Embed Size (px)

Citation preview

Corporate Investor Presentation

Full Cycle Oilfield Consumable Chemical Solutions

April 2016

Forward-looking Information and Statements

Certain statements in this presentation may constitute forward-looking information or forward-looking statements (collectively referred to as “forward-looking information”) which involves

known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of CES, or industry results, to be materially different from

any future results, performance or achievements expressed or implied by such forward-looking information. When used in this presentation, such information uses such words as “may”,

“would”, “could”, “will”, “intend”, “expect”, “believe”, “plan”, “anticipate”, “estimate”, and other similar terminology. This information reflects CES’ current expectations regarding future

events and operating performance and speaks only as of the date of the presentation. Forward-looking information involves significant risks and uncertainties, should not be read as a

guarantee of future performance or results, and will not necessarily be an accurate indication of whether or not such results will be achieved. A number of factors could cause actual

results to differ materially from the results discussed in the forward-looking information, including, but not limited to, the factors discussed below. The management of CES believes the

material factors, expectations and assumptions reflected in the forward-looking information and statements are reasonable but no assurance can be given that these factors,

expectations and assumptions will prove to be correct. The forward-looking information and statements contained in this document speak only as of the date of the document, and CES

assumes no obligation to publicly update or revise them to reflect new events or circumstances, except as may be required pursuant to applicable securities laws or regulations. The

material assumptions in making forward-looking statements include, but are not limited to, the factors discussed below. The management of CES believes the material factors,

expectations and assumptions reflected in the forward-looking information and statements are reasonable but no assurance can be given that these factors, expectations and

assumptions will prove to be correct.

In particular, this presentation may contain forward-looking information pertaining to the following: future estimates as to dividend levels; the potential means of funding dividends; the

intention to make future dividend payments; the seasonality of CES’ business and anticipated reduction in exposure to the effects of spring break-up in the WCSB; the duration of spring

break-up; the certainty and predictability of future cash flows and earnings; the sufficiency of liquidity and capital resources to meet long-term payment obligations; the long-term capital

investments required for CES to execute on its business plan; the amount of CES’ non-acquisition related capital expenditures, including maintenance capital and discretionary

expansion capital; the expected timing for completion of expansions at JACAM facilities; the anticipated timing for completion of the laboratories in Midland and Houston Texas;

management’s opinion of the impact of any potential litigation or disputes; potential outcomes of the CRA’s intent to challenge the Canadian tax consequences of the Conversion; the

application of critical accounting estimates and judgements; the collectability of accounts receivable; CES’ ability to increase or maintain its market share, including expectations that

PureChem, Sialco and JACAM will increase market-share in the oilfield consumable chemical market; supply and demand for CES’ products and services, including expectations for

growth in CES’ production and speciality chemical sales and expected growth in the consumable chemicals market; industry activity levels; commodity prices; treatment under

governmental regulatory and taxation regimes; expectations regarding expansion of services in Canada and the United States; development of new technologies; expectations

regarding CES’ growth opportunities in Canada and the United States; the effect of acquisitions on the Company; expectations regarding the performance or expansion of CES’

operations; expectations regarding demand for CES’ services and technology; investments in research and development and technology advancements; access to debt and capital

markets; and competitive conditions.

CES’ actual results could differ materially from those anticipated in the forward-looking information as a result of the following factors: general economic conditions in Canada, the United

States, and internationally; geopolitical risk; fluctuations in demand for consumable fluids and chemical oilfield services, and the recent downturn in oilfield activity; a decline in activity in

the WCSB, the Permian and other basins in which the Company operates; volatility in market prices for oil, natural gas, and natural gas liquids and the effect of this volatility on the

demand for oilfield services generally; the recent declines in prices for oil, and pricing differentials between world pricing and pricing in North America; competition, and pricing pressures

from customers in the current commodity environment; currency risk as a result of recent fluctuations in value of the U.S. dollar; liabilities and risks, including environmental liabilities and

risks inherent in oil and natural gas operations; sourcing, pricing and availability of raw materials, consumables, component parts, equipment, suppliers, facilities, and skilled

management, technical and field personnel; the collectability of accounts receivable, particularly in the current low oil and natural gas price environment; ability to integrate technological

advances and match advances of competitors; availability of capital; uncertainties in weather and temperature affecting the duration of the oilfield service periods and the activities that

can be completed; the ability to successfully integrate and achieve synergies from the Company’s acquisitions; changes in legislation and the regulatory environment, including

uncertainties with respect to programs to reduce greenhouse gas and other emissions and regulations restricting the use of hydraulic fracturing; reassessment and audit risk associated

with the Conversion and other tax filing matters; changes to the fiscal regimes applicable to entities operating in the WCSB and the US; access to capital and the liquidity of debt

markets; fluctuations in foreign exchange and interest rates, and the other factors considered under “Risk Factors” in CES’ Annual Information Form for the year ended December 31,

2014 and “Risks and Uncertainties” in the September 30, 2015 management’s discussion and analysis.

