Embed Size (px)

Citation preview

Commercial economics week 5

About About Franchising Franchising and Leasing and Leasing

About About Franchising Franchising and Leasing and Leasing

Commercial economics week 5

Describe the significance of franchising

Identify the major advantages and limitations of franchising

Discuss the process for evaluating a franchise opportunity.

Evaluate franchising for the franchisor’s perspective.

Describe the franchisor/franchisee relationship.

Commercial economics week 5

Franchising TermsFranchising Terms

FranchisingA marketing system revolving around a two-party

legal agreement, whereby the franchisee conducts business according to the terms specified by the franchisor

Franchise contractThe legal agreement between franchisor and

franchiseeFranchise

The privileges conveyed in the franchise contract

…continued

Commercial economics week 5

Franchising TermsFranchising Terms

FranchiseeAn entrepreneur whose power is limited by a

contractual agreement with a franchisorFranchisor

The party in the franchise contract that specifies the methods to be followed and the terms to be met by the other party

Commercial economics week 5

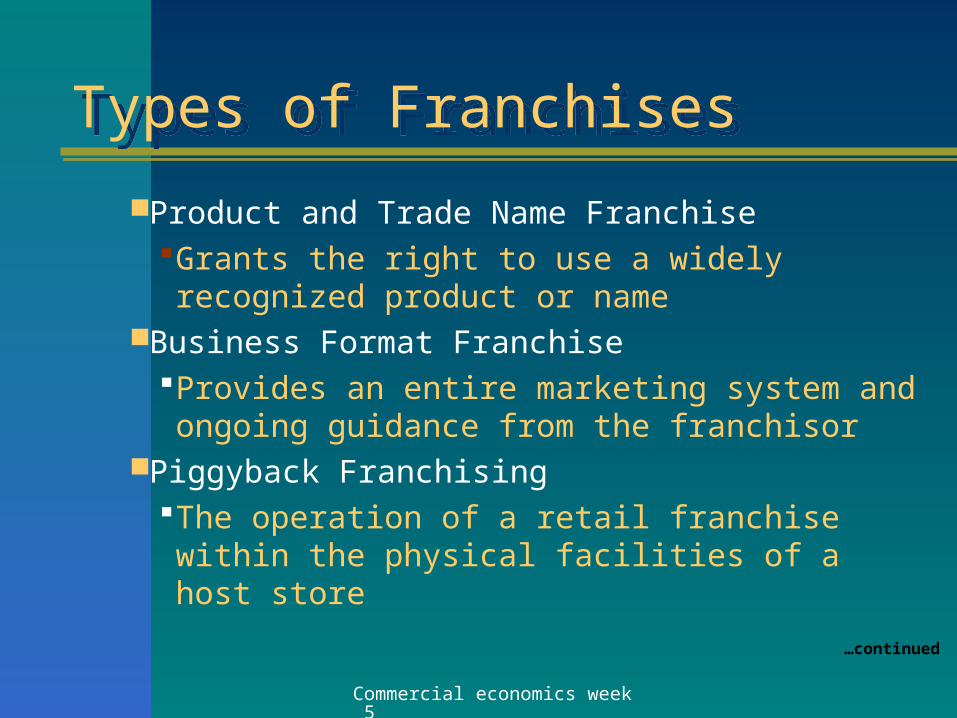

Types of FranchisesTypes of Franchises

Product and Trade Name FranchiseGrants the right to use a widely recognized product or name

Business Format FranchiseProvides an entire marketing system and ongoing guidance from the franchisor

Piggyback FranchisingThe operation of a retail franchise within the physical facilities of a host store

…continued

Commercial economics week 5

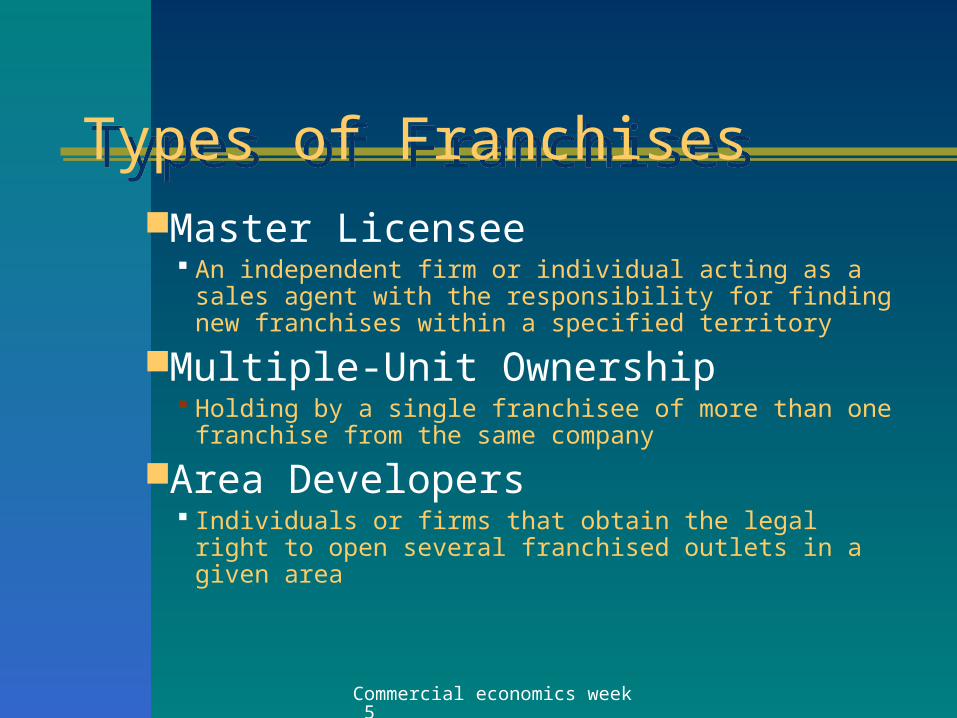

Types of FranchisesTypes of FranchisesMaster Licensee

An independent firm or individual acting as a sales agent with the responsibility for finding new franchises within a specified territory

