Embed Size (px)

Citation preview

Contents

INTR

OEL

ECTR

ICIT

Y

01

02

03

04

05

06

Forewordby Miloš Vučković, Senior Partner and Petar Mitrović, Advokat* / Senior Associate, Karanović & Nikolić

Electricity – Market and Regulatory OverviewKaranović & Nikolić, in cooperation with local lawyers

One Region – One Market / Coupling of electricity markets in the Balkansby Petar Mitrović, Advokat* / Senior Associate, Karanović & Nikolić

The First Anniversary of the Serbian Power Exchangeby Dejan Stojcevski, COO, SEEPEX

TPPS in Bosnia and Herzegovina – The Interplay between „Life“ and „Death“by Robert Kordić, External Counsel, Karanović & Nikolić

EFT’s Stanari: The First Private TPP in Bosnia and Herzegovinaby EFT Group

04

07

20

24

28

32

* Independent attorney at law in cooperation with Karanović & Nikolić

REN

EWA

BLES

& E

FFIC

ENC

YO

IL &

GA

S

07

13

14

15

16

17

08

09

10

11

12

Renewables – Market and Regulatory OverviewKaranović & Nikolić, in cooperation with local lawyers

Oil & Gas – Market and Regulatory OverviewKaranović & Nikolić, in cooperation with local lawyers

The Energy Community: Gas Markets in Transitionby Andrius Šimkus, Gas Expert, Energy Community Secretariat

Quo Vadis? – Gas Destination Clauses and Competition Lawby Veljko Smiljanić, Advokat* / Senior Associate, Karanović & Nikolić

Gasification of the Balkansby Veton Qoku, Advokat* / Attorney at Law , Karanović & Nikolić

Drilling in the Adriatic Seaby Milan Keker, Advokat* / Senior Associate, Karanović & Nikolić & Boris Dvoršćak, Trainee / Junior Associate at Law Office Perica in cooperation with Karanović & Nikolić

Support Scheme for Renewables in Serbia - The Opportunity for Boost?by Petar Mitrović, Advokat* / Senior Associate, Karanović & Nikolić

The Akuo Perspective: Renewable Energies in South East Europeby Vjeka Ercegovac, Akuo

Incentives in Renewable Energy – Tendencies to Followby Leonid Ristev, Advokat* / Attorney at Law and Božidar Milošević

The Development of Community Participation Arrangements in the Renewable Energy Sector in Ireland and the Emergence of the ‘Active Citizen’by Alex McLean, Partner, Arthur Cox

Energy Renovation of Buildings in Sloveniaby Kevin Rihtar, Associate, Karanović & Nikolić

38

58

64

68

76

82

89

96

104

108

112

* Independent attorney at law in cooperation with Karanović & Nikolić

4

01Foreword

Dear friends,

We are pleased to present you with the fourth edition of our Focus on Energy publication. In 2017, we wish to bring to your attention a number of interesting stories and articles within energy sector in Southeast Europe.

Energy is inextricably tied to the economy of a country, and our future is directly influenced by the availability of energy. It is an input for nearly all the goods and services. Energy price shocks and supply interruptions can shake entire regions. So, the importance of this sector can hardly be understated. Perhaps, most especially for the countries that are still developing from an economic point of view.

Without a doubt, the energy sector plays a crucial role in the context of the future developments in Southeast Europe. With that in mind, we would like to use our publication to present the novelties in the markets, new hot opportunities, as well as the success stories of our clients that operate within the sector.

Intensified old initiatives and new ones – the coupling of energy markets, the reassessment and redefining of incentives for renewable energy, views on coal fired plants and carbon emissions, and other important issues make the energy sector one of the most dynamic and challenging sectors in this part of the world.

We would especially like to thank our friends and guest contributors from the Energy Community and SEEPEX for providing us with their views on the energy markets in the region, our colleagues from the Arthur & Cox Law Firm of Dublin for providing us with their views on the community participation arrangements in Ireland and our esteemed clients Akuo Energy and EFT on sharing their experiences with us in this publications. Also, we would like to thank all our colleagues from the Karanović & Nikolić team, who helped us in creating the Energy and Infrastructure Practice Group that is responsible for making the 2017 Focus on Energy publication and for providing a great overview on the current and future tendencies in the region.

Our hopes are that you will enjoy reading this publication, at least as much as we enjoyed preparing it. Should you think that there is room for improvement, please let us know. We appreciate and welcome your feedback, comments and suggestions.

