Embed Size (px)

Citation preview

1

NOVEMBER 2016

COMPANY OVERVIEW

AGENDA

I. COMPANY DESCRIPTION

II. CMPC’S VALUE PROPOSAL

1. LEADING DIVERSIFIED LATIN AMERICAN P&P PLAYER

2. LOW COST PRODUCER WITH WORLD CLASS ASSETS

3. STRONG BALANCE SHEET AND FINANCIAL TRACK RECORD

4. COMMITTED TO SUSTAINABLE DEVELOPMENT AND CORPORATE GOVERNANCE

5. DIVERSIFIED INVESTMENT PORTFOLIO

III. CHALLENGES 2016-2017

IV. APPENDIX

I. COMPANY DESCRIPTION

4

Matte Group

56%

Chilean and

Foreign Investors

34%

Chilean

Pension Funds

10%

CMPC AT A GLANCE

CMPC is a P&P company, established in 1920, that produces solid wood products, pulp,, paper and

packaging products and tissue in Latin America

International rating BBB+ (negative) - Fitch

BBB- (stable) - S&P Baa3 (stable) - Moodys

Local rating AA (Fitch) AA (ICR)

CMPC’s Figures

Sales: 4,844

EBITDA: 1,059

EBITDA Margin: 22%

Net Income: 144

Net Debt: 3,610

Assets: 14,883

Shareholders’ Structure* Market capitalization of

US$5.4 billion

as of October 31st, 2016

Figures for the LTM as of September, 2016 (US$ million) * As of September 30th, 2016. Source: CMPC

II. CMPC’S VALUE PROPOSAL

1. LEADING DIVERSIFIED LATIN AMERICAN P&P PLAYER

6

A DIVERSIFIED BUSINESS PORTFOLIO PROVIDES CMPC A STABLE CASH FLOW

Source: CMPC. Figures in US$ million for the LTM as of September 2016 / Figures do not include Holding and Intercompany Sales.

Main Figures % of third parties total

sales

% of consolidated

EBITDA

Total capacity &

Employees

Pu

lp-F

ore

str

y

Pa

pe

rs

Tis

su

e

Sales: 2,526

Sales 3rd parties: 2,236

EBITDA: 722

EBITDA margin: 29%

647 Th. has. Planted

17 M m3/y harvested

1.7 M m3/y Solid wood

4.1 M tons/y Pulp

5,048 employees

US$11.1 billion in assets

Sales: 878

Sales 3rd parties: 839

EBITDA: 120

EBITDA margin: 14%

1.3 M tons/y

3,538 employees

US$1.4 billion in assets

Sales: 1,771

Sales 3rd parties: 1,769

EBITDA: 241

EBITDA margin: 14%

657 Th. tons/y

8,638 employees

US$2 billion in assets

46%

17%

37%

68%

11%

23%

7

CMPC HAS EVOLVED FROM A LOCAL COMPANY TO A GLOBAL PLAYER

Assets of US$14,883 million

40% outside of Chile

Operations in 8 countries in

Latin America

Forestry Operations

Pulp Operations

Paper and Packaging

Operations

Tissue Operations

Sales of US$4,844 million

45% from operations

outside of Chile

17,605 Direct Employees

46% outside of Chile

CMPC has expanded significantly

throughout Latin America over the past

two decades and has evolved from a local

company to a global player in the P&P

industry

Source: CMPC. Figures for the LTM as of September 2016

8

CMPC HAS A PRODUCT AND GEOGRAPHIC DIVERSIFICATION OF SALES THAT PROVIDES FLEXIBILITY

Source: CMPC. Figures in US$ million for the LTM as of September 2016 / Figures do not include Holding and Intercompany Sales.

2. LOW COST PRODUCER WITH WORLD CLASS ASSETS

II. CMPC’S VALUE PROPOSAL

10

CMPC BENEFITS FROM ITS PRODUCTION COST EFFICIENCIES AND WORLD CLASS ASSETS

Energy investments based

in biomass and natural gas

cogeneration

Access to

low cost fiber Research and Development

to enhance efficiency,

productivity and customer

satisfaction

State of art

facilities strategically

located

11

Eucalyptus Average hardwood growth rate

(m3ssc/ha/year)

Radiata Pine Average softwood growth rate

(m3ssc/ha/year)

11

2023

43 43

E.

Glo

bu

lus

Ibe

ria

n

E.

Glo

bu

lus

Ch

ile

Aca

cia

Ma

ng

ium

Eu

ca

lyp

tus

Bra

zil

E.

