Embed Size (px)

Citation preview

Digital SignagePartner Summit

Bob O’MalleyInFocus CEOChairman CompTIA

My 45 Minutes of Fame

•What’s happening across the audio, visual and data industries that makes me believe that convergence is upon us?• How do vendors/manufacturers build

capability for the future of converged applications?• What should you be doing to prepare your

customers, your staff and your business model for the next wave of opportunity?

Digital Content Drivers* – 2010 & BeyondIP is the universal information conductorCE sets the price points, China is the manufacturerEvery display device is connected, is smart and is managed remotely Visual Collaboration Systems and Solution Elements need to be componentized to match their life cycleDelivery to mobile devices requires standardized Any2AnyContent becomes more valuable, needs to be re-purposed, communicated and shared across the enterpriseThe IT/AV channels accelerate migration to services

* Drawn from CompTIA/InfoComm Summit, July 2010

4

Managed Services Cornerstones*

MSPDemandGeneration

MSPSolution Offerings

RemoteManagement

& Hosting

MSP Financing

*Bob O’Malley at Tech Data MSP Summit, August 2007

5

Managed Services Cornerstones*

MSPDemandGeneration

MSPSolution Offerings

RemoteManagement

& Hosting

MSP Financing

*Bob O’Malley at Tech Data MSP Summit, August 2007

The Universal Utility Computing and Communications Model

6

Dimensions of Convergence?

Cost Professional Consumer

Infrastructure

Cloud

Connected

GUI

Customer

Open

Public

IP Network

Simple

IT

Closed

Private

Special purpose

Complex

AV

7

Dimensions – What Wins?

