Embed Size (px)

Citation preview

© Software Publications Pty Ltd, 2013

Computerised Accounting using MYOB AccountRight Plus v19.8

covering BSBFIA301A Maintain financial records BSBFIA303A Process accounts payable and receivable BSBFIA304A Maintain a general ledger

© Software Publications Pty Ltd, June 2015 No part of this material may be reproduced or copied in any form or by any means (graphic, electronic or mechanical, including photocopying or by information retrieval systems) without permission in writing from Software Publications

Written by: Marian Brown Dip T [Commerce], MICB BAS Agent Cert IV Training and Assessment, Cert IV in Financial Services [Bookkeeping] MYOB Certified Consultant since 1995 MYOB Accredited Author, MYOB Accredited Trainer ICB Education Specialist

Revised by: Lyn Joyce Dip T (Commerce), B Ed Cert IV Training and Assessment Secondary and tertiary teacher for 40 years Publishers: Software Publications Pty Ltd [ABN 75078026150] Head Office – Sydney Unit 10, 171 Gibbes Street Chatswood NSW 2067 www.softwarepublications.com.au ISBN 978-1-922012-82-1

SUITABLE FOR

BSBFIA301 BSBFIA303 BSBFIA304

© Software Publications Pty Ltd, 2013

Copyright/Trademark Information: MYOB®, AccountantConnect®, AccountantsEnterprise®, AccountantsOffice®, AccountEdge®, AccountRight®, AccountRight Basics™, AccountRight Standard™, AccountRight Plus™, AccountRight Premier™, AccountRight Enterprise™, Accounting™, Accounting Plus™, Atlas by MYOB™, MYOB BusinessBasics™, BankConnect®, MYOB CashBasics™, ClientConnect®, ClientConnect Plus®, Exo™, FirstEdge®, LiveAccounts®, Love Your Work™, Mind Your Own Business®, MYOB - Making Business Life Easier®, MYOB Atlas®, MYOB ClientConnect®, MYOB Enterprise®, MYOB Exo®, MYOB M-Powered®, MYOB M-Power®, M-Powered Services™, M-Powered Bank Statements™, M-Powered Invoices™, M-Powered MoneyController™, M-Powered Payments™, M-Powered Superannuation™, ODBC DeveloperPack™, ODBC Direct™, PowerPay®, Premier®, Premier Enterprise®, RetailBasics®, RetailHospitality®, RetailManager®, RetailManager Enterprise®, RetailManager Professional®, RetailManager Standard®, RetailReady®, Smarter Connections™ are registered trademarks or trademarks of MYOB Technology Pty Ltd and their use is prohibited without prior consent. Ceedata, Solution 6 MAS and Xlon are registered trademarks or trademarks of Solution 6 Holdings Limited, a member of the MYOB group.

Adobe®, Acrobat®, Acrobat Reader®, Adobe Reader®, PDF™, and PostScript® are trademarks or registered trademarks of Adobe Systems Incorporated. AddressBook, Apple®, iMac, AirPort, iCal, Macintosh®, and QuickTime® and the QuickTime logo are registered trademarks of Apple Inc. MobileMeSM is a service mark of Apple Inc. Mac and the Mac logo are trademarks of Apple Inc., used under licence. Brio Intelligence and Hyperion Intelligence are trademarks or registered trademarks of Hyperion Solutions Corporation, Ctree use by permission from Faircom, Dapper used under licence with Apache Software, NiXPS used under licence, WinForms control set used by permission from DevExpress. Crystal Reports® is a registered trademark of Crystal Decisions, Inc. in the United States or other countries. FlexNet Connect® is a registered trademark of Flexera Software™ Inc. Google Maps™ card links included with permission. MasterCard® is a registered trademark of MasterCard International Inc, xerces is licenced under Apache Software. Microsoft, Access, Azure, DotNetZip, Excel, Fluent.Net, Internet Explorer, .Net Framework,Office, N-Log used under open source licence, Outlook, Smart Tags, Ribbon Control Library, SQL Azure, SQL CE, Windows, Word and WFPToolkit, are registered trademarks or trademarks of Microsoft Corporation in the United States or other countries.

Quicken® and QuickBooks® are registered trademarks of Intuit Inc. SM2DGraphView Copyright Snowmint Creative Solutions LLC snowmintcs.com. VISA® is a registered trademark of Visa International Service Association. RightNow CX® is a registered trademark of RightNow Technologies Inc. Sentry Spelling Checker Engine for Windows, copyright Wintertree Software Inc.

Other products mentioned may be service marks, trademarks or registered trademarks of their respective owners.

Limitations of Liability:

This material is designed to provide basic information on how to use MYOB AccountRight/AccountRight Plus v19.8. Because business circumstances can vary greatly, the material is not designed to provide specific GST or business advice for particular circumstances. Also, because aspects of the GST are complex and detailed, the material is not designed to comprehensively cover all aspects of the GST. Further, the laws implementing GST and rulings and decisions under those laws may change.

Before you rely on this material for any important matter for your business, you should make your own enquiries about whether the material is relevant and still current, and whether it deals accurately and completely with that particular matter; and as appropriate, seek your own professional advice relevant to that particular matter.

This information is for the general information of MYOB clients and is not to be taken as a substitute for specific advice. Consequently Software Publications Pty Ltd and Marian Brown will accept no responsibility to any person who acts on information herein without consultation with Software Publications Pty Ltd.

The information in this book is relevant to MYOB AccountRight Plus v19.8. Earlier or later versions of MYOB AccountRight software could change the instructions in this workbook.

References to websites may also change owing to the changing nature of this type of information.

ii About this Workbook © Software Publications Pty Ltd, 2013

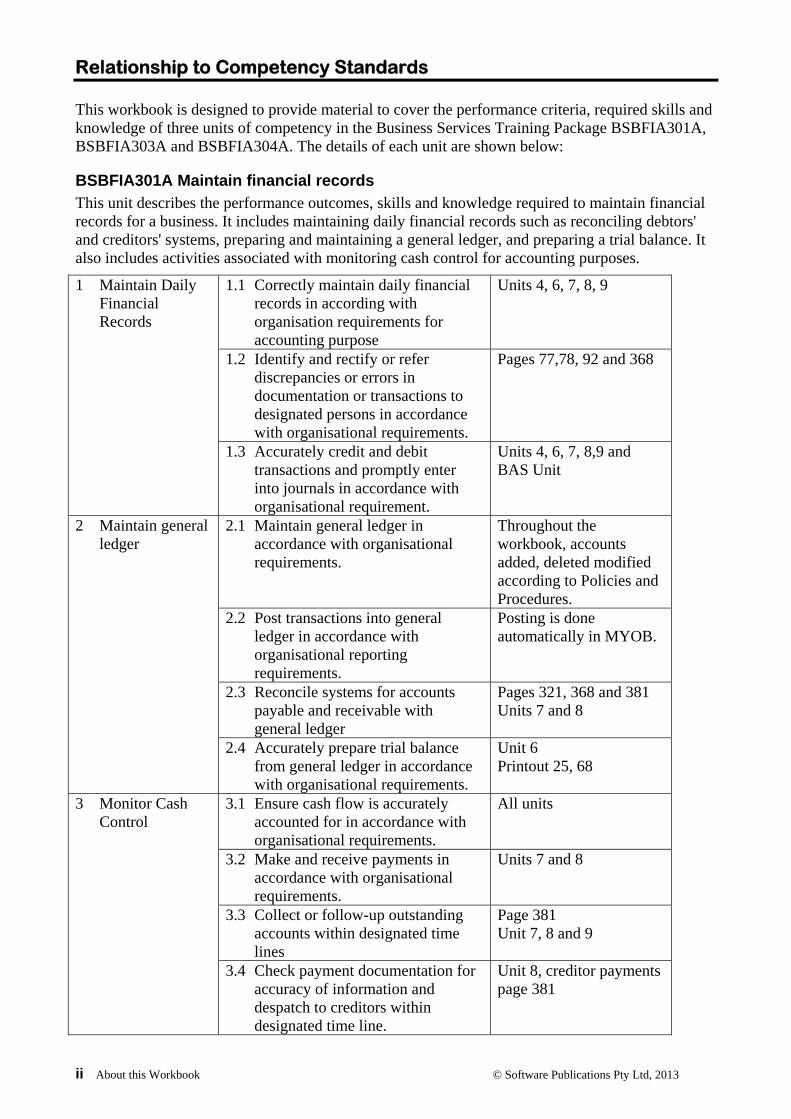

Relationship to Competency Standards

This workbook is designed to provide material to cover the performance criteria, required skills and knowledge of three units of competency in the Business Services Training Package BSBFIA301A, BSBFIA303A and BSBFIA304A. The details of each unit are shown below:

BSBFIA301A Maintain financial records This unit describes the performance outcomes, skills and knowledge required to maintain financial records for a business. It includes maintaining daily financial records such as reconciling debtors' and creditors' systems, preparing and maintaining a general ledger, and preparing a trial balance. It also includes activities associated with monitoring cash control for accounting purposes.

1 Maintain Daily Financial Records

1.1 Correctly maintain daily financial records in according with organisation requirements for accounting purpose

Units 4, 6, 7, 8, 9

1.2 Identify and rectify or refer discrepancies or errors in documentation or transactions to designated persons in accordance with organisational requirements.

Pages 77,78, 92 and 368

1.3 Accurately credit and debit transactions and promptly enter into journals in accordance with organisational requirement.

Units 4, 6, 7, 8,9 and BAS Unit

2 Maintain general ledger

2.1 Maintain general ledger in accordance with organisational requirements.

Throughout the workbook, accounts added, deleted modified according to Policies and Procedures.

2.2 Post transactions into general ledger in accordance with organisational reporting requirements.

Posting is done automatically in MYOB.

2.3 Reconcile systems for accounts payable and receivable with general ledger

Pages 321, 368 and 381 Units 7 and 8

2.4 Accurately prepare trial balance from general ledger in accordance with organisational requirements.

Unit 6 Printout 25, 68

3 Monitor Cash Control

3.1 Ensure cash flow is accurately accounted for in accordance with organisational requirements.

All units

3.2 Make and receive payments in accordance with organisational requirements.

Units 7 and 8

3.3 Collect or follow-up outstanding accounts within designated time lines

Page 381 Unit 7, 8 and 9

3.4 Check payment documentation for accuracy of information and despatch to creditors within designated time line.

Unit 8, creditor payments page 381

© Software Publications Pty Ltd, 2013 About this Workbook iii

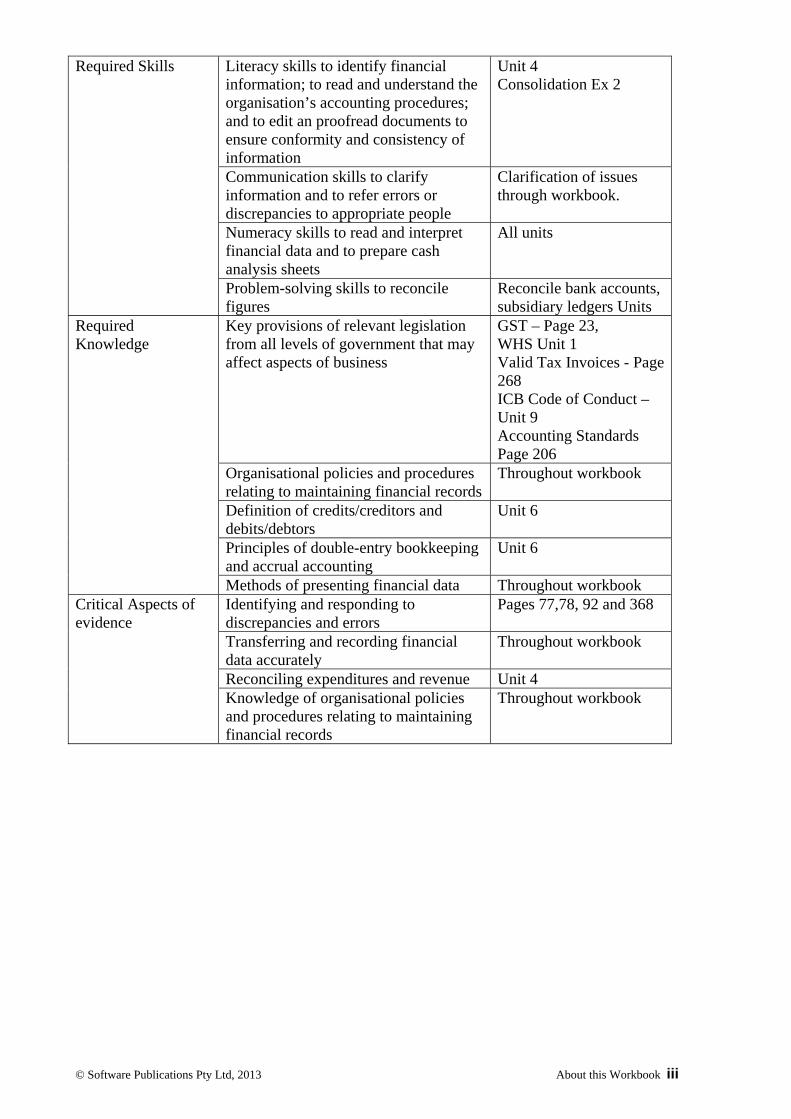

Required Skills Literacy skills to identify financial information; to read and understand the organisation’s accounting procedures; and to edit an proofread documents to ensure conformity and consistency of information

Unit 4 Consolidation Ex 2

Communication skills to clarify information and to refer errors or discrepancies to appropriate people

Clarification of issues through workbook.

Numeracy skills to read and interpret financial data and to prepare cash analysis sheets

All units

Problem-solving skills to reconcile figures

Reconcile bank accounts, subsidiary ledgers Units

Required Knowledge

Key provisions of relevant legislation from all levels of government that may affect aspects of business

GST – Page 23, WHS Unit 1 Valid Tax Invoices - Page 268 ICB Code of Conduct – Unit 9 Accounting Standards Page 206

Organisational policies and procedures relating to maintaining financial records

Throughout workbook

Definition of credits/creditors and debits/debtors

Unit 6

Principles of double-entry bookkeeping and accrual accounting

Unit 6

Methods of presenting financial data Throughout workbook Critical Aspects of evidence

Identifying and responding to discrepancies and errors

Pages 77,78, 92 and 368

Transferring and recording financial data accurately

Throughout workbook

Reconciling expenditures and revenue Unit 4 Knowledge of organisational policies and procedures relating to maintaining financial records

Throughout workbook

iv About this Workbook © Software Publications Pty Ltd, 2013

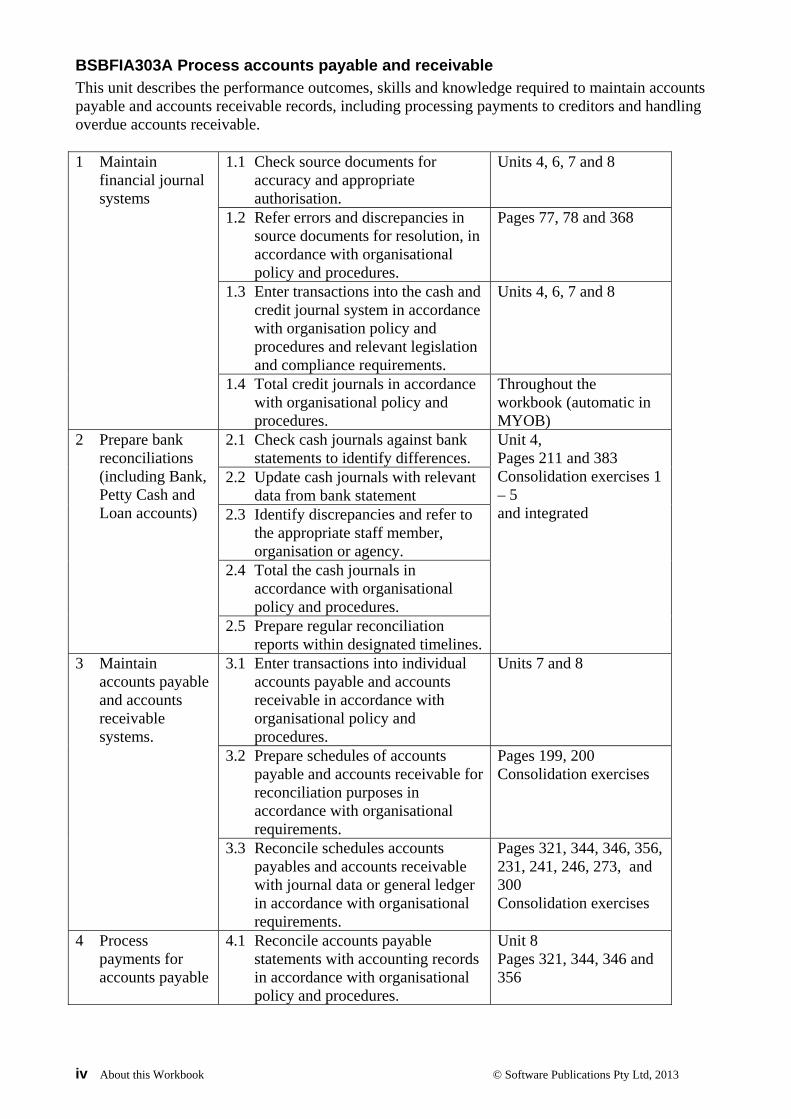

BSBFIA303A Process accounts payable and receivable This unit describes the performance outcomes, skills and knowledge required to maintain accounts payable and accounts receivable records, including processing payments to creditors and handling overdue accounts receivable. 1 Maintain

financial journal systems

1.1 Check source documents for accuracy and appropriate authorisation.

Units 4, 6, 7 and 8

1.2 Refer errors and discrepancies in source documents for resolution, in accordance with organisational policy and procedures.

Pages 77, 78 and 368

1.3 Enter transactions into the cash and credit journal system in accordance with organisation policy and procedures and relevant legislation and compliance requirements.

Units 4, 6, 7 and 8

1.4 Total credit journals in accordance with organisational policy and procedures.

Throughout the workbook (automatic in MYOB)

2 Prepare bank reconciliations (including Bank, Petty Cash and Loan accounts)

2.1 Check cash journals against bank statements to identify differences.

Unit 4, Pages 211 and 383 Consolidation exercises 1 – 5 and integrated

2.2 Update cash journals with relevant data from bank statement

2.3 Identify discrepancies and refer to the appropriate staff member, organisation or agency.

2.4 Total the cash journals in accordance with organisational policy and procedures.

2.5 Prepare regular reconciliation reports within designated timelines.

3 Maintain accounts payable and accounts receivable systems.

3.1 Enter transactions into individual accounts payable and accounts receivable in accordance with organisational policy and procedures.

Units 7 and 8

3.2 Prepare schedules of accounts payable and accounts receivable for reconciliation purposes in accordance with organisational requirements.

Pages 199, 200 Consolidation exercises

3.3 Reconcile schedules accounts payables and accounts receivable with journal data or general ledger in accordance with organisational requirements.

Pages 321, 344, 346, 356, 231, 241, 246, 273, and 300 Consolidation exercises

4 Process payments for accounts payable

4.1 Reconcile accounts payable statements with accounting records in accordance with organisational policy and procedures.

