Embed Size (px)

Citation preview

DES MOINES DISTRICT DENTAL SOCIETY

FALL MEETING

October 17, 2014

BrownWinick Law Firm

666 Grand Avenue, Suite 2000

Des Moines, IA 50309-2510

Telephone: 515-242-2400

Facsimile: 515-283-0231

WWW.BROWNWINICK.COM

HIPAA FOR THE

DENTAL PRACTICE

Catherine C. Cownie

Adam J. Freed

BrownWinick

666 Grand Avenue, Suite 2000

Des Moines, IA 50309-2510

Telephone: 515-242-2490

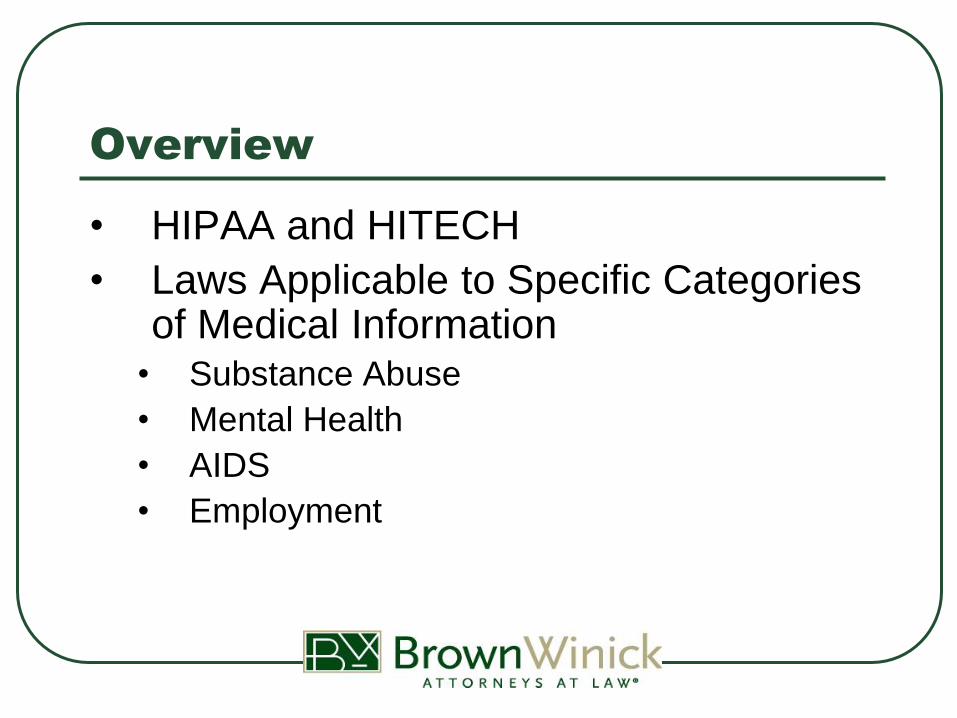

Overview

• HIPAA and HITECH

• Laws Applicable to Specific Categories of Medical Information

• Substance Abuse

• Mental Health

• AIDS

• Employment

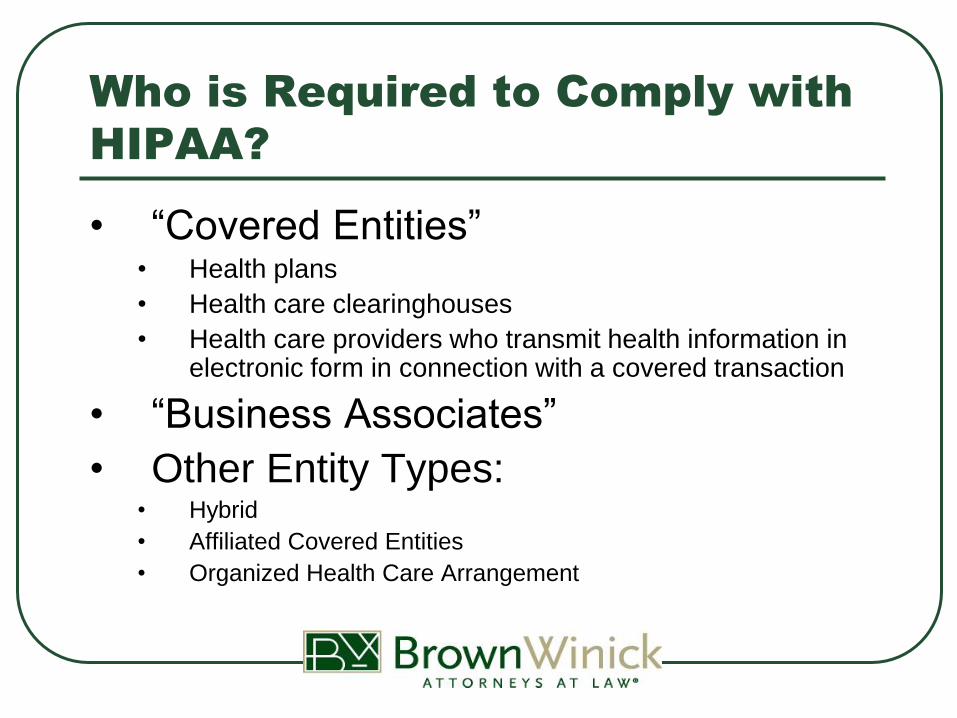

Who is Required to Comply with

HIPAA?

• “Covered Entities” • Health plans

• Health care clearinghouses

• Health care providers who transmit health information in electronic form in connection with a covered transaction

• “Business Associates”

• Other Entity Types: • Hybrid

• Affiliated Covered Entities

• Organized Health Care Arrangement

Who is a “Business Associate”?

A “business associate” is a person who:

1. “On behalf of [a] covered entity . . . but other than in the capacity of a member of the workforce of such covered entity . . . creates, receives, maintains, or transmits protected health information for a function or activity regulated by this subchapter, including claims processing or administration, data analysis, processing or administration, utilization review, quality assurance, patient safety activities listed at 42 CFR 3.20, billing, benefit management, practice management, and repricing; or”

2. “Provides, other than in the capacity of a member of the workforce of such covered entity, legal, actuarial, accounting, consulting, data aggregation (as defined in § 164.501 of this subchapter), management, administrative, accreditation, or financial services to or for such covered entity, or to or for an organized health care arrangement in which the covered entity participates, where the provision of the service involves the disclosure of protected health information from such covered entity or arrangement, or from another business associate of such covered entity or arrangement, to the person.”

Source: 45 C.F.R. § 160.103

A “Business Associate” includes

Subcontractors.

A “business associate” includes:

• “a subcontractor that creates, receives,

maintains, or transmits protected health

information on behalf of the business

associate.”

