Embed Size (px)

Citation preview

Caroline)Baier JensenEmma)Caroline) Jaksland

Madelon)K.)Grandjean)PoulsenMikkel Holst)Schou Hansen

Marc)Faarborg Toft

Columbia)Business)SchoolTurnaround)ManagementFinal)ProjectProfessor)Doug)SquasoniDecember)15,)2017

Competing for Survival: A Turnaround of Department Store J.C. Penney

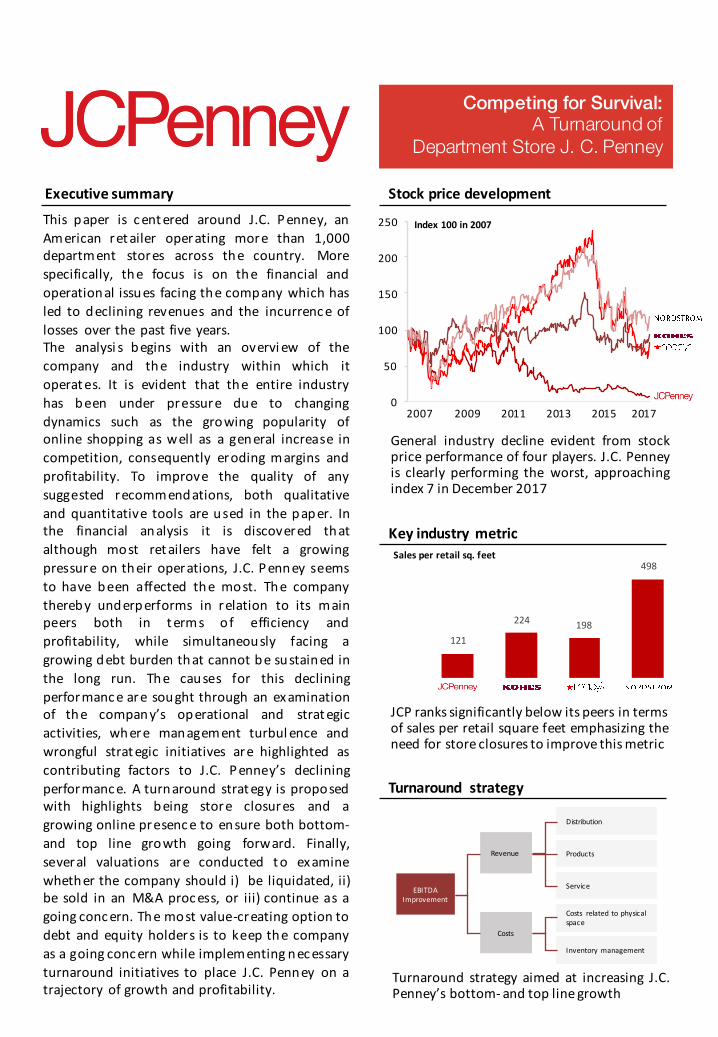

Key)industry)metric)

EBITDA)Improvement

Costs

Costs) related) to)physical)space

Inventory)management

Revenue

Distribution

Service

Products

Turnaround) strategy

Turnaround strategy aimed at increasing J.C.Penney’s bottomQ and top linegrowth

121)

224) 198

498)Sales)per)retail)sq.)feet

JCP ranks significantly below its peers in termsof sales per retail square feet emphasizing theneed for store closures to improve thismetric

0

50

100

150

200

250

Stock)price)development

Competing for Survival: A Turnaround of

Department Store J. C. Penney

This paper is centered around J.C. Penney, anAmerican retailer operating more than 1,000department stores across the country. Morespecifically, the focus is on the financial andoperational issues facing the company which hasled to declining revenues and the incurrence oflosses over the past five years.The analysi s begins with an overvi ew of thecompany and the industry within which itoperates. It is evident that the entire industryhas been under pressure due to changingdynamics such as the growing popularity ofonline shopping as well as a general increase incompetition, consequently eroding margins andprofitability. To improve the quality of anysuggested recommendations, both qualitativeand quantitative tools are used in the paper. Inthe financial analysis it is discovered thatalthough most retailers have felt a growingpressure on their operations, J.C. Penney seemsto have been affected the most. The companythereby underperforms in relation to its mainpeers both in terms of efficiency andprofitability, while simultaneously facing agrowing debt burden that cannot be sustained inthe long run. The causes for this decliningperformance are sought through an examinationof the company’s operational and strategicactivities, where management turbul ence andwrongful strategic initiatives are highlighted ascontributing factors to J.C. Penney’s decliningperformance. A turnaround strategy is proposedwith highlights being store closures and agrowing online presence to ensure both bottomQand top line growth going forward. Finally,several valuations are conducted to examinewhether the company should i) be liquidated, ii)be sold in an M&A process, or iii) continue as agoing concern. The most valueQcreating option todebt and equity holders is to keep the companyas a going concern while implementing necessaryturnaround initiatives to place J.C. Penney on atrajectory of growth and profitability.

Executive)summary

2007))))))))2009))))))))2011))))))))2013))))))))2015))))))2017

General industry decline evident from stockprice performance of four players. J.C. Penneyis clearly performing the worst, approachingindex 7 in December 2017

Index)100)in)2007

TableofContents

1.Introduction............................................................................................................................1

2.CompanyOverview.................................................................................................................22.1KeyCompanyFacts.........................................................................................................................2

3.PeerComparison.....................................................................................................................33.1Non-FinancialPeerAnalysis............................................................................................................33.2FinancialComparison......................................................................................................................3

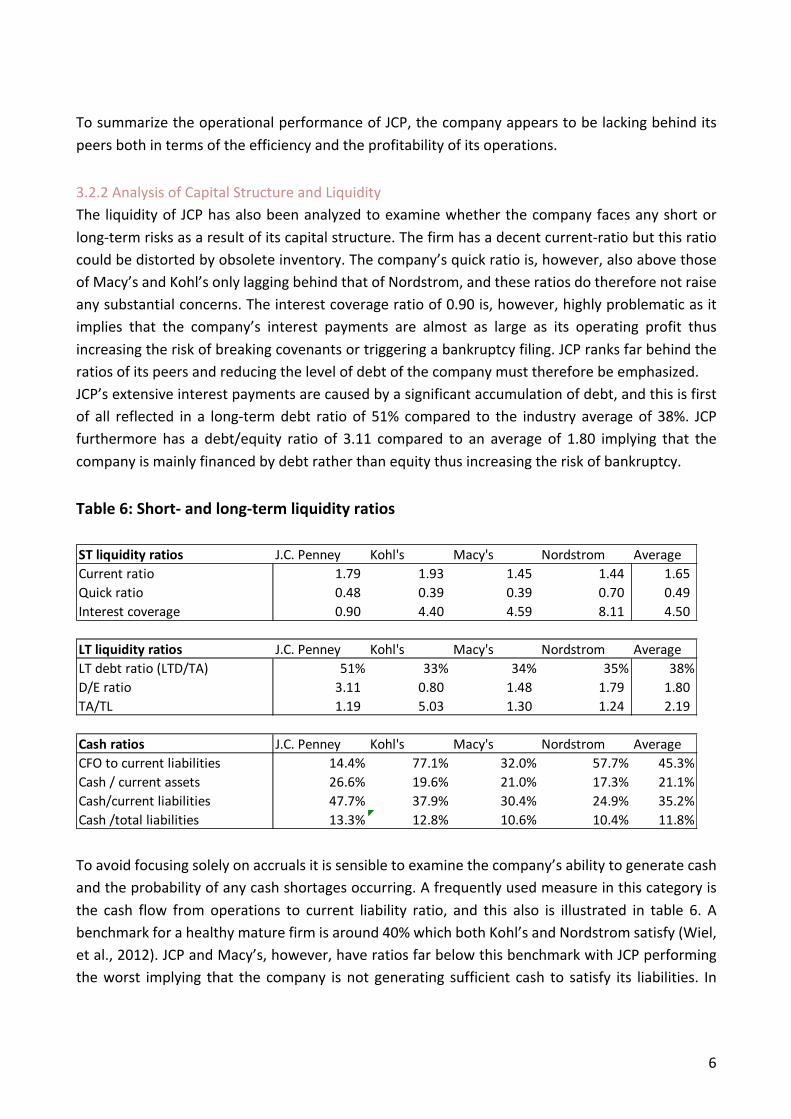

3.2.1OperationalAnalysis........................................................................................................................43.2.2AnalysisofCapitalStructureandLiquidity......................................................................................6

4.CausesofDecline.....................................................................................................................74.1ManagementFailure......................................................................................................................74.2CorporateGovernance....................................................................................................................94.3OrganizationalDistressCurve.......................................................................................................10

5.OptionsAvailableforJCPenney............................................................................................115.1Liquidation...................................................................................................................................11

5.1.1WaterfallAnalysis..........................................................................................................................125.2Chapter11Filing...........................................................................................................................135.3TurnaroundStrategy.....................................................................................................................14

5.3.1CorporateStrategy........................................................................................................................155.3.2OrganizationalArrangements........................................................................................................195.3.3FinancialChanges..........................................................................................................................20

5.4Valuation......................................................................................................................................215.4.1BaseCaseAssumptions.................................................................................................................215.4.2RestructuringAssumptions............................................................................................................225.4.3M&AAnalysis.................................................................................................................................24

6.Recommendation..................................................................................................................28

7.Conclusion.............................................................................................................................29

Bibliography..............................................................................................................................31

Exhibits.....................................................................................................................................35

1

1.IntroductionTheretaillandscapeisprojectedtochangemorewithinthenextfiveyearsthanithasdoneoverthepastcentury(MacKenzie,etal.,2013).Lookingnotonlyatdepartmentstores,butattheretailspaceingeneral,thefirstsevenmonthsof2017saw19bankruptcies,surpassingtherecordof18filingsduring2009(Thomas,2017).Someattributethedecliningperformanceofretailerstothegrowingimportanceofonlineshoppingwhileothersviewitasamarketcorrectionforthosechainsthatwerenotproperlyequippedtocompeteintheindustryintoday’scompetitiveenvironment.All,however,agreethattheconceptofadepartmentstoreasweknowit,isabouttochange(Cohen,2017).Thedepartmentstoreindustryhasbeenindeclineforthepastfiveyears,andthistrendisexpectedtocontinuewithrevenueprojectedtofallatarateof4%annuallyto$156.4billionin2017(Cohen,2017). Annual growth between 2017 and 2020 is furthermore expected to fall -2.6% (Statista,2017a).Cohen(2017)projectsthattheaverageindustryprofitmarginwillbe2.6%in2017,adeclineof1.4percentagepointsfrom2012.Inadditiontodecliningsales,brick-and-mortarstoresincurhighoperationalcost,relativetoonlinecompetitors,primarilyduetosalariesandretailspace.Trendsamong physical department stores are lower prices, higher frequency of promotions andmorefundsallocatedtomarketingandadvertising.Inthepastdecade,brick-and-mortarstoreshavefollowedthegrowthformulaofopeningstorestoacquireandservicemorecustomers(MacKenzie,etal.,2013).Thisgrowthstrategy,however,isnolongervalidasconsumerpurchasingdecisionshavechangeddramatically.Previously,acustomer’spurchasedecisionprocessstartedwithchoosingastoreandthenselectingaproductinthatstore.This is in linewith thedesignofdepartmentstores,whochoosebrands relevant to their targetcustomergroup.However,consumersnowresearchonlinebeforegoingtothestoresreducingtheneed for assistance in the shopping process. Customers are thereby taking charge of the initialscreeningofbrands,makingthevaluepropositionofdepartmentstoresobsoletetoacertainextent.Departmentstoresalsofacethechallengeofshiftingconsumerpreferences,asshoppersde-selecttraditional brands in favor of non-traditional, startup brands, which are rarely present in largedepartmentstores(Roeder&Rupp,2017).Inaddition,customersareusingtheirsmartphonestobenchmarkprices,getinputfromsocialmediaand friendsand family - andwhen theyare ready tobuy;numerousonline retailers createandincrease price transparency in themarket, to the detriment of physical stores (Baird, 2017). Inaddition,onlineretailersdeliverproductsdirectlytotheendconsumer,oftenwithinthesameday.Goingforward,fivetrendsareconsideredsignificantinwinningadominantpositionintheretailmarket, including demographic changes, multichannel and mobile commerce, personalized

2

marketing, the distribution revolution, and emerging retail businessmodels (MacKenzie, et al.,2013).All of the above elements present traditional department store retailers such as J.C. Penney(hereinafter, JCP)witha significant challenge.Majorplayers in the industry areKroger,Macy´s,Nordstrom, Kohl’s, and JCP, the latter being the subject of analysis in this paper. The followingsectionwillgiveanintroductiontoJCPandthechallengesitisfacingintheseturbulenttimesinachallengingindustry.

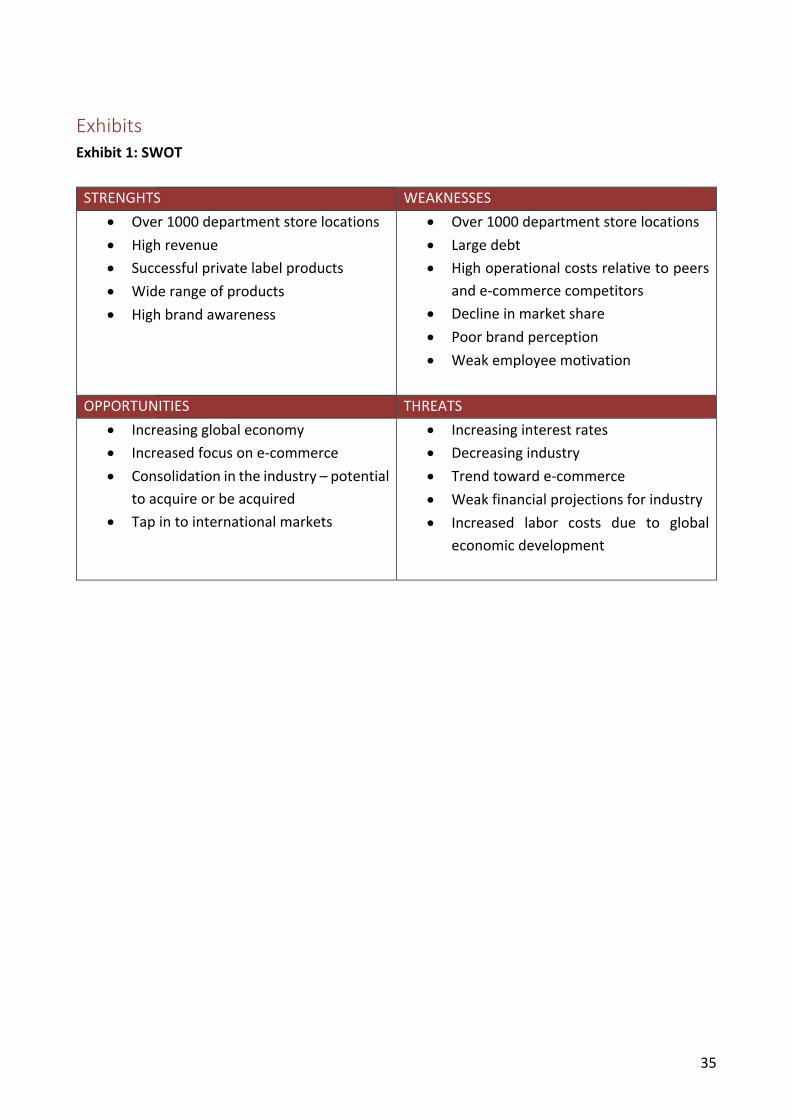

2.CompanyOverview2.1KeyCompanyFactsJamesCashPenneyandWilliamHenryMcManusfoundedJCPin1902,andithassincethenbecomeoneofthelargestdepartmentstorechainsintheUS,operating1,013locationsacrossthecountryandemploying106,000people.Currently,JCP’sheadquartersarelocatedinPlano,Texaswherethecompany is led by CEO Marvin Ellison. JCP targets low- and mid-income households sellingmerchandisewithinthefollowingsegments:clothing,cosmetics,electronics,footwear,furniture,housewares,jewelryandappliances.Asapartofarecentgrowthstrategy,thecompanyhasdividedkeyoperationsintothreepillarsi)beauty,ii)homerefresh,andiii)specialsizes.Thecompanyholdsbothnational-andprivate-labelbrands.Asof2016,private-labelbrandsaccountedfor44%ofsales(J.C.Penney10K,2016).Overthepastcoupleofyears,JCPhasexperiencedfinancialproblems.Priorto2011,thegrowthofJCPwasstagnatingfortwodecades,whichmadetheboardhireRonJohnsonfromAppleasthecompany’snewCEO.RonJohnsontriedtoimplementradicalchangesbygoingawayfromcoupons,salesanddiscounts,andmoretowardseveryday“fairandsquare”lowprices.However,thiswasnotreceivedwellbycustomers.After16months,withRonJohnsonasCEO,saleshaddeclinedmorethan25%,andthestockpricehaddecreasedbyalmost50%.This furtherresulted inaroundoflayoffs,with19,000peoplelosingtheirjobs.From2011to2015JCPexperiencedfivestraightlosingyears,whichamountedtoa$3.5bnlossintheperiod(Isidore,2017).Thecompanystillfacesseveralchallenges;revenueisdeclining,debtobligationsamounttonearly$3,6billion,andthecompanyhashighoperationalcostrelativetoe-commercecompetitorswhocontinuetowinmarketshare.Becauseofaliquidationofpoorlysellinginventory,especiallyintheappareldivision,andtheclosingof127oftheleastprofitablestores,JCPmanagedtogeneratea$1millionadjustedEBITDAin2016,whichisthefirstshadowofprofitabilityinsixyears.Thiswas,amongotherelements,aresultofthegrowingfocusonprivatelabels,allwithahighergrossmarginthanbrandsnotapartoftheJCPumbrella.This,combinedwiththecompany´shighbrandawarenessandalargeproductportfolio,poses opportunities for the organization going forward. For a complete list of strengths,weaknesses,opportunitiesandthreatscf.SWOT-analysisinExhibit1.

