Embed Size (px)

Citation preview

Debra Peters North Central Kansas Community Network, Co. (NCKCN)

Printed On: 30 January 2018 Requests of more than $5,000 1

NCKCN-NCRPC Home Ownership Loan/Grant Program-2 County PilotRequests of more than $5,000

North Central Kansas Community Network, Co. (NCKCN)Mr. Douglas McKinney 109 N. Mill StreetP.O. Box 565Beloit, KS 67420

O: 785-738-2218M: 785-738-8350

Mrs. Debra Peters 109 N. Mill StreetP.O. Box 565Beloit, KS 67420

[email protected]: 785-738-2218M: 785-823-6016

Debra Peters North Central Kansas Community Network, Co. (NCKCN)

Printed On: 30 January 2018 Requests of more than $5,000 2

Application Form

Organization InformationVerification of tax-exempt status* Organization is:

501(c)(3) public charity

Verification of status Please note: Applications from public charities (501(c)3 organizations) are required to attach verification of charitable status in order to be considered. A state sales tax exemption DOES NOT complete this requirement. Applications from churches and/or government entities are not required to attach a verification document.

NCKCN IRS 501[c]3 Determination Ltr 7-7-93.pdf

Physical Address If the physical address of your organization is different than the mailing address, please enter your physical address below.

NA

Project InformationProject Name* Name of Project.

NCKCN-NCRPC Home Ownership Loan/Grant Program-2 County Pilot

Amount requested* $251,200.00

Primary objectives* The Foundation has six primary objectives. Which of these does your program or project best addresses:

Economic Development

Debra Peters North Central Kansas Community Network, Co. (NCKCN)

Printed On: 30 January 2018 Requests of more than $5,000 3

County or Counties Served* Please check the primary county served by the program/project for which you are requesting funds.

CloudMitchell

Communities Served* Please list the primary community served by the program/project for which you are requesting funds.

Our proposed program will serve two Counties, Cloud and Mitchell, through this pilot program; however, with any success, our hope is that we will ultimately be able to service a much larger area. Cloud County communities served include Aurora, Concordia (county seat), Clyde, Glasco, Jamestown, Miltonvale, and Simpson (partly in Mitchell County). Mitchell County communities include Beloit (county seat), Cawker City, Glen Elder, Hunter, Tipton, Scottsville, and Simpson (partly in Cloud County).

Strategic Doing Project* Was this application generated through the Strategic Doing initiative?

No

Target Population* Please check one or more populations served by the program/project for which you are requesting funds.

All

Project Description* Briefly describe the program/project for which you are requesting funds.

We request your reconsideration of our December 2017 request to create the NCKCN-NCRPC Home Ownership Loan/Grant Program. Housing is one of the biggest issues in both retaining and attracting residents in rural Kansas. Knowing the excessive housing on the market, we are again proposing to create a loan/grant program to make existing homes on the market more affordable and attractive to current and future residents. The updated proposed program seeks to make home ownership more affordable by offering a combination of a 0% down payment assistance loan of up to 10% of the purchase price ($10,000 limit) and closing cost grant of up to 2.5% of the purchase price (limit $2,500) when purchasing an existing home.

There is a tremendous need for support in our current housing market. Our desire is to improve current and future Northwest Kansas residents’ quality of life through home ownership. Home ownership not only creates a greater sense of independence and confidence for the future, it also makes residents more prideful, engaged and connected to their community through greater participation and volunteerism. We believe it will be a catalyst for someone to buy something closer to their workplace or to buy their first home. Additionally, our proposed program is designed to address the ongoing issue of having too many homes on the market. In January 2018, there were approximately 122 homes on the market in Cloud County and 60 homes in Mitchell County. Funds will be utilized to reduce these vacancies by approximately 32 homes within approximately one year.

Debra Peters North Central Kansas Community Network, Co. (NCKCN)

Printed On: 30 January 2018 Requests of more than $5,000 4

We have decreased the maximum amount of loan and grant funding available to each applicant. We have also developed a greater approach to sustainability. We believe these changes make the program more impactful to the region.

Grant Request Description* If funded, how will you specifically use the Dane G. Hansen funds?

