Embed Size (px)

Citation preview

DEAL DRIVERS EMEAThe comprehensive review of mergers and acquisitions in the EMEA region.

2016FULL-YEAR EDITION

Published by:

In association with:

FINANCIAL TRANSACTIONS & REPORTING | MARKETING & COMMUNICATIONS FOR REGULATED INDUSTRY | CUSTOMER CONTENT & COLLABORATION SOLUTIONS

MERRILL DATASITE

This year, Merrill DataSite reached the 1 billion mark.

That’s 1 billion pages uploaded to our award-winning virtual data room since 2004.

Thousands of companies worldwide trust us to securely host their confidential information. Our single platform exists to support your rapidly changing needs.

Contact us at +44 20 3031 6300 to see how we can help you with your next transaction.

merrillcorp.com

© Merrill Communications LLC. All rights reserved.

Reaching the summit is no small feat.

1,000,000,000PAGES UPLOADED

41,000+VIRTUAL DATA ROOM PROJECTS SECURED

SINCE 2003

31,000+M&A TRANSACTIONS

SINCE 2003

20TECHNOLOGY AWARDS

IN THE PAST 8 YEARS

14LANGUAGES

SPOKEN

03

DEAL DRIVERS – EMEA

CONTENTS

ABOUT MERGERMARKET

Mergermarket is an unparalleled mergers and acquisitions intelligence tool. In any market, the lifeblood of advisers is deal flow. Mergermarket is unique in the provision of origination intelligence to the investment banking, legal, private equity, acquisition finance, public relations and corporate markets.

With an unrivalled network of journalists and analysts covering global M&A, Mergermarket generates proprietary

intelligence and delivers it, together with daily aggregated content, on its Mergermarket.com platform and by real-time email alerts to its subscribers.

This wealth of intelligence, together with a series of deal databases, individual and house league tables, profiles and editorial, has proven time and time again that this product can, and does, provide real revenues for Mergermarket’s clients. This is apparent when you see that Mergermarket

is used by over 400 of the world’s foremost advisory firms to assist in their origination process. Mergermarket is not interested in news, by then the opportunity has usually passed. Mergermarket focuses on revenue-generating intelligence and proves daily that it is one of the most useful and powerful tools for the M&A market.

Foreword 04

EMEA Heat Chart 05

All Sectors 06

Financial Services 14

Industrials & Chemicals 18

Energy, Mining & Utilities 22

Consumer 26

Telecoms, Media & Technology 30

Transportation 34

Pharma, Medical & Biotech 38

Construction 42

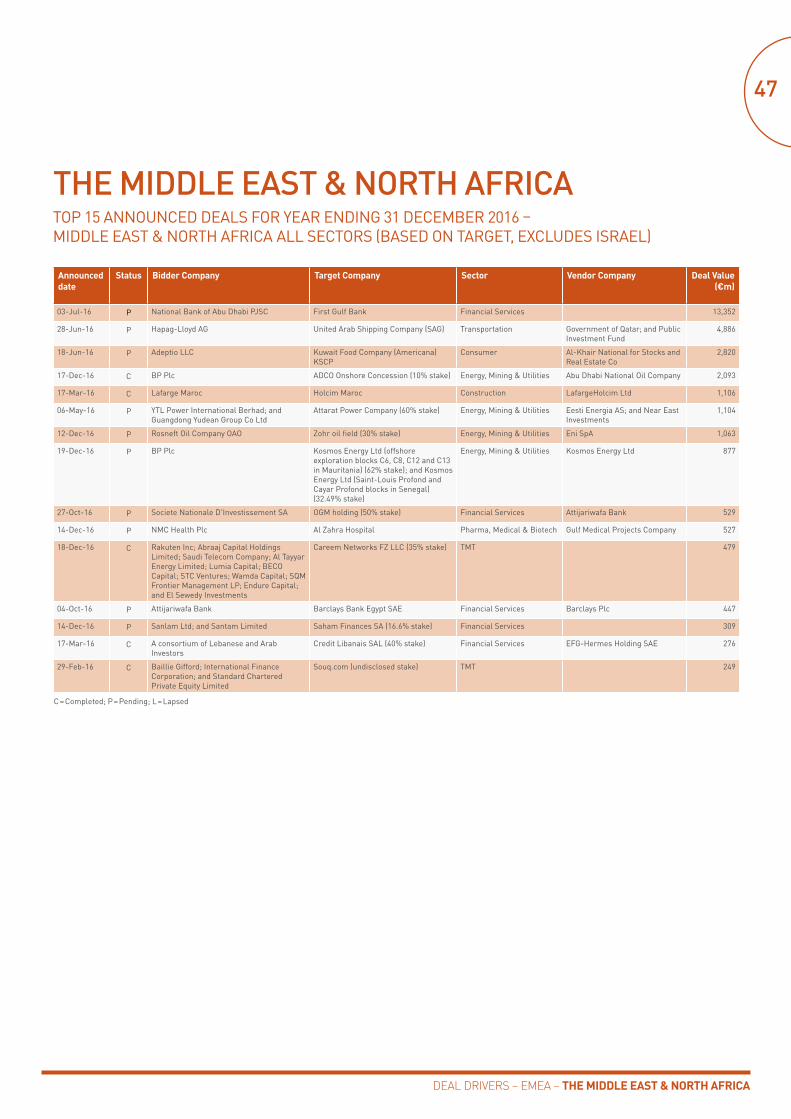

The Middle East & North Africa 46

About Merrill DataSite 50

Merrill DataSite Contacts 52

Welcome to the full-year 2016 edition of Deal Drivers EMEA, published by Mergermarket in association with Merrill Corporation.

This report provides an extensive review of M&A activity across Europe, the Middle East and North Africa. It offers detailed analysis of specific regions and sectors. It also identifies key trends that are set to develop over the course of the next six months.

Political uncertainty rocked Europe following the UK referendum in June and the severance process continues to cloud investor sentiment. However, M&A figures belie impressions of doom and gloom – deal volume in Europe reached a record high in 2016. Inbound value in particular sky rocketed in Q4, helping to make it a great year.

Market participants, and in particular PE firms, are also eager to seize any advantage arising out of the uncertainty and associated currency fluctuations. Transatlantic M&A remained unfazed, amounting to €344.8bn, continuing the record-highs of the past two years. A weaker pound (and euro) may make European targets more attractive for transatlantic buyers as the dollar gains strength. But uncertainty looms over the new US administration with market participants wary to predict policy changes. Monetary policy remains loose for the time being and corporates and Private Equity (PE) alike will take advantage of cheap cash while it lasts.

The partial rebound in Brent crude oil to a more comfortable level above US$50 per barrel provided some relief to struggling companies. This sparked mergers and helping to bridge the price expectation gap in a largely lacklustre dealmaking landscape. Nevertheless, the main attraction in the sector remains renewable energy, where several PE firms made successful exits over the past year. This sector has benefitted from a perk up in European power wholesale prices, making generating assets more attractive.

Distressed situations also continued to attract buyers to the Southern European regions. Here private capital is much needed by small and medium enterprises, as well as the financial services sector, with banks looking to chip away at non-performing loans.

In addition, Italian financial services experienced considerable consolidation, with several large mergers including the €3.7bn deal between Banca Popolare di Milano and Banco Popolare Societa Cooperativa.

Asian buyers, driven by China, have also enlivened dealmaking across Europe in 2016, with Asian acquirers bidding for strategic targets. Whether this trend will continue will greatly depend on the regulatory landscape, with China currently reigning in the outflow of capital, and governments in Europe looking to protect companies and IP of national interest. The sale of Germany’s Aixtron in September to Fujian Grand Chip Investment Fund was subject to much local scrutiny before ultimately failing due to US security concerns, and European governments have developed a heightened political awareness of bids for ‘critical’ infrastructure and technology.

However, European targets once highly prized for their location in a stable market now suddenly bear more risk. An increase in Euro-scepticism ahead of elections in Germany and France has the potential to polarise countries and brings with it the possibility of a volatile policy agenda.

This has already led to many investors branching out into less mature M&A markets such as Central and Eastern Europe, including into what were previously considered frontier markets such as Romania. Overall, it has been a record year for PE value in the CEE region and this trend is likely to continue. A number of privatisations in hot sectors such as pharma and telecoms are expected to contribute to the pipeline for 2017, which is also supported by a fast-growing software and technology scene.

The European M&A market for companies upgrading through digitalisation and the acquisition of technology across sectors is far from saturated and will continue to draw in international buyers. If not to London then to Berlin or perhaps to Tallinn.

04

DEAL DRIVERS – EMEA

FOREWORD

Sincerely,

Richard Martin Senior Director

05

DEAL DRIVERS – EMEA

EMEA HEAT CHART

Sector UK & Ireland

CEE German speaking

Italy Russia Nordics Benelux France SEE Iberia MENA Total

TMT 98 51 52 21 33 28 30 49 35 30 21 458

Consumer 36 79 41 87 49 29 40 45 19 18 15 458

Industrials & Chemicals 36 79 85 56 20 52 28 35 29 21 15 456

Energy, Mining & Utilities 59 35 16 28 29 30 15 7 16 19 14 268

Financial Services 44 30 38 26 37 14 18 10 10 12 9 248

Business Services 65 24 26 26 16 21 14 16 6 8 11 233

Pharma, Medical & Biotech 41 19 57 16 13 16 15 18 4 5 8 212

Leisure 32 22 11 6 9 10 16 11 10 11 5 143

Transportation 8 11 10 20 6 11 17 3 7 5 4 102

Construction 4 24 10 8 11 8 8 2 6 4 4 89

Real Estate 3 6 5 3 7 3 6 2 1 5 5 46

Agriculture 6 2 18 1 1 2 2 1 33

Defence 4 1 1 1 7

Other 2 2 4

Government 1 1 2

Total 432 387 353 298 249 233 209 199 147 140 112 2759

Hot Warm Cold

80 50 20

70 40 10

60 30 1

Note: Mergermarket’s Heat Chart of predicted deal flow is based on the intelligence collected in our database relating to companies rumoured to be up for sale, or officially up for sale, in the EMEA region. It is therefore indicative of areas that are likely to be active in the months to come. The intelligence comes from a range of sources, including press reports, company statements and our own team of journalists gathering proprietary intelligence from M&A practitioners across the region. The data does not differentiate between small and large transactions, nor between deals that could happen in the short or long term.