Unit 8 Pages 321, 344, 346 and 356

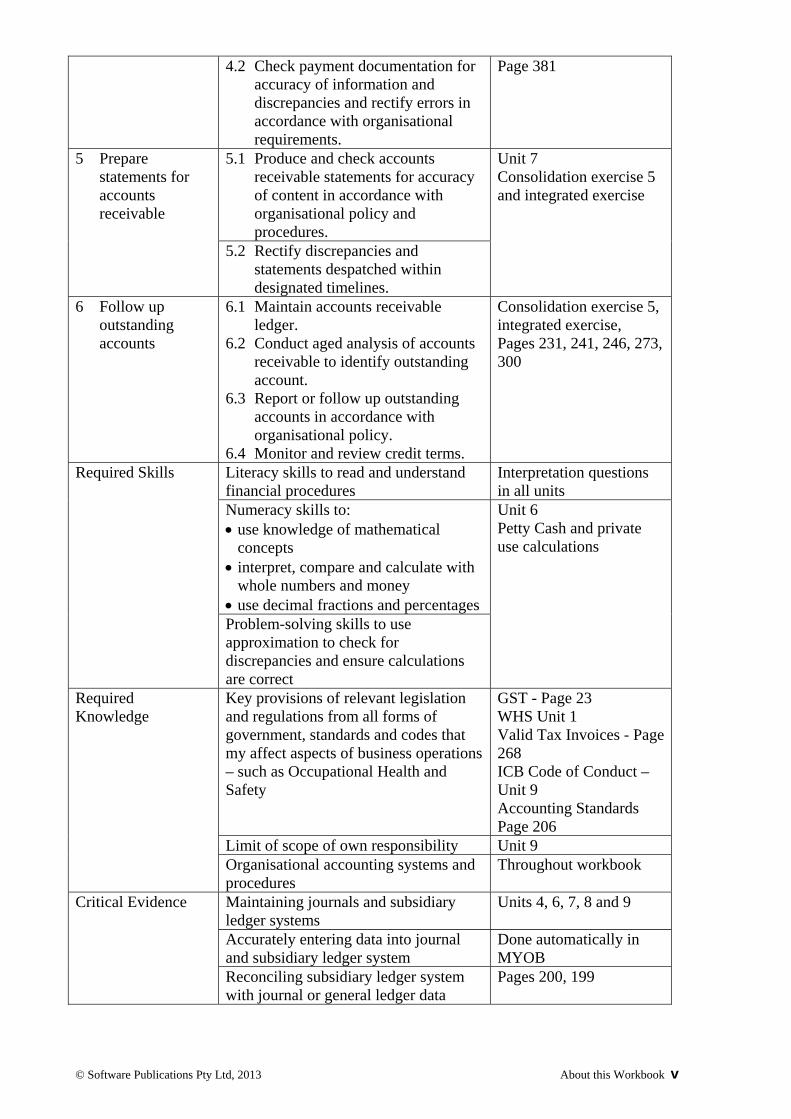

© Software Publications Pty Ltd, 2013 About this Workbook v

4.2 Check payment documentation for accuracy of information and discrepancies and rectify errors in accordance with organisational requirements.

Page 381

5 Prepare statements for accounts receivable

5.1 Produce and check accounts receivable statements for accuracy of content in accordance with organisational policy and procedures.

Unit 7 Consolidation exercise 5 and integrated exercise

5.2 Rectify discrepancies and statements despatched within designated timelines.

6 Follow up outstanding accounts

6.1 Maintain accounts receivable ledger.

6.2 Conduct aged analysis of accounts receivable to identify outstanding account.

6.3 Report or follow up outstanding accounts in accordance with organisational policy.

6.4 Monitor and review credit terms.

Consolidation exercise 5, integrated exercise, Pages 231, 241, 246, 273, 300

Required Skills Literacy skills to read and understand financial procedures

Interpretation questions in all units

Numeracy skills to: use knowledge of mathematical

concepts interpret, compare and calculate with

whole numbers and money use decimal fractions and percentages

Unit 6 Petty Cash and private use calculations

Problem-solving skills to use approximation to check for discrepancies and ensure calculations are correct

Required Knowledge

Key provisions of relevant legislation and regulations from all forms of government, standards and codes that my affect aspects of business operations – such as Occupational Health and Safety

GST - Page 23 WHS Unit 1 Valid Tax Invoices - Page 268 ICB Code of Conduct – Unit 9 Accounting Standards Page 206

Limit of scope of own responsibility Unit 9 Organisational accounting systems and procedures

Throughout workbook

Critical Evidence Maintaining journals and subsidiary ledger systems

Units 4, 6, 7, 8 and 9

Accurately entering data into journal and subsidiary ledger system

Done automatically in MYOB

Reconciling subsidiary ledger system with journal or general ledger data

Pages 200, 199

vi About this Workbook © Software Publications Pty Ltd, 2013

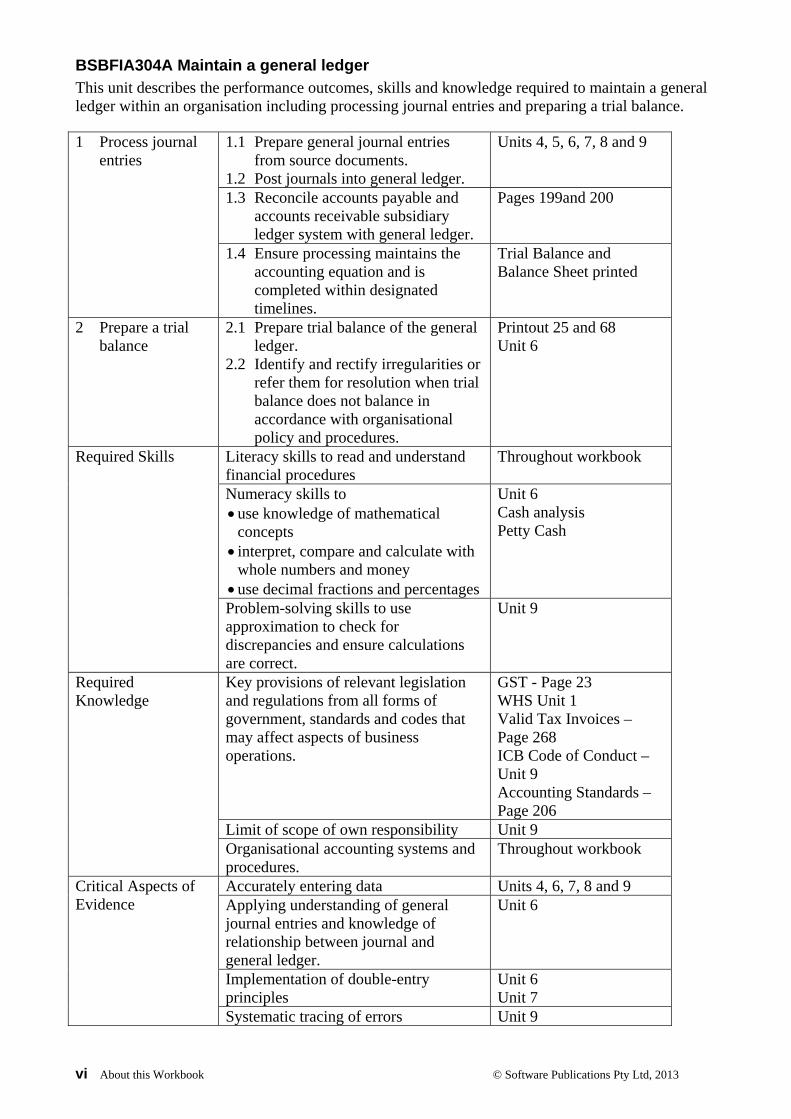

BSBFIA304A Maintain a general ledger This unit describes the performance outcomes, skills and knowledge required to maintain a general ledger within an organisation including processing journal entries and preparing a trial balance. 1 Process journal

entries 1.1 Prepare general journal entries

from source documents. 1.2 Post journals into general ledger.

Units 4, 5, 6, 7, 8 and 9

1.3 Reconcile accounts payable and accounts receivable subsidiary ledger system with general ledger.

Pages 199and 200

1.4 Ensure processing maintains the accounting equation and is completed within designated timelines.

Trial Balance and Balance Sheet printed

2 Prepare a trial balance

2.1 Prepare trial balance of the general ledger.

2.2 Identify and rectify irregularities or refer them for resolution when trial balance does not balance in accordance with organisational policy and procedures.

Printout 25 and 68 Unit 6

Required Skills

Literacy skills to read and understand financial procedures

Throughout workbook

Numeracy skills to use knowledge of mathematical

concepts interpret, compare and calculate with

whole numbers and money use decimal fractions and percentages

Unit 6 Cash analysis Petty Cash

Problem-solving skills to use approximation to check for discrepancies and ensure calculations are correct.

Unit 9

Required Knowledge

Key provisions of relevant legislation and regulations from all forms of government, standards and codes that may affect aspects of business operations.

GST - Page 23 WHS Unit 1 Valid Tax Invoices – Page 268 ICB Code of Conduct – Unit 9 Accounting Standards – Page 206

Limit of scope of own responsibility Unit 9 Organisational accounting systems and procedures.

Throughout workbook

Critical Aspects of Evidence

Accurately entering data Units 4, 6, 7, 8 and 9 Applying understanding of general journal entries and knowledge of relationship between journal and general ledger.

Unit 6

Implementation of double-entry principles

Unit 6 Unit 7

Systematic tracing of errors Unit 9

© Software Publications Pty Ltd, 2013 Unit 2 5

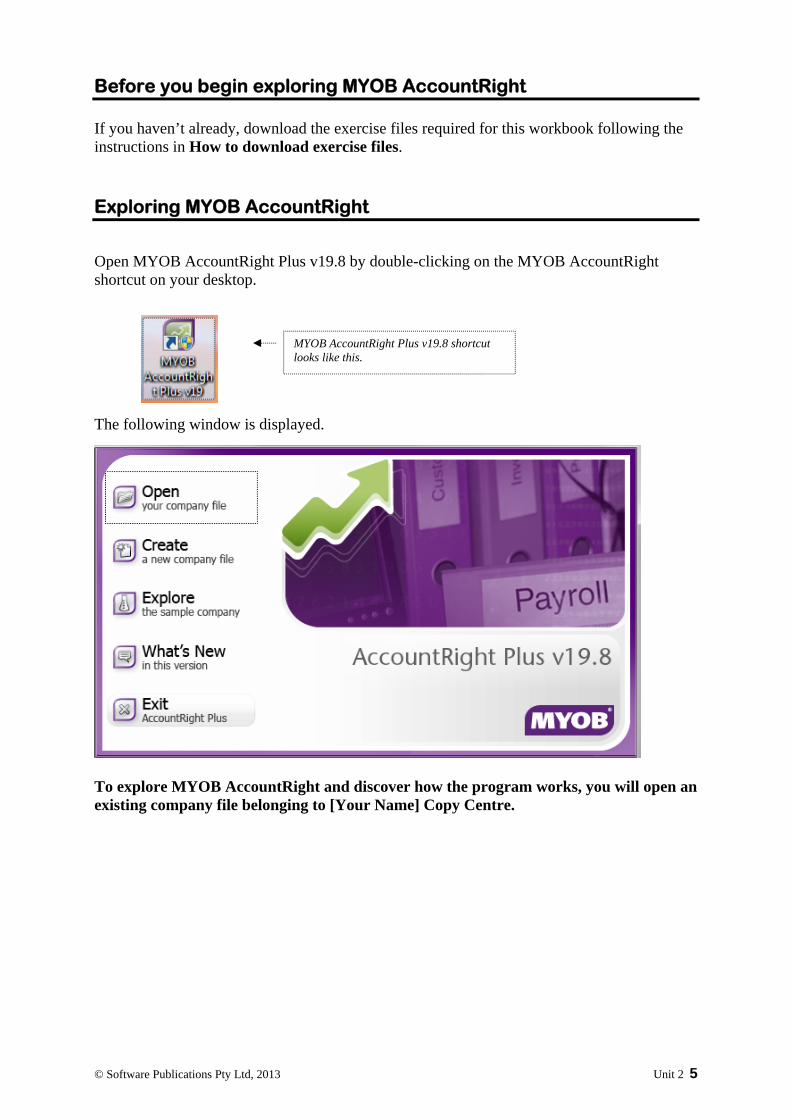

Before you begin exploring MYOB AccountRight

If you haven’t already, download the exercise files required for this workbook following the instructions in How to download exercise files.

Exploring MYOB AccountRight Open MYOB AccountRight Plus v19.8 by double-clicking on the MYOB AccountRight shortcut on your desktop.

The following window is displayed.

To explore MYOB AccountRight and discover how the program works, you will open an existing company file belonging to [Your Name] Copy Centre.

MYOB AccountRight Plus v19.8 shortcut looks like this.

6 Unit 2 © Software Publications Pty Ltd, 2013

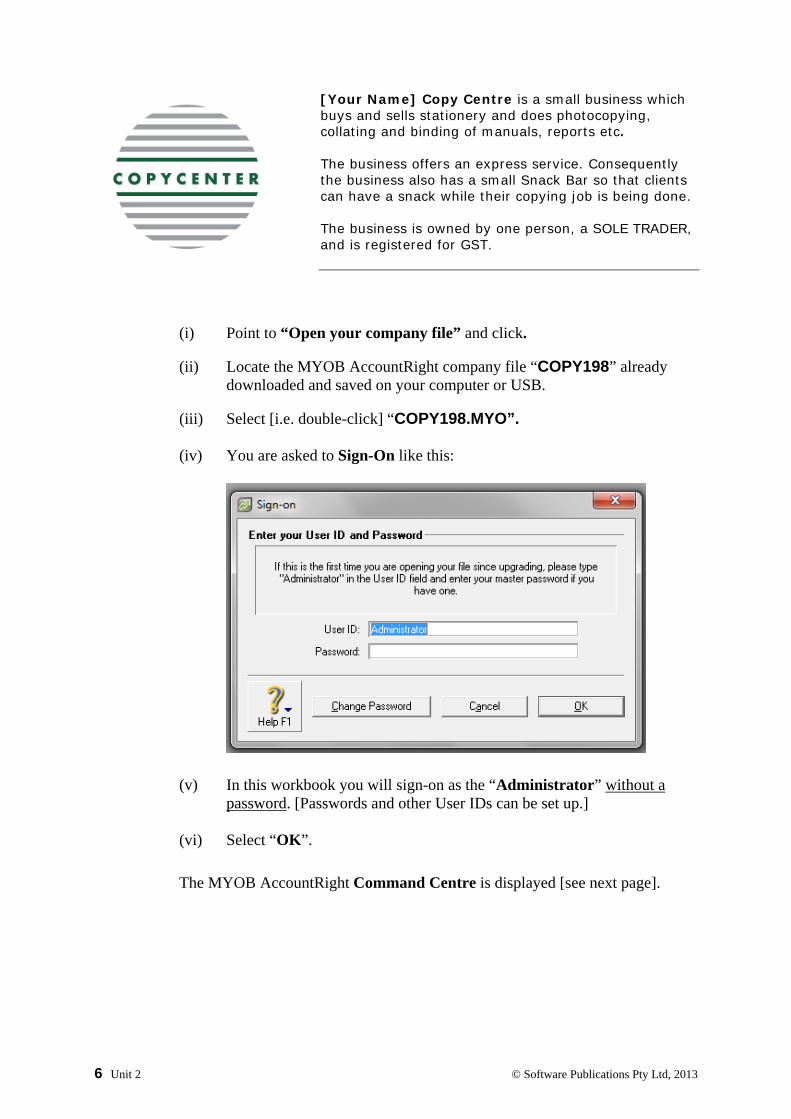

[Your Name] Copy Centre is a small business which buys and sells stationery and does photocopying, collating and binding of manuals, reports etc. The business offers an express service. Consequently the business also has a small Snack Bar so that clients can have a snack while their copying job is being done. The business is owned by one person, a SOLE TRADER, and is registered for GST.

(i) Point to “Open your company file” and click.

(ii) Locate the MYOB AccountRight company file “COPY198” already downloaded and saved on your computer or USB.

(iii) Select [i.e. double-click] “COPY198.MYO”.

(iv) You are asked to Sign-On like this:

(v) In this workbook you will sign-on as the “Administrator” without a password. [Passwords and other User IDs can be set up.]

(vi) Select “OK”.

The MYOB AccountRight Command Centre is displayed [see next page].

© Software Publications Pty Ltd, 2013 Unit 2 7

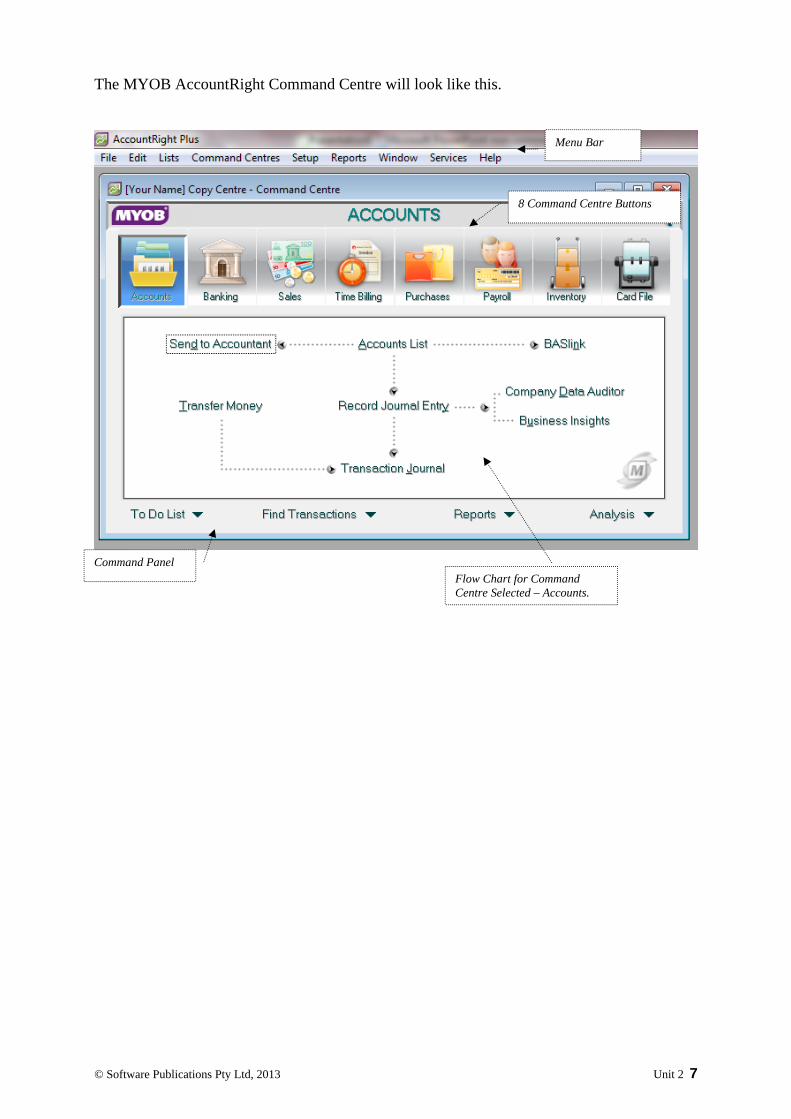

The MYOB AccountRight Command Centre will look like this.

Menu Bar

8 Command Centre Buttons

Flow Chart for Command Centre Selected – Accounts.

Command Panel

© Software Publications Pty Ltd, 2013 Unit 4 71

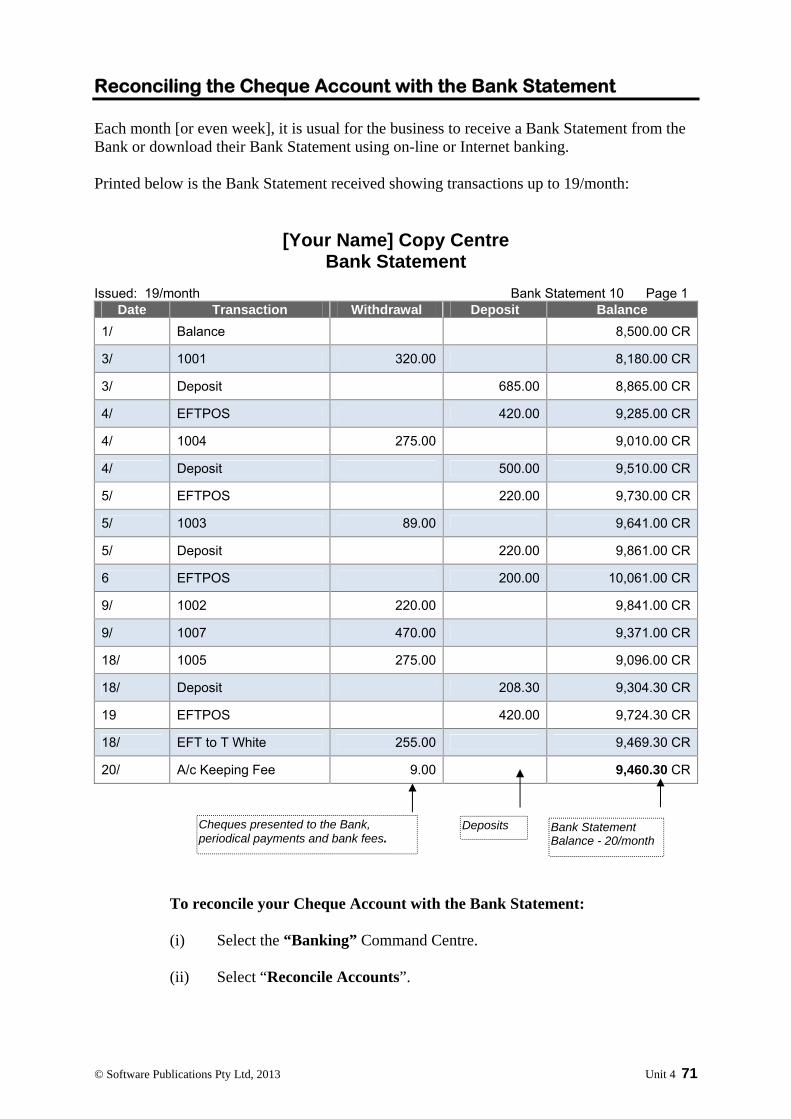

Reconciling the Cheque Account with the Bank Statement Each month [or even week], it is usual for the business to receive a Bank Statement from the Bank or download their Bank Statement using on-line or Internet banking.