Nit

en

s C

hil

e

2 4 511

19

Ru

ssia

Sca

nd

ina

via

Ca

na

da

US

A

Ch

ile

HIGH YIELD FORESTRY ASSETS THAT PROVIDE LOW COST FIBER RESOURCES

647,000 Planted hectares

474,200 Chile

117,600 Brazil *

55,200 Argentina

CMPC Forest

Base is FSCR

Certified

Improvement in Forestry Yields **

** Evolution of the weighted increase of volume per

hectare expected for eucalyptus and pine plantations

established in Chile in the respective year

CMPC has a high quality and sustainable forestry base with fast growth cycles which optimizes capital invested in land,

reduces average distance to mills and increases gains due to genetic and sylvicultural practices

Source: CMPC.

*There is an agreement to acquire from Fibria aprox. 100 Th. hectares of which 39 Th. are planted. CMPC is waiting the approval of Brazilian authorities to consolidate this land

** m3ssc: solid m3 without bark

Over 1 million hectares of land

0%3%

9%

14%

23%

32%

1975 1980 1990 2000 2010 2020P

12

PULP DIVISION: LARGE SCALE PRODUCER WITH GLOBAL CLIENT BASE

Market Pulp Capacity Ranking

Laja BSKP - Chile 340 Th. tons/y

Pacífico BSKP - Chile 500 Th. tons/y

Santa Fe BEKP - Chile

1,500 Th. tons/y

Guaíba BEKP - Brazil

1,759Th. tons/y

Source: CMPC and Hawkins Wright as of August 2016 (million tons)

1,440

2,210

1,610

1,070

905

60

700

1,765

340

100

170

1,335

1,715

3,285

3,560

3,055

3,055

5,300

215

635

60

485

- 2,000 4,000 6,000

Illim

Georgia Pacific

Paper Exellence

Stora Enso

UPM-Kymmene

APRIL

Suzano

CMPC

Arauco

Fibria

BSKP BHKP Other

13

0

100

200

300

400

500

600

700

0 5,000 10,000 15,000 20,000 25,000 30,000

(US

$/T

on

c.i.

f. C

hin

a)

(Th. metrics Tonnes)

0

100

200

300

400

500

600

700

0 5,000 10,000 15,000 20,000 25,000

(US

$/T

on

c.i.

f. C

hin

a)

( Th. metrics Tonnes)

BSKP1 Supply Curve (US$/ton)

CMPC’S CASH COSTS ARE AMONG THE LOWEST OF THE PULP INDUSTRY GLOBALLY

Source: CMPC and Hawkins Wright as of August 2016

(1) BSKP: Bleached Softwood Kraft Pulp

(2) BHKP: Bleached Hardwood Kraft Pulp

CMPC’s pulp facilities

CMPC’s pulp facilities

BHKP2 Supply Curve (US$/ton)

CMPC’s average distance from… to…

Source: CMPC

163 Km.

93 Km.

119 Km.

208 Km.

80 Km.

93 Km.

99 Km.

260 Km.

(by train)

(by train)

(by train)

(by barges)

Laja

Guaíba

Pacífico

Santa Fe

Plantations Ports

II. CMPC’S VALUE PROPOSAL

3. STRONG BALANCE SHEET AND FINANCIAL TRACK RECORD

15

Financial Debt / Equity (Covenant: <0.8x) Interest Coverage Ratio (Covenant: >3.25x)

Sales Evolution (US$ million) EBITDA and EBITDA Margin Evolution (US$ million)

KEY FINANCIAL FIGURES AS OF SEPTEMBER 30TH, 2016

Source: CMPC

Source: CMPC

Source: CMPC

Source: CMPC

4,759 4,974 4,900 4,841 4,844

2012 2013 2014 2015 LTM

914964 985

1,0991,059

19% 19% 20%23% 22%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

200

400

600

800

1,000

1,200

2012 2013 2014 2015 LTM

0.48x 0.48x

0.56x

0.52x0.53x

0.44

0.46

0.48

0.50

0.52

0.54

0.56

0.58

2012 2013 2014 2015 3Q16

5.45x

5.67x

5.31x

5.94x

5.19x

4.80x

5.00x

5.20x

5.40x

5.60x

5.80x

6.00x

2012 2013 2014 2015 3Q16

16

4.5

1.5

2.3

0.9

2.8

1.5

3.3

1.8

3.4

3.8

3.4

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0 Acquisition of Pacífico and Santa

