Embed Size (px)

Citation preview

Considering the DAPM: Low-beta and High-beta Industries

Are low- and high-risk industries empirically consistent with the DAPM?

Abstract

This thesis researches if the Dichotomous Asset Pricing Model (DAPM) is consistent with industry portfolio’s. A distinction between low-risk and high-risk industries is made and the beta will be used to measure this riskiness. Low-risk industries are defined as industries having a beta below 0.8 and are labelled as industries where demand will by stable overtime (e.g. healthcare). High-risk industries are defined as industries having a beta above 1.2 and are labelled as pro-cyclical and sensitive to the conditions of the market (e.g. luxurious companies). Neutral industries (beta between 0.8 and 1.2) are not the subject of this thesis. Results show that low-risk industries are more or less consistent with the DAPM whereas high-risk industries show some deviations. These deviations from the DAPM can be explained by using concepts from behavioral finance and transaction cost theory.

Table of Content

1. Introduction ......................................................................................................................... 3

2. Literature Review ................................................................................................................ 6

2.1. Low-beta and high-beta industries .............................................................................. 6

2.2. Dichotomous Asset Pricing Model (DAPM) ............................................................. 10

3. Methodology ..................................................................................................................... 14

3.1. Data ............................................................................................................................ 14

3.2. Two-pass regression model ....................................................................................... 15

3.3. Ratio’s ........................................................................................................................ 16

4. Results ............................................................................................................................... 17

4.1. Low- and High-beta industry analysis ....................................................................... 17

4.2. Lower- and upper economic environment ................................................................. 18

4.3. High-beta industries recovering from an economic downturn .................................. 22

5. Conclusion ........................................................................................................................ 29

Appendix I ................................................................................................................................ 31

Appendix II .............................................................................................................................. 42

Appendix III ............................................................................................................................. 54

References ................................................................................................................................ 55

University of Amsterdam Thesis July, 2014

Claire de Jager Studentnumber: 10409890 Supervisor: Dr. L. Zou

2

1. Introduction

Asset pricing theory makes an attempt to understand and determine prices or values that

should be paid for an asset in theory (Cochrane, 2000). To value an asset, several models have

been developed to determine the appropriate rate of return of an asset considering its risk.

Using the rate of return and the level of risk (usually measured by the “beta” of the asset), the

value of the asset or portfolio can be determined. To construct optimal portfolios, the investor

attempts to maximize expected return and minimize risk by having various assets in a

portfolio, also called Modern Portfolio Theory (Shipway, 2009). Using asset pricing models,

beta is a good indicator of what will be the level of risk for investors, where a low beta

indicates less risk while a high beta indicates substantial higher risk.

Several investment strategies have been outlined to create an optimized portfolio and generate

returns against lowest possible risk (see for example Dybvig, 1988; Merton, Scholes and

Gladstein, 1978). These strategies are used by investors to make investment decisions that

will yield long-term excessive returns on their portfolio (Woolridge and Snow, 1990; Hayes

and Abernathy, 1980). These strategies make use of diversification to construct an optimal

portfolio for the investor; investing in different companies, different industries and different

types of assets can mitigate the risk and increase return (Bloomfield, Leftwich, and Long Jr.,

1997).

As mentioned above, one of the ways to diversify could be by constructing a portfolio of

stocks in different industries (based on Lessard, 1976). This thesis makes a distinction

between low-risk versus high-risk industries where low-risk industries are labelled as

industries where demand will by stable overtime, even in a downturn economy or scarcity

(e.g. health care) (Wilson, 1999). High-risk industries are labelled as pro-cyclical and

sensitive to the conditions of the market (e.g. luxurious companies) (ibid). Indicating low-risk

industries (i.e. industries with a low beta) and high-risk industries (i.e. industries with a high

beta) is important for investors to execute their investment strategy which implies assessing

3

the riskiness of these industries and optimize their portfolio (based on Asness, Frazzini and

Pedersen, 2013).

In the history of modern portfolio theory, several models have been developed to value assets

and compose optimal portfolios. One of the latest development in the field of asset pricing is

the Dichotomous Asset Pricing Model (DAPM). The DAPM makes a distinction between the

value of an asset when the market is in an economic downturn or upturn (Zou, 2005).

According to this model, the riskiness of the firm can be divided according to these two

different growth stages (the market is in an upturn or in a downturn), therefore, the beta of the

firm can be separated into a beta when the market is in an economic downturn and a beta

when the market is in an economic upturn. In other words, the DAPM will value the riskiness

of the asset individually, i.e. when the market is in an upper-state and when the market is in a

lower-state. The DAPM predicts and confirms that the beta in the lower-state will equal the

beta in the higher-state, therefore the difference in betas of the asset will equal zero.

Combining the distinction between low-beta and high-beta industries (based on Wilson, 1998)

and the DAPM as an asset pricing model (Zou, 2005), the investment strategies in low- and

high-risk industries should empirically be consistent with the DAPM. This means that the beta

in the lower-state will equal the beta in the upper-state, and this will hold for all industries

(i.e. for all low-risk and high-risk industries). The first part of this thesis will investigate

whether this statement is true. The second part of this thesis will investigate why industries or

a cluster of industries will deviate from this statement (i.e. low and high beta-industries are

not consistent with the DAPM). Therefore, the objective of this thesis is in twofold: “are the

low- and high-beta industries empirically consistent with the DAPM? If not, what can be the

reasons for this inconsistency?”.

Fama and French provide several industry classifications based on SIC-codes (Standard

Industrial Classification, used by the government of the United States). This system classifies

firms according to their division, major group and industry group. Fama and French base their

categorization on these codes and classify American firms ranging from 5 to 49 different

industries. This thesis used a specification of 30 industries where daily average value

weighted return in the US market and the daily risk free rate was subtracted from the data of

Fama and French. The CRSP database provided average market returns. With this

4

information, the beta (in lower- and upper-state) according to the DAPM was calculated. For

all data, a time period between 01-01-2003 and 31-12-2013 was chosen.

Results are statistically not significant, however, a closer look showed that low-beta industries

are more or less consistent with the DAPM (Δβ ≈ 0 or Δβ > 0), whereas high-beta industries

showed some deviations (i.e. negative Δβ for most inconsistent industries) Arguments about

loss-aversion, bounded rationality and future prospects and overconfident investors explain

the results from a behavioral point of view. The results also confirm a decrease in transaction

costs and the presence of high frequency traders, where high frequency traders function as

market-makers.

This thesis makes a contribution in two ways, first, a distinction between low-risk and high-

risk industries is made. Previous research has not labelled industries as more or less risky, this

distinction clarifies which industries could add/eliminate risk according to the investor’s

portfolio and preferences. Second, this thesis shows some regularity among inconsistent

industries when using the DAPM. Several explanations are provided why some high-beta

industries are not consistent with the DAPM and show a negative difference between the beta

in the upper-state and the beta in the lower-state. Arguments are mostly found in behavioral

finance but also transaction costs theory gives reasonable explanations.

This thesis proceeds as follows, section 2 will review important literature concerning the

distinction between low-risk and high-risk industries and development of the DAPM. An

outline of the data and methodology will be given in section 3. Section 4 will analyze the

results. Lastly, section 5 will summarize and conclude.

5

2. Literature Review This chapter will outline important theory and empirical findings in the literature regarding

the riskiness of an industry. This thesis will make a distinction between high-risk and low-risk

industries where the beta will be the indicator to measure that risk. In that sense, low-beta and

high-beta industries are considered. Furthermore, the Dichotomous Asset Pricing Model

(DAPM) is explained. Combining the concepts of low- and high-beta industries and the

DAPM will lead to some assumptions and hypothesis at the end of this chapter.

2.1. Low-beta and high-beta industries As Markowitz (1952) explains, preferences of the investor shape their portfolios but the

overall goal of investment portfolios is to maximize return and minimize risk. To hedge risk,

the investor’s portfolio consists of several assets with different characteristics to diversify as

much as possible (this way, risk is reduced). By investing in low-risk stocks yielding a lower

return and investing in high-risk stocks yielding a higher return, the investor has a balanced

strategy. According to his preferences and utility, the investor can take more risk by having

more high-risk stocks or the investor can take less risk by having more low-risk stocks in his

portfolio. In this case, the systematic risk of an individual assets contributing to the portfolio

can increase or decrease the overall risk/return relationship of that portfolio (Klemkosky and

Martin, 1975).

Important is the notion of systematic risk of the asset. Different types and categories of

financial risk are researched. For example, Artzner, et al. (1999) provide two broad categories

of risk: market and nonmarket, also called systematic and non-systematic risk. Dowd (2002)

distinguishes also different types of financial risks: market risk, credit risk, operational risk,

etc. This thesis will only consider market (systematic) risk. Broadly defined, market risk is

6

“the risk of loss (or gain) arising from unexpected changes in the market prices (e.g., such as

security prices) or market rates (e.g., such as interest or exchange rates)” (Dowd, 2002, p.1).

Throughout this thesis, risk will refer to systematic (market) risk unless stated differently.

The beta of a company (partly) reflects its sensitivity to systematic (market) risk and thus its

level of return considering the riskiness of that company (Campell and Mei, 1993). The first

model that demonstrated this relationship was the Capital Asset Pricing Model (CAPM),

where a high beta indicates an asset with higher risk but also the likelihood of higher returns

while a low beta indicates a less risky asset with more stable returns (chapter 2.2 will

elaborate more on the CAPM) (Sharpe, 1964; Lintner, 1965). Risk is created through, among

others, uncertainty in the general environment, industry and/or firm-specific variables (Miller,

1992). Uncertainty in the general environment is created because of political and

governmental instability, and uncertainty coming from the macroeconomic environment

(ibid). Uncertainty related to the industry includes input and product market, competition and

technologies (ibid). Lastly, firm-specific uncertainty is related to firm-specific operations,

management and employees (ibid). This thesis will only focus on industry risk, other forms of

risk will be considered as constant.