Source: 45 CFR § 160.103

What is “Protected Health

Information”?

“Individually identifiable health information”

that is:

• Transmitted by electronic media;

• Maintained in electronic media; or

• Transmitted or maintained in any other

form or medium.

Are Dentists Subject to HIPAA?

Health

Information Billing

Company

Are Dentists Subject to HIPAA?

Health

Information Law

Firm

Are Dentists Subject to HIPAA?

Health

Information

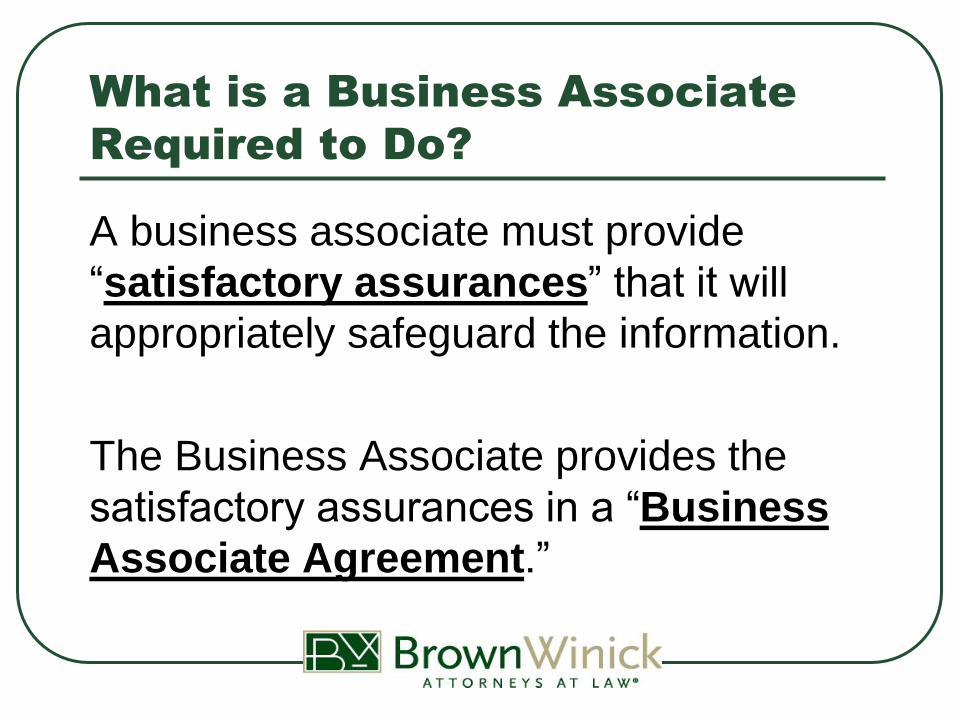

What is a Business Associate

Required to Do?

A business associate must provide

“satisfactory assurances” that it will

appropriately safeguard the information.

The Business Associate provides the

satisfactory assurances in a “Business

Associate Agreement.”

What are the Penalties for Failure to

Comply with HIPAA and HITECH?

Civil Penalties:

CE or BA did not know and by exercising reasonable diligence would not have known of the violation:

• $100 to $50,000 per violation.

• Not to exceed $1,500,000 for identical violations during a year.

Violation due to reasonable cause and not willful neglect:

• $1,000 to $50,000 per violation.

• Not to exceed $1,500,000 for identical violations during a year.

45 C.F.R. § 160.404

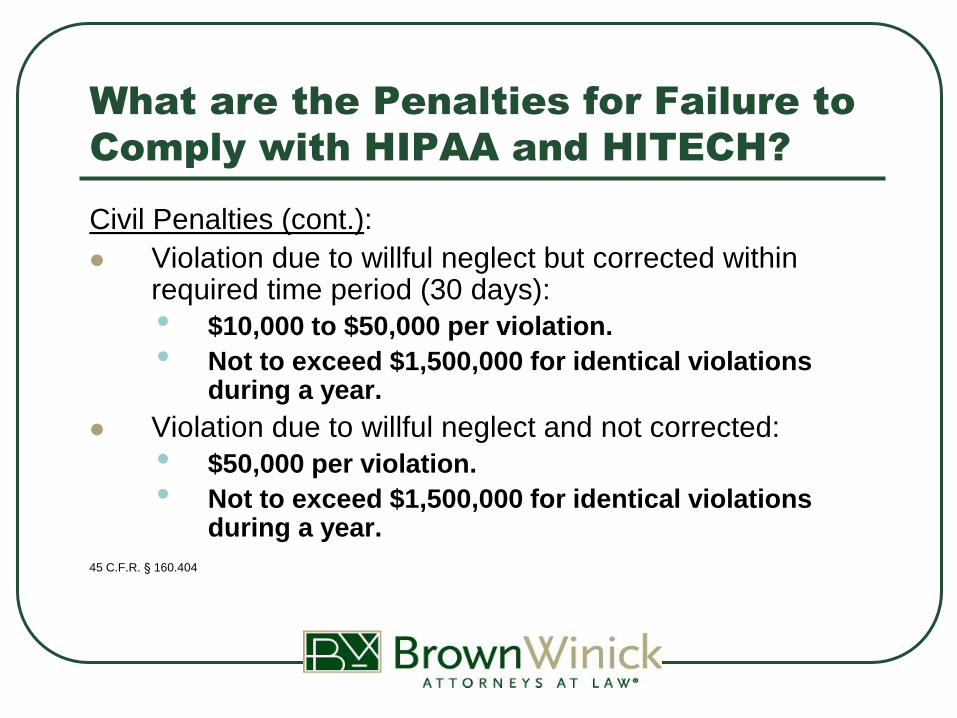

What are the Penalties for Failure to

Comply with HIPAA and HITECH?

Civil Penalties (cont.):

Violation due to willful neglect but corrected within required time period (30 days):

• $10,000 to $50,000 per violation.

• Not to exceed $1,500,000 for identical violations during a year.

Violation due to willful neglect and not corrected:

• $50,000 per violation.

• Not to exceed $1,500,000 for identical violations during a year.

45 C.F.R. § 160.404

What are the Penalties for Failure to

Comply with HIPAA and HITECH?

Criminal Penalties:

Knowingly obtain or disclose PHI in violation:

• Up to 1 year in prison

Offenses committed under false pretenses:

• Up to 5 years in prison

Offenses committed for personal gain or

malicious harm:

• Up to 10 years in prison

Famous Breaches of PHI

QUESTIONS ?