Printed below is the Bank Statement received showing transactions up to 19/month:

[Your Name] Copy Centre Bank Statement

Issued: 19/month Bank Statement 10 Page 1

Date Transaction Withdrawal Deposit Balance

1/ Balance 8,500.00 CR

3/ 1001 320.00 8,180.00 CR

3/ Deposit 685.00 8,865.00 CR

4/ EFTPOS 420.00 9,285.00 CR

4/ 1004 275.00 9,010.00 CR

4/ Deposit 500.00 9,510.00 CR

5/ EFTPOS 220.00 9,730.00 CR

5/ 1003 89.00 9,641.00 CR

5/ Deposit 220.00 9,861.00 CR

6 EFTPOS 200.00 10,061.00 CR

9/ 1002 220.00 9,841.00 CR

9/ 1007 470.00 9,371.00 CR

18/ 1005 275.00 9,096.00 CR

18/ Deposit 208.30 9,304.30 CR

19 EFTPOS 420.00 9,724.30 CR

18/ EFT to T White 255.00 9,469.30 CR

20/ A/c Keeping Fee 9.00 9,460.30 CR

To reconcile your Cheque Account with the Bank Statement:

(i) Select the “Banking” Command Centre. (ii) Select “Reconcile Accounts”.

Cheques presented to the Bank, periodical payments and bank fees.

Deposits Bank Statement Balance - 20/month

72 Unit 4 © Software Publications Pty Ltd, 2013

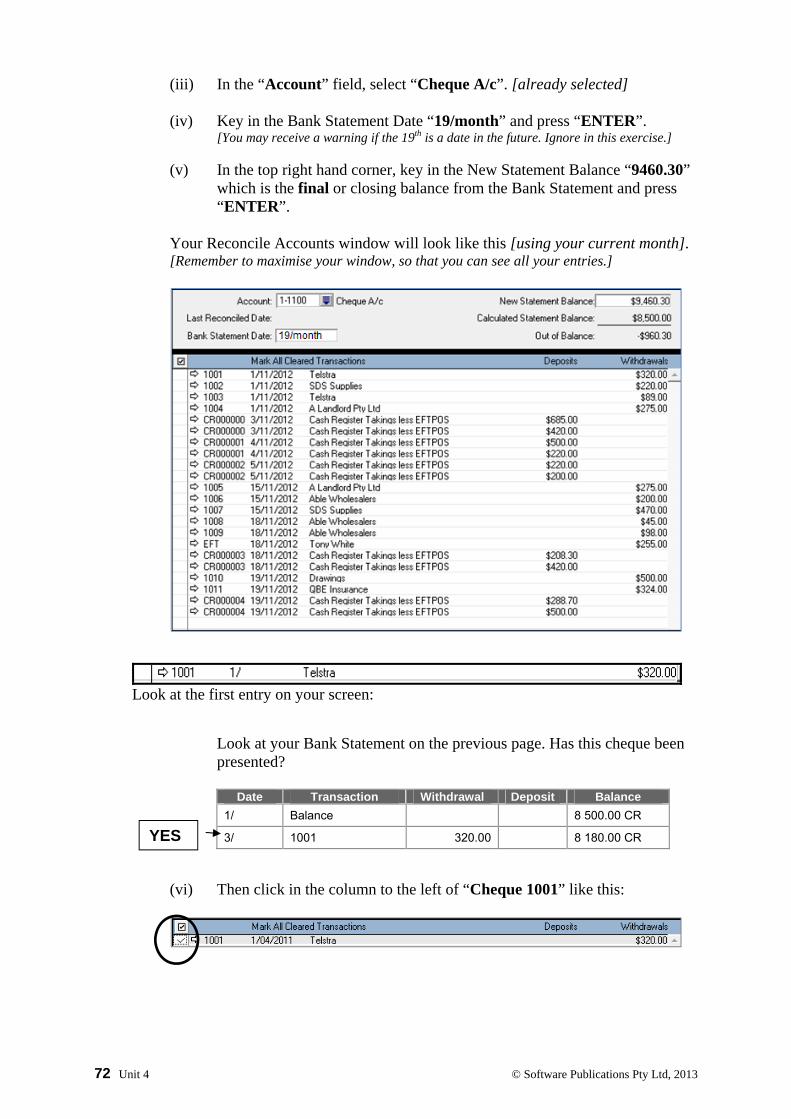

(iii) In the “Account” field, select “Cheque A/c”. [already selected] (iv) Key in the Bank Statement Date “19/month” and press “ENTER”.

[You may receive a warning if the 19th is a date in the future. Ignore in this exercise.]

(v) In the top right hand corner, key in the New Statement Balance “9460.30” which is the final or closing balance from the Bank Statement and press “ENTER”.

Your Reconcile Accounts window will look like this [using your current month]. [Remember to maximise your window, so that you can see all your entries.]

Look at the first entry on your screen:

Look at your Bank Statement on the previous page. Has this cheque been presented?

Date Transaction Withdrawal Deposit Balance

1/ Balance 8 500.00 CR

3/ 1001 320.00 8 180.00 CR

(vi) Then click in the column to the left of “Cheque 1001” like this:

YES

© Software Publications Pty Ltd, 2013 Unit 4 73

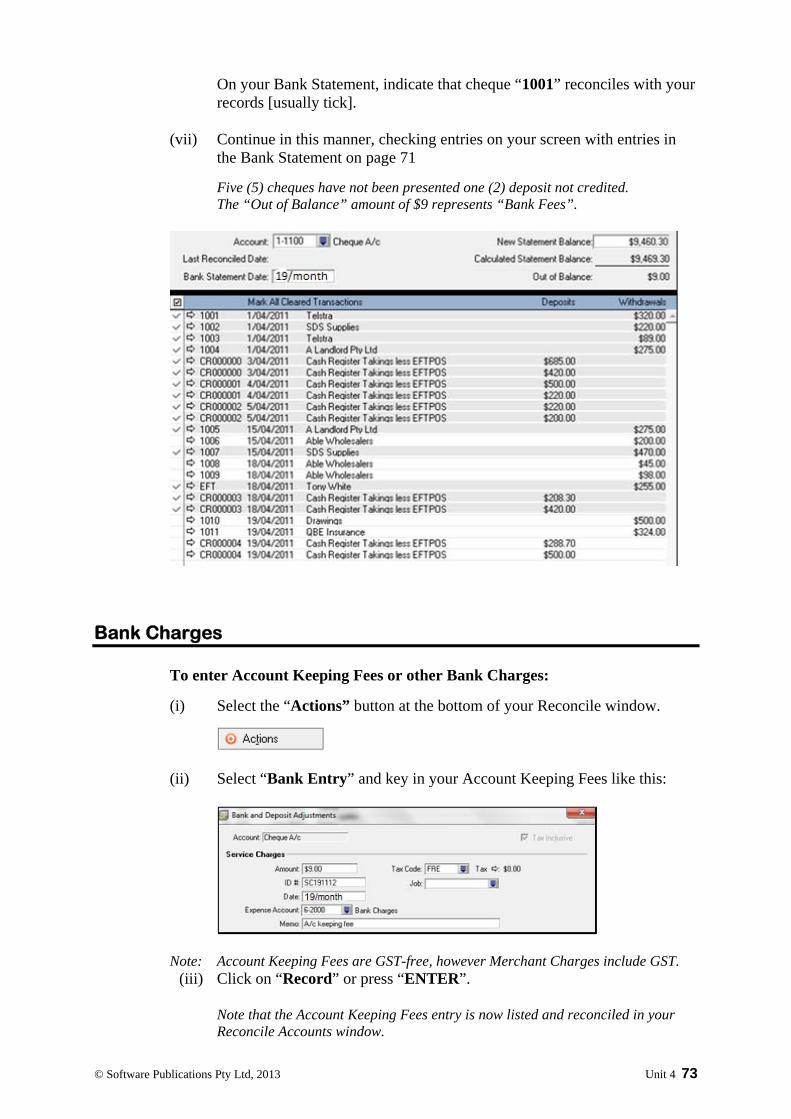

On your Bank Statement, indicate that cheque “1001” reconciles with your records [usually tick].

(vii) Continue in this manner, checking entries on your screen with entries in

the Bank Statement on page 71

Five (5) cheques have not been presented one (2) deposit not credited. The “Out of Balance” amount of $9 represents “Bank Fees”.

Bank Charges To enter Account Keeping Fees or other Bank Charges:

(i) Select the “Actions” button at the bottom of your Reconcile window.

(ii) Select “Bank Entry” and key in your Account Keeping Fees like this:

Note: Account Keeping Fees are GST-free, however Merchant Charges include GST. (iii) Click on “Record” or press “ENTER”.

Note that the Account Keeping Fees entry is now listed and reconciled in your Reconcile Accounts window.

74 Unit 4 © Software Publications Pty Ltd, 2013

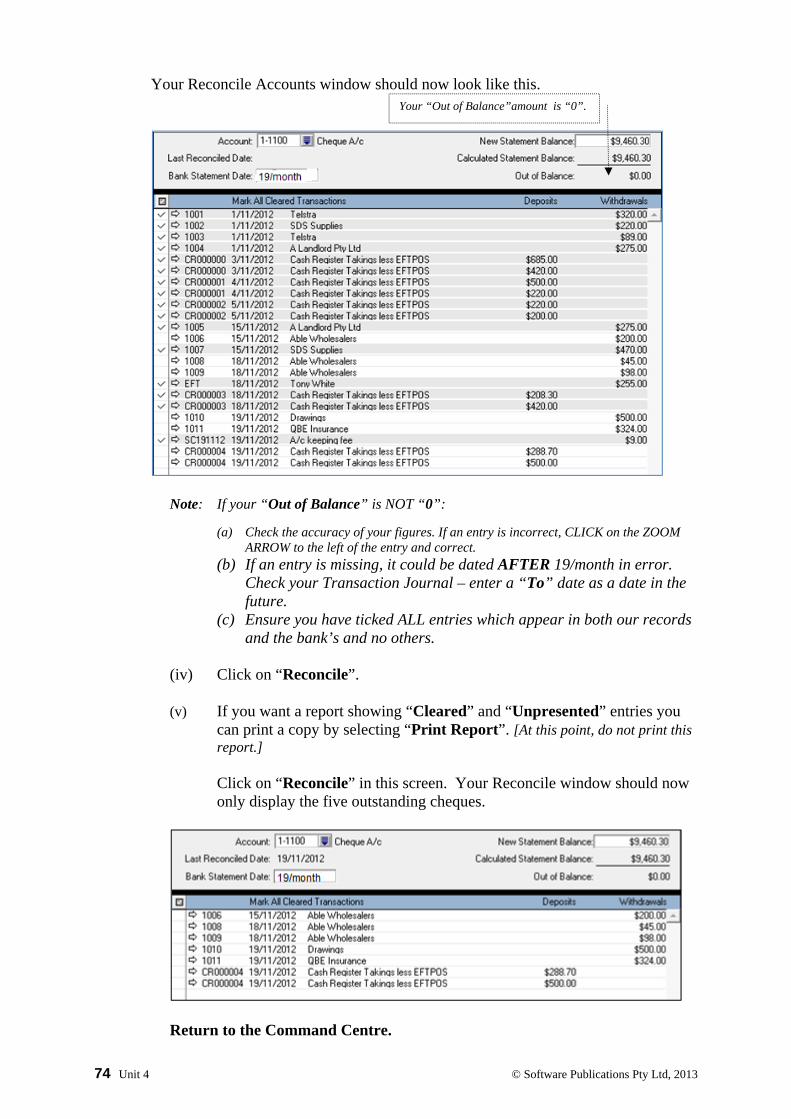

Your Reconcile Accounts window should now look like this.

Note: If your “Out of Balance” is NOT “0”:

(a) Check the accuracy of your figures. If an entry is incorrect, CLICK on the ZOOM ARROW to the left of the entry and correct.

(b) If an entry is missing, it could be dated AFTER 19/month in error. Check your Transaction Journal – enter a “To” date as a date in the future.

(c) Ensure you have ticked ALL entries which appear in both our records and the bank’s and no others.

(iv) Click on “Reconcile”.

(v) If you want a report showing “Cleared” and “Unpresented” entries you can print a copy by selecting “Print Report”. [At this point, do not print this report.]

Click on “Reconcile” in this screen. Your Reconcile window should now only display the five outstanding cheques.

Return to the Command Centre.

Your “Out of Balance”amount is “0”.

© Software Publications Pty Ltd, 2013 Unit 4 75

Undo the Bank Reconciliation

You will now “Undo Reconciliation” so that you can practise reconciling a second time.

[In business, you would undo the reconciliation if you have made an error or entered the incorrect reconciliation date. You can undo the last reconciliation, then the previous reconciliation and so on.]

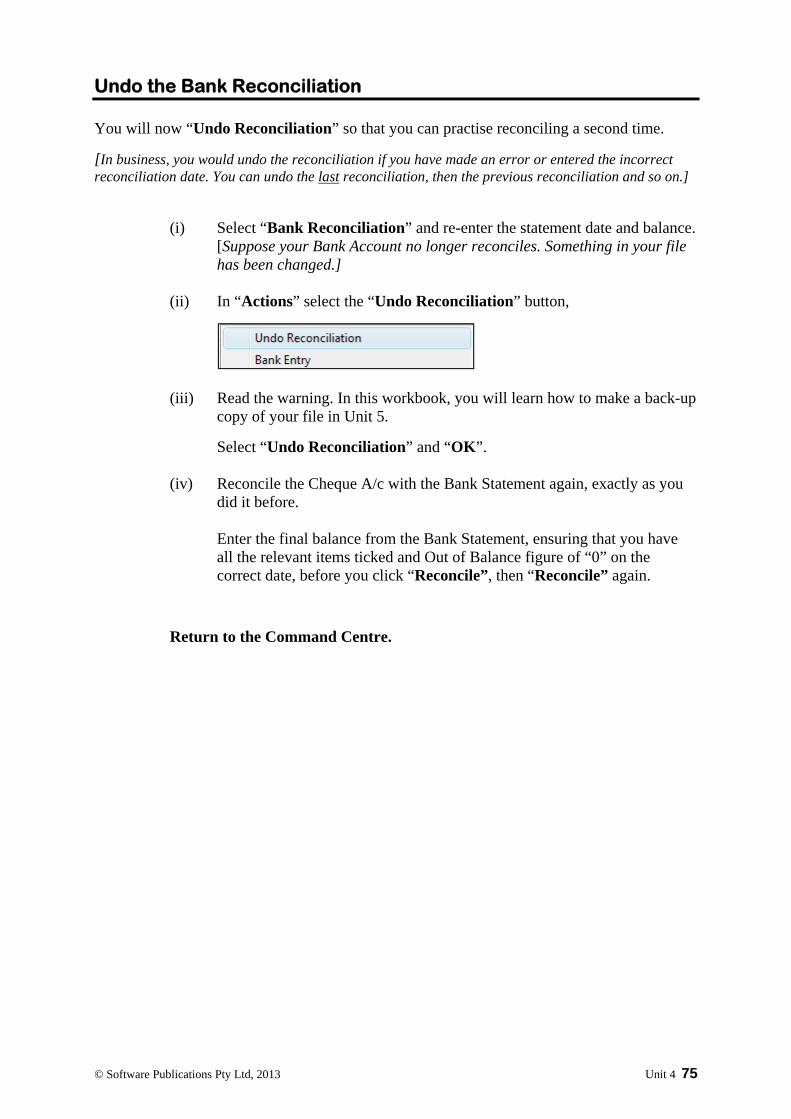

(i) Select “Bank Reconciliation” and re-enter the statement date and balance. [Suppose your Bank Account no longer reconciles. Something in your file has been changed.]

(ii) In “Actions” select the “Undo Reconciliation” button,

(iii) Read the warning. In this workbook, you will learn how to make a back-up

copy of your file in Unit 5.

Select “Undo Reconciliation” and “OK”. (iv) Reconcile the Cheque A/c with the Bank Statement again, exactly as you

did it before.

Enter the final balance from the Bank Statement, ensuring that you have all the relevant items ticked and Out of Balance figure of “0” on the correct date, before you click “Reconcile”, then “Reconcile” again.

Return to the Command Centre.

76 Unit 4 © Software Publications Pty Ltd, 2013

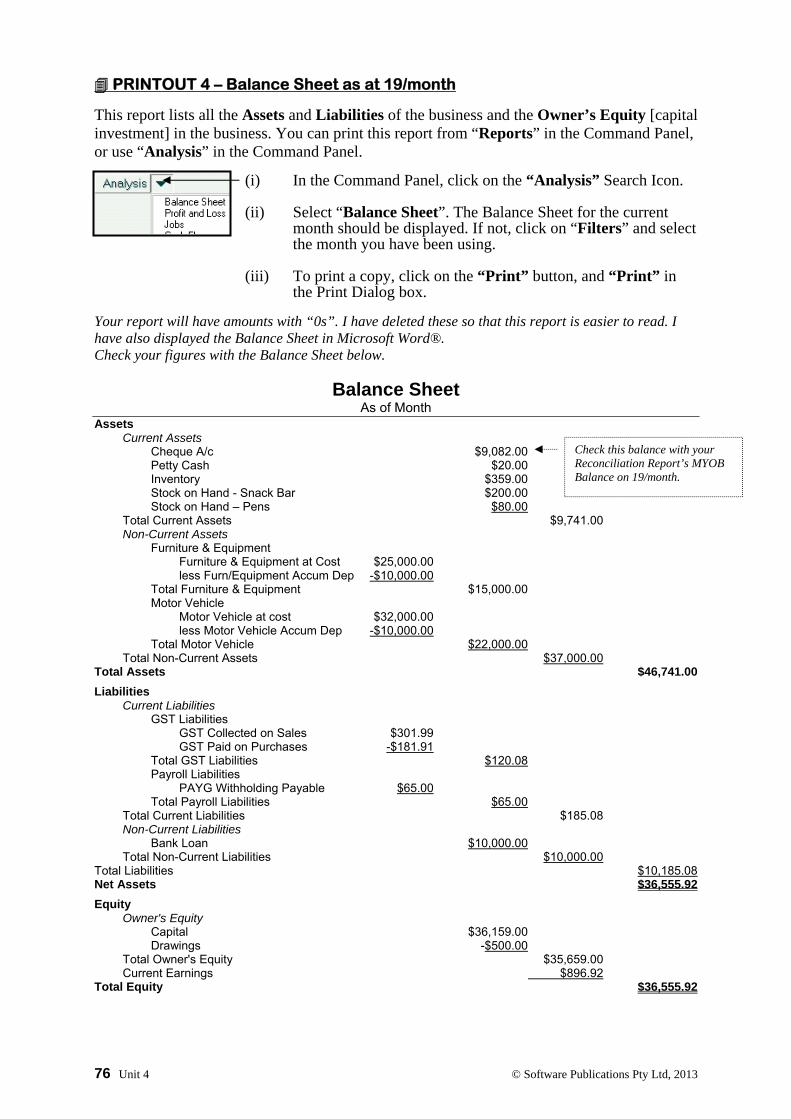

PRINTOUT 4 – Balance Sheet as at 19/month

This report lists all the Assets and Liabilities of the business and the Owner’s Equity [capital investment] in the business. You can print this report from “Reports” in the Command Panel, or use “Analysis” in the Command Panel.