Fe I

Santa Fe II

Investment Period

Guaíba I

AcquisitionGuaíba II

Investment Period

DEMONSTRATED CAPACITY TO MANAGE LEVERAGE

Net Debt / EBITDA

Source: CMPC

17

- -

499 498

-

495

991

479

57

260

152 195

147

281

106

47

2016 2017 2018 2019 2020 2021/2022 2023/29 2030/39

Bonds Banks Interests

CMPC’S DEBT PROFILE AS OF SEPTEMBER 30TH, 2016

Amortization schedule (as of today)

Source: CMPC

Debt Profile

Average term: 5.7 years

Average cost in US$: 4.2%

Total Debt: US$4,206 million

Cash: US$596 million

Net Debt: US$3,610 million

Debt by Type Debt by Interest Rate Debt by Currency Debt by Issuer

Banks

7%

Bonds

71%

BNDES

14%

ECA

8%

Fixed

Rate

94%

Variable

Rate

6%

CLP

3%

USD 87%

BRL

6%

Other

4%

Inversion

es CMPC

72%

Tissue

6%

Pulp

22%

II. CMPC’S VALUE PROPOSAL

4. COMMITTED TO SUSTAINABLE DEVELOPMENT AND CORPORATE GOVERNANCE

19

CORPORATE SOCIAL RESPONSIBILITY AND SUSTAINABILITY

Throughout its history, CMPC has maintained a way of doing business and engaging with employees,

customers and shareholders. With a 96-year tradition, the following five values summarize our vision of how we

should work.

Strict compliance

with the legal

regulation

Consideration for

neighbors' needs Respect for people

Fairness when

competing

Care of the

environment

Development of

certified

renewable

forest plantations

Replacement

of fossil fuels

with biomass

Efficient use of

energy, water

and raw

materials

Certified

industrial

processes

Recycling old

paper

5 Pillars of CMPC’s Environmental Agenda

20

BOARD OF DIRECTORS

CORPORATE GOVERNANCE IN CMPC

Luis Felipe

Gazitúa

Chairman

Vivianne

Blanlot

Jorge

Marín

Independent

Jorge

Larraín Jorge

Matte

Ramiro

Mendoza

Bernardo

Matte Rafael

Fernández

Independent

Pablo

Turner

Current members: Vivianne Blanlot,

Rafael Fernández and Jorge Marín CMPC’s Board of

Directors

CMPC’s

Management

CMPC’s Subsidiary’s

Board of Directors

CMPC’s Subsidiary’s

Management

Appoints

Board

Members

Directors

Committee

Financial Risk

Committee

Audit

Committee Comptroller

Current members: Vivianne Blanlot

and Ramiro Mendoza

Current members: Bernardo Matte

and Jorge Marín

Other initiatives: Business Ethics Guidelines, Corporate Governance Guidelines, Antitrust Guidelines,

Anticorruption Policies, Whistle Blower Hotline

II- CMPC’S VALUE PROPOSAL

5. DIVERSIFIED INVESTMENT PORTFOLIO

22

CMPC HAS A DIVERSIFIED INVESTMENT PORTFOLIO

CMPC is finishing the largest investment cycle of its

history

Guaíba II Project – May 2015

Tissue paper machine in Altamira, México (2Q15)

Cogeneration Facilities: Puente Alto Mill,

Talagante Mill and Altamira Mill.

Focus in 2016-2017

Continue to increase tissue paper and conversion

capacity

Cañete Mill (Peru)

• Capacity: 50 th. tons/year

• Investment: US$ 139 million

• Start-up: 1Q17

Operational continuity projects to further increase

efficiency

Laja Pulp Mill

Guaíba I Pulp Mill

Maule Boxboard Mill

Cañete Mill - Perú

23

TISSUE DIVISION: CMPC IS FAVOURABLY POSITIONED TO CAPTURE THE DEVELOPMENT AND GROWTH OF THESE MARKETS

Chile

Argentina

Uruguay

Peru

Mexico

Colombia

Brazil

76%

8%

44%

83%

8%

7%

54%

CMPC Tissue Paper Market Share

Source: CMPC as of December 31st 2015

Ecuador

24%

CMPC has a strong

presence in all main

categories of tissue,

sanitary and away

from home

products

CMPC: 134 th. tons*

CMPC: 71 th. tons*

CMPC: 166 th. tons*

CMPC: 27 th. tons*

CMPC: 135 th. tons*

CMPC: 35 th. tons*

CMPC: 99 th. tons*

CMPC successfully

evolved from a local

player into a leading

LatAm tissue player due to its

ability to enter new markets with

high potential based on a

pioneering spirit sustained by

world-class innovations

* CMPC’s tissue paper capacity

24

Per Capita Tissue Consumption

Source: CMPC as of December 2015

CMPC SEEKS TO TAP LATAM UNDERPENETRATED TISSUE MARKETS

High growth potential in Tissue Paper and Sanitary Products in Latin America based on the following fundamentals,