2014 Iowa Legislative

Update

Marc Beltrame

BrownWinick

666 Grand Avenue, Suite 2000

Des Moines, IA 50309-2510

Telephone: 515-242-2449 (direct)

Telephone: 515-229-9134 (cell)

Facsimile: 515-323-8549

E-mail: [email protected]

Political Considerations

Iowa Senate:

26 (Democrats) 24 (Republicans)

Iowa House:

53 (Republicans) 47 (Democrats

Governor Terry Branstad (Republican)

2014 = Election Year

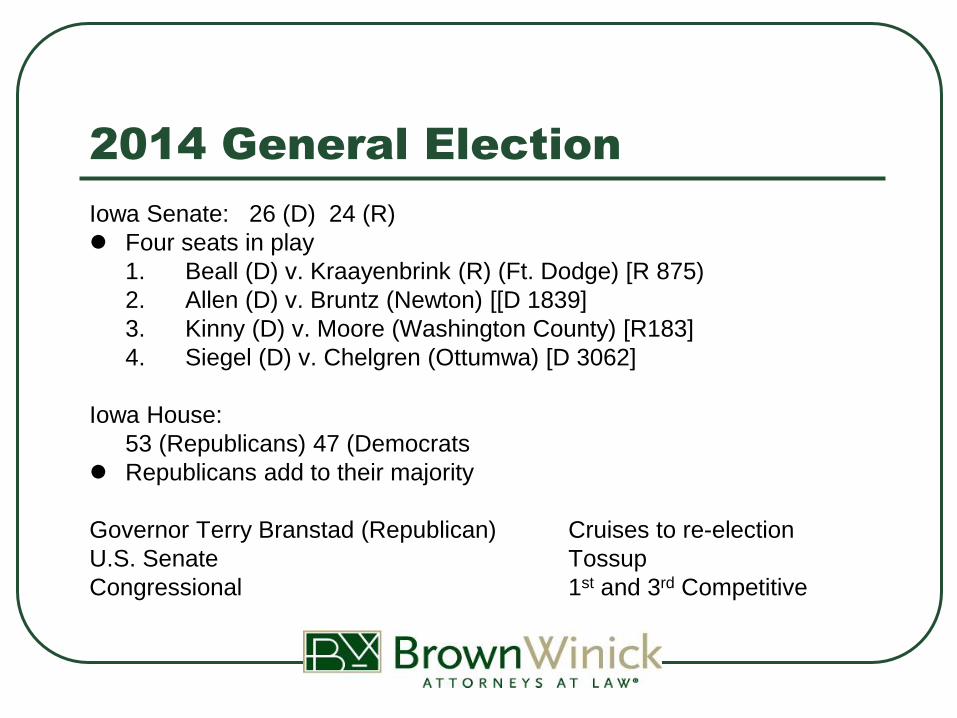

2014 General Election

Iowa Senate: 26 (D) 24 (R)

Four seats in play

1. Beall (D) v. Kraayenbrink (R) (Ft. Dodge) [R 875)

2. Allen (D) v. Bruntz (Newton) [[D 1839]

3. Kinny (D) v. Moore (Washington County) [R183]

4. Siegel (D) v. Chelgren (Ottumwa) [D 3062]

Iowa House:

53 (Republicans) 47 (Democrats

Republicans add to their majority

Governor Terry Branstad (Republican) Cruises to re-election

U.S. Senate Tossup

Congressional 1st and 3rd Competitive

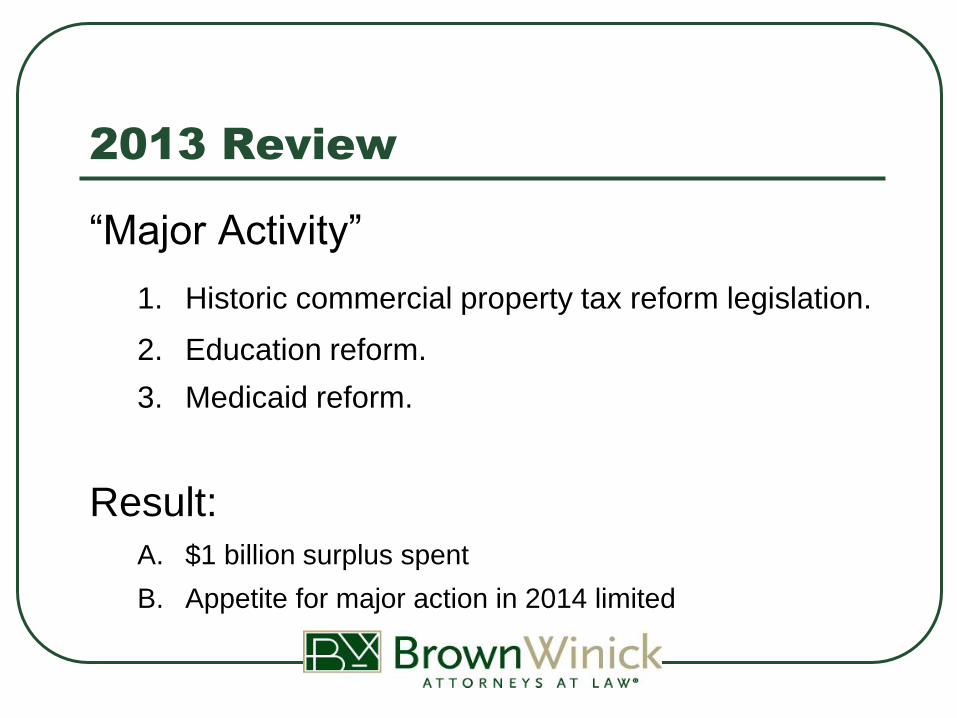

2013 Review

“Major Activity”

