Embed Size (px)

DESCRIPTION

Construction Insurance 101 or: What You Don’t Know Can Hurt You. Illinois Association of School Business Officials 57 th Annual Conference May 15, 2008. Agenda. The Goals of Risk Management Three Options for Managing Risk The Transfer of Risk Insurance Bonds - PowerPoint PPT Presentation

Citation preview

Construction Insurance Construction Insurance 101 or:101 or:

What You Don’t Know What You Don’t Know CanCan Hurt You Hurt You

Illinois Association of School Illinois Association of School Business Officials Business Officials

5757thth Annual Conference Annual Conference May 15, 2008May 15, 2008

AgendaAgenda

The Goals of Risk ManagementThe Goals of Risk Management

Three Options for Managing RiskThree Options for Managing Risk

The Transfer of RiskThe Transfer of Risk

InsuranceInsurance BondsBonds Other Ways to Transfer RiskOther Ways to Transfer Risk

Planning for the negative consequences Planning for the negative consequences of any decision process or action by usingof any decision process or action by usingwhatever means feasible to control thewhatever means feasible to control thechance of financial loss.chance of financial loss.

Public Sector Risk Public Sector Risk Management ManualManagement Manual

Defining Risk ManagementDefining Risk Management

Basically, RM Involves:Basically, RM Involves:

• Trying to stop losses from happeningTrying to stop losses from happening (through avoidance, risk control, (through avoidance, risk control, loss control or loss prevention)loss control or loss prevention) • Paying for the losses that do occurPaying for the losses that do occur (through reduction, insurance or (through reduction, insurance or risk transfer)risk transfer)

R I S KR I S KAVOIDAVOID CONTROLCONTROL FINANCEFINANCE TRANSFERTRANSFER

Sub-Sub-ContractContract ExitExit PeoplePeople PlantPlant FundFund InsuranceInsurance ContractsContracts

ABSORBABSORB

Risk Management ToolkitRisk Management Toolkit

InsuranceInsurance

A contractual relationship that A contractual relationship that exists when one party (the insurer) exists when one party (the insurer) for a consideration (premium) for a consideration (premium) agrees to reimburse another party agrees to reimburse another party (the insured) for loss to a specified (the insured) for loss to a specified subject (the risk) caused by subject (the risk) caused by designated contingencies (hazards designated contingencies (hazards or perils).or perils).

Why would we Why would we do that??do that??

What Will the Policy Pay?What Will the Policy Pay?

Attachment point = When will the Attachment point = When will the policy begin to pay?policy begin to pay?

Policy limits = the maximum amount Policy limits = the maximum amount the policy will pay (per occurrence or the policy will pay (per occurrence or in the aggregate)in the aggregate)

What are the terms of payment? What are the terms of payment? (When, to whom, conditions)(When, to whom, conditions)

Pay attention to proper notice Pay attention to proper notice (notification of potential claim)(notification of potential claim)

AA FewFewImportant Insurance TermsImportant Insurance Terms

IndemnificationIndemnification To indemnify = to make wholeTo indemnify = to make whole

Waiver of SubrogationWaiver of Subrogation

Waive (release) all rightsWaive (release) all rights Subrogation – to recover from a third Subrogation – to recover from a third

party (e.g., auto salvage)party (e.g., auto salvage)

SubrogationSubrogation

A common law principle inherent in A common law principle inherent in insurance and other insurance and other indemnification transactionsindemnification transactions

It is the right of an insurer to It is the right of an insurer to assume the rights of the insured to assume the rights of the insured to seek remedy against a responsible seek remedy against a responsible partyparty

Most insurance contracts require Most insurance contracts require the insured’s full cooperation in the insured’s full cooperation in this endeavorthis endeavor

Lines of CoverageLines of Coverage

Builders RiskBuilders Risk

BondsBonds

Builders RiskBuilders Risk A Property insurance policy A Property insurance policy

that provides direct damage that provides direct damage coverage on buildings or coverage on buildings or structures while they are structures while they are under construction. under construction.