Multiple-Unit Ownership Holding by a single franchisee of more than one franchise

from the same company

Area Developers Individuals or firms that obtain the legal right to open

several franchised outlets in a given area

Commercial economics week 5

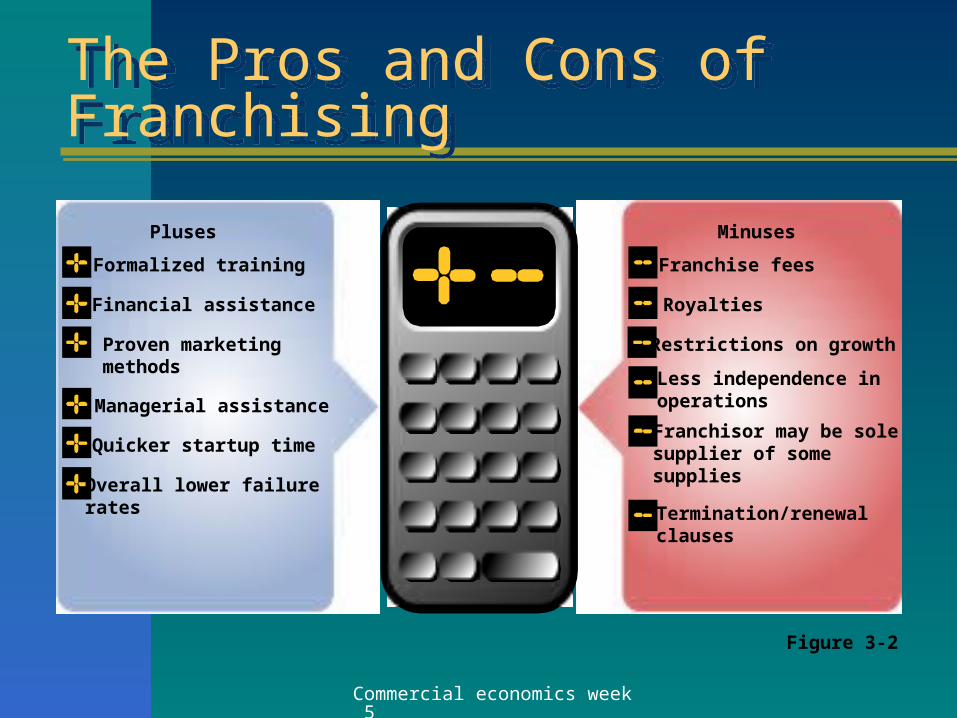

Figure 3-2

Pluses Minuses

Formalized training

Financial assistance

Proven marketingmethods

Managerial assistance

Quicker startup time

Overall lower failurerates

Franchise fees

Royalties

Restrictions on growth

Less independence inoperations

Franchisor may be solesupplier of somesupplies

Termination/renewalclauses

The Pros and Cons of FranchisingThe Pros and Cons of Franchising

Commercial economics week 5

The Advantages of FranchisingThe Advantages of Franchising

Proven marketing concept and customer base

Training Financial assistance Operating assistance

Commercial economics week 5

Financial AssistanceFinancial Assistance

Start-up business costs are normally high and thus by teaming up with a franchise organization, the individual can increase her/his chance of receiving financial help.

The franchisor might chose to use liberal payment schemes to the franchisee in order to get over the initial financial hurdle.

Commercial economics week 5

Operating AssistanceOperating Assistance

The franchisor provides a range of operating services including site selection, bulk purchasing of equipment, and inventory.

Other areas of assistance include the use of an established, nation-wide brand

Commercial economics week 5

Pros and Cons of FranchingPros and Cons of Franching

Advantages– Probability of success

Proven line of business

Pre-qualification of franchisee

– Training Franchisor-

provided– Financial assistance

Franchisor assistance

– Operating benefits Franchisor-aided

Limitations– Franchise costs

Initial franchise fee Investment costs Royalty payments Advertising costs

– Restrictions on Business Operations

– Loss of independence

Commercial economics week 5

Limitations of Franching: Restriction of Business Operations

Limitations of Franching: Restriction of Business Operations

Restricting of sales territoryRequiring site approval and

imposing requirement on the outlet’s appearance

Restricting the goods/services that can be sold

Restricting the resale of

the franchise without their permissionRestricting advertising and hours of operation

Commercial economics week 5

Evaluating Franchise OpportunitiesEvaluating Franchise Opportunities

Locating a Franchise Opportunity Investigating the Potential Franchise

Information sources Independent, third-party sources Franchisors themselves Existing and previous franchisees

Commercial economics week 5

Explanation of CostsExplanation of Costs

Franchise fee First and Last Month’s Rent Leasehold Improvements Equipment Furniture and Fixtures Signage

Insurance, Licences and Permits

Training Initial Inventory Working Capital Royalty

Commercial economics week 5

Global Franchising OpportunitiesGlobal Franchising Opportunities

Historically, many Canadian franchisors have expanded into the United States.

Canadian franchising enterprises are now expanding into countries beyond North America.

Commercial economics week 5

Investigating the Franchise CandidateInvestigating the Franchise Candidate

Three sources of information:

– independent third party sources

– franchisors

– existing and previous franchisees

Commercial economics week 5

Selling a FranchiseSelling a Franchise

Why would a businessperson wish to become a franchisor? Three benefits can be identified:

1. Reduction of capital requirements

2. Increase in management motivation

3. Speed of expansion…continued

Commercial economics week 5

Selling a FranchiseSelling a Franchise

Drawbacks associated with franchising from the franchisor’s perspective.

1. Reduction in control

2. Sharing of profits

3. Increase in operating support

Commercial economics week 5

Franchising FraudsFranchising Frauds

The Rented Rolls Royce Syndrome The Hustle The Cash-Only Transaction The Boast The Big-Money Claim The Couch Potato’s Dream Location, Location, Location The Disclosure Dance

Commercial economics week 5

LEASING and Cross border transactions Key tax and financial considerations Income stream Entry strategy Financing options Debt structuring Cash repatriation Exit considerations