.

page 2

page 3

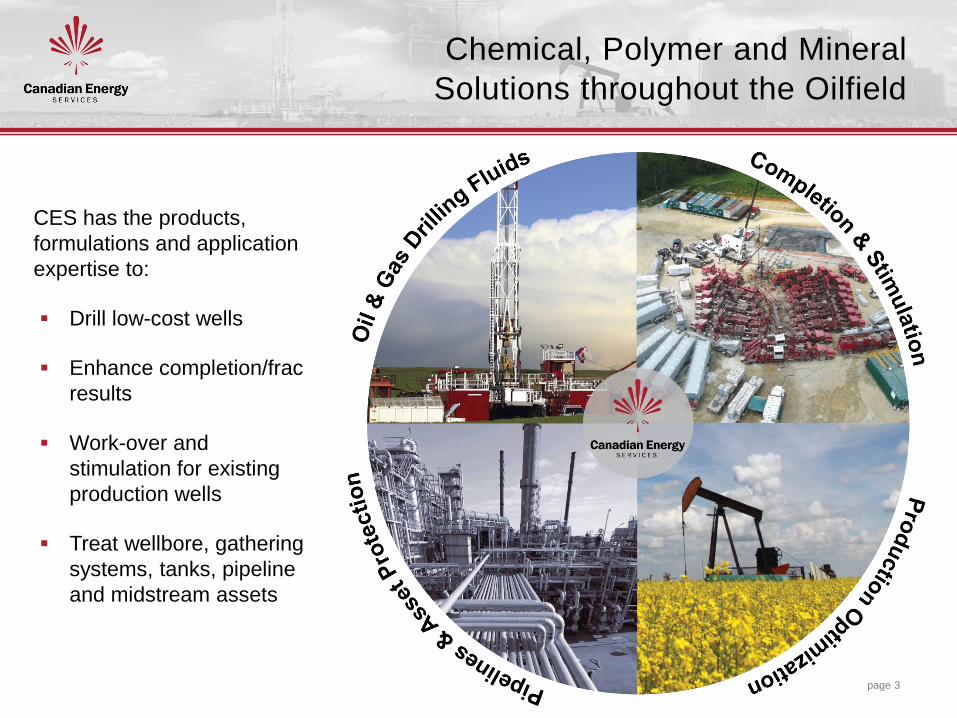

CES has the products,

formulations and application

expertise to:

Drill low-cost wells

Enhance completion/frac

results

Work-over and

stimulation for existing

production wells

Treat wellbore, gathering

systems, tanks, pipeline

and midstream assets

Chemical, Polymer and Mineral

Solutions throughout the Oilfield

page 4

Critical Technology & Manufacturing Infrastructure Underpinning all Sales Channels

