Embed Size (px)

Citation preview

8/3/2019 DNH Sri Lanka Weekly 17-21 October 2011

http://slidepdf.com/reader/full/dnh-sri-lanka-weekly-17-21-october-2011 1/11

21-Oct

Prime Lending Rate (Avg. Weighted) 9.21%

Deposit Rate (Avg. Weighted) 6.48%

Treasury Bill Rate (360 Days) 7.34%

Dollar Denominated Bond Rate 6.25%

LKR/US$ (Selling Rate) 111.05

LKR/EURO (Selling Rate) 154.00

14-Oct 21-Oct WoW%

Sri Lanka - ASPI 6550 6357 -2.9

India - Sensex 17083 16785 -1.7

Pakistan - KSE 100 11992 11525 -3.9

Taiwan Weighted 7358 7255 -1.4

Singapore - Straits Times 2744 2712 -1.2

Hong Kong - Hang Seng 18502 18026 -2.6

D N H

M A R K

E T W

A T C H

Sri Lanka Weekly

Market Indices

In the absence of any significant news, the

Sri Lanka bourse continued its downward

trajectory with the ASPI and MPI losing

2.9% and 3.5%WOW to close at 6357 and

5675 respectively. With the majority of

investors sitting in the wings, turnover

dropped to its lowest level in recent

months, falling to LKR4.4 bn (-

35.3%WoW) with the only notable trades

recorded by John Keells Holdings, Colombo

Land and HVA Foods which collectively

accounted for 14% of the week’s total.

Global markets meanwhile traded largely

lower during the week as a result of

Moody’s cut of Spain’s credit rating to A1

Global Markets

17-21 October 2011

Market Performance

Interest Rates & Currencies

32.

14.3

12.8

9.4

-50.0

-37.5

-32.4

-25.0

Infrastructure

SMB Leasing (X)

Colombo Investment Trust

Ceylinco Ins. (X)

Serendib Land

Kalamazoo

Miramar

SMB Leasing (W 0016)

Gainers & Losers (%)

from Aa2 and the rating agency’s

war ning that it may lower France’ s

rating amid growing eurozone debt

concerns.

DNH Financial (Pvt) Ltd.

www.dnhfinancial.com

+94-11-5700777

This Week

Prv. Week WoW%

ASPI 6,357 6,550 -2.9

MPI 5,675 5,878 -3.5

Turnover (bn) 4.4 6.8 -35.3

Foreign Purchases (mn) 425 1213 -65.0

Foreign Sales (mn) 755 621 21.6

Traded Companies 253 255 -0.8

Market PER (X) 16.35 16.84 -2.9

Market Cap (LKR bn) 2,283 2,353 -3.0

Market Cap (US$ bn) 20.6 21.2 -3.0

Dividend Yield (%) 1.66 1.61 3.1

Price to Book (X) 2.07 2.13 -2.8

8/3/2019 DNH Sri Lanka Weekly 17-21 October 2011

http://slidepdf.com/reader/full/dnh-sri-lanka-weekly-17-21-october-2011 2/11

Page 2Sri Lanka Weekly17-21 October 2011

Market Performance

All eyes are now however focused on

Sunday’s EU meeting as investors wait with

bated breath in the hopes of securing a muchneeded panacea to the region’s crisis.

Kicking off the 3Q2011 corporate results

season, Piramal Glass released its results

recording a 25% jump in revenues and 54%

rise in earnings on the back of increased

volume growth notwithstanding relatively

higher input prices. Benefiting from the

robust growth in the local economy, we

expect the majority of the 3Q2011 corporate

results to record double digit quality

earnings growth as a result of higher

volumes and improved margins.

While the market PE on the local bourse has

been on a declining trend, we believe that

the current multiple of 16X does not fully

reflect the valuations of a number of

fundamentally strong stocks which aretrading at multiples of below 10X. With

investors having pushed up the price of

lower quality companies during the

2009/2010 bull run, an opportunity to invest

in companies of higher fundamental value

now exists with significant upside potential

of reversing relative underperformance.With

trading volumes showing increasing signs of

declining, we believe that the market iscoming close to a consolidation point before

changing course to a rerating. With the

majority of 3Q2011 results yet to be

released, we advise investors to take

advantage of this window period to select

stocks that are likely to outperform based

on solid intrinsic values.

Looking beyond the reported numbers

While the majority of economic indicators

point to a strong acceleration in the

domestic economy, we attempted to defy

the skeptics and look beyond the reportednumbers and test out the figures once and

for all. With the Sri Lankan economy

growing at an amazing 8.3%, it was highly

important for us to determine the extent of

the trickle down effect on the masses,

especially the middle income class that

accounts for the majority of the population

and whose consumer patterns will largely

fuel future economic growth and shape its

trajectory.

A Random walk down Colombo

We started our journey with the dine-outs.

Restaurants are generally a good proxy of

consumer spending and a reasonably

reliable indicator of economic momentum in

the country. Having stopped by several ofColombo’s restaurants, both fine dining and

low to mid end quick service

establishments, we were not surprised by

our findings. Most restaurants were full,

notably fine dining areas. What was

interesting to note was that up to 75-90% of

guests at city five star restaurants were

locals indicating that disposable incomes

were rising with domestic consumers clearly

not in a hurry to tie up their purse strings

against the backdrop of international

recessionary pressures and a slowdown in

global consumption.

8/3/2019 DNH Sri Lanka Weekly 17-21 October 2011

http://slidepdf.com/reader/full/dnh-sri-lanka-weekly-17-21-october-2011 3/11

Page 3Sri Lanka Weekly17-21 October 2011

Checking in to hotels

It is definitely encouraging to note that

tourist arrivals to Sri Lanka is growing at

strong double digit rates, notwithstanding a

slowdown in the global travel industry andtourists becoming more value conscious

with their tourist dollars. While foreign

tourists have traditionally been responsible

for high hotel occupancy levels, a recent

development has been the increasing take

up of hotel rooms by local guests, a trend

that clearly reveals a specific rise in the

disposable income of selected consumer

segments.