Case Study Business reorganisations

Transaction imperatives

Leasing transactions

Key tax and financial considerations

Commercial economics week 5

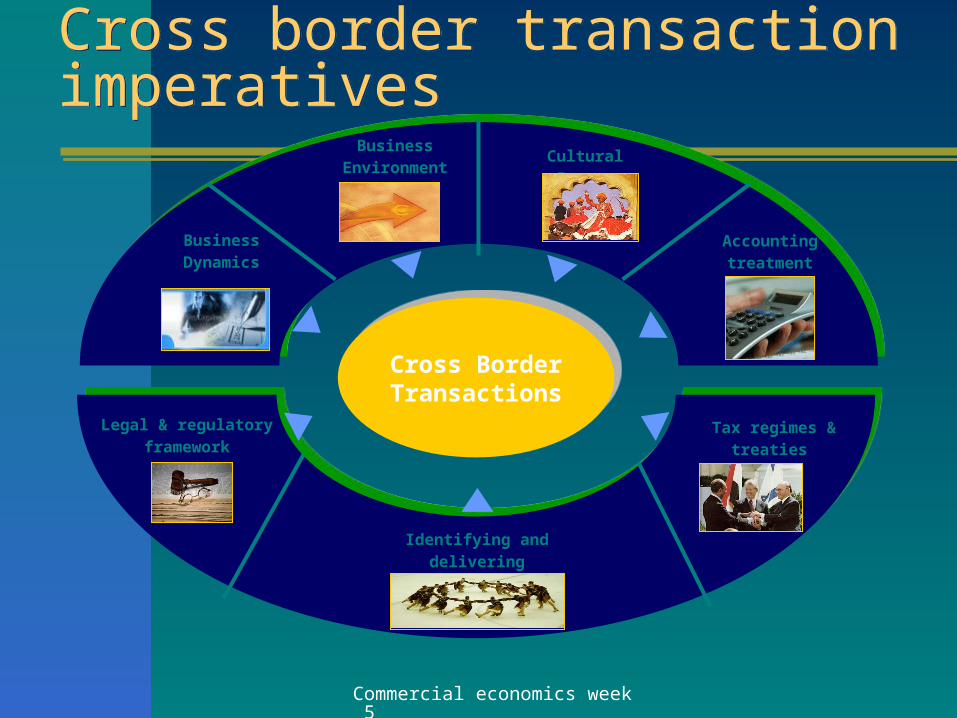

Cross border transaction imperativesCross border transaction imperatives

Cross Border Transactions

Cross Border Transactions

Legal & regulatory framework

Identifying and delivering synergies

Tax regimes & treaties

Business Dynamics

Business Environment

Cultural Issues

Accounting treatment

Commercial economics week 5

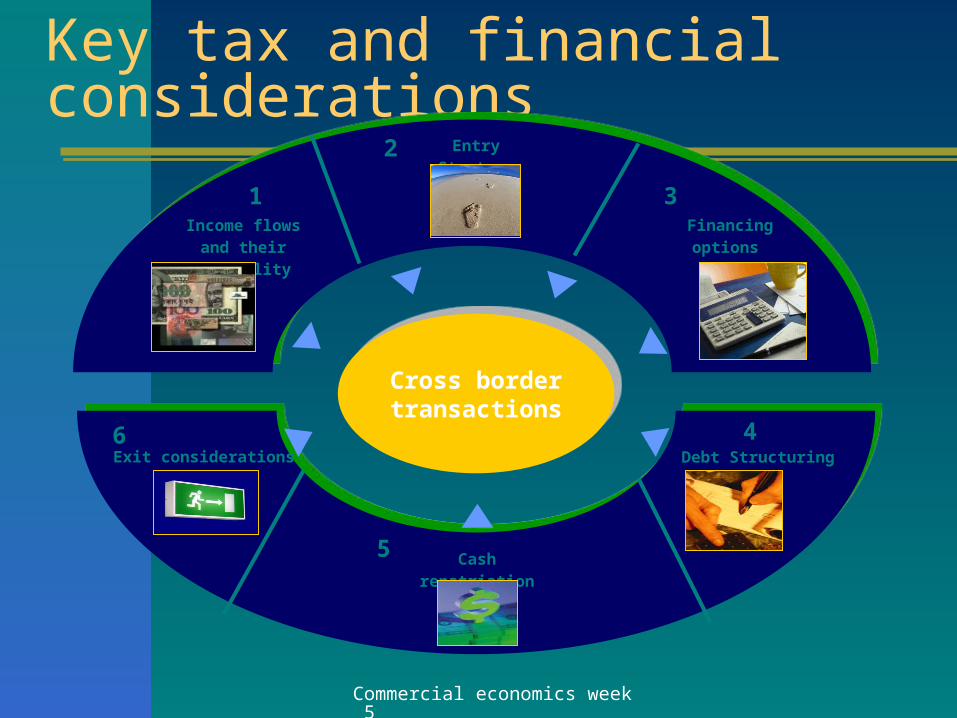

Key tax and financial considerations

Cross border transactions

Cross border transactions

Exit considerations

Cash repatriation

Debt Structuring

Income flows and their taxability

Entry Strategy

Financing options

1

2

3

4

5

6

Commercial economics week 5

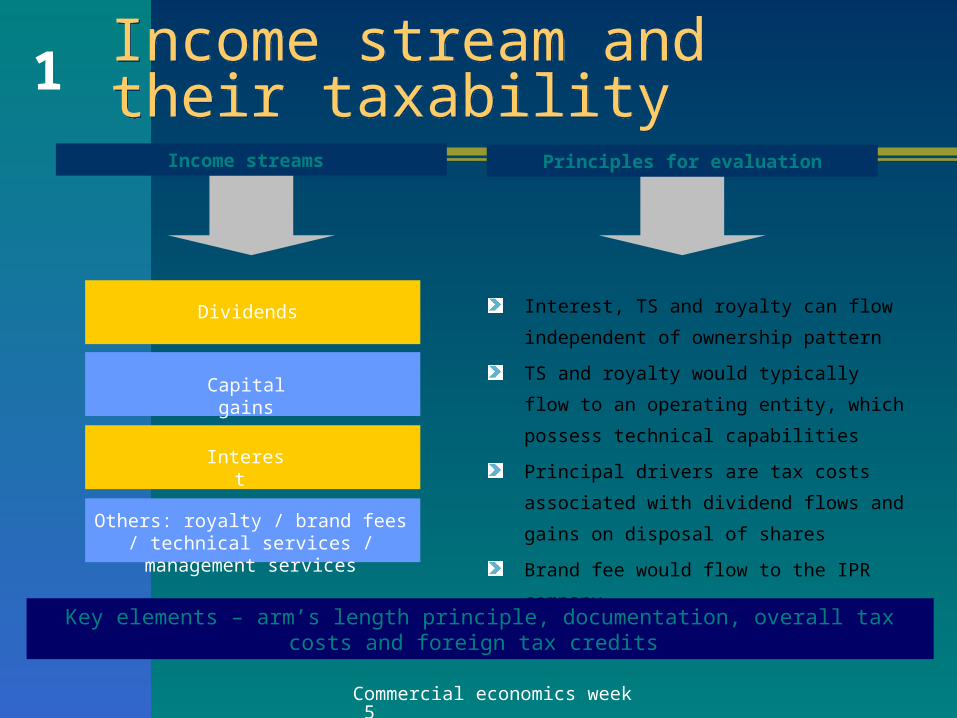

Others: royalty / brand fees / technical services / management services

Income stream and their taxability Income stream and their taxability

Dividends

Capital gains

Interest

Interest, TS and royalty can flow independent

of ownership pattern

TS and royalty would typically flow to an

operating entity, which possess technical

capabilities

Principal drivers are tax costs associated with

dividend flows and gains on disposal of

shares

Brand fee would flow to the IPR company

Income streams Principles for evaluation

1

Key elements – arm’s length principle, documentation, overall tax costs and foreign tax credits