(i) In the Command Panel, click on the “Analysis” Search Icon. 4

(ii) Select “Balance Sheet”. The Balance Sheet for the current month should be displayed. If not, click on “Filters” and select the month you have been using.

(iii) To print a copy, click on the “Print” button, and “Print” in the Print Dialog box.

Your report will have amounts with “0s”. I have deleted these so that this report is easier to read. I have also displayed the Balance Sheet in Microsoft Word®. Check your figures with the Balance Sheet below.

Balance Sheet As of Month

Assets Current Assets Cheque A/c $9,082.00 Petty Cash $20.00 Inventory $359.00 Stock on Hand - Snack Bar $200.00 Stock on Hand – Pens $80.00 Total Current Assets $9,741.00 Non-Current Assets Furniture & Equipment Furniture & Equipment at Cost $25,000.00 less Furn/Equipment Accum Dep -$10,000.00 Total Furniture & Equipment $15,000.00 Motor Vehicle Motor Vehicle at cost $32,000.00 less Motor Vehicle Accum Dep -$10,000.00 Total Motor Vehicle $22,000.00 Total Non-Current Assets $37,000.00 Total Assets $46,741.00

Liabilities Current Liabilities GST Liabilities GST Collected on Sales $301.99 GST Paid on Purchases -$181.91 Total GST Liabilities $120.08 Payroll Liabilities PAYG Withholding Payable $65.00 Total Payroll Liabilities $65.00 Total Current Liabilities $185.08 Non-Current Liabilities Bank Loan $10,000.00 Total Non-Current Liabilities $10,000.00 Total Liabilities $10,185.08 Net Assets $36,555.92

Equity Owner's Equity Capital $36,159.00 Drawings -$500.00 Total Owner's Equity $35,659.00 Current Earnings $896.92 Total Equity $36,555.92

Check this balance with your Reconciliation Report’s MYOB Balance on 19/month.

© Software Publications Pty Ltd, 2013 Unit 4 77

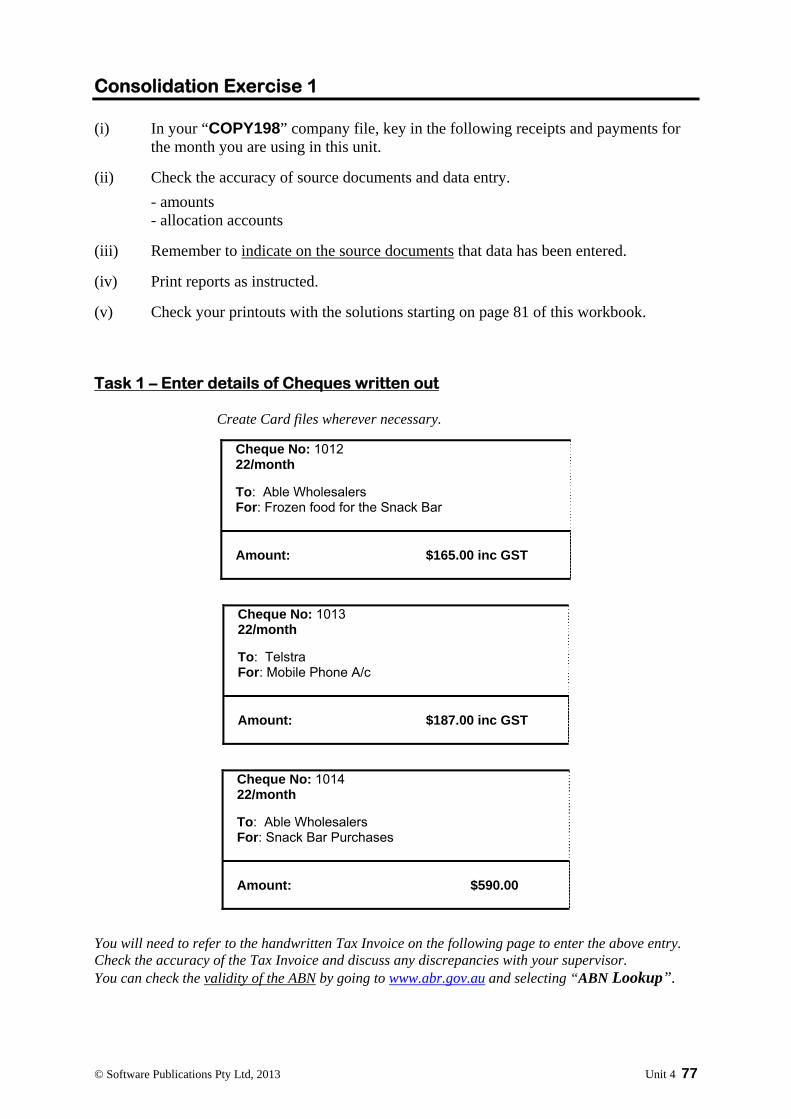

Consolidation Exercise 1

(i) In your “COPY198” company file, key in the following receipts and payments for the month you are using in this unit.

(ii) Check the accuracy of source documents and data entry.

- amounts - allocation accounts

(iii) Remember to indicate on the source documents that data has been entered.

(iv) Print reports as instructed.

(v) Check your printouts with the solutions starting on page 81 of this workbook.

Task 1 – Enter details of Cheques written out Create Card files wherever necessary.

Cheque No: 1012 22/month To: Able Wholesalers For: Frozen food for the Snack Bar Amount: $165.00 inc GST

Cheque No: 1013 22/month To: Telstra For: Mobile Phone A/c Amount: $187.00 inc GST

Cheque No: 1014 22/month To: Able Wholesalers For: Snack Bar Purchases Amount: $590.00

You will need to refer to the handwritten Tax Invoice on the following page to enter the above entry. Check the accuracy of the Tax Invoice and discuss any discrepancies with your supervisor. You can check the validity of the ABN by going to www.abr.gov.au and selecting “ABN Lookup”.

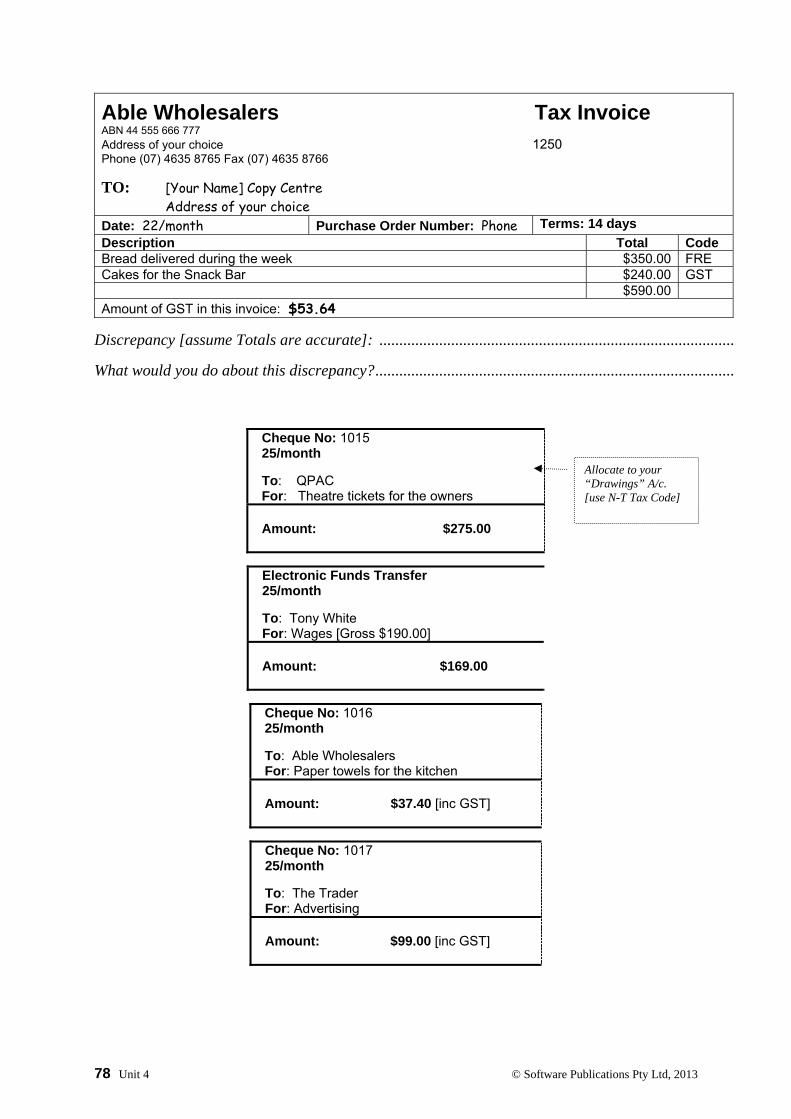

78 Unit 4 © Software Publications Pty Ltd, 2013

Able Wholesalers Tax Invoice ABN 44 555 666 777 Address of your choice 1250 Phone (07) 4635 8765 Fax (07) 4635 8766

TO: [Your Name] Copy Centre Address of your choice Date: 22/month Purchase Order Number: Phone Terms: 14 days

Description Total Code Bread delivered during the week $350.00 FRE Cakes for the Snack Bar $240.00 GST $590.00 Amount of GST in this invoice: $53.64

Discrepancy [assume Totals are accurate]: .........................................................................................

What would you do about this discrepancy? ..........................................................................................

Cheque No: 1015 25/month To: QPAC For: Theatre tickets for the owners Amount: $275.00

Electronic Funds Transfer 25/month To: Tony White For: Wages [Gross $190.00] Amount: $169.00

Cheque No: 1016 25/month To: Able Wholesalers For: Paper towels for the kitchen Amount: $37.40 [inc GST]

Cheque No: 1017 25/month To: The Trader For: Advertising Amount: $99.00 [inc GST]

Allocate to your “Drawings” A/c. [use N-T Tax Code]

© Software Publications Pty Ltd, 2013 Unit 4 79

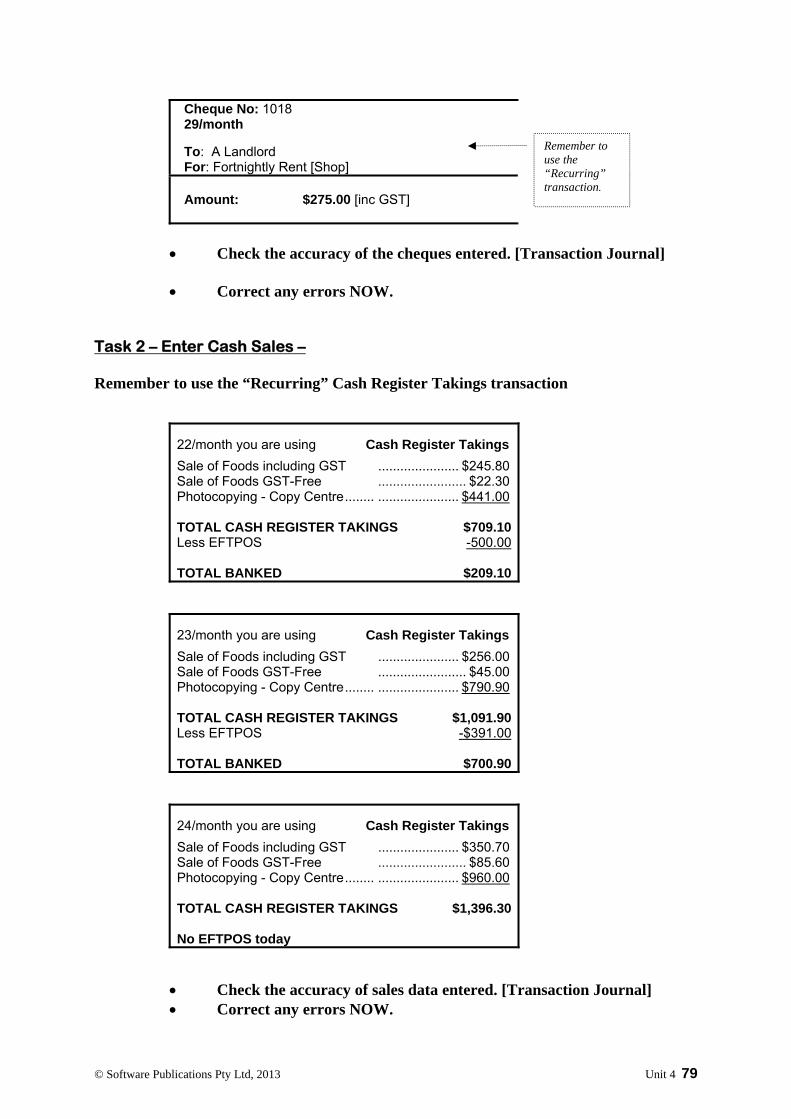

Cheque No: 1018 29/month To: A Landlord For: Fortnightly Rent [Shop] Amount: $275.00 [inc GST]

Check the accuracy of the cheques entered. [Transaction Journal] Correct any errors NOW.

Task 2 – Enter Cash Sales – Remember to use the “Recurring” Cash Register Takings transaction

22/month you are using Cash Register Takings

Sale of Foods including GST ...................... $245.80 Sale of Foods GST-Free ........................ $22.30 Photocopying - Copy Centre ........ ...................... $441.00 TOTAL CASH REGISTER TAKINGS $709.10Less EFTPOS -500.00 TOTAL BANKED $209.10

23/month you are using Cash Register Takings

Sale of Foods including GST ...................... $256.00 Sale of Foods GST-Free ........................ $45.00 Photocopying - Copy Centre ........ ...................... $790.90 TOTAL CASH REGISTER TAKINGS $1,091.90Less EFTPOS -$391.00 TOTAL BANKED $700.90

24/month you are using Cash Register Takings

Sale of Foods including GST ...................... $350.70 Sale of Foods GST-Free ........................ $85.60 Photocopying - Copy Centre ........ ...................... $960.00 TOTAL CASH REGISTER TAKINGS $1,396.30 No EFTPOS today

Check the accuracy of sales data entered. [Transaction Journal] Correct any errors NOW.

Remember to use the “Recurring” transaction.

162 Unit 7 © Software Publications Pty Ltd, 2013

Entering Credit Card Payments – using “Spend Money”

The following invoices were paid by credit card. The invoices will not be recorded in purchases. [Add invoice number to Memo.] You are required to enter the payments using “Spend Money”.

Metropolitan Chemicals Tax Invoice ABN 78 124 784 222 4578111 TO: Your Fitness Centre Address Date: 10/current month

Description Total inc GST Tax

CodePool Chemicals $256.00 GST

The above entry will look like this.

Mojo Advertising Invoice ABN 78 445 114 229 11457

TO: Your Fitness Centre Address Date: 10/current month

Description Total ex GST Advertising $140.00

PAID 10/month

Make sure “MasterCard” is selected.

PAID $140 10/month

© Software Publications Pty Ltd, 2013 Unit 7 163

Before entering the above invoice, answer the following questions?

(i) Does the above invoice include GST? ...................................................................

(ii) Give a reason for your answer. ................................................................................

.................................................................................................................................

(iii) What Tax Code will be used? ................................................................................. [Answers can be found at the end of this unit.]

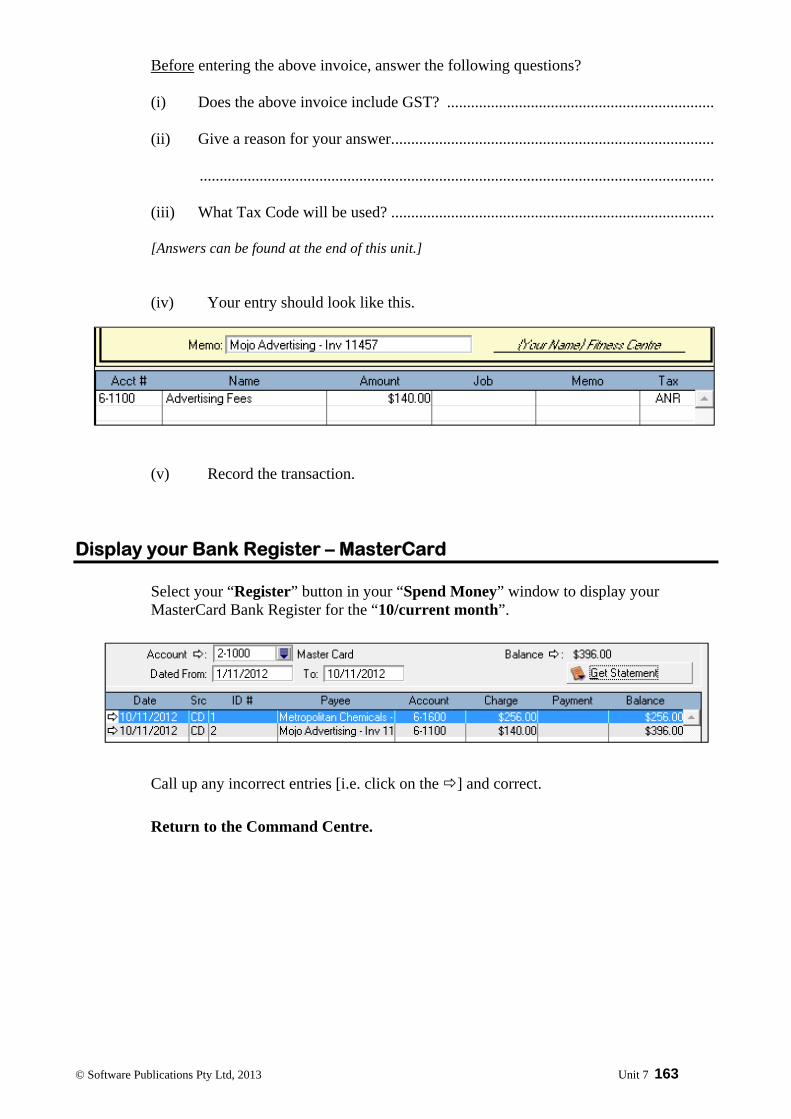

(iv) Your entry should look like this.

(v) Record the transaction. Display your Bank Register – MasterCard Select your “Register” button in your “Spend Money” window to display your

MasterCard Bank Register for the “10/current month”.

Call up any incorrect entries [i.e. click on the ] and correct.

Return to the Command Centre.

164 Unit 7 © Software Publications Pty Ltd, 2013

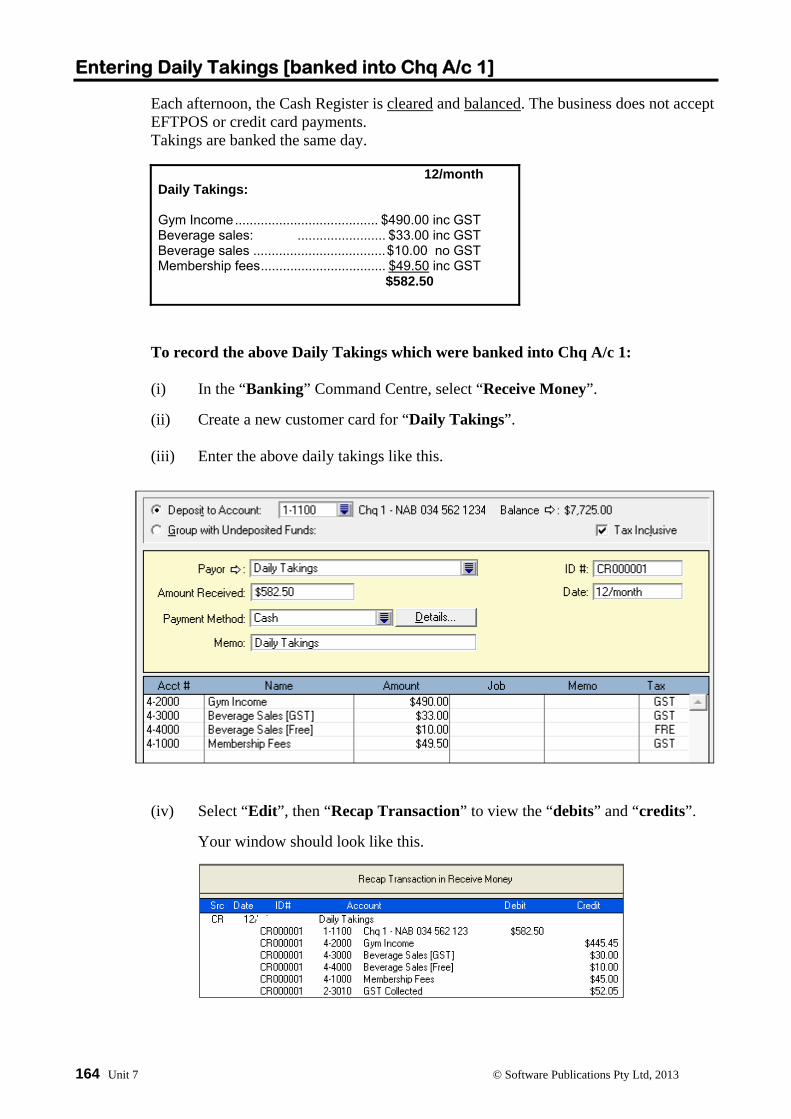

Entering Daily Takings [banked into Chq A/c 1]

Each afternoon, the Cash Register is cleared and balanced. The business does not accept EFTPOS or credit card payments. Takings are banked the same day.