1. Historic commercial property tax reform legislation.

2. Education reform.

3. Medicaid reform.

Result: A. $1 billion surplus spent

B. Appetite for major action in 2014 limited

2014 Overview

Major Accomplishments of Session

Major Disappointments

Tax

Litigation

Agriculture/Environmental

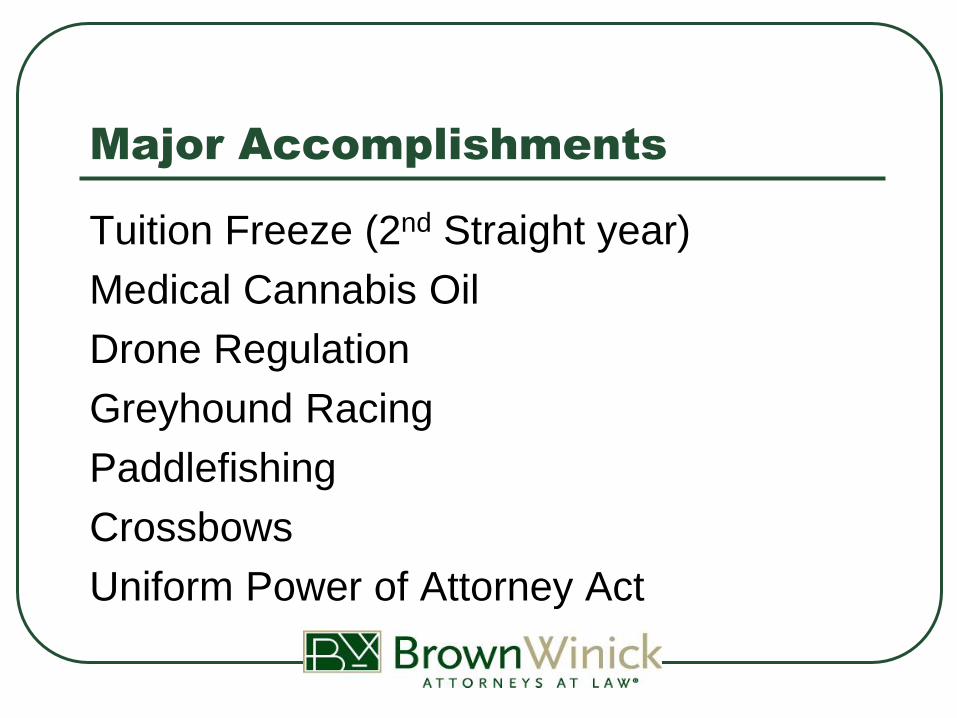

Major Accomplishments

Tuition Freeze (2nd Straight year)

Medical Cannabis Oil

Drone Regulation

Greyhound Racing

Paddlefishing

Crossbows

Uniform Power of Attorney Act

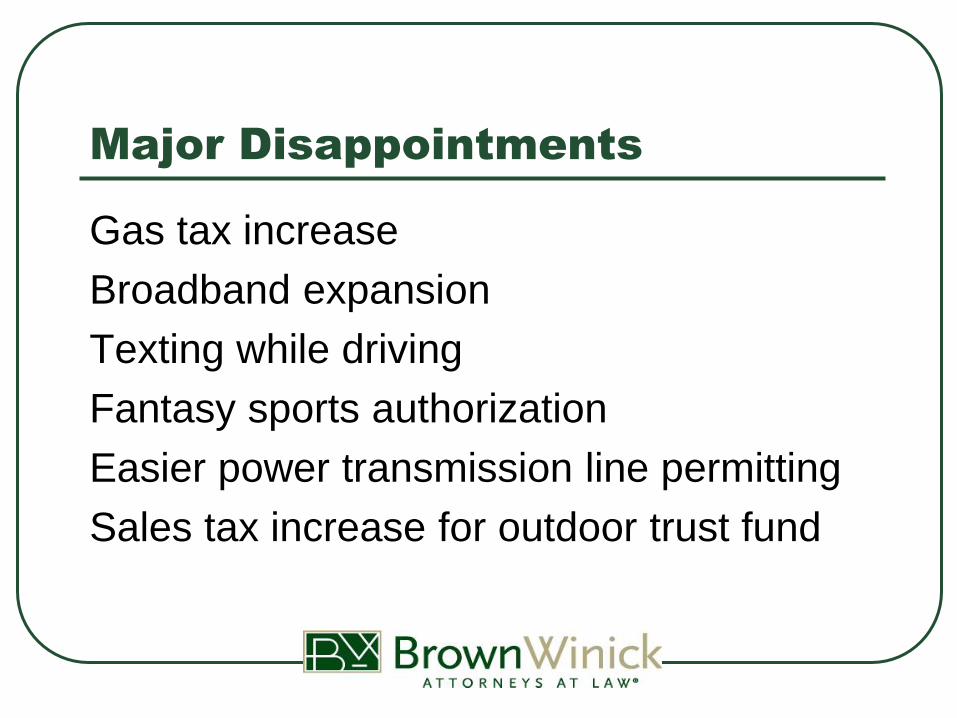

Major Disappointments

Gas tax increase

Broadband expansion

Texting while driving

Fantasy sports authorization

Easier power transmission line permitting

Sales tax increase for outdoor trust fund

Tax

Military Veterans (SF 303)

1. Exempts military pensions from state income tax

(surviving spouses included in exemption)

2. Part of “Home Base Iowa” proposal to recruit

veterans from others states to Iowa.

3. Passed.

Litigation

Wage Payment Collection Act (SF 2295) 1. Makes violations strict liability (removes intent

requirement).

2. Expands retaliatory action to persons other than employees (so-called “whistleblower”).

3. Creates a rebuttable presumption that employer did not pay required minimum wage if records are not kept property by employer.

4. Passed Senate but did not become law.

QUESTIONS ?

Real Estate Matters for

Dental Practices

Kelly Hamborg

BrownWinick

666 Grand Avenue, Suite 2000

Des Moines, IA 50309

Telephone: 515-242-2447

E-mail: [email protected]

QUESTIONS ?

Common Structures for

Selling a Dental Practice

Drew D. Larson

BrownWinick

666 Grand Avenue, Suite 2000

Des Moines, IA 50309-2510

Telephone: 515-242-2485

E-mail: [email protected]

Selling a Practice

All dental practices are going to

transition at some point.

Hopefully the owner is able to get some

value out of it through a sale.

Usually through sale to a younger

dentist/employee or to a competitor.

Common Goals

Clarity regarding ongoing duties and

obligations.

Reaching a deal that meets each party’s

needs and expectations.

Managing tax issues and risks.

Maintaining continuing business

operations during transition.

Goals - Seller

Get the best price for the business.

Minimize ongoing obligations and

liabilities.

Maximize up front cash.

Goals - Buyer

Get the best price for the business.

Ensure you know what you are getting

into.

Ensure you have a remedy if the seller

breached the agreement.

Due Diligence

Begins pre-agreement, opportunity for

Buyer to research Seller.

Process to overcome information

asymmetry. Seller knows its own

business better than Buyer.

Covers everything.

Due Diligence – Seller Prep

Be ready to disclose the key items.

• Financials

• Assets and Real Estate

• Corporate Documentation

• Tax Information

• Litigation

• Employee Matters

• Regulatory/Payer Compliance

Due Diligence – Seller Prep

If a Seller does not have clean records

and good information, it increases the

Buyer’s risk.

Buyers (and their financing sources)

abhor risk.

Poor documentation and financial

information can easily sink a deal or

substantially lower the price.

Advantages to Selling Dental

Practice

Buyer already knows how business

works.

If Buyer an employee, already knows the

business.

Financing generally available.

Two Basic Structures

Asset Purchase

Stock Purchase

Asset Purchase

Generally preferred by Buyers.