3

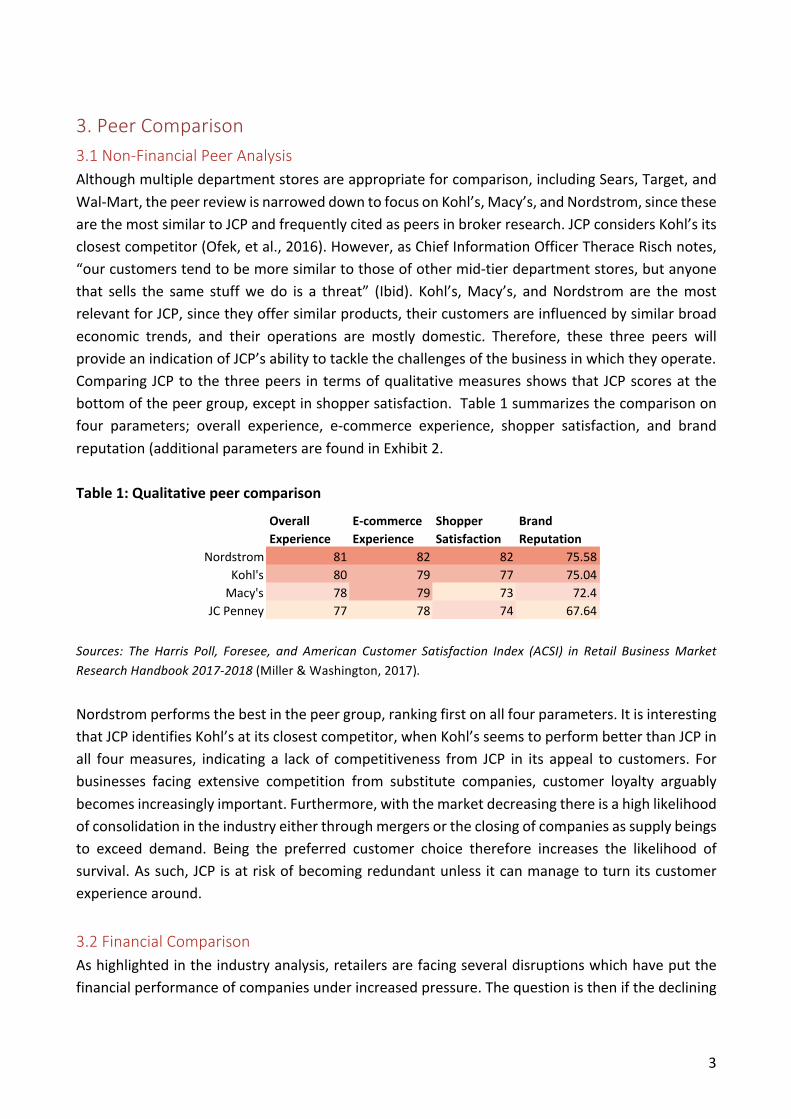

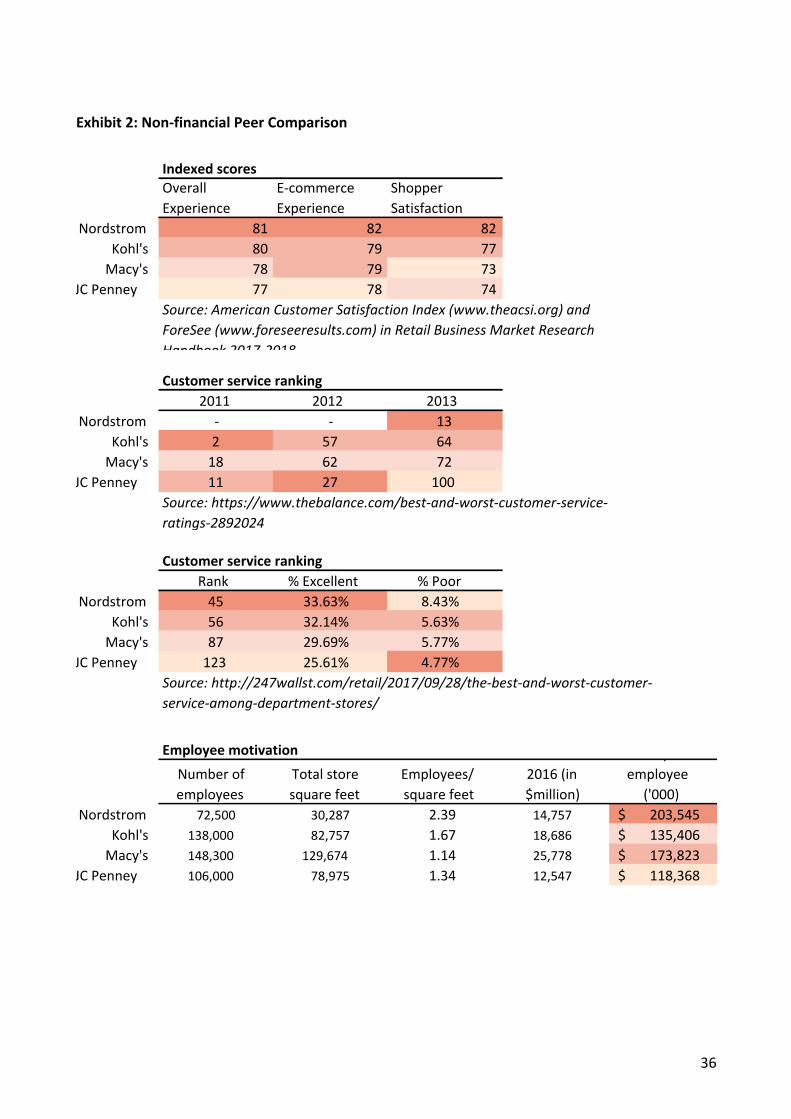

3.PeerComparison3.1Non-FinancialPeerAnalysisAlthoughmultipledepartmentstoresareappropriateforcomparison,includingSears,Target,andWal-Mart,thepeerreviewisnarroweddowntofocusonKohl’s,Macy’s,andNordstrom,sincethesearethemostsimilartoJCPandfrequentlycitedaspeersinbrokerresearch.JCPconsidersKohl’sitsclosestcompetitor(Ofek,etal.,2016).However,asChiefInformationOfficerTheraceRischnotes,“ourcustomerstendtobemoresimilartothoseofothermid-tierdepartmentstores,butanyonethat sells the same stuffwe do is a threat” (Ibid). Kohl’s,Macy’s, andNordstromare themostrelevantforJCP,sincetheyoffersimilarproducts,theircustomersareinfluencedbysimilarbroadeconomic trends, and their operations are mostly domestic. Therefore, these three peers willprovideanindicationofJCP’sabilitytotacklethechallengesofthebusinessinwhichtheyoperate.ComparingJCPtothethreepeers intermsofqualitativemeasuresshowsthatJCPscoresatthebottomofthepeergroup,exceptinshoppersatisfaction.Table1summarizesthecomparisononfour parameters; overall experience, e-commerce experience, shopper satisfaction, and brandreputation(additionalparametersarefoundinExhibit2.Table1:Qualitativepeercomparison

Sources: The Harris Poll, Foresee, and American Customer Satisfaction Index (ACSI) in Retail BusinessMarketResearchHandbook2017-2018(Miller&Washington,2017).Nordstromperformsthebestinthepeergroup,rankingfirstonallfourparameters.ItisinterestingthatJCPidentifiesKohl’satitsclosestcompetitor,whenKohl’sseemstoperformbetterthanJCPinall fourmeasures, indicating a lackof competitiveness from JCP in its appeal to customers. Forbusinesses facing extensive competition from substitute companies, customer loyalty arguablybecomesincreasinglyimportant.Furthermore,withthemarketdecreasingthereisahighlikelihoodofconsolidationintheindustryeitherthroughmergersortheclosingofcompaniesassupplybeingsto exceed demand. Being the preferred customer choice therefore increases the likelihood ofsurvival.Assuch,JCPisatriskofbecomingredundantunlessitcanmanagetoturnitscustomerexperiencearound.3.2FinancialComparisonAshighlightedintheindustryanalysis,retailersarefacingseveraldisruptionswhichhaveputthefinancialperformanceofcompaniesunderincreasedpressure.Thequestionisthenifthedeclining

Overall'Experience

E.commerce'Experience

Shopper'Satisfaction

Brand'Reputation

Nordstrom 81 82 82 75.58Kohl's 80 79 77 75.04Macy's 78 79 73 72.4

JC<Penney 77 78 74 67.64

4

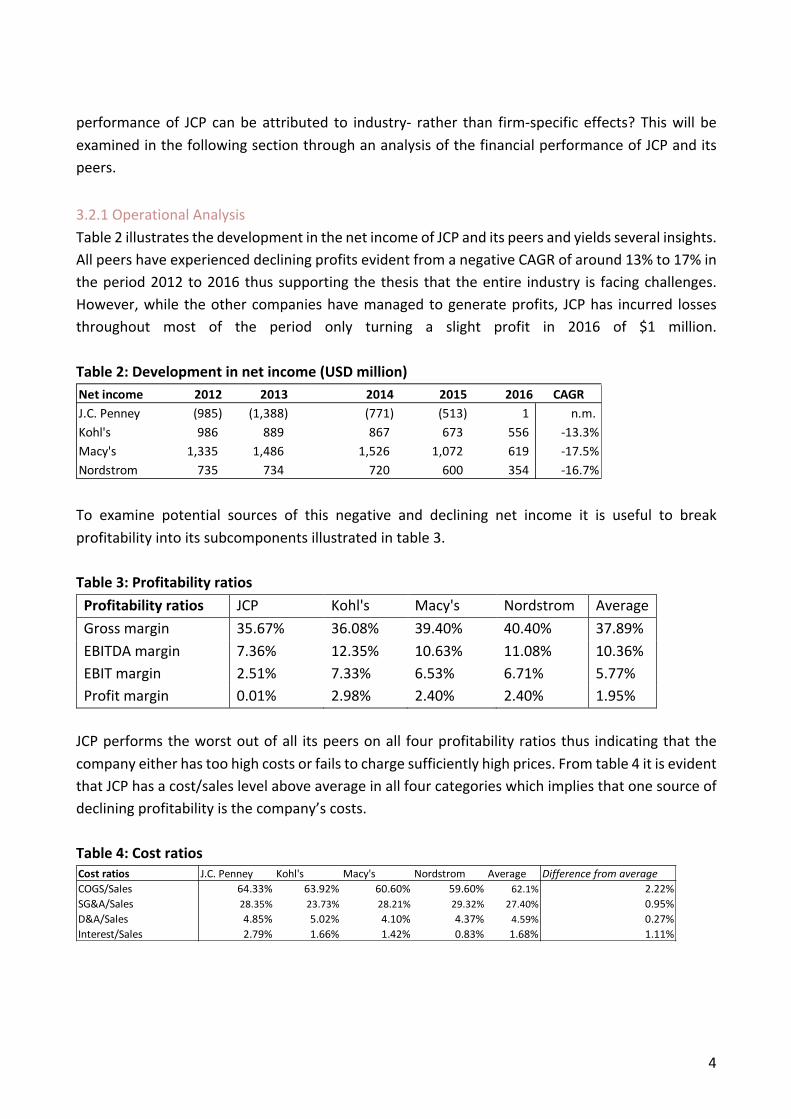

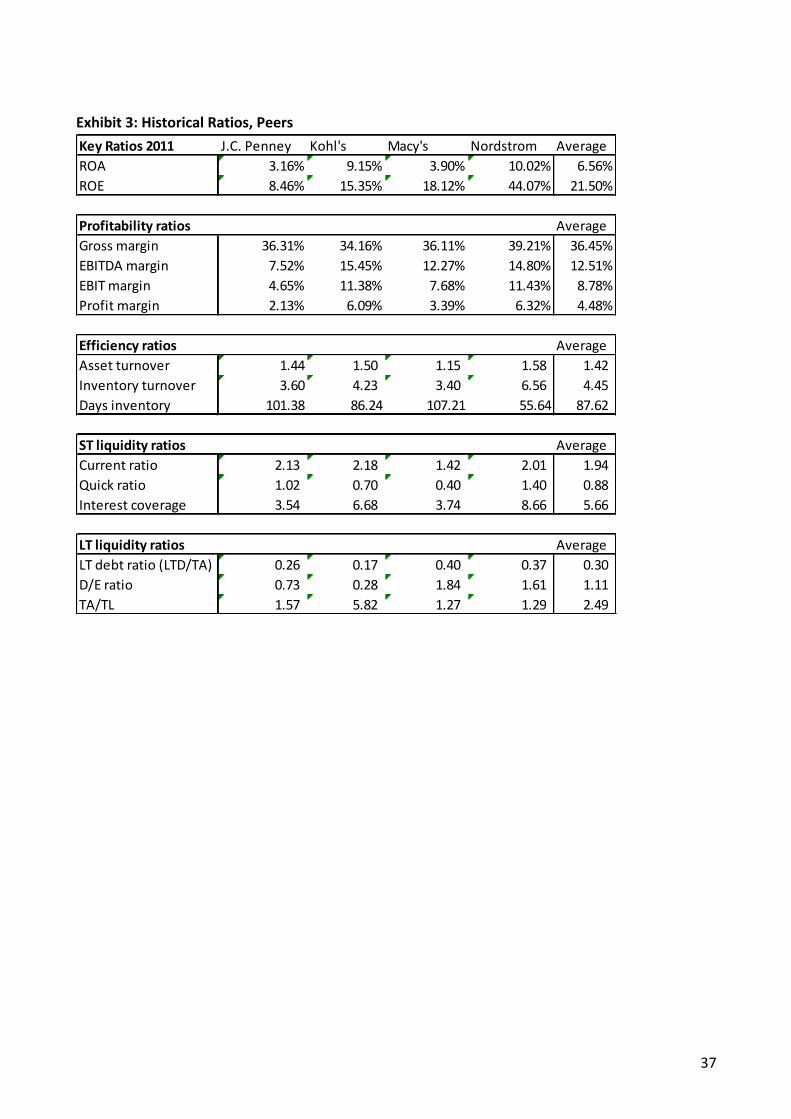

performanceof JCP canbeattributed to industry- rather than firm-specific effects? Thiswill beexaminedinthefollowingsectionthroughananalysisofthefinancialperformanceofJCPanditspeers.3.2.1OperationalAnalysisTable2illustratesthedevelopmentinthenetincomeofJCPanditspeersandyieldsseveralinsights.AllpeershaveexperienceddecliningprofitsevidentfromanegativeCAGRofaround13%to17%intheperiod2012to2016thussupporting the thesis that theentire industry is facingchallenges.However,while theothercompanieshavemanagedtogenerateprofits, JCPhas incurred lossesthroughout most of the period only turning a slight profit in 2016 of $1 million.Table2:Developmentinnetincome(USDmillion)

To examine potential sources of this negative and declining net income it is useful to breakprofitabilityintoitssubcomponentsillustratedintable3.Table3:ProfitabilityratiosProfitabilityratios JCP Kohl's Macy's Nordstrom AverageGrossmargin 35.67% 36.08% 39.40% 40.40% 37.89%EBITDAmargin 7.36% 12.35% 10.63% 11.08% 10.36%EBITmargin 2.51% 7.33% 6.53% 6.71% 5.77%Profitmargin 0.01% 2.98% 2.40% 2.40% 1.95%JCPperformstheworstoutofall itspeersonall fourprofitabilityratiosthus indicatingthatthecompanyeitherhastoohighcostsorfailstochargesufficientlyhighprices.Fromtable4itisevidentthatJCPhasacost/saleslevelaboveaverageinallfourcategorieswhichimpliesthatonesourceofdecliningprofitabilityisthecompany’scosts.Table4:Costratios

Netincome 2012 2013 2014 2015 2016 CAGRJ.C.Penney (985) (1,388) (771) (513) 1 n.m.Kohl's 986 889 867 673 556 -13.3%Macy's 1,335 1,486 1,526 1,072 619 -17.5%Nordstrom 735 734 720 600 354 -16.7%

Costratios J.C.Penney Kohl's Macy's Nordstrom Average DifferencefromaverageCOGS/Sales 64.33% 63.92% 60.60% 59.60% 62.1% 2.22%SG&A/Sales 28.35% 23.73% 28.21% 29.32% 27.40% 0.95%D&A/Sales 4.85% 5.02% 4.10% 4.37% 4.59% 0.27%Interest/Sales 2.79% 1.66% 1.42% 0.83% 1.68% 1.11%

5

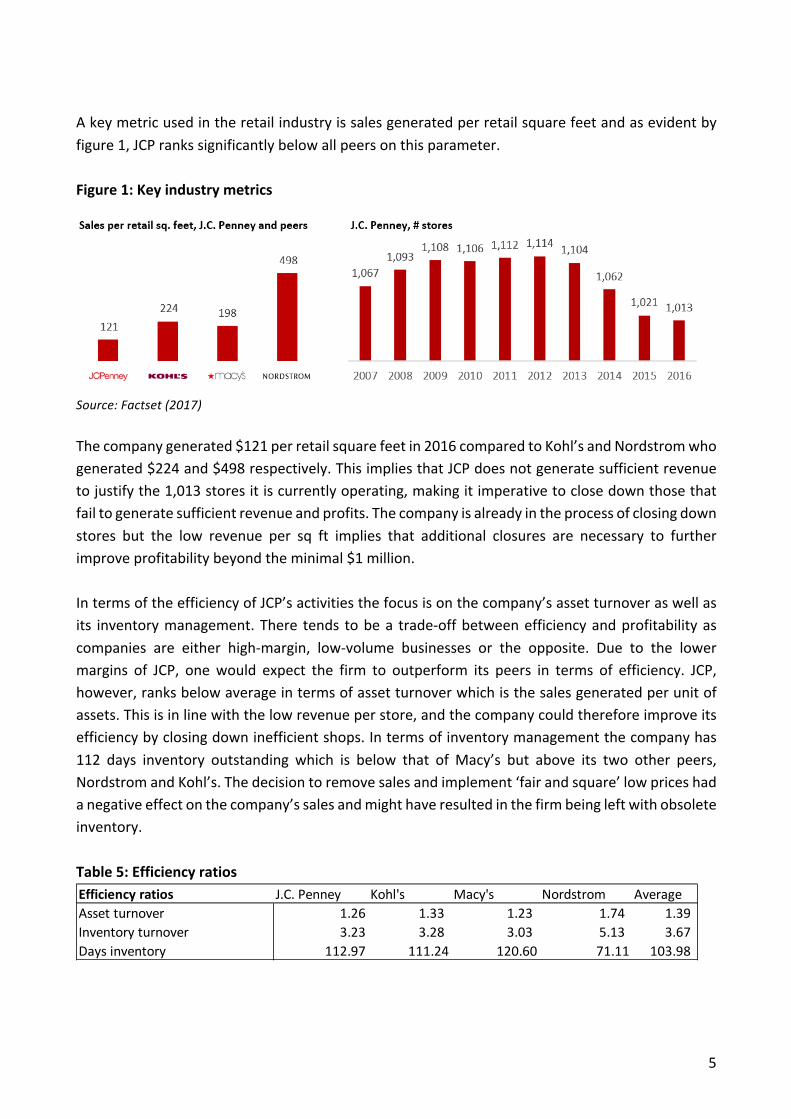

Akeymetricusedintheretailindustryissalesgeneratedperretailsquarefeetandasevidentbyfigure1,JCPrankssignificantlybelowallpeersonthisparameter.Figure1:Keyindustrymetrics

Source:Factset(2017)Thecompanygenerated$121perretailsquarefeetin2016comparedtoKohl’sandNordstromwhogenerated$224and$498respectively.ThisimpliesthatJCPdoesnotgeneratesufficientrevenuetojustifythe1,013storesitiscurrentlyoperating,makingitimperativetoclosedownthosethatfailtogeneratesufficientrevenueandprofits.Thecompanyisalreadyintheprocessofclosingdownstores but the low revenue per sq ft implies that additional closures are necessary to furtherimproveprofitabilitybeyondtheminimal$1million.IntermsoftheefficiencyofJCP’sactivitiesthefocusisonthecompany’sassetturnoveraswellasits inventorymanagement.There tends tobea trade-offbetweenefficiencyandprofitabilityascompanies are either high-margin, low-volume businesses or the opposite. Due to the lowermargins of JCP, onewould expect the firm to outperform its peers in terms of efficiency. JCP,however,ranksbelowaverageintermsofassetturnoverwhichisthesalesgeneratedperunitofassets.Thisisinlinewiththelowrevenueperstore,andthecompanycouldthereforeimproveitsefficiencybyclosingdowninefficientshops.Intermsofinventorymanagementthecompanyhas112 days inventory outstanding which is below that ofMacy’s but above its two other peers,NordstromandKohl’s.Thedecisiontoremovesalesandimplement‘fairandsquare’lowpriceshadanegativeeffectonthecompany’ssalesandmighthaveresultedinthefirmbeingleftwithobsoleteinventory.Table5:Efficiencyratios