The requested grant funds of $251,200 will be used to create a $200,000 loan pool/$51,200 grant pool. The program offers a combination of a 0% down payment assistance loan up to 10% of the purchase price ($10,000 limit) and closing cost grant up to 2.5% of the purchase price (limit $2,500) on existing homes. See the additional document section for the calculation of the $251,200 grant being requested and the proposed terms/conditions of the program.

Example based on the purchase of a $62,500 home:

$6,250 10% NCKCN-NCRPC Home Ownership Program Loan/10% of purchase price $6,250 10% Borrower cash down payment could be combined with up to $5,000 from the

FHLB Home Ownership Set Aside Program (available May-November 2018) $50,000 80% Bank loan (see commitment letters attached to budget) ---------- $62,500 100% Total

====== $1,600 NCKCN-NCRPC Home Ownership Program Grant for closing costs/2.5% of purchase price

Project Objectives* What do you hope to achieve and how will it benefit the people of Northwest Kansas?

Through this pilot project, our hope is to assist in the purchase of approximately 32 homes in Cloud & Mitchell Counties. Our first objective is to improve the quality of life for both current and future residents through home ownership. Our secondary objective is to reduce the numbers of homes on the market.

Objective 1: Increase the Quality of Life: The proposed program will benefit the people of Northwest Kansas through home ownership. We believe our program will be a catalyst for someone to buy something closer to their workplace or to buy their first home - not only shortening commute times but also allowing the homeowners to become more rooted in the community in which they work. Helping someone buy a home can improve their quality of life because home ownership is often a source of pride, independence and confidence for the future. It can also help home owners to build personal wealth. Home ownership helps commuting employees spend less on fuel and offers more time with family. By encouraging employees to relocate in the community in which they work, it gives them more time to participate in community affairs and volunteerism that we think is vital to strengthening our communities and counties.

Objective 2: Reducing Homes on the Market: While this objective may seem obvious, we feel it is extremely valuable for the region. By potentially assisting in the sale of 32 homes in Cloud and Mitchell County, it will provide multiple benefits to those counties and the region. First, new residents mean more sales and property taxes being generated in the community. Next, with some of these homes sitting vacant, we will be preventing these homes from deteriorating overtime. Bringing in new people also means potentially bringing in new workforce, especially a more professional workforce. Due to less of a burden during purchase time, the home buyer may have more personal funds to spend on improving the quality of the existing home from participating in this down payment/closing cost assistance program. This would help

Debra Peters North Central Kansas Community Network, Co. (NCKCN)

Printed On: 30 January 2018 Requests of more than $5,000 5

with both increased valuation for the communities overtime, as well as a greater sense of pride from surrounding neighbors.

By partnering with various stakeholders in the County to market the program, the following objectives will also be met:

Realtors/Bankers: Improve employees quality of life through home ownership including a greater sense of pride, happiness, independence, and confidence for the future. In addition, homeowners are more engaged and connected to their community including community affairs/volunteerism.

Businesses/Economic Development: Assist employers in recruiting/retaining quality employees by helping them becoming more invested in their community and staking roots through home ownership, which provides more stability in the local job market. In addition, employers retaining their investment in on-the-job training and paid training/certification could result from the program. Also business retention could result from the program through employment stabilization and increased population. We will provide marketing flyers for employers to hand out to employees and post in their break room. Statistics show housing assistance programs marketed by employers to employees improves productivity, loyalty, reduces commute times, increases longevity, reduces turnover and thus reduces recruitment and training costs.

High school/City/County Government: Alumni mailings to families desiring to move back to their hometowns to raise the number of people relocating to their hometowns. Additional marketing through annual alumni banquet/celebrations will be useful.

We believe these marketing efforts will be successful partially based on information provided by Benjamin Winchester with Minnesota Extension presented at the March 18, 2017 Dane Hansen Community Foundation Forum entitled “Rewriting the Rural Narrative”. Winchester indicated that quality of life trumps a specific job opening when a person/families decide to move to a rural area. The Minnesota Extension’s research on newcomers indicated 36% having lived there previously, 68% held a bachelor’s degree, 67% had household incomes over $50,000, and 51% had children in the household. Those newcomers may be leaving their career or be currently underemployed and move back to be closer to family and other quality of life issues. Newcomers are moving for a simpler pace of life, safety and security, and lower housing costs. Newcomers are looking for more work-life balance. Those most likely to move to rural areas have an average age range of 30-49 and are providing a “brain gain” to our rural areas. Our objective would be to draw these “rural by choice” individuals and families into our rural communities through the incentive of offering this home ownership assistance program.

