Embed Size (px)

Citation preview

D5.3 Roadmap v23

1

D5.3 Roadmap v23

Document Information

Contract Number 619788

Project Website www.rethinkbig-project.eu

Contractual Deadline Month 22 (Dec 2015)

Dissemination Level Public

Nature Report

Author RETHINK big Editorial Team: Gina Alioto, Christophe Avare, Paul Carpenter, Marcus Leich, Osman Unsal

Reviewer RETHINK big Editorial Team

Keywords See complete list of terms and abbreviations.

This project has received funding from the European Union’s Seventh Framework Programme for research, technological development and demonstration under grant agreement no 619788. This content of this document reflects only the author’s views; the Union is not

liable for any use that may be made of the information contained therein. 2016 RETHINK big Project. All rights reserved. www.rethinkbig-project.eu

D5.3 Roadmap v23

2

Change Log

Version Description of Change

v20 This is the first version sent to the European Commission.

v22 This version addresses anonymization concerns (from v20) as well as implements some additional Validation Interview feedback. All changes have been marked in gray.

v23 This version no longer shows the changes from the previous version marked in gray.

D5.3 Roadmap v23

3

Table of Contents

Terms and Abbreviations ........................... ................................................... 5

Introduction ...................................... ....................................................... 6 11.1 Objectives ......................................................................................................................6 1.2 Target audience and scope ............................................................................................6

1.2.1 Big Data within the context of this document ...........................................................6 1.2.2 The EC Public Private Partnership for Big Data and beyond ...................................7

1.3 Process ..........................................................................................................................8 1.4 Document organization .................................................................................................9

Roadmap at-a-glance................................ ............................................ 10 22.1 Industry key findings ...................................................................................................10 2.2 High level action summary ..........................................................................................11

Network: Beyond the backbone, edging out the compet ition .......... 13 33.1 Scope of network architecture .....................................................................................13 3.2 Where we are today: Market trends and main actors .................................................13

3.2.1 Network appliance hardware: from specialized to bare metal ................................13 3.2.2 From hardware to “softwarization” and virtualization ............................................14

3.2.3 Deconstructing the data center (beyond +400GE) ..................................................15 3.3 Where we want to be ...................................................................................................17

3.3.1 Industry pains and expected gains ...........................................................................17 3.3.2 Key findings ............................................................................................................20

3.4 How we are going to get there ....................................................................................20 3.4.1 TRL > 5: Accelerating adoption of current technologies ........................................20 3.4.2 TRL 3 - 5: Preparing the next generation ................................................................22 3.4.3 TRL < 3: Anticipating future challenges ................................................................24

Architecture: Accelerating compute for machine lear ning for 4analytics ......................................... .............................................................. 26

4.1 Scope of compute node architecture ............................................................................26 4.2 Where we are today: Market trends and main actors .................................................27

4.2.1 The march toward heterogeneous systems ..............................................................27 4.2.2 Specialization and vendor lock-in ...........................................................................28 4.2.3 Integration inside the compute node .......................................................................29 4.2.4 Verticalization and hyperscalers .............................................................................30 4.2.5 Non-von Neumann ..................................................................................................31

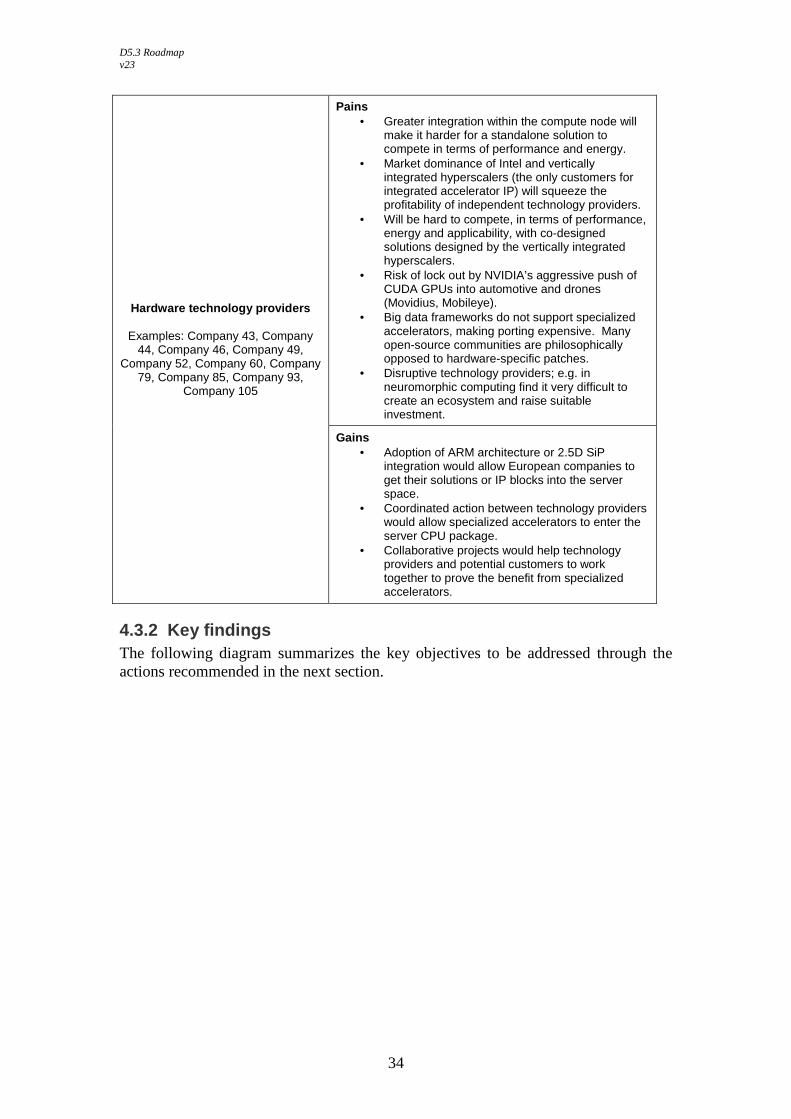

4.3 Where we want to be ...................................................................................................32 4.3.1 Industry pains and expected gains ...........................................................................32 4.3.2 Key findings ............................................................................................................34

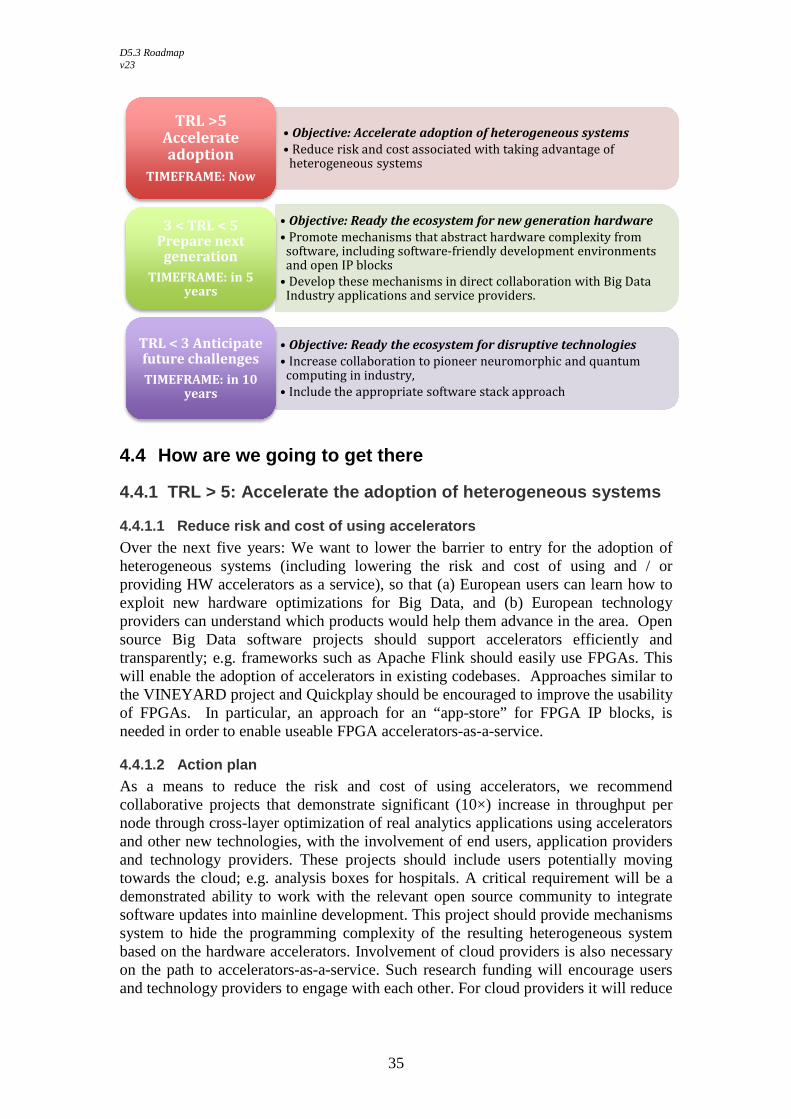

4.4 How are we going to get there ....................................................................................35 4.4.1 TRL > 5: Accelerate the adoption of heterogeneous systems .................................35

4.4.2 TRL 3 - 5: Preparing the next generation hardware ................................................36 4.4.3 TRL < 3: Anticipating future challenges ................................................................37

Software and beyond: Supporting hardware optimizati ons for Big 5Data ............................................................................................................... 39

5.1 Where we are today: Market trends and main actors .................................................40 5.1.1 Big Data processing: From query languages to frameworks ..................................40 5.1.2 March toward hardware dependence ......................................................................40

5.1.3 Too many hardware programming abstractions ......................................................40 5.1.4 Complex cloud service offerings: ML-as-a-Service and beyond ............................42

5.1.5 A lack of Big Data benchmarks ..............................................................................42

D5.3 Roadmap v23

4

5.2 Where we want to be ...................................................................................................42 5.2.1 Industry pains and expected gains ...........................................................................42 5.2.2 Key findings ............................................................................................................44

5.3 How we are going to get there ....................................................................................44 5.3.1 TRL > 5: Accelerating adoption of current technologies ........................................44 5.3.2 TRL 3 - 5: Preparing the next generation for adoption of new technologies ..........47 5.3.3 TRL < 3: Anticipating future challenges ................................................................48

Bibliography ...................................... .................................................... 49 6

D5.3 Roadmap v23

5

Terms and Abbreviations ADAS Advanced Driver Assistance System API Application Programmer Interface ASIC Application Specific Integrated Circuit Chiplet Individual die in a Silicon-in-Package (SiP) CMOS Complementary Metal Oxide Semiconductor CPU Central Processing Unit CUDA Compute Unified Device Architecture (Nvidia’s language for GPGPUs) DARPA (U.S.) Defense Advanced Research Agency DCI Data Center Interconnect DRAM Dynamic Random Access Memory DSP Digital Signal Processor DWDM Dense Wavelength Division Multiplexing EMIB Embedded Multi-die Interconnect Bridge FPGA Field Programmable Gate Array GPGPU General Purpose Graphics Processing Unit (compute-capable GPU) GPU Graphics Processing Unit HDL Hardware Description Language, e.g. VHDL or Verilog HLS High Level Synthesis (designing hardware using high-level programming languages) HPC High-Performance Computing IoT Internet of Things IP Intellectual Property / Internet Protocol LAN Large Area Network ML Machine Learning MPI Message Passing Interface NIC Network Interface Controller NFV Network Function Virtualization NLP Natural Language Processing NOS Network Operating System NRE Non-Recurring Engineering (cost) PCIe Peripheral Component Interconnect Express RDMA Remote Direct Memory Access ROI Return on Investment SaaS Software as a Service (e.g. Facebook, LinkedIn, Bluebee) SATA Serial Advanced Technology Attachment SDN Software Defined Network SIMD Single Instruction Multiple Data SIMT Single Instruction Multiple Thread SiP System-in-Package SoC System-on-Chip SME Small and Medium Enterprises SPARQL SPARQL Protocol and RDF Query Language SQL Standard Query Language TCO Total Cost of Ownership TPC Transaction Processing Performance Council TRL Technology Readiness Level USB Universal Serial Bus VHDL VHSIC Hardware Description Language VPS Virtual Private Server

D5.3 Roadmap v23

6

Introduction 1

1.1 Objectives The overarching objective of the RETHINK big Roadmap is to provide a set of coordinated technology development recommendations (focused on optimizations in networking and hardware) that would be in the best interest of European Big Data companies to undertake in concert as a matter of competitive advantage. As authors, we had the following objectives in mind when we started writing the document:

• Identify business opportunities from European industry stakeholders in the area of Big Data

• Predict the future technologies that will disrupt the state of the art in Big Data processing in terms of hardware and networking optimizations

• Identify a critical mass of European industry stakeholders that see a clear competitive advantage enabled by embracing specific future technologies

• Develop clear recommendations for the European Commission that ultimately facilitate timely European industry access to these future technologies via instruments that bring together the appropriate mix of technology providers, system integrators, Big Data analytics providers and academic research.

