Embed Size (px)

Citation preview

Divorce: When a Spouse Files BankruptcyDischargeability of Domestic Support Obligations and Property Settlements

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

WEDNESDAY, FEBRUARY 15, 2012

Presenting a live 90-minute webinar with interactive Q&A

Kenneth Paul Carp, Atty, Law Office of Kenneth P. Carp, Clayton, Mo.

Amy L. Gervich, Atty, Law Office of Amy L. Gervich, St. Louis

Charles E. N. Rosene, Atty, Law Office of Charles E.N. Rosene, Saint Charles, Mo.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits

For CLE purposes, please let us know how many people are listening at your location by completing each of the following steps:

• Close the notification box

• In the chat box, type (1) your company name and (2) the number of attendees at your location

• Click the SEND button beside the box

FOR LIVE EVENT ONLY

Tips for Optimal Quality

Sound QualityIf you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory and you are listening via your computer speakers, you may listen via the phone: dial 1-866-961-9091 and enter your PIN -when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

BANKRUPTCY AND DIVORCE

Kenneth P. CarpAmy L. Gervich

Charles E. N. Rosene 5

OVERVIEW• Bankruptcy Basics

– Chapter 7 vs. Chapter 13• Who files and When

• Bankruptcy Estate and Limitation

• Qualified Domestic Support Obligations – Exception: 11 U.S.C. § 523(a)(5)– Property Settlement Debt Exception: 11 U.S.C. § 523(a)(15)– Automatic Stay– Preferential Treatment of Creditors

• Separation Agreements– Factors Courts look at– Intent of the parties– Protect your fee– Protect your client from “spousal revenge”

• Foreclosure• Practical Tips/Possible Pitfalls

6

Divorce vs. BankruptcyEither the last thing together or the first thing separate

• Divorce– Can provide:

• fresh start • separation of assets• visitation of children

• Just a divorce can help you start over and rebuild life, bankruptcy can help you rebuild your financial affairs by getting rid of old debts and allow you to rebuild your financial future

7

CHAPTER 7• Purpose

– Fresh Start– To have the debts discharged while keeping exempt property

• Debt is Discharged– Section 523(a) of the bankruptcy code sets forth all non-

dischargeable debts• Means test is qualifying criteria

– Looks at income from all sources in last 6 months– If the mean income exceeds income threshold, then there are

deductions to see whether they qualify– Deductions including:

• Non cmi income • Taxes• Secured debt repayment• Court ordered DSO

– If they don’t qualify for a 7 (too much income or failed means test), then Chapter 13

8

CHAPTER 13• Repayment of debt over 3 or 5 years

– Allows debtor to keep your property– Some unsecured debt can get discharged– Some junior mortgages can be discharged

• Characterization of DSO– Unsecured DSO has priority over other debts– No discharge unless all DSO obligations are met

• Including pre-petition arrearages• Non-Filing Spouse and Chapter 13

– Ex-spouse can: • review plan and object to confirmation of Chapter 13 plan• file a claim• appear at the meeting of creditors

– If debtor is not current in post-petition domestic support, the ex-spouse may consider filing a motion to dismiss

• Is that in his/her best interest?• Assessing value of assets

– Bankruptcy = liquidation value– Divorce = market value– Be sensitive to the interplay between valuing assets in bankruptcy and divorce

9

CHAPTER 7 CHAPTER 13

• Discharge of Debts• Means Test to Qualify• Keep exempt

Property• Over in 3 or 5 months• Reaffirm mortgages

• Easy to complete

• Pay Debts• Plan to Qualify• Keep all Property

• Over in 3 or 5 years• Renegotiate

mortgages• Very difficult to

complete10

Chapter 7/Chapter 13 Income Qualifiers

• Chapter 7– Means Test/Threshold

(Missouri only)• Single <$39,332• 2 People <$51,120• 3 People <$58,610• 4 People <$69,832• 5 People <$77,332• 6 People <$84,832