Cost Professional Consumer

Infrastructure

Cloud

Connected

GUI

Customer

Open

Public

IP Network

Simple

IT&AV

Closed

Private

Special purpose

Complex

InFocus Confidential

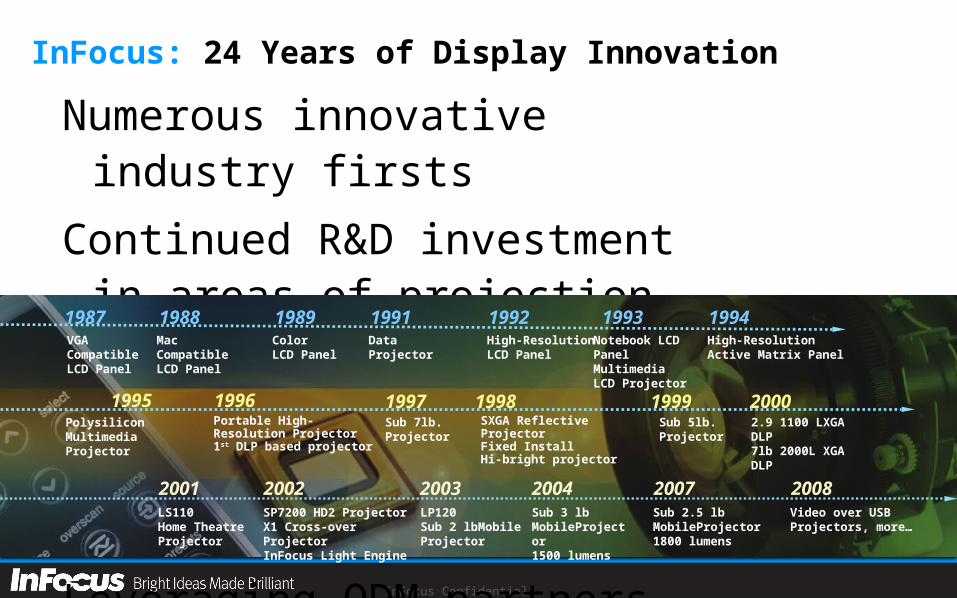

InFocus: 24 Years of Display InnovationNumerous innovative industry firsts

Continued R&D investment in areas of projection and illumination

Full range of complementary display products, software

Leveraging ODM partners for mainstream platform development

Public to Private company in May, 2009

Polysilicon Multimedia Projector

Portable High-Resolution Projector1st DLP based projector

Sub 7lb.Projector

SXGA Reflective ProjectorFixed InstallHi-bright projector

Sub 5lb. Projector

2.9 1100 LXGA DLP7lb 2000L XGA DLP

LS110Home TheatreProjector

LP120 Sub 2 lbMobileProjector

SP7200 HD2 ProjectorX1 Cross-over Projector InFocus Light Engine

Mac Compatible LCD Panel

Color LCD Panel

Data Projector High-ResolutionLCD Panel

Notebook LCD PanelMultimediaLCD Projector

High-ResolutionActive Matrix Panel

VGA Compatible LCD Panel

1987 1988 1989 1991 1992 1993 1994

2001 2002 2003

1995 1996 19981997 1999 2000

Sub 3 lbMobileProjector1500 lumens

2004 2008Video over USB Projectors, more…

Sub 2.5 lbMobileProjector1800 lumens

2007

We

InFocus Confidential

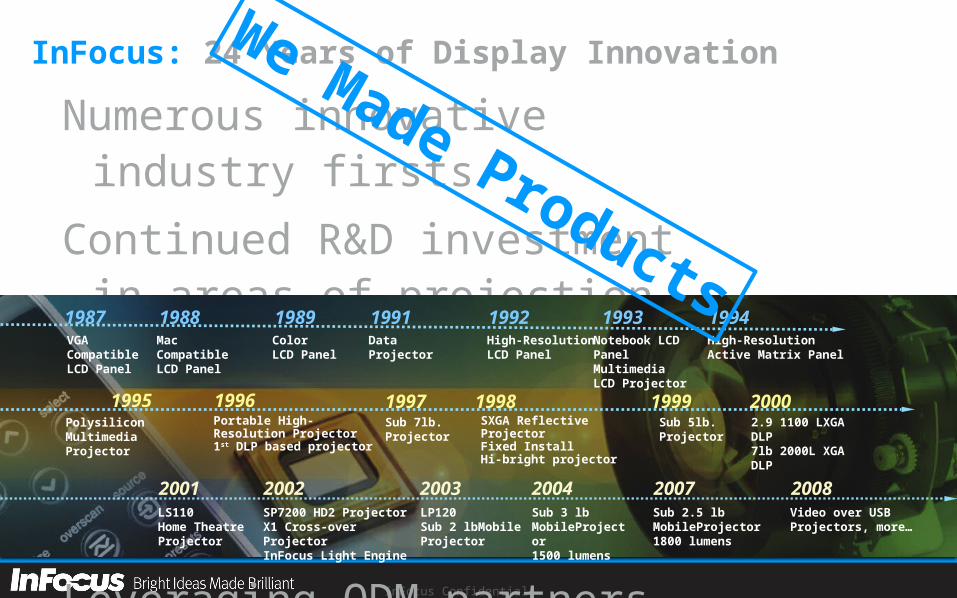

InFocus: 24 Years of Display InnovationNumerous innovative industry firsts

Continued R&D investment in areas of projection and illumination

Full range of complementary display products, software

Leveraging ODM partners for mainstream platform development