Best limits successor liability.

Provides a stepped up basis.

Requires depreciation recapture for

Seller, if applicable.

Generally ordinary income up to amount

of depreciation recapture, then capital

gains.

Stock Purchase

Generally preferred by Sellers.

Can be simpler, no transfer of contracts,

etc. (may have notice requirements).

No step up in basis for Buyer.

Generally all capital gains in excess of

basis.

Financing

Cash

Bank

Seller Financing

Combination

Indemnification and Remedies

Survival – Protection and Certainty

Indemnification

Defense of Claims

Baskets, Caps

Setoff

Exclusivity of Remedies?

Other Issues

Employment Agreement

Non-Compete Obligations

Confidentiality

Earn Out

Transition Assistance

QUESTIONS ?

Estate Planning: A Basis

Check-Up

Robert D. Hodges

BrownWinick

666 Grand Avenue, Suite 2000

Des Moines, IA 50309-2510

Telephone: 515-242-2465

Facsimile: 515-343-8465

E-mail: [email protected]

Disclaimer

IRS Circular 230 Notice: To ensure compliance with requirements imposed by

the IRS, we inform you that, except to the extent expressly provided to the

contrary, any federal tax advice contained in this communication is not intended

or written to be used, and cannot be used, for the purpose of (i) avoiding

penalties under the Internal Revenue Code or (ii) promoting, marketing, or

recommending to another party any transaction or matter addressed herein.

Please consult your tax advisor for advice specific to your individual situation.

This presentation should be considered general in nature and not specific legal

advice. No attorney-client relationship is intended or implied.

“BIG PICTURE” ENVIRONMENT

$5,340,000 for unified credit 2014

Increased rate to 40%

“Portability” permanent

GST mirrors unified credit

Annual exclusion gifting still viable

“CHOPPING BLOCK” ITEMS

$5,340,000 for unified credit

Minority/Marketability Discounts

“File and suspend” for Social Security

“Rolling GRATs”

NON-TAXABLE ESTATES

Income tax efficiency may drive decisions

Portability return part of standard practice

Planning for non-involved children

Right of first refusals

COMMON MISTAKES

Incorrect beneficiary designations

No powers of attorney

Reluctance to use trusts

No periodic “check ups”

BENEFICIARY PROBLEMS

The will NOT “figure it out”

“Fair” vs. Equal

Fix a valuation formula in the plan

Be explicit regarding property distribution

Fiduciary designations

PROBATE AVOIDANCE

Pitfalls of probate

• Public, Slow, and Expensive

• Not a catastrophic result

“All or nothing” approach

Non-attorney involvement

QUESTIONS ?

AVOIDING FRAUD AND

ABUSE PITFALLS

BRADLEY R. KRUSE

BrownWinick

666 Grand Avenue, Suite 2000

Des Moines, IA 50309-2510

Telephone: 515-242-2460

Facsimile: 515-323-8560

E-mail: [email protected]

INTRODUCTION AND OVERVIEW

Identification and avoidance of

fraudulent and abusive practices

RAC audits

Responding to insurance companies and

governmental agencies

IDENTIFICATION AND

AVOIDANCE OF FRAUDULENT

AND ABUSIVE PRACTICES

Introduction • The National Health Care Anti-Fraud Association

(NHCAA) estimates that between 3 and 10 percent of

the nation’s annual benefits paid for health care were

paid for fraudulent or abusive submissions.

• Estimations by fraud analysts indicate that there is a

greater percentage of fraud in dentistry than there is in

medicine.

• The result is potentially more scrutiny on dentistry.

Dental Fraud Defined

Dental Fraud is any act of intentional

deception or misrepresentation of

treatment facts made for the purpose of

gaining unauthorized benefits.

Acts of dental fraud contain 3 defining

features, namely intent, deception and

unlawful gain.

Types and Examples of

Fraudulent and Abusive Practices

Billing for Services Not Performed

• Avoiding this problem is basically self-explanatory.

• Certain situations can be more complicated.

• E.g., billing for a crown at the prep date rather than the

cementation date; question arises when the service was

actually performed. Many dentists send in for payment for

crowns at the prep time, but many insurance carriers consider

the crown completed only after it is cemented.

• Important to check benefits manual.

• Honest disclosure of the situation is best practice for avoiding

any problems with the carrier.

Types and Examples of

Fraudulent and Abusive Practices

Upcoding

• Upcoding occurs when a coding procedure with a

more extensive degree of difficulty is used than what

was actually performed.

• E.g., the provider renders a standard prophylaxis

(01110) but the insurance carrier is billed for a

periodontal scaling and root planing (04341).

Types and Examples of

Fraudulent and Abusive Practices

Waiver of Co-Payments

• Co-payments considered essential element of

cost structure of contract between the insured

and the insurance carrier.

• Waiving co-payments arguably encourages

more usage of the coverage than would

normally occur, distorting the cost structure of

the insurance.

Types and Examples of

Fraudulent and Abusive Practices

Waiver of Deductibles

• As with co-payments, deductibles considered

an essential element of an insurance carrier’s

cost structure.

• Waiver of deductibles arguably encourages

more usage of coverage, potentially distorting

cost structure.

Types and Examples of

Fraudulent and Abusive Practices

Altering Dates of Service

• The date a procedure is performed is

important, as it relates to patient eligibility

requirements and waiting periods.

• It is fraudulent to send a claim for treatment

using a date other than the actual date of

service.

Types and Examples of

Fraudulent and Abusive Practices

Unbundling or Improper Use of Codes • The American Dental Association defines unbundling

as “the separating of a dental procedure into

component parts with each part having a charge, so

that the cumulative charge for the components is

greater than the total charge to patients who are not

beneficiaries of a dental benefit plan for the same

procedure.”

• It is considered fraudulent to use several codes, i.e.,

unbundling, to describe a service where one code is

sufficient.

Types and Examples of

Fraudulent and Abusive Practices

Unbundling or Improper Use of Codes • Example: Dentist performs a 1-surface occlusal amalgam

and sends in separate claims for local anesthesia (09210),

office visit (09430), amalgam-1 surface (02140) and pulp

cap indirect (03120); instead, coding the matter as

amalgam-1 surface (02140) is sufficient.

• Another example occurs when dentist charges not just for an

extraction, but also separately for elevating the flap, curetting

out the periapical tissue, incision, and drainage that were in

connection with the extraction, as well as charging for

suturing the socket. Such procedures are all part of the

global fee for extraction of a tooth and should not be billed

separately.

Types and Examples of

Fraudulent and Abusive Practices

Misrepresenting Patient Identities

• Self-explanatory: Performing on one patient

but sending in a claim for a different person is

fraud.