12/month Daily Takings: Gym Income ....................................... $490.00 inc GST Beverage sales: ........................ $33.00 inc GST Beverage sales .................................... $10.00 no GST Membership fees .................................. $49.50 inc GST $582.50

To record the above Daily Takings which were banked into Chq A/c 1:

(i) In the “Banking” Command Centre, select “Receive Money”.

(ii) Create a new customer card for “Daily Takings”.

(iii) Enter the above daily takings like this.

(iv) Select “Edit”, then “Recap Transaction” to view the “debits” and “credits”.

Your window should look like this.

© Software Publications Pty Ltd, 2013 Unit 7 165

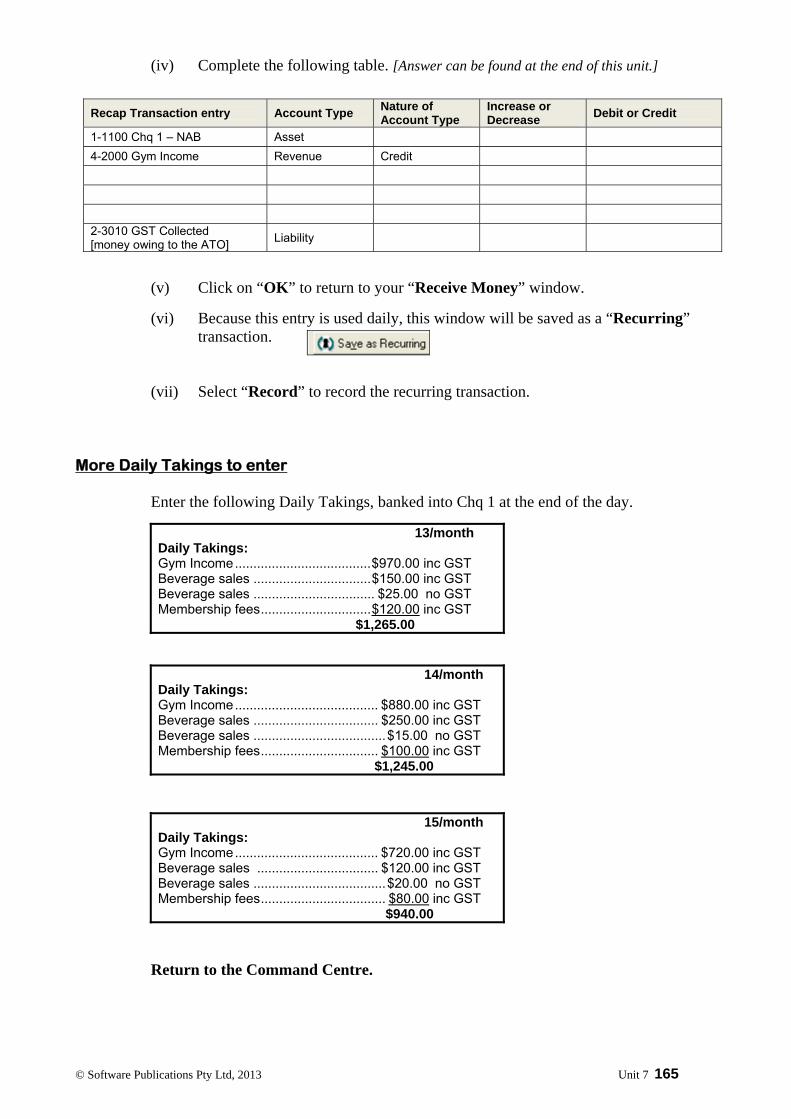

(iv) Complete the following table. [Answer can be found at the end of this unit.]

Recap Transaction entry Account Type

Nature of Account Type

Increase or Decrease

Debit or Credit

1-1100 Chq 1 – NAB Asset

4-2000 Gym Income Revenue Credit

2-3010 GST Collected [money owing to the ATO]

Liability

(v) Click on “OK” to return to your “Receive Money” window.

(vi) Because this entry is used daily, this window will be saved as a “Recurring” transaction.

(vii) Select “Record” to record the recurring transaction.

More Daily Takings to enter

Enter the following Daily Takings, banked into Chq 1 at the end of the day.

13/month Daily Takings: Gym Income ..................................... $970.00 inc GST Beverage sales ................................ $150.00 inc GST Beverage sales ................................. $25.00 no GST Membership fees .............................. $120.00 inc GST $1,265.00

14/month Daily Takings: Gym Income ....................................... $880.00 inc GST Beverage sales .................................. $250.00 inc GST Beverage sales .................................... $15.00 no GST Membership fees ................................ $100.00 inc GST $1,245.00

15/month Daily Takings: Gym Income ....................................... $720.00 inc GST Beverage sales ................................. $120.00 inc GST Beverage sales .................................... $20.00 no GST Membership fees .................................. $80.00 inc GST $940.00

Return to the Command Centre.

© Software Publications Pty Ltd, 2013 Unit 8 227

Unit 8: Accounts Receivable using MYOB

Learning Outcomes

On completion of this unit you should be able to:

Enter sales invoice data and check for accuracy Print invoices, adjustment notes and statements Create items and enter item invoices Customise an invoice according to the requirements of the business Maintain customer information – address, credit limits, answer enquiries Print Accounts Receivable reports – sales analysis, aged receivables, bank

deposit slip Enter over and under charges correction, error correction, returns, allocate

commission to sales staff, write off a bad debt Carry out end of period processing Account for cash discount Identify discrepancies and refer to appropriate person Identify outstanding accounts and follow up in accordance with

organisational policy Reconcile the Accounts Receivable Ledger with the General Ledger.

228 Unit 8 © Software Publications Pty Ltd, 2013

Simulation Exercise

To learn how to perform the functions set out on the previous page, you will set up a landscaping business and maintain the Accounts Receivable transactions for this business.

The LANDSCAPING business is owned by a Sole Trader. This business sells a variety of landscaping supplies for cash and on credit, designs and builds gardens and hires out the bobcat.

This business has stock on hand of landscaping supplies and irrigation equipment, however quantities are small. Consequently, the business does not wish to inventory stock items. The business will use the Periodic [Physical] Stock system, and take a stocktake at the end of the financial year to estimate the value of stock on hand. The business has an ABN and is registered for GST, reporting quarterly on a CASH BASIS. The business has a Procedures Manual for staff to follow – see next page. REVENUE: Sales – landscaping supplies Sales – irrigation systems Consultancy – designing gardens Hire of Bobcat Sales - Labour BANK ACCOUNTS: The business has the following accounts: Cheque A/c – main business account

Undeposited Funds – all money received is paid into this account, then banked.

© Software Publications Pty Ltd, 2013 Unit 8 229

[Your Name] Landscaping POLICIES AND PROCEDURES – ACCOUNTS RECEIVABLE 1 Accounting System The business keeps an Accrual set of books, accounting for debtors and creditors. 2 Invoicing The business always issues “Tax Inclusive” service invoices on plain paper for landscaping sales. A “Tax Inclusive” Professional Invoice is used for consultancy invoices. An item invoice is used for landscaping material sales. The business uses Items for sales of landscaping materials, however Physical Inventory is used. 3 Accounts Receivable A card for each cash or credit customer must be established. This card must contain postal and street address, phone numbers and contacts. Under the Privacy Act 1988, details kept must be accurate and not given to any person without the consent of the customer. A Credit Application must be completed by account customers and at least 1 of the referees contacted before credit is given. All sales are recorded in MYOB at the point of sale and a Tax Invoice meeting legislation requirements printed. Before credit is given, the customer account balance must be checked. Payments in the form of cash and cheques are processed immediately upon receipt and stored in the cash register during the day, and allocated to “undeposited funds” in MYOB. The till is balanced at the end of each day. All cash and cheques are stored in the safe overnight. Only a small amount of cash is received, therefore a weekly banking of cash and cheques takes place. Bank Deposit Slips are printed and submitted to the bank with a credit summary slip. Customers are requested to fax or email a remittance if payment is made by Electronic Funds Transfer. These payments must be entered in MYOB as soon as possible. Cheques are only accepted from long-term customers. On receipt of the cheque, the date, amounts and signature must be checked. All customer requests and complaints must be handled immediately in a professional manner. 4 Customer Credit Policy Credit terms are as follows: Full payment is required within 30 days of the date of the invoice. Credit facilities will be placed on hold when accounts are outstanding for more than 60 days, unless an alternative payment arrangement has been negotiated with the customer. Details of such arrangements should be made in the Contact Log in MYOB. An aged receivables report is printed at the end of each month and overdue accounts and credit terms reviewed. Monthly statements are printed by the 5th of the following month. 5 Overdue Accounts Policy Account overdue up to 30 days: An overdue reminder sticker will be attached to the next

statement. Account overdue 60 days: Credit facilities will be put on hold. The customer should be

contacted to assess financial position and negotiate a payment plan. A note should be made in the MYOB Contact Log.

Account overdue 90 or more days: A letter of demand will be sent to the customer asking for payment within 14 days. If this fails, the MYOB Debt Recovery service will be used to collect the debt if more than $200. Small debts < $200 will be written off as a bad debt. The Debt Collection Guideline for Collectors and Creditors [www.accc.gov website] must be adhered to at all times.

230 Unit 8 © Software Publications Pty Ltd, 2013

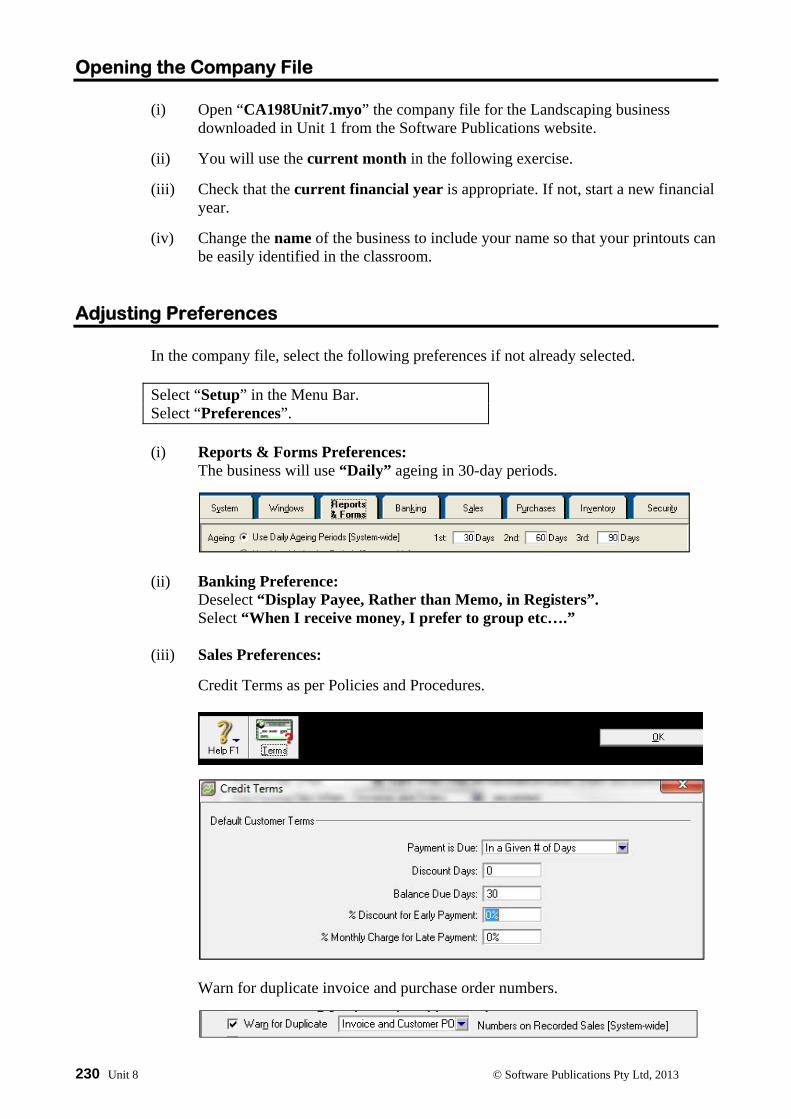

Opening the Company File

(i) Open “CA198Unit7.myo” the company file for the Landscaping business downloaded in Unit 1 from the Software Publications website.

(ii) You will use the current month in the following exercise.

(iii) Check that the current financial year is appropriate. If not, start a new financial year.

(iv) Change the name of the business to include your name so that your printouts can be easily identified in the classroom.

Adjusting Preferences

In the company file, select the following preferences if not already selected.

Select “Setup” in the Menu Bar. Select “Preferences”.

(i) Reports & Forms Preferences:

The business will use “Daily” ageing in 30-day periods.

(ii) Banking Preference: Deselect “Display Payee, Rather than Memo, in Registers”. Select “When I receive money, I prefer to group etc….”

(iii) Sales Preferences:

Credit Terms as per Policies and Procedures.

Warn for duplicate invoice and purchase order numbers.

© Software Publications Pty Ltd, 2013 Unit 8 231

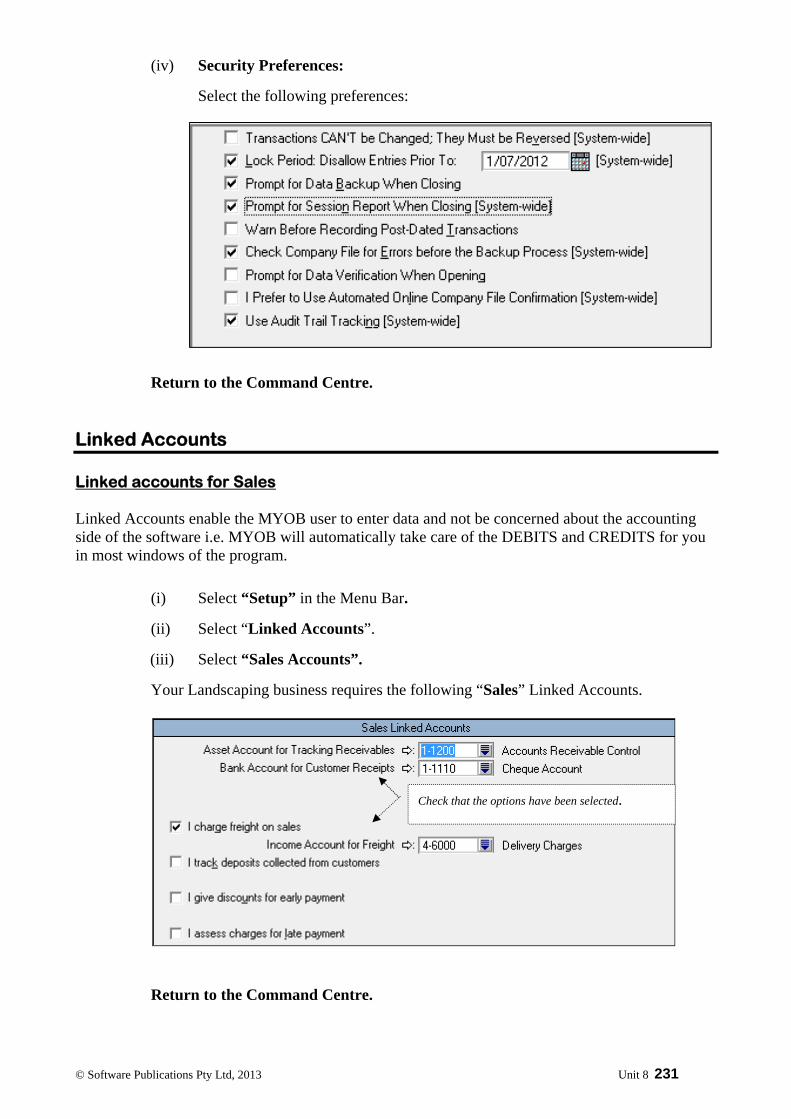

(iv) Security Preferences:

Select the following preferences:

Return to the Command Centre. Linked Accounts Linked accounts for Sales Linked Accounts enable the MYOB user to enter data and not be concerned about the accounting side of the software i.e. MYOB will automatically take care of the DEBITS and CREDITS for you in most windows of the program.

(i) Select “Setup” in the Menu Bar.

(ii) Select “Linked Accounts”.

(iii) Select “Sales Accounts”.

Your Landscaping business requires the following “Sales” Linked Accounts.

Return to the Command Centre.

Check that the options have been selected.

© Software Publications Pty Ltd, 2013 Unit 11 393

Completing the Activity Statement For information on preparing the Activity Statement, Google “NAT 7392”.

In this document, there is a list of what and what not to report at each field on the Activity Statement. [Extract printed below.] Report at G1 DO NOT report at G1 Total amounts for sales including: ■ goods or services you sell or supply ■ dividends you receive ■ sales of trading stock ■ donations and gifts you receive ■ the sale of business assets such as office equipment or ■ private sales not related to your business, for example, motor vehicles, including trade-ins selling your home or furniture from your home ■ the sale, lease or rental of land and buildings ■ salary and wages you receive ■ the provision of memberships ■ government pensions and allowances ■ earnings from financial supplies you make (for example, ■ amounts you receive from hobby activities interest from bank accounts or for lending money but not ■ any trust and partnership distributions you receive including the loan principal) ■ tax refunds ■ the provision of goods or services in return for sponsorship■ receipts for services provided under a pay as you go

voluntary agreement unless made to a business that ■ goods and services provided in return for government is not fully entitled to claim GST credits for the services ■ business loans you receive ■ grants and certain private sector grants ■ the amount on the sale of a luxury car representing the ■ cancelled lay-by sales luxury car tax paid or payable by you ■ forfeited customer security deposits ■ taxes, fees and charges you have received that don’t ■ employee contributions for fringe benefits you have include GST, and provided ■ amounts received for sales not connected with Australia, ■ the sale of property of a debtor in order to satisfy a debt unless a special rule makes the sales taxable, GST-free, owed to you by the debtor, if the debtor otherwise would or input taxed. have had to pay GST on the sale ■ creating, granting, transferring, assigning or surrendering a right (for example, royalties received) ■ entry into, or release from, an obligation to – do anything – refrain from an act, or – tolerate an act or situation (for example, agreeing, as part of the sale of your business, not to operate a similar business within a certain area) ■ the GST-inclusive market value of goods and services or other things that you receive in barter transactions, and ■ the GST-inclusive market value of anything you supply to your associate for no payment or sell to your associate for less than the GST-inclusive market value if: – your associate is not registered, or required to be registered, for GST – your associate has not received the thing either partly or wholly for their business – the thing received by your associate relates partly or wholly to making sales that would be input taxed, or – the thing supplied is partly or wholly of a private or domestic nature.