Different risk levels due to the nature of the industry has received significant attention in the

literature (i.e. Lessard, 1976; King, 1966). King (1966) shows that differences in risk/return

levels between industries are large enough to subscribe these differences to the industry

effect. He concludes that the industry structure explains the similar risk/return relations for all

firms in that industry, based on this notion, it makes sense to divide industries according to

their riskiness (i.e. low-beta and high-beta industries) (Wilson, 1998). Low-beta industries

will be industries less sensitive to market changes and can be seen as more safely industries

than the market average. Investing in these industries provides less risk but also lower returns.

Conversely, high-beta industries will be industries more sensitive to market changes and can

be seen as more risky industries than the market average. Investing in these industries provide

more risk but also higher returns. Implicitly, there is an assumption made about the

relationship between the average industry beta and the risk of that industry which is the basic

idea behind the CAPM: the beta of the industry reflects the riskiness of that specific industry.

However, this thesis stretches the meaning of the CAPM over industries and not specifically

to firms. In other words, it is assumed that the beta does not only measure risk for firms but

will also hold across industries as a good indicator to measure risk.

7

Assumption 1: The riskiness of the industry is measured by the average beta of all the firms in

that industry, as theorized by the CAPM.

How important are these industry effects? Schmalensee (1985) researches the influence of

industry effects on accounting rates of return at a business level and he finds that performance

is strongly influenced by industry effects. King (1966) finds that 20% of the variance in stock

prices can be explained because of differences between industries. Other studies find

somewhat moderate confirmation. Hawanini and Subramanian (2001) show that for “a few

dominant value creators” [firms that are frontrunners in their industry] and “destroyers” [firms

that are stragglers in their industry] firm-specific factors matter more than industry factors.

However, “for most of firms, i.e. for those that are not notable leaders or losers in their

industry, the industry effect turns out to be an important determinant for the level of

performance rather than firm-specific factors” (Hawanini and Subramanian, 2001, p. 2).

Livingston (1977) empirically investigates the co-movement of stocks within industries and

concludes that there are different industry patterns per industry which supports the view that

efficient diversification can be achieved by having multiple stocks across different industries.

Overall, previous research implies that it makes sense to divide firms in industry clusters.

Therefore, it is assumed that firms can be categorized according to their industry and

industries can be categorized according to their average riskiness.

What is the nature of these differences between industries? In other words, what factors

contribute to the difference in risk across industries? As King (1966) points out, the stock

market is exposed to information that will affect the value of an asset or firm. If there is new

information, this will impact the price of stock A, however, the nature of information may not

only be subjected to stock A. Rather, the information may be important for the industry (or

sub-industry) in which stock A is active. In other words, information (e.g. policy changes,

regulation) is most often relevant for the whole industry and not specifically affecting one

firm (it will also affect stock B, stock C, etc. who are active in the same industry).

Another explanation could be the competitiveness within the industry. MacKay and Phillips

(2005) explain that decisions of the firm (and thus the value of the firm) are partly determined

by the position a firm occupies within the industry. In a competitive industry, the riskiness of

the firm partly depends on actions of other firms in the industry and “its status as entrant,

8

incumbent or existing firm” (MacKay and Phillips, 2005, p. 1433). Maksimowic and Zechner

(1991) represent an example concerning technology. They assume that firms can choose to

adopt a safe technology at a marginal cost, implying lower returns against lower risk, or adopt

a riskier technology at an uncertain cost, implying higher returns against higher risk. In a

competitive environment, it will be most attractive for all firms to adopt the riskier technology

financed with debt to outperform and to compete with each other, therefore, most firms will

do so. In other words, strategic and financing decisions (thus the level of risk) are jointly

determined within competitive industries. In a less competitive environment, there is no force

to choose the risky technology because there is less pressure to outperform, therefore, each

firm does not make decisions based on the industry standard. The extra risk added when

adopting a “riskier” technology is not hedged in a less competitive industry because other

firms within the industry are not forced to meet a specific industry standard in order to

compete. Therefore, less competition within an industry will reduce risk-taking behavior

while highly competitive industries will induce risk-taking behavior in order to be able to

compete.

Furthermore, uncertainty may also be attributable to the industry life cycle (Klepper and

Graddy, 1990; Suarez and Utterback, 1995). Three stages in the industry can be distinguished:

early exploratory stage, intermediated development stage, and mature stage” (Klepper, 1997,

pp. 146/147). The first stage is characterized by a few firms adopting new technologies and

involves a high degree of uncertainty (and thus risk). In the next stage, intermediate

development stage, technologies will be more refined and fit with the demand of the market.

This stage is characterized with less uncertainty compared to the previous stage. The last stage

is characterized by stable and predictable growth where there are no new innovation but just

refinements and improvements. At the end of the mature stage, the industry can experience

renewal (where a new technology takes over the industry) or decline (where the industry

decreases in volume and eventually become extinct) which might increase the degree of

uncertainty. Each stage, especially the exploratory and the possibility of renewal in the mature

stage, brings uncertainty because of market approval of the majority and/or new competitors

entering the industry with a more advanced technology (early adaptors).

Note that the division between industry- and firm-specific factors might have some overlap.

Some firms within the industry will be early adaptors (firm-specific), while sometimes the

whole industry will adopt a new technology (industry-specific). Similarly, some firms can

9

become extinct (firm-specific) but also the entire industry can become irrelevant because of a

new invention (industry-specific).

2.2.Dichotomous Asset Pricing Model (DAPM) As previously stated, asset pricing models are used to assess the relationship between risk and

return of an asset. In history, the Capital Asset Pricing Model (CAPM) of Sharpe (1964) and

Linter (1965) has been the most prominent and discussed asset pricing model. The model was

widely accepted by the financial community because of its theoretical appeal, simplicity and

applicability. The CAPM describes a linear relation between the asset’s expected excess

return and the market expected excess return. The CAPM implies that assets with higher

sensitivity to the market (i.e. these assets bear more risk) should offer higher expected return

as a compensation for bearing such risk. According to the CAPM, the beta is a well-known

indicator to measure the sensitivity of the company to the market (i.e. to measure systematic

or market risk). The Security Market Line (SML) represents a graphical explanation of the

relationship between the expected return and the risk of a company (see figure 1). The risk-

free rate (rf) imposes no risk to the investor, every increase in beta (β) (thus additional risk)

results in higher return (E(ri)) for the investor. Higher return compensates the investor for the

additional risk he takes compared to the market. Therefore, CAPM can be expressed as

𝐸𝐸(𝑟𝑟) = 𝑟𝑟𝑓𝑓 + 𝛽𝛽𝑖𝑖(𝐸𝐸(𝑟𝑟𝑚𝑚) − 𝑟𝑟𝑓𝑓 or rewritten in expected asset’s payoff as 𝐸𝐸(𝑥𝑥) = 𝛽𝛽𝑖𝑖(𝐸𝐸(𝑥𝑥𝑚𝑚).

Besides the great insides of the CAPM, numerous empirical studies have shown that the

CAPM has some failures, e.g. the CAPM fails to explain the cross-section of average stock

returns (Campbell and Voulteenaho, 2003).

Figure 1. Security Market Line

Source: e.g. Sharpe (1964) and Linter (1965)

10

Since the CAPM, multiple variations of asset pricing models have come across. One of the

variations is the Dichotomous Asset Pricing Model (DAPM). The DAPM is one of the newest

asset pricing models by Zou (2005) allowing investors to make rational decisions about their

investments. The basic rationale behind asset pricing models, as described above, will hold

because the DAPM is an extension of the CAPM. The DAPM model considers a two-state

model where the market can be in an upper-state or lower-state. If it is more profitable to

invest in the market than in a risk-free asset, the market is in an upper-state (i.e. 𝑟𝑟𝑚𝑚 > 𝑟𝑟0). If it

is more profitable to invest in a risk-free asset than in the market, the market is in a lower-

state (i.e. 𝑟𝑟𝑚𝑚 ≤ 𝑟𝑟0). Therefore, the return of asset i (ri) depends whether the market is in an

upturn or downturn. It follows for all assets i, their upper-market expected gain equals

x�i = ri − r0, 𝑖𝑖𝑖𝑖 rm > r0 𝑎𝑎𝑎𝑎𝑎𝑎 x�i = 0 otherwise. Similarly, for all assets i, their lower-

market expected loss equals 𝑥𝑥i = r0 − ri, 𝑖𝑖𝑖𝑖 rm ≤ r0 𝑎𝑎𝑎𝑎𝑎𝑎 𝑥𝑥i = 0 otherwise. Following the

logic of the CAPM (written in asset’s expected payoff),

𝑈𝑈𝑈𝑈𝑈𝑈𝑈𝑈𝑟𝑟 𝑚𝑚𝑎𝑎𝑟𝑟𝑚𝑚𝑈𝑈𝑚𝑚 𝑠𝑠𝑚𝑚𝑎𝑎𝑚𝑚𝑈𝑈: 𝐸𝐸(𝑥𝑥𝑖𝑖) = 𝛽𝛽𝑖𝑖+𝐸𝐸(𝑥𝑥𝑚𝑚), 𝛽𝛽𝑖𝑖+ = 𝐸𝐸(𝑥𝑥𝑚𝑚𝑥𝑥𝑖𝑖)𝐸𝐸�𝑥𝑥𝑚𝑚

