Embed Size (px)

Citation preview

Accountancy Business and the Public Interest 2018

202

Corporate Social Responsibility (CSR) Standards and Reporting: Conventional (Australian) Banks Versus Islamic Bank s

Dr. Mansoor Khan Lecturer in Accounting

School of Commerce, University of South Australia PO Box 2471, Adelaide, SA 5001; Email: [email protected]

Abstract Conventional banks and Islamic banks follow quite opposite ideologies and modalities for conducting their business affairs, but both recognise corporate social responsibility (CSR) as a key to securing community support, sustainability and success. This paper explores CSR initiatives at the Big Four Australian banks and 10 major Islamic banks. It observes that conventional (Australian) banks follow universal standards in measuring and reporting their CSR performance, whereas Islamic banks exhibit inconsistent and unsatisfactory CSR standards and reporting despite the fact that they came into being to serve a humanitarian and societal agenda. There are increasing pressures on Islamic banks to meet their CSR commitments. Islamic banks may take advantage of the rich experience of Australian and other conventional banks to develop their CSR framework based on Shariah principles and underlying socio-economic conditions of Muslim business and society. By adopting the very intensified and universal CSR standards, Islamic banks stand a better chance to win greater legitimacy, community support, market share and long-term success. Keywords – Business sustainability, community expectations, ethical finance, humanitarian aids, societal and environmental causes, supply chain

1. Introduction There has been a growing pressure from stakeholders and community groups on business firms to incorporate societal and environmental dimensions in their corporate strategies and reporting. Business firms have gradually learned that their CSR initiatives are the key to their long-term success in globally competitive markets. They have been developing their corporate strategies within social and environmental frameworks. Research studies find that business firms with consistent CSR performance are able to secure greater financial success because they enjoy stronger community support (Gray et al., 1996; Porter and Kramer 2006; Adams and Whelan, 2009). Business firms are an integral part of communities and they hold an implied social contract to utilize community resources in the best interest of people. They pursue their corporate goals within societal dimensions and engage different stakeholder groups to devise their CSR policies (Wood 1991; Donaldson and Dunfee, 1999; Beckmann et al., 2006; Chaudary et al., 2016; Kabir and Thai, 2017). They provide a full account of their CSR performance to their stakeholders and community groups. International business firms are now more actively engaged in CSR initiatives in host and developing countries to win greater local and global community support for their operations (Deegan, 2000; Jenkins, 2005; Hossain et al., 2016).

Accountancy Business and the Public Interest 2018

203

Financial and banking institutions are also keen to register a very strong CSR performance. They pursue a vigorous CSR agenda of serving their customers, employees, shareholders, community, suppliers and environment. They work on developing socially responsible and sustainable solutions to the financial problems of business and community groups. They do business with the parties which hold impressive CSR credentials. Their CSR-based corporate behaviours help them to earn higher profits and reduce the financial and social costs of legal disputes, litigations and regulations (Ogrizek, 2002; Bihari and Pradhan, 2011; Hadfield-Hill, 2014; Jain et al., 2015; Cornett et al., 2016). Islamic banks follow their CSR initiatives with deeper ethical and social conscience. They promote business dealings on the basis of Islamic economic principles such as risk-sharing, equity, mutual cooperation, community welfare and social justice. They offer universal solutions for the growing socio-economic problems of the contemporary human polity (Chapra, 1985; Siddiqi, 2000). In 2015, the Islamic banking and finance industry consisted of 400 financial institutions in 75 countries across the globe (Islamic Financial Services Industry Stability Report 2016; The World Bank’s Financial Development Report 2014). The 2016 Moody’s Report on Islamic banks observes that Islamic banking has been growing at a faster rate than conventional banking in the global finance (www.moodys.com). Islamic banks are fully capable to attract main stream ethical finance and investments across the globe. This research paper explores CSR standards and reporting at conventional banks and Islamic banks so as to appraise which party is more committed in serving the community and environment. It compares and contrasts the CSR initiatives at the Big Four Australian banks and 10 major Islamic banks worldwide. It relies on secondary data available in annual reports, media reports, websites and other sources to examine CSR initiatives at these Australian banks and Islamic banks. This paper is organized as follows. Section 2 presents a literature review on CSR in the global business and finance. Section 3 undertakes a theoretical discussion on CSR initiatives at conventional banking and Islamic banking. Section 4 gives an account of data and analytical techniques used in this study. Section 5 explores the CSR standards and reporting at the Big Four Australian banks. Section 6 evaluates the CSR standards and reporting at 10 major Islamic banks in order to capture the main CSR themes prevailing in the worldwide Islamic banking industry. Section 7 extends a critique over the CSR initiatives at Australian banks and Islamic banks. The summary and conclusions are presented at the end of this paper.

2. Literature Review The discussion on CSR took cognizance in academic and research circles in the 1950s. Earlier, traditionalists such as Friedman contended that businesses hold a sole responsibility of maximizing their profit and shareholder wealth – ‘The business of business is business.’ There should not be any additional burden or detractor for businesses to contribute towards the community

Accountancy Business and the Public Interest 2018

204

welfare. Businesses pursuing higher profits and market efficiency are in fact serving the CSR cause (Friedman, 1962, 1970). However, a number of scholars from the opposite camp argued that businesses should integrate ethical, social and economic dimensions in their corporate strategies and decision making for their long-term success and sustainability (Bowen, 1953; Freeman, 1984; Schuman, 1995). The Friedman’s vision gathered more criticism as being too narrow and selfish. The increasing prominence and acceptance of stakeholder theory, legitimacy theory, stewardship theory and political economy in modern business and society have broadened the role of business entities in economic, social and environmental arenas. A large number of research studies observed that the financial performance and CSR initiatives of business firms are complementary to each other and henceforth increasingly interrelated. Business firms with proven societal and environmental credentials secure stronger legitimacy and higher profits. Business firms are keen to deliver social welfare to broaden their economic base for profit making (Pava and Krausz, 1996; Porter and Kramer, 2006; Lu, Abeysekera and Cortese, 2015; Fish and Wood, 2017). Business firms and community have developed a better understanding about their respective roles in serving each other’s interest. Business firms rely on community resources to survive and succeed in the market. Thus, they are under ethical obligations to contribute towards the socio-economic and political developments of the community (Gray et al., 1996; Donaldson and Dunfee, 1999; Simms, 2002; Gray et al., 2014; Schnurbein, Seele and Lock, 2016). Due to increasing community expectations and awareness, business firms have largely aligned their economic focus with the social paradigm. They are very conscious about the ever-changing socio-economic landscapes wherein they foresee that their economic success is increasingly based on contributing towards the community’s welfare. They incorporate societal undertakings into their corporate operations and CSR reporting. They have been positioning themselves as democratic institutions and responsible corporate citizens to win legitimacy and community support so as to survive in the competitive global markets (Carroll, 2004; Porter and Kramer, 2006; Usman and Amran, 2015; Dobbs and Staden, 2016). Financial institutions have developed a very unique CSR focus. They have been working hard to transform their traditional role into a more socially and environmentally responsible one – serving societal and environmental causes. They handle funds and resources of the community and thereby bear strong impacts on the socio-economic and political developments of community. They strive to maximize their customer satisfaction by offering a ray of efficient products and services. They integrate environmental and social sustainability criteria into their project and investment appraisal techniques. They undertake socially and environmentally responsible financing and investment operations to promote sustainable communities and environment. They do business with parties holding proven CSR credentials. They assume a very effective role in reducing global warming, environmental pollution, wastes and cost of legal claims and regulations in the business and society (Ogrizek, 2002; Jain et al., 2015; Cornett et al., 2016; Narayanan and Adams, 2016). It is encouraging to see that financial institutions in developing markets

Accountancy Business and the Public Interest 2018

205

have been showing a marked improvement in their CSR performance and reporting over the recent years (Bihari and Pradhan, 2011; Hu and Scholtens, 2012; Hadfield-Hill, 2014; Patwary and Rahman, 2015). A number of recent studies have explored CSR dimensions in Islamic business and financial institutions. For example, some scholars observe that Islamic business firms have a very poor CSR performance. However these business firms have been showing more awareness to incorporate societal and environmental dimensions in their corporate behaviours (Anuar et al., 2004; Yaha et al., 2004). A number of research studies observe a very dismal CSR performance and reporting at Islamic banks (Maali et al., 2003; Haniffa and Hudaib, 2007; Hassan et al., 2010; Farook et al., 2011; Rashid et al., 2013). A research study observes that Islamic banks do not put satisfactory efforts in serving the credit and financial needs of small enterprises and other under-privileged groups in society (Aggarwal and Youssef 2000). Another research study conducts the regression analysis on data collected from annual reports of 47 Islamic banks across 14 countries to explore their CSR initiatives. It observe that the selected Islamic banks follow many and varied CSR standards and practices which are determined by key factors such as public influence, Sharaih board governance, level of social and political freedom and proration of investment account deposits to total assets (Haniffa and Cooke, 2001). However, Islamic banks have been gradually improving their CSR performance and reporting under increasing community and market pressures (Hassan et al., 2010; Khan, 2013; Belal et al., 2015; Rania and Farid, 2016).

3. CSR Theoretical Dimensions: Conventional Banking Versus Islamic Banking Conventional banks perform an intermediary role by charging a fixed rate of interest on loaned capital from borrowers and giving the predetermined rate of return to depositors on their deposits. They assign a great deal of value to creditworthiness of borrowers and strongly collaterals to ensure a risk-free return on their financing and investment portfolios. They throw all sorts of business risks on borrowers and entrepreneurs which quash the spirit of social justice and entrepreneurship for optimal returns. They may provide funds to businessmen or borrowers presenting stronger collaterals. Thus bad projects with stronger collaterals may phase out good projects with weaker collaterals. The very risk-averse nature of conventional banks may seriously handicap the scope of wider economic growth and public welfare (Chapra, 1985; El-Ghazali, 1994; Khan and Bhatti, 2008). Conventional banks collect funds from small investors and extend them to big borrowers for investment in multi-billion dollar projects. They do not have an in-built capacity to account for the financing and venture capital needs of small and weaker business and community groups. The very basic modalities of financing and investment at conventional banks could not promote risk-sharing, entrepreneurship, efficiency, sustainability and wider economic growth in the best public interest. Some Western and Islamic scholars strongly criticize conventional banks for largely serving the vested interests of a few

Accountancy Business and the Public Interest 2018

206

capitalists worldwide. Conventional banks facilitate the concentration of power and wealth in the hands of a small group of people. This harbours gross socio-economic inequities, class conflicts and abject poverty. Quite interestingly, the conventional banking and finance system offers a piecemeal solution in terms of humanitarian aids, grants and bail-outs to developing and weaker groups and countries to resolve their socio-economic problems which have been created and compounded by it. Thus, conventional banks do not hold any true humanitarian agenda and capacity to promote communal welfare and altruistic economic behaviours in the global business and community (Weber, 1958; Bulow and Rogoff, 1990; Smith, 2005). Islamic banks came into being to serve the humanitarian and CSR-based agenda in the contemporary business and society. They are governed by Islamic Shariah which lays down a framework for ethical and material developments of individuals and society as a whole. They conduct business and finance operations to ensure a wider circulation of money, equitable distribution, healthy consumption, community spending, capital formation and risk-sharing business environment. They strictly refrain from engaging in all sorts of antisocial and unethical economic activities such as interest, gambling, speculation, hoarding of capital, profiteering, frauds and wine trade. These fundamental Islamic economic principles promote ethical values such as justice, fairness, equality and universal brotherhood in economic and social spheres. Thus Islamic banks hold natural thirst and ability to serve the universal CSR agenda of ensuring optimal utilization of financial resources in the best interest of people (Khan and Mirakhor, 1987; Wilson, 1997; Siddiqi, 2000).