While this is not uncommon in the case of

resort hotels which normally experience a

flurry of local guests during the weekends,

this appears to be a new phenomenon for

the city hotels whose live-in guests have

traditionally being wholly foreign visitors.

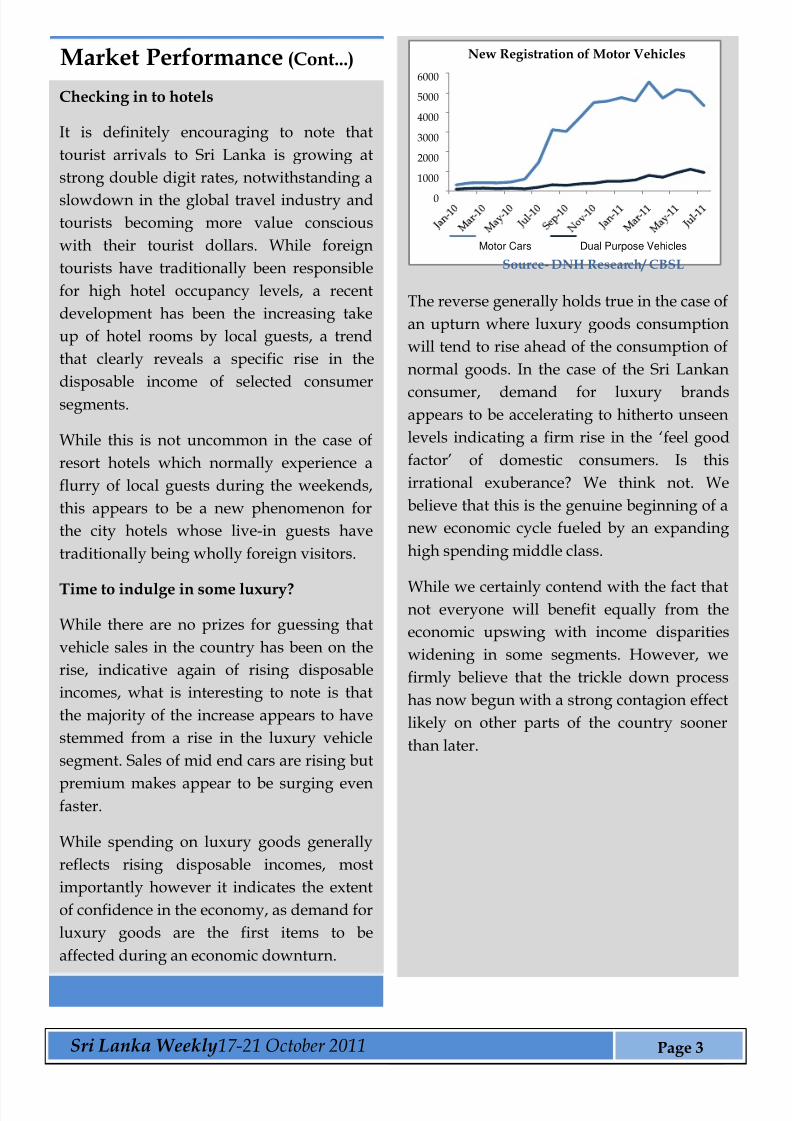

Time to indulge in some luxury?

While there are no prizes for guessing that

vehicle sales in the country has been on the

rise, indicative again of rising disposable

incomes, what is interesting to note is that

the majority of the increase appears to have

stemmed from a rise in the luxury vehicle

segment. Sales of mid end cars are rising but

premium makes appear to be surging evenfaster.

While spending on luxury goods generally

reflects rising disposable incomes, most

importantly however it indicates the extent

of confidence in the economy, as demand for

luxury goods are the first items to be

affected during an economic downturn.

Market Performance (Cont...)

The reverse generally holds true in the case of

an upturn where luxury goods consumption

will tend to rise ahead of the consumption of

normal goods. In the case of the Sri Lankan

consumer, demand for luxury brandsappears to be accelerating to hitherto unseen

levels indicating a firm rise in the ‘feel good

factor’ of domestic consumers. Is this

irrational exuberance? We think not. We

believe that this is the genuine beginning of a

new economic cycle fueled by an expanding

high spending middle class.

While we certainly contend with the fact thatnot everyone will benefit equally from the

economic upswing with income disparities

widening in some segments. However, we

firmly believe that the trickle down process

has now begun with a strong contagion effect

likely on other parts of the country sooner

than later.

0

1000

2000

3000

4000

5000

6000

New Registration of Motor Vehicles

Motor Cars Dual Purpose Vehicles

Source- DNH Research/ CBSL

8/3/2019 DNH Sri Lanka Weekly 17-21 October 2011

http://slidepdf.com/reader/full/dnh-sri-lanka-weekly-17-21-october-2011 4/11

Page 4Sri Lanka Weekly17-21 October 2011

Outbound not just inbound tourism is on the

rise

While inbound tourist traffic has clearly seen a

prolific rise, outbound tourism appears to beenjoying similar growth. While we do agree

that this is partly due to a general decline in

the price of holiday packages, the volume of

traffic nevertheless indicates that domestic

consumers do have pockets deep enough to

indulge in an overseas leisure experience and

we expect this trend to only increase going

forward.