Miloš VučkovićSenior Partner

Petar MitrovićAdvokat* / Senior Associate, Karanović & Nikolić

01 FOREWORD

–* Independent attorney at law in cooperation with Karanović & Nikolić

Electricity

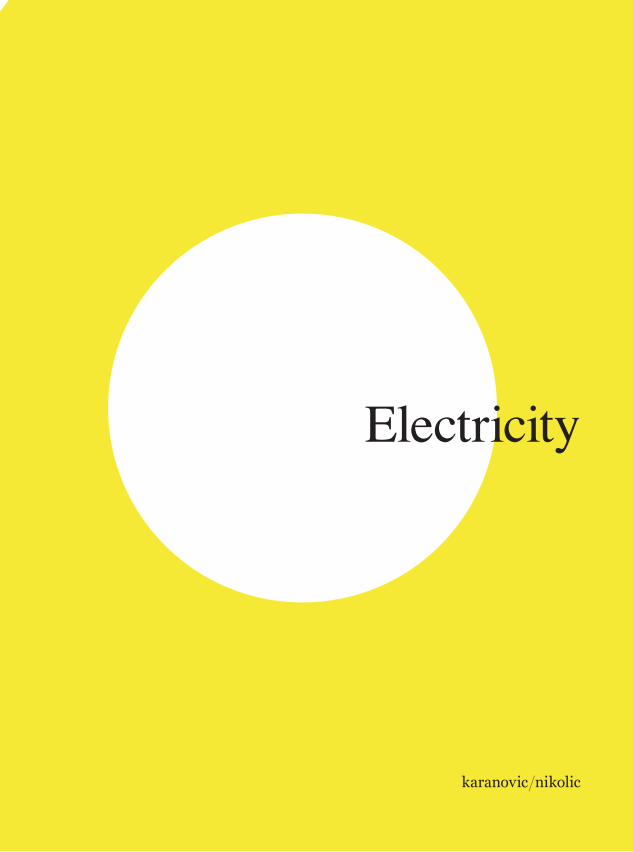

/ Coal-fired Plants / Hydropower Plants

BiH

Croatia

Macedonia

Montenegro

Serbia

Slovenia

Structure of ElectricityGeneration 2017

51.73%

19.61%

68%

41.26%

74%

31.59%

32.22%

54.90%

28.5%

52.78%

24%

31.54%

* small hydropower plants, solar plants and wind plants, industrial power plants

/ Public and utility activities

/ Energy / Other

/ Other *BiH

Croatia

Macedonia

Montenegro

Serbia

Slovenia

16.05%

5.88%

3.5%

9.02%

2%

1.63%

/ Nuclear Power Plants

Croatia

Slovenia

19.61%

35.24%

Serbia 18% Slovenia 0.98% 18.78%BiHBiH

Croatia

Macedonia

Montenegro

Serbia

Slovenia

/ Export1,308

-

787

6,578

7,372

BiH

Macedonia

Montenegro

Serbia

Slovenia

/ Import

3,445

2,591

901

5,564

8,325

BiH

Macedonia

Montenegro

Serbia

Slovenia

Macedonia

Slovenia

18%

26.29%

/ Households42.99%

40.4%

46.5%

51%

26.08%

BiH

Croatia

Macedonia

Serbia

Slovenia

/ Industry36.22%

59.6%

34.5%

29%

45.37%

BiHCroatia

Macedonia

Serbia

Slovenia

/ Construction0.63%BiH

/ Agriculture45.82%

1%

1%

1.28%

BiHSerbia

/ Transport0.85%

0.3%

BiH

Macedonia

Serbia

Slovenia

Structure of ElectricityConsumption

(GWh)

02Electricity – Market and Regulatory OverviewKaranović & Nikolić,in cooperation with local lawyers