4. Data and Analytical Techniques This research paper relies on secondary and published data available in annual reports, media reports and websites of the Big Four Australian banks and 10 major Islamic banks worldwide. These banks are selected on the basis of their size and weightage in the Australian and Islamic financial markets. The Australian banking sector is largely dominated by the Big Four banks, namely, National Australia Bank (NAB), Commonwealth Bank (CommBank), Australia, New Zealand Banking Group (ANZ) and Westpac Bank (Westpac). They hold 80-85% of the Australian home loan market and their combined total market capitalization at share price in 2016 amounted to $369.28 billion. Even in the 2008-2009 global recession, the concentration of Australian and New Zealand banking and finance industry into the Big Four Australian banks was further strengthened by merging ST. George Bank in to Westpac and Bankwest into Commonwealth Bank. The Big Four Australian banks are also effectively operating and controlling the banking sector of New Zealand. They are globally competitive and follow the International Financial Reporting Standards (IFRS) and Global Reporting Initiative (GRI) standards for reporting their economic, social and environmental initiatives and outcomes. Thus, the Big Four Australian banks stand as ideal candidates to capture the running CSR themes in Australian, New Zealand as well as global financial markets.

Accountancy Business and the Public Interest 2018

207

The sample also comprises of 10 major Islamic banks of the global Islamic banking industry. It includes 8 largest Islamic banks in the Middle Eastern region which is the main hub of Islamic banking over the past decades. It contains Bank Islam Malaysia Berhad which is a key player of Islamic banking practice in Malaysia. It includes Meezan Bank which holds the majority share of Islamic banking sector in Pakistan. Thus the selected Islamic banks are the main trend setters of Islamic banking industry across the globe. They have been making serious efforts to adopt the IFRS and GRI standards to report their economic, social and environmental performance. They hold candid credentials to capture the recent CSR developments in the global Islamic banking industry. This study adopts both quantitative and descriptive analytical techniques to examine secondary and published data of the selected banks. It relies on the ANOVA modalities to analyse the means and t-test statistics of CSR variables of the Big Four Australian banks and 10 major Islamic banks worldwide. The main limitation of this study lies in its use of secondary data and published reports of the selected banks.

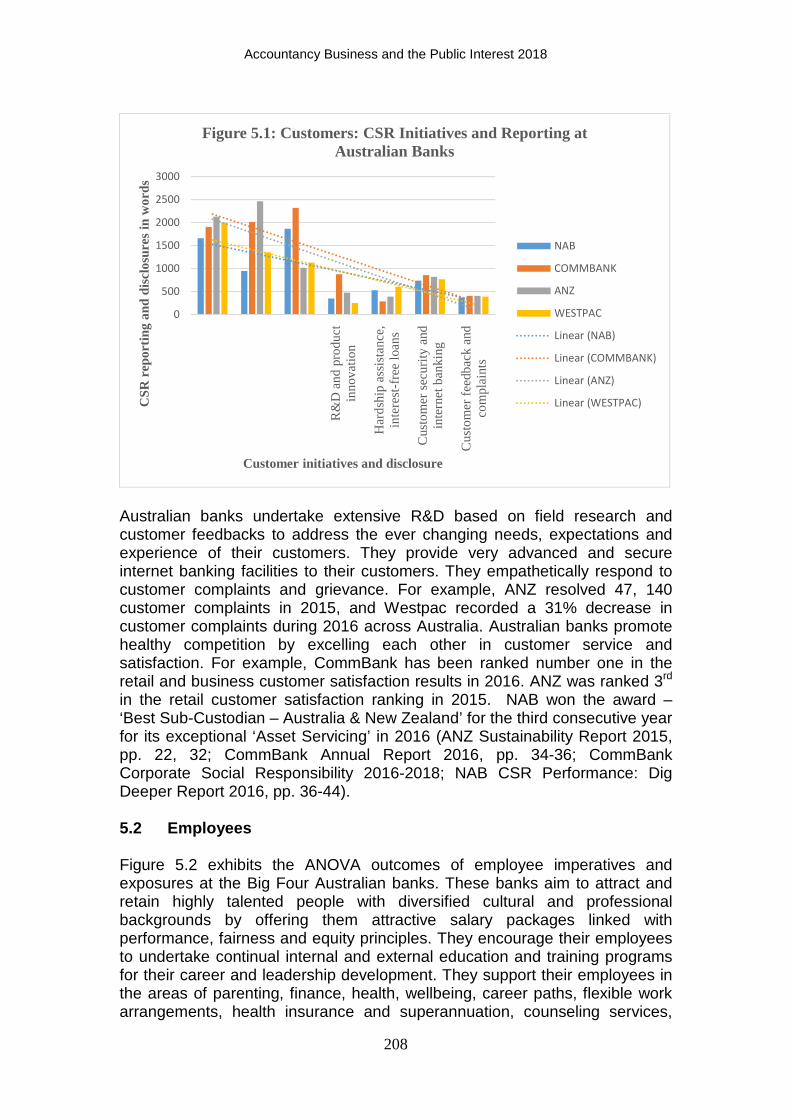

5. Empirical Results: CSR Standards and Reporting a t Australian Banks The forthcoming discussion explores the CSR standards and reporting in the areas of customers, employees, community, environment and supply chain at the Big Four Australian Banks, namely, National Australia Bank (NAB), Commonwealth Bank (CommBank), Australia, New Zealand Banking Group (ANZ) and Westpac Bank (Westpac). 5.1 Customers Figure 5.1 shows the ANOVA results on the customer service imperatives and exposures at the Big Four Australian banks. These banks deliver quality products and services to best serve their personal, business and corporate customers. They undertake socially and environmentally responsible lending and investment decisions to ensure sustainable development of the community and environment. They offer customized solutions to the financing problems of small business and agriculture customers. For example, ANZ delivers special products and services to meet all the banking needs of small and regional businesses. Westpac provides special assistance to businessmen to start or grow their small business. Australian banks grant fee exemptions to war veteran pensioners, minors, students and people with special needs. They help communities in developing their financial literacy and skills and responsible credit practices.They help customers through their financial difficulties in loans and accounts. They offer special products and concessions to support under-served and unbanked communities, social sector, sport clubs, schools and charity organizations. For example, NAB extended $190 million microfinance products since 2005 to help more than 440,000 Australians with low incomes. The bank assisted 21,303 customers through financial hardship in 2016 (NAB CSR Performance: Dig Deeper Report 2016, pp. 36-44). ANZ approved hardship assistance to 43,385 customers in 2015 (ANZ Sustainability Report 2015, p. 33). Westpac helped 30, 579 customers through financial assistance packages in 2016 (Westpac Sustainability Performance Report 2016, p. 2).

Accountancy Business and the Public Interest 2018

208

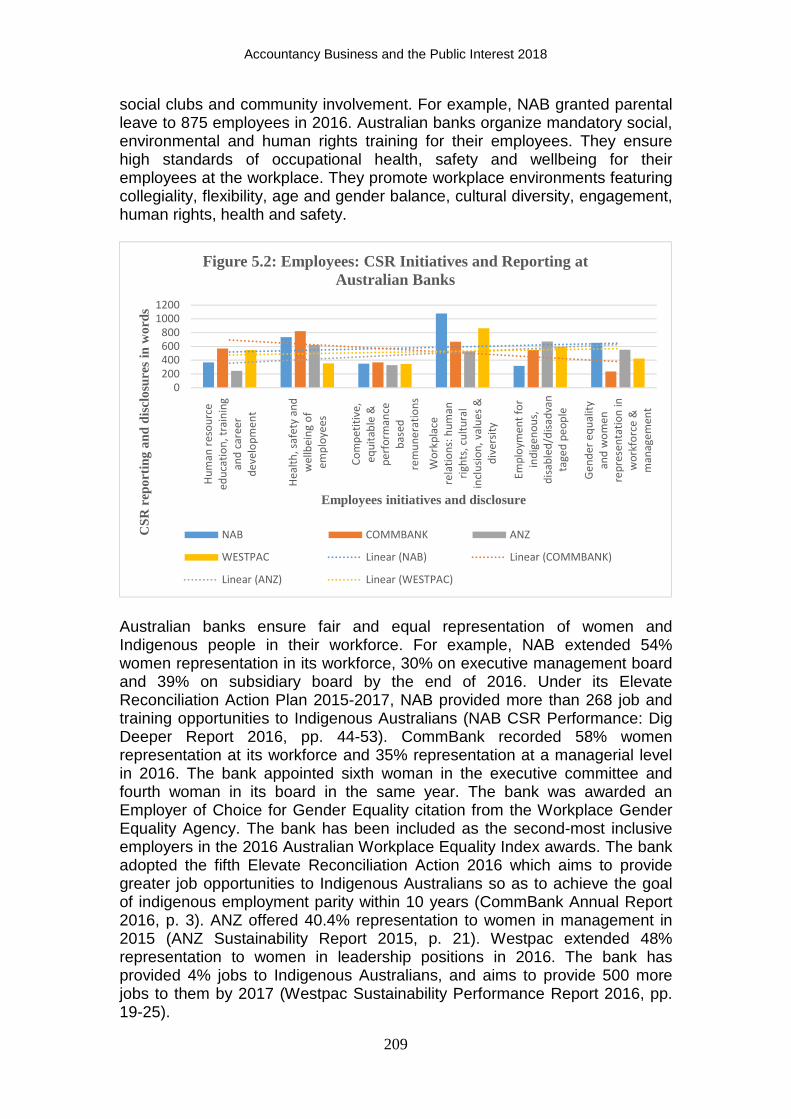

Australian banks undertake extensive R&D based on field research and customer feedbacks to address the ever changing needs, expectations and experience of their customers. They provide very advanced and secure internet banking facilities to their customers. They empathetically respond to customer complaints and grievance. For example, ANZ resolved 47, 140 customer complaints in 2015, and Westpac recorded a 31% decrease in customer complaints during 2016 across Australia. Australian banks promote healthy competition by excelling each other in customer service and satisfaction. For example, CommBank has been ranked number one in the retail and business customer satisfaction results in 2016. ANZ was ranked 3rd in the retail customer satisfaction ranking in 2015. NAB won the award – ‘Best Sub-Custodian – Australia & New Zealand’ for the third consecutive year for its exceptional ‘Asset Servicing’ in 2016 (ANZ Sustainability Report 2015, pp. 22, 32; CommBank Annual Report 2016, pp. 34-36; CommBank Corporate Social Responsibility 2016-2018; NAB CSR Performance: Dig Deeper Report 2016, pp. 36-44). 5.2 Employees Figure 5.2 exhibits the ANOVA outcomes of employee imperatives and exposures at the Big Four Australian banks. These banks aim to attract and retain highly talented people with diversified cultural and professional backgrounds by offering them attractive salary packages linked with performance, fairness and equity principles. They encourage their employees to undertake continual internal and external education and training programs for their career and leadership development. They support their employees in the areas of parenting, finance, health, wellbeing, career paths, flexible work arrangements, health insurance and superannuation, counseling services,

0

500

1000

1500

2000

2500

3000

R&

D a

nd p

rodu

ctin

nova

tion

Har

dshi

p as

sist

ance

,in

tere

st-f

ree

loan

s

Cus

tom

er s

ecur

ity a

ndin

tern

et b

anki

ng

Cus

tom

er f

eedb

ack

and

com

plai

nts

CSR

rep

orti

ng a

nd d

iscl

osur

es in

wor

ds

Customer initiatives and disclosure

Figure 5.1: Customers: CSR Initiatives and Reporting at Australian Banks

NAB

COMMBANK

ANZ

WESTPAC

Linear (NAB)

Linear (COMMBANK)

Linear (ANZ)

Linear (WESTPAC)

Accountancy Business and the Public Interest 2018

209

social clubs and community involvement. For example, NAB granted parental leave to 875 employees in 2016. Australian banks organize mandatory social, environmental and human rights training for their employees. They ensure high standards of occupational health, safety and wellbeing for their employees at the workplace. They promote workplace environments featuring collegiality, flexibility, age and gender balance, cultural diversity, engagement, human rights, health and safety.