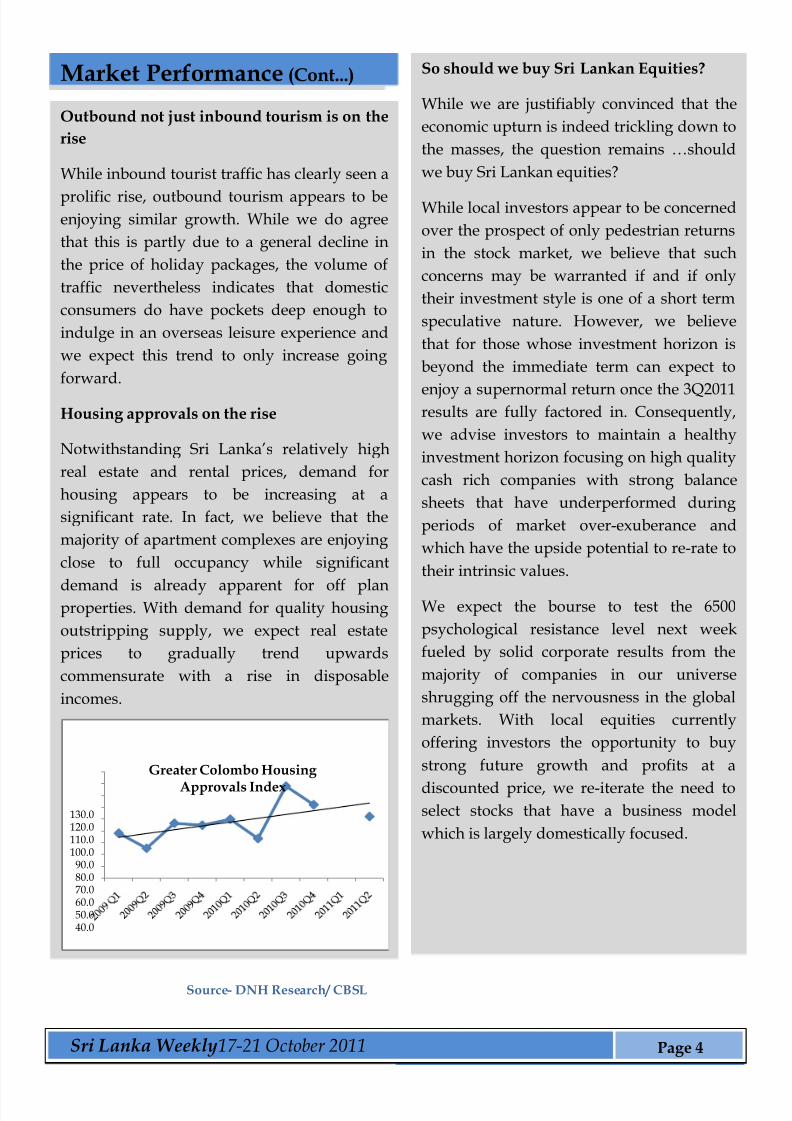

Housing approvals on the rise

Notwithstanding Sri Lanka’s relatively high

real estate and rental prices, demand for

housing appears to be increasing at a

significant rate. In fact, we believe that the

majority of apartment complexes are enjoying

close to full occupancy while significant

demand is already apparent for off planproperties. With demand for quality housing

outstripping supply, we expect real estate

prices to gradually trend upwards

commensurate with a rise in disposable

incomes.

40.050.060.070.080.090.0

100.0110.0120.0130.0

Greater Colombo Housing

Approvals Index

Source- DNH Research/ CBSL

Market Performance (Cont...) So should we buy Sri Lankan Equities?

While we are justifiably convinced that the

economic upturn is indeed trickling down to

the masses, the question remains …should

we buy Sri Lankan equities?

While local investors appear to be concerned

over the prospect of only pedestrian returns

in the stock market, we believe that such

concerns may be warranted if and if only

their investment style is one of a short term

speculative nature. However, we believe

that for those whose investment horizon is

beyond the immediate term can expect to

enjoy a supernormal return once the 3Q2011results are fully factored in. Consequently,

we advise investors to maintain a healthy

investment horizon focusing on high quality

cash rich companies with strong balance

sheets that have underperformed during

periods of market over-exuberance and

which have the upside potential to re-rate to

their intrinsic values.

We expect the bourse to test the 6500

psychological resistance level next week

fueled by solid corporate results from the

majority of companies in our universe

shrugging off the nervousness in the global

markets. With local equities currently

offering investors the opportunity to buy

strong future growth and profits at a

discounted price, we re-iterate the need toselect stocks that have a business model

which is largely domestically focused.

8/3/2019 DNH Sri Lanka Weekly 17-21 October 2011

http://slidepdf.com/reader/full/dnh-sri-lanka-weekly-17-21-october-2011 5/11

Page 5Sri Lanka Weekly17-21 October 2011

Kicking off the corporate results season,

Piramal Glass released its 3Q2011 results

recording a 25% jump in revenues and 54% rise

in earnings on the back of increased volume

growth notwithstanding higher input pricesduring the period. Benefiting from the robust

growth in the local economy, we expect the

majority of the 3Q2011 corporate results

releases to follow a similar trend of higher

volume growth driving double digit earnings

growth. In this respect, we advise investors to

focus on companies with largely monopolistic

attributes and brand loyalty within sectors and

sub-sectors that are both growth and resilient

and will be direct beneficiaries of the domestic

economic upturn.

by strong macroeconomic fundamentals

and a continued expansion in both the

private and government sectors. With real

GDP growth forecast at between 8-9% in the

coming years, bank credit should grow

faster enabling commercial banks to report

robust interest income which will bereflected in strong earnings growth for most

banks. Firm capital structures and sound

leverage ratios will provide a solid

foundation for growth while consumer,

commercial and government related

lending activities will drive sector earnings

as private consumption continues to rise.

