relationship test

B. They have two qualifying children under the relationship test

C. They have one qualifying child under the relationship test

D. They have three qualifying children under the relationship test

4. Peter is considered permanently and totally disabled. He is a student at the local community college and lives with his brother and his brother’s wife. What is the maximum age Peter may be and still meet the age test for purposes of the EIC?

A. Younger than age 19

B. Younger than age 21

C. Younger than age 24

D. No age limit applies in this case

5. What is the maximum age an unmarried taxpayer with no qualifying children may be at the end of the tax year and still qualify for the earned income credit?

A. Age 21

B. Age 25

C. Age 64

D. Age 70 ½

17

Chapter 2 – Earned Income Credit Errors

Introduction

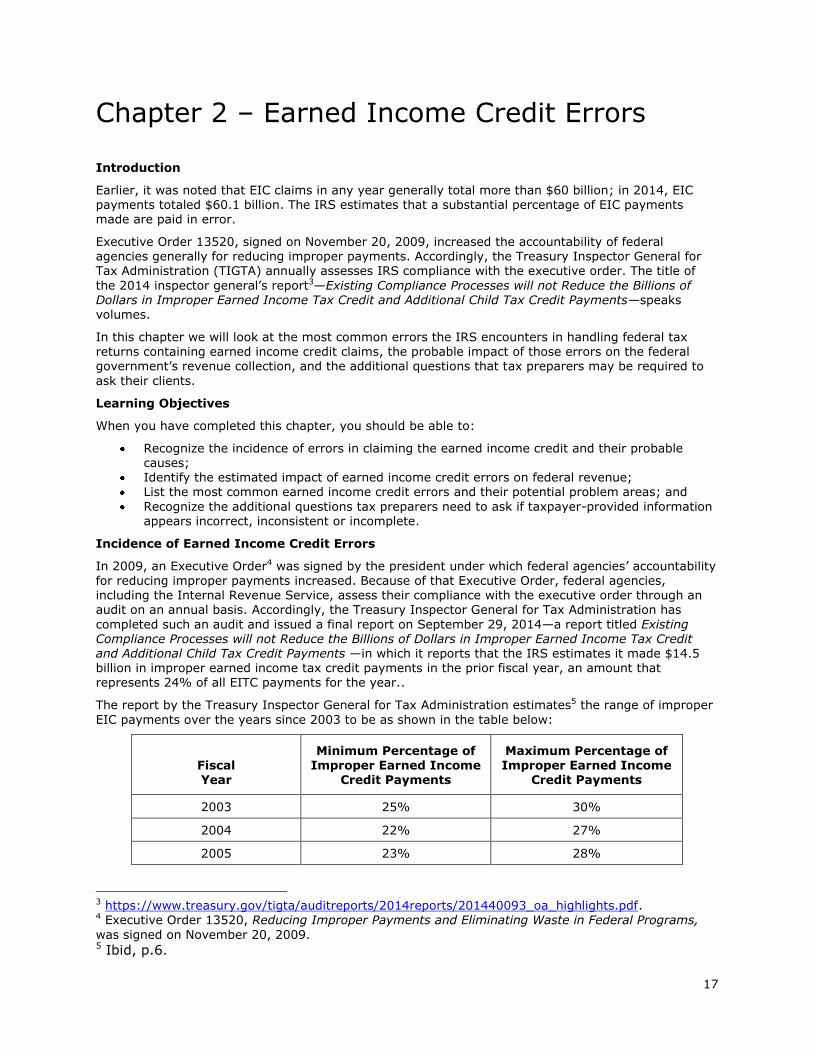

Earlier, it was noted that EIC claims in any year generally total more than $60 billion; in 2014, EIC payments totaled $60.1 billion. The IRS estimates that a substantial percentage of EIC payments made are paid in error.

Executive Order 13520, signed on November 20, 2009, increased the accountability of federal agencies generally for reducing improper payments. Accordingly, the Treasury Inspector General for Tax Administration (TIGTA) annually assesses IRS compliance with the executive order. The title of

the 2014 inspector general’s report3—Existing Compliance Processes will not Reduce the Billions of Dollars in Improper Earned Income Tax Credit and Additional Child Tax Credit Payments—speaks volumes.