Also covers:Also covers:

Foundations Foundations

FixturesFixtures

Machinery & EquipmentMachinery & Equipment

Materials & SuppliesMaterials & Supplies

Builders RiskBuilders Risk

Coverage may be written on the Coverage may be written on the following forms:following forms:

Complete Value (100% Complete Value (100% Coinsurance)-Coinsurance)-RECOMMENDEDRECOMMENDED

Reporting Form (Values Reporting Form (Values Reported as Completed)Reported as Completed)

Builders RiskBuilders Risk

Completed value should include all Completed value should include all permanent fixtures and decorations that permanent fixtures and decorations that will be a permanent part of the buildingwill be a permanent part of the building

CONTRACT PRICE DOES NOT CONTRACT PRICE DOES NOT NECESSARILY EQUAL THE FULL VALUE NECESSARILY EQUAL THE FULL VALUE AT COMPLETIONAT COMPLETION

Now That Insurance Is Now That Insurance Is Perfectly Clear…Perfectly Clear…

BondsBonds A form of insurance, but there are A form of insurance, but there are

three partiesthree parties Not Not an aleatory contractan aleatory contract Insurance: premium $$ protects Insurance: premium $$ protects

against defined risksagainst defined risks Bond: premium $$ guarantees a Bond: premium $$ guarantees a

performance, completion or performance, completion or protectionprotection

The surety does not expect lossesThe surety does not expect losses

Definition of (not James) BondDefinition of (not James) Bond

A written instrument guaranteeing the A written instrument guaranteeing the performance, compliance, integrity and performance, compliance, integrity and honesty of the principal by the surety for honesty of the principal by the surety for the benefit of the obligee. The the benefit of the obligee. The instrument binds itself to the terms of an instrument binds itself to the terms of an underlying contract or obligation underlying contract or obligation consisting of a formal agreement, a consisting of a formal agreement, a fiduciary relationship or an official dutyfiduciary relationship or an official duty

Key DefinitionsKey Definitions

ObligeeObligee – The entity protected against – The entity protected against loss and guaranteed adequate loss and guaranteed adequate completion of the underlying completion of the underlying obligation obligation

SuretySurety – The one promising to answer – The one promising to answer for the debt, default or miscarriage of for the debt, default or miscarriage of another another

PrincipalPrincipal – The person whose debt or – The person whose debt or obligation is secured or guaranteed by obligation is secured or guaranteed by the bond the bond

BondsBonds A surety bond is a written contract A surety bond is a written contract

like insurancelike insurance Suretyship = means one party Suretyship = means one party

“answers” for the faults of another“answers” for the faults of another Surety guarantees to an obligee on Surety guarantees to an obligee on

behalf of a principalbehalf of a principal Unlike insurance it guarantees in Unlike insurance it guarantees in

the event of a “failure” to performthe event of a “failure” to perform

Other Types of BondsOther Types of Bonds

Bid Bond = Difference in Bid Bid Bond = Difference in Bid AmountsAmounts

Performance Bond = Failure to do Performance Bond = Failure to do the workthe work

Payment Bond = Guarantee all Payment Bond = Guarantee all bills get paidbills get paid

Maintenance Bond = WarrantyMaintenance Bond = Warranty Supply Contract Bond = Difference Supply Contract Bond = Difference

in Costin Cost

Other Ways to Transfer RiskOther Ways to Transfer Risk

ContractsContracts Additional Insured & Additional Insured &

Named InsuredNamed Insured

Contractual Risk Transfer is NOT Contractual Risk Transfer is NOT Rocket Science…Rocket Science…

…but it is important to understand the “moving parts”

A Valid ContractA Valid Contract

OfferOffer AcceptanceAcceptance ConsiderationConsideration

Legal IntentLegal Intent Agreeable FormAgreeable Form

““A promise recognized by the law as A promise recognized by the law as amounting to a duty, the breach of which amounting to a duty, the breach of which may trigger a legal remedy”may trigger a legal remedy”