Cor orate News

Economic News

Bank credit growth slows in July 2011

Bank credit rose by 34.1% to LKR 1.78 trillion as

of Aug 2011 compared to 33.9% recorded as at

July. Credit issued by domestic banks grew by

35.9% to LKR1.59 trillion while foreign banks

accounted for LKR181.8 bn (+19.7%).

Meanwhile, new loans generated during the

first 8 months of the year recorded LKR260 bn

with a significant proportion of this made to the

government reflecting the heightened economicactivity in the country.

In Sri Lanka, credit growth is not only pro-

cyclical, but tends to grow faster than GDP

during expansions and more slowly during

recessions. While credit growth could see an

easing off during the 4th quarter, we expect

momentum to resume in 2012 underpinned

Global Outlook

Unites States

On the back of the twin impact of strong

3Q2011 corporate profits combined with

expectations of positive announcements

from the EU summit, US equities posted its

third straight week of gains with the S&P

500 up 1.1% for the week. While recent

market gains have pushed the S&P 500 to

the top of its trading range between 1,230

and 1,250, investors are likely to

increasingly watch developments in Europe

before allowing company earnings to push

stocks higher. Given that US equities arecurrently trading at a multiple of 10-11X on

2012 earnings, the critical question is

whether to selectively buy fundamentally

strong stocks that are attractively valued or

continue to remain on the sidelines in

expectation of a bottoming out. With US

equities having traditionally traded on a PE

of 13-14X during a recession, current

trading multiples appear increasingly

8/3/2019 DNH Sri Lanka Weekly 17-21 October 2011

http://slidepdf.com/reader/full/dnh-sri-lanka-weekly-17-21-october-2011 6/11

Page 6Sri Lanka Weekly17-21 October 2011

attractive for certain counters.

Notwithstanding market valuations, it may

take more than an attractive PE to lure

investors into equities with strong positive

signals from the EU Summit likely to be adeciding factor.

Eurozone

Eurozone equities traded with a downward

bias as investors sat in the wings ahead of the

EU meeting on Sunday where talks are to be

held by the region’s policymakers on how to

contain the ongoing debt crisis. The Eurostoxx

50 consequently declined by 1.3% during the

week led mainly by declines in the DAX and

FTSE 100. Notwithstanding the prospect of a

possible positive outcome at the EU meetings,

Germany and France still appear to be at

relative disagreement on how to scale up the

European Financial Stability Facility and how

to cut Greek debt. Europe’s economic roller-

coaster ride meanwhile continued during theweek with Moody’s downgrading Spain’s

credit rating by two notches to A1 from Aa2

followed by downgrades by S&P and Fitch. In

addition, Moody’s has also warned France that

by backing the European rescue fund, its own

credit rating could be at risk. While a positive

trajectory for the markets could eventuate

following Sunday’s EU summit

announcements, the medium to longer termoutlook remains merky given the highly

complicated structure of the euro zone and the

difficulty in swift implementation of any

decisions reached.

Asia

Asian equities closed the week on a neutral

note ahead of the Eurozone’s crucial

meeting on Sunday aimed at finding a

solution to Europe’s debt crisis.

Consequently, the Asia Pacific index closedmarginally lower to end the week down

0.9%. Stocks suffered on Thursday in the

run-up to the weekend’s scheduled EU

summit as a barrage of conflicting headlines

pointed to discord between key parties and

delays in announcing a plan. Meanwhile

China announced during the week that it

would allow four of its local governments to

begin issuing their own debt widely seen asa boost for the Chinese banking sector and

the broader economy especially after Beijing

released lower than expected 3Q2011

economic growth figures which showed

Chinese GDP growth slowing down to 9.1%

compared to market expectations of 9.2%

and higher. The figures may stoke concerns

that a slowdown in orders from the U.S. and

Europe could be denting Chinese growth

while stubbornly high inflationary figures

could also pose a challenge.