394 Unit 11 © Software Publications Pty Ltd, 2013

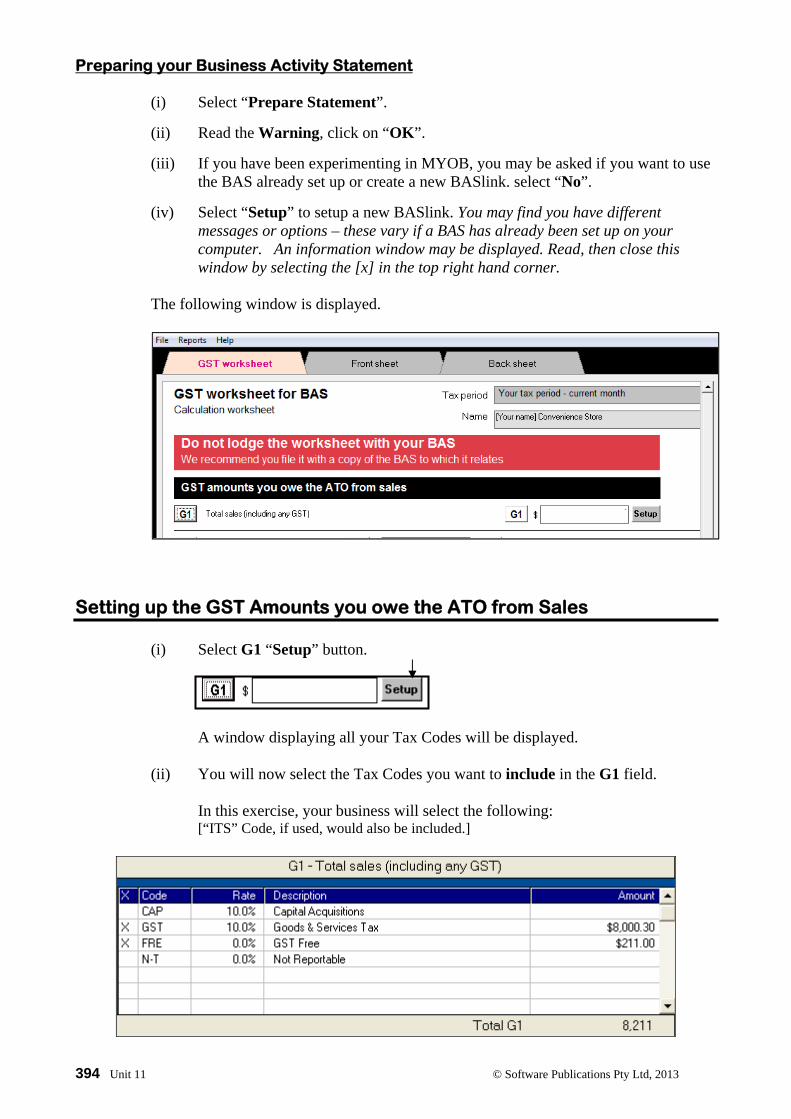

Preparing your Business Activity Statement

(i) Select “Prepare Statement”.

(ii) Read the Warning, click on “OK”.

(iii) If you have been experimenting in MYOB, you may be asked if you want to use the BAS already set up or create a new BASlink. select “No”.

(iv) Select “Setup” to setup a new BASlink. You may find you have different messages or options – these vary if a BAS has already been set up on your computer. An information window may be displayed. Read, then close this window by selecting the [x] in the top right hand corner.

The following window is displayed.

Setting up the GST Amounts you owe the ATO from Sales (i) Select G1 “Setup” button.

A window displaying all your Tax Codes will be displayed.

(ii) You will now select the Tax Codes you want to include in the G1 field.

In this exercise, your business will select the following: [“ITS” Code, if used, would also be included.]

© Software Publications Pty Ltd, 2013 Unit 11 395

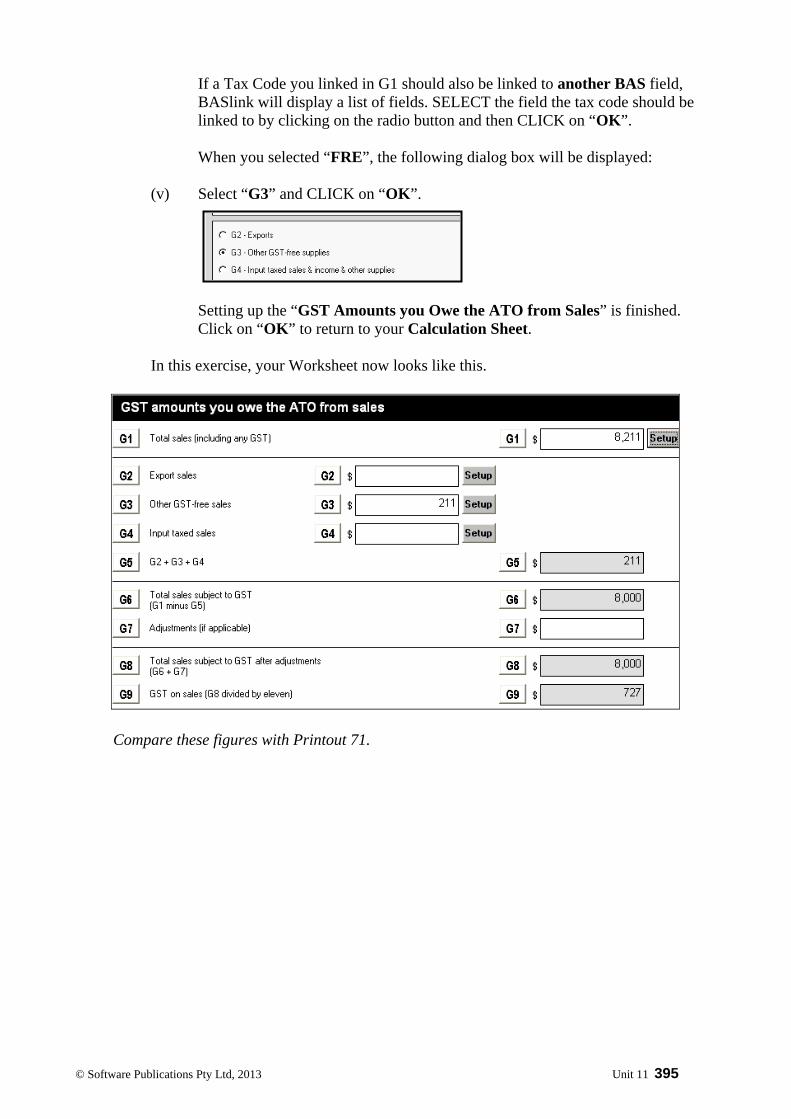

If a Tax Code you linked in G1 should also be linked to another BAS field,

BASlink will display a list of fields. SELECT the field the tax code should be linked to by clicking on the radio button and then CLICK on “OK”.

When you selected “FRE”, the following dialog box will be displayed: (v) Select “G3” and CLICK on “OK”.

Setting up the “GST Amounts you Owe the ATO from Sales” is finished. Click on “OK” to return to your Calculation Sheet. In this exercise, your Worksheet now looks like this.

Compare these figures with Printout 71.

BSB Supplement 405

BSB Business Services Training Package

Supplement This workbook can be used by learners completing a qualification in the BSB Business Services Training Package.

406 BSB Supplement

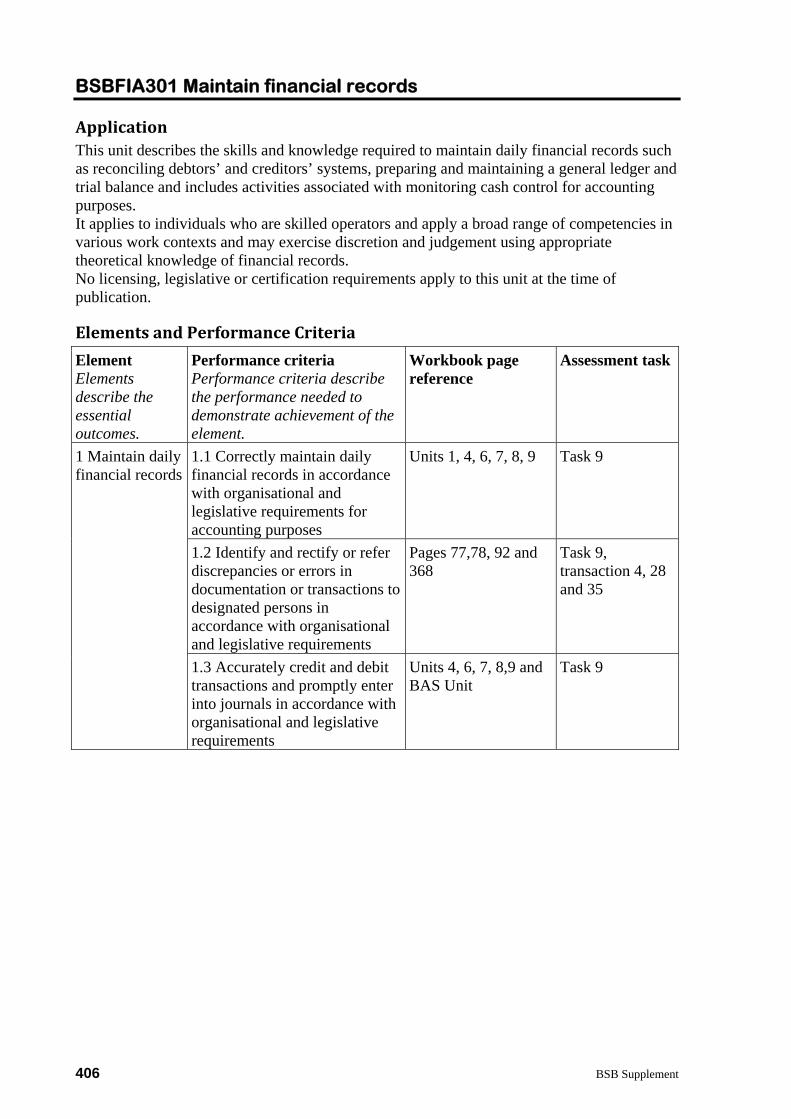

BSBFIA301 Maintain financial records

Application This unit describes the skills and knowledge required to maintain daily financial records such as reconciling debtors’ and creditors’ systems, preparing and maintaining a general ledger and trial balance and includes activities associated with monitoring cash control for accounting purposes. It applies to individuals who are skilled operators and apply a broad range of competencies in various work contexts and may exercise discretion and judgement using appropriate theoretical knowledge of financial records. No licensing, legislative or certification requirements apply to this unit at the time of publication.

Elements and Performance Criteria Element Elements describe the essential outcomes.

Performance criteria Performance criteria describe the performance needed to demonstrate achievement of the element.

Workbook page reference

Assessment task

1 Maintain daily financial records

1.1 Correctly maintain daily financial records in accordance with organisational and legislative requirements for accounting purposes

Units 1, 4, 6, 7, 8, 9 Task 9

1.2 Identify and rectify or refer discrepancies or errors in documentation or transactions to designated persons in accordance with organisational and legislative requirements

Pages 77,78, 92 and 368

Task 9, transaction 4, 28 and 35

1.3 Accurately credit and debit transactions and promptly enter into journals in accordance with organisational and legislative requirements

Units 4, 6, 7, 8,9 and BAS Unit

Task 9

BSB Supplement 407

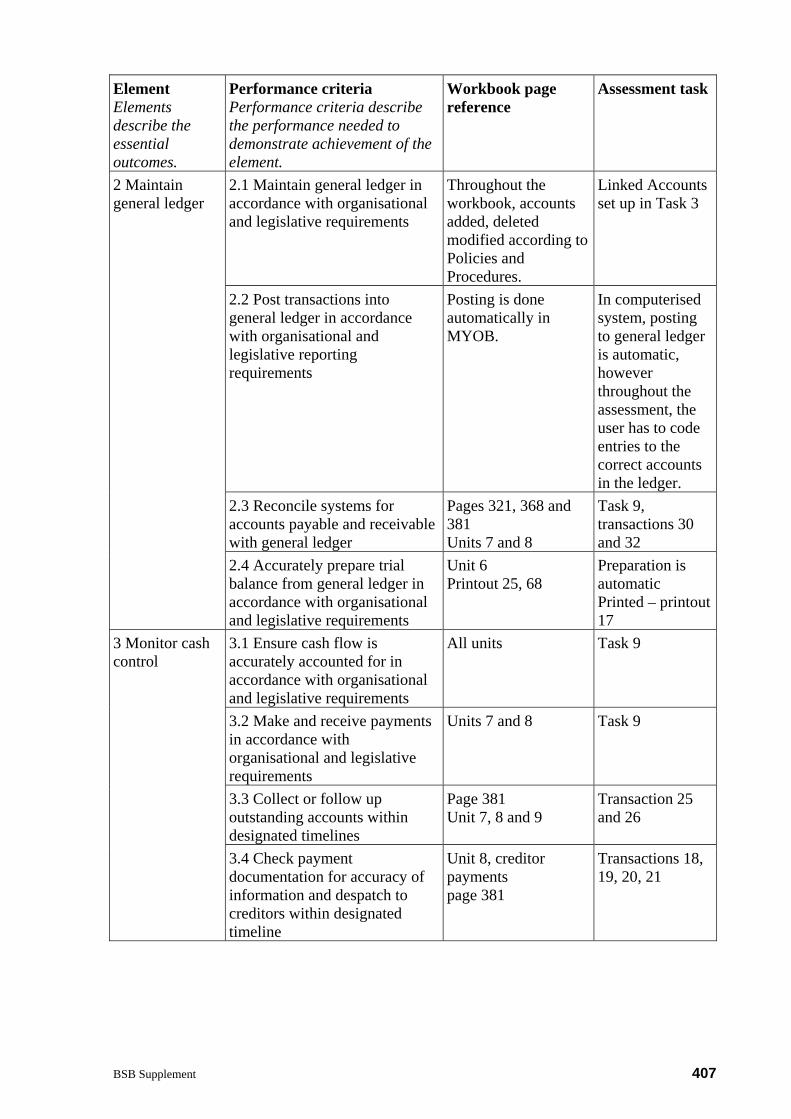

Element Elements describe the essential outcomes.

Performance criteria Performance criteria describe the performance needed to demonstrate achievement of the element.

Workbook page reference

Assessment task

2 Maintain general ledger

2.1 Maintain general ledger in accordance with organisational and legislative requirements

Throughout the workbook, accounts added, deleted modified according to Policies and Procedures.

Linked Accounts set up in Task 3

2.2 Post transactions into general ledger in accordance with organisational and legislative reporting requirements

Posting is done automatically in MYOB.

In computerised system, posting to general ledger is automatic, however throughout the assessment, the user has to code entries to the correct accounts in the ledger.

2.3 Reconcile systems for accounts payable and receivable with general ledger

Pages 321, 368 and 381 Units 7 and 8

Task 9, transactions 30 and 32

2.4 Accurately prepare trial balance from general ledger in accordance with organisational and legislative requirements

Unit 6 Printout 25, 68

Preparation is automatic Printed – printout 17

3 Monitor cash control

3.1 Ensure cash flow is accurately accounted for in accordance with organisational and legislative requirements

All units Task 9

3.2 Make and receive payments in accordance with organisational and legislative requirements

Units 7 and 8 Task 9

3.3 Collect or follow up outstanding accounts within designated timelines

Page 381 Unit 7, 8 and 9

Transaction 25 and 26

3.4 Check payment documentation for accuracy of information and despatch to creditors within designated timeline

Unit 8, creditor payments page 381

Transactions 18, 19, 20, 21

408 BSB Supplement

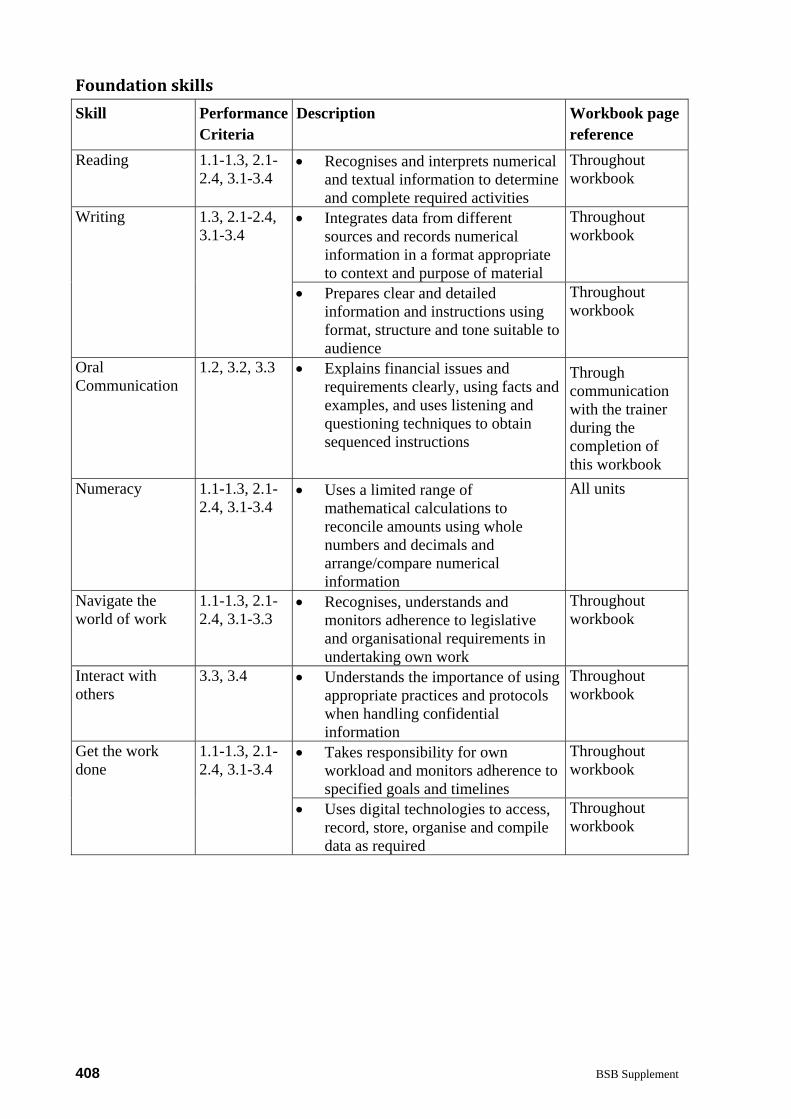

Foundation skills Skill Performance

Criteria Description Workbook page

reference Reading 1.1-1.3, 2.1-

2.4, 3.1-3.4 Recognises and interprets numerical

and textual information to determine and complete required activities

Throughout workbook

Writing 1.3, 2.1-2.4, 3.1-3.4

Integrates data from different sources and records numerical information in a format appropriate to context and purpose of material

Throughout workbook

Prepares clear and detailed information and instructions using format, structure and tone suitable to audience

Throughout workbook

Oral Communication

1.2, 3.2, 3.3 Explains financial issues and requirements clearly, using facts and examples, and uses listening and questioning techniques to obtain sequenced instructions

Through communication with the trainer during the completion of this workbook

Numeracy 1.1-1.3, 2.1-2.4, 3.1-3.4

Uses a limited range of mathematical calculations to reconcile amounts using whole numbers and decimals and arrange/compare numerical information

All units

Navigate the world of work

1.1-1.3, 2.1-2.4, 3.1-3.3

Recognises, understands and monitors adherence to legislative and organisational requirements in undertaking own work

Throughout workbook

Interact with others

3.3, 3.4 Understands the importance of using appropriate practices and protocols when handling confidential information

Throughout workbook

Get the work done

1.1-1.3, 2.1-2.4, 3.1-3.4

Takes responsibility for own workload and monitors adherence to specified goals and timelines

Throughout workbook

Uses digital technologies to access, record, store, organise and compile data as required