Efficiencyratios J.C.Penney Kohl's Macy's Nordstrom AverageAssetturnover 1.26 1.33 1.23 1.74 1.39Inventoryturnover 3.23 3.28 3.03 5.13 3.67Daysinventory 112.97 111.24 120.60 71.11 103.98

6

TosummarizetheoperationalperformanceofJCP,thecompanyappearstobelackingbehinditspeersbothintermsoftheefficiencyandtheprofitabilityofitsoperations.3.2.2AnalysisofCapitalStructureandLiquidityThe liquidityofJCPhasalsobeenanalyzedtoexaminewhetherthecompanyfacesanyshortorlong-termrisksasaresultofitscapitalstructure.Thefirmhasadecentcurrent-ratiobutthisratiocouldbedistortedbyobsoleteinventory.Thecompany’squickratiois,however,alsoabovethoseofMacy’sandKohl’sonlylaggingbehindthatofNordstrom,andtheseratiosdothereforenotraiseanysubstantialconcerns.Theinterestcoverageratioof0.90is,however,highlyproblematicasitimplies that the company’s interest payments are almost as large as its operating profit thusincreasingtheriskofbreakingcovenantsortriggeringabankruptcyfiling.JCPranksfarbehindtheratiosofitspeersandreducingthelevelofdebtofthecompanymustthereforebeemphasized.JCP’sextensiveinterestpaymentsarecausedbyasignificantaccumulationofdebt,andthisisfirstof all reflected in a long-termdebt ratioof 51% compared to the industry averageof 38%. JCPfurthermore has a debt/equity ratio of 3.11 compared to an average of 1.80 implying that thecompanyismainlyfinancedbydebtratherthanequitythusincreasingtheriskofbankruptcy.Table6:Short-andlong-termliquidityratios

Toavoidfocusingsolelyonaccrualsitissensibletoexaminethecompany’sabilitytogeneratecashandtheprobabilityofanycashshortagesoccurring.Afrequentlyusedmeasureinthiscategoryisthe cash flow from operations to current liability ratio, and this also is illustrated in table 6. Abenchmarkforahealthymaturefirmisaround40%whichbothKohl’sandNordstromsatisfy(Wiel,etal.,2012).JCPandMacy’s,however,haveratiosfarbelowthisbenchmarkwithJCPperformingtheworst implying that the company is not generating sufficient cash to satisfy its liabilities. In

STliquidityratios J.C.Penney Kohl's Macy's Nordstrom AverageCurrentratio 1.79 1.93 1.45 1.44 1.65Quickratio 0.48 0.39 0.39 0.70 0.49Interestcoverage 0.90 4.40 4.59 8.11 4.50

LTliquidityratios J.C.Penney Kohl's Macy's Nordstrom AverageLTdebtratio(LTD/TA) 51% 33% 34% 35% 38%D/Eratio 3.11 0.80 1.48 1.79 1.80TA/TL 1.19 5.03 1.30 1.24 2.19

Cashratios J.C.Penney Kohl's Macy's Nordstrom AverageCFOtocurrentliabilities 14.4% 77.1% 32.0% 57.7% 45.3%Cash/currentassets 26.6% 19.6% 21.0% 17.3% 21.1%Cash/currentliabilities 47.7% 37.9% 30.4% 24.9% 35.2%Cash/totalliabilities 13.3% 12.8% 10.6% 10.4% 11.8%

7

contrast,uponexaminationoftheothercashratios,JCPappearstohaveahighlevelofcashonitsbalancesheetwithahighercashasapercentageofassetsandliabilitiesthanallitspeers.A key takeaway from the financial analysisof JCP is that although the company currentlyhas areasonableassetbaseandasubstantiallevelofcashtoserviceinterestpayments,thehighlevelofleverageandcorrespondinglyhigh interestpayments,almostexceedingthecompany’sEBIT,arenotsustainableinthelongrun.

4.CausesofDecline4.1ManagementFailureMikeUllmanheadedthecompanyfrom2004to2011(Ofek,etal.,2016).Towardstheendofhistenure, JCP was underperforming materially relative to its peers. The company performedsignificantly below all peers in terms of ROA, ROE, EBITDAmargin, profit margin, and interestcoverageratioin2011asillustratedinExhibit3.ActivisthedgefundmanagersBillAckmanandStevenRothacquired27%ofthecompanyin2010.Bothwere given seats on JCP’s board, andAckmanprompted the firing of long-timeCEOMikeUllman(Subramanian,2015).Heendorsedhisreplacement,RonJohnson,in2011,tothenre-hireUllmansixteenmonthslaterandthen,again,pushforhisreplacement.ThefollowingpresentsananalysisoftheleadershipofJCPstartingwiththearrivalofRonJohnson.Within a yearof takingover asCEO,Ron Johnsonhad replaced the chief financial officer, chiefoperatingofficer,chieftechnologyofficer,chiefmarketingofficer,andchieftalentofficer(Bhasin,2012).Itiscertainlyadvisableforaturnaroundmanagertoscantheexistingmanagementteamformemberswhounceasinglyworkagainstthenewagenda,butacompleteswitch-upoftheC-suitecouldeliminatevaluableexperienceandinsight,andfeedalienationbetweenthenewstrategyandtheremainderoftheexistingorganization.OneofJohnson’sstrategicfiascoswasthereplacementoffrequentpricediscountsandpromotionswithout prior testing on how the existing customer base would respond. In 2012, the averagediscountonsoldproducts reached60percent (Ofek,etal.,2016)Discountswere replacedwitheveryday lowpricing through the ‘Fair andSquare’ campaign,andhigher-endproduct linesanddesigner collaborationswere added. Johnson removed sales commissionswith the intention ofincreasingcustomerfocusanddecreasingfocusonsales(and,onecouldspeculate,toincreasethedistressedbottomline),astepwhichfrustratedmanyemployees(Ibid).Despite double-digit decreases in sales, storeswhich had been updated according to Johnson’sstrategyperformedrelativelybetterthanthosewhichhadnot.Somehavesincearguedthatthestrategicoverhaul,which catered toa ratherdifferent customer,wasnotgivenenough time tocultivateproperly (Ofek,etal.,2016).Ackman,whohired Johnson to replaceUllman,cited ‘too

8

muchchangetooquicklywithoutadequatetestingonwhatthe impactwouldbe’asthereasonbehind the failure of Johnson’s strategy, which Ackman described as ‘very close to a disaster’(Wapner,2013).StrategicfailureunderJohnsonappearstohavebeenanissueof inhabitingthewrongfocus:whileJohnsoncertainlyshowedexceedingcompetenceinpastendeavours,hewassteel-setonafocusonthewrongcustomer–amove,whichculminatedinconfusionamongexistingcustomersaboutwhatJCPstoodfor.WhilestrategicfailuremayhavecontributedgreatlytoJCP’sdemiseunderJohnson,severalsourcessuggestthatalackofbuy-infromtheorganizationalsoaffectedtheturnaroundprocessadversely.Johnsonhadaverycleargroupofafewexecutiveswhomheconfidedin.Employeescomplainedabout lack of communication and transparency from Ron Johnson’s management team. As anexample, store managers only had access to their own sales numbers whereas relative storeperformance was kept under wraps. Bhasin (2013a) points towards Johnson’s past at Apple, acompany where confidentiality is key for very sensible reasons, as a potential part of theexplanation. But at JCP, the move towards opacity resulted in loss of trust in management.AccordingtoCovert(2013),JohnsonandeightotherexecutivescontinuedUllman’spracticeandcommutedfromtheirhomesinotherstatestoJCP’sheadquartersbycorporatejet.Johnsonwasrarelyintownfortheentireworkweek,andstayedattheRitz-Carltonhotelonthecompany’sbillwhenhewas.Theuseof corporate jetsand luxuryhotelsduring timesof cutbacksand lay-offscreatesavividcontrastandmaysignalthattopmanagementhasnointerestin“sharingthepain”.Theperceiveddistancecreatedasaresultlikelyhurtbuy-infromtherestoftheorganizationwhich,due to the issues of lacking transparency, were already subject to a stark communicationalhierarchy.Therapidspreadofrumors(surrounding,amongotherthings,newroundsof lay-offs,eliminationsofcertainpositions,andshut-downsofdivisionsandstores)alsoultimatelycreatedanenvironmentofuncertainty,distrust,andinsecurity.Lastly,Tuttle(2013)notesthatJohnsonhaddifficulties relating to and appeared to have little respect for JCP’s existing customer base. Forexample, he publically suggested that customers needed to be ‘educated’ when they did notrespondwelltothenew‘fairandsquare’pricingstrategy.MikeKramerwascarriedoverfromApplebyRonJohnson,takingthepositionasCOOatJCP.KramerwasquotedinintheWallStreetJournalin2013,describingtheJCPcultureatthebeginningofhistenure:‘IhatedtheJCPenneyculture,itwaspathetic’suggestingthatJCP’sheadquarterswere‘overstaffedandunderproductive’(Bhasin,2013b).ThedemeaningrhetoricwithwhichthenewC-suitedescribedtheJCPculturewasanotherlikelysourceofalienationbetween“old”and“new”.When Ullman returned in 2013, hemoved the focus back to the preceding JCP customer andreinstated hefty discounts. Large losses were incurred again in 2013, when Home Stores, asoverhauled by Johnson at higher price points,were established and did not resonatewellwithcustomers(Ofek,etal.,2016).In2015,UllmanhandedoverthereinstocurrentCEOMarvinEllisonmarkingthetransitiontowardsbettermanagementpractices.EllisonmakesapointoutofvisitingJCPstoresasoftenaspossible,andallseniormanagementisexpectedtodothesame.Whenvisiting

9

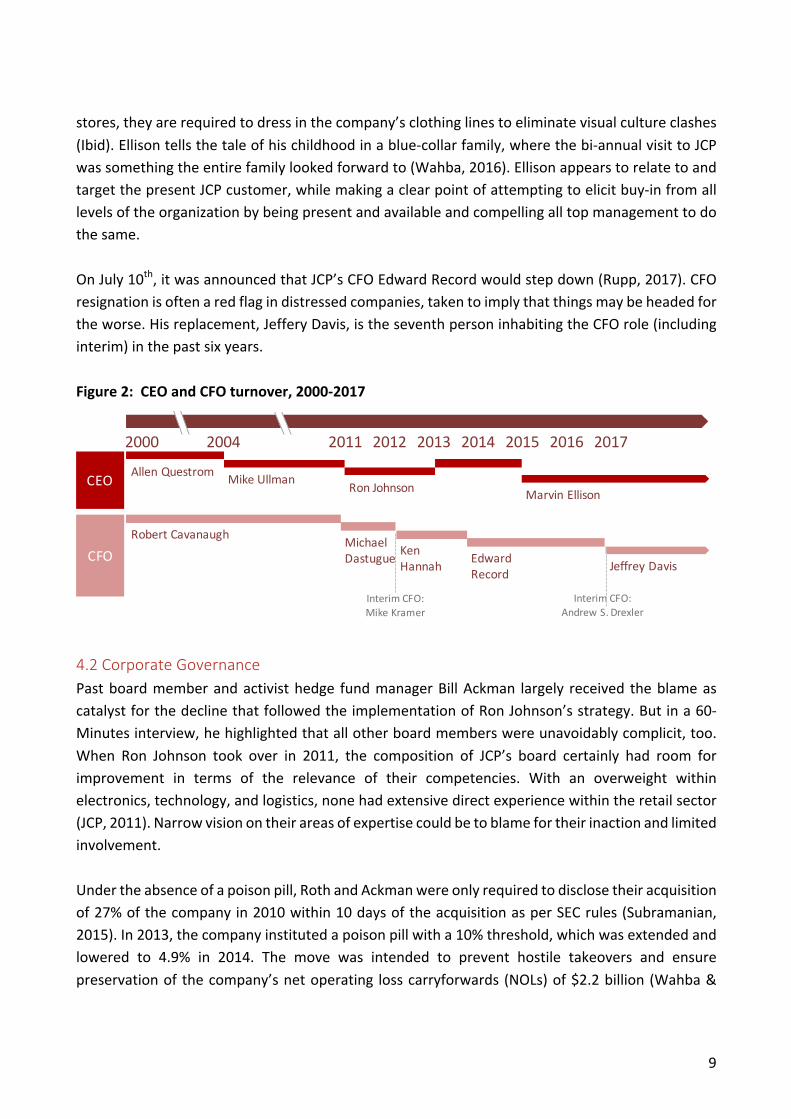

stores,theyarerequiredtodressinthecompany’sclothinglinestoeliminatevisualcultureclashes(Ibid).Ellisontellsthetaleofhischildhoodinablue-collarfamily,wherethebi-annualvisittoJCPwassomethingtheentirefamilylookedforwardto(Wahba,2016).EllisonappearstorelatetoandtargetthepresentJCPcustomer,whilemakingaclearpointofattemptingtoelicitbuy-infromalllevelsoftheorganizationbybeingpresentandavailableandcompellingalltopmanagementtodothesame.OnJuly10th,itwasannouncedthatJCP’sCFOEdwardRecordwouldstepdown(Rupp,2017).CFOresignationisoftenaredflagindistressedcompanies,takentoimplythatthingsmaybeheadedfortheworse.Hisreplacement,JefferyDavis,istheseventhpersoninhabitingtheCFOrole(includinginterim)inthepastsixyears.Figure2:CEOandCFOturnover,2000-2017

4.2CorporateGovernancePastboardmemberandactivisthedge fundmanagerBillAckman largely received theblameascatalystforthedeclinethatfollowedtheimplementationofRonJohnson’sstrategy.Butina60-Minutesinterview,hehighlightedthatallotherboardmemberswereunavoidablycomplicit,too.When Ron Johnson took over in 2011, the composition of JCP’s board certainly had room forimprovement in terms of the relevance of their competencies. With an overweight withinelectronics,technology,andlogistics,nonehadextensivedirectexperiencewithintheretailsector(JCP,2011).Narrowvisionontheirareasofexpertisecouldbetoblamefortheirinactionandlimitedinvolvement.Undertheabsenceofapoisonpill,RothandAckmanwereonlyrequiredtodisclosetheiracquisitionof27%ofthecompanyin2010within10daysoftheacquisitionasperSECrules(Subramanian,2015).In2013,thecompanyinstitutedapoisonpillwitha10%threshold,whichwasextendedandlowered to 4.9% in 2014. The move was intended to prevent hostile takeovers and ensurepreservationof thecompany’snetoperating losscarryforwards (NOLs)of$2.2billion(Wahba&

Michael(

Dastugue

2000 2004 2011 2013 2015

Allen(QuestromMike(Ullman

Ron(JohnsonMarvin(Ellison

Robert(Cavanaugh

Edward(

Record

CEO

CFO

2012 2014

Ken(

Hannah

20172016

Jeffrey(Davis(

Interim(CFO:(

Mike(Kramer

Interim(CFO:(

Andrew(S.(Drexler

10

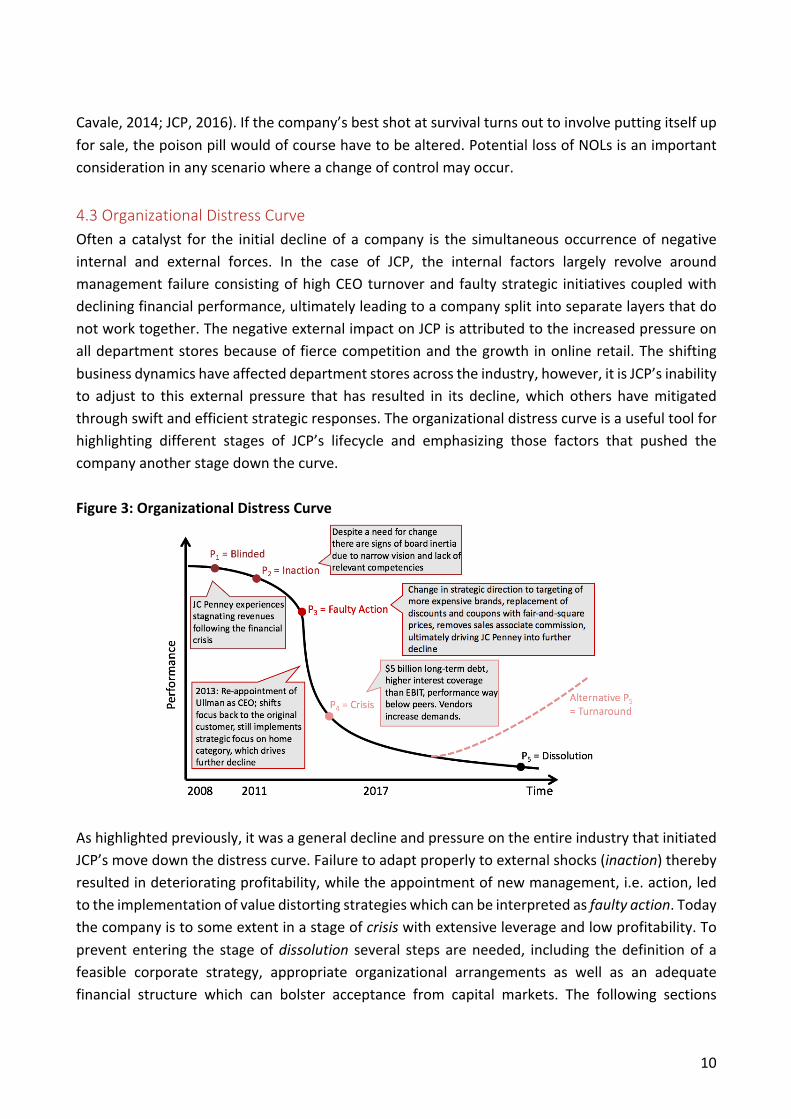

Cavale,2014;JCP,2016).Ifthecompany’sbestshotatsurvivalturnsouttoinvolveputtingitselfupforsale,thepoisonpillwouldofcoursehavetobealtered.PotentiallossofNOLsisanimportantconsiderationinanyscenariowhereachangeofcontrolmayoccur.4.3OrganizationalDistressCurveOftena catalyst for the initialdeclineof a company is the simultaneousoccurrenceofnegativeinternal and external forces. In the case of JCP, the internal factors largely revolve aroundmanagement failureconsistingofhighCEOturnoverandfaultystrategic initiativescoupledwithdecliningfinancialperformance,ultimatelyleadingtoacompanysplitintoseparatelayersthatdonotworktogether.ThenegativeexternalimpactonJCPisattributedtotheincreasedpressureonalldepartmentstoresbecauseoffiercecompetitionandthegrowth inonlineretail.Theshiftingbusinessdynamicshaveaffecteddepartmentstoresacrosstheindustry,however,itisJCP’sinabilityto adjust to this external pressure that has resulted in its decline,which others havemitigatedthroughswiftandefficientstrategicresponses.Theorganizationaldistresscurveisausefultoolforhighlighting different stages of JCP’s lifecycle and emphasizing those factors that pushed thecompanyanotherstagedownthecurve.Figure3:OrganizationalDistressCurve

Ashighlightedpreviously,itwasageneraldeclineandpressureontheentireindustrythatinitiatedJCP’smovedownthedistresscurve.Failuretoadaptproperlytoexternalshocks(inaction)therebyresultedindeterioratingprofitability,whiletheappointmentofnewmanagement,i.e.action,ledtotheimplementationofvaluedistortingstrategieswhichcanbeinterpretedasfaultyaction.Todaythecompanyistosomeextentinastageofcrisiswithextensiveleverageandlowprofitability.Toprevententering the stageofdissolution several stepsareneeded, including thedefinitionof afeasible corporate strategy, appropriate organizational arrangements as well as an adequatefinancial structure which can bolster acceptance from capital markets. The following sections

11

highlightsomeoftheoptionsavailabletoJCPandevaluatewhetherthecompanyisworthmoredead(throughabankruptcyfilingandliquidation)thanalive(asagoingrestructuredconcern).