4.4 Kg. 1.2 kg 0.4 kg 0.1 kg

LatAm Average Tissue Consumption 6.1 kg/person

Baby Diapers Feminine

Protection Incontinence

LatAm Sanitary Products Penetration*

73% 72%

TISSUE PAPER Population growth and urbanization

Economic growth

Increase in per capita consumption

Higher quality products

SANITARY PRODUCTS Child population growth

Economic growth

Higher penetration levels

14%

Source: Price Hanna

India

Phillippines

Indonesia

Vietnam IranThailand

RussiaSouth AfricaEcuadorColombia MalaysiaGuatemala China

Peru

VenezuelaBrazil Turkey

RomaniaArgentina

El SalvadorLebanonMexico Slovakia

TaiwanCzech RepublicRepublic of Korea

Lithuania

Poland Estonia CroatiaHungaryChileCosta Rica Italy FrancePortugal

SpainGreece

AustraliaBelgiumJapan

NetherlandsSlovenia New Zealand

Israel IrelandUK

FinlandDenmark

SwitzerlandGermany

Austria Sweden

Hong KongCanada

USA

0.00

5.00

10.00

15.00

20.00

25.00

0 10 20 30 40 50

Tís

su

e P

ap

er

Ap

p. C

on

su

mp

tio

n (

k/h

ab

.)

GNI p/c (thousand US$ at ppp)

III. CHALLENGES 2016-2017

26

CMPC WILL BASE ITS STRATEGY IN 4 PILLARS TO CONSOLIDATE ITS LEADERSHIP IN THE P&P INDUSTRY

1. Continue running at full capacity across all business units

2. Expand tissue capacity with new facility in Peru

3. Focus in cost control and enhance efficiency

4. Reduce leverage, lower Net Debt / EBITDA

among all business divisions and countries

IV. APPENDIX

28

APPENDIX I: ANNUAL CAPACITY BY PRODUCT/COUNTRY

Business Area Product / Country Capacity

Forestry

Sawn wood 1.0 M m3

Remanufactured wood 190 th. m3

Plywood 500 th. m3

Pulp

BSKP (Laja) 340 th. tons

BSKP (Pacífico) 500 th. tons

BEKP (Guaíba) 1.750 th. tons

BEKP (Santa Fe) 1.496 th. tons

Papers

Boxboard 431 th. tons

Paper Bags 93 th. tons

660 M bags

Corrugated Paper 330 th. tons

Corrugated boxes 285 th. tons

Molded Pulp trays 18 th. tons

296 M units

Other Papers 140 th. tons

Tissue

Chile 166 th. tons

Brazil 135 th. tons

Argentina 99 th. tons

Mexico 134 th. tons

Peru 71 th. tons

Uruguay 35 th. tons

Colombia 27 th. tons 28

29

APPENDIX II: NEW BEKP CAPACITY IN THE 4OO+ MILLION TONNES FIBER MARKET

Source: Own elaboration based on RISI 5-year Forecast (2016-2020) Data 2015 - June 2016 + HW data April 2016

422 million tons of total

fibers

62 million tons

of market pulp

30 million tons

of BHKP

Fiber World Consumption required

to produce 408 million tons of

Paper&Board Virgin fiber used to produce

Paper&Board

(million tons) Market Pulp consumed to

manufacture Paper&Board

(million tons)

Virgin Pulp 181 million

tons (43%)

Recovered Paper

241 million tons

(57%)

Market Pulp

62 million tons

(34%)

Integrated 119

million tons

(66%)