Timetable for the Project* When is the project projected to begin and end? For ongoing projects, when will the Dane G. Hansen funds be utilized?

The 2-County pilot project estimated are to begin as soon as funds are available and be completed within one year. The program is available for existing homes only. Once approved by Dane Hansen, NCKCN-NCRPC will finalize the creation of the NCKCN-NCRPC Home Ownership Program including application and loan closing documents to be completed by Debra Peters, proposed Program Manager. Debra has 28+ years of experience in lending. Then, we will implement the marketing plan for the NCKCN-NCRPC Home Ownership Program outlined in project objectives above.

The proposed pilot program will test the demand for the program, application/closing processes, and measure the results/outcomes in an effort to see if the program is meeting/exceeding expectations. These measurements will be used to fine-tune the program to expand it to our remaining 6-county Dane Hansen service area adding Ellsworth, Jewell, Lincoln, Ottawa, Republic, and Saline Counties. See Sustainability Section for more details.

Debra Peters North Central Kansas Community Network, Co. (NCKCN)

Printed On: 30 January 2018 Requests of more than $5,000 6

Additional Support Describe additional sources of support (if any) that have been secured or that will be pursued for this project.

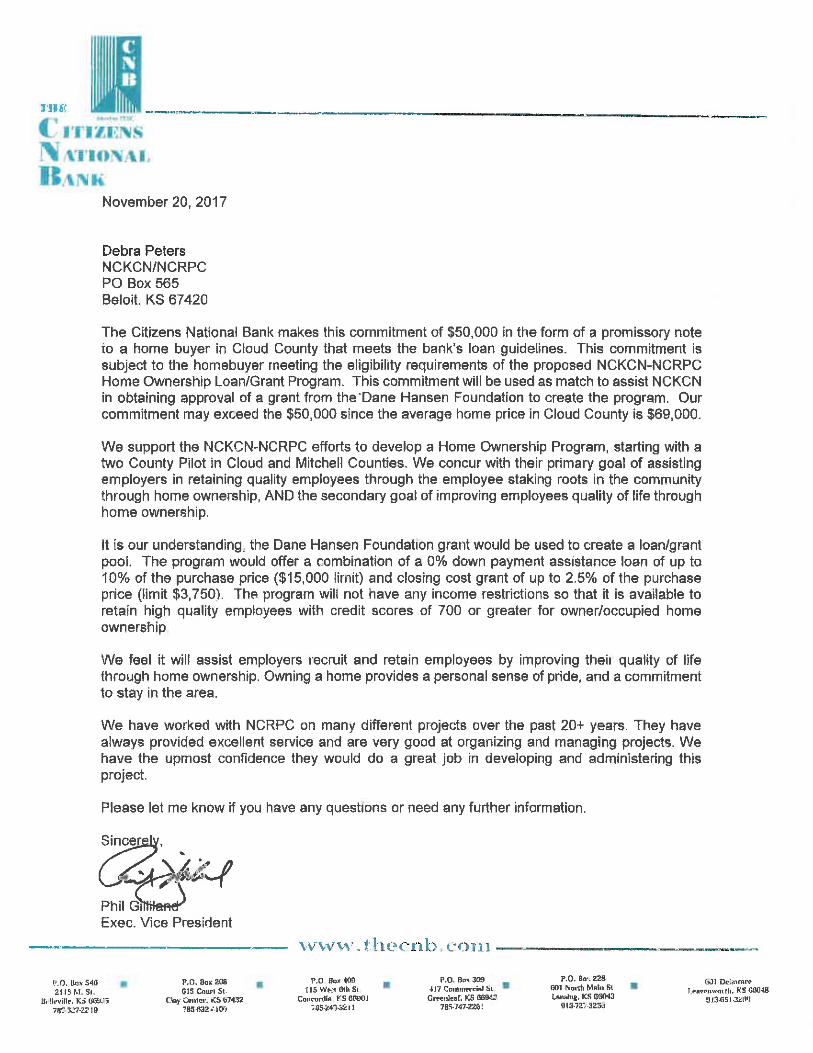

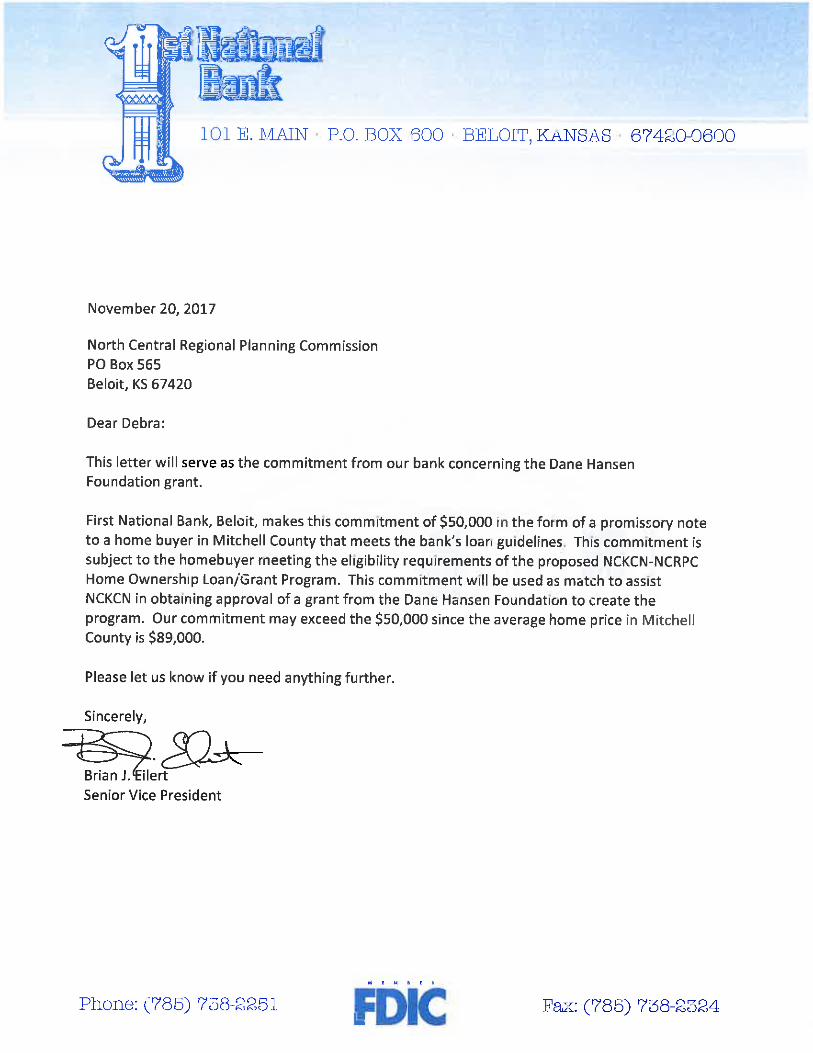

NCKCN estimates the bank’s portion of the 32 home purchases will total $1,600,000. Thus far, NCKCN has secured local match/financial commitment letters from eleven (11) banks in Cloud County & Mitchell Counties totaling $550,000 to be provided in the form of loans to purchase homes.

NCKCN estimates the applicant’s down payment contribution on the 32 home purchases will total approximately $200,000 (32 homes x $6,250).

In addition, Cloud Corp (county-wide economic and community development organization serving Cloud) and Solomon Valley Economic Development (county-wide economic and community development organization serving Mitchell) have provided support letters (See support letters attached below). Both organizations recognize the positive impact the proposed program will have in their counties and they have agreed to assist in the marketing of the program.

Evaluation* How will you evaluate the success of the project/program? Be specific. (If funded, this will be helpful when completing the final grant report.)