The Intelligence Heat Chart is based on ‘companies for sale’ stories tracked by Mergermarket in EMEA between 01/07/2016 and 31/12/2016. Opportunities are captured according to the dominant geography and sector of the potential target company.

EMEA HEAT CHART – INTELLIGENCE

For the coming months, Europe’s biggest M&A market, the UK and Ireland, is tipped to be the hottest with the TMT and business services sectors generating lots of market chatter, according to Mergermarket’s Heat Chart, which tracks ‘companies for sale’ stories.

The end of 2016, saw 21st Century Fox’s bid for a 60.9% stake in UK-based media company Sky for €21.4bn in order to diversify geographic reach across the Atlantic. Momentum in the sector looks set to build as the long-term attractiveness of such UK companies is coupled with big US players scouring Europe for the right set of capabilities.

Inbound investors are expected to become more active as uncertainty may begin to give way to an increasingly clear understanding of the impact of the UK’s decision to leave the EU and the processes involved.

Italy’s consumer sector remains hot for both the luxury and the fast-moving consumer goods segment as foreign investors look to

invest in the country’s brands. Further consolidation in the Italian financial services sector has been discussed in the context of difficulties facing the country’s banks.

Regulations aimed to make the financial services sector more stable in the wake of the financial crisis are also expected to continue to spark M&A among insurers, as large players seek diversified revenue streams and smaller businesses buckle under the weight of new capital and reporting rules.

The industrials & chemicals sector looks set to see considerable dealmaking including from bidders seeking out targets in Germany and the Central Eastern European region, commentators say. A number of industrials & chemicals companies in the Nordics have also been tipped for M&A activity.

Market participants also anticipate continued M&A in the MENA region as lower oil prices continue to exert pressure on cash flows of many of the Gulf region’s businesses.

06

DEAL DRIVERS – EMEA – ALL SECTORS

ALL SECTORSOVERVIEW

ALL SECTORS

Dealmakers seized on opportunities in Europe over the past year, pushing deal volume to a record high. Following a stellar year for global M&A in 2014 and 2015, 2016 continued to be a busy year for M&A in Europe. European deal volume amounted to 6,999 deals, topping 2015 with a 4% year-on-year increase. Deal value saw a slight decline of 10% year-on-year with a combined €729.5bn worth of announced deals. This included 21 megadeals above €5bn, amounting to €298.4bn – a similar outturn to 2015.

Despite Brexit woes, the UK & Ireland maintained pole position in European M&A with 22.3% of volume and 27.5% of value. The third quarter, in the immediate aftermath of the UK referendum, included the €27.3bn acquisition of microprocessor technology business ARM Holdings by Japanese SoftBank Group, with the latter transaction making up close to two-thirds of total deal value that quarter. Deal flow continued at a steady pace afterwards.

US buyers were also keen to tap into European technology, with this trend yielding the top deal of the year with the acquisition of Dutch company NXP Semiconductors by Qualcomm Inc for €42.1bn, and thereby making telecoms, media & technology (TMT) the top sector by value in 2016.

Rush for technology The German-speaking countries (Germany, Austria and Switzerland), followed on the heels of the UK & Ireland as the second most-targeted destination in Europe. While industrials & chemicals remain a staple of the German economy, the government has made it its mission to advance automation and the Internet-of-Things under the banner of Industrie 4.0. The success of this strategy is evident in bids such as the €3.8bn offer for robotics company KUKA AG from Chinese household appliances business Midea Group. While this deal received final regulatory approvals at the year’s end, the bid by Fujian Grand Chip Investment Fund for semiconductor business Aixtron lapsed following heightened attention by the Committee on Foreign Investment in the United States (CIFIUS).

Nevertheless, Chinese outbound activity reached a record high in 2016, according to Mergermarket data, and China's was the second biggest inbound force by value and volume in Europe after the US.

The inrush of Asian buyers also contributed to unprecedented dealflow in Central and Eastern Europe, where new transport infrastructure would have the potential to bolster access to both the CEE region and to Western European consumer markets.

The 2015 blockbuster acquisition of UK brewer SABMiller by AB InBev also sparked more deal flow in the region with the divestment of Anheuser-Busch’s CEE portfolio, which includes the popular Pilsner Urquell brand, to Japan’s Asahi Group for €7.3bn.

Private equity in Eastern Europe also shot to new heights in 2016, amounting to €4.3bn in deal value. This is partly due to GDP growth projections above the EU average in many of the region’s countries which have sparked a positive outlook for consumer spending and the growth of e-commerce.

Energy futures Commodities futures prices continued to spark M&A in the energy, mining & utilities sector across Europe, but in particular in Russia and the Middle East. National oil companies squeezed by the prolonged downturn in oil prices began in 2016 to seek out mergers to implement cost-efficiencies and, in the case of Russia, maintain cashflow and stake out market share. A consortium between Qatar Investment Authority and commodities trading giant Glencore made a €10.5bn-bid for a 19.5% stake in Rosneft Oil Company which effectively represents the biggest privatisation in Russia in many years.

Corporates were also keen to maximise efficiencies. While the merger between the US’ BakerHughes and Halliburton fell through, FMC Technologies jumped on the opportunity to merge with France’s Technip following their Forsys Subsea joint-venture in 2015.

In the utility segment, renewable assets (and in particular wind farm portfolios) continued to change hands across Europe, with many PE holding cycles winding down. Among the largest such exits was US PE firm Blackstone Energy Partners’ sale of a 80% stake in German WindMW for €1.7bn to China’s Three Georges, and UK-based firm Bridgepoint Advisers’ exit from Spanish Bora Wind Energy for €500m.

Private equity Buyouts were up 10% in volume in 2016 but combined value amounted to €108bn, a decrease of 11% compared to the previous year. Nevertheless, the 1,245 buyout deals accounted for 18% of total European deal flow by volume. The largest buyout of the year was the sale of a majority stake for €13.4bn (40x EBITDA multiple) in the UK’s gas distribution business, National Grid, by Macquarie, Allianz Capital Partners, Qatar Investment Authority and China Investment Authority among others. This deal is also indicative of the appetite sovereign wealth funds and insurance companies have in stable, long-term infrastructure, in particular in utilities and transportation. North American buyers were also active in 2016, with a €2.5bn bid for London City Airport by a consortium led by Canadian Ontario Teachers’ Pension Plan and including Kuwait Investment Authority.

As the infrastructure gap across Europe remains wide this trend is set to continue, with inbound investors willing to park funds long-term, especially as long as bank debt remains cheap.

However, growing Euroscepticism, Italy’s banking travails and the Brexit process may yet prove to be testing for investors seeking safe havens ahead of a tightening in interest rates.

ALL SECTORSTOP 20 ANNOUNCED DEALS FOR YEAR ENDING 31 DECEMBER 2016 (EUROPEAN TARGET)

DEAL DRIVERS – EMEA – ALL SECTORS

07

Announced Date

Status Bidder Company Target Company Sector Vendor Company Deal Value (€m)

27-Oct-16 P Qualcomm Incorporated NXP Semiconductors NV TMT 42,058

03-Feb-16 P China National Chemical Corporation

Syngenta AG Industrials & Chemicals 42,039

18-Jul-16 C SoftBank Group Corp ARM Holdings Plc (98.55% stake) TMT 27,276

15-Dec-16 P 21st Century Fox Inc Sky Plc (60.9% stake) TMT 21,373

21-Jul-16 C Sacam Mutualisation Credit Agricole – Regional Banks (25% stake) Financial Services Credit Agricole SA 18,542

12-Apr-16 C DZ Bank AG Westdeutsche Genossenschafts-Zentralbank Financial Services 17,000

25-Jan-16 C Johnson Controls Inc Tyco International plc Industrials & Chemicals 14,973

08-Dec-16 P A Consortium led by Macquarie Infrastructure and Real Assets

National Grid Gas Distribution Ltd (61% stake) Energy, Mining & Utilities National Grid Plc 13,428

16-Mar-16 P Deutsche Boerse AG London Stock Exchange (LSE) Plc Financial Services 13,339

27-Jun-16 C Boehringer Ingelheim GmbH Merial SAS Pharma, Medical & Biotech Sanofi SA 11,400

07-Dec-16 P A Consortium led by Qatar Investment Authority

Rosneft Oil Company OAO (19.5% stake) Energy, Mining & Utilities Rosneftegaz OAO 10,503

10-Feb-16 C Mylan NV Meda AB Pharma, Medical & Biotech 8,844

21-Jun-16 P Tencent Holdings Ltd Supercell Oy (84.3% stake) TMT SoftBank Group Corp 7,607

13-Feb-16 P Asahi Group Holdings Ltd Anheuser-Busch InBev NV (Central and East European Beer Business)

Consumer Anheuser-Busch InBev NV 7,300

07-Sep-16 P Liberty Media Corporation Formula One Group Leisure CVC Capital Partners Limited; Waddell & Reed Financial Inc; BlackRock Inc; and Norges Bank

6,969

17-Jun-16 P Siemens AG Gamesa Corporacion Tecnologica SA Industrials & Chemicals 6,640

15-Feb-16 C Liberty Global Europe Holding BV/Vodafone International Holdings BV

Ziggo BV; and Vodafone Libertel BV TMT Vodafone International Holdings BV; and Liberty Global Europe Holding BV

6,200

10-Oct-16 C Rosneft Oil Company OAO Bashneft ANK OAO (50.08% stake) Energy, Mining & Utilities The Federal Agency for State Property Management

5,929

05-Sep-16 P HELIOS Kliniken GmbH Quironsalud Pharma, Medical & Biotech CVC Capital Partners Limited 5,760

04-Mar-16 C Inversora Carso SA de CV Fomento de Construcciones y Contratas SA (48.3% stake)

Construction 5,734

C = Completed; P = Pending; L = Lapsed

DEAL DRIVERS – EMEA – ALL SECTORS

ALL SECTORSEUROPEAN M&A SPLIT BY DEAL SIZE

VALUE VOLUME

Moving average trend line

Based on announced deals, excluding those that lapsed or were withdrawn, where the dominant location of the target is in Europe.