2 �

𝐿𝐿𝐿𝐿𝐿𝐿𝑈𝑈𝑟𝑟 𝑚𝑚𝑎𝑎𝑟𝑟𝑚𝑚𝑈𝑈𝑚𝑚 𝑠𝑠𝑚𝑚𝑎𝑎𝑚𝑚𝑈𝑈: 𝐸𝐸�𝑥𝑥𝑖𝑖� = 𝛽𝛽𝑖𝑖−𝐸𝐸�𝑥𝑥𝑚𝑚�, 𝛽𝛽𝑖𝑖− = 𝐸𝐸(𝑥𝑥𝑚𝑚𝑥𝑥𝑖𝑖)𝐸𝐸�𝑥𝑥𝑚𝑚2 �

In theory, the DAPM will hold if the market portfolio meets two conditions. First, the market

portfolio should be mean-variance (MV) efficient (see condition 1). This implies that that the

portfolio should minimize the variance for any given value of the mean. In other words, there

is no other portfolio that has a higher return (E(rm)) against lower risk (r𝑚𝑚) than the market

portfolio. This condition is met when the market portfolio has the highest Sharpe ratio (𝜂𝜂2)

compared to all other portfolios. Second, the portfolio should be gain-loss (GL) efficient (see

condition 2). This implies that the market portfolio has the highest gain-loss ratio, i.e.

portfolio has the highest gains (𝐸𝐸�̅�𝑥) against the lowest possible losses (𝐸𝐸𝑥𝑥). In this case, there

is no investment strategy that will generate higher returns against possible losses than the

market portfolio (Zou, 2005). It is assumed that the market MV and GL efficient when using

the DAPM, i.e. the following conditions hold:

Condition 1: 𝜂𝜂2(𝑥𝑥𝑖𝑖) ≤ 𝜂𝜂2(𝑥𝑥𝑚𝑚) < 1, 𝐿𝐿ℎ𝑈𝑈𝑟𝑟𝑈𝑈 𝜂𝜂(𝑥𝑥) = 𝐸𝐸(𝑥𝑥)�𝐸𝐸(𝑥𝑥2)

Condition 2: 𝑍𝑍(𝑥𝑥𝑖𝑖) ≤ 𝑍𝑍(𝑥𝑥𝑚𝑚) < ∞, 𝐿𝐿ℎ𝑈𝑈𝑟𝑟𝑈𝑈 𝑍𝑍(𝑥𝑥) = 𝐸𝐸(𝑥𝑥+)𝐸𝐸(−𝑥𝑥−)

11

When the market is MV and GL efficient, i.e. condition 1 and 2 are met, the beta in the upper

market state will be equal to the beta in the lower market state. Intuitively explained; when the

market is MV and GL efficient, the expected return of the investor’s portfolio cannot be

higher than the return of the market because the market portfolio will generate the highest

expected return, holding risk constant (i.e. no arbitrage). This also holds for the level of risk:

the level of risk the investor’s portfolio bears cannot be lower than the risk of the market

because the market portfolio will provide the lowest possible level of risk, holding return

constant (i.e. no risk arbitrage). This implies that an investor cannot profit from opportunities

where an asset will have different risk/return levels, i.e. 𝛽𝛽𝑖𝑖+ = 𝛽𝛽𝑖𝑖−. For a mathematical proof,

see Zou (2005).

Difference between the DAPM and CAPM is the extension of a two-state model where the

beta of an asset is expressed in different states of the economy (i.e. lower-state or higher-

state). Where the CAPM assumes one beta, regardless the state of the market, the DAPM

takes the external economic conditions into account. Furthermore, the DAPM implies the

CAPM but not the other way around. Because of MV efficiency, the CAPM should hold but

the DAPM will only hold if there is also GL efficiency. As pointed out before, similarities

exist because of the same rationale (i.e. the DAPM is based on the CAPM with some

additional insights).

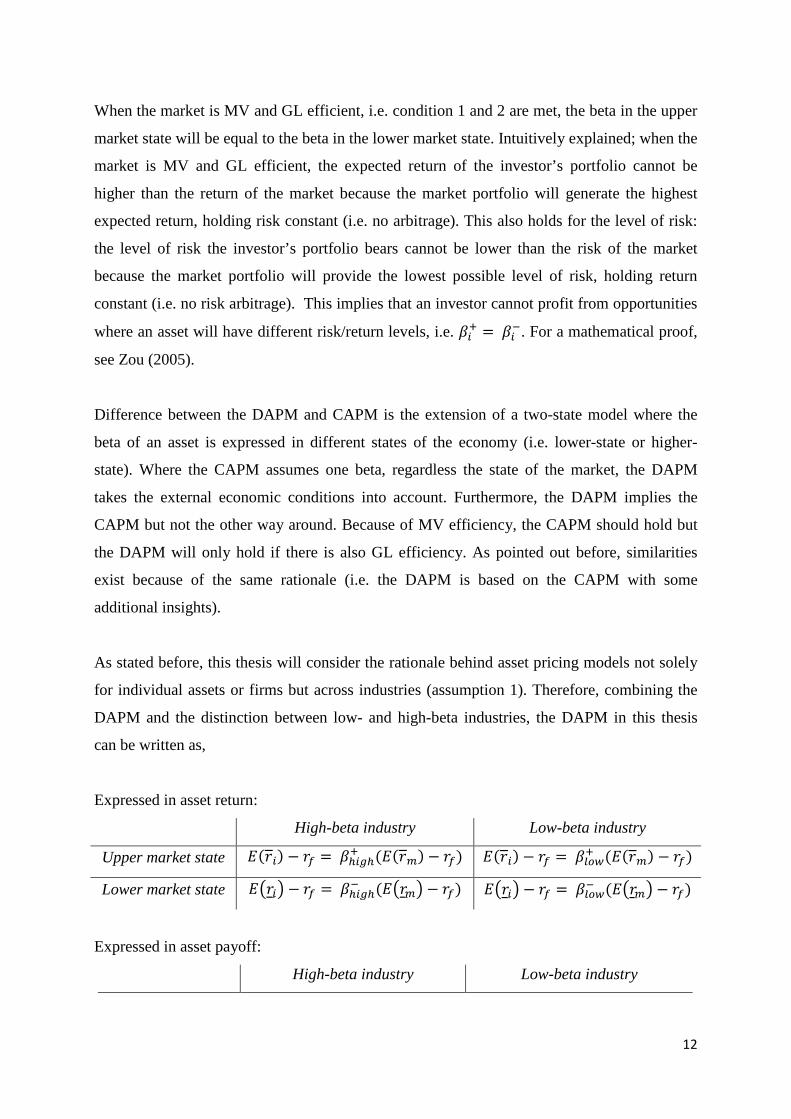

As stated before, this thesis will consider the rationale behind asset pricing models not solely

for individual assets or firms but across industries (assumption 1). Therefore, combining the

DAPM and the distinction between low- and high-beta industries, the DAPM in this thesis

can be written as,

Expressed in asset return:

High-beta industry Low-beta industry

Upper market state 𝐸𝐸(𝑟𝑟𝑖𝑖) − 𝑟𝑟𝑓𝑓 = 𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ+ (𝐸𝐸(𝑟𝑟𝑚𝑚) − 𝑟𝑟𝑓𝑓) 𝐸𝐸(𝑟𝑟𝑖𝑖) − 𝑟𝑟𝑓𝑓 = 𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙+ (𝐸𝐸(𝑟𝑟𝑚𝑚) − 𝑟𝑟𝑓𝑓)

Lower market state 𝐸𝐸�𝑟𝑟𝑖𝑖� − 𝑟𝑟𝑓𝑓 = 𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ− (𝐸𝐸�𝑟𝑟𝑚𝑚� − 𝑟𝑟𝑓𝑓) 𝐸𝐸�𝑟𝑟𝑖𝑖� − 𝑟𝑟𝑓𝑓 = 𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙− (𝐸𝐸�𝑟𝑟𝑚𝑚� − 𝑟𝑟𝑓𝑓)

Expressed in asset payoff:

High-beta industry Low-beta industry

12

Upper market state 𝐸𝐸(𝑥𝑥𝑖𝑖) = 𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ+ 𝐸𝐸(𝑥𝑥𝑚𝑚) 𝐸𝐸(𝑥𝑥𝑖𝑖) = 𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙+ 𝐸𝐸(𝑥𝑥𝑚𝑚)

Lower market state 𝐸𝐸�𝑥𝑥𝑖𝑖� = 𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ− 𝐸𝐸�𝑥𝑥𝑚𝑚� 𝐸𝐸�𝑥𝑥𝑖𝑖� = 𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙− 𝐸𝐸�𝑥𝑥𝑚𝑚�

Where 𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙 represents the beta of the industries that are less sensitive to market changes, i.e.

these industries provides less risk but also lower returns for investors and 𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ represents the

beta of the industries that are more sensitive to market changes, i.e. these industries provide

more risk but also higher returns for investors. Since a high beta indicates higher risk but also

the likelihood of higher returns, this is characterizing for high-beta industries. Conversely, a

low beta indicates a less risky assets with more stable returns, characterizing low-beta

industries. The plus (𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ/𝑙𝑙𝑙𝑙𝑙𝑙+ ) and minus (𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ/𝑙𝑙𝑙𝑙𝑙𝑙

− ) signs indicate respectively if the

market is in an upturn or downturn.

Assuming categorization of industries according to their beta, one could distinguish low-,

neutral- and high-risk industries (as explained above, this thesis will focus on the difference

between low- and high-beta industries). According to the CAPM (and DAPM), a risk-free

asset has a beta of 0 and the market has an average beta of 1 (Sharpe, 1964; Lintner, 1965).