Australian banks ensure fair and equal representation of women and Indigenous people in their workforce. For example, NAB extended 54% women representation in its workforce, 30% on executive management board and 39% on subsidiary board by the end of 2016. Under its Elevate Reconciliation Action Plan 2015-2017, NAB provided more than 268 job and training opportunities to Indigenous Australians (NAB CSR Performance: Dig Deeper Report 2016, pp. 44-53). CommBank recorded 58% women representation at its workforce and 35% representation at a managerial level in 2016. The bank appointed sixth woman in the executive committee and fourth woman in its board in the same year. The bank was awarded an Employer of Choice for Gender Equality citation from the Workplace Gender Equality Agency. The bank has been included as the second-most inclusive employers in the 2016 Australian Workplace Equality Index awards. The bank adopted the fifth Elevate Reconciliation Action 2016 which aims to provide greater job opportunities to Indigenous Australians so as to achieve the goal of indigenous employment parity within 10 years (CommBank Annual Report 2016, p. 3). ANZ offered 40.4% representation to women in management in 2015 (ANZ Sustainability Report 2015, p. 21). Westpac extended 48% representation to women in leadership positions in 2016. The bank has provided 4% jobs to Indigenous Australians, and aims to provide 500 more jobs to them by 2017 (Westpac Sustainability Performance Report 2016, pp. 19-25).

0

200

400

600

800

1000

1200

Hu

ma

n r

eso

urc

e

ed

uca

tio

n,

tra

inin

g

an

d c

are

er

de

ve

lop

me

nt

He

alt

h,

safe

ty a

nd

we

llb

ein

g o

f

em

plo

ye

es

Co

mp

eti

tiv

e,

eq

uit

ab

le &

pe

rfo

rma

nce

ba

sed

rem

un

era

tio

ns

Wo

rkp

lace

rela

tio

ns:

hu

ma

n

rig

hts

, cu

ltu

ral

incl

usi

on

, v

alu

es

&

div

ers

ity

Em

plo

ym

en

t fo

r

ind

ige

no

us,

dis

ab

led

/dis

ad

van

tag

ed

pe

op

le

Ge

nd

er

eq

ua

lity

an

d w

om

en

rep

rese

nta

tio

n i

n

wo

rkfo

rce

&

ma

na

ge

me

nt

CSR

rep

orti

ng a

nd d

iscl

osur

es in

wor

ds

Employees initiatives and disclosure

Figure 5.2: Employees: CSR Initiatives and Reporting at Australian Banks

NAB COMMBANK ANZ

WESTPAC Linear (NAB) Linear (COMMBANK)

Linear (ANZ) Linear (WESTPAC)

Accountancy Business and the Public Interest 2018

210

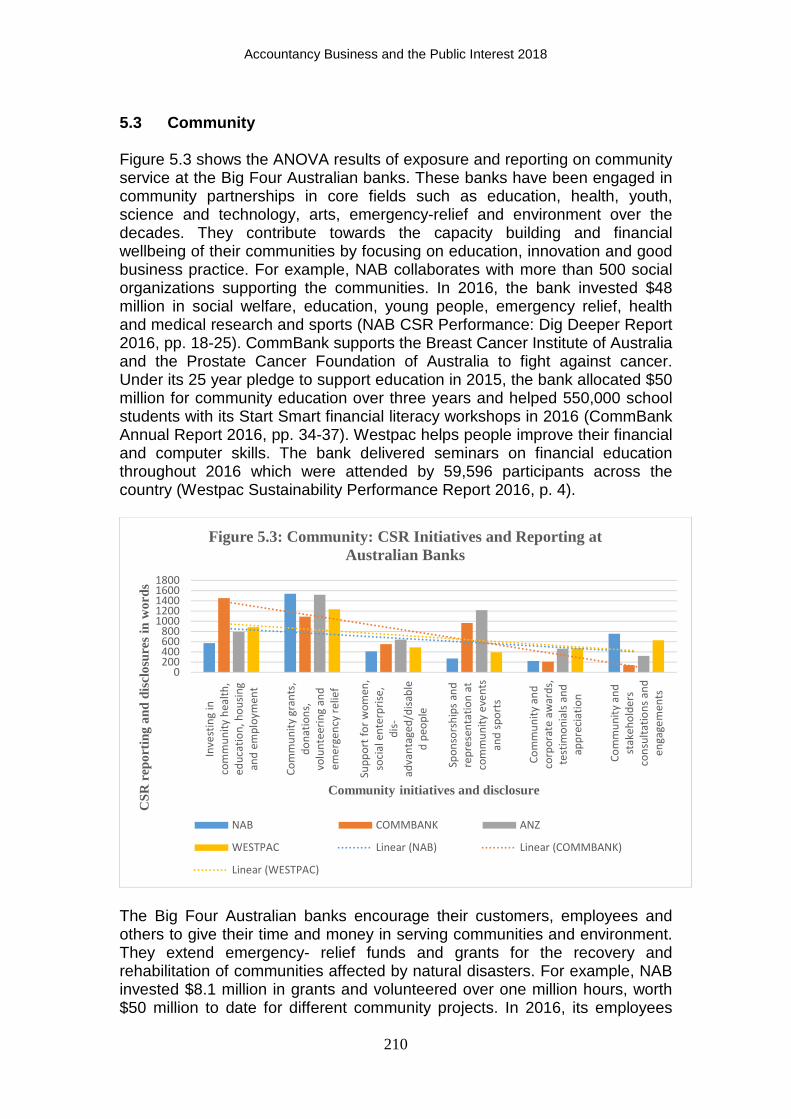

5.3 Community Figure 5.3 shows the ANOVA results of exposure and reporting on community service at the Big Four Australian banks. These banks have been engaged in community partnerships in core fields such as education, health, youth, science and technology, arts, emergency-relief and environment over the decades. They contribute towards the capacity building and financial wellbeing of their communities by focusing on education, innovation and good business practice. For example, NAB collaborates with more than 500 social organizations supporting the communities. In 2016, the bank invested $48 million in social welfare, education, young people, emergency relief, health and medical research and sports (NAB CSR Performance: Dig Deeper Report 2016, pp. 18-25). CommBank supports the Breast Cancer Institute of Australia and the Prostate Cancer Foundation of Australia to fight against cancer. Under its 25 year pledge to support education in 2015, the bank allocated $50 million for community education over three years and helped 550,000 school students with its Start Smart financial literacy workshops in 2016 (CommBank Annual Report 2016, pp. 34-37). Westpac helps people improve their financial and computer skills. The bank delivered seminars on financial education throughout 2016 which were attended by 59,596 participants across the country (Westpac Sustainability Performance Report 2016, p. 4).

The Big Four Australian banks encourage their customers, employees and others to give their time and money in serving communities and environment. They extend emergency- relief funds and grants for the recovery and rehabilitation of communities affected by natural disasters. For example, NAB invested $8.1 million in grants and volunteered over one million hours, worth $50 million to date for different community projects. In 2016, its employees

0200400600800

10001200140016001800

Inv

est

ing

in

com

mu

nit

y h

ea

lth

,

ed

uca

tio

n,

ho

usi

ng

an

d e

mp

loy

me

nt

Co

mm

un

ity

gra

nts

,

do

na

tio

ns,

vo

lun

tee

rin

g a

nd

em

erg

en

cy r

eli

ef

Su

pp

ort

fo

r w

om

en

,

soci

al

en

terp

rise

,

dis

-

ad

va

nta

ge

d/d

isa

ble

d p

eo

ple

Sp

on

sors

hip

s a

nd

rep

rese

nta

tio

n a

t

com

mu

nit

y e

ven

ts

an

d s

po

rts

Co

mm

un

ity

an

d

corp

ora

te a

wa

rds,

test

imo

nia

ls a

nd

ap

pre

cia

tio

n

Co

mm

un

ity

an

d

sta

ke

ho

lde

rs

con

sult

ati

on

s a

nd

en

ga

ge

me

nts

CSR

rep

orti

ng a

nd d

iscl

osur

es in

wor

ds

Community initiatives and disclosure

Figure 5.3: Community: CSR Initiatives and Reporting at Australian Banks

NAB COMMBANK ANZ

WESTPAC Linear (NAB) Linear (COMMBANK)

Linear (WESTPAC)

Accountancy Business and the Public Interest 2018

211

made donations of more than $2 million to over 590 charities under its workplace giving program (NAB CSR Performance: Dig Deeper Report 2016, pp. 18-25). Since 2007, CommBank donated more than $13.7 million to 1,600 Australian youth-focused organizations. The bank’s employees volunteered 31,000 hours to support 264 community organizations during 2016. The bank contributed over $262 million to disaster relief (NAB Annual Report 2016, pp. 1-7, 34-37). ANZ contributes towards the opportunity and prosperity of communities under its ‘GIVE’ program which entails Giving, Investing, Volunteering and Emergency. The bank encourages its employees, customers and shareholders to give regular and once-off donations to community organizations helping poor and needy people. In 2015, the bank’s employees volunteered 108,142 hours in mentoring high school students, formulating social media strategies for a community organization and establishing habitats for native animals (ANZ Sustainability Report 2015, p. 21). Westpac runs the Family of Five Philanthropic Foundations which offer various grants for social enterprises and community organizations. In 2016, the bank made $148 million community contributions and its ‘Westpac Bicentennial Foundation’ with $100 million funding appointed the first 100 Westpac scholars every year in perpetuity. The bank extended special financial and intellectual capital supports to 200 selected ‘Business of Tomorrow Programme’ (Westpac Sustainability Performance Report 2016, p. 4). The Big Four Australian banks are very keen to empower women in their life and money matters. They offer greater education and employment opportunities to Indigenous Australians and other disadvantaged communities. They support farmers, small and regional business by providing them special tailored banking services and buying their products and services. For example NAB provided $20 million in safe and affordable microfinance products and services to over 15,000 Indigenous Australians since 2008. More than 7,000 people have been benefited from its Indigenous money mentor program. The bank also helps small businesses and entrepreneurs with concessional loans from $500-$20,000 and business skills and training to ensure their success in the early years of operations (NAB CSR Performance: Dig Deeper Report 2016, pp. 18-25). Under its 5th Elevate Reconciliation Action Plan, CommBank has been providing greater education, employment, business opportunities and banking facilities to indigenous Australians (CommBank CSR Report 2016-2018). ANZ helped more than 67, 000 people from disadvantaged communities in building their money management skills in 2015 (ANZ Sustainability Report 2015, p. 21). Westpac supports the Salvation Army and Mission Australia in helping the homeless people in the country. The bank’s lending to social and affordable housing sector amounted to $1.05 billion in 2016 (Westpac Sustainability Performance Report 2016, p. 5). The Big Four Australian banks extend generous donations and sponsorships to different community groups and society events. For example, CommBank encourages talented people in business, education, sports and community by extending them the Australian of the Year Awards, Australian Export Awards, Commonwealth Bank Teaching Awards, CommBank Cricket Club sponsorships, Regional Achievement and Community Awards. The bank