Throughout workbook

BSB Supplement 409

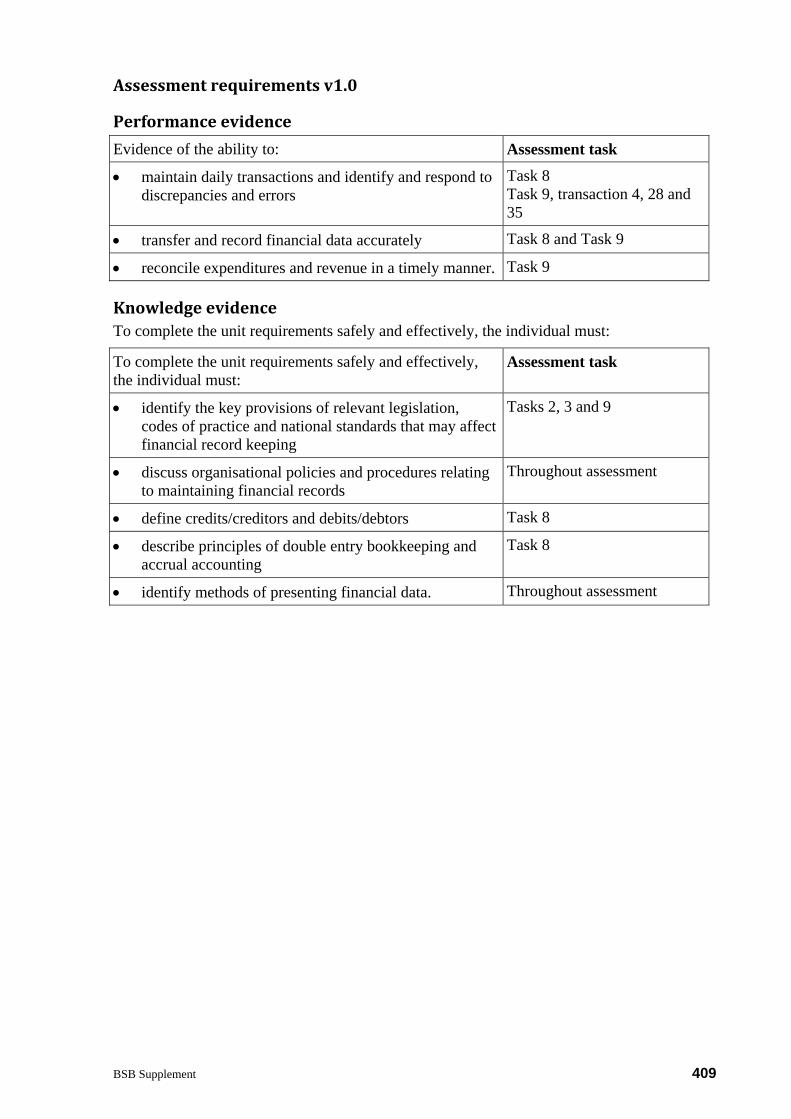

Assessment requirements v1.0

Performance evidence Evidence of the ability to: Assessment task

maintain daily transactions and identify and respond to discrepancies and errors

Task 8 Task 9, transaction 4, 28 and 35

transfer and record financial data accurately Task 8 and Task 9

reconcile expenditures and revenue in a timely manner. Task 9

Knowledge evidence To complete the unit requirements safely and effectively, the individual must:

To complete the unit requirements safely and effectively, the individual must:

Assessment task

identify the key provisions of relevant legislation, codes of practice and national standards that may affect financial record keeping

Tasks 2, 3 and 9

discuss organisational policies and procedures relating to maintaining financial records

Throughout assessment

define credits/creditors and debits/debtors Task 8

describe principles of double entry bookkeeping and accrual accounting

Task 8

identify methods of presenting financial data. Throughout assessment

410 BSB Supplement

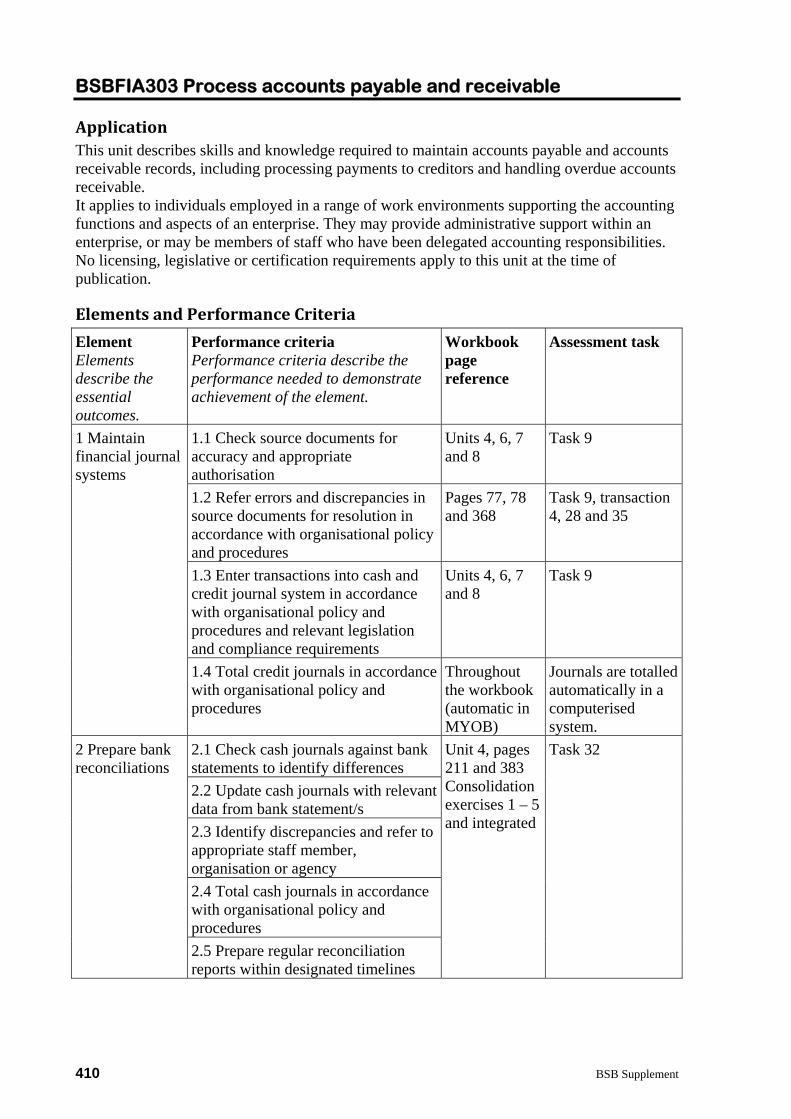

BSBFIA303 Process accounts payable and receivable

Application This unit describes skills and knowledge required to maintain accounts payable and accounts receivable records, including processing payments to creditors and handling overdue accounts receivable. It applies to individuals employed in a range of work environments supporting the accounting functions and aspects of an enterprise. They may provide administrative support within an enterprise, or may be members of staff who have been delegated accounting responsibilities. No licensing, legislative or certification requirements apply to this unit at the time of publication.

Elements and Performance Criteria Element Elements describe the essential outcomes.

Performance criteria Performance criteria describe the performance needed to demonstrate achievement of the element.

Workbook page reference

Assessment task

1 Maintain financial journal systems

1.1 Check source documents for accuracy and appropriate authorisation

Units 4, 6, 7 and 8

Task 9

1.2 Refer errors and discrepancies in source documents for resolution in accordance with organisational policy and procedures

Pages 77, 78 and 368

Task 9, transaction 4, 28 and 35

1.3 Enter transactions into cash and credit journal system in accordance with organisational policy and procedures and relevant legislation and compliance requirements

Units 4, 6, 7 and 8

Task 9

1.4 Total credit journals in accordance with organisational policy and procedures

Throughout the workbook (automatic in MYOB)

Journals are totalled automatically in a computerised system.

2 Prepare bank reconciliations

2.1 Check cash journals against bank statements to identify differences

Unit 4, pages 211 and 383 Consolidation exercises 1 – 5 and integrated

Task 32

2.2 Update cash journals with relevant data from bank statement/s 2.3 Identify discrepancies and refer to appropriate staff member, organisation or agency 2.4 Total cash journals in accordance with organisational policy and procedures 2.5 Prepare regular reconciliation reports within designated timelines

BSB Supplement 411

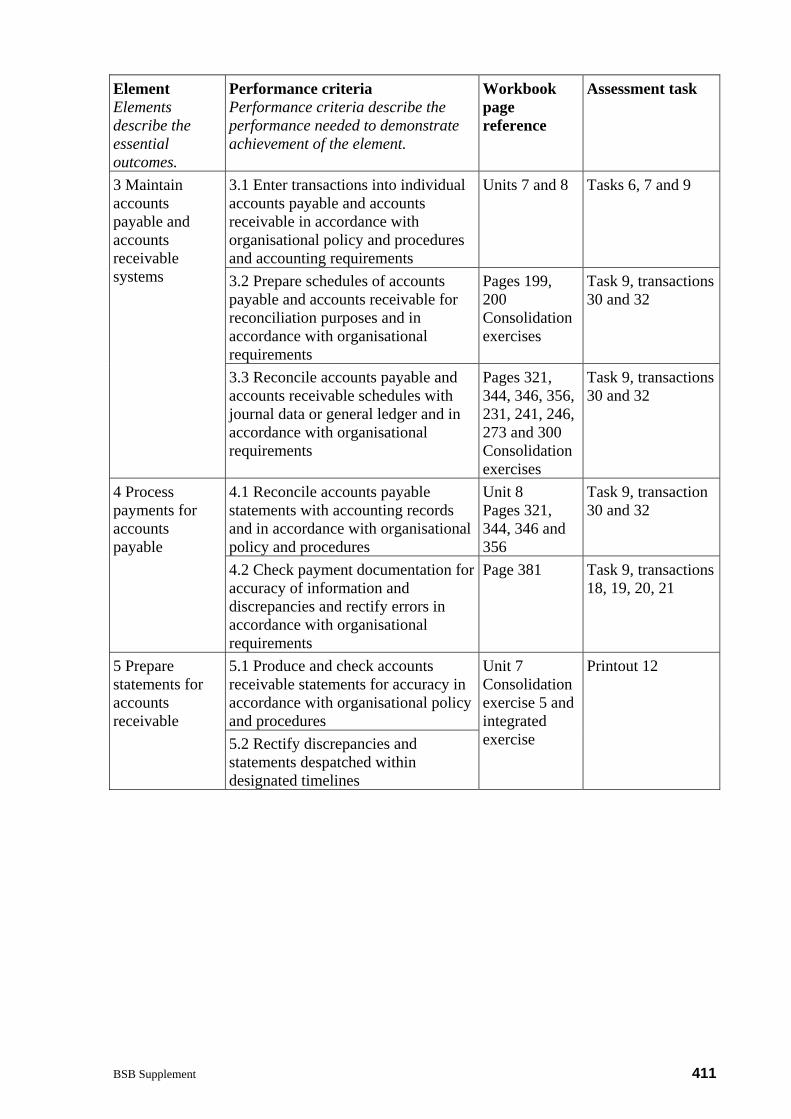

Element Elements describe the essential outcomes.

Performance criteria Performance criteria describe the performance needed to demonstrate achievement of the element.

Workbook page reference

Assessment task

3 Maintain accounts payable and accounts receivable systems

3.1 Enter transactions into individual accounts payable and accounts receivable in accordance with organisational policy and procedures and accounting requirements

Units 7 and 8 Tasks 6, 7 and 9

3.2 Prepare schedules of accounts payable and accounts receivable for reconciliation purposes and in accordance with organisational requirements

Pages 199, 200 Consolidation exercises

Task 9, transactions 30 and 32

3.3 Reconcile accounts payable and accounts receivable schedules with journal data or general ledger and in accordance with organisational requirements

Pages 321, 344, 346, 356, 231, 241, 246, 273 and 300 Consolidation exercises

Task 9, transactions 30 and 32

4 Process payments for accounts payable

4.1 Reconcile accounts payable statements with accounting records and in accordance with organisational policy and procedures

Unit 8 Pages 321, 344, 346 and 356

Task 9, transaction 30 and 32

4.2 Check payment documentation for accuracy of information and discrepancies and rectify errors in accordance with organisational requirements

Page 381 Task 9, transactions 18, 19, 20, 21

5 Prepare statements for accounts receivable

5.1 Produce and check accounts receivable statements for accuracy in accordance with organisational policy and procedures

Unit 7 Consolidation exercise 5 and integrated exercise

Printout 12

5.2 Rectify discrepancies and statements despatched within designated timelines

412 BSB Supplement

Element Elements describe the essential outcomes.

Performance criteria Performance criteria describe the performance needed to demonstrate achievement of the element.

Workbook page reference

Assessment task

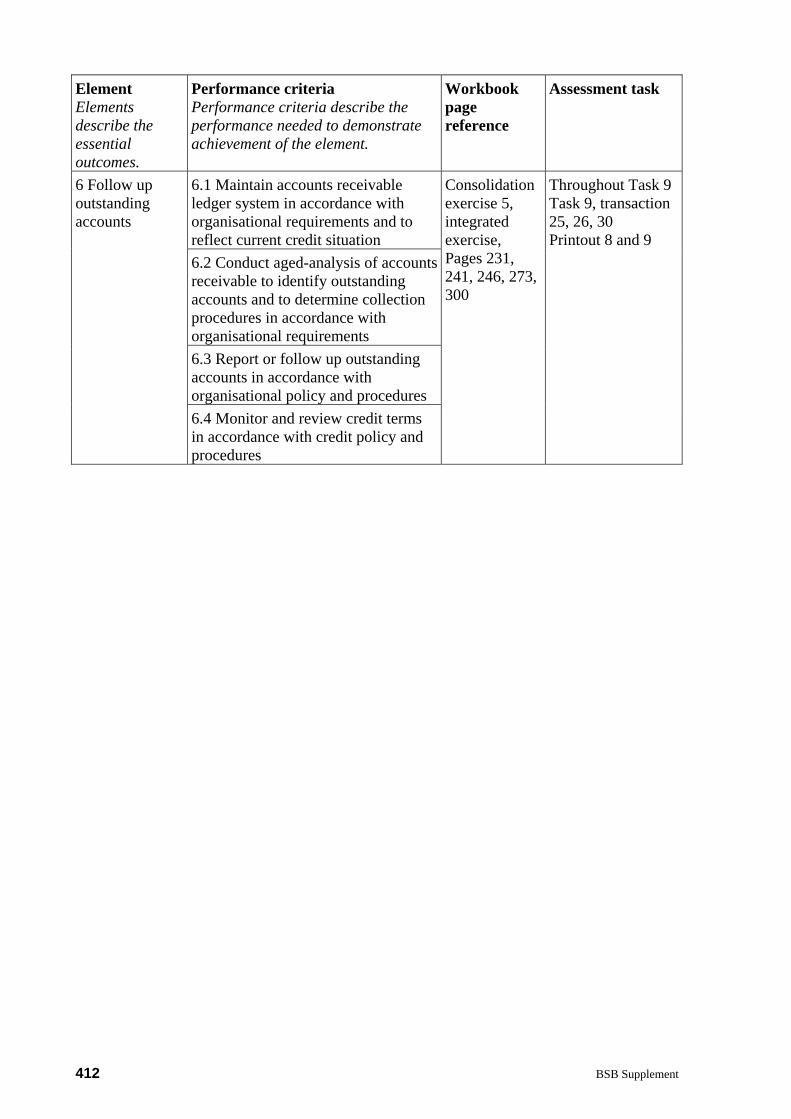

6 Follow up outstanding accounts

6.1 Maintain accounts receivable ledger system in accordance with organisational requirements and to reflect current credit situation

Consolidation exercise 5, integrated exercise, Pages 231, 241, 246, 273, 300

Throughout Task 9 Task 9, transaction 25, 26, 30 Printout 8 and 9

6.2 Conduct aged-analysis of accounts receivable to identify outstanding accounts and to determine collection procedures in accordance with organisational requirements 6.3 Report or follow up outstanding accounts in accordance with organisational policy and procedures 6.4 Monitor and review credit terms in accordance with credit policy and procedures

BSB Supplement 413

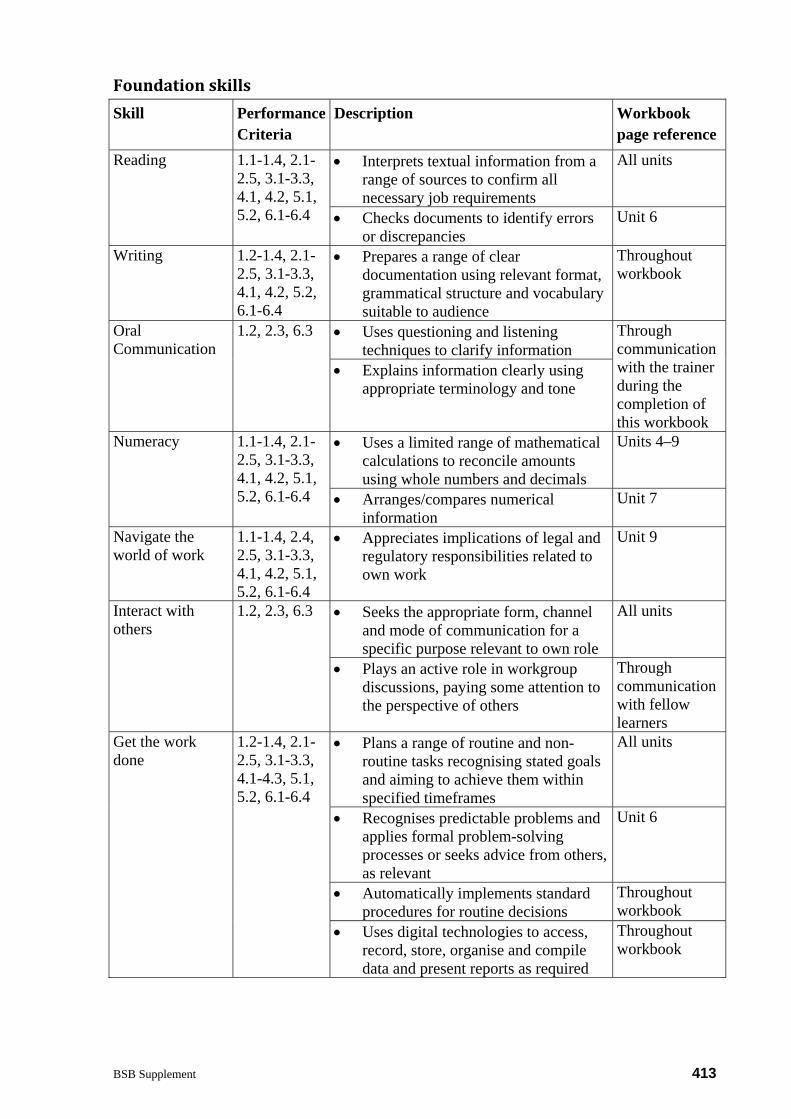

Foundation skills Skill Performance

Criteria Description Workbook

page reference Reading 1.1-1.4, 2.1-

2.5, 3.1-3.3, 4.1, 4.2, 5.1, 5.2, 6.1-6.4

Interprets textual information from a range of sources to confirm all necessary job requirements

All units

Checks documents to identify errors or discrepancies

Unit 6

Writing 1.2-1.4, 2.1-2.5, 3.1-3.3, 4.1, 4.2, 5.2, 6.1-6.4

Prepares a range of clear documentation using relevant format, grammatical structure and vocabulary suitable to audience

Throughout workbook

Oral Communication

1.2, 2.3, 6.3 Uses questioning and listening techniques to clarify information

Through communication with the trainer during the completion of this workbook

Explains information clearly using appropriate terminology and tone

Numeracy 1.1-1.4, 2.1-2.5, 3.1-3.3, 4.1, 4.2, 5.1, 5.2, 6.1-6.4

Uses a limited range of mathematical calculations to reconcile amounts using whole numbers and decimals

Units 4–9

Arranges/compares numerical information

Unit 7

Navigate the world of work

1.1-1.4, 2.4, 2.5, 3.1-3.3, 4.1, 4.2, 5.1, 5.2, 6.1-6.4

Appreciates implications of legal and regulatory responsibilities related to own work

Unit 9

Interact with others

1.2, 2.3, 6.3 Seeks the appropriate form, channel and mode of communication for a specific purpose relevant to own role

All units

Plays an active role in workgroup discussions, paying some attention to the perspective of others

Through communication with fellow learners

Get the work done

1.2-1.4, 2.1-2.5, 3.1-3.3, 4.1-4.3, 5.1, 5.2, 6.1-6.4

Plans a range of routine and non-routine tasks recognising stated goals and aiming to achieve them within specified timeframes

