Embed Size (px)

Citation preview

Corporate Governance in Bulgaria:Results from the Corporate Governance ROSC

A presentation by Sebastian MolineusWorld Bank Corporate Governance GroupIn Sofia on December 12, 2008

2 out of 19

Presentation Outline

1. The Definition of and Business Case for Corporate Governance (CG)

The World Bank’s CG ROSC Program

Key Findings of the CG ROSC for Bulgaria

Policy Recommendations

3 out of 19

Corporate governance is the system by which companies are directed and controlled.

Corporate governance involves a set of relationships between:

- A company’s management

- Board of directors

- its shareholders and

- Other stakeholders

Corporate governance provides the structure through which company objectives are set, attained and monitored.

The “What & Why” of CG >> WB CG ROSC >> Key Findings >> Policy Recommendations

Corporate Governance Defined

4 out of 19

Go

od

bo

ard

pra

ctic

es

and

Co

ntr

ol

Str

uct

ure

s

Man

agin

g S

take

ho

lder

R

elat

ion

s

Str

on

g d

iscl

osu

re &

tr

ansp

aren

cy r

egim

e

Pro

tect

ion

of

(min

ori

ty)

shar

eho

lder

rig

hts

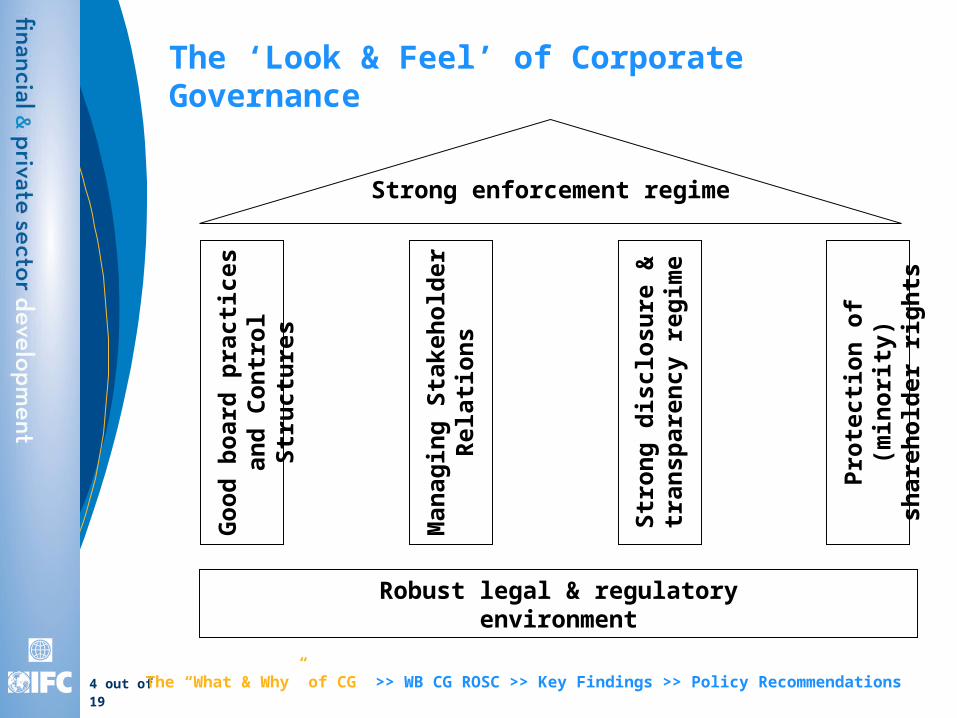

The ‘Look & Feel’ of Corporate Governance

The “What & Why” of CG >> WB CG ROSC >> Key Findings >> Policy Recommendations

Robust legal & regulatoryenvironment

Strong enforcement regime

5 out of 19

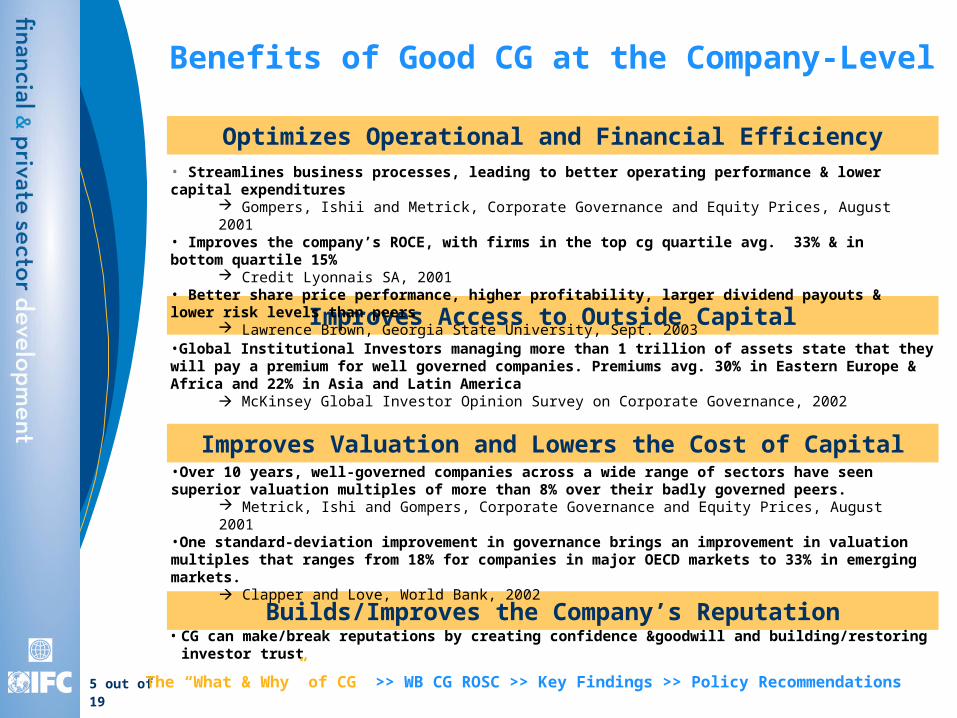

Improves Access to Outside Capital