08

Quarter endedQuarter ended

QUARTERLY M&A ACTIVITY – ALL SECTORS

VALUE VOLUME

Volu

me

Valu

e (€

bn)

Volu

me

Valu

e (€

m)

>€5,001m

€2,001m – €5,000m

€501m – €2,000m

€251m – €500m

€5m – €250m >€5,001m

€2,001m – €5,000m

€501m – €2,000m

€251m – €500m

€5m – €250m

Value not disclosed

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

7,000

7,500

2016201520142013201220112010

1,963

4,631

2,065

4,270

2,239

197

3,974

1,907

3,611

1,798

3,323

2,030

3,187

1,896

2,702

9

12

20 1921

15632

133

1611312

34

153

180

17336

172

14035

170

42 17118641

184178

35

0

100

200

300

400

500

600

700

800

900

2016201520142013201220112010

336.5

127.2

64.0

298.4

106.3

100.5

160.3

65.5

101.9

213.1

119.4

70.4

108.2

106.7

97.5

60.8

90.9

104.9

161.8

148.9 137.4176.8 177.8

52.9

92.7

88.9

113.1

159.6

61.3

100.1

109.8

99.1

140.1

46.1

86.8

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

2010 2011 2012 2013 2014 2015 2016

0

25,000

50,000

75,000

100,000

125,000

150,000

175,000

200,000

225,000

250,000

275,000

300,000

Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

2010 2011 2012 2013 2014 2015 2016

09

DEAL DRIVERS – EMEA – ALL SECTORS

European bidder acquiring a North American target

North American bidder acquiring a European target

Total North American/ European deals

Based on dominant location of target and bidder and excludes all buyouts.

ALL SECTORSEUROPEAN BUYOUTS EUROPEAN EXITS

Quarter endedQuarter ended

Value Volume

Based on announced deals, excluding those that lapsed or were withdrawn, where the dominant location of the target is in Europe.

TRANSATLANTIC DEALS

VALUE VOLUME

Valu

e (€

m)

Volu

me

Valu

e (€

m)

Volu

me

Volume

Valu

e (€

m)

Valu

e (€

m) Volum

e

Quarter ended Quarter ended

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

110,000

120,000

Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

2010 2011 2012 2013 2014 2015 2016

0

25

50

75

100

125

150

175

200

225

250

275

300

325

350

Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

2010 2011 2012 2013 2014 2015 2016

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q10

25

50

75

100

125

150

175

200

225

250

275

300

2010 2011 2012 2013 2014 2015 2016

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q10

50

100

150

200

250

300

350

400

2010 2011 2012 2013 2014 2015 2016

22.2%

16.7%

12.7%7.5%

6.5%

8.8%

14.2%

9.4%2.0%

27.4%

19.8%

10.5%

6.8%

7.0%

10.4%

8.1%

9.0%

1.0%1.0%

19.8%

13.9%

5.8%

5.7%12.7%

21.1%

4.0%

2.5%

7.1%

2.1%

0.3%

4.4%0.6%

20.5%

6.7%

15.9%

13.9%

6.0%

14.4%

4.7%

3.5%

6.6%

4.8%

1.6%0.1%

1.3%

DEAL DRIVERS – EMEA - ALL SECTORS

ALL SECTORSMIX OF DEALS BY GEOGRAPHIC REGION

VALUE VOLUME

UK & Ireland

German speaking

France

Italy

Iberia

Benelux

Nordic

Central & Eastern Europe

Other

MIX OF DEALS BY INDUSTRY SECTOR

VALUE VOLUME

Industrials & Chemicals

Financial Services

Business Services

Consumer

Energy, Mining & Utilities

TMT

Leisure

Transportation

Pharma, Medical & Biotech

Construction

Real Estate

Defence

Agriculture

Based on announced deals, excluding those that lapsed or were withdrawn. Geographic region is determined with reference to the dominant location of the target.

Based on announced deals, excluding those that lapsed or were withdrawn, where the dominant location of the target is in Europe. Industry sector is based on the dominant industry of the target.

10

ALL SECTORSFINANCIAL ADVISERS

DEAL DRIVERS – EMEA - ALL SECTORS

LEGAL ADVISERS

TOP 20 – RANKED BY VALUE TOP 20 – RANKED BY VOLUME

TOP 20 – RANKED BY VALUE TOP 20 – RANKED BY VOLUME

2016 2015 Company Name Value (€m)

Number of Deals

1 1 Goldman Sachs 355,544 110

2 2 Morgan Stanley 321,710 96

3 4 Bank of America Merrill Lynch 217,102 88

4 11 Credit Suisse 209,792 71

5 8 Rothschild 204,918 259

6 3 JPMorgan 194,315 117

7 6 Barclays 189,538 80

8 5 Lazard 156,032 146

9 7 Deutsche Bank 145,329 64

10 15 UBS Investment Bank 142,799 84

11 12 Citi 125,294 86

12 13 Centerview Partners 101,673 13

13 21 Evercore Partners 100,839 47

14 19 HSBC 78,136 38

15 9 Robey Warshaw 60,243 4

16 - Ducera Partners 56,454 1

17 33 RBC Capital Markets 51,559 35

18 10 BNP Paribas 49,901 98

19 94 ALANTRA 48,091 68

20 75 China International Capital 44,297 3

2016 2015 Company Name Value (€m)

Number of Deals

1 4 Freshfields Bruckhaus Deringer 243,620 209

2 10 White & Case 225,877 212

3 19 Allen & Overy 210,934 220

4 1 Cravath, Swaine & Moore 203,539 19

5 13 Linklaters 189,459 220

6 2 Clifford Chance 181,776 214

7 15 Davis Polk & Wardwell 175,661 32

8 6 Sullivan & Cromwell 152,039 45

9 3 Cleary Gottlieb Steen & Hamilton 149,593 61

10 5 Skadden Arps Slate Meagher & Flom 132,091 72

11 39 Shearman & Sterling 126,086 61

12 50 Paul Weiss Rifkind Wharton & Garrison 107,423 27

13 8 Wachtell, Lipton, Rosen & Katz 101,068 15

14 162 Morrison & Foerster 95,354 16

15 31 Simpson Thacher & Bartlett 94,179 46

16 25 Slaughter and May 93,679 50

17 51 Jones Day 91,747 145

18 9 Weil Gotshal & Manges 78,142 112

19 14 Debevoise & Plimpton 73,713 23

20 38 Kirkland & Ellis 73,346 85

2016 2015 Company Name Value (€m)

Number of Deals

1 1 DLA Piper 68,670 276

2 2 CMS 24,680 254

3 3 Allen & Overy 210,934 220

4 4 Linklaters 189,459 220

5 5 Clifford Chance 181,776 214

6 7 White & Case 225,877 212

7 6 Baker & McKenzie 51,269 211

8 8 Freshfields Bruckhaus Deringer 243,620 209

9 9 Jones Day 91,747 145

10 12 Eversheds 22,741 145

11 10 Latham & Watkins 69,056 140

12 11 Hogan Lovells International 27,435 126

13 13 Weil Gotshal & Manges 78,142 112

14 23 Dentons 14,856 107

15 30 Pinsent Masons 9,631 103

16 42 PwC legal 6,368 97

17 18 Squire Patton Boggs 2,510 97

18 92 Orrick Herrington & Sutcliffe 7,210 94

19 19 Norton Rose Fulbright 11,762 87

20 20 Kirkland & Ellis 73,346 85

2016 2015 Company Name Value (€m)

Number of Deals

1 3 KPMG 18,464 280

2 1 PwC 12,964 266

3 2 Rothschild 204,918 259

4 5 Deloitte 17,131 233

5 4 EY 7,963 196

6 7 Lazard 156,032 146

7 15 BDO 1,130 125

8 8 JPMorgan 194,315 117

9 6 Goldman Sachs 355,544 110

10 16 BNP Paribas 49,901 98

11 9 Morgan Stanley 321,710 96

12 12 Bank of America Merrill Lynch 217,102 88

13 11 Citi 125,294 86

14 10 Oaklins 1,428 86

15 17 UBS Investment Bank 142,799 84

16 14 Barclays 189,538 80

17 25 Clearwater International 1,019 79

18 20 Lincoln International 2,136 73

19 18 Credit Suisse 209,792 71

20 23 Grant Thornton 853 69

The financial adviser league tables by value and volume have been run from 01/01/2016 to 31/12/2016, excluding lapsed and withdrawn deals. The tables are pan-European and cover all sectors.

The legal adviser league tables by value and volume have been run from 01/01/2016 to 31/12/2016 and include lapsed and withdrawn deals. The tables are pan-European and cover all sectors.

11

DEAL DRIVERS – EMEA - ALL SECTORS

ALL SECTORSFINANCIAL ADVISERS – SMALL-CAP (€5M – €250M)

LEGAL ADVISERS – SMALL-CAP (€5M – €250M)

TOP 20 – RANKED BY VALUE TOP 20 – RANKED BY VOLUME

TOP 20 – RANKED BY VALUE TOP 20 – RANKED BY VOLUME

The financial adviser small-cap league tables by value and volume have been run from 01/01/2016 to 31/12/2016, excluding lapsed and withdrawn deals.The tables are pan-European and cover all sectors.

The legal adviser small-cap league tables by value and volume have been run from 01/01/2016 to 31/12/2016 and include lapsed and withdrawn deals.The tables are pan-European and cover all sectors.