1.2 Target audience and scope This document is intended for the European Commission as a guide for promoting targeted industry / academic collaborations in future funding calls over the next 10 years. However, it is equally targeted at Big Data analytics and computer science professionals, students, and professors, as well as the public at large interested in technology and technology use. While we tried to be complete and exhaustive, it is inevitable that some technologies and aspects have been omitted. In most cases when a technology has been omitted, it is largely due to the lack of potential European competitive advantage which is the foundation of this document. A clear example of this type of omission is memory technology, a capital-intensive low margin industry in which there is currently no major European player.

1.2.1 Big Data within the context of this document In a 2014 article in Forbes [Pre14] technology “thought leader” Gil Press provides no fewer than twelve – yes, twelve! – definitions for the term Big Data. He begins with the classical Oxford English Dictionary definition (definition #1) “data of a very large size, typically to the extent that its manipulation and management present significant logistical challenges” but quickly moves on to the widely quoted 2011 McKinsey study definition of (#3) “datasets whose size is beyond the ability of typical database software tools to capture, store, manage, and analyze,” only to later settle on the more esoteric “A new attitude by businesses, non-profits, government agencies, and individuals that combining data from multiple sources could lead to better decisions.” Even world renowned American linguist and adjunct professor at the U.C. Berkeley School of Information, Geoffrey Nunberg (and champion of Big Data for his own research) in his 2012 push to make Big Data “word of the year” [Nun12] concedes that Big Data is “no more exact a notion than Big Hair… The fact is that an exponential curve looks just as overwhelming wherever you get onboard… After all,

D5.3 Roadmap v23

7

digital data has been accumulating for decades in quantities that always seemed unimaginably vast at the time.” He then concludes that it’s not the amount of data that makes Big Data but rather “…the way data is generated and processed… It's only when all those little chunks are aggregated that they turn into Big Data.” Stack Overflow believes the definition of Big Data is a matter of opinion with endless scope: “If you can imagine an entire book that answers your question, you’re asking too much.” [STA16] while Quora users posted more than 100 definitions, most of them lengthy. Despite the philosophical discussions that this topic seems to incite, there seems to be a general recognition that the proof is in the processing, meaning that what makes it BIG data is the fact that the standard and traditional methods and architectures are not enough to process (and store) the data within a reasonable timeframe. For the purposes of this roadmap, we will assume that Big Data is precisely that, Big enough to cause undesirable processing bottlenecks be them at the chip, node or network level.

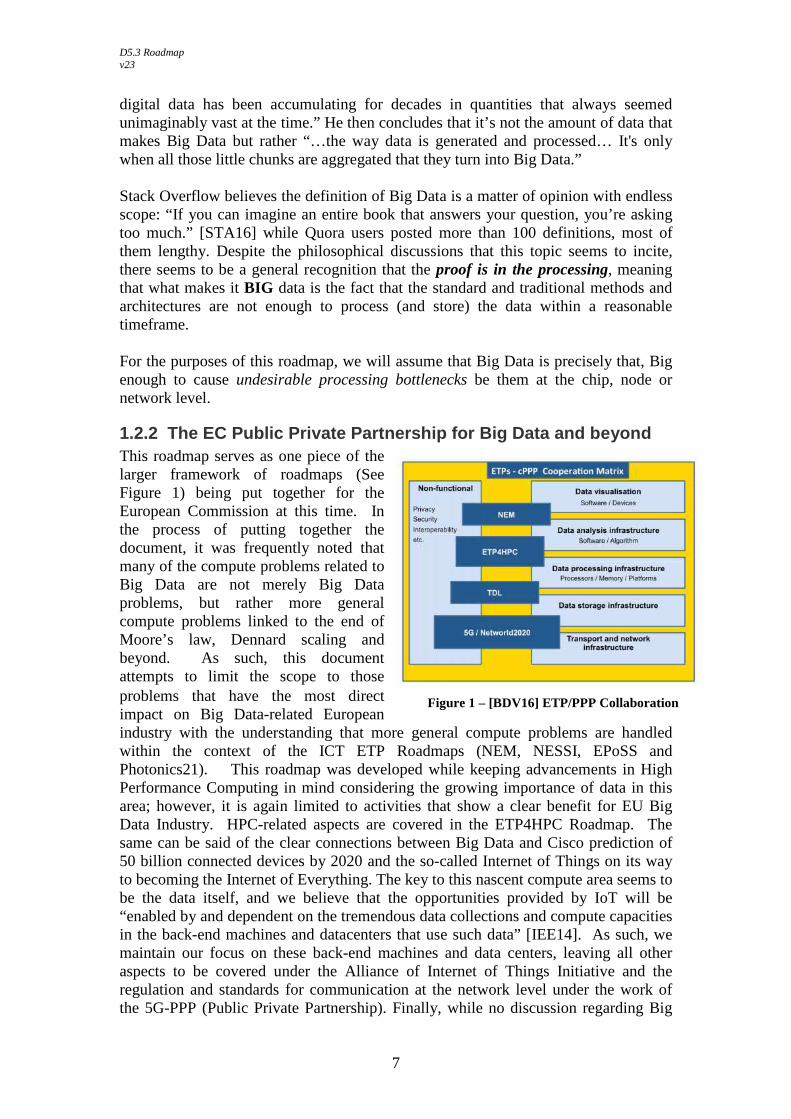

1.2.2 The EC Public Private Partnership for Big Dat a and beyond This roadmap serves as one piece of the larger framework of roadmaps (See Figure 1) being put together for the European Commission at this time. In the process of putting together the document, it was frequently noted that many of the compute problems related to Big Data are not merely Big Data problems, but rather more general compute problems linked to the end of Moore’s law, Dennard scaling and beyond. As such, this document attempts to limit the scope to those problems that have the most direct impact on Big Data-related European industry with the understanding that more general compute problems are handled within the context of the ICT ETP Roadmaps (NEM, NESSI, EPoSS and Photonics21). This roadmap was developed while keeping advancements in High Performance Computing in mind considering the growing importance of data in this area; however, it is again limited to activities that show a clear benefit for EU Big Data Industry. HPC-related aspects are covered in the ETP4HPC Roadmap. The same can be said of the clear connections between Big Data and Cisco prediction of 50 billion connected devices by 2020 and the so-called Internet of Things on its way to becoming the Internet of Everything. The key to this nascent compute area seems to be the data itself, and we believe that the opportunities provided by IoT will be “enabled by and dependent on the tremendous data collections and compute capacities in the back-end machines and datacenters that use such data” [IEE14]. As such, we maintain our focus on these back-end machines and data centers, leaving all other aspects to be covered under the Alliance of Internet of Things Initiative and the regulation and standards for communication at the network level under the work of the 5G-PPP (Public Private Partnership). Finally, while no discussion regarding Big

Figure 1 – [BDV16] ETP/PPP Collaboration

D5.3 Roadmap v23

8

Data is complete without a detailed discussion of Software, it is important to understand that the treatment of Software in this document is limited to lower level system software that supports hardware and networking optimizations for Big Data. We leave the more detailed discussion of the Big Data analytics applications and the data itself to the roadmap of the Big Data Value Association.

1.3 Process This document is the direct outcome of a 2-year project (RETHINK big) funded by the European Commission. During the first year of the project a core team of ten technologists met once in person as well as monthly by phone in preparation for a face-to-face expert workshop held in Madrid. The workshop aimed to bring together representatives from both industry applications and technology domains to establish a common vocabulary and an understanding of Big Data business barriers. The team also conducted a detailed technical survey prior to the event in order to set the discussion topics. Through these two methods, we were able to identify a comprehensive list of largely industry-related Big Data problems; however, we did not have enough information from the individual companies to understand how each respective problem generated a specific business need nor did we posit the potential business benefit that could be achieved by solving each problem. We focused on remedying the fact that we had not gathered sufficient information from industry during the second year of the project. We began by developing a set of Initial Company Interview Questions, tailoring our questions to both Software

Applications and Services providers and to Technology providers while at the same time focusing on the business plan of each specific company. We began each interview by asking the interviewee to explain their product and / or service offering and then would characterize the company in terms of their product type and business model. Next, we focused directly on each

company’s own roadmap by asking whether or not each

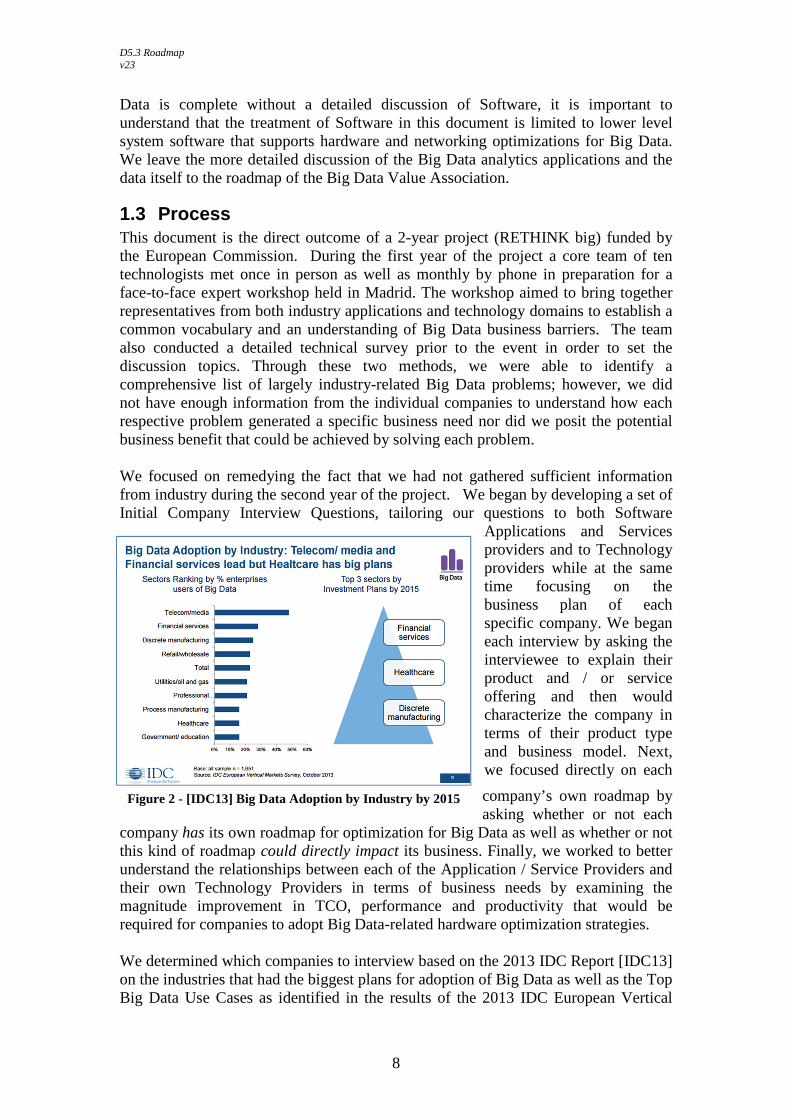

company has its own roadmap for optimization for Big Data as well as whether or not this kind of roadmap could directly impact its business. Finally, we worked to better understand the relationships between each of the Application / Service Providers and their own Technology Providers in terms of business needs by examining the magnitude improvement in TCO, performance and productivity that would be required for companies to adopt Big Data-related hardware optimization strategies. We determined which companies to interview based on the 2013 IDC Report [IDC13] on the industries that had the biggest plans for adoption of Big Data as well as the Top Big Data Use Cases as identified in the results of the 2013 IDC European Vertical