Improves Valuation and Lowers the Cost of Capital

Builds/Improves the Company’s Reputation

Optimizes Operational and Financial Efficiency• Streamlines business processes, leading to better operating performance & lower capital expenditures

Gompers, Ishii and Metrick, Corporate Governance and Equity Prices, August 2001• Improves the company’s ROCE, with firms in the top cg quartile avg. 33% & in bottom quartile 15%

Credit Lyonnais SA, 2001• Better share price performance, higher profitability, larger dividend payouts & lower risk levels than peers

Lawrence Brown, Georgia State University, Sept. 2003

•Over 10 years, well-governed companies across a wide range of sectors have seen superior valuation multiples of more than 8% over their badly governed peers.

Metrick, Ishi and Gompers, Corporate Governance and Equity Prices, August 2001•One standard-deviation improvement in governance brings an improvement in valuation multiples that ranges from 18% for companies in major OECD markets to 33% in emerging markets.

Clapper and Love, World Bank, 2002

•Global Institutional Investors managing more than 1 trillion of assets state that they will pay a premium for well governed companies. Premiums avg. 30% in Eastern Europe & Africa and 22% in Asia and Latin America

McKinsey Global Investor Opinion Survey on Corporate Governance, 2002

• CG can make/break reputations by creating confidence &goodwill and building/restoring investor trust