Bosnia and Herzegovina

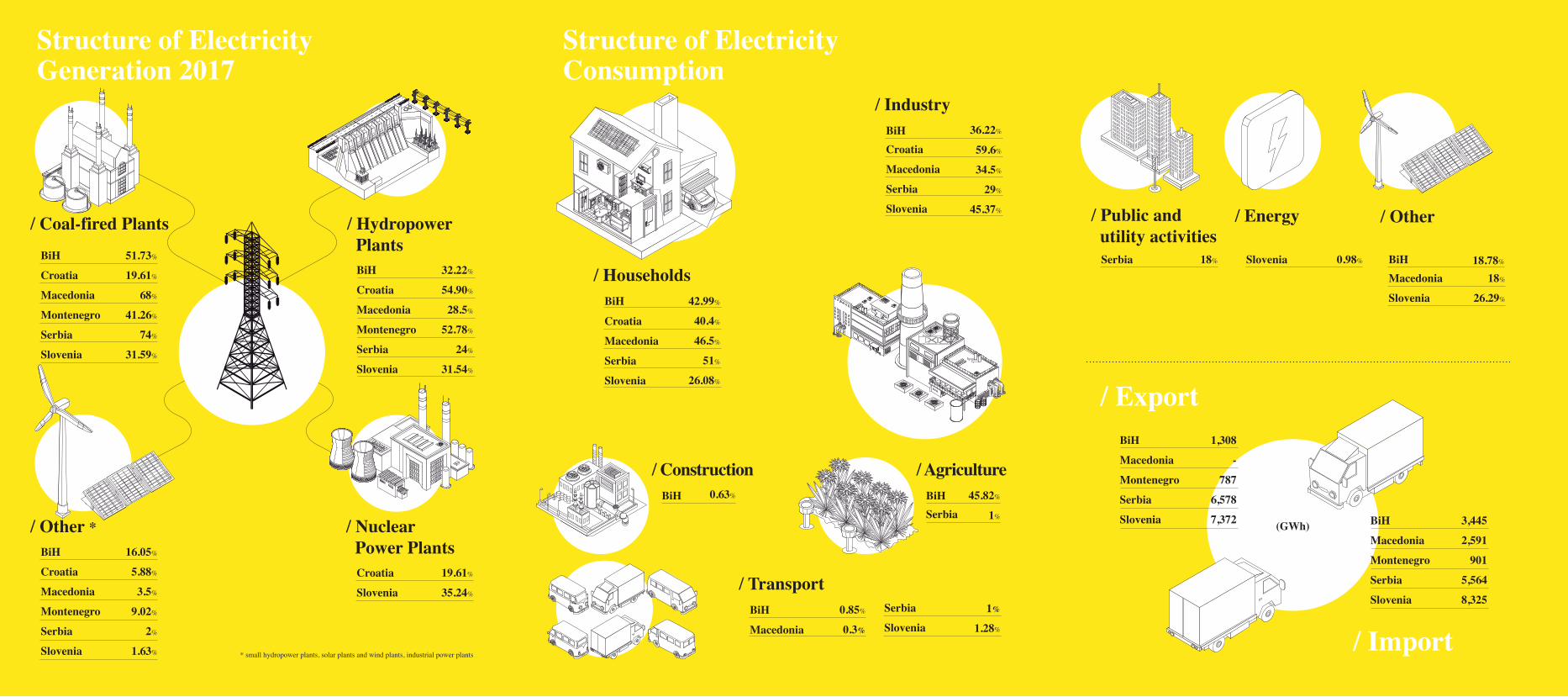

The 2013 Electrical Energy Law and the 2009 Electrical Energy Law (subsequently amended) govern electricity activities in the RS and the FBH respectively. Competencies in the electricity sector in BiH are divided between the central government and the entities RS and FBH. At the central level, the State Electricity Regulatory Commission regulates the transmission of electricity across the entire territory of BiH and the export of electricity, alongside the supply and distribution of electricity to customers in Brčko District1. At the entity level, (i) the governments of the RS and FBH hold policy-making functions; (ii) the RS and FBH Ministries of Industry, Energy and Mining are responsible for implementing energy policy; and (iii) the Regulatory Commission of the RS and the Federal Electricity Regulatory Commission acts as independent regulatory bodies in the RS and FBH respectively, which decide on the issuance of licenses and regulate tariffs.

As of 1 January 2015, customers are able to freely choose their electricity supplier. Gross production of electricity in 2015 decreased by 4.1% compared to 2014 levels, while gross consumption increased by 3.2 % during the same period. Directive 2009/72/EC of the European Parliament and of the Council of 13 July 2009 concerning common rules for the internal market in electricity was not implemented in BiH as per the 1 January 2015 deadline. The FBH 2013 Electrical Energy Law is mostly aligned with the Directive 2009/72/EC, but has yet to be fully implemented.

–1 Brčko District is not an entity, but it has a special status and its own legislation and functions under the decentralized system of local government. In contrast to the RS and FBH, Brčko District does not exercise regulatory powers and accordingly does not have a separate regulatory authority.

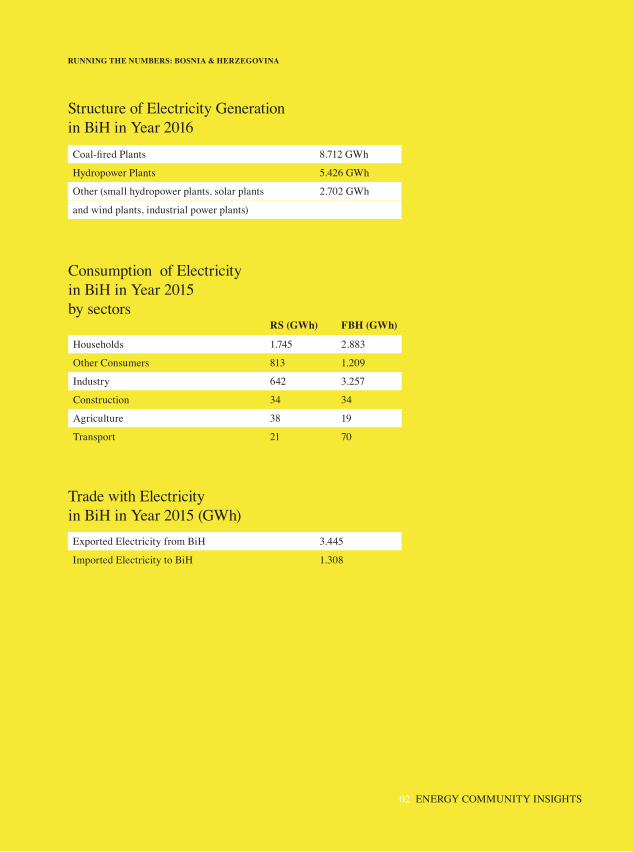

RUNNING THE NUMBERS: BOSNIA & HERZEGOVINA

Structure of Electricity Generation in BiH in Year 2016

Consumption of Electricity in BiH in Year 2015by sectors

Trade with Electricityin BiH in Year 2015 (GWh)

Coal-fired Plants

Exported Electricity from BiH

Imported Electricity to BiH

Other (small hydropower plants, solar plants

and wind plants, industrial power plants)

Hydropower Plants

8.712 GWh

3.445

1.308

2.702 GWh

5.426 GWh

RS (GWh) FBH (GWh)

Households

Industry

Agriculture

Other Consumers

Construction

Transport

1.745

642

38

813

34

21

2.883

3.257

19

1.209

34

70

02 ENERGY COMMUNITY INSIGHTS

10

Croatia

The current regulatory framework governing electricity in Croatia is comprised of the 2012 Energy Law and the 2013 Electricity Market Act, which were adopted as part of the final preparation for the EU membership. As Croatia is an EU member state since July 2013, national electricity market is fully aligned to EU directives, and EU regulations apply directly.

The main authorities responsible for the energy sector are: (i) the Government of the Republic of Croatia, introducing policies and strategy; (ii) the newly established Ministry of Environmental Protection and Energy, in charge of developing Croatian Energy policies; (iii) the Croatian Energy Regulatory Agency (HERA), the independent public institution in charge of regulating energy activities; and (iv) the Croatian Hydrocarbons Agency, the governmental agency in charge of regulating and supervising exploration and production of hydrocarbons in Croatia.