Accountancy Business and the Public Interest 2018

212

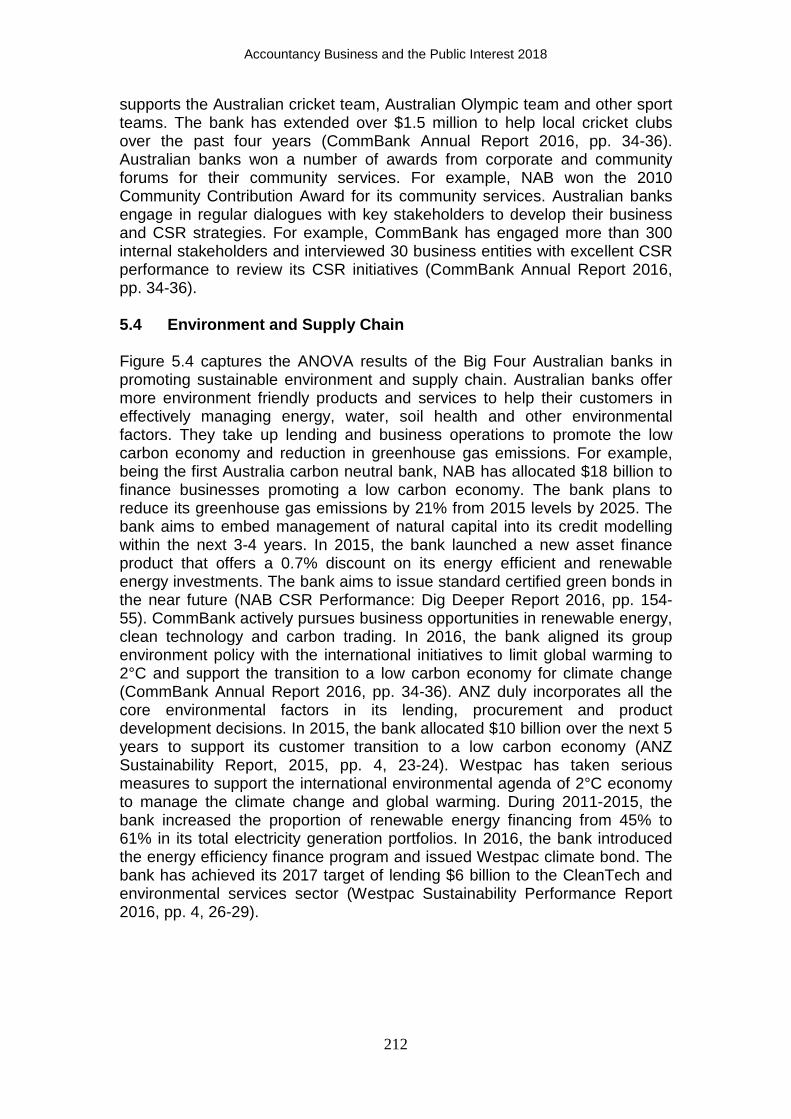

supports the Australian cricket team, Australian Olympic team and other sport teams. The bank has extended over $1.5 million to help local cricket clubs over the past four years (CommBank Annual Report 2016, pp. 34-36). Australian banks won a number of awards from corporate and community forums for their community services. For example, NAB won the 2010 Community Contribution Award for its community services. Australian banks engage in regular dialogues with key stakeholders to develop their business and CSR strategies. For example, CommBank has engaged more than 300 internal stakeholders and interviewed 30 business entities with excellent CSR performance to review its CSR initiatives (CommBank Annual Report 2016, pp. 34-36). 5.4 Environment and Supply Chain Figure 5.4 captures the ANOVA results of the Big Four Australian banks in promoting sustainable environment and supply chain. Australian banks offer more environment friendly products and services to help their customers in effectively managing energy, water, soil health and other environmental factors. They take up lending and business operations to promote the low carbon economy and reduction in greenhouse gas emissions. For example, being the first Australia carbon neutral bank, NAB has allocated $18 billion to finance businesses promoting a low carbon economy. The bank plans to reduce its greenhouse gas emissions by 21% from 2015 levels by 2025. The bank aims to embed management of natural capital into its credit modelling within the next 3-4 years. In 2015, the bank launched a new asset finance product that offers a 0.7% discount on its energy efficient and renewable energy investments. The bank aims to issue standard certified green bonds in the near future (NAB CSR Performance: Dig Deeper Report 2016, pp. 154-55). CommBank actively pursues business opportunities in renewable energy, clean technology and carbon trading. In 2016, the bank aligned its group environment policy with the international initiatives to limit global warming to 2°C and support the transition to a low carbon economy for climate change (CommBank Annual Report 2016, pp. 34-36). ANZ duly incorporates all the core environmental factors in its lending, procurement and product development decisions. In 2015, the bank allocated $10 billion over the next 5 years to support its customer transition to a low carbon economy (ANZ Sustainability Report, 2015, pp. 4, 23-24). Westpac has taken serious measures to support the international environmental agenda of 2°C economy to manage the climate change and global warming. During 2011-2015, the bank increased the proportion of renewable energy financing from 45% to 61% in its total electricity generation portfolios. In 2016, the bank introduced the energy efficiency finance program and issued Westpac climate bond. The bank has achieved its 2017 target of lending $6 billion to the CleanTech and environmental services sector (Westpac Sustainability Performance Report 2016, pp. 4, 26-29).

Accountancy Business and the Public Interest 2018

213

The Big Four Australian banks support the environmental, social and governance (ESG) performance of their suppliers. They promote supplier diversity and integrity and take effective measures to enhance their responsible procumbent and overall EGS performance. For example, ANZ advised its 133 suppliers to ensure their full compliance with the ANZ’s Supplier Code of Practice (SCOP) in order to continue their business affairs with the bank. Australian banks strictly discipline their own environmental performance and footprints in operations. For example, NAB reduced its use of 1.8 million sheets of paper per month in 2016 (NAB CSR Performance: Dig Deeper Report 2016, pp. 154-55). CommBank aims to further improve its environmental performance in Australian property, fleet and procurement activities and also raise its targets for reduction in waste, water and energy usage in operations in 2016. The bank strongly supports environment related activities such as Clean Up Australia Day, Earth Hour and the Great Barrier Reef (CommBank CSR Report 2016-2018). ANZ has been pursuing its environmental targets of reducing its wastes, water and energy use. In 2015, the bank reduced emissions from air travel by 0.7% compared to 2014. The bank aims to improve urban sustainability and increase its lower-carbon gas and renewables power generation lending up to 15-20% by 2020 (ANZ Sustainability Report, 2015, pp. 4, 23-24). Westpac extends interest free loans to employees to install solar panels and solar water systems (Westpac Sustainability Performance Report 2016, p. 26-29). The Big Four Australian banks hold memberships, affiliations and declarations with international bodies promoting sustainable environment. They provide fair exposure about their environmental standards, targets, achievements, corporate awards and appreciations. For example, NAB won the sustainability leadership award at the United Nations Association of Australia (UNAA) World Environment Day Awards 2011. The bank is a signatory of the 2011 Natural Capital Declaration (NCD) (NAB CSR Performance: Dig Deeper 2016, pp.

0200400600800

1000120014001600

En

vir

on

me

nta

l

go

ve

rna

nce

-

en

vir

on

me

nt

frie

nd

ly p

rod

uct

s

an

d s

erv

ice

s

Pro

mo

tin

g l

ow

carb

on

eco

no

my

-

glo

ba

l w

arm

ing

,

EG

S l

en

din

g

Su

pp

lie

r su

pp

ort

,

go

ve

rna

nce

an

d

div

ers

ity

pro

gra

ms

En

vir

on

me

nta

l

foo

tpri

nts

–

red

uct

ion

in

wa

ste

, w

ate

r a

nd

en

erg

y u

se

En

vir

on

me

nta

l

aff

ilia

tio

ns

,

targ

ets

,

ach

ieve

me

nts

an

d

rep

ort

ing

CSR

rep

orti

ng a

nd d

iscl

osur

es in

wor

ds

Environment and supply chain initiatives and disclosure

Figure 5.4: Environment and Supply Chain: CSR Initiatives and Reporting at Australian Banks

NAB COMMBANK ANZ

WESTPAC Linear (NAB) Linear (COMMBANK)

Linear (ANZ) Linear (WESTPAC)

Accountancy Business and the Public Interest 2018

214

154-55). In 2016, CommBank was named to be the number one bank in the world in the Global 100 (G100) Index. The bank was also included in the Dow Jones Sustainability Index, the CDP ASX 200 Climate Disclosure Leadership Index, and the FTSE4Good Index (CommBank Annual Report 2016, p.34-36). Westpac successfully accomplished its 2015 environmental targets. The bank has been engaged in a number of environmental initiatives such as the Climate Partners Network, UN Global Compact, Equator Principles and Advance Green Network (Westpac Sustainability Performance Report 2016, pp. 4, 26-29). Table 5.1 shows the overall ANOVA results which hold that CSR initiatives and exposures at the Big Four Australian banks do not differ significantly (p≤0.1). It implies that the Big Four Australian banks largely follow universal standards to measure and report their CSR targets and outcomes. Table 5.1: The CSR Initiatives and Reporting at Fou r Big Banks in Australia The results of ANOVA showing how the CSR initiatives and reporting differ at the four big Australian banks Source of Variation SS df MS F