– Household Size– Secured Debt

Payments

• Chapter 13– Every dollar is

accounted for– Can’t have over

$336,900 unsecured debt OR

– Over $1,010,650 secured debts

11

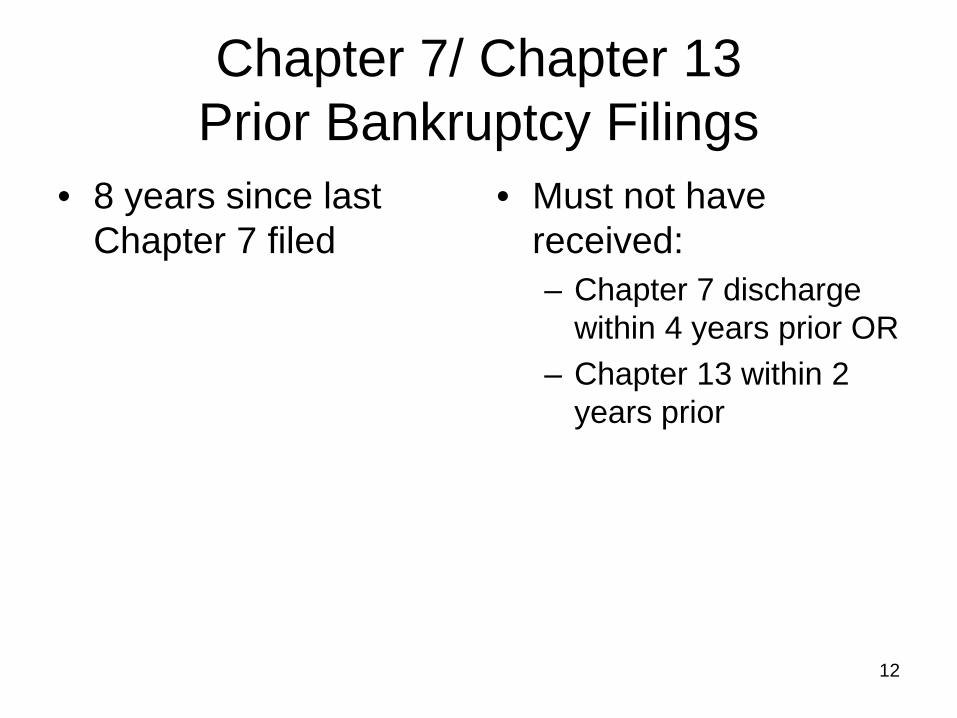

Chapter 7/ Chapter 13 Prior Bankruptcy Filings

• 8 years since last Chapter 7 filed

• Must not have received:– Chapter 7 discharge

within 4 years prior OR– Chapter 13 within 2

years prior

12

BANKRUPTCY ESTATE

• 11 U.S.C. 541– All assets owned by debtor comprise

bankruptcy estate– RSMO 513.430, RSMO 513.440, RSMO

513.475:• Property can be exempted

13

AUTOMATIC STAY• 11 U.S.C. 362

– Divorce court loses jurisdiction to divide property. • Crowley v. Crowley, 715 S.W.2d 934 (Mo.App. 1986).• Automatic Stay does not prevent:

– Establishment of Paternity– Establishment of Modification– Child Custody or Visitation– All other dissolution issues other than property

» Trial can be bifurcated

– Stay against all creditors – Only applies to filing party (not to non-filing spouse)– Relief from stay can be obtained from bankruptcy