Global Outlook

8/3/2019 DNH Sri Lanka Weekly 17-21 October 2011

http://slidepdf.com/reader/full/dnh-sri-lanka-weekly-17-21-october-2011 7/11

Page 7Sri Lanka Weekly17-21 October 2011

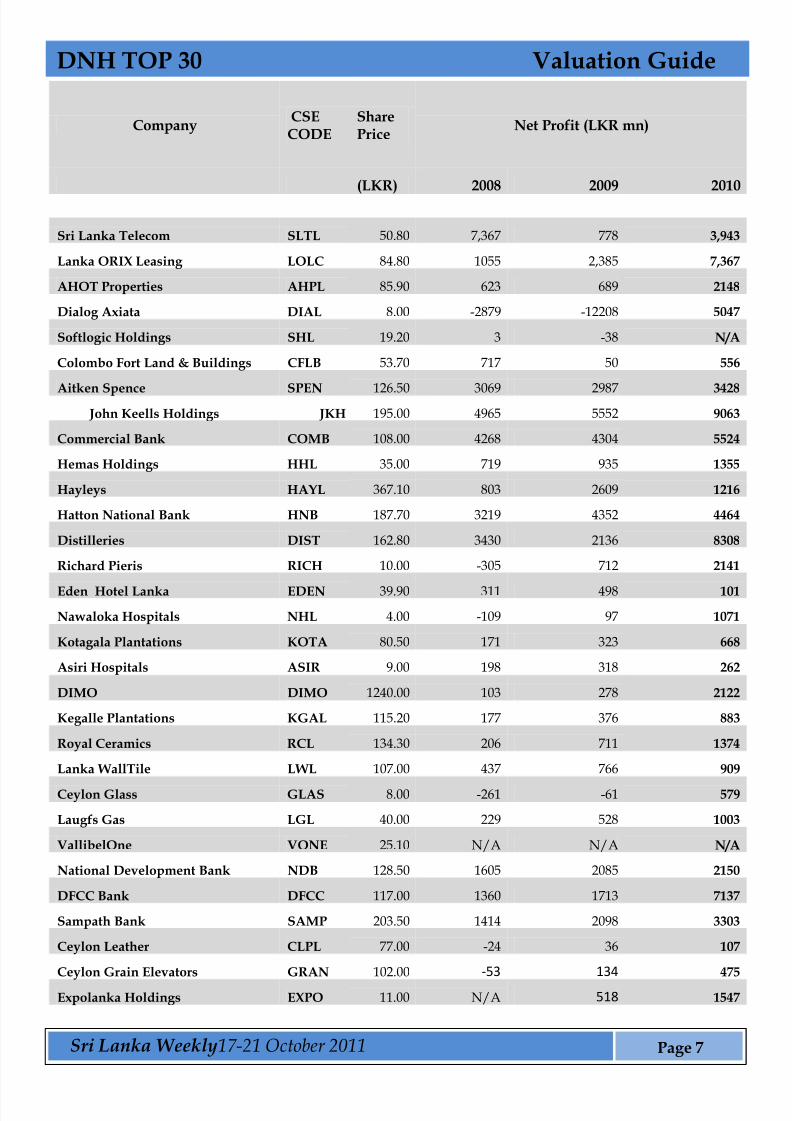

CompanyCSECODE

SharePrice

Net Profit (LKR mn)

(LKR) 2008 2009 2010

Sri Lanka Telecom SLTL 50.80 7,367 778 3,943

Lanka ORIX Leasing LOLC 84.80 1055 2,385 7,367

AHOT Properties AHPL 85.90 623 689 2148

Dialog Axiata DIAL 8.00 -2879 -12208 5047

Softlogic Holdings SHL 19.20 3 -38 N/A

Colombo Fort Land & Buildings CFLB 53.70 717 50 556

Aitken Spence SPEN 126.50 3069 2987 3428 John Keells Holdings JKH 195.00 4965 5552 9063

