Embed Size (px)

Citation preview

CUSTOMER LOYALTY IN RETAIL BANKING: GLOBAL EDITION 2014

Going DigicalSM: Customers love thesmart fusion of digital and physical assets

Copyright © 2014 Bain & Company, Inc. All rights reserved.

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page i

Contents

Going Digical . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . pg. 1

1. Global loyalty trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . pg. 7

2. Channel behavior and its infl uence on loyalty . . . . . . . . . . . . . . . . . . . . . pg. 11

3. Product purchasing and ownership trends . . . . . . . . . . . . . . . . . . . . . . . pg. 21

Page ii

• Customers conducted more than 50% of their banking interactions through digital channels in 18 of 22 countries surveyed.

• Mobile is the most-used banking channel in 13 of 22 countries and accounts for around 30% of all interactions worldwide.

• The share of customers using mobile applications rose by19 percentage points in the past year. Online usage via computers dropped 3 percentage points.

• More than half of customers used both digital and physical channels such as branches and call centers.

• These “omnichannel” customers gave their bank a Net Promoter Score 16 percentage points higher than customers using only digital channels and 22 points higher than those using only physical channels.

• Customers use several channels to research and buy new banking products. 47% of US customers con- sulted their bank’s website, and 37% got recommen- dations from bank employees.

• Hidden defection of customers from their primary bank is rampant: More than one-third bought a product from a competitor during the past year.

By the numbers: Mobility and the state of customer loyalty in banking

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 1

Going Digical

Banking customers now handle more of their banking interactions, on average, via smartphones and tablets than

through any other channel, this year’s report shows—and the mobile channel has become a key element in the bid

to earn customer loyalty. Increased loyalty, in turn, pays off for a bank with customers buying more products and

making more referrals, which allow the bank to capture more than its fair share of new sales.

Mobile does not stand alone, however; it must be integrated with other channels like branches and contact centers

to deliver seamless and simple customer experiences. Most banks realize that they need to reimagine their end-

to-end customer experiences across all channels to make the most of the new mobile capabilities. But they have

been struggling to integrate channels across the numerous departments of their large, complex organizations.

Still, many of the largest banks worldwide have made progress in closing the loyalty gap with the loyalty leaders,

which often are smaller, more focused and nimble banks.

JPMorgan Chase, for instance, has gained in almost every region of the US; Royal Bank of Canada made strides

during the year; and all four big banks in Australia improved their scores signifi cantly. The banks that have begun

to pull ahead will likely accelerate their progress as they further sharpen their focus on earning loyalty. Those that

don’t pick up the pace risk falling further behind.

This year’s report, based on Bain’s survey of roughly 83,000 consumers in 22 countries, explores how people

do their banking and how banks are adapting their distribution and service channels to address customer needs

and improve the economics of the business. The research occurred online in July through November 2014, through

market research fi rm Research Now.

The meteoric rise of mobile

Mobile has become the dominant means for consumers to interact with their banks. Customers completed more

interactions with their banks via smartphones or tablets than through any other channel in 13 of 22 countries we

surveyed. And the share of customers using a using a bank’s mobile app rose a striking 19 percentage points

during 2014, with strong increases across all age groups in most markets.

Until recently, consumers layered digital onto other ways of interacting with their bank—for instance, using mobile

devices to check their balance more often while keeping their use of other channels the same. This year, the data

shows a meaningful decline in usage of not only branches and ATMs but even online via computers; the latter

dropped an average of 3 percentage points. (It’s possible that our survey slightly overstates growth in mobile usage,

because the survey is conducted online and survey companies have been making questionnaires easier to answer

via mobile devices. But we’re confi dent the trends are valid.)

Mobile does not replace other channels but fundamentally changes how consumers use them. Most customers

in most markets (60% of respondents overall) used a combination of digital and physical channels to do their

banking—what we call “omnichannel” behavior. This is critical for effective service, marketing and selling,

because customers expect to be able to hop from one channel to another.

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 2

A virtuous circle: More channels, greater loyalty, more money

Omnichannel customers gave their bank an NPS that is 16 percentage points higher, on average, than the score customers

who rely only on digital channels gave and 22 percentage points higher than the score given by those who use only physical

channels. And NPS was even higher for omnichannel customers who had more interactions.

The payoff is higher product ownership: Omnichannel customers held an average of 1.0 more product with their

primary bank than digital-only customers and 1.3 more than branch-only customers. While the data doesn’t prove

a linear cause-and-effect relationship, it shows a virtuous circle of greater engagement across channels, greater

loyalty and increased product holdings.

For many years, interactions in person or via phone were critical for delighting or angering customers during

moments of truth, such as seeking advice. Now, leading banks are investing heavily in digital innovations designed

to become powerful “wow” factors in their own right. In Spain, NPS leader Bankinter has an early lead in infusing

its branches with useful digital technologies, such as biometric signatures for contracts, which save time, and

tablets that enable self-service.

Likewise, Citibank in the US has steadily improved its NPS over the past four years, in part by deploying practical

digital innovations. Examples include sending fraud alert texts to customers at the point of sale and deploying smart

ATMs that allow customers to open accounts or hold videoconferences with experts. Several Asian banks, meanwhile,

have pioneered personalization features. Shinhan in South Korea maintains a human touch through its use of

“smart letters,” delivered through a mobile app. These letters range from simple birthday greetings to coupons

providing higher interest rates.