Figure 2 - [IDC13] Big Data Adoption by Industry by 2015

D5.3 Roadmap v23

9

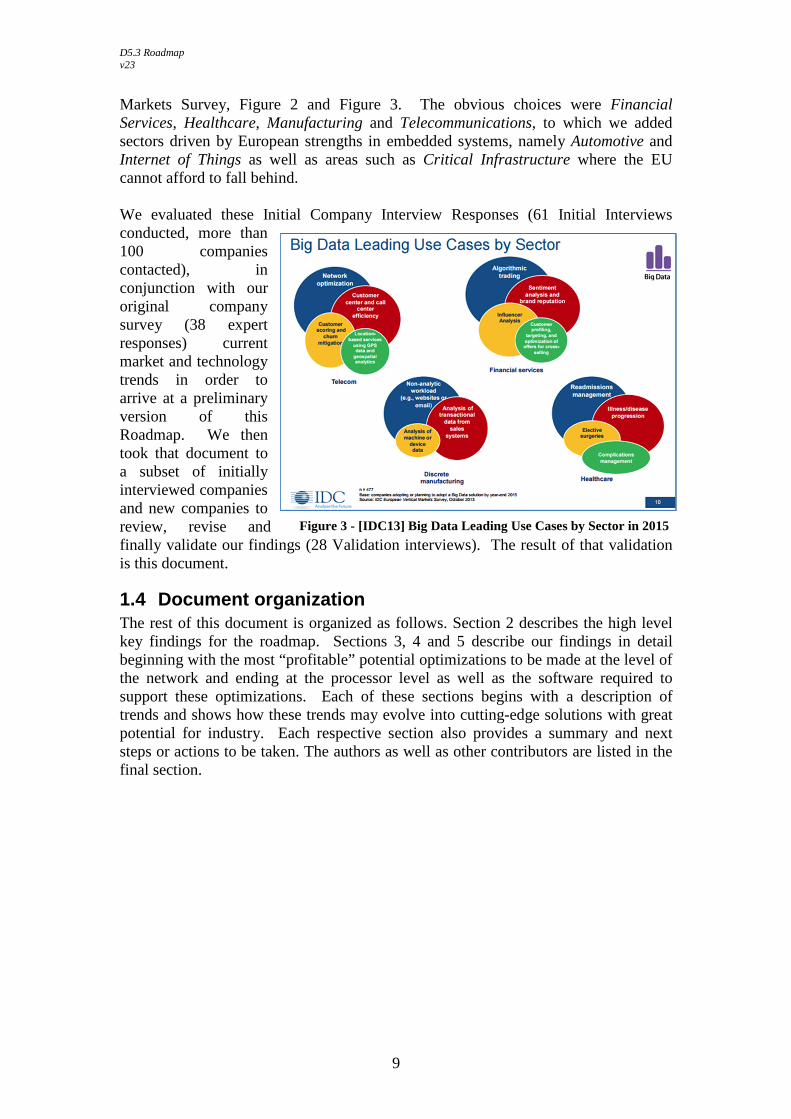

Markets Survey, Figure 2 and Figure 3. The obvious choices were Financial Services, Healthcare, Manufacturing and Telecommunications, to which we added sectors driven by European strengths in embedded systems, namely Automotive and Internet of Things as well as areas such as Critical Infrastructure where the EU cannot afford to fall behind. We evaluated these Initial Company Interview Responses (61 Initial Interviews conducted, more than 100 companies contacted), in conjunction with our original company survey (38 expert responses) current market and technology trends in order to arrive at a preliminary version of this Roadmap. We then took that document to a subset of initially interviewed companies and new companies to review, revise and finally validate our findings (28 Validation interviews). The result of that validation is this document.

1.4 Document organization The rest of this document is organized as follows. Section 2 describes the high level key findings for the roadmap. Sections 3, 4 and 5 describe our findings in detail beginning with the most “profitable” potential optimizations to be made at the level of the network and ending at the processor level as well as the software required to support these optimizations. Each of these sections begins with a description of trends and shows how these trends may evolve into cutting-edge solutions with great potential for industry. Each respective section also provides a summary and next steps or actions to be taken. The authors as well as other contributors are listed in the final section.

Figure 3 - [IDC13] Big Data Leading Use Cases by Sector in 2015

D5.3 Roadmap v23

10

Roadmap at-a-glance 2In this section, we first summarize the key findings based on the collective response from our interviews and surveys. Additionally, we introduce the high level actions that will be presented in detail in later sections of the document.

2.1 Industry key findings (1) Industry is still focused on finding how to extract value from their data, and they are also still looking for the right business model to turn this value into profit. Consequently, they are not focused on processing (and storage) bottlenecks, let alone on the underlying hardware. As we mentioned in the previous section, we were in touch via interview or survey with more than 100 companies across a broad spectrum of Big Data-related Industries including major and up-and-coming players from telecommunications, hardware design and manufacturers as well as a strong representation from health, automotive, financial and analytics sectors. The overwhelming response is that Industry does not see Big Data problems, only Big Data opportunities. We believe that this is largely the case because the industry is not yet mature enough for most companies to be trying to do that kind of analytics and all-encompassing Big Data processing that leads to undesirable bottlenecks. (2) European companies are not convinced of the Return on Investment of using novel architectures. First, it is important to note that all of the analytics companies with which we spoke were extremely price-sensitive. Moreover, they are content to use the currently available hardware as long as they continue to receive the most competitive pricing. All of this coupled with the fact that there is no clean metric or benchmark for side-by-side comparisons for heterogeneous architectures, the majority of the companies were not convinced that the investment in expensive hardware coupled with the person months required to make their products work with new hardware were worthwhile. (3) Europe is at a strong disadvantage with respect to hardware / software co-design. The European ecosystem is highly fragmented while media and internet giants such as Google, Amazon, Facebook, Twitter and Apple and others (also known as hyperscalers) are pursuing verticalization and designing their own infrastructures from the ground up. European companies that are not closely considering hardware and networking technologies as a means to cutting cost and offering better future services run the risk of falling further and further behind. Hyperscalers will continue to take risks and transform themselves because they are the “ecosystem”, moving everybody else in their trail. (4) Dominance of non-European companies in the server market complicates the possibility of new European entrants in the area of specialized architectures. Intel is currently the gatekeeper for new Data Center architectures; moreover, Intel is spearheading the effort to increase integration into the CPU package which can only exacerbate this problem.

D5.3 Roadmap v23

11

Consolidation among DRAM manufacturers has reduced the worldwide number of DRAM suppliers to three: Samsung, SK Hynix and Micron. It is unrealistic for Europe to enter the DRAM industry. Without the right support, the best outcome for any European hardware provider will be that it is acquired by a non-European company, so the IP leaves Europe.

2.2 High level action summary Promote adoption of current and upcoming networking standards Europe should accelerate the adoption of the current and upcoming standards (10 and 40Gb Ethernet) based on low-power consumption components proposed by European Companies and connect these companies to end users and data-center operators so that they can demonstrate their value compared to the bigger players. Prepare for the next generation of hardware and take advantage of the convergence of HPC and Big Data interests In particular, Europe must take advantage of its strengths in HPC and embedded systems by encouraging dual-purpose products that bring these different communities together (e.g. HPC / Big Data hardware that can be differentiated in SW). This would allow new companies to sell to a bigger market and decrease the risk associated with development of new product. Anticipate the changes in Data Center design for 400Gb Ethernet networks (and beyond) This includes paying special attention to photonics-on-silicon integration and novel Data Center interconnect designs. Reduce risk and cost of using accelerators Europe must lower the barrier to entry of heterogeneous systems and accelerators; collaborative projects should bring together end users, application providers and technology providers to demonstrate significant (10x) increase in throughput per node on real analytics applications. Encourage system co-design for new technologies Europe must bring together end users, application providers, system integrators and technology providers to build balanced system architectures based on silicon-in-package integration of new technologies, I/O interfaces and memory interfaces, driven by the evolving needs of big data. Improve programmability of FPGAs Europe should also fund research projects involving providers of tools, abstractions and high-level programming languages for FPGAs or other accelerators with the aim of demonstrating the effectiveness of this approach using real applications. Europe should also encourage a new entrant into the FPGA industry. Pioneer markets for neuromorphic computing and increase collaboration For neuromorphic computing and other disruptive technologies, the principal issue is the lack of a market ecosystem, with insufficient appetite for risk and few European companies with the size and clout to invest in such a risky direction. Europe should encourage collaborative research projects that bring together actors across the whole

D5.3 Roadmap v23

12

chain: end users, application providers and technology providers to demonstrate real value from neuromorphic computing in real applications. Create a sustainable business environment including access to training data Europe should address access to training data by encouraging the collection of open anonymized training data and encouraging the sharing of anonymized training data inside EC-funded projects. To address the lack of information sharing, Europe should encourage interaction between hardware providers and Big Data companies using the network-of-excellence instrument or similar. Establish standard benchmarks It is difficult for Industry to assess the benefits of using novel hardware. We propose establishing benchmarks to compare current and novel architectures using Big Data applications. Identify and build accelerated building blocks We propose to identify often-required functional building blocks in existing processing frameworks and to replace these blocks with (partially) hardware-accelerated implementations. Investigate intelligent use of heterogeneous resources With edge computing and cloud computing environments calling for heterogeneous hardware platforms, we propose the creation of dynamic scheduling and resource allocation strategies. Continue to ask the question – Do companies think that hardware and networking optimizations for Big Data can solve the majority of their problems? As more and more companies learn how to extract value from Big Data as well as determine which business models lead to profits, the number of service offerings and products based on Big Data analytics will grow sharply. This growth will likely lead to an increase in consumer expectations with respect to these Big Data-driven products and services, and we expect companies to run into more and more undesirable performance bottlenecks that will require optimized hardware.

D5.3 Roadmap v23

13

Network: Beyond the backbone, edging out 3the competition

3.1 Scope of network architecture The network is the most pervasive element of any modern technology-based business, and network optimizations targeted at Big Data could profoundly affect those businesses focused on analytics and beyond. However, these optimizations may not be as straightforward as the employment of accelerators for a specific Big Data workload due to emerging trends in “softwarization” and virtualization of conventional networking appliances. As such, we will explain the potential of optimizations for Big Data with innovative technologies applied to these appliances - specifically routers and switches - as related to this virtualization, and from there explore advancements in the area of interconnects, new materials and beyond. Our analysis will consider network requirements for executing Big Data workloads, be they inside a large public cloud, a private corporate data center or even in a future high performance / Big Data embedded system. We will examine these requirements from the perspective of the “data receiving end”, meaning that we will initially limit our scope to the network communication inside of the Data Center. As a result, we will only consider the nascent IoT sensors market, the Internet or mobile infrastructure challenges faced by the global telecom networks, and the actual access to the data by businesses (including regulatory & privacy concerns) from this perspective. After a brief survey of the market and current trends, we define several industry user profiles and summarize their respective concerns and requirements related to Big Data as gathered through our interviews and other publicly available information sources such as product roadmaps, published papers and international conferences. Additionally, for each profile, we describe the potential impact to overcoming the previously mentioned concerns via action. The roadmap proposals for networking are the result of this analysis.

3.2 Where we are today: Market trends and main actors The “network” consists of multiple functions embedded at different layers spread across many physical devices ranging from the server motherboard and interface peripherals to the top of rack switches, routers and the operator infrastructure. Until now, the networking hardware lifecycle has been driven by the quest for increasing bandwidth. But today’s market landscape is rapidly changing under the pressure of demand coming from Big Data, mobile phones and IoT combined requirements.

3.2.1 Network appliance hardware: from specialized to bare metal To get a sense of what this business globally represents, we can look at the router and switch market as a proxy indicator for the leading companies. In 2016, the switch market is forecast to reach $26 billion [Del15a] driven by large data center deployments. The interesting shift is that while the majority of revenue is for 10GE, the 40-100GE is forecast to top $3 billion by 2016, with 100GE adoption by major players as early as 2015 [Del15b].