Vertically Integrated Technology & Manufacturing U

niq

ue

Te

ch

no

log

y

Ex

pe

rts

in

Ap

pli

ca

tio

n

2001 2006 2008 2010 2011 2012 2013 2014 2015

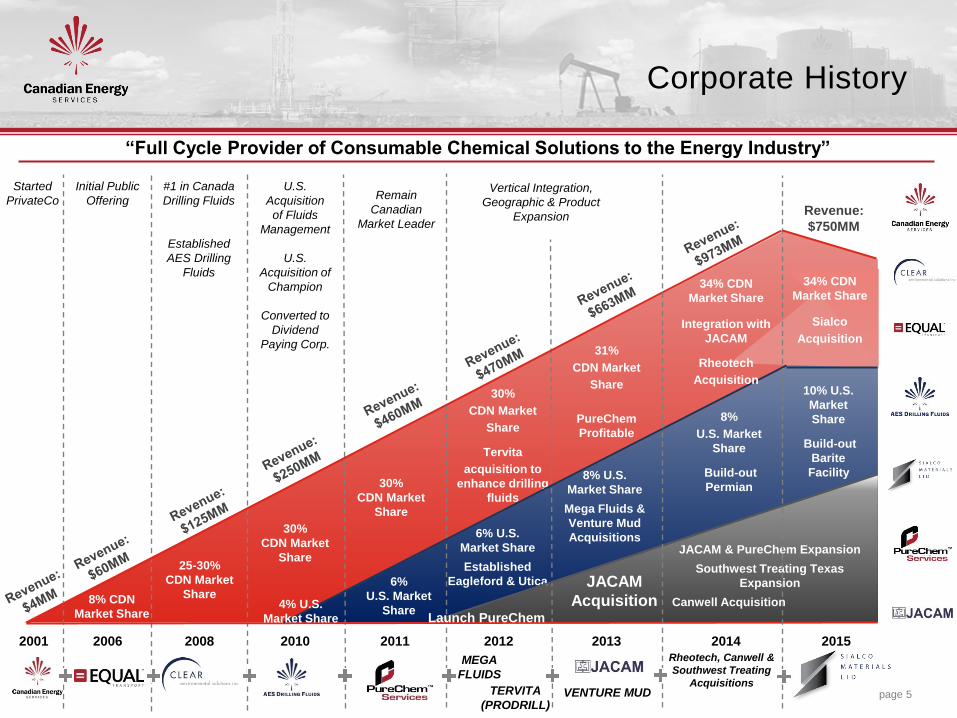

Corporate History

page 5

“Full Cycle Provider of Consumable Chemical Solutions to the Energy Industry”

Started

PrivateCo

Initial Public

Offering

#1 in Canada

Drilling Fluids

Established

AES Drilling

Fluids

U.S.

Acquisition

of Fluids

Management

U.S.

Acquisition of

Champion

Converted to

Dividend

Paying Corp.

Remain

Canadian

Market Leader

TERVITA

(PRODRILL)

25-30%

CDN Market

Share

30%

CDN Market

Share

30%

CDN Market

Share

Vertical Integration,

Geographic & Product

Expansion

30%

CDN Market

Share

Tervita

acquisition to

enhance drilling

fluids

31%

CDN Market

Share

PureChem

Profitable

VENTURE MUD

6%

U.S. Market

Share

6% U.S.

Market Share

Established

Eagleford & Utica

8% U.S.

Market Share

Mega Fluids &

Venture Mud

Acquisitions

JACAM

Acquisition 8% CDN

Market Share

MEGA

FLUIDS

4% U.S.

Market Share

Launch PureChem

JACAM & PureChem Expansion

Southwest Treating Texas

Expansion

Canwell Acquisition

Rheotech, Canwell &

Southwest Treating

Acquisitions

34% CDN

Market Share

Sialco

Acquisition

8%

U.S. Market

Share

Build-out

Permian

34% CDN

Market Share

Integration with

JACAM

Rheotech

Acquisition

Revenue:

$750MM

10% U.S.

Market

Share

Build-out

Barite

Facility

page 6

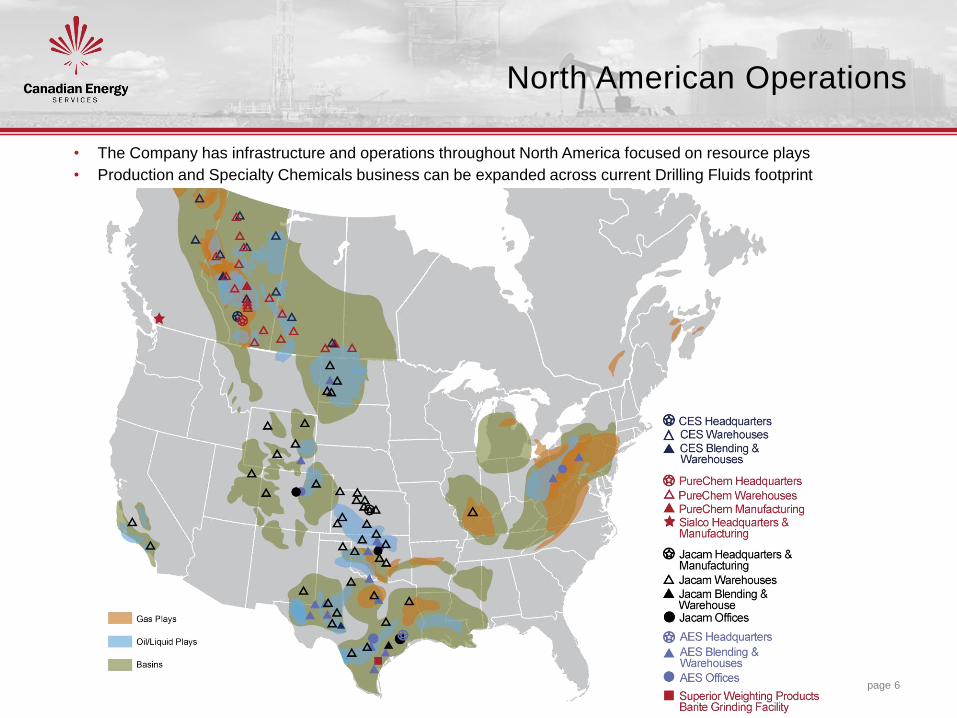

• The Company has infrastructure and operations throughout North America focused on resource plays

• Production and Specialty Chemicals business can be expanded across current Drilling Fluids footprint