Banks that pull ahead in loyalty by investing heavily in mobile to deliver a better experience will reap fi nancial

benefi ts. Those banks that lag in effectively investing in the mobile advantage will miss reaping the fi nancial

benefi ts and also fall further behind in their ability to invest.

The hidden defection problem—and opportunity

Accelerating the development of mobile sales capabilities will help banks address a signifi cant but little-noticed

problem: the hidden defection of customers who go to another provider for additional products such as mortgages

and credit cards. Globally, more than one-third of customers bought a new banking product at a bank other than

their primary bank this year.

Imagine the uproar that would ensue if one-third of a bank’s customers were completely defecting each year. Yet

the defection highlighted here passes unnoticed because banks usually don’t know their customers were

shopping in the fi rst place and seldom know that they lost the sale. Mobile banking has the potential to

either exacerbate or mitigate this problem.

Hidden defection could worsen as digital start-ups and specialist fi rms that are less encumbered by legacy systems

and regulations offer better, simpler solutions and make it easy for people to fi nd them. Banks that fail to respond

risk getting saddled with the bulk of low-margin accounts, while other fi rms siphon off high-margin products

like credit cards and mortgages. Young fi rms such as Betterment, which simplifi es the process of investing, or

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 3

Kabbage, which has developed an underwriting process to instantly lend up to $100,000, stand to capture a

greater share of banks’ more profi table lines of business.

Some banks, such as JPMorgan Chase and USAA in the US, Nationwide in the UK and Hang Seng in Hong Kong,

have begun to address defection through different combinations of earning strong loyalty, fi elding strong

products and improving sales capabilities. But for all banks, digital technology increasingly is critical for effective

selling. When US consumers researched or considered a new fi nancial product like a mortgage, they typically

used at least four or five sources of information, with the most frequently used source being their bank’s

website and the least used being mobile apps. Deploying mobile apps to make it easy for customers to con-

nect to the right bank resources and employees during their shopping process, and preapproving them for the best

offer, could substantially raise the odds of winning the sale.

How is the hard part

Winning in a Digical world, by fusing the best of customer-friendly digital tools and processes with physical assets,

presents a challenge for banks, especially with their current operating model. Most banks’ operating models

are characterized by products and channels that operate in silos and by processes that require extensive signoff from

compliance, legal, fi nance, operations, marketing and other functions to make any change—50 people who can

say no against just one who can say yes.

Banks will need to redesign their operating model, and they can take a cue from leading retailers. Macy’s, for example,

has integrated most of its online shopping with its physical facilities, turning virtually all of its stores into omnichannel

fulfi llment centers. Its iconic Herald Square store in New York is undergoing a $400 million remodeling that features

innovations such as interactive directories, digital signage, widespread use of radio-frequency identifi cation (RFID)

tagging and a new mobile app to guide customers as they shop. Macy’s has evolved its operating model in order to

pursue this integration. The company now has a chief omnichannel offi cer, who reports directly to the CEO and

manages the development of strategies to closely integrate stores and online and mobile activities. He also has

responsibility for systems and technology, logistics and related operating functions.

Apple likewise recognized a need to change how it manages its online and physical stores. When Apple hired

Angela Ahrendts, the former Burberry chief executive, it gave her responsibility for both online and retail stores,

with a mission to make the customer experience seamless across channels.

Some leading banks are overcoming their organizational obstacles by taking a fresh “design, build, use” approach

to developing exceptional customer experiences. Notably, the approach enlists customers to create the experience

(see Figure 1). Here’s how it works.

1. Design for the customer’s ideal experience.

Effective digital design focuses on the customers’ priorities—buy a home, provide for a daughter’s college edu-

cation, manage cash and so on. Leading banks have found it useful to select the critical customer journeys by

ranking them according to frequency of use and emotional importance (see Figure 2). The next step is to

reimagine each journey from the customer’s perspective. Buying a home, for instance, should start at the moment

the customer considers house hunting and extend all the way through moving in.

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 4

Journey mapping and benchmarking against banking competitors and best-in-class fi rms in other industries provide

a data-driven audit to identify gaps in capabilities and appeal. It should be easy and intuitive for customers to

navigate a website or a mobile app, and the presentation should feel empathetic and not clinical.

Benchmarking must be complemented by a design process that will allow a bank to stand out from the crowd.

We have found that an effective mechanism to bring key customer moments to life is a storyboard created with

the help of artists and writers. Storyboards, when combined with engaging real customers to cocreate digital tools

through rapid prototyping and hands-on testing, lead to a clear view of the next horizon for each customer journey.

2. Build with a modern development model.

Given the speed of digital innovation these days, banks can’t afford to use the traditional waterfall IT development

approach, which relies on remote release dates and thus struggles to catch up as the marketplace changes. The

trend among leading organizations, such as Capital One Labs, is toward Agile delivery models. These deliver function-

ality in many bite-sized pieces.