Types and Examples of

Fraudulent and Abusive Practices

Not Disclosing Existence of Additional

Primary Coverage

• Patients covered by more than one dental

plan may receive benefits from all plans.

• Sending in multiple claims to different carriers

as if they were each the primary carrier is

considered fraudulent.

Types and Examples of

Fraudulent and Abusive Practices

Performing Unnecessary Services

• Performing and billing for services that were

not needed or providing additional services or

procedures beyond what is required by the

patient’s condition is considered fraudulent.

Types and Examples of

Fraudulent and Abusive Practices

Misrepresentation of Services

• Involves changing the code to increase the

amount of the claim.

• Example: A provider that performs a routine

dental extraction but used the procedure code

for impacted teeth.

Types and Examples of

Fraudulent and Abusive Practices

Unlicensed Employees

• Use of hygienists, assistants or other staff to

perform treatments if such persons are not

licensed or qualified and then billing the

procedure as if performed by the dentist.

RAC Audits

Introduction

• The Recovery Audit Contractor (RAC)

Program was created through the Medicare

Modernization Act of 2003 to identify and

recovery improper Medicare payments made

to health care providers under fee-for-service

Medicare plans.

RAC Audits

• The mission of the Recovery Audit Program is

to identify and correct Medicare improper

payments and collect overpayments made on

health care services provided to Medicare

beneficiaries, so that the CMS can implement

actions that will prevent future improper

payments in all 50 states.

RAC Audits

• Detection and collection of overpayments is

made through RAC audits conducted by RAC

vendors (in Iowa, Optum Public Sector

Solutions, Inc.)

• RAC audit contractors paid contingency fee

based on amounts they identify and recover.

• Iowa uses a tiered contingency fee

percentage structure.

RAC Audits

• RAC audits can be very burdensome on

practitioners.

• Nebraska example

• Roughly 1000 claims all representing $22 fees for

periodic routine dental cleanings were erroneously

reviewed.

• Administrative burden required the assignment of

one dental hygienist for a full week in order to pull

all the records related to the claims being

reviewed.

RAC Audits

RAC Audit Facts • Very small percentage of claims that have been

collected have been challenged and overturned

on appeal.

• RAC auditors may not create their own policies

but are bound by CMS regulations, National

Coverage Determinations (NCDs).

• Recovery auditors required to comply with

Reopening Regulations located at 42 CFR

405.980.

RAC Audits

RAC Audit Facts • Recovery auditors required to comply with

Reopening Regulations located at 42 CFR

405.980.

• Before recovery auditor makes a decision to

reopen a claim, the recovery auditor must have

good cause and must clearly articulate the good

cause in correspondence with providers.

RAC Audits

RAC Audit Facts • CMS has limited lookback period for recovery auditor

reviews limited to a maximum of 3 years.

• CMS has limited the number of additional

documentation requests that a recovery auditor may

request at one time.

• Recovery auditors required to give provider a detailed

rationale of improper payment determination and are

required to issue detailed review results and letters to

providers.

Tips on Avoiding Fraud and

Abuse Pitfalls

Be aware of and guard against committing

the examples and types of fraud noted

above.

Work with and monitor staff:

• Practitioner may not be aware of staff member who is

improperly coding.

Be aware of incentivizing staff to use higher

codes to increase incentive compensation.

Tips on Avoiding Fraud and

Abuse Pitfalls

Be wary for what is represented at trade

conferences and by medical device

salespeople as to coding coverage.

Heed warnings and educational

correspondence from auditors.

• Once educated or warned regarding a billing

problem, future issues go from waste and abuse to

fraud because there is now intent.

Tips on Avoiding Fraud and

Abuse Pitfalls

Avoid billing red flags

• Overutilization of a particular code or codes – most

practices typically should show a broad mix of

codes.

• Consistently providing all or most patients with the

same or similar treatment.

• Consistently billing the highest level of codes.

Responding to Inquiries and

Audits

Responding to inquiries is key – ignoring

inquiries makes matters worse.

Cooperation and communication.

When to lawyer up.

QUESTIONS ?

The ACA – aka “Obamacare”

What You Need to Know Now

Alice Helle

BrownWinick

666 Grand Avenue, Suite 2000

Des Moines, IA 50309-2510

Telephone: 515-242-2407

Facsimile: 515-323-8507

E-mail: [email protected]

INDIVIDUAL MANDATE

Individuals required to have health

coverage or pay a penalty

2014 – greater of $95 or 1% of household

income

2015 – greater of $325 or 2% of income

2016 on - greater of $695 or 2.5% of income

INDIVIDUAL MANDATE (CONT.)

Qualified Coverage Employer-sponsored group health plan

Grandfathered health plan

Certain government coverage

Ex: Medicare, Medicaid, CHIP, Tricare, VA

Health plans offered in the individual market

Other coverage recognized by HHS and Treasury

Catastrophic coverage if under age 30 or other

exemption

Coverage purchased through Exchange

(“Marketplace”) operating in the state

WHAT IS THE EXCHANGE?

Two Types American Health Benefit Exchange for individuals

and families

Small Business Health Options Program (“SHOP”)

for small (under 50) businesses

A state may elect to combine both into one

exchange

ESSENTIAL BENEFITS

Ambulatory patient services

Emergency services

Hospitalization

Maternity and newborn care

Mental health and substance use disorder services, including behavioral health treatment

Prescription drugs

Rehabilitative and habilitative services and devices

Laboratory services

Preventive and wellness services and chronic disease management

Pediatric services, including oral and vision care

COVERAGE LEVELS

Bronze (60/40)

Silver (70/10)

Gold (80/20)

Platinum (90/10)

SUBSIDIES

Potential subsidies for coverage purchased from Exchange

Premium assistance tax credits for individuals with income between 100% and 400% of the federal poverty level

FPL for family of 4 for 2013 is $23,550

400% = $94,200

Cost-sharing subsidies for individuals with income up to 250% of the federal poverty level to reduce out-of-pocket costs for plans purchased through an Exchange

Not available if individual has affordable coverage available from employer that provides minimum value

EXCHANGE NOTICE

NOTICE TO EMPLOYEES OF COVERAGE OPTIONS

Notifies employees of coverage options available through state insurance exchange

Two model notices are provided on the DOL website – one for employers who provide coverage and one for employers who don’t.