Commercial Bank COMB 108.00 4268 4304 5524

Hemas Holdings HHL 35.00 719 935 1355

Hayleys HAYL 367.10 803 2609 1216

Hatton National Bank HNB 187.70 3219 4352 4464

Distilleries DIST 162.80 3430 2136 8308

Richard Pieris RICH 10.00 -305 712 2141

Eden Hotel Lanka EDEN 39.90 311 498 101

Nawaloka Hospitals NHL 4.00 -109 97 1071

Kotagala Plantations KOTA 80.50 171 323 668

Asiri Hospitals ASIR 9.00 198 318 262

DIMO DIMO 1240.00 103 278 2122

Kegalle Plantations KGAL 115.20 177 376 883

Royal Ceramics RCL 134.30 206 711 1374

Lanka WallTile LWL 107.00 437 766 909

Ceylon Glass GLAS 8.00 -261 -61 579

Laugfs Gas LGL 40.00 229 528 1003

VallibelOne VONE 25.10 N/A N/A N/A

National Development Bank NDB 128.50 1605 2085 2150

DFCC Bank DFCC 117.00 1360 1713 7137

Sampath Bank SAMP 203.50 1414 2098 3303

Ceylon Leather CLPL 77.00 -24 36 107

Ceylon Grain Elevators GRAN 102.00 -53 134 475

Expolanka Holdings EXPO 11.00 N/A 518 1547

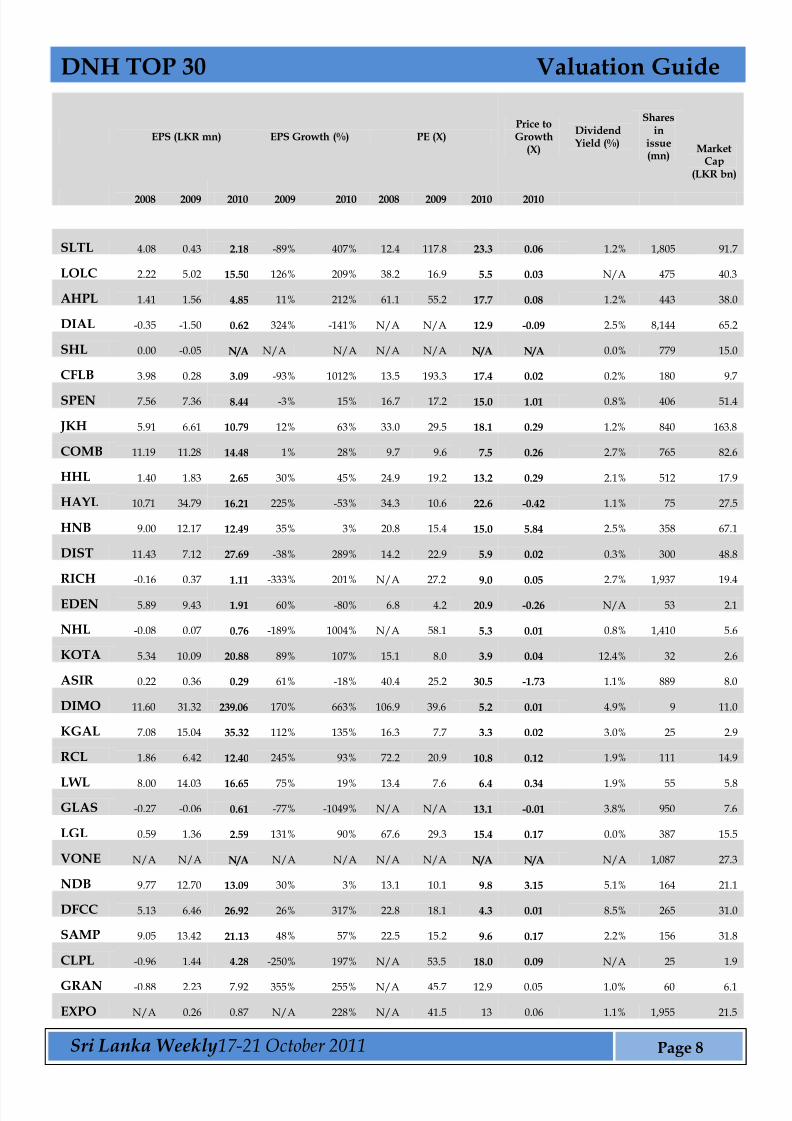

DNH TOP 30 Valuation Guide

8/3/2019 DNH Sri Lanka Weekly 17-21 October 2011

http://slidepdf.com/reader/full/dnh-sri-lanka-weekly-17-21-october-2011 8/11

Page 8Sri Lanka Weekly17-21 October 2011

EPS (LKR mn) EPS Growth (%) PE (X)Price toGrowth

(X)

DividendYield (%)

Sharesin

issue(mn)

MarketCap

(LKR bn)