We have four key objectives: increased quality of life for all residents, especially employees, reducing homes on the market and resulting benefits, assisting employers in recruiting/retaining quality employees and drawing alumni to relocate to hometowns. We will evaluate our pilot project as being most successful if the following goals are met: purchase of 32 homes, recruitment of 10 new employees, retention of 22 employees, 16 students being retained or added to the schools and increased employee longevity. We will measure these results by having each applicant to the program complete a questionnaire at the time of application (details below). Also, we will follow up with employers/applicants in the future to see if their employee who participated in the program are still employed after 1, 3, and 5 years. Debra Peters, proposed Program Manager of the NCKCN-NCRPC Home Ownership Program, will track and submit the following results from the 2-county pilot program to the Dane Hansen Foundation:

NCKCN HOME OWNERSHIP TRACKING

___ Number of homes purchased through the program $__Average purchase price ___Number of in-house/conventional financed homes by area banks$__Average Program loan amount$__Average Program grant amount$__Local matching funds – total bank loans$__Local matching funds – total applicant’s own cash down payment

APPLICANT QUESTIONNAIRE

Improvements in Quality of Life:How many miles are you currently commuting to work (round trip)?Do you consider yourself to be activity involved in your current community? Do you hope to become more actively involved in the County where you are purchasing your home?

Debra Peters North Central Kansas Community Network, Co. (NCKCN)

Printed On: 30 January 2018 Requests of more than $5,000 7

Measurement of Employee Recruitment/Retainage:How many in your household are employed?Where are the residents of your home employed?Has anyone started a new job in the last 12 months? If so, was this relocation incentive a factor in youremployment decision?

Stabilizing/Increasing Population:How many are in your household moving to the County?How many of your children will start attending the new school in the community you purchased yourhome?

Supplementary Information:Where did you move from (City/County/State)?Did you rent or own a home prior to this purchase?Are you a first time homebuyer?Why did you decide to move to this community?How did you hear about the NCKCN-NCRPC Home Ownership Program?Was the NCKCN-NCRPC Home Ownership Program important in your decision to purchase a home in thiscommunity? If so, how?

Sustainability* How will the project/program be sustained in the future? (For capital projects, how will you maintain or operate the item or facility?)

The program will be administered and delivered by NCKCN-NCRPC. Proposed program manager Debra Peters with NCRPC has 28+ years of experience in lending.

Phase 1 –If 32 homes are purchased at an average of $6,250 through the proposed 2 County pilot program, it will contribute $200,000 into the loan portfolio. Portfolio of $200,000 in loans at 0% interest with an average term of 5 years will provide monthly payments of approximately $3,300 per month or $39,600 per year. Loan repayments of approximately $39,600 per year would allow the program to assist in the purchase of approximately 6 additional homes per year. NCKCN will require borrower to have good credit in order to better ensure and improve the sustainability of the program.

Phase 2 –Once the proposed pilot program proves there is a demand for the program it is meeting/exceeding expectations, we will create a permanent program by seeking additional funding to expand to our remaining 6-county Dane Hansen service area.

Phase 3 – Knowing the grant portion of the program would eventually eat into the capital base decreasing future sustainability of the loan pool, it would not be continued. New loans would be offered at 4% fixed interest rate to generate additional income to sustain the program. Should the program not generate enough repayments to meet market demands, it may be changed to a “relocation incentive” program only being available to applicants moving from outside Dane Hansen’s 26-county service area.

Debra Peters North Central Kansas Community Network, Co. (NCKCN)

Printed On: 30 January 2018 Requests of more than $5,000 8

Supporting DocumentsProposal Budget* Complete the budget form attached on the Grant Criteria page under document requirements and upload here.

NCKCN-NCRPC Project Budget and Local Financial Commitment Letters-Reconsideration.pdf

Balance Sheet* A detailed financial statement is required. Please do not attach your entire audit report. An example can be found on the Grant Criteria page, under document requirements.

NCKCN-Balance Sheet-12-31-17.pdf

Income Statement* A detailed financial statement is required. Please do not attach your entire audit report. An example can be found on the Grant Criteria page, under document requirements.

NCKCN-Income Stmt YTD thru 12-31-17.pdf

Board of Directors* Please attach a list of your board members. (Name and title, no biographies.)