P-value F crit

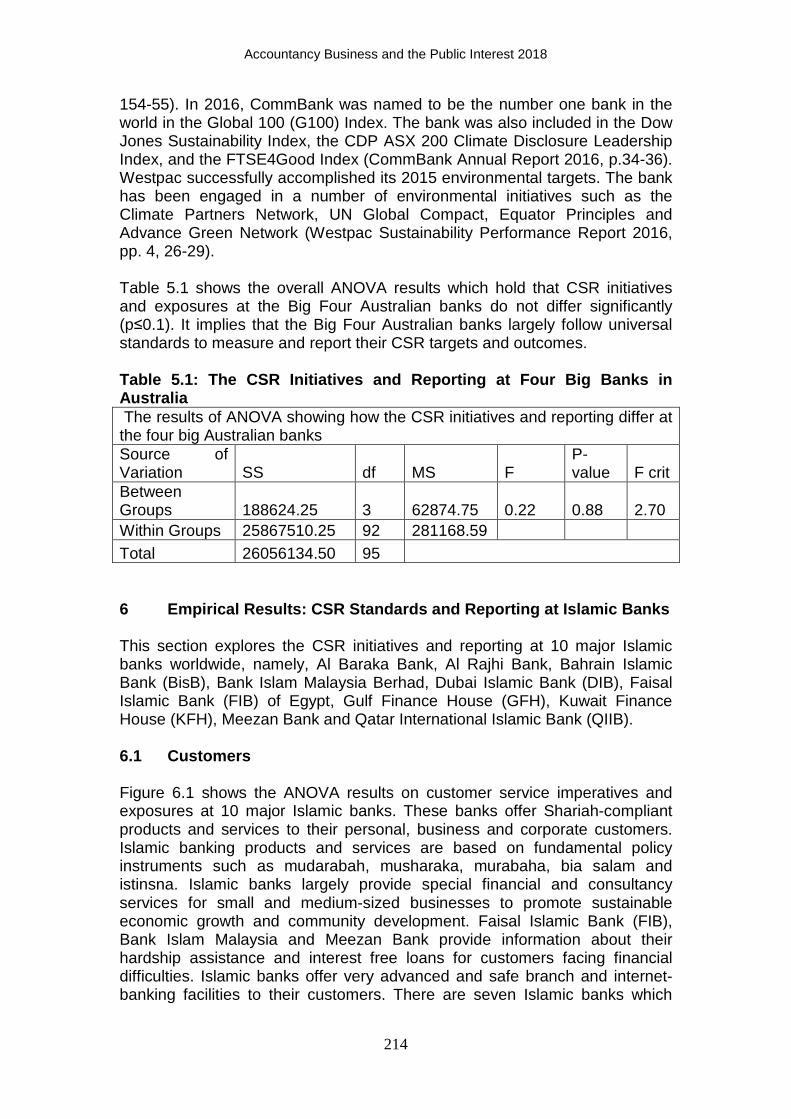

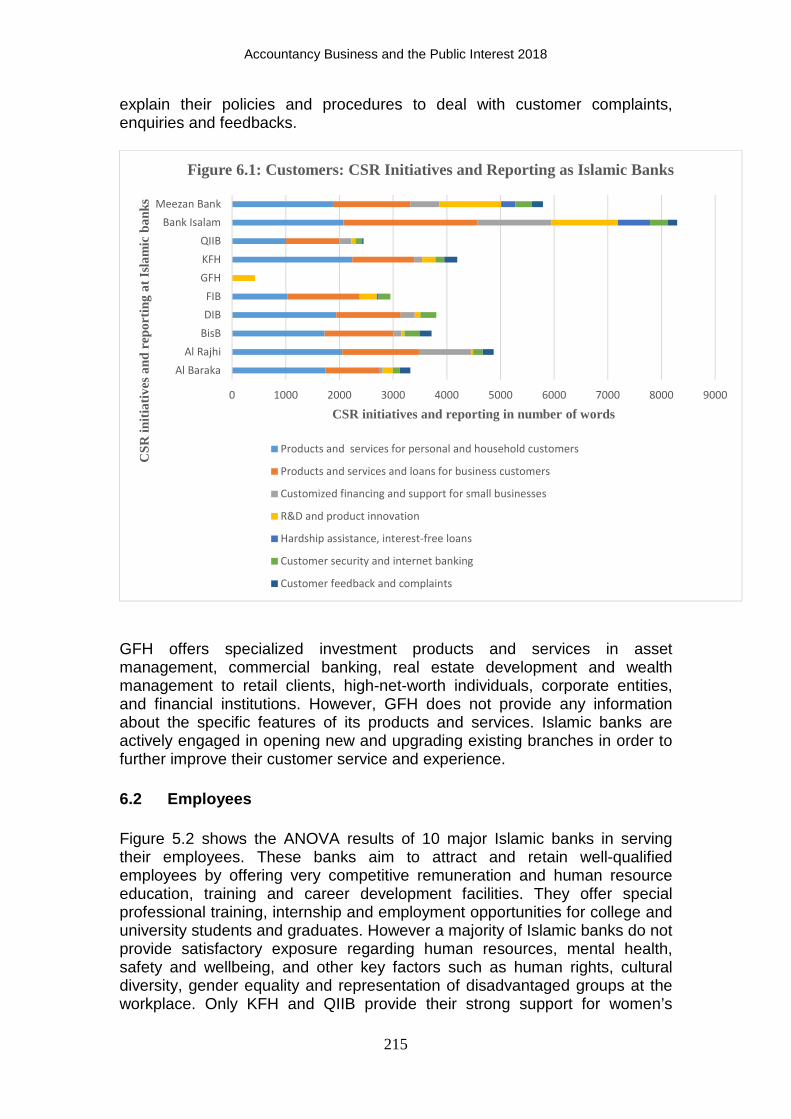

Between Groups 188624.25 3 62874.75 0.22 0.88 2.70 Within Groups 25867510.25 92 281168.59 Total 26056134.50 95 6 Empirical Results: CSR Standards and Reporting at Islamic Banks This section explores the CSR initiatives and reporting at 10 major Islamic banks worldwide, namely, Al Baraka Bank, Al Rajhi Bank, Bahrain Islamic Bank (BisB), Bank Islam Malaysia Berhad, Dubai Islamic Bank (DIB), Faisal Islamic Bank (FIB) of Egypt, Gulf Finance House (GFH), Kuwait Finance House (KFH), Meezan Bank and Qatar International Islamic Bank (QIIB). 6.1 Customers Figure 6.1 shows the ANOVA results on customer service imperatives and exposures at 10 major Islamic banks. These banks offer Shariah-compliant products and services to their personal, business and corporate customers. Islamic banking products and services are based on fundamental policy instruments such as mudarabah, musharaka, murabaha, bia salam and istinsna. Islamic banks largely provide special financial and consultancy services for small and medium-sized businesses to promote sustainable economic growth and community development. Faisal Islamic Bank (FIB), Bank Islam Malaysia and Meezan Bank provide information about their hardship assistance and interest free loans for customers facing financial difficulties. Islamic banks offer very advanced and safe branch and internet-banking facilities to their customers. There are seven Islamic banks which

Accountancy Business and the Public Interest 2018

215

explain their policies and procedures to deal with customer complaints, enquiries and feedbacks.

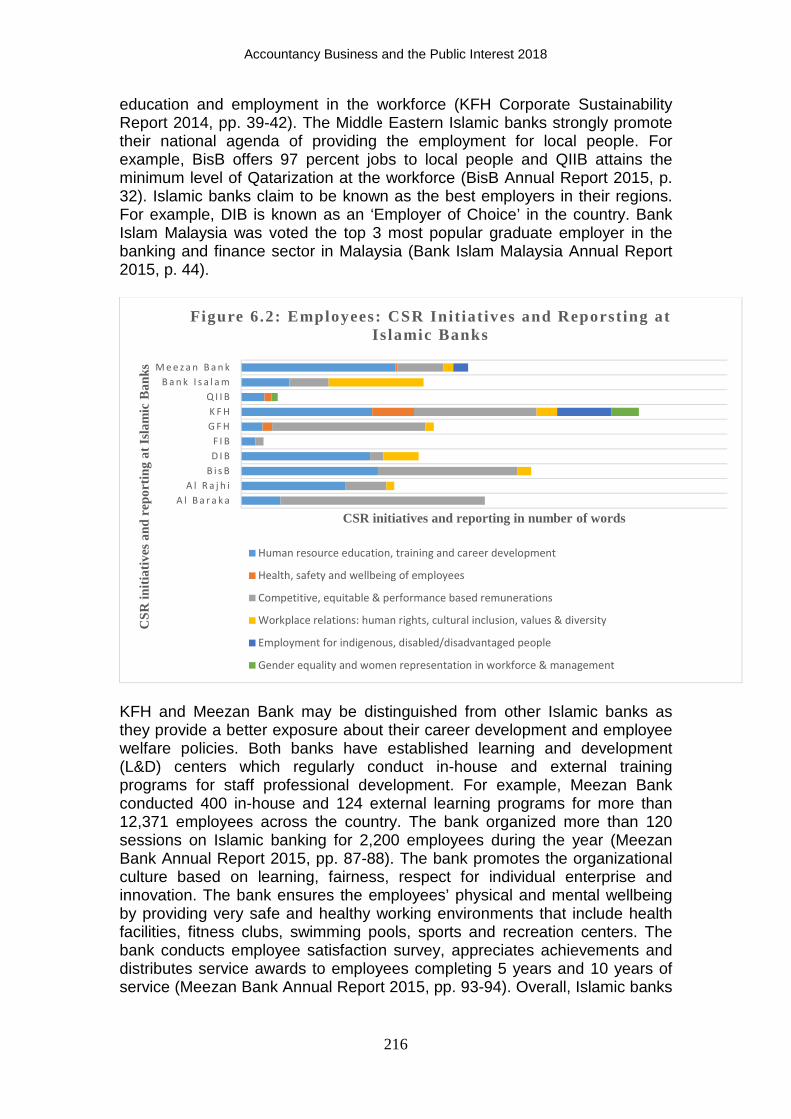

GFH offers specialized investment products and services in asset management, commercial banking, real estate development and wealth management to retail clients, high-net-worth individuals, corporate entities, and financial institutions. However, GFH does not provide any information about the specific features of its products and services. Islamic banks are actively engaged in opening new and upgrading existing branches in order to further improve their customer service and experience. 6.2 Employees Figure 5.2 shows the ANOVA results of 10 major Islamic banks in serving their employees. These banks aim to attract and retain well-qualified employees by offering very competitive remuneration and human resource education, training and career development facilities. They offer special professional training, internship and employment opportunities for college and university students and graduates. However a majority of Islamic banks do not provide satisfactory exposure regarding human resources, mental health, safety and wellbeing, and other key factors such as human rights, cultural diversity, gender equality and representation of disadvantaged groups at the workplace. Only KFH and QIIB provide their strong support for women’s

0 1000 2000 3000 4000 5000 6000 7000 8000 9000

Al Baraka

Al Rajhi

BisB

DIB

FIB

GFH

KFH

QIIB

Bank Isalam

Meezan Bank

CSR initiatives and reporting in number of words

CSR

init

iati

ves

and

repo

rtin

g at

Isl

amic

ban

ks

Figure 6.1: Customers: CSR Initiatives and Reporting as Islamic Banks

Products and services for personal and household customers

Products and services and loans for business customers

Customized financing and support for small businesses

R&D and product innovation

Hardship assistance, interest-free loans

Customer security and internet banking

Customer feedback and complaints

Accountancy Business and the Public Interest 2018

216

education and employment in the workforce (KFH Corporate Sustainability Report 2014, pp. 39-42). The Middle Eastern Islamic banks strongly promote their national agenda of providing the employment for local people. For example, BisB offers 97 percent jobs to local people and QIIB attains the minimum level of Qatarization at the workforce (BisB Annual Report 2015, p. 32). Islamic banks claim to be known as the best employers in their regions. For example, DIB is known as an ‘Employer of Choice’ in the country. Bank Islam Malaysia was voted the top 3 most popular graduate employer in the banking and finance sector in Malaysia (Bank Islam Malaysia Annual Report 2015, p. 44).