Croatia has adopted the ITO model of market unbundling, with the Croatian TSO being separate from Hrvatska Elektroprivreda (“HEP Group”) which owns the entire Croatian transmission network. While certification is in progress, the Croatian TSO takes part in the Regional Security Coordination Initiative of the Energy Community and the SEE Coordinated Allocation Office for forward capacity allocation and the ITC Agreement compensation mechanism. The most recent activities are aimed at European electricity market coupling and moving from bilateral trading to wholesale with the start of Croatian Power Exchange, CROPEX (fully owned by the TSO and DSO). The Croatian Electricity Market Operator which maintains the certificates of origin registry, became a member of the Association of Issuing Bodies, paving the way for international trading with certificates of origin. There is also a single electricity DSO separated from the HEP Group. Licenses are issued to multiple traders, suppliers and producers.

The installed power of plants on Croatian territory is 4,252 MW, not including the 348 MW generated by the Krško nuclear power plant in Slovenia, in which Croatia has a 50% stake. Almost 85% of electricity is generated within the HEP Group, mostly from hydro and thermal power plants. The capacities of the Croatian electric power system are largely limited with system’s dependence on seasonal hydrological conditions. 2014 saw a 10-year high with 8.4 TWh of production, covering 72% of total consumption of 19.6 TWh. Electricity imports amount to 25% of total consumption. However, because 3 TWh represent imports from the Krško nuclear power plant, actual consumption not covered by domestic capacities is around 13%. This figure fluctuates by up to 5% in years when the seasonal hydrological conditions cause the system to underperform.

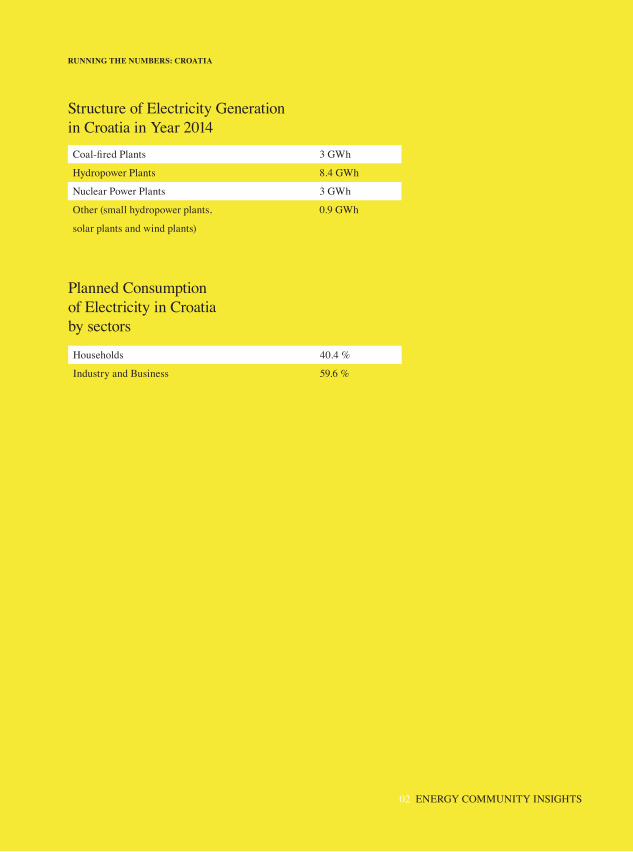

RUNNING THE NUMBERS: CROATIA

Structure of Electricity Generation in Croatia in Year 2014

Planned Consumption of Electricity in Croatiaby sectors

Coal-fired Plants

Nuclear Power Plants

Hydropower Plants

Other (small hydropower plants,

solar plants and wind plants)

3 GWh

3 GWh

8.4 GWh

0.9 GWh

Households

Industry and Business

40.4 %

59.6 %

02 ENERGY COMMUNITY INSIGHTS

12

Macedonia

The regulatory framework for electricity in Macedonia is based on the 2011 Energy Law and accompanying secondary legislation. The 2011 Energy Law is the primary legislation covering energy policies, structure of the electricity market and the protection of consumers, while bylaws regulate the electricity market in more detail. Policy documents include the Energy Development Strategy 2030 and the Strategy for Improvement of Energy Efficiency 2020.

The key authorities in charge of the energy sector are: (i) the Macedonian Government responsible energy sector policy and enacting certain secondary legislation; (ii) the Ministry of Economy, responsible for implementation and supervision of energy laws and policy, and recommending amendments and new laws to the Macedonian Assembly; (iii) the Energy Regulatory Commission, an independent regulatory authority in charge of the issuance of licenses and regulation of the prices and tariff systems for different types of energy by enacting bylaws; and (iv) the Energy Agency which supports implementation of the country’s energy policy.

The electricity market in Macedonia has been fully unbundled since 2006. The state controlled MEPSO is in charge of the electricity transmission system while the privately owned EVN Macedonia (part of EVN Austria Group) operates the distribution system. Although the Macedonian electricity market was to be fully open as of 1 January 2015, only around 430 companies are currently free to choose their supplier. Full liberalisation has been postponed by the Government until 2020 in order to protect households and small businesses from potential ‘price shocks’. Due to the failure to liberalise the electricity market, the Ministerial Council of the Energy Community found that Macedonia did not meet its obligations under the Directive 2009/72/EC and if Macedonia will not take appropriate measures to rectify the breach, the Secretariat of the Energy Community can initiate a procedure for suspending certain rights that arise from the Treaty on Establishing of the Energy Community.