NCKCN Board Members 2018.pdf

Bid or Quote A copy of the bid or quote is required for a capital project or purchase.

Letter of Support 1 A letter of support may be attached, but is not required.

Solomon Valley Support Ltr 11-21-17.pdf

Letter of Support 2 A second letter of support may be attached, but is not required.

Cloud Corp Support Ltr 11-17-17.pdf

Letter of Support 3 A third letter of support may be attached, but is not required.

Jamestown State Bank Support Ltr 11-24-17.pdf

Debra Peters North Central Kansas Community Network, Co. (NCKCN)

Printed On: 30 January 2018 Requests of more than $5,000 9

Additional Documents If there are additional documents that are critical to the trustees’ understanding of your proposal, upload them here.

Additional Documentation and Supporting Data-Reconsideration 1-26-18.pdf

Electronic SignatureSignature of Applicant* By entering my full legal name here, I warrant the truthfulness of the information provided in this application.

Debra Peters

Title of Applicant* NCKCN-NCRPC Business Finance Director

Signature of Principal or College President (if required) By entering my full legal name here, I warrant that I have read and support this application.

NA

Title of Principal or College President NA

Signature of CEO, Director, Mayor, etc. If this request is for a City, 501 (c)(3) Organization, Government Entity, etc., the signature of the CEO, Director, Mayor, etc., is required.

By entering my full legal name here, I warrant that I have read and support this application.

Douglas L. McKinney

Title of CEO, Director, Mayor, etc. Executive Director of NCKCN-NCRPC

Debra Peters North Central Kansas Community Network, Co. (NCKCN)

Printed On: 30 January 2018 Requests of more than $5,000 10

InternalTracking Number*

2018-2-11

501c3* Yes

Debra Peters North Central Kansas Community Network, Co. (NCKCN)

Printed On: 30 January 2018 Requests of more than $5,000 11

File Attachment SummaryApplicant File Uploads• NCKCN IRS 501[c]3 Determination Ltr 7-7-93.pdf• NCKCN-NCRPC Project Budget and Local Financial Commitment Letters-Reconsideration.pdf• NCKCN-Balance Sheet-12-31-17.pdf• NCKCN-Income Stmt YTD thru 12-31-17.pdf• NCKCN Board Members 2018.pdf• Solomon Valley Support Ltr 11-21-17.pdf• Cloud Corp Support Ltr 11-17-17.pdf• Jamestown State Bank Support Ltr 11-24-17.pdf• Additional Documentation and Supporting Data-Reconsideration 1-26-18.pdf

NCKCN BOARD OF DIRECTORS, AS OF JANUARY 1, 2018

Doug Clingman AG Solutions IT

204 E. Court St Beloit, KS 67420 Ian Draemel NCK Tech College IT Director 1103 Ash Beloit, KS 67420 ofc 785-738-9031 cell 785-738-7650 Deb Hadacheck Belleville Telescope/Beloit Presbytarian Church 2494 Penn Rd Cuba, KS 66940 Kris Heinze WireReady Inc. 1013 N. 183rd Rd. Lincoln, KS 67455 Charles R. Heidrick, Sec.-Treasurer Former Banker/Former City Councilmember/Former County Commissioner 1905 Plymouth Landing Manhattan, KS 66502 Jenny Russell Jen Rus Freelance 314 Main Street Courtland, KS 67437

Additional Documentation Supporting Data NCKCN-NCRPC Relationship NCKCN was organized as a 501c3 by the North Central Regional Planning Commission (NCRPC) to enhance the NCRPC’s mission of advancing North Central Kansas through comprehensive community and economic planning/development (www.ncrpc.org). NCKCN will hold the funds for the proposed NCKCN-NCRPC Home Ownership Program. NCKCN is managed by the North Central Regional Planning Commission (NCRPC) having the same address/phone number. Dane Hansen Project Cost Estimates The proposed project cost is $2,051,200 based on purchasing 32 homes with an average purchase price of $62,500 ($2,000,000) and 32 grants at average of $1,600 each ($51,200). The Dane Hansen Foundation request of $251,200 is based on the following:

$6,250 average NCKCN-NCRPC Home Ownership loan amount x 32 homes = $200,000 in loans $1,600 average NCKCN-NCRPC Home Ownership grant amount x 32 homes = $51,200 in grants