2008 2009 2010 2009 2010 2008 2009 2010 2010

SLTL 4.08 0.43 2.18 -89% 407% 12.4 117.8 23.3 0.06 1.2% 1,805 91.7

LOLC 2.22 5.02 15.50 126% 209% 38.2 16.9 5.5 0.03 N/A 475 40.3

AHPL 1.41 1.56 4.85 11% 212% 61.1 55.2 17.7 0.08 1.2% 443 38.0

DIAL -0.35 -1.50 0.62 324% -141% N/A N/A 12.9 -0.09 2.5% 8,144 65.2

SHL 0.00 -0.05 N/A N/A N/A N/A N/A N/A N/A 0.0% 779 15.0

CFLB 3.98 0.28 3.09 -93% 1012% 13.5 193.3 17.4 0.02 0.2% 180 9.7

SPEN 7.56 7.36 8.44 -3% 15% 16.7 17.2 15.0 1.01 0.8% 406 51.4

JKH 5.91 6.61 10.79 12% 63% 33.0 29.5 18.1 0.29 1.2% 840 163.8

COMB 11.19 11.28 14.48 1% 28% 9.7 9.6 7.5 0.26 2.7% 765 82.6

HHL 1.40 1.83 2.65 30% 45% 24.9 19.2 13.2 0.29 2.1% 512 17.9

HAYL 10.71 34.79 16.21 225% -53% 34.3 10.6 22.6 -0.42 1.1% 75 27.5

HNB 9.00 12.17 12.49 35% 3% 20.8 15.4 15.0 5.84 2.5% 358 67.1

DIST 11.43 7.12 27.69 -38% 289% 14.2 22.9 5.9 0.02 0.3% 300 48.8

RICH -0.16 0.37 1.11 -333% 201% N/A 27.2 9.0 0.05 2.7% 1,937 19.4

EDEN 5.89 9.43 1.91 60% -80% 6.8 4.2 20.9 -0.26 N/A 53 2.1

NHL -0.08 0.07 0.76 -189% 1004% N/A 58.1 5.3 0.01 0.8% 1,410 5.6

KOTA 5.34 10.09 20.88 89% 107% 15.1 8.0 3.9 0.04 12.4% 32 2.6

ASIR 0.22 0.36 0.29 61% -18% 40.4 25.2 30.5 -1.73 1.1% 889 8.0

DIMO 11.60 31.32 239.06 170% 663% 106.9 39.6 5.2 0.01 4.9% 9 11.0

KGAL 7.08 15.04 35.32 112% 135% 16.3 7.7 3.3 0.02 3.0% 25 2.9

RCL 1.86 6.42 12.40 245% 93% 72.2 20.9 10.8 0.12 1.9% 111 14.9

LWL 8.00 14.03 16.65 75% 19% 13.4 7.6 6.4 0.34 1.9% 55 5.8

GLAS -0.27 -0.06 0.61 -77% -1049% N/A N/A 13.1 -0.01 3.8% 950 7.6

LGL 0.59 1.36 2.59 131% 90% 67.6 29.3 15.4 0.17 0.0% 387 15.5

VONE N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A 1,087 27.3

NDB 9.77 12.70 13.09 30% 3% 13.1 10.1 9.8 3.15 5.1% 164 21.1

DFCC 5.13 6.46 26.92 26% 317% 22.8 18.1 4.3 0.01 8.5% 265 31.0

SAMP 9.05 13.42 21.13 48% 57% 22.5 15.2 9.6 0.17 2.2% 156 31.8

CLPL -0.96 1.44 4.28 -250% 197% N/A 53.5 18.0 0.09 N/A 25 1.9

GRAN -0.88 2.23 7.92 355% 255% N/A 45.7 12.9 0.05 1.0% 60 6.1

EXPO N/A 0.26 0.87 N/A 228% N/A 41.5 13 0.06 1.1% 1,955 21.5

DNH TOP 30 Valuation Guide

8/3/2019 DNH Sri Lanka Weekly 17-21 October 2011

http://slidepdf.com/reader/full/dnh-sri-lanka-weekly-17-21-october-2011 9/11

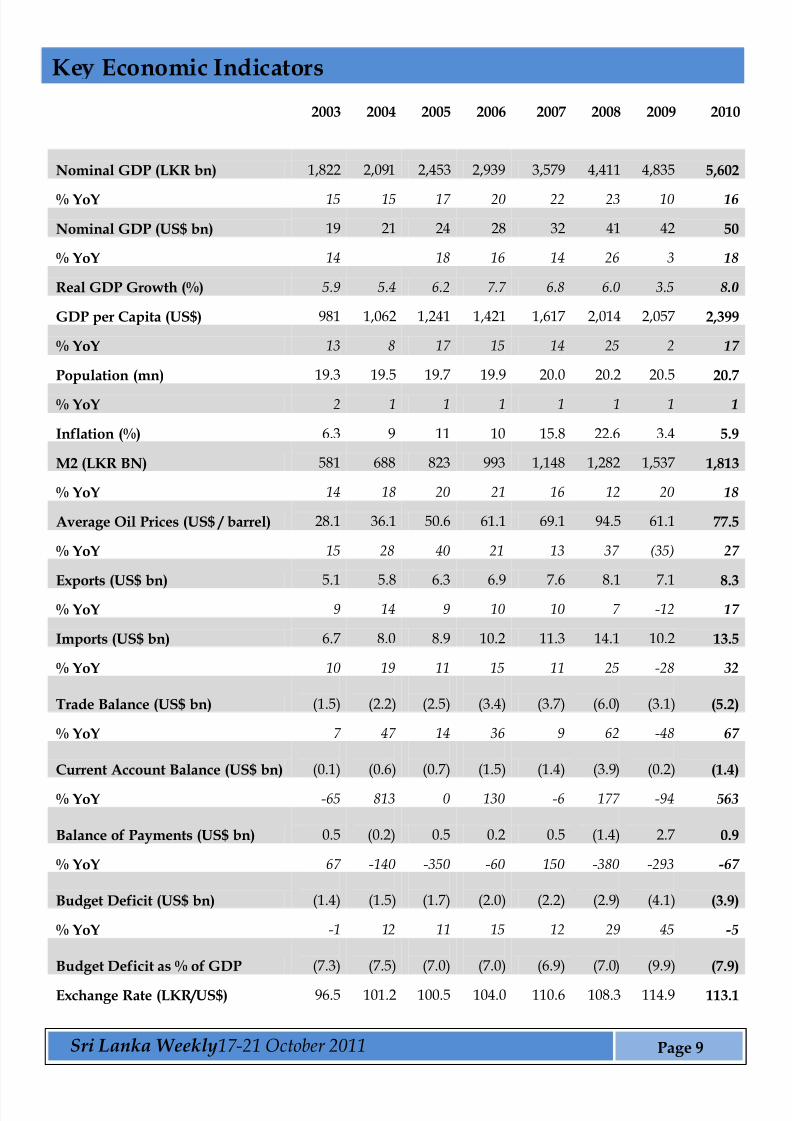

Page 9Sri Lanka Weekly17-21 October 2011

2003 2004 2005 2006 2007 2008 2009 2010

Nominal GDP (LKR bn) 1,822 2,091 2,453 2,939 3,579 4,411 4,835 5,602

% YoY 15 15 17 20 22 23 10 16

Nominal GDP (US$ bn) 19 21 24 28 32 41 42 50

% YoY 14 18 16 14 26 3 18

Real GDP Growth (%) 5.9 5.4 6.2 7.7 6.8 6.0 3.5 8.0

GDP per Capita (US$) 981 1,062 1,241 1,421 1,617 2,014 2,057 2,399

% YoY 13 8 17 15 14 25 2 17

Population (mn) 19.3 19.5 19.7 19.9 20.0 20.2 20.5 20.7

% YoY 2 1 1 1 1 1 1 1

Inflation (%) 6.3 9 11 10 15.8 22.6 3.4 5.9

M2 (LKR BN) 581 688 823 993 1,148 1,282 1,537 1,813

% YoY 14 18 20 21 16 12 20 18

Average Oil Prices (US$ / barrel) 28.1 36.1 50.6 61.1 69.1 94.5 61.1 77.5

% YoY 15 28 40 21 13 37 (35) 27

Exports (US$ bn) 5.1 5.8 6.3 6.9 7.6 8.1 7.1 8.3

% YoY 9 14 9 10 10 7 -12 17

Imports (US$ bn) 6.7 8.0 8.9 10.2 11.3 14.1 10.2 13.5

% YoY 10 19 11 15 11 25 -28 32

Trade Balance (US$ bn) (1.5) (2.2) (2.5) (3.4) (3.7) (6.0) (3.1) (5.2)

% YoY 7 47 14 36 9 62 -48 67

Current Account Balance (US$ bn) (0.1) (0.6) (0.7) (1.5) (1.4) (3.9) (0.2) (1.4)

% YoY -65 813 0 130 -6 177 -94 563

Balance of Payments (US$ bn) 0.5 (0.2) 0.5 0.2 0.5 (1.4) 2.7 0.9

% YoY 67 -140 -350 -60 150 -380 -293 -67

Budget Deficit (US$ bn) (1.4) (1.5) (1.7) (2.0) (2.2) (2.9) (4.1) (3.9)

% YoY -1 12 11 15 12 29 45 -5

Budget Deficit as % of GDP (7.3) (7.5) (7.0) (7.0) (6.9) (7.0) (9.9) (7.9)