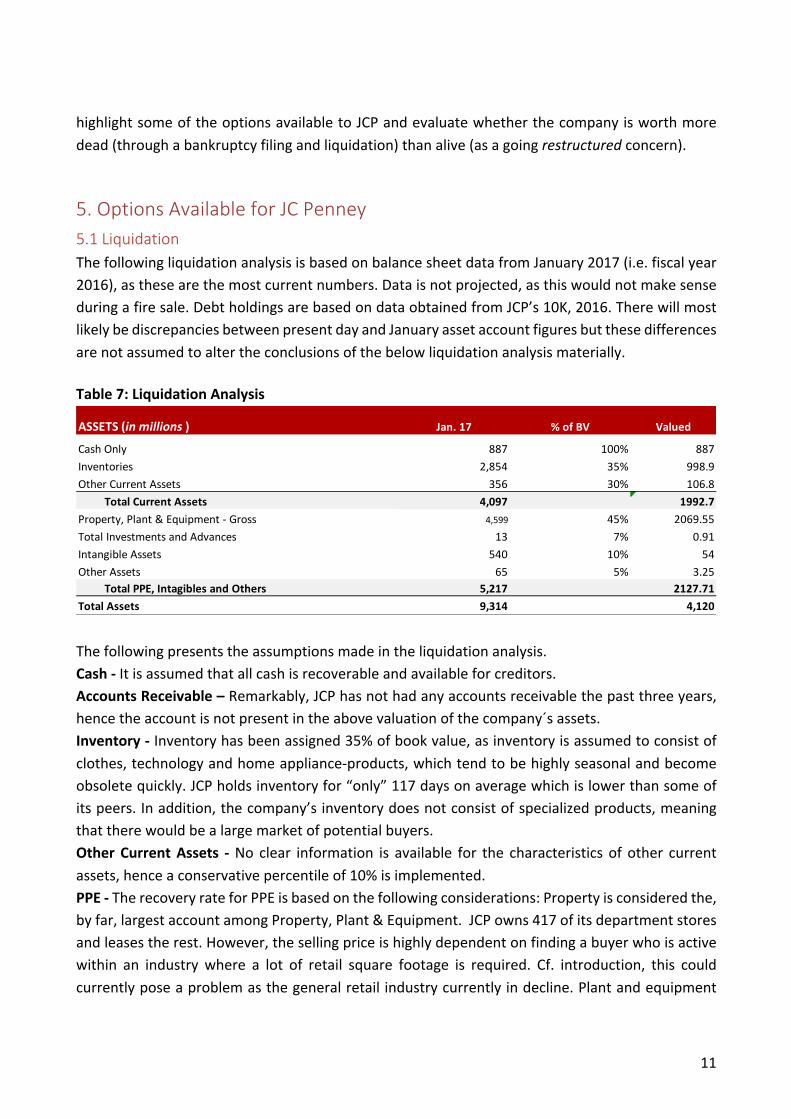

5.OptionsAvailableforJCPenney5.1LiquidationThefollowingliquidationanalysisisbasedonbalancesheetdatafromJanuary2017(i.e.fiscalyear2016),asthesearethemostcurrentnumbers.Dataisnotprojected,asthiswouldnotmakesenseduringafiresale.DebtholdingsarebasedondataobtainedfromJCP’s10K,2016.TherewillmostlikelybediscrepanciesbetweenpresentdayandJanuaryassetaccountfiguresbutthesedifferencesarenotassumedtoaltertheconclusionsofthebelowliquidationanalysismaterially.Table7:LiquidationAnalysis

Thefollowingpresentstheassumptionsmadeintheliquidationanalysis.Cash-Itisassumedthatallcashisrecoverableandavailableforcreditors.AccountsReceivable–Remarkably,JCPhasnothadanyaccountsreceivablethepastthreeyears,hencetheaccountisnotpresentintheabovevaluationofthecompany´sassets.Inventory-Inventoryhasbeenassigned35%ofbookvalue,asinventoryisassumedtoconsistofclothes,technologyandhomeappliance-products,whichtendtobehighlyseasonalandbecomeobsoletequickly.JCPholdsinventoryfor“only”117daysonaveragewhichislowerthansomeofitspeers.Inaddition,thecompany’sinventorydoesnotconsistofspecializedproducts,meaningthattherewouldbealargemarketofpotentialbuyers.OtherCurrentAssets -No clear information is available for the characteristics of other currentassets,henceaconservativepercentileof10%isimplemented.PPE-TherecoveryrateforPPEisbasedonthefollowingconsiderations:Propertyisconsideredthe,byfar,largestaccountamongProperty,Plant&Equipment.JCPowns417ofitsdepartmentstoresandleasestherest.However,thesellingpriceishighlydependentonfindingabuyerwhoisactivewithin an industry where a lot of retail square footage is required. Cf. introduction, this couldcurrentlyposeaproblemasthegeneralretailindustrycurrentlyindecline.Plantandequipment

ASSETS(inmillions ) Jan.17 %ofBV Valued

CashOnly 887 100% 887Inventories 2,854 35% 998.9OtherCurrentAssets 356 30% 106.8

TotalCurrentAssets 4,097 1992.7Property,Plant&Equipment-Gross 4,599 45% 2069.55TotalInvestmentsandAdvances 13 7% 0.91IntangibleAssets 540 10% 54OtherAssets 65 5% 3.25

TotalPPE,IntagiblesandOthers 5,217 2127.71TotalAssets 9,314 4,120

12

shouldnottakeupalargeproportionofthePPEaccount,asJCPdoesnotmanufactureproductsitself.Equipmentismerelyconsideredtobecashregisters,pallettrucksetc.alldeemedtobeoflittletonosalvagevalue.Ontheotherhand,Statista,(2017)findsthatbrick-and-mortarstoreswillaccountfor85%ofUSretailin2025,supportingaslightlystrongerrecoveryrateforPPE.Itisalsoassumed that JCP´s property is located in fairly populated areaswhich should be attractive forpotential customers, supporting theoverall recovery rate. The recovery rate is set at45%,as itseemslikelythatadominantmarketplayerwouldfindmanyofJCP´slocationsattractive.Total Investments andAdvances -Retrieving investments andadvances aredeemeduncertain,hence a very conservative percentile of 7% is set for the recovery rate. Some advances could,however,beattributabletosubsidiaries,supportingarateabove0%.IntangibleAssets–ItisassumedthatthetrademarkofJCPanditsin-housebrandswillstillhavesomevalueafteraliquidation,hencetheretrievalrateissettobe10%.OtherAssets-Noclearinformationisavailableforthecharacteristicsofothercurrentassets,henceaconservative5%recoveryrateisapplied.

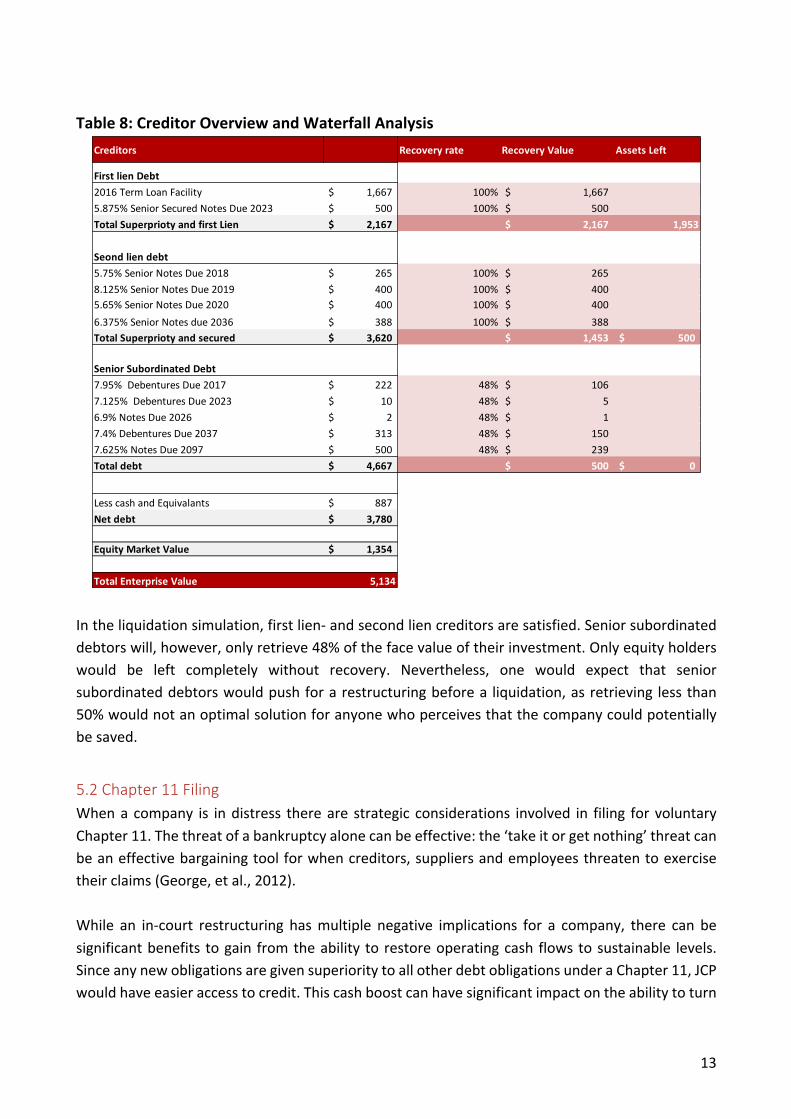

5.1.1WaterfallAnalysisThe purpose of a waterfall analysis is to sort creditors according to their seniority. Further, itprovidesanoverviewofwhateachcreditorcouldexpecttoreceiveintheeventofaliquidation,assumingthepeckingorderoftheabsolutepriority(AP)ruleholds.Creditors inthesamegroupmustbetreatedequally,accordingtotheparipassuprinciple,andnoonelendercanbeunfairlydiscriminatedagainstrelativetoitspeers.Theanalysiscommencesatthetopoftheseniorityladder,asperJanuary2017.JCPhastwofirstliencreditorswithacombinedclaimof$2.16billion,whichwouldbesatisfiedcompletelyinaliquidation.Theclaimofsecondliendebtholdersis$1.45billion,allwithdifferentmaturities,withtheclosestupcomingduedatein2018.Allsecondliencreditorswillalsorecover100%oftheirfacevalue.JCPholds$1.04billioninseniorsubordinateddebt-anobligationthecompanywillnotbeabletomeetcompletelyinthecaseofanimmediateliquidation.

13

Table8:CreditorOverviewandWaterfallAnalysis

Intheliquidationsimulation,firstlien-andsecondliencreditorsaresatisfied.Seniorsubordinateddebtorswill,however,onlyretrieve48%ofthefacevalueoftheirinvestment.Onlyequityholderswould be left completely without recovery. Nevertheless, one would expect that seniorsubordinateddebtorswouldpushforarestructuringbeforea liquidation,asretrieving lessthan50%wouldnotanoptimalsolutionforanyonewhoperceivesthatthecompanycouldpotentiallybesaved.

5.2Chapter11FilingWhena company is indistress thereare strategic considerations involved in filing for voluntaryChapter11.Thethreatofabankruptcyalonecanbeeffective:the‘takeitorgetnothing’threatcanbeaneffectivebargainingtoolforwhencreditors,suppliersandemployeesthreatentoexercisetheirclaims(George,etal.,2012).While an in-court restructuring hasmultiple negative implications for a company, there can besignificantbenefits togain fromtheability torestoreoperatingcash flowstosustainable levels.SinceanynewobligationsaregivensuperioritytoallotherdebtobligationsunderaChapter11,JCPwouldhaveeasieraccesstocredit.Thiscashboostcanhavesignificantimpactontheabilitytoturn

Creditors Recoveryrate RecoveryValue AssetsLeft

FirstlienDebt2016TermLoanFacility 1,667$ 100% 1,667$5.875%SeniorSecuredNotesDue2023 500$ 100% 500$TotalSuperpriotyandfirstLien 2,167$ 2,167$ 1,953

Seondliendebt5.75%SeniorNotesDue2018 265$ 100% 265$8.125%SeniorNotesDue2019 400$ 100% 400$5.65%SeniorNotesDue2020 400$ 100% 400$6.375%SeniorNotesdue2036 388$ 100% 388$TotalSuperpriotyandsecured 3,620$ 1,453$ 500$

SeniorSubordinatedDebt7.95%DebenturesDue2017 222$ 48% 106$7.125%DebenturesDue2023 10$ 48% 5$ 6.9%NotesDue2026 2$ 48% 1$ 7.4%DebenturesDue2037 313$ 48% 150$7.625%NotesDue2097 500$ 48% 239$Totaldebt 4,667$ 500$ 0$

LesscashandEquivalants 887$Netdebt 3,780$

EquityMarketValue 1,354$

TotalEnterpriseValue 5,134

14

operations around (George, et al., 2012). However, management actions may be remarkablyconstrainedduetocourtscrutiny,despitethetimegainedtomakedecisionsandproposeasolution(Ibid).Besideshighcosts,lackofcontrol,andthepotentialofpublicizingsensitiveinformationofanin-court restructuring, what makes a Chapter 11 filing less attractive for JCP is the affiliatedreputationalriskthatgivesrisetoskepticismfrombothdownstreamandupstreamstakeholders.Vendorsarelikelytobecomereluctanttosupplyproductsormaterials inthefearofnotgettingpaid,whileconsumersmaybelessinclinedtobuyproductsthatpotentiallycannotbereturnedorservicedinthefuture.Expensiveproductswithlongexpectedliveswhichhaveafter-salesserviceandembeddedguaranteesattachedwillbeparticularlyaffectedbythisreputationalrisk.Customerslookingforproductssuchashomeapplianceswhicharemeanttobeusedforyearswilllikelybeacutelyreluctanttobuyfromafirmindistress,whichwouldbeexpectedtohaveadiscouragingeffectonsales.AnexaminationofthefinancialsofJCPwillfacilitateansweringthequestionofwhetherthefirm’slevelofdistressindeedqualifiesabankruptcyfilingasabsolutelynecessary.Theessentialquestionstoaskarewhetherthecompanyfacesliquidityproblems,andifso,whenitwillbeunabletoserviceitsdebt.Thenextthreerepaymentsdebtincludeadebentureof$220millionin2017,$265millionofSeniorNotesin2018,and$400millionofSeniorNotesin2019.AquicklookatthecashsituationconsideringthedebtlevelsandperformanceprojectionssuggeststhatJCPmaybeunabletoservicethe Senior Notes in 2019. However, JCP has already mitigated the threat through a recentrenegotiationoftheWellsFargorevolverof$4billion,whichprovidesJCPwithatemporaryoptionto use its cash holdings to financematuring debt, and the revolver to finance operations. Butfinancingoperationsthroughincurringmoredebtiscertainlynotasustainablesolutioninthelongterm.JCPmustbeabletoorganicallyfinancetheiroperationsthroughnetincomegrowth.Insummary,astrategicChapter11filingwouldbemoreappropriateinasituationwherecashwassignificantlyandurgentlyconstrained.DuetotheinherentreputationalrisksbankruptcycouldposetotheJCPbrand,bankruptcyshouldbealastresort.JCP’scurrentfinancialsituationdoesnotyetmeritthedrasticmeasure.Thecompanyshouldinsteadassesstheprobabilityofasuccessfulout-of-court turnaround strategy. If the company concludes that another turnaround is unlikely tosucceed,orthat industrydeterioration isultimately likelytodrivethecompany intodissolution,liquidationunderChapter7maybemorerelevant.

5.3TurnaroundStrategyToconvertJCPfromafirmindistressintoawell-performingentity,threeingredientsareneeded:i)a feasiblecorporatestrategy, ii)appropriateorganizationalarrangements,and iii)acceptanceby

15

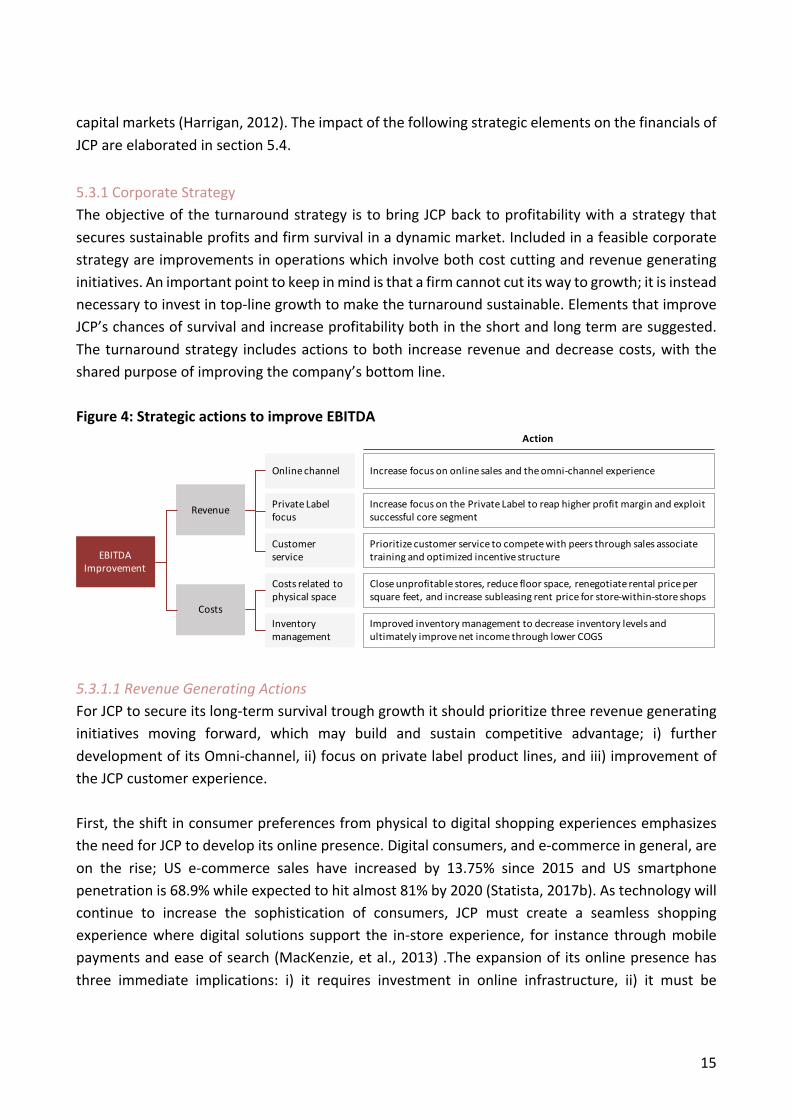

capitalmarkets(Harrigan,2012).TheimpactofthefollowingstrategicelementsonthefinancialsofJCPareelaboratedinsection5.4.5.3.1CorporateStrategyTheobjectiveoftheturnaroundstrategy istobringJCPbacktoprofitabilitywithastrategythatsecuressustainableprofitsandfirmsurvivalinadynamicmarket.Includedinafeasiblecorporatestrategyareimprovementsinoperationswhichinvolvebothcostcuttingandrevenuegeneratinginitiatives.Animportantpointtokeepinmindisthatafirmcannotcutitswaytogrowth;itisinsteadnecessarytoinvestintop-linegrowthtomaketheturnaroundsustainable.ElementsthatimproveJCP’schancesofsurvivalandincreaseprofitabilitybothintheshortandlongtermaresuggested.Theturnaroundstrategy includesactionstoboth increaserevenueanddecreasecosts,withthesharedpurposeofimprovingthecompany’sbottomline.Figure4:StrategicactionstoimproveEBITDA