A revised COBRA notice incorporating information about the exchange is also on the website

Deadline was October 1, 2013

DOL clarified that the general $100/day penalty for noncompliance is not applicable to the exchange notice provision

PEDIATRIC DENTAL INSURANCE

Inside Exchange - Iowa

Health insurance policies not required to

include pediatric dental coverage

Instead, “stand-alone” dental plans are

offered in the Exchange

Delta Dental

BESTOne

PEDIATRIC DENTAL INSURANCE

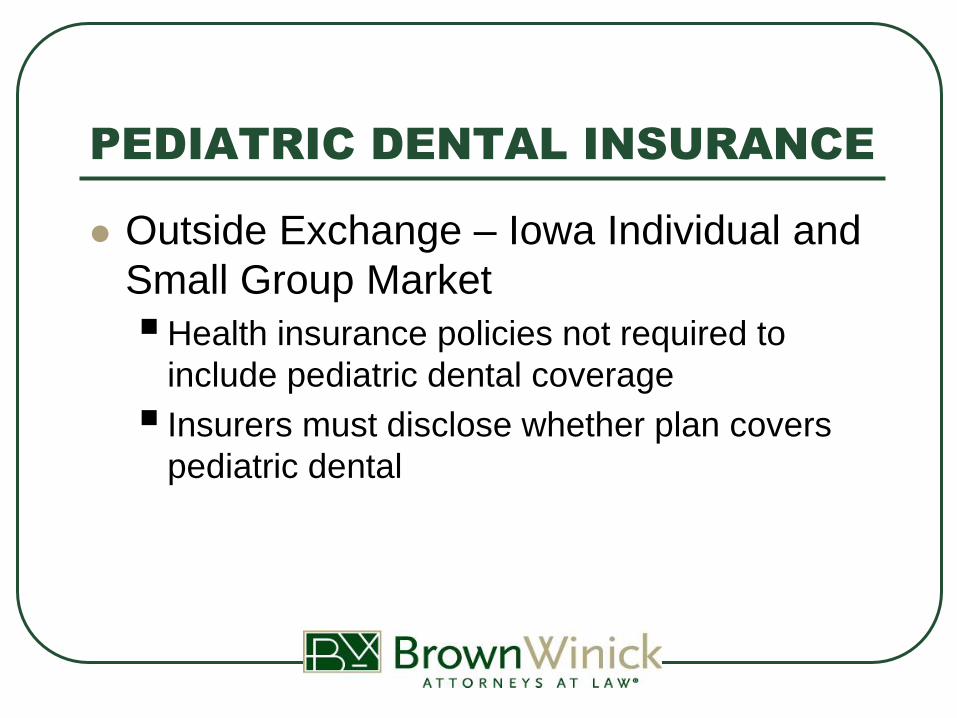

Outside Exchange – Iowa Individual and

Small Group Market

Health insurance policies not required to

include pediatric dental coverage

Insurers must disclose whether plan covers

pediatric dental

PEDIATRIC DENTAL INSURANCE

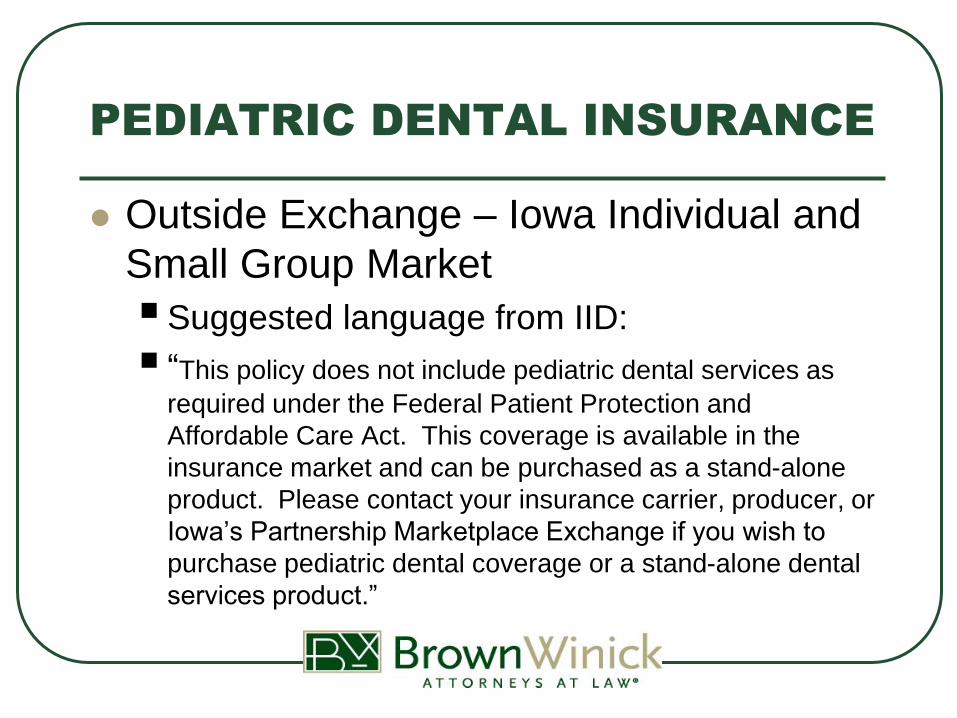

Outside Exchange – Iowa Individual and

Small Group Market

Suggested language from IID:

“This policy does not include pediatric dental services as

required under the Federal Patient Protection and

Affordable Care Act. This coverage is available in the

insurance market and can be purchased as a stand-alone

product. Please contact your insurance carrier, producer, or

Iowa’s Partnership Marketplace Exchange if you wish to

purchase pediatric dental coverage or a stand-alone dental

services product.”

EMPLOYER MANDATE

No requirement for small (under 50)

employer to provide health coverage

Large (50+) employers will be required

to provide coverage or pay a penalty

Delayed to 2015

Delayed to 2016 for employers of 50 - 100

2014 will be the measuring period for

determining “large employer” status

QUESTIONS ?

Uncle Sam “Needs” More Cash – Recent

Tax Law Changes Affecting You and Your

Business

Christopher L. Nuss

666 Grand Ave, Suite 2000

Des Moines, IA 50309-2510

Telephone: 515-242-2432

E-mail: [email protected]

Example of Federal Tax Increase

from 2012 to 2013 (and

continuing into 2014)

Assumptions: Married filing jointly (w/o

dependents) with mixture of salary ($65K),

investment income ($90K), pass-through

income from S corporations or LLCs ($400K),

and pension/social security ($200K), and

various itemized deductions and exemptions.

For illustrative purposes only.

Example of Federal Tax Increase

from 2012 to 2013/2014 (cont.)

2012 2013/2014 Increase

AGI (before

deductions)

$825,000 $825,000 ___

Taxable Income 768,000 792,000 $24,000

Income Tax 219,000 243,000 24,000

FICA/Medicare

on W-2

3,700 5,000 1,300

3.8% Medicare

on NII

___ 3,500 3,500

Total Taxes $222,700 $251,500 $28,800

(or 12-13%)

Why Increase in Taxes from

2012 to 2013/2014?