Commercial economics week 5

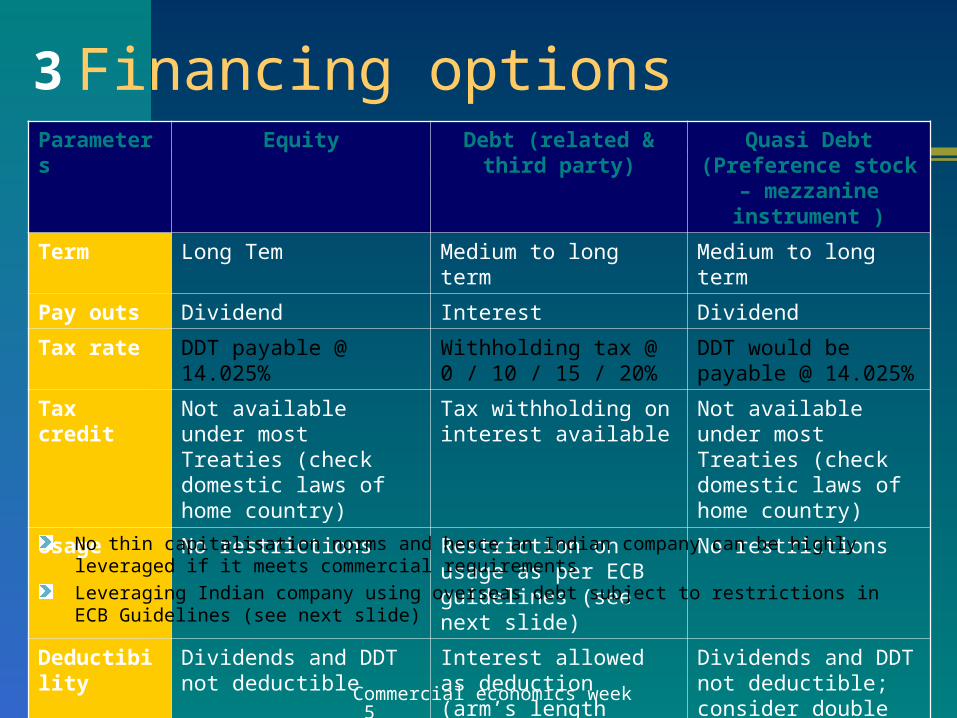

Financing optionsParameters Equity Debt (related & third

party)Quasi Debt

(Preference stock – mezzanine instrument

)

Term Long Tem Medium to long term Medium to long term

Pay outs Dividend Interest Dividend

Tax rate DDT payable @ 14.025%

Withholding tax @ 0 / 10 / 15 / 20%

DDT would be payable @ 14.025%

Tax credit Not available under most Treaties (check domestic laws of home country)

Tax withholding on interest available

Not available under most Treaties (check domestic laws of home country)

Usage No restrictions Restriction on usage as per ECB guidelines (see next slide)

No restrictions

Deductibility

Dividends and DDT not deductible

Interest allowed as deduction (arm’s length principle)

Dividends and DDT not deductible; consider double dip deduction

No thin capitalisation norms and hence an Indian company can be highly leveraged if it meets commercial requirements

Leveraging Indian company using overseas debt subject to restrictions in ECB Guidelines (see next slide)

3

Commercial economics week 5

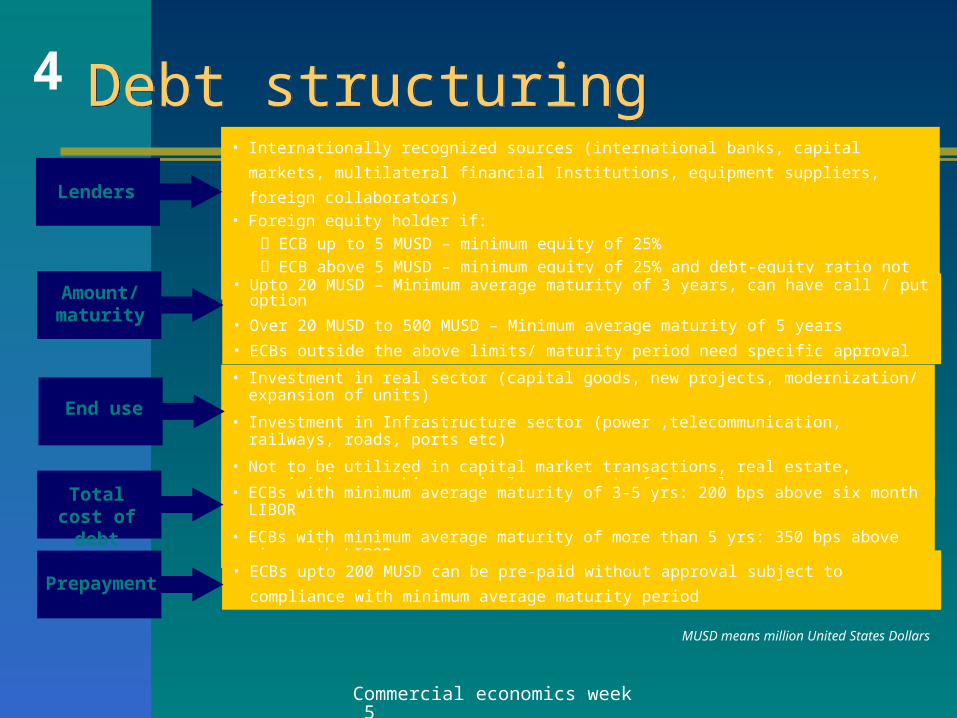

Debt structuring Debt structuring • Internationally recognized sources (international banks, capital markets, multilateral financial

Institutions, equipment suppliers, foreign collaborators)• Foreign equity holder if:

ECB up to 5 MUSD – minimum equity of 25% ECB above 5 MUSD – minimum equity of 25% and debt-equity ratio not exceeding 4:1

• Upto 20 MUSD – Minimum average maturity of 3 years, can have call / put option

• Over 20 MUSD to 500 MUSD – Minimum average maturity of 5 years

• ECBs outside the above limits/ maturity period need specific approval

• Investment in real sector (capital goods, new projects, modernization/ expansion of units)

• Investment in Infrastructure sector (power ,telecommunication, railways, roads, ports etc)

• Not to be utilized in capital market transactions, real estate, acquisition, working capital, repayment of Rupee loans

• ECBs with minimum average maturity of 3-5 yrs: 200 bps above six month LIBOR

• ECBs with minimum average maturity of more than 5 yrs: 350 bps above six month LIBOR

• ECBs upto 200 MUSD can be pre-paid without approval subject to compliance with minimum