North American Operations

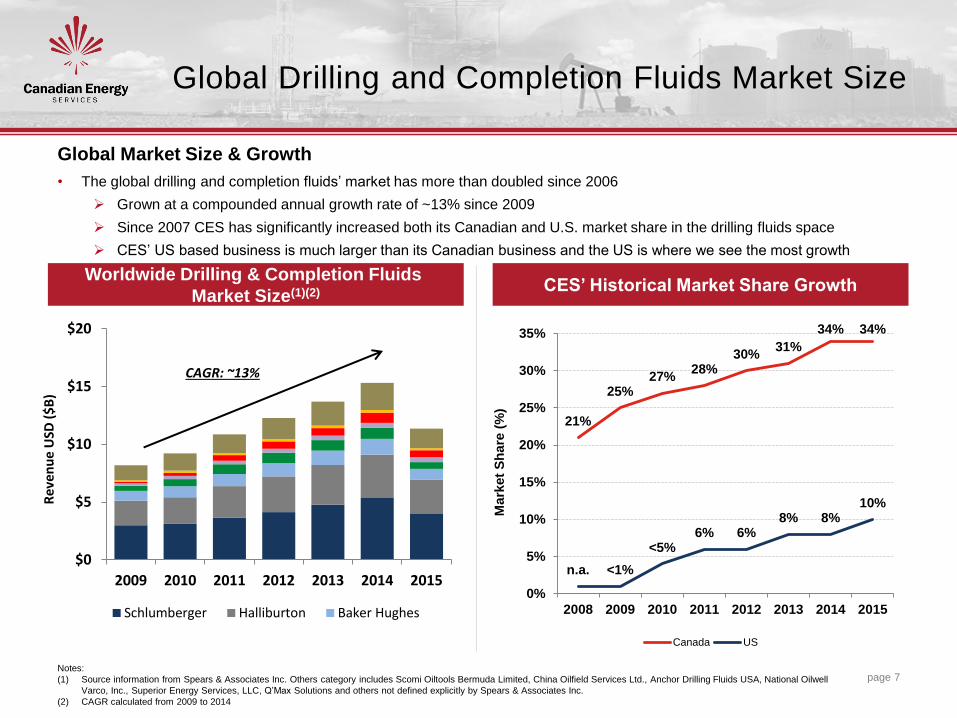

Global Drilling and Completion Fluids Market Size

Global Market Size & Growth

• The global drilling and completion fluids’ market has more than doubled since 2006

Grown at a compounded annual growth rate of ~13% since 2009

Since 2007 CES has significantly increased both its Canadian and U.S. market share in the drilling fluids space

CES’ US based business is much larger than its Canadian business and the US is where we see the most growth

page 7

Worldwide Drilling & Completion Fluids

Market Size(1)(2)

Notes:

(1) Source information from Spears & Associates Inc. Others category includes Scomi Oiltools Bermuda Limited, China Oilfield Services Ltd., Anchor Drilling Fluids USA, National Oilwell

Varco, Inc., Superior Energy Services, LLC, Q’Max Solutions and others not defined explicitly by Spears & Associates Inc.

(2) CAGR calculated from 2009 to 2014

CES’ Historical Market Share Growth

CAGR: ~13%

$0

$5

$10

$15

$20

2009 2010 2011 2012 2013 2014 2015

Schlumberger Halliburton Baker Hughes

Re

ven

ue

USD

($

B)

21%

25% 27%

28% 30%

31%

34% 34%

n.a. <1%

<5% 6% 6%

8% 8% 10%

0%

5%

10%

15%

20%

25%

30%

35%

2008 2009 2010 2011 2012 2013 2014 2015

Mark

et

Sh

are

(%

)