Benefits of Good CG at the Company-Level

The “What & Why” of CG >> WB CG ROSC >> Key Findings >> Policy Recommendations

6 out of 19

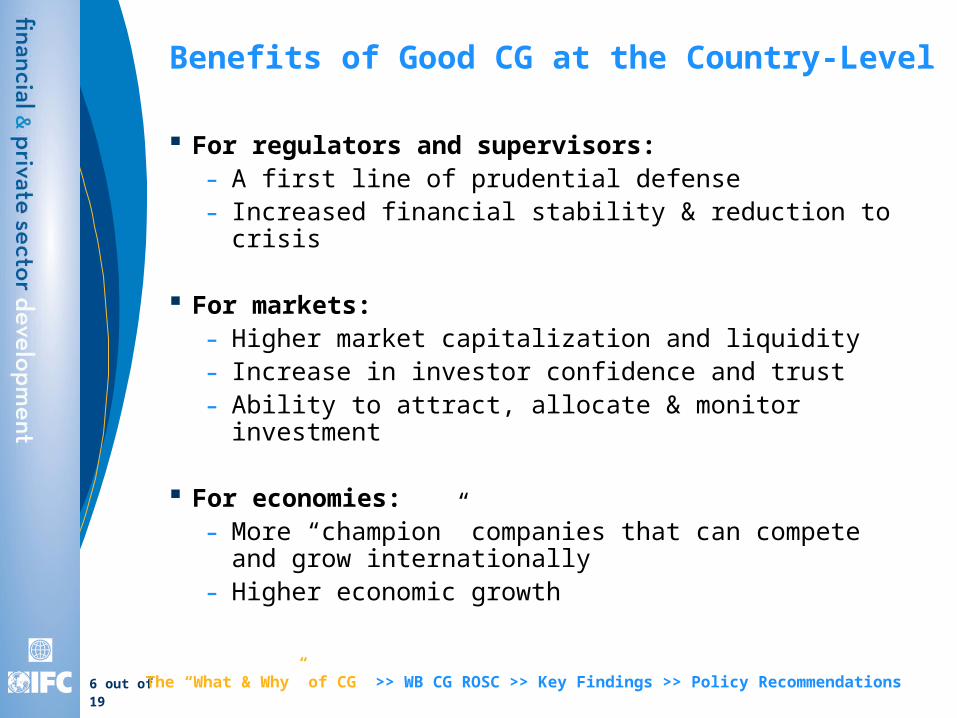

Benefits of Good CG at the Country-Level

For regulators and supervisors: - A first line of prudential defense- Increased financial stability & reduction to crisis

For markets: - Higher market capitalization and liquidity- Increase in investor confidence and trust- Ability to attract, allocate & monitor investment

For economies: - More “champion” companies that can compete and

grow internationally- Higher economic growth

The “What & Why” of CG >> WB CG ROSC >> Key Findings >> Policy Recommendations

7 out of 19

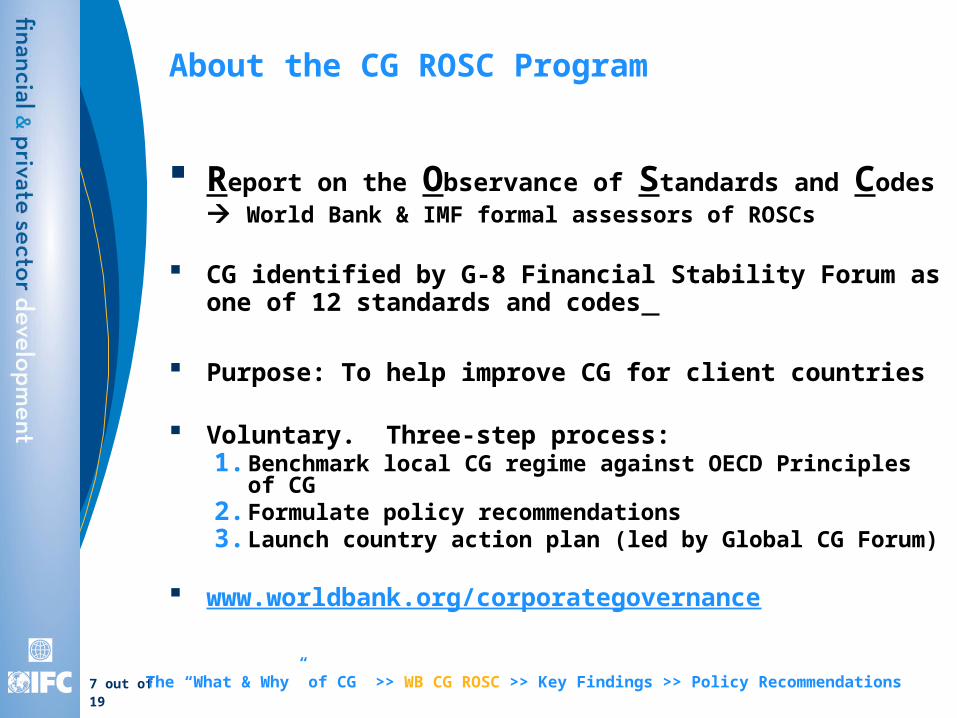

Report on the Observance of Standards and Codes World Bank & IMF formal assessors of ROSCs