average maturity period

Lenders

End use

Total cost of debt

Amount/ maturity

Prepayment

4

MUSD means million United States Dollars

Commercial economics week 5

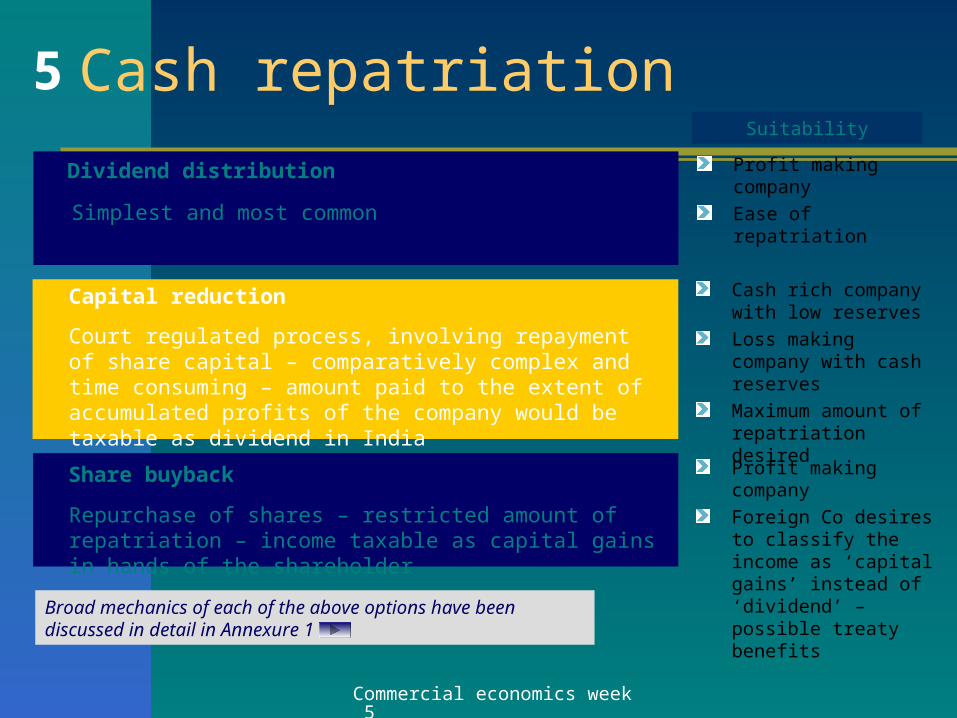

Cash repatriation

Dividend distribution

Broad mechanics of each of the above options have been discussed in detail in Annexure 1

Simplest and most common

Suitability

Profit making company

Ease of repatriation

Capital reduction

Court regulated process, involving repayment of share capital – comparatively complex and time consuming – amount paid to the extent of accumulated profits of the company would be taxable as dividend in India

Cash rich company with low reserves

Loss making company with cash reserves

Maximum amount of repatriation desired

Share buyback

Repurchase of shares – restricted amount of repatriation – income taxable as capital gains in hands of the shareholder

Profit making company

Foreign Co desires to classify the income as ‘capital gains’ instead of ‘dividend’ – possible treaty benefits

5

Commercial economics week 5

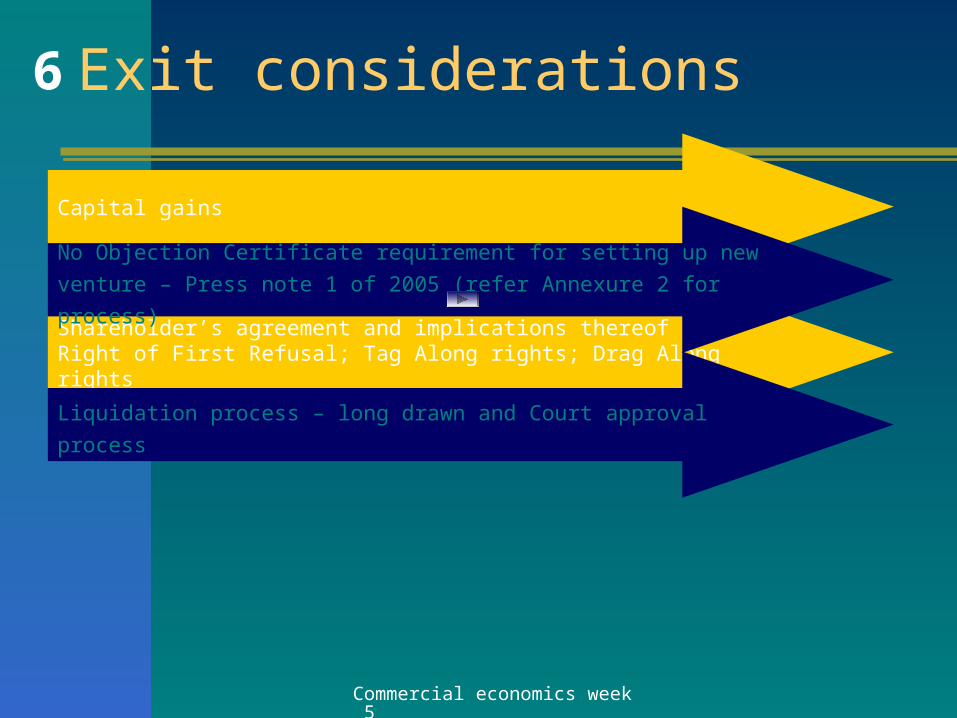

Exit considerations

Capital gains

Shareholder’s agreement and implications thereof – Right of First Refusal; Tag Along rights; Drag Along rights

No Objection Certificate requirement for setting up new venture – Press note

1 of 2005 (refer Annexure 2 for process)

Liquidation process – long drawn and Court approval process

6

Commercial economics week 5

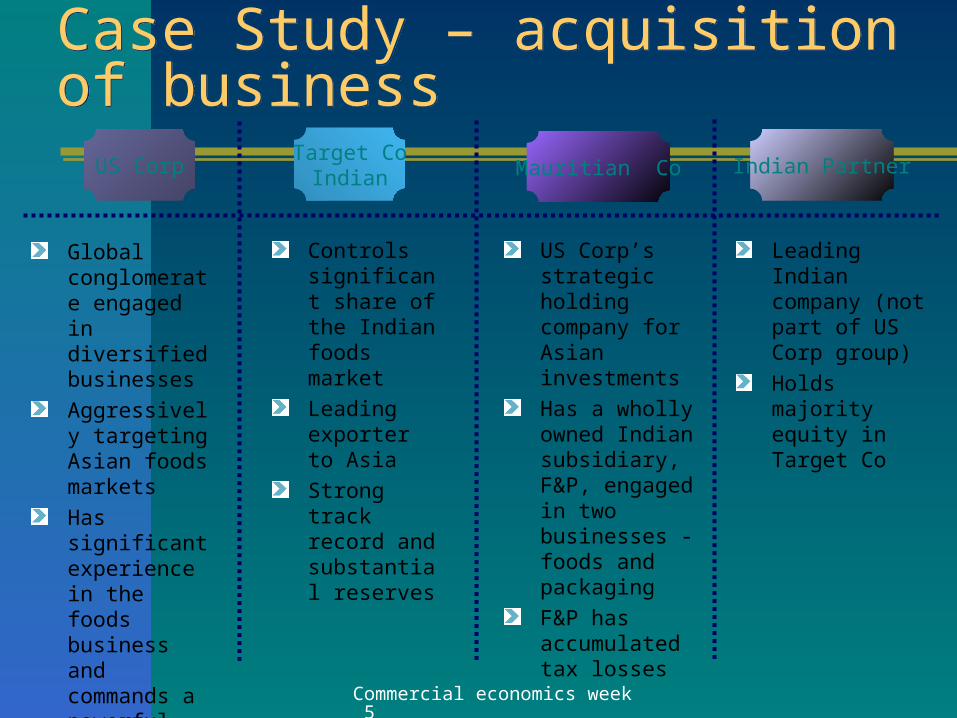

Case Study – acquisition of businessCase Study – acquisition of business

US Corp

Global conglomerate engaged in diversified businesses

Aggressively targeting Asian foods markets

Has significant experience in the foods business and commands a powerful brand name