Just installing Agile development teams is not enough. The entire ecosystem around the team needs to be

redesigned and should include a process to ensure that the team building a particular journey has a pre-allocated

budget, resources and approvals. The Agile model should also involve relevant compliance and legal staff on the

team from the start. It should maintain regular communications with a senior executive leading the relevant line

of business. And it can employ cloud-based development environments in order to reduce cycle times.

Figure 1: Guiding principles for digital innovations

Personalized to the customer, reflects wants and needs

Intuitive, simple and easy to use

Has human touch and clear, jargon-free language

Available anywhere, any time and on any device

Has everything the customer wants

Map and prioritize experiences that matter most to customers

Engages customers and business partners

Uses rapid prototyping to test ideas Simplify processes and reinforce behaviors

Identify choke points and organize for nimble development

Build

Use

Adopt Agile development models

Employ “test and learn” for continuous improvement

Des

ign

prin

cipl

esD

esig

n pr

oces

s

Reimagine the key end-to-end experiences

What does your digital experience look like? How do you develop your digital properties?

Source: Bain & Company

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 5

3. Use what really works with customers and employees.

In most bank trials, new approaches tend to succeed initially through small pilots in highly managed, carefully

selected situations. But they fail to deliver the expected results in a mass rollout with all its complexity and variation.

The more effective approach, which complements Agile development, is to test and learn more broadly, based

on fast loops of customer feedback.

The test-and-learn approach relies on behavioral psychology, in which slight nuances can spell the difference

between success and failure. Insights about what works often come from frontline employees and analysis of

real customer behavior. At one Australian bank, for instance, a branch greeter charged with convincing customers

to use self-service solutions realized that asking “Do you know how to do that yourself?” made customers defensive

and thus fell fl at. The more positive tone in “May I show you how to skip the line?” was much more effective.

These sorts of insights happen regularly in every bank’s branch, but this bank had a process to quickly identify

and spread the insight throughout the bank, so the entire system could benefi t.

The chapters that follow explore the 2014 survey data on customer loyalty, how the right omnichannel approach

in a mobile world earns loyalty and what the untapped opportunity is in capturing new purchases of banking

products. These insights can inform the migration of transactional activities to digital channels, in order to

reduce costly and avoidable volumes entering the branch. That will allow the branch network to become leaner

and more oriented toward higher-value sales and service activities. Done right, the Digical journey can combine

higher productivity with the ultimate touchstone: strong customer advocacy.

Figure 2: Focus on the experiences that matter most to customers

0

50

100

150

5,000

10,000

75 80 85 90%

Remotedeposit capture

Dealing withmatters for deceased

relative

Freq

uenc

y of

use

(Ave

rage

mon

thly

vis

its, i

ndex

ed)

Priorityexperiences

Emotional importance(Percentage of detractors + percentage of promoters)

Everyday transactions

Check balance

Pay bills Resolve a complex problem

Account unexpectedly blocked

Withdraw cash

Source: Bain & Company disguised case example

1.Global loyalty trends

• Customer loyalty as measured by NPS improved in 2014 from the previous year, as leading banks inten-sifi ed their efforts to earn loyalty and many banks continued their recovery after the fi nancial crisis.

• What matters most to an individual bank is how it performs relative to its peer group. Within national markets, NPS varied widely from bank to bank. In Germany, for instance, top-performer DKB had an NPS that was 74 percentage points higher than the worst performer and 55 percentage points above the country average. Sparda-Banken, a credit union, had a score 12 percentage points lower than DKB.

• Large traditional banks made meaningful improve- ments in NPS relative to their direct or smaller competitors in 2014. Several big banks, such as Santander and Barclays in the UK and JPMorgan Chase in the US, have shown sustained progress over the past few years.

• Several factors account for the progress of these banks, with digital innovation being one factor. Previous surveys have shown that using mobile banking contributed to higher loyalty scores. This year, we found that promoters of a bank, who score a 9 or 10 on a zero-to-10 NPS scale, were more likely to use mobile apps than were detractors, who score 6 or less on the same scale.