In this chapter we will look at the most common errors the IRS encounters in handling federal tax

returns containing earned income credit claims, the probable impact of those errors on the federal government’s revenue collection, and the additional questions that tax preparers may be required to

ask their clients.

Learning Objectives

When you have completed this chapter, you should be able to:

Recognize the incidence of errors in claiming the earned income credit and their probable causes;

Identify the estimated impact of earned income credit errors on federal revenue; List the most common earned income credit errors and their potential problem areas; and

Recognize the additional questions tax preparers need to ask if taxpayer-provided information appears incorrect, inconsistent or incomplete.

Incidence of Earned Income Credit Errors

In 2009, an Executive Order4 was signed by the president under which federal agencies’ accountability

for reducing improper payments increased. Because of that Executive Order, federal agencies, including the Internal Revenue Service, assess their compliance with the executive order through an audit on an annual basis. Accordingly, the Treasury Inspector General for Tax Administration has

completed such an audit and issued a final report on September 29, 2014—a report titled Existing Compliance Processes will not Reduce the Billions of Dollars in Improper Earned Income Tax Credit and Additional Child Tax Credit Payments —in which it reports that the IRS estimates it made $14.5 billion in improper earned income tax credit payments in the prior fiscal year, an amount that represents 24% of all EITC payments for the year..

The report by the Treasury Inspector General for Tax Administration estimates5 the range of improper

EIC payments over the years since 2003 to be as shown in the table below:

Fiscal Year

Minimum Percentage of Improper Earned Income

Credit Payments

Maximum Percentage of Improper Earned Income

Credit Payments

2003 25% 30%

2004 22% 27%

2005 23% 28%

3 https://www.treasury.gov/tigta/auditreports/2014reports/201440093_oa_highlights.pdf. 4 Executive Order 13520, Reducing Improper Payments and Eliminating Waste in Federal Programs,

was signed on November 20, 2009. 5 Ibid, p.6.