CG identified by G-8 Financial Stability Forum as one of 12 standards and codes

Purpose: To help improve CG for client countries

Voluntary. Three-step process:1. Benchmark local CG regime against OECD Principles of CG2. Formulate policy recommendations3. Launch country action plan (led by Global CG Forum)

www.worldbank.org/corporategovernance

About the CG ROSC Program

The “What & Why” of CG >> WB CG ROSC >> Key Findings >> Policy Recommendations

8 out of 19

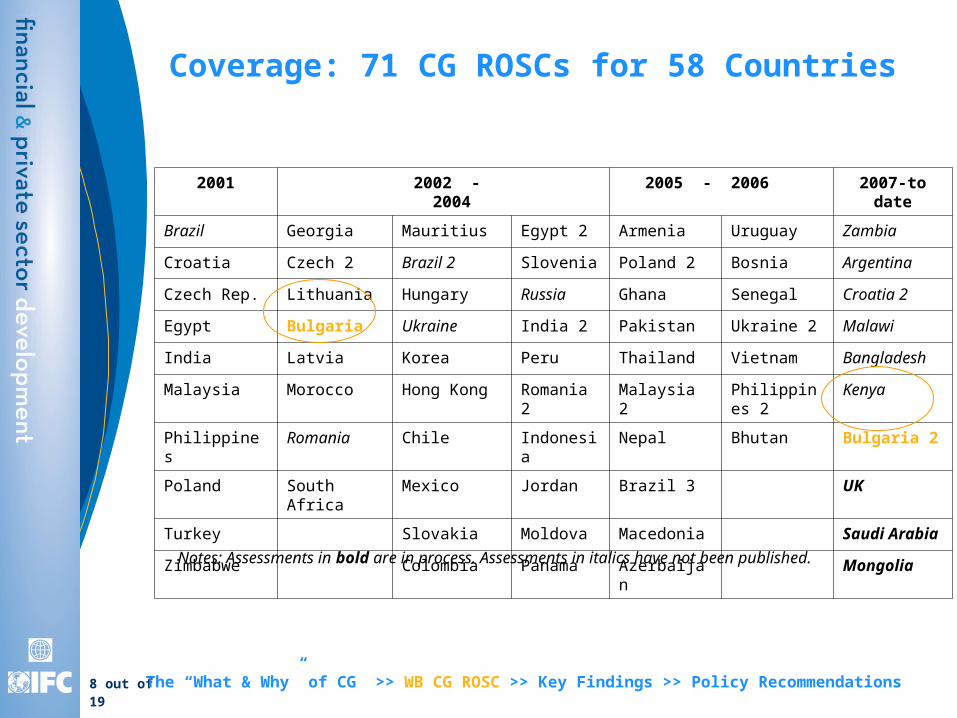

Notes: Assessments in bold are in process. Assessments in italics have not been published.