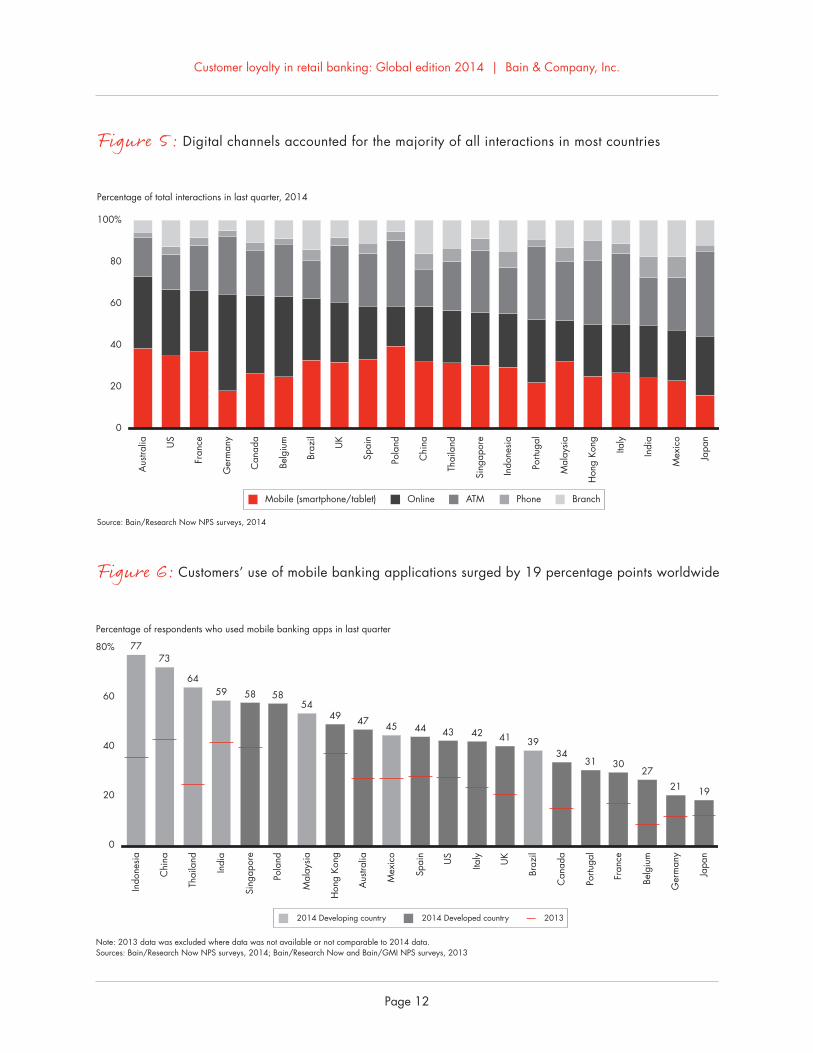

• Digital usage now accounts for the majority of banking interactions in virtually every country, with Australia, France, the US, Canada and Germany leading the digital share of all interactions. The sharpest growth came in mobile usage, which for the fi rst time reached about 30% of all interactions in most countries. Mobile remains a relatively small share of digital interactions only in Germany, Portugal, Mexico and Japan.

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 8

Figure 3: In most markets, there is a large gap between leaders and laggards

Canada

Primary banks’ Net Promoter Scores relative to loyalty leader, which is indexed to zero, 2014

Mexico

US: Northeast

US: Midwest

US: South

US: West

Am

eric

as

RBC, TD Canada Trust President's Choice Financial

Banorte Santander, HSBC

PNC Bank, TD Bank, Chase Bank

Huntington

USAA Chase Bank, Regions Bank

USAA Union Bank, Bank of the West, Citibank

−100% −80 −60 −40 –20 0

Australia

China

Hong Kong

India

Indonesia

Japan

Malaysia

Singapore

South Korea

Asi

a-Pa

cific

China Construction Bank, Bank of Communications, China Merchants Bank

Citibank

Maybank, Public Bank, CIMB

Citibank

Shinhan Bank

HDFC, Bank of Baroda

BCA

Shinsei Bank

ING Direct Bendigo Bank

Belgium

France

Germany

Italy

Poland

Spain

UK

Euro

pe

Sparda-Banken

Banca Mediolanum

Bankinter

Highest traditional bank Highest direct bank

Lowest bankAverage

Argenta Spaarbank

La Banque Postale

DKB

ING Direct, Fineco

ING Bank

first direct Nationwide

Notes: Country averages include all banks; highest and lowest banks include only banks where n≥200 for the Americas and Europe and n≥100 for Asia-Pacific; excludes markets with insufficient number of banks; traditional banks include large building societies or credit unions.Source: Bain/Research Now NPS surveys, 2014

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 9

Figure 4: In many countries, large branch big banks have been closing the loyalty gap with direct banks

US Canada Australia

Germany UK Italy

–20

0

20

40

60

80%

Directbanks

Regionalbanks

Nationalbanks

–20

0

20

40

60

80%

Big Fivebanks

Directbanks

2011 ‘12 ‘13 ‘14

–20

0

20

40

60

80%

Regional/smaller banks

Directbanks

2012 ‘13 ‘14

Big Four banks

Large branchbanks

Directbanks

‘14

0

–20

20

40

60

80%

Creditunions

2012 ‘13

–20

0

20

40

60

80%

Buildingsocieties

Directbanks

2012 ‘13 ‘14

Large branchbanks

–20

0

20

40

60

80%

US Canada Australia

Direct banks

2013 ‘14

Internationalbanks

Largeregional banks

Nationalbanks

2009 ‘10 ‘11 ‘12 ‘13 ‘14

Source: Bain/Research Now NPS surveys, 2009–2014

Net Promoter Score

2.Channel behavior and its infl uence on loyalty

• Mobile applications have arrived at the stage of mass appeal. Almost every country showed a huge increase in the share of respondents using mobile apps, with an average 19 percentage point rise globally. Indonesia and China led in usage.

• Online usage showed declines or was fl at every-where except in Indonesia, Mexico and Japan—an average 3 percentage point decline worldwide.

• Growth in mobile has not just cut into online usage; it also coincided with declines in branch, ATM and phone usage. In the US the share of respondents using these channels dropped by 5, 3 and 5 per-centage points, respectively, since 2012.