18

2006 23% 28%

2007 23% 28%

2008 23% 28%

2009 23% 28%

2010 24% 29%

2011 21% 26%

2012 21% 25%

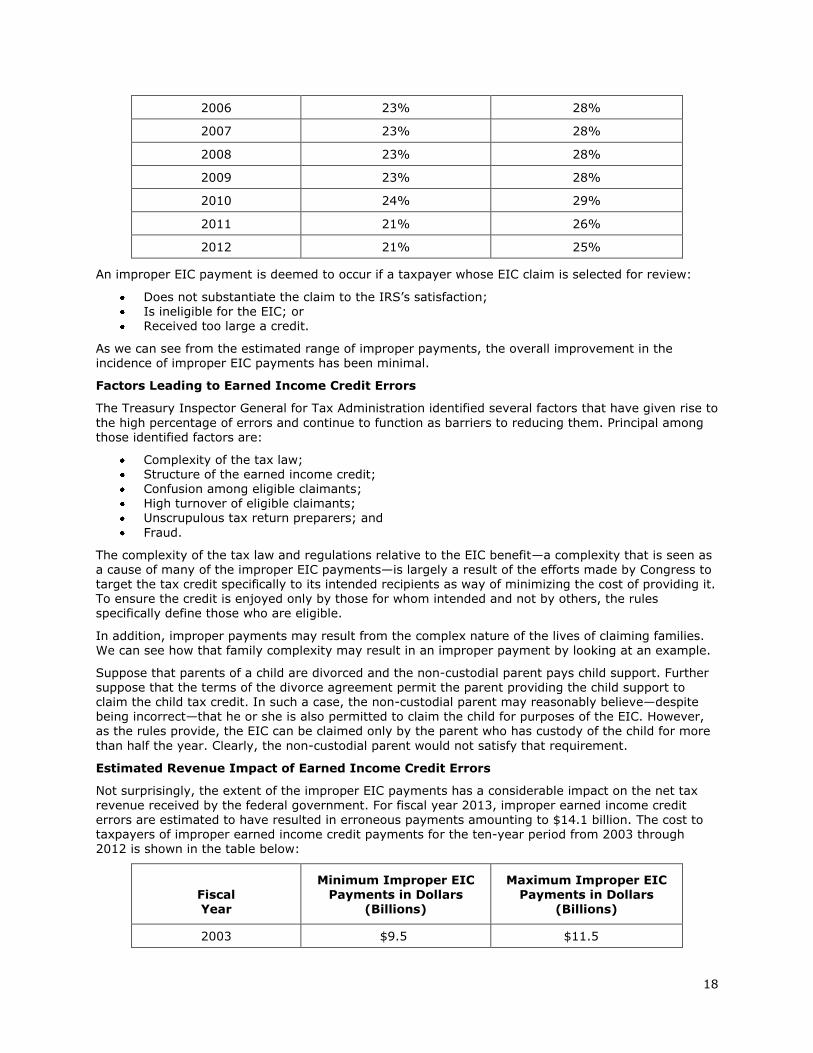

An improper EIC payment is deemed to occur if a taxpayer whose EIC claim is selected for review:

Does not substantiate the claim to the IRS’s satisfaction; Is ineligible for the EIC; or Received too large a credit.

As we can see from the estimated range of improper payments, the overall improvement in the incidence of improper EIC payments has been minimal.

Factors Leading to Earned Income Credit Errors

The Treasury Inspector General for Tax Administration identified several factors that have given rise to

the high percentage of errors and continue to function as barriers to reducing them. Principal among those identified factors are:

Complexity of the tax law; Structure of the earned income credit; Confusion among eligible claimants; High turnover of eligible claimants; Unscrupulous tax return preparers; and

Fraud.

The complexity of the tax law and regulations relative to the EIC benefit—a complexity that is seen as a cause of many of the improper EIC payments—is largely a result of the efforts made by Congress to

target the tax credit specifically to its intended recipients as way of minimizing the cost of providing it. To ensure the credit is enjoyed only by those for whom intended and not by others, the rules specifically define those who are eligible.

In addition, improper payments may result from the complex nature of the lives of claiming families. We can see how that family complexity may result in an improper payment by looking at an example.

Suppose that parents of a child are divorced and the non-custodial parent pays child support. Further suppose that the terms of the divorce agreement permit the parent providing the child support to claim the child tax credit. In such a case, the non-custodial parent may reasonably believe—despite being incorrect—that he or she is also permitted to claim the child for purposes of the EIC. However, as the rules provide, the EIC can be claimed only by the parent who has custody of the child for more

than half the year. Clearly, the non-custodial parent would not satisfy that requirement.