5.3.1.1RevenueGeneratingActionsForJCPtosecureitslong-termsurvivaltroughgrowthitshouldprioritizethreerevenuegeneratinginitiatives moving forward, which may build and sustain competitive advantage; i) furtherdevelopmentofitsOmni-channel,ii)focusonprivatelabelproductlines,andiii)improvementoftheJCPcustomerexperience.First,theshiftinconsumerpreferencesfromphysicaltodigitalshoppingexperiencesemphasizestheneedforJCPtodevelopitsonlinepresence.Digitalconsumers,ande-commerceingeneral,areon the rise; US e-commerce sales have increased by 13.75% since 2015 and US smartphonepenetrationis68.9%whileexpectedtohitalmost81%by2020(Statista,2017b).Astechnologywillcontinue to increase the sophistication of consumers, JCP must create a seamless shoppingexperiencewheredigital solutions support the in-storeexperience, for instance throughmobilepaymentsandeaseofsearch(MacKenzie,etal.,2013).Theexpansionofitsonlinepresencehasthree immediate implications: i) it requires investment in online infrastructure, ii) it must be

Increase(focus(on(online(sales(and(the(omni2channel(experience(

EBITDA(Improvement

Costs

Costs(related(to(physical(space

Inventory(management

Improved(inventory(management(to(decrease(inventory(levels(and(ultimately(improve(net(income(through(lower(COGS

Close(unprofitable(stores,(reduce(floor(space,(renegotiate(rental(price(per(square(feet,(and(increase(subleasing(rent(price(for(store2within2store(shops((

Action

Revenue

Online(channel

Customer(service

Increase(focus(on(the(Private(Label(to(reap(higher(profit(margin(and(exploit(successful(core(segment

Prioritize(customer(service(to(compete(with(peers(through(sales(associate(training(and(optimized(incentive(structure

Private(Label(focus

16

executedsystemicallyacrosschannels,andiii)marketingeffortsmustbealignedaccordingly.First,thecapitaltoinvestinatechnology-driveninfrastructureshouldbefreedupthroughtheclosingofa number of current stores, which will be elaborated below. Secondly, key to the success ofexpandingitsonlinepresenceistoexecutesystemicallyacrosschannels.Productsorderedonlineshould be available for pick up in the nearest JCP, to save the customer shipping costs and toencouragespontaneouspurchases.Thecompanymustalsobeconsistentintermsofthequality,priceandproductselectionitoffersin-storeandonlinetostreamlineitsoffering.Third, JCPshould leveragephysical storesasamarketing tool tomaintainbrandawarenessandachievehigheronlinesalesvolumes.Someof JCP’scurrent locationscouldserveasstorageunitleasesfor itse-commercebusinesstosupportgrowingvolumethroughthischannel.Throughitssubstantialnetworkofstorageunits,i.e.olddepartmentstores,JCPwouldpotentiallybeabletooffer shippingdealscomparable toAmazonboth in speedandprice,whichare importantvaluedriversforconsumers(Gulisano,2017).However,thefirmcanextractcheapersolutionsbyrentingorbuyingsquarefeetinlessattractiveshoppingareasandbycentralizingdistributioninlargerhubs.Theconversionofphysicalstorespaceshouldthereforeonlysupportonlinepurchaseswithin-storepickup,whoseneedforspacemustbeevaluatedcontinuously.Additionally,JCPshouldleveragetheimmenseamountofdataavailablethroughitsonlineplatformstopersonalizemarketing.

Anenhancedfocusonprivatelabelbrandsshouldbeundertakenaswell,asthisproductlinealreadyperformswellandexhibitssignificantsalesvolumepotentialforJCP.Privatelabelproductsshowhighergrossmarginpotentialrelativetodistributedproductsduetotheabsenceofdouble-margins.Thebelow three segmentsare recommendedas targets forR&Dandpromotionalefforts goingforward:

• Millennials,thefirstgroupwhogrewupwiththeinternet,socialmediaandmobilephones,isagedbe-tween13-30,andmakesup15%oftheUSconsumers.Thesegmentisexpectedtoaccountfor1/3oftotalspendingintheUSby2020(MacKenzie,etal.,2013).

• Baby Boomers, approximately 47 million households in the US alone, are projected toaccountforthelargestspendingproportionswithincategoriessuchashousewares(73%)and apparel (56%) in the coming years. The sheer size of the segment underlines theimportanceoftargetingthegroupgoingforward.However,shoppingpatternsneedtobeevaluated, as the segment is expected to spend a larger proportion of their income onexperiencesrelativetooff-the-shelf-products(MacKenzie,etal.,2013).

• HispanicsspendingisexpectedtodoubleoverthenexttenyearsandaccountforonefifthoftotalspendingintheUS(MacKenzie,etal.,2013).Inadditiontogrowingbuyingpower,theirshoppingpatternsareinterestingfordepartmentstores,asthesegmentspends1.5timesmoreonchildren’sapparel,footwear,andfreshfoodthannon-Hispanicconsumers-providing substantial opportunities for department stores and brands that succeed intargetingthesegment.

17

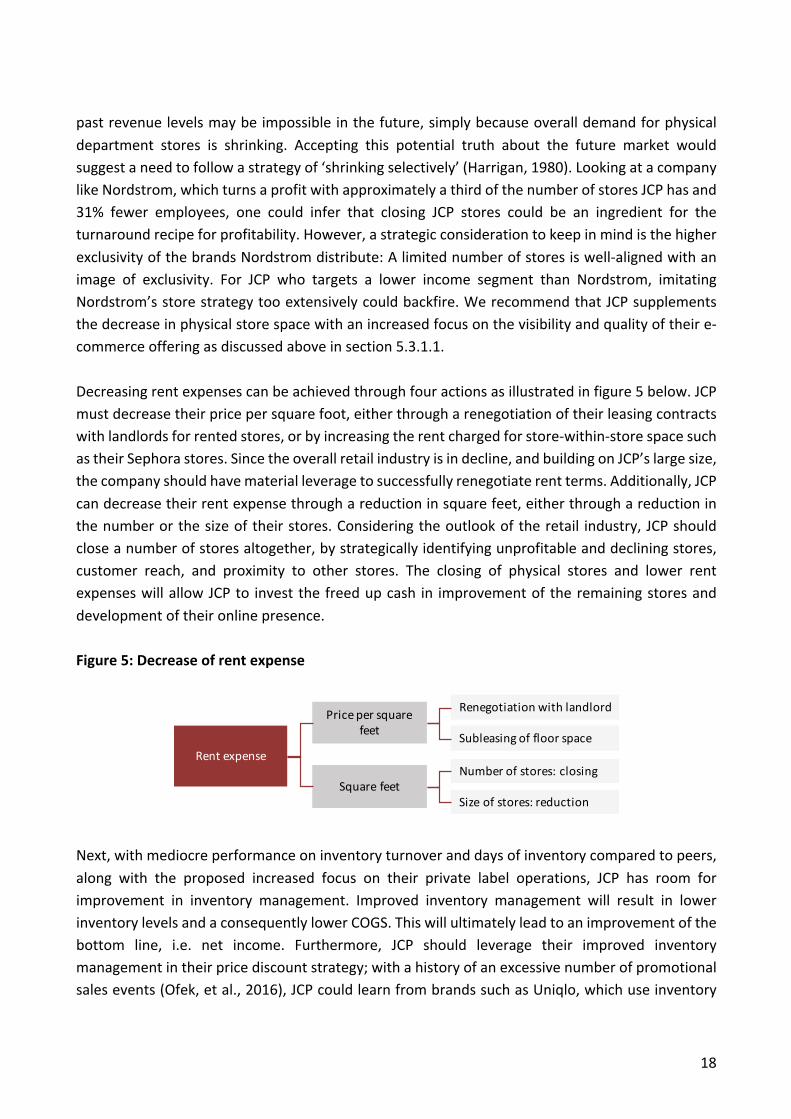

Asapartofaprivatelabelstrategy,storesacrossthecountryshouldbedesignedtopromoteandshowcaseprivatelabelproductsinmoreoptimalwaysrelativetodistributedbrands.Inrelationtoanincreasedfocusontheprivatelabelproductportfolio,privatebrandsnotownedbyJCPwouldand should not be ditched, as these products drive traffic to JCP stores. By implementing theinitiativesabove,JCPwill‘shootwheretheducksare’(Whitney,n.d.),i.e.continueitsfocusonitscorebusiness,whilealsoinitiatingtargetingofnewsegments,adaptingtothefuture.Finally,JCPshouldprioritizeanimprovementofitscustomerexperienceduetogrowingcompetitionforsurvivalintheindustrywhereexperienceisadriverofrepeatpurchases.AsshowninTable1,JCP performsworst in overall customer experience relative to its peers, and in the low end inrelationtoshoppersatisfactiononlybeatingMacy’swhoalsohappentohavealowernumberofemployees per square feet. Twomain drivers for an improved customer experience should beconsidered:i)thephysicalspaceandii)theserviceprovidedbyemployees.First,thetidinessofthephysicalspaceis importantforastimulatingshoppingexperience,withmessytablesandlowin-store inventories currently discouraging sales (Loeb, 2016). A way to improve efficiency is toeliminatenarrow jobdescriptionsandtraineveryemployee in thestoretoassistandcheckoutcustomers,torestock,andtomaintaintidystorespaces.Second,sincein-storeemployeesaretheones interactingwith customers, customer service constitutes a crucial part of the experience.Excellentcustomerservicecandriveimmediateandrepeatpurchases.JCPshouldstimulateintrinsicmotivation through i) increased and continuous employee training, ii) moving away from taskspecializationandtowardsareaspecialization,andiii)jobadvancementopportunities.Continuoustraining and area specialization will make employees more competent in the provision ofexceptionalcustomerservice,stimulatepersonallearningaspirations,andincreasethedegreetowhich they feel valuedby company through itswillingness to invest in them. Job advancementopportunitiesshouldincreaseemployeecommitmenttoJCPandwillinthelong-runresultincostsavings,asre-trainingofexistingemployees istypicallycheaperthantrainingnewpersonnel.Assuch,JCPshouldaimatchangingthepeople,ratherthanchangingthepeople.5.3.1.2CostCuttingActionsAlthoughacompanycannotcutitswaytogrowth,reducingunnecessarycostscandowonderstoastrategicallyviablecompany’sprofitability.ForJCP,twothingsinitsoperatingcostsstandout:i)thehighnumberofphysicalstoresandii)aneedforimprovedinventorymanagement.JCPhasalargenumberofstoresbothrelativetotheirpeergroupandinwhenconsideringthattheretail industry is showing a clear shift from physical to online shopping. The overall decliningperformanceofdepartmentstoresresultingfromshiftingconsumerpreferencesawayfromphysicalandtowardsonlineretail,meritsadiscussionoftheoutlookfordemandandanassessmentofhowJCPmaystrategicallyrepositionitselfinthealteredmarket.JCPmustacknowledgethatreaching

18

pastrevenuelevelsmaybeimpossibleinthefuture,simplybecauseoveralldemandforphysicaldepartment stores is shrinking. Accepting this potential truth about the future market wouldsuggestaneedtofollowastrategyof‘shrinkingselectively’(Harrigan,1980).LookingatacompanylikeNordstrom,whichturnsaprofitwithapproximatelyathirdofthenumberofstoresJCPhasand31% fewer employees, one could infer that closing JCP stores could be an ingredient for theturnaroundrecipeforprofitability.However,astrategicconsiderationtokeepinmindisthehigherexclusivityofthebrandsNordstromdistribute:Alimitednumberofstoresiswell-alignedwithanimage of exclusivity. For JCP who targets a lower income segment than Nordstrom, imitatingNordstrom’sstorestrategytooextensivelycouldbackfire.WerecommendthatJCPsupplementsthedecreaseinphysicalstorespacewithanincreasedfocusonthevisibilityandqualityoftheire-commerceofferingasdiscussedaboveinsection5.3.1.1.Decreasingrentexpensescanbeachievedthroughfouractionsasillustratedinfigure5below.JCPmustdecreasetheirpricepersquarefoot,eitherthrougharenegotiationoftheirleasingcontractswithlandlordsforrentedstores,orbyincreasingtherentchargedforstore-within-storespacesuchastheirSephorastores.Sincetheoverallretailindustryisindecline,andbuildingonJCP’slargesize,thecompanyshouldhavematerialleveragetosuccessfullyrenegotiaterentterms.Additionally,JCPcandecreasetheirrentexpensethroughareductioninsquarefeet,eitherthroughareductioninthenumberorthesizeoftheirstores.Consideringtheoutlookoftheretail industry,JCPshouldcloseanumberofstoresaltogether,bystrategicallyidentifyingunprofitableanddecliningstores,customer reach, and proximity to other stores. The closing of physical stores and lower rentexpenseswillallowJCPto investthefreedupcash in improvementoftheremainingstoresanddevelopmentoftheironlinepresence.Figure5:Decreaseofrentexpense

Next,withmediocreperformanceoninventoryturnoveranddaysofinventorycomparedtopeers,along with the proposed increased focus on their private label operations, JCP has room forimprovement in inventory management. Improved inventory management will result in lowerinventorylevelsandaconsequentlylowerCOGS.Thiswillultimatelyleadtoanimprovementofthebottom line, i.e. net income. Furthermore, JCP should leverage their improved inventorymanagementintheirpricediscountstrategy;withahistoryofanexcessivenumberofpromotionalsalesevents(Ofek,etal.,2016),JCPcouldlearnfrombrandssuchasUniqlo,whichuseinventory

Renegotiation)with)landlord

Subleasing)of)floor)space

Square)feet

Price)per)square)feet

Rent)expenseNumber)of)stores:)closing

Size)of)stores:)reduction

19

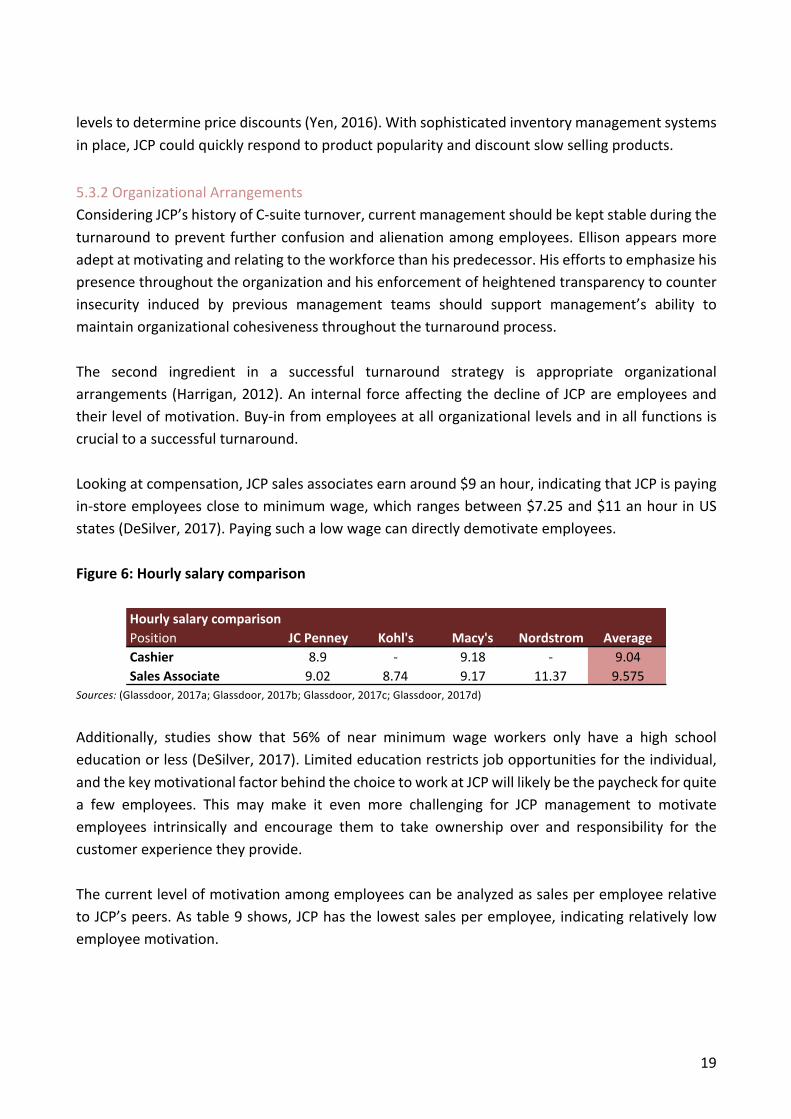

levelstodeterminepricediscounts(Yen,2016).Withsophisticatedinventorymanagementsystemsinplace,JCPcouldquicklyrespondtoproductpopularityanddiscountslowsellingproducts.5.3.2OrganizationalArrangementsConsideringJCP’shistoryofC-suiteturnover,currentmanagementshouldbekeptstableduringtheturnaroundtopreventfurtherconfusionandalienationamongemployees.Ellisonappearsmoreadeptatmotivatingandrelatingtotheworkforcethanhispredecessor.Hiseffortstoemphasizehispresencethroughouttheorganizationandhisenforcementofheightenedtransparencytocounterinsecurity induced by previous management teams should support management’s ability tomaintainorganizationalcohesivenessthroughouttheturnaroundprocess.The second ingredient in a successful turnaround strategy is appropriate organizationalarrangements(Harrigan,2012).An internalforceaffectingthedeclineofJCPareemployeesandtheirlevelofmotivation.Buy-infromemployeesatallorganizationallevelsandinallfunctionsiscrucialtoasuccessfulturnaround.Lookingatcompensation,JCPsalesassociatesearnaround$9anhour,indicatingthatJCPispayingin-storeemployeesclosetominimumwage,whichrangesbetween$7.25and$11anhourinUSstates(DeSilver,2017).Payingsuchalowwagecandirectlydemotivateemployees.Figure6:Hourlysalarycomparison

Sources:(Glassdoor,2017a;Glassdoor,2017b;Glassdoor,2017c;Glassdoor,2017d)

Additionally, studies show that 56% of near minimum wage workers only have a high schooleducationorless(DeSilver,2017).Limitededucationrestrictsjobopportunitiesfortheindividual,andthekeymotivationalfactorbehindthechoicetoworkatJCPwilllikelybethepaycheckforquitea few employees. This may make it even more challenging for JCP management to motivateemployees intrinsically and encourage them to take ownership over and responsibility for thecustomerexperiencetheyprovide.ThecurrentlevelofmotivationamongemployeescanbeanalyzedassalesperemployeerelativetoJCP’speers.Astable9shows,JCPhasthelowestsalesperemployee,indicatingrelativelylowemployeemotivation.