• Respondents under age 35 were more likely than older customers to bank via mobile devices. But the share of customers age 65 and older who use mobile is a substantial 30%—and mobile usage rose sharply among all age groups.

• Roughly 60% of customers used a combination of digital and physical channels. These omnichannel customers gave their primary bank an NPS that was 16 percentage points higher than the NPS of custom-ers using only digital channels and 22 points higher than the NPS of those using only physical channels. They also own more products through their primary bank than those who use only digital or only physi-cal channels: 1.0 and 1.3 products, respectively.

• For product research and consideration, US respon-dents most frequently turned to their bank’s web-site, highlighting the importance of a well-designed, intuitive site. Next, respondents turned to bank employees. Other sources—such as direct mail or, for credit cards, another website—had a prominent infl uence for individual products. Mobile has yet to be effectively tapped for selling.

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 12

0

20

40

60

80%

Indo

nesi

a

77

Chi

na

73

Thai

land

64

Indi

a

59

Sing

apor

e

58

Pola

nd

58

Mal

aysi

a

54

Hon

g Ko

ng

49

Aus

tralia

47

Mex

ico

45

Spai

n

44

US

43

Italy

42

UK

41

Braz

il

39

Can

ada

34

Portu

gal

31

Fran

ce

30

Belg

ium

27

Ger

man

y

21

Japa

n

19

Percentage of respondents who used mobile banking apps in last quarter

Note: 2013 data was excluded where data was not available or not comparable to 2014 data.Sources: Bain/Research Now NPS surveys, 2014; Bain/Research Now and Bain/GMI NPS surveys, 2013

2014 Developing country 2014 Developed country 2013

Figure 5: Digital channels accounted for the majority of all interactions in most countries

0

20

40

60

80

100%

Aus

tralia US

Fran

ce

Ger

man

y

Can

ada

Belg

ium

Braz

il

UK

Spai

n

Pola

nd

Chi

na

Thai

land

Sing

apor

e

Indo

nesi

a

Portu

gal

Mal

aysi

a

Hon

g Ko

ng

Italy

Indi

a

Mex

ico

Japa

n

Percentage of total interactions in last quarter, 2014

Mobile (smartphone/tablet) Online ATM Phone Branch

Source: Bain/Research Now NPS surveys, 2014

Figure 6: Customers’ use of mobile banking applications surged by 19 percentage points worldwide

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 13

Figure 7: In most countries, the use of online tools for routine transactions declined

0

20

40

60

80

100%

81 79 77 76 74 74 73 71 70 69 6661 59

52

Chi

na

Indo

nesi

a

Aus

tralia

Can

ada

Indi

a

Belg

ium

Ger

man

y

Sing

apor

e

Hon

g Ko

ng UK

Italy US

Portu

gal

Fran

ce

Spai

n

Thai

land

Braz

il

Mal

aysi

a

Mex

ico

Japa

n

Pola

nd

52

Percentage of respondents who used online tools (via computer, not mobile) for routine transactions in last quarter

Note: 2013 data was excluded where data was not available or not comparable to 2014 data.Sources: Bain/Research Now NPS surveys, 2014; Bain/Research Now and Bain/GMI NPS surveys, 2013

88

78 7776

68 67

2014 Developing country 2014 Developed country 2013

Figure 8: Branch visits continued their slow decline

0

20

40

60

80

100%

82 80 77 75

66 64 63 60 59 58 57 55 54 5349 47 44

Chi

na

Indo

nesi

a

Mex

ico

Braz

il

Indi

a

US

Italy

Spai

n

Can

ada

UK

Sout

h Ko

rea

Mal

aysi

a

Thai

land

Portu

gal

Hon

g Ko

ng

Aus

tralia

Fran

ce

Sing

apor

e

Belg

ium

Pola

nd

Japa

n

Ger

man

y

Percentage of respondents who used branches for routine transactions in last quarter

Note: 2013 data was excluded where data was not available or not comparable to 2014 data.Sources: Bain/Research Now NPS surveys, 2014; Bain/Research Now and Bain/GMI NPS surveys, 2013

79

68

60

33 33

2014 Developing country 2014 Developed country 2013

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 14

Figure 9: Mobile’s rise came at the expense of online, ATM and branch usage

Canada IndiaSpain

0

20

40

60

80

100%

+15

–11

–3

0

–1

Change(% points)

Change(% points)

Change(% points)

0

20

40

60

80

100%

+8

–3

–3

–1

–1

0

20

40

60

80

100%

2013 2014 2013 2014 2013 2014

+12

–4

–4

–1

–2

Mobile Online ATM Phone Branch

Sources: Bain/Research Now NPS surveys, 2014; Bain/Research Now and Bain/GMI NPS surveys, 2013

Total interactions in last quarter

Figure 10: With the rise of mobile, even online usage has started to decline

0

20

40

60

80

100%

Percentage of respondents using channel in US

Phone

Mobile

2012 2013 2014

Online–5–3

20

–5

2012–2014change

(% points)

Branch

Note: Online and branch include transactions, sales and service.Source: Bain/Research Now US NPS surveys, 2012–2014