Therefore, low-risk industries should have a beta between 0 and >1, neutral-risk industries

have a beta around 1, and high-risk industries should have a beta higher than 1. For simplicity,

it is assumed that an industry with a beta below 0.8 is indicated as a low-risk industry and an

industry with a beta above 1.2 will be labelled as a high-risk industry. Everything in between

will be considered as a neutral-“risk” industry and not be relevant for this thesis. Note that the

term neutral-risk does not mean risk-free, it means that the differences with the risk/return of

the market portfolio are not substantial enough to classify themselves as low- or high-risk

industries. In that sense, neutral-risk industries have more or less the same characteristics as

the market portfolio and were therefore not mentioned before.

Assumption 2: Industries can be categorized according to their riskiness of the average firm

within that industry measured by calculating the beta. A distinction between

low-, neutral- and risky industries can be made where;

Beta < 0.8 is categorized as low-beta industry (βlow)

0.8 ≤ Beta ≤ 1 is categorized as neutral-beta industry (βneutral)

Beta > 1 is categorized as high-beta industry (βhigh)

13

Logically, βlow < βhigh. Besides the separation between low- and high-beta industries, the

DAPM includes the dynamics of the overall economic environment. Because the beta in an

upturn equals the beta in a downturn, assumption 2 implicitly validates 𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙+ = 𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙− < 𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ+ =

𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ− . Next, the DAPM will be consistent with low- and high-risk industries if the following

hypothesis holds:

Hypothesis: Because the market is MV and GL efficient, the beta in an upturn and the beta

in a downturn will be equal across industries, therefore,

∆𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙 = 𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙+ − 𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙− = 0

∆𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ = 𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ+ − 𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ− = 0

3. Methodology

Testing the assumptions and hypothesis, two different analyses should be done. First, an

industry analysis should indicate which industries can be labelled as low- or high-beta

industries. Second, the upper- or lower-state of the economic environment and the beta in

each state should be examined per industry in order to test the hypothesis.

3.1. Data To test the hypothesis, a distinction in industries should be made to indicate which industries

bear more (high-beta industry) or less risk (low-beta industry) compared to the market.

According to the U.S. Security and Exchange Commission (SEC) there are 12 industries

(labelled as A/D) and several sub-industries (labelled as SIC). Appendix I gives an overview

of all the industries and sub-industries according to the SEC. Within an industry, there exist

differences in risk per company due to company-specific characteristics. However, following

Fama and French it is assumed that the industry average will display an even picture despite

some outliers, therefore, the average beta industry will give a clear indication about the

overall riskiness of the industry. Fama and French provide several industry portfolios based

on the SEC and data according to these industry portfolios, therefore, their research data will

be used. The range of these portfolios differs; e.g. Fama and French provide several

definitions of industries and their sub-industries where they divide U.S. firms in 5, 10, 12, 17,

14

30, 38, 48 or 49 different industry portfolios. Using a narrow definition of industry groups

(e.g. separating all companies in 5 different industries) might cause extreme outliers but still

have an average beta because of the large differences within the industry. However, a wide

definition of industry groups (e.g. separating all companies in 49 different industries) might

lead to fragmentation and will make it more difficult to analyze. Therefore, a specification of

30 industries is used. A definition of the industries according to the SIC-codes can be found in

appendix II. For each industry, the daily average value weighted return (𝑟𝑟𝑖𝑖) in the period 01-

01-2003 until 31-12-2013 in the US market will be used. Also the daily risk-free rate (𝑟𝑟𝑓𝑓) is

available in this database for the same time-period (risk-free rate is based on the T-bill rate).

In order to calculate the beta of the industry, market return should be used. The CRSP

database provides returns on the market (𝑟𝑟𝑚𝑚) and therefore, the market premium (𝑟𝑟𝑚𝑚 - 𝑟𝑟𝑓𝑓) can

be calculated.

3.2. Two-pass regression model The DAPM consists of a two-pass regression model. In order to obtain the beta of the

industry, only the first pass of the model is needed. In the first pass, the return of each

industry is regressed on the market return to obtain the beta of the industry. It is expected that

the lower-market and upper-market return of any industry is proportional to its beta in the

lower-state (𝛽𝛽𝑖𝑖−) or its beta in the upper-state (𝛽𝛽𝑖𝑖+). If the DAPM holds, the intercept of the

security market line (SML) will be zero. In other words, the SML+ and SML- will pass

through the origin. Figure 2 gives a graphical explanation.

Figure 2. Graphical explanation DAPM

Source: Zou (2005)

15

The SML is important to determine which industries can be classified as low- or high-beta

industries. Theory assumes that the SML represents the relationship between the expected

return and risk of an asset (in this case, an industry). Consider a positive market (i.e. upturn)

where the industry is plotted above the SML+, this means that the industry is undervalued

because the investor will expect a greater return given the risk he/she is taking. Conversely, if

the industry is below the SML+, the industry will be overvalued because the investor accepts

less return given the risk of that particular industry. The same holds when the market is in a

negative spiral: industries above the SML- provide the same risk but against a lower return

and therefore, are overvalued. Conversely, if the industry is below the SML- the industry is

undervalued. Empirical studies show that the real SML (the real relationship between risk and

return) is less steep than the hypothesized SML (displayed in figure 2) due to the market

premium (in reality there is no riskless asset). The area between the real and hypothesized

SML is the “abnormal extra return [or loss] over the market”, denoted as alpha (Jensen,

1969). Therefore, the alpha represents the average return above the expected return predicted

by the hypothesized SML, ceteris paribus the portfolio’s beta and market return. In other

words, the alpha can be seen as residuals of all means excess return, which is also calculated

in the first pass. The second pass will see if condition 1 (MV-efficient) and condition 2 (GL-

efficient) are satisfied. However, as explained before, these conditions are assumed to be met

and therefore the second pass will not be used.

3.3. Ratio’s To assess the link between the industries and their risk, several variables can be used. In order

to identify the riskiness of the industry, the beta and alpha will be used. The beta is defined

according to the best-beta (measures the beta for all states, no distinction between lower- and

upper-state), 𝛽𝛽 = 𝐸𝐸(𝑥𝑥𝑚𝑚𝑥𝑥)𝐸𝐸(𝑥𝑥𝑚𝑚2 )

, where a beta > 1.2 indicates a more risky investment compared to

the market average and a beta < 0.8 indicates a less risky investment compared to the market

average (see assumption 2). The alpha will be defined as 𝛼𝛼 = 𝐸𝐸(𝑥𝑥𝑖𝑖) − 𝛽𝛽𝐸𝐸(𝑥𝑥𝑚𝑚), where alpha

< 0 implies that the asset earned too little given its risk and alpha > 0 implies excess return for

the assumed risk for the investor. The beta will be used to divide industries in low-beta or

high-beta industries, the alpha will be an additional indicator and give information about the

correctness of the division.

16

This thesis focusses specifically on the difference between low-beta and high-beta industries

because of the more extreme difference in their risk/return relationship. As explained before,

neutral-risk industries will have similar results since their risk/return relation is less extreme

and results will be less obvious. Therefore, the beta in the upper state and lower state will be

computed for the low-beta and high-beta industry following the DAPM;

𝛽𝛽𝑖𝑖− = 𝐸𝐸(𝑥𝑥𝑚𝑚𝑥𝑥𝑖𝑖)𝐸𝐸�𝑥𝑥𝑚𝑚2 �

, 𝛽𝛽𝑖𝑖+ = 𝐸𝐸(𝑥𝑥𝑚𝑚𝑥𝑥𝑖𝑖)𝐸𝐸�𝑥𝑥𝑚𝑚

2 �

Thereafter, ∆𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙 and ∆𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ are computed and its t-statistic which is defined as

𝑚𝑚 − 𝑠𝑠𝑚𝑚𝑎𝑎𝑚𝑚𝑖𝑖𝑠𝑠𝑚𝑚𝑖𝑖𝑠𝑠 = ∆𝛽𝛽𝑖𝑖 − 0𝑆𝑆𝑆𝑆(∆𝛽𝛽𝑖𝑖)

= 𝛽𝛽𝑖𝑖+ − 𝛽𝛽𝑖𝑖−

�𝑉𝑉𝑉𝑉𝑉𝑉(𝛽𝛽𝑖𝑖+ − 𝛽𝛽𝑖𝑖−)=

𝛽𝛽𝑖𝑖+ − 𝛽𝛽𝑖𝑖−

�𝑉𝑉𝑉𝑉𝑉𝑉(𝛽𝛽𝑖𝑖+|𝐺𝐺) + 𝑉𝑉𝑉𝑉𝑉𝑉(𝛽𝛽𝑖𝑖−|𝐿𝐿)

= 𝛽𝛽𝑖𝑖+ − 𝛽𝛽𝑖𝑖−

�𝜎𝜎𝑖𝑖

𝑇𝑇1𝐸𝐸(𝑥𝑥𝑚𝑚2 |𝐺𝐺)

+ 𝜎𝜎𝑖𝑖𝑇𝑇2𝐸𝐸(𝑥𝑥𝑚𝑚2 |𝐿𝐿)

4. Results This section will analyze the division of industries and analyze results across low- and high-

risk industries. First, the industry analysis will outline the riskiness of each industry (30

industries in total). In other words, a distinction between low-, neutral- and high-risk

industries is made. Next, the hypothesis across low- and high-risk industries is tested.

4.1. Low- and High-beta industry analysis This subsection will divide 30 industries (see Appendix II) according to their riskiness. As

mentioned before, a risky industry will have an estimated beta higher than 1.2. Conversely, a

low-risk industry will have a beta lower than 0.8. “Neutral” industries are not the topic of this

research but are given for completeness. Also the alpha is calculated to give a more complete

overview of the different industries and their dynamics. Using the DAPM, the following

results are found;

Low-risk Neutral High-risk

Industry Beta Alpha Industry Beta Alpha Industry Beta Alpha

Food 0,677 0,020 Games 1,187 0,013 Textiles 1,206 0,013

Beer 0,539 0,017 Books 1,105 -0,028 Construction 1,343 0,001

Smoke 0,585 0,055 Clothes 1,070 0,026 Steel 1,609 -0,001

17

The categorization of the industries is not surprising according to the literature (e.g. Wilson,

1998). Basic needs (“Households”, “Utilities”, “Health”, “Food”) are classified as low-risk

because they will always be important even if the economy experiences a slowdown.