D5.3 Roadmap v23

14

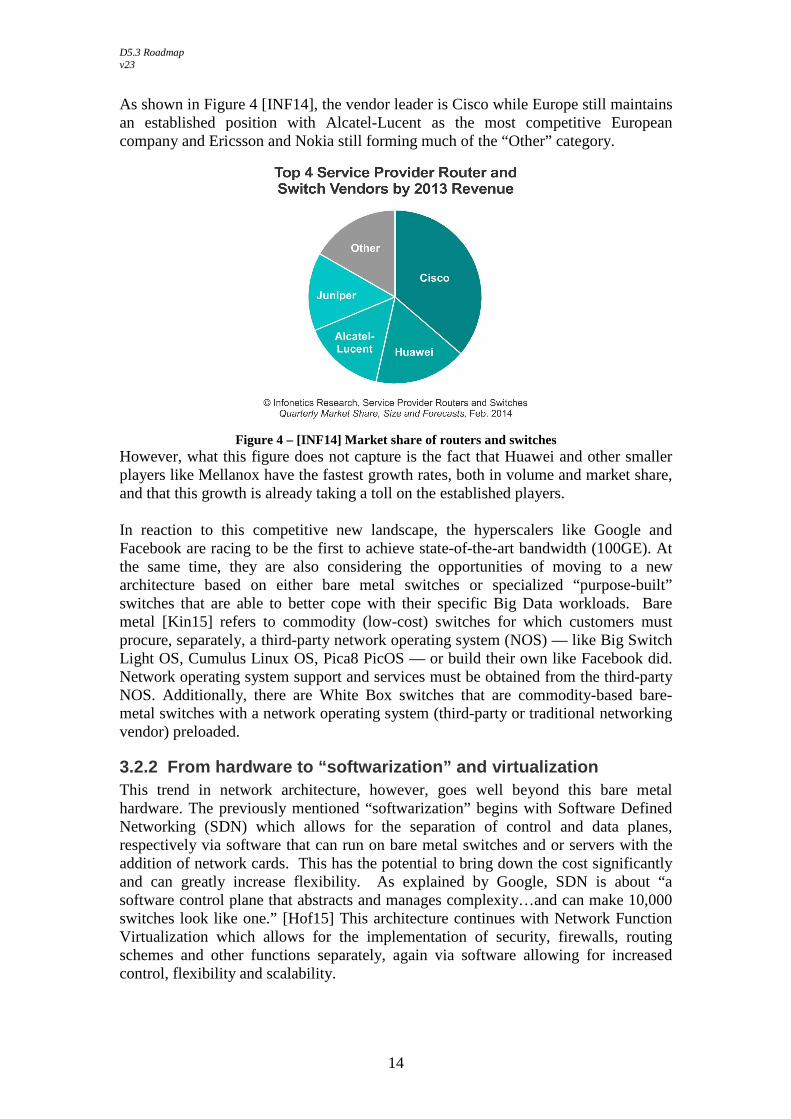

As shown in Figure 4 [INF14], the vendor leader is Cisco while Europe still maintains an established position with Alcatel-Lucent as the most competitive European company and Ericsson and Nokia still forming much of the “Other” category.

Figure 4 – [INF14] Market share of routers and switches

However, what this figure does not capture is the fact that Huawei and other smaller players like Mellanox have the fastest growth rates, both in volume and market share, and that this growth is already taking a toll on the established players. In reaction to this competitive new landscape, the hyperscalers like Google and Facebook are racing to be the first to achieve state-of-the-art bandwidth (100GE). At the same time, they are also considering the opportunities of moving to a new architecture based on either bare metal switches or specialized “purpose-built” switches that are able to better cope with their specific Big Data workloads. Bare metal [Kin15] refers to commodity (low-cost) switches for which customers must procure, separately, a third-party network operating system (NOS) — like Big Switch Light OS, Cumulus Linux OS, Pica8 PicOS — or build their own like Facebook did. Network operating system support and services must be obtained from the third-party NOS. Additionally, there are White Box switches that are commodity-based bare-metal switches with a network operating system (third-party or traditional networking vendor) preloaded.

3.2.2 From hardware to “softwarization” and virtual ization This trend in network architecture, however, goes well beyond this bare metal hardware. The previously mentioned “softwarization” begins with Software Defined Networking (SDN) which allows for the separation of control and data planes, respectively via software that can run on bare metal switches and or servers with the addition of network cards. This has the potential to bring down the cost significantly and can greatly increase flexibility. As explained by Google, SDN is about “a software control plane that abstracts and manages complexity…and can make 10,000 switches look like one.” [Hof15] This architecture continues with Network Function Virtualization which allows for the implementation of security, firewalls, routing schemes and other functions separately, again via software allowing for increased control, flexibility and scalability.

D5.3 Roadmap v23

15

The importance of the link between the evolving hardware (bare metal Ethernet switches) market and “softwarization” of the network (via SDN and NFV) becomes more evident when examining recent Ethernet switch forecast analysis Figure 5 [IHS15] which predicts that the bare metal and purpose-built switch market will grow, while the general-purpose market will shrink over the next four years. This shift could pose a real threat to those established vendors that are not willing to adapt.

Figure 5 – [IHS15] Forecast analysis of Ethernet switch ports

If bare metal switches dominate future data center networks, the question of differentiation among vendors will focus on switch performance, followed by the market for control plane open software where this new balance of forces will potentially create new ecosystems. We can see the initial possibilities for this general trend toward open hardware demonstrated by Facebook’s Open Compute initiative and the Open Networking Foundation’s OpenFlow. OpenFlow, as it relates to the White Box market, could be instrumental in taking the control out of the established vendors’ hands, a movement that may help companies like Arista and others to capture a sizable market share. This change will not happen all at once, though. Enterprise LAN and general purpose data centers, which often have industry cycles of 5 to 10 years for IT infrastructure, will most definitely show a slower rate of adoption for these bare metal Ethernet switches.

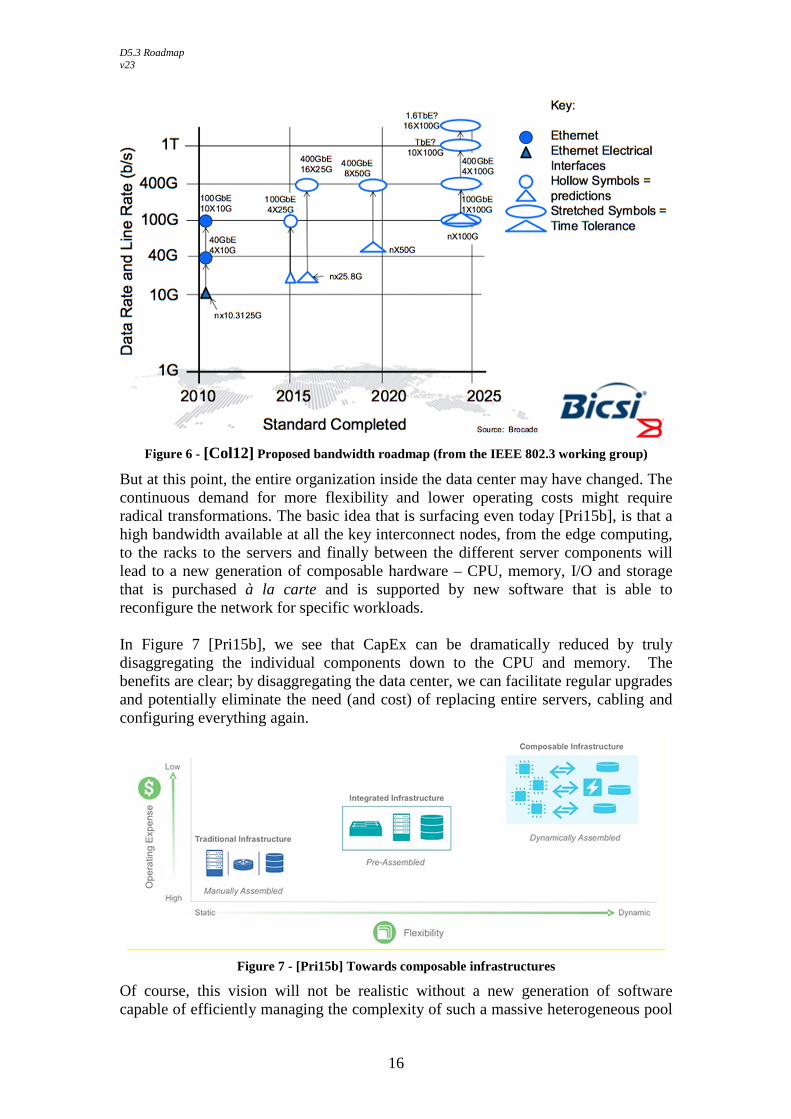

3.2.3 Deconstructing the data center (beyond +400GE ) If the industry roadmap described in Figure 6 [Col12] is respected, high-end (beyond 400GE) network appliances should be available after 2020.

D5.3 Roadmap v23

16

Figure 6 - [Col12] Proposed bandwidth roadmap (from the IEEE 802.3 working group)

But at this point, the entire organization inside the data center may have changed. The continuous demand for more flexibility and lower operating costs might require radical transformations. The basic idea that is surfacing even today [Pri15b], is that a high bandwidth available at all the key interconnect nodes, from the edge computing, to the racks to the servers and finally between the different server components will lead to a new generation of composable hardware – CPU, memory, I/O and storage that is purchased à la carte and is supported by new software that is able to reconfigure the network for specific workloads. In Figure 7 [Pri15b], we see that CapEx can be dramatically reduced by truly disaggregating the individual components down to the CPU and memory. The benefits are clear; by disaggregating the data center, we can facilitate regular upgrades and potentially eliminate the need (and cost) of replacing entire servers, cabling and configuring everything again.

Figure 7 - [Pri15b] Towards composable infrastructures

Of course, this vision will not be realistic without a new generation of software capable of efficiently managing the complexity of such a massive heterogeneous pool

D5.3 Roadmap v23

17

of resources – each resource potentially located anywhere in a data center. This could lead to interesting opportunities for SMEs, especially if we can help to reinforce the trend toward open hardware and networking and potentially move the ecosystem out the hands of the big vertical chip makers.

3.3 Where we want to be

3.3.1 Industry pains and expected gains In our survey, we have identified the following categories of industrial users for which we have found the corresponding major concerns. The information is conveniently captured in the following tables, and organized around two main areas:

• “Pains” identifies the root cause of the problem beyond the obvious ones (i.e. not enough revenue, too many taxes, …)

• “Gains” captures the concrete benefits that could be achieved if some of the current pains are removed.

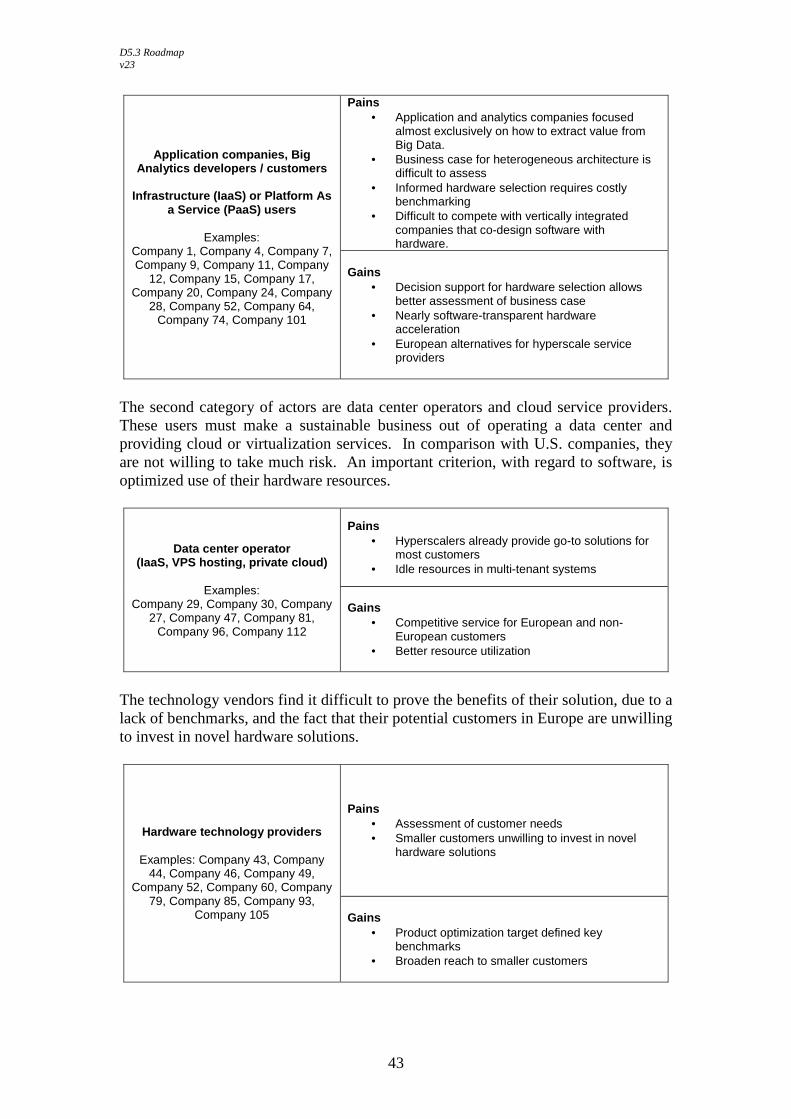

The information captured at this stage (with a focus on the network) is not always directly amenable to solutions, as some specific problems could also come from a wrong business model, regulatory constraints and so on. But it is important that any solution must at some point be connected to these pains and the impact will certainly be measured against the expected gains. The first category of users consists of those using Big Data infrastructure be it in the Cloud or on Premises. For this category, the network is both an enabler and a cost.