Canada US

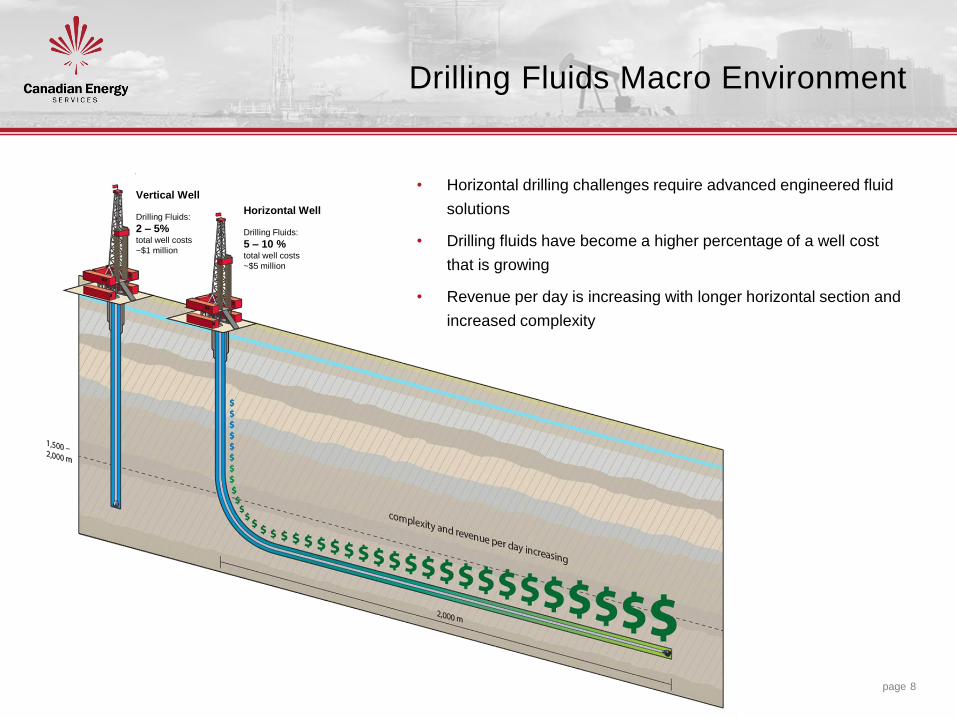

Drilling Fluids Macro Environment

• Horizontal drilling challenges require advanced engineered fluid

solutions

• Drilling fluids have become a higher percentage of a well cost

that is growing

• Revenue per day is increasing with longer horizontal section and

increased complexity

Horizontal Well

Drilling Fluids:

5 – 10 % total well costs

~$5 million

Vertical Well

Drilling Fluids:

2 – 5% total well costs

~$1 million

page 8

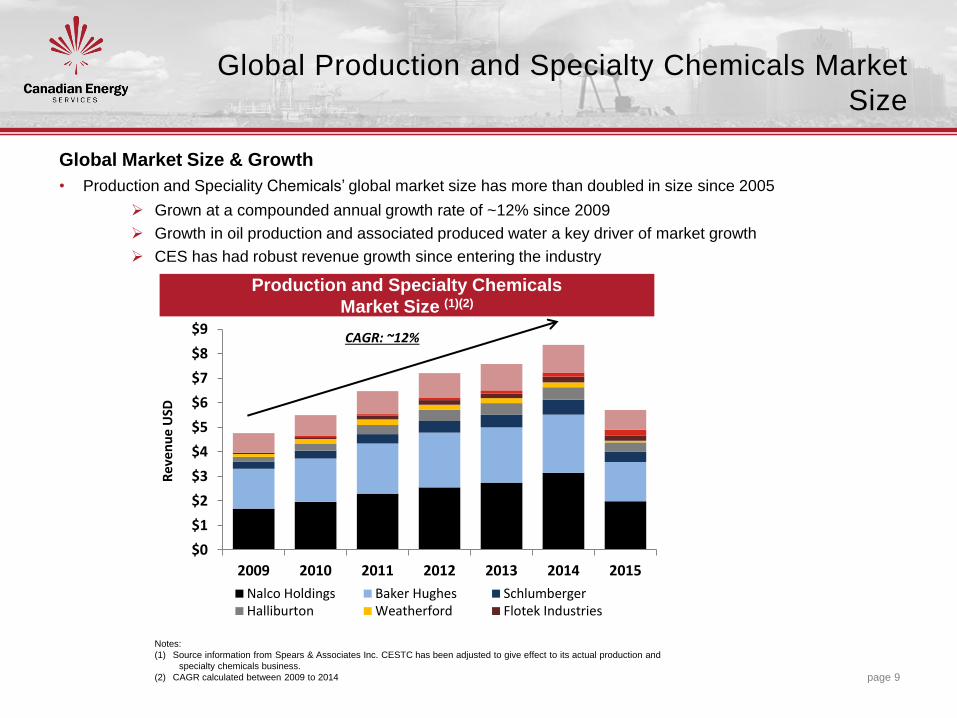

Global Production and Specialty Chemicals Market

Size

Global Market Size & Growth

• Production and Speciality Chemicals’ global market size has more than doubled in size since 2005

Grown at a compounded annual growth rate of ~12% since 2009

Growth in oil production and associated produced water a key driver of market growth

CES has had robust revenue growth since entering the industry

page 9

Production and Specialty Chemicals

Market Size (1)(2)

CAGR: ~12%

Notes:

(1) Source information from Spears & Associates Inc. CESTC has been adjusted to give effect to its actual production and

specialty chemicals business.