The bank loan portion of the home purchase is anticipated to total approximately $1,600,000 based on the following:

$50,000 average bank loan amount x 32 homes = $1,600,000 in loans The applicant’s portion of the cash down payment is anticipated to total approximately $200,000 based on the following: $6,250 average cash down payment x 32 homes = $200,000. Proposed terms/conditions for the NCKCN-NCRPC Home Ownership Loan/Grant Program NCKCN-NCRPC Home Ownership Loan proposed terms/conditions: Maximum loan: 10% of purchase price, not to exceed $10,000, subject to availability of funds

Interest rate: 0% fixed interest rate Term: 5-year term

Fee: 1% closing fee to assist in covering NCKCN/NCRPC administration Eligibility: Owner/occupied home in qualifying county Existing homes, not new construction

Meeting bank qualifications for its loan No borrower income guidelines, so the program is more broadly available

Borrower with 700+ credit score Education: Bank will provide home ownership education for first time homebuyers that is

available in the area. NCKCN-NCRPC Home Ownership Grant proposed terms/conditions: Maximum grant: 2.5% of purchase price, not to exceed $2,500, subject to availability of funds Eligibility: Must be combined with loan program, not available by itself

Same eligibility requirements as loan program

Example of how the proposed program would work on the purchase of an existing $62,500 home: $6,250 10% NCKCN-NCRPC Home Ownership Program Loan/10% of purchase

Price ($10,000 maximum) $6,250 10% Borrower cash down payment could be combined with up to $5,000 from the FHLB Home Ownership Set Aside Program (available May- November 2018) $50,000 80% Bank loan (see commitment letters attached to budget) $62,500 100% Total ======

$1,600 NCKCN-NCRPC Home Ownership Program Grant for closing costs/2.5% of purchase price ($2,500 maximum)

Sustainability Phase 1 – 2 County Pilot Phase 1 is a 2-County Pilot for Cloud/Mitchell Counties to evaluate the success of the proposed program. The $51,200 grant for closing cost assistance will not be recaptured. The $200,000 in initial loans will be made at 0% interest. There will be a 1% closing fee to assist in NCKCN-NCRPC time/effort. Administration will be covered by in-kind donation from NCKCN-NCRPC. Here’s an example of how much funds are needed to launch the 2-county pilot and how many additional homes can be purchased in the future from the repayment of the loans $6,250 average NCKCN-NCRPC Home Ownership Loan x 32 homes = $200,000 in loan portfolio

Portfolio of $200,000 in loans at 0% interest with an average term of 5 years will provide monthly payments of approximately $3,300 per month or $39,600 per year.

Program Sustainability: Loan repayments of approximately $39,600 per year would allow the program to assist in the purchase of approximately 6 additional homes per year.

Phase 2 – Add 6 Counties The proposed pilot program will test the demand for the program, application/closing processes, and measure the results/outcomes in an effort to determine if the program is meeting/exceeding expectations. If our pilot programs prove to be successful, we plan to fine-tune the program and create a permanent program by seeking additional Dane Hansen Foundation funds to expand the program to our remaining 6-county Dane Hansen service area including Ellsworth, Jewell, Lincoln, Ottawa, Republic, and Saline Counties. See Sustainability Section for more details. Phase 3 After completing the permanent program implement in Phase 2, the grant portion of the program will not be continued in the future. Continuing the grant portion of the program would eat into the capital base of the program and over time decrease the future sustainability of the loan pool. Also in this phase, new loans would be offered at 4% fixed interest rate to generate additional income to sustain the program.