Big Analytics developers / customers

Infrastructure (IaaS) or Platform As

a Service (PaaS) users

Examples: Company 1, Company 4, Company 7, Company 9, Company 11, Company

12, Company 15, Company 17, Company 20, Company 24, Company

28, Company 52, Company 64, Company 74, Company 101

Pains • Cost of using the network grows faster than

revenue generated from business • Lack of network control / flexibility compared to

application needs (semantic gap) • Complex architecture designs required to

compensate for lack of “reliability”

Gains • Lower latency means faster end-to-end

performance • Increase in available bandwidth can be

translated into better global efficiency for workloads that are I/O bound

• More power efficient datacenters will decrease overall TCO and possibly lead to better offerings for Users

• Low power devices also relevant for edge computing

The second user profile is focused on the “offer” side of the market. These users must make a sustainable business out of operating a data center and providing Cloud or Virtualization services. The spectrum is now quite large, both in size and offerings, but these users generally still share a common set of concerns with respect to the network.

D5.3 Roadmap v23

18

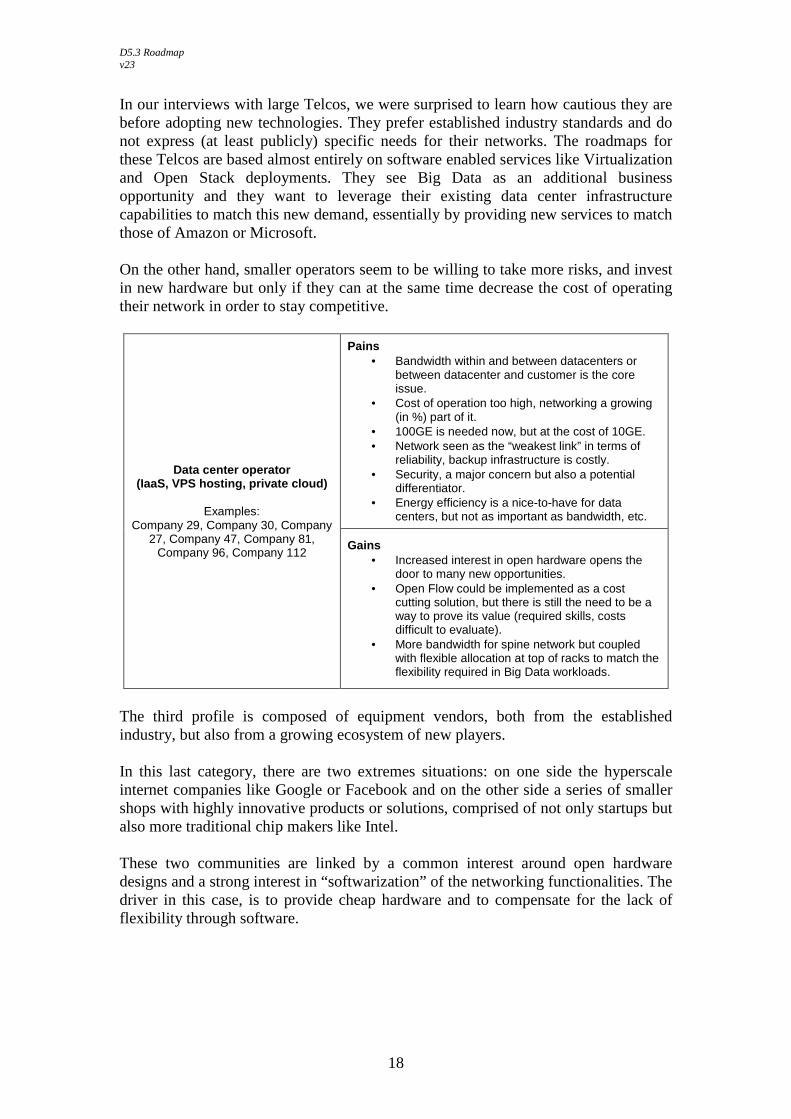

In our interviews with large Telcos, we were surprised to learn how cautious they are before adopting new technologies. They prefer established industry standards and do not express (at least publicly) specific needs for their networks. The roadmaps for these Telcos are based almost entirely on software enabled services like Virtualization and Open Stack deployments. They see Big Data as an additional business opportunity and they want to leverage their existing data center infrastructure capabilities to match this new demand, essentially by providing new services to match those of Amazon or Microsoft. On the other hand, smaller operators seem to be willing to take more risks, and invest in new hardware but only if they can at the same time decrease the cost of operating their network in order to stay competitive.

Data center operator (IaaS, VPS hosting, private cloud)

Examples:

Company 29, Company 30, Company 27, Company 47, Company 81,

Company 96, Company 112

Pains • Bandwidth within and between datacenters or

between datacenter and customer is the core issue.

• Cost of operation too high, networking a growing (in %) part of it.

• 100GE is needed now, but at the cost of 10GE. • Network seen as the “weakest link” in terms of

reliability, backup infrastructure is costly. • Security, a major concern but also a potential

differentiator. • Energy efficiency is a nice-to-have for data

centers, but not as important as bandwidth, etc.

Gains • Increased interest in open hardware opens the

door to many new opportunities. • Open Flow could be implemented as a cost

cutting solution, but there is still the need to be a way to prove its value (required skills, costs difficult to evaluate).

• More bandwidth for spine network but coupled with flexible allocation at top of racks to match the flexibility required in Big Data workloads.

The third profile is composed of equipment vendors, both from the established industry, but also from a growing ecosystem of new players. In this last category, there are two extremes situations: on one side the hyperscale internet companies like Google or Facebook and on the other side a series of smaller shops with highly innovative products or solutions, comprised of not only startups but also more traditional chip makers like Intel. These two communities are linked by a common interest around open hardware designs and a strong interest in “softwarization” of the networking functionalities. The driver in this case, is to provide cheap hardware and to compensate for the lack of flexibility through software.

D5.3 Roadmap v23

19

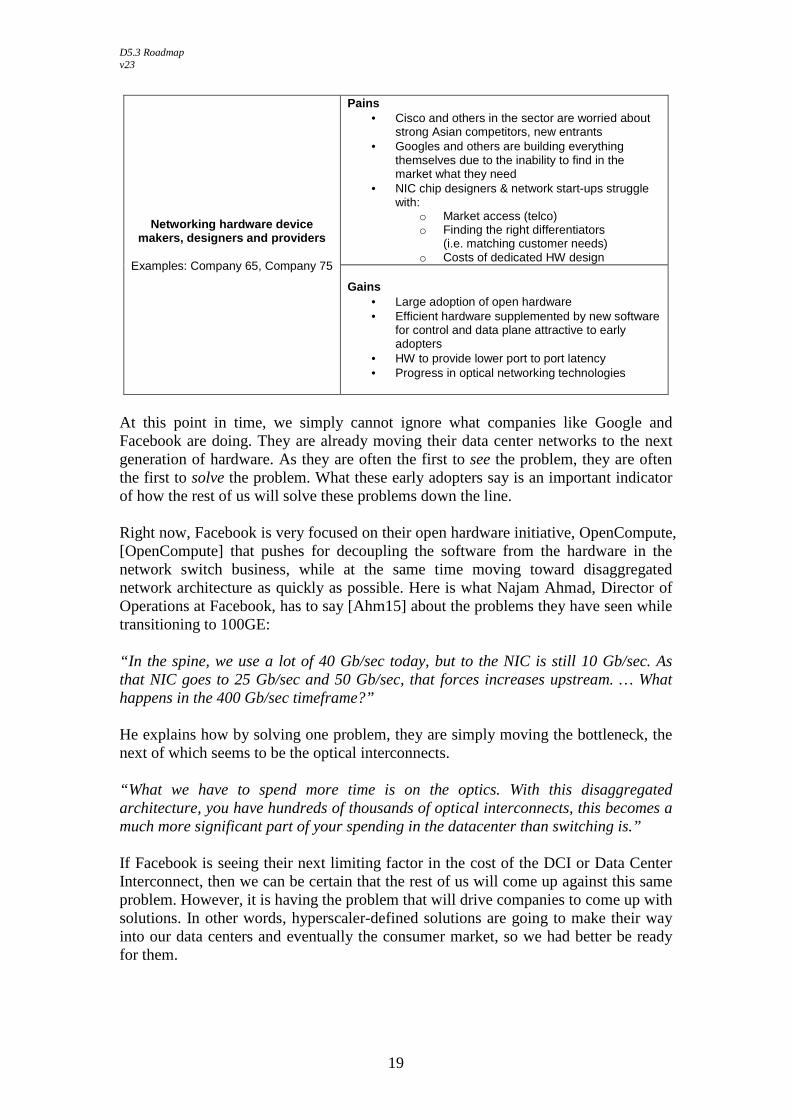

Networking hardware device makers, designers and providers

Examples: Company 65, Company 75

Pains • Cisco and others in the sector are worried about

strong Asian competitors, new entrants • Googles and others are building everything

themselves due to the inability to find in the market what they need

• NIC chip designers & network start-ups struggle with:

o Market access (telco) o Finding the right differentiators

(i.e. matching customer needs) o Costs of dedicated HW design

Gains • Large adoption of open hardware • Efficient hardware supplemented by new software

for control and data plane attractive to early adopters

• HW to provide lower port to port latency • Progress in optical networking technologies

At this point in time, we simply cannot ignore what companies like Google and Facebook are doing. They are already moving their data center networks to the next generation of hardware. As they are often the first to see the problem, they are often the first to solve the problem. What these early adopters say is an important indicator of how the rest of us will solve these problems down the line. Right now, Facebook is very focused on their open hardware initiative, OpenCompute, [OpenCompute] that pushes for decoupling the software from the hardware in the network switch business, while at the same time moving toward disaggregated network architecture as quickly as possible. Here is what Najam Ahmad, Director of Operations at Facebook, has to say [Ahm15] about the problems they have seen while transitioning to 100GE: “In the spine, we use a lot of 40 Gb/sec today, but to the NIC is still 10 Gb/sec. As that NIC goes to 25 Gb/sec and 50 Gb/sec, that forces increases upstream. … What happens in the 400 Gb/sec timeframe?” He explains how by solving one problem, they are simply moving the bottleneck, the next of which seems to be the optical interconnects. “What we have to spend more time is on the optics. With this disaggregated architecture, you have hundreds of thousands of optical interconnects, this becomes a much more significant part of your spending in the datacenter than switching is.” If Facebook is seeing their next limiting factor in the cost of the DCI or Data Center Interconnect, then we can be certain that the rest of us will come up against this same problem. However, it is having the problem that will drive companies to come up with solutions. In other words, hyperscaler-defined solutions are going to make their way into our data centers and eventually the consumer market, so we had better be ready for them.