2001 2002 - 2004

2005 - 2006 2007-to date

Brazil Georgia Mauritius Egypt 2 Armenia Uruguay Zambia

Croatia Czech 2 Brazil 2 Slovenia Poland 2 Bosnia Argentina

Czech Rep. Lithuania Hungary Russia Ghana Senegal Croatia 2

Egypt Bulgaria Ukraine India 2 Pakistan Ukraine 2 Malawi

India Latvia Korea Peru Thailand Vietnam Bangladesh

Malaysia Morocco Hong Kong Romania 2

Malaysia 2 Philippines 2

Kenya

Philippines Romania Chile Indonesia Nepal Bhutan Bulgaria 2

Poland South Africa

Mexico Jordan Brazil 3 UK

Turkey Slovakia Moldova Macedonia Saudi Arabia

Zimbabwe Colombia Panama Azerbaijan Mongolia

Coverage: 71 CG ROSCs for 58 Countries

The “What & Why” of CG >> WB CG ROSC >> Key Findings >> Policy Recommendations

9 out of 19

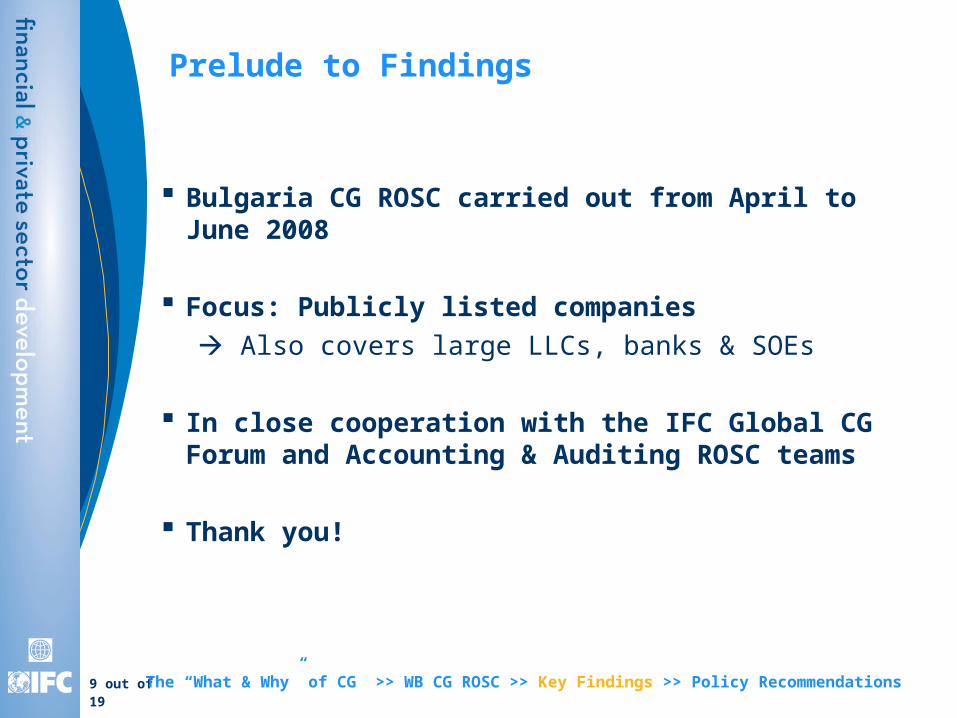

Bulgaria CG ROSC carried out from April to June 2008

Focus: Publicly listed companies Also covers large LLCs, banks & SOEs

In close cooperation with the IFC Global CG Forum and Accounting & Auditing ROSC teams

Thank you!