court14

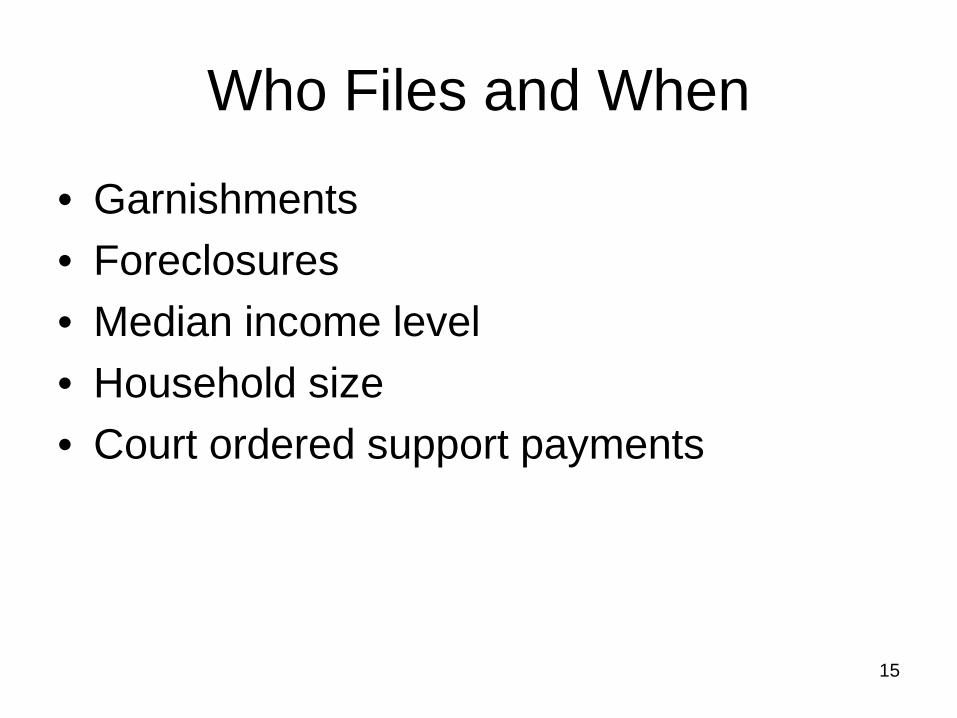

Who Files and When

• Garnishments• Foreclosures• Median income level• Household size• Court ordered support payments

15

Statement of Affairs vs.

Bankruptcy Petition• Assessing value of assets

– Bankruptcy = liquidation value– Divorce = market value– Be sensitive to the interplay between valuing assets

in bankruptcy and divorce• Bankruptcy trustee has the ability to look at

Statement of Affairs just like the divorce attorney can look at the bankruptcy petition

16

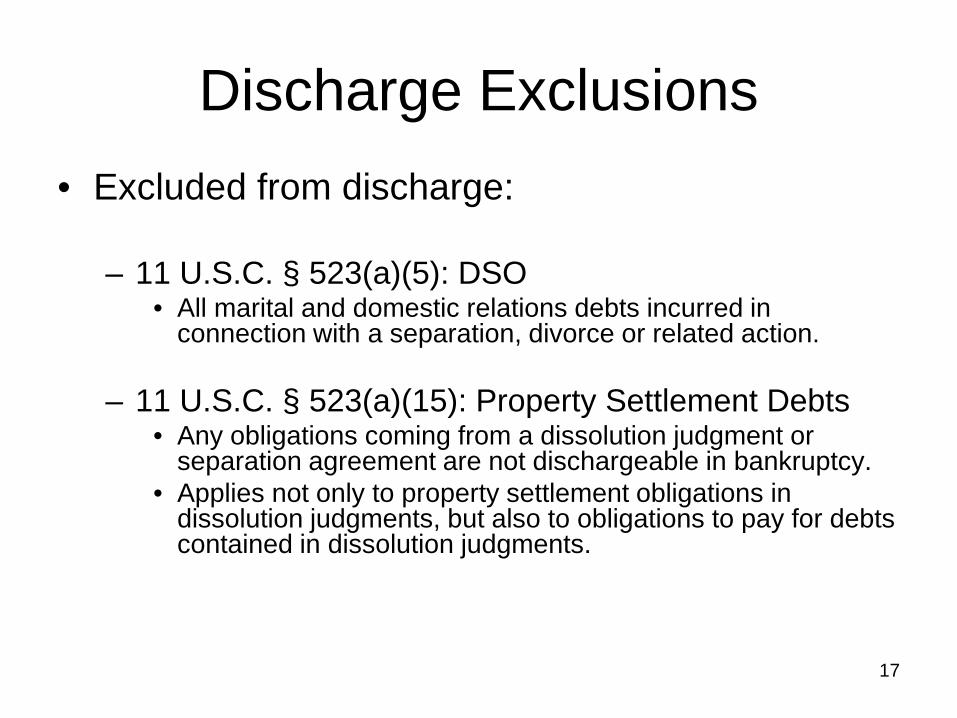

Discharge Exclusions• Excluded from discharge:

– 11 U.S.C. § 523(a)(5): DSO• All marital and domestic relations debts incurred in

connection with a separation, divorce or related action.

– 11 U.S.C. § 523(a)(15): Property Settlement Debts• Any obligations coming from a dissolution judgment or

separation agreement are not dischargeable in bankruptcy.• Applies not only to property settlement obligations in

dissolution judgments, but also to obligations to pay for debts contained in dissolution judgments.