(2) CAGR calculated between 2009 to 2014

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

2009 2010 2011 2012 2013 2014 2015

Nalco Holdings Baker Hughes SchlumbergerHalliburton Weatherford Flotek Industries

Re

ven

ue

USD

North American Production and Specialty Chemicals

page 10

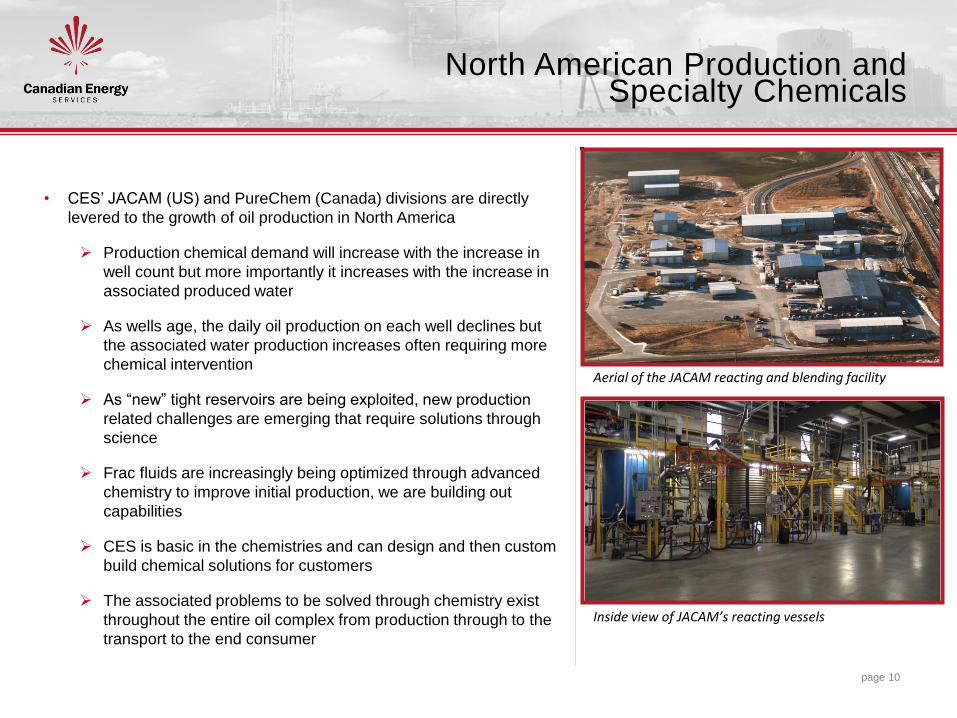

• CES’ JACAM (US) and PureChem (Canada) divisions are directly

levered to the growth of oil production in North America

Production chemical demand will increase with the increase in

well count but more importantly it increases with the increase in

associated produced water

As wells age, the daily oil production on each well declines but

the associated water production increases often requiring more

chemical intervention

As “new” tight reservoirs are being exploited, new production

related challenges are emerging that require solutions through

science

Frac fluids are increasingly being optimized through advanced

chemistry to improve initial production, we are building out

capabilities

CES is basic in the chemistries and can design and then custom

build chemical solutions for customers

The associated problems to be solved through chemistry exist

throughout the entire oil complex from production through to the

transport to the end consumer

Aerial of the JACAM reacting and blending facility

Inside view of JACAM’s reacting vessels