Secondary industries, like “Beer” and “Smoke”, might be unexpected since these products

will be far from essential for humans. An additional explanation might be the addictive nature

of these products (people “have to” smoke and people “have to” drink), however, further

research should explore these industries more in depth. Also the classification of high-risk

industries are logical and predictable. Especially industries related to engineering/industrial

(e.g. steel, coals, mines, construction and fabricated products) and luxury expenditures (e.g.

cars) experience significant declines when the economy is in a recession. The classification of

these industries will be valid across several time periods and will remain valid in the future

because the nature of an industry “cannot easily, if at all, change” (Bettis and Mahajan, 1985,

p. 786).

4.2. Lower- and upper economic environment Table 2 gives an overview of the beta when the market is in an upper- or lower-state for all

low-risk and high-risk industries. As explained before, the beta of low-risk and high-risk

industries in an upper-state (β+) should equal the beta in a lower-state (β-) (and equal the best-

beta (β)). Industries showing strong differences between the upper- and lower-beta are marked

Households 0,656 0,012 Chemicals 1,170 0,018 Fabricated Products 1,292 0,016

Health 0,710 0,014 Carry 1,012 0,029 Electrical Equipment 1,208 0,012

Utilities 0,748 0,021 Oil 1,115 0,025 Autos 1,337 -0,008

Telecom 0,960 0,009 Mines 1,286 0,014

Services 0,965 0,011 Coals 1,726 0,017

Business

Equipment 1,072 0,009 Finance 1,364 -0,018

Paper 0,951 0,009

Transport 1,040 0,016

Wholesale 0,914 0,018

Retail 0,855 0,016

Meals 0,832 0,036

Other 0,916 0,000

Table 1. Low-, Neutral and High-risk industries

18

with red (βi+ − βi− ≥ |0.03|), these industries are expected to be inconsistent with the

hypothesis (i.e. Δβ ≉ 0) (table 3, next page). To see if these industries will be inconsistent

with the DAPM, a t-test is used (Appendix III gives a complete overview of low-, neutral and

high-risk industries).

Low-risk industries High-risk industries

Industry β β+ β- Industry β β+ β-

Food 0,68 0,67 0,68 Textiles 1,21 1,21 1,20

Beer 0,54 0,56 0,52 Construction 1,34 1,34 1,35

Smoke 0,59 0,58 0,59 Steel 1,61 1,57 1,65

Household 0,66 0,67 0,64 Fabricated Products 1,29 1,30 1,29

Health 0,71 0,71 0,71 Electronic Equipment 1,21 1,22 1,19

Utilities 0,75 0,75 0,75 Autos 1,34 1,33 1,34

Mines 1,29 1,26 1,31

Coal 1,73 1,68 1,77

Finance 1,36 1,37 1,36

Table 2. Industry-betas according to the DAPM

Low-beta industries High-beta industries

Industry β+ β- β+ - β- t-stat Industry β+ β- β+ - β- t-stat

Food 0,67 0,68 0,00 -0,15 Textiles 1,21 1,20 0,00 0,07

Beer 0,56 0,52 0,05 1,56 Construction 1,34 1,35 -0,01 -0,12

Smoke 0,58 0,59 -0,01 -0,29 Steel 1,57 1,65 -0,07 -1,03

Household 0,67 0,64 0,03 0,81 Fabricated Products 1,30 1,29 0,01 0,14

Health 0,71 0,71 0,00 0,13 Electronic Equipment 1,22 1,19 0,03 0,54

Utilities 0,75 0,75 0,00 0,15 Autos 1,33 1,34 -0,02 -0,26

Mines 1,26 1,31 -0,05 -0,79

Coal 1,68 1,77 -0,10 -1,00

Finance 1,37 1,36 0,00 0,08

Table 3. Results according to the DAPM

As expected, industries where ∆β deviates significantly from zero also have higher t-statistics

than industries who are more or less consistent with the DAPM. None of the t-statistics are

significant at a 5% significance level (t-stat = 1.96) and therefore cannot be rejected, however,

19

one sees a clear movement of higher t-statistics when the industry differs significantly from

the DAPM. Therefore, t-statistic should not be interpreted too strictly since the estimator does

not give a complete overview of the correctness of the model. It can be concluded that the

industries marked with green are more or less consistent with the DAPM. In other words,

∆𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙 = 𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙+ − 𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙− ≈ 0 or ∆𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ = 𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ+ − 𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ− ≈ 0 for these industries. The

industries marked with red are inconsistent with the DAPM. In other words, ∆𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙 = 𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙+ −

𝛽𝛽𝑙𝑙𝑙𝑙𝑙𝑙− ≉ 0 or ∆𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ = 𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ+ − 𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ− ≉ 0 for these industries.

Industries consistent with the DAPM imply that the “net riskiness” of a low-risk industry

compared to a high-risk industry should be equal and not be an issue for the investor when

shaping his portfolio. In other words, low-beta industries (like “Food”, “Smoke”, “Health”

and “Utilities”) should have equal risk/return levels as high-beta industries (like “Textiles”,

“Construction”, “Fabricated Products”, “Auto’s” and “Finance”). Therefore, the investor

could construct portfolios of solely low-beta industries or solely high-beta industries with the

same amount of risk. This implies that diversification and combinations of industries in the

investors’ portfolio (involving any risky industry or a combination of less risky industries)

represent the preferences and utility of the investor (based on Sharpe, 1964).

When the investor is indifferent between low- and high-beta stocks, one could make a

portfolio of solely low-beta industries that will outperform a portfolio of solely high-beta

stocks. To construct such a portfolio (solely low-beta industries with lower risk and higher

returns), investors should borrow money and invest in low-beta stocks to shift to a position

with similar risk but higher returns (Black, 1972). The beta indicates how exposed the

industry is to the economic environment where a higher beta will increase the average price of

the stocks in that industry because of an increase in willingness to bear risk (based on Miller,

1977). As a result, the payoff on assets in a high-risk industry will be lowered because of this

higher price. Assuming interest rates on equal terms for each investor, the payoff on high-beta

industry will be less compared to constructing a portfolio when money is borrowed in order to

invest in low-beta industries (Miller, 1977). However, the reason why investor will not invest

in low-beta industries is because you need to borrow money which in itself brings additional

risk. Yet, results show that completely rational investors will be indifferent between the two

options (holding interest rates constant).

20

Overall, the DAPM model is a consistent model for investors to asses different industries and

their riskiness in most cases. However, is there an explanation why the DAPM does not hold

for all industries? Are there some similarities across inconsistent industries that can explain

these deviations? Taking a closer look at the deviations, results show that the inconsistent

low-beta industries (“Beer” and “Household”) have higher betas when the market is in an

upturn and lower betas when the market is in a downturn (i.e. positive Δβ). This implies that

the average risk of the industry will be higher when the economy is doing well and lower

when the economy is performing badly. One could argue that industries with a positive Δβ,

are the industries that experience a slow down when there is a recession but will experience

superior growth as soon as the market will move towards the upper-state because of the

“neediness” of that particular industry. In other words, “Households” and “Beer” are the first

industries that become significant to consumers when the economy is recovering from a

slowdown and therefore, profitable for investors. This means that investing in “Beer” or

“Households” is a profitable opportunity because the risk (and thus return) will recover from

economic downturns. This thesis will not argue why this is the case but only explain the

behavior of industries with a positive Δβ.

Inconsistent high-beta industries have higher betas when the market is in a downturn and

lower betas when the market is in an upturn (i.e. negative Δβ). This implies that the investor

overvalues these industries, where the only exception is “Electrical Equipment” which is

classified as a high-beta industry but behaves like a low-beta industry. For these high-beta

industries (“Steel”, “Mines” and “Coal”), it means that the industry recovers less fast from an

economic downturn (e.g. the market is moving towards the upper-state) and it will be

confronted as first when there is an economic downturn. In other words, the industry will

experience less growth in economic ups compared to the decline in an economic downturn

because investors are hesitant to invest in these industries (i.e. leads to a negative Δβ). Why

are investors cautious when investing in these industries? Is there a logical explanation that

could explain the hesitance of investors to invest less in these industries when the economy is

recovering from a downturn (i.e. the economy is moving towards an upper-state)? This

interesting notion might be explained by using concepts from behavioral economics and the

transaction cost theory. The next paragraph will explain these arguments more in depth

(“Electrical Equipment” will not be explained since this industry behaves like a low-risk

industry).

21

4.3. High-beta industries recovering from an economic downturn As shown in table 2 and 3, high-beta industries who are inconsistent with the DAPM show

some similarities with respect to the differences in their riskiness when the market is in an

upturn or downturn. All inconsistent high-risk industries (except “Electrical Equipment”)

have a negative Δβ. Is this coincidence? Or is there a theoretical explanation that could

explain this regularity? Theories and concepts from behavioral finance and transaction cost

theory might give an explanation for this effect.

Behavioral finance focusses on the psychological and social dimension of finance (Shiller,

2003). One of the new insights gathered by behavioral finance is the notion of bounded

rationality. Asset pricing models assume rational investors, i.e. the investor makes optimal

choices that benefit the utility of the investor (Simon, 1997). However, in the real world

investors’ rational is limited, also called bounded rationality; decision-making has “systematic

biases that separate the beliefs that people have and the choices they make from the optimal

beliefs and choices that rational investors would make” (Kahneman, 2003, p. 1449). This

means that investors will not make optimal choices because their psyche limits them to do so.