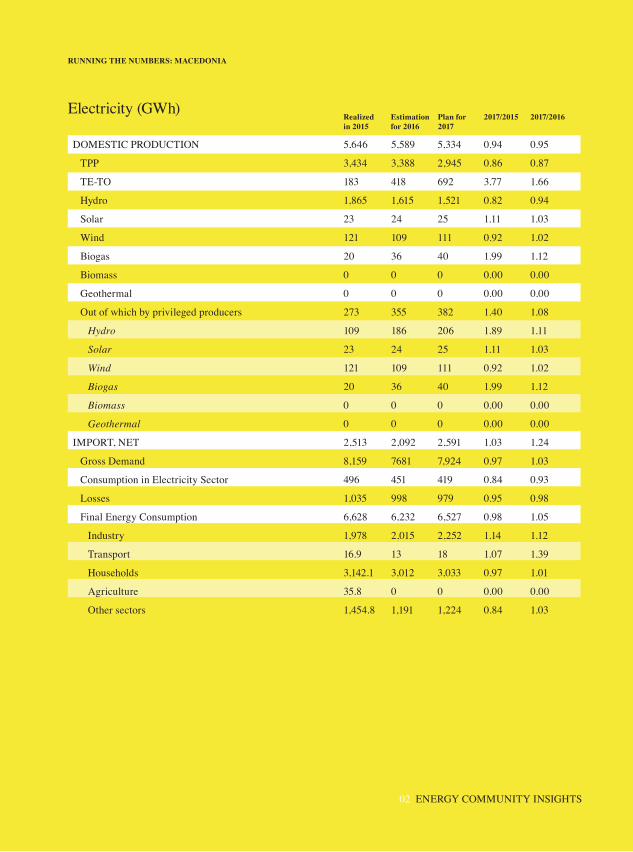

RUNNING THE NUMBERS: MACEDONIA

Electricity (GWh)

DOMESTIC PRODUCTION

TPP

TE-TO

Hydro

Solar

Wind

Biogas

Biomass

Geothermal

Out of which by privileged producers

Hydro

Solar

Wind

Biogas

Biomass

Geothermal

IMPORT, NET

Gross Demand

Consumption in Electricity Sector

Losses

Final Energy Consumption

Industry

Transport

Households

Agriculture

Other sectors

5,646

3,434

183

1,865

23

121

20

0

0

273

109

23

121

20

0

0

2,513

8,159

496

1,035

6,628

1,978

16.9

3,142.1

35.8

1,454.8

5,589

3,388

418

1,615

24

109

36

0

0

355

186

24

109

36

0

0

2,092

7681

451

998

6,232

2,015

13

3,012

0

1,191

5,334

2,945

692

1,521

25

111

40

0

0

382

206

25

111

40

0

0

2,591

7,924

419

979

6,527

2,252

18

3,033

0

1,224

0.94

0.86

3.77

0.82

1.11

0.92

1.99

0.00

0.00

1.40

1.89

1.11

0.92

1.99

0.00

0.00

1.03

0.97

0.84

0.95

0.98

1.14

1.07

0.97

0.00

0.84

0.95

0.87

1.66

0.94

1.03

1.02

1.12

0.00

0.00

1.08

1.11

1.03

1.02

1.12

0.00

0.00

1.24

1.03

0.93

0.98

1.05

1.12

1.39

1.01

0.00

1.03

Realizedin 2015

Estimation for 2016

Plan for 2017

2017/2015 2017/2016

02 ENERGY COMMUNITY INSIGHTS

14

Planned Electricity Generation in Macedonia in Year 2017

Planned Export / Importfor 2017 (GWh)

Planned Consumption of Electricityin Macedonia in Year 2017by sectors

Coal-fired Plants / Natural Gas-fired Plants

Hydropower Plants

Other (solar plants, wind plants and biogas plants)

Exported Electricity from MK

Imported Electricity to MK

68 %

28.5 %

3.5 %

-

2,591

Industry

Transport

Households

Agriculture

Other sectors

34.5 %

0.3 %

46.5 %

0 %

18.7 %

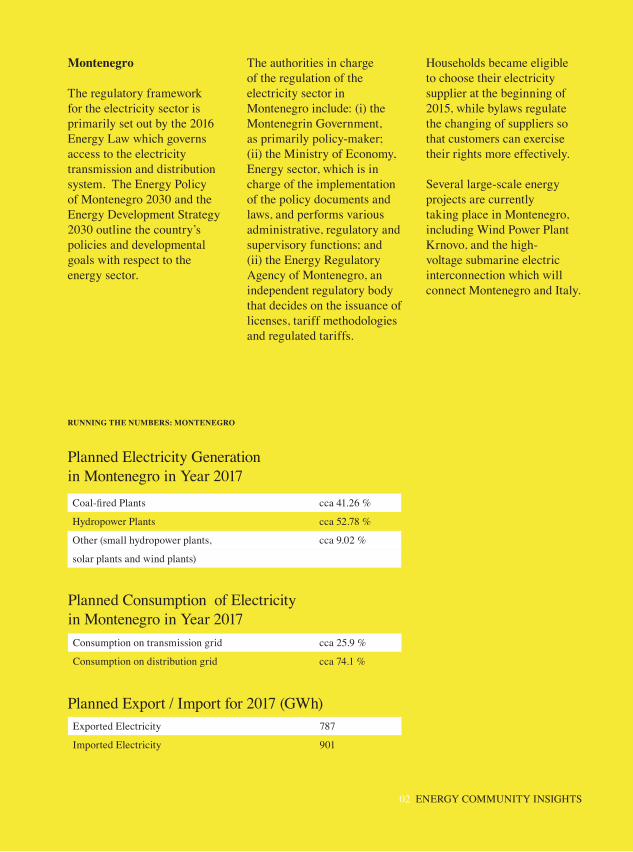

Montenegro

The regulatory framework for the electricity sector is primarily set out by the 2016 Energy Law which governs access to the electricity transmission and distribution system. The Energy Policy of Montenegro 2030 and the Energy Development Strategy 2030 outline the country’s policies and developmental goals with respect to the energy sector.