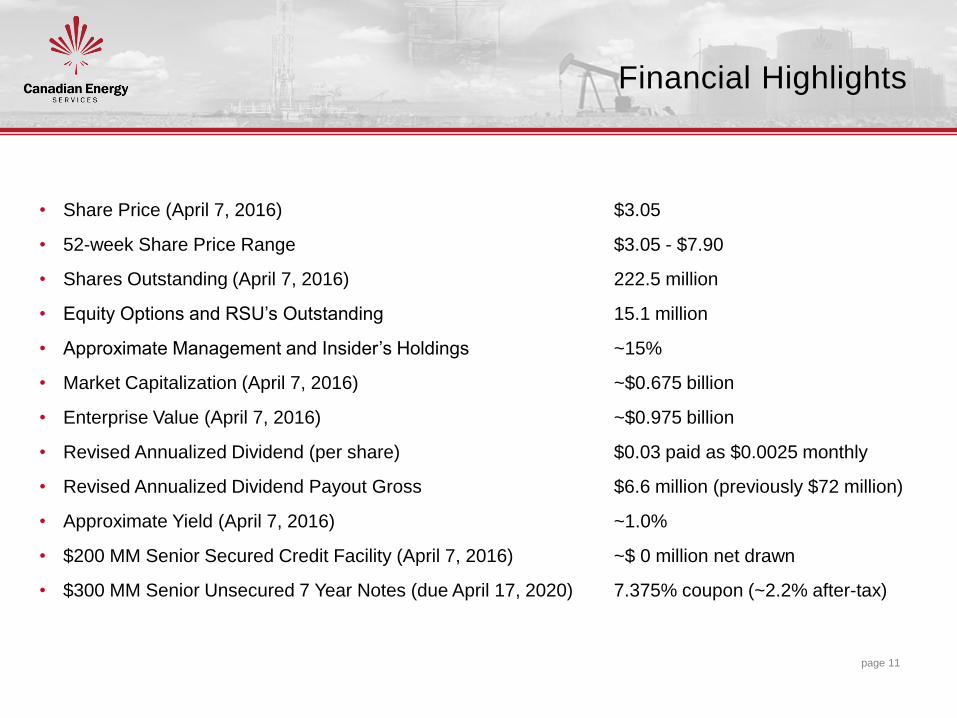

Financial Highlights

page 11

• Share Price (April 7, 2016) $3.05

• 52-week Share Price Range $3.05 - $7.90

• Shares Outstanding (April 7, 2016) 222.5 million

• Equity Options and RSU’s Outstanding 15.1 million

• Approximate Management and Insider’s Holdings ~15%

• Market Capitalization (April 7, 2016) ~$0.675 billion

• Enterprise Value (April 7, 2016) ~$0.975 billion

• Revised Annualized Dividend (per share) $0.03 paid as $0.0025 monthly

• Revised Annualized Dividend Payout Gross $6.6 million (previously $72 million)

• Approximate Yield (April 7, 2016) ~1.0%

• $200 MM Senior Secured Credit Facility (April 7, 2016) ~$ 0 million net drawn

• $300 MM Senior Unsecured 7 Year Notes (due April 17, 2020) 7.375% coupon (~2.2% after-tax)

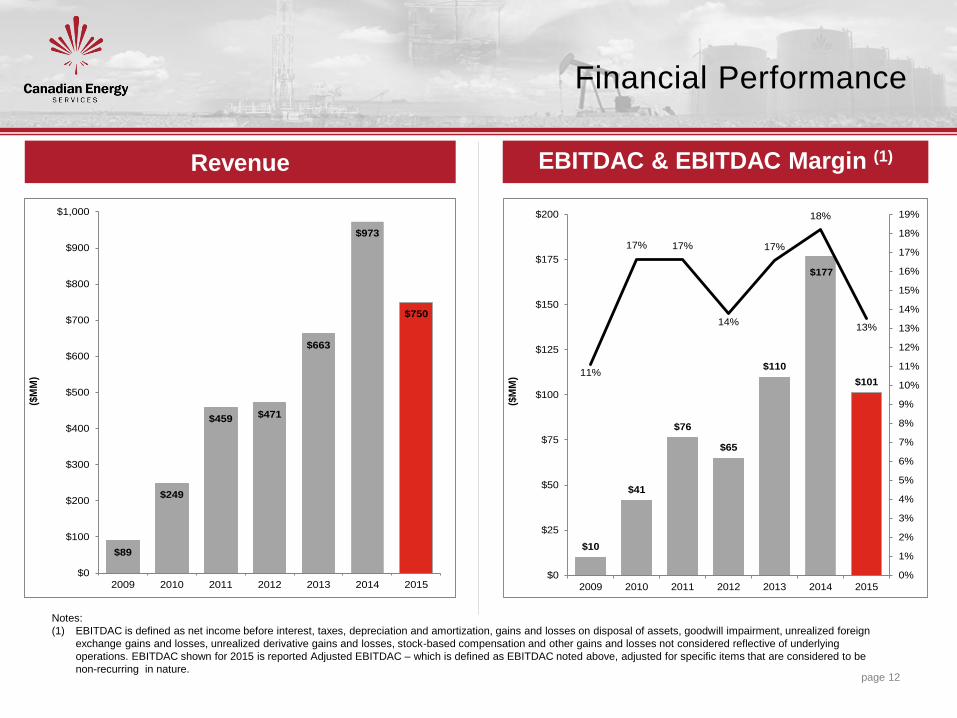

Financial Performance

page 12

Revenue EBITDAC & EBITDAC Margin (1)

Notes:

(1) EBITDAC is defined as net income before interest, taxes, depreciation and amortization, gains and losses on disposal of assets, goodwill impairment, unrealized foreign

exchange gains and losses, unrealized derivative gains and losses, stock-based compensation and other gains and losses not considered reflective of underlying

operations. EBITDAC shown for 2015 is reported Adjusted EBITDAC – which is defined as EBITDAC noted above, adjusted for specific items that are considered to be

non-recurring in nature.