Hourly'salary'comparison'Position JC'Penney Kohl's Macy's Nordstrom AverageCashier 8.9 * 9.18 * 9.04Sales'Associate 9.02 8.74 9.17 11.37 9.575

20

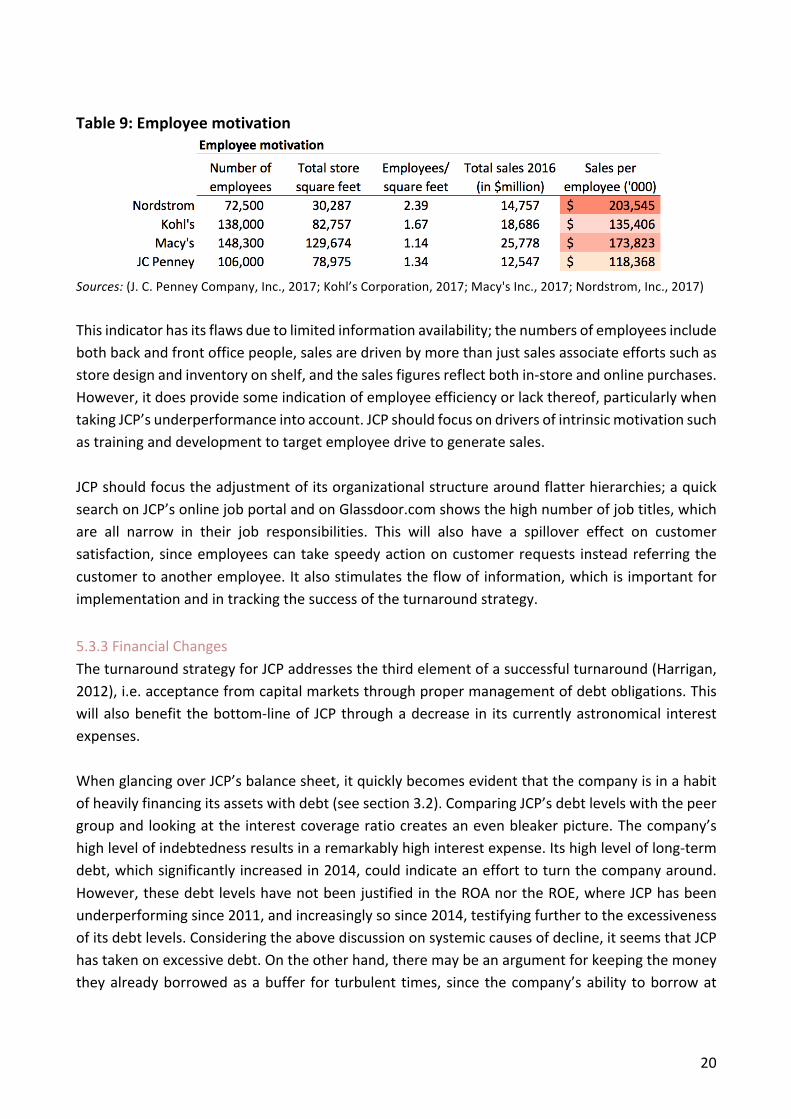

Table9:Employeemotivation

Sources:(J.C.PenneyCompany,Inc.,2017;Kohl’sCorporation,2017;Macy'sInc.,2017;Nordstrom,Inc.,2017)Thisindicatorhasitsflawsduetolimitedinformationavailability;thenumbersofemployeesincludebothbackandfrontofficepeople,salesaredrivenbymorethanjustsalesassociateeffortssuchasstoredesignandinventoryonshelf,andthesalesfiguresreflectbothin-storeandonlinepurchases.However,itdoesprovidesomeindicationofemployeeefficiencyorlackthereof,particularlywhentakingJCP’sunderperformanceintoaccount.JCPshouldfocusondriversofintrinsicmotivationsuchastraininganddevelopmenttotargetemployeedrivetogeneratesales.JCPshouldfocustheadjustmentofitsorganizationalstructurearoundflatterhierarchies;aquicksearchonJCP’sonlinejobportalandonGlassdoor.comshowsthehighnumberofjobtitles,whichare all narrow in their job responsibilities. This will also have a spillover effect on customersatisfaction,sinceemployeescantakespeedyactiononcustomerrequests insteadreferringthecustomertoanotheremployee.Italsostimulatestheflowofinformation,whichisimportantforimplementationandintrackingthesuccessoftheturnaroundstrategy.5.3.3FinancialChangesTheturnaroundstrategyforJCPaddressesthethirdelementofasuccessfulturnaround(Harrigan,2012),i.e.acceptancefromcapitalmarketsthroughpropermanagementofdebtobligations.Thiswillalsobenefit thebottom-lineof JCPthroughadecrease in itscurrentlyastronomical interestexpenses.WhenglancingoverJCP’sbalancesheet,itquicklybecomesevidentthatthecompanyisinahabitofheavilyfinancingitsassetswithdebt(seesection3.2).ComparingJCP’sdebtlevelswiththepeergroupandlookingattheinterestcoverageratiocreatesanevenbleakerpicture.Thecompany’shighlevelofindebtednessresultsinaremarkablyhighinterestexpense.Itshighleveloflong-termdebt,whichsignificantlyincreasedin2014,couldindicateanefforttoturnthecompanyaround.However,thesedebtlevelshavenotbeenjustifiedintheROAnortheROE,whereJCPhasbeenunderperformingsince2011,andincreasinglysosince2014,testifyingfurthertotheexcessivenessofitsdebtlevels.Consideringtheabovediscussiononsystemiccausesofdecline,itseemsthatJCPhastakenonexcessivedebt.Ontheotherhand,theremaybeanargumentforkeepingthemoneytheyalreadyborrowedasabuffer for turbulent times, since thecompany’sability toborrowat

21

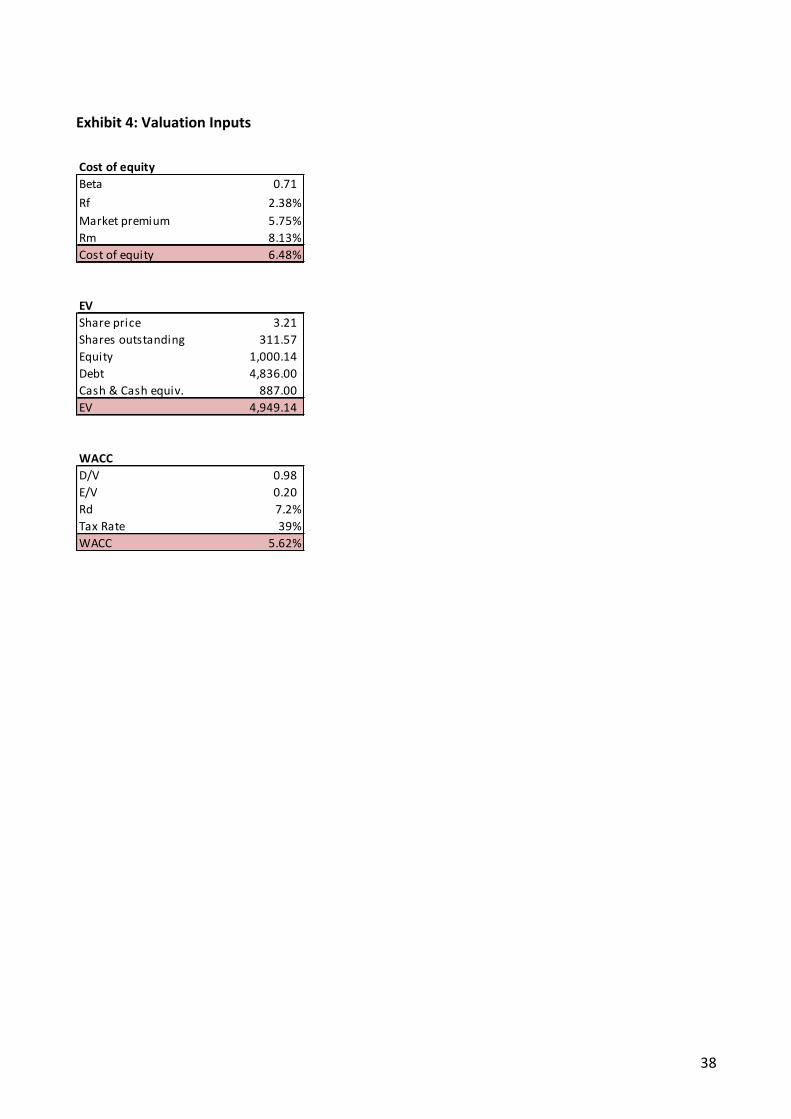

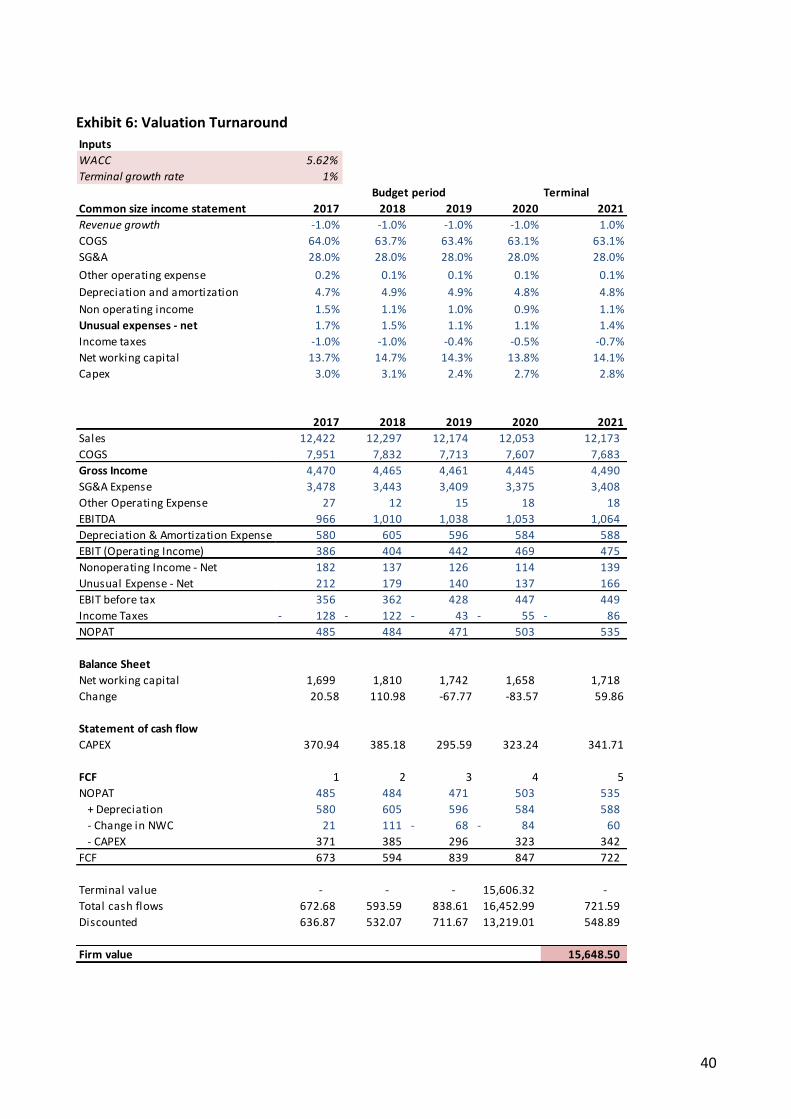

reasonable interestmay deteriorate if their performance does not improve in the near future.However,webelievethecurrentdebtlevelisexcessiverelativetoJCP’scurrentrevenues,andwethereforerecommendthatJCPloweritsinterestexpensebydiligentlypayingdownexistinglong-termdebtandrefrainingfromtakingnewloans.5.4ValuationThefollowingsectionpresentsavaluationofJCPbasedonaprojectionofthecompany’sfuturecashflows. Two valuations are presented, namely a base case valuation and a post-restructuringvaluationwheretheturnaroundinitiativesareimplementedandaccountedforintheprojections.5.4.1BaseCaseAssumptionsThe valuation of JCP is conducted using an all-equitymethod based on cash flows rather thanearningsandnottakingintoaccountthecompany’scapitalstructureinthevaluation(Shefter,n.d.).TodiscountprojectedfuturecashflowsforJCP,it isnecessarytoestimatethecompany’sWACCandallthesubcomponentsusedinthecalculationillustratedinthefollowing:

!"## = %& ∗ 1 − *+ ∗ ,- + /0 ∗1-

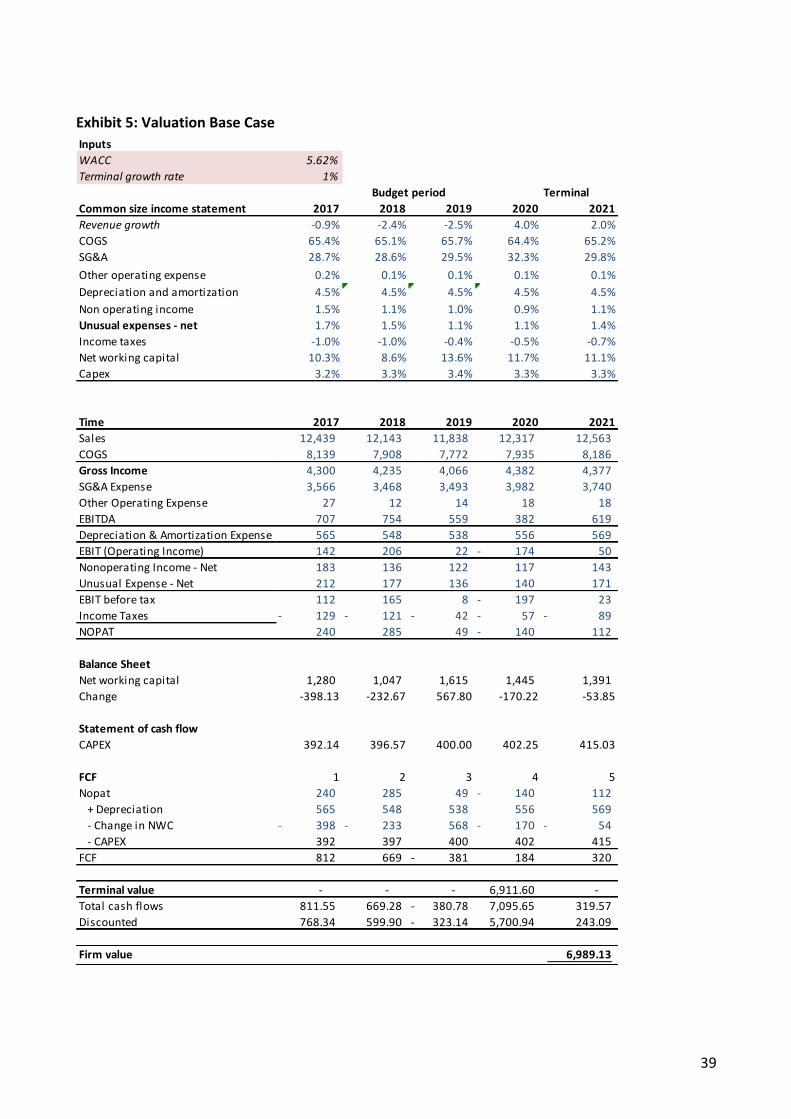

Forthebasecaseanalysis,allcomponentsarebasedonthecompany’s2016financialstatementexcept for themarketpremium,risk freerateandtax ratewhicharebasedonthemost recentestimates.Thecostofdebt isestimatedbydividing2016 interestpaymentswith total leverageyielding/& = 7.2%.TheD/VandE/Vratiosarebasedonthecompany’senterprisevalueandlevelofdebtandequity.Therisk-freerateisbasedonthe10-yearUSTreasuryRate(U.S.DepartmentoftheTreasury,2017)andthemarketriskpremiumisderivedfromareportbyKPMG(2017).JCP’sbetaisobtainedfromGoogleFinance(2017)butadjustedusingtheBloombergmethodwiththeformula:adjustedbeta=2/3*rawbeta+1/3*1,inordertogeta‘cleaner’beta,lesssensitivetoanyshocks ormarket riseswhich could producemisleading results (NYU Stern, n.d.). Following thisadjustment,abetaof0.7isobtained.Usingtheseinputsresultsinacostofequityof6.5%,whichyieldsaWACCof5.6%.OnemightbeinclinedtothinkthataWACCof5.6%seemstoolowforacompany in need of a turnaround. However, similar and even lower results for theWACC areobtainedwhenconsultingexternalsources.Gurufocus(2017)estimatesaWACCforJCPof5.11%andbasedonthisdata,theaverageWACCamongJCPanditspeersis6.55%.TheWACCfoundusingthemethodologyabovethereforeappearstobeareasonableinputinthevaluation.Theprojectionsinthebasecasearebasedonmeanbrokerestimatesfortheperiod2017-2020forSales,COGS,SG&A,interest,Capexandnetworkingcapital(Factset,2017).Sincebrokerprojectionsareonlyavailablefortheperiod2017to2019andforsomeitems2017-2020,threeyearrollingaveragesareusedfortheremainingyears.