BSKP 24

BHKP 30

Sulphite

UKP 2

Mec 5

30

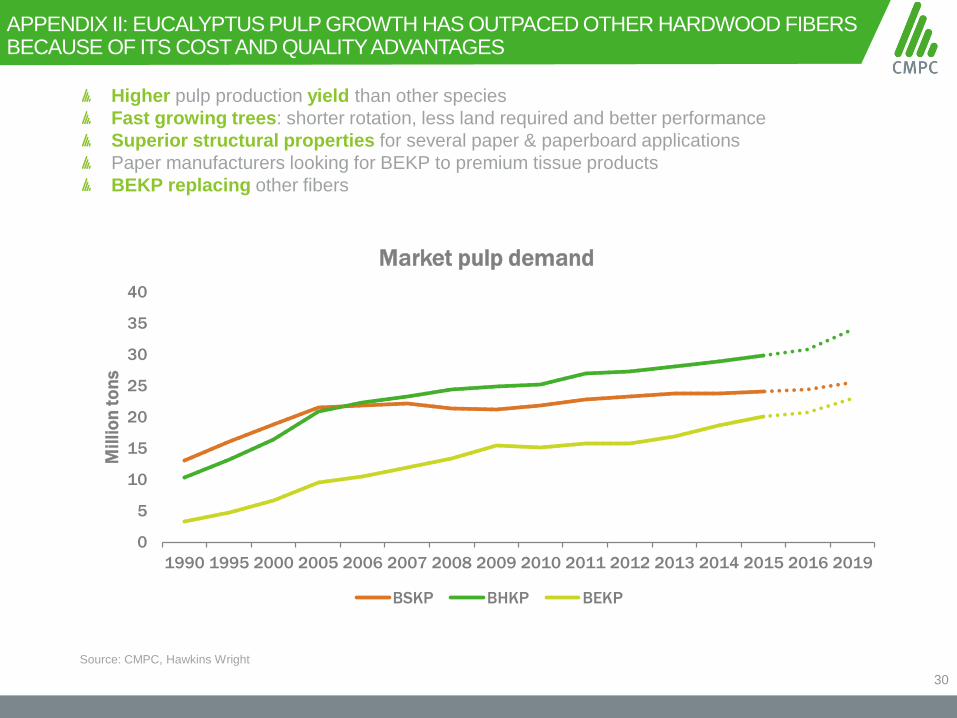

APPENDIX II: EUCALYPTUS PULP GROWTH HAS OUTPACED OTHER HARDWOOD FIBERS BECAUSE OF ITS COST AND QUALITY ADVANTAGES

Source: CMPC, Hawkins Wright

Higher pulp production yield than other species

Fast growing trees: shorter rotation, less land required and better performance

Superior structural properties for several paper & paperboard applications

Paper manufacturers looking for BEKP to premium tissue products

BEKP replacing other fibers

0

5

10

15

20

25

30

35

40

1990 1995 2000 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2019

Millio

n t

on

s

Market pulp demand

BSKP BHKP BEKP

31

APPENDIX II: THE PAPER INDUSTRY HAS GROWN, SPECIALLY IN THE PACKAGING SEGMENT

Since 1992 paper production has grown 61%, mainly explained by: 106 million additional tons of packaging paper

33 million additional tons of P&W papers

18 million additional tons of tissue papers

Since 2007, Packaging and Tissue have continued to grow, while P&W has declined

Source: RISI

Mill

ion T

ons

32 33 34 35 35 36 36 38 39 38 37 37 39 38 38 38 37 32 32 31 30 28 26

74 76 83 85 85 93 94 98 104 99 102 105 112 113 117 119 116 106 111 110 108 106 105

114 115 123 127 131

138 138 144

148 148 156 161 171 177

186 194 196 191

206 210 214 220 226 15 16

16 17 18 19 19

20 21 22

23 23

24 25 26

27 28

28

29 30 31 32 33

15 14 15

15 16 16 15

16 15 15

14 15

15 14

15 15 15

14

16 17 16 16 16

-

50

100

150

200

250

300

350

400

450

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mil

lio

n t

on

s

Newsprint P&W Packaging Tissue Other P&B

32

CONTACT INVESTOR RELATIONS

Colomba Henríquez

+(562) 2 441 2791

Isidora Farías

isidora.farí[email protected]

+(562) 2 441 2713

Disclaimer:

This document provides information about Empresas CMPC SA. In any case this constitutes a comprehensive analysis of the financial, production and

sales situation of the company, so to evaluate whether to purchase or sell securities of the company, the investor must conduct its own independent

analysis.

In compliance with the applicable rules, Empresas CMPC SA. publishes this document in its web site (www.cmpc.cl) and sends to the Superintendencia

de Valores y Seguros, the financial statements of the company and its corresponding notes, which are available for consultation and review.