D5.3 Roadmap v23

20

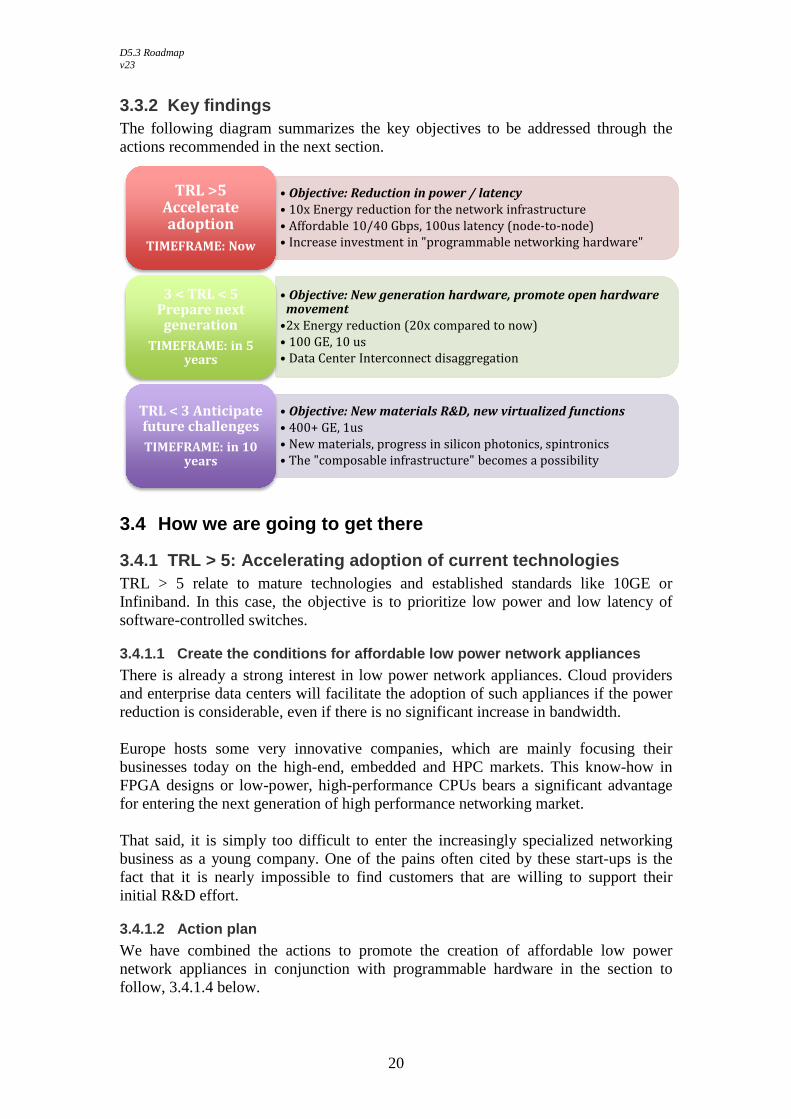

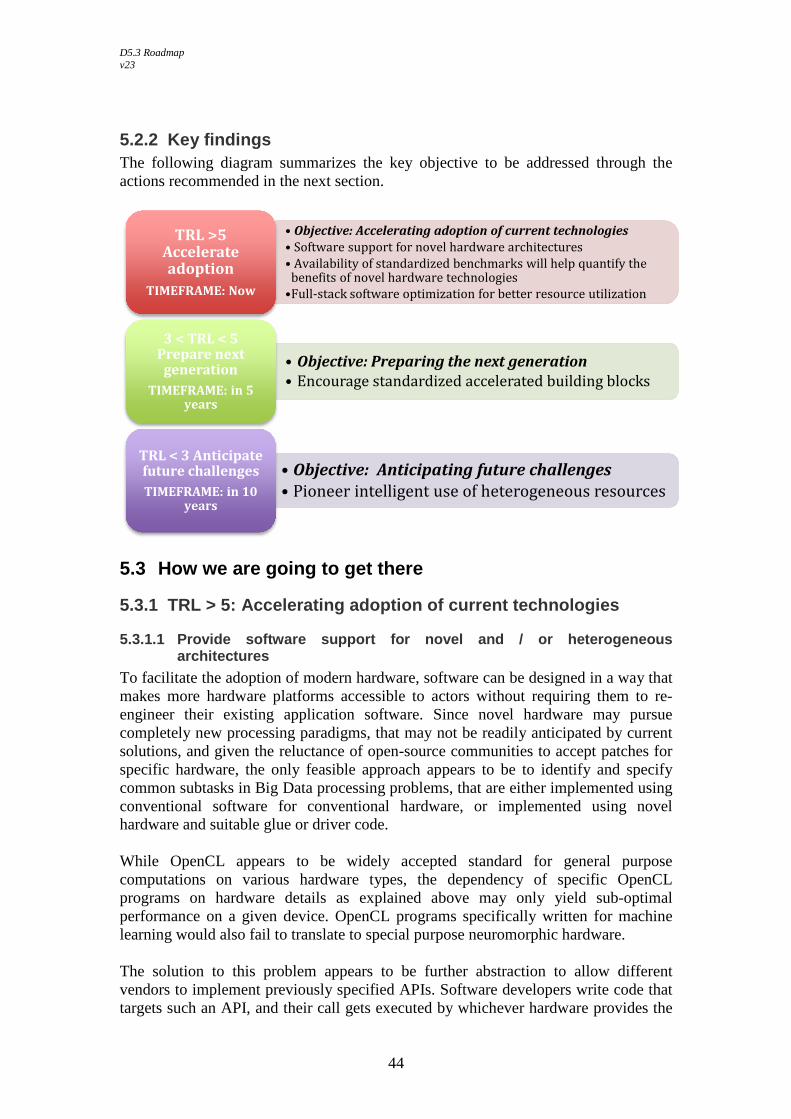

3.3.2 Key findings The following diagram summarizes the key objectives to be addressed through the actions recommended in the next section.

3.4 How we are going to get there

3.4.1 TRL > 5: Accelerating adoption of current tec hnologies TRL > 5 relate to mature technologies and established standards like 10GE or Infiniband. In this case, the objective is to prioritize low power and low latency of software-controlled switches.

3.4.1.1 Create the conditions for affordable low po wer network appliances There is already a strong interest in low power network appliances. Cloud providers and enterprise data centers will facilitate the adoption of such appliances if the power reduction is considerable, even if there is no significant increase in bandwidth. Europe hosts some very innovative companies, which are mainly focusing their businesses today on the high-end, embedded and HPC markets. This know-how in FPGA designs or low-power, high-performance CPUs bears a significant advantage for entering the next generation of high performance networking market. That said, it is simply too difficult to enter the increasingly specialized networking business as a young company. One of the pains often cited by these start-ups is the fact that it is nearly impossible to find customers that are willing to support their initial R&D effort.

3.4.1.2 Action plan We have combined the actions to promote the creation of affordable low power network appliances in conjunction with programmable hardware in the section to follow, 3.4.1.4 below.

• Objective: Reduction in power / latency

• 10x Energy reduction for the network infrastructure

• Affordable 10/40 Gbps, 100us latency (node-to-node)

• Increase investment in "programmable networking hardware"

TRL >5 Accelerate adoption

TIMEFRAME: Now

• Objective: New generation hardware, promote open hardware movement

•2x Energy reduction (20x compared to now)

• 100 GE, 10 us

• Data Center Interconnect disaggregation

3 < TRL < 5 Prepare next

generation

TIMEFRAME: in 5 years

• Objective: New materials R&D, new virtualized functions

• 400+ GE, 1us

• New materials, progress in silicon photonics, spintronics

• The "composable infrastructure" becomes a possibility

TRL < 3 Anticipate future challenges

TIMEFRAME: in 10 years

D5.3 Roadmap v23

21

3.4.1.3 Promote programmable network appliance hard ware However, effort to build less power hungry devices alone will not be enough. Network improvements must evolve with architecture, ideally supported by different use cases to address the diversity of the workloads. These new kinds of workloads found in Big Data applications, the disaggregation of storage or the need for more stream-based analytics puts a huge, but different, pressure on the network. In recent years, we have seen a strong trend toward open hardware that has demonstrated the value of simpler efficient hardware designs, coupled with dedicated software. We also see this approach applied to networking, first through the adoption of SDN and then as OpenFlow as a standard for programming data paths directly into networking equipment. OpenFlow allows for the use of commodity hardware for control plane decision-making and inexpensive programmable switches for packet forwarding. Progress is still needed on the OpenFlow API and design or implementations for different hardware will be needed. But coupled with this new generation of programmable hardware, a new market for early adopters and cloud providers willing to move away from the expensive vendor appliances might be created. Reducing latency by improving the low network layers is necessary but must be accompanied by a complete review of the software architecture so that the benefits are actually visible at the level of the application. This is particularly true in the case of Big Data software stacks. To date, much progress has been made by reducing slow disk usage and moving as much data as possible into memory, but there are still many inefficiencies that are open for improvement. For example, ScyllaDB proposes a 10x performance improvement over Cassandra, (a commonly used noSQL database for very large datasets), while preserving compatibility by simply moving from a Java-based implementation to C++ in addition to using a direct data path between the network interface and the application memory. Another interesting evolution can be seen in the HPC community where Mellanox is working to shift parts of the MPI responsibilities directly into the switch [Pri16]. In essence, Mellanox is working to move compute as close to the network as possible, to which we should respond: Could this be replicated for the Big Data architectures? Both of these examples demonstrate how critical it is to address the network concurrently with the architecture evolution, while applying different use cases to address the diversity of the workloads.

3.4.1.4 Action plan In order to promote the creation of affordable low power network appliances in conjunction with programmable hardware, we recommend short term actions that facilitate projects where:

• A Hardware Company or Telco willing to develop a new network appliance targeting the Cloud Computing market can work with

• A Cloud Operator looking for cost reductions and differentiators to attract • A Big Data Customer able to provide data and use cases

D5.3 Roadmap v23

22

• Supported by Academics and SMEs interested in validating new OpenFlow functionalities or new software designs

• For testing at scale an end-to-end optimized solution. As an example:

• Kalray [Kalray] wants to expand its many-core SMARTNIC product line, which currently provides 8x10GE for less than 20W, a 10x improvement over traditional vendor switches;

• This might interest a Cloud provider like OVH, which is aggressively looking at reducing its operational costs [OVH], thus increasing its vendor independence and expanding its customer base outside its traditional VPS hosting & CDN business;

• Based on the use-case and data provided by a customer, a sandbox cluster can be setup so that;

• Researchers at the INRIA Sophia-Antipolis can validate some of their ideas about new efficient OpenFlow routing modes presented in [Ngu14].

The outcome of such projects could serve as a starting point to push a de facto standard and build on a larger ecosystem, such as the Open Networking Foundation (ONF)1 and help bootstrap the emergence of highly optimized software.

3.4.2 TRL 3 - 5: Preparing the next generation For TRL between 3 and 5, the danger zone known as the Innovation “Valley of Death”, it is then logical to double the effort on current technologies with the same kind of action plan, but now targeting new hardware and software.

3.4.2.1 Take advantage of the convergence of HPC an d Big Data interests

As we move toward implementing 100GE interconnect while reducing the energy and latency, the network appliance hardware will have to evolve from a 32-bit to 64-bit (micro-architecture) and 20nm to 14nm (technology). With this new compute power available inside a switch, another round of opportunities for implementing network functions in software will be possible. We propose that HPC and Big Data communities work together to co-design this novel network appliance hardware, and then differentiate to meet the respective needs of their communities in software. The combined interest from both these communities would provide a larger customer base and lower the risk for hardware companies unwilling to focus on “niche markets”. We are already witnessing some transformations in this direction via initiatives like “CaffeOnSpark” [Caf16] from Yahoo. CaffeOnSpark takes advantage of state-of-the-art Big Data architecture for deep learning while at the same time utilizing a common set-up for HPC clusters (MPI on RDMA). The end result of this Big Data / HPC convergence is that training and inference tasks may be performed on a single cluster instead of two separate clusters which both reduces system cost and complexity.

1However, we should be cautious concerning such organizations: besides Ericsson, there are few established European companies or startups currently referenced by the ONF, pointing at a lack of interest and/or awareness of the potential benefits of being part of this industry effort.

D5.3 Roadmap v23

23

3.4.2.2 Action plan Under these conditions, we recommend an initiative that is oriented towards a converged Big Data / HPC networking hardware product line with differentiators implemented in software. This could be a key business enabler for European companies willing to compete with the market leaders.