An example of bounded rationality is loss-aversion. Loss-aversion means that investors are

more sensitive to losses than to gains (Benartzi, and Thailer, 1995) and could explain a

negative Δβ for inconsistent high-beta industries. This concept is used in the prospect theory

of Kahneman and Tversky (1979), where it is argued that the utility function of investors

comes from gains and losses in pay-off. In this case, the investor will not make optimal

choices because its utility depends on relative returns and the (investment) decision is not

evaluated on an absolute level, i.e. the final outcome is less relevant to the investor than the

value of gains and losses. Figure 3a and 3b illustrate the prospect theory where the value

displays the reference point between what is experienced as a loss or gain by the investor.

Note: investors can be more/less loss averse, therefore, the value function might differ

between investors; figure 3a displays an investor who is very loss-averse while the investor

displayed in figure 3b values his losses to a lesser extent.

22

Figure 3a and 3b. Examples of value functions from investors

Source: Kahneman and Tversky (1979)

Because loss-averse investors will value losses more intensive than gains, even when the loss-

or gain-differential is equal, investors will try to avoid losses as much as possible even if the

compensation to avoid losses is imbalanced with the actual loss. In other words, where

rational investors would take the loss to avoid additional risk, a loss-averse investor would

avoid the loss even if the additional risk involved is not rational. Taking a look at the results

of inconsistent high-beta industries, one sees that in the lower state the investor is willing to

take more risk (i.e. 𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ+ < 𝛽𝛽ℎ𝑖𝑖𝑖𝑖ℎ− ) even if the additional loss in return is not proportional to

the additional risk. Because investors put greater weight on the losses, they “demand

additional compensation” for these industries when the economy is in a downturn (based on

Ang, Chen, and Xing, 2006, pp. 1191). In other words, they will value these industries as

more risky and therefore the beta will increase during a downturn of the economy because the

downturn will cause additional loss for the industry and thus for the investor. Compared to

low-beta industries, investors will take their loss in an early stage because the deviations are

less and thus the impact on the value function is limited. Concluding, when the market is

going down, investors demand higher returns than the difference in return when the market is

going up because they put more weight to their losses than to equal gains. In other words, the

investor will demand a higher return in a downturn compared the return asked by the investors

when the market is in an upturn than rational investors, holding the additional

increase/decrease in risk equal.

Second, forecasting errors might be a reason for a negative Δβ. As Chandler (1990) describes,

there are some industries that have continously new innovations that require firms in that

23

industry to adapt and develop new resources/capabilities. A good example are energy

companies who need to compete and innovate for their share of “clean energy” (this includes

the “Coal” and “Mine” industry). This brings additional risk for investors because a bounded

rational investor cannot forcast the future and the precise pattern of the industry (or firm). A

frequent used indicator for innovation is the number of patents (Lanjouw and Schankerman,

2004). For industries where there is a high number of patents, it is assumed that these

industries will be most competitive on innovation and have increased uncertainty (ibid). In

other words, figure 4 (next page) shows how innovative the industries in the U.S are and

indeed it can be concluded that coal and mining will be industries where innovation is

important and the competition is severe. This means that the forecast of these industries tend

to be more difficult (Will your company still be profitable after the completion of the

innovation? Will your company also beat the competition when there is a new innovation

wave?), therefore, uncertainty is increased and investors will demand a higher compensation

which marks a higher average beta.

In general, high-innovative industries have an uncertain future because of their systematic

innovations. Because it is impossible for the investor to be completely rational, his respond to

this increased uncertainty will be based on heuristics and affect. Indeed, because of this

uncertainty, investors have to rely on their instincts and will tend to be more loss-averse, as

explained before, loss-averse investors will hold on to their losses even if the additional risk is

not proportional. This might be an explanation why industries with a highly innovative

character and uncertainty have higher betas in the lower state and lower betas in the upper

state.

24

Figure 4. Number of patents per industry in the U.S.

Source: OECD statistics, number of patents per industry

25

Concluding, whether the market will experience an upturn or downturn, the uncertainty about

the competitive industries will remain the same. However, the investor will experience the

lower-state of the economy as more uncertain and they become more attached to their losses

and therefore ask a higher return to compensate. Furthermore, in the lower-state of the

economy the pressure to innovate in highly competitive industries might truly increase

because of the limited performance and declining results (Roberts, 2003). This will increase

uncertainty in the lower-state, leading to a higher beta. The exact mechanism of the two

scenarios should be researched in the future. Note that human necessities (see figure 4) also

have an innovative character, however, because they are considered as a basic need for human

presence, innovation will not create uncertainty but rather create efficiency.

Another example of bounded rationality is an overconfident investor, defined as an investor

“who overestimates the precision of his private information and underestimates the value of

public information” (Daniel, Hirshleifer, and Subrahmanyam, 1998, p. 1841). Evidence

supports overreaction of investors that lead to a negative correlation between stock returns

and volatility (Daniel, et. al, 1998). In other words, the investor bears more risk (excess

volatility) given the return than a rational investors would do. In case of the high-beta

industries, investors overreact on their private information in the lower-state of the economy,

probably because they want to avoid their loss (loss-averse). This implies that investor is

taking excess risks in the lower state, at least in excess of what a rational investor would

obtain. In the upper state, investors underreact to public information (i.e. macro-economic

signals) about the industry (Daniel, et. al, 1998). This means that the investor does not adjust

their risk level according to the change in return on the industry compared to rational

investors (risk-averse) given the public information about the industry.

More specific, investors will be overconfident in the lower-state since they think they have

more credible signals because of private information and thus overreact their accuracy of the

prediction of the market based on this information (Daniel, et. al, 1998). This means that the

investors will take excess risk but do not experience this additional risk as imbalanced

compared to the change in return (as rational investors would do). In case of the upper state,

the macro-economic signals (i.e. public information) is undervalued and investors will

underreact since they do not take these signals as credible enough (Daniel, et. al, 1998). They

will see the industry as “safe” while a rational investor would give more credibility to publicly

available information which changes the risk level. This implies that investors will overvalue

26

private information in the lower-state to justify their loss-averse behavior and undervalue

public information in the upper-state in order to avoid additional risk (risk-averse behavior).

This leads to a lower beta in the upper-state and a higher beta in the lower-state, i.e. a negative

Δβ. This might be specifically the case for high-beta industries since the investor has more to

lose and more to gain. Because the deviation between “winning” and “losing” is increased,

the relation to over-/under-reaction of private/public information tends to be stronger.

Especially for the “Steel” and “Coal” industry, the average gain and loss will be higher since

the overall beta is higher compared to the average of the high-beta industries.

Besides behavioral aspects, transaction costs and frequency traders also confirm the results.

The lower- and higher-state betas of high-risk industries are consistent with the idea that high

frequency traders indeed have impact on the market since they can trade repeated times a day

at very low costs. Classical theory reviews the bid-ask spread as a compensation for the

market maker (Madhaven, 2000). This compensation is needed because the market maker has

order-handling costs, the cost of adverse selection and price risk (ibid). Logically, a market

maker would prefer to have markets where these costs are as low as possible. Research shows

that high frequency trades are likely to change the average transaction cost (Kirilenkoz and

Cvitanik, 2010). Several costs decrease, e.g. search costs, order-processing costs and fees,

because of these high frequency traders. This implies that the bid-ask spread will decrease and

therefore, transaction costs improve and trades can be continuously and instantly done

(Menkveld, 2011). In other words, high frequency traders will instantly sell stocks in

industries that underperform because they are not stopped because of high transaction costs

(i.e. transactions are insignificant to the loss that is made by the stock).

This means that a high frequency trader “enables a market-making strategy to quickly update

quotes on the arrival of public information and thus reduce the risk of being adversely

selected” (Menkveld, 2011, p. 5). Furthermore, the response time will decrease (i.e. low

latency) which enables the high frequency trader to have a market-making role for investors

(ibid). Therefore, high frequency traders will be the new market-maker who instantly can sell

and buy stocks as a rational investor would do in offset of the transaction costs. Previously

research shows that systematic risk (β) in an increasing function of the expected return of an

stock where return is an increasing function of the bid-ask spread (i.e. asset illiquidity)

(Amihud and Mendelson, 1986). If high frequency traders value in industry as more risky,

they will not invest in these industries or sell the stock in these industries which will decrease

27

the liquidity of that industry which will increase the risk of that industry. Logically, in the

lower-state of the economy, high frequency-traders will sell or not invest, and the industry

will experience more risk and will demand additional return because of decreased liquidity.

This particular industry will become even more illiquid and thus risk is even more increased

(i.e. the loss-spiral). Indeed, the beta in the lower state will increase significantly compared to

the beta in the upper state for industries that are sensitive to the economic environment

because of instant trades done by the higher frequency trader.

This thesis tried to gather first insights in possible explanations for the behavior of investors

when considering patterns of risk and return. The focus is on irregular high-risk industries and

further research should clarify the exact mechanism behind this notion.

28

5. Conclusion

The central question in this thesis explores if low- and high-risk industries are empirically

consistent with the DAPM. An important distinction is the division between low- and high-

risk industries where low-risk industries are labelled as industries where demand will by

stable overtime, even in a downturn economy or scarcity (e.g. health care) (Wilson, 1999).

High-risk industries are labelled as pro-cyclical and sensitive to the conditions of the market

(e.g. luxurious companies) (ibid). The beta is used as an indicator of the industry’s riskiness

and is derived by using the DAPM. This DAPM (Zou, 2005) advances the CAPM because it

makes a distinction between the upper- and lower-state of the market. Therefore, the beta of

the firm (industry) can be divided into a beta when the market is in an economic downturn

and a beta when the market is in an economic upturn. Overall, the thesis uses the DAPM to

derive the upper-beta and lower-beta for low-risk and high-risk industries.