The authorities in charge of the regulation of the electricity sector in Montenegro include: (i) the Montenegrin Government, as primarily policy-maker; (ii) the Ministry of Economy, Energy sector, which is in charge of the implementation of the policy documents and laws, and performs various administrative, regulatory and supervisory functions; and (ii) the Energy Regulatory Agency of Montenegro, an independent regulatory body that decides on the issuance of licenses, tariff methodologies and regulated tariffs.

Households became eligible to choose their electricity supplier at the beginning of 2015, while bylaws regulate the changing of suppliers so that customers can exercise their rights more effectively.

Several large-scale energy projects are currently taking place in Montenegro, including Wind Power Plant Krnovo, and the high-voltage submarine electric interconnection which will connect Montenegro and Italy.

RUNNING THE NUMBERS: MONTENEGRO

Planned Electricity Generationin Montenegro in Year 2017

Planned Consumption of Electricityin Montenegro in Year 2017

Planned Export / Import for 2017 (GWh)

Coal-fired Plants

Hydropower Plants

Other (small hydropower plants,

solar plants and wind plants)

cca 41.26 %

cca 52.78 %

cca 9.02 %

Consumption on transmission grid

Consumption on distribution grid

Exported Electricity

Imported Electricity

cca 25.9 %

cca 74.1 %

787

901

02 ENERGY COMMUNITY INSIGHTS

16

Serbia

The legal framework for electricity in Serbia is set out under the 2014 Energy Law which, as an umbrella law, prescribes general rules for performing electricity related activities. Serbia transposed the Third Energy Package in the Energy Law in most of its entirety, with the exception of permitting the Energy Agency to issue penalties.

Most of the bylaws have been aligned with the Energy Law during 2016.

The main authorities responsible for the energy sector are: (i) the Serbian Government, in charge of introducing sector policy and strategy; (ii) the Ministry of Mining and Energy, in charge of implementing the energy legal framework and its monitoring and supervision; and (iii) the Energy Agency, an independent regulatory authority in charge of the issuance of licenses, tariff methodologies and regulated tariffs.

State owned enterprises Elektromreža Srbije (EMS) and Elektroprivreda Srbije (EPS) remain the dominant players in the electricity sector. EMS is the transmission system operator. EPS is engaged in production, wholesale and supply of electricity. EPS’s subsidiary, “EPS Distribucija” carries out the distribution and operates the distribution system.

The electricity market is fully liberalised – all consumers are entitled to freely choose their suppliers and be supplied under market terms. Around 40 wholesale suppliers were active on the market, with 8 of them engaged in the supply of final consumers.

Households and small consumers remain, for the time being, entitled to opt to be supplied under regulated tariffs (unlike other consumers which do not have the right to regulated tariffs). The intention of the law is to phase out the regulated supply of electricity, once the Energy Agency finds that there is no more need for the regulation of the electricity prices. Even though the decision to terminate regulated supply may be issued as early as in May 2017, it is unlikely that this will happen in the next few years.

The breakthrough of the year was the launch of the electricity spot market operated by SEEPEX A.D., a joint stock company established by EMS – 75% shares and EPEX SPOT (European Power Exchange) – 25% shares. The maximum tenor of the trades available on SEEPEX are day-ahead, provided that the intention is to gradually introduce new products.

RUNNING THE NUMBERS: SERBIA

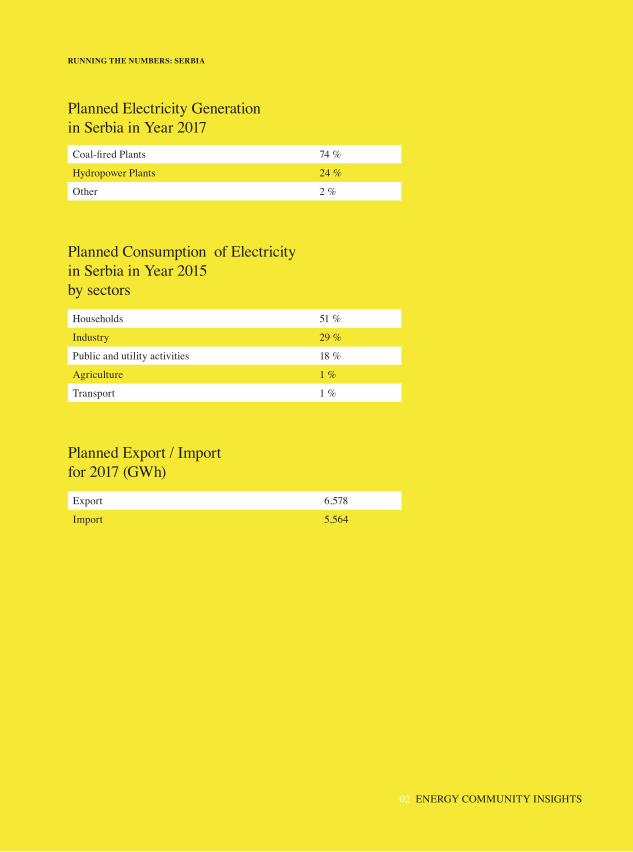

Planned Electricity Generationin Serbia in Year 2017

Planned Consumption of Electricityin Serbia in Year 2015by sectors

Planned Export / Importfor 2017 (GWh)