17

DSODomestic Support Obligation is defined in Section 101(14A) of the Bankruptcy Code. Section

101(14A) provides that a DSO is:[A]debt that accrues before, on, or after the date of the order of relief in a case under this title, including interest that accrues on that debt as provided under applicable nonbankrtuptcy law notwithstanding any other provision of this title, that is

(A) owed to or recoverable by –(i) a spouse, former spouse, or child of the debtor or such child’s parent, legal

guardian, or responsible relative; or(ii) a governmental unit

(B) in the nature of alimony, maintenance, or support (including assistance provided by a governmental unit) of such spouse, former spouse, or child of the debtor or such child’s parent, without regard to whether such debt is expressly so designated;

(C) established or subject to establishment before, on, or after the date of the order for relief in a case under this title, by reason of applicable provisions of –

(i) a separation agreement, divorce decree, or property settlement agreement;(ii) an order of a court of record; or(iii) a determination made in accordance with applicable nonbankruptcy law by

a governmental unit; and(D) not assigned to a nongovernmental entity, unless that obligation is assigned voluntarily

by the spouse, former spouse, child of the debtor, or such child’s parent, legal guardian, or responsible relative for the purpose of collecting the debt. 11 U.S.C. § 101(14A).

18

Domestic Support Obligations• A debt owed to a spouse which is in the nature of

alimony, maintenance, or support and established by agreement or Court order.

• Obligation must be owed to, or recoverable by, a spouse, former spouse, or child of debtor, or child’s parent/guardian/relative, or government unit.– The definition broadens the scope of who qualifies as a

bankruptcy creditor• This language provides protection for a direct award of

attorney’s fees to an attorney representing a custody litigant

• Designation of a DSO is not binding on the bankruptcy court– Court can look behind language to determine nature of debt 19

Factors to Determine DSO/Property Settlement

Exception1) Intent of the parties or the family court at

the time the obligations were created2) Respective financial situation at the time

of the obligation3) Actual substance and language of the

agreement/order4) Function served by the obligation at the

time of the agreement

20

Negotiating and Drafting

• Has Bankruptcy been filed – Yes or No– If not, what’s the likelihood of a bankruptcy

being filed• Divide marital assets and debts• If you want an obligation to survive

bankruptcy, make sure it’s worded as a DSO

• Are Attorney Fees in the DSO?

21

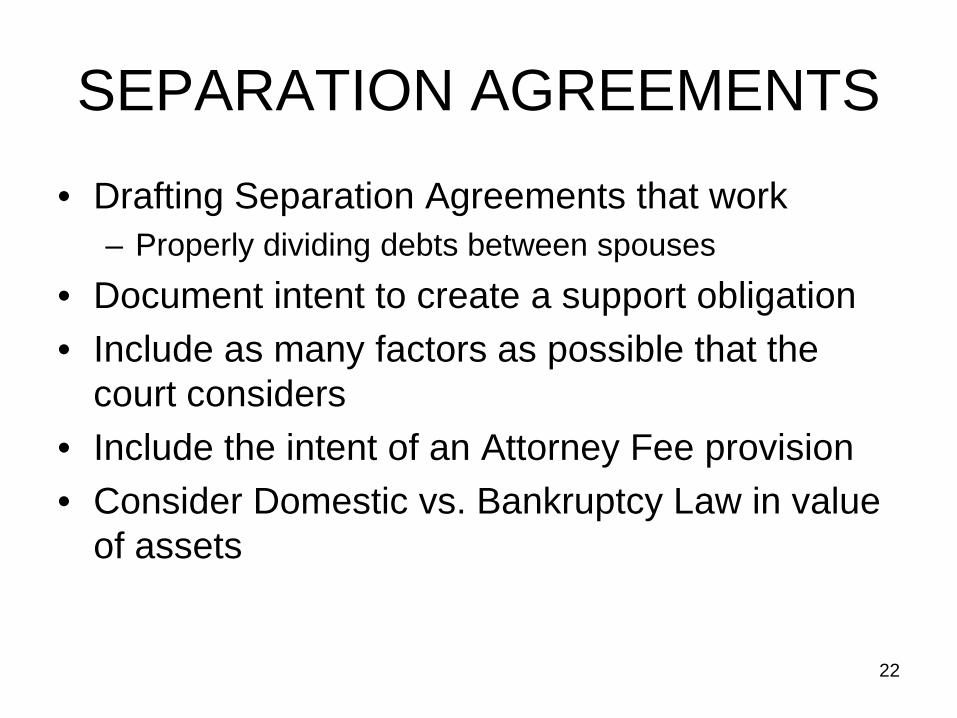

SEPARATION AGREEMENTS

• Drafting Separation Agreements that work– Properly dividing debts between spouses