2016 2015 Company Name Value (€m)

Number of Deals

1 1 Rothschild 7,951 75

2 4 KPMG 6,063 91

3 2 PwC 5,371 81

4 3 Deloitte 4,689 58

5 6 Lazard 4,361 34

6 12 JPMorgan 3,964 24

7 9 BNP Paribas 3,116 29

8 5 EY 3,037 51

9 34 UniCredit Group 2,465 27

10 10 Morgan Stanley 2,405 13

11 21 Jefferies 2,352 17

12 8 Goldman Sachs 2,230 15

13 15 Barclays 2,174 17

14 27 ALANTRA 2,075 35

15 43 William Blair & Company 1,930 16

16 28 Houlihan Lokey 1,884 20

17 18 Robert W. Baird & Co 1,839 14

18 38 Societe Generale 1,794 12

19 67 Carnegie Investment Bank 1,761 18

20 7 Citi 1,755 11

2016 2015 Company Name Value (€m)

Number of Deals

1 5 Clifford Chance 6,764 62

2 4 Allen & Overy 6,074 56

3 1 DLA Piper 5,568 77

4 2 Linklaters 5,423 66

5 7 Baker & McKenzie 5,001 69

6 3 CMS 4,614 65

7 12 Freshfields Bruckhaus Deringer 4,439 40

8 6 White & Case 4,296 53

9 15 Norton Rose Fulbright 3,606 41

10 31 Travers Smith 3,154 28

11 10 Jones Day 3,034 45

12 9 Hogan Lovells International 2,952 44

13 26 King & Wood Mallesons 2,845 33

14 11 Weil Gotshal & Manges 2,843 24

15 8 Eversheds 2,735 40

16 25 Latham & Watkins 2,644 28

17 76 Dentons 2,618 37

18 30 Pinsent Masons 2,536 40

19 19 Ashurst 2,477 22

20 22 Skadden Arps Slate Meagher & Flom 2,290 20

2016 2015 Company Name Value (€m)

Number of Deals

1 1 DLA Piper 5,568 77

2 3 Baker & McKenzie 5,001 69

3 4 Linklaters 5,423 66

4 2 CMS 4,614 65

5 7 Clifford Chance 6,764 62

6 5 Allen & Overy 6,074 56

7 8 White & Case 4,296 53

8 9 Jones Day 3,034 45

9 10 Hogan Lovells International 2,952 44

10 20 Norton Rose Fulbright 3,606 41

11 15 Cuatrecasas 2,142 41

12 14 Freshfields Bruckhaus Deringer 4,439 40

13 6 Eversheds 2,735 40

14 22 Pinsent Masons 2,536 40

15 11 Squire Patton Boggs 2,237 38

16 47 Dentons 2,618 37

17 13 King & Wood Mallesons 2,845 33

18 75 Orrick Herrington & Sutcliffe 1,662 33

19 12 Osborne Clarke 1,537 32

20 27 Bird & Bird 1,942 31

2016 2015 Company Name Value (€m)

Number of Deals

1 5 KPMG 6,063 91

2 1 PwC 5,371 81

3 3 Rothschild 7,951 75

4 4 Deloitte 4,689 58

5 2 EY 3,037 51

6 11 ALANTRA 2,075 35

7 6 Lazard 4,361 34

8 9 BDO 1,130 34

9 7 BNP Paribas 3,116 29

10 25 UniCredit Group 2,465 27

11 22 JPMorgan 3,964 24

12 8 Oaklins 1,065 24

13 42 Houlihan Lokey 1,884 20

14 10 Grant Thornton 853 20

15 19 Investec 1,368 19

16 41 Carnegie Investment Bank 1,761 18

17 23 Clearwater International 756 18

18 24 Jefferies 2,352 17

19 28 Barclays 2,174 17

20 37 William Blair & Company 1,930 16

12

DEAL DRIVERS – EMEA - ALL SECTORS

ALL SECTORSPR ADVISERS

PR ADVISERS – SMALL-CAP (€5M – €250M)

TOP 20 – RANKED BY VALUE TOP 20 – RANKED BY VOLUME

TOP 20 – RANKED BY VALUE TOP 20 – RANKED BY VOLUME

The PR adviser small-cap league tables by value and volume have been run from 01/01/2016 to 31/12/2016 and exclude lapsed and withdrawn deals.The tables are based on advice to a European bidder, target or vendor.

The PR adviser league tables by value and volume have been run from 01/01/2016 to 31/12/2016 and exclude lapsed and withdrawn deals.The tables are pan-European and cover all sectors.

2016 2015 Company Name Value (€m)

Number of Deals

1 1 Brunswick Group 254,540 145

2 6 Sard Verbinnen & Co 187,917 44

3 2 Finsbury 155,782 66

4 5 FTI Consulting 143,828 157

5 21 CNC (Publicis/MSLGROUP) 138,768 37

6 10 Hering Schuppener (Finsbury) 105,846 37

7 3 Joele Frank Wilkinson Brimmer Katcher 89,876 33

8 43 Hirzel.Neef.Schmid.Counselors (AMO) 59,443 4

9 8 Kekst (Publicis/MSLGROUP) 53,757 39

10 24 Weber Shandwick Worldwide 44,636 13

11 - Dynamics Group 42,479 5

12 11 Maitland (AMO) 36,444 73

13 13 Citigate 19,656 56

14 30 Image Sept 19,176 67

15 9 Greenbrook Communications 18,492 56

16 12 Abernathy MacGregor Group (AMO) 17,770 19

17 85 Cardew Group 14,038 4

18 17 Powerscourt 13,680 35

19 25 Fitzroy Communications 13,339 2

20 75 Adfactors PR 11,711 5

2016 2015 Company Name Value (€m)

Number of Deals

1 1 FTI Consulting 5,206 74

2 2 Brunswick Group 3,019 38

3 6 Finsbury 2,360 19

4 4 Maitland (AMO) 2,001 24

5 8 Greenbrook Communications 1,897 15

6 3 Citigate 1,607 17

7 10 Instinctif Partners 1,594 30

8 9 Tulchan Communications 1,506 24

9 148 Community Group 1,423 22

10 7 Bell Pottinger Financial & Corporate 1,414 23

11 5 Hering Schuppener (Finsbury) 1,184 8

12 19 Hudson Sandler 1,146 12

13 17 Barabino & Partners 1,090 16

14 20 Kekst (Publicis/MSLGROUP) 1,022 8

15 44 Powerscourt 966 20

16 11 MHP Communications 897 20

17 15 Edelman 871 8

18 25 CityPress PR 821 9

19 65 Kreab 792 14

20 14 Image Sept 762 10

2016 2015 Company Name Value (€m)

Number of Deals

1 1 FTI Consulting 5,206 74

2 2 Brunswick Group 3,019 38

3 4 Instinctif Partners 1,594 30

4 6 Maitland (AMO) 2,001 24

5 9 Tulchan Communications 1,506 24

6 8 Bell Pottinger Financial & Corporate 1,414 23

7 154 Community Group 1,423 22

8 24 Powerscourt 966 20

9 5 MHP Communications 897 20

10 7 Finsbury 2,360 19

11 10 Buchanan Communications 415 18

12 3 Citigate 1,607 17

13 14 Barabino & Partners 1,090 16

14 22 Greenbrook Communications 1,897 15

15 67 Kreab 792 14

16 17 Hudson Sandler 1,146 12

17 19 Walbrook PR 150 12

18 13 Camarco 487 11

19 11 Redleaf Polhill 172 11

20 16 Image Sept 762 10

2016 2015 Company Name Value (€m)

Number of Deals

1 1 FTI Consulting 143,828 157

2 2 Brunswick Group 254,540 145

3 4 Maitland (AMO) 36,444 73

4 14 Image Sept 19,176 67

5 6 Finsbury 155,782 66

6 3 Citigate 19,656 56

7 8 Greenbrook Communications 18,492 56

8 5 Tulchan Communications 8,875 48

9 7 Instinctif Partners 5,717 47

10 18 Sard Verbinnen & Co 187,917 44

11 30 Community Group 9,498 42

12 11 Kekst (Publicis/MSLGROUP) 53,757 39

13 20 CNC (Publicis/MSLGROUP) 138,768 37

14 12 Hering Schuppener (Finsbury) 105,846 37

15 23 Powerscourt 13,680 35

16 13 Joele Frank Wilkinson Brimmer Katcher 89,876 33

17 9 Bell Pottinger Financial & Corporate 7,121 33

18 32 Kreab 2,854 32

19 47 Kable Communication Finance 2,278 32

20 19 Barabino & Partners 3,159 31

13

FINANCIAL SERVICESOVERVIEW

14

DEAL DRIVERS – EMEA - FINANCIAL SERVICES

Europe’s financial services sector last year wrestled with an increasingly stringent regulatory environment, the threat of pending interest rate hikes and highly volatile foreign exchange markets, alongside the additional distractions of Brexit and a US presidential election, yet still ended the year with a more active M&A market than in 2015.

Last year’s 468 deals compare favourably with a 6% increase to the 441 announced in 2015, with value similarly on the rise. A total €101.2bn changed hands throughout last year’s financial services deals versus €84.14bn a year prior, a 20% increase year-on-year.

The two largest contributors to this total came from the banking sector in the form of French holding company Sacam Mutualisation’s 25% stake acquisition in Credit Agricole’s regional banks worth €18.5bn, closely followed by the €17bn merger of Germany’s DZ Bank and Westdeutsche Genossenschafts-Zentralbank (WGZ).

Credit Agricole’s deal served to bolster the French banking group’s capital base in response to Basel III regulations while DZ and WGZ created the country’s third largest bank in terms of total assets. Post-merger, the combined entity has approximately €500bn of assets, placing closely behind German counterpart Commerzbank with €533bn. The deal was taking place barely months before Germany’s largest, Deutsche Bank, was being investigated for misleading and deceiving investors over repackaged mortgages.

Away from banking, insurance deals were hampered by the low interest rate environment, Solvency II and changes to tax regimes across Europe, causing operators to take a hard look at their portfolios and rethink their growth strategies. This led to many insurers divesting non-performing assets and using the cash to improve their capital adequacy ratios. Small to mid-market acquisitions were undertaken in an effort to offset the lack of growth potential in core European markets. That is not to say that the insurance sector was short of sizable deals last year.

Canadian property and casualty insurance provider Fairfax Financial acquired Switzerland-based Allied World for €4.5bn, and the €2.5bn merger between Dutch NN Group and Delta Lloyd Group were both announced in 2016.

The merger between the Canadian and Swiss insurers, along with Fairfax’s acquisition of UK-based Brit insurance in 2015, created a world leader in property and casualty insurance, reinsurance and investments. Meanwhile, NN Group’s decision to acquire its Dutch rival, Delta Lloyd, is expected to generate annual pre-tax cost savings of around €150m by 2020, as well as bringing increased stability to the company in a market full of challenges through benefits of scale.

Regulators’ decision to put in place greater transparency requirements has placed considerable pressure on investment managers operating across the EU to simplify and, ultimately, lower their overall fee structure, especially headline fees. Client fees have often provided a significant level of return for fund, wealth and asset managers alike. However, the Markets in Financial Instruments Directive II (MiFID II) will shed much-needed light on this source of income, permitting clients to heavily scrutinise the charges they incur. The increase in regulation has not only negatively impacted a major revenue stream for fund managers, but the added compliance burden imposed by regulators is ramping up the overall cost of conducting business too. This has led many firms to pursue M&A in order to swell their assets under management (AuM) in a bid to provide a buffer against rising costs coupled with a reduction in fees driven by increased transparency.