Prelude to Findings

The “What & Why” of CG >> WB CG ROSC >> Key Findings >> Policy Recommendations

10 out of 19

The “What & Why” of CG >> WB CG ROSC >> Key Findings >> Policy Recommendations

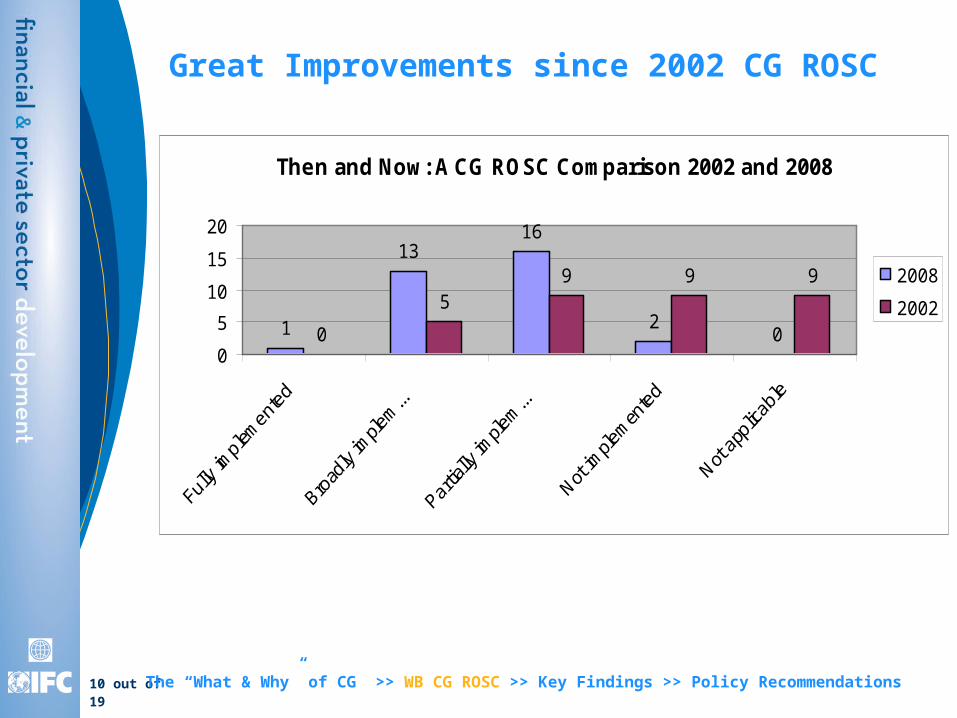

Great Improvements since 2002 CG ROSC

Then and Now: A CG ROSC Comparison 2002 and 2008

1

1316

200

59 9 9

0

5

10

15

20

2008

2002

11 out of 19

Key Message: “Law on the Books” Not Practiced

A few gaps remain in legal and regulatory framework. For example:- Company Law- Code - Enforcement framework

Majority owners dominate board & CG processes

Actual practices lag behind legal reforms as per:- Board practices- Non-financial disclosure- Control frameworks

Key Obstacles

The “What & Why” of CG >> WB CG ROSC >> Key Findings >> Policy Recommendations

Substantial legal, regulatory & institutional reforms, in particular per:- Board practices- Shareholder rights- Disclosure

Launch of National CG Code (NCGC) and National CG Task Force in late 2007

Forty companies have agreed to implement the NCGC

Key Achievements

12 out of 19

While Basic Shareholder Rights are in Place …

Shareholder are able to participate and vote in the GSM- Basic information rights in place

- Ability to vote for directors, executive compensation and dividends

- Preferred SHs, creditors & employees invited to participate w/o vote

Take-over provisions in-line with good CG- Tender offers, squeeze-out and sell-out rights

Special 2/3 and ¾ voting requirements on key issues

Shareholders able to launch direct and derivate suits- Of note: Concept of shadow directors introduced

The “What & Why” of CG >> WB CG ROSC >> Key Findings >> Policy Recommendations

13 out of 19

… Some General Concerns Remain

Cumulative voting not endorsed or practiced

Risk of politicizing non-executive remuneration in GSM

Companies do not generally have dividend policies and declared dividends not fully paid to minority shareholders

No recommendations for institutional investors to participate in governance process

Whistle-blowing procedures should be required or recommended

The “What & Why” of CG >> WB CG ROSC >> Key Findings >> Policy Recommendations

14 out of 19

Findings on Disclosure and Transparency

Disclosure of financial information has improved- See ensuing Accounting & Auditing ROSC

The disclosure of non-financial information remains weak:- Company objectives

- Ownership, in particular control structures and beneficial SHs

- Risk, audit and control frameworks

- CG, despite legal requirement

Most companies do not have CG sections on website or AR

The “What & Why” of CG >> WB CG ROSC >> Key Findings >> Policy Recommendations

15 out of 19

Need to Build Stronger Control Structures …

Risk management and internal controls- Little practical guidance offered, hence underdeveloped

- Compliance function thought to be underdeveloped in banks

Internal audit function- Should report to board’s independent audit cttee.