Target CoIndian

Indian Partner

Controls significant share of the Indian foods market

Leading exporter to Asia

Strong track record and substantial reserves

Mauritian Co

US Corp’s strategic holding company for Asian investments

Has a wholly owned Indian subsidiary, F&P, engaged in two businesses - foods and packaging

F&P has accumulated tax losses

Leading Indian company (not part of US Corp group)

Holds majority equity in Target Co

Commercial economics week 5

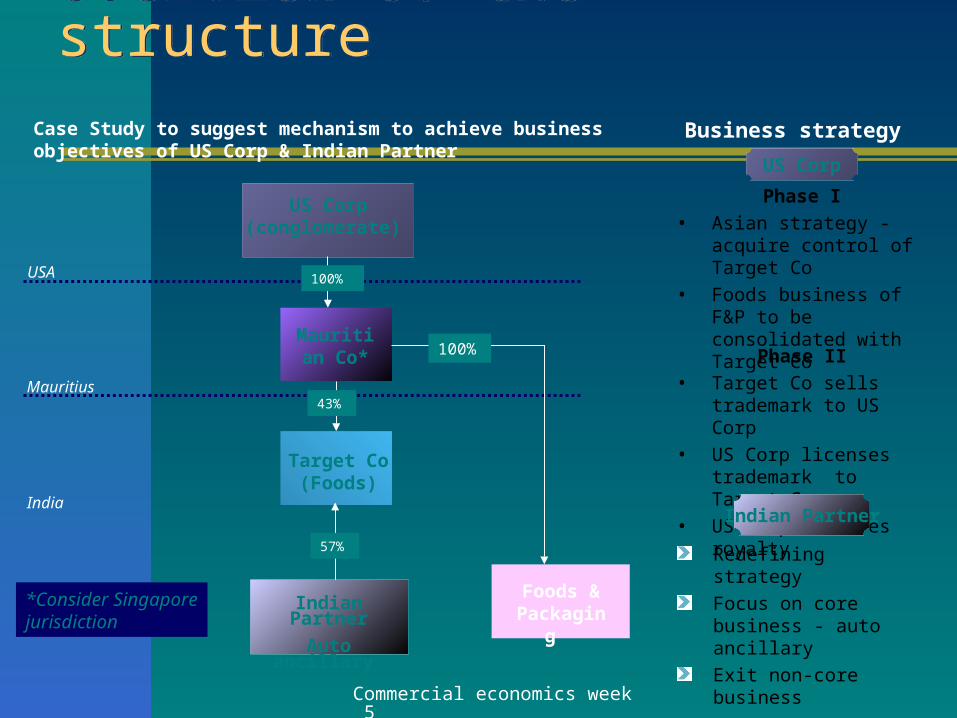

Overview of the structure Overview of the structure

*Consider Singapore jurisdiction

Mauritian Co*

Target Co(Foods)

43%

US Corp(conglomerate)

100%USA

Mauritius

India

Foods & Packaging

100%

Case Study to suggest mechanism to achieve business objectives of US Corp & Indian Partner

Phase I

• Asian strategy - acquire control of Target Co

• Foods business of F&P to be consolidated with Target Co

Phase II

• Target Co sells trademark to US Corp

• US Corp licenses trademark to Target Co

• US Corp receives royalty

Redefining strategy

Focus on core business - auto ancillary

Exit non-core business

US Corp

Indian Partner

Business strategy

57%

Indian Partner

Auto ancillary

Commercial economics week 5

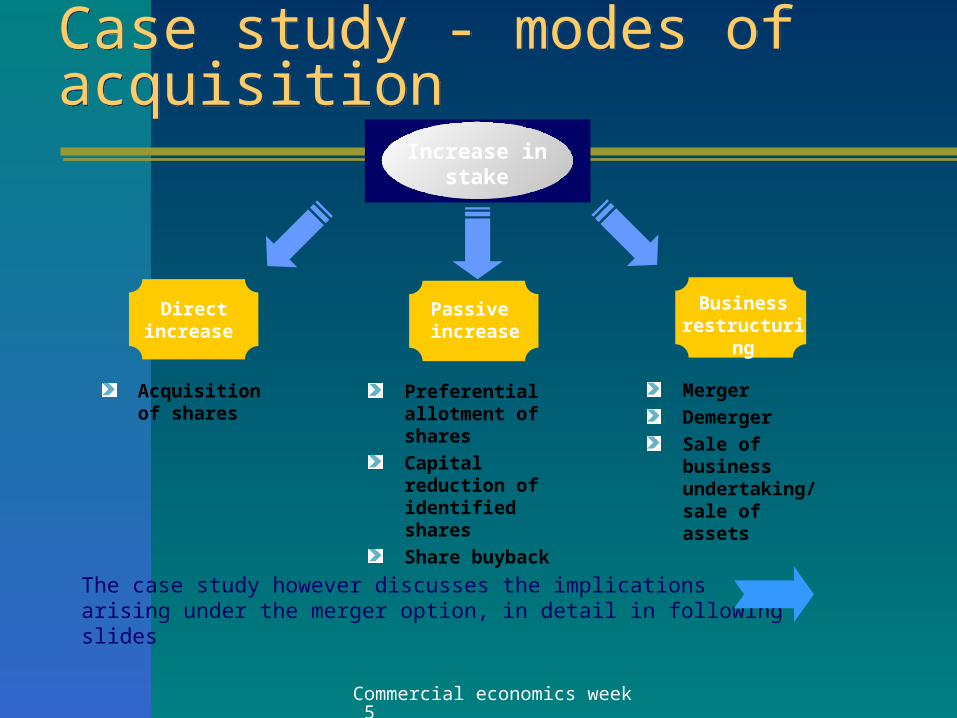

Case study - modes of acquisitionCase study - modes of acquisition

Increase in stake

Acquisition of shares

Merger

Demerger

Sale of business undertaking/sale of assets

Directincrease

Passive increase

Business restructuring

Preferential allotment of shares

Capital reduction of identified shares

Share buyback

The case study however discusses the implications arising under the merger option, in detail in following slides