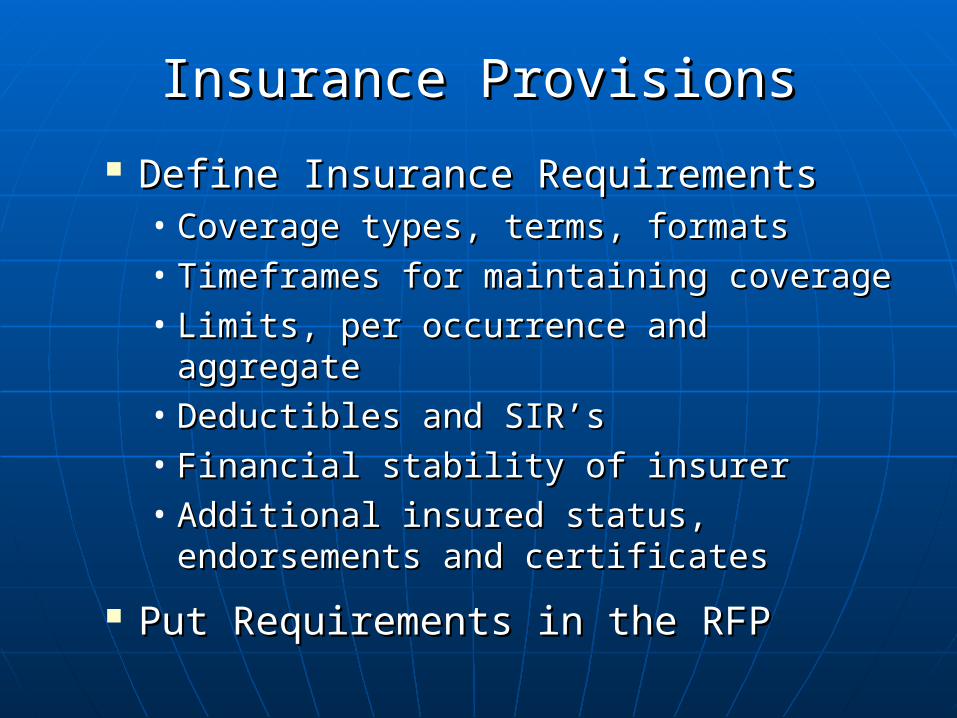

Insurance ProvisionsInsurance Provisions

Define Insurance RequirementsDefine Insurance Requirements• Coverage types, terms, formatsCoverage types, terms, formats• Timeframes for maintaining coverageTimeframes for maintaining coverage• Limits, per occurrence and aggregateLimits, per occurrence and aggregate• Deductibles and SIR’sDeductibles and SIR’s• Financial stability of insurerFinancial stability of insurer• Additional insured status, Additional insured status,

endorsements and certificatesendorsements and certificates

Put Requirements in the RFPPut Requirements in the RFP

Recommended Insurance Recommended Insurance RequirementsRequirements

For purposes of establishing For purposes of establishing insurance requirements, hazard insurance requirements, hazard levels are broken down into three levels are broken down into three categories:categories:

LOW HAZARDLOW HAZARD

MEDIUM HAZARDMEDIUM HAZARD

HIGH HAZARDHIGH HAZARD

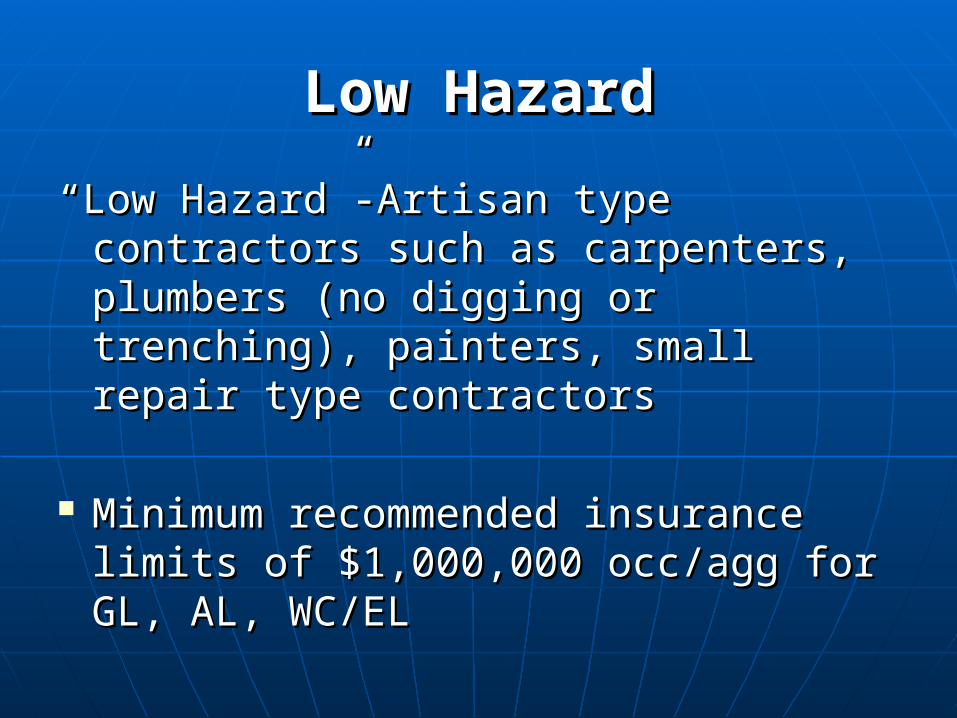

Low HazardLow Hazard

““Low Hazard”-Artisan type contractors Low Hazard”-Artisan type contractors such as carpenters, plumbers (no such as carpenters, plumbers (no digging or trenching), painters, small digging or trenching), painters, small repair type contractorsrepair type contractors

Minimum recommended insurance Minimum recommended insurance limits of $1,000,000 occ/agg for GL, limits of $1,000,000 occ/agg for GL, AL, WC/ELAL, WC/EL

Medium HazardMedium Hazard

““Medium Hazard”-Roofers, plumbing Medium Hazard”-Roofers, plumbing with minor digging, cement with minor digging, cement contractors, grading of land, contractors, grading of land, landscapers, cleaning contractors, landscapers, cleaning contractors, brick layersbrick layers

Minimum recommended insurance Minimum recommended insurance limits of $1,000,000 occ/$2,000,000 limits of $1,000,000 occ/$2,000,000 agg for GL, AL, WC/EL, Prof. Liab.agg for GL, AL, WC/EL, Prof. Liab.

High HazardHigh Hazard

““High Hazard”-Excavation, High Hazard”-Excavation, underground contractors, road underground contractors, road contractors, erection, welding contractors, erection, welding projects, and all major building projects, and all major building construction and renovationconstruction and renovation

Minimum recommended insurance Minimum recommended insurance limits of $1,000,000 occ/$3,000,000 limits of $1,000,000 occ/$3,000,000 agg for GL, AL, WC/EL, Prof. Liab.agg for GL, AL, WC/EL, Prof. Liab.

Using Certificates of InsuranceUsing Certificates of Insurance

Shows evidence that coverage Shows evidence that coverage exists (proof of workers’ exists (proof of workers’ compensation, professional compensation, professional liability coverage, etc.)liability coverage, etc.)

Verifies coverage detailsVerifies coverage details

It It does notdoes not guarantee coverage guarantee coverage for you – the endorsement does for you – the endorsement does thatthat

Certificates & EndorsementsCertificates & Endorsements

How do I review the certificate?How do I review the certificate?