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 15

Figure 11 : Mobile has overtaken online in most markets

5

15

25

35

45

55%

5 15 25

2013

35 45 55%

UK

Australia

US

Online interactions as a percentage of total interactions

Mobile interactions as a percentage of total interactions

Spain

France

Italy

Belgium

Hong Kong

China

Singapore

IndonesiaJapan India CanadaMexico

Mobile exceeds online

Online exceeds mobile

2014

Note: Country excluded where 2013 data was not available or not comparable to 2014 data.Source: 2014 Bain/Research Now NPS surveys; 2013 Bain/Research Now and Bain/GMI NPS surveys

Figure 12: Customers who are promoters of their bank were far more likely than detractors to use mobile banking apps

US

Poland

Canada

Belgium

UK

Hong Kong

Spain

SingaporeAustralia

Mexico

Respondents using mobile banking apps as a percentage of total respondents, 2014

3543

3139

4148

4050

4050

45

60

40

59

39

51

26 30

5162

Detractor Promoter

Note: Includes traditional bank respondents only.Source: Bain/Research Now NPS surveys, 2014

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 16

Figure 13: Most customers used both digital and physical channels

Figure 14: Omnichannel customers are more loyal and more engaged

Traditional banks' Net Promoter Scores in US, 2014

11 10

Low

22

Medium

27

High

31

Branch-only

Digital-only

2.4 2.6 3.0 3.2 3.2

0

10

20

30

40%

Average number of products owned

Omnichannel users gave higher Net Promoter Scores and held more products at their primary bank

They are more engaged, especially through digital channels

OmnichannelLow Medium High

Branch-only

Digital-only

Omnichannel

Note: Branch-only, omnichannel and digital-only include respondents who interact via ATM and phone. Source: Bain/Research Now US NPS surveys, 2014

0

20

40

60

80

9

24

13

26

68

Average number of interactions in last quarter, traditional bank respondentsin US, 2014

Mobile Online ATM Phone Branch

Number of digital interactionsNumber of digital interactions

0

20

40

60

80

100%

Chi

na

Indo

nesi

a

Indi

a

Braz

il

Italy

Mex

ico

Can

ada

US

Spai

n

Thai

land

Mal

aysi

a

UK

Aus

tralia

Hon

g Ko

ng

Fran

ce

Pola

nd

Belg

ium

Sing

apor

e

Portu

gal

Ger

man

y

Japa

n

Percentage of traditional bank respondents, 2014

Branch-only users Digital-only users Omnichannel users

Note: Branch only, omnichannel and digital only include respondents who interact via ATM and phone. Source: Bain/Research Now NPS surveys, 2014

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 17

Figure 15: The omnichannel difference applies across all countries

–20

–10

0

10

20

Mexico

–7 –9

4

Brazil–16

–8

5

Canada

–8

–17

5

US

–9 –11

7

Percentage point difference in Net Promoter Scores relative to traditional banks' average, 2014

1.2 0.6 1.3 0.7Increase in productownership frombranch-only users toomnichannel users

Increase in productownership frombranch-only users toomnichannel users

Increase in productownership frombranch-only users toomnichannel users

–20

–10

0

10

20

–21

1 0

–28

–11

4 6

–6–9

6

–14

–7

6

–16

–10

7

–21

–8

8

–19

–13

12

–13

–5

20

Indonesia India China

–45 –34

Australia Singapore Hong Kong Malaysia Thailand Japan

2.3 1.9 2.7 1.1 1.5 2.7 1.5 1.5 0.7

Americas

Asia-Pacific

Europe

–20

–10

0

10

20

–9

–2

3

–12

–6

5

–8 –7

5

–22

–5

5

–16

–9

6

–8–6

7

–7 –6

9

–6–10

9

France Spain UK Poland Italy Belgium Germany Portugal

0.8 1.2 1.0 0.6 1.2 1.2 0.8 0.9

Branch-only users Digital-only users Omnichannel users

Note: Branch only, omnichannel and digital only include respondents who interact via ATM and phone. Source: Bain/Research Now NPS surveys, 2014

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 18

0 20 40 60%

20

25

13

28

25

25

30

28

38

30

40

0 20 40 60%

18

18

19

21

27

31

31

44

45

39

56

0 20 40 60%

Bank's tablet app 15

Bank'ssmartphone app 15

Nonaffiliatedfinancial adviser 23

Phone call withbank 15

TV, radio, printadvertising or media

19

Email from bank 19

Friend or family 28

Nonaffiliatedwebsite 23

Mail from a bank 28

Employee at a bank branch 40

Bank's website 40

Percentage of purchasers using sources for research and decisions, 2014

0 20 40 60%

23

26

29

45

32

29

42

32

32

39

45

0 20 40 60%

18

20

21

25

26

26

32

33

37

37

47

SavingsCredit card (primary)

Home mortgages Weighted averageChecking

Human Digital Other

Note: Average is weighted by product purchases.Source: 2014 Bain/Research Now survey of product purchasers

Figure 16: Customers used both digital and human sources when researching and making purchases in the US

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 19

Figure 17: The human touch remains important for loyalty when people are looking to buy new products