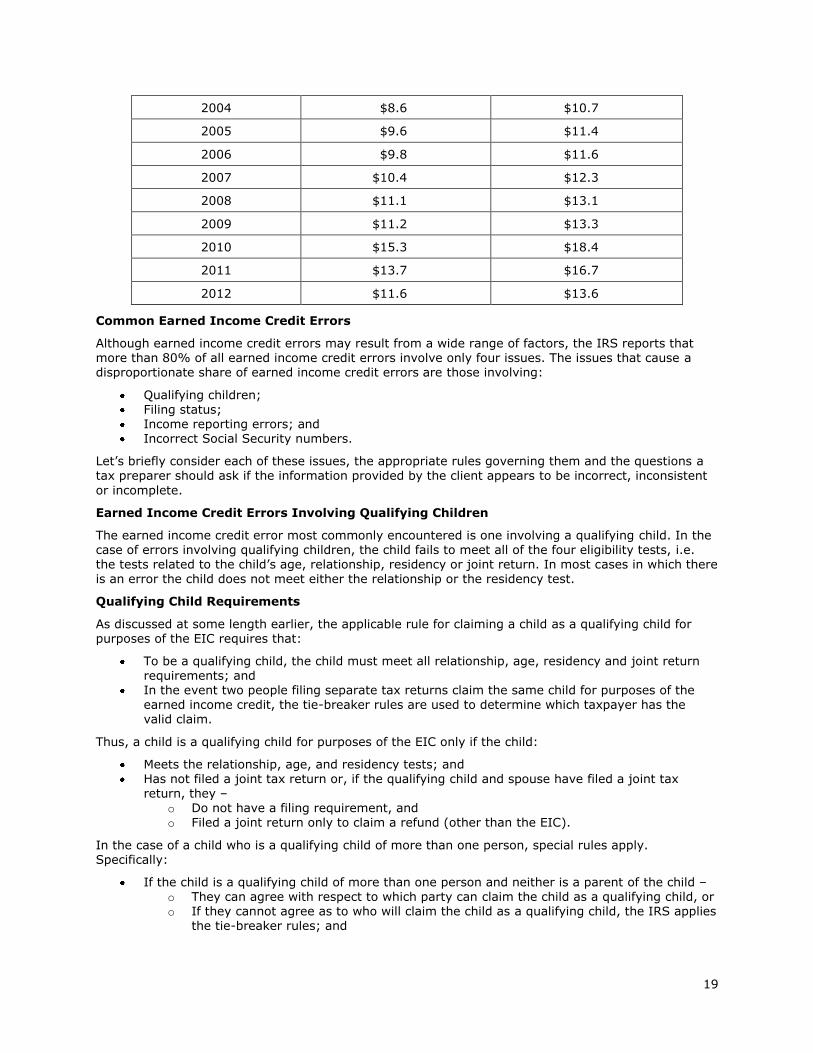

Estimated Revenue Impact of Earned Income Credit Errors

Not surprisingly, the extent of the improper EIC payments has a considerable impact on the net tax

revenue received by the federal government. For fiscal year 2013, improper earned income credit errors are estimated to have resulted in erroneous payments amounting to $14.1 billion. The cost to taxpayers of improper earned income credit payments for the ten-year period from 2003 through 2012 is shown in the table below:

Fiscal Year

Minimum Improper EIC Payments in Dollars

(Billions)

Maximum Improper EIC Payments in Dollars

(Billions)

2003 $9.5 $11.5

19

2004 $8.6 $10.7

2005 $9.6 $11.4

2006 $9.8 $11.6

2007 $10.4 $12.3

2008 $11.1 $13.1

2009 $11.2 $13.3

2010 $15.3 $18.4

2011 $13.7 $16.7

2012 $11.6 $13.6

Common Earned Income Credit Errors

Although earned income credit errors may result from a wide range of factors, the IRS reports that more than 80% of all earned income credit errors involve only four issues. The issues that cause a disproportionate share of earned income credit errors are those involving:

Qualifying children; Filing status; Income reporting errors; and Incorrect Social Security numbers.

Let’s briefly consider each of these issues, the appropriate rules governing them and the questions a tax preparer should ask if the information provided by the client appears to be incorrect, inconsistent

or incomplete.

Earned Income Credit Errors Involving Qualifying Children

The earned income credit error most commonly encountered is one involving a qualifying child. In the case of errors involving qualifying children, the child fails to meet all of the four eligibility tests, i.e. the tests related to the child’s age, relationship, residency or joint return. In most cases in which there

is an error the child does not meet either the relationship or the residency test.

Qualifying Child Requirements

As discussed at some length earlier, the applicable rule for claiming a child as a qualifying child for purposes of the EIC requires that:

To be a qualifying child, the child must meet all relationship, age, residency and joint return requirements; and

In the event two people filing separate tax returns claim the same child for purposes of the earned income credit, the tie-breaker rules are used to determine which taxpayer has the valid claim.

Thus, a child is a qualifying child for purposes of the EIC only if the child:

Meets the relationship, age, and residency tests; and Has not filed a joint tax return or, if the qualifying child and spouse have filed a joint tax

return, they –

o Do not have a filing requirement, and o Filed a joint return only to claim a refund (other than the EIC).

In the case of a child who is a qualifying child of more than one person, special rules apply. Specifically:

If the child is a qualifying child of more than one person and neither is a parent of the child – o They can agree with respect to which party can claim the child as a qualifying child, or o If they cannot agree as to who will claim the child as a qualifying child, the IRS applies

the tie-breaker rules; and

20

If the child is a qualifying child of more than one person and one or more of those persons is a

parent of a child, a person other than a parent can claim the child only if his or her AGI is higher than the AGI of any parent of the child.

When a Child is Disabled

In order for a non-disabled child to be considered a qualifying child, he or she must normally meet the relationship, age and residency tests. Accordingly, to meet the age test to be a qualifying child a non-disabled child must be under age 19 at the end of the year or a full-time student under the age of 24 at the end of the year. When a person meets the relationship, residency and joint return tests and is permanently and totally disabled, however, the age requirements applicable to being a qualifying child do not apply.

A person is considered “permanently and totally disabled” for purposes of the EIC if both of the

following conditions apply:

The person cannot engage in any substantial gainful activity due to a physical or mental condition; and

A doctor determines the condition has lasted or can be expected to last continuously for at

least a year or can lead to death.