3.4.2.3 Prepare for Data Center Interconnect (DCI) disaggregation

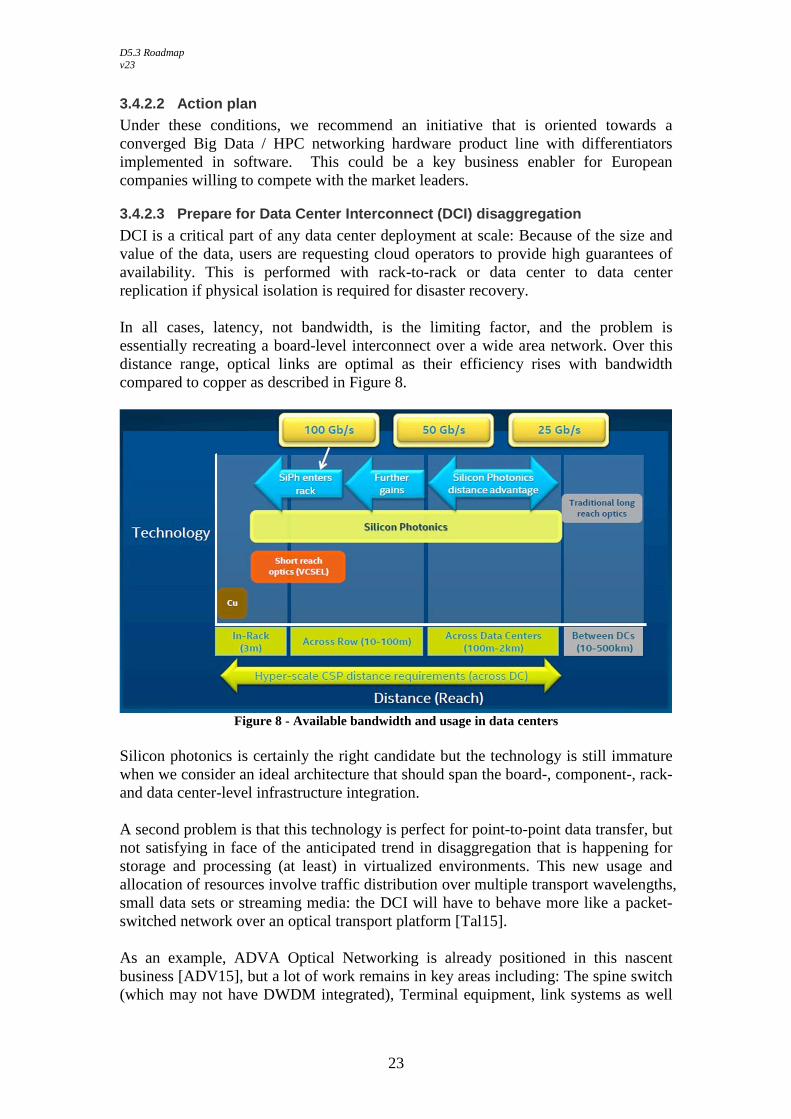

DCI is a critical part of any data center deployment at scale: Because of the size and value of the data, users are requesting cloud operators to provide high guarantees of availability. This is performed with rack-to-rack or data center to data center replication if physical isolation is required for disaster recovery. In all cases, latency, not bandwidth, is the limiting factor, and the problem is essentially recreating a board-level interconnect over a wide area network. Over this distance range, optical links are optimal as their efficiency rises with bandwidth compared to copper as described in Figure 8.

Figure 8 - Available bandwidth and usage in data centers

Silicon photonics is certainly the right candidate but the technology is still immature when we consider an ideal architecture that should span the board-, component-, rack- and data center-level infrastructure integration. A second problem is that this technology is perfect for point-to-point data transfer, but not satisfying in face of the anticipated trend in disaggregation that is happening for storage and processing (at least) in virtualized environments. This new usage and allocation of resources involve traffic distribution over multiple transport wavelengths, small data sets or streaming media: the DCI will have to behave more like a packet-switched network over an optical transport platform [Tal15]. As an example, ADVA Optical Networking is already positioned in this nascent business [ADV15], but a lot of work remains in key areas including: The spine switch (which may not have DWDM integrated), Terminal equipment, link systems as well

D5.3 Roadmap v23

24

as network management systems in order to make them highly integrated with little if any multiple peripherals, converters, amplifiers or multiplexers as is the case today.

3.4.2.4 Action plan As a means to preparing for this DCI disaggregation, we encourage the creation of an Optical DCI Open Architecture Initiative, inspired by open hardware and associated with suitable control software. Because this specific topic is not yet organized, there is room for establishing a de facto standard for the European companies. Involving large networking, telecom operators and optical network manufacturers will be a key success factor.

3.4.3 TRL < 3: Anticipating future challenges Even if the hardware/software designs do make progress according to the roadmap, some questions will remain unanswered:

• Can latency be reduced below the microsecond? • What does it mean for the network if the hardware accelerators are widely

used? Does the network become the next bottleneck? • What does finally having a 400GE network really mean?

In this paragraph, we put the emphasis on some possible future evolutions that can heavily disrupt the way the “data center” can be transformed. Because a low power, high performance network will allow distributed systems built with more sensors processing more data, connected to more remote resources, the very notion of “data center” will change: the future self-driving car will be a kind of “data center” in itself.

3.4.3.1 Anticipate the changes in Data Center desig n towards the composable infrastructure (and beyond)

Let’s suppose that environments will be more heterogeneous, denser and more applications or devices will share the same physical ports through virtualization. Now the physical interface becomes the new bottleneck. We recommend the following research topics for investigation in order to remove this next bottleneck:

• Adoption of new network topologies. High-end HPC clusters are using 2D or 3D torus topology networks that are cheaper than the classical fat-tree and links are on average shorter, providing lower latency, etc. Adopting this topology for Big Data workloads might be interesting, but will require non-trivial software modifications.

• New routing decision algorithms. With these new topologies, new “shortest path” or equivalent algorithms that go beyond what the current Internet Protocol (IP) can do (Spanning Tree and its variants) will be interesting to investigate

• Towards a more “functional” network. By separating the control and data planes, the routing decisions can be made “on the fly” and per packet. Leveraging this capability, an application might only declare its “intent” in terms of results (store this chunk of data into the database called x), without a priori knowledge of some target server/proxy/service on the network. The same way bio-inspired computing has led to advances in neuromorphic

D5.3 Roadmap v23

25

computing, there are some ideas to borrow from the “functional network” organization of the brain.

3.4.3.2 Action plan Our final recommendation in the area of Networking would be to facilitate partnership between Users, Data Center Operators and Network experts via research calls to explore and experiment with new network topologies, routing algorithms and higher level networking functions based on the research topics mentioned above. Based on the next generation of hardware, these projects will accelerate the return of experience and help reduce time to market by providing on the field validation. Associated with the composable infrastructure (see Figure 7), these approaches will open an entirely new set of opportunities. The basis for this research could be, for example, the RapidIO [Bol15] interconnect protocol which provides such flexibility, with the interesting addition over PCIe of supporting asymmetric links. These links not only require less power to transmit information, but the resulting pattern also fits nicely with the majority of Big Data workload data flows.

D5.3 Roadmap v23

26

Architecture: Accelerating compute for 4machine learning for analytics

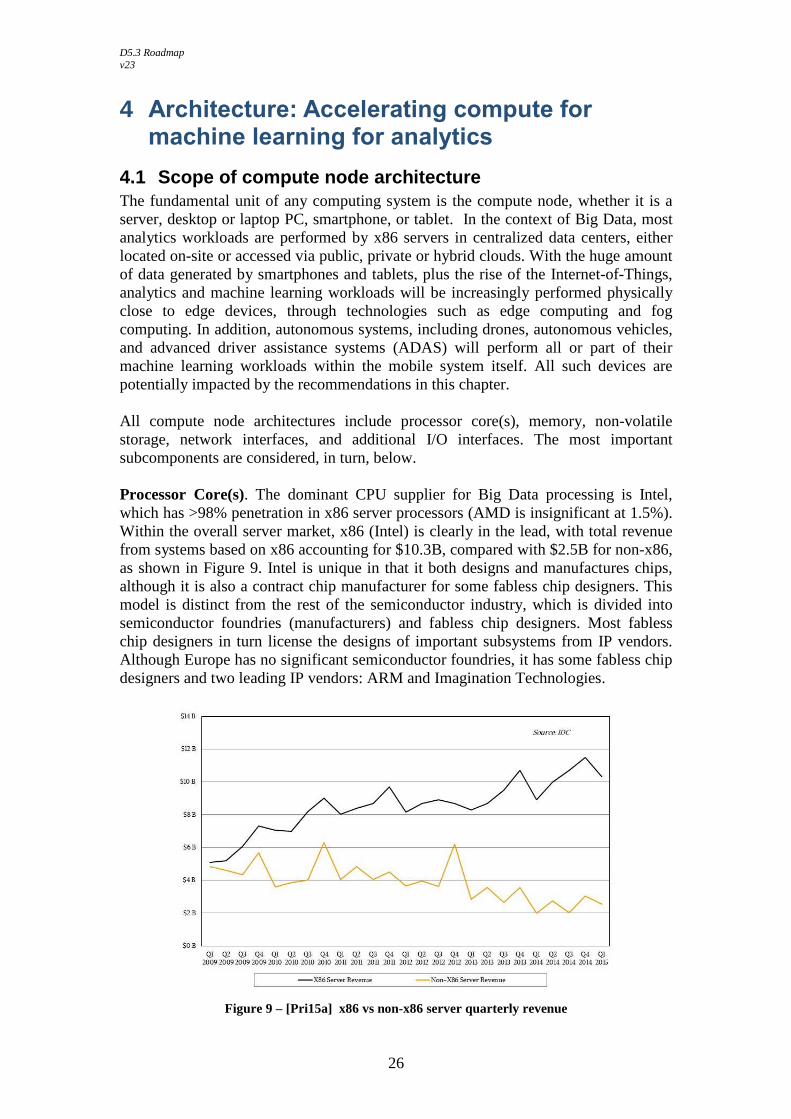

4.1 Scope of compute node architecture The fundamental unit of any computing system is the compute node, whether it is a server, desktop or laptop PC, smartphone, or tablet. In the context of Big Data, most analytics workloads are performed by x86 servers in centralized data centers, either located on-site or accessed via public, private or hybrid clouds. With the huge amount of data generated by smartphones and tablets, plus the rise of the Internet-of-Things, analytics and machine learning workloads will be increasingly performed physically close to edge devices, through technologies such as edge computing and fog computing. In addition, autonomous systems, including drones, autonomous vehicles, and advanced driver assistance systems (ADAS) will perform all or part of their machine learning workloads within the mobile system itself. All such devices are potentially impacted by the recommendations in this chapter. All compute node architectures include processor core(s), memory, non-volatile storage, network interfaces, and additional I/O interfaces. The most important subcomponents are considered, in turn, below. Processor Core(s). The dominant CPU supplier for Big Data processing is Intel, which has >98% penetration in x86 server processors (AMD is insignificant at 1.5%). Within the overall server market, x86 (Intel) is clearly in the lead, with total revenue from systems based on x86 accounting for $10.3B, compared with $2.5B for non-x86, as shown in Figure 9. Intel is unique in that it both designs and manufactures chips, although it is also a contract chip manufacturer for some fabless chip designers. This model is distinct from the rest of the semiconductor industry, which is divided into semiconductor foundries (manufacturers) and fabless chip designers. Most fabless chip designers in turn license the designs of important subsystems from IP vendors. Although Europe has no significant semiconductor foundries, it has some fabless chip designers and two leading IP vendors: ARM and Imagination Technologies.

Figure 9 – [Pri15a] x86 vs non-x86 server quarterly revenue

D5.3 Roadmap v23

27

Memory. Regarding memory components, consolidation among DRAM manufacturers has reduced the number of suppliers to three: Samsung (47%), SK Hynix (28%), and Micron (19%) [TRE15]. Given the high fixed costs [Shi15], low margins and extensive patent cross licensing, it is unrealistic to expect a European company to compete in this market, or in the similar market in NAND flash. There may, however, be an opportunity for European entrants in advanced non-volatile memory (NVM) technologies, since relevant European research is close to market, but a successful European company would likely soon be acquired by one of the big three memory companies.

4.2 Where we are today: Market trends and main actors Regarding Big Data compute node hardware, there are three important trends to consider. The first is toward heterogeneous computing. Several European companies may potentially benefit from a trend towards heterogeneity, either as fabless/IP vendors or as suppliers of programming tools or languages. Most European companies in this space, however, will be too small on their own to overcome the significant difficulties in programmability and the risk of vendor lock-in through proprietary programming languages and frameworks. A second major trend is towards increased integration within the compute node, with more and more functionality being integrated into a single CPU package. Given Intel’s dominance in Big Data server processors, smaller fabless/IP vendors will therefore have their profitability squeezed by a single dominant customer. Finally, we see the hyperscalers pursuing verticalization, in order to benefit not only from economies of scale but also from hardware–software co-design. In comparison with hyperscalers such as Google, Amazon and Facebook, the European industry is highly fragmented, and there is a considerable disconnect between data-driven companies, analytics companies and technology providers. We discuss each of these trends in detail in the sections that follow.