$10

$41

$76

$65

$110

$177

$10111%

17% 17%

14%

17%

18%

13%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

15%

16%

17%

18%

19%

$0

$25

$50

$75

$100

$125

$150

$175

$200

2009 2010 2011 2012 2013 2014 2015

($M

M)

$89

$249

$459 $471

$663

$973

$750

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

2009 2010 2011 2012 2013 2014 2015

($M

M)

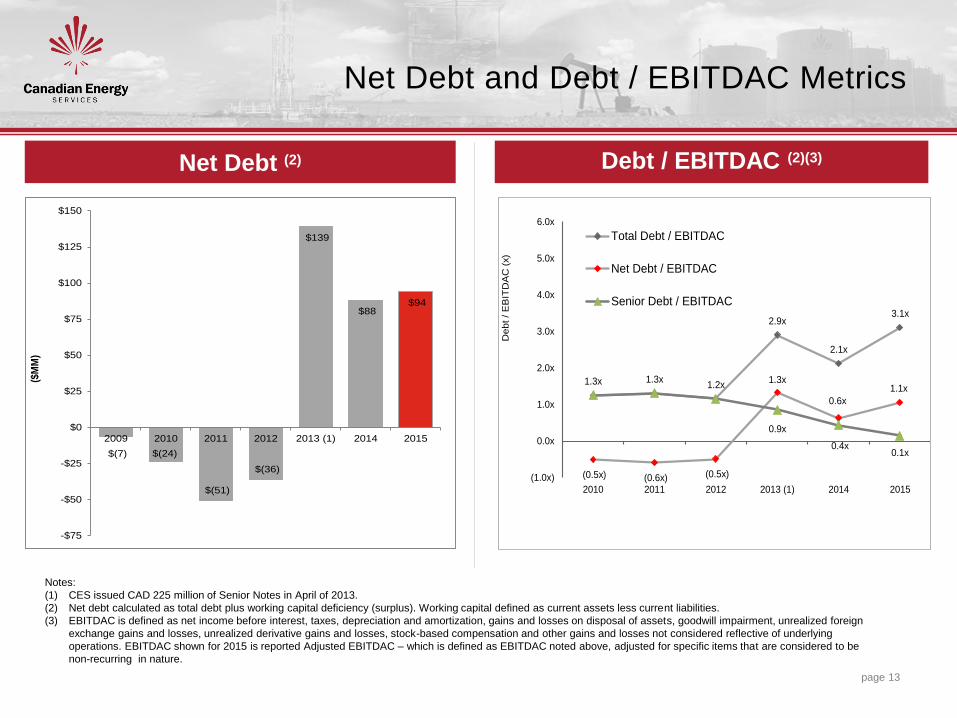

Net Debt and Debt / EBITDAC Metrics

page 13

Net Debt (2) Debt / EBITDAC (2)(3)

Notes:

(1) CES issued CAD 225 million of Senior Notes in April of 2013.

(2) Net debt calculated as total debt plus working capital deficiency (surplus). Working capital defined as current assets less current liabilities.

(3) EBITDAC is defined as net income before interest, taxes, depreciation and amortization, gains and losses on disposal of assets, goodwill impairment, unrealized foreign

exchange gains and losses, unrealized derivative gains and losses, stock-based compensation and other gains and losses not considered reflective of underlying

operations. EBITDAC shown for 2015 is reported Adjusted EBITDAC – which is defined as EBITDAC noted above, adjusted for specific items that are considered to be

non-recurring in nature.

1.3x 1.3x 1.2x

2.9x

2.1x

3.1x

(0.5x) (0.6x) (0.5x)

1.3x

0.6x

1.1x

0.9x

0.4x 0.1x

(1.0x)

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

2010 2011 2012 2013 (1) 2014 2015

Debt / E

BIT

DA

C (

x).

..

Total Debt / EBITDAC

Net Debt / EBITDAC

Senior Debt / EBITDAC

$(7) $(24)

$(51)

$(36)

$139

$88 $94

-$75

-$50

-$25

$0

$25

$50

$75

$100

$125

$150

2009 2010 2011 2012 2013 (1) 2014 2015

($M

M)

page 14

CES is focused on being a leading provider of technically advanced consumable chemical solutions throughout the life-cycle of the oilfield

• CES is a market leader in the Canadian drilling fluids space and expanding position in

the US

• CES’ production and specialty chemicals businesses (PureChem & JACAM) are

expanding sales of consumable chemicals into all facets of the energy industry

• We have a strong balance sheet with debt termed out until 2020 and a low capex business model

• Our vertically integrated business model is positioned to weather current downturn and then capitalize on favorable industry conditions as they return

• Experienced, aligned management team (Management and Insiders hold ~ 15% of common stock)

• We pay a monthly dividend of $0.0025 which is annualized at $0.03/year. CES will protect the balance sheet and be prudent with its dividend

• CES’ competitive advantage is combining our oilfield knowledge and service company culture with vertically integrated manufacturing capabilities

Conclusion

Our Divisions