Europe’s largest asset manager, Amundi’s €3.6bn acquisition of UniCredit’s Pioneer Investments last year reflects this trend. The transaction increases the French asset manager’s AuM to €1.27tn, making it the 10th largest investment company globally, while also providing the scale required to weather the regulatory storm. In the UK, Tilney Bestinvest’s takeover of wealth manager Towry off Palamon Capital Partners was another such deal

last year. The transaction served to turn Tilney Bestinvest into one of the largest UK wealth management firms providing both financial planning and investment management, boasting €23bn-plus of AuM and a little more than €230m in revenues.

The megamerger between London Stock Exchange (LSE) and Deutsche Boerse announced in March has served to prop up deal value for the financial services sector and will continue to do so this year, as it faces further scrutiny from EU regulators over competition concerns. On top of the antitrust element, the Brexit vote has served to make this one of the most politically charged deals the market has seen in recent years, as German politicians, uncomfortable with the prospect of having euro-denominated clearing in London, push for the headquarter to be relocated to Frankfurt. Despite merger parties eager for the deal to be finalised and remaining adamant that the structure of the deal should remain unchanged, there is still a real risk of it falling through.

The same drivers that spurred deal volumes in financial services last year are likely to continue to do so in 2017. Increased regulation is expected to force companies to assess their portfolios and make divestments in order to bring stability to their balance sheets, while simultaneously looking out for inorganic opportunities in a Europe suffering from a prolonged period of low growth. This year will see national elections in both Germany and France, with opinion polls suggesting that euro-sceptic parties, France’s National Front and Germany’s Alternative fuer Deutschland, threaten to upset the pro-Europe equilibrium and usher in a period of greater uncertainty over the stability of the EU. This is likely to bring more volatility to the stock market and wider fluctuations in exchange rates that will likely spur inbound investment from US businesses looking to take advantage of a weaker euro and sterling.

by Aaran Fronda

15

DEAL DRIVERS – EMEA - FINANCIAL SERVICES

FINANCIAL SERVICESTOP 15 ANNOUNCED DEALS FOR YEAR ENDING 31 DECEMBER 2016 (EUROPEAN TARGET)

Announced Date

Status Bidder Company Target Company Vendor Company Deal Value (€m)

21-Jul-16 C Sacam Mutualisation Credit Agricole – Regional Banks (25% stake) Credit Agricole SA 18,542

12-Apr-16 C DZ Bank AG Westdeutsche Genossenschafts-Zentralbank 17,000

16-Mar-16 P Deutsche Boerse AG London Stock Exchange (LSE) Plc 13,339

18-Dec-16 P Fairfax Financial Holdings Limited Allied World Assurance Company Holdings AG 4,503

23-Mar-16 C Banco Popolare Societa Cooperativa Banca Popolare di Milano Scarl 3,714

12-Dec-16 P Amundi SA Pioneer Investment Management SGR UniCredit Group 3,545

28-Jul-16 C Banca Ifis SpA GE Capital Interbanca SpA General Electric Company 2,555

02-Nov-16 P NN Group NV Delta Lloyd Group 2,459

08-Dec-16 P Powszechny Zaklad Ubezpieczen SA; and Polish Development Fund SA

Bank Pekao SA (32.8% stake) UniCredit Group 2,382

20-Dec-16 P Lloyds Banking Group Plc MBNA Limited Bank of America Corporation 2,262

18-Apr-16 C Quaestio Capital Management Sgr Srl Banca Popolare di Vicenza SpA (99.33% stake) 1,500

28-Apr-16 C WiZink Bank SA Barclays Plc (Barclaycard business in Portugal and Spain)

Barclays Plc 1,300

12-Sep-16 L HarbourVest Global Private Equity Ltd SVG Capital Plc 1,200

01-Jul-16 C Mercedes-Benz Financial Services Nederland BV Athlon Car Lease International BV De Lage Landen International BV 1,100

28-Sep-16 P Phoenix Group Holdings Limited Abbey Life Assurance Company Ltd Deutsche Bank AG 1,085

C = Completed; P = Pending; L = Lapsed

Quarter ended

30.7%

13.5%

6.6%8.3%

5.6%

7.9%

8.8%

15.0%

3.6%

23.3%

20.3%

23.9%

15.8%

2.8%

6.0%

1.7% 5.3%

0.9%

16

DEAL DRIVERS – EMEA - FINANCIAL SERVICES

VALUE VOLUME

UK & Ireland

German speaking

France

Italy

Iberia

Benelux

Nordic

Central & Eastern Europe

Other

QUARTERLY TRENDS

VALUE VOLUME

Based on announced deals, excluding those that lapsed or were withdrawn. Geographic region is determined with reference to the dominant location of the target.

Based on announced deals, excluding those that lapsed or were withdrawn, where the dominant location of the target is in Europe.Industry sector is based on the dominant industry of the target.

FINANCIAL SERVICESMIX OF DEALS BY GEOGRAPHIC REGION

Volu

me

Valu

e (€

m)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

2010 2011 2012 2013 2014 2015 2016

0

25

50

75

100

125

150

Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

2010 2011 2012 2013 2014 2015 2016

Quarter endedMoving average trend line

17

DEAL DRIVERS – EMEA - FINANCIAL SERVICES

FINANCIAL SERVICESFINANCIAL ADVISERS

TOP 20 – RANKED BY VALUE TOP 20 – RANKED BY VOLUME

LEGAL ADVISERS

TOP 20 – RANKED BY VALUE TOP 20 – RANKED BY VOLUME

2016 2015 Company Name Value (€m)

Number of Deals

1 9 Bank of America Merrill Lynch 35,759 17

2 1 Morgan Stanley 29,827 13

3 2 JPMorgan 29,119 27

4 5 Rothschild 25,036 25

5 - Credit Agricole 22,629 6

6 3 Goldman Sachs 22,099 13

7 11 Deutsche Bank 21,675 11

8 16 Credit Suisse 20,362 7

9 4 UBS Investment Bank 19,861 11

10 10 Lazard 19,758 10

11 12 Barclays 18,365 18

12 15 HSBC 14,916 4

13 164 Perella Weinberg Partners 14,794 3

14 28 Societe Generale 14,449 9

15 20 RBC Capital Markets 13,703 3

16 - Robey Warshaw 13,339 1

17 29 Mediobanca 9,130 5

18 34 UniCredit Group 8,551 11

19 7 Citi 7,604 12

20 47 KPMG 5,153 26

2016 2015 Company Name Value (€m)

Number of Deals

1 9 Freshfields Bruckhaus Deringer 29,351 29

2 51 Cleary Gottlieb Steen & Hamilton 22,575 8

3 48 White & Case 20,369 16

4= - Brandford-Griffith 18,542 1

4= - Darrois Villey Maillot Brochier 18,542 1

6 2 Linklaters 15,093 28

7 85 Latham & Watkins 13,652 9

8 24 Herbert Smith Freehills 13,386 6

9 131 Baker & McKenzie 11,434 20

10 14 Allen & Overy 10,675 28

11 46 Gianni, Origoni, Grippo, Cappelli & Partners

8,168 7

12 3 Clifford Chance 7,419 21

13 61 Gatti Pavesi Bianchi 7,352 8

14 8 Skadden Arps Slate Meagher & Flom 5,834 10

15 64 Torys 5,745 3

16 38 Shearman & Sterling 5,685 6

17 84 Willkie Farr & Gallagher 5,170 4

18 18 Slaughter and May 4,980 12

19 235 Walder Wyss 4,941 4

20 78 Homburger 4,550 2

2016 2015 Company Name Value (€m)

Number of Deals

1 2 JPMorgan 29,119 27

2 1 KPMG 5,153 26

3 6 Rothschild 25,036 25

4 9 Barclays 18,365 18

5 7 Deloitte 1,463 18

6 14 Bank of America Merrill Lynch 35,759 17

7 3 Morgan Stanley 29,827 13

8 5 Goldman Sachs 22,099 13

9 8 PwC 1,667 13

10 10 Citi 7,604 12

11 16 Deutsche Bank 21,675 11

12 11 UBS Investment Bank 19,861 11

13 28 UniCredit Group 8,551 11

14 4 EY 441 11

15 13 Lazard 19,758 10

16 22 Societe Generale 14,449 9

17 12 Fenchurch Advisory Partners 1,092 9

18 17 BNP Paribas 2,163 8

19 23 ALANTRA 163 8

20 20 Credit Suisse 20,362 7

2016 2015 Company Name Value (€m)

Number of Deals

1 2 Freshfields Bruckhaus Deringer 29,351 29

2 1 Linklaters 15,093 28

3 4 Allen & Overy 10,675 28

4 3 Clifford Chance 7,419 21

5 12 Baker & McKenzie 11,434 20

6 5 CMS 123 17

7 13 White & Case 20,369 16

8 6 DLA Piper 732 13

9 10 Slaughter and May 4,980 12

10 23 Schoenherr Rechtsanwaelte 1,443 11

11 32 Skadden Arps Slate Meagher & Flom 5,834 10

12 15 Hogan Lovells International 1,964 10

13 42 Eversheds 498 10

14 27 Latham & Watkins 13,652 9

15 17 Dentons 392 9

16 20 Cleary Gottlieb Steen & Hamilton 22,575 8

17 67 Gatti Pavesi Bianchi 7,352 8

18 7 Weil Gotshal & Manges 3,446 8

19 9 Norton Rose Fulbright 2,021 8

20 16 Uria Menendez 941 8

The legal adviser league tables by value and volume have been run from 01/01/2016 to 31/12/2016, and include lapsed and withdrawn deals.The tables are pan-European and cover the Financial Services sector.

The financial adviser league tables by value and volume have been run from 01/01/2016 to 31/12/2016, excluding lapsed and withdrawn deals.The tables are pan-European and cover the Financial Services sector.

INDUSTRIALS & CHEMICALSOVERVIEW

DEAL DRIVERS – EMEA - INDUSTRIALS & CHEMICALS

18

The European industrials & chemicals sector last year notched up its second most successful year of deal value and volume on Mergermarket record since 2001, spearheaded by multibillion euro transactions that helped navigate through a year otherwise punctuated with political and economic uncertainty.

Deal value spiked 45% to €144.7bn, catapulting it to becoming the second best performing sector in Europe, with 19.8% of the region’s total M&A value. Deal volume in 2016 ticked up 5% year-on-year, totalling 1,427 transactions.