From this thesis we learn that rational investors should be indifferent between investing in

low-beta or high-beta industries. Investors could achieve the same returns from a portfolio of

solely low-beta stocks as they expect to generate when investing in high-beta industries, this

is achieved by borrowing money. However, because investors are not rational and the

borrowing rate is not constant overtime, they do not like to invest in low-beta industries

because borrowing money in itself adds additional risk. Results also show that low-beta

industries are more or less consistent with the DAPM (Δβ ≈ 0 or Δβ > 0). High-beta industries

show some deviations (i.e. negative Δβ for most inconsistent industries) but the results are not

statistically significant to reject.

The second part of this thesis tries to explain why inconsistent high-beta industries have

higher betas in the lower-state and lower betas in the upper-state (i.e. negative Δβ). Reasons

for a negative Δβ across high-beta industries can be found in behavioral finance and the

transaction cost theory. Arguments from concepts like loss-aversion, bounded rationality,

future prospects, and overconfident investors are explaining the results from a behavioral

point of view. The results also confirm a decrease in transaction costs and the presence of

high frequency traders, where high frequency traders function as market-makers. This thesis

is just a start to explain this irregularity, further research should explore these arguments more

in depth.

29

These findings have some important implications; first, it shows that the DAPM (as also holds

for the CAPM) does not incorporate irrational behavior of investors and therefore, does not

fully predict the movements of the market. However, the DAPM is a consistent model which

is a useful tool for investors to get some sense of investment decisions and portfolios.

Furthermore, this research highlights the importance of diversification. Holding several stocks

across industries reduces market risk for investors, this way, investors can reduce risk by

adding more stocks from low-beta industries but can increase risk (and thus expected return)

by adding stocks from high-beta industries. This thesis gives a clear indication about creating

diversified investment by investing in different industries according to the preference of the

investor.

Overall, the DAPM is useful for investor when assessing their portfolio and changing the

risk/return relationship of that portfolio. Assuming that investors are rational, the model can

give a clear prediction of the market. However, results confirm that the assumption about full

rational behavior is not representing reality. Behavioral finance gives some clear arguments

why the prediction according to the DAPM does not corresponds with the actual risk/return

relationship. Lastly, further development of the DAPM should incorporate transaction costs to

give a more accurate and rational picture of the market.

30

Appendix I Industry Sub Name

1 2833 MEDICINAL CHEMICALS & BOTANICAL PRODUCTS

1 2834 PHARMACEUTICAL PREPARATIONS

1 2835 IN VITRO & IN VIVO DIAGNOSTIC SUBSTANCES

1 2836 BIOLOGICAL PRODUCTS, (NO DISGNOSTIC SUBSTANCES)

1 5912 RETAIL-DRUG STORES AND PROPRIETARY STORES

1 6311 LIFE INSURANCE

1 6321 ACCIDENT & HEALTH INSURANCE

1 6324 HOSPITAL & MEDICAL SERVICE PLANS

1 6331 FIRE, MARINE & CASUALTY INSURANCE

1 6351 SURETY INSURANCE

1 6361 TITLE INSURANCE

1 6399 INSURANCE CARRIERS, NEC

1 6411 INSURANCE AGENTS, BROKERS & SERVICE

1 8011 SERVICES-OFFICES & CLINICS OF DOCTORS OF MEDICINE

1 8060 SERVICES-HOSPITALS

1 8062 SERVICES-GENERAL MEDICAL & SURGICAL HOSPITALS, NEC

1 8093 SERVICES-SPECIALTY OUTPATIENT FACILITIES, NEC

1 8731 SERVICES-COMMERCIAL PHYSICAL & BIOLOGICAL RESEARCH

2 2200 TEXTILE MILL PRODUCTS

2 2211 BROADWOVEN FABRIC MILLS, COTTON

2 2221 BROADWOVEN FABRIC MILLS, MAN MADE FIBER & SILK

2 2250 KNITTING MILLS

2 2273 CARPETS & RUGS

2 3873 WATCHES, CLOCKS, CLOCKWORK OPERATED DEVICES/PARTS

2 3910 JEWELRY, SILVERWARE & PLATED WARE

2 3911 JEWELRY, PRECIOUS METAL

2 4900 ELECTRIC, GAS & SANITARY SERVICES

2 4911 ELECTRIC SERVICES

2 4922 NATURAL GAS TRANSMISSION

2 4923 NATURAL GAS TRANSMISISON & DISTRIBUTION

2 4924 NATURAL GAS DISTRIBUTION

2 4931 ELECTRIC & OTHER SERVICES COMBINED

2 4932 GAS & OTHER SERVICES COMBINED

2 4941 WATER SUPPLY

2 4961 STEAM & AIR-CONDITIONING SUPPLY

2 4991 COGENERATION SERVICES & SMALL POWER PRODUCERS

2 5000 WHOLESALE-DURABLE GOODS

2 5020 WHOLESALE-FURNITURE & HOME FURNISHINGS

31

2 5040 WHOLESALE-PROFESSIONAL & COMMERCIAL EQUIPMENT & SUPPLIES

2 5090 WHOLESALE-MISC DURABLE GOODS

2 5094 WHOLESALE-JEWELRY, WATCHES, PRECIOUS STONES & METALS

2 5099 WHOLESALE-DURABLE GOODS, NEC

2 5140 WHOLESALE-GROCERIES & RELATED PRODUCTS

2 5141 WHOLESALE-GROCERIES, GENERAL LINE

2 5190 WHOLESALE-MISCELLANEOUS NONDURABLE GOODS

2 5271 RETAIL-MOBILE HOME DEALERS

2 5311 RETAIL-DEPARTMENT STORES

2 5331 RETAIL-VARIETY STORES

2 5399 RETAIL-MISC GENERAL MERCHANDISE STORES

2 5400 RETAIL-FOOD STORES

2 5411 RETAIL-GROCERY STORES

2 5412 RETAIL-CONVENIENCE STORES

2 5500 RETAIL-AUTO DEALERS & GASOLINE STATIONS

2 5531 RETAIL-AUTO & HOME SUPPLY STORES

2 5700 RETAIL-HOME FURNITURE, FURNISHINGS & EQUIPMENT STORES

2 5712 RETAIL-FURNITURE STORES

2 5731 RETAIL-RADIO, TV & CONSUMER ELECTRONICS STORES

2 5734 RETAIL-COMPUTER & COMPUTER SOFTWARE STORES

2 5735 RETAIL-RECORD & PRERECORDED TAPE STORES

2 5900 RETAIL-MISCELLANEOUS RETAIL

2 5940 RETAIL-MISCELLANEOUS SHOPPING GOODS STORES

2 5944 RETAIL-JEWELRY STORES

2 5945 RETAIL-HOBBY, TOY & GAME SHOPS

2 5960 RETAIL-NONSTORE RETAILERS

2 5961 RETAIL-CATALOG & MAIL-ORDER HOUSES

2 5990 RETAIL-RETAIL STORES, NEC

2 & 3 7389 SERVICES-BUSINESS SERVICES, NEC

3 3570 COMPUTER & OFFICE EQUIPMENT

3 3571 ELECTRONIC COMPUTERS

3 3572 COMPUTER STORAGE DEVICES

3 3575 COMPUTER TERMINALS

3 3576 COMPUTER COMMUNICATIONS EQUIPMENT

3 3577 COMPUTER PERIPHERAL EQUIPMENT, NEC

3 3578 CALCULATING & ACCOUNTING MACHINES (NO ELECTRONIC COMPUTERS)

3 3579 OFFICE MACHINES, NEC

3 3672 PRINTED CIRCUIT BOARDS

3 5045 WHOLESALE-COMPUTERS & PERIPHERAL EQUIPMENT & SOFTWARE

3 6794 PATENT OWNERS & LESSORS

3 7370 SERVICES-COMPUTER PROGRAMMING, DATA PROCESSING, ETC.

3 7371 SERVICES-COMPUTER PROGRAMMING SERVICES

3 7372 SERVICES-PREPACKAGED SOFTWARE

3 7373 SERVICES-COMPUTER INTEGRATED SYSTEMS DESIGN

32

3 7374 SERVICES-COMPUTER PROCESSING & DATA PREPARATION

3 7377 SERVICES-COMPUTER RENTAL & LEASING

4 1311 CRUDE PETROLEUM & NATURAL GAS

4 1381 DRILLING OIL & GAS WELLS

4 1382 OIL & GAS FIELD EXPLORATION SERVICES

4 1389 OIL & GAS FIELD SERVICES, NEC

4 2000 FOOD AND KINDRED PRODUCTS

4 2020 DAIRY PRODUCTS

4 2024 ICE CREAM & FROZEN DESSERTS

4 2030 CANNED, FROZEN & PRESERVD FRUIT, VEG & FOOD SPECIALTIES

4 2033 CANNED, FRUITS, VEG, PRESERVES, JAMS & JELLIES

4 2040 GRAIN MILL PRODUCTS

4 2050 BAKERY PRODUCTS

4 2052 COOKIES & CRACKERS

4 2060 SUGAR & CONFECTIONERY PRODUCTS

4 2070 FATS & OILS

4 2090 MISCELLANEOUS FOOD PREPARATIONS & KINDRED PRODUCTS

4 2092 PREPARED FRESH OR FROZEN FISH & SEAFOODS

4 2600 PAPERS & ALLIED PRODUCTS

4 2611 PULP MILLS

4 2621 PAPER MILLS

4 2631 PAPERBOARD MILLS

4 2650 PAPERBOARD CONTAINERS & BOXES

4 2670 CONVERTED PAPER & PAPERBOARD PRODS (NO CONTANERS/BOXES)