• Document intent to create a support obligation• Include as many factors as possible that the

court considers• Include the intent of an Attorney Fee provision• Consider Domestic vs. Bankruptcy Law in value

of assets

22

Best Practice Strategies• Enforcement of Judgment for Attorney Fees• Effects of Wage withholdings prior to Bankruptcy• Non-Exempt assets worth fighting over? Marital exception and equity in the

house.• Executing a Judgment and the Auto-Stay.• Attorney Fees as preferential transfer or contemporaneous exchange.• Tax refund, and Dependants.• Conflict of Interests between BK Atty and DIVx Atty• Credit Card payments from a client prior to Bankruptcy• Inside transactions to family members for debts prior to filing BKY• 522 Analysis, Where did the debtor live prior to filing BKY determines what

states exemptions to use. • Timing: tax refunds, foreclosure, Judgments, DSO, Debt on Date of filing,

Assets on date of filing. • Motion for relief to PDL?

23

FORECLOSURE

• Foreclosure affects everyone– All economic brackets

• Factors contributing to foreclosure– Irresponsibility– Unemployment– Loan Modification process– Divorce

• Bankruptcy and Automatic Stay• Cash For Keys, Short Sale, Deed in Lieu

24

FORECLOSURE• During automatic stay

– Keep House or Not– Chapter 7

• Reaffirm Debt• Renegotiate• Back payments

– Chapter 13• Back Debt• Loan Modification• Junior Mortgages

• Timing– Chapter 7– Chapter 13

25

PREFERENTIAL TREATMENT

• Must disclose payments to individual creditors of $600 within 90 days prior to filing

• Only applies to Chapter 7• Retainers in Trust • Earned Fees

26

TIDBITS AND TIPS

• Ethics– Bankruptcy or Divorce First– Fee

• Separation Agreement– Tighter after bankruptcy

• Domestic Support Obligations– Non-Dischargeable

• Foreclosure27

TIDBITS AND TIPS

– Joint/Individual Bankruptcy– Financial/Property Statements

• Conflicting Statements = Perjury– Valuation in divorce vs. bankruptcy

– Why NOT to be a bankruptcy attorney (intentionally or otherwise)

• All attorneys have to certify the accuracy of their clients bankruptcy schedules and list of assets, as well as the ability to make payments, or face sanctions.

28

CONCLUSION• Ethics/Risk Avoidance

– Ethical obligation to discuss timing– Ethical obligation to discuss joint vs. individual– Can you represent a couple/individual in bankruptcy and divorce

• Economic Survival after Divorce– Separation Agreements

• Tighter after bankruptcy• Division of Debt to protect your client

– Prevent spousal revenge– The relief in divorce isn’t the same relief as in bankruptcy

• Contempt vs. Sanctions– Setting the spouses free from each other

29

REAFFIRMATION AGREEMENTS

• Written agreement between debtor and creditor to reaffirm the debt• Generally terms are the same as the original loan plus a substantial

payment of arrearages. • Generally, reaffirmation agreements are a bad idea because the

same results can be achieved simply by the debtor staying current in the payments.

Binding only when: • Agreement is enforceable under applicable non-bankruptcy law;• Agreement was filed before the discharge; and• Approved forms are used

30

Kenneth Paul Carp314-685-8928

Amy L. Gervich314-725-7901

Charles E. N. Rosene314-398-5260

31

![Spouse/Divorced Spouse Annuity - RRB1].pdf · B. Divorced Spouse - The marriage requirement for a divorced spouse annuity is met if your marriage ended by a fi nal divorce decree](https://img.dokumen.tips/doc/110x75/5f62dc9db64703484b5ef91a/spousedivorced-spouse-annuity-rrb-1pdf-b-divorced-spouse-the-marriage.jpg)