Exchange Rate (LKR/US$) 96.5 101.2 100.5 104.0 110.6 108.3 114.9 113.1

Ke Economic Indicators

8/3/2019 DNH Sri Lanka Weekly 17-21 October 2011

http://slidepdf.com/reader/full/dnh-sri-lanka-weekly-17-21-october-2011 10/11

Page 10Sri Lanka Weekly17-21 October 2011

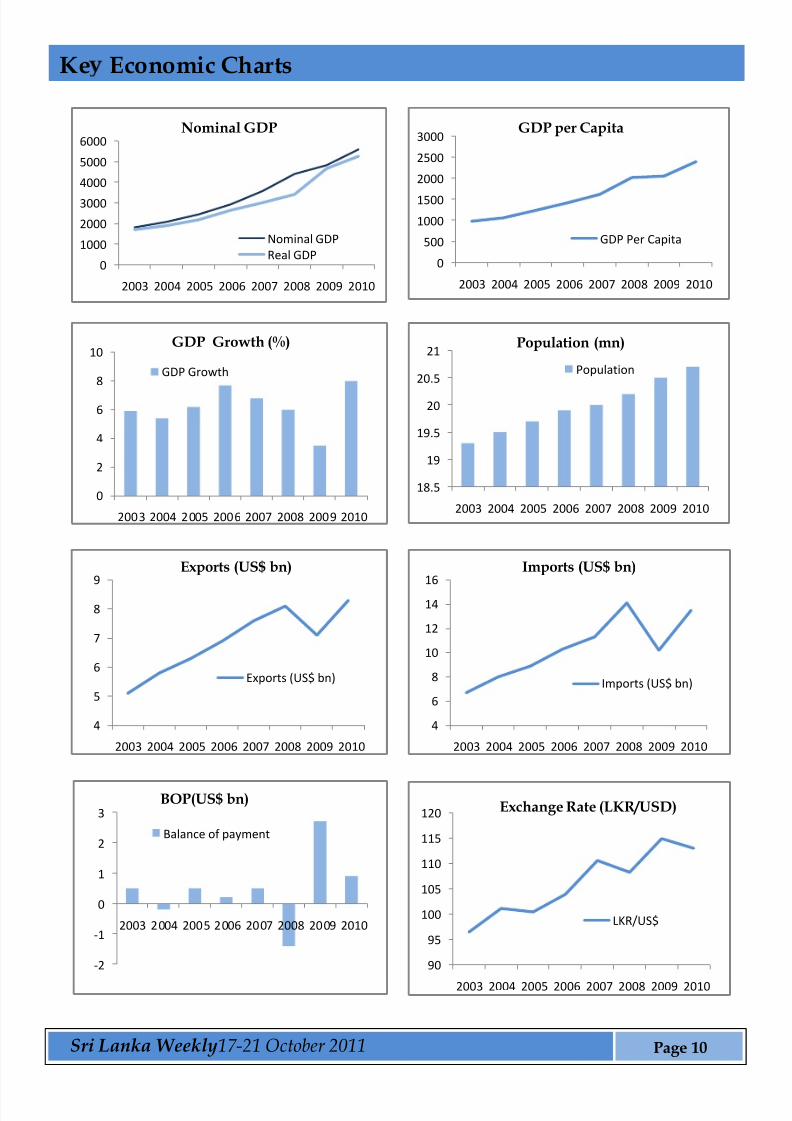

0

1000

2000

3000

4000

5000

6000

2003 2004 2005 2006 2007 2008 2009 2010

Nominal GDP

Nominal GDP

Real GDP0

500

1000

1500

2000

2500

3000

2003 2004 2005 2006 2007 2008 2009 2010

GDP per Capita

GDP Per Capita

0

2

4

6

8

10

2003 2004 2005 2006 2007 2008 2009 2010

GDP Growth (%)

GDP Growth

18.5

19

19.5

20

20.5

21

2003 2004 2005 2006 2007 2008 2009 2010

Population (mn)

Population

4

5

6

7

8

9

2003 2004 2005 2006 2007 2008 2009 2010

Exports (US$ bn)

Exports (US$ bn)

4

6

8

10

12

14

16

2003 2004 2005 2006 2007 2008 2009 2010

Imports (US$ bn)

Imports (US$ bn)

-2

-1

0

1

2

3

2003 2004 2005 2006 2007 2008 2009 2010

BOP(US$ bn)

Balance of payment

90

95

100

105

110

115

120

2003 2004 2005 2006 2007 2008 2009 2010

Exchange Rate (LKR/USD)

LKR/US$

Ke Economic Charts

8/3/2019 DNH Sri Lanka Weekly 17-21 October 2011

http://slidepdf.com/reader/full/dnh-sri-lanka-weekly-17-21-october-2011 11/11

Page 11Sri Lanka Weekly17-21 October 2011

Disclaimer

This Review is prepared and issued by DNH Financial (Pvt.) Ltd. (DNH) based on information in the public domain, internally developed and other sources, believed to be correct. Although all reasonable carehas been taken to ensure the contents of the Review are accurate, DNH and/or its Directors,employees, are not responsible for the correctness, usefulness, reliability of same. DNH may act as a

Broker in the investments which are the subject of this document or related investments and may haveacted on or used the information contained in this document, or the research or analysis on which it isbased, before its publication. DNH and/or its principal, their respective Directors, or Employees may alsohave a position or be otherwise interested in the investments referred to in this document. This is not anoffer to sell or buy the investments referred to in this document. This Review may contain data which areinaccurate and unreliable. You hereby waive irrevocably any rights or remedies in law or equity you haveor may have against DNH with respect to the Review and agree to indemnify and hold DNH and/or its principal, their respective directors and employees harmless to the fullest extent allowed by law regarding all matters related to your use of this Review.No part of this document may be reproduced, distributed or published in whole or in part by any means to any other person for any purpose without prior permission.DNH Financial is a fully owned subsidiary of Environmental Resources Investment PLC(ERI).

Contacts

Sales Desk: +94115700707, +94115732222, +94115700777

Branch Sales: Negombo- +94 31-5676451, Jaffna-+94212224929

Research:+94115700726

Website: www.dnhfinancial.com

E- mail: [email protected]

Head Office Branch Service Center

Level 16, West Tower,

World Trade Centre,

Colombo-01, Sri Lanka.

No.72, Palaly Road,

Iluppaiyadi Junction,

Jaffna.

No. 142, Greens Rd,

Negombo.