Check limits, company, date, nameCheck limits, company, date, name

The A.M. Best Rating Guide The A.M. Best Rating Guide Hard copy is available from A.M. BestHard copy is available from A.M. Best Computer website:Computer website: www.Ambest.com Grades A – D denotes the financial Grades A – D denotes the financial

performance of the insurerperformance of the insurer Size category I – XV denotes the Size category I – XV denotes the

financial size of the insurerfinancial size of the insurer

EndorsementExample

Back ofCertificate

Certificate of Liability InsuranceACORD Form

Reading an ACORD FormReading an ACORD Form

*

Certificate Review

Additional Insured

Policy may not be obtained

Policy may be modified or

cancelled mid-term

Limits not adequate

Insurer not acceptable

Insurance Certificate

The “Big” PictureThe “Big” Picture

Additional InsuredAdditional Insured

It’s when “Who is an Insured?” (in an It’s when “Who is an Insured?” (in an insurance policy) is amended to include:insurance policy) is amended to include:

The School as an insured party on a The School as an insured party on a contractor’s or vendor’s insurance policy contractor’s or vendor’s insurance policy when the School and the contractor or when the School and the contractor or vendor have entered into a written vendor have entered into a written contract or agreement for the contract or agreement for the performance or operation of some service performance or operation of some service or task. This is done through an or task. This is done through an endorsement to the policy.endorsement to the policy.

Why be an Additional Insured?Why be an Additional Insured?

Reinforces risk transfer Reinforces risk transfer accomplished via contractaccomplished via contract

Effectively waives insurer’s Effectively waives insurer’s ability to subrogate against ability to subrogate against youyou

Provides direct right of Provides direct right of action against insureraction against insurer

CautionCaution

Additional insured status does not Additional insured status does not automatically extend to your employees, automatically extend to your employees,

officers, directors, etc.officers, directors, etc.

This is accomplished This is accomplished only via contract only via contract

languagelanguage

Drafting Contract Insurance Drafting Contract Insurance RequirementsRequirements

Keep both contracting parties in Keep both contracting parties in mind; make it realistic and fairmind; make it realistic and fair

““Boilerplate” language is a guide, Boilerplate” language is a guide, not a rule – exceptions will be not a rule – exceptions will be necessarynecessary

Specify minimum financial rating Specify minimum financial rating standards standards

Make your expectations clear up Make your expectations clear up frontfront

Best PracticesBest Practices Contractual Risk Transfer Contractual Risk Transfer

Put insurance requirements in bidsPut insurance requirements in bids Request & review certificates – be Request & review certificates – be

specific and exactspecific and exact Require proof Require proof beforebefore work begins work begins Know when to ask for help!Know when to ask for help!

ConclusionConclusion

MOST COMMOM MISTAKES MADE SCHOOLS:MOST COMMOM MISTAKES MADE SCHOOLS: Not notifying insurance agent/broker of projectNot notifying insurance agent/broker of project Not insuring to completed valueNot insuring to completed value Not obtaining certificate of insurance from Not obtaining certificate of insurance from

architect, construction manager, and architect, construction manager, and contractorscontractors

Not being named as an additional insured by Not being named as an additional insured by the abovethe above

Not forwarding above certificate to Not forwarding above certificate to agent/broker for reviewagent/broker for review

SIGNING A WAIVER OF SUBROGATION UNDER SIGNING A WAIVER OF SUBROGATION UNDER STANDARD AIA CONTRACTSTANDARD AIA CONTRACT

Speaker InformationSpeaker Information

Ryan Isaacs-Area Vice PresidentPublic Entity & Scholastic DivisionArthur J. Gallagher Risk Mgmt Services

(630)694-5279

![[GAMENEXT] What you don’t know CAN hurt you: Understanding the true meaning of localization](https://img.dokumen.tips/doc/110x75/554d1f73b4c905c5208b49c9/gamenext-what-you-dont-know-can-hurt-you-understanding-the-true-meaning-of-localization-5584a2dfe9de4.jpg)