The term substantial gainful activity is defined and discussed in IRS Publication 524. As discussed in

Publication 524 “Credit for the Elderly or Disabled” substantial gainful activity is the performance of significant duties over a reasonable period of time while working for pay or profit, or in work generally done for pay or profit. Full-time work (or part-time work done at an employer's convenience) in a competitive work situation for at least the minimum wage conclusively shows that the individual is able to engage in substantial gainful activity.

Substantial gainful activity is not work done by the individual to take care of himself or herself or the person’s home. It is not unpaid work on hobbies, institutional therapy or training, school attendance,

clubs, social programs, and similar activities. However, doing this kind of work may show that the individual is able to engage in substantial gainful activity.

The fact that the individual has not worked for some time is not, of itself, conclusive evidence that he or she cannot engage in substantial gainful activity.

Avoiding Qualifying Child Earned Income Credit Errors

It is important, as a way of avoiding EIC errors, for the tax preparer to ask the client additional questions if the preparer believes the information provided by the client is incorrect, inconsistent or

incomplete. Thus, additional questions about the qualifying child and the child’s relationship to the client should be asked of the client if the preparer encounters any of the following:

A client claims a qualifying child other than a son or daughter, the tax preparer should inquire as to –

o the location of the child’s parents, o whether the parent lives in the client’s household,

o whether any other relative lives in the client’s household, and o whether anyone else can claim the child as a qualifying child;

The client’s age is inconsistent with the age of the qualifying child, the tax preparer should verify the relationship between the client and the qualifying child;

The client is very young and has a qualifying child, the tax preparer should ask if the client could be a qualifying child of another person;

The client is a single taxpayer with a young qualifying child but no child care expenses, the tax

preparer should verify the child care arrangements or ask whether anyone else lives in the client’s household; or

The client claims an adult with a disability as a qualifying child, the tax preparer should verify that the adult meets the tax law definition of permanently and totally disabled (discussed above).

Earned Income Credit Errors Involving a Client’s Filing Status

A second common EIC error involves a client’s filing status. A client may qualify for the EIC with a

filing status of Married Filing Joint, Qualified Widow(er) with Dependent Child, Single or Head of

21

Household provided he or she is otherwise qualified for the credit. The only filing status that would

preclude a client’s eligibility for EIC is Married Filing Separate. However, the IRS notes that some married taxpayers falsely state they qualify for single or Head of Household filing status in order to claim more EIC.

Let’s briefly review the requirements for a client to file as Single or Head of Household.

Single Filing Status

A client may file as single only if he or she:

Had never been married; Was legally separated according to applicable state law under a divorce or separate

maintenance decree at the end of the year (if a divorce was not final at the end of the year, the client is considered married); or

Was widowed before the beginning of the tax year and did not remarry before the end of the year.

Head of Household Filing Status

More problematic from the perspective of filing status is the client who wishes to file as Head of Household. The ability to file as Head of Household is limited to unmarried individuals who provide a home for certain other persons and meet one of two tests related to the costs of maintaining a home

during the year.

A client is considered unmarried for purposes of filing as Head of Household if any of the following applies:

The client was legally separated according to applicable state law under a divorce or separate maintenance decree at the end of the year (if a divorce was not final at the end of the year, the client is considered married);

The client was married but lived apart from his or her spouse for the last 6 months of the year

and meets certain other rules applicable to married persons living apart; or The client is married to a nonresident alien at any time during the year and the client does not

elect to treat the spouse as a resident alien.

In addition to being considered unmarried, the client must meet one of the following tests:

The client paid more than half the cost of keeping up a home that was the main home for all of the year of the client’s parent who is claimed as a dependent (the parent does not have to live with the client); or

The client paid more than half the cost of keeping up a home in which the client lived and in which one of the following also lived for more than half the year –

o A person the client can claim as a dependent, except for – The client’s child who is claimed as a dependent because of the rule for

children of divorced or separated parents, A person who is the client’s dependent only because of living with the client

for all the year, or A person the client claimed as a dependent under a multiple support

agreement, o The client’s unmarried qualifying child who is not the client’s dependent, o The client’s married qualifying child who is not the client’s dependent only because the

client can be claimed as a dependent on another person’s return for the year, or

o The client’s qualifying child who is not the client’s dependent because of the rule for