Coal-fired Plants

Hydropower Plants

Other

74 %

24 %

2 %

Households

Industry

Public and utility activities

Agriculture

Transport

Export

Import

51 %

29 %

18 %

1 %

1 %

6,578

5,564

02 ENERGY COMMUNITY INSIGHTS

18

Slovenia

As a member of the EU, Slovenia is bound by European energy legislation. The Third Energy Package was fully implemented by the 2014 Energy Act. The 2014 Energy Act provides for relatively high consumer protection standards. The Slovenian Energy Concept is still in the process of adoption.

The authorities in charge of the regulation of the electricity sector in Slovenia include: (i) the Slovenian Government, as a primarily policy-maker; (ii) the Energy Agency, which is responsible for ensuring sustainable, reliable and high-quality supply of electricity, developing the sector, and reporting functions; (iii) TSO ELES d.o.o. which owns and operates the Slovenian transmission network. SODO d.o.o.; and (iv) the DSO which ensures secure, reliable and efficient supply of electricity to approximately 1 million consumers in

Slovenia, through five public distribution networks managed by regional electricity companies, which are partially or fully owned by the state. The electricity market organiser is BORZEN d.o.o., which manages the Slovenian Balance Scheme. Any legal or natural person that would like to actively operate in the wholesale and/or retail electricity market must become a member of the Balance Scheme.

The Slovenian network is well integrated with the European electricity system, with interconnectors linking Slovenia to the Italian, Croatian and Austrian networks. A connection with Hungary is in the preparatory phase of construction.

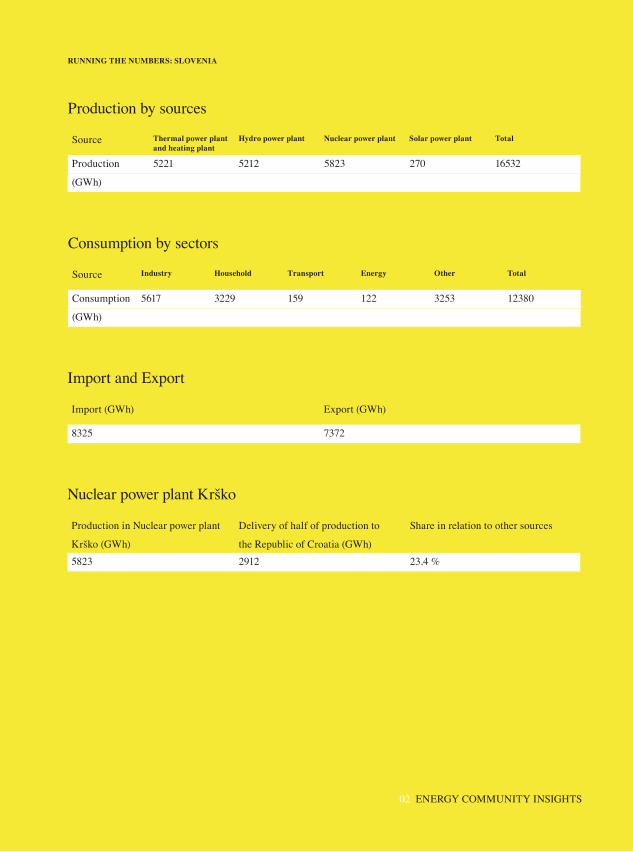

RUNNING THE NUMBERS: SLOVENIA

Production by sources

Consumption by sectors

Import and Export

Nuclear power plant Krško

5221

5617

5212

3229

5823

159

270

122

7372

2912

16532

3253 12380

Thermal power plant and heating plant

Industry

Source

Source

Import (GWh)

Production in Nuclear power plant

Krško (GWh)

Export (GWh)

Delivery of half of production to

the Republic of Croatia (GWh)

Share in relation to other sources

Production

(GWh)

Consumption

(GWh)

8325

5823 23,4 %

Hydro power plant

Household

Nuclear power plant

Transport

Solar power plant

Energy Other

Total

Total

02 ENERGY COMMUNITY INSIGHTS

20

03One Region –One Market/ Coupling ofelectricity marketsin the Balkansby Petar Mitrović, Advokat2 / Senior Associate, Karanović & Nikolić

–2 Independent attorney at law in cooperation with Kranović & Nikolić

03 ONE REGION – ONE MARKET / COUPLING OF ELECTRICITY MARKETS IN THE BALKANS

If necessity is the mother of invention, it is also the father of cooperation.

John David Ashcroft,legal expert

At the Vienna Western Balkans Summit held on 27 August 2015, Albania, Bosnia and Herzegovina, Kosovo*, Macedonia, Montenegro and Serbia (“WB6 Countries”) decided to establish a regional electricity market.

The Needs for Integration

The potential benefits of the integration, of once completely isolated electricity markets of the WB6 Countries, are notable.

All WB6 Countries, taken individually, have small and fragmented electricity markets. As such, they do not have the size to develop efficient markets in isolation.

By coupling once isolated, small and illiquid markets, the WB6 Countries will lay foundations towards the creation of a liquid market of considerable size (with the ultimate step being the full integration of these markets into a pan-European electricity market).