4.2.1 The march toward heterogeneous systems There is a noticeable movement away from general-purpose architectures towards heterogeneous systems and specialized accelerators. This change is mainly driven by a slowdown in Moore’s Law [Hua15], the exponential growth in the number of transistors per chip that has been consistently followed from the 1960s until now. As recently pointed out in Nature, “The doubling [in transistors per chip] has already started to falter, thanks to the heat that is unavoidably generated when more and more silicon circuitry is jammed into the same small area” [Wal16]. System integrators are therefore looking to heterogeneous systems, which combine multiple kinds of processors and accelerators, including GPUs, many-cores, FPGAs, and application-specific accelerators, in order to improve performance or energy efficiency. Several European companies seem poised to benefit from a diverse accelerator market, including fabless companies (Movidius and Kalray), IP vendors (ARM and Imagination Technologies), as well as the suppliers of programming tools, abstractions or languages (Xtremlogic, Mitrionics or Maxeler). Despite the potential benefits of moving toward heterogeneous systems, the barriers to entry are substantial. Perhaps the most obvious barrier is the cost of purchasing accelerator hardware, such as FPGAs or GPGPUs. More important than the actual

D5.3 Roadmap v23

28

equipment costs is the fact that these systems introduce significant software complexity. The effort to run a Big Data application on these systems requires specialized skills and usually knowledge of hardware due to the complex nature of the available tools and programming models. Even after investing in the appropriate human capital, there are still no guarantees of achieving a Return on Investment (ROI), as these systems often require hand optimization to attain near theoretical performance. On top of this, software for heterogeneous systems is not portable and subject to vendor lock-in. For example, once an application has been ported and optimized for one type of heterogeneous system (e.g. GPU-based), a company would have to start again from scratch in order to make that same application run on a different heterogeneous system (e.g. FPGA-based). In addition, many open-source communities are philosophically opposed to accepting hardware-specific software patches [Cor05], meaning that only open standard languages and APIs are likely to be supported by general software beyond specific driver modules connected using general-purpose (and often) restrictive interfaces. Finally, many of these new technologies have yet to be proven in terms of performance due to the lack of standard real-world benchmarks. The overarching result is that in order for European software vendors to adopt heterogeneous systems, they would need to keep pace with each successive new candidate technology, which is not economically viable. This is evident in the results of our project surveys, in which the majority of European software vendors reported these they had no hardware roadmap and they preferred to wait until new technologies became widely accepted and inexpensive commodities. Upon further research, we found a limited number of companies that were engaging with new technologies, including SAP with Intel and Neo4j with IBM, but these companies were the exceptions to the rule.

4.2.2 Specialization and vendor lock-in General-purpose GPU (GPGPU) is a maturing technology with a growing rate of adoption, especially in the area of high-performance computing (HPC). GPUs are especially suitable for computer vision and deep learning and in particular for training convolutional neural networks. Facebook is already using GPUs for face recognition while in the automotive market; Nvidia is pushing GPUs in the DRIVE PX on-board compute platform for computer vision and deep learning for Advanced Driver Assistance Systems (ADAS) [DRI15]. The GPGPU market is currently dominated by Nvidia (>95% of GPU-accelerated systems in the TOP500 use Nvidia), and their next target market is the server market. That said, GPGPUs have not yet achieved wide-scale penetration into data centers due an uncertain ROI. Small to medium-sized data center operators are unwilling to deploy GPGPUs at large scale, as the power consumption is too high and utilization too low to justify the investment. Moreover, even at the level of GPGPU implementation, there are elements of vendor lock-in. Nvidia’s market lead is sustained through aggressive promotion of its proprietary CUDA programming language, while other programming languages, namely OpenCL, are supported by other GPGPU vendors including AMD and ARM. As is the case for moving from a GPGPU-based heterogeneous architecture to an FPGA-based one, there is considerable Non-recurring Engineering (NRE) cost required for a change in GPU vendor.

D5.3 Roadmap v23

29

FPGAs (field-programmable gate arrays) were originally designed for ASIC prototyping. An FPGA device can be programmed at a later time, after its manufacture, to emulate hardware (hence “field programmable”). The possibility of being able to re-implement functionality on-the-fly makes FPGAs a prime candidate for the server market where services are currently evolving rapidly. More important, however, is their potential to “shoulder a large proportion of the processing burden while reducing power consumption”. The Catapult project was designed to speed up Microsoft’s Bing web ranking algorithm using FPGAs, and it resulted in Bing’s web ranking being achieved using approximately half the number of servers that were required previously [Put14]. The success of this architecture has led to its implementation in Microsoft’s production data centers largely driven by the significant reduction in Total Cost of Ownership (TCO) as well as increased sustainability. Upon acquiring Altera, Intel said that it expected a third of cloud service providers to be using hybrid CPU–FPGA servers by 2020 [INT15]. Moreover, the implications of using FPGA heterogeneous systems are particularly clear with respect to Big Data–related tasks that are similarly suited to hardware acceleration [Fee15]:

• Image recognition and classification • Encryption and decryption • Video applications (e.g. encode and decode) • Cloud security • Load balancing • Internet key exchange • Deep learning and neural networks

That said, even more so than GPGPUs, FPGAs are expensive and difficult to program, meaning that the tools and programming models are not accessible to software developers: FPGA hardware programming abstractions expose the facts that FPGA hardware is inherently concurrent, timing is explicit, memory is subdivided into multiple distributed memory blocks, and communication between subsystems requires special hardware rather than shared memory [Bai15]. The potentially high NRE to develop FPGA-based accelerators means that adopting FPGAs is high risk and it has a potentially low ROI. We see the two major FPGA vendors finally starting to take this programmability issue seriously. Altera was the first to support OpenCL on its FPGAs. Xilinx has released High Level Synthesis tools like Vivado, in addition to adding support for OpenCL.

4.2.3 Integration inside the compute node A second clear trend for compute node architecture is for increased integration within the CPU node, in order to improve performance and reduce energy consumption. There are two approaches: System-on-Chip (SoC) and System-in-Package (SiP). A System-on-Chip (SoC) integrates a complete computing system onto a single silicon die. This approach has been used for some time in embedded systems, mobile phones and tablets, where space and power are at a premium and volumes are very high. The SoC approach is now being extended into the server market. Intel Xeon D integrates dual 10GE, PCIe, USB, and SATA (disk) interfaces. In addition, all companies that are supplying or will soon supply ARM-based server chips, such as Applied Micro, AMD, Broadcom and Qualcomm are adopting the SoC approach.

D5.3 Roadmap v23

30

Given the above trend for heterogeneous systems and specialization (Specialization and vendor lock-in 4.2.2), together with fast evolution in the Ethernet standard (see Section 3.2.3), investing in a market-specific server SoC is likely to be cost-prohibitive, unless the designer can support the SoC vertically through its business or address a very large-volume market (such as mobile). SoCs provide no flexibility: adding a new technology such as 40Gb Ethernet to a die that currently supports only 10GE requires a costly redesign, resulting in the loss of the NRE that was invested into the original die. In addition, an SoC must be implemented in its entirety using a single silicon process. Since the SoC includes the performance- and energy-critical processing cores, the entire die must be fabricated using a leading edge, i.e. expensive, silicon technology. An alternative approach is System-in-Package (SiP). Intel supports SiP for its foundry customers through a technology it calls Embedded Multi-die Interconnect Bridge (EMIB). A similar approach is 2.5D/3D integration using a silicon or organic interposer, which enables efficient high-bandwidth interfacing between multiple silicon dies (chiplets) inside the same package. The latter approach was pioneered by the EC EUROSERVER project [Euroserver], led by CEA, with partners including STMicroelectronics and ARM. EUROSERVER has led to two start-ups, one of which is commercializing a European solution for microservers [Kaleao], based on ARM cores and 2.5D integration. Having multiple dies in the same package provides flexibility in that faster evolving technologies may be separated from more slowly evolving ones and thus replaced without affecting the rest of the design. This means that new technologies such as 40GE could replace older ones without a need to re-engineer the whole die. In addition, market-specific products can be built from standard commodity compute chiplet(s) connected to specialized chiplet(s) providing accelerators and I/O interfaces, without the need to design an entire SoC. This flexibility may give smaller companies the opportunity to compete on a more level playing field with their standalone accelerator solutions, as there will be better integration into a state-of-the-art system. Finally, this 2.5D integration may allow European accelerators to be fabricated using less expensive silicon technologies on a separate die from the CPU while at the same time remaining closely integrated with the CPU, which must be fabricated using a leading edge process.

4.2.4 Verticalization and hyperscalers The final major trend is the increasing dominance of a small number of vertically-integrated companies that co-design all or parts of the server stack, to varying degrees, ranging from the user-visible software, through (Big Data) frameworks, down to system integration and potentially even chip design. Examples include Google, Apple, Facebook, Twitter and Amazon (“GAFTA”), plus Baidu, Alibaba and others, none of which is European. These companies have enormous market share and economies of scale, made more so through efficiencies from their vertically-integrated perspective. In Europe, however, the industry is fragmented, with a large disconnect between technology providers and analytics companies. Almost all analytics companies expressed that they have no hardware roadmap, take little notice of new hardware trends and are only looking at existing commodity hardware. Since Europe currently has no market share in server compute CPUs, there is limited opportunity for these companies to engage with the incumbent supplier(s). Technology providers need

D5.3 Roadmap v23

31

software vendor input into the design of future architectures and they face specific problems, such as the lack of labeled training data sets, the most comprehensive of which are being collected by vertically-integrated companies.2 This large disconnect between technology providers and analytics companies carries a significant risk of being left behind by the larger U.S. companies. Even when a company releases its technology as open-source software; e.g. TensorFlow, the public version is limited (in the case of TensorFlow to a single node). The concern is not just that Europe will fall behind, but that European companies will be put out of business.

4.2.5 Non-von Neumann A final, longer-term, trend is towards non-von Neumann computing architectures. The von Neumann architecture, defined in 1945 by John von Neumann and others, defines the fundamental architecture of a stored-program computer, consisting of a Central Processing Unit (CPU), memory containing both data and instructions, non-volatile storage, and input/output (I/O) interfaces. FPGAs are non-Von Neumann devices, at least when they are programmed using Hardware Description Languages (HDLs) such as VHDL and Verilog; but High-Level Synthesis (HLS) and OpenCL programmability mean that FPGAs are increasingly programmed in a von-Neumann style. New technologies, including resistive computing, neuromorphic computing, and quantum computing are fundamentally non-Von Neumann architectures. Defining the programming models for these devices is still an open research problem, with, as yet, no compatibility with existing software programming paradigms, tools, or software frameworks. Among non-von Neumann accelerators, this roadmap makes specific recommendations only for FPGAs and neuromorphic computing. Quantum computing, in particular, is still at very low TRL, and is subject to specific research funding mechanisms outside the context of Big Data. Neuromorphic computing originally referred to hardware operating using the same (analog) principles as the human brain, but the term is commonly used nowadays to refer to a computer architecture inspired by the brain, whether built from many-cores, analog electronics, custom CMOS, or new technologies such as memristors. Neuromorphic computing systems use a large number of primitive “neurons” to break the von-Neumann bottleneck, greatly reducing energy consumption [Cal13].The potential improvement in energy efficiency is illustrated by comparing IBM Watson, which won Jeopardy! in 2011 with a human brain. IBM Watson consumes 80 kW, whereas a human brain consumes only about 100 W. Neuromorphic devices are relevant for Big Data algorithms including those in computer vision and machine learning. A significant improvement in neuromorphic computing will enable new applications, including face recognition, target tracking (military), toys, automatic defect checking in manufacturing, market research, self-driving cars, and ADAS. Many research projects are working towards neuromorphic computing, including SpiNNaker and the Human Brain Project in Europe, the DARPA SyNAPSE project, Stanford Brains in Silicon, and Neuflow. Some large U.S. companies are working

2 Access to data is an important reason why a consortium of German automotive companies, including Audi, BMW and Daimler, bought Nokia HERE for $3.2B in 2015.

D5.3 Roadmap v23

32