Public to Private company in May, 2009

Polysilicon Multimedia Projector

Portable High-Resolution Projector1st DLP based projector

Sub 7lb.Projector

SXGA Reflective ProjectorFixed InstallHi-bright projector

Sub 5lb. Projector

2.9 1100 LXGA DLP7lb 2000L XGA DLP

LS110Home TheatreProjector

LP120 Sub 2 lbMobileProjector

SP7200 HD2 ProjectorX1 Cross-over Projector InFocus Light Engine

Mac Compatible LCD Panel

Color LCD Panel

Data Projector High-ResolutionLCD Panel

Notebook LCD PanelMultimediaLCD Projector

High-ResolutionActive Matrix Panel

VGA Compatible LCD Panel

1987 1988 1989 1991 1992 1993 1994

2001 2002 2003

1995 1996 19981997 1999 2000

Sub 3 lbMobileProjector1500 lumens

2004 2008Video over USB Projectors, more…

Sub 2.5 lbMobileProjector1800 lumens

2007

We Made Products

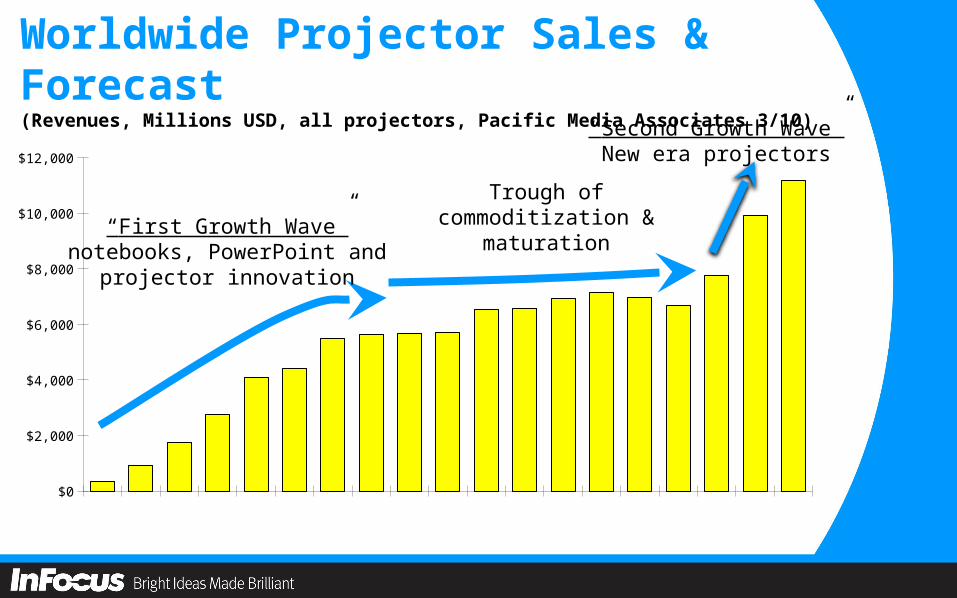

Worldwide Projector Sales & Forecast(Revenues, Millions USD, all projectors, Pacific Media Associates 3/10)

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Revenue 330 912 1763 2763 4079 4418 5508 5630 5675 5702 6523 6584 6915 7137 6982 6695 7744 9933 11186

$1,000

$3,000

$5,000

$7,000

$9,000

$11,000

“First Growth Wave”notebooks, PowerPoint and

projector innovation

“Second Growth Wave”New era projectors

Trough ofcommoditization &

maturation

Worldwide Projector Sales & Forecast(Revenues, Millions USD, all projectors, InFocus, 5/10)

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Revenue 330 912 1763 2763 4079 4418 5508 5630 5675 5702 6523 6584 6915 7137 6982 6695 6895 7102 7315