It is expected that an integrated regional market will lead to cost savings for consumers as they enhance competition and offer more efficient use of the existing generation and transmission infrastructure in the region.

The regional market should also enhance the investments in renewable energy – large markets will become a pre-condition for the integration of more renewable energy, since the expansion of renewables in small markets is connected to significant investments in backup production.

By definition, this should attract new investments and increase supply security in the sector.

–* This designation is without prejudice to positions on status, and is in line with UNSC 1244 and the ICJ Opinion on the Kosovo declaration of independence.

22

The Measures

At the Vienna Summit, the WB6 Countries agreed to implement a number of measures in order to establish a regional electricity market. These measures include both regional and national measures.

The regional measures are aimed at strengthening the regional institutions and cooperation.

National measures are primarily intended to remove the countries’ individual barriers to the development of a regional electricity market through the adoption of an appropriate market and regulatory framework, in order to eliminate fragmented markets and uncompetitive practices in the energy sector. These include:

a) Spot Market Development – the countries should (i) adhere to a power exchange or create and own a power exchange, enabling a wholesale market; (ii) remove legal and contractual obstacles identified by the Secretariat of the Energy Community (“EC”); (iii) ensure the liquidity of domestic markets; and (iv) facilitate the coupling of the organised, day-ahead markets with at least one neighbouring country.

b) Cross-border Balancing – the countries agreed to (i) prescribe in their national legislations the possibility for TSOs to acquire balancing services from all operators in the national and, ultimately, regional market under competitive conditions and (ii) adopt a market-based balancing model to allow the non-discriminatory cross-border exchange of balancing services.

c) Regional Capacity Allocation – where the parties concerned should ensure, inter alia: (i) that the transmission system operator (“TSO”) of Serbia – EMS and the TSO of Kosovo* - KOSTT implement the Framework and Inter-TSO Agreement; (ii) that the TSOs from Macedonia and Serbia enter into agreements with the Coordinated Auction Office in South East Europe (“SEE CAO”) on a coordinated allocation; and (iii) the introduction of a coordinated capacity calculation process for the allocation of day-ahead capacities based on a regionally coordinated congestion forecast.

d) Cross-cutting Measures including the liberalisation of national markets, the deregulation of prices, unbundling of the DSOs and supply, strengthening the independence of the national regulatory authorities and increasing the efficiency and capacities of administrative bodies, unbundling and certification of the TSOs.

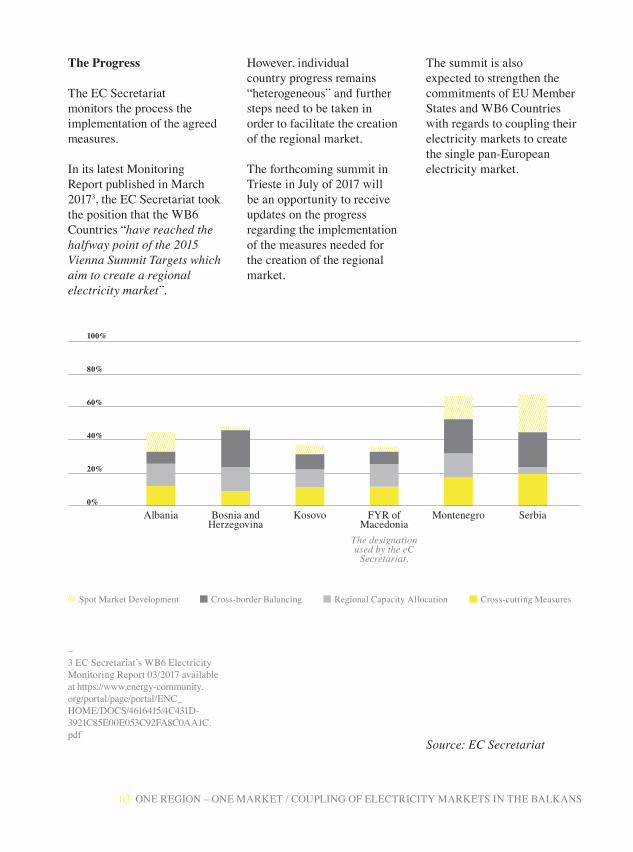

The Progress

The EC Secretariat monitors the process the implementation of the agreed measures.

In its latest Monitoring Report published in March 20173, the EC Secretariat took the position that the WB6 Countries “have reached the halfway point of the 2015 Vienna Summit Targets which aim to create a regional electricity market”.

However, individual country progress remains “heterogeneous” and further steps need to be taken in order to facilitate the creation of the regional market.

The forthcoming summit in Trieste in July of 2017 will be an opportunity to receive updates on the progress regarding the implementation of the measures needed for the creation of the regional market.

The summit is also expected to strengthen the commitments of EU Member States and WB6 Countries with regards to coupling their electricity markets to create the single pan-European electricity market.

–3 EC Secretariat’s WB6 Electricity Monitoring Report 03/2017 available at https://www.energy-community.org/portal/page/portal/ENC_HOME/DOCS/4616415/4C431D-3921C85E00E053C92FA8C0AA1C.pdf

Albania Bosnia and Herzegovina

Kosovo Montenegro SerbiaFYR ofMacedonia

100%

80%

60%

40%

20%

0%

Spot Market Development Cross-border Balancing Regional Capacity Allocation Cross-cutting Measures

Source: EC Secretariat

The designation used by the eC

Secretariat.

03 ONE REGION – ONE MARKET / COUPLING OF ELECTRICITY MARKETS IN THE BALKANS