• Earlier phaseout of itemized deductions &

loss of exemptions.

• Increase of top tax rate on dividends &

capital gain.

• Increase in top tax rate on ordinary income.

• Increase in FICA & Medicare on earnings.

• New 3.8% Medicare on net investment

income.

Planning Points Going Forward

• Estimated tax payments & wage withholding even more important (to avoid large tax bill in April and underpayment penalty).

• Defer recognition of income and gain, while accelerating deductions.

• Section 179 expense & bonus depreciation (but see below)

• Equity interests in LLCs/partnerships

• Other basic deferral mechanisms

• “Active” participation in S corporation – NII tax and employment taxes.

Planning Points Going Forward

• Gifts & distributions from trusts to family

members or other taxpayers in lower tax

brackets.

• Revise mix of investment assets.

• Dependency exemption on children in

college.

• Consider change in business entity form.

Other Tax Planning

Considerations

• Beware of multi-state operations, especially

for pass-through entities – Compliance!!

• Personal goodwill for C corporation

shareholders.

• New Iowa business property tax exemption – http://www.brownwinick.com/news-blogs/legal-news/state-of-iowa-

property-tax-reform.aspx

What Is Upcoming? Possible

Future Changes

• Keep eye on Congress through end of year,

many key provisions set to expire –

“extenders” bill.

• No cash basis of accounting for service

businesses with gross receipts exceeding

$10M.

• Any questions?

QUESTIONS ?

SOCIAL MEDIA IN

THE WORKPLACE

Haley R. Van Loon

BrownWinick

666 Grand Avenue, Suite 2000

Des Moines, IA 50309-2510

Telephone: 515-248-6625

Facsimile: 515-248-6626

E-mail: [email protected]

Social Media

Social Media

Social Networking Sites

Status updates

Relationship status

Online chatting capabilities

Listing favorites

• (books, movies, quotes, hobbies)

Political affiliation

Groups or networks

And the list goes on and on . . .

People like to share . . .

Real Tweets

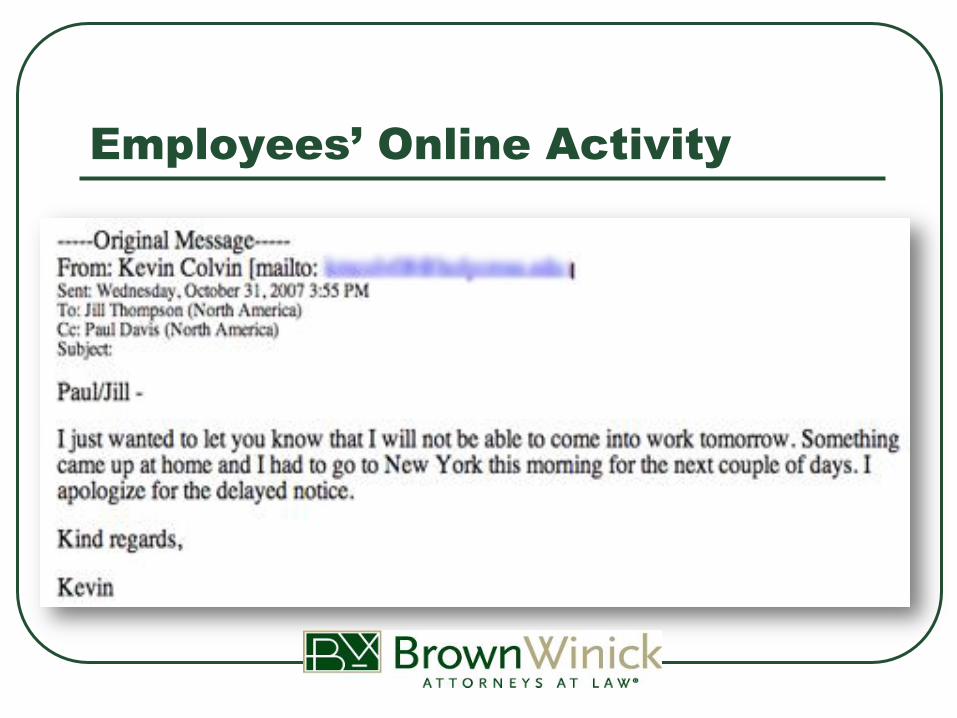

Employees’ Online Activity

Employees’ online activity may

• Harm employer’s reputation

• Disparage managers, co-workers, etc.

• Disclose confidential information

• Result in vicarious liability

• Misuse or waste company assets

• Violate FTC guidelines

• Otherwise violate company policy or the law

Not limited to work hours or company technology

What’s an Employer to do?

How to deal with employees’ online

activity?

Preventative steps

• (i.e., monitoring)

Reactive steps

• (i.e., discipline or termination)

Employees’ Online Activity

Employees’ Online Activity

Kevin,

Thanks for letting us

know – hope everything

is ok in New York.

(cool wand)

Cheers,

PCD

Responding to Employees’

Online Activity

General Rule: At-Will Employment, but . . .

Contractual Limitations

Responding to Employees’

Online Activity

Contractual Limitations

Anti-Discrimination/Harassment Laws

Responding to Employees’

Online Activity

Contractual Limitations

Anti-Discrimination/Harassment Laws

State or Local Laws

Responding to Employees’

Online Activity

Contractual Limitations

Anti-Discrimination/Harassment Laws

State or Local Laws

Retaliation Protections

Responding to Employees’

Online Activity

Contractual Limitations

Anti-Discrimination/Harassment Laws

State or Local Laws

Retaliation Protections

Labor Laws

Responding to Employees’

Online Activity

Contractual Limitations

Anti-Discrimination/Harassment Laws

State or Local Laws

Retaliation Protections

Labor Laws

Privacy Issues

QUESTIONS ?

Website: www.brownwinick.com

Toll Free Phone Number: 1-888-282-3515

OFFICE LOCATIONS:

666 Grand Avenue, Suite 2000

Des Moines, Iowa 50309-2510

Telephone: (515) 242-2400

Facsimile: (515) 283-0231

616 Franklin Place

Pella, Iowa 50219

Telephone: (641) 628-4513

Facsimile: (641) 628-8494

DISCLAIMER: No oral or written statement made by BrownWinick attorneys should

be interpreted by the recipient as suggesting a need to obtain legal counsel from

BrownWinick or any other firm, nor as suggesting a need to take legal action. Do not

attempt to solve individual problems upon the basis of general information provided

by any BrownWinick attorney, as slight changes in fact situations may cause a

material change in legal result.