If the program is not generating enough repayments to meet market demands, then program may be changed to a “relocation incentive” and only being available to applicants moving into the 8-counties from outside of Dane Hansen’s 26-county service area. Borrower May Save Private Mortgage Insurance We hope the program will result in more conventional financed homes by area banks, which helps the local economy. In addition if the bank originates a 80% loan-to-value loan, then the borrower can avoid private mortgage insurance (PMI). Thus, the money that would have paid for PMI can now go to the payment on our down payment loan and build more equity in the home. Average Home Affordability Based on Median Household Income It is recommended that a household spend no more than 25% of its income on housing. Based on the median household income of $39,282 per year in 2015 for Cloud County and $48,217 per year in Mitchell County x 25% housing allowance = $818-$1,005 per month less $200 per month allowance for real estate insurance/tax escrow would result in a loan of approximately $93,000-$122,000. Source: 2015 American Community Survey – Median income Potential Impact on Schools Average household size in Cloud & Mitchell Counties is 2.01 and 1.91. Note: Average household size includes some single parent households with 1-2 children. Source: 2015 American Community Survey estimates. If 32 homes were purchased with the proposed NCKCN-NCRPC Home Ownership Program with an average of .5 children impacted per home, this could result in an estimated 16 students being retained/added in Cloud & Mitchell County School Districts with an estimated value of $64,096 based on $4,006 per pupil base state aid per Kansas School Finance Bill.

Housing & Other Data – Cloud County County population: 9,339 Housing Units: 4,637 Median family income: $39,282 Median home value: $69,000 Median age: 44 Average household size: 2.01 Source: The 2015 American Community Survey estimates. January 2018 Estimated Homes for Sale: 122 Aurora 1 Concordia 77 Clyde 7 Glasco 12 Jamestown 2 Miltonvale 23

Source: Cloud County Realtors

Housing & Other Data – Mitchell County County population: 6,296 Households: 3,294 Median family income: $48,217 Median home value: $89,000 Median age: 44 Average household size: 1.91

Source: The 2015 American Community Survey estimates. January 2018 Homes for Sale: 60 Beloit 54 Glen Elder 3 Tipton 3

Source: Mitchell County Realtors

Initial Marketing Plan NCKCN-NCRPC will notify the banks when grant funding has been secured and the program is ready to launch. Cloud Corp (county-wide economic and community development organization serving Cloud) and Solomon Valley Economic Development (county-wide economic and community development organization serving Mitchell) have agreed to assist in the marketing of the program including: a)notify area employers; b)advise and provide program materials to realtors; c)post program information on social media accounts and the City/County web pages; d)coordinate with the Chamber of Commerce and other organizations to disseminate program information through newsletters and other written means; e)place a public service announcement regarding the program in the county newspaper; and f)provide information through radio interviews. By partnering with various stakeholders in the County to market the program, the following objectives will also be met: Realtors/Bankers: Improve employees quality of life through home ownership including a greater sense of pride, happiness, independence, and confidence for the future. In addition, homeowners are more engaged and connected to their community including community affairs/volunteerism. Businesses/Economic Development: Assist employers in recruiting/retaining quality employees by helping them becoming more invested in their community and staking roots through home ownership, which provides more stability in the local job market. In addition, employers retaining their investment in on-the-job training and paid training/certification could result from the program. Also business retention could result from the program through employment stabilization and increased population. We will provide marketing flyers for employers to hand out to employees and post in their break room. Statistics show housing assistance programs marketed by employers to employees improves productivity, loyalty, reduces commute times, increases longevity, reduces turnover and thus reduces recruitment and training costs. High school/City/County Government: Alumni mailings to families desiring to move back to their hometowns to raise the number of people relocating to their hometowns. Additional marketing through annual alumni banquet/celebrations will be useful. We believe these marketing efforts will be successful partially based on information provided by Benjamin Winchester with Minnesota Extension presented at the March 18, 2017 Dane Hansen Community Foundation Forum entitled “Rewriting the Rural Narrative”. Winchester indicated that quality of life trumps a specific job opening when a person/families decide to move to a rural area. The Minnesota Extension’s research on newcomers indicated 36% having lived there previously, 68% held a bachelor’s degree, 67% had household incomes over $50,000, and 51% had children in the household. Those newcomers may be leaving their career or be currently underemployed and move back to be closer to family and other quality of life issues. Newcomers are moving for a simpler pace of life, safety and security, and lower housing costs. Newcomers are looking for more work-life balance. Those most likely to move to rural areas have an average age range of 30-49 and are providing a “brain gain” to our rural areas. Our objective would be to draw these “rural by choice” individuals and families into our rural communities through the incentive of offering this home ownership assistance program.