The German-speaking countries, Germany; Austria and Switzerland, made up the lion’s share of deal activity with 49.2% of value and 25.1% of volume. The UK and Ireland followed with 18.4% of the sector’s value and 15.3% of volume.

Industrials & chemicals deals accounted for three of Europe’s top 20 largest deals last year. China National Chemical Corp (ChemChina), which in 2015 acquired tire manufacturer Pirelli for €8.1bn, this time pursued Switzerland-headquartered agrochemicals business Syngenta. The €42.04bn acquisition, announced in February, eventually became the second-largest European deal after Qualcomm’s €42.06bn takeover of NXP Semiconductor.

Other top-ranking industrials & chemicals sector deals included Johnson Controls’ €15bn acquisition of Irish building controls manufacturer Tyco International, and Siemens AG’s €6.6bn takeover of Gamesa, a Spanish wind turbine maker.

Such high-profile deals helped make up for the slowing pace that Brexit and the US elections brought into play. Following the largely unexpected result in Britain’s referendum on EU membership in June, dealmakers paused for breath – and in some cases extended their summer of holidays – to try to make sense what impact currency fluctuations and potential subsequent trade deals and new regulatory frameworks could have upon manufacturing companies.

The build-up to the US presidential election – and its similarly unforeseen result – added a further layer of uncertainty, which is expected to spill into 2017 as president Donald Trump is set to impose a protectionist agenda over manufacturing businesses in the US, including the automotive segment.

This uncertainty led to more subdued deal activity in the second half of the year, which nevertheless saw an above-average €45.6bn deal value and 691 transactions. Despite the upheaval caused by a stream of political events, factors that had earlier benefitted M&A have not entirely disappeared as low yields and cheap money continued to fill the tanks of buyout firms and companies’ balance sheets.

Inbound interest from Chinese buyers was another factor that pushed deal activity across the sector. Besides ChemChina’s combination with Syngenta deal, other high-profile Chinese bids included Midea Group’s €3.8bn takeover of German industrial robots manufacturer Kuka; China Tianying’s acquisition of Urbaser, a Spanish waste management business, for €2.2bn; and Yinyi’s purchase of Punch Powertrain, a Belgian automotive technology developer, for €1bn.

The industrials & chemicals sector has been of particular interest to China’s M&A outbound efforts as per its ‘Made in China 2025’ plan – a government-led initiative pushing companies to upgrade the country’s manufacturing capabilities via acquisitions. European businesses with technology in areas such as automation, robotics and artificial intelligence have increasingly become targets for cash-rich Chinese corporations and buyout firms.

M&A has also resulted from companies’ efforts to rearrange their businesses. French oil major, Total, sold its German chemical division Atotech in a €2.9bn deal to US PE firm The Carlyle Group. The sale, which ranked among the largest sponsor-backed transaction in the sector last year, was part of a US$10bn disposal plan set in response to the weakness in oil prices.

Such a rationale was also behind deals carried out by diversified industrials groups looking to gain focus in certain segments. Johnson Controls spun off Adient, its unit specialised in the automotive market, in a €3.9bn transaction that was part of its efforts to concentrate on the building controls segment. These were later reaffirmed with the acquisition of Tyco International. US-headquartered Emerson Electric, which had been running a strategic review for a couple of years, announced the sale of its European-based Motors, Drives and Electric Power Generation businesses, including branches in France and the UK, to Nidec, a Japanese motor maker, for €1bn.

On the back of a strong year, dealmakers have started 2017 on a bullish note as low yields appear likely to continue fuelling PE firms with cheap money while sluggish organic growth perspectives in Europe could prompt companies to hunt external growth alternatives. Setbacks may come from uncertainty in political events such as the developments on the Brexit process and the unpredictable polices arising from the new US administration.

More headwinds could come from potential curbs on outbound Chinese M&A. Protectionism over the country could be on the rise. China’s Fujian Grand Chip abandoned its takeover of Aixtron, a German semiconductor group with US branches, as the US administration blocked the deal based on national security grounds while the German government hesitated amid concerns over an increasing number of Chinese takeovers. Obstacles could also come from the Chinese government itself. At the end of 2016, Chinese authorities announced new plans to control capital outflow and keep the renminbi stable, in a measure that is likely to affect outbound M&A.

by Joao Grando

19

DEAL DRIVERS – EMEA - INDUSTRIALS & CHEMICALS

INDUSTRIALS & CHEMICALSTOP 15 ANNOUNCED DEALS FOR YEAR ENDING 31 DECEMBER 2016 (EUROPEAN TARGET)

Announced Date

Status Bidder Company Target Company Vendor Company Deal Value (€m)

03-Feb-16 P China National Chemical Corporation Syngenta AG 42,039

25-Jan-16 C Johnson Controls Inc Tyco International plc 14,973

17-Jun-16 P Siemens AG Gamesa Corporacion Tecnologica SA 6,640

08-Sep-16 C Johnson Controls Inc (Shareholders) Adient plc Johnson Controls Inc 3,910

18-May-16 C Midea Group Co Ltd KUKA AG (86.5% stake) 3,778

06-Oct-16 P The Carlyle Group Atotech Total SA 2,861

17-Jun-16 C BASF SE Chemetall GmbH Albemarle Corporation 2,843

18-Aug-16 P Emerson Electric Co Pentair Plc (Valves & Controls) Pentair Plc 2,783

26-Sep-16 C China Tianying Inc Urbaser SA ACS Actividades de Construccion y Servicios SA 2,212

16-Nov-16 P Electricite de France SA New NP (75% stake) AREVA SA 1,875

11-Oct-16 P General Electric Company LM Wind Power Holding A/S Doughty Hanson & Co 1,500

08-Jul-16 C Dmitry Lobyak (Private investor) Uralkali OJSC (20% stake) The ONEXIM Group 1,492

02-Jun-16 C EQT Partners AB Apleona GmbH Bilfinger SE 1,400

16-May-16 C Konecranes Plc Terex Corporation (Material handling & port solutions business)

Terex Corporation 1,127

02-Aug-16 C Nidec Corporation Emerson Electric Co (Motors, drives and electric power generation businesses)

Emerson Electric Co 1,072

C = Completed; P = Pending; L = Lapsed

Quarter endedQuarter ended

20

DEAL DRIVERS – EMEA - INDUSTRIALS & CHEMICALS

INDUSTRIALS & CHEMICALSMIX OF DEALS BY GEOGRAPHIC REGION

VALUE VOLUME

UK & Ireland

German speaking

France

Italy

Iberia

Benelux

Nordic

Central & Eastern Europe

Other

VALUE VOLUME

Moving average trend line

Based on announced deals, excluding those that lapsed or were withdrawn. Geographic region is determined with reference to the dominant location of the target.

Based on announced deals, excluding those that lapsed or were withdrawn, where the dominant location of the target is in Europe.Industry sector is based on the dominant industry of the target.

QUARTERLY TRENDS

Valu

e (€

m)

Volu

me

Quarter endedQuarter ended

0

50

100

150

200

250

300

350

400

Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

2010 2011 2012 2013 2014 2015 2016

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

2010 2011 2012 2013 2014 2015 2016

15.3%

25.0%

12.7%11.3%

5.8%

8.1%

13.5%

6.8% 1.5%

49.1%

18.4%

7.3%

3.3%

9.1%

3.5%

7.1%

1.9%0.3%

21

DEAL DRIVERS – EMEA - INDUSTRIALS & CHEMICALS

INDUSTRIALS & CHEMICALSFINANCIAL ADVISERS

TOP 20 – RANKED BY VALUE TOP 20 – RANKED BY VOLUME

LEGAL ADVISERS

TOP 20 – RANKED BY VALUE TOP 20 – RANKED BY VOLUME

2016 2015 Company Name Value (€m)

Number of Deals

1 10 Morgan Stanley 116,113 18

2 7 Credit Suisse 104,398 14

3 1 Goldman Sachs 87,106 23

4 2 Rothschild 75,049 56

5 3 Bank of America Merrill Lynch 65,327 9

6 4 JPMorgan 62,003 18

7 - Ducera Partners 56,454 1

8 8 UBS Investment Bank 47,847 13

9 40 HSBC 46,612 10

10 66 ALANTRA 43,167 21

11= - CCB International 42,039 1

11= - China CITIC Bank Corporation 42,039 1

11= 304 China International Capital 42,039 1

11= - Dyalco 42,039 1

15 14 Citi 34,883 20

16 13 Lazard 28,344 29

17 6 Barclays 26,523 16

18 - Centerview Partners 21,305 4

19 5 Deutsche Bank 13,143 6

20 9 BNP Paribas 9,905 18

2016 2015 Company Name Value (€m)

Number of Deals

1 13 Clifford Chance 109,328 40

2 49 Cravath, Swaine & Moore 98,493 2

3 19 Allen & Overy 84,269 33

4 9 Wachtell, Lipton, Rosen & Katz 79,739 6

5 4 Sullivan & Cromwell 76,863 10

6 5 Linklaters 71,081 36

7 51 Shearman & Sterling 67,789 13

8 14 Simpson Thacher & Bartlett 62,757 10

9 3 Cleary Gottlieb Steen & Hamilton 61,461 16

10 18 Paul Weiss Rifkind Wharton & Garrison 59,986 13

11 78 Debevoise & Plimpton 59,583 5

12 - Morrison & Foerster 58,107 5

13 339 Luthra & Luthra Law Offices 56,481 2

14 128 WilmerHale 56,467 2

15 71 Stikeman Elliott 56,454 5

16 - Franceschini e Miranda Advogados 56,454 1

17 11 White & Case 51,962 52

18 12 Davis Polk & Wardwell 51,509 9

19 80 Fangda Partners 50,927 8

20 414 Homburger 45,552 5

2016 2015 Company Name Value (€m)

Number of Deals

1 3 KPMG 2,717 65

2 1 PwC 1,902 62

3 4 Rothschild 75,049 56

4 5 Deloitte 8,711 50

5 2 EY 879 41

6 6 Lincoln International 839 31

7 8 BDO 205 30

8 7 Lazard 28,344 29

9 17 Goldman Sachs 87,106 23

10 16 Global M&A Partners 192 22

11 22 ALANTRA 43,167 21

12 9 Oaklins 325 21

13 20 Citi 34,883 20

14 25 Clearwater International 422 19

15 14 Morgan Stanley 116,113 18

16 13 JPMorgan 62,003 18

17 38 BNP Paribas 9,905 18

18 29 Barclays 26,523 16

19 12 DC Advisory 773 15

20 26 Credit Suisse 104,398 14

2016 2015 Company Name Value (€m)

Number of Deals

1 4 CMS 3,799 61

2 1 DLA Piper 4,342 53

3 6 White & Case 51,962 52

4 3 Baker & McKenzie 6,270 48

5 8 Jones Day 5,281 47

6 5 Clifford Chance 109,328 40

7 11 Freshfields Bruckhaus Deringer 28,954 38

8 10 Linklaters 71,081 36

9 2 Allen & Overy 84,269 33

10 7 Latham & Watkins 9,547 32

11 9 Eversheds 3,440 30

12 44 McDermott Will & Emery 5,249 27

13 19 Mannheimer Swartling 2,942 25

14 33 PwC legal 1,725 24

15 25 Vinge 1,534 24

16 15 Hengeler Mueller 5,420 21

17 16 Gleiss Lutz 44,770 20

18 17 King & Wood Mallesons 43,349 20

19 54 Noerr 890 20

20 79 Orrick Herrington & Sutcliffe 798 20

The financial adviser league tables by value and volume have been run from 01/01/2016 to 31/12/2016, excluding lapsed and withdrawn deals. The tables are pan-European and are based on the following sectors: Automotive; Chemicals & Materials; Industrials – electronics, automation and products and services; and Manufacturing – other.