KFH and Meezan Bank may be distinguished from other Islamic banks as they provide a better exposure about their career development and employee welfare policies. Both banks have established learning and development (L&D) centers which regularly conduct in-house and external training programs for staff professional development. For example, Meezan Bank conducted 400 in-house and 124 external learning programs for more than 12,371 employees across the country. The bank organized more than 120 sessions on Islamic banking for 2,200 employees during the year (Meezan Bank Annual Report 2015, pp. 87-88). The bank promotes the organizational culture based on learning, fairness, respect for individual enterprise and innovation. The bank ensures the employees’ physical and mental wellbeing by providing very safe and healthy working environments that include health facilities, fitness clubs, swimming pools, sports and recreation centers. The bank conducts employee satisfaction survey, appreciates achievements and distributes service awards to employees completing 5 years and 10 years of service (Meezan Bank Annual Report 2015, pp. 93-94). Overall, Islamic banks

A l B a r a k a

A l R a j h i

B i s B

D I B

F I B

G F H

K F H

Q I I B

B a n k I s a l a m

M e e z a n B a n k

CSR initiatives and reporting in number of words

CSR

init

iati

ves

and

repo

rtin

g at

Isl

amic

Ban

ks

Figure 6.2: Employees: CSR Init iatives and Reporsting at Is lamic Banks

Human resource education, training and career development

Health, safety and wellbeing of employees

Competitive, equitable & performance based remunerations

Workplace relations: human rights, cultural inclusion, values & diversity

Employment for indigenous, disabled/disadvantaged people

Gender equality and women representation in workforce & management

Accountancy Business and the Public Interest 2018

217

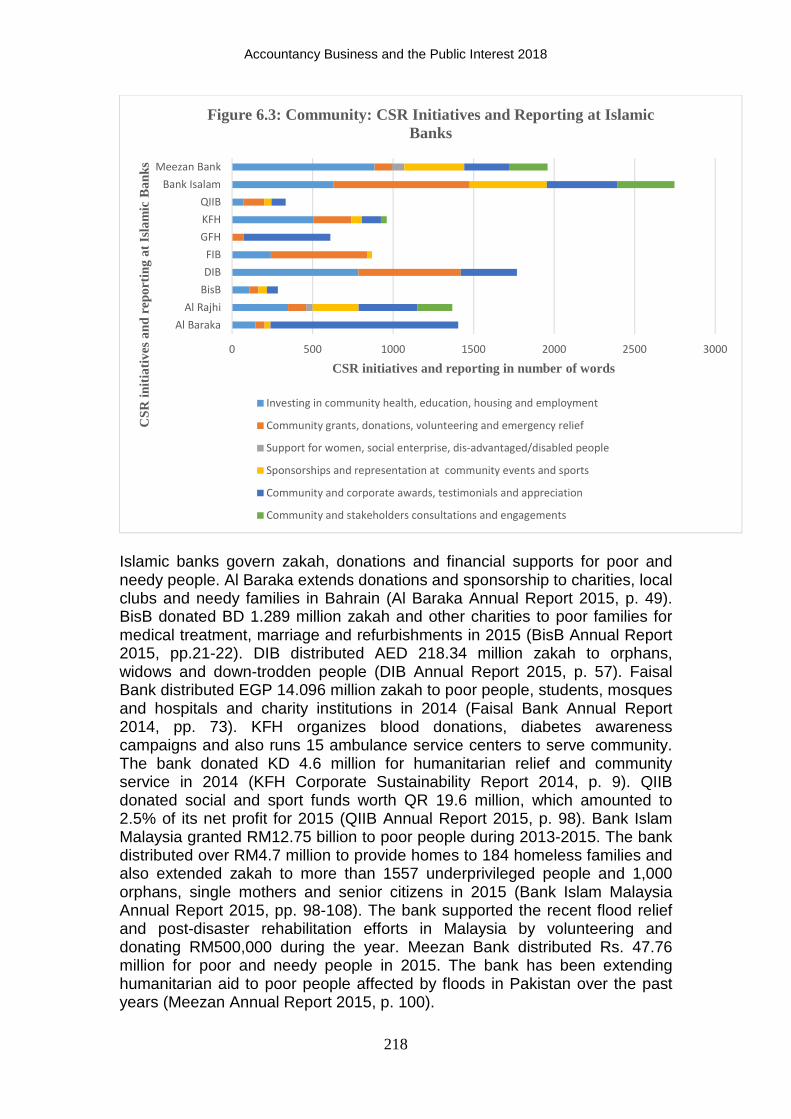

have not provided a satisfactory disclosure about their initiatives in serving their employees. 6.3 Community Figure 6.3 captures the ANOVA results on the exposure and reporting of community service at 10 major Islamic banks. These banks have nurtured a long-term partnership with government and private organizations to promote community education, health, youth welfare, grants and donations, social awareness, security and humanitarian aids. Al Baraka trains a number of university students each year in different professions (Al Baraka Annual Report 2015, p. 49). Al Rajhi Bank operates 100 special units for women to empower them in business (Al Rajhi Annual Report 2015, p. 41). BisB promotes Islamic knowledge, entrepreneurship and leadership in business and community (BisB Annual Report 2015, pp.21-22). DIB extends financial help to schools and hospitals to buy computers and other equipment. The bank promotes community education and awareness about Islamic banking through its monthly magazine – Al Iqtisad Al Islami (www.dib.ae). Faisal Bank supports research seminars and invites foreign delegations to benefit from its vast experience and library resources in Islamic banking and finance (www.faisalbank.com). KFH operates 15 ambulance service centers nationwide and sponsors diabetes awareness campaigns. The bank supports health and education in poor and developing countries. Bank Islam Malaysia runs education clinics, workshops and seminars to promote education, talent, innovation and responsibility among college and university students and community as a whole. The bank organizes a number of educational training and skills programs to support talented students from poor families and rural communities. Meezan Bank invests in community education, healthcare, NGOs and charity bodies working for the welfare of down-trodden people in Pakistan. The bank extends financial and logistic supports to the Indus Hospital, Shaukat Khanum Memorial Cancer Hospital and Research Centre and Sind Institute of Urology Transplant (Meezan Bank Annual Report 2015, pp. 91-96).

Accountancy Business and the Public Interest 2018

218

Islamic banks govern zakah, donations and financial supports for poor and needy people. Al Baraka extends donations and sponsorship to charities, local clubs and needy families in Bahrain (Al Baraka Annual Report 2015, p. 49). BisB donated BD 1.289 million zakah and other charities to poor families for medical treatment, marriage and refurbishments in 2015 (BisB Annual Report 2015, pp.21-22). DIB distributed AED 218.34 million zakah to orphans, widows and down-trodden people (DIB Annual Report 2015, p. 57). Faisal Bank distributed EGP 14.096 million zakah to poor people, students, mosques and hospitals and charity institutions in 2014 (Faisal Bank Annual Report 2014, pp. 73). KFH organizes blood donations, diabetes awareness campaigns and also runs 15 ambulance service centers to serve community. The bank donated KD 4.6 million for humanitarian relief and community service in 2014 (KFH Corporate Sustainability Report 2014, p. 9). QIIB donated social and sport funds worth QR 19.6 million, which amounted to 2.5% of its net profit for 2015 (QIIB Annual Report 2015, p. 98). Bank Islam Malaysia granted RM12.75 billion to poor people during 2013-2015. The bank distributed over RM4.7 million to provide homes to 184 homeless families and also extended zakah to more than 1557 underprivileged people and 1,000 orphans, single mothers and senior citizens in 2015 (Bank Islam Malaysia Annual Report 2015, pp. 98-108). The bank supported the recent flood relief and post-disaster rehabilitation efforts in Malaysia by volunteering and donating RM500,000 during the year. Meezan Bank distributed Rs. 47.76 million for poor and needy people in 2015. The bank has been extending humanitarian aid to poor people affected by floods in Pakistan over the past years (Meezan Annual Report 2015, p. 100).

0 500 1000 1500 2000 2500 3000

Al Baraka

Al Rajhi

BisB

DIB

FIB

GFH

KFH

QIIB

Bank Isalam

Meezan Bank

CSR initiatives and reporting in number of words

CSR

init

iati

ves

and

repo

rtin

g at

Isl

amic

Ban

ks

Figure 6.3: Community: CSR Initiatives and Reporting at Islamic Banks

Investing in community health, education, housing and employment

Community grants, donations, volunteering and emergency relief

Support for women, social enterprise, dis-advantaged/disabled people

Sponsorships and representation at community events and sports

Community and corporate awards, testimonials and appreciation

Community and stakeholders consultations and engagements

Accountancy Business and the Public Interest 2018

219

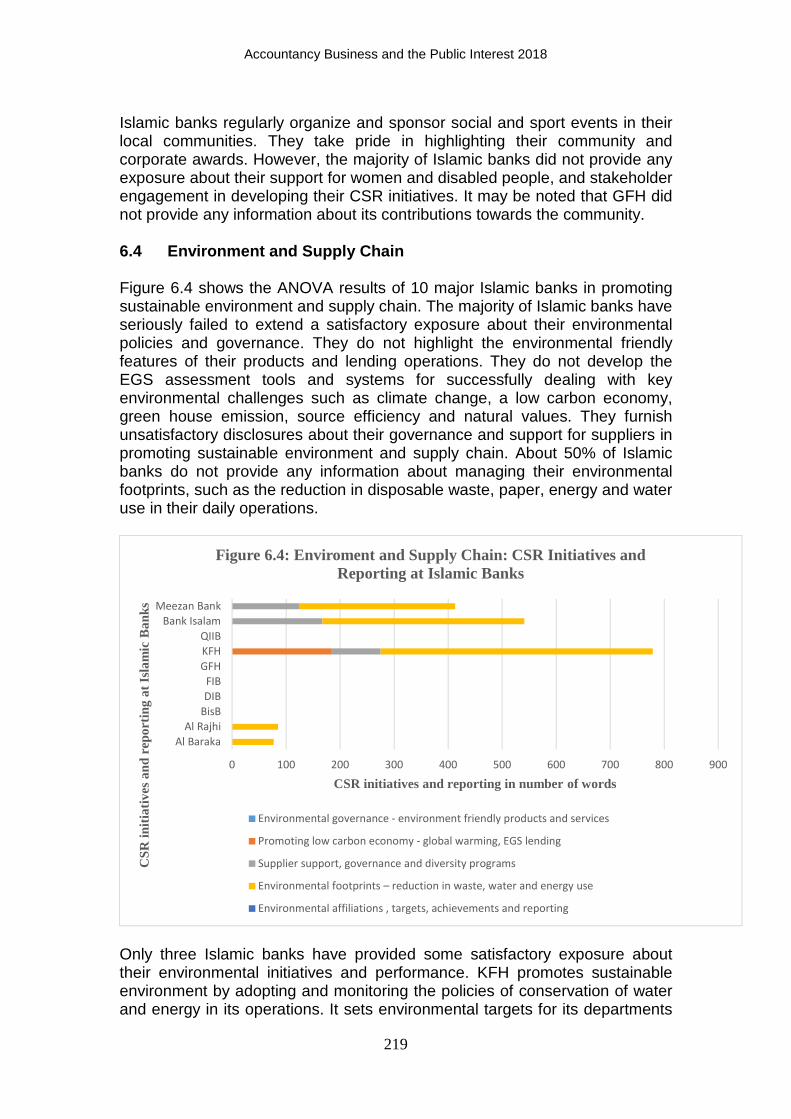

Islamic banks regularly organize and sponsor social and sport events in their local communities. They take pride in highlighting their community and corporate awards. However, the majority of Islamic banks did not provide any exposure about their support for women and disabled people, and stakeholder engagement in developing their CSR initiatives. It may be noted that GFH did not provide any information about its contributions towards the community. 6.4 Environment and Supply Chain Figure 6.4 shows the ANOVA results of 10 major Islamic banks in promoting sustainable environment and supply chain. The majority of Islamic banks have seriously failed to extend a satisfactory exposure about their environmental policies and governance. They do not highlight the environmental friendly features of their products and lending operations. They do not develop the EGS assessment tools and systems for successfully dealing with key environmental challenges such as climate change, a low carbon economy, green house emission, source efficiency and natural values. They furnish unsatisfactory disclosures about their governance and support for suppliers in promoting sustainable environment and supply chain. About 50% of Islamic banks do not provide any information about managing their environmental footprints, such as the reduction in disposable waste, paper, energy and water use in their daily operations.