$1,000

$3,000

$5,000

$7,000

$9,000

$11,000

“First Growth Wave”notebooks, PowerPoint and

projector innovation

The Likely RealitySlow growth – 3% per year

12

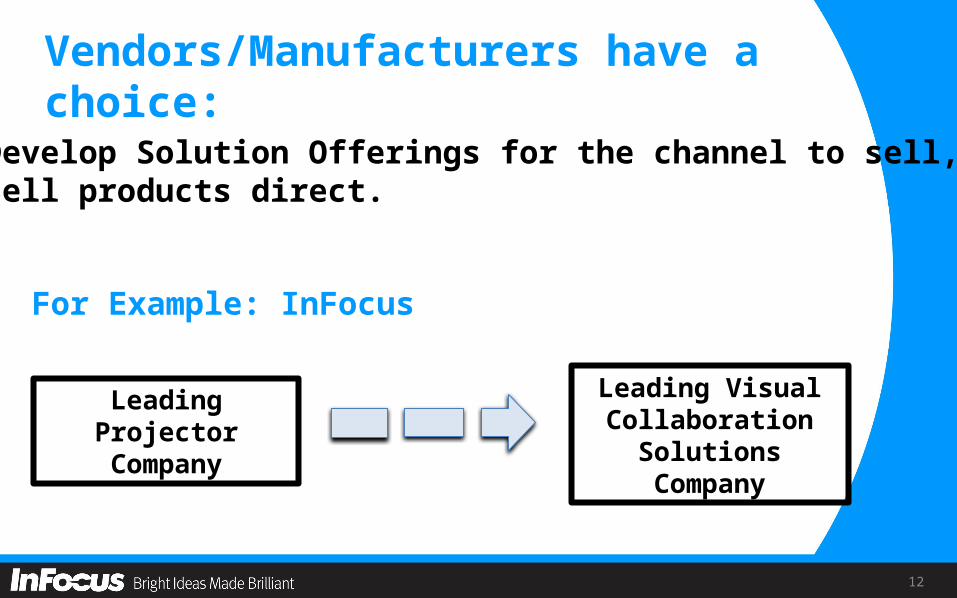

For Example: InFocus

Leading ProjectorCompany

Leading Visual Collaboration Solutions

Company

1. Develop Solution Offerings for the channel to sell, or2. Sell products direct.

Vendors/Manufacturers have a choice:

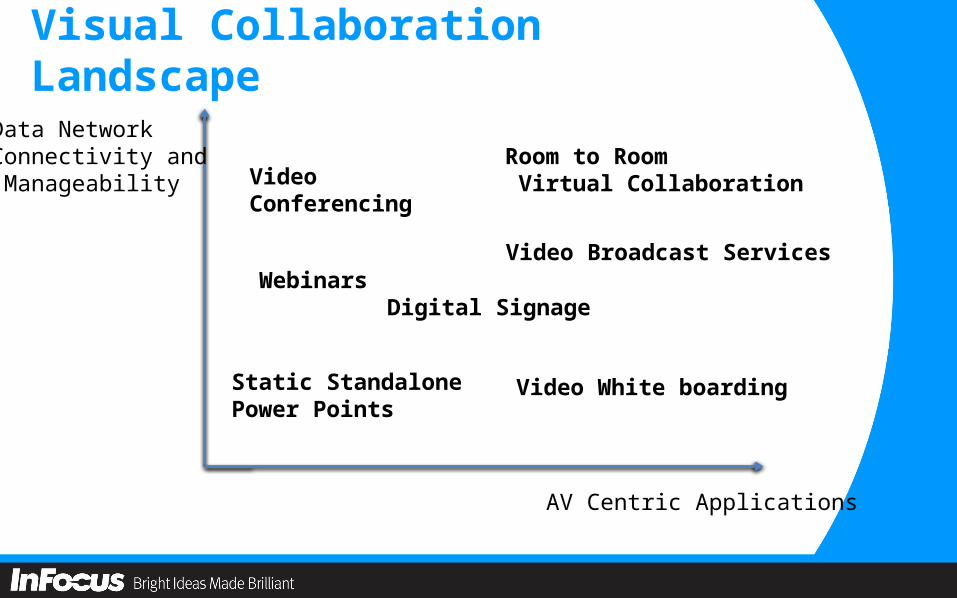

Visual Collaboration Landscape

Data NetworkConnectivity and Manageability Video

Conferencing

Webinars

Static Standalone Power Points

Room to Room Virtual Collaboration

Video Broadcast Services

Video White boarding

AV Centric Applications

Digital Signage

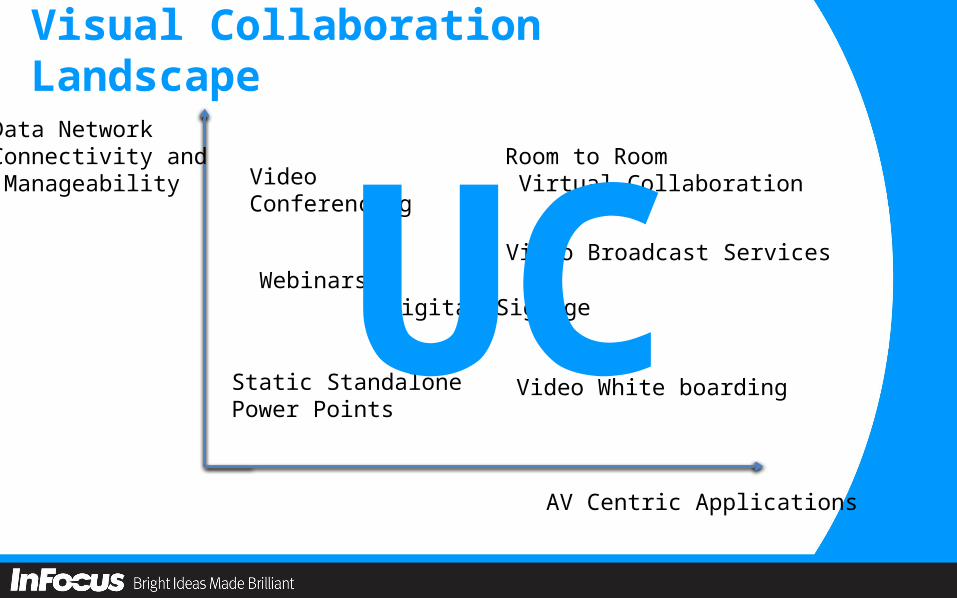

Visual Collaboration Landscape

Data NetworkConnectivity and Manageability Video

Conferencing

Webinars

Static Standalone Power Points

Room to Room Virtual Collaboration

Video Broadcast Services

Video White boarding

AV Centric Applications

Digital SignageUC

15

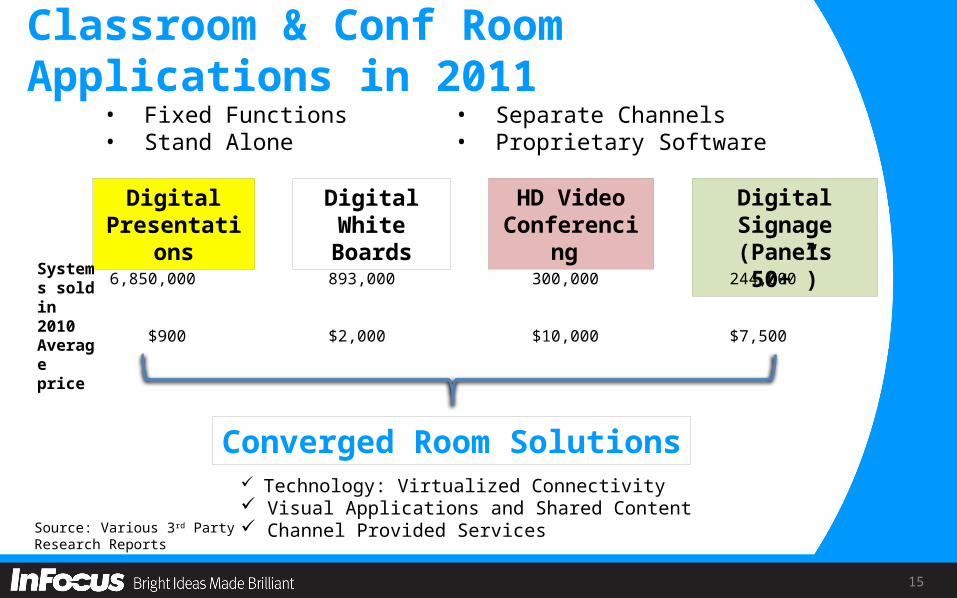

Classroom & Conf Room Applications in 2011• Fixed Functions• Stand Alone

• Separate Channels• Proprietary Software

Digital Presentations

Digital White Boards

HD Video Conferencing

Digital Signage (Panels 50+”)

Systems sold in 2010Average price

6,850,000

$900

893,000

$2,000

300,000

$10,000

244,000

$7,500

Converged Room Solutions Technology: Virtualized Connectivity Visual Applications and Shared Content Channel Provided ServicesSource: Various 3rd Party Research Reports

16

Who Will Win In The UC Battle?

Who? Strength ?

The Network

The Workstation

The Personal User

The Cloud

17

Who Will Win In The UC Battle?

Cisco, Microsoft, Apple, Google…

or YOU?

18

Who Will Win In The UC Battle?

YOU, because:

•You are the last mile•You know your customers’ business•Your customers trust you as a solution provider and want a local throat to choke•UC comes together at the customer. It is Customer in, not supplier out.

If you want to, if you prepare for it, if you start now, and if you are willing to take some risk.

19

In my humble opinion, what you need to do is:

1. Know Your Customers and their needs, much better and broader. It is more important than knowing the latest technology.

2. Verticalize on your Customers, and horizontalize on technologies.

3. Embrace Customers with leading technology appetites. They are the initiators of change.

4. Acquire or partner for the skills you need, but do not have.