22

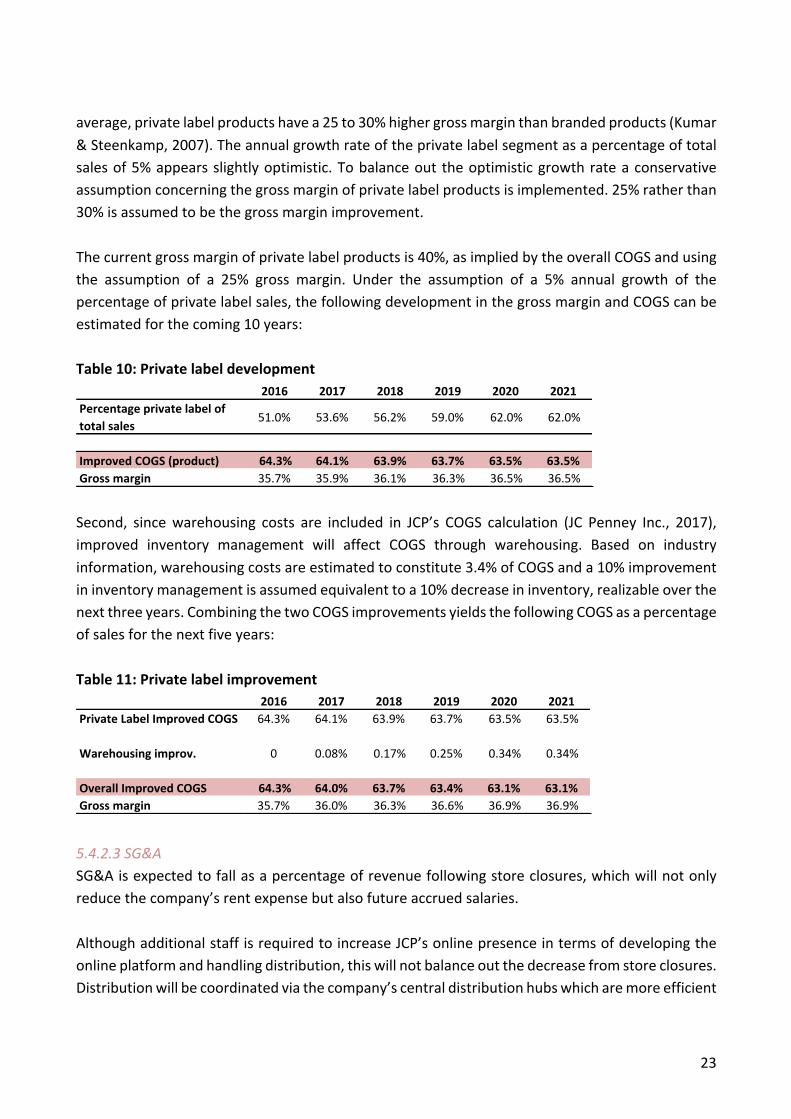

Thecashflowsarediscountedbacktothestartof2017asthiswillenableapropercomparisontothevalueobtainedintheliquidationanalysis.Basedonthesebasecaseprojections,thevalueofJCPisestimatedtobe$6.99billioninthebasecase.5.4.2RestructuringAssumptionsImplementationoftheoutlinedturnaroundplanisexpectedtoresultinchangesinseveralofthecost and margin ratios outlined previously, and these changes are presented in the followingsection.5.4.2.1RevenueAspreviouslyhighlighted,firmsintheretailindustryareunderincreasedpressureduetodisruptionssuchasthegrowthinonlineretailingandfiercecompetition,andthisalsohasimplicationsfortheprojected futurerevenueof JCP.Thehighlightedrestructuring initiatives focusonbothcostandrevenuewithamajorityemphasisonthecostsideasthiswashighlightedasakeyissueforJCP.Effortstoincreaserevenueare,however,pursuedbyincreasingJCP’sonlineexposure.Arangeofunprofitablestoresareclosed,toreducethecompany’sSG&Aandincreaseitsrevenueperstore.Despiteahigher revenueper store, JCP’soverall salesareexpected todeclinebecauseof storeclosings,somewhatoffsetbyanincreaseinitsonlinesales.Giventhegeneralpressurefacingtheindustry, JCP’srevenue isnotexpectedto increaseoverthebudgetperiod.Only intheterminalperiodwillrevenuegrowthconvergeto1%asitisassumedthattherestructuringinitiativeshavebeenimplementedatthatpoint,andthatJCP’sonlineservicehasgainedtraction.Closingstoreswillresultinlowersaleswhileincreasingonlineexposurewillincreasesales.Giventhecurrentdevelopmentoftheindustry,asmalldeclineinsalesisthereforeassumed.5.4.2.2COGS/GrossmarginAlthough‘youcannotcutyourwaytogrowth’severalinitiativesaremadetoreduceJCP’scostsandimprovethecompany’sprofitabilitymargins.Ashighlightedpreviously,theincreasingfocusonthefirm’sprivatelabelsegmentisexpectedtoincreaseJCP’smargins.Betterinventoryorganizationwillalsofacilitatebetterpricingmanagementbyidentifyinglowversushighsellingproductsandenablethecompanytoofferdiscountsononlytheproductsinlowdemand.BasedontheaboveinitiativesJCP’sgrossmarginsareexpectedtoimproveoverthebudgetperiodbeginningin2018.Specifically,the improvement in the grossmarginwill come from; i) the growing emphasis on private labelproductsandii)improvedinventorymanagement.TheincreasedfocusonprivatelabelproductsisassumedtoimpactJCP’sCOGSinthefollowingway:CurrentemphasisontheprivatelabelinJCP’sproductportfoliois51%ofsales,whichisintendedtoincreaseannuallyby5%untilitreaches60%atwhichpointitisexpectedstagnateasthecompanyreachesitstargetscopefortheproductportfolio.Thepercentageofprivatelabelsalesisdepictedforthenextfiveyearsintable10.By2020,privatelabelproductswillconstitute62%ofsales.On

23

average,privatelabelproductshavea25to30%highergrossmarginthanbrandedproducts(Kumar&Steenkamp,2007).Theannualgrowthrateoftheprivatelabelsegmentasapercentageoftotalsalesof5%appearsslightlyoptimistic.Tobalanceout theoptimisticgrowthrateaconservativeassumptionconcerningthegrossmarginofprivatelabelproductsisimplemented.25%ratherthan30%isassumedtobethegrossmarginimprovement.Thecurrentgrossmarginofprivatelabelproductsis40%,asimpliedbytheoverallCOGSandusingthe assumption of a 25% gross margin. Under the assumption of a 5% annual growth of thepercentageofprivatelabelsales,thefollowingdevelopmentinthegrossmarginandCOGScanbeestimatedforthecoming10years:Table10:Privatelabeldevelopment

Second, sincewarehousing costs are included in JCP’s COGS calculation (JC Penney Inc., 2017),improved inventory management will affect COGS through warehousing. Based on industryinformation,warehousingcostsareestimatedtoconstitute3.4%ofCOGSanda10%improvementininventorymanagementisassumedequivalenttoa10%decreaseininventory,realizableoverthenextthreeyears.CombiningthetwoCOGSimprovementsyieldsthefollowingCOGSasapercentageofsalesforthenextfiveyears:Table11:Privatelabelimprovement

5.4.2.3SG&ASG&Aisexpectedtofallasapercentageofrevenuefollowingstoreclosures,whichwillnotonlyreducethecompany’srentexpensebutalsofutureaccruedsalaries.AlthoughadditionalstaffisrequiredtoincreaseJCP’sonlinepresenceintermsofdevelopingtheonlineplatformandhandlingdistribution,thiswillnotbalanceoutthedecreasefromstoreclosures.Distributionwillbecoordinatedviathecompany’scentraldistributionhubswhicharemoreefficient

2016 2017 2018 2019 2020 2021Percentage0private0label0of0total0sales 51.0% 53.6% 56.2% 59.0% 62.0% 62.0%

Improved0COGS0(product) 64.3% 64.1% 63.9% 63.7% 63.5% 63.5%Gross0margin 35.7% 35.9% 36.1% 36.3% 36.5% 36.5%

2016 2017 2018 2019 2020 2021Private/Label/Improved/COGS 64.3% 64.1% 63.9% 63.7% 63.5% 63.5%

Warehousing/improv. 0 0.08% 0.17% 0.25% 0.34% 0.34%

Overall/Improved/COGS 64.3% 64.0% 63.7% 63.4% 63.1% 63.1%Gross/margin 35.7% 36.0% 36.3% 36.6% 36.9% 36.9%

24

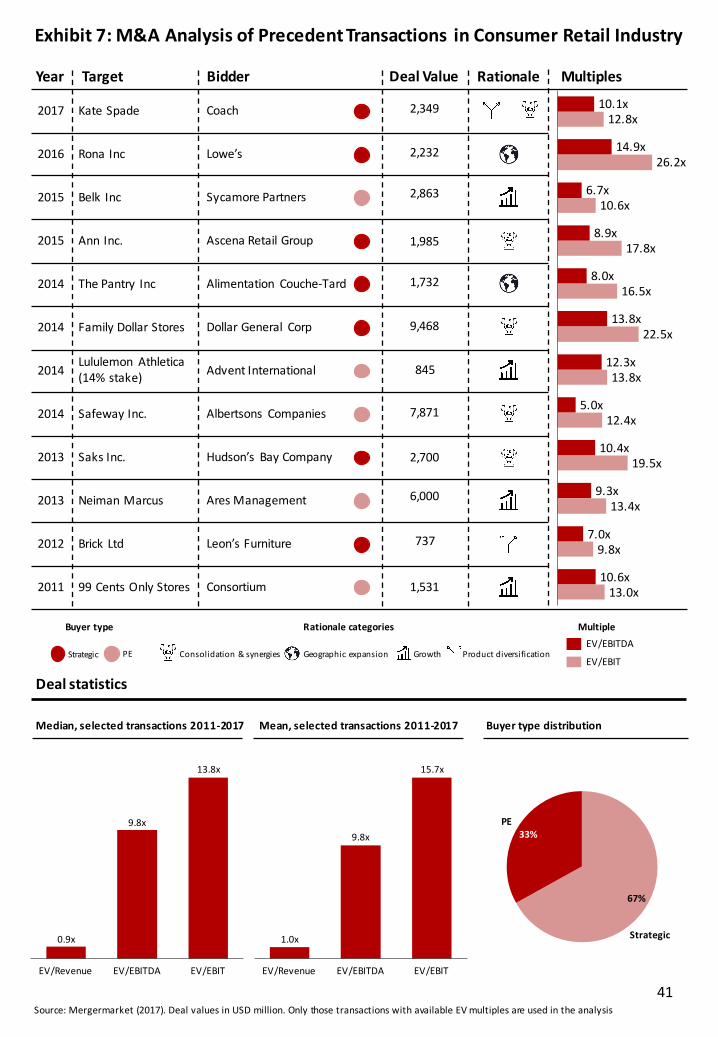

and require less staff compared to its physical stores. Development of the online platformwillrequireanexpansionofbackofficeemployeesandwillincludeoutsourcingofcustomerservicetoe.g.India,wherecostoflaborischeaper.Thus,theneteffectoftherelocationofresourceswillnotcounterweightheimmensedecreaseinSG&Afromstoreclosures.Additionally,thestrategicfocusonimprovedcustomerservicerequiresconsequentinvestmentinemployeetraining,development,andspecialization,thusincreasingSG&A.TakingthesethreeSG&Aincreasedriversintoaccount,JPC’stotalcostsareestimatedtobelessthanthedecreaseinSG&Afromstoreclosures.Hence,anoveralldecreaseinthecompany’sSG&Aoversalesisexpected.AlthoughJCPdidnotranksignificantlyaboveaverageintermsofSG&Aexpense,onemightexpectthe company to have lower expenses compared to a high-end retailer such as Nordstrom andBloomingdales(partofMacy’s)whomightofferpersonalshoppersandrelatedservicesandchoosemore high-end locations for their stores. JCP should therefore target an SG&A ratio below theindustryaverage,andfollowingstoreclosuresSG&Aasapercentageofrevenuewillthereforebereducedto28%,andshouldbedecreasedfurtherovertime.5.4.2.4InterestPaymentsIntherestructuringplan,agoalforreducingthecompany’soutstandingdebtwasdefined,whichwillaffectthecompany’sinterestpaymentsdownwards.Partofthecashgeneratedfromthesaleofphysicalstoresandlowerrentpaymentswillthusbeallocatedtorepayingtheprincipaloftheoutstandingdebt.Lower interestpaymentswill increasethecompany’sbottomlineandfreeupmorecashtofinanceongoingoperationsandhelpexpandthecompany’sonlinepresence.Itwill,however,notaffecttheFCFofthemodelasthevaluationisbasedonNOPATratherthanNetincometoremovetheeffectofcapitalstructureonthevaluation.5.4.2.5CapitalExpendituresTheincreasedcommitmenttoitsonlineplatformislikelytorequireaninvestmentinITsoftwaresuchascloudspace,whichwillleadtoanincreaseinCAPEX.However,theCAPEXsavingsrealizedfromclosingstoresareassumedtocounterbalancetheincrease,resultinginaneteffectonCAPEXofzero.5.4.3M&AAnalysisA finaloption tobeevaluated iswhether JCPmight serveasanattractiveacquisition target (orbidder), and whether this would generate additional value to shareholders. As emphasizedcontinuously, traditionalretailerstodayfaceseveralchallenges, includingstagnatinggrowth,thegrowingpressure fromonline retailers, and fierce competitionerodingprofitability, allofwhichpushesfirmstoseeknewwaysofachievinggrowth(Friedman,etal.,2016).In2016,consolidationintheretailindustryreachedanall-timehighsincetherecession,allegedlydrivenbystrongbalancesheets,cashaccumulationaswellasstagnatinggrowth-allofwhichareexpectedtocontinuegoing

25

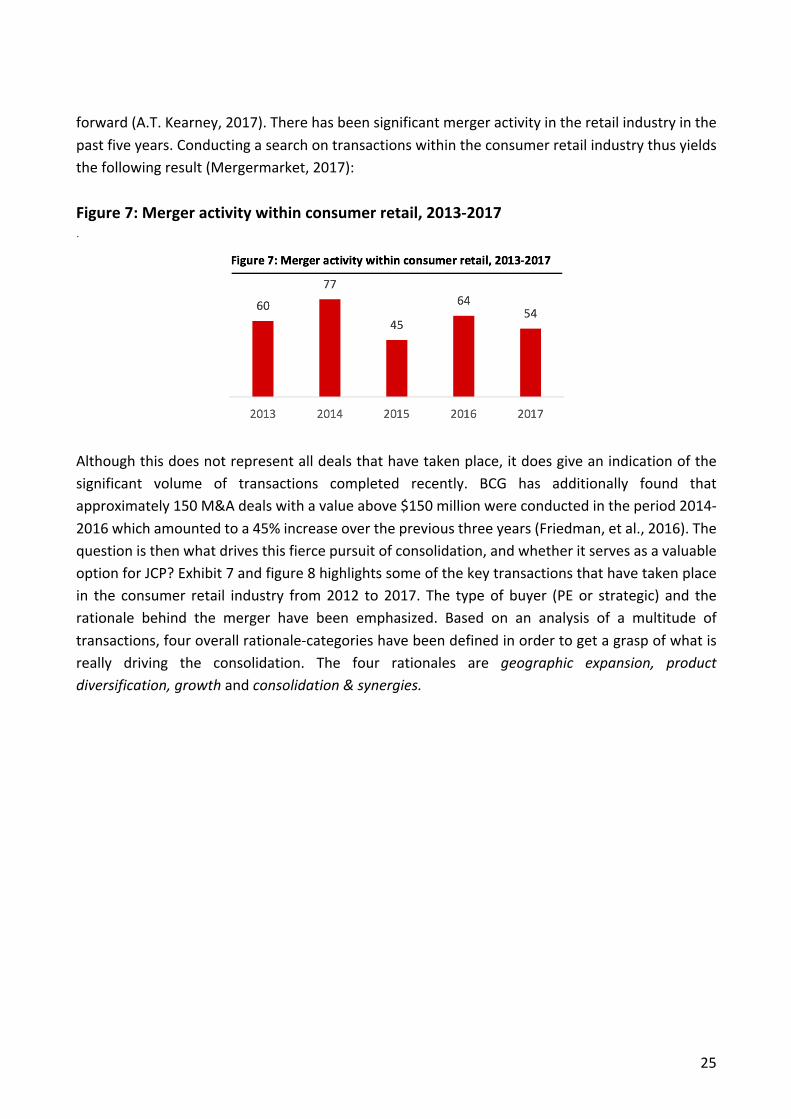

forward(A.T.Kearney,2017).Therehasbeensignificantmergeractivityintheretailindustryinthepastfiveyears.Conductingasearchontransactionswithintheconsumerretailindustrythusyieldsthefollowingresult(Mergermarket,2017):Figure7:Mergeractivitywithinconsumerretail,2013-2017.

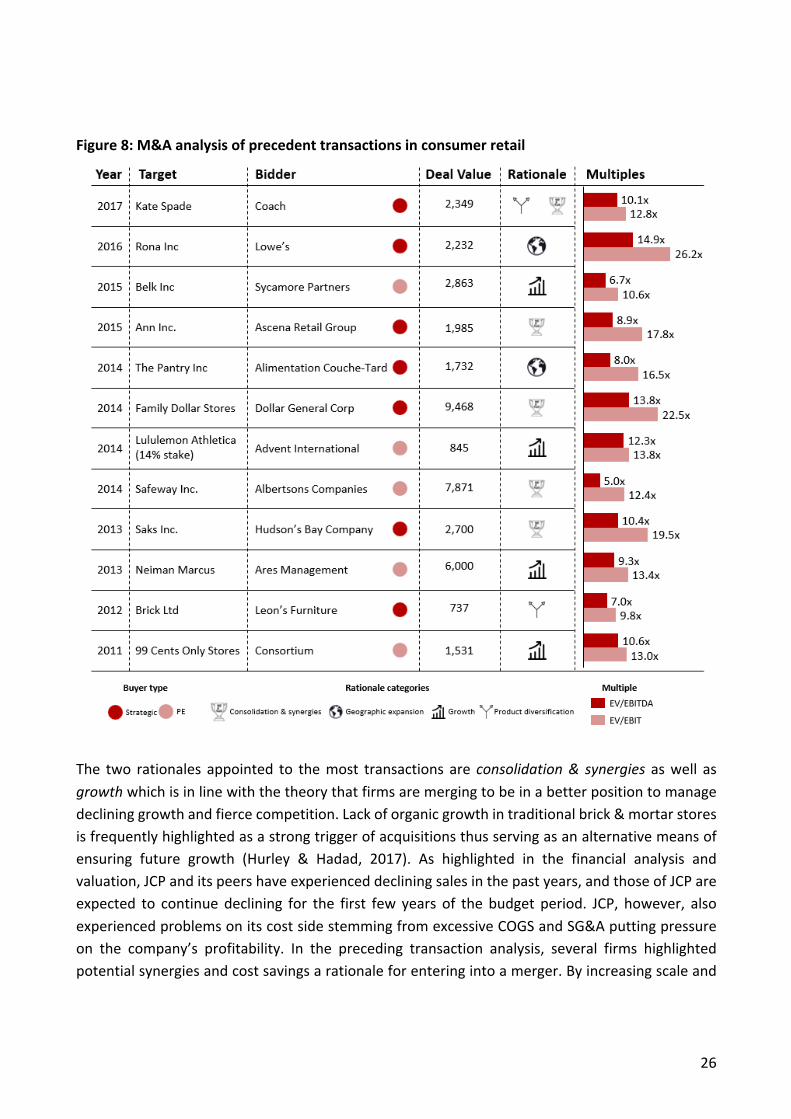

Althoughthisdoesnotrepresentalldealsthathavetakenplace,itdoesgiveanindicationofthesignificant volume of transactions completed recently. BCG has additionally found thatapproximately150M&Adealswithavalueabove$150millionwereconductedintheperiod2014-2016whichamountedtoa45%increaseoverthepreviousthreeyears(Friedman,etal.,2016).Thequestionisthenwhatdrivesthisfiercepursuitofconsolidation,andwhetheritservesasavaluableoptionforJCP?Exhibit7andfigure8highlightssomeofthekeytransactionsthathavetakenplacein the consumer retail industry from2012 to 2017. The typeof buyer (PEor strategic) and therationale behind the merger have been emphasized. Based on an analysis of a multitude oftransactions,fouroverallrationale-categorieshavebeendefinedinordertogetagraspofwhatisreally driving the consolidation. The four rationales are geographic expansion, productdiversification,growthandconsolidation&synergies.