The legal adviser league tables by value and volume have been run from 01/01/2016 to 31/12/2016 and include lapsed and withdrawn deals.The tables are pan-European and are based on the following sectors: Automotive; Chemicals & Materials; Industrials – electronics, automation and products and services; and Manufacturing – other.

DEAL DRIVERS – EMEA - ENERGY, MINING & UTILITIES

22

ENERGY, MINING & UTILITIESOVERVIEW

Deal activity across energy, mining and utility companies in 2016 somewhat mirrored that of commodity prices, rising throughout the year eventually ending 3% higher in terms of volume with 421 deals taking place versus 408 in 2015.

In January 2016, the oil prices sank below US$28-a-barrel, its lowest level since 2003, giving the industry already struggling to come to terms with a supply glut reality check.

But with Brent now happily trading above US$50-a-barrel, long-term investor appetite in 2016 resulted in slightly more dealmaking than in 2015.

However, combined value of Europe deals across all three sectors reached €93bn compared to €130bn in 2015, representing a 29% decrease on the previous year.

Energy, mining and utilities deals accounted for around 12.7% of the total value of M&A conducted across Europe in 2016, and 6% of total M&A volume.

Although not an entirely bullish year on the outset, there remains reason for optimism. Last year saw both the oil price nadir and political tumult – two trends that, by right, should depress both natural resource and utility deals.

However, the foot-dragging seen in 2015 among natural resource companies has seemingly been overcome. While depressed oil prices gave sellers the rationale and reasoning needed to exit, the steady rise in prices in the second half gave buyers confidence in mid- to long-term valuations.

The second-largest oil and gas deal was Rosneft’s capital hike, which saw a consortium led by Qatar Investment Authority and involving Glencore, take a 19.5% stake in the company for around €10.5bn.

Earlier in the year, the oil crunch saw other deals filter through as upstream and services companies sought out cleverly structured combinations to keep themselves competitive.

Topping this list was the €4bn merger between FMC Technologies and Technip, announced in May. The market downturn

drove the US equipment manufacturer and the French contractor together in order to cut costs and provide a single oilfield services offering to operators.

Mining likewise experienced a year divided by bearish and bullish commodity prices. The swing in prices became a disruptive influence on potentially large deals, as EMEA-headquartered major miners first launched and then hesitated on large disposal programmes. Glencore and Anglo American both set ambitious divestment targets in order to reduce their debt pile. These sales launched in earnest at the beginning of 2016 but the vendors’ expectations rose in line with commodity prices, and most of the deals fizzled out as markets improved and the urgency to sell abated.

Renewables saw a positive 2016 deal flow, with offshore wind catching the majority of interest, as highlighted by Blackstone Energy Partners’ €1.7bn sale of an 80% stake in Germany’s 288MW Meerwind wind farm to China Three Gorges.

Buyer interest in European power and utilities also yielded lively dealmaking activity in 2016. The largest deal of the year was the National Grid’s sale of a 61% stake in its UK gas distribution networks in December to a consortium of bidders led by Macquarie Infrastructure and Real Assets and China Investment Corp for €13.4bn.

French utility EDF’s sale of a 49.9% stake in French electricity distributor RTE for €4bn, as well as Spanish company Repsol and investment group Criteria Caixa’s 20% sale of Gas Natural Fenosa for €3.8bn are further examples of highly valued and highly competitive deals that took place in 2016.

These deals also became indicative of the appetite of long term investors – infrastructure and pension funds – for regulated and stable European assets.

Additionally, many deals that took place saw an element of interest from Asian investors looking to deploy capital in Europe. The €1.4bn sale of German waste-to-energy company EEW by EQT to Beijing Enterprise, being yet a further example.

Already 2017 appears to be shaping towards continuation of those trends seen in the second half of last year. A more stable oil price has created a positive deal environment and investor sentiment has returned to the sector, which may lead to a number of small-and-mid cap IPOs, as well as provide a little vim and vigour needed for larger players to return more active and acquisitive. A number of large oil and gas assets remain for sale and only time will tell whether the bid-ask disparity eventually aligns and these are successfully executed.

Mining should see a similar level of improved activity, with capital returning to exploration and with mid-tier producers seeing an opportunity to consolidate. With Glencore’s head, Glasenberg, returning to his entrepreneurial form and Anglo American’s spin-off plans afoot, the major miners could also surprise the sector with left-field transactions.

Power producers and utilities, however, remain the safest bet for a bullish 2017. The pipeline looks set with the sale of Goldman Sachs’ Spanish and Finnish portfolio gas distribution companies, Redexis and Elenia, due to kick off. Many large utilities such as EDF, Engie, Centrica, E.ON and Enel are carefully looking at adapting their portfolios and business focus, which could create opportunities for players looking to consolidate in their space.

by Patrick Harris

23

DEAL DRIVERS – EMEA – ENERGY, MINING & UTILITIES

ENERGY, MINING & UTILITIESTOP 15 ANNOUNCED DEALS FOR YEAR ENDING 31 DECEMBER 2016 (EUROPEAN TARGET)

Announced Date

Status Bidder Company Target Company Vendor Company Deal Value (€m)

08-Dec-16 P A Consortium led by Macquarie Infrastructure and Real Assets

National Grid Gas Distribution Ltd (61% stake) National Grid Plc 13,428

07-Dec-16 P A Consortium led by Qatar Investment Authority Rosneft Oil Company OAO (19.5% stake) Rosneftegaz OAO 10,503

10-Oct-16 C Rosneft Oil Company OAO Bashneft ANK OAO (50.08% stake) The Federal Agency for State Property Management

5,929

14-Dec-16 P Caisse des Depots et Consignations; and CNP Assurances SA

Réseau de Transport d'Electricité (49.9% stake) Electricite de France SA 4,092

19-May-16 C FMC Technologies Inc Technip SA 4,060

12-Sep-16 C Global Infrastructure Partners Gas Natural Fenosa (20% stake) Repsol SA; and Criteria Caixa SAU 3,803

28-Oct-16 C Rosneft Oil Company OAO Bashneft ANK OAO (31.2% stake) 2,849

29-Jun-16 P Snam SpA (Shareholders) Italgas SpA (86.5% stake) Snam SpA 2,836

30-Nov-16 C E.ON SE (Shareholders) Uniper SE (53.35% Stake) E.ON SE 1,955

17-Oct-16 C EP Investment SARL; and EP Investment 2 SARL Energeticky a Prumyslovy Holding AS (35% stake) Milees Limited 1,862

15-Jul-16 P Gazprom PJSC Gazprom PJSC (3.59% stake) Vnesheconombank 1,728

13-Jun-16 C China Three Gorges Corporation WindMW GmbH (80% stake) Blackstone Energy Partners LP 1,700

17-Oct-16 P Energeticky a Prumyslovy Holding AS Energeticky a Prumyslovy Holding AS (30% stake) Biques Limited; EP Investment SARL; and Milees Limited

1,500

17-Oct-16 P Consortium of investors led by Macquarie Group Limited

EP Infrastructure AS (30% stake) Energeticky a Prumyslovy Holding AS 1,500

04-Feb-16 C Beijing Enterprises Holdings Limited EEW Energy from Waste GmbH EQT Partners AB 1,438

C = Completed; P = Pending; L = Lapsed

Quarter endedQuarter ended

24

DEAL DRIVERS – EMEA - ENERGY, MINING & UTILITIES

ENERGY, MINING & UTILITIESMIX OF DEALS BY GEOGRAPHIC REGION

VALUE VOLUME

UK & Ireland

German speaking

France

Italy

Iberia

Benelux

Nordic

Central & Eastern Europe

Other

QUARTERLY TRENDS

VALUE VOLUME

Based on announced deals, excluding those that lapsed or were withdrawn. Geographic region is determined with reference to the dominant location of the target.

Based on announced deals, excluding those that lapsed or were withdrawn, where the dominant location of the target is in Europe.Industry sector is based on the dominant industry of the target.