Only three Islamic banks have provided some satisfactory exposure about their environmental initiatives and performance. KFH promotes sustainable environment by adopting and monitoring the policies of conservation of water and energy in its operations. It sets environmental targets for its departments

0 100 200 300 400 500 600 700 800 900

Al Baraka

Al Rajhi

BisB

DIB

FIB

GFH

KFH

QIIB

Bank Isalam

Meezan Bank

CSR initiatives and reporting in number of words

CSR

init

iati

ves

and

repo

rtin

g at

Isl

amic

Ban

ks

Figure 6.4: Enviroment and Supply Chain: CSR Initiatives and Reporting at Islamic Banks

Environmental governance - environment friendly products and services

Promoting low carbon economy - global warming, EGS lending

Supplier support, governance and diversity programs

Environmental footprints – reduction in waste, water and energy use

Environmental affiliations , targets, achievements and reporting

Accountancy Business and the Public Interest 2018

220

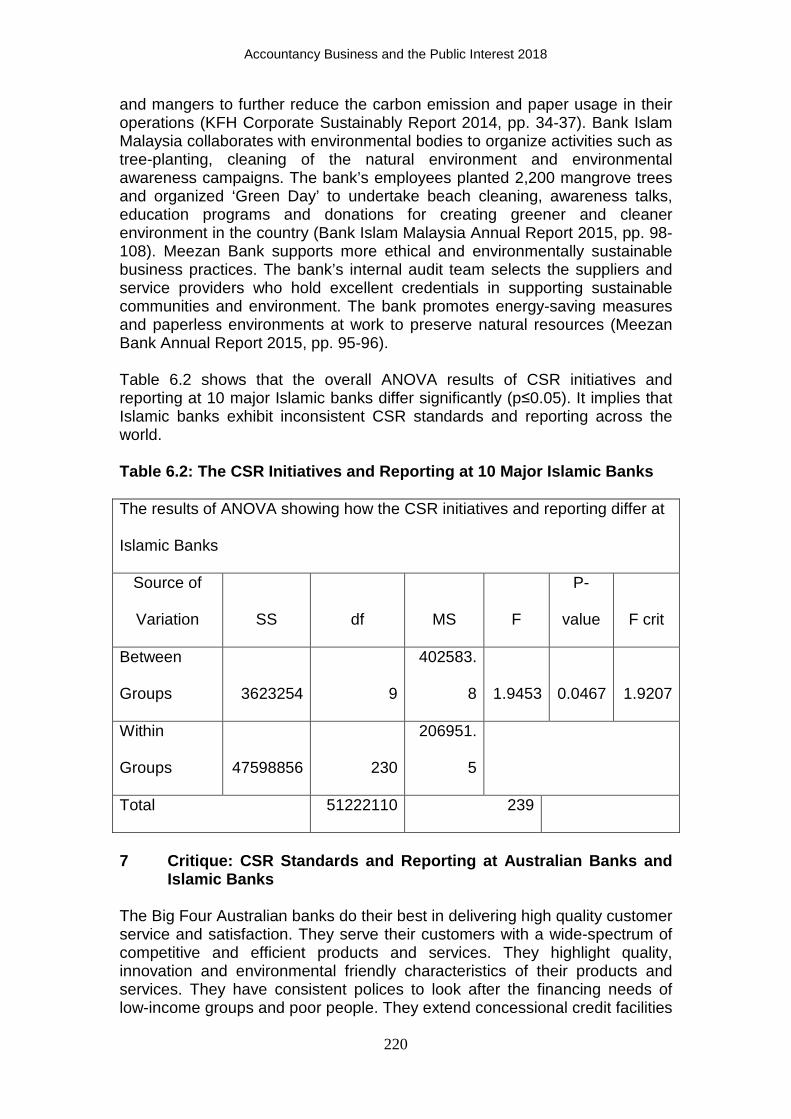

and mangers to further reduce the carbon emission and paper usage in their operations (KFH Corporate Sustainably Report 2014, pp. 34-37). Bank Islam Malaysia collaborates with environmental bodies to organize activities such as tree-planting, cleaning of the natural environment and environmental awareness campaigns. The bank’s employees planted 2,200 mangrove trees and organized ‘Green Day’ to undertake beach cleaning, awareness talks, education programs and donations for creating greener and cleaner environment in the country (Bank Islam Malaysia Annual Report 2015, pp. 98-108). Meezan Bank supports more ethical and environmentally sustainable business practices. The bank’s internal audit team selects the suppliers and service providers who hold excellent credentials in supporting sustainable communities and environment. The bank promotes energy-saving measures and paperless environments at work to preserve natural resources (Meezan Bank Annual Report 2015, pp. 95-96). Table 6.2 shows that the overall ANOVA results of CSR initiatives and reporting at 10 major Islamic banks differ significantly (p≤0.05). It implies that Islamic banks exhibit inconsistent CSR standards and reporting across the world. Table 6.2: The CSR Initiatives and Reporting at 10 Major Islamic Banks

The results of ANOVA showing how the CSR initiatives and reporting differ at

Islamic Banks

Source of

Variation SS df MS F

P-

value F crit

Between

Groups 3623254 9

402583.

8 1.9453 0.0467 1.9207

Within

Groups 47598856 230

206951.

5

Total 51222110 239

7 Critique: CSR Standards and Reporting at Australi an Banks and

Islamic Banks The Big Four Australian banks do their best in delivering high quality customer service and satisfaction. They serve their customers with a wide-spectrum of competitive and efficient products and services. They highlight quality, innovation and environmental friendly characteristics of their products and services. They have consistent polices to look after the financing needs of low-income groups and poor people. They extend concessional credit facilities

Accountancy Business and the Public Interest 2018

221

and managerial support to small business and urban community groups. On the other hand, Islamic banks highlight the Shariah-compliant attributes of their products and services for attracting the Muslim clientele. However, Islamic banking products are publically regarded as too expensive, outdated and carbon copies of their conventional counterparts. Islamic banks have failed to promote sustainable business and community by undertaking finance and investment ventures with small entrepreneurs, farmers and other weaker-economic groups on the risk-sharing basis. They have hugely invested in extravagant real estate projects in the Middle East which largely serve the interest of a handful of business tycoons and wealthy people (Warde, 2000; Chapra, 2001; Khan, 2013; Azmat, Skully and Brown, 2015). The Big Four Australian banks provide better job and career opportunities to their employees. They strongly support their employees with education and training to develop their professional skills and behaviours benefiting them and the community as a whole. Islamic banks always struggle to attract and groom talented people with technical and Shariah expertise. They largely appoint conventional banking employees who follow conventional policies in the garb of Islamic notions (El-Diwany, 2006; Khan, 2013; Azmat, Skully and Brown, 20150. Australian banks’ employees volunteer their time in serving community and environment, whereas a majority of Islamic banks have not given any information about their employees’ involvement in serving community and environment. More importantly, Australian banks give a very balanced representation to females in their workforce. Whereas, Islamic banks offer jobs to their nationals and have a strong representation of males in their workforce. In sum, Australian banks offer better working environments than Islamic banks in terms of collegiality, age and gender balance, flexible working hours, cultural and professional diversity, career and training opportunities and employee wellbeing. The Big Four Australian banks hold consistent policies and performance in promoting community partnerships in education, health, youth, science and technology, arts and environment. They actively sponsor research, advocacy, sports, arts and community and business events. Some Islamic banks have been showing satisfactory performance in serving the community. However, other Islamic banks hold a narrow CSR vision of just helping poor and weaker economic groups through zakah and donations. Islamic banks do not ensure a stronger stakeholder engagement in developing their CSR initiatives. The Big Four Australian banks have been actively promoting efficient environmental governance and supply chain systems through their corporate behaviours. They follow international standards for CSR exposure and reporting. They develop their CSR targets based on the expectations and feedback from shareholders, government, regulatory bodies, NGOs, academia and business associates. They appraise their CSR performance under Global Reporting Initiative (GRI) G4 Framework. They incorporate human rights, labour, environmental and other key indicators in their CSR exposures and reporting. They have received many awards from national and international bodies and community groups for their societal and environmental performance and reporting.

Accountancy Business and the Public Interest 2018

222

Islamic banks have not taken a much needed environmental stewardship role in promoting a low-carbon economy and governing their suppliers on environmental policies and performance. The majority of Islamic banks in the Middle East are not very keen to develop their CSR initiatives on the basis of stakeholder consultation and market research. They hold heterogeneous and unsatisfactory CSR standards and reporting. For example, Al Baraka, Al Rajhi and BisB have not provided any information regarding their CSR initiatives on their websites, and their 2015 Annual Reports contain a 309-word, 354-word and 306-word CSR exposure respectively (Al Baraka Bank Annual Report 2015, p. 49; Al Rajhi Bank Annual Report 2015, p. 55; BisB Annual Report 2015, p. 32). Faisal Bank, KFH and QIIB did not provide any CSR exposure in their latest posted annual reports (Faisal Bank Annual Report 2014; KFH Annual Report 2015; QIIB Annual Report 2015). Whereas QIIB provides a 225-word CSR exposure about the community services on its website. However, KFH, Bank Islam Malaysia and Meezan Bank have shown far better CSR standards, performance and reporting in the Islamic banking industry worldwide. In sum, Islamic banks run very high CSR and reputational risks because Muslim communities expect from them to take up a very holistic and aggressive approach to meet their ethical, societal and environmental responsibilities. 8 Summary and Conclusions This research paper explores the Western and Islamic perspectives of CSR initiatives. It takes account of CSR standards and reporting at the Big Four Australian banks and 10 major Islamic banks. Australian banks hold proven credentials in promoting sustainable communities and environment. They offer a wide range of innovative products and services to serve different segments of business and society. They attract and retain highly qualified people and invest in their professional development and wellbeing. They commit their financial and human resources to help community, poor and weaker economic groups. They aim to find effective solutions for emerging societal issues through stakeholder engagement and participation. They ensure that their corporate behaviour strongly promote sustainable environments and supply chain. They provide detailed and externally audited reports about their CSR targets and achievements to stakeholders and community groups. They enjoy a great deal of support and recognitions for their CSR initiatives from local and international business and community groups. Islamic banks have been struggling to follow their etho-religious agenda of serving people and environment. They deliver products and services to their customers which are not truly Shariah-compliant, innovative and cost-efficient. They offer lucrative remuneration, human resource education, training and career development opportunities to their employees. They largely hire the conventional banking staff whose professional knowledge and competence on Shariah matters always remain a question mark. Overall, Islamic banks may improve their exposure in relation to human rights, cultural diversity, gender equality and women representation at workplace. Some Islamic banks have been promoting community health, education, charities and welfare in their

Accountancy Business and the Public Interest 2018

223

communities. Islamic banks hold dismal disclosure and performance in promoting sustainable environment and supply chain. Like their conventional counterparts, Islamic banks need to promote consistent and universal CSR imperatives and reporting across the board. They may ensure community participation and stakeholder engagement in formulating their CSR standards and practice. References Al Baraka Islamic Bank 2015, Annual Report 2015, viewed 23 November 2017, http://www.barakaonline.com. Adams, C A & Whelan, G 2009, ‘Conceptualising future change in corporate sustainability reporting Accounting’, Auditing and Accountability Journal, Vol. 22, no. 1, pp. 118–143. Aggarwal, R K & Youssef, T 2000, ‘Islamic banks and investment financing’, Journal of Money, Credit and Banking, vol. 32, no. 1, pp. 93-120. Al Rajhi Bank 2015, Annual Report 2015, viewed 22 March 2018, http://www.alrajhibank.com.sa. Anuar, H, Sulaiman, M & Ahmad, N 2004, ‘Environmental reporting of Shariah approved companies in Malaysia’, Conference proceedings of International Accounting Conference 11, International Islamic University, Kuala Lumpur. Australia, New Zealand Banking Group 2016, Annual Report 2016 & Sustainability Report 2015, viewed 25 April 2018, http://www.anz.com.au. Azmat, S, Skully, M & Brown, K 2015, ‘Can Islamic banking ever become Islamic?’ Pacific-Basin Finance Journal, vol. 34, pp. 253-272. Bahrain Islamic Bank 2015, Annual Report 2015, viewed 6 December 2017, http://www.bisb.com. Bank Islam Malaysia Berhad 2015, Annual Report 2015, viewed 24 March 2018, http://www.bankislam.com. Beckmann, S, Morsing, M & Reisch, L 2006, ‘Strategic CSR communication: an emerging field’, in Morsing, M. and Beckmann, S (ed.), Strategic CSR Communication, DJOF, Copenhagen, pp.11-32. Belal, A R, Abdelsalam, O & Nizamee, S S 2015, ‘Ethical reporting in Islami Bank Bangladesh Limited 1983-2010’, Journal of Business Ethics, vol. 129, no. 4, pp. 769-784. Bihari, S C & Pradhan, S 2011, ‘CSR and performance: the story of banks in India’, Journal of Transnational Management, vol. 16, no.1, pp. 20-35.