Commercial economics week 5

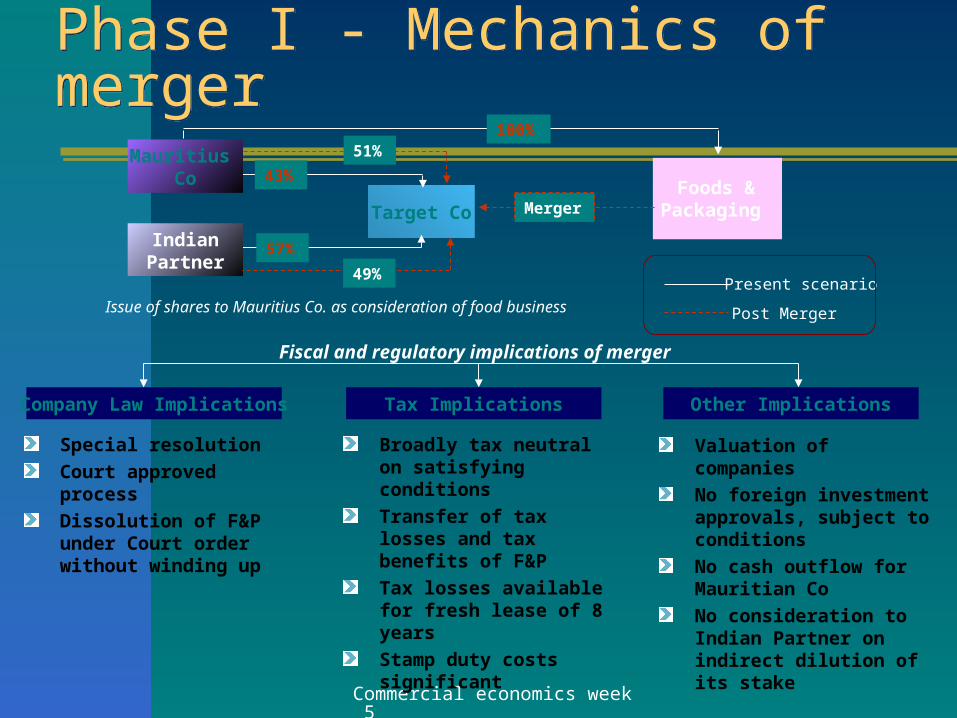

Phase I - Mechanics of merger Phase I - Mechanics of merger

Mauritius Co

Post Merger

Foods & Packaging

43%

Target Co

IndianPartner

57%

100%51%

49%Present scenario

Company Law Implications Tax Implications Other Implications

Special resolution

Court approved process

Dissolution of F&P under Court order without winding up

Broadly tax neutral on satisfying conditions

Transfer of tax losses and tax benefits of F&P

Tax losses available for fresh lease of 8 years

Stamp duty costs significant

Valuation of companies

No foreign investment approvals, subject to conditions

No cash outflow for Mauritian Co

No consideration to Indian Partner on indirect dilution of its stake

Fiscal and regulatory implications of merger

Issue of shares to Mauritius Co. as consideration of food business

Merger

Commercial economics week 5

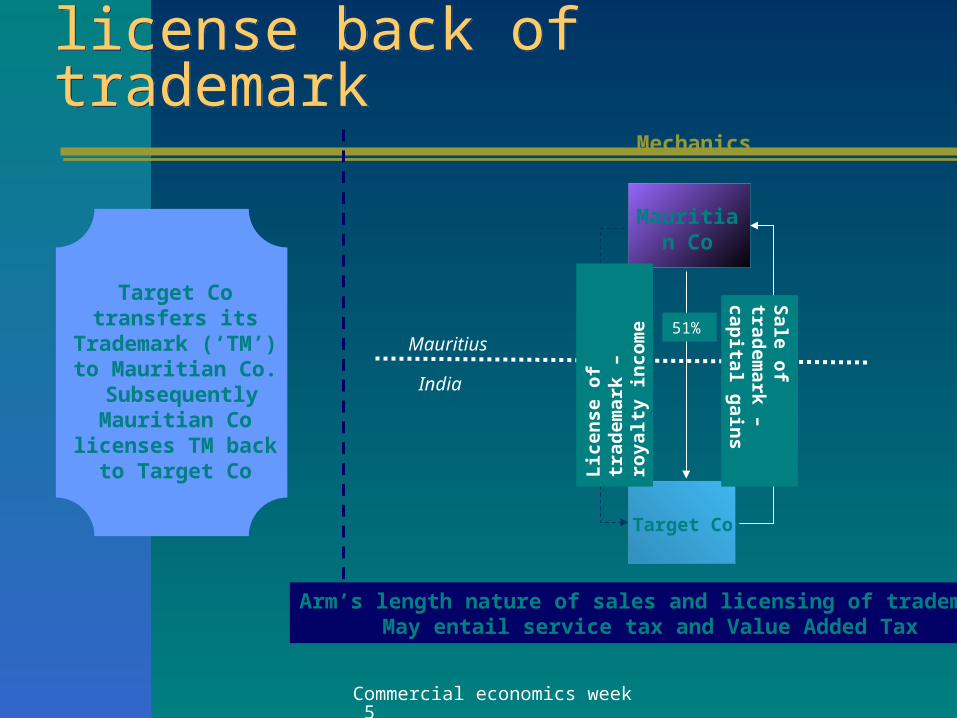

Phase II – Sale and license back of trademarkPhase II – Sale and license back of trademark

Mauritian Co

Target Co

Mauritius

India

Sale o

f tradem

ark – cap

ital gain

s

Lic

en

se o

f tr

ad

emar

k –

ro

yalt

y i

nco

me

Target Co transfers its Trademark (‘TM’)

to Mauritian Co. Subsequently Mauritian Co

licenses TM back to Target Co

Mechanics

51%

Arm’s length nature of sales and licensing of trademarkMay entail service tax and Value Added Tax