4 2911 PETROLEUM REFINING

4 3533 OIL & GAS FIELD MACHINERY & EQUIPMENT

4 4610 PIPE LINES (NO NATURAL GAS)

4 5110 WHOLESALE-PAPER & PAPER PRODUCTS

4 5171 WHOLESALE-PETROLEUM BULK STATIONS & TERMINALS

4 5172 WHOLESALE-PETROLEUM & PETROLEUM PRODUCTS (NO BULK STATIONS)

4 6792 OIL ROYALTY TRADERS

5 100 AGRICULTURAL PRODUCTION-CROPS

5 200 AGRICULTURAL PROD-LIVESTOCK & ANIMAL SPECIALTIES

5 700 AGRICULTURAL SERVICES

5 800 FORESTRY

5 900 FISHING, HUNTING AND TRAPPING

5 2011 MEAT PACKING PLANTS

5 2013 SAUSAGES & OTHER PREPARED MEAT PRODUCTS

5 2015 POULTRY SLAUGHTERING AND PROCESSING

5 2100 TOBACCO PRODUCTS

5 2111 CIGARETTES

5 2711 NEWSPAPERS: PUBLISHING OR PUBLISHING & PRINTING

5 2721 PERIODICALS: PUBLISHING OR PUBLISHING & PRINTING

5 2731 BOOKS: PUBLISHING OR PUBLISHING & PRINTING

33

5 2732 BOOK PRINTING

5 2741 MISCELLANEOUS PUBLISHING

5 2750 COMMERCIAL PRINTING

5 2761 MANIFOLD BUSINESS FORMS

5 2771 GREETING CARDS

5 2780 BLANKBOOKS, LOOSELEAF BINDERS & BOOKBINDG & RELATD WORK

5 2790 SERVICE INDUSTRIES FOR THE PRINTING TRADE

5 2870 AGRICULTURAL CHEMICALS

5 3711 MOTOR VEHICLES & PASSENGER CAR BODIES

5 3713 TRUCK & BUS BODIES

5 3714 MOTOR VEHICLE PARTS & ACCESSORIES

5 3715 TRUCK TRAILERS

5 3716 MOTOR HOMES

5 3720 AIRCRAFT & PARTS

5 3721 AIRCRAFT

5 3724 AIRCRAFT ENGINES & ENGINE PARTS

5 3728 AIRCRAFT PARTS & AUXILIARY EQUIPMENT, NEC

5 3730 SHIP & BOAT BUILDING & REPAIRING

5 3743 RAILROAD EQUIPMENT

5 3751 MOTORCYCLES, BICYCLES & PARTS

5 3760 GUIDED MISSILES & SPACE VEHICLES & PARTS

5 3790 MISCELLANEOUS TRANSPORTATION EQUIPMENT

5 3812 SEARCH, DETECTION, NAVAGATION, GUIDANCE, AERONAUTICAL SYS

5 3931 MUSICAL INSTRUMENTS

5 3942 DOLLS & STUFFED TOYS

5 3944 GAMES, TOYS & CHILDREN'S VEHICLES (NO DOLLS & BICYCLES)

5 3949 SPORTING & ATHLETIC GOODS, NEC

5 4011 RAILROADS, LINE-HAUL OPERATING

5 4013 RAILROAD SWITCHING & TERMINAL ESTABLISHMENTS

5 4100 LOCAL & SUBURBAN TRANSIT & INTERURBAN HWY PASSENGER TRANS

5 4210 TRUCKING & COURIER SERVICES (NO AIR)

5 4213 TRUCKING (NO LOCAL)

5 4220 PUBLIC WAREHOUSING & STORAGE

5 4231 TERMINAL MAINTENANCE FACILITIES FOR MOTOR FREIGHT TRANSPORT

5 4400 WATER TRANSPORTATION

5 4412 DEEP SEA FOREIGN TRANSPORTATION OF FREIGHT

5 4512 AIR TRANSPORTATION, SCHEDULED

5 4513 AIR COURIER SERVICES

5 4522 AIR TRANSPORTATION, NONSCHEDULED

5 4581 AIRPORTS, FLYING FIELDS & AIRPORT TERMINAL SERVICES

5 4700 TRANSPORTATION SERVICES

5 4731 ARRANGEMENT OF TRANSPORTATION OF FREIGHT & CARGO

5 5010 WHOLESALE-MOTOR VEHICLES & MOTOR VEHICLE PARTS & SUPPLIES

5 5013 WHOLESALE-MOTOR VEHICLE SUPPLIES & NEW PARTS

34

5 5050 WHOLESALE-METALS & MINERALS (NO PETROLEUM)

5 5051 WHOLESALE-METALS SERVICE CENTERS & OFFICES

5 5150 WHOLESALE-FARM PRODUCT RAW MATERIALS

5 5810 RETAIL-EATING & DRINKING PLACES

5 5812 RETAIL-EATING PLACES

5 7500 SERVICES-AUTOMOTIVE REPAIR, SERVICES & PARKING

5 7510 SERVICES-AUTO RENTAL & LEASING (NO DRIVERS)

5 7812 SERVICES-MOTION PICTURE & VIDEO TAPE PRODUCTION

5 7819 SERVICES-ALLIED TO MOTION PICTURE PRODUCTION

5 7822 SERVICES-MOTION PICTURE & VIDEO TAPE DISTRIBUTION

5 7829 SERVICES-ALLIED TO MOTION PICTURE DISTRIBUTION

5 7830 SERVICES-MOTION PICTURE THEATERS

5 7841 SERVICES-VIDEO TAPE RENTAL

5 7900 SERVICES-AMUSEMENT & RECREATION SERVICES

5 7948 SERVICES-RACING, INCLUDING TRACK OPERATION

5 7990 SERVICES-MISCELLANEOUS AMUSEMENT & RECREATION

5 7997 SERVICES-MEMBERSHIP SPORTS & RECREATION CLUBS

5 8600 SERVICES-MEMBERSHIP ORGANIZATIONS

6 1520 GENERAL BLDG CONTRACTORS - RESIDENTIAL BLDGS

6 1531 OPERATIVE BUILDERS

6 1540 GENERAL BLDG CONTRACTORS - NONRESIDENTIAL BLDGS

6 1600 HEAVY CONSTRUCTION OTHER THAN BLDG CONST - CONTRACTORS

6 1623 WATER, SEWER, PIPELINE, COMM & POWER LINE CONSTRUCTION

6 1700 CONSTRUCTION - SPECIAL TRADE CONTRACTORS

6 1731 ELECTRICAL WORK

6 2400 LUMBER & WOOD PRODUCTS (NO FURNITURE)

6 2421 SAWMILLS & PLANTING MILLS, GENERAL

6 2430 MILLWOOD, VENEER, PLYWOOD, & STRUCTURAL WOOD MEMBERS

6 2451 MOBILE HOMES

6 2452 PREFABRICATED WOOD BLDGS & COMPONENTS

6 2510 HOUSEHOLD FURNITURE

6 2511 WOOD HOUSEHOLD FURNITURE, (NO UPHOLSTERED)

6 2520 OFFICE FURNITURE

6 2522 OFFICE FURNITURE (NO WOOD)

6 2531 PUBLIC BLDG & RELATED FURNITURE

6 2540 PARTITIONS, SHELVG, LOCKERS, & OFFICE & STORE FIXTURES

6 2590 MISCELLANEOUS FURNITURE & FIXTURES

6 2673 PLASTICS, FOIL & COATED PAPER BAGS

6 2800 CHEMICALS & ALLIED PRODUCTS

6 2810 INDUSTRIAL INORGANIC CHEMICALS

6 2820 PLASTIC MATERIAL, SYNTH RESIN/RUBBER, CELLULOS (NO GLASS)

6 2821 PLASTIC MATERIALS, SYNTH RESINS & NONVULCAN ELASTOMERS

6 2840 SOAP, DETERGENTS, CLEANG PREPARATIONS, PERFUMES, COSMETICS

6 2842 SPECIALTY CLEANING, POLISHING AND SANITATION PREPARATIONS

35

6 2844 PERFUMES, COSMETICS & OTHER TOILET PREPARATIONS

6 2851 PAINTS, VARNISHES, LACQUERS, ENAMELS & ALLIED PRODS

6 2860 INDUSTRIAL ORGANIC CHEMICALS

6 2890 MISCELLANEOUS CHEMICAL PRODUCTS

6 2891 ADHESIVES & SEALANTS

6 2950 ASPHALT PAVING & ROOFING MATERIALS

6 2990 MISCELLANEOUS PRODUCTS OF PETROLEUM & COAL

6 3011 TIRES & INNER TUBES

6 3021 RUBBER & PLASTICS FOOTWEAR

6 3050 GASKETS, PACKG & SEALG DEVICES & RUBBER & PLASTICS HOSE

6 3060 FABRICATED RUBBER PRODUCTS, NEC

6 3080 MISCELLANEOUS PLASTICS PRODUCTS

6 3081 UNSUPPORTED PLASTICS FILM & SHEET

6 3086 PLASTICS FOAM PRODUCTS

6 3089 PLASTICS PRODUCTS, NEC

6 3211 FLAT GLASS

6 3220 GLASS & GLASSWARE, PRESSED OR BLOWN

6 3221 GLASS CONTAINERS

6 3231 GLASS PRODUCTS, MADE OF PURCHASED GLASS

6 3241 CEMENT, HYDRAULIC

6 3250 STRUCTURAL CLAY PRODUCTS

6 3260 POTTERY & RELATED PRODUCTS

6 3270 CONCRETE, GYPSUM & PLASTER PRODUCTS