0

10

20

30

40

50%

Friend orfamily

member

Employeeat a bankbranch

Bank'swebsite

TV, radio,print

advertisingor media

Emailfrom bank

Non-affiliatedwebsite

Mail frombank

Bank'smobileapp

Phone callwith bank

Bank'stablet app

Non-affiliated

bankadviser

Respondents' Net Promoter Scores, by source used for product research and purchase decisions in the US, 2014

Source: 2014 Bain/Research Now survey of product purchasers

Human Digital Other

4440

37 36 35 33 33 32

2623

19

Figure 18: A virtuous circle of more channels, greater loyalty, more money

Average numberof products owned

Number ofinteractions

–20

–10

0

10

20%

–13

–1

6

Branch-only users

Low Medium High

2.3 2.8 3.2

–20

–10

0

10

20%

–8

0

6

Digital-only users

Low Medium High

2.3 2.6 2.9

–20

–10

0

10

20%

9

15

19

Omnichannel users

Net Promoter Scores of traditional bank respondents in Germany, 2014

Low Medium High

3.2 3.6 3.7

Note: Branch-only, omnichannel and digital-only users include respondents who interact via ATM and phone.Source: Bain/Research Now Germany NPS survey, 2014

3.Product purchasing and ownershiptrends

• Globally, more than one-third of respondents bought fi nancial products from a provider that was not their primary bank. That behavior was most pervasive in Asia, where a growing share of consumers are buying fi nancial products for the fi rst time, and least common in Western Europe. These hidden defectors bought high-value prod-ucts in many cases, especially credit cards, loans, investments and insurance.

• Loyalty has a strong effect on additional product purchases at the primary bank. Promoters were more likely to buy from their bank than were detrac-tors. This held true across almost every product in every country.

• The specific product effect varies by country because of regulatory and market structure differ-ences. In the UK, the promoter uplift was strongest for pension products and weakest for checking accounts. In Germany, the greatest uplift came in instant-access accounts and life insurance. In the US and Japan, by contrast, auto loans had the greatest uplift.

• In retail banking, Bain estimates the lifetime value of a promoter is worth 2 to 2.5 times that of a detractor, depending on the national market, type of bank and wealth of the customer. That multiple stems largely from promoters’ tendency to buy more products from their bank, combined with their stay-ing longer and recommending the bank to others.

• Banks have more latitude to infl uence customers’ purchases than they might realize. About one-third of respondents said that they were not planning to apply for a credit card but, upon receiving an offer, decided to accept the card. Product offers had a lower but still signifi cant role in checking and mortgage products.

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 22

Figure 19: Hidden defection exists everywhere, especially in developing markets

Figure 20: Hidden defectors often bought high-value products, such as lending, investments and insurance

0

20

40

60

80

100%

Potu

gal

Thai

land

Japa

n

Pola

nd

Hon

g Ko

ng

Italy

Spai

n

Mex

ico

Aus

tralia

Indi

a

Sout

h Ko

rea

Can

ada

Mal

aysi

a

Fran

ce

Sing

apor

e

Ger

man

y

US

Chi

na UK

Belg

ium

Braz

il

Indo

nesi

a

Percentage of products purchased at a bank other than primary bank, 2014

Source: Bain/Research Now NPS surveys, 2014

Deposit Credit card Loans Investment Insurance Other

Developing country Developed country

0

10

20

30

40

50

60

70%

Developed country average: 28%

Mal

aysi

a

68

Chi

na

63

Hon

g Ko

ng

53

Thai

land

51

Sing

apor

e

48

Indi

a

Indo

nesi

a

Sout

h Ko

rea

40

UK

37

Mex

ico

32

Braz

il

28

Spai

n

28

US

Pola

nd

Japa

n

Can

ada

Ger

man

y

Aus

tralia

19

Fran

ce

17

Portu

gal

17

Italy

17

Belg

ium

17

Percentage of respondents who purchased at a bank other than their primary bank, 2014

Developing country average: 47%

4644

2725 24 23 23

Source: Bain/Research Now NPS surveys, 2014

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 23

Figure 21: Customers who are promoters were far more likely than detractors to buy their next product from their primary bank

82 9074

83

49

70

44 48 48

84

44

74

5370

587253

6550

76

Checking account

Term deposit

Savings account

Personal loan

Credit card (secondary)

Investment management

Home loan

Investment property loanSmall business account

Credit card (primary)

Purchases made at primary bank as a percentage of all purchases in that category in Australia, 2014

Detractor Promoter

Source: Bain/Research Now Australia NPS survey, 2014

Figure 22 : Banks have leeway to infl uence product purchases, especially in credit cards

0

20

40

60

80

100%

Percentage of purchasers of financial products in the US, 2014

Home mortgage Checking Savings account Credit card (primary)

I was looking to buy it

Received an offer and decided

to get it

Source: 2014 Bain/Research Now survey of product purchasers

Customer loyalty in retail banking: Global edition 2014 | Bain & Company, Inc.

Page 24

Further reading

• “Winning operating models that convert strategy to results,” Marcia Blenko, Eric Garton, Ludovica Mottura

and Oliver Wright, Bain Brief, December 2014.

• “Rebooting IT: Why fi nancial institutions need a new technology model,” Mike Baxter, Steve Berez and Vishy

Padmanabhan, Bain Brief, September 2014.