All units

Recognises predictable problems and applies formal problem-solving processes or seeks advice from others, as relevant

Unit 6

Automatically implements standard procedures for routine decisions

Throughout workbook

Uses digital technologies to access, record, store, organise and compile data and present reports as required

Throughout workbook

414 BSB Supplement

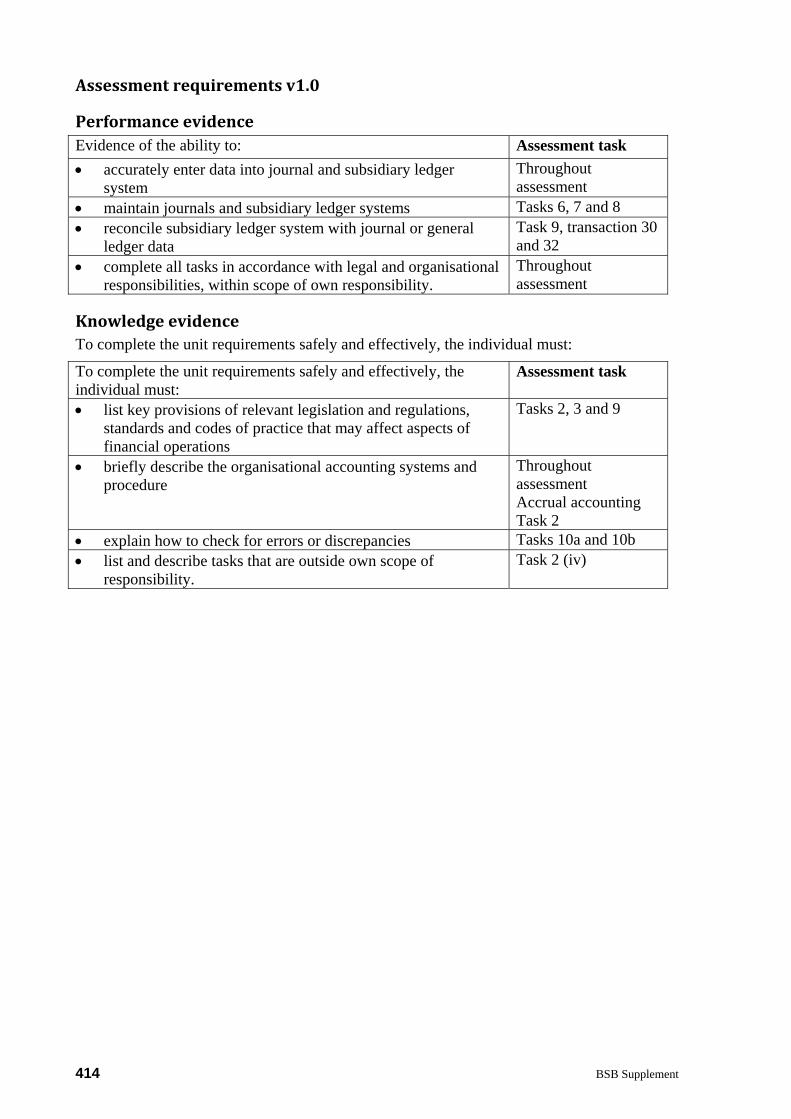

Assessment requirements v1.0

Performance evidence Evidence of the ability to: Assessment task accurately enter data into journal and subsidiary ledger

system Throughout assessment

maintain journals and subsidiary ledger systems Tasks 6, 7 and 8 reconcile subsidiary ledger system with journal or general

ledger data Task 9, transaction 30 and 32

complete all tasks in accordance with legal and organisational responsibilities, within scope of own responsibility.

Throughout assessment

Knowledge evidence To complete the unit requirements safely and effectively, the individual must:

To complete the unit requirements safely and effectively, the individual must:

Assessment task

list key provisions of relevant legislation and regulations, standards and codes of practice that may affect aspects of financial operations

Tasks 2, 3 and 9

briefly describe the organisational accounting systems and procedure

Throughout assessment Accrual accounting Task 2

explain how to check for errors or discrepancies Tasks 10a and 10b list and describe tasks that are outside own scope of

responsibility. Task 2 (iv)

BSB Supplement 415

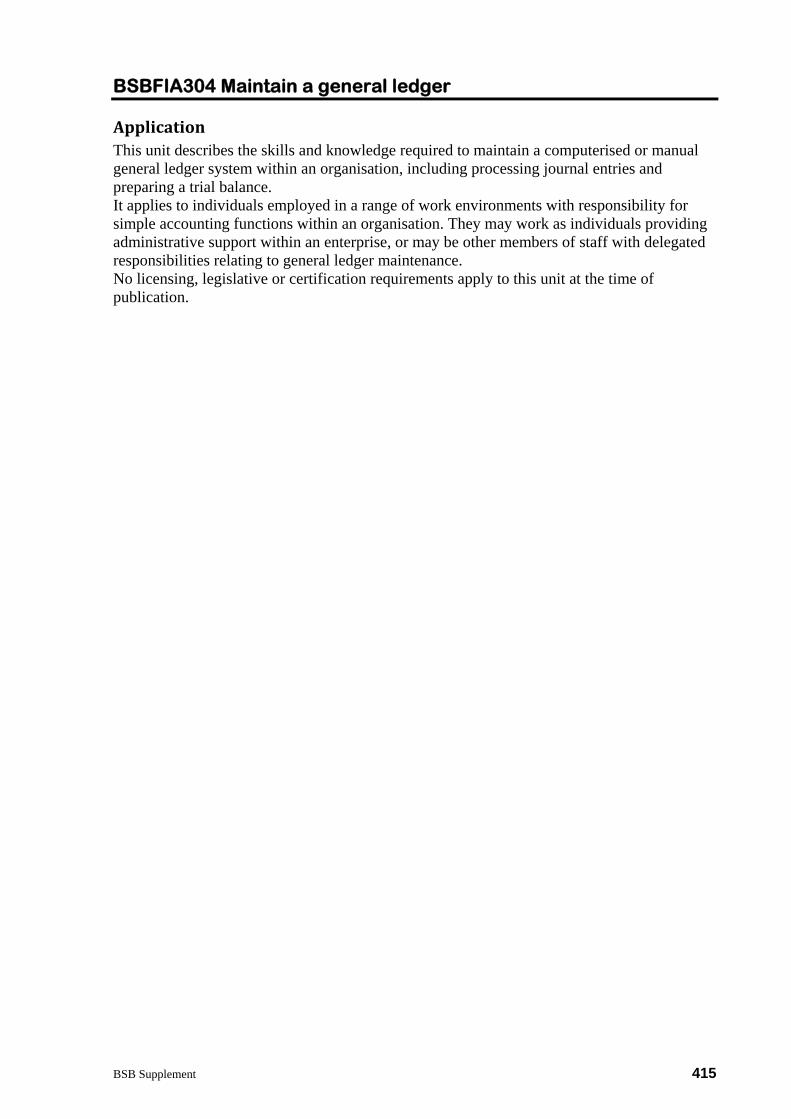

BSBFIA304 Maintain a general ledger

Application This unit describes the skills and knowledge required to maintain a computerised or manual general ledger system within an organisation, including processing journal entries and preparing a trial balance. It applies to individuals employed in a range of work environments with responsibility for simple accounting functions within an organisation. They may work as individuals providing administrative support within an enterprise, or may be other members of staff with delegated responsibilities relating to general ledger maintenance. No licensing, legislative or certification requirements apply to this unit at the time of publication.

416 BSB Supplement

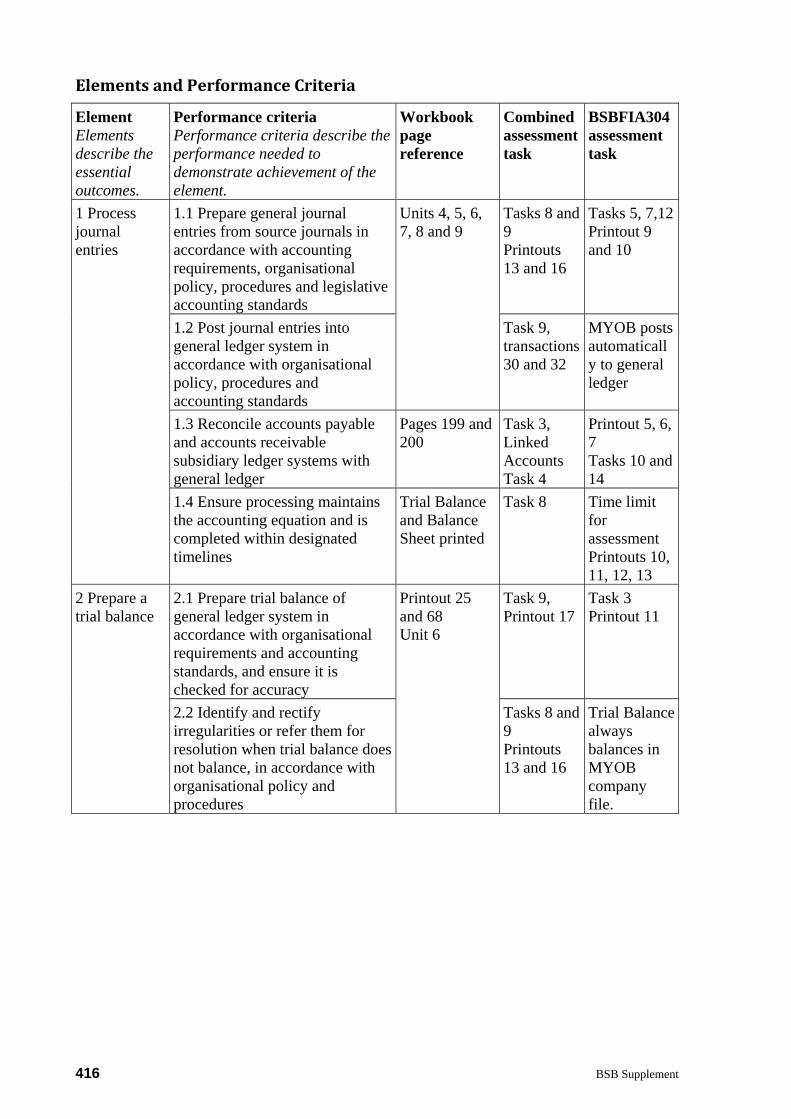

Elements and Performance Criteria

Element Elements describe the essential outcomes.

Performance criteria Performance criteria describe the performance needed to demonstrate achievement of the element.

Workbook page reference

Combined assessment task

BSBFIA304 assessment task

1 Process journal entries

1.1 Prepare general journal entries from source journals in accordance with accounting requirements, organisational policy, procedures and legislative accounting standards

Units 4, 5, 6, 7, 8 and 9

Tasks 8 and 9 Printouts 13 and 16

Tasks 5, 7,12Printout 9 and 10

1.2 Post journal entries into general ledger system in accordance with organisational policy, procedures and accounting standards

Task 9, transactions 30 and 32

MYOB posts automatically to general ledger

1.3 Reconcile accounts payable and accounts receivable subsidiary ledger systems with general ledger

Pages 199 and 200

Task 3, Linked Accounts Task 4

Printout 5, 6, 7 Tasks 10 and 14

1.4 Ensure processing maintains the accounting equation and is completed within designated timelines

Trial Balance and Balance Sheet printed

Task 8 Time limit for assessment Printouts 10, 11, 12, 13

2 Prepare a trial balance

2.1 Prepare trial balance of general ledger system in accordance with organisational requirements and accounting standards, and ensure it is checked for accuracy

Printout 25 and 68 Unit 6

Task 9, Printout 17

Task 3 Printout 11

2.2 Identify and rectify irregularities or refer them for resolution when trial balance does not balance, in accordance with organisational policy and procedures

Tasks 8 and 9 Printouts 13 and 16

Trial Balance always balances in MYOB company file.

BSB Supplement 417

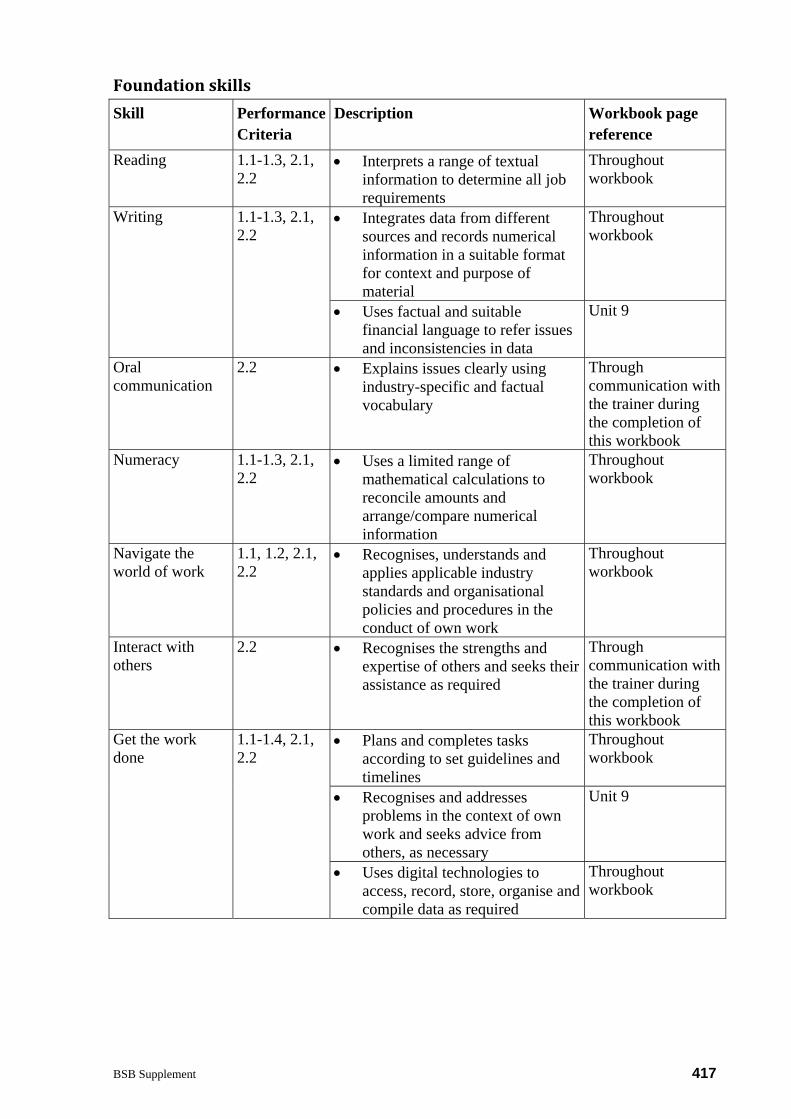

Foundation skills Skill Performance

Criteria Description Workbook page

reference Reading 1.1-1.3, 2.1,

2.2 Interprets a range of textual

information to determine all job requirements

Throughout workbook

Writing 1.1-1.3, 2.1, 2.2

Integrates data from different sources and records numerical information in a suitable format for context and purpose of material

Throughout workbook

Uses factual and suitable financial language to refer issues and inconsistencies in data

Unit 9

Oral communication

2.2 Explains issues clearly using industry-specific and factual vocabulary

Through communication with the trainer during the completion of this workbook

Numeracy 1.1-1.3, 2.1, 2.2

Uses a limited range of mathematical calculations to reconcile amounts and arrange/compare numerical information

Throughout workbook

Navigate the world of work

1.1, 1.2, 2.1, 2.2

Recognises, understands and applies applicable industry standards and organisational policies and procedures in the conduct of own work

Throughout workbook

Interact with others

2.2 Recognises the strengths and expertise of others and seeks their assistance as required

Through communication with the trainer during the completion of this workbook

Get the work done

1.1-1.4, 2.1, 2.2

Plans and completes tasks according to set guidelines and timelines

Throughout workbook

Recognises and addresses problems in the context of own work and seeks advice from others, as necessary

Unit 9

Uses digital technologies to access, record, store, organise and compile data as required

Throughout workbook

418 BSB Supplement

Assessment requirements v1.0

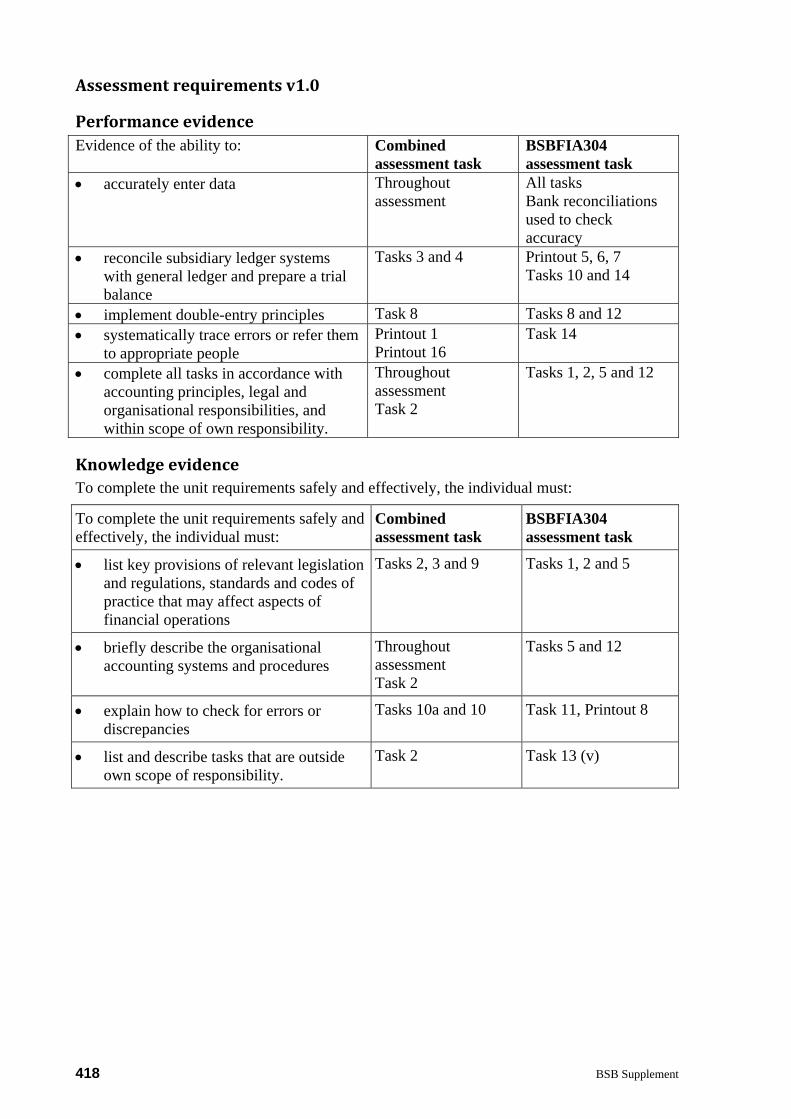

Performance evidence Evidence of the ability to: Combined

assessment task BSBFIA304 assessment task

accurately enter data Throughout assessment

All tasks Bank reconciliations used to check accuracy

reconcile subsidiary ledger systems with general ledger and prepare a trial balance

Tasks 3 and 4 Printout 5, 6, 7 Tasks 10 and 14

implement double-entry principles Task 8 Tasks 8 and 12 systematically trace errors or refer them

to appropriate people Printout 1 Printout 16

Task 14

complete all tasks in accordance with accounting principles, legal and organisational responsibilities, and within scope of own responsibility.

Throughout assessment Task 2

Tasks 1, 2, 5 and 12

Knowledge evidence To complete the unit requirements safely and effectively, the individual must:

To complete the unit requirements safely and effectively, the individual must:

Combined assessment task

BSBFIA304 assessment task

list key provisions of relevant legislation and regulations, standards and codes of practice that may affect aspects of financial operations

Tasks 2, 3 and 9 Tasks 1, 2 and 5

briefly describe the organisational accounting systems and procedures

Throughout assessment Task 2

Tasks 5 and 12

explain how to check for errors or discrepancies

Tasks 10a and 10 Task 11, Printout 8

list and describe tasks that are outside own scope of responsibility.

Task 2 Task 13 (v)