26

Figure8:M&Aanalysisofprecedenttransactionsinconsumerretail

The two rationales appointed to themost transactions are consolidation& synergies aswell asgrowthwhichisinlinewiththetheorythatfirmsaremergingtobeinabetterpositiontomanagedeclininggrowthandfiercecompetition.Lackoforganicgrowthintraditionalbrick&mortarstoresisfrequentlyhighlightedasastrongtriggerofacquisitionsthusservingasanalternativemeansofensuring future growth (Hurley & Hadad, 2017). As highlighted in the financial analysis andvaluation,JCPanditspeershaveexperienceddecliningsalesinthepastyears,andthoseofJCPareexpected to continue declining for the first few years of the budget period. JCP, however, alsoexperiencedproblemsonitscostsidestemmingfromexcessiveCOGSandSG&Aputtingpressureon the company’s profitability. In the preceding transaction analysis, several firms highlightedpotentialsynergiesandcostsavingsarationaleforenteringintoamerger.Byincreasingscaleand

27

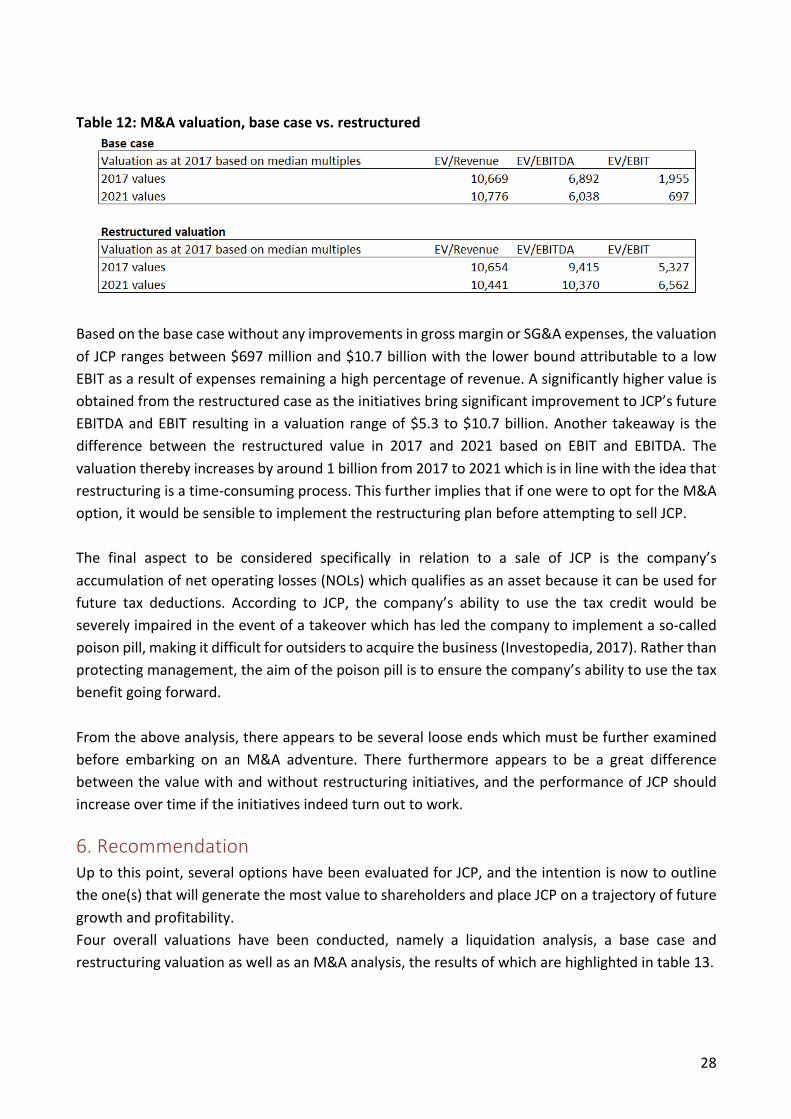

operational efficiencies or obtaining better inventory and supply chain management, thesecompaniestherebysawmergingasawayofimprovingtheircompetitiveness.Basedon theabove, it appears thatmerging could solvemanyof theproblems facing JCP. Thecompanyhas struggledwithboth top lineandbottom linegrowth,and itmustmakeefforts toincreasebothitsefficiencyandprofitability,andthiswouldperhapsbeachievedthroughsynergiesderivedfromcombiningitsoperationswithanothercompany.Mergingis,however,acomplicatedprocessandseveralquestionsmustbeansweredbeforeoptingforthissolution.Thefirstrelatestopotentialbuyers.An obvious candidatewould be one of the company’s close competitors, to increase scale andefficienciesandconsolidatetheirpositionwithintheretailmarket.Thedeclininggrowthofseveralpeers implies that theseplayersmayalsobeexaminingalternativeoptions forobtaining futuregrowththusincreasingthelikelihoodofthembeinginterestedinJCP.A.T.KearneyhasputforwardthreekeytrendsthatwilldominateM&Aintheretailsectorintheforthcomingperiod,onebeingthe growing acquisition activity of private equity and other financial buyers looking forcomplementary firms that bring synergies to their current portfolio businesses. Based thetransactionanalysisbidders inconsumerretailmergershavebeenamixofstrategicandprivateequitybuyers,andbothcategoriescouldthereforeserveaspotentialbiddersforJCP.Thesecond issue in relation toamerger is thedifficulty in realizinganticipatedsynergies.Post-merger integration for retail firms can be particularly challenging because of the difficulties ofclosing down stores, due to lease obligations, the complexity of supply chains as well as thechallengeinrelationtointegratingorupdatingoutdatedITinfrastructures(Friedman,etal.,2016).Torealizeexpectedsynergies,companiesmustproperlyplanforsuchintegrationtopreventthemergerfrombeingacostincreaserratherthanacostandefficiencyenhancer.ThethirdaspectwhichmustbeconsideredisthepriceshareholdersofJCPwouldrealizefollowingitsacquisition.ToestimatethevalueobtainedifJCPweretobeacquired,theaverageandmedianEV/revenue,EV/EBITDAandEV/EBITmultiplesforthehighlightedprecedenttransactionanalysishavebeencalculated.Themedianisusedinthevaluationofthecompanyasitislesssensitivetopotentialoutliers.ThevaluationofJCPiscalculatedbothusingthebasecaseandtherestructuringvalueforboth2017and2021andyieldsthefollowingresults:

28

Table12:M&Avaluation,basecasevs.restructured

BasedonthebasecasewithoutanyimprovementsingrossmarginorSG&Aexpenses,thevaluationofJCPrangesbetween$697millionand$10.7billionwiththelowerboundattributabletoalowEBITasaresultofexpensesremainingahighpercentageofrevenue.AsignificantlyhighervalueisobtainedfromtherestructuredcaseastheinitiativesbringsignificantimprovementtoJCP’sfutureEBITDAandEBIT resulting inavaluationrangeof$5.3 to$10.7billion.Another takeaway is thedifference between the restructured value in 2017 and 2021 based on EBIT and EBITDA. Thevaluationtherebyincreasesbyaround1billionfrom2017to2021whichisinlinewiththeideathatrestructuringisatime-consumingprocess.ThisfurtherimpliesthatifoneweretooptfortheM&Aoption,itwouldbesensibletoimplementtherestructuringplanbeforeattemptingtosellJCP.The final aspect to be considered specifically in relation to a sale of JCP is the company’saccumulationofnetoperatinglosses(NOLs)whichqualifiesasanassetbecauseitcanbeusedforfuture tax deductions. According to JCP, the company’s ability to use the tax credit would beseverelyimpairedintheeventofatakeoverwhichhasledthecompanytoimplementaso-calledpoisonpill,makingitdifficultforoutsiderstoacquirethebusiness(Investopedia,2017).Ratherthanprotectingmanagement,theaimofthepoisonpillistoensurethecompany’sabilitytousethetaxbenefitgoingforward.Fromtheaboveanalysis,thereappearstobeseverallooseendswhichmustbefurtherexaminedbefore embarking on anM&A adventure. There furthermore appears to be a great differencebetweenthevaluewithandwithoutrestructuringinitiatives,andtheperformanceofJCPshouldincreaseovertimeiftheinitiativesindeedturnouttowork.

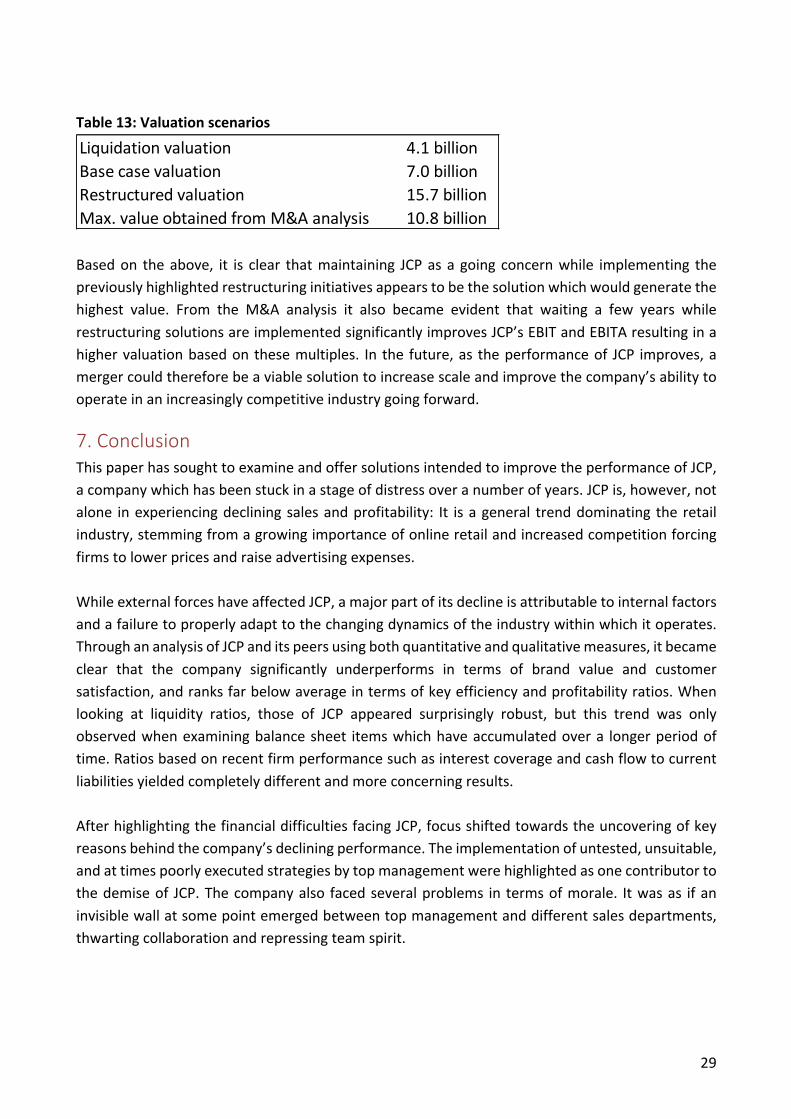

6.RecommendationUptothispoint,severaloptionshavebeenevaluatedforJCP,andtheintentionisnowtooutlinetheone(s)thatwillgeneratethemostvaluetoshareholdersandplaceJCPonatrajectoryoffuturegrowthandprofitability.Four overall valuations have been conducted, namely a liquidation analysis, a base case andrestructuringvaluationaswellasanM&Aanalysis,theresultsofwhicharehighlightedintable13.

29

Table13:Valuationscenarios

Basedon theabove, it is clear thatmaintaining JCPasagoing concernwhile implementing thepreviouslyhighlightedrestructuringinitiativesappearstobethesolutionwhichwouldgeneratethehighest value. From the M&A analysis it also became evident that waiting a few years whilerestructuringsolutionsareimplementedsignificantlyimprovesJCP’sEBITandEBITAresultinginahighervaluationbasedonthesemultiples. In the future,as theperformanceof JCP improves,amergercouldthereforebeaviablesolutiontoincreasescaleandimprovethecompany’sabilitytooperateinanincreasinglycompetitiveindustrygoingforward.

7.ConclusionThispaperhassoughttoexamineandoffersolutionsintendedtoimprovetheperformanceofJCP,acompanywhichhasbeenstuckinastageofdistressoveranumberofyears.JCPis,however,notalone inexperiencingdecliningsalesandprofitability: It isageneral trenddominating the retailindustry,stemmingfromagrowingimportanceofonlineretailandincreasedcompetitionforcingfirmstolowerpricesandraiseadvertisingexpenses.WhileexternalforceshaveaffectedJCP,amajorpartofitsdeclineisattributabletointernalfactorsandafailuretoproperlyadapttothechangingdynamicsoftheindustrywithinwhichitoperates.ThroughananalysisofJCPanditspeersusingbothquantitativeandqualitativemeasures,itbecameclear that the company significantly underperforms in terms of brand value and customersatisfaction,andranksfarbelowaverageintermsofkeyefficiencyandprofitabilityratios.Whenlooking at liquidity ratios, those of JCP appeared surprisingly robust, but this trend was onlyobservedwhenexaminingbalancesheet itemswhichhaveaccumulatedovera longerperiodoftime.Ratiosbasedonrecentfirmperformancesuchasinterestcoverageandcashflowtocurrentliabilitiesyieldedcompletelydifferentandmoreconcerningresults.AfterhighlightingthefinancialdifficultiesfacingJCP,focusshiftedtowardstheuncoveringofkeyreasonsbehindthecompany’sdecliningperformance.Theimplementationofuntested,unsuitable,andattimespoorlyexecutedstrategiesbytopmanagementwerehighlightedasonecontributortothedemiseof JCP.Thecompanyalso facedseveralproblems in termsofmorale. Itwasas ifaninvisiblewallatsomepointemergedbetweentopmanagementanddifferentsalesdepartments,thwartingcollaborationandrepressingteamspirit.

Liquidationvaluation 4.1billionBasecasevaluation 7.0billionRestructuredvaluation 15.7billionMax.valueobtainedfromM&Aanalysis 10.8billion

30

Liquidation and Chapter 11 filingswere deemed less viable solutions for JCP, and restructuringinitiativeswereinsteadhighlightedasawayofimprovingperformance.Bothinitiativestargetingtoplinegrowthandcostreductionswerepresentedwithkeyaspectsbeingstoreclosuresandagrowingonlinepresence.Giventheincreasingneedforcostreductionandachievinghigherscale,amergerwasdiscussedasapotentialoptiontoconsolidateJCP’spositioninthemarket.However,basedonpreviousindustrytransactionsandthecurrentoperatingprofitofJCP,thisappearstobea less valuable option today, but could serve as an opportunity in the future when the firm’sperformancehasstabilized.Failingtoinnovateandcontinuouslyadapttotheexternalenvironmentisoneofthebiggestmistakesacompanycanmake.JCPfellintothedangeroustrapofassumingthat ‘we’ve always done it that way’ was a reasonable argument, and faulty actions furtherdeteriorated performance, letting the firm spiral another step down the organizational distresscurve.Toreturntoprofitability,JCPmustlookinwardsandimplementthehighlightedstrategicandorganizationalchangesandintroduceasustainable,lessriskycapitalstructure.Thefollowingquoteshouldserveasaguidingpillarforthecompanyinthefuture:“itisyourjobtomakeeveryproductyoumakeobsolete. Ifyoudon’tsomeoneelsewill”.JCPshouldbealeadershapingtheindustrydynamicsratherthanmakingex-postadaptationsandbecomingthevictimofcreativedestruction.

31

BibliographyA.T.Kearney,2017.ConsumerandRetainM&Ain2017-OfftoNewPeaksinUncertainTimes.[Online]

Available at: https://www.atkearney.com/consumer-goods/article?/a/consumer-and-retail-m-a-abstract[Accessed13December2017].

Baird, N., 2017. How J.C. Penney Can Fix Its Stores. [Online]Available at: https://www.forbes.com/sites/nikkibaird/2017/02/27/how-to-fix-jcpenneys-stores/#73c797aa1e3e[Accessed11December2017].

Bhasin,K.,2012.RonJohnsonHasNowForcedOutEveryTop-LevelExecutiveFromJCPenney'sPreviousRegime. [Online]Availableat:http://www.businessinsider.com/jcpenneys-cfo-is-leaving-2012-4

Bhasin,K.,2013a.INSIDEJCPENNEY:WidespreadFear,Anxiety,AndDistrustOfRonJohnsonAndHisNew Management Team. [Online]Availableat:http://www.businessinsider.com/inside-jcpenney-2013-2

Bhasin, K., 2013b. JCPenney COO: 'I Hated The JCPenney Culture, It Was Pathetic'. [Online]Availableat:http://www.businessinsider.com/jcpenney-coo-michael-kramer-culture-2013-2

Cohen,A.,2017.IBISWorldIndustryReport45211-DepartmentStoresintheUS,s.l.:IBISWorld.Covert, J., 2013. Ritz crackpot: CEO stays in luxe hotel while Penney flounders. [Online]

Available at: https://nypost.com/2013/02/11/ritz-crackpot-ceo-stays-in-luxe-hotel-while-penney-flounders/

DeSilver, D., 2017. 5 facts about the minimum wage. [Online]Availableat:http://www.pewresearch.org/fact-tank/2017/01/04/5-facts-about-the-minimum-wage/[Accessed13December2017].

Factset,2017.J.C.PenneyConsensusEstimates.s.l.:s.n.Friedman,D.,Drescher,C.,DeBoer,R.&Brown,A.,2016.PostmergerIntegrationinRetail.[Online]

Available at: https://www.bcgperspectives.com/content/articles/merger-acquisitions-postmerger-integration-retail/[Accessed13December2017].

George,B.,Sharpe,J.&McLean,A.N.,2012.AStrategicPerspectiveonBankruptcy.HarvardBusinessReview,16August.pp.1-7.

Glassdoor, 2017a. J.C. Penney Hourly Pay. [Online]Available at: https://www.glassdoor.com/Hourly-Pay/J-C-Penney-Hourly-Pay-E361.htm[Accessed11December2017].

Glassdoor, 2017b. Macy's Hourly Pay. [Online]Available at: https://www.glassdoor.com/Hourly-Pay/Macy-s-Hourly-Pay-E1079.htm[Accessed11December2017].

Glassdoor, 2017c. Kohl's Hourly Pay. [Online]Available at: https://www.glassdoor.com/Hourly-Pay/Kohl-s-Hourly-Pay-E592.htm[Accessed11December2017].

32

Glassdoor, 2017d. Nordstrom Salaries. [Online]Available at: https://www.glassdoor.com/Salary/Nordstrom-Salaries-E1704.htm[Accessed11Decemeber2017].

Google Finance, 2017. J C Penney Company Inc. [Online]Available at: https://finance.google.com/finance?q=NYSE:JCP[Accessed11December2017].

Gulisano,V., 2017.eCommerce Shipping: Is Costor SpeedMore Important toCustomers?. [Online]Available at: https://www.amwarelogistics.com/blog/ecommerce-shipping-cost-vs-speed[Accessed11December2017].

Gurufocus, 2017. JC Penney Co Inc. [Online]Available at: https://www.gurufocus.com/term/wacc/NYSE:JCP/WACC-/JC-Penney-Co-Inc[Accessed13December2017].

Harrigan,K.R.,1980.StrategiesforDecliningIndustries.JournalofBusinessManagement,VolumeFall,pp.20-34.

Harrigan,K.R.,2012.ATurnaroundFramework.ColumbiaCaseWorks,6September.pp.1-9.Hurley,M.&Hadad,J.,2017.IncreasedMergersandAcquisitionswillPropeltheRetailSectorForward.

[Online]Available at: https://www.ibisworld.com/media/2017/07/14/increased-mergers-acquisitions-propel-the-retail-sector-forward/[Accessed12122017].

Investopedia, 2017. J.C. Penney Extends Plan to Prevent Takeovers. [Online]Available at: https://www.investopedia.com/stock-analysis/012417/jc-penney-extends-plan-prevent-takeovers.aspx[Accessed9December2017].

Isidore, C., 2017. JCPenney warns: Losses are growing. [Online]Availableat:http://money.cnn.com/2017/10/27/news/companies/jcpenney-losses/index.html

J. C. Penney Company, Inc., 2017. 2016 Form 10-K. [Online]Availableat:http://ir.jcpenney.com/phoenix.zhtml?c=70528&p=irol-reportsAnnual

JCPenneyInc.,2017.10KFiling2016,s.l.:SEC.JCP,2011.JCPenney2011ProxyStatement,Plano,Texas:s.n.JCP,2016.JCPenneyForm10-K,Plano,Texas:s.n.Kohl’s Corporation, 2017. 2016 Form 10-K. [Online]

Availableat:http://corporate.kohls.com/investors/financial-informationKPMG,2017.EquityMarketRiskPremium–ResearchSummary,s.l.:KPMG.Kumar, N. & Steenkamp, J.-B. E. M., 2007. Private Label Strategy: How to Meet the Store Brand

Challenge.Boston(MA):HarvardBusinessPress.Loeb, W., 2016. J.C. Penney Must Attract Millennials Or Perish. [Online]

Availableat:https://www.forbes.com/sites/walterloeb/2016/12/05/j-c-penney-struggles-with-its-aging-consumer/#6ff9b8641f21[Accessed11December2017].