• “Building the retail bank of the future,” Mike Baxter and Dirk Vater, Bain Brief, June 2014.

• “Digital-Physical mashups,” Darrell Rigby, Harvard Business Review, September 2014.

Appendix: Methodology

Bain & Company partnered with Research Now, the online global market research organization, to survey consumer

panels in Australia, Belgium, Brazil, Canada, China, France, Germany, Hong Kong, India, Indonesia, Italy, Japan,

Malaysia, Mexico, Poland, Portugal, Singapore, South Korea, Spain, Thailand, the UK and the US. The survey’s

purpose was to gauge customers’ loyalty to their principal bank and the underlying reasons customers hold the views

they do. Conducted between July and November 2014, the survey polled 82,914 consumers of national branch net-

work banks, regional banks, private banks, direct banks, community banks and credit unions in these countries.

Additionally, in Brazil, we also conducted face-to-face interviews with roughly 1,200 customers. In the Americas and

Europe, for the individual bank analysis, we included only those banks for which we received at least 200 valid responses.

In Asia, we included banks with at least 100 responses. In many instances, sample sizes exceeded these thresholds.

Survey questionsRespondents were fi rst asked to identify their primary bank, after which they were asked the following questions to

assess their loyalty to that institution:

• On a scale of zero to 10, where zero represents “not at all likely” and 10 represents “extremely likely,” how

likely are you to recommend your primary bank to a friend or relative?

• Tell us why you gave your primary bank the score you did.

We asked what major products respondents hold with their primary bank and with other banks, and which of these

products were purchased in the past year. We also asked which channels they use to do their banking. The remaining

questions elicited demographic profi le information: household income, investable assets and region of residence.

We followed up with 602 US respondents to ask more detailed questions about their purchase of specifi c products,

including the methods they used to research their purchases and the channel they used to purchase the product.

On the question of statistical signifi cance, the results of our data analysis are robust both for the measurement of

bank NPS by country and for respondent NPS for each demographic category. For the Americas and Europe, the

NPS measured for each bank in the country and US regional rankings is statistically significant to an 80%

confi dence level, with a two-tailed test of the confi dence interval ranging from ±2.6% (n=1,189) to ±6.5% (n=200).

In Asia, where sample sizes were smaller, confi dence intervals are wider, with a maximum of ±9.5%.

Countries classifi ed as developed are based on the World Bank’s high-income category; the developing countries

are based on the World Bank’s middle- and low-income categories.

Acknowledgments

This report was prepared by Gerard du Toit and Maureen Burns, partners in Bain’s Financial Services practice,

and a team led by Christy de Gooyer, a practice area director, and Shilpi Goel, a project leader. Team members

are Alejandro Gonzalez, Devyani Gupta, Alexandra Reuter, Ricardo Sherwell and Abheek Talukdar. The authors

thank Bain partners in each of the countries covered in the report for their valuable input and John Campbell for

his editorial support.

Key contacts in Bain’s Global Financial Services practice

Global: Philippe De Backer in Dubai ([email protected]) Edmund Lin in Singapore ([email protected])

Americas: Mike Baxter in New York ([email protected])

Europe, Middle East and Africa: Henrik Naujoks in Düsseldorf ([email protected])

Asia-Pacifi c: Gary Turner in Sydney ([email protected])

NPS® is a registered trademark of Bain & Company, Inc., Fred Reichheld and Satmetrix Systems, Inc.Net Promoter ScoreSM is a trademark of Bain & Company, Inc., Fred Reichheld and Satmetrix Systems, Inc.

For more information, visit www.bain.com

Amsterdam • Atlanta • Bangkok • Beijing • Boston • Brussels • Buenos Aires • Chicago • Copenhagen • Dallas • Dubai • Düsseldorf • Frankfurt

Helsinki • Hong Kong • Houston • Istanbul • Jakarta • Johannesburg • Kuala Lumpur • Kyiv • London • Los Angeles • Madrid • Melbourne

Mexico City • Milan • Moscow • Mumbai • Munich • New Delhi • New York • Oslo • Palo Alto • Paris • Perth • Rio de Janeiro • Rome • San Francisco

Santiago • São Paulo • Seoul • Shanghai • Singapore • Stockholm • Sydney • Tokyo • Toronto • Warsaw • Washington, D.C. • Zurich

Shared Ambit ion, True Re sults

Bain & Company is the management consulting fi rm that the world’s business leaders come to when they want results.

Bain advises clients on strategy, operations, technology, organization, private equity and mergers and acquisitions. We develop

practical, customized insights that clients act on and transfer skills that make change stick. Founded in 1973, Bain has 51 offi ces

in 33 countries, and our deep expertise and client roster cross every industry and economic sector. Our clients have outperformed

the stock market 4 to 1.

What sets us apart

We believe a consulting fi rm should be more than an adviser. So we put ourselves in our clients’ shoes, selling outcomes, not

projects. We align our incentives with our clients’ by linking our fees to their results and collaborate to unlock the full potential

of their business. Our Results Delivery® process builds our clients’ capabilities, and our True North values mean we do the right

thing for our clients, people and communities—always.