The external audit process. Independence an issue:- Provision of non-audit work

- Audit partners stay with clients beyond rotation period

- Auditor review process by ICPAB should be strengthened

Best practice calls for independent audit committee

The “What & Why” of CG >> WB CG ROSC >> Key Findings >> Policy Recommendations

16 out of 19

… and Professional and Independent Boards

Role of (supervisory) board not properly understood- Duties of loyalty and care mentioned, but not defined - Little to no succession planning- CG framework built by IR; no ownership by board

Conflicts of interests on board remain an issue- Legal framework is strong, practice is underdeveloped- NCGC recommends ethics code, few have followed suit

Board effectiveness thought to be an issue- Few boards have committees- Board evaluations virtually non-existent

Independent directors not thought to play assigned role

Outside members on management boardThe “What & Why” of CG >> WB CG ROSC >> Key Findings >> Policy Recommendations

17 out of 19

The Legal, Institutional & Enforcement Regime

Legal and regulatory framework much improved- Key amendments to CA, LPOS- Launch of NCGC

Institutional framework robust- Regulatory authorities enjoy positive reputation- Clear enforcement framework- Division of responsibilities clearly articulated- Enforcement takes place in practice- Some difficulty in implementing EU directives in timely manner

Court system remains underdeveloped

The “What & Why” of CG >> WB CG ROSC >> Key Findings >> Policy Recommendations

18 out of 19

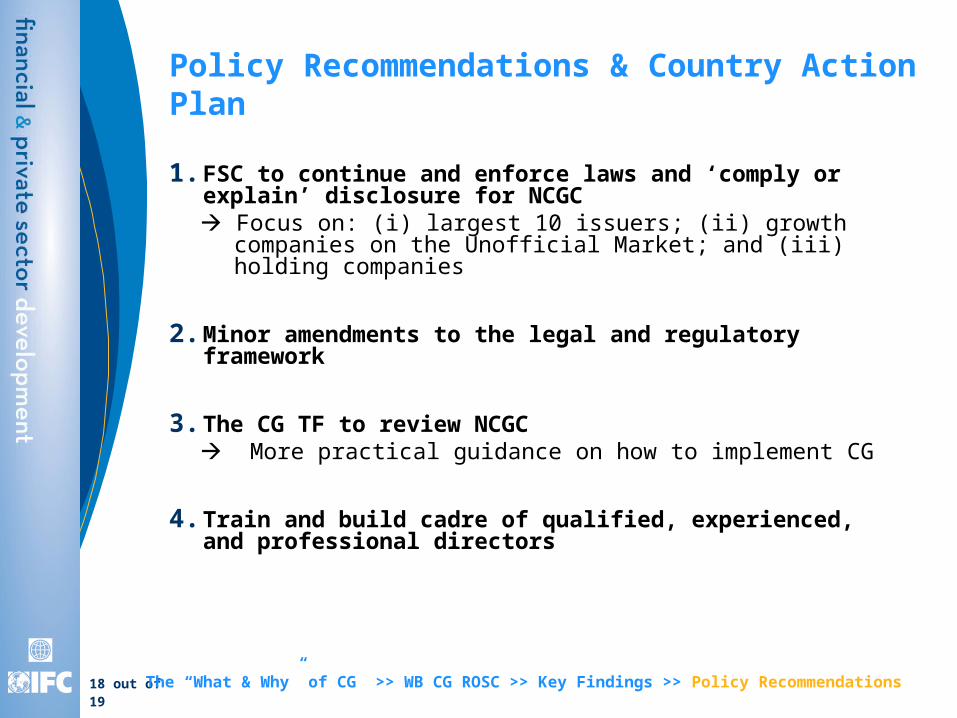

Policy Recommendations & Country Action Plan

1. FSC to continue and enforce laws and ‘comply or explain’ disclosure for NCGC Focus on: (i) largest 10 issuers; (ii) growth companies

on the Unofficial Market; and (iii) holding companies

2. Minor amendments to the legal and regulatory framework

3. The CG TF to review NCGC More practical guidance on how to implement CG

4. Train and build cadre of qualified, experienced, and professional directors

The “What & Why” of CG >> WB CG ROSC >> Key Findings >> Policy Recommendations

19 out of 19

Thank you!

![Corporate Governance Manualpaisalo.in/pdf/corporate-governance-en.pdf · [ 1 ] DEFINITIONS Corporate Governance Corporate Governance is the system of internal controls and procedures](https://img.dokumen.tips/doc/110x75/60457b037dc32d128b177c66/corporate-governance-1-definitions-corporate-governance-corporate-governance.jpg)