Valu

e (€

m)

Volu

me

0

20

40

60

80

100

120

140

Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

2010 2011 2012 2013 2014 2015 2016

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

2010 2011 2012 2013 2014 2015 2016

19.2%

11.6%

8.3%

10.9%9.3%

4.8%

14.3%

18.5%

3.1%

23.6%

7.0%

11.6%

6.1%8.0%0.7%

4.9%

37.4%

0.7%

Moving average trend line

25

DEAL DRIVERS – EMEA - ENERGY, MINING & UTILITIES

ENERGY, MINING & UTILITIESFINANCIAL ADVISERS

TOP 20 – RANKED BY VALUE TOP 20 – RANKED BY VOLUME

LEGAL ADVISERS

TOP 20 – RANKED BY VALUE TOP 20 – RANKED BY VOLUME

2016 2015 Company Name Value (€m)

Number of Deals

1 3 Bank of America Merrill Lynch 30,301 11

2 2 Morgan Stanley 22,702 10

3 15 VTB Capital 20,901 8

4 33 RBC Capital Markets 20,659 13

5 24 Macquarie Group 17,124 9

6 13 Barclays 16,718 7

7 4 Goldman Sachs 15,958 11

8 7 Citi 14,977 16

9 6 Robey Warshaw 13,428 1

10 5 Rothschild 12,417 24

11= - Arpwood Capital 11,490 2

11= - JM Financial 11,490 2

13 1 Lazard 9,626 16

14 31 Societe Generale 9,113 5

15 8 Deutsche Bank 8,855 7

16 50 UBS Investment Bank 8,750 5

17 17 BNP Paribas 8,314 14

18 20 Evercore Partners 6,774 7

19 22 Santander Global Corporate Banking 6,044 8

20 - Sberbank 5,929 1

2016 2015 Company Name Value (€m)

Number of Deals

1 14 Linklaters 40,232 31

2 17 White & Case 22,613 25

3 23 Clifford Chance 19,244 28

4 6 Freshfields Bruckhaus Deringer 17,896 13

5 37 CMS 16,081 25

6 165 Eversheds 15,180 11

7 64 Baker & McKenzie 14,760 9

8= 140 AZB & Partners 11,490 2

8= 132 Cyril Amarchand Mangaldas 11,490 2

10 29 Latham & Watkins 10,840 10

11 - Cleary Gottlieb Steen & Hamilton 10,508 5

12 - Darrois Villey Maillot Brochier 8,441 3

13 - Talwar Thakore & Associates 6,573 3

14 1 Herbert Smith Freehills 5,903 16

15 30 Garrigues 5,130 5

16 24 Skadden Arps Slate Meagher & Flom 4,914 6

17 48 Weil Gotshal & Manges 4,749 5

18 26 Sullivan & Cromwell 4,561 3

19 15 Norton Rose Fulbright 4,542 25

20 31 Uria Menendez 4,171 8

2016 2015 Company Name Value (€m)

Number of Deals

1 5 Rothschild 12,417 24

2 4 KPMG 1,875 20

3 2 Citi 14,977 16

4 9 Lazard 9,626 16

5 3 BNP Paribas 8,314 14

6 1 EY 604 14

7 18 RBC Capital Markets 20,659 13

8 8 PwC 667 13

9 14 Bank of America Merrill Lynch 30,301 11

10 10 Goldman Sachs 15,958 11

11 6 Morgan Stanley 22,702 10

12 7 Macquarie Group 17,124 9

13 11 UniCredit Group 3,805 9

14 25 VTB Capital 20,901 8

15 26 Santander Global Corporate Banking 6,044 8

16 16 Credit Suisse 5,673 8

17 17 Barclays 16,718 7

18 15 Deutsche Bank 8,855 7

19 20 Evercore Partners 6,774 7

20 12 JPMorgan 5,193 6

2016 2015 Company Name Value (€m)

Number of Deals

1 5 Linklaters 40,232 31

2 1 Clifford Chance 19,244 28

3 11 White & Case 22,613 25

4 3 CMS 16,081 25

5 2 Norton Rose Fulbright 4,542 25

6 40 Orrick Herrington & Sutcliffe 3,989 18

7 4 Allen & Overy 3,000 18

8 7 Herbert Smith Freehills 5,903 16

9 9 DLA Piper 1,145 15

10 19 Freshfields Bruckhaus Deringer 17,896 13

11 16 Watson, Farley & Williams 2,037 13

12 8 Hogan Lovells International 2,746 12

13 18 Eversheds 15,180 11

14 33 Latham & Watkins 10,840 10

15 35 Dentons 2,366 10

16 10 Baker & McKenzie 14,760 9

17 41 BA-HR 1,713 9

18 22 Thommessen 1,400 9

19 15 Cuatrecasas 269 9

20 20 Uria Menendez 4,171 8

The financial adviser league tables by value and volume have been run from 01/01/2016 to 31/12/2016, excluding lapsed and withdrawn deals. The tables are pan-European and are based on the following sectors: Energy, Mining and Utilities.

The legal adviser league tables by value and volume have been run from 01/01/2016 to 31/12/2016 and include lapsed and withdrawn deals.The tables are pan-European and are based on the following sectors: Energy, Mining and Utilities.

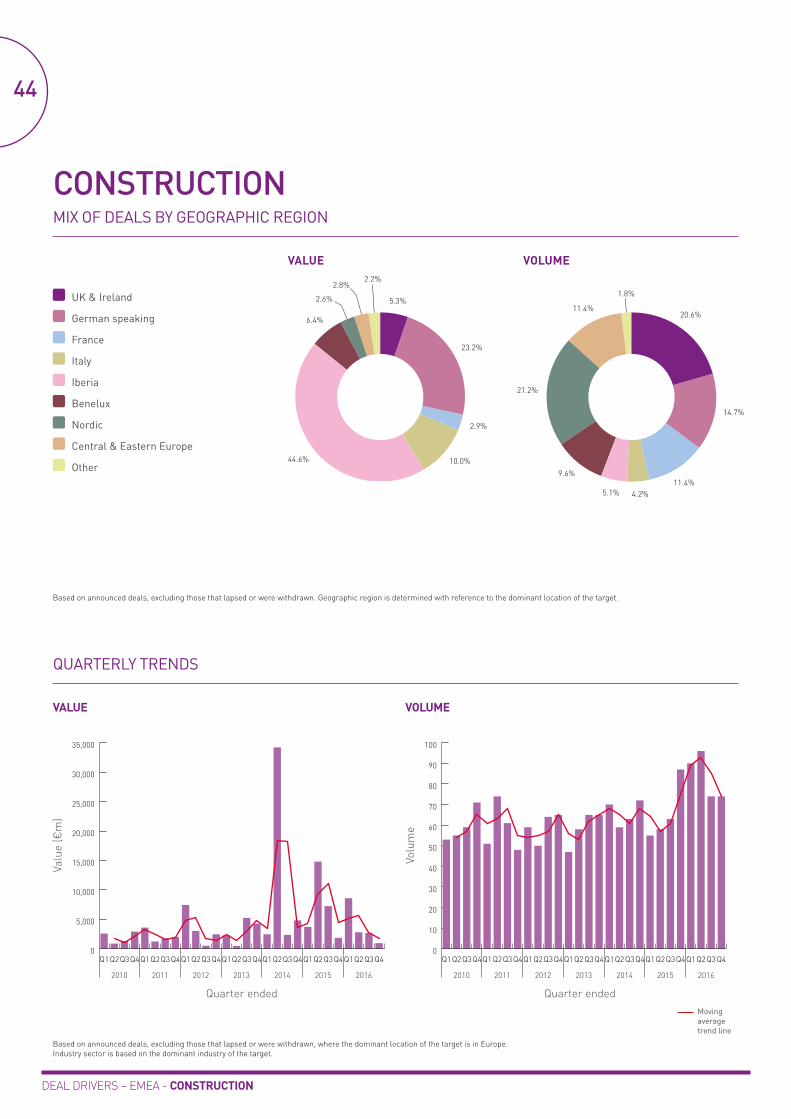

DEAL DRIVERS – EMEA - CONSUMER

26

CONSUMEROVERVIEW

While in 2015 European consumer and retail M&A activity was characterised by a series of mega deals, 2016 gave way to a more balanced environment dominated by post-deal disposals, increased levels of tactical M&A and more reasonable valuations, particularly for higher-risk deals. Macroeconomic uncertainty surrounding Brexit, alongside tightening credit markets, impacted activity but as yet there has been no strong indication of a long-term downturn in M&A levels. Deals have continued, albeit more focused on the small to mid-market.

The last quarter of the year registered the highest deal value, reaching €16.6bn, but this was still a far cry from the impressive €124.7bn registered in Q4 2015 thanks to the €114.5bn 'megabrew' merger between AB InBev and SABMiller. Still, Q4 2016 was a substantial improvement from Q3 2016, which registered €5.1bn in deal value, the lowest recorded since Q3 2009, when activity reached a mere €4.2bn.

Total deal value for the year stood at €40.6bn across 974 deals. Volume was similar to the 982 registered in 2015 and slightly above the 941 of 2014.

Only one consumer transaction made it to the top 20 largest deals of the year – the Asahi Group’s takeover of Anheuser-Busch InBev’s Eastern European assets, for €7.3bn. This compares to the three deals included in 2015’s equivalent list. Moreover, the Asahi deal would not have even broken into 2015’s top 20 largest deals, such has been the shift in M&A values.

Asahi’s deal was, however, the most expensive transaction the Japanese company has completed so far. Asahi also played a part in the second-largest consumer deal last year having acquired a package of beer brands in Western Europe from SABMiller. The disposals were needed to secure competition regulators’ approval for the megabrew.

Activity in the retail space was particularly strong in the UK, despite the initial panic in the immediate aftermath of the result of the EU referendum and the expectations

for a decline in consumer spending and high-street metrics. The UK registered 71 retail deals for the whole year, behind France’s 91 deals. However, in value terms, the UK was well ahead seeing €4.3bn worth of deals take place, while France only recorded €918m. The retail segment in the European consumer sector, was the most prolific, with a total of 367 deals.

The largest retail deal of the year was French Groupe SEB’s takeover of German tableware and kitchenware supplier WMF for €1.6bn. A similar-sized deal was J Sainsbury's acquisition of UK-based Home Retail Group. Also in the UK, discount retailer Poundland, was acquired by Steinhoff International for €578m. The latter two deals are examples of how companies in the space continue to look at ways to diversify and reposition themselves in a challenging landscape characterised by changing consumer behaviours and fierce competition.

The foods segment continued to see relatively subdued levels of activity. There were 298 deals announced across Europe for the whole year, amounting to €5.75bn. The UK and Ireland together were the most active with 47 deals totalling €1.13bn. Relevant UK deals include the sale of potato chips manufacturer Tyrrells Group by Investcorp to US-based snack food group Amplify Snack Brands for €354m, the acquisition of a 50% stake in fresh food producer Bakkavor Group by Bakk AL Holdings for €215m, and the sale ofa 19.9% stake in Premier Foods to Nissin Foods Holdings of Japan for €131m.

Private equity activity bounced back, particularly in the second half of the year. Significant levels of dry powder on the back of successful fund closes in previous years and sponsors keen to deploy capital have driven activity. There have been a number of large disposals by PE houses, including KKR’s sale of WMF to SEB for €1.6bn; German lighting company SLV, which was sold to Ardian by Cinven for €800m; and Ardian’s exit from German fashion retailer Schustermann & Borenstein to Permira for €700m.