Commercial economics week 5

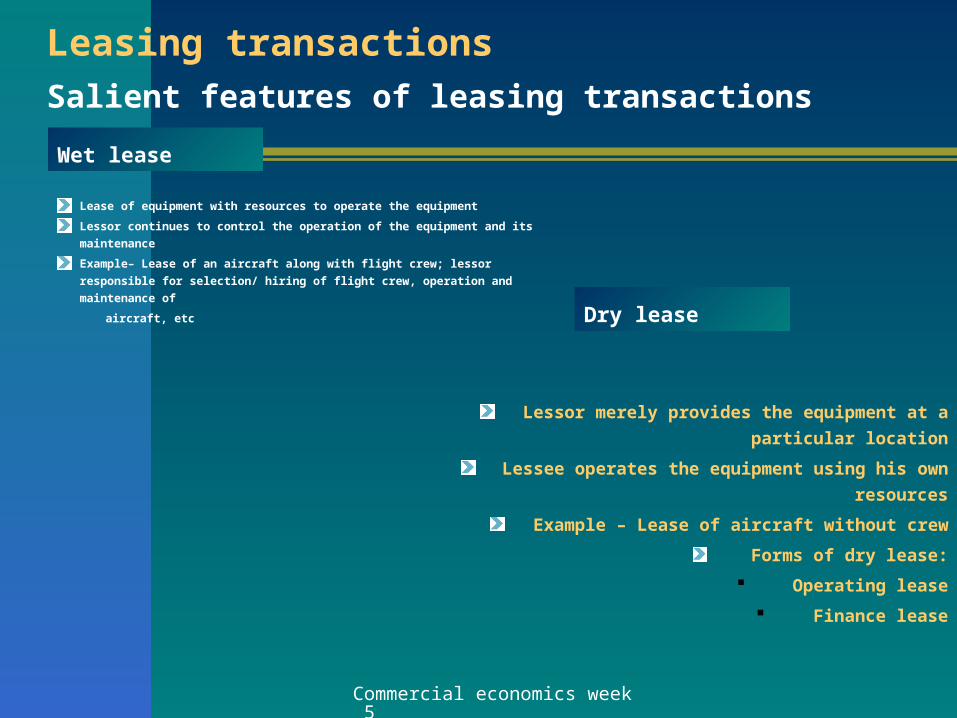

Leasing transactionsSalient features of leasing transactions

Lease of equipment with resources to operate the equipment

Lessor continues to control the operation of the equipment and its

maintenance

Example– Lease of an aircraft along with flight crew; lessor responsible

for selection/ hiring of flight crew, operation and maintenance of

aircraft, etc

Lessor merely provides the equipment at a particular

location

Lessee operates the equipment using his own resources

Example – Lease of aircraft without crew

Forms of dry lease:

Operating lease

Finance lease

Wet lease

Dry lease

Commercial economics week 5

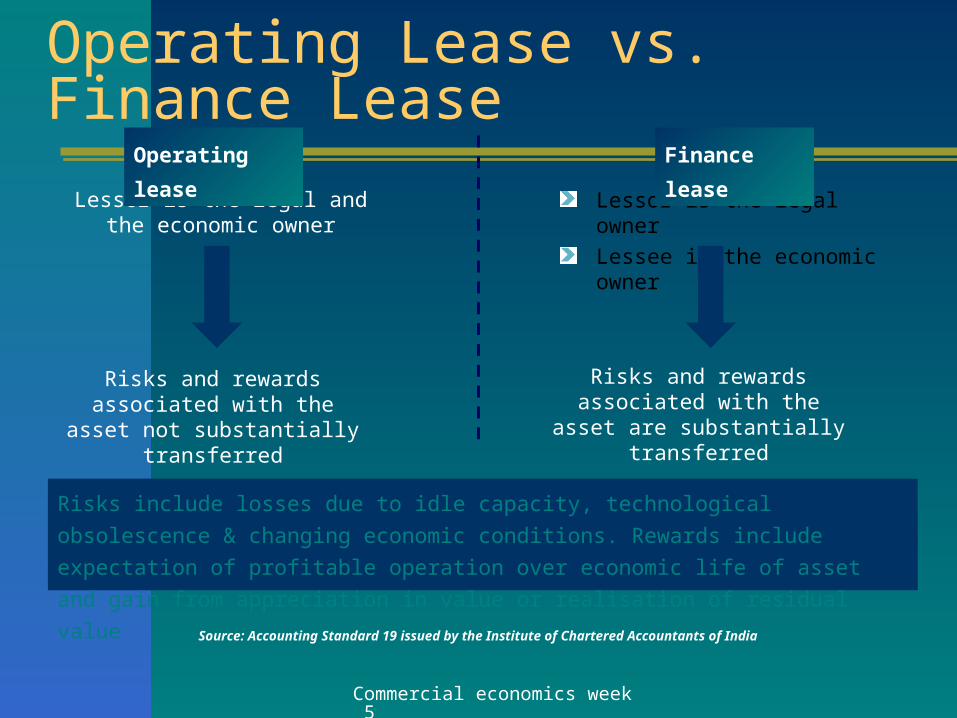

Operating Lease vs. Finance Lease

Lessor is the legal and the economic owner

Lessor is the legal owner

Lessee is the economic owner

Risks and rewards associated with the asset not substantially

transferred

Risks and rewards associated with the asset are substantially

transferred

Operating lease Finance lease

Risks include losses due to idle capacity, technological obsolescence & changing

economic conditions. Rewards include expectation of profitable operation over economic

life of asset and gain from appreciation in value or realisation of residual value

Source: Accounting Standard 19 issued by the Institute of Chartered Accountants of India

Commercial economics week 5

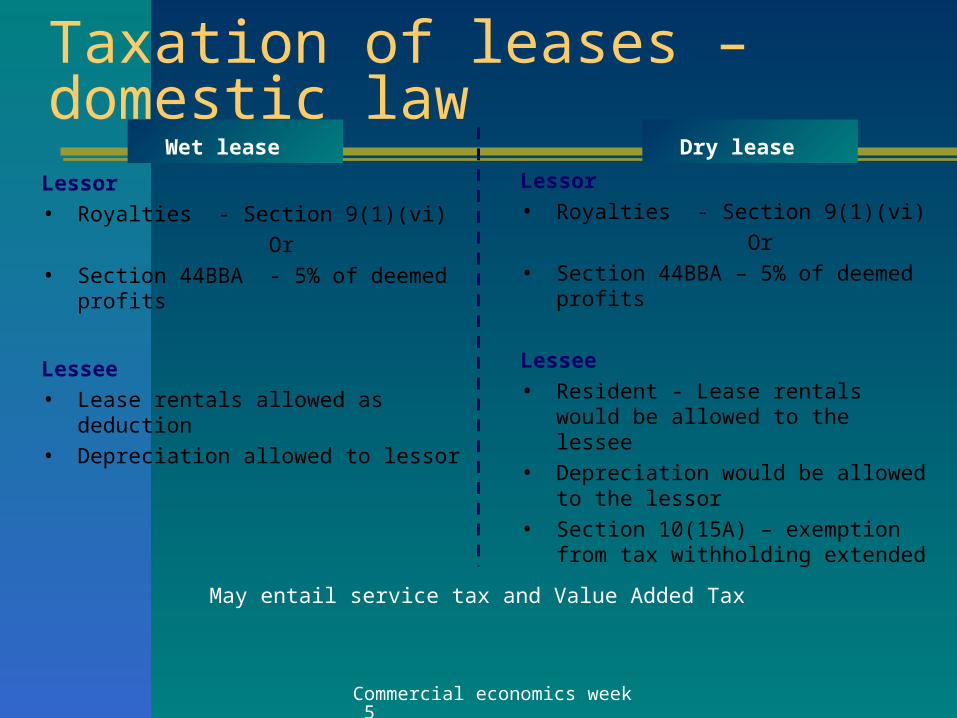

Taxation of leases – domestic law

Lessor

• Royalties - Section 9(1)(vi)

Or

• Section 44BBA - 5% of deemed profits

Lessee

• Lease rentals allowed as deduction

• Depreciation allowed to lessor

Dry lease

Lessor

• Royalties - Section 9(1)(vi)

Or

• Section 44BBA – 5% of deemed profits

Lessee

• Resident - Lease rentals would be allowed to the lessee

• Depreciation would be allowed to the lessor

• Section 10(15A) – exemption from tax withholding extended

Wet lease

May entail service tax and Value Added Tax