Accountancy Business and the Public Interest 2018

224

Bowen, H R 1953, Social responsibilities of businessmen, L. Harper & Brothers, New York. Bulow, J & Rogoff, K 1990, ‘Cleaning up third world debt without getting taken to the cleaners’, Journal of Economic Perspective, vol. 4, no.1, pp. 31-42. Carroll, A B 2004, ‘Managing ethically with global stakeholders: a present and future challenge’, The Academy of Management Executive, vol. 18, no. 2, pp. 114-120. Chapra, M U 2001, ‘Islamic banking and finance: the dream and reality’, Journal of Banking and Finance, vol. 18, no. 2, pp. 7-39. Chapra, M U 1985, Towards a just monetary system, The Islamic Foundation, Leicester. Chaudary, S, Zahid, Z, Shahid, S, Khan, S N, & Azar, S 2016, ‘Customer perception of CSR initiatives: its antecedents and consequences’, Social Responsibility Journal, vol. 12, no. 2, pp. 263 – 279. Common Wealth Bank 2016, Annual Report 2016 & CSR Report 2016-2018, viewed 24 January 2018, http://www.commbank.com.au. Cornett, M M, Erhemjamts, O & Tehranian, H 2016, ‘Greed or good deeds: An examination of the relation between corporate social responsibility and the financial performance of U.S. commercial banks around the financial crisis’, viewed 12 May 2018, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2333878## Deegan, C 2000, ‘The legitimising effect of social and environmental disclosures – a theoretical foundation’, Accounting, Auditing and Accountability Journal, vol. 15, no. 3, pp. 282-312. Donaldson, T & Dunfee, T W 1999, Ties that bind: a social contracts approach to business ethics, Harvard Business School Press, Boston. Dobbs, S & Staden, C V 2016 ‘Motivations for corporate social and environmental reporting: New Zealand evidence’, Sustainability Accounting, Management and Policy Journal, vol. 7, no. 3, pp.449 – 472. Dubai Islamic Bank 2015, Annual Report 2015, viewed 23 April 2018, http://www.dib.ae/home. El-Diwany, T 2006, ‘Islam today: Is Islamic banking Islamic?’, reviewed 15 March 2018, www.interactiveislam.com/html/modules.php?name=News&file=article&sid=199 . El-Ghazali, A H 1994, Profit versus bank interest in economic analysis and Islamic Law, IDB, IRTI, Jeddah.

Accountancy Business and the Public Interest 2018

225

Faisal Islamic Bank of Egypt 2014, Annual Report 2014, viewed 23 February 2018, http://www.faisalbank.com.eg. Farook, S, Hassn, K & Lanis, R 2011, ‘Determinants of corporate social responsibility disclosure: the case of Islamic banks’, Journal of Islamic Accounting and Business Research, vol. 2, no. 2, pp. 114-141. Fish A J & Wood, J 2017, ‘Promoting a strategic business focus to balance competitive advantage and corporate social responsibility – missing elements’, Social Responsibility Journal, vol. 13. no. 1, pp. 78 – 94. Freeman, R E 1984, Strategic management. A stakeholder approach, Pitman Marshfield, MA. Friedman, M 1970, ‘The social responsibility of business is to increase its profits’, New York Times Magazine, vol. 33, pp. 122-126. Friedman, M 1962, Capitalism and freedom, University of Chicago Press, Chicago. Gray, R, Owen, D & Adams, C A 1996, Accounting and accountability, changes and challenges in corporate social and environmental reporting, Prentice-Hall, London. Gray, R, Adams, C A & Owen D 2014, Accountability, social responsibility and sustainability: Accounting for society and environment, Pearson Education, UK. Gulf Finance House 2015, Annual Report 2015 & Corporate Sustainability Report 2014, viewed 25 April 2018, http://www.gfh.com. Hadfield-Hill, S 2014, ‘CSR in India: reflections from the banking sector’, Social Responsibility Journal, vol. 10, no. 1, pp. 21 – 37. Haniffa, R M & Hudaib, M 2007, ‘Exploring the ethical identity of Islamic banks via communication in annual reports’, Journal of Business Ethics, vol. 76, no. 1, pp. 97-116. Haniffa, R M & Cooke, T 2001, ‘Corporate social reporting in Malaysia: Impact of culture and corporate governance structure’, Discussion Paper in Accounting and Finance, University of Exeter, Exeter. Hassan M K, Rashid, M, Imran, M Y & Shahid, A I 2010, ‘Ethical gaps and market value in the Islamic banks of Bangladesh’, Review of Islamic Economics, vol. 14, no. 1, pp. 49-75. Hossain, M M et al 2016, ‘Contributing barriers to corporate social and environmental responsibility practices in a developing country: A stakeholder

Accountancy Business and the Public Interest 2018

226

perspective’, Sustainability Accounting, Management and Policy Journal, vol. 7, no. 2, pp.319 – 346. Hu, Vi-in & Scholtens, B 2012, ‘Corporate social responsibility policies of commercial banks in developing countries’, viewed 23 July 2017, http://onlinelibrary.wiley.com/doi/10.1002/sd.1551/epdf. Islamic Financial Services Board 2016, Islamic Financial Services Industry Stability Report 2016, viewed 23 September 2017, http://www.ifsb.org. Jenkins, R 2005, ‘Globalization, corporate social responsibility and poverty’, International Affairs, vol. 81, no. 3, pp. 525–540. Kabir, R & Thai, H M 2017, ‘Does corporate governance shape the relationship between corporate social responsibility and financial performance?’, Pacific Accounting Review, vol. 29, no. 2, pp. 227-258. Khan, M M 2013, ‘Developing a conceptual framework to appraise the corporate social responsibility performance of Islamic banking and finance institutions’, Accounting and the Public Interest, vol. 13, no. 1, pp. 191-207.

Khan, M M & Bhatti, M I 2008, Developments in interest-free banking, Palgrave Macmillan, UK. Khan, S K & Mirakhor, A 1987, Theoretical studies in Islamic banking and finance, Book Distribution Centre, Houston. Kuwait Finance House 2015, Annual Report 2015, viewed 24 October 2017, http://www.kfh.com. Lu, Y, Abeysekera, I & Cortese, C 2015, ‘Corporate social responsibility reporting quality, board characteristics and corporate social reputation Evidence from China’, Pacific Accounting Review, vol. 27, no. 1, pp. 95 – 118. Maali, B, Casson P & Napier C 2003, Social reporting by Islamic banks, Working Paper, University of Southampton. Meezan Bank 2015, Annual Report 2015, viewed 25 August 2017, http://www.meezanbank.com. Moody’s Investors Service 2016, Islamic finance; prospects remain strong despite subdued sukuk issuance, viewed 20 September 2017, https://www.moodys.com. National Australia Bank 2016, Annual Report 2016 & CSR Performance: Dig Deeper Report 2016, viewed 23 August 2017, http://www.nab.com.au.

Accountancy Business and the Public Interest 2018

227

Ogrizek, M 2002, The effect of corporate social responsibility on the branding of financial services’, Journal of Financial Services Marketing, vol. 6, no. 3, pp. 215-228. Patwary, M. & Rahman, A 2015 ‘The evaluation of CSR on banks' performance to promote sustainable banking in Bangladesh: a study on supply chain context’, viewed 28 August 2017, http://dspace.bracu.ac.bd/jspui/handle/10361/4921. Pava, M L & Krausz, J 1996, Corporate responsibility and financial performance. the paradox of social cost, Quorum Books, London. Porter, M E & Kramer, M R 2006, ‘The link between competitive advantage and corporate social responsibility’, Harvard Business Review, vol. 80, no. 12, pp. 56-69. Qatar International Islamic Bank 2015, Annual Report 2015, viewed 23 September 2017, http://www.qiib.com.qa. Rania, B M & Farid, E 2016, ‘Exploring the mechanism of consumer responses to CSR activities of Islamic banks’, International Journal of Bank Marketing, vol. 34, no. 6, pp. 940 – 962. Rashid, M, Abdeljawad, I, Ngalim, S M & Hassan, M K 2013, ‘Customer centric corporate social responsibility’, Management Research Review, vol. 36, no. 4, pp. 359- 378. Schnurbein. G V, Seele, P & Lock, I. 2016, ‘Exclusive corporate philanthropy: rethinking the nexus of CSR and corporate philanthropy’, Social Responsibility Journal, vol. 12, no. 2, pp. 280 – 294. Schuman, M C 1995, ‘Managing legitimacy: strategic and institutional approaches’, Academy of Management Review, vol. 20, no. 3, pp.571-610. Siddiqi, M N 2000, ‘Islamic finance and beyond: premises and promises of Islamic economics’, Conference proceedings of the Third Harvard University Forum on Islamic Finance, Harvard University, Cambridge, Mass. Simms, J 2002, ‘Business: corporate social responsibility – you know it makes sense’, Accountancy, vol. 130, no. 11, pp. 48-50. Smith, J W 2005, Economic democracy: the political struggle of the 21st century, Democracy Press, W. Camden. The World Bank 2014, The World Bank’s Financial Development Report 2014: Financial Inclusion”, viewed 22 September 2017https://openknowledge.worldbank.org/bitstream/handle/10986/ 16238/9780821399859.pdf?sequence=4.

Accountancy Business and the Public Interest 2018

228

Usman, A B & Amran, N A B 2015, ‘Corporate social responsibility practice and corporate financial performance: evidence from Nigeria companies’, Social Responsibility Journal, vol. 11, no. 4, pp. 749 – 763. Warde, I 2000, Islamic finance in the global economy, Edinburgh University Press, Edinburgh. Weber, M 1958, The protestant ethics and the spirit of capitalism, Charles Scribner’ s Sons, New York. Westpac Banking Corporation 2016, Annual Report 2016 & Sustainability Performance Report 2016, viewed 29 March 2018, http://www.westpac.com.au. Wilson, R 1997, ‘Islamic finance and ethical investment’, International Journal of Social Economics, vol. 24, no. 11, pp. 1325-1342. Wood, D J 1991, ‘Corporate social performance revisited’, Academy of Management Review, vol. 16, no. 4, pp. 691–718. Yahya, M A, Adbul-Rahman, A & Taybi, M 2004, ‘The relationship between corporate social disclosure and Islamic unit trust shareholding’, The Islamic Perspective, International Conference V proceedings of Accounting, Commerce and Finance, Brisbane, Australia.

![S R ] a R Z O R AABA Annual Gala & Silent Auction NEWSLETTER · Asian American Bar Association of Houston 3 2 %R[ +RXVWRQ 7H[DV AABA Project Blueprint Grant Application The AABA is](https://img.dokumen.tips/doc/110x75/5e48ce0fa84ebe38f03e7f92/s-r-a-r-z-o-r-aaba-annual-gala-silent